Qianjie Li1*

Qianjie Li1* Shi Yin

Shi Yin

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Energy Res., 28 September 2023

Sec. Sustainable Energy Systems

Volume 11 - 2023 | https://doi.org/10.3389/fenrg.2023.1277164

Based on the data of China’s new energy listed companies, this paper empirically studies the impact of the patent signal on the financing constraints of new energy enterprises and its mechanism. The results show that: (i) Both the invention patent application and the non-invention patent application can play a signaling role to alleviate the financing constraints of new energy enterprises; (ii) Analyst attention plays an intermediary role between the patent signal and the financing constraints of new energy enterprises. Compared with non-invention patents, analyst attention plays a more vital intermediary role on invention patents; (iii) Patent signal can alleviate the financing constraints of new energy enterprises in the growth and maturity stages by increasing analyst attention but has no apparent effect on the recession period; (iv) Compared with non-main board listed and small-scale new energy enterprises, patent signal has a more substantial effect on alleviating the financing constraints of main board listed and large-scale new energy enterprises.

The global climate problem has been prominent in recent years. Exploring renewable energy is related to the country’s stability and long-term development. According to the report of the 20th CPC National Congress, China needs to speed up the building of a new energy system, deepen the energy revolution and constantly move towards the goal of “carbon peak and carbon neutrality”. So new energy enterprises play a vital role as an essential subject to realize energy transition. However, the research and development of new energy enterprises needs a large scale of capital investment. Although several policies have been issued to support the development of the new energy industry In recent years, including The Implementation Plan on Promoting the High-quality Development of New Energy in the New Era and The 14th Five-Year Plan for Industrial Green Development. Due to the long asset payback period and high research and development risk of new energy enterprises (Dong et al., 2023a), more than government funds are needed to meet the development of new energy enterprises. Therefore, resolving the financial constraints faced by China’s new energy enterprises is an urgent problem.

The R&D achievements of new energy enterprises are not only required by enterprise production and operation but also concerned by investors. Because patents are strictly examined by the Patent Office and the information is public. The behavior of patent application easily has a signal effect on the outside world (Hu et al., 2022). But even if there are open channels to check the patent applications of enterprises, the ordinary investor probably will only spend a small amount of time learning this information. Compared with ordinary investors, analysts will collect and evaluate the patent information of new energy enterprises. They will then transmit information to investors, alleviating the information asymmetry between enterprises and investors.

The existing research on the economic effects of patent signals mainly focuses on helping enterprises improve financial performance, enhance enterprise value, protect innovation achievements, and obtain enterprise competitiveness (Arora and Ceccagnoli, 2006; Yin et al., 2022a; Dong et al., 2023b). However, there are few studies on the effect of patent signal on corporate financial constraints. What are the effects of different patent signals on financial constraints? What is the mechanism of analyst attention in the relationship between patent signal and financial constraints? The existing literature still lacks systematic theoretical discussion and empirical verification.

In view of this, this paper incorporates patent application, analyst attention and financial constraints into an analytical framework. The possible marginal contribution of this paper is as follows: First, taking new energy enterprises as the research object, this paper proves that patent application can be used as a market signal to help alleviate corporate financing constraints. Therefore, the R&D activities of enterprises can also be used as a strategic consideration to attract investment. Second, this paper takes securities analysts, an important participant and information intermediary in the capital market, into the research scope, and finds that the patenting behavior of enterprises can increase the attention of analysts, thus alleviating the financing constraints of new energy enterprises. Thirdly, from a life-cycle perspective, we also find that the signaling effect of patent applications and the mediating effect of analyst attention are only significant in the growth and maturity periods, but not in the decline period. In practice, this study explores solutions to the financing constraints faced by new energy enterprises from the aspects of patent application and analyst attention. The research conclusions have important practical significance for improving the innovation willingness of enterprises and guiding the formulation of government subsidy policies.

The firm’s internal and external financing costs are the same if the market is efficient. The cost of capital varies only in response to the demand for capital. However, due to the information asymmetry between enterprises and investors caused by the incomplete market, external financing costs are often higher than internal financing costs in the natural environment. Therefore, the firm cannot reach the optimal investment allocation state. That is, enterprises are subject to financing constraints (Fazzari et al., 1988).

New energy enterprises have the characteristics of long capital payback periods, high investment and high uncertainty of research and development, which cause the new energy enterprises to face financing constraints. Investors’ doubts will be reduced if new energy enterprises produce innovative results. The reasons are as follows: Firstly, the patent output can more substantively reflect the current progress of enterprise R&D projects than other innovation behaviors or conditions. External capital providers can use the information contained in patent documents to evaluate the company’s investment value, improving the probability and amount of financing for the enterprise; Secondly, patents not only carry innovation information of enterprises but also attract excellent R&D personnel and government subsidies, which will enhance investor confidence and thus ease the financing constraints of new energy enterprises; Thirdly, Patent pledge financing is also an adequate financing means in financing. It helps new energy companies solve the problem of low collateral and improve credit levels (Zhang and Tang, 2022). Compared with the other two patents, competitors do not easily imitate invention patents since they require more resources and take a longer innovation cycle. Therefore, the invention patent has a higher value for enterprises, which will have a more substantial easing effect on the financing constraints of new energy enterprises.

Based on this, this paper proposes the following hypothesis:

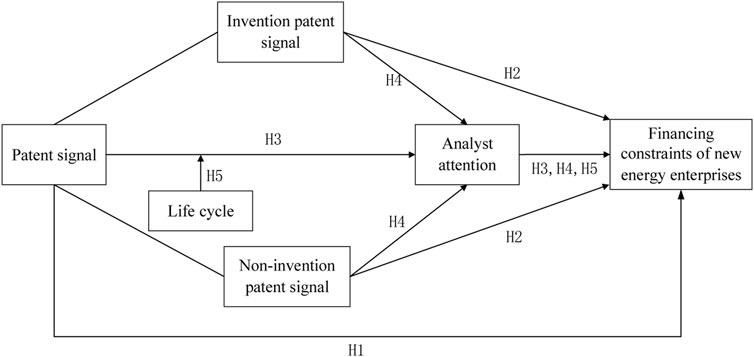

H1. As a market signal, patent application can alleviate the financing constraints of new energy enterprises.

H2. The signal of an invention patent has a more substantial effect on new energy enterprises’ financing constraints than a non-invention patent’s signal.

As the direct output of innovation activities, patents are easier to be recognized and accepted by the market than other innovation information. However, since China’s capital market is not developed enough, many retail investors lack corresponding professional knowledge, and new energy enterprises are generally characterized by high risk and long payback periods. Investors hold a conservative attitude towards the development of new energy enterprises (Wang and Lu, 2022). In contrast, analysts are more professional and have strong information mining abilities. Their research reports can save investors time in obtaining such information so that the patent output signals of enterprises can be effectively transmitted to investors (Cheng et al., 2020). Suppose investors have a high degree of trust in analysts’ analysis reports and have enough confidence in the development prospects of enterprises. In that case, they will naturally be more willing to invest in enterprises. Compared with non-invention patents, invention patents reflect a higher degree of innovation. Analysts have a wide range of information collection channels. They can measure the degree of patent output and the utility of patents among different enterprises by comparing the information of different enterprises. Therefore, analysts will pay more attention to invention patents to analyze enterprises’ innovation capability in patent information collection.

