Pina Murè

Pina Murè Saverio Giorgio

Saverio Giorgio Valeria Antonelli

Valeria Antonelli Antonino Crisafulli

Antonino Crisafulli- 1Dipartimento di Management, Università degli Studi di Roma “La Sapienza”, Rome, Italy

- 2Dipartimento di Medicina Traslazionale e di Precisione, Università degli Studi di Roma “La Sapienza”, Rome, Italy

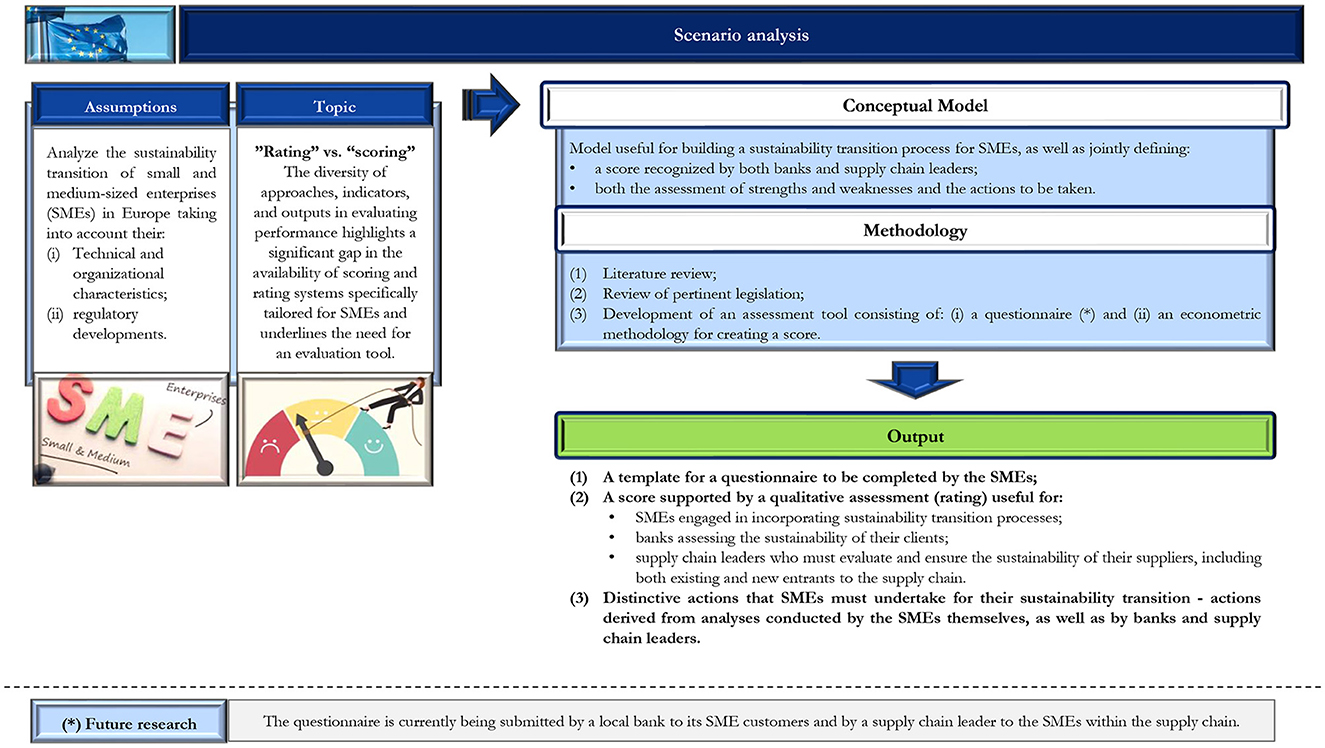

This paper aims to contribute to the ongoing discourse regarding the distinctions and application of scoring and rating systems by presenting a conceptual model designed to assess and self-assess small and medium-sized enterprises (hereinafter also “SMEs”) on their sustainability transition. Indeed, SMEs operate in very different economic contexts and have simplified organizational and governance structures. These characteristics can be effectively captured through this conceptual model based on a customized questionnaire tailored to the specificities of SMEs. Following an analysis of existing literature and regulatory frameworks, a conceptual model is proposed that includes a questionnaire that, unlike commonly proposed industry questionnaires, is designed to generate an Environmental, Social and Governance (hereinafter also “ESG”) Score complemented by a forward-looking perspective. This model can be useful for SMEs, as it allows them to self-assess their strengths and weaknesses in the sustainability transition process, highlighting specific needs and suggesting actions to improve their sustainability transition. It also allows banks to make a more accurate assessment of the sustainability of their customers, facilitating the redefinition of green and social credit products according to the needs of SMEs. Additionally, it also supports supply chain leaders in ensuring a sustainable supply chain by facilitating the sustainability assessment of SMEs. This is so that everything complies with the new European Union (hereinafter also “EU”) regulations. Finally, the questionnaire is currently being tested at a local bank and has been proposed to SME suppliers in a specific supply chain. It will be possible to make changes to the questionnaire based on the feedback received during the administration phase.

Graphical Abstract.

1 Introduction

This study aims to propose a conceptual model that can be utilized by both banks and supply chain leaders to assess the characteristics of SMEs, as well as by SMEs themselves for self-assessment purposes during their process of sustainability transition: a course of large-scale societal changes, necessary to solve societal challenges (Loorbach et al., 2017).

This is due to the consideration of the EU regulatory evolution concerning ESG factors, including the Non-Financial Reporting Directive [NFRD, European Parliament and Council (2014) Directive 2014/95/EU], the Corporate Sustainability Reporting Directive [CSRD, European Parliament and Council (2022) Directive EU 2022/2464], European Parliament and Council (2020) Regulation 2020/852 (Taxonomy Regulation), the Corporate Sustainability Due Diligence Directive [CSDDD, European Parliament and Council (2024a) Directive (EU) 2024/1760], and the Proposal for a Regulation of the European Parliament and Council on the transparency and integrity of ESG Rating activities (European Parliament and Council, 2023), along with the various obligations that SMEs are required to comply with in a short timeframe. Additionally, the literature addressing the confusion surrounding these instruments (La Torre et al., 2020; Capizzi et al., 2021; Berg et al., 2022; Lee and Raschke, 2023; Lee et al., 2023) is analyzed to contribute to the debate clarifying the distinction between ESG Score and ESG Rating (BCBS, 2004; Altman and Sabato, 2008; Del Pozzo, 2011; Resti and Sironi, 2021), aiming to highlight how both currently fail to adequately capture the sustainability characteristics of SMEs.

Currently, SMEs exhibit significant deficiencies in their sustainability transition, particularly regarding: (i) the “Governance” factor, which is often addressed by scoring/rating companies through the use of proxies; (ii) the “Social” factor, which, due to the absence of a taxonomy and the lack of specific indicators, is even more neglected, leading to a subjective assessment by rating/scoring companies. In contrast, the “Environmental” factor is more developed, as it is subject to more stringent regulation.

These results highlight the need to develop a conceptual model that can serve as a basis for the creation of an ESG score specifically adapted to the characteristics of European SMEs and that highlights the evaluation/rating of strengths and weaknesses in addition to actions to be taken by SMEs for the sustainability transition.

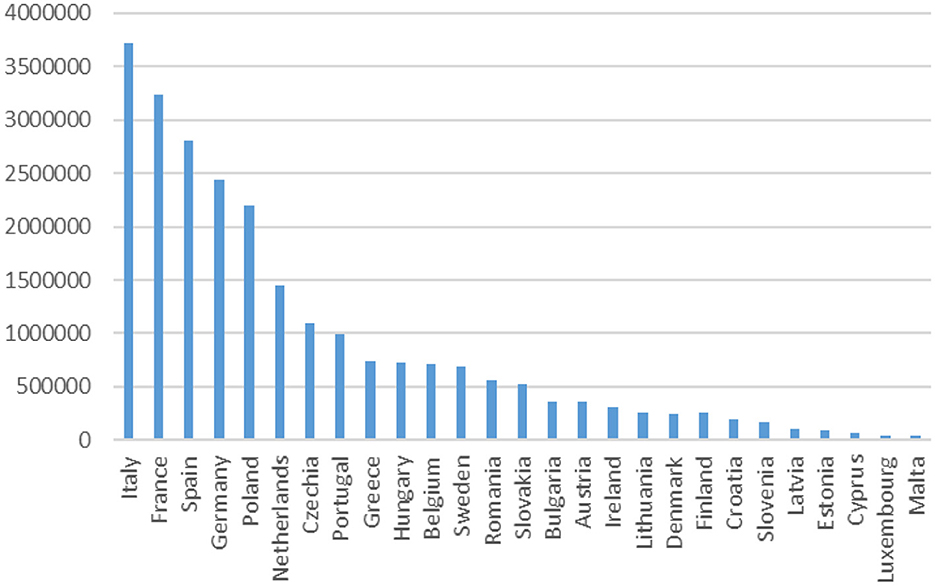

A model such as this can be useful to assess the stage in the process toward sustainability in which SMEs find themselves, but to do so it is necessary to be aware of the context of SMEs in Europe: according to the most recent report on SMEs released by the European Commission, as of 2022, 99% of European companies were part of the “SME” category, a percentage that is equivalent to as many as 24,281,159 SMEs (see Figure 1) mainly in the wholesale and retail trade (24%), professional, scientific, and technical activities (20%), and Construction (15%) sectors (Di Bella et al., 2023).

Figure 1. Number of SMEs for countries of the European Union. Own elaboration on Eurostat and European Commission Data.

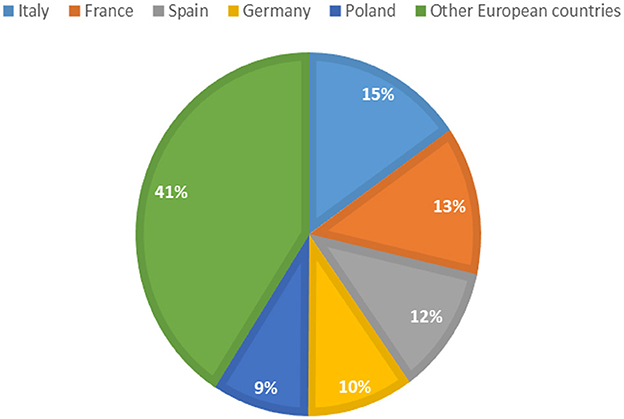

These are therefore the basis of the European industrial sector. Most of these SMEs are concentrated in Italy, France, Spain, Germany, and Poland (see Figure 2). Of these SMEs, many are included in supply chains and influence their sustainability.

Figure 2. Number of SMEs- focus on the top 5 countries in the European Union for number of SMEs. Own elaboration on Eurostat and European Commission Data.

