Muyun Li

Muyun Li Lihua Wang1

Lihua Wang1 Zhongyan Liu

Zhongyan Liu Qile He

Qile He- 1Business School, Hunan University of Technology, Zhuzhou, China

- 2International Business Center, Zhejiang CRRC Shangchi Electric Co., Ltd., Haining, China

- 3College of Business, Law, and Social Sciences, University of Derby, Derby, United Kingdom

In recent years, because of the increasingly severe global environmental protection situation and the superimposed effect of the new crown epidemic, the importance of green finance has been highlighted and gradually elevated to an important future development strategy for the country. However, it is unclear how to improve the effectiveness of green finance in each province. Using 30 Chinese provinces and regions as research samples, this paper summarizes five influencing factors, including regional logistics, carbon emission index, regional finance, economic level, and environmental regulation. Considering the complex causal relationship between factors and green finance performance, fsQCA is used to explore the different configurations formed in the process of developing green finance in each province. The results comprise four different configurations for high performance and four types of configurations for the absence of high performance. Currently, with the regional green finance development model still in its infancy, regional logistics and carbon emission index factors play a key role in stimulating the development of green finance in the provinces and regions. This study has important theoretical and practical significance for the construction of regional green financial system and local government performance appraisal system with local characteristics in each province of China, and provides locally adapted policy suggestions for different provinces to achieve optimal allocation of resources.

1 Introduction

With the development of the world economy, the economic constraints brought about by resource and environmental issues are becoming more and more obvious and have attracted the general attention of all countries in the world (Zhang Dongyang et al., 2021). In this process, global warming caused by carbon emissions has become an important factor threatening the sustainable development of the world. Green finance is a key element in the global response to the extreme climate threat and the goal of carbon neutrality (Lee, 2022). It grafted the concept of “green” and “low-carbon” onto traditional financial instruments, and raised capital to support the response to climate change and efficient use of resources by issuing bonds, institutional financing and credit loans, etc (Larsen et al., 2023). It is a key element that connects the concept of “green” and “low-carbon” to traditional financial instruments, and raises capital to support economic activities in response to climate change and efficient use of resources by issuing bonds, institutional financing and credit loans, and guides the transformation of high-pollution, high-energy-consumption and high-emission industries to green, low-carbon, safe and efficient (Zhou et al., 2020). As the world’s largest energy consumer, China is striving to achieve “peak carbon dioxide emissions” by 2030 and “carbon neutrality” by 2060. Since the interval from peak carbon to carbon neutral is only 30 years, which is shorter than the 70-year transition cycle in Europe, China need to accelerate the transformation and upgrade industrial and energy structures, which will generate huge demand for investment and finance (Zhang Dongyang et al., 2021). Therefore, China must now promote the development of green finance in order to solve the finance problem (Diaz et al., 2023).

The development of green finance in China relies on the reform and development of the financial industry and capital market, as well as strong policy support (Yu et al., 2021). To further promote the construction of an ecological civilization, China has taken a series of measures in the construction of a green financial system and the development of green finance and has made breakthrough progress (Zhang Shengling et al., 2021). From 2012 to 2021, China’s green financial system has undergone a process of development from scratch from slow to fast and from surface to surface (Lee, 2022). The scale of green financial products and markets continues to expand, with the total amount of green credit, the number of green bonds, and the scale of the carbon emissions trading market all ranking among the highest in the world (Jinru et al., 2022). In September 2020, General Secretary Xi Jinping made a solemn commitment to the world that China would achieve “peak carbon dioxide emissions” by 2030 and “carbon neutrality” by 2060. With the proposed “peak carbon dioxide emissions” and “carbon neutrality” targets, the task of improving the green financial system to guide the green transformation of the economy and society has become more urgent (Zhou et al., 2020).

In recent years, most scholars have conducted research on the content of green financial development. From the traditional mainstream academic viewpoint, as green finance needs to fully rely on the financial sector environment and related resources in the place where it is developed (Zhou et al., 2020), Chinese provinces and regions with a developed financial sector, such as Beijing and Shanghai, have achieved more significant results in developing green finance, while Chinese provinces and regions with a relatively weak financial sector development have achieved relatively weaker results in implementing local green regional finance (Zhang Shengling et al., 2021). In other words, developed provinces from eastern China have an inherent advantage over central and western regions in building a green financial system. However, according to the IIGE’s 2019 Local Green Regional Finance Report, the level of green regional finance in China is uneven across regions, with significant disparities among provinces (Zhou et al., 2020). In particular, the cluster of Chinese provinces with high green finance indices includes central and western provinces such as Jiangxi, Xinjiang, and Sichuan, while the cluster of provinces with low indices includes developed eastern provinces and regions (Lee, 2022). The degree of financialization of each province in China is not the only factor determining the performance of local green finance, and there are other factors exist that jointly influence the development of green finance in China (Yu et al., 2021). For instance, regional logistics can enhance the strength of regional information exchange capacity and can minimize the negative impact of the information asymmetry in the region (Wei et al., 2022). The carbon emission index can reflect the overall environmental conditions and changes in the industrial structure of the city, which can effectively assist government decision-making (Bin et al., 2022). The economic level can represent the comprehensive strength of the provinces and regions and the potential of supporting the green finance industry, which can allocate more public resources (Wang Hui et al., 2021). The stricter the environmental regulation is, the more enterprises will reduce pollution through emission reduction or transformation, which can make provincial and regional industries develop in the direction of environmental protection and low carbon (Xie et al., 2020). Because of the differences in local resource endowments and inherent conditions (Afshan et al., 2023), each Chinese province and region has gradually developed different development configurations in the process of building a regional green financial system by considering their own characteristics (Zhang Dongyang et al., 2021). Therefore, it is important to explore the configuration to improve green financial performance and identify the causative factors of the differences in green financial performance, so as to provide theoretical reference for Chinese provinces to build a regional green financial system with local characteristics and a local government performance appraisal system.

Based on the above analysis, it is obvious that the existing literature still has the following three shortcomings. First, scholars (e.g., Zhou et al., 2022; Li et al., 2022; Bakry et al., 2023; Zhang et al., 2023; etc.) have evaluated regional green finance as a whole, yet the variables used are not simultaneously universal and targeted to some degree, and cannot give full play to the evaluation of green finance. Second, existing studies (e.g., Yu et al., 2022; Li et al., 2022; Wang Yanli et al., 2021; Ran et al., 2023; etc.) focus more on factors or combinations that can improve green finance performance, yet lack analysis on the differential aspects of green finance performance. However, this has practical implications for how Chinese provinces allocate factors to achieve high green financial performance or avoid non-high green financial performance. In addition, some scholars (e.g., Wang Hui et al., 2021; Mao et al., 2021; Wei et al., 2022; Xu et al., 2023; Li et al., 2023; Ip et al., 2023; etc.) focus on green financial performance as an influencing factor, and explore more how green financial performance contributes to high-quality economic development or other variable growth, yet few studies analyze in depth how to enhance green finance. However, if a province or a country wants to achieve the ultimate goal, it should firstly clarify the configuration of enhancing green financial performance in light of its own actual situation. Therefore, this paper constructs a data sample based on 30 Chinese provinces from a holistic perspective and conducts an empirical study to explore the different histories formed by each province and region in the process of developing green finance using fsQCA. In particular, this study examines the following three questions:

RQ1: How does each conditioning variable affects green finance performance? Is it influenced by a single variable? Or is it influenced by multiple variables?

RQ2: What are the variables or combinations that lead to high green financial performance and non-high green financial performance?

RQ3: What are the relationships between the different configurations? Are there any similarities or contradictions among them?

Compared with previous studies, the main innovation of this paper is using fsQCA to explore the configurations to improve green financial performance from a configuration perspective and the causal factors of the differences in green financial performance. fsQCA has been recognized as an effective method for exploring the combined effects (Chen et al., 2021) and has been widely used in various fields of management disciplines (Zhong Weishun et al., 2022). First, it enables us to explore and compare the key factors affecting the performance of green finance across Chinese provinces and regions from both a high perspective and the absence of one (Wang Quan et al., 2022). Second, this paper exceeds previous single-factor studies and conducts a multi-factor combination configuration analysis with the help of fsQCA, which introduces a new way to study the state of green finance and expands and enriches previous findings (Liang et al., 2022). In addition, the multi-case analysis approach is more general than that of single-case analysis (Diao and Liu, 2021).