Based on the above analysis, this paper proposes the following hypotheses:

H3. Patent signal can alleviate the financing constraints of new energy listed enterprises by increasing analyst attention.

H4. Compared with non-invention patents, the mediating effect of analyst attention on invention patents is more substantial.

New energy enterprises’ financing constraints differ in different life cycles, and the patent output level is also different. , and the patent output level is also different. Therefore, the life cycle may be an essential factor affecting the patent signalling effect of new energy enterprises in enterprise growth. Investors value the development prospects and operational stability of enterprises, Enterprises in the growth stage are committed to opening the market quickly. They will pay attention to research to improve their market competitiveness. The innovation output of enterprises can reflect the business potential of enterprises and help enterprises gain more recognition from the outside world; After entering the mature period, the enterprise develops to a specific scale, the capital chain is stable, the asset structure is reasonable, and the operating profit also remains stable with the increase of its business volume. Enterprises have substantial risk-bearing capacity in innovation activities. During this period, the continuous pursuit of new product development will send a positive signal to investors that the enterprise has a better prospect; For enterprises in the recession period, their market share and profitability have declined sharply, and they are often faced with multiple pressures such as deterioration of financial conditions and stagnation of enterprise development. Even if enterprises want to change the direction of corporate profits through R&D, they can only attract investors to invest a little due to the high investment risk.

The goal of analysts’ research is to help investors predict the market prospects of investment companies. Analysts are more accurate than ordinary investors in judging the life cycle of companies. The market prospect is broad if the enterprise is in the growth and maturity stage. Analysts will have a positive attitude towards the benefits that their innovation output can bring, which will affect the investment choice of investors. Analysts question the role of patent signals for companies in a recession and study the investment value less.

Based on the above analysis, this paper proposes the following hypotheses:

H5. Patent signal can alleviate the financing constraints of new energy enterprises in the growth and maturity stages by increasing analyst attention but has no noticeable effect on enterprises in the decline stage.

To sum up, the theoretical model framework of this paper is shown in Figure 1.

FIGURE 1. Theoretical model framework.

This paper selects new energy listed enterprises in Shanghai and Shenzhen stock markets from 2010 to 2021 as the research objects. Affected by the policy, the new energy industry began to develop on a large scale in 2010. Therefore, 2010 is the study’s starting point (Chen et al., 2022). The sample selection is limited to new energy enterprises mainly based on two considerations: First, the business scope of the new energy industry is mainly concentrated in solar energy, wind energy, nuclear energy, geothermal energy and other fields. Therefore, new energy enterprises are prone to “credit discrimination”; Second, patent signals have different effects in different industries. Studying new energy enterprises in the context of green development is of more practical significance.

Referring to the sample selection methods of other scholars (Yu and Yu, 2019; Zhao et al., 2021; Li et al., 2022), we select companies whose primary business involves new energy, new energy vehicles, lithium power batteries, photoelectric products, photovoltaic, wind energy, solar energy, biomass energy, nuclear energy and clean energy as new energy enterprises. Finally, a total of 152 enterprises are obtained as initial research samples. After that, the following exclusions were made: (i) We eliminate abnormal listed enterprises; (ii) For the follow-up lag processing, we eliminate the samples of companies with a sample size of fewer than 3 years; (iii) Since the financing of listed companies in the current year is significantly different from that of other companies, the samples of listed companies in the current year are excluded (Wei et al., 2014); (iv) We eliminate the samples with missing values. Finally, this paper obtains 949 research samples from 116 listed companies. At the same time, this paper winsorizes the continuous variables at the upper and lower 1% to eliminate the influence of extreme values.

The enterprise’s basic information and financial data in this paper come from the CSMAR database. Patent data were obtained from the CNRDS database and the Patent search system of the Intellectual Property Office. According to the classification of economic zones by the statistical system and classification standard of the National Bureau of Statistics, all provinces and cities in China are divided into the eastern, central, western and northeastern regions.

There is no agreement on how to measure financing constraints. The main methods include the single index, sensitivity coefficient, and multi-dimensional financial index. The single index method is simple and easy to operate but inevitably one-sided. Commonly used sensitivity indicators are investment-cash flow sensitivity and cash-cash flow sensitivity indicators, But they all rely on certain assumptions that are questionable in the Chinese context. For example, Lian et al. (Lian and Cheng, 2007) found that overinvestment caused by agency problems would improve investment-cash flow sensitivity. Zhang et al. (Zhang and Wu, 2006) found that enterprises may hold cash not only because of the high degree of financing constraints but also because of the motivation to avoid external supervision. Multi-dimensional financial indicators mainly include KZ index, WW index and SA index. They are more comprehensive than the single index method. KZ index and WW index have a common drawback with an endogeneity problem, but the SA index can circumvent this drawback. SA index is constructed by Hadlock and Pierce (Hadlock and Pierce, 2010) using the two exogenous variables of an enterprise. It can describe the characteristics of corporate financing constraints from a long-term perspective.

Based on the advantages and disadvantages of the above measurement methods of financial constraints and referring to previous studies (Ju et al., 2013; Dou et al., 2014), this paper uses SA index to measure financial constraints. The specific calculation formula is as follows: SA = −0.737size+0.043size2-0.04age. Size is the log value of total assets in millions. Age is the company’s listed years. The bigger the SA index’s absolute value, the more serious the financing constraints are. Since the SA index is negative, to ensure the consistency between the symbol and the interpretation direction, thus this paper takes the absolute value of the SA index and defines the symbol as FC. When FC is more giant, the financing constraints are more considerable.

The behaviour of patent applications can reflect the physical innovation results of the enterprise. Only when a firm is reasonably confident about its degree of innovation will it file for a patent (Ma et al., 2022). Therefore, this paper chooses the number of patent applications of enterprises to measure the patent signal. The number of patents granted is not used because although some inventions fail to be authorized, these patents can still generate profits in production and operation (Feng et al., 2011). Moreover, a patent grant is susceptible to various uncertain factors, such as testing and annual fee payment (Zhou et al., 2012). Referring to the research of Liu (Liu et al., 2021) and Wu (Wu et al., 2020), we select the patent application data at the group level. According to different patent types, all patents are divided into invention patents (Patenti) and non-invention patents (Patentud) (Zheng and Zhang, 2019).

Referring to the variable selection method of existing research (Yin et al., 2022b; Yang et al., 2023; Yu and Yin, 2023), we use natural logarithm of the number of analysts following after adding one to measure analyst attention.