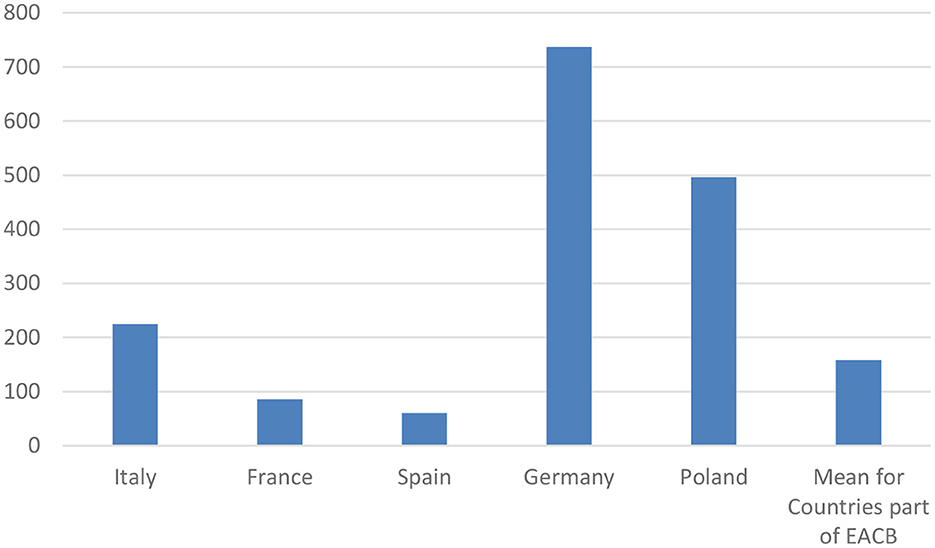

Another key feature is the importance of the relationship between SMEs and local banks which, by providing financial support, as well as helping SMEs in the sustainability transition, generate positive effects on their economic activity (Meslier et al., 2022). This is often done by cooperative banks (Crovini et al., 2018). To show this relation, Figure 3 shows the number of cooperative banks in the top 5 EU Countries for number of SMEs using data from the European Association of Cooperative Banks (hereinafter also “EACB”). The figure also shows the mean of banks situated in Countries that have associations as part of the EACB to highlight that 3 out of 5 of the top 5 EU Countries for number of SMEs have a number of cooperative banks higher than the mean, suggesting a relation between the two characteristics (see Figure 3).

Figure 3. Number of cooperative banks in the top 5 countries in the European Union for number of SMEs. Own elaboration on EACB Data.

Given this context, the conceptual model starts from the analysis of the questionnaire of an Italian data provider used by banks and supply chain leaders. Subsequently, since the proposed questionnaire does not reflect the peculiarities and characteristics of SMEs, a new questionnaire based on the specificities of SMEs is created.

The conceptual model proposed as a result of this research provides a holistic view focusing on the role of several key actors, including banks and supply chain leaders, that support SMEs in promoting their long-term sustainability. In particular, it can be useful for banks to assess the characteristics of SMEs before granting “green” or “social” financing, thereby facilitating the disbursement process and evaluating the impact on the probability of default (also “PD”).

Furthermore, while acknowledging that regulations do not impose direct obligations on SMEs, supply chain leaders are beginning to require sustainability standards from their suppliers. This could result in the exclusion of SMEs that do not comply with such requirements, making it urgent to implement a model that fosters a culture of sustainability within these SMEs.

Although the model is useful to banks and supply chain leaders, it does not neglect the importance of consumers: they, in fact, gain access to more sustainable products as a results of the improved sustainability of companies. In addition, the consumer is always the fulcrum of the policies of banks and companies: the bank with green and social credit products, for the Environmental and Social perspective, supports consumers with incentives (e.g., green mortgages); companies also benefit from the sale of green and social products to increase their reputation and push for this sale, bringing consumers closer to this perspective through adequate product offerings and marketing and communication strategies that focus on the characteristics most observed by consumers, such as: recyclability of the packaging, fair payment of producers, low energy use and low carbon dioxide emissions during production and shipping (Hanss and Böhm, 2012). To take this into account, some questions from the Governance and Environmental sections of the proposed questionnaire focus on this perspective.

Therefore, considering the role of sustainability in these different perspectives, the need for self-assessment is crucial to ensure that SMEs understand the importance of sustainability, particularly in the production process, and to facilitate the transition toward more responsible practices that align with emerging regulations.

This approach does not intend to replace a rating or scoring system; rather, it aims to facilitate a self-assessment for SMEs that serves as a preliminary step toward measurement in line with the developments in regulation. It highlights the importance of solid Governance as a foundation for an effective transition to sustainable practices.

The aim of this paper is to present a conceptual model for the assessment of SMEs by banks and supply chain leaders, as well as for the self-assessment of the sustainability of SMEs. This model is developed in response to a still incomplete regulation and the specific characteristics of SMEs (mainly simplified governance and lack of normative for sustainability transition), with the aim of supporting the transition to sustainability from the point of view of banks, considering their relationship with companies, and supply chain leaders. It is therefore essential, to adopt the perspective of these actors, to identify key elements for the ESG performance of SMEs, highlighting the state of the art and the actions to be taken from a forward-looking perspective in order to be compliant with regulations. From a banking perspective, SMEs need to make sure they meet the requirements to obtain green and social credit products from banks. From a supply chain leader perspective, SMEs need to ensure that they meet the requirements to be chosen by supply chain leaders for their sustainable supply chains. To do this, SMEs will have to carry out a self-assessment of their sustainability and understand what actions to take in the sustainability transition process. Based on an existing questionnaire offered by a data provider, a new one has been created to provide a self-diagnosis and assessment perspective to highlight the weaknesses of SMEs in the sustainability transition and the actions to be taken to improve in this perspective. Once the results have been obtained, it will be possible to understand whether the questionnaire has adequately captured the problems of SMEs. The next steps will be (i) the proposal of interventions by banks and supply chain leaders to improve the sustainability prospects of SMEs and (ii) the implementation of an econometric methodology on the conceptual model, taking inspiration from what has been proposed, to derive an ESG score for SMEs.

The paper is structured as follows: this Section 1 presents the introduction and reconstructs the scope of the research; the following Section 2 reconstructs the normative review and presents the literature review. Section 3 presents the research methods used in this paper. This is followed by Section 4 which presents the architecture of the conceptual model and its implications. And finally, Section 5 presents conclusions and identifies limits and possible future research perspectives.

2 Normative context and literature review

The main assumption underlying this study is that both EU legislation, scientific literature and current market practices highlight how providers and rating agencies mainly focus on the analysis of large companies (Zumente and Lāce, 2021), which are currently more regulated from a sustainability perspective, unlike SMEs,1 although they have a huge importance in Europe, as they represent 99% of European companies (Udell, 2020), they suffer from a lack of regulation in this regard.

In fact, large companies are subject to reporting obligations following the introduction of the NFRD in 2014. In particular, the NFRD established the obligation for large companies to prepare the non-financial declaration (also “NFD”) focusing mainly on environmental and social aspects. It was later amended by the CSRD, which imposes new sustainability reporting requirements aimed at promoting greater transparency and accountability in corporate sustainability practices. The CSRD not only addresses large companies, but also requires SMEs pointed by the normative to report on sustainability starting from 2026. All companies subject to the CSRD must report their sustainability-related information according to the European Sustainability Reporting Standards (hereinafter also “ESRS”), which have been adopted by the European Commission through delegated acts, taking into account the technical advice provided by the European Financial Reporting Advisory Group (hereinafter also “EFRAG”). On 25 December 2023, the European Commission approved, through Delegated Regulation (EU) 2023/2772, a first set of ESRS standards, divided into cross-cutting and thematic standards. The first two standards deal with general requirements and themes, while five standards are dedicated to the Environment, four to Social and one to Governance. In addition, the concept of double materiality is introduced, which requires companies to consider both the impact of their activities on sustainability issues and how these issues affect their business performance. Currently, SMEs are exempt from non-financial reporting requirements. However, EFRAG has been tasked with developing simplified standards for listed SMEs (hereinafter also “LSME”), known as ESRS LSME, and a voluntary standard for non-listed SMEs, called VSME. The EU Platform on Sustainable Finance believes that EFRAG's ESRS LSME and VSME should assist SMEs in the following ways (EU Platform on Sustainable Finance, 2024): (i) facilitate decarbonization, resilient and greening activities; (ii) access to sustainable finance (green and/or transitional); (iii) address the cascading effects of the regulatory framework on sustainable financing, as SMEs should be supported in managing requests for information from large companies that are required to report non-financial information. ESRS are integrated with the Global Reporting Initiative (hereinafter also “GRI”) Standards, defined by the GRI, an organization founded in 1997, which provides a variety of topics related to sustainability, the protection of human rights and Governance, with the aim of promoting a sustainable world economy in which organizations responsibly manage and transparently communicate their performance and their economic and ESG impacts (Luo and Tang, 2023) and avoid phenomena such as “greenwashing2” and “social washing”3 in financial and institutional communication. The standards are divided into (i) universal standards (GRI 1, GRI 2, and GRI 3): they apply to all organizations, regardless of sector or size; (ii) Industry standards (GRI 11, GRI 12, and GRI 13): they are specific to certain sectors and are designed to address the peculiarities and reporting needs of each sector; (iii) Specific standards (GRI 101; GRI 201 to GRI 207; GRI 301 to GRI 308; GRI 401 to GRI 411; and GRI 413 to GRI 418): they refer to specific topics (e.g., economic performance, health, biodiversity, waste, working conditions, etc.).

Therefore, several stakeholders, including banks and supply chain leaders, who are subject to mandatory regulations, are starting to support SMEs in strengthening their sustainability efforts. Indeed, EU authorities have played a crucial role in developing a targeted regulatory framework, highlighting the importance of the impact of environmental and social risks on the economic and financial stability of both financial institutions (La Torre, 2022) and, more recently, for supply chain leaders.

For banks, the European Commission has introduced the Taxonomy Regulation, aimed at establishing a European classification of sustainable activities by referring to the eligibility and alignment requirements established by the Regulation. In particular, starting from 1 January 2024, financial institutions must publish the Green Asset Ratio4 (also GAR) and the Banking Book Taxonomy Alignment Ratio5 (also BTAR), in order to provide a greater degree of accuracy, transparency and comparability of data in the assessment of green finance activities. The measure aims to mitigate the risk of greenwashing and social washing and to allow a more uniform assessment of the performance and sustainability characteristics of large companies and SMEs. In particular, banks play a crucial role in promoting a sustainability transition (Giorgio, 2023) especially for SMEs, as they are called to play a crucial role in analyzing their financing needs. This is in order to provide “green” or “social” financing more suited to the characteristics of SMEs, such as for the purchase of sustainable materials (Gulzhan et al., 2023), thus improving their ESG performance (Zhang et al., 2024). On the other hand, providing green and social financing allows banks to increase their net interest margin and reduce both the probability of default (Mirza et al., 2023) and credit risk (Tian et al., 2023), also in view of the future capital absorption expected for climate and environmental risks.

