Changjiang Zhang

Changjiang Zhang Yue Zhang

Yue Zhang Sihan Zhang

Sihan Zhang

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 04 October 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.1015061

This article is part of the Research Topic ESG Investment and Its Societal Impacts View all 28 articles

Based on a quasi-natural experiment generated by the Shenzhen Stock Exchange (SZSE) of China, which issued the Guidance for Social Responsibility of Listed Companies (referred to as Guidance) in 2006, this paper utilizes a panel dataset of A-share listed companies at Shanghai Stock Exchange (SSE) and SZSE from 2004 to 2008, and employ difference-in-differences (DID) method to investigate impact of the Guidance on environmental information disclosure quality (Eidq) of listed companies. The finding shows that exchange’s corporate social responsibility (CSR) regulation contributes to improving the Eidq of listed companies. Furthermore, policy effects of the Guidance are more significant in eastern region, heavily polluting industries and state-owned enterprises (SOEs). This study provides theoretical evidence and policy implications for the “two-wheel drive” of China’s stock market regulation and social supervision, and for the construction of an environmental information disclosure system that is more targeted in terms of region, industry and property rights, and that effectively promotes fulfillment of environmental governance responsibility by listed companies and guides their sustainable development actions.

This article aims to investigate the impact of stock exchange regulation in capital market on environmental information disclosure quality (Eidq) of listed companies. The Guidance for Social Responsibility of Listed Companies (the Guidance) issued by the SZSE in 2006 is the first regulatory system in the Chinese capital market that requires listed companies to disclose social responsibility reports and environmental information. The Guidance provided natural control and test groups for quasi-natural experiments as it is only for companies listed on the SZSE. We provide theoretical support and practical guidance for the formulation of mandatory environmental information disclosure policies being implemented in China by examining the impact of the Guidance’s publication on the Eidq of Chinese listed companies and heterogeneity analysis of region characteristics, industry attributes, and property rights.

From Adam Smith’s “invisible hand” to Keynes’s “visible hand”, the debate on regulatory effectiveness has been discussed for a long time. Most studies demonstrated the positive effect of CSR regulation on corporate environmental activities (Ramanathan et al., 2018; Younis et al., 2021), but others found that institutional regulation is not sufficient to force firms to substantially “green” (He et al., 2020). Existing research on CSR regulatory effectiveness is shown as follows. First, studies focus on macro effects of regulation, such as effects of institutional regulation on green innovation (Liu et al., 2021c; Zhang H. et al., 2022; Ma et al., 2022; Zhao et al., 2022), high-quality economic development (Liu et al., 2021b), inclusive growth (Ge and Li, 2020), and green transformation (Cai et al., 2020). Second, studies majority are based on comprehensive CSR and environmental regulations, such as environmental fees to taxes (Cheng et al., 2022), central environmental inspections (Deng et al., 2022), new environmental protection law implementation (Zhang and Cheng, 2022), emissions trading system (Zhi et al., 2022), environmental information disclosure system (Zhang et al., 2021; Fang et al., 2022) and China’s national ecological civilization pilot zone (Hou et al., 2022). Third, regarding CSR system effects of regulators, existing research mainly explores the effects of environmental protection system regulation on corporate energy efficiency (Li et al., 2021), total factor productivity (Tang et al., 2020) and enterprise location choices (Lu and Li, 2020). The role of CSR regulation in driving environmental information disclosure is mainly based on China’s new environmental protection law (Zeng et al., 2022) and green finance policies (Wang et al., 2019). As a result, existing literature is biased toward discussing macro effects of CSR regulation, but its impact on micro-organizational behavior is not sufficiently discussed and is mostly limited to the impact on corporate performance, discussing policy effects of overarching institutional arrangements, and specific impact analysis of sector-specific institutional regulation is still in depth. In quasi-natural experimental studies, researchers prefer to examine policy spillovers, and few literatures investigate institutional regulation effects from a particular regulatory sector perspective. Existing literature has not identified the causal relationship between CSR regulation and Eidq, and has failed to explore intensively the role mechanism of regulation on environmental information disclosure behavior of listed companies. This article intends to examine the impact of CSR regulation issued by stock exchange on the probability and quality of environmental information disclosure of listed companies as an external shock event, which can fill research gap on real impact of CSR regulation on “jurisdiction”.

This paper employs quasi-natural experiment method to accurately analyze the impact of institutional supervision on the Eidq of listed companies. The empirical results show that the issuance of the Guidance positively influences the Eidq of listed companies. Based on the main test, this paper further analyzed the heterogeneity of region characteristics, industry attributes, and property rights. With different levels of economic development and differences in marketization, the degree of influence of institutional regulation on the Eidq of listed companies may vary among regions (Liu XB. and Anbumozhi V., 2009). Heavily polluting industries are the focus of Chinese environmental protection departments, financial regulators, and securities regulators. So the impact of institutional regulation on environmental information disclosure of heavily polluting listed companies will be different compared to non-heavily polluting companies (Zeng et al., 2021). In China, SOEs and non-SOEs fulfill different social responsibilities and attach heterogeneous importance to environmental governance and environmental information disclosure (Jiang et al., 2014). We find that the influence of capital market CSR regulation on Eidq of listed companies in eastern regions, heavily polluting industries, and SOEs is more significant.

This article has the following contributions. First, we opened up a pioneering research perspective. Existing literature rarely studies listed companies’ environmental information from a regulatory authority perspective. This paper explores the impact of the Guidance on listed companies’ behavior from exchanges perspective, provides suggestions for the supervision of China’s listed companies, and investigates the relationship between environmental information disclosure of listed companies and regulatory policies. Second, we expanded environmental information disclosure supervision theory. We combine environmental information disclosure supervision and quasi-natural experiments, which enrich supervision theory of environmental information disclosure of listed companies. This paper surveys the effectiveness of the relationship between regulatory authorities and environmental information disclosure of listed companies, to provide helpful decision-making ideas for regulatory authorities to supervise environmental information disclosure effectively.

The rest of this paper is organized as follows. Section 2 introduces the institutional background for the issuance of the Guidance and reviews relevant literature. Section 3 discusses theoretical assumptions. Section 4 presents sample selection, data sources and variable definitions. Section 5 reports empirical findings, robustness tests and heterogeneity tests. Section 6 summarizes research findings and policy implications.

With the SSE, SZSE, and Beijing Stock Exchange (BSE) presently (Kathiravan et al., 2021), China’s capital market, which established in 1990, has made tremendous development over the past 30 years, is moving towards the goal of building an international financial center (Ho et al., 2022). However, China’s capital market needs to consolidate the “barometer” function of economic development unremittingly, continue to enhance opening level, and steadily improve multi-level capital market system (Yan and Qi, 2021). The regulatory history of CSR and environmental information disclosure in China’s capital market can be roughly divided into three stages (Akbar et al., 2021; Huang et al., 2021), namely voluntary disclosure before 2008, a combination of voluntary and mandatory disclosure from 2008 to 2015, and mandatory disclosure from 2015 to the present. In December 2008, the SSE and SZSE simultaneously issued the Notice on the Work of 2008 Annual Reports of Listed Companies (Han et al., 2019), which required companies listed on the SSE Corporate Governance Index, companies issuing overseas-listed foreign shares, and financial companies to disclose CSR reports, and required listed companies included in the SZSE 100 Index to disclose CSR reports, and encourages other companies to disclose CSR reports. In 2002, China Securities Regulatory Commission (CSRC) issued the Code on Governance of Listed Companies, which clarified listed companies’ social responsibility for the first time (Sun et al., 2022). In 2018, CSRC revised the Code on Governance of Listed Companies to build a framework for environmental, social and governance (ESG) information disclosure for listed companies in China (Ruan and Liu, 2021). In 2015, the CPC Central Committee and the State Council published the Integrated Reform Plan for Promoting Ecological Progress, which proposed the establishment of a mandatory environmental disclosure mechanism for listed companies (Yang J. et al., 2022). Since then, the construction of a regulatory mechanism for mandatory environmental disclosure of listed companies in China has entered the “fast track” (Du et al., 2022). In 2017, the CSRC and the former Ministry of Environmental Protection (MEP) jointly signed the Cooperation Agreement on Jointly Carrying Out Environmental Information Disclosure for Listed Companies, which clearly stated that “a mandatory environmental information disclosure system for listed companies and debt-issuing enterprises shall be gradually established and improved” (Dong and Zheng, 2022). In 2017, the CSRC issued the “Guidelines on the Content and Format of Information Disclosure by Companies Issuing Public Securities No. 2: Content and Format of Annual Reports (Revised 2017)”, which mandated listed companies or their significant subsidiaries that are among the key emission enterprises announced by environmental protection authorities to disclose environmental information in annual reports. In 2022, the CSRC issued the Guidelines on Investor Relations Management for Listed Companies, introducing ESG information disclosure in investor relations management for the first time. In 2022, the SSE issued “No. 9 of the Self-regulatory Guidelines for Listed Companies on the SSE: Evaluation of Information Disclosure Work” and the SZSE issued “No. 11 of the Self-regulatory Guidelines for Listed Companies on the SZSE: Evaluation of Information Disclosure Work”, both of which required evaluation of the quality of ESG information disclosure of listed companies.

There were 2,578 listed companies on the SZSE by the end of 2021, with a total market capitalization of about RMB 40 trillion. According to the World Federation of Exchanges (WFE), the SZSE respectively ranked third, third and fourth in the world in terms of annual turnover, financing amount, and IPO companies’ number. In September 2006, the SZSE issued the Guidelines, which became the first regulatory system on social responsibility disclosure in the Chinese capital market. The Guidelines consist of eight chapters and thirty-eight articles, which require listed companies on the SZSE to assume relevant social responsibilities while pursuing economic interests and protecting related interests. In terms of environmental protection and sustainable development, Chapter 5, Articles 27 to 31 of the guidelines set out requirements for environmental information disclosure by listed companies, which should establish a policy system on environmental governance and protection according to the extent of their impact on the environment, and support the disclosure of corporate environmental information in all aspects. However, the Guidance is not mandatory and only encourages listed companies to establish relevant institutional systems to disclose external CSR reports and publish environment-related information. Therefore, based on the profit maximization principle, the proportion of listed companies that perform environmental governance and disclose environmental information will be relatively low.