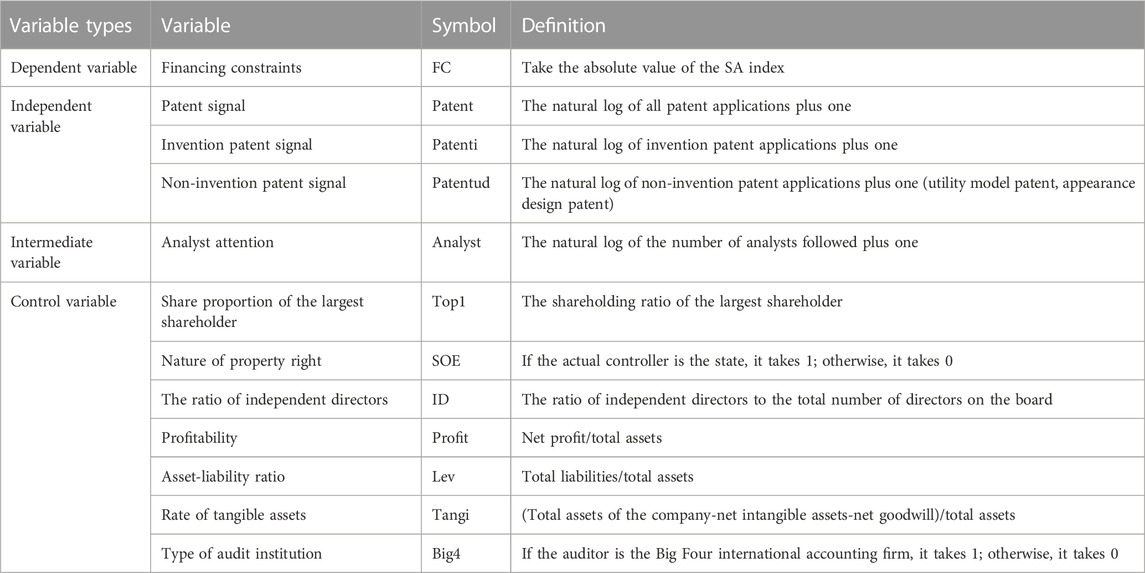

To control the possible bias of regression results caused by missing essential variables, we refer to the existing literature and select a series of factors that may affect corporate financial constraints (Zhong and Shi, 2016; Jiang et al., 2017; Tang et al., 2019). Specific variable symbols and definitions are shown in Table 1.

TABLE 1. Symbols and definitions of variables.

Currently, the methods of dividing the enterprise life cycle in academia mainly include univariate analysis, comprehensive score discrimination method and cash flow model method (Xiao and Lin, 2019). As new energy enterprises involve multiple industries, there are considerable differences between industries. So univariate analysis is biased. Composite score discrimination is subjective. The cash flow method is operable and objective. Therefore, this paper refers to the life cycle division method of Dickinson (Dickinson, 2011) and Yao (Yao et al., 2023), which divides the enterprise life cycle into three life cycle stages: growth period, maturity period and decline period. The specific classification criteria are shown in Table 2.

TABLE 2. Division of enterprise life cycle.

To control the influence of endogeneity, the explanatory variables and all control variables are lagged by one period (Yin et al., 2022c). Different regions may have different attitudes towards corporate innovation activities due to different regional cultures and development levels (Hu and Ji, 2017). Therefore, this paper adds year and region dummy variables to the model. This paper draws on the practice of Wen et al. (2005) on the mediation model and constructs models of Equations (1)–(3). FCi,t represents the financing constraints of firm i in year t. Patenti,t−1 is the total number of patent applications of enterprise i in year t−1. Controls denote control variables. The Year is the year-fixed effect. The Zone is the region-fixed effect. ε is the random disturbance term. When the coefficient α1 in Model (1) is significantly negative, it indicates that the patent signal can alleviate the financing constraints of new energy enterprises, and H1 is proved. If β1 is significantly positive and ω2 is significantly negative, it indicates that the patent signal can alleviate the financing constraints of new energy enterprises by increasing analyst attention, and H3 is proved. In addition, to verify H2 and H4, We divide Patenti,t−1 into invention patent signal (Patentii,t−1) and non-invention patent signal (Patentudi,t−1) for regression, respectively, and compare their regression coefficients and mediating effect regression coefficients. At the same time, to ensure the conclusion’s robustness, this paper uses heteroscedasticity robust standard errors.

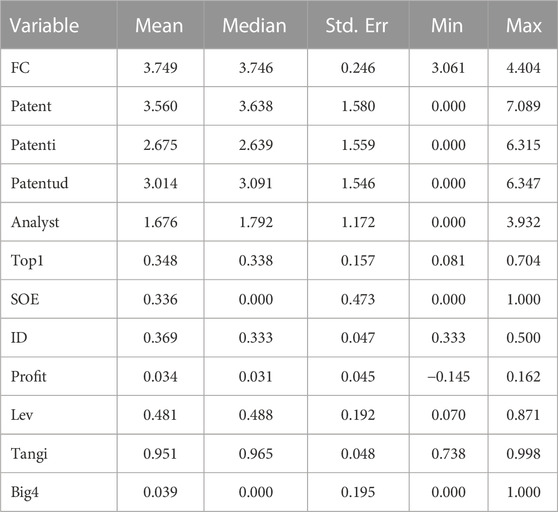

Table 3 reports the descriptive statistics of variables. There are 1,065 observations. The mean and median of financial constraints are 3.749 and 3.746, respectively. It shows that new energy enterprises are generally subject to financing constraints. The variance of patent signal and analyst attention are both large, which indicates that R&D levels and analyst attention vary significantly among firms.

TABLE 3. Descriptive statistics of variables.

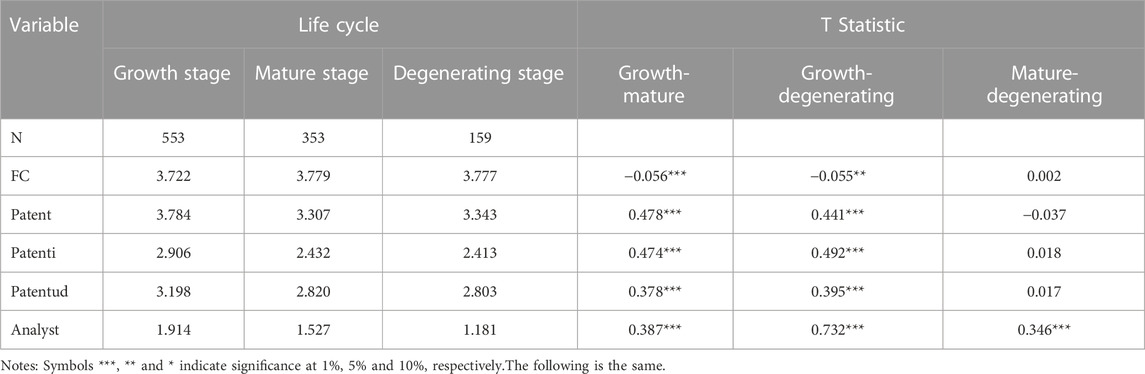

We conduct the t-test on the mean values of the main variables according to the life cycle groups. The results are shown in Table 4. As can be seen from the table, the differences in the mean value of the financial constraints between the growth and maturity stages and between the growth and recession stages are significantly negative. Nevertheless there is no significant difference between the mean values of mature and decline periods. It shows that the new energy enterprises in the mature stage and the decline stage are subject to more significant financial constraints than the new energy enterprises in the growth stage; For patent signal, no matter invention patent or non-invention patent, the mean difference between growth and maturity period, growth and decline period is significantly positive, and the mean difference between maturity and decline period is not significant, indicating that the patent output level of new energy enterprises in the growth period is relatively high, while that of new energy enterprises in the maturity and decline period is relatively low. For analyst attention, the differences between periods are significant and show a gradual decline over the life cycle.