This study contributes in several ways. First, a co-occurring network analysis was conducted to identify the latest research trends and categorize the literature. Second, a research framework of green financial performance was constructed. Third, it explored the configurations to improve green financial performance from a configuration perspective, identified the causal factors for differences in green financial performance, and enriched the existing literature. Ultimately this study found four different types of high-performance configurations and four types of non-high performance configurations. Comparing the different types of conditional configurations, it found that regional logistics and carbon emission indicator factors played a key role in incentive’s the development of green finance in each province. This study has important theoretical and practical significance for the formulation of green finance policies in Chinese provinces, and provides a reference for different provinces to improve their green finance performance according to local conditions. Since this study only focuses on China, the largest emerging economy, thus limiting the generalization of the results to other emerging economies, future studies will compare the results with those of other countries to further discuss the similarity and heterogeneity of the results obtained.

The remainder of this paper will proceed as follows. Section 2 presents the literature review and the theoretical framework. Section 3 and Section 4 present the research methodology and data analysis, respectively. Section 5 discusses the results of the data analysis. Section 6 reports the conclusions, implications, and limitations of the study.

2 Literature review and theoretical framework

2.1 Literature review

This study retrieved data from the WoS database (with SCI-EXPANDED and SSCI only) created by Clarivate Analytics on 1 January 2023. The study topic was selected as Topic: “Green Finance” OR “Green Financial Effectiveness” and refined by Language: English AND Document types: Article OR Review Article OR Meeting Abstract. The time frame chosen for this paper was 2011–2022 because the first article was published in 2011.We refined and retrieved 533 records using the above settings. The literature data download completed the first step in the process of creating the database. Next, we imported the data into CiteSpace. CiteSpace can identify hot research topics and cutting-edge research in the field of green finance based on the frequency of popular keywords used in journal articles (Jia et al., 2019). Bursts of certain keywords can be used to analyze the evolution of green finance research and identify the latest research trends (Ding and Zhong, 2022). An outburst is a significant change in the value of a variable over a relatively short period of time (Jia et al., 2020). The value of a variable can change significantly in a relatively short period of time (Li and Wang, 2016). CiteSpace considered this type of change to be a way of identifying research frontiers (Ying et al., 2022).

As shown in Figure 1, co-occurring network analyses were performed using keywords such as “node type.” It indicated that recent popular research topics in green finance included green credit, green innovation, driving factor, climate change, performance, and economic growth. Topics with high centrality included energy, environmental performance, policy, carbon emission reduction, finance, economic development, determinant, technology, and management. As can also be seen from the visualization, green finance was linked to current political hotspots such as carbon finance and sustainable development and has been used by many scholars for cross-sectional research because of the policy-oriented nature of the subject itself. Overall, from the results analyzed by CiteSpace, the research in this field was divided into the following two categories, the context of the real-life contextual application of green finance and the factors influencing green finance.

FIGURE 1. Popular research topics.

2.1.1 Real-life contextual applications of green finance

Green finance is mainly applied in real life around the government’s policy strategy, social development of specific industries and innovation of environmental protection industry. The implementation of green finance in China is an effective measure to mitigate greenhouse gas emissions because green finance can influence the greenhouse effect by promoting the rapid growth of the provincial economy, curbing energy efficiency, and accelerating the optimization of the current industrial structure (Wang and Ying, 2022a). Zhou et al. (2022) found that the levels of financial development and environmental governance promote the development of green finance, while the levels of economic growth and energy consumption inhibit the development of green finance. On this basis, he proposed countermeasures and recommendations in terms of strengthening government functions and adjusting industrial structures in line with economic growth. Wang Yanli et al. (2021) considered that the development of green finance facilitated the transformation of traditional energy consumption to renewable energy consumption. The impact of green finance on the structural transformation of energy consumption is mainly reflected in the direct effect. Therefore, the government should support green finance to reduce traditional energy consumption and increase renewable energy consumption. Mao et al. (2021) found that green finance works by improving economic efficiency, enhancing people’s wellbeing, optimizing economic structure, and promoting innovation and development. However, the impact of green finance implementation varies from region to region (Zhang et al., 2023). For example, it is stronger in western China than in the central and eastern regions. Still, other scholars have found that environmental performance can positively influence green innovation in the long run in non-emerging countries and countries with better green innovation or environmental performance (Yu et al., 2022). Furthermore, green finance has a positive impact on green innovation in emerging countries and countries with low levels of green finance, while green finance has a negative impact on green innovation in countries with better green innovation or environmental performance (Wang Yunbo et al., 2022).

2.1.2 Factors influencing green finance

Academic research on the influence factors of green finance began earlier and was richer in detail, but the influence factors used by scholars were relatively single, and there was less comparative analysis between the roles of various factors, as shown in Table 1. Jinru et al. (2022) collected data from 240 respondents in the Chinese manufacturing sector and analyzed them using structural equation modeling, finding that green financing and green logistics have a significant positive impact on sustainable production and the circular economy. He also proposed that green financing and green logistics should be incorporated into companies' sourcing and financing strategies to manufacture green and sustainable goods and to advance circular economy goals. Wei et al. (2022) claimed that green finance has clear negative and positive impacts on carbon emissions and green economic recovery. In his study of the relationship between economic, financial, and environmental development and green finance, he found that inadequate transport-related infrastructure and logistics services are the other important contributors to overall carbon dioxide and greenhouse gas emissions. He also found that sustainable energy development can be facilitated by promoting the growth of green finance. The logistics sector plays a vital role in the economic development of a country (Bin et al., 2022). However, logistics development can also affect the quality of the environment, as the logistics sector is seen as a major energy-consuming sector (Wei et al., 2022). Therefore, emerging countries need to align their logistics sector policies with sustainable development goals. At the same time, more resources should be allocated to the green innovation and renewable energy sectors (Jinru et al., 2022; Taridala et al., 2023), and the globalization of the economy should be promoted in order to foster sustainable development. Li et al. (2022) constructed a comprehensive evaluation system for green finance, using the number of patents granted for low-carbon innovations to measure low-carbon technology innovation. In his study, he found that green finance can significantly contribute to the transformation of a low-carbon economy, but this contribution decreases with the intervention of low-carbon technological innovation (Li et al., 2022). As a result, he recommended helping China improve the development of green finance to facilitate the transformation and upgrading of a low-carbon economy. Wang Hui et al. (2021) examined the policy effects, the mechanisms for establishing green financial reforms, and the impact of innovation pilot zones on green development. The results indicated that the high level of financial input for environmental protection and marketization helped the pilot zones to further play a positive role in promoting regional green development (Wang Quan et al., 2022). He also proposed that China make reasonable arrangements among regions according to local conditions and that the government should guide market players to establish the concept of green development, gradually build an environmentally friendly and circular economic model, and enhance the overall green development capacity of the region. The development of green finance in the Yangtze River Delta region of China has a clear spatial clustering effect and there are large regional differences (Xie et al., 2020). Regional GDP, regional innovation level and air quality are the most important factors influencing green finance, but the degrees of financial development and industrial structure optimization are not significant (Qian et al., 2022). In fact, financial agglomeration and green economic growth have become a global trend in financial and economic development, and financial agglomeration has a significant positive impact on green financial growth (Wang Hui et al., 2021). By comparing different regions, Zhou et al. (2022) found that the impact of green finance on ecological development has a U-shaped relationship and that the level of tertiary industry development, economic development, and foreign direct investment also have a significant positive impact on ecological development, but the level of urbanization has a negative relationship with regional ecological development.

TABLE 1. Factors influencing green financial performance from prior studies.

2.2 Research framework

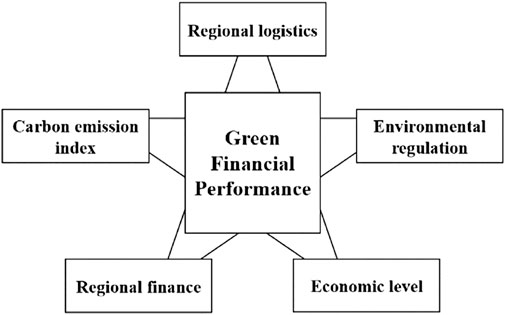

According to the literature described above, and the statistical analysis of scholars' use of each factor, this study have developed a research framework to explain the influence on the performance of green finance, as shown in Figure 2. We propose that regional logistics, carbon emission index, regional finance, economic level, and environmental regulation will have an impact on green finance. Although scholars have analyzed each of these five factors having an influence on green finance individually, the causal relationship between green financial performance and these conditional variables is very complex, and it is not inevitable that a single variable plays a role in causing green finance to have high or non-high performance. So the study need to further explore the configurations of improving green financial performance and the differences in the green financial performance of causal factors in allocation terms.

