Qian Feng1

Qian Feng1 Wang Jinghua

Wang Jinghua

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Energy Res. , 03 April 2023

Sec. Smart Grids

Volume 11 - 2023 | https://doi.org/10.3389/fenrg.2023.1170138

This article is part of the Research Topic Advances in Artificial Intelligence Application in Data Analysis and Control of Smart Grid View all 20 articles

Multi-interval settlement is conducive to meeting the needs of growing renewable energy resources with great intermittency and volatility and managing the effective operation in the electricity spot market. However, the insufficient incentive of market price inaccurately reflecting the total cost of the electricity spot market caused by the inaccuracy of generation and load prediction in the current multi-interval settlement will lead to inefficient market scheduling, causing the market participants to deviate from dispatch instructions. Based on the problem above, a new multi-interval settlement system of rolling-horizon scheduling including the period selection of look-ahead schedules and enhanced settlement mechanism is proposed to improve the price incentive for the electricity spot market. The proposed multi-interval settlement system can produce a better look-ahead period and a more economically efficient dispatch solution inducing dispatch-following incentives. A numerical example shows that the proposed multi-interval settlement system outperforms the traditional settlement mechanism regarding economic efficiency.

According to the plan vision of carbon peak and carbon neutrality, Chinese renewable energy will enter a new stage of high-quality leapfrog development, and a high proportion of renewable energy grid connection will become the basic new feature of the power system in the future. In order to adapt to the development of renewable energy, the demand for power system flexibility has increased significantly, the role of cross-time constraints of spot market optimization has been significantly strengthened, and the coupling between optimization periods has become closer. How to design a real-time prospective and optimized settlement mechanism with universal practicality for the spot market of electricity to meet the construction and development needs of the electricity market adapting to the characteristics of the new power system is a practical problem that needs to be solved urgently in the construction of Chinese electricity market. On the basis of the current operation mechanism, this paper improves and designs a set of new real-time prospective optimization settlement mechanism for the spot market of electricity, which can provide reference for the construction of the spot market of electricity in China.

According to the plan vision of “30 carbon peak, 60 carbon neutral,” Chinese renewable energy will enter a new stage of high-quality leapfrog development, and a high proportion of renewable energy grid connection will become the basic new feature of the power system in the future (Jiang et al., 2020; Chen et al., 2021). In order to adapt to the development of renewable energy, the demand for flexibility of the power system has increased significantly, and the role of cross-time constraints in the optimization of the spot market has been significantly strengthened, and the coupling between the optimization periods has become closer (CAISO, 2014; Massachusetts gov, 2016). Therefore, in order to better adapt to the characteristics of flexible resources operating across time periods, the mature spot power markets at home and abroad have adopted the look-ahead optimization method (CAISO, 2019; NYISO, 2020).

Compared with single-period optimization, look-ahead optimization can more effectively improve the success rate of solving the mathematical model by expanding the time range, reduce inefficient scheduling by pre-regulating resources (Xie and Ilic, 2009), avoid peak electricity prices due to insufficient power supply capacity, and give the clearing price cross-period economic significance (Ela and O’Malley, 2016).

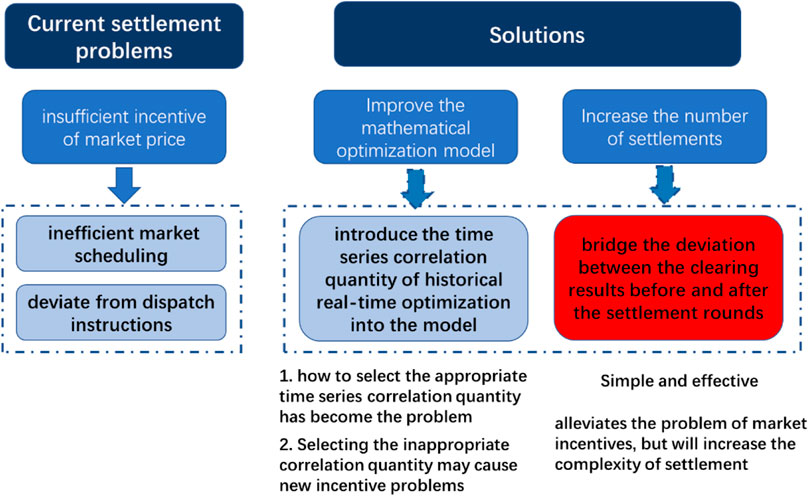

However, there is still a problem of insufficient price incentives in forward-looking optimization. In typical practice, look-ahead optimization is based on short-term load forecasting to optimize the scheduling of resources in future multi-periods, but only the optimization results of the current period are settled (single settlement mechanism) (Bakirtzis et al., 2014; CAISO, 2019; NYISO, 2020). When the current outlook optimization is applied to the real-time market rolling clearing scenario, the supporting single settlement mechanism will regard the historical clearing results as “sunk costs,” directly ignoring the components that affect the current or future optimization results, and implicitly “burying” the economic value of cross-time constraints. Even if the day-ahead market has made a perfect load forecast, the forward order settlement mechanism will still lead to the lack of market price incentives, and the power generation companies cannot recover costs through the market price, but choose to deviate from the dispatching order (Wilson, 2002). Literature (Peng et al., 2013) pointed out the motivation of market members to deviate from scheduling in look-ahead optimization, but only gave qualitative solutions.