TABLE 4. Descriptive statistics of the main variables under different life cycles.

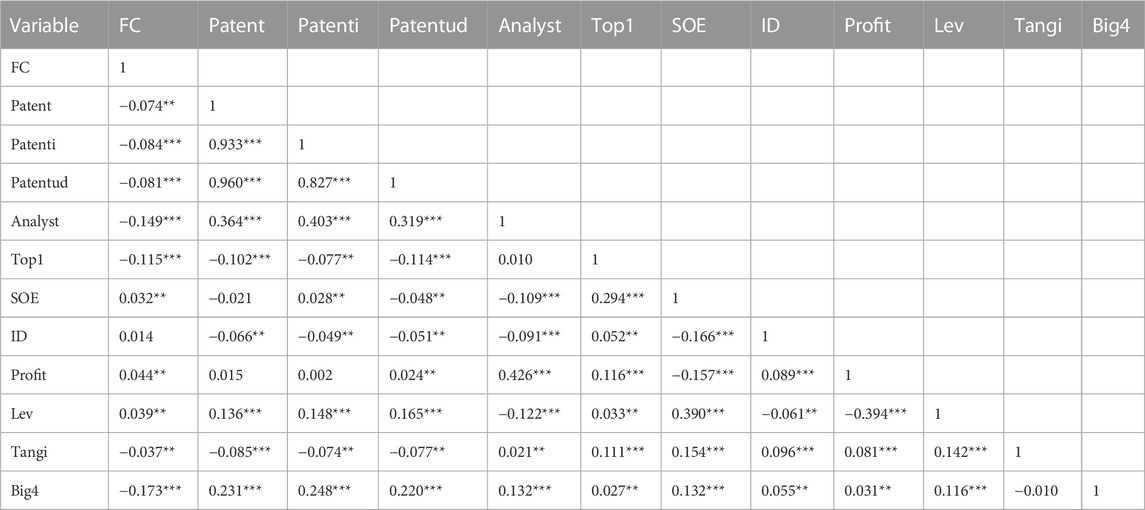

Table 5 reports the correlation coefficients between variables, showing that the correlation between financial constraints and patent signals is significantly negative. Invention patents have a stronger correlation with financial constraints than non-invention patents. The degree of analyst attention is negatively correlated with the degree of financial constraints and positively correlated with the degree of patent signal. The correlation coefficient between analyst attention and invention patents is more significant than that of non-invention patents. The above results preliminarily confirm the hypothesis of this paper, and further regression analysis is needed to explore whether there is a causal relationship between variables.

TABLE 5. Correlation coefficients of variables.

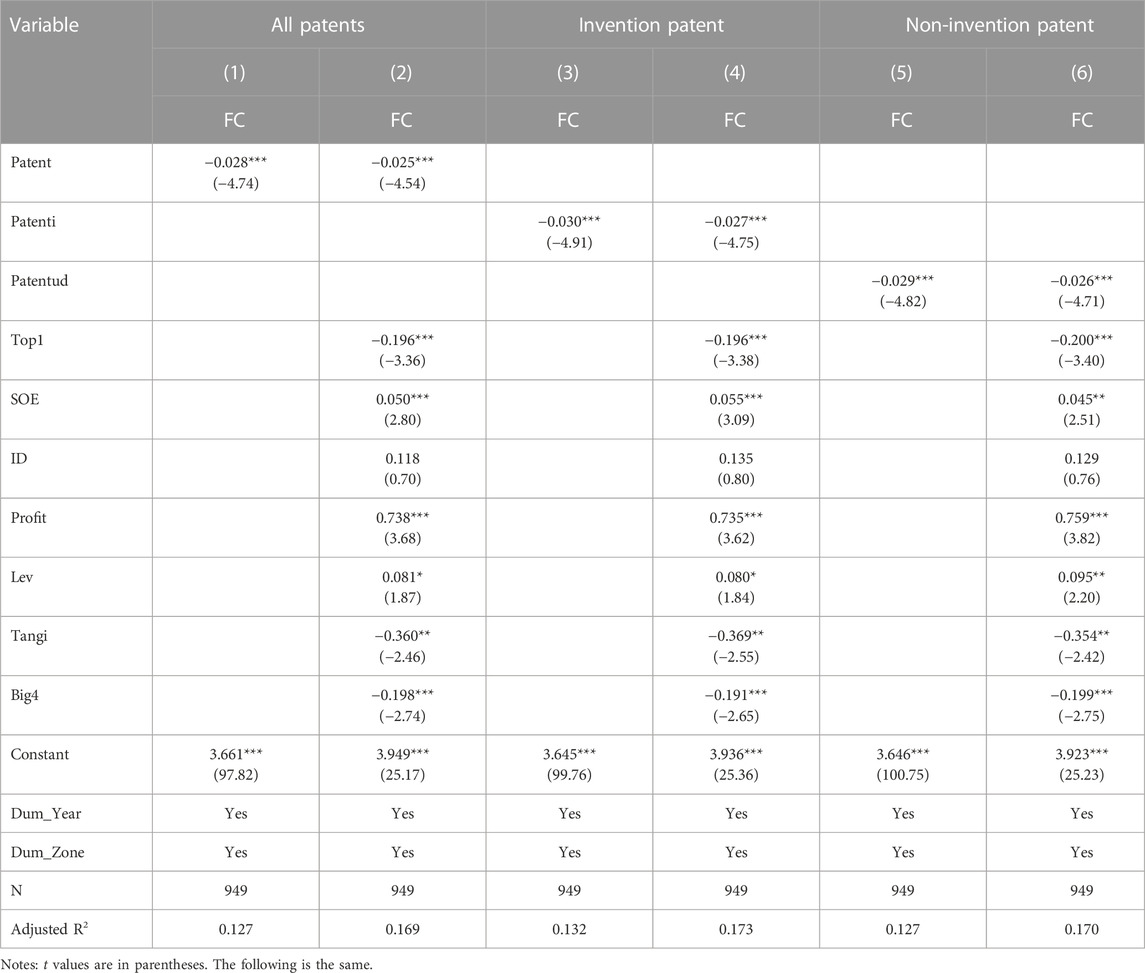

Table 6 reports the benchmark regression results of the impact of patent signals of new energy enterprises on financial constraints. The VIF value of each regression is less than 5, so the model has no multicollinearity problem. The first two columns in the table show the regression results of financing constraints of new energy enterprises on all patent signals. Column (1) shows the regression results with only time-fixed and region-fixed effects added. Column (2) shows the regression results with further control variables added. The coefficients of the patent signal are all significantly negative, indicating that the patent signal can alleviate the financing constraints of new energy enterprises.

TABLE 6. Patent signal and financing constraints of new energy enterprises.