FIGURE 2. Research framework.

2.2.1 Regional logistics

Regional logistics is not only a reflection of regional transport capacity but also represents the strength of the regional information exchange capacity (Jinru et al., 2022). Regional information will flow with the transactions between social capital in the supply chain, and in the process of information exchange and flow, there are often regions that become information nodes because of their geographical or economic advantages in gathering a large amount of information flow (Wei et al., 2022). The higher the level of regional logistics, the more it indicates that the region occupies the core position of information and dominates the process of information flow (Bin et al., 2022). A high level of regional logistics can minimize the negative impact of information asymmetries, which is a major risk in the financial sector (Wei et al., 2022).

2.2.2 Carbon emissions index

A city’s carbon emissions index can measure the total carbon emissions of a city over a specific period, reflecting the changes in the overall environmental conditions and industrial structure of the city (Li et al., 2022). It also assists the government in decision making, provides a real-time scientific basis for the development of regional carbon emission reduction plans, and provides a useful reference for the development of green finance (Wei et al., 2022). When the carbon emission index of a region remains low, the place can be judged to have entered the post-industrialization stage or the implementation of environmental protection work is more efficient, which is conducive to regional green regional finance (Bin et al., 2022).

2.2.3 Regional finance

Differentiation in regional financialization is closely related to green regional finance (Wang Hui et al., 2021). When a locality has a more mature regional financial system, it will be more likely to develop green financial products and services (Xie et al., 2020). In addition, green finance has been pushed as a national strategy in recent years. By creating new green finance businesses (Qian et al., 2022), financial institutions can help to open new markets while strengthening their own sense of social responsibility and creating a good institutional image (Wei et al., 2022).

2.2.4 Economic level

The level of the local economy represents to some extent the comprehensive strength of the region and the potential to support the green finance industry (Wei et al., 2022; Bin et al., 2022). In an actual situation, developed regions can allocate more public resources and implement policies more effectively when developing green finance (Xie et al., 2020; Wang Hui et al., 2021; Zhou and Xu, 2022).

2.2.5 Environmental regulation

From the traditional research perspective, the more stringent the environmental regulations, the more enterprises will reduce their pollution by reducing emissions or transforming themselves in order to escape the pressure of related policies and systems (Wang Yanli et al., 2021), which will lead to higher costs and lower production capacity during the initial period and indirectly cause the local economy to regress and the financial sector to develop poorly (Zhou and Xu, 2022). At the same time, considering severe control measures will bias the regional industry toward environmental protection and low carbon development, which is conducive to the construction of a more reasonable industrial structure system in the long run (Xie et al., 2020). In addition, the improvement of the overall environment will have a positive impact on the innovation of green finance industry (Wei et al., 2022).

3 Research methodology

3.1 Qualitative comparative analysis

Qualitative comparative analysis (QCA) is an empirical research method based on the pooling theory proposed by Charles C. Ragin, an American sociologist, and is generally applied to small and medium-sized samples (Du and Kim, 2021). QCA aims to focus on the grouping of configurations that arise when problematic outcomes occur and to analyze multiple configurations that lead to the same outcome from a pooling perspective by looking at real-life situational cases behind different configuration representatives (Chuah et al., 2021). QCA is considered a new type of research method between qualitative and quantitative (Mei et al., 2022). In addition, QCA is divided into three specific operations based on the type of variables: crispy set (csQCA), fuzzy set (fsQCA), and multi-set (mvQCA). Among them, csQCA is only used to deal with dichotomous variables (Chen et al., 2021), mvQCA is suitable for dealing with multi-category variables (Zhang and Long, 2022), while fsQCA can solve problems such as partial affiliation or causal changes (Ren et al., 2016).

The fsQCA method was chosen for three main reasons. First, the fsQCA method can reorganize many influencing factors to form a condition configuration and enable a holistic analysis to investigate how the combination of antecedent conditions leads to continuous changes in the outcome variables (Chu et al., 2019) and to explore the conditions and combinations of conditions that have explanatory power on the outcome variables (Zhong Weishun et al., 2022). The fsQCA approach can highlight the combined effect of multiple factors and the effectiveness mechanism driving regional green regional finance. Second, fsQCA is based on the principle of equivalence (Cheng et al., 2019), which summarizes various combinations of conditions that may lead to the same outcome (Xie et al., 2016). The fsQCA method has the advantage of considering multiple condition configurations leading to a specific outcome (Cheng et al., 2022), and it can focus on the diversity of causal relationships (Ren et al., 2016). Although the history of green regional finance varies across Chinese provinces and regions, the impacts of changes in the development of various factors on their ultimate performance may be somewhat consistent (Chuah et al., 2021). fsQCA can be applied to explore which condition configurations can lead to the improvement of regional green finance from a holistic perspective and to uncover the group causes of the relative lag of green regional finance in individual Chinese provinces. The fsQCA method can be applied to explore which condition configurations can be inferred to cause the improvement of regional green finance, as well as the condition configurations that cause the relative lag of green regional finance in individual provinces in China.

Therefore, in order to better elaborate the green regional finance configurations of Chinese provinces and regions and understand the utility mechanisms driving local green regional finance, this paper conducted an exploratory study using fsQCA.

3.2 Variable selection and measurement

Result variable: In the variable design process, we tried to ensure that the variables were as objective as possible and that the measures were well documented (Du and Kim, 2021). Therefore, we used the data from the green finance index for each region in the China Local Green Finance Development Report (2021) published by the International Institute of Green Finance of the Central University of Finance and Economics to measure the outcome variable. This report provides data tracking and an annual evaluation of 31 Chinese provinces in terms of green finance policy system construction, market product and service innovation, and regional exchange and cooperation. The report also analyzes the correlation between local green finance and local government financial capacity, macroeconomic development, financial system development, social and environmental conditions, and ecological environment quality. Its data meet authority, credibility, and objectivity (Cheng et al., 2022).

Conditional variables: Consideration of the indicators for the antecedent variables mainly followed the principle of diversification to ensure the reliability of the variables (Zhang and Long, 2022). Based on the literature and the specific conditions of each province and region, the conditional variables affecting the effectiveness of green finance in each province and region were set as five indicators: regional logistics, carbon emission index, regional finance, economic level, and environmental regulation. The data were processed using nine indicators with standardization and the principal component analysis method as a measure of the regional logistics variable, including the regional logistics value added, regional population, regional GDP index, regional total employment, regional logistics employment, per capita cargo turnover, regional total retail sales of consumer goods, regional total investment in fixed assets in logistics, and regional total freight volume. The carbon emission index was applied to calculate the carbon dioxide emissions from energy consumption in each province as a measure of the carbon emission index variables. The regional financial data from the Report on Local Green Financial Development in China (2021) published by the International Institute of Green Finance of the Central University of Finance and Economics were used as a measure of the criteria of the regional financial variable. For the economic level variable, the economic level output value of each province was used as a measure. Using industrial SO2, industrial wastewater, and industrial soot emissions per unit of output value, a composite index was calculated for measuring the environmental regulation variable.

3.3 Data source

In order to explore the principle and inner mechanism of the green regional financial configurations among the regions, this paper considered 34 provincial-level administrative regions in China as the research objects. Because of the wide scope of data collection, there were gaps and deficiencies in the data of some provinces. In order to ensure the relative completeness and relevance of the final empirical findings (Zhong Weishun et al., 2022), 30 provinces (except Tibet, Hong Kong, Macao, and Taiwan) were finally selected as the research sample. In total, we spent more than 3 months collecting and processing data, and these raw data were obtained from the China Local Green Finance Development Report (2021), China Statistical Yearbook (2022), China Urban Statistical Yearbook (2022), China Energy Statistical Yearbook (2022), and the statistical yearbooks of each province in 2022.