Overall, the publication of the Guidance has prompted a portion of listed companies to engage in environmental governance and disclose environmental information, which provided material for research on the relationship between institutional regulation and environmental information disclosure. In addition, since the regulatory regime is only for the disclosure of social responsibility reports of companies listed on the SZSE, which provided a natural test group and control group for quasi-natural experiments to study the effect of the regulatory regime on the disclosure of environmental information of listed companies based on this policy.

Institutional regulatory theory, which originated in developed countries, has been extensively investigated by various scholars (Adler and Posner, 2000). Government and market, being two instruments of resource allocation, perform “visible hand” and “invisible hand” functions in economic development (Wang et al., 2021). Institutional regulation is main external pressure in business operation, which affects enterprises’ behavior (Zhang et al., 2015). Government regulation effectiveness has been a highly controversial topic and is influenced by the complexity and scope of regulation (Polishchuk, 2009). Previous research has shown that regulated firms tend to comply with government system (Beyers and Arras, 2020). Institutional regulation is main pusher behind corporate efforts (Ramanathan et al., 2018).

Capital market regulation includes government agency regulation, such as SEC regulation, and market self-regulation, such as exchange regulation (Hart and Moore, 1996). It has been shown that stock markets are responsive to regulatory enforcement in terms of stock price and the degree of response is correlated with the severity of enforcement (Nourayi, 1994). Exchanges are more likely to regulate in a way that optimizes trade-off between investor protection and regulation cost than government agency regulation (Pritchard, 2003). Public objectives of stock market disclosure regulation are to prevent market failures, enhance market confidence, and reduce investment risks (Schulte, 1988). How information providers are regulated depends on the generic properties of information categories they convey to investors and the uncertainty of investors’ interests in information suppliers (Stocken, 2022). Environmental regulation needs to be strengthened in Chinese capital market to punish environmental violators (Huang et al., 2017), and company self-regulation is not enough to ensure effective environmental disclosure (Maassen et al., 2004).

Existing studies demonstrate that CSR and environmental regulation contributed to environmental investment (Yang Y. et al., 2022), total factor productivity (Ford et al., 2014; Ai et al., 2020), capacity utilization (Du et al., 2020; Yu and Shen, 2020), technological innovation (Porter and linde, 1995; Qi et al., 2021), corporate performance (Unermana and O’Dwyer, 2007), and corporate environmental information disclosure (Zhang et al., 2010; Fang et al., 2021). Capital market disclosure regulation creates market reactions such as changes in stock prices (Ingram and Chewning, 1983; Pham et al., 2020). Environmental disclosure regulation enhances executives’ environmental awareness, stimulates changes in production processes (Lee, 2010), and imposes isomorphic effects on environmental disclosure (Stanny, 1998; Anwar et al., 2021; Wilestari et al., 2021). For instance, the Directive 2014/95/EU contributes to Eidq of listed companies (Caputo et al., 2021). Mandatory environmental disclosure regulation can improve social welfare (Cohen and Santhakumar, 2007). Specific normative regulation exerts a greater influence on corporate disclosure than broad government regulation (Mateo-Márquez et al., 2021). However, China’s environmental regulation is still weak (van Rooij and Lo, 2010; Wang and Hao, 2012), regulatory enforcement is lax (Chen et al., 2018), and most listed companies are still experiencing passive disclosure of environmental information (Chen et al., 2022).

External pressure theory and internal motivation theory are two sides of the same coin (Chen et al., 2022). The determinants of corporate environmental disclosure consist of both external and internal factors, with external factors including regulatory pressure, government stress, media concerns, socio-cultural factors and industry aspects, and internal factors including company size, corporate governance, financial performance, social and environmental performance, equity characteristics, executive characteristics, corporate strategy and management factors (Ali et al., 2022).

It remains controversial whether CSR regulation, a compulsory instrument for environmental protection, can improve corporate Eidq (Delgado-Márquez et al., 2017; Liu and Bai, 2022). Performance-impression theory can be employed to explain voluntary disclosure behavior, while pressure-legitimacy theory can be adopted to describe mandatory disclosure behavior (Meng et al., 2013). Most studies demonstrated the significance of external institutional pressures on corporate environmental disclosure (Kerret et al., 2010). With the rising risks associated with climate change, external pressure on corporate environmental disclosure increases (Tollefson, 2007). Studies have found that air pollution negatively affects the probability and qualitative of corporate environmental disclosures (Li et al., 2020; Lin et al., 2021). Strict environmental regulation has greatly contributed to the level of environmental disclosure (Zheng et al., 2020; Wu and Memon, 2022). Legitimacy requirements of national policies and market-incentivized financing demand force listed companies to issue environmental reports (Ng, 2018). Mandatory environmental disclosure regulation has functions such as reflexive, deterrent, and enhancement mechanisms (Liu et al., 2010). Environmental administrative penalties have a significant positive effect on the level of voluntary disclosure of environmental information by enterprises (Ding et al., 2019). It has been shown that negative media coverage significantly enhances the quality of environmental information disclosure of listed companies, and the interaction between public media and local government regulation has a significant positive effect on the quality of corporate environmental disclosure (Xue et al., 2021).

Imperfect regulation is frequently responsible for poor environmental disclosure (Senn and Giordano-Spring, 2020). A certain constraint can improve Eidq (Freedman and Stagliano, 2002). Alciatore and Carol (2006) proved that institutional regulation significantly affects the probability and quality of environmental information disclosure of listed companies, and government regulation significantly contributes to Eidq. Regarding the investigation of the relationship between regulation and Eidq, researchers focus on heterogeneity analysis for region characteristics, industry attributes, and property rights. The degree of influence of regulatory policies on the Eidq of listed companies varies by region, industry, and property rights. For example, the degree of impact of regulatory policies on listed companies varies according to the differences in regional economic development and marketization (Zhao et al., 2018). Industry sensitivity is the main driver of social and environmental disclosure among Chinese listed companies (Liu X. and Anbumozhi V., 2009; Zeng et al., 2010; Dyduch and Krasodomska, 2017; Suarez-Rico et al., 2018). Compared to other industries, heavy-polluting industries are more strictly monitored and more responsive to regulation (Zeng et al., 2021). SOEs are controlled by the state and pay more attention to CSR and environmental information disclosure than non-SOEs (Yekini et al., 2019; Ren et al., 2020; Liu et al., 2021a). Environmental regulations tend to influence SOEs more significantly (Jiang et al., 2014).

In summary, a growing body of existing literature focuses on the impact of institutional regulation on firms, and most studies have demonstrated the effectiveness of institutional regulation as firms comply with regulatory requirements in pursuit of legitimacy (Wang and Chen, 2017). Scholars have verified the effects of institutional regulation on firm behavior, firm value and capacity utilization, which in turn illustrate institutional regulation effectiveness. For example, Yekini et al. (2019) examined environmental information disclosure status of listed companies following the issuance of the “Environmental Information Disclosure Guidelines for Chinese Listed Companies” by the Ministry of Environmental Protection (MEP) in 2010, without using a quasi-natural experiment approach. Ren et al. (2020) and Liu et al. (2021a) use the “Guidelines on Environmental Disclosure of Listed Companies on the SSE” as a quasi-natural experiment, and employ DID model to investigate the impact of mandatory CSR disclosure policies on win-win for firm’s environmental and economic performance, and the fulfillment of corporate environmental responsibility. However, limited literature has examined the differences in listed companies’ behavior from the exchange perspective of their institutional regulation and implementation effects. The academic community has not identified a causal relationship between exchange CSR regulation and the Eidq of listed companies, and have not investigated in-depth the mechanism of the effect of institutional regulation on the behavior of corporate environmental information disclosure.

Exploring the relationship between institutional regulation and Eidq requires a natural experiment of a specific institutional policy release. Issued in 2006, as the first institutional document of China’s stock exchange requiring listed companies to disclose environmental information, the Guidance has a landmark influence on CSR policy. To a certain extent, it constrains the environmental governance behavior of listed companies and motivates them to disclose environmental information, providing a direction to study the influence of institutional regulation on the disclosure of environmental information of listed companies. This article uses the Guidance to conduct a quasi-natural experiment with the SZSE and SSE as the test group and the control group respectively to investigate the impact of institutional policy regulation on environmental information disclosure of listed companies.

First, according to the signaling theory, environmental information disclosure helps stakeholders to understand the environmental protection status of enterprises, improves the market’s understanding of enterprises’ non-financial information, and affects the market evaluation of enterprises, which in turn promotes corporate value (Blacconiere and Patten, 1994; Patten and Nance, 1998). Secondly, according to the legitimacy theory, the survival and development of enterprises must be based on legal contracts, and enterprises must behave in a way that meets compliance requirements. Suppose a company’s actions do not meet the contractual requirements of external stakeholders. In that case, its operation legitimacy cannot be guaranteed and the company may face the risk of related litigation (Deegan and Rankin, 1996). So, it is the primary goal of a listed company to make itself visible to outside as legitimate (Tzouvanas et al., 2020). When relevant policies require companies to disclose environmental information, management will consider the economic benefits of environmental information disclosure. If companies want to communicate positive environmental governance information to the public and improve Eidq, they need to invest heavily in environmental protection. Finally, principal-agent theory holds that management needs to bear environmental management cost and benefits uncertainty, and is under great pressure of cost (Frondel et al., 2008). Thus, management may be reluctant to disclose environmental information voluntarily as well as unwilling to improve Eidq. This directly leads to the generally low Eidq in China. Moreover, the environmental information that enterprises choose to disclose only reflects their efforts to manage the environment but does not reflect negative information such as environmental problems existing in firms and the discharge of related pollutants.