For supply chain leaders, the CSDDD has recently been introduced, which focuses on companies' sustainability due diligence and represents a significant step toward greater corporate responsibility for sustainability. This is because supply chains have a major impact on the progress of all the Sustainable Development Goals6 (hereinafter also “SDGs”), given their cross-cutting nature and scope (United Nations Global Compact, 2022). In fact, supply chains are responsible for more than 80% of companies' total environmental impact (Bove and Swartz, 2016), and being part of a sustainable supply chain can improve the public perception of the company (Tamayo-Torres et al., 2019), as integrating ESG factors and related risks into business strategy and models could help them strengthen their resilience (Cardillo et al., 2023). In this sense, sustainability is seen as key to achieving supply chain resilience and economic growth (Jiang et al., 2021). In fact, in recent years, both scholars and practitioners have recognized the importance of broadening the scope of supply chain assessment systems, considering the environmental and social impacts of upstream and downstream organizations (Noci, 1997; Clift, 2003; Kusi-Sarpong et al., 2019; Martins and Pato, 2019). In particular, supply chain leaders are expected to guide SMEs toward sustainability, paying attention to business models and transition plans to reduce emissions by 2029, playing a central role in identifying and implementing more sustainable options (Acquaye et al., 2018). However, SMEs, even if they are not directly subject to the requirements of the CSDDD, will still have to adapt to the requests of supply chain leaders.

These observations highlighted the urgency of developing a conceptual model that can serve as a basis for the creation of an ESG score for SMEs. Therefore, the study aims to introduce a conceptual model that can serve as a basis for the development of an ESG score tailored to the specific needs of European SMEs. This model is not intended to replace traditional ratings, but rather to facilitate a self-assessment process for SMEs, preparing them for measurement in compliance with emerging regulations, highlighting the importance of strong governance as a basis for an effective transition to sustainable practices. It is crucial to note that many SMEs have inadequate governance systems and weaknesses in internal control (Linjie and Xuedong, 2010). According to Broccardo et al. (2019), governance is one of the main determinants of sustainability of SMEs. Strong governance not only improves transparency and accountability, but also helps SMEs integrate ESG principles into their operational strategies. Furthermore, the proposed model, resulting from this research work, offers a holistic view, as it can be used not only by SMEs for self-assessment, but also by banks and supply chain leaders.

In a larger context, both rating and scoring play a key role both for banks for estimating credit losses and regulatory credit risk capital (Roy and Shaw, 2020; Van Dyk and Van Vuuren, 2023) and for supply chain leaders to judge a company on the basis of past financial statements data and on the prospects of the supply chain in which it is included (Sardanelli et al., 2022). While the rating can provide an opinion on the solvency of the counterparty, reflecting the ability of a company to repay its debts, incorporating a qualitative judgment; the score is a numerical evaluation derived from a quantitative analysis based on statistical models that have used a large amount of information regarding the history and performance of the company being evaluated (BCBS, 2004; Altman and Sabato, 2008; Del Pozzo, 2011; Resti and Sironi, 2021). Specifically, credit rating agencies produce a rating upon request from a potential borrower, called a solicited rating (White, 2010); however, they can also provide unsolicited ratings (Gibert, 2020). However, despite the regulatory effort and the existence of many different ESG ratings and scores from different rating agencies (such as Fitch, Moody's, and Standard & Poor's and Cerved Rating Agency) and scoring [Experian, Equifax, Fair Isaac Corporation (FICO) which provides the so-called FICO score] for large companies (Zumente and Lāce, 2021; Drempetic et al., 2020; Kotsantonis and Serafeim, 2019), to date there are only a few agencies providing ESG Scores for SMEs (e.g., Modefinance), as they are taken into account less due to the reduced attention from the regulatory context. Only a few are adapted to the specific characteristics of SMEs and include in their assessments, for example, (i) the presence of basic or absent governance systems; (ii) the need for financial support for sustainability-related initiatives; and (iii) the importance of intangible capital (Selma, 2020).

Furthermore, there is an increasing tendency to consider sustainability indicators, in addition to the more traditional financial and management ones (Mishra et al., 2018) and the integration of ESG factors into investment strategies has become a distinct service offered by many investment service providers (Van Duuren et al., 2016). Thanks to this assessment, it is possible to have a precise knowledge of the commitment of companies toward sustainability, and for this reason ESG ratings and ESG scores will become useful tools for financial institutions to better capture ESG attitudes of enterprises and SMEs (La Torre et al., 2021) and also for supply chain leaders. However, the current ESG ratings market has significant gaps that undermine its optimal functioning, including a lack of: (i) transparency regarding the characteristics, methodologies and sources of ESG ratings data, (ii) clarity on how ESG ratings are evaluated (European Parliament and Council, 2024b), and (iii) ESG ratings and scores suitable to SMEs.

In fact, there are divergences among the ESG ratings provided by different rating agencies, this is because, as underlined by La Torre et al. (2020), ESG rating providers have substantial differences in judgment, methodology and disclosure. As also demonstrated by Capizzi et al. (2021), the divergence between ESG ratings is not only due to differences in analyst ratings, but also disagreement on underlying methodological issues and metrics. This implies that the ESG ratings generated by different rating providers could differ significantly, making it, on the one hand, difficult to evaluate the ESG performance of companies, funds and portfolios and, on the other hand, decreasing the incentives for companies to improve their performance (Berg et al., 2022). Indeed, ESG ratings are based on several comparable ESG metrics that are similar but not the same in terms of scope and measurement (Lee and Raschke, 2023). These differences in scope and measurement lead to even greater divergences in E, S, and G weights in rating agencies' ESG ratings (Lee et al., 2023).

Therefore, in order to improve the reliability and comparability of ESG ratings, the European Parliament adopted on 24 April 2024 the “Proposal for a Regulation of the European Parliament and of the Council on transparency and integrity of environmental, social and governance (ESG) rating activities,” (European Parliament and Council, 2023) thus introducing a common regulatory approach that improves the transparency and integrity of ESG rating providers' operations and prevents potential conflicts of interest. In particular, the regulation identifies four types of ESG ratings currently on the market and assigns them to specific agencies focused on the assessment of: risk (MSCI), impact (Carbon4Finance), compliance with international principles and guidelines (Standard Ethics), and supply chain (EcoVadis). The European Parliament's regulatory proposal is a significant step toward improving the ESG rating system, but also highlights the need for a more inclusive approach that takes into account the unique challenges faced by SMEs, which currently lack regulatory support compared to large companies.

3 Research methods

This paper is based on a literature and normative review and a theoretical framework concerning the “SMEs sustainability transition.” This leads to a conceptual model and related questionnaire created as a reference for the perspectives of banks and supply chain leaders that can form the basis for the assessment and self-assessment of the sustainability transition of SMEs. The questionnaire also highlights the actions to be taken to increase SMEs' degree of sustainability for each of the sections (E, S, and G), so it can also act as a guide for the SMEs themselves. It can also be a starting point for future econometric applications that lead to an ESG score that considers the characteristics of SMEs taking inspiration from what is proposed in the paragraph 4.4.

4 The architecture of the conceptual model and its implications

The proposal of the ESG assessment methodology proposed in this paper aims to offer a tool that goes beyond the simple analysis of the environmental sustainability, social responsibility and governance profile of SMEs. The approach aims to establish a sustainability transition process for SMEs, as it seeks to accurately integrate the sustainability transition of SMEs, their level of sustainability, and their compliance with specific sustainability standards. Currently, these elements are assessed separately by rating agencies. However, an integrated approach would allow for a more comprehensive and accurate evaluation, providing a holistic view of the sustainability of SMEs. In particular, the conceptual model involves determining a scoring for SMEs recognized by both banks and supply chain leaders and evaluating/rating the strengths and weaknesses and the related actions that SMEs must initiate toward the sustainability transition. The proposed model aims to create a unitary and comprehensive vision, as it is based on the sharing of information between the SME taken as a reference, the bank selected for the evaluation of its own clients, and the supply chain leader interested in knowing the characteristics of the companies belonging to its own supply chain in order to become sustainable.

The conceptual model developed is based on a questionnaire (see following Tables 1–4) that distinguishes itself from other methodologies for two main reasons: (i) a greater emphasis on governance, considering the “simplified” governance structure of SMEs and (ii) a forward-looking perspective.

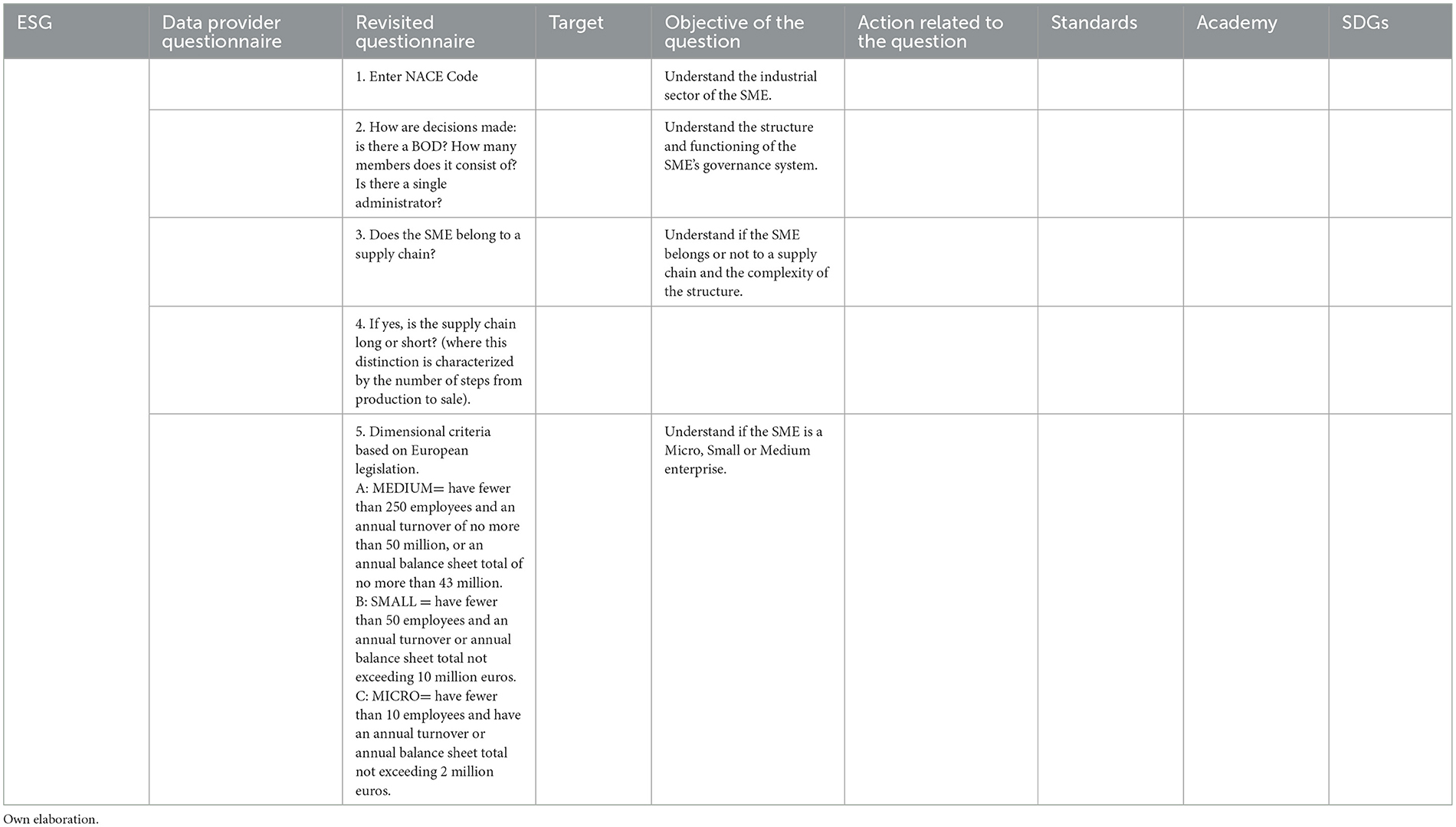

Table 1. Comparison between data provider questionnaire and custom questionnaire–preliminary analysis.