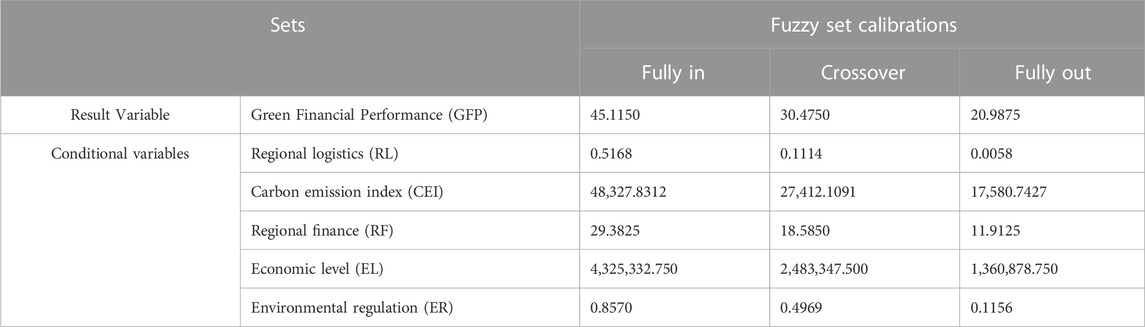

3.4 Data calibration

Before using fsQCA to analyze the data, all variables were calibrated (Mei et al., 2022). The calibration was set at three anchor points according to the theoretical knowledge and combined with the actual situation: fully in, crossover, and fully out, and the calibrated variables were between 0 and 1 (Du and Kim, 2021). In this paper, the upper quartile (75% quartile value), the middle value (50% quartile value), and the lower quartile (25% quartile value) of the outcome variables and the five conditional variables for measuring the high performance of green finance in each province and region of China were selected as the three anchor points (Chuah et al., 2021). The three anchor points for measuring the absence of green finance high performance in each province and region of China were set as the opposite of the above (Chu et al., 2019). The three anchor points for each calibration standard are shown in Table 2.

TABLE 2. Variable calibration.

4 Results

We performed two types of analysis using fsQCA (Xie et al., 2016). The first was necessary conditions analysis (Cheng et al., 2022), which detects whether the presence of a variable will directly lead to the generation of the result variable (Ren et al., 2016). The second type of analysis was sufficiency analysis for configuration conditions (Chen et al., 2021), which finds the configuration conditions that lead to the generation of the result variable (Zhong Shen et al., 2022), where the different conditions are analyzed to understand the causal relationship between the conditional variables and the result variable (Chu et al., 2019).

4.1 Necessary conditions analysis

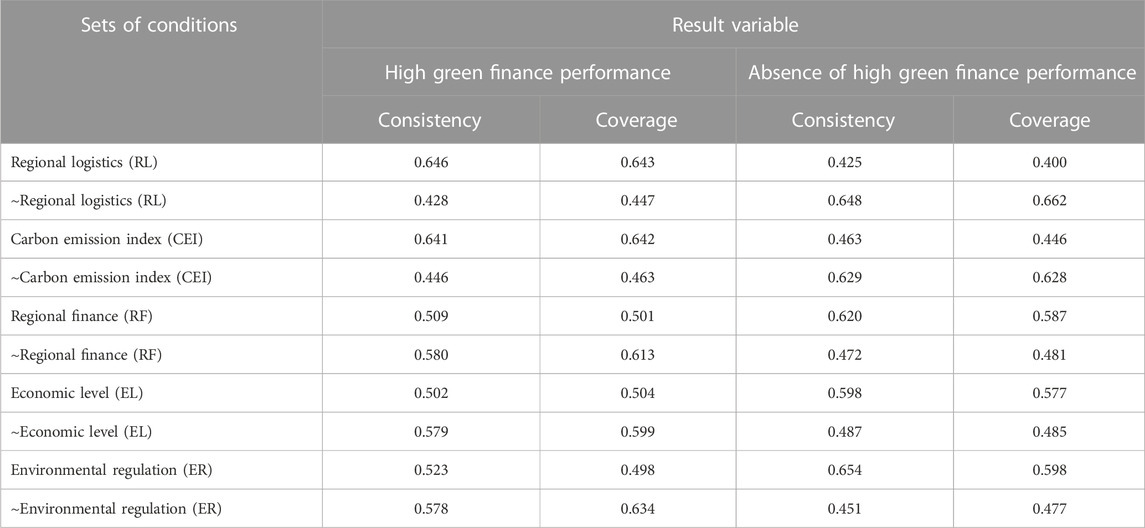

In this paper, FsQCA 3.0 software was used to test the consistency and coverage of variables to measure the sufficiency and necessity of the relationship between variables (the symbol “∼” indicates the absence of the given variable). Consistency refers to the extent to which all samples included in the analysis conform to a given condition or combination of conditions that affect the occurrence of the result variable (Mei et al., 2022). Coverage refers to the extent to which a given condition or combination of conditions has explanatory power over the result variable (Zhang and Long, 2022). For single condition variable necessity analysis, if the necessary consistency of a conditional variable is greater than 0.9, the factor is necessary and the resulting necessary condition will be excluded in the subsequent sufficient condition analysis, and if it is less than 0.9, it cannot be considered necessary (Cheng et al., 2022). For the single condition variable sufficiency analysis, a factor is sufficient if the sufficient consistency of a conditional variable is greater than 0.8, indicating that this single factor constitutes a configuration to explain the results (Ren et al., 2016). As shown in Table 3, the results of the necessary condition test indicated that the necessary consistency of all conditional variables was below 0.9, indicating that the single conditional variable lacked sufficient explanatory power for the result variable and that no single variable was necessary to influence the result variable. The results of the sufficient condition test indicated that the sufficient consistency of all the single conditional variables was also less than 0.8, which was also insufficient to constitute a sufficient condition to influence the result variable, indicating that no single conditional variable constituted a configuration to explain the result variable.

TABLE 3. Analysis of necessary conditions for green finance performance in fsQCA.

4.2 Sufficiency analysis for configuration conditions

After analyzing the data, the fsQCA 3.0 software presented three different solutions: complex, intermediate, and parsimonious (Wang Yunbo et al., 2022). The complex solution does not contain logical residuals (Liang et al., 2022), the intermediate solution contains only logical residuals that match the theoretical basis and the actual situation (Diao and Liu, 2021), and the simple solution contains all logical residuals but does not evaluate their reasonableness (Mei et al., 2022). Compared with the other two solutions, the intermediate solution was less complex, reasonable, and did not eliminate the necessary conditions, so the intermediate solution was chosen for the subsequent study (Chen et al., 2021). In addition, the intermediate solution determined the peripheral and core conditions that were useful for the outcome variable (Chu et al., 2019). If they do not exist in the simple solution but exist in the intermediate solution, they are peripheral conditions (Cheng et al., 2022). If they exist in both solutions, they are core conditions (Ren et al., 2016). The core condition has a greater effect on the outcome variable, and the peripheral condition plays a secondary role (Xie et al., 2016).