Therefore, relevant regulatory systems are needed to restrict corporate behavior. The regulatory authorities require companies to conduct environmental governance and disclose environmental information and related governance to outside through the system. The environmental supervision system can help improve the level of environmental information disclosure by Chinese listed companies, and can stimulate companies to actively disclose environmental information from the perspectives of mandatory constraints and voluntary incentives. As a landmark system for supervision, the publication of the Guidance will impact the environmental information disclosure of listed companies. Thus, hypothesis 1 is proposed as follows.

Hypothesis 1. The implementation of the Guidance has a positive impact on the environmental information disclosure of listed companies and improved the Eidq.The uneven economic and technological development of different countries or regions, as well as the different levels of regulatory may lead to various disclosures of environmental information (Liu and Anbumozhi, 2009). China is a vast country, containing different regions with different economic development patterns and levels. Due to geographical advantages, eastern regions in China take the lead in optimizing development, with a more developed economy and a higher degree of marketization. While the central and western regions are restricted in many aspects of development due to environmental resources, transportation, and economic structure, and the level of economic development and marketization is lower than that of the eastern region. In the early days, China developed its economy at the expense of the environment to solve the problem of food and clothing. The high level of economic development has brought about higher environmental awareness, which has driven the regulatory agencies to impose stricter legislation and enforcement. Under this circumstance, enterprises have a stronger incentive to disclose environmental information, and the level of environmental information disclosure is higher (Fan et al., 2020).After the regulator issues environmental information disclosure system, enterprises may avoid disclosing environmental information or enhance Eidq when illegality cost is lower than environmental treatment cost. In areas with a high level of economic development, the government and the public have a relatively high awareness of environmental protection, leading to high competitive pressure. The cost for companies to disclose environmental information as required may be much lower than economic losses caused by non-compliance. Under competition from government departments, the public, and enterprises, in regions with a high level of economic development, institutional supervision has a more significant impact on Eidq. Thus, hypothesis 2a is proposed as follows.

Hypothesis 2a. Compared with regions with lower economic development levels, the Guidance has a more significant impact on the Eidq of listed companies in regions with higher economic development levels.Listed companies in different industries have distinct degrees of environmental pollution, different levels of attention from government departments, and different degrees of response to institutional supervision (Zou et al., 2015). Since listed companies in China are required to disclose environmental information, especially for heavily polluting industries. In 2003, the former State Environmental Protection Administration (SEPA) issued the Announcement on Corporate Environmental Information Disclosure, which mandated heavy polluters to disclose environmental information. As a key target of state regulation, every move of enterprises in heavily polluting industry is monitored. When their environmental governance and information disclosure behaviors fail to meet institutional requirements, it will damage their reputation and affect future development. So enterprises in heavily polluting industry are more sensitive to regulation responses (Zeng et al., 2021). On the contrary, the environmental information disclosure behavior of enterprises in non-heavily polluting industries receives less attention, and failure to disclose environmental information does not lead to serious economic consequences. Therefore, enterprises in heavily polluting industries will disclose more environmental information. The Guidance is Chinese first institution on CSR disclosure. Therefore, affected by this system, the Eidq of listed companies in heavily polluting industries is higher than that of non-heavily polluting listed companies. Hypothesis 2b is proposed as follows.

Hypothesis 2b. Compared with non-heavy polluting industries, the Guidance has a more significant impact on the Eidq by listed companies in heavily polluting industries.To date, there are no mandatory requirements for environmental information disclosure for most listed companies in China. The property rights has a significant impact on the Eidq (Liu and Anbumozhi, 2009). According to the property rights, companies are divided into SOEs and non-SOEs. SOEs need to respond to national strategic decisions and help the country achieve non-economic goals while pursuing economic benefits. So, when government departments introduced relevant policies, SOEs always pursue the maximization of both profit and social interest. On the contrary, the requirement for non-SOEs to assume CSR is relatively low, and managers of non-SOEs are more concerned with economic efficiency than CSR and environmental governance. When the investment cost of environmental governance and disclosure is greater than its economic benefits, non-SOEs lack the incentive to engage in environmental governance and disclosure. After the implementation of environmental system, the Eidq of non-SOEs has been weakly improved. Under the dual effects of external institutional pressure and internal governance mechanisms, SOEs are more inclined to disclose high-quality environmental information. Thus, hypothesis 2c is proposed as follows.

Hypothesis 2c. Compared with non-SOEs, the Guidance has a more significant impact on the Eidq of SOEs.

To find the impact of the Guidance on the environmental information disclosure of listed companies, this paper selects A-share listed companies in the SZSE and SSE from 2004 to 2008 as research samples. Since the Guidance is only valid for companies listed on the SZSE and has no impact on companies listed on the SSE, the A-share listed companies in SZSE are test group, and the A-share listed companies in SSE are control group. The Guidance began to be implemented in the middle of 2006. This paper selects 2004–2005 as the time before the implementation of the system, and 2006–2008 as the time after the implementation of the system. In addition, based on the original data obtained, companies listed after 2004, listed companies in the financial industry, listed companies with incomplete data, and ST or *ST companies were deleted. Finally, 5,270 observations were obtained. To exclude outliers, the continuous variables are trimmed by the upper and lower 1% quantile. Before 2008, the sample data of the social responsibility report was collected manually from Juchao Information Network (www.cninfo.com.cn), which is the statutory information disclosure platform of SZSE. Environmental information disclosure in social responsibility report of listed companies in 2008 came from CSMAR database, and other financial data came from WIND database.

We set explained variable as the Eidq of enterprises. The Guidance, the first institutional regulatory policy on social responsibility disclosure of listed companies in China’s stock exchanges, has no specific requirements or mandatory disclosure requirements for environmental information disclosure of listed companies, stating that “information on environmental protection of listed companies should be disclosed in social responsibility reports”. We draw on Wiseman (1982), Lee (2017) and Fan et al. (2020) to measure Eidq by a scoring method. When a listed company published a social responsibility report and disclosed monetized environmental information, general environmental information, or non-relevant environmental information, Eidq is correspondingly assigned a score of 2, 1, or 0.

This paper sets whether the experimental variable is an SZSE listed company (Treat), if the company is an SZSE listed company, define Treat = 1, otherwise, Treat = 0; whether the time variable is after 2005 (Time), if the sample year is after 2005, Time = 1 is defined, otherwise Time = 0.

Drawing on Luo et al. (2022), Meng and Zhang (2022), we control characteristic variables such as company size, solvency, profitability, listing ages, board size, and property rights, industry attributes, and company location. Specifically, company size, marked as Asset, is measured as the natural logarithm of company’s total assets. Solvency, marked as Lev, is measured by the ratio of total liabilities to total assets. Profitability, marked as Roe, is measured by the ratio of net income to average net shareholders’ equity. Listing ages, marked as Age, is measured by the natural logarithm of the company’s time to market. Board size, marked as Boardsize, is measured by the natural logarithm of the number of directors on the board. Property right, marked as State, is assigned 1 if it is SOEs, otherwise 0. Industry attributes, marked as Industry, is assigned 1 if it belongs to the heavy pollution industry, otherwise 0. Company location, marked as Region, is assigned 1 if the company is located in a region with a high level of economic development, otherwise 0.

When testing the impact of regulatory system implementation, DID method is usually used for regression analysis. Drawing on Bertrand et al. (2004) and Zhang Y. et al. (2022), this paper sets up the following model (1).

In model (1), Eidq represents the quality of environmental information disclosure, i represents listed company, t represents time, j represents industry, r represents region, Time represents the implementation of the Guidance, Treat represents whether it is an SZSE listed company, X represents control variable, Ɛ is a random disturbance term. When analyzing regression results, this paper is interested in the coefficient of Treat × Time. If the coefficient of Treat × Time is significant in model (1), it means that the implementation of the Guidance has significantly improved the Eidq by SZSE listed companies and hypothesis 1 gets verified.

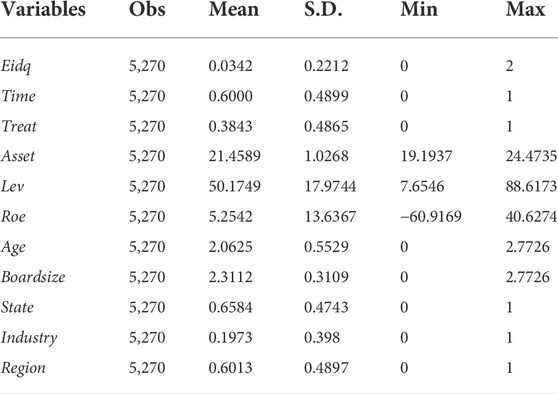

Table 1 reports the descriptive statistics of main variables. The sample includes 1,054 listed companies with a total of 5,270 observations. The mean of Time is 0.6000, indicating that the sample share after the implementation of the Guidance was 60%. The mean of Treat is 0.3843, which means SZSE-listed companies accounting for 38.43%. The average value is only 0.0342, which means that there are few listed companies that disclose environmental information in social responsibility reports.

TABLE 1. Descriptive statistics.

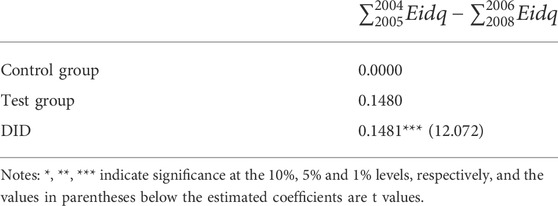

According to listing locations, univariate tests are analyzed for test group (companies listed on the SZSE) and control group (companies listed on the SSE). As shown in Table 2, before the implementation of the Guidance, there was no difference between test group and control group, and all of them had no environmental information disclosure of social responsibility information; after the implementation of the Guidance, control group was not affected, and the Eidq of test group improved by 0.148, which initially verified the Guidance’s effectiveness.

