95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Energy Res. , 26 July 2023

Sec. Sustainable Energy Systems

Volume 11 - 2023 | https://doi.org/10.3389/fenrg.2023.1121853

Muhammad Imran1*

Muhammad Imran1* Xiangyang Liu1Muhammad Arif2Shams Ur Rahman3*Fazal Manan4Sajid Rahman Khattak3Rongyu Wang1

Xiangyang Liu1Muhammad Arif2Shams Ur Rahman3*Fazal Manan4Sajid Rahman Khattak3Rongyu Wang1It is crucial for the corporate sector to set aside a reasonable proportion of revenues for a sustainable corporate environment to transfer favorable and long-lasting impact to the upcoming generations. This study analyzed the impact of firm performance (FP) of the 25 energy sector sample firms of the Shanghai stock exchange (SSE) on corporate social responsibility (CSR) for the period 2011–2020 in light of the role of the intervening variable, corporate governance (CG). The data of the sample firms were analyzed and tested through multiple regression and structural equation models. This study is conducted in a developed economy with the rare mediator of CG to attempt to fill the gap of the previous studies conducted in a specific region of developing economies. The results show a pivotal role of FP in favorable CSR practices. In addition, the more established CG mechanism, as a mediator, has a considerable role between the predictor and predicted variables in the study. It is concluded from the results that firms in developed economies are more sustainability conscious than developing countries’ firms in terms of CG and CSR practices, which has been observed from the findings of the previously conducted studies in developing nations. Furthermore, structural equation model analysis values of βs for return on assets (ROA = 0.48), return on equity (ROE = 0.65), return on sales (ROS = 0.80), and debt-ratio (LIB = 0.40) considerably affects FP in the sample firms. It is also observed from the correlation matrix that FP indicators (ROA, ROS, ROE, and LIB) have positive as well as significant effects on CG and CSR practices. This study’s detailed policy implications are provided in the conclusion section.

It is the stakeholder theory that paves a theoretical foundation for amalgamating business as well as social domain research (Javeed & Lefen, 2019). The long-term sustainability of enterprises is due to the backup provided by stakeholders in the form of resource supply, while at the same time, the stakeholders are also expecting those enterprises to provide a satisfactory level of value proposition. It is said that for the safe and long-term stability of a car, the skills of a driver are more important than the quality of that car. So, in the case of corporate matters too, researchers have focused their attention on the key role of corporate governance in terms of various factors that jointly constitute a huge interdisciplinary coalition. There is an association between how a company governs and its effects on various aspects of the business ventures as well as a visible effect on how to survive in such a tough competitive environment (Manning et al., 2019). This topic has recently been gaining a considerable amount of attention from researchers and, therefore, studies appeared engaged in thoroughly studying various aspects of the board of directors’ composition in order to clarify the best determinants for excellent mutually beneficial business management practices (Miglani et al., 2020).

The concept of “Responsible Innovation” was proposed by the (European Commission’s Horizon, 2020) Framework Plan, which suggests that there should be a matching between society and technological innovations subject to visible cooperation (Barney, 1986; Hung et al., 2010). The aim of responsible innovation should not compromise on moral, social, ethical, or sustainable desirability; the focus shall be given, in the first place, on the fulfillment of future needs via collective-based management (Smith, 2010). The concept of “balance” thought is included in responsible innovation and, therefore, it has been introduced in business management research as a new management paradigm. Over the last few decades, corporate social responsibility (CSR) has been introduced, grown, and emerged as an excellent sustainable corporate strategy. There are various reasons behind the popularity and significance of CSR, such as governmental regulations, demand from consumers, and market conditions which consistently play a key role in the international economic slump (Smith, 2010). As far as the role of CSR practices is concerned, it is the businesses’ understanding and handling of social, economic, and environmental issues both in their business operations and in their interactions with stakeholders that matter (Murtazavi et al., 2013). Similarly, CSR can also be defined as companies’ keen consideration of their legal due responsibilities to safeguard society and the environment from its effects, with a focus not only on sustainable development but also on ensuring a feasible public and environmental policy (Martinuzzi et al., 2011). In the broad spectrum, CSR is a tool for mitigating the weak results of corporations in terms of their production and operation layout in order to ensure the welfare of society while creating an environment for strong business practices under tough conditions by owners and stakeholders that will maximize the profitability of the organizations rather than just aiming to build or preserve it (Crifo & Vanina, 2015). Additionally, the concept of CSR is centered on integrating social and environmental concerns into business operations as well as making interactions in line with mandatory and voluntary activities (Sen, 2017). The scope of such activities covers its citizenship, ethics, good corporate governance, and other significant activities (Zheng et al., 2015). It is clear from the above-mentioned literature that there are various concepts and contextual definitions of CSR. Consequently, as the CSR knowledge base is considered to be limited in the context of availability, understanding, and promotion, the successful adoption of CSR commonly depends upon firms and countries’ development capabilities. It is concluded that all these aspects concerning CSR concepts have room for improvement and, therefore, are still being debated. The link between CSR and firm performance has been detected by various researchers at different times through diversified approaches.