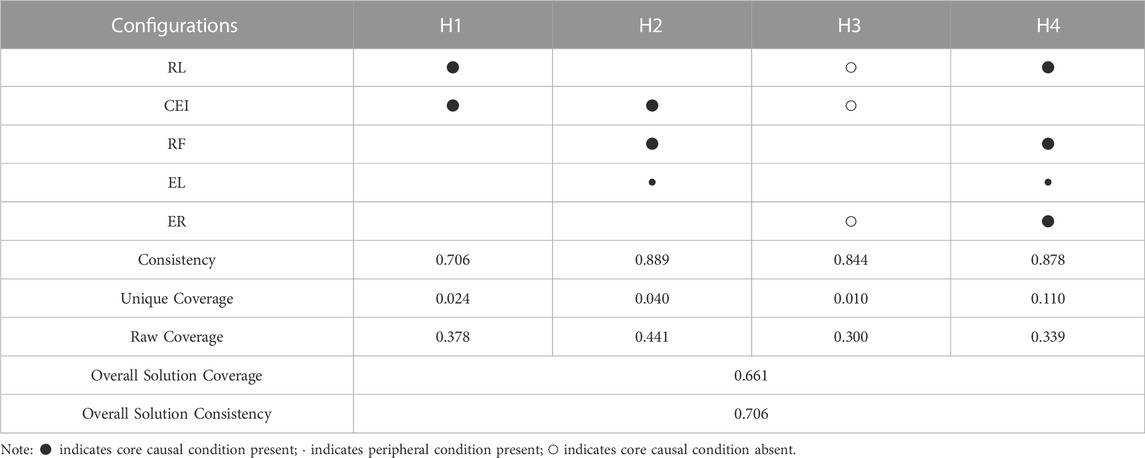

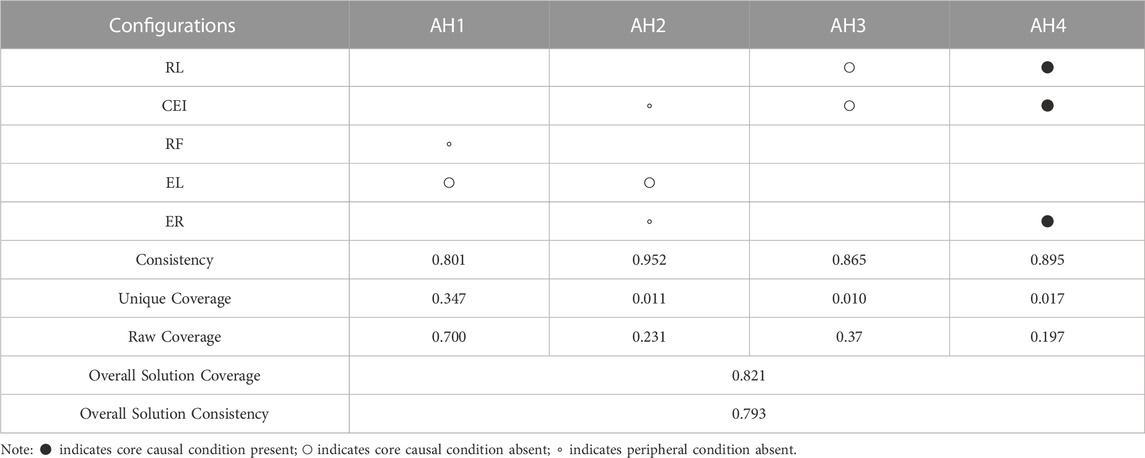

We adopted default thresholds to filter the data, with the case frequency benchmark set as 1 and the raw consistency benchmark as 0.8 (Du and Kim, 2021). This paper first assumed that the presence of all the conditional variables was likely to have a positive impact on green finance performance (Chu et al., 2019), which led to four configurations that produced high green finance performance (as shown in Table 4). The consistency of the results was 0.706, indicating that 70.6% of the provinces and regions that satisfied the four configurations had a high level of green finance performance. The coverage of the results was 0.661, indicating that the three types of configurations explained 66.1% of the provinces and regions with better green regional finance. Second, if the absence of the conditional variables had a negative impact on green finance performance (Mei et al., 2022), four types of configurations were derived to represent the absence of high green finance performance, and these four types of configurations explained 82.1% of the provinces and regions with a low performance of green regional finance (as shown in Table 5). For all cases that satisfied these four types of configurations, 79.3% of the provincial and regional cases showed low levels. In order to better compare the differences between the different configurations at various levels, we explored the four types of configurations that determined the emergence of high green finance performance and the four types of configurations that determined the absence of high green finance performance.

TABLE 4. Analysis of necessary conditions for high green finance performance in fsQCA.

TABLE 5. Analysis of necessary conditions for absence of high green finance performance in fsQCA.

4.2.1 Configurations for high green finance performance

4.2.1.1 H1 (RL-CEI)

This configuration is defined as the green regional financial dynamics whereby the region is expected to be enhanced when the two prerequisites of a high level of transportation and logistics construction and a high-quality ecological environment are both present. In this configuration, regional logistics (RL) and carbon emission index (CEI) are the core conditions, indicating that the importance of RL and CEI is much higher than other elements in this configuration. In addition, since only two core conditions are identified in this configuration, superior logistics and transportation conditions and a good ecological environment, as the “hard conditions” and “soft power” of regional development, are the key factors in the further development of green finance in these regions. The other factors play a relatively weak role. When RL conditions are more prominent, the provinces and regions belonging to this configuration have a significant advantage over other provinces and regions in terms of livelihood infrastructure. However, RL combined with lower CEI indicates that the relevant regions initially completed the transformation of industrialization or implemented the green energy-saving and emission reduction policies effectively. The provincial and regional representative of this configuration was Beijing Province. In the context of the national construction of a green financial system, Beijing, as the first city, has explored a new configuration of green regional finance in recent years. By combining the actual local development and introducing relevant draft practices, a policy framework focusing on building a global green financial center was initially formed. Specifically, on the one hand, it has actively gathered a few green financial institutions in the city’s sub-center zone to form a large-scale business platform, laying a realistic foundation for the city’s green regional finance strategy while expanding the market supply capacity. On the other hand, relying on the twin core advantages of being a national political center and a transportation pivot, Beijing is making efforts to strengthen international exchange and cooperation in green finance, providing a strong impetus to build a national carbon financial trading market.

4.2.1.2 H2 (CEI-RF-EL)

This construction allows that when the regional economy is developing well, focusing on consolidating financial development and promoting the transformation of the “three high” industries will help develop the green finance industry. In this construction, carbon emission index (CEI) and regional finance (RF) are the core conditions and economic level (EL) is the peripheral condition. This indicates that CEI and RF are more effective than EL for the green finance industry in this construction. This again confirms that a good economic foundation will provide support for the local green finance industry, but the strength of the local economy does not represent the development height of its green finance industry to some extent. The representative province of this construction was Hubei Province. In recent years, around its traditional industrial transformation and development needs, Hubei has formed a preliminary framework of green regional finance, embedding green elements in the process, such as many banks have jointly launched a number of green financial products, explored the pilot work of sewage rights mortgage, etc.

4.2.1.3 H3 (∼RL- ∼ CEI - ∼ ER)

This construction is peculiar compared to other constructions because it is composed of missing factors, i.e., it promotes the development and growth of the local green finance industry when the regional infrastructure is not yet complete, the modern industrial transformation is not yet completed, and the regional regulation is relatively broad. In this construction, regional logistics (RL), carbon emission index (CEI), and environmental regulation (ER) are all absent, indicating that the development of regions belonging to this construction is relatively lagging. However, the development of its green finance industry is in its prime, implying that factors not included in the measurement must be at play in influencing the green regional finance of the region. The representative province and region of this construction was Guizhou Province. Guizhou has a relatively disadvantaged level of economic development but superior ecological and environmental conditions. This is one reason why Guizhou was identified as one of the first national experimental zones for green financial reform and innovation, i.e., to explore new ways of development for economically disadvantaged regions and to open new horizons for green industrialization. Therefore, Guizhou has benefited more from the relevant supporting policies of the central government in promoting the development of green finance. In other words, the model of developing green finance in Guizhou reflects the criticality of policies from the central government level.

4.2.1.4 H4 (RL-RF-EL-ER)

The construction reflects an overall positive tendency. When a region with a high level of regional logistics, a good level of economic development, a certain financial industry foundation, and more stringent local government regulation of environmental aspects, the level of green finance is better. In this configuration, regional logistics (RL), regional finance (RF), economic level (EL), and environmental regulation (ER) all exist, reflecting that the provinces and regions belonging to this construction have a good development status in all aspects. When EL is classified as a peripheral variable and as an antecedent variable, it reflects the strong economic power of the provinces belonging to this construction from the side. Market capital transactions are active, and the corresponding environmental control initiatives are in line with the local economic development rhythm, thus playing a facilitating rather than a moderating role. In this construction, the corresponding environmental regulation policies and financial industries are more of a hotbed for the development of local green finance. The representative province of this construction was Guangdong Province. As China’s window to the outside world, Guangdong is regarded as a pilot zone for many early policies. In the financial sector, the development scale and standardization of financial trading platforms in Guangdong are more comprehensive and complete than those in other provinces and regions, and the basic platform for various markets such as banks and securities for horizontal linkage and vertical development has been basically established. Objectively, it provides the original ecological conditions for the development of green finance; that is, with the support of the local financial industry it will be more conducive to the issuance and trading of various green credit, bonds, and other products, and revitalize green financial assets. This is also a characteristic that distinguishes Guangdong from other provinces and regions with better economic strength. It is also a realistic reason why the variable of “economic development” is not a core variable in this construction, and the level of provincial and regional economic development is not a key pillar supporting the development of green finance in this type of city.

4.2.2 Configurations for absence of high green finance performance

4.2.2.1 AH1 (∼RF- ∼ EL)

This configuration reflects that poor economic development in the region and a relatively weak local financial sector will have a negative impact on the local green regional finance. In this configuration, both regional finance (RF) and economic level (EL) are indicated as absent, and the former is a peripheral variable while the latter is a key variable. It indicates that in this configuration the weakening of the local financial industry is only the surface, and the level of regional economic development is the key check on local green regional finance. The representative province of this configuration was Qinghai Province. As a large western province, Qinghai has the “double contradiction” dilemma of abundant energy resources and fragile ecological environment. From the perspective of economic development, Qinghai belongs to the third echelon, its own economic development is backward, and the surrounding transportation network is sparse, which makes it difficult to link the development of the region to the neighboring provinces and thus difficult to create systemic advantages and synergistic effects. In addition, compared with the provinces in the Yangtze River Delta region, the development of the financial industry in this area is relatively backward, which makes the development of the green financial industry inherently insufficient. In addition, considering the severe situation of ecological environmental protection in the region, grasping the balance between ecological protection and economic development and then strengthening the practical application of green finance will also become key issues for the province.