TABLE 2. Univariate test.

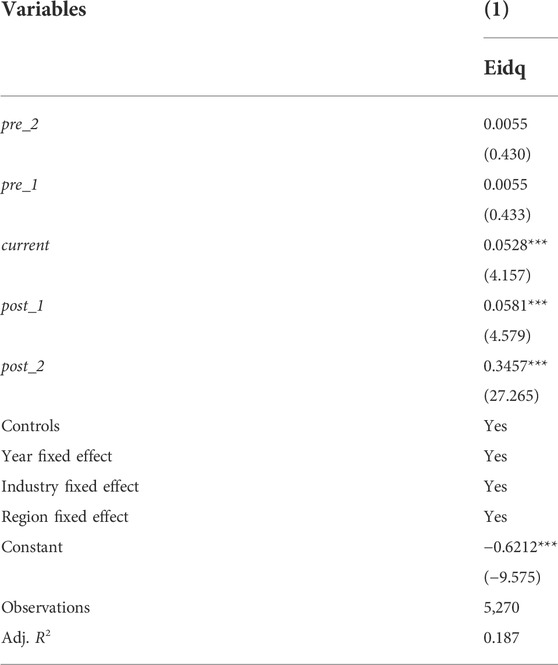

One of the prerequisites for DID estimation validity is that test group and control group must satisfy parallel trend assumptions before treated (Bertrand et al., 2004). That is, before the Guidance implementation, temporal trends in social responsibility report disclosure and environmental information disclosure behavior changes between control group and test group were as identical as possible. While after the Guidance implementation, the break of parallel trends was mainly reflected in trend changes existence in the environmental information disclosure behavior of SZSE listed companies relative to SSE listed companies. The premise for performing DID regression is that test group and control group meet trend prior to the publication of the Guidance. Therefore, dynamic effect model 2) is used to test parallel trend and dynamic effect.

Where i represents company, t represents year, j represents industry, and r represents region. Pre_1, pre_2, current, post_1, post_2 are dummy variables. If listed company is in test group before the Guidance shock, it is assigned a value of 1, otherwise, 0. If company is in policy shock year and is in test group, current is assigned a value of 1, otherwise, 0. If company is after the policy shock and is in test group, post_1 and post_2 are assigned a value of 1, otherwise 0. The significance of each dummy variable coefficient can reflect whether there is a common trend between test group and control group.

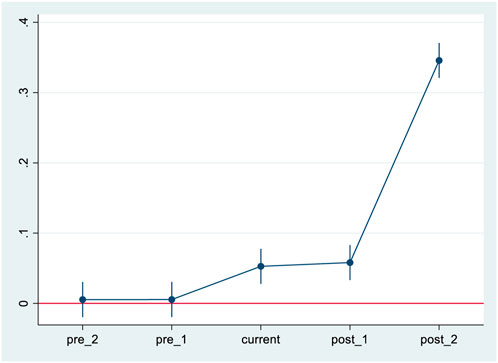

Table 3 shows that the coefficients of pre_1 and pre_2 are not significant. This means that the difference in environmental information disclosure between test group and control group will not change over time before the Guidance implementation, which meet parallel trend hypothesis. The coefficients of current, post_1, and post_2 are significant, which means that after the implementation of the Guidance, the Eidq of listed companies has changed significantly. In 2006, there was a significant change in environmental information disclosure, while in 2007 it increased slowly. In 2008, listed companies’ behavior changed significantly, increasing the disclosure of environmental information (Figure 1). Based on institutional theory, there is imitation behavior and resulting institutional isomorphism in corporate disclosure under conditions of legitimacy pressure and uncertainty, and imitation behavior can be specified as frequency imitation of the market average and feature imitation of the market leader (Bernard et al., 2021). This is the reason for the change in the coefficient from 2006 to 2008.

TABLE 3. Parallel trend test.

FIGURE 1. Parallel trend chart.

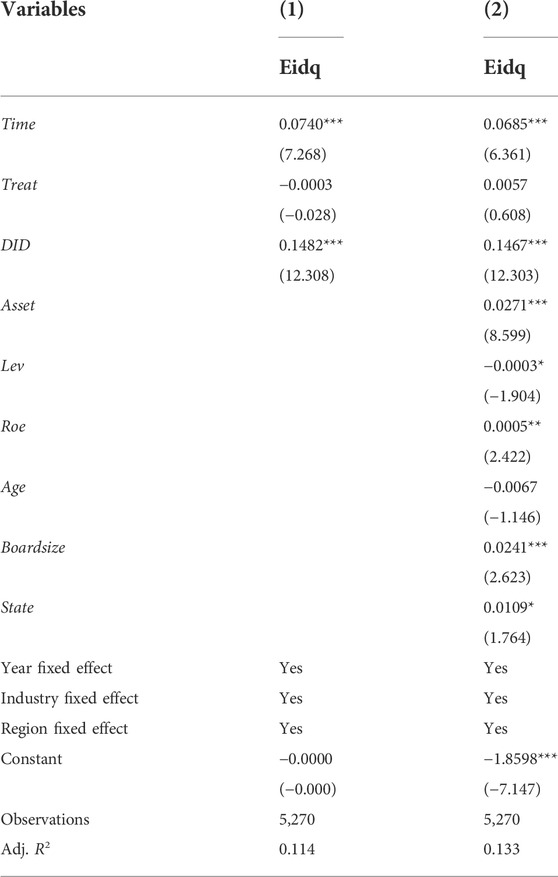

Table 4 reports Eidq changes before and after the Guidance implementation. Column 1) shows the results only considering fixed effects, and column 2) shows the results considering control variables and fixed effects. The regression results show that when only fixed effect is considered, the regression coefficient of DID term is 0.1482, which is significantly indigenous at 1% level. It shows that the implementation of the Guidance has had a significant impact on Eidq. Eidq has increased by 14.82%. After considering control variables, DID term is 0.1467, which shows a significance at 1% level. It means that the Guidance implementation improved Eidq. Hypothesis 1 is verified. As the regulator and guide of listed companies, the exchange positively influences CSR and environmental disclosure behavior (Ali et al., 2022). The issuance of the Guidance affects not only listed companies in SZSE but also listed companies in SSE, which indicates the possible interaction of regulatory measures from multiple exchanges in the same country or region. That is, CSR regulatory policies introduced by one exchange can have spillover effects on listed companies at other exchanges (Ingram and Chewning, 1983). Although the motivation for environmental disclosure by listed companies in China today is no longer as dependent on institutional pressure as it was in the days when the Guidance was issued, it is undeniable that exchange regulation still holds a vital role.

TABLE 4. Baseline results.

The empirical result that the Eidq of listed companies has improved significantly after the implementation of the Guidance may be caused by other factors. Drawing on Topalova (2010), We use the samples before the event to conduct a placebo test. This paper selects the listed companies from 2002 to 2005 as the sample, sets the implementation year of the Guidance as 2004, and reassigns the samples belonging to 2002 to 2005 to Treat = 0, otherwise, define Treat = 1. Because before 2006, there was no relevant institutional regulation requiring the disclosure of social responsibility and environmental information, so the environmental information disclosure of listed companies was 0. At this time, hypothesis 1 could not be verified, which indicates that research conclusion is robust.

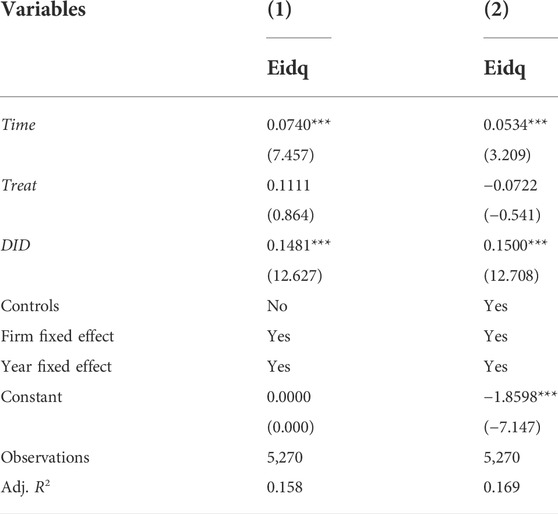

Regional fixed effects, industry fixed effects, and time fixed effects have been used in the previous section, but they do not fully reflect the impact of the Guidance on the quality of individual environmental information disclosure of listed companies. To clarify the specific impact of the Guidance on listed companies, we use firm fixed effects to replace toriginal industry and regional effects referencing Meng et al. (2013). Column 1) and Column 2) of Table 5 show that the coefficients of DID term are 0.1481 and 0.1500, and are aboriginal at 1% level, which is consistent with previous results. Hypothesis 1 is still valid.

TABLE 5. Firm fixed effect test.

The impact of institutional policies on environmental information disclosure differs across region characteristics, industry distribution and property rights, and now the heterogeneity of these three aspects is tested to figure out the impact of the Guidance on the Eidq of different types of listed companies.