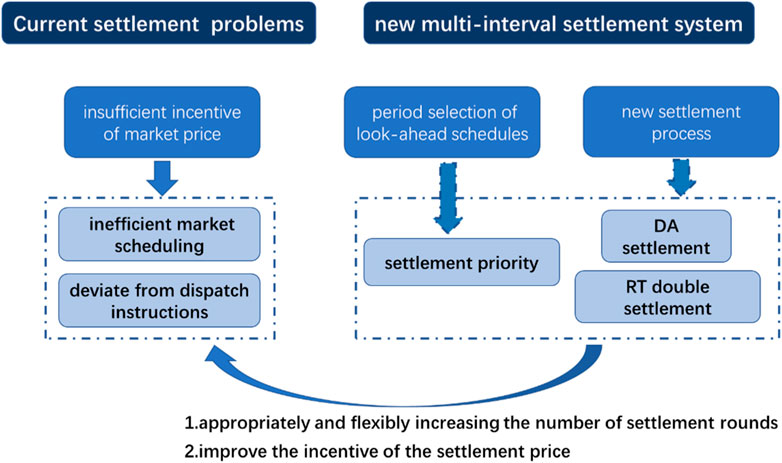

The academic solutions can be divided into two categories: one is to improve the mathematical optimization model, and introduce the time series correlation quantity of historical real-time optimization into the model (Schiro, 2017; Zhou et al., 2017). However, how to select the appropriate time series correlation quantity has become the problem faced by this method. Selecting the inappropriate correlation quantity may cause new incentive problems. There is no definite result of this research idea at present. The second is to increase the number of settlement rounds, bridge the gap between the clearing results before and after the settlement rounds, eliminate the motivation of market users to speculate, reduce compensation costs, and improve the incentive of market participants to follow the schedule. This article adopts the second train of thought. Based on this idea, the literature (Yao et al., 2020) proposed a real-time multi-settlement mechanism based on look-ahead optimization. The prices of all periods in the optimization cycle need to be settled. This settlement method alleviates the problem of market incentives, but will increase the complexity of settlement. Therefore, it is necessary to redesign the look-ahead and optimized settlement mechanism to alleviate the problem of insufficient settlement price. The overviews of the literature survey can be seen in Figure 1.

FIGURE 1. Overview of the survey.

The fairness and rationality of the electricity spot market settlement mechanism plays an important role in the sound operation of the entire power system and the optimal allocation of power market resources (Huang et al., 2019). Due to the particularity of electricity commodities, electricity trading needs to establish a centralized electricity spot market, and support the corresponding deviation electricity settlement mechanism. At present, most mature electricity spot markets adopt a double settlement mechanism.

On the basis of the current double settlement mechanism in the spot electricity market, this paper focuses on the analysis of the factors that affect the prospective optimization incentive, and selects a quantifiable priority standard for this purpose, and innovatively designs a new real-time prospective optimization settlement mechanism in the spot electricity market. This mechanism can effectively improve the incentive of the settlement price, and will not cause excessive settlement burden, It can better meet the demand of real-time prospective optimization of power in the new era.

Unlike ordinary commodities, electric power commodities have obvious particularity: 1) Physical electric power commodities are almost conducted at the same time in the four links of power generation, transmission, distribution and utilization. The electricity market transactions need to be consistent with the actual operation of the power system as much as possible, and the execution of the electricity trading contract needs to simulate the real-time balance scenario of the power generation and consumption of the power system as much as possible; 2) With the access of centralized and distributed renewable energy to the grid, there will inevitably be prediction errors on both sides of the power system’s power generation and consumption, which will cause the actual power generation and consumption curve to deviate from the market transaction curve, which is inconsistent with the real-time balance of the power system, and the market subject is required to bear the costs of real-time power balance according to the transaction agreement; 3) There is a strong homogeneity of power commodities, and the power commodities delivered by each market transaction cannot be measured separately. It is necessary to formulate unified measurement and settlement rules to deal with the deviation between the actual electricity generated and the electricity traded in the market, so as to realize the decoupling of the power transaction contract and the actual electricity consumption at the level of settlement time sequence, so that the two can be settled separately (Xiao et al., 2021). Therefore, it is necessary to establish a centralized electricity spot market and set up a corresponding offset electricity settlement mechanism.

Most of the world’s centralized electricity spot markets use the double settlement system to settle between the day-ahead market and the real-time market. Some scholars also call it multi-settlement systems. In the field of electric power, the double settlement mechanism refers to the power transaction settlement mechanism that divides the power transaction settlement into pre-settlement and post-settlement according to the contract behavior and default deviation behavior. Among them, prior settlement refers to the prior settlement of the signed contract according to the contract agreement before the physical delivery of electric power to ensure the full implementation of the electric power contract; After the physical delivery of electricity, the settlement refers to the settlement according to the agreed deviation price according to whether there is any deviation between the behavior of the market subject and the agreement and the extent of the deviation, and the negative incentive for breach of contract is given economically. The double-settlement mechanism in the spot electricity market means that the day-ahead market is based on the day-ahead price to settle the bid-winning electricity quantity in the day-ahead market, while the real-time market is based on the real-time price to settle the deviation between the real-time bid-winning electricity quantity and the day-ahead bid-winning electricity quantity.

The spot market of PJM and ERCOT in the United States adopts the double settlement system to realize the settlement of the day-ahead market and the real-time market. The real-time price of PJM is calculated every 5 min, but the weighted average price within 1 h of each node is taken as the settlement price of the real-time market; The time granularity of ERCOT’s day-ahead market clearing is 1 h, while that of real-time market is 5 min. The real-time market is settled according to the weighted average price within 15 min, and the settlement price does not include the network loss component.