4.2.2.2 AH2 (∼CEI- ∼ EL- ∼ ER)

The configuration proposes that a high carbon emission index (CEI) in the region, a declining economic level (EL), and a lack of strong controls on the environmental revolution (ER) will have a negative impact on local green finance. The similarity between AH1 and AH2 is that the low level of economic strength is the key factor leading to poor local green regional finance. The difference is that the marginal factors of AH2 are ∼ CEI and ∼ER, i.e., a too high carbon emission index and lax environmental control. The representative province and region of this configuration was Liaoning Province. Liaoning’s green regional finance journey alongside the other two northeastern provinces reflects the transformation configuration of heavily industrial city clusters in northern China. From the perspective of policy instruments, Liaoning’s government signed a cooperation agreement with the European Union to establish China’s first green credit instrument, and its green finance industry had an early start. However, many factors, such as transformation difficulties and weak policy promotion in the later stage indicate that the green regional finance is still in its embryonic stage.

4.2.2.3 AH3 (∼RL- ∼ CEI)

The configuration states that when a province or region does not dominate the surrounding regional transportation pattern and its own carbon emission index is high, the capacity of green finance in that location to generate superior effectiveness will also be relatively insignificant. This configuration contains two conditional variables, namely, regional logistics (RL) and carbon emission index (CEI), and both are key variables. The representative province of this configuration was Henan Province. In the industrial distribution of Henan, secondary industry dominates, the share of green and environmental industries is very small, and the overall scale of green economy is small, with limited financing channels and lack of landing support, making it difficult to form a synergy to stimulate green regional finance.

4.2.2.4 AH4 (RL-CEI-ER)

This configuration behaves in the same paradoxical way as H3, which proposes that when the region is close to the transportation pivot, with low carbon emission levels and strong local government environmental controls, the momentum of local green regional finance slows down. The three variables belonging to this configuration are all core variables. The representative province of this configuration was Fujian Province. Among the provinces planning green development, Fujian was one of the early pathfinders. In 2014, Fujian was awarded the earliest ecological civilization demonstration zone in the country. However, in the later development process, its policies were not suitable for practical application, and there was a misalignment with local market development. In addition, the lack of financial institution participation and the high cost of green industry development have also become important problems that hurt local green regional finance.

4.3 Robustness checks

Robustness checks are an integral part of the analysis when using the fsQCA method (Mei et al., 2022). In this paper, we prioritized a specific approach in set theory for robustness checks (Du and Kim, 2021). First, using the varying consistency benchmark test, the raw consistency benchmark of 0.8 was reduced to 0.77, and the results indicated similarity to the previous condition configurations. Second, the frequency benchmark was adjusted by increasing the original benchmark from 1 to 2 (Ren et al., 2016), and the same results and consistent conclusions were still obtained. Therefore, it can be concluded that the findings of this paper were robust.

5 Discussion

By distinguishing the different types of condition configurations, it was apparent that the individualized characteristics among configurations were obvious, but from a systematic perspective, there was an overall lack of a common basis. According to the distribution of comparison configurations and conditional variables, the commonality of regional logistics factors was high, and they were mostly the key factors in various types of condition configurations, indicating that the level of regional logistics in each Chinese province played a macroscopic role in the enhancement of local green finance performance. However, it is also important to note that the core variable of regional logistics was not the only decisive factor in each condition configuration but needed to be combined with other variables to produce a corresponding high green finance performance. It can be concluded that this variable’s heterogeneity tendency was more prominent in the condition configurations that led to the absence of high green finance performance. In retrospect, the main reason for the diversification of green finance was the variability of the development process in different regions, which made it difficult to generalize the corresponding development model. In setting up the first batch of green financial reform and innovation pilot zones, the state also set up different development goals according to the heterogeneity of the logistics development level, industrial structure, and resource endowment of each region. For example, Guangdong Province has a high level of logistics development, a strong financial industry, and a more mature policy system, and it needs to focus on developing a modern green financial market. Guizhou Province, for example, is rich in natural resources and has little development effort, and it needs to develop a green financial industry based on its existing advantages and pursue sustainable green development.

Looking at the eight types of condition configurations affecting the performance of green finance and their representative provincial cases, we deduced that the government-led policy variable and driver played a key role in stimulating the development of green finance in each province. The reason is that among the eight configurations mentioned above, one conditional variable, the carbon emission index, played a significant role in promoting the result variable, but the carbon emission index variable was mainly driven by local government policies to reduce emission levels. For example, among the condition configurations leading to the high performance of green finance, H3 represents Guizhou Province and H4 represents Guangdong Province, which were included in the first batch of green finance reform and innovation pilot zones by the state as early as 2016 and became the first implementers and beneficiaries of relevant policies. In fact, considering both the positive externalities generated by green finance and its still nascent development status in China, adopting policy tools to accelerate the pace of green finance development is currently one of the more effective approaches. Under the policy influence, the government departments in these provinces and regions guided the transitioning enterprises and regulated the enterprises with high pollution, high energy, and high water consumption, which helped the enterprises to move toward green development. This also maximized their economic benefits, thus achieving the high-quality development of the local society and economy, which was also in line with the hypothesis of the economic man. However, through the condition configuration leading to the absence of high green finance performance, the limitations of government policy instruments in promoting local green regional finance can also be glimpsed. The relevant shortcomings were more evident in the development history of Liaoning Province, a province and region represented by AHb2, and Fujian Province, a province and region represented by AH4. In both cases, the regions acted early in the development of green finance and achieved corresponding results in the early stage, but in the middle and late stages of development, they both showed weaknesses. On the one hand, this proved that policy instruments can play a more significant incentive role in the initial stage of regional green regional finance and achieve effective management. On the other hand, because of the uneven development among Chinese regions and the uneven levels of the overall economy, culture, science, and technology, there are gaps in the development capacity of each region, making it difficult for green finance to ensure growth-oriented and sustainable development. In other words, it is difficult for green policy instruments to fully solve the problems of regional green finance.

5.1 Theoretical implications

By comparing the combined relationship between different configurations, a substitution relationship between conditional variables can be derived to help provinces and regions improve the performance of green finance find a more suitable solution for themselves.

By comparing the four condition configurations that produce high green finance performance, three substitution relationships were found. First, comparing H1 with H2, we found that regional logistics (RL) can be substituted with regional finance (RF) and economic level (EL). This means that if regions with better control of carbon emissions, regardless of whether the environment is well-regulated or not, meet the conditions of superior logistics and transportation, or they meet the combination of “high financial development + high economic level,” they can generate a high performance of green finance. This had similarities and differences with the findings of a previous study (Jinru et al., 2022). The similarity was that RL did have an impact on green finance in each province and region. The difference was that, in the previous study, the RL factor influenced the green finance of each province and region only through its influence on environmental quality, but we found that RL can directly influence the green finance performance of provinces and regions as a core condition. Second, comparing H1 with H4 and H2 with H4, we found that the carbon emission index (CEI) could be replaced with RF, EL, and environmental regulation (ER), or with RL and ER. It suggested that if the region has excellent logistics and transportation capacity, it can show a high performance of green finance if the carbon emission is well controlled or the combination of “high financial development + high economic level + good environmental regulation” is satisfied. It also indicated that if the region has high financial development and a high economic level, it can maintain high green finance performance by controlling the carbon emission index or meeting the combination of “high logistics and transportation capacity + good environmental regulation.”

A further comparison of the four condition configurations that produced an absence of high green finance performance revealed a substitution relationship. Comparing AH2 with AH3, we found that an RL absence can be substituted with an EL absence and an ER absence. In other words, if a region has a high index of its own carbon emissions, the surrounding regional transportation pattern does not dominate or is at a low level of economic development, and the government lacks strong controls on environmental management, it will have a negative impact on the local green finance.

5.2 Policy implications

Three policy implications for policymakers and policy implementers in the provinces are set out below.