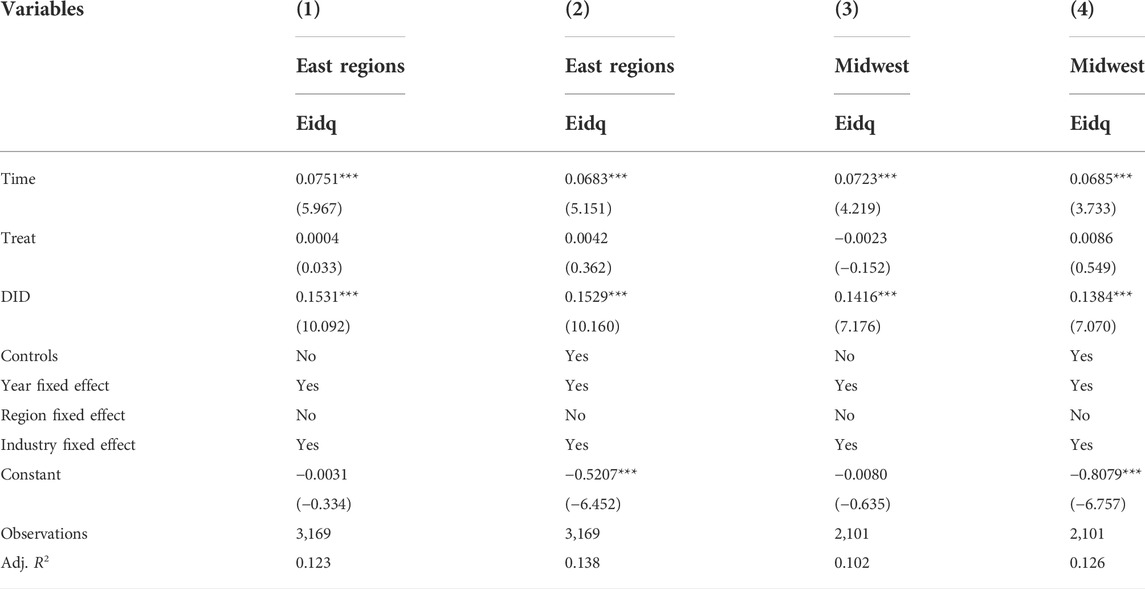

According to the classification standard of the National Bureau of Statistics (NBS) of China (excluding Hong Kong, Macao, and Taiwan), regions classification is as follows. The eastern regions include Beijing, Tianjin, Hebei, Liaoning, Shanghai, Jiangsu, Zhejiang, Fujian, Shandong, Guangdong and Hainan. These provinces (cities) have good geographical locations and are key areas for national economic development with relatively high levels of economic development. The rest regions belong to the Midwest. The regression results are shown in Table 6. The coefficient of DID term in the eastern region is 0.1529, the coefficient of DID term in the Midwest is 0.1384, and the coefficient of the higher economic development level is more significant. In regions with a higher level of economic development, the Guidance has a more significant impact on the Eidq, which is consistent with hypothesis 2a. The level of regional economic development and marketization are important perspectives for analyzing the variability of listed companies’ responses to CSR regulation. This finding is consistent with Fang et al. (2022) and Liu and Anbumozhi (2009). To this day, the uneven regional development in China remains. Listed companies in different regions are subject to varying degrees of exchange CSR regulation, which implies the need to strengthen CSR regulation instruments other than exchange regulation, such as local government regulation, social supervision and industry self-regulation.

TABLE 6. Heterogeneity test of economic development level.

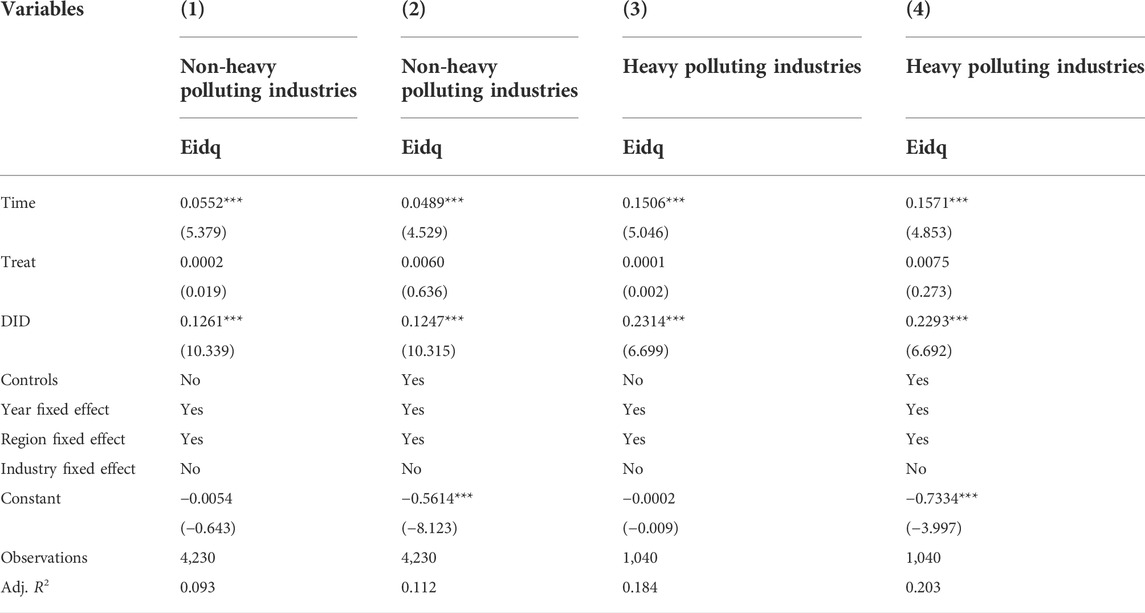

The Guidance is aimed at companies listed on the SZSE, and there is no clear distinction between heavily polluting and non-heavy polluting industries. However, the heavily polluting industry has always been regulatory focus. After the publication of system supervision on social responsibility and environmental information disclosure, legality pressure faced by listed companies in heavily polluting industry is particularly prominent. Therefore, their environmental governance and environmental information disclosure behaviors will be different from non-heavy polluting industries. We re-performed the regression analysis by the Guidance for Industry Classification of Listed Companies issued by the CSRC in 2001, and the List of Industry Classification Management of Listed Companies for Environmental Protection Inspection issued by the General Office of the Ministry of Environmental Protection in 2008 Classification. The regression results are shown in columns 2) and 4) of Table 7. The DID regression coefficients of listed companies in heavily polluting industries and non-heavy polluting industries are respectively 0.2293 and 0.1247, which are significant at 1% level, and are consistent with the baseline test results. Moreover, the coefficient of listed companies in heavily polluting industries is greater than that in non-heavy polluting industries, and the positive effect of Guidance on Eidq is more significant. Heavily polluting industries are CSR regulation focus. This finding can guide the design and implementation of mandatory environmental information disclosure system for key industries implemented in China.

TABLE 7. Heterogeneity test of industry nature.

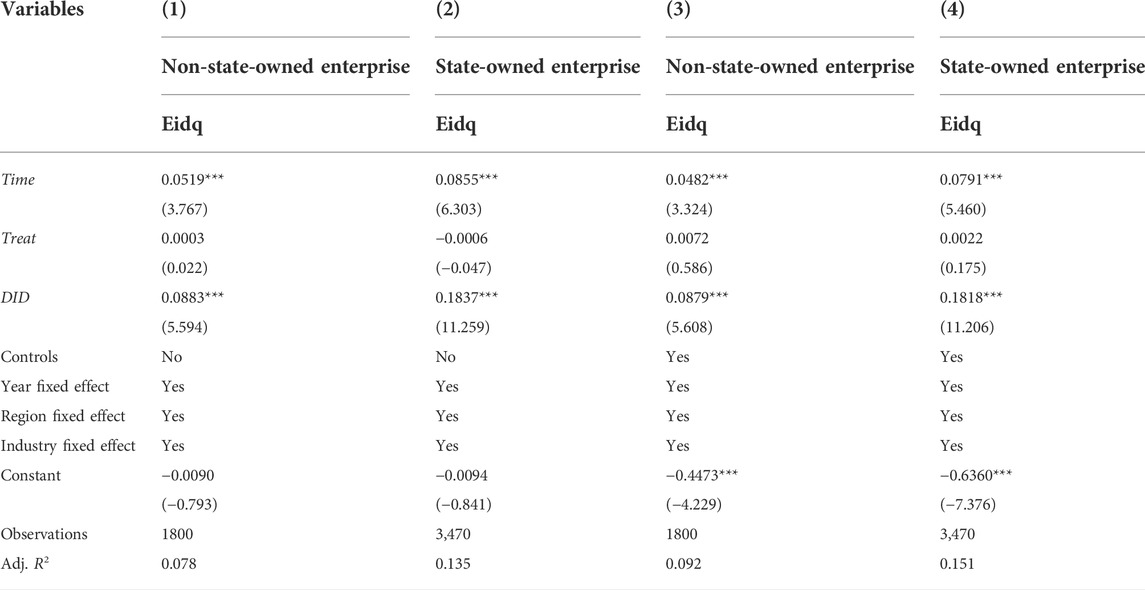

Based on legitimacy theory, SOEs are more responsive to policies in facing exchange regulation compared to non-SOEs. According to ultimate controller, we divided sample companies into SOEs and non-SOEs, and conducted regression analysis on each pair. Table 8 shows that the DID coefficients in the case of considering control variables are 0.1818 and 0.0879, which are significant at 1% level, consistent with the results of main hypothesis test, and the Eidq of SOEs is better than that of non-SOEs, which is consistent with hypothesis 2c. The government and society expect more from state-owned listed companies (Ervits, 2021), which are more responsible and effective in fulfilling CSR (Hu et al., 2018).

TABLE 8. Heterogeneity test of property rights.

Based on the exogenous impact of the Guidance, this paper finds a positive impact of stock exchange CSR regulation on Eidq of listed companies in China. In addition, multiple factors have heterogeneity on environmental information disclosure, the positive impact is more significant in the sub-samples of regions with high economic development levels, heavy pollution industries, and SOEs. Since the Guidance does not impose mandatory requirements on environmental information disclosure of listed companies, the proportions of listed companies disclosing environmental information after the implementation of the Guidance are still at a low level. Today, listed companies on the SZSE still follow the requirements of the Guidelines for CSR and environmental information disclosure.