The centralized power real-time market model can be divided into single-period optimization model and look-ahead optimization model according to the optimization cycle, and the corresponding real-time settlement mechanism can be divided into real-time single settlement and real-time multi-settlement.

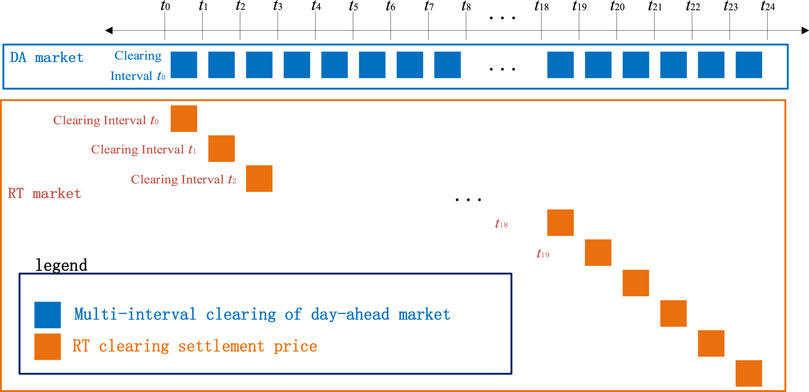

This optimization model does not take into account the future predicted power grid operation, and only optimizes the current period in each round when the real-time market rolls out. Each round of clearing only generates the market price and clearing electricity quantity of the current period, and the market will use the price and electricity quantity as the basis for single period settlement.

Real-time single settlement mechanism is a real-time single settlement mechanism connected with single-period optimization. It is applicable to single-period optimization. The operation mode is shown in Figure 2.

FIGURE 2. Single-interval settlement.

The mathematical model corresponding to single-period optimization has a small solution scale, is easy to search for optimization in a short time, and is easy to meet the calculation speed requirements of the real-time market; In addition, real-time single settlement is relatively simple and intuitive, easy for market participants to understand, and the workload of settlement is also less. Therefore, the single-period price model has been adopted by many market operators in the United States, such as ISO New England, MISO, PJM and SPP. However, the single-period optimization model has obvious defects in the economy and reliability of market clearing. In terms of economy, compared with multi-period optimization, if the current single period is successfully cleared, because it only considers the load situation of the current period for optimization, and ignores the economic value of the cross-period constraints before and after, the result is not necessarily the global optimal solution, but only the sub-optimal solution, and there is still large optimization space in general; In terms of reliability, if the clearing of the current period fails, the market members will not be able to actively respond to the regulation instructions because they cannot obtain real-time market information, and the system stability will be affected. The market operating agencies may need to take measures outside the market to regulate resources.

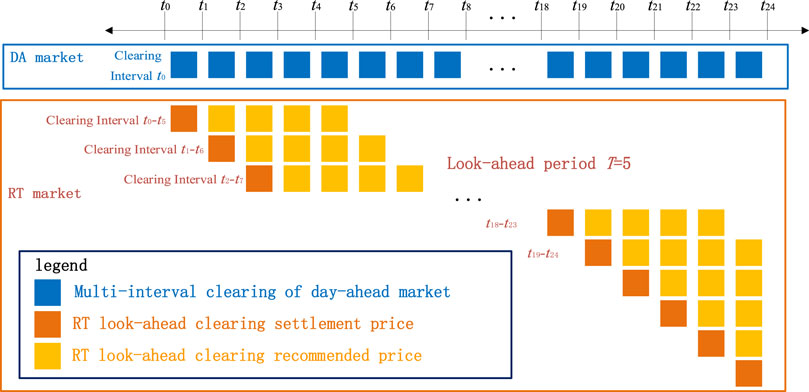

The look-ahead optimization model takes into account the forecast situation of the future power grid. When the real-time market is rolling out, each round will carry out look-ahead optimization for the current and future periods, and obtain the market price and clearing electricity of all periods in the look-ahead period.

Look-ahead single settlement mechanism is a real-time single settlement mechanism connected with look-ahead optimization. It is applicable to forward-looking optimization. See Figure 3 for its operation mode.

FIGURE 3. Look-ahead single-interval settlement.

Under normal circumstances, only the price and energy of the current period have the basis for settlement; The market information in the other look-ahead periods is only instructive, which can provide the basis for market members to make future decisions, and can also be used as the “backup” basis for the settlement of subsequent clearing rounds. When the clearing fails in the current period, the market cannot form the current settlement scheme. The “standby” basis of the previous round of settlement corresponding to the current period can be used to ensure the reliability of settlement. Therefore, the power market operators in New York (NYISO) and California (CAISO) have adopted the look-ahead single settlement mechanism. However, the current look-ahead optimization still has some defects, because the look-ahead order settlement mechanism needs to introduce real-time look-ahead optimization, and taking the clearing result as the basis for settlement may lead to inefficient scheduling, insufficient system compensation, incentive incompatibility and increased price volatility.

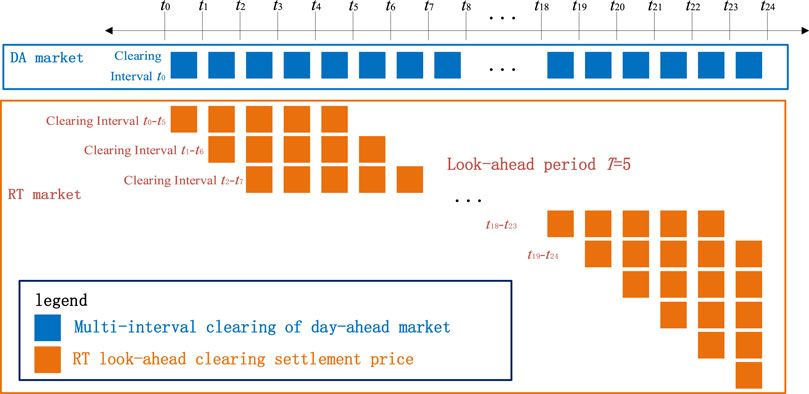

Look-ahead multi-settlement mechanism is also a real-time multi-settlement mechanism connected with look-ahead optimization. It is also applicable to forward-looking optimization. See Figure 4 for its operation mode.