Columns (3) and (4) are the results of the influence of the invention patent signal on the financial constraints of new energy enterprises. Columns (5) and (6) are the results of the influence of non-invention patent signals on the financial constraints of new energy enterprises. The results are significantly negative, indicating that both invention and non-invention patents can send positive signals to the market and alleviate the financing constraints of new energy enterprises. Comparing the regression coefficients of explanatory variables in columns (4) and (6), the Chi2 value of SUE test is 0.02, indicating that the difference between the two is insignificant. That is, there is no significant difference in the mitigation effect of invention and non-invention patents on the financing constraints of new energy enterprises, so H2 is rejected. The reason may be that enterprises with a high output of invention patents tend to have a high output of non-invention patents. The correlation coefficient between the two reaches 0.827. Investors generally only pay attention to the overall output of enterprise patents and do not compare the patent types among different enterprises, so there is no significant difference in the alleviation degree of financing constraints of new energy enterprises by the two patent signals.

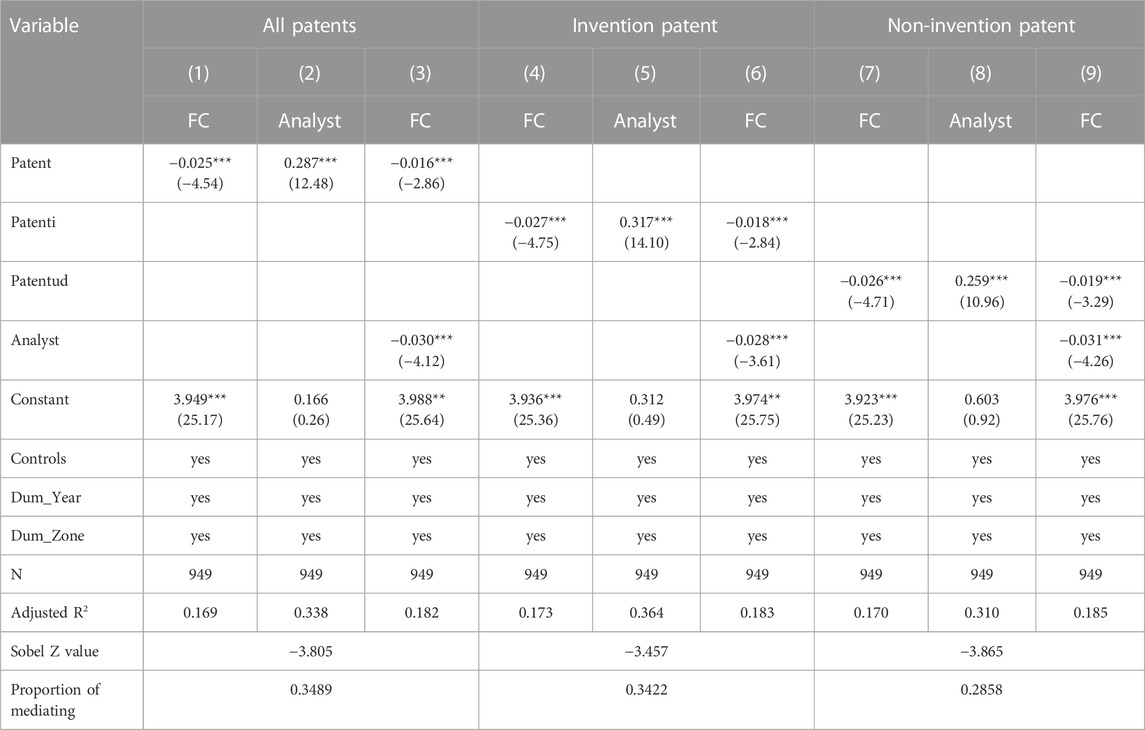

The above research results preliminarily show that patent signals can alleviate the financing constraints of new energy enterprises. On this basis, this paper further tests the internal mechanism of patent signal to alleviate the financing constraints of new energy enterprises. Table 7 shows the test results of the analyst attention’s mediating effect between patent signals and the financing constraints of new energy enterprises. The first three columns show the test results for all patents. It can be seen that after adding analyst attention, the influence coefficient of patent signal on analyst attention is significantly positive, and the influence coefficient of analyst attention on financial constraints of new energy enterprises is significantly negative. In addition, the influence coefficient of patent signal on the financial constraints of new energy enterprises becomes smaller, indicating that analyst attention plays an intermediary role between patent signal and the financial constraints of new energy enterprises. In the Sobel test, the Z-value of Sobel is −3.805, which is significant at 1%. It further proves that analyst attention mediates between patent signals and financing constraints of new energy enterprises. There is a transmission path of “increasing patent signal → increasing analyst attention → easing financial constraints”, which confirms Hypothesis H3.

TABLE 7. Regression results of the analyst attention’s mediating effect.

Table 7 (4) to (9) shows the test results of the mediating effect of analyst attention on invention patents and non-invention patents. Columns (4) to (9) in Table 7 show the test results of analyst attention’s mediating effect after distinguishing patent types. The results show that analyst attention is mediating in all of them. From the perspective of influence size, column (5) shows that the influence coefficient of the invention patent signal on analyst attention is 0.317. Column (8) shows that the influence coefficient of the non-invention patent signal on analyst attention is 0.259. SUE test shows that the Chi2 value is 13.77, which significantly rejected the null hypothesis that there is no difference between the two. It is indicated that the rise of analyst attention caused by invention and non-invention patents is different, and the impact of invention patents is more significant, which validates Hypothesis H4.

According to the Sobel test results, the invention patent signal’s total effect on new energy enterprises’ financial constraints is −0.027, and the direct effect is −0.018. The mediating effect of analyst attention is −0.009, accounting for 34.22% of the total effect. It is indicated that 34.22% of the influence of invention patent signals on the financial constraints of new energy enterprises comes from analyst attention. The total effect of the non-invention patent signal on the financial constraints of new energy enterprises is −0.026, and the direct effect is −0.019. The mediating effect of analyst attention is −0.007, accounting for 28.58% of the total effect. It shows that 28.58% of the influence of non-invention patent signals on the financial constraints of new energy enterprises comes from analyst attention. Therefore, compared with non-invention patents, analyst attention plays a more significant mediating role between invention patents and financing constraints of new energy enterprises.

To sum up, analyst attention plays an intermediary role between the two patent signals and the financing constraints of new energy enterprises. However, compared with non-invention patents, analysts will pay more attention to invention patents. Analysts do not give the same value to the signals of invention and non-invention patents, indicating that Chinese analysts can distinguish the value of different patent types to help investors make better investment decisions.