4.1 The structure of the conceptual model

A conceptual model provides a synthesis of existing knowledge and explains key factors, elements, dimensions, and possible relationships among them (Miles and Huberman, 1994) and allows for the formulation of propositions that can provide pathways for empirical research (Esposito De Falco et al., 2024). In this regard, Wirtz and Daiser (2017) conducted a literature analysis on the topic of Business Model Innovation (hereinafter also “BMI”), proposing an integrated conceptual model to deepen the understanding of BMI elements, which is useful for constructing innovative business models. Conversely, Zhang and Benjamin (2007) present a conceptual model focused on information gathering applicable to various disciplines, while Kroeger and Weber (2014) have developed a conceptual model to compare social value creation across distinct and unrelated interventions, each addressing specific needs of different treatment groups situated in diverse socioeconomic and institutional contexts. Conceptual models can also be used to identify, analyze and manage non-quantifiable risks, such as strategic risk and processes (Di Antonio, 2020) or to analyze the impact of financial and strategic control techniques, i.e. eco-control on environmental management (Henri and Journeault, 2010).

A conceptual model is different from a “theoretical framework:” the latter is in fact based on the review of the literature and the prevailing ideas, on data and on the connections between problems and research questions.

In the case of this paper, considering that conceptual models include the vision and ideas of the authors as well as the assumptions and concepts underlying the research (Mensah et al., 2020; Kivunja, 2018; Hughes et al., 2019), the proposed one is a conceptual model because the ideas in this paper, in fact, are not only derived from the literature review, but also from the authors themselves. The increased focus on governance, the forward-looking approach, the distinction of questions in consideration of the size of the companies and the actions to be taken related to each question are in fact elements of own elaboration that guide the conceptual model.

Starting from a review of the literature and a regulatory analysis, the proposed conceptual model involves several steps:

1. First, information is collected through a questionnaire provided by an Italian data provider,7 which is analyzed to assess the suitability of the applications for an SME;

2. Subsequently, since the proposed questionnaire does not reflect the peculiarities and characteristics of SMEs, a new questionnaire based on the specificities of SMEs is created, in order to have a questionnaire representative of the business landscape. Furthermore, the proposed questionnaire is the result of an in-depth analysis of the legislation and literature on SMEs and has benefited from the contribution of a local bank that is submitting it to its SMEs, in order to assess their credit portfolio, and of a supply chain leader, committed to responding to the CSDDD, that is submitting it to supplier companies;

3. Finally, there is the transition from qualitative to quantitative analysis, through the development of a formula that will be applied once the answers collected from the bank and the supply chain leader have been obtained. This analysis process is essential to ensure that the scoring model developed is not only effective, but also able to reflect the real dynamics of risk and opportunity present in the SMEs landscape. After reviewing the responses, the weights and scores for each question will be recalibrated.

The proposed conceptual model is clearly different from traditional econometric approaches. The latter, in fact, rely on econometric analysis to generate a score based on the results of standardized questionnaires. On the contrary, the questionnaire proposed in this study is designed to capture the perspective of SMEs' sustainability transition more effectively considering their specificities. This can help understanding the possibility of sustainable development and sustainability in SMEs considering that (i) sustainable development is “development that meets the needs of the present without compromising the ability of future generations to meet their own needs” (World Commission on Environment and Development, 1987) and (ii) “sustainability means that the choice of goods and technologies must be oriented to the requirements of ecosystem integrity and species diversity as well as to social goals” (Harris, 2003). This methodology is designed to generate a score starting from the proposed conceptual paradigm, allowing a more in-depth and contextualized assessment of SMEs. This approach represents a significant step forward compared to traditional econometric models, as it is able to better capture the complexity and diversity of SMEs' experiences in the current economic landscape.

4.2 SMEs recipients of the questionnaire

The questionnaire is aimed at all categories of SMEs, allowing for a more in-depth analysis and contributing to a deeper understanding of the specific needs and challenges of each SME. In particular:

• Micro-enterprises are required to answer all questions marked with the letter “M”;

• Small enterprises must provide answers to all questions marked with the letter “S”;

• Medium-sized enterprises must answer all questions.

The questionnaire is currently being tested. In particular, the local bank is selecting a series of SMEs characterizing the territory to ascertain their degree of sustainability in order to offer green and social credit products that meet their financial needs; the supply chain leader, on the other hand, is administering it to suitable companies belonging to different product sectors and of different sizes, all connected to a supply chain.

4.3 The questionnaire

Following the analysis and evaluation of the questionnaire of the Italian data provider, it is believed that the proposed questions do not capture the peculiarities of SMEs. Consequently, a new questionnaire was created based on specific questions suitable for SMEs. In particular, it was considered appropriate to: (i) modify some questions and add others, with particular reference to the Governance factor, to make it more in line with the objective of this research work. A good governance is essential not only to improve the sustainability of the company, but also to guarantee access to credit. In fact, governance is what makes the difference in making a company truly “green,” because if an SME does not demonstrate adequate governance, it will be difficult to obtain credit from bank; (ii) exclude from the questionnaire the questions that did not require a “yes” or “no” answer, in order to make the questionnaire clearer and more direct, allowing an easier evaluation of the answers.

The questionnaire currently consists of a total of 31 questions and was designed to be administered to all categories of SMEs, identified through the NACE code.8 In particular, the proposed questions take into account existing literature and align with international standards, in particular with the sustainability reporting principles, namely the GRI and the SDGs.

In particular, the questionnaire is composed of: 5 questions for the introductory section, 13 questions for the Governance factor, 7 questions for the Social factor and 6 questions for the Environmental factor. Furthermore, the questionnaire is divided into 4 tables: one containing the questions of the preliminary analysis section (Table 1), one with the questions of the Governance section (Table 2), one with those of the Social section (Table 3) and finally one with the questions for the Environmental section (Table 4). The comparison tables between the questionnaires contains 9 columns:

• “ESG”: indicates the reference sustainability factor (Environmental, Social, Governance);

• “Data provider Questionnaire”: reports the questions of the original questionnaire of the data provider. The column is used to perform the analysis and will not be included in the final questionnaire;

• “Revisited Questionnaire”: contains the questions of the proposed revisited questionnaire;

• “Target”: specifies the reference target for each question (micro, small or medium enterprises);

• “Objective of the question”: describes the objective of each question;

• “Action related to the question”: highlights a series of actions in the process that SMEs need to take toward sustainability, which not only aim to optimize business practices but can also serve as a valuable guide for SMEs seeking to embark on a sustainability transition;

• “Standards”: the GRI standards are used as a regulatory reference in formulating the questions, as they are internationally recognized as an authoritative guide for reporting on sustainable performance, which facilitates data comparability. Furthermore, since they encompass both general and specific standards, they assist SMEs in identifying the most relevant areas for their operational context and ensuring that the information is complete and pertinent;

• “Academy”: indicates the academic literature of reference for the proposed questionnaire;

• “SDGs”: reports the SDGs to which each question of the questionnaire refers. Aligning the questionnaire questions with the SDGs is not only a matter of compliance, but represents a strategic opportunity for SMEs to improve their transition toward sustainability. In fact, for each factor the reference SDGs have been described. However, they are not present in every question.

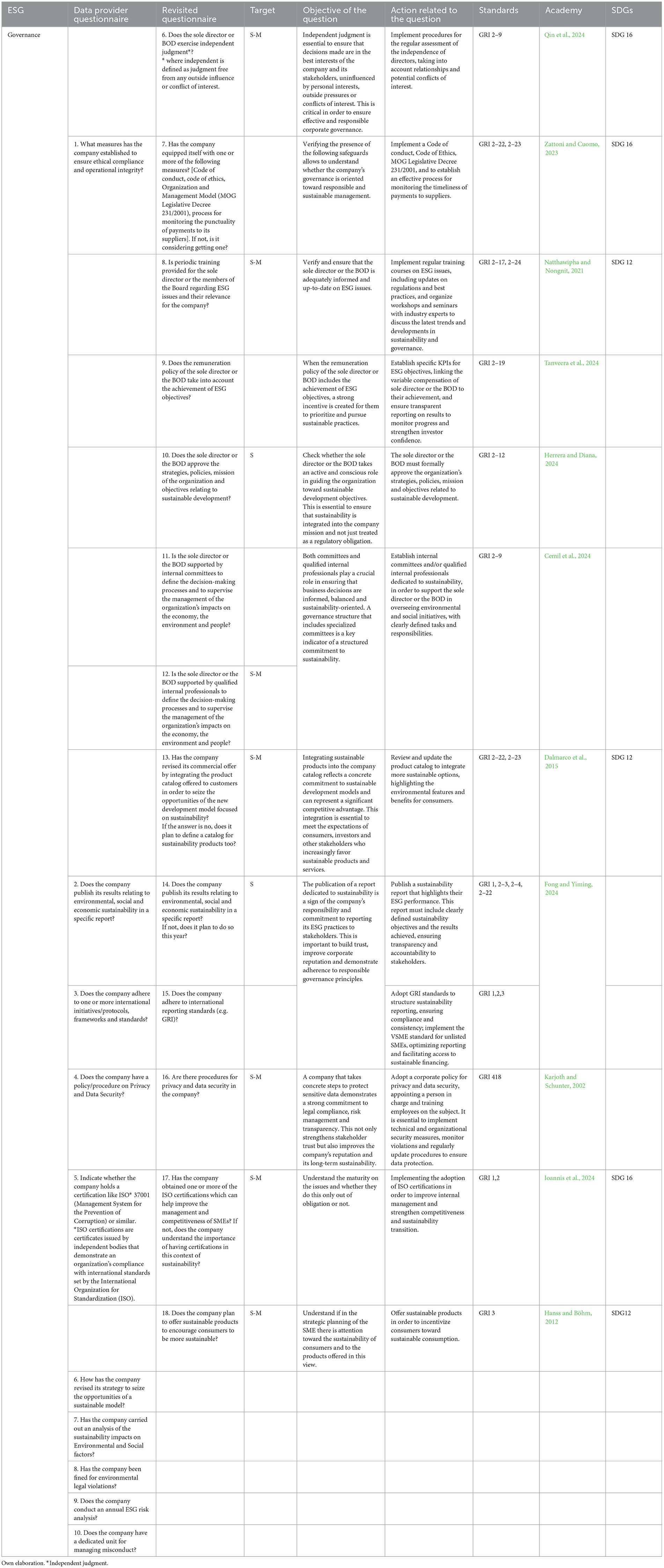

Table 2. Comparison between data provider questionnaire and custom questionnaire–governance section.