FIGURE 4. Look-ahead multi-interval settlement.

Similar to the nature of the look-ahead single settlement mechanism, the look-ahead multiple settlement mechanism also needs to carry out real-time rolling look-ahead optimization to obtain the clearing information of all periods in the look-ahead period. However, the look-ahead multi-settlement mechanism will take the clearing information of the whole period as the settlement basis, without distinguishing between the current period or the look-ahead period.

Due to the increase of settlement frequency, look-ahead multi-settlement can better adapt to the problem of increased real-time volatility of the power system, promote the price response of flexible resources, and to some extent alleviate the problems of insufficient compensation and incentive incompatibility caused by forward-looking optimization. Compared with the forward single settlement mechanism, forward multiple settlement relies more on the reliability of market solution. Once the market clearing fails, it will lead to the loss of settlement data, which is not conducive to the settlement work. In addition, look-ahead multi-settlement requires several times of real-time clearing data, which greatly increases the settlement complexity of the real-time market, and also puts forward higher requirements for the storage space, accuracy and security of market data. At present, the settlement mechanism is still only the proposed scheme (Schiro, 2017), and has not been applied in the actual market.

Cross-period constraint is an important factor affecting the incentive of forward-looking optimization settlement. Cross-period constraints couple the optimization results of different periods in the electricity spot market, and the clearing prices of each period are intertwined. Therefore, look-ahead optimization is not suitable for the optimization and pricing of resources by simply cutting the period. However, due to the lack of incentives for the price of the look-ahead single settlement mechanism, power generation companies may not be able to recover costs through the market price and choose to deviate from the dispatching order. Therefore, when necessary, they should appropriately and flexibly increase the number of settlement rounds to make the settlement price highlight the real value of the actual resources as much as possible, thus increasing the incentive of the settlement price. In general, the longer the optimization period is considered, the more the clearing results can reflect the real economic signals, and the more incentive. Therefore, in the case of perfect forecast or low forecast deviation, compared with real-time look-ahead optimization, the day-ahead market takes into account the 24-h load situation, and the economic signals expressed by the clearing result are more comprehensive and more incentive, which can be regarded as the best clearing result. The problem to be solved by the new settlement mechanism is to minimize the deviation of clearing results between day-ahead and real-time settlement rounds, and improve the incentive of market participants to follow the schedule.

The look-ahead optimization cycle is 3–5 h, and the day-ahead optimization cycle is 24 h. Under the same load, the essential difference between the two is the optimization cycle. Therefore, it is necessary to analyze the influencing factors closely related to the look-ahead cycle. The constraint of ramp rate has a cross-time nature, and its shadow price reflects the economic value of the cross-time component, which has a great relationship with the look-ahead cycle.

When the real-time market adopts the forward optimization with a forward period of T, T electricity prices will be calculated for each period. The forward single settlement only selects the electricity prices of the current period as the basis for settlement, while the forward multiple settlement will include all electricity prices in the settlement system. The former is too mechanical and lacks motivation; The latter is too complex and lacks flexibility. Therefore, it is necessary to choose a balance between them, which can not only increase the incentive of settlement, but also limit the settlement complexity to a reasonable range.

For this reason, this paper designs a new mechanism of two settlements in the real-time market, and adds another settlement process on the basis of prospective single settlement, in order to increase the incentive of settlement without excessively increasing the complexity of settlement. In connection with the day-ahead market settlement, real-time one-time settlement can form the original double settlement mechanism with the day-ahead settlement combination. This content is the same as the existing double settlement mechanism, which will not be repeated in this article.

Real-time secondary settlement is based on the current target period’s settlement electricity price and clearing electricity quantity, and the deviation electricity quantity between secondary settlement and primary settlement is settled according to the target period’s settlement electricity price. The new settlement mechanism design can be seen in Figure 5.

FIGURE 5. New settlement mechanism.

It is known that when the real-time market adopts the forward optimization with a forward period of T, T electricity prices will be calculated in each time period, and the calculated electricity prices need to be prioritized. Therefore, it is necessary to explore the economic value of the cross-time components in the look-ahead optimization of electricity prices. See Eq. 1 for the mathematical model of real-time prospective optimization.

Where:

By constructing the Lagrange function and according to the Karush-Kuhn-Tucker (KKT) condition, it can be concluded that:

Where: L is the Lagrange function of optimization problem Eq. 1.

According to the definition of locational marginal price, spot market electricity price has two expressions:

Where:

Eq. 3 explains the connotation of spot market electricity price from the perspective of system and generator respectively (Shi et al., 2019). It can be seen from Formula 3 that the economic value of the cross-time component in the electricity price is mainly reflected in the Lagrangian multiplier constrained by the ramp rate, which is also a key factor affecting the incentive of look-ahead optimization (Hua et al., 2019; Zhao et al., 2020). There is a significant price deviation from the day-ahead optimization model using the traditional forward optimization rolling clearing electricity price, because it cannot reflect the value of cross-time constraints. All clearing results in history are regarded as “sunk costs” without distinction, which will make the unit have the impulse to deviate from scheduling (Schiro et al., 2016).