Compared to Yekini et al. (2019), Ren et al. (2020) and Liu et al. (2021a), this paper expands the existing literature in the following aspects. First, this paper exploits the CSR regulation data of SZSE for the first time, which expands quasi-natural experiments research on CSR system regulation. Secondly, in an empirical test, we examined the effect of CSR regulation of SZSE on environmental information disclosure of all A-share listed companies by using SZSE listed companies as test group and SSE listed companies as the control group, which enhances the refinement of CSR regulation research. Finally, this study particularly emphasizes the practical value of exploring historical policy effects. In 2022, the Ministry of Ecology and Environment of China issued the Reform Plan for the Legal Disclosure of Environmental Information, which clarified the idea and framework of the system reform based on legal disclosure, focusing on collaborative management, strengthening supervision as a means, and technical support as the guarantee. Mandatory disclosure of environmental information and coordinated management of various departments will be the development trend of environmental governance systems in China and even developing countries.

The policy implications of this paper are as follows. First, the role of the Exchange in CSR and environmental disclosure regulation should be further strengthened. Meanwhile, a single department needs to cooperate with other departments to conduct joint governance to make up for the shortcomings of the system. Second, environmental information disclosure regulation of non-heavily polluting industries and non-state enterprises needs to be strengthened. Third, besides the CSR regulation of the exchange, we should simultaneously improve the “soft regulation” mechanism of local government, industry self-regulation and social supervision of environmental information disclosure of listed companies.

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Author contribution Conceptualization: CZ; Methodology: CZ, YZ; Data curation: YZ, YC; Software: SZ; Formal analysis: CZ, MH; Investigation: CZ, SZ; Writing—original draft: CZ, MH; Writing—review and; editing: CZ, MH, YZ, YC. All authors approved the current study.

This work was supported by the National Social Science Foundation Key Projects of China (Grant Nos. 19AGL009).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Adler, M., and Posner, E. A. (2000). Cost-benefit analysis: Legal, economic and philosophical perspective introduction. J. Leg. Stud. 29, 837–842. doi:10.1086/468096

Ai, H., Hu, S., Li, K., and Shao, S. (2020). Environmental regulation, total factor productivity, and enterprise duration: Evidence from China. Bus. Strategy Environ. 29, 2284–2296. doi:10.1002/bse.2502

Akbar, A., Jiang, X., Qureshi, M. A., and Akbar, M. (2021). Does corporate environmental investment impede financial performance of Chinese enterprises? The moderating role of financial constraints. Environ. Sci. Pollut. Res. 28, 58007–58017. doi:10.1007/s11356-021-14736-2

Alciatore, M., and Carol, D. (2006). Environmental disclosures in the oil and gas industry. Adv. Environ. Account. Manag. 3, 49–75. doi:10.1016/S1479-3598(06)03002-0

Ali, W., Wilson, J., and Husnain, M. (2022). Determinants/motivations of corporate social responsibility disclosure in developing economies: A survey of the extant literature. Sustainability 14 (6), 3474. doi:10.3390/su14063474

Anwar, M., Rahman, S., and Kabir, M. N. (2021). Does national carbon pricing policy affect voluntary environmental disclosures? A global evidence. Environ. Econ. Policy Stud. 23 (2), 211–244. doi:10.1007/s10018-020-00287-2

Bernard, D., Kaya, D., and Wertz, J. (2021). Entry and capital structure mimicking in concentrated markets: The role of incumbents’ financial disclosures. J. Account. Econ. 71, 101379. doi:10.1016/j.jacceco.2020.101379

Bertrand, M., Duflo, E., and Mullainathan, S. (2004). How much should we trust differences in differences estimates? Q. J. Econ. 119, 249–275. doi:10.1162/003355304772839588

Beyers, J., and Arras, S. (2020). Stakeholder consultations and the legitimacy of regulatory decision-making: A survey experiment in Belgium. Regul. Gov. 15, 877–893. doi:10.1111/rego.12323

Blacconiere, W. G., and Patten, D. M. (1994). Environmental disclosures, regulatory costs, and changes in firm value. J. Account. Econ. 18, 357–377. doi:10.1016/0165-4101(94)90026-4

Cai, X., Zhu, B. Z., Zhang, H. J., Li, L., and Xie, M. Y. (2020). Can direct environmental regulation promote green Technology innovation in heavily polluting industries? Evidence from Chinese listed companies. Sci. Total Environ. 746, 140810. doi:10.1016/j.scitotenv.2020.140810

Caputo, F., Pizzi, S., Ligorio, L., and Leopizzi, R. (2021). Enhancing environmental information transparency through corporate social responsibility reporting regulation. Bus. Strategy Environ. 30 (8), 3470–3484. doi:10.1002/bse.2814

Chen, X., Li, X. X., and Huang, X. Y. (2022). The impact of corporate characteristics and external pressure on environmental information disclosure: A model using environmental management as a mediator. Environ. Sci. Pollut. Res. 29 (9), 12797–12809. doi:10.1007/s11356-020-11410-x

Chen, Y. J., Li, P., and Lu, Y. (2018). Career concerns and multitasking local bureaucrats: Evidence of a target-based performance evaluation system in China. J. Dev. Econ. 133, 84–101. doi:10.1016/j.jdeveco.2018.02.001

Cheng, Z. C., Chen, X. Y., and Wen, H. W. (2022). How does environmental protection tax affect corporate environmental investment? Evidence from Chinese listed enterprises. Sustainability 14 (5), 2932. doi:10.3390/su14052932

Cohen, M., and Santhakumar, V. (2007). Information disclosure as environmental regulation: A theoretical analysis. Environ. Resour. Econ. (Dordr). 37 (3), 599–620. doi:10.1007/s10640-006-9052-9

Deegan, C., and Rankin, M. (1996). Do Australian companies report environmental news objectively? An analysis of environmental disclosures by firms prosecuted successfully by the environmental protection authority. Account. Audit account. J 9, 50–67. doi:10.1108/09513579610116358

Delgado-Márquez, B. L., Pedauga, L. E., and Cordón-Pozo, E. (2017). Industries regulation and firm environmental disclosure: A stakeholders’ perspective on the importance of legitimation and international activities. Organ. Environ. 30 (2), 103–121. doi:10.1177/1086026615622028

Deng, X., Huang, B. X., Zheng, Q. Y., and Ren, X. H. (2022). Can environmental governance and corporate performance be balanced in the context of carbon neutrality? - a quasi-natural experiment of central environmental inspections. Front. Energy Res. 10, 852286. doi:10.3389/fenrg.2022.852286

Ding, X. N., Qu, Y., and Shahzad, M. (2019). The impact of environmental administrative penalties on the disclosure of environmental information. Sustainability 11 (20), 5820. doi:10.3390/su11205820

Dong, F., and Zheng, L. (2022). The impact of market-incentive environmental regulation on the development of the new energy vehicle industry: A quasi-natural experiment based on China’s dual-credit policy. Environ. Sci. Pollut. Res. 29, 5863–5880. doi:10.1007/s11356-021-16036-1

Du, M., Chai, S., Wei, W., Wang, S., and Li, Z. (2022). Will environmental information disclosure affect bank credit decisions and corporate debt financing costs? Evidence from China’s heavily polluting industries. Environ. Sci. Pollut. Res. 29, 47661–47672. doi:10.1007/s11356-022-19229-4

Du, W., Wang, F., and Li, M. (2020). Effects of environmental regulation on capacity utilization: Evidence from energy enterprises in China. Ecol. Indic. 113, 106217. doi:10.1016/j.ecolind.2020.106217

Dyduch, J., and Krasodomska, J. (2017). Determinants of corporate social responsibility disclosure: An empirical study of polish listed companies. Sustainability 9 (11), 1934. doi:10.3390/su9111934

Ervits, I. (2021). CSR reporting in China’s private and state-owned enterprises: A mixed methods comparative analysis. Asian Bus. manage. doi:10.1057/s41291-021-00147-1

Fan, L., Yang, K., and Liu, L. (2020). New media environment, environmental information disclosure and firm valuation: Evidence from high-polluting enterprises in China. J. Clean. Prod. 277, 123253. doi:10.1016/j.jclepro.2020.123253

Fang, Z. W., Li, Z. H., and Tao, S. (2022). Environmental information disclosure, fiscal decentralization, and exports: Evidence from China. Front. Environ. Sci. 10, 813786. doi:10.3389/fenvs.2022.813786

Fang, Z., Kong, X., Sensoy, A., Cui, X., and Cheng, F. (2021). Government’s awareness of environmental protection and corporate green innovation: A natural experiment from the new environmental protection law in China. Econ. Anal. Policy 70, 294–312. doi:10.1016/j.eap.2021.03.003

Ford, J. A., Steen, J., and Verreynne, M. L. (2014). How environmental regulations affect innovation in the Australian oil and gas industry: Going beyond the porter hypothesis. J. Clean. Prod. 84, 204–213. doi:10.1016/j.jclepro.2013.12.062

Freedman, M., and Stagliano, A. J. (2002). Environmental disclosure by companies involved in initial public offerings. J 15, 94–105. doi:10.1108/09513570210418914

Frondel, M., Horbach, J., and Rennings, K. (2008). What triggers environmental management and innovation? Empirical evidence for Germany. Ecol. Econ. 66, 153–160. doi:10.1016/j.ecolecon.2007.08.016

Ge, T., and Li, J. Y. (2020). The effect of environmental regulation intensity deviation on China’s inclusive growth. Environ. Sci. Pollut. Res. 27 (27), 34158–34171. doi:10.1007/s11356-020-09574-7

Han, C., Wang, Y., and Xu, Y. (2019). Efficiency and multifractality analysis of the Chinese stock market: Evidence from stock indices before and after the 2015 stock market crash. Sustainability 11, 1699. doi:10.3390/su11061699

Hart, O., and Moore, J. (1996). The governance of exchanges: Members’ cooperatives versus outside ownership. Oxf. Rev. Econ. Policy 12, 53–69. doi:10.1093/oxrep/12.4.53