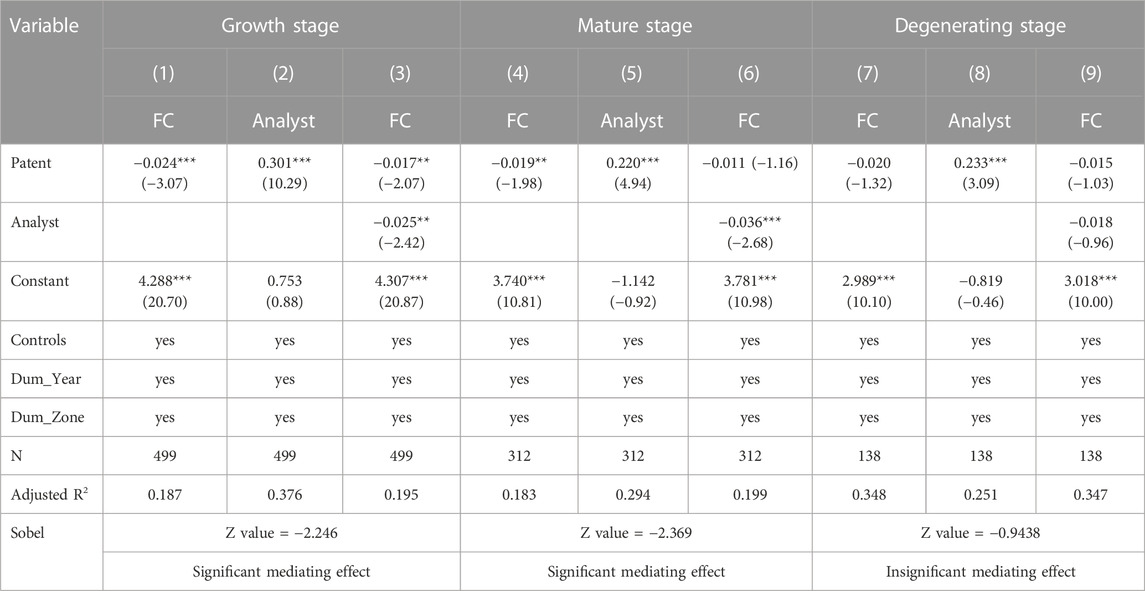

Table 8 shows the regression results of sub-samples under different life cycles. According to the estimation results in columns (1), (4) and (7), the estimated coefficients of patent signal on the financing constraints of new energy enterprises are all negative, but the significance is different. Specifically, the influence coefficient of patent signal on the financing constraints of new energy enterprises in the growth stage is −0.024, which is significant at 1%. The influence coefficient in the mature period is −0.019, which is significant at 5%. The influence coefficient is the smallest for enterprises in the recession period and does not pass the significance test. It shows that the patent signal has a mitigating effect on the financing constraints of new energy enterprises in the growth and maturity stages but has an insignificant mitigating effect on the financing constraints of new energy enterprises in the decline stage.

TABLE 8. Regression results of sub-samples in different life cycles.

From the estimated results of mediating effect in different life cycles, the patent signal significantly impacts analyst attention for the new energy enterprises in the growth and maturity stages. Analyst attention has a significantly negative impact on the financial constraints of the new energy enterprises. The influence coefficient of patent signal on the financial constraints of the new energy enterprises decreases gradually. The results of Sobel test also show that the Z-value in the growth and maturity stages is −2.246 and −2.369, respectively. Both are significant at 5%. While the Z-value in the recession stage is −0.9438, indicating that the result is insignificant. To sum up, the patent signal can alleviate the financing constraints of new energy enterprises in the growth and maturity stages by increasing analyst attention but has no apparent effect on enterprises in the decline stage, which verifies Hypothesis H5.

Companies listed on the main board generally have powerful risk resistance and slight stock price fluctuation. Although investors invest in such enterprises, the rate of return is relatively low, but the degree of risk is also low. The non-main board listed companies (including small and medium Board, Growth Enterprise Board and Science and Technology Innovation Board) face higher risks of market speculation and stock price manipulation due to their generally small equity size. Therefore, whether new energy enterprises are listed on the main board will send different information to investors. Will the heterogeneity of the listed sector affect the signalling effect of patents? So we conducted benchmark regression tests on the sample new energy enterprises in different listed sectors. The regression results are shown in columns (1) and (2) of Table 9. The results show that the influence coefficient of the patent signal on the financial constraints of new energy enterprises listed on the main board is significantly negative, while the influence coefficient of the patent signal on the financial constraints of new energy enterprises listed on the main board is insignificant. The SUE test shows that the difference in coefficients between groups is not zero. It shows that for the new energy enterprises listed on the main board, the patent signal can alleviate the financing constraints of the enterprises, while for the new energy enterprises listed on the non-main board, the alleviating effect of the patent signal on the financing constraints of the new energy enterprises is not apparent.

TABLE 9. Sector heterogeneity and size heterogeneity.

The scale of an enterprise is the basis of its comprehensive strength. The larger the scale of an enterprise is, the less affected the enterprise is by external risks. So will patent signals’ effect on enterprises differ at different scales? This paper uses the log value of total assets to measure enterprise size, and the sample enterprises are divided into high and low groups according to the median. The regression results are shown in columns (3) and (4) of Table 9. It is found that in the group of large-scale enterprises, the coefficient of the patent signal is significantly negative, while in the group of small-scale enterprises, the coefficient of the patent signal is insignificant. Moreover, SUE test shows that the coefficient difference between groups is significantly different from 0. It shows that the patent signal can alleviate the financing constraints of large-scale new energy enterprises, but the easing effect on the financing constraints of small-scale new energy enterprises is not significant.

The above results prove that the risk size and comprehensive strength of new energy enterprises will affect the utility of the patent signal. The patent signal will ease the financing constraints if the enterprise is large and its risk is low. On the contrary, if the enterprise has high operating risks, the patenting behaviour of such enterprises cannot help them relieve financial constraints. The failure rate of innovation in small and medium-sized enterprises is very high, and the future earnings are uncertain, which leads to a very high degree of aversion of investors to innovation in small and medium-sized enterprises (Yin and Yu, 2022).

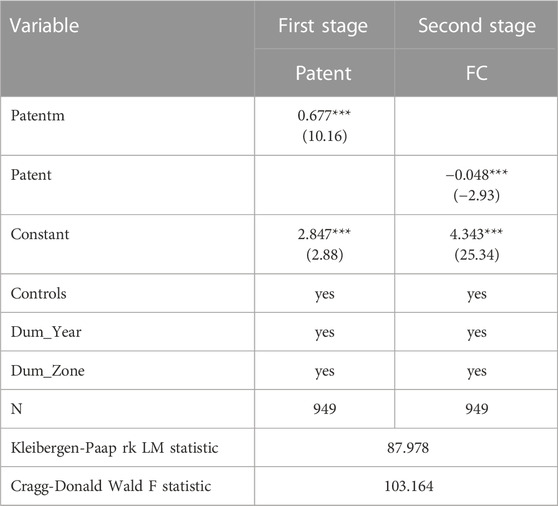

Since the degree of financial constraints will also affect the innovation output level of the company (Ju et al., 2013), the variables affecting financial constraints will inevitably be omitted in the regression. Therefore, to try to solve the errors caused by the above endogeneity problems, in addition to lagging the independent variables by one period in the model design, this paper also uses the two-stage least squares (2SLS) method to identify the causal relationship between patent signal and financing constraints of new energy enterprises. Referring to the method of choosing instrumental variables in Wei et al. (Yin et al., 2022c), we construct the instrumental variables based on the logarithm of the average number of patent applications of enterprises in the same city after plus 1(Patentm).