First, China’s provinces and regions must quickly refine the consensus reached in the development of green finance in each region, learn from the valuable experience of local governments in developing green finance, and build a green regional financial system with local characteristics. They must focus on the cities that have made achievements in the field of green finance, guide financial institutions to invest more in green finance, provide better green financial services, focus on creating generic demonstration projects, and enhance the guiding role of advanced demonstration cities. It is also necessary for universities and research institutes to increase support on cultivating excellent financial talents to provide professional vitality for the long-term development of the green financial system in each province.

Second, China’s provinces and regions need to rely on a solid industrial base and actively develop local logistics linkages to strengthen urban infrastructure and transportation. At the same time, governments in each province should also increase local resource environmental protection efforts, promote the development of green branding strategies actively, highlight the green development orientation, realize the optimal allocation of resources, prioritize the increase of green financial resource allocation to environmental protection industries, and standardize the policy and financial support to enterprises. This conclusion is roughly the same as the improved countermeasures proposed in previous studies (Wang Hui et al., 2021; Zhou et al., 2022), all aimed at providing a breeding ground for the development of urban green finance.

Third, based on policy orientation, Chinese provinces and regions should integrate green finance as a measurement indicator into the performance assessment system of local governments to stimulate them to be more proactive as a driving force to promote green finance development because a single policy utility is not enough to promote green finance development. We suggest that local governments introduce more detailed policy guidelines based on the country strategy to further stimulate market dynamics. For instance, a green information-sharing platform should be created to enhance provincial interconnections and find emerging development momentum in the society.

6 Conclusion

In this paper, based on CiteSpace and the fsQCA method, a qualitative comparative analysis of fuzzy sets was conducted for 30 provincial and district cases in China. We found four types of condition configurations that determined the emergence of high green finance performance and four types that determined the absence of high green finance performance. Among them, regional logistics factors play a greater role in the regional green finance process in the provinces and regions. This confirms the view of Wei et al. (2022), who also argues that a high level of regional logistics can reduce financial risks. However, the regional green finance model is still in the embryonic stage due to the influence of objective factors such as local characteristic endowment. It points out (Zhou et al., 2020) that the level of green finance varies across regions in China, and this study finds that provinces show diversified development in the process of growth, which is attributed to the lack of a mature theoretical framework system as a standardized paradigm to be promoted at the macro level. In addition, the government policy-driven carbon emission indicator factor plays a key role in stimulating the development of green finance in the provinces and regions, yet it cannot guarantee sustainable growth and plays little role in regulating the development of regional green finance in the later stage. This supports the findings of Bin et al. (2022) and broadens his findings.

This study has three research contributions. First, co-occurring network analysis is conducted through CiteSpace to identify the latest research trends and categorize the different literature. Second, a scientific and reasonable research framework of green financial performance is constructed, which lays a theoretical foundation for subsequent empirical research. Third, this study introduces the fsQCA to explore the configurations to improve green financial performance from the allocation point of view, identify the causal factors of the differences in green financial performance, and enrich the existing literature, which definitely enriches the research methodology instrumental tools in this field.

Despite our best efforts, there are some limitations in this paper. In the data collection stage, because of the narrow scope of data collection and some data gaps, Tibet, Hong Kong, Macao, and Taiwan were not included in the analysis process, and the empirical results were not comprehensive enough to describe the actual green finance development scenario in China, more effective data should be obtained for exploratory research in later studies. In addition, this study collected and analyzed samples from Chinese provinces only, thus limit the generalization of the findings to other countries or regions, and it is necessary to conduct similar studies to compare the results of this study with those of other countries to further discuss the similarities and heterogeneity in the future.

Data availability statement

The datasets presented in this study can be found in online repositories. The names of the repository/repositories and accession number(s) can be found below: the China Local Green Finance Development Report (2021), China Statistical Yearbook (2022), China Urban Statistical Yearbook (2022), China Energy Statistical Yearbook (2022), and the statistical yearbooks of each province in 2022.

Author contributions

Conceptualization, ML and ZL; methodology, ML and LW; software, ML; validation, ML, ZL and QH; formal analysis, ML; resources, ZL and LW; data curation, ML; writing—original draft preparation, ML and LW; writing—review and editing, ML, ZL, and QH; visualization, ML; supervision, ZL and QH; project administration, ZL and LW; funding acquisition, ZL and QH. All authors contributed to the article and approved the submitted version.

Funding

This research was supported by the grant from China Scholarship Council. It was funded by the National Social Science Foundation of China, grant number 22BGL049; Project of Humanity and Social Science Foundation of the Ministry of Education in China, grant number 20YJC630137; the Key Project of Hunan Provincial Education Department, grant number 22A0403; the Hunan Provincial Philosophy and Social Science Foundation Project, grant number 18JD25.

Conflict of interest

Authors ML was employed by Zhejiang CRRC Shangchi Electric Co., Ltd.

The remaining authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Afshan, S., Yaqoob, T., Meo, M. S., and Hamid, B. (2023). Can green finance, green technologies, and environmental policy stringency leverage sustainability in China: evidence from quantile-ardl estimation. Environ. Sci. Pollut. Res. Int. 30, 61726–61740. 22. doi:10.1007/s11356-023-26346-1

Bakry, W., Mallik, G., Nghiem, X. H., Sinha, A., and Vo, X. V. (2023). Is green finance really ‘green’? Examining the long-run relationship between green finance, renewable energy and environmental performance in developing countries. Renew. energy 208, 341–355. doi:10.1016/j.renene.2023.03.020

Chen, Wen, Song, Xiao-Jiao, and Li, Yanping (2021). Factors affecting the sustainable development of hrs in transforming economies: A fsQCA approach. Sustain. (Basel, Switz. 13, 1727–1819. 4. doi:10.3390/su13041727

Cheng, C., Cao, L., Zhong, H., He, Y., and Qian, J. (2019). The influence of leader encouragement of creativity on innovation speed: findings from sem and fsqca. Sustain. (Basel, Switz. 11, 2693. 9. doi:10.3390/su11092693

Cheng, C., Yang, Z., He, Y., and Yan, L. (2022). How configuration theory explains performance growth and decline after Chinese firms cross-border M&A: using the fsqca approach. Asia Pac. Bus. Rev. 28, 555–578. 4. doi:10.1080/13602381.2021.1910900

Chu, Y., Chi, M., Wang, W., and Luo, B. (2019). The impact of information technology capabilities of manufacturing enterprises on innovation performance: evidences from sem and fsqca. Sustain. (Basel, Switz. 11, 5946. 21. doi:10.3390/su11215946

Chuah, Stephanie, Hui-Wen, , Wu, K. J., and Cheng, C. F. (2021). Factors influencing the adoption of sharing economy in B2B context in China: findings from pls-sem and fsqca. Resour. conservation Recycl. 175, 105892. doi:10.1016/j.resconrec.2021.105892

Diao, Qibo, and Liu, Yuanchun (2021). Fuzzy set qualitative comparative analysis (fsQCA) applied to the driving mechanism of total factor productivity growth. J. Math. (Hidawi) 2021, 1–8. doi:10.1155/2021/8182454

Diaz-Rainey, I., Corfee-Morlot, J., Volz, U., and Caldecott, B. (2023). Green finance in asia: challenges, policies and avenues for research. Clim. policy 23, 1–10. 1. doi:10.1080/14693062.2023.2168359

Ding, Xue, and Yang, Zhong (2022). Knowledge mapping of platform research: A visual analysis using VOSviewer and CiteSpace. Electron. Commer. Res. 22, 787–809. 3. doi:10.1007/s10660-020-09410-7

Du, Yunzhou, and Kim, Phillip H. (2021). One size does not fit all: strategy configurations, complex environments, and new venture performance in emerging economies. J. Bus. Res. 124, 272–285. doi:10.1016/j.jbusres.2020.11.059

Ip, Y., Iqbal, W., Du, L., and Akhtar, N. (2023). Assessing the impact of green finance and urbanization on the tourism industry—An empirical study in China. Environ. Sci. Pollut. Res. Int. 30, 3576–3592. 2. doi:10.1007/s11356-022-22207-5

Jia, Guo-Ling, Ma, Rong-Guo, and Hu, Zhi-Hua (2019). Review of urban transportation network design problems based on CiteSpace. Math. problems Eng. 2019, 1–22. doi:10.1155/2019/5735702

Jia, Weichen, Peng, Jun, and Cai, Na (2020). An approach to improving the analysis of literature data in Chinese through an improved use of citespace. Knowl. Manag. e-learning 12, 256–267. 2. doi:10.34105/j.kmel.2020.12.013