Among them, the willingness of the unit to deviate from the dispatching can be measured by the opportunity cost (LOC) compensation cost. The LOC compensation cost of units in the real-time market is defined as the difference between the maximum revenue of unit self-dispatch under the determined market clearing price and the actual revenue of units following the dispatching order. The calculation formula is shown in Formula 4:

Where:

At the real-time one-time settlement meeting, the settlement electricity price with the highest priority of prospective optimization and the clearing electricity quantity will be selected as the basis for settlement. Among them, the determination of settlement priority needs to select quantifiable criteria. The standard needs to reflect the deviation of clearing results between the day-ahead and real-time settlement rounds, and highlight the incentive of following the schedule. There are two types of quantifiable criteria that meet the requirements, namely, the Lagrange multiplier that reflects the economic value of cross-time components, or the LOC compensation that reflects the incentive to follow the scheduling.

Because the calculation of LOC compensation cost is relatively complex, it does not meet the time requirement of real-time rolling calculation. The Lagrange multiplier of the ramping constraint is the companion variable of the real-time prospective optimization result, which can be directly extracted, greatly simplifying the calculation process of settlement priority. Therefore, this paper selects the Lagrangian multiplier with ramping constraints as the key factor to quantify the deviation between the real-time prospective optimization results and the day-ahead optimization results, in order to maximize the incentive of cross-cycle prospective optimization. In this paper, LOC compensation cost of real-time one-time settlement price is taken as one of the incentive evaluation indicators.

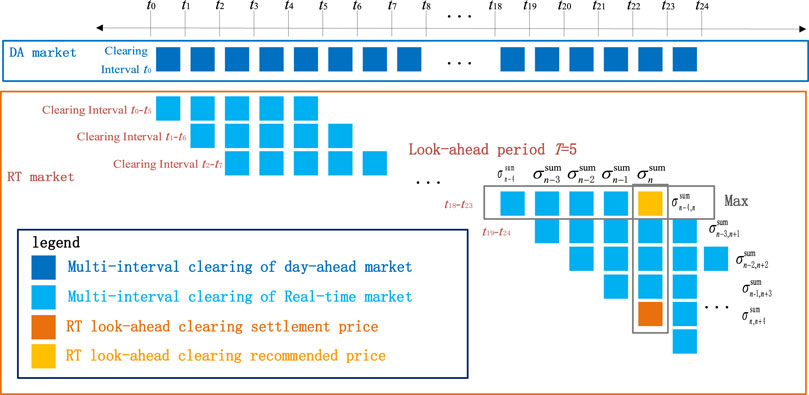

1) Calculation of settlement priority. The look-ahead period has a periodicity, and the factors affected by the optimization period in the optimization model are mainly cross-time components. According to Formula 3, the cross-time component in the electricity price is mainly the ramping constraint, and the formula is expressed as

Where:

Summarize the cross-time component values of all time periods in the look-ahead optimization cycle to form a qualitative settlement priority. The formula is shown in Formula 6. By summing the Lagrange multipliers with cross-time constraints in the T cycle, the economic value of the cross-time components in the T cycle can be comprehensively obtained. The larger the sum, the more real the economic value can be reflected by selecting this cycle. Taking this as the basis for settlement can better reduce the deviation from the day-ahead settlement, more truly reflect the scarce value of the system’s cross-era resources, and improve the incentive of the settlement price.

Where: TL is the number of intervals extended by the forward looking optimization. The forward looking period described above is T=(TL+1);

To make a settlement selection for time period t, it is necessary to compare the settlement priority of each optimization cycle including time period t. Select the clearing result of the optimized round with the highest priority as the basis for real-time one-time settlement.

Assuming that the result of Formula 7 is

2) Day-ahead settlement. The day-ahead settlement is consistent with the current market model, and the day-ahead electricity price and the day-ahead clearing electricity quantity are used for settlement. The formula can be seen in Formula 8.

Where:

3) Real-time settlement. Real-time settlement adopts the mode of deviation power settlement. The real-time first settlement will select the settlement electricity price with the highest priority of prospective optimization and the settled electricity as the settlement basis. Real-time secondary settlement is based on the settlement electricity price and clearing electricity quantity of the current target period. The deviation electricity quantity between secondary settlement and primary settlement is settled according to the settlement electricity price of the target period. The formula can be seen in Formula 9.

Where:

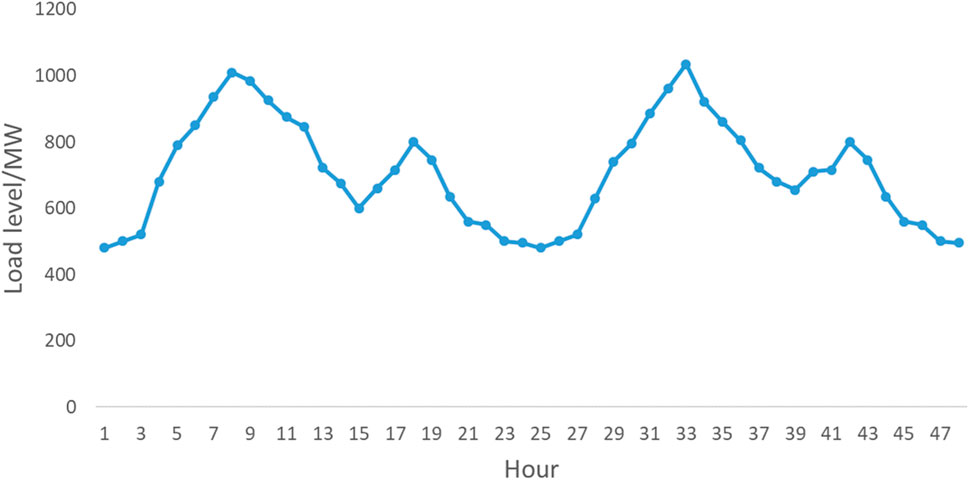

The calculation example uses IEEE 9- node-3-units system to demonstrate the incentive of the new mechanism of prospective optimization settlement. The example sets 48 time periods, and the period of real-time prospective optimization is 4. See Table 1 for the technical parameters and cost quotation of the unit and Figure 6 for the load parameters. It can be seen from the price characteristics that unit 1 has the lowest cost and the largest capacity, and is suitable for serving as the base load unit. Unit 3 has the highest climbing speed and is suitable for being a flexible unit. In period 3, period 20, period 27 and period 44, the electricity price drops sharply, which proves that the economic effect of cross-period constraints in the model is more obvious and can better verify the incentive of the new settlement mechanism in this paper.

TABLE 1. Technical parameters and cost quotation.

FIGURE 6. Load parameters.

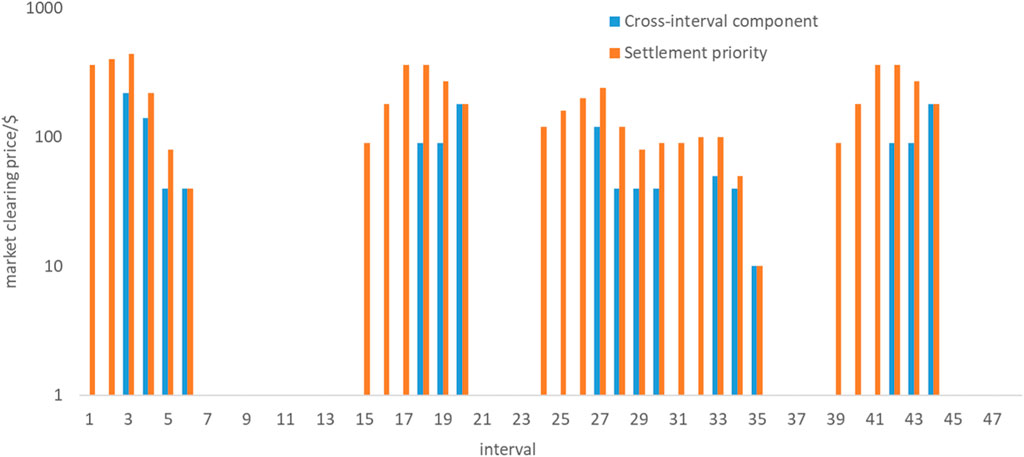

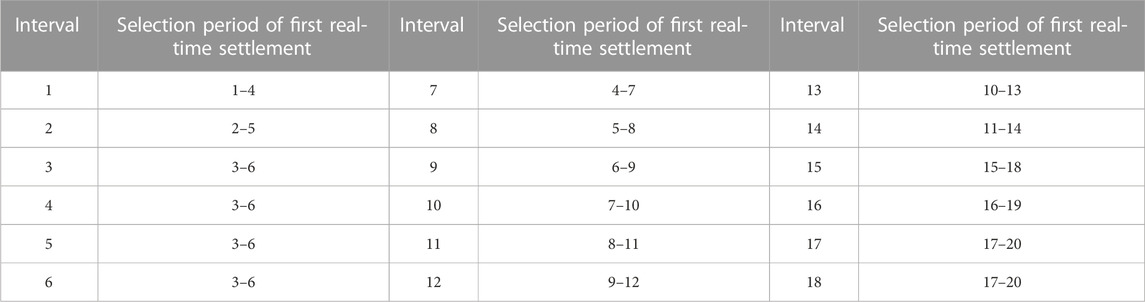

The settlement priority is shown in Figure 7. See Table 1 for the selection results of partial time periods for real-time one-time settlement. When the settlement priority of all optimization rounds is completely consistent, the earliest optimization round is generally selected as the basis for a settlement.

FIGURE 7. Settlement priority.

According to Figure 7; Table 2, the time period with high settlement limit is easier to be selected as the optimal time period for first real-time settlement.

TABLE 2. The selection result of first-settlement in the first 18 intervals.

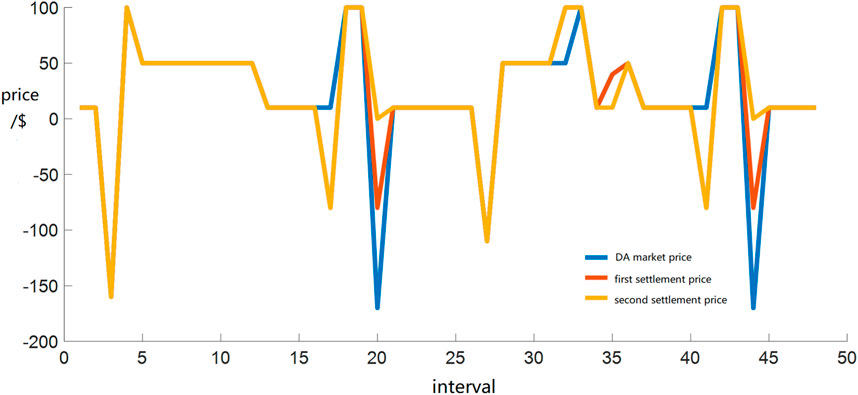

The situation of real-time one-time settlement electricity price is shown in Figure 8. It can be seen that compared with the secondary settlement electricity price (the real-time settlement electricity price of the original mode), the one-time settlement electricity price is closer to the day-ahead electricity price.