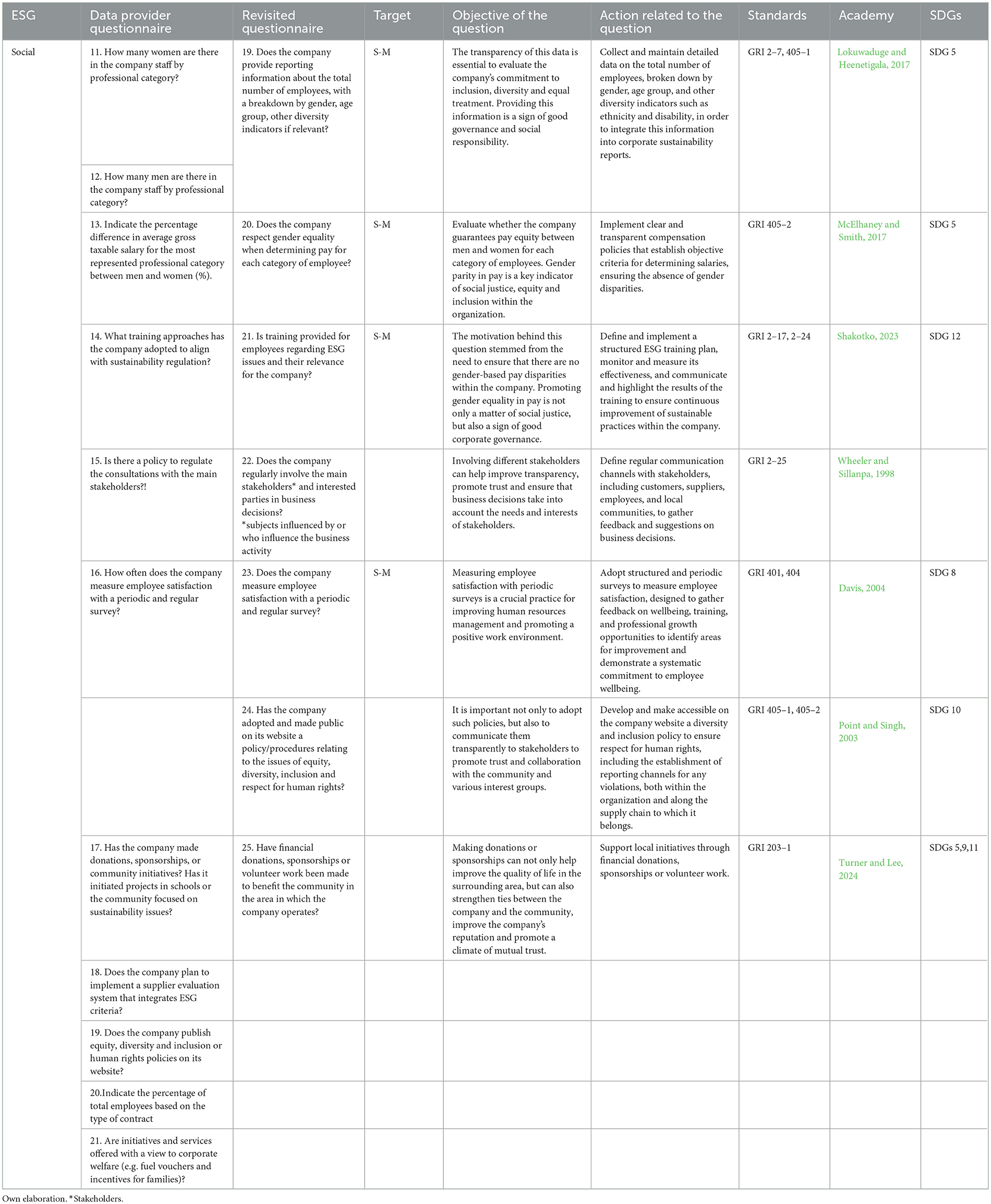

Table 3. Comparison between data provider questionnaire and custom questionnaire–social section.

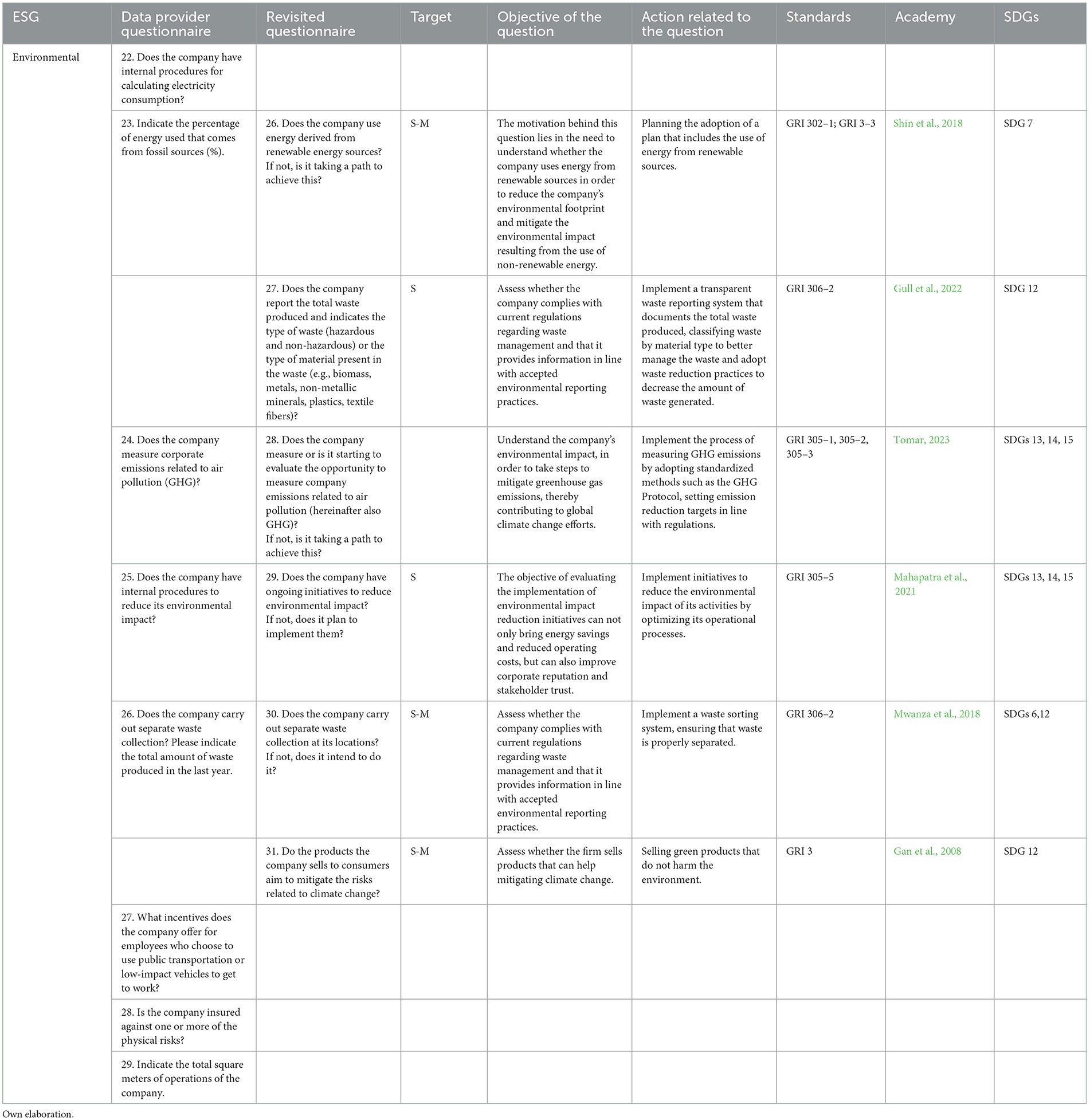

Table 4. Comparison between data provider questionnaire and custom questionnaire–environmental section.

4.3.1 Preliminary analysis section

A fundamental aspect that the data provider has neglected is the initial clustering phase of SMEs, which is a crucial process as it allows segmenting the information into specific categories, thus facilitating the analysis and formulation of more targeted questions. Therefore, five targeted questions are proposed to understand the main characteristics of SMEs in order to make a dimensional, governance model and organizational structure of production check (see following Table 1).

4.3.2 G - Governance

The G factor is often perceived as an afterthought; however, it is crucial to recognize it as the first step toward an effective transition to sustainability, as it is the foundation upon which sustainable business practices are built. This aspect not only establishes the basis for business management, but also serves as a guide for governance and internal control practices, which are essential for the long-term success of SMEs. The relevance of this section is amplified by two key factors: first, many SMEs show a lack of governance and internal control, which can compromise their ability to operate in a sustainable way; second, strong governance can act as a catalyst for social and environmental initiatives, helping to build a positive corporate image and meet stakeholders' expectations. For the governance section, 13 questions are proposed (see following Table 2) and are mainly associated with: (i) SDG 12 that focuses on promoting sustainable consumption and production patterns. Governance practices within a company play a key role in the efficient and responsible management of resources, ensuring transparency and appropriate disclosure through adequate reporting practices; (ii) SDG 16 that aims to promote peaceful and inclusive societies, ensuring access to justice for all and building effective, accountable, and inclusive institutions at all levels. In this context, the composition and independence of the Board of Directors (hereinafter also “BOD”) are essential to prevent conflicts of interest and ensure fair and transparent decision-making. Furthermore, the adoption of an ethical code, a code of conduct, and the MOG Legislative Decree 231/2001 represents the outcome of well-structured Governance.

G factor in determining scores and ratings is often addressed by rating agencies through rating proxies, which may be inadequate. It is therefore essential to develop more tailored and inclusive approaches to governance assessment, which can support SMEs in strengthening their governance practices and improving their long-term sustainability. Therefore, to fill this gap, alternative questions to those of the data provider are proposed, in order to highlight whether and how SMEs, to date, are able to outline and formalize the most appropriate strategies and organizational structures as well as policies to ensure the transition process. As an example, the most relevant ones are listed:

- Question 7 (column “Revisited questionnaire”) thanks to its flexible format, allows SMEs to assess their situation realistically because the question acknowledges that SMEs may not have adopted measures yet, but highlights that these may be under evaluation;

- Question 8 (column “Revisited questionnaire”) highlights the importance of periodic training of company executives on ESG issues, a key indicator of an evolved governance system, able to structurally integrate these factors into the management of the SME and guide it toward sustainable development over time;

- Question 9 (column “Revisited questionnaire”) underlines the role of remuneration policies that consider ESG objectives; these demonstrate a commitment to sustainability and social responsibility. Furthermore, establishing links between compensation and ESG objectives encourages executives to pursue sustainable business practices;

- Question 14 (column “Revisited questionnaire”) offers an opportunity for follow-up; it not only asks if the SME publishes a report, but also explores its future intentions, allowing for the collection of more detailed and useful information for ESG assessment, also in a forward-looking perspective.