Jinru, L., Changbiao, Z., Ahmad, B., Irfan, M., and Nazir, R. (2022). How do green financing and green logistics affect the circular economy in the pandemic situation: key mediating role of sustainable production. Ekon. istraživanja 35, 3836–3856. 1. doi:10.1080/1331677x.2021.2004437

Larsen, (2023). Adding ‘origination’ to diffusion theory: contrasting the roles of china and the eu in green finance. RIPE 30 4, 1203–1219. doi:10.1080/09692290.2023.2204532

Lee, Chi-Chuan, and Lee, Chien-Chiang (2022). How does green finance affect green total factor productivity? Evidence from China. Energy Econ. 107, 105863. doi:10.1016/j.eneco.2022.105863

Li, G., Jia, X., Khan, A. A., Khan, S. U., Ali, M. A. S., and Luo, J. (2023). Does green finance promote agricultural green total factor productivity? Considering green credit, green investment, green securities, and carbon finance in China. Environ. Sci. Pollut. Res. Int. 30, 36663–36679. 13. doi:10.1007/s11356-022-24857-x

Li, Wenqi, Fan, Jingjing, and Zhao, Jiawei (2022). Has green finance facilitated China’s low-carbon economic transition? Environ. Sci. Pollut. Res. Int. 29, 57502–57515. 38. doi:10.1007/s11356-022-19891-8

Li, Zong-Wei, and Wang, Ming-Yan (2016). “Hot topics and fronts of E-commerce teaching research: A scientometric analysis in CiteSpace,” in PROCEEDINGS OF THE 2015 CONFERENCE ON EDUCATION AND TEACHING IN COLLEGES AND UNIVERSITIES, Sanya, Hainan, December 26-27, 2015 (PARIS: Atlantis Press), 160–162. 25.

Liang, Chen, Wang, S. J., Foley, M., and Ma, G. H. (2022). The path selection on improving the quality of environmental information disclosure - configuration analysis based on fsQCA. Appl. Econ. ahead-of-print.ahead-of-print 55, 2207–2222. doi:10.1080/00036846.2022.2102134

Mao, Qian (2021). Effect of green finance on regional economic development: evidence from china. TRANSFORMATIONS Bus. Econ. 20 (3C), 505–525.

Mei, S., Lv, J., Ren, H., Guo, X., Meng, C., Fei, J., et al. (2022). Lifestyle behaviors and depressive symptoms in Chinese adolescents using regression and fsQCA models. Front. public health 10, 825176. doi:10.3389/fpubh.2022.825176

Qian, Yu, Liu, Jun, and Forrest, Jeffrey Yi-Lin (2022). Impact of financial agglomeration on regional green economic growth: evidence from china. J. Environ. Plan. Manag. 65, 1611–1636. 9. doi:10.1080/09640568.2021.1941811

Ran, Chenyang, and Zhang, Yuru (2023). Does green finance stimulate green innovation of heavy-polluting enterprises? Evidence from green finance pilot zones in China. Environ. Sci. Pollut. Res. Int. 30, 60678–60693. 21. doi:10.1007/s11356-023-26758-z

Ren, S., Tsai, H.-T., Eisingerich, , and Andreas, B. (2016). “Case-Based asymmetric modeling of firms with high versus low outcomes in implementing changes in direction”. J. Bus. Res. 69, 500–507. 2. doi:10.1016/j.jbusres.2015.05.007

Taridala, Sitti Aida Adha, Alzarliani, W. O., Fauziyah, E., Rianse, I. S., and Arimbawa, P. (2023). Green finance, innovation, agriculture finance and sustainable economic development: the case of indonesia’s provincial carbon emissions. Int. J. energy Econ. policy 13, 271–280. 1. doi:10.32479/ijeep.13959

Wang, H., Jiang, L., Duan, H., Wang, Y., Jiang, Y., and Lin, X. (2021a). The impact of green finance development on China’s energy structure optimization. Discrete Dyn. Nat. Soc. 2021, 1–12. doi:10.1155/2021/2633021

Wang, Jianda, and Ma, Ying (2022). How does green finance affect CO2 emissions? Heterogeneous and mediation effects analysis. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.931086

Wang, Quan-Jing, Wang, Hai-Jie, and Chang, Chun-Ping (2022a). Environmental performance, green finance and green innovation: what’s the long-run relationships among variables? Energy Econ. 110, 106004. doi:10.1016/j.eneco.2022.106004

Wang, Y., Zhao, N., Lei, X., and Long, R. (2021b). Green finance innovation and regional green development. Sustain. (Basel, Switz. 13, 8230. 15. doi:10.3390/su13158230

Wang, Yunbo, Duan, Xiuping, and Chen, Ziyi (2022b). Pathways to the sustainable development of quality education for international students in China: an fsqca approach. Sustain. (Basel, Switz. 14, 15254. 22. doi:10.3390/su142215254

Xie, Hualin, Ouyang, Zhenyi, and Choi, Yongrok (2020). Characteristics and influencing factors of green finance development in the Yangtze River Delta of China: analysis based on the spatial durbin model. Sustain. (Basel, Switz. 12, 9753. 22. doi:10.3390/su12229753

Xie, Xuemei, Fang, Liangxiu, and Zeng, Saixing (2016). Collaborative innovation network and knowledge transfer performance: A fsQCA approach. J. Bus. Res. 69, 5210–5215. doi:10.1016/j.jbusres.2016.04.114

Xu, Aiting, Zhu, Yuhan, and Wang, Wenpu (2023). Micro green technology innovation effects of green finance pilot policy—from the perspectives of action points and green value. J. Bus. Res. 159, 113724. doi:10.1016/j.jbusres.2023.113724

Yu, C.-H., Wu, X., Zhang, D., Chen, S., and Zhao, J. (2021). Demand for green finance: resolving financing constraints on green innovation in china. Energy policy 153, 112255. doi:10.1016/j.enpol.2021.112255

Yu, M., Zhou, Q., Cheok, M. Y., Kubiczek, J., and Iqbal, N. (2022). Does green finance improve energy efficiency? New evidence from developing and developed economies. Econ. change Restruct. 55, 485–509. 1. doi:10.1007/s10644-021-09355-3

Zhang, D., Mohsin, M., Rasheed, A. K., Chang, Y., and Taghizadeh-Hesary, F. (2021a). Public spending and green economic growth in BRI region: mediating role of green finance. Energy policy 153, 112256. doi:10.1016/j.enpol.2021.112256

Zhang, H., Wang, Y., Li, R., Si, H., and Liu, W. (2023). Can green finance promote urban green development? Evidence from green finance reform and innovation pilot zone in China. Environ. Sci. Pollut. Res. Int. 30, 12041–12058. 5. doi:10.1007/s11356-022-22886-0

Zhang, Hui, and Long, Shujing (2022). How business environment shapes urban tourism industry development? Configuration effects based on NCA and fsQCA. Front. Psychol. 13, 947794. doi:10.3389/fpsyg.2022.947794

Zhang, S., Wu, Z., Wang, Y., and Hao, Y. (2021b). Fostering green development with green finance: an empirical study on the environmental effect of green credit policy in china. J. Environ. Manag. 296, 113159. doi:10.1016/j.jenvman.2021.113159

Zhang, Ying, and He, Ming (2022). Visualization analysis of NoSQL research field based on SCI by CiteSpace V. Int. J. Adv. Netw. Monit. controls 2, 129–134. 3. doi:10.21307/ijanmc-2017-039

Zhang, Y., Fang, X., Yang, Z., Sun, Y., and Wang, Q. (2023). Emotional experiences of service robots' anthropomorphic appearance: A multimodal measurement method. Emerg. Mark. finance trade ahead-of-print.ahead-of-print, 1–19. doi:10.1080/00140139.2023.2182751

Zhong, S., Hou, J., Li, J., and Gao, W. (2022b). Exploring the relationship of ESG score and firm value using fsQCA method: cases of the chinese manufacturing enterprises. Front. Psychol. 13, 1019469. doi:10.3389/fpsyg.2022.1019469

Zhong, Weishun, Zong, Like, Yin, Weihua, Syed Ahtsham Ali, , Mouneer, Salma, and Haider, Jahanzaib (2022a). Assessing the nexus between green economic recovery, green finance, and CO2 emission: role of supply chain performance and economic growth. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.914419

Zhou, Hongji, and Xu, Guoyin (2022). Research on the impact of green finance on China’s regional ecological development based on system GMM model. Resour. policy 75, 102454. doi:10.1016/j.resourpol.2021.102454