FIGURE 8. Settlement price.

According to Table 2, the shadow price of cross-time constraints corresponding to optimization periods 3–6 and 17–20 is higher, and the settlement priority is also higher. Corresponding to the change rule of the settlement electricity price in Figure 8, periods 3–6 and 17–20 are periods of violent fluctuations in electricity price. The system needs more flexible resources for cross-time scheduling, and the flexible resources have cross-time economic value in this situation.

Assuming zero error in real-time load forecasting, that is, there is no deviation between day-ahead load and real-time load, it can be seen from Table 3 that the electricity price selected for one-time settlement can better connect the results of day-ahead market, and the deviation is relatively low, and the average deviation rate of electricity price is reduced by 7.8%. In addition, through calculation, the opportunity cost (LOC) compensation cost of the real-time one-time settlement electricity price is reduced by about 30% compared with the original look-ahead settlement and only increased 7.2% of the calculation burden. If the updated research (Changshuo et al., 2022; Liping et al., 2022; Ning et al., 2022) methods are applied, the computational burden can be further reduced.

TABLE 3. The incentive of first-settlement price.

It should be noted that the biggest difference between the new settlement mechanism and the original settlement mechanism is to add real-time primary settlement. The real-time secondary settlement in the new settlement mechanism is the real-time settlement in the original settlement mechanism. The example deeply analyzes the most direct difference, that is, the incentive of one-time settlement electricity price, which can eliminate unnecessary interference, and is more conducive to directly and objectively highlight the differences between different mechanisms, reflecting the incentive effect of the new mechanism.

The calculation example shows that the new mechanism of look-ahead optimization settlement designed in this paper and the introduction of real-time one-time settlement electricity price can effectively reduce the deviation rate of real-time market electricity price, and can significantly reduce the opportunity cost compensation costs of power generation companies, and greatly improve the incentive of market members to follow the dispatching instructions. Figure 9 summarizes the effect of the calculation example.

FIGURE 9. Proposed multi-interval settlement system.

Prospective optimization plays an important role in adapting to the development needs of renewable energy and ensuring the good operation of the electricity spot market. However, the current look-ahead optimization model has the problem of insufficient electricity price incentives, which brings challenges to market construction. For this reason, this paper introduces the settlement priority. By appropriately and flexibly increasing the settlement rounds, it will not cause excessive settlement burden, but also enable the settlement price to highlight the real value of actual resources as much as possible, effectively improve the incentive of the settlement price, better adapt to the demand of real-time prospective optimization of the new era, and provide reference for the construction of Chinese electricity spot market. (Peng and Chatterjee, 2013).

In view of the above conclusions, the following conclusions are drawn:

1. Increase the incentive of real-time optimization. Under the current look-ahead optimization model, the value of cross-time constraints is only reflected in the day-ahead market clearing results, but not in the real-time market rolling optimization. Therefore, the price factor of cross-time constraints in the spot market can be introduced into the objective function of the mathematical optimization model, so that the price of real-time optimization covers the value of cross-time constraints and increases the incentive of real-time optimization.

2. Select an appropriate look-ahead settlement period. The current look-ahead optimization model always has differences between the day-ahead and real-time settlement due to the forecast deviation, and the selection of different look-ahead settlement periods will affect this deviation. Therefore, on the premise of not reducing the real-time incentive, select the most efficient look-ahead settlement cycle, try to reduce the settlement difference between the day-ahead market and the real-time market, and ensure the stability of the market.

3. Flexibly increase the number of settlement rounds and improve the settlement mechanism. Under the current look-ahead settlement mode, the settlement basis is relatively mechanical, and the market entities may deliver at the settlement price with insufficient incentive. Therefore, the incentive of settlement price can be increased by flexibly increasing the number of settlement rounds at the cost of increasing the amount of calculation, or the most efficient settlement price can be selected by the priority of settlement incentive, and the incentive of real-time optimization can be increased at the cost of increasing the complexity of settlement process, so as to improve the settlement mechanism.

4. Improve the calculation efficiency of settlement and increase the adaptability of practical engineering applications. Under the current forward-looking settlement mode, there is an obvious lack of incentive, and increasing the number of settlement rounds is a relatively feasible solution. Increasing the number of settlement rounds will inevitably increase the computational burden, so applying the latest research results to improve the computational efficiency of the actual settlement operation is the future development direction.

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

FQ: Supervision, review and editing; DX: Validation and experimentation; WJ: Methodology, validation and software.

Author QF was employed by State Grid Shanghai Electric Power Company. XD was employed by State Grid Shanghai PuDong Electric Power Company.

The remaining authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Bakirtzis, E. A., Biskas, P. N., Labridis, D. P., and Bakirtzis, A. G. (2014). Multiple time resolution unit commitment for short-term operations scheduling under high renewable penetration. IEEE Trans. Power Syst. 29 (1), 149–159. doi:10.1109/tpwrs.2013.2278215

CAISO (2014). Advancing and maximizing the value of energy storage technology: A California road map. https://www.caiso.com/Documents/AdvancingMaximizingValueofEnergyStorageTechnology_CaliforniaRoadmap.pdf.

CAISO (2019). Business practice manual for market operations. https://bpmcm.caiso.com/BPM%20Document%20Library/Market%20Operations/BPM_for_Market%20Operations_V71_redline.pdf.