4.3.3 S - Social

The proposed 7 questions related to the Social factor aim to examine the management of social responsibilities by SMEs. Firstly questions refer to the company policies and practices regarding employee involvement and treatment, including workers' rights, to ensure safe working conditions. Secondly, they focus on the promotion of diversity and inclusion, promoting gender, ethnic and cultural diversity. Finally, they aim to assess the involvement of SMEs in the communities in which they operate, contributing to their economic and social wellbeing, this is the case, for example, of companies that produce medical devices, which create useful products for society and the wellbeing of its citizens, thus enabling the achievement of SDG 3. Each question is associated with one or more of the following SDGs: (i) SDG 5, which promotes gender equality and empowerment of all women, key elements for creating an inclusive work environment; (ii) SDG 8, focused on promoting decent work for all, sustainable economic growth and employment, crucial aspects for the success of SMEs and economic stability; (iii) SDG 9, which highlights the importance of building resilient infrastructure, promoting sustainable industrialization and fostering innovation, factors that can have a positive impact on SMEs; (iv) SDG 10, aimed at reducing inequalities within and among countries, an objective to which SMEs can contribute by adopting ethical and inclusive business practices; (v) SDG 11, which focuses on creating inclusive, safe, resilient and sustainable cities, and communities, an objective that SMEs can influence through social responsibility, financial donations, sponsorships or volunteer work; and (vi) SDG 12, which aims to promote sustainable consumption and production patterns, a principle that SMEs can integrate to improve their environmental and social sustainability (see previous Table 3).

Therefore, it can be noted how the Social factor is emerging as a crucial element in the context of sustainability helping companies to pursue the public good (as in the case of companies producing medical devices); however, there is currently a lack of a defined taxonomy and clear criteria for its assessment. Rating agencies, in fact, fail to adequately capture social aspects, mainly because they expect the implementation of specific regulations that can guide such assessments. To date, the social commitment of companies can be drawn from their vision, mission and their values of sustainability; but beyond that, the data is lacking. This leads to subjectivity in interpreting social data, especially for SMEs. In this case, to capture the peculiarities of SMEs in more detail, alternative questions to those from the data provider are proposed:

- Question 19 (column “Revisited Questionnaire”) requires the total number of employees, providing an overview of the company's workforce, in addition to the gender breakdown. Furthermore, it also requests a classification by age group and allows space to include relevant diversity indicators for the company, such as ethnicity, disability, sexual orientation, etc. Diversity is thus assessed comprehensively considering the entire workforce;

- Question 20 (column “Revisited Questionnaire”) focuses on a qualitative aspect, allowing for the assessment of the presence of policies and corporate practices that actively influence gender equality. The importance of gender equality is recognized as a fundamental element for corporate social responsibility, making the assessment more relevant for the S factor in the ESG context.

4.3.4 E - Environmental

This section evaluates the company's policies and practices related to environmental management, including strategies for reducing environmental impact, adopting sustainable practices, and awareness of environmental regulations. The Environmental factor is the most developed factor, as it is subject to more stringent regulation. However, it could result in companies using certifications or self-declarations, without an actual awareness of the necessary sustainable practices. It is essential, therefore, to question the motivations that push SMEs to try to become sustainable, in particular whether their choice is dictated by a concrete commitment to achieving sustainability, or whether it is an attempt to obtain green and social financing and therefore incur the risk of greenwashing and social washing. In this sense, 6 questions are proposed referring to the Environmental factor (see previous Table 4) associated with one or more of the following SDGs: (i) SDG 6, which aims to ensure availability and sustainable management of water and sanitation for all; (ii) SDG 7, which seeks to ensure access to affordable, reliable, sustainable, and modern energy systems for all, with a commitment from SMEs toward energy efficiency and the adoption of renewable energy; (iii) SDG 12, which promotes sustainable consumption and production patterns, encouraging practices such as waste management and the circular economy; (iv) SDG 13, which calls for urgent measures to combat climate change and its impacts, by monitoring and reducing Greenhouse Gas Emissions; (v) SDG 14, which addresses the conservation and sustainable use of oceans, seas, and marine resources for sustainable development; and (vi) SDG 15, which commits to ensuring and promoting the sustainable use of terrestrial ecosystems.

To capture the peculiarities of SMEs, are proposed questions like question 26 (column “Revised questionnaire”) that is suitable to SMEs because it has a forward-looking perspective exploring future intentions.

4.4 Econometric model for pilot testing

The final step involves transitioning from qualitative analysis to quantitative analysis through the development of a formula, which will be applied once responses are obtained from the bank and the supply chain leader, as it does not currently represent the core of the paper. This is because the questionnaire is presently being administered by a local bank to a series of SMEs that characterize the territory to assess their sustainability level, with the aim of offering more targeted sustainable products, as well as by a supply chain leader to suitable companies belonging to various sectors and of different sizes, all connected to a supply chain. After examining the responses and recalibrating weights and evaluations, the questionnaire will be further refined and the formula suggested can be used as a starting point for the development of an econometric model based on the conceptual model proposed.

To use the questionnaire as a basis for an ESG score, the conceptual paradigm to follow must be to associate, as proposed by the Italian data provider, a score to each factor (whose sum amounts to 100). In particular:

• The E factor is assigned a score of 35, since companies are interested in their bankability and therefore it is necessary to stress the E which allows for greater access to credit;

• The S factor is assigned a score of 30, as to date there is still no specific Taxonomy for the same factor;

• The G factor is given a score of 35, as it makes sense to stress a deficient factor in the specific case of SMEs.

With the exception of the first five questions concerning general company characteristics, each question offers two response options: “yes” or “no.” If the response is “yes,” the question is assigned a score of 1; otherwise, it is assigned a score of 0. In detail:

• The “Environment” section consists of a number of questions “qE,” each of which is evaluated with a score “pi.” The total weight of the category is “pE.”

• The “Social” section consists of a number of questions “qs,” each of which is evaluated with a score “pj.” The total weight of the category is “pS.”

• The “Governance” consists of a number of questions qG, each of which evaluated with a score “Pz;” The total weight of the category is “pG.”

The number of questions, in order to take into account the differences among medium, small and micro enterprises, is different. In detail, excluding the five questions of general assessment:

- Medium enterprises have to answer to 26 questions (6 for Environment, 7 for Social and 13 for Governance).

- Small enterprises have to answer to 18 questions (5 for Environment, 4 for Social and 9 for Governance).

- Micro enterprises have to answer to 14 questions (3 for Environment, 4 for Social and 7 for Governance).

Subsequently, to calculate the ESG Score, we proceed with the weighted average of the individual factors (E, S, G) and their relative weights according to three different formulas: one for medium enterprises (me), one for small enterprises (sm), and one for micro enterprises (mi). This distinction is made to take into account an adjustment factor μ that changes based on whether the company is medium, small or micro in order to consider that for micro enterprises it is more difficult to address ESG issues than for small enterprises, and for small enterprises it is more difficult than for medium ones. To do so three different μ are considered such that the one for medium is smaller than the one for small that is smaller than the one for micro enterprises:

- μme = 0.9 (adjustment factor for medium enterprises).

- μsm = 0.95 (adjustment factor for small enterprises).

- μmi = 1 (adjustment factor for microenterprises).

Considering these adjusting factors, the following formulas can give the score for medium enterprises (ESG SCORE me), small enterprises (ESG SCORE sm) and micro enterprises (ESG SCORE mi).

• E = Number of “Yes” answers in the E category;

• S = Number of “Yes” answers in the S category;

• G= Number of “Yes” answers in the G category;

• , is given by the weight of the E factor on the number of questions in category E;

• , is given by the weight of the S factor on the number of questions in category S;

• , is given by the weight of the G factor on the number of questions in category G;

• μ = adjustment factor.

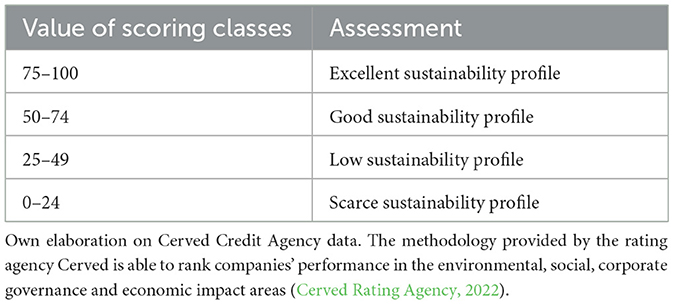

Once the ESG Score has been determined, the sustainability profile of the interviewee is determined according to following Table 5.

Table 5. Assessment based on the scoring classes.

5 Conclusions

This conceptual model, that starts from a literature and normative review and the consideration of the perspectives of banks and supply chain leaders, was created in response to: (i) the current divergence between ratings and scorings which are not able to capture the peculiarities of SMEs; (ii) the characteristics of SMEs that show a simplified governance structure; (iii) the indirect regulatory obligations related to the SMEs' sustainability transition, to which SMEs, especially young ones, should be compliant in order to obtain finance from banks (Veugelers et al., 2019) and be included in supply chain by supply chain leaders, enhancing their growth and performance.

Considering that SMEs are peculiar and have characteristics difficult to catch through a traditional score or rating, a conceptual model can be useful because it has a broader view and allows to catch those peculiarities combining different perspectives.

The proposed conceptual model, that ultimately materializes in the questionnaire, can be useful: (i) to SMEs, which can carry out a self-assessment to understand their sustainability profile, their financial needs and the actions to be taken to support the sustainability transition related to each of the questions for each factor (E, S, and G); (ii) to banks to analyze the sustainability of their customers and redefine the offer of green credit products [such as Green Loans (ASL et al., 2018a,b) and Sustainability-Linked Loans (ASL et al., 2019a,b)] and social credit products [such as Social Loans (ASL et al., 2021a,b)] with respect to the needs of SMEs; and (iii) to supply chain leaders to ensure a sustainable supply chain and support supplier SMEs toward a rapid and effective transition process. Considering these different perspectives, the model is useful for assessing the sustainability transition of SMEs, their level of sustainability, and their compliance with specific sustainability standards.

The questionnaire is currently in a pilot phase and is being submitted by an Italian local bank to its SMEs customers (that are an important part of its customer portfolio) and by an Italian supply chain leader to SMEs in its supply chain. Once the results are obtained, it will be possible to understand whether the questionnaire captures the problems of SMEs in this transition. Once this is done, it will be possible to propose interventions by banks and supply chain leaders and implement an econometric methodology on the proposed conceptual model to arrive at a specific ESG score for SMEs.

However, this model has two limitations. First, the questionnaire is currently being tested, as it is being administered to companies that are already customers of a local bank in order to offer more targeted sustainable products, and by the supply chain leader to eligible companies belonging to different product sectors and of different sizes, all connected to a supply chain. The questions will be recalibrated based on the answers received and following the administration of the questionnaire, the scoring formula will be used as a starting point for an econometric model.

Secondly, filling out the questionnaire and distorting the answers to make them appear more sustainable than they actually are could lead to greenwashing and social washing. It is therefore crucial to develop an adequate sustainability culture that promotes responsible business practices. Only through clear information and rigorous regulation it will be possible to counteract the phenomenon of greenwashing and social washing, ensuring that sustainability claims are supported by concrete and measurable actions.