He, Q. H., Wang, Z. L., Wang, G., Zuo, J., Wu, G. D., and Liu, B. S. (2020). To be green or not to be: How environmental regulations shape contractor greenwashing behaviors in construction Projects. Sustain. Cities Soc. 63, 102462. doi:10.1016/j.scs.2020.102462

Ho, K., Yang, L., and Luo, S. (2022). Information disclosure ratings and continuing overreaction: Evidence from the Chinese capital market. J. Bus. Res. 140, 638–656. doi:10.1016/j.jbusres.2021.11.030

Hou, J. D., Zhou, R., Ding, F., and Guo, H. X. (2022). Does the construction of ecological civilization institution system promote the green innovation of enterprises? A quasi-natural experiment based on China’s national ecological civilization pilot zones. Environ. Sci. Pollut. Res. Int. doi:10.1007/s11356-022-20523-4

Hu, Y. Y., Zhu, Y. H., Tucker, J., and Hu, Y. X. (2018). Ownership influence and CSR disclosure in China. Acc. Res. J. 31 (1), 8–21. doi:10.1108/arj-01-2017-0011

Huang, H., Wu, D., and Gaya, J. (2017). Chinese shareholders'’ reaction to the disclosure of environmental violations: A CSR perspective. Int. J. Corp. Soc. Responsib. 2 (1), 12–16. doi:10.1186/s40991-017-0022-z

Huang, X., Jiang, X., Liu, W., and Chen, Q. (2021). Business group-affiliation and corporate social responsibility: Evidence from listed companies in China. Sustainability 13, 2110. doi:10.3390/su13042110

Ingram, R. W., and Chewning, E. G. (1983). The effect of financial disclosure regulation on security market behavior. Account. Rev. 58 (3), 562–581.

Jiang, L., Lin, C., and Lin, P. (2014). The determinants of pollution levels: Firm-level evidence from Chinese manufacturing. J. Comp. Econ. 42, 118–142. doi:10.1016/j.jce.2013.07.007

Kathiravan, C., Selvam, M., Venkateswar, S., and Balakrishnan, S. (2021). Investor behavior and weather factors: Evidences from asian region. Ann. Oper. Res. 299, 349–373. doi:10.1007/s10479-019-03335-7

Kerret, D., Menahem, G., and Sagi, R. (2010). Effects of the design of environmental disclosure regulation on information provision: The case of Israeli securities regulation. Environ. Sci. Technol. 44 (21), 8022–8029. doi:10.1021/es102361k

Lee, E. (2010). Information disclosure and environmental regulation: Green lights and gray areas. Regul. Gov. 4 (3), 303–328. doi:10.1111/j.1748-5991.2010.01087.x

Lee, K-H. (2017). Does size matter? Evaluating corporate environmental disclosure in the Australian mining and metal industry: A combined approach of quantity and quality measurement. Bus. Strategy Environ. 26, 209–223. doi:10.1002/bse.1910

Li, B., Gao, F. Y., and Zeng, Y. T. (2020). Impact of air pollution on corporate environmental information disclosure: Evidence from China. J. Environ. Prot. Ecol. 21 (5), 1628–1638.

Li, S., Liu, J. J., and Shi, D. Q. (2021). The impact of emissions trading system on corporate energy efficiency: Evidence from a quasi-natural experiment in China. Energy 233, 121129. doi:10.1016/j.energy.2021.121129

Lin, Y. T., Huang, R. T., and Yao, X. (2021). Air pollution and environmental information disclosure: An empirical study based on heavy polluting industries. J. Clean. Prod. 278, 124313. doi:10.1016/j.jclepro.2020.124313

Liu, X. B., and Anbumozhi, V. (2009a). Determinant factors of corporate environmental information disclosure: An empirical study of Chinese listed companies. J. Clean. Prod. 17 (6), 593–600. doi:10.1016/j.jclepro.2008.10.001

Liu, X. B., Yu, Q. Q., Fujitsuka, T., Liu, B. B., Bi, J., and Shishime, T. (2010). Functional mechanisms of mandatory corporate environmental disclosure: An empirical study in China. J. Clean. Prod. 18 (8), 823–832. doi:10.1016/j.jclepro.2009.12.022

Liu, X., and Anbumozhi, V. (2009b). Determinant factors of corporate environmental information disclosure: An empirical study of Chinese listed companies. J. Clean. Prod. 17, 593–600. doi:10.1016/j.jclepro.2008.10.001

Liu, Y., Failler, P., and Chen, L. (2021a). Can mandatory disclosure policies promote corporate environmental responsibility?-quasi-natural experimental research on China. Int. J. Environ. Res. Public Health 18 (11), 6033. doi:10.3390/ijerph18116033

Liu, Y., Liu, M., Wang, G., Zhao, L., and An, P. (2021b). Effect of environmental regulation on high-quality economic development in China-an empirical analysis based on dynamic spatial durbin model. Environ. Sci. Pollut. Res. 28 (39), 54661–54678. doi:10.1007/s11356-021-13780-2

Liu, Y., Wang, A., and Wu, Y. (2021c). Environmental regulation and green innovation: Evidence from China’s new environmental protection law. J. Clean. Prod. 297, 126698. doi:10.1016/j.jclepro.2021.126698

Liu, Z. B., and Bai, Y. (2022). The impact of ownership structure and environmental supervision on the environmental accounting information disclosure quality of high-polluting enterprises in China. Environ. Sci. Pollut. Res. 29 (15), 21348–21364. doi:10.1007/s11356-021-17357-x

Lu, J., and Li, H. (2020). The impact of government environmental information disclosure on enterprise location choices: Heterogeneity and threshold effect test. J. Clean. Prod. 277, 124055. doi:10.1016/j.jclepro.2020.124055

Luo, Y., Xiong, G., and Mardani, A. (2022). Environmental information disclosure and corporate innovation: The “inverted U-shaped” regulating effect of media attention. J. Bus. Res. 146, 453–463. doi:10.1016/j.jbusres.2022.03.089

Ma, R. W., Li, F. F., and Du, M. Y. (2022). How does environmental regulation and digital finance affect green technological innovation: Evidence from China. Front. Environ. Sci. 10, 928320. doi:10.3389/fenvs.2022.928320

Maassen, G. F., Van Den Bosch, F. a. J., and Volberda, H. (2004). The importance of disclosure in corporate governance self-regulation across europe: A review of the winter report and the EU action plan. Int. J. Discl. Gov. 1 (2), 146–159. doi:10.1057/palgrave.jdg.2040020

Mateo‐Márquez, A. J., González‐González, J. M., and Zamora‐Ramírez, C. (2021). The influence of countries’ climate change‐related institutional profile on voluntary environmental disclosures. Bus. Strategy Environ. 30 (2), 1357–1373. doi:10.1002/bse.2690

Meng, J., and Zhang, Z. (2022). Corporate environmental information disclosure and investor response: Evidence from China’s capital market. Energy Econ. 108, 105886. doi:10.1016/j.eneco.2022.105886

Meng, X., Zeng, S., Tam, C., and Xu, X. D. (2013). Whether top executives’ turnover influences environmental responsibility: From the perspective of environmental information disclosure. J. Bus. Ethics 114, 341–353. doi:10.1007/s10551-012-1351-1

Ng, A. W. (2018). From sustainability accounting to a green financing system: Institutional legitimacy and market heterogeneity in a global financial centre. J. Clean. Prod. 195, 585–592. doi:10.1016/j.jclepro.2018.05.250

Nourayi, M. M. (1994). Stock price responses to the SEC’s enforcement actions. J. Account. Public Policy 13, 333–347. doi:10.1016/0278-4254(94)90003-5

Patten, D. M., and Nance, J. R. (1998). Regulatory cost effects in a good news environment: The intra-industry reaction to the alaskan oil spill. J. Account. Public Policy 17, 409–429. doi:10.1016/S0278-4254(98)10007-8

Pham, H. N. A., Ramiah, V., and Moosa, I. (2020). The effects of environmental regulation on the stock market: The French experience. Acc. Finance 60 (4), 3279–3304. doi:10.1111/acfi.12469

Polishchuk, L. (2009). Corporate social responsibility or government regulation: An analysis of institutional choice. Problems Econ. Transition 52 (8), 73–94. doi:10.2753/PET1061-1991520805

Porter, M. E., and linde, C. V. D. (1995). Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 9, 97–118. doi:10.1257/jep.9.4.97

Pritchard, A. (2003). Self-regulation and securities markets. SSRN J. 26, 32–39. doi:10.2139/ssrn.318939

Qi, G., Jia, Y., and Zou, H. (2021). Is institutional pressure the mother of green innovation? Examining the moderating effect of absorptive capacity. J. Clean. Prod. 278, 123957. doi:10.1016/j.jclepro.2020.123957

Ramanathan, R., Ramanathan, U., and Bentley, Y. (2018). The debate on flexibility of environmental regulations, innovation capabilities and financial performance-A novel use of DEA. Omega 75, 131–138. doi:10.1016/j.omega.2017.02.006

Ren, S. G., Wei, W. J., Sun, H. L., Xu, Q. Y., Hu, Y. C., and Chen, X. H. (2020). Can mandatory environmental information disclosure achieve a win-win for a firm’s environmental and economic performance? J. Clean. Prod. 250, 119530. doi:10.1016/j.jclepro.2019.119530

Ruan, L., and Liu, H. (2021). Environmental, social, governance activities and firm performance: Evidence from China. Sustainability 13, 767. doi:10.3390/su13020767

Schulte, D. J. (1988). The debatable case for securities disclosure regulation. J. Corp. Law 13 (2), 535.