Changshuo, W., Ning, X., Linjun, S., Zhang, L., Li, W., and Bai, X. (2022). Learning discriminative features by covering local geometric space for point cloud analysis. IEEE Trans. Geoscience Remote Sens. 60, 1–15. doi:10.1109/tgrs.2022.3170493

Chen, Y., Zhuo, Y., Liu, Y., Guan, L., Lu, C., Xiao, L., et al. (2021). Development and recommendation of fast frequency response market for power system with high proportion of renewable energy. Automation Electr. Power Syst. 45 (10), 174–183. doi:10.7500/AEPS20200726004

Ela, E., and O’Malley, M. (2016). Scheduling and pricing for expected ramp capability in real-time power markets. IEEE Trans. Power Syst. 31 (3), 1681–1691. doi:10.1109/tpwrs.2015.2461535

Hua, B., Schiro, D., Zheng, T., Baldick, R., and Litvinov, E. (2019). Pricing in multi-interval real-time markets. IEEE Trans. Power Syst. 34 (4), 2696–2705. doi:10.1109/tpwrs.2019.2891541

Huang, X., Zhang, T., and Xu, Z. (2019). Analysis on characteristics of Singapore′s power market settlement and risk management. South. Energy Constr. 6 (4), 29–34. doi:10.16516/j.gedi.issn2095-8676.2019.04.004

Jiang, H., Du, E., Zhu, G., Huang, J., Qian, M., Zhang, N., et al. (2020). Review and prospect of seasonal energy storage for power system with high proportion of renewable energy. Automation Electr. Power Syst. 44 (19), 194–207. doi:10.7500/AEPS20200204003

Liping, Z., Linjun, S., Weijun, L., Zhang, J., Cai, W., Cheng, C., et al. (2022). A joint bayesian framework based on partial least squares discriminant analysis for finger vein recognition. IEEE Sensors J. 22, 785–794. doi:10.1109/jsen.2021.3130951

Massachusetts gov (2016). State of charge, Massachusetts energy storage initiative study https://www.mass.gov/files/2017-07/state-ofcharge-report.pdf.

Ning, X., Weijun, L., Feng, H., Bai, X., Sun, L., and Li, W. (2022). Hyper-sausage coverage function neuron model and learning algorithm for image classification. Pattern Recognit. 136 (2023), 109216–109313. doi:10.1016/j.patcog.2022.109216

NYISO (2020). New York independent system operator services tariff. https://nyisoviewer.etariff.biz/ViewerDocLibrary/MasterTariffs/9FullTariffNYISOOATT.pdf.

Peng, T., and Chatterjee, D. (2013). Pricing mechanism for time coupled multi-interval real-time dispatch. https://cms.ferc.gov/sites/default/files/2020-05/20140411125224-M2%2520-%2520Peng.pdf.

Schiro, D. A. (2017). Flexibility procurement and reimbursement: A multi-period pricing approach. https://www.ne-rto.net/static-assets/documents/2017/09/20170920-procurement-pricing-of-ramping-capability.pdf.

Schiro, D. A., Zheng, T., Zhao, F., and Litvinov, E. (2016). Convex hull pricing in electricity markets: Formulation, analysis, and implementation challenges. IEEE Trans. Power Syst. 31 (5), 4068–4075. doi:10.1109/tpwrs.2015.2486380

Shi, X., Zheng, Y., Xue, B., and Feng, S. (2019). Effect analysis of unit operation constraints on locational marginal price of unit nodes. Power Syst. Technol. 43 (8), 2658–2664. doi:10.13335/j.1000-3673.pst.2019.0540

Wilson, R. (2002). Architecture of power markets. Econometrica 70 (4), 1299–1340. doi:10.1111/1468-0262.00334

Xiao, Y., Guan, Y., Zhang, L., Cai, Q., Liu, S., and Lin, S. (2021). Analysis and construction path of risk hedging mechanism in centralized LMP-based electricity spot market. Power Syst. Technol. 45 (10), 3981–3991. doi:10.13335/j.1000-3673.pst.2020.1975

Xie, L., and Ilic, M. D. (2009). Model predictive economic/environmental dispatch of power systems with intermittent resources. Proceedings of the 2009 IEEE Power Energy Society General Meeting, Calgary, AB, Canada, July 2009 1–6.

Yao, X., Zeng, Z., Yang, W., Wu, J., Yang, L., and Zhong, H. (2020). Electricity market settlement mechanism design and practice in Guangdong. Power Syst. Prot. Control 48 (2), 76–85. doi:10.19783/j.cnki.pspc.190253

Zhao, J., Zheng, T., and Litvinov, E. (2020). A multi-period market design for markets with intertemporal constraints. IEEE Trans. Power Syst. 35 (4), 3015–3025. doi:10.1109/tpwrs.2019.2963022

Keywords: multi-interval settlement, rolling-horizon scheduling, period selection, electricity spot market, settlement priority

Citation: Feng Q, Dong X and Jinghua W (2023) Multi-interval settlement system of rolling-horizon scheduling for electricity spot market. Front. Energy Res. 11:1170138. doi: 10.3389/fenrg.2023.1170138

Received: 20 February 2023; Accepted: 14 March 2023;

Published: 03 April 2023.

Edited by:

Praveen Kumar Donta, Vienna University of Technology, AustriaReviewed by:

Banoth Ravi, Indian Institute of Information Technology Tiruchirappalli, IndiaCopyright © 2023 Feng, Dong and Jinghua. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Wang Jinghua, amFuZTk1MDExMEBzanR1LmVkdS5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.