The regression results of instrumental variables are shown in (1) of Table 10. The Cragg-Donald Wald F-statistic is 103.164, which is much larger than the 10% critical value of the Stock-Yogo weak identification test, so the instrumental variable is not a weak instrumental variable. The LM statistic value of Kleibergen-Paap rk is 87.978, which significantly rejects the null hypothesis of insufficient identification of instrumental variables. Therefore, after considering the endogeneity problem, the influence coefficient of the patent signal on the financing constraints of new energy enterprises is still significantly negative, indicating that the results of this paper are robust.

TABLE 10. Instrumental variable regression results.

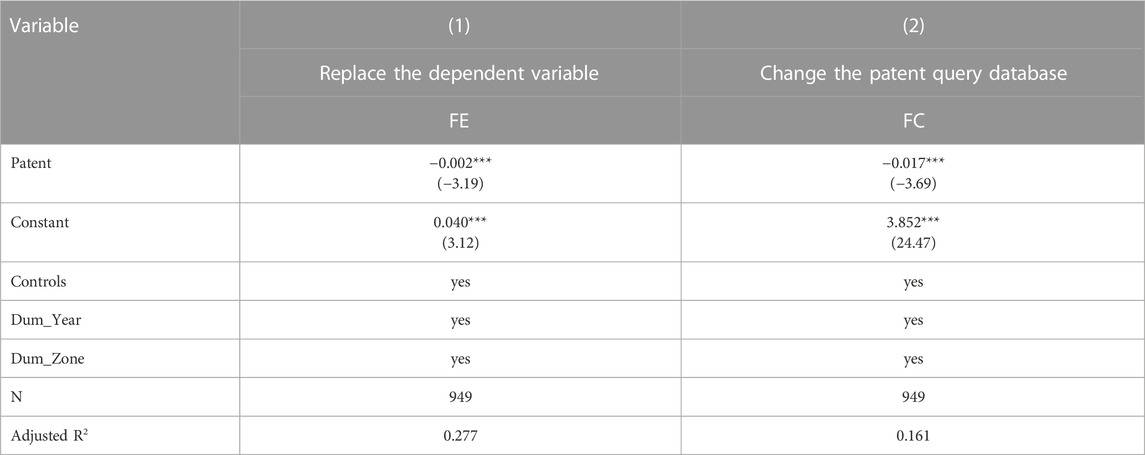

Referring to Wang et al. (Wang and Lu, 2022), we use debt financing cost, the ratio of financial expenses to total liabilities (FE), as the explained variable. The greater the level of financing constraints on enterprises, the higher the cost of debt financing is. If the patent signal can alleviate the financing constraints of new energy enterprises, then the influence coefficient of the patent signal on debt financing cost should be negative. The regression results are shown in Column (2) of Table 11. The coefficient of the patent signal is also significantly negative, indicating that the results of this paper are robust.

TABLE 11. Robustness regression results.

In this part, we use the patent retrieval system of the State Intellectual Property Office to query the patent application data. We used the company name for the search. If the company name is changed, we search different names separately and use the patent disclosure number to confirm that the patents obtained by multiple searches are not repeated. The regression results are shown in Column (3) of Table 11. The results are consistent with the sign of the benchmark test regression results and are significant at 1%, indicating that the benchmark test results are robust.

In the context of green development, this paper takes A-share new energy listed enterprises in Shanghai and Shenzhen as samples to explore the impact of patent signals on the financing constraints of new energy enterprises and their mechanism. The conclusions are as follows: (i) Patent signal can send positive information to the market and alleviate the financing constraints of new energy listed enterprises, and there is no significant difference in the effect of invention and non-invention patent signals on the financing constraints of new energy enterprises; (ii) Analyst attention plays an intermediary role between patent signals and financing constraints of new energy enterprises. Compared with non-invention patents, analysts will pay more attention to invention patents so that invention patent information is more transmitted to investors; (iii) Compared with the new energy enterprises in the decline period, the signal effect of patents and the mediating effect of analyst attention are more significant when the new energy enterprises are in the growth and maturity stages; (iv) The comprehensive strength and risk of new energy enterprises will affect the utility of patent signal.

From the research conclusions of this paper, the following implications can be obtained:

For the government, it can take tax subsidies and other ways to guide new energy enterprises to carry out innovation activities to alleviate the financing constraints of new energy enterprises; Strengthen the credit system construction for small and medium-sized new energy enterprises. Due to the lack of an adequate credit guarantee, new energy SMEs are disadvantaged in financing, and investors cannot recognize their patent signals well. Explore the establishment of government-guaranteed financing platforms. Provide corresponding subsidies, Actively promote diversified financing methods of new energy enterprises and establish a scientific and practical financing evaluation system to reduce investors’ investment risks (Xiao et al., 2022).

For managers of new energy enterprises, to alleviate financing constraints, they can consider sending positive information to the market through patent applications. But they should first consider their life cycle and resilience to risk. If the enterprise is in the growth or maturity stage and has a strong ability to resist risks, the behavior of patent application can play a positive signal role and help the enterprise relieve financial constraints. If the enterprise is already in the recession period and its ability to resist risks is relatively weak, the effect of patent application on alleviating the financial constraints of the enterprise is not great, and the high risk of R&D projects may also aggravate the financial constraints of the enterprise; At the same time, it should be noted that analysts are more sensitive to the trend of enterprises than ordinary investors, so they should pay attention to the information transmission role of securities analysts in the capital market.

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

QL: Methodology, Validation, Writing–review and editing. LP: Formal Analysis, Investigation, Project administration, Writing–original draft. SY: Conceptualization, Funding acquisition, Investigation, Project administration, Resources, Writing–review and editing.

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. This research was funded by the National Social Science Fund of China, grant number (22CJY043).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Arora, A., and Ceccagnoli, M. (2006). Patent protection, complementary assets, and firms' incentives for technology licensing. Manag. Sci. 52, 293–308. doi:10.1287/mnsc.1050.0437

Chen, Y., Xu, W., and Zhou, Y. Y. (2022). Impact of innovation policy on technological innovation of new energy enterprises: an empirical analysis based on Chinese new energy enterprises. Sci. Technol. Manag. Res. 42, 8–15.

Cheng, X. S., Zheng, H. A., and Cheng, Y. A. (2020). Study of innovation disclosure, analyst tracking and market reaction. Res. Manag. 41, 161–173.

Dickinson, V. (2011). Cash flow patterns as a proxy for firm life cycle. Account. Rev. 86, 1969–1994. doi:10.2308/accr-10130

Dong, T., Yin, S., and Zhang, N. (2023a). New energy-driven construction industry: digital green innovation investment project selection of photovoltaic building materials enterprises using an integrated fuzzy decision approach. Systems 11 (1), 11. doi:10.3390/systems11010011

Dong, T., Yin, S., and Zhang, N. (2023b). The interaction mechanism and dynamic evolution of digital green innovation in the integrated green building supply chain. Systems 11 (3), 122. doi:10.3390/systems11030122

Dou, H., Zhang, H. L., and Lu, Z. F. (2014). Enterprise groups, majority shareholder monitoring and overinvestment. Manag. World 134-143, 171.