Finally, future studies could focus on the implementation of an econometric model that follows the proposed conceptual paradigm or on the dissemination of similar questionnaires to make a comparison with the results of more traditional questionnaires.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Author contributions

PM: Conceptualization, Supervision, Validation, Writing – review & editing. SG: Conceptualization, Investigation, Methodology, Resources, Writing – review & editing. VA: Formal analysis, Investigation, Writing – original draft. AC: Investigation, Methodology, Writing – original draft.

Funding

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article.

Acknowledgments

We are grateful to Sabau G. (the Handling Editor) and the reviewers for their valuable comments. Their observations had a significant impact on our work, allowing us to significantly improve the quality of the article, contributing to making our study more robust and relevant. We also thank the referents of both the local bank and the supply chain leader for their support in administering the questionnaire, both of which requested to remain anonymous. Pina Murè acknowledges the support from the Università degli Studi di Roma “La Sapienza” through the Economic Research Grants “ESG Factors and Supply Chain: the Role of Banks and Supply Chains Leaders in Promoting SMEs transition to Sustainability” (RM123188F7C30402) and “ESG and banks stability: are banks ready to face climate-related risks and to avoid sanctions by supervisors?” (RM12117A8AF9F869). Saverio Giorgio acknowledges the support from the Università degli Studi di Roma “La Sapienza” through the Economic Research Grants “L’offerta di prodotti e servizi assicurativi attraverso il canale bancario: la bancassicurazione” (AR223188B4D2FA5D). This work was supported by MUR under the PNRR M4C2I1.4 project “Rome Technopole” Flagship 4, CUP, Sapienza University of Rome. This work was also supported by the European Union - Next Generation EU, Mission 4 Component 1 CUP: B53C23002550006.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher's note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

1. ^Over the years, SME legislation and criteria for their definition have been modified, with harmonisations in 2003, 2020 and 2023 (European Commission, 2003, 2020, 2023). Currently, SMEs are classified as follows: (i) small enterprises: less than 50 employees and annual turnover or balance sheet total not exceeding EUR 10 million; (ii) medium-sized enterprises: Less than 250 employees and annual turnover not exceeding €50 million or balance sheet total not exceeding €43 million; and (iii) micro enterprises: Less than 10 employees and annual turnover or balance sheet total not exceeding € 2 million.

2. ^Defined by the Directive 2024/825 of the European Parliament and of the Council as “unfair commercial practices that deceive consumers and prevent them from making sustainable consumer choices, such as practices associated with the premature obsolescence of goods, misleading environmental claims ('greenwashing'), misleading information on the social characteristics of products or businesses of economic operators or non-transparent and non-credible sustainability labels.”

3. ^“The deceptive use of advertising strategies to promote the perception that products are socially responsible” (Rizzi et al., 2020), it thus consists of presenting the company to stakeholders as more social responsible (e.g., pretending to show attention to goals such as SDG 3 that aims to ensure healthy lives and promote well-being for all) than it really is, with the aim of profiting from the reputational gain.

4. ^GAR is the proportion of company activities aligned to taxonomy objectives on total assets.

5. ^Compared to the GAR, the BTAR explicitly includes exposures to companies excluded from the NFDR, such as SMEs.

6. ^The 2030 Agenda for Sustainable Development (United Nations, 2015), contains the 17 SDGs and 169 sub-goals, which aim to end poverty, fight inequality and social and economic development. They also address aspects of fundamental importance for sustainable development, such as the fight against climate change by 2030.

7. ^The data provider in question wants to maintain its privacy. It is one of the Italian providers that deal with scoring and rating in the credit sector.

8. ^Nomenclature statistique des Activités économiques dans la Communauté Européenne Code (NACE Code) is a classification system used to standardize the definitions of economic and industrial activities in the countries that are part of the European Union.

References

Acquaye, A., Ibn-Mohammed, T., Genovese, A., Afrifa, A. G., Yamoah, F. A., and Oppon, E. (2018). A quantitative model for environmentally sustainable supply chain performance measurement. Eur. J. Oper. Res. 269, 188–205. doi: 10.1016/j.ejor.2017.10.057

Altman, E. I., and Sabato, G. (2008). Modeling credit risk for SMEs: evidence from the US market. A journal of accounting. Fin. Bus. Stud. 43, 332–357. doi: 10.1111/j.1467-6281.2007.00234.x

ASL LMA, and LSTA. (2018a). “Guidance on Green Loan Principles,” in Asia Pacific Loan Market Association, Loan Market Association & Loan Syndications and Trading Association. Last updated April 2023.

ASL LMA, and LSTA. (2018b). “Green Loan Principles,” in Asia Pacific Loan Market Association, Loan Market Association & Loan Syndications and Trading Association. Last updated April 2023.

ASL LMA, and LSTA. (2019a). “Guidance on Sustainability-Linked Loan Principles,” in Asia Pacific Loan Market Association, Loan Market Association & Loan Syndications and Trading Association. Last updated April 2023.

ASL LMA, and LSTA. (2019b). “Sustainability-Linked Loan Principles,” in Asia Pacific Loan Market Association, Loan Market Association & Loan Syndications and Trading Association. Last updated April 2023.

ASL LMA, and LSTA. (2021a). “Guidance on Social Loan Principles,” in Asia Pacific Loan Market Association, Loan Market Association & Loan Syndications and Trading Association. Last updated April 2023.

ASL LMA, and LSTA. (2021b). “Social Loan Principles,” in Asia Pacific Loan Market Association, Loan Market Association & Loan Syndications and Trading Association. Last updated April 2023.

BCBS (2004). Basel II: International Convergence of Capital Measurement and Capital Standards: a Revised Framework. Banco de Pagos Internacionales.

Berg, F., Koelbel, J. F., and Rigobon, R. (2022). Aggregate confusion: the divergence of ESG ratings. Rev. Fin. 26, 1315–1344. doi: 10.1093/rof/rfac033

Bove, A. T., and Swartz, S. (2016). Starting at the source: Sustainability in supply chains. McKinsey Sustain. Resour. Prod. 4, 36–43.

Broccardo, L., Truant, E., and Zicari, A. (2019). Internal corporate sustainability drivers: What evidence from family firms? A literature review and research agenda. Corpor. Soc. Respons. Environ. Manag. 26, 1–18. doi: 10.1002/csr.1672

Capizzi, V., Gioia, E., Giudici, G., and Tenca, F. (2021). The divergence of ESG ratings: an analysis of Italian listed companies. J. Fin. Manag. Markets Inst. 9:2150006. doi: 10.1142/S2282717X21500067

Cardillo, G., Bendinelli, E., and Torluccio, G. (2023). COVID-19, ESG investing, and the resilience of more sustainable stocks: evidence from European firms. Bus. Strat. Environ. 32, 602–623. doi: 10.1002/bse.3163

Cemil, K., Amal, H., Ali, U., and Abdullah, K. (2024). Social reputation, loan contracting and governance mechanisms. Int. J. Account. Inf. Manag. 32, 502–531. doi: 10.1108/IJAIM-12-2023-0321

Clift, R. (2003). Metrics for supply chain sustainability. Clean Technol. Environ. Policy 5, 240–247. doi: 10.1007/s10098-003-0220-0

Crovini, C., Ossola, G., and Giovando, G. (2018). Italian credit cooperative banks: the fundamental role in supporting the growth of SMEs and family businesses. Global Bus. Econ. Rev. 20, 602–611. doi: 10.1504/GBER.2018.094447

Dalmarco, D. D. A. S., Hamza, K. M., and Aoqui, C. (2015). The implementation of product development strategies focused on sustainability: from Brazil-the case of Natura Sou Cosmetics brand. Environ. Quality Manag. 24, 1–15. doi: 10.1002/tqem.21394

Davis, G. (2004). Job satisfaction survey among employees in small businesses. J. Small Bus. Enterpr. Dev. 11, 495–503. doi: 10.1108/14626000410567143

Di Antonio, M. (2020). Rischio strategico, business delle banche e processi. Tre modelli per gestirli e controllarli. Rivista Bancaria, 3.

Di Bella, L., Katsinis, A., Lagüera-González, J., Odenthal, L., Hell, M., and Lozar, B. (2023). “Annual Report on European SMEs 2022/2023,” in Publications Office of the European Union.

Drempetic, S., Klein, C., and Zwergel, B. (2020). The influence of firm size on the ESG score: corporate sustainability ratings under review. J. Bus. Ethics 167, 333–360. doi: 10.1007/s10551-019-04164-1

Esposito De Falco, S., Montera, R., and Cucari, N. (2024). “Deconstructing corporate purpose: a conceptual framework in an evolutionary perspective,” in Academy of Management Proceedings (Valhalla, NY: Academy of Management), 17207. doi: 10.5465/AMPROC.2024.17207abstract

EU Platform on Sustainable Finance (2024). Platform Briefing on EFRAG's Consultation on LSME and VSME ESRS.

European Commission (2003). Commission Recommendation of 6 May 2003 concerning the definition of micro, small and medium-sized enterprises. Official Journal of the European Union.

European Commission (2023). Commission Delegated Directive (EU) 2023/2775 of 17 October 2023 amending Directive 2013/34/EU of the European Parliament and of the Council as regards the adjustments of the size criteria for micro, small, medium-sized and large undertakings or groups. Official Journal of the European Union.

European Parliament and Council (2014). Directive 2014/95/EU of the European Parliament and of the Council of 22 October 2014 amending Directive 2013/34/EU as regards disclosure of non-financial and diversity information by certain large undertakings and groups.

European Parliament and Council (2020). Regulation (EU) 2020/852 of the European Parliament and of the Council of 18 June 2020 on the establishment of a framework to facilitate sustainable investment, and amending Regulation (EU) 2019/2088. Official Journal of the European Union.

European Parliament and Council (2022). Directive (EU) 2022/2464 of the European Parliament and of the Council of 14 December 2022 amending Regulation (EU) No 537/2014, Directive 2004/109/EC, Directive 2006/43/EC and Directive 2013/34/EU, as regards corporate sustainability reporting.

European Parliament and Council (2023). Proposal for a Regulation of the European Parliament and of the Council on the Transparency and Integrity of Environmental, Social and Governance (ESG) Rating Activities.

European Parliament and Council (2024a). Directive (EU) 2024/1760 of the European Parliament and of the Council of 13 June 2024 on corporate sustainability due diligence and amending Directive (EU) 2019/1937 and Regulation (EU) 2023/2859.

European Parliament and Council (2024b). Directive (EU) 2024/825 of the European Parliament and of the Council of 28 February 2024 amending Directives 2005/29/EC and 2011/83/EU as regards empowering consumers for the green transition through better protection against unfair practices and through better information. Official Journal of the European Union.