Senn, J., and Giordano-Spring, S. (2020). The limits of environmental accounting disclosure: Enforcement of regulations, standards and interpretative strategies. Accounting. Auditing Account. J. 33 (6), 1367–1393. doi:10.1108/AAAJ-04-2018-3461

Stanny, E. (1998). Effect of regulation on changes in disclosure of and reserved amounts for environmental liabilities. J. Financial Statement Analysis 3 (4), 34–49.

Stocken, P. C. (2022). Disclosure regulation and incentive uncertainty. Account. Finance 62 (2), 2267–2281. doi:10.1111/acfi.12862

Suarez-Rico, Y. M., Gomez-Villegas, M., and Garcia-Benau, M. A. (2018). Exploring twitter for CSR disclosure: Influence of CEO and firm characteristics in Latin American companies. Sustainability 10 (8), 2617. doi:10.3390/su10082617

Sun, H., Zhang, Z., and Liu, Z. (2022). Does air pollution collaborative governance promote green Technology innovation? Evidence from China. Environ. Sci. Pollut. Res. 29, 51609–51622. doi:10.1007/s11356-022-19535-x

Tang, H. L., Liu, J. M., and Wu, J. G. (2020). The impact of command-and-control environmental regulation on enterprise total factor productivity: A quasi-natural experiment based on China’s “two control zone” policy. J. Clean. Prod. 254, 120011. doi:10.1016/j.jclepro.2020.120011

Tollefson, J. (2007). Pressure for environmental disclosure increases. Nature 449 (7161), 383. doi:10.1038/449383a

Topalova, P. (2010). Factor immobility and regional impacts of trade liberalization: Evidence on poverty from India. Am. Econ. J. Appl. Econ. 2, 1–41. doi:10.5089/9781455208838.001

Tzouvanas, P., Kizys, R., Chatziantoniou, I., and Sagitova, R. (2020). Environmental disclosure and idiosyncratic risk in the European manufacturing sector. Energy Econ. 87, 104715. doi:10.1016/j.eneco.2020.104715

Unermana, J., and O’Dwyer, B. (2007). The business case for regulation of corporate social responsibility and accountability. Account. Forum 31, 332–353. doi:10.1016/j.accfor.2007.08.002

Van Rooij, B., and Lo, C. W. H. (2010). Fragile convergence: Understanding variation in the enforcement of China’s industrial pollution law. Law Policy 32, 14–37. doi:10.1111/J.1467-9930.2009.00309.X

Wang, F., Yang, S. Y., Reisner, A., and Liu, N. (2019). Does green credit policy work in China? The correlation between green credit and corporate environmental information disclosure quality. Sustainability 11 (3), 733. doi:10.3390/su11030733

Wang, K., Zhao, B., Ding, L., and Miao, Z. (2021). Government intervention, market development, and pollution emission efficiency: Evidence from China. Sci. Total Environ. 757, 143738. doi:10.1016/j.scitotenv.2020.143738

Wang, M. Z., and Chen, Y. G. (2017). Does voluntary corporate social performance attract institutional investment? Evidence from China. Corp. Gov. 25, 338–357. doi:10.1111/corg.12205

Wang, S., and Hao, J. (2012). Air quality management in China: Issues, challenges, and options. J. Environ. Sci. 24, 2–13. doi:10.1016/S1001-0742(11)60724-9

Wilestari, M., Syakhroza, A., Djakman, C. D., and Diyanty, V. (2021). The influence of regulation and financial performance on the disclosure of corporate social responsibility and corporate reputation moderated by ownership structure. Acc. Fin. Rev. 5 (4), 13–22. doi:10.35609/10.35609/afr.2021.5.4(2

Wiseman, J. (1982). An evaluation of environmental disclosures made in corporate annual reports. Account. Organ. Soc. 7, 53–63. doi:10.1016/0361-3682(82)90025-3

Wu, D., and Memon, H. (2022). Public pressure, environmental policy uncertainty, and enterprises'’ environmental information disclosure. Sustainability 14 (12), 6948. doi:10.3390/su14126948

Xue, J., He, Y. S., Liu, M., Tang, Y., and Xu, H. Y. (2021). Incentives for corporate environmental information disclosure in China: Public media pressure, local government supervision and interactive effects. Sustainability 13 (18), 10016. doi:10.3390/su131810016

Yan, Y., and Qi, W. (2021). The impact of capital market opening on stock market stability: Based on D-MST method complex Network perspective. Ann. Oper. Res. doi:10.1007/s10479-021-04289-5

Yang, J., Shi, D., and Yang, W. (2022a). Stringent environmental regulation and capital structure: The effect of NEPL on deleveraging the high polluting firms. Int. Rev. Econ. Finance 79, 643–656. doi:10.1016/j.iref.2022.02.020

Yang, Y., Yang, F., and Zhao, X. (2022b). The impact of the quality of environmental information disclosure on financial performance: The moderating effect of internal and external stakeholders. Environ. Sci. Pollut. Res. Int. doi:10.1007/s11356-022-20553-y

Yekini, K., Adelopo, I., Wang, Y., and Song, S. (2019). Post-regulation effect on factors driving environmental disclosures among Chinese listed firms. Account. Res. J. 32 (3), 477–495. doi:10.1108/ARJ-01-2017-0018

Younis, I., Naz, A., Shah, S. A. A., Nadeem, M., and Cheng, L. (2021). Impact of stock market, renewable energy consumption and urbanization on environmental degradation: New evidence from BRICS countries. Environ. Sci. Pollut. Res. Int. 28, 31549–31565. doi:10.1007/s11356-021-12731-1

Yu, B., and Shen, C. (2020). Environmental regulation and industrial capacity utilization: An empirical study of China. J. Clean. Prod. 246, 118986. doi:10.1016/j.jclepro.2019.118986

Zeng, H., Zhang, X., Zhou, Q., Jin, Y., and Cao, J. (2022). Tightening of environmental regulations and corporate environmental irresponsibility: A quasi-natural experiment. Environ. Dev. Sustain. doi:10.1007/s10668-021-01988-8

Zeng, H., Dong, B., Zhou, Q., and Jin, Y. (2021). The capital market reaction to central environmental protection inspection: Evidence from China. J. Clean. Prod. 279, 123486. doi:10.1016/j.jclepro.2020.123486

Zeng, S. X., Xu, X. D., Dong, Z. Y., and Tam, V. W. Y. (2010). Towards corporate environmental information disclosure: An empirical study in China. J. Clean. Prod. 18 (12), 1142–1148. doi:10.1016/j.jclepro.2010.04.005

Zhang, B., Fei, H., Zhang, Y., and Liu, B. (2015). Regulatory uncertainty and corporate pollution control strategies: An empirical study of the “pay for permit” policy in the tai lake basin. Environ. Plann. C. Gov. Policy 33, 118–135. doi:10.1068/c12101

Zhang, C., and Cheng, J. K. (2022). Environmental regulation and corporate cash holdings: Evidence from China’s new environmental protection law. Front. Environ. Sci. 10, 835301. doi:10.3389/fenvs.2022.835301

Zhang, H., Xu, T., and Feng, C. (2022a). Does public participation promote environmental efficiency? Evidence from a quasi-natural experiment of environmental information disclosure in China. Energy Econ. 108, 105871. doi:10.1016/j.eneco.2022.105871

Zhang, L., Arthur, P. J. M., He, G., and Lu, Y. (2010). An implementation assessment of China’s environmental information disclosure decree. J. Environ. Sci. 22, 1649–1656. doi:10.1016/S1001-0742(09)60302-8

Zhang, Q., Chen, W. Y., and Feng, Y. C. (2021). The effectiveness of China’s environmental information disclosure at the corporate level: Empirical evidence from a quasi-natural experiment. Resour. Conservation Recycl. 164, 105158. doi:10.1016/j.resconrec.2020.105158

Zhang, Y., Hu, H. Y., Zhu, G. J., and You, D. M. (2022b). The impact of environmental regulation on enterprises’ green innovation under the constraint of external financing: Evidence from China’s industrial firms. Environ. Sci. Pollut. Res. Int. 22. doi:10.1007/s11356-022-18712-2

Zhao, T., Zhou, H. H., Jiang, J. D., and Yan, W. Y. (2022). Impact of green finance and environmental regulations on the green innovation efficiency in China. Sustainability 14 (6), 3206. doi:10.3390/su14063206

Zhao, X., Fan, Y., Fang, M., and Hua, Z. (2018). Do environmental regulations undermine energy firm performance? An empirical analysis from China’s stock market. Energy Res. Soc. Sci. 40, 220–231. doi:10.1016/j.erss.2018.02.014

Zheng, Y., Ge, C., Li, X., Duan, X., and Yu, T. (2020). Configurational analysis of environmental information disclosure: Evidence from China’s key pollutant-discharge listed companies. J. Environ. Manage. 270, 110671. doi:10.1016/j.jenvman.2020.110671

Zhi, H. J., Ni, L. Y., and Zhu, D. D. (2022). The impact of emission trading system on clean energy consumption of enterprises: Evidence from A quasi-natural experiment in China. J. Environ. Manage. 318, 115613. doi:10.1016/j.jenvman.2022.115613

Keywords: corporate social responsibility (CSR) regulation, environmental information disclosure, listed companies, capital market, shenzhen stock exchange (SZSE), difference-in-differences (DiD)

Citation: Zhang C, Zhang Y, Zhang S, Hou M and Chen Y (2022) Corporate social responsibility regulation in capital market and environmental information disclosure of listed companies: A quasi-natural experiment from China. Front. Environ. Sci. 10:1015061. doi: 10.3389/fenvs.2022.1015061

Received: 09 August 2022; Accepted: 13 September 2022;

Published: 04 October 2022.

Edited by:

Lu Yang, Shenzhen University, ChinaReviewed by:

Shahid Ali, Nanjing University of Information Science and Technology, ChinaCopyright © 2022 Zhang, Zhang, Zhang, Hou and Chen. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Changjiang Zhang, emNqQG5qdGVjaC5lZHUuY24=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.