Fazzari, S., Hubbard, R. G., Petersen, B. C., Blinder, A. S., and Poterba, J. M. (1988). Financing constraints and corporate investment. Brookings Pap. Econ. Activity 1988, 141–195. doi:10.2307/2534426

Feng, Z. X., Wang, Q., and Hou, X. H. (2011). Government input, degree of marketization and technological innovation efficiency of Chinese industrial enterprises. Res. Quantitative Tech. Econ. 28, 3–17.

Hadlock, C. J., and Pierce, J. R. (2010). New evidence on measuring financial constraints: moving beyond the KZ index. Rev. Financial Stud. 23, 1909–1940. doi:10.1093/rfs/hhq009

Hu, C., Yang, H., and Yin, S. (2022). Insight into the balancing effect of a digital green innovation (DGI) network to improve the performance of DGI for industry 5.0: roles of digital empowerment and green organization flexibility. Systems 10 (4), 97. doi:10.3390/systems10040097

Hu, Y. M., and Ji, D. (2017). Directors' technical expertise, innovation efficiency and firm performance. Nankai Manag. Rev. 20, 40–52.

Jiang, F. X., Wang, Y. T., Tian, Y., and Wu, K. (2017). . Multiple large shareholders and corporate finance constraints: Empirical evidence based on textual analysis. Management World, 61–74.

Ju, X. S., Lu, D., and Yu, Y. H. (2013). Financing constraints, working capital management and corporate innovation sustainability. Econ. Res. 48, 4–16.

Li, X., Liu, X., Huang, Y., Li, J., He, J., and Dai, J. (2022). Evolutionary mechanism of green innovation behavior in construction enterprises: evidence from the construction industry. Eng. Constr. Archit. Manag. doi:10.1108/ecam-02-2022-0186

Lian, Y. J., and Cheng, J. (2007). Investment-cash flow sensitivity:financing constraint or agency cost? Financial Res., 37–46.

Liu, M., Jiang, L. H., and Shi, J. C. (2021). Government regulation and corporate innovation: A case study based on listed vaccine companies. Econ. Theory Econ. Manag. 41, 97–112.

Ma, R. M., Zhang, D. X., and Ge, Y. (2022). Ineffective innovation signal or insufficient market incentive: the mystery of ineffective resource allocation of venture capital market to science and technology enterprises. Sci. Technol. Prog. Countermeas., 1–10.

Tang, W., Xia, X. X., and Jiang, F. X. (2019). Controlling shareholders' equity pledges and corporate financing constraints. Account. Res., 51–57.

Wang, Z. J., and Lu, Z. J. (2022). Green finance, analysts' concern and new energy enterprise financing relief. Contemp. Finance Econ., 52–63.

Wei, Z. H., Zeng, A. M., and Li, B. (2014). Financial ecosystem and corporate financing constraints: an empirical study based on Chinese listed companies. Account. Res. 73-80, 95.

Wen, Z. L., Hou, J. T., and Zhang, L. (2005). Comparison and application of moderating and mediating effects. J. Psychol., 268–274.

Wu, Y., Shen, K. R., and Lu, Y. (2020). Photocaged functional nucleic acids for spatiotemporal imaging in biology. Macro Qual. Res. 8, 95–104. doi:10.1016/j.cbpa.2020.05.003

Xiao, X., Yu, Z. Q., and Li, X. Y. (2022). Utilizational innovation strategies, undervaluation and financing constraints under substantive orientation: an empirical study based on technology-based SMEs. Finance Econ., 57–68.

Xiao, Z. Y., and Lin, L. (2019). Firm financialization, life cycle and continuous innovation: an empirical study based on industry classification. Financial Res. 45, 43–57.

Yang, Y. L., Cheng, J. Y., You, P. P., and Wang, K. (2023). Can online media reports pierce the private information barrier: an empirical investigation based on analysts' alumni relationship with listed company executives. Financial Res., 1–18.

Yao, D. J., Hu, J. Z., and Xie, Y. F. (2023). Will digital finance affect innovation investment of environmentally sensitive enterprises: the perspective of corporate life cycle. Financial Theory Pract., 26–37.

Yin, S., Dong, T., Li, B., and Gao, S. (2022c). Developing a conceptual partner selection framework: digital green innovation management of prefabricated construction enterprises for sustainable urban development. Buildings 12 (6), 721. doi:10.3390/buildings12060721

Yin, S., Wang, Y., and Xu, J. (2022b). Developing a conceptual partner matching framework for digital green innovation of agricultural high-end equipment manufacturing system toward agriculture 5.0: A novel niche field model combined with fuzzy vikor. Front. Psychol. 13, 924109. doi:10.3389/fpsyg.2022.924109

Yin, S., and Yu, Y. (2022). An adoption-implementation framework of digital green knowledge to improve the performance of digital green innovation practices for industry 5.0. J. Clean. Prod. 363, 132608. doi:10.1016/j.jclepro.2022.132608

Yin, S., Zhang, N., Ullah, K., and Gao, S. (2022a). Enhancing digital innovation for the sustainable transformation of manufacturing industry: A pressure-state-response system framework to perceptions of digital green innovation and its performance for green and intelligent manufacturing. Systems 10 (3), 72. doi:10.3390/systems10030072

Yu, J. H., and Yu, M. C. (2019). Fiscal subsidies, rent-seeking costs and business performance of new energy enterprises. Soft Sci. 33, 59–63.

Yu, Y., and Yin, S. (2023). Incentive mechanism for the development of rural new energy industry: new energy enterprise–village collective linkages considering the quantum entanglement and benefit relationship. Int. J. Energy Res. 2023, 1–19. doi:10.1155/2023/1675858

Zhang, C., and Tang, Jie. (2022). Does patent pledge financing ease the financing constraints of small and medium-sized enterprises? J. Central Univ. Finance Econ., 39–51.

Zhang, X. X., and Wu, C. F. (2006). Do financing constraints affect the cash holding policies of listed companies in China: an analysis from cash-cash flow sensitivity. Manag. Rev., 59–62.

Zhao, X. L., Hu, X. W., Wu, P., and Gao, L. (2021). The impact of policy uncertainty on new energy enterprise investment under limited rationality. Manag. Sci. 34, 43–54.

Zheng, Y., and Zhang, Q. L. (2019). How patent signaling eases corporate financing constraints: an evaluation of the effectiveness of patent pledge financing policies based on patent pledge. Manag. Q. 4, 55–72.

Zhong, Q. Y., and Shi, X. F. (2016). Media attention, nature of property rights and financing constraints of listed companies: an empirical test based on heckman's two-stage model. Bus. Econ. Manag., 87–97.

Keywords: patent signal, financing constraints, new energy, analyst attention, life cycle

Citation: Li Q, Pang L and Yin S (2023) Patent signal and financing constraints: a life cycle perspective and evidence from new energy industry. Front. Energy Res. 11:1277164. doi: 10.3389/fenrg.2023.1277164

Received: 14 August 2023; Accepted: 18 September 2023;

Published: 28 September 2023.

Edited by:

Xingwei Li, Sichuan Agricultural University, ChinaReviewed by:

Jian Hou, Henan Agricultural University, ChinaCopyright © 2023 Li, Pang and Yin. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Qianjie Li, bGlxaWFuamllMTFAMTI2LmNvbQ==

†ORCID: Shi Yin, https://orcid.org/0000-0001-6885-7412

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.