Fong, M. A., and Yiming, C. (2024). Board attributes, ownership structure, and corporate social responsibility: evidence from A-share listed technological companies in China. Soc. Bus. Rev. 19, 181–206. doi: 10.1108/SBR-08-2022-0225

Gan, C., Wee, H. Y., Ozanne, L., and Kao, T. H. (2008). Consumers' purchasing behavior towards green products in New Zealand. Innov. Market. 4:11. doi: 10.1016/S1351-4210(08)70087-8

Gibert, A. (2020). Solicited versus unsolicited ratings: the role of selection. J. Fin. Manag. Markets Inst. 7:1950005. doi: 10.1142/S2282717X19500051

Giorgio, S. (2023). I prodotti creditizi come volano di una transizione sostenibile: tra opportunità e rischi in ottica di conformità. Quaderni di Minerva Bancaria.

Gull, A. A., Atif, M., Ahsan, T., and Derouiche, I. (2022). Does waste management affect firm performance? International evidence. Econ. Modell. 114:105932. doi: 10.1016/j.econmod.2022.105932

Gulzhan, A., Kerimkulova, D., Yessymkhanova, Z., Orazbayeva, A., and Alibekova, A. (2023). ““Green” loan – a “green” financing instrument,” in E3S Web of Conferences (EDP Sciences), 08036. doi: 10.1051/e3sconf/202340208036

Hanss, D., and Böhm, G. (2012). Sustainability seen from the perspective of consumers. Int. J. Consum. Stud. 36, 678–687. doi: 10.1111/j.1470-6431.2011.01045.x

Henri, J. F., and Journeault, M. (2010). Eco-control: the influence of management control systems on environmental and economic performance. Account. Organ. Soc. 35, 63–80. doi: 10.1016/j.aos.2009.02.001

Herrera, B. R., and Diana, E. B. (2024). Synergizing board dynamics, sustainability, and strategy for international success. Corpor. Soc. Respon. Environ. Manag. 31, 3368–3378. doi: 10.1002/csr.2742

Hughes, S., Davis, T. E., and Imenda, S. N. (2019). Demystifying theoretical and conceptual frameworks: a guide for students and advisors of educational research. J. Soc. Sci. 58, 24–35. doi: 10.31901/24566756.2019/58.1-3.2188

Ioannis, M., Grigoris, G., and Nikolaos, S. (2024). Impact of board gender diversity on environmental, social, and ESG controversies performance: The moderating role of United Nations Global Compact and ISO. J. Cleaner Prod. 444:141047. doi: 10.1016/j.jclepro.2024.141047

Jiang, Y., Lai, P., Chang, C. H., Yuen, K. F., Li, S., and Wang, X. (2021). Sustainable management for fresh food E-commerce logistics services. Sustainability 13:3456. doi: 10.3390/su13063456

Karjoth, G., and Schunter, M. (2002). “A privacy policy model for enterprises,” in Proceedings 15th IEEE Computer Security Foundations Workshop.

Kivunja, C. (2018). Distinguishing between theory, theoretical framework, and conceptual framework: a systematic review of lessons from the field. Int. J. High. Educ. 7. doi: 10.5430/ijhe.v7n6p44

Kotsantonis, S., and Serafeim, G. (2019). Four things no one will tell you about ESG data. J. Appl. Corpor. Finan. 31, 50–58. doi: 10.1111/jacf.12346

Kroeger, A., and Weber, C. (2014). Developing a conceptual framework for comparing social value creation. Acad. Manag. Rev. 39, 513–540. doi: 10.5465/amr.2012.0344

Kusi-Sarpong, S., Gupta, H., and Sarkis, J. (2019). A supply chain sustainability innovation framework and evaluation methodology. Int. J. Prod. Res. 57, 1990–2008. doi: 10.1080/00207543.2018.1518607

La Torre, M. (2022). Banche e finanza sostenibile: per un business model Esg-oriented. BANCARIA 5, 2–19.

La Torre, M., Leo, S., and Panetta, I. C. (2021). Banks and environmental, social and governance drivers: follow the market or the authorities? Corpor. Soc. Respons. Environ. Manag. 28, 1620–1634. doi: 10.1002/csr.2132

La Torre, M., Mango, F., Cafaro, A., and Leo, S. (2020). Does the ESG index affect stock return? Evidence from the Eurostoxx50. Sustainability 12:6387. doi: 10.3390/su12166387

Lee, M. T., and Raschke, R. L. (2023). Stakeholder legitimacy in firm greening and financial performance: what about greenwashing temptations??. J. Bus. Res. 155:113393. doi: 10.1016/j.jbusres.2022.113393

Lee, M. T., Raschke, R. L., and Krishen, A. S. (2023). Understanding ESG scores and firm performance: are high-performing firms E, S, and G-balanced? Technol. Forec. Soc. Change 195:122779. doi: 10.1016/j.techfore.2023.122779

Linjie, J., and Xuedong, L. (2010). Discussions on the improvement of the internal control in SMEs. Int. J. Bus. Manage. 5:214. doi: 10.5539/ijbm.v5n9p214

Lokuwaduge, C. S. D. S., and Heenetigala, K. (2017). Integrating environmental, social and governance (ESG) disclosure for a sustainable development: an Australian study. Bus. Strat. Environ. 26, 438–450. doi: 10.1002/bse.1927

Loorbach, D., Frantzeskaki, N., and Avelino, F. (2017). Sustainability transitions research: transforming science and practice for societal change. Ann. Rev. Environ. Resour. 42, 599–626. doi: 10.1146/annurev-environ-102014-021340

Luo, L., and Tang, Q. (2023). The real effects of ESG reporting and GRI standards on carbon mitigation: international evidence. Bus. Strateg. Environ. 32, 2985–3000. doi: 10.1002/bse.3281

Mahapatra, S. K., Schoenherr, T., and Jayaram, J. (2021). An assessment of factors contributing to firms' carbon footprint reduction efforts. Int. J. Prod. Econ. 235:108073. doi: 10.1016/j.ijpe.2021.108073

Martins, C. L., and Pato, M. V. (2019). Supply chain sustainability: a tertiary literature review. J. Clean. Prod. 225, 995–1016. doi: 10.1016/j.jclepro.2019.03.250

McElhaney, K., and Smith, G. (2017). Eliminating the Pay Gap: An Exploration of Gender Equality, Equal Pay, and A Company that Is Leading the Way. Berkeley: UC Berkeley - Haas School of Business.

Mensah, R. O., Agyemang, F., Acquah, A., Babah, P. A., and Dontoh, J. (2020). Discourses on conceptual and theoretical frameworks in research: meaning and implications for researchers. J. African Interdisc. Stud. 4, 53–64.

Meslier, C., Rehault, P. N., Sauviat, A., and Yuan, D. (2022). Benefits of local banking in local economic development: Disparities between micro firms and other SMEs. J. Bank. Fin. 143:106594. doi: 10.1016/j.jbankfin.2022.106594

Miles, M. B., and Huberman, A. M. (1994). Qualitative Data Analysis: An Expanded Sourcebook. 2nd ed. Thousand Oaks: Sage Publications.

Mirza, N., Afzal, A., Umar, M., and Skare, M. (2023). The impact of green lending on banking performance: evidence from SME credit portfolios in the BRIC. Econ. Anal. Policy 77, 843–850. doi: 10.1016/j.eap.2022.12.024

Mishra, D., Gunasekaran, A., Papadopoulos, T., and Dubey, R. (2018). Supply chain performance measures and metrics: a bibliometric study. Benchmarking 25, 932–967. doi: 10.1108/BIJ-08-2017-0224

Mwanza, B. G., Mbohwa, C., and Telukdarie, A. (2018). The influence of waste collection systems on resource recovery: a review. Procedia Manuf. 21, 846–853. doi: 10.1016/j.promfg.2018.02.192

Natthawipha, K., and Nongnit, C. (2021). The impact of board structure on performance of Thai-listed companies in Market for Alternative Investment (mai). Int. J. Mon. Econ. Fin. 14, 332–341. doi: 10.1504/IJMEF.2021.116975

Noci, G. (1997). Designing ‘green' vendor rating systems for the assessment of a supplier's environmental performance. Eur. J. Purch. Supply Manag. 3, 103–114. doi: 10.1016/S0969-7012(96)00021-4

Point, S., and Singh, V. (2003). Defining and dimensionalising diversity: Evidence from corporate websites across Europe. Eur. Manag.J. 21, 750–761. doi: 10.1016/j.emj.2003.09.015

Qin, L., He, Q., Fu, X., Wang, Y., and Wang, G. (2024). Peer effects on corporate social responsibility engagement of chinese construction firms through board interlocking ties. J. Constr. Eng. Manag. 150:04024064. doi: 10.1061/JCEMD4.COENG-14479

Resti, A., and Sironi, A. (2021). “Rischio e valore nelle banche: misura, regolamentazione, gestione,” in Egea 927.

Rizzi, F., Gusmerotti, N., and Frey, M. (2020). How to meet reuse and preparation for reuse targets? Shape advertising strategies but be aware of “social washing”. Waste Manag. 101, 291–300. doi: 10.1016/j.wasman.2019.10.024

Roy, P. K., and Shaw, K. (2020). A credit scoring model for SMEs using AHP and TOPSIS. Int. J. Fin. Econ. 28, 372–391. doi: 10.1002/ijfe.2425

Sardanelli, D., Bittucci, L., Mirone, F., and Marzioni, S. (2022). An integrative framework for supply chain rating: from financial-based to ESG-based rating models. Total Quality Manag. Bus. Excell. 2022, 1–20. doi: 10.1080/14783363.2022.2069557

Selma, H. K. (2020). Ratings for innovative smes and start-ups and intangible capital: literature review and proposal of a new approach. Stud. Appl. Econ. 38:4014. doi: 10.25115/eea.v38i4.4014

Shin, H., Ellinger, A. E., Nolan, H. H., DeCoster, T. D., and Lane, F. (2018). An assessment of the association between renewable energy utilization and firm financial performance. J. Bus. Ethics 151, 1121–1138. doi: 10.1007/s10551-016-3249-9

Tamayo-Torres, I., Gutierrez-Gutierrez, L., and Ruiz-Moreno, A. (2019). Boosting sustainability and financial performance: the role of supply chain controversies. Int. J. Prod. Res. 57, 3719–3734. doi: 10.1080/00207543.2018.1562248

Tanveera, H. R., Khubaiba, A., Fiazb, A., Ahmadc, S., and Summaira, M. (2024). Examining the intervening effect of earning management in governance mechanism and financial misstatement with lens of SDG and ESG: a study on non-financial firms of Pakistan. Environ. Sci. Pollut. Res. 31, 46325–46341. doi: 10.1007/s11356-023-30128-0

Tian, G., Wang, K. T., and Wu, Y. (2023). Does the market value the green credit performance of banks? Evidence from bank loan announcements. Br. Account. Rev. 2023:101282. doi: 10.1016/j.bar.2023.101282

Tomar, S. (2023). Greenhouse gas disclosure and emissions benchmarking. J. Account. Res. 61, 451–492. doi: 10.1111/1475-679X.12473

Turner, K., and Lee, J. (2024). To whom and how much? An assessment of philanthropic donation variety in relation to firm performance. Soc. Respons. J. 20, 1597–1613. doi: 10.1108/SRJ-08-2023-0476