Some of these studies have shown mixed associations between CSR and firm performance, that is, a positive, negative, or neutral relationship. Corporate performance is positively affected by CSR activities while firms giving less attention to social activities witnessed a considerable decrease in performance (Wei et al., 2020). The various valid performance indicators like ROA, ROE, and EPS ratios are positively and significantly influenced by the CSR activities of the firms (yang et al., 2019). Concurrently, there is a positive association between CSR dimensions (environment, suppliers, customers, employees, and social) and a firm’s performance. Javeed & Lefen (2019) concluded that there is a positive and significant relationship between CSR and firm performance, whereas there is a positive correlation between the effect of the Chief Executive Officer (CEO) and ownership, as a mediator, on firms’ performance and ownership with CSR. Additionally, the moderation of CSR has played a significant and positive role between corporate governance and firms’ performance (Ali et al., 2020). The firms fulfilling CSR would significantly impact firm performance (Wang et al., 2012). It is crystal clear from the previous research findings that there is a significant relationship between companies’ performance and their CSR (Cherian et al., 2019). It is CSR that not only increases the social value of the firm and its reputation, but also boosts profitability and long-term performance. The companies with better financial performance also assume more CSR practices because firm performance has a statistically significant and positive impact on CSR (Sial et al., 2018). Contrary, there may be a negative association between CSR and PF. Similarly, it is also evident that firms that have a lower rate of return on assets disclose a considerable amount of information regarding CSR initiatives as compared to the firms with a higher return on assets (Selcuk & Kiymaz, 2017). Furthermore, in the context of post-controlling the debt and size of the firms, there is less profitability found in the firms with a high ratio of leverage in their capital structure, unlike for the larger firms in the form of higher profits. It can be interpreted that there is no sizeable relationship between CSR and corporate performance (Alexander & Buchholz, 1978). While the causal association between CSR and FP makes known about this angle that better FP does not because of the greater social responsibility as well as a negative impact of PF on CSR is found (Hirigoyen & Poulain, 2015). Similarly, the possible contra effect of FP on CSR has been examined and found mixed results (Lee et al., 2013; Imran, 2021).

The mentioned various studies’ findings exposed a positive relationship between operational dimensions of CSR and FP, while at the same time showing a negative association between non-operational elements of corporate social responsibility and FP. Some of this multifaceted literature examines the firms’ value under the influence of firm performance, firms’ CSR practice, and CSR activities by adopting descriptive modes in the context of the selected study area. The stakeholder and CSR implementation has been evaluated in the context of a causal relationship (Eyasu & Endale, 2020). The results show that CSR is significantly affected by the environment, customers, shareholders, and community. In this way, the evidence of CSR practices, its key determinants, and various considerable challenges have been examined in the context of theoretical as well as empirical dimensions (Ayalew, 2018). Furthermore, the study has concluded that CSR should get attention through the CSR centers.

In order to promote CSR on one side and at the same time foster the academic study, awareness should be created by encouraging the private sector to perform responsibly with its business practices. Besides the core practices performed by CSR, the study also focused on the significant aspect of CSR, that is, the people and planet perspectives that have been examined (Gereziher & Shiferaw, 2020). Firm performance and CSR can be further investigated for more generalized findings that could help management to restructure their policies (Khan et al., 2023). The effect of FP and CSR can be found through the inclusion of a mediator supported by theory (S) in order to extract more authentic findings both for developed and developing stock markets (Jiafeng, 2023). According to these findings, it is concluded that an imbalanced situation exists between environmental and social aspects of CSR practices while it is the need of the hour to create well-defined, strong, and effective community engagement and meaningful public relations that will be beneficial to all stakeholders. Therefore, the teaching-learning of CSR practices in various selected listed firms has been examined in the form of a qualitative case study (Bimir, 2016). The study concluded that there are considerable theoretical implications, that is, CSR is one of the most attractive and debatable issues, mainly in developing countries such as Ethiopia. The study further concluded that firms’ performance, corporate governance, and CSR are two sides of the same coin. CSR practices are mainly based on firms’ performance and the position of corporate governance. This research further added that the explained variable CSR is influenced by firm performance while firm performance is influenced by corporate governance, and CSR is affected by the active role of corporate governance (Yang et al., 2019). Furthermore, CSR practices are difficult to manage for firms operating in developing nations (Ying et al., 2021).

Thus, the findings of previous studies are inconsistent; some outcomes seem reasonable, while many of them are contradicting one another and, therefore, there is a mismatch in their conclusions. Some studies have focused on the data from a specific state/region of a country by using panel data while some used survey data. Therefore, in light of the above literature, this study will attempt to fill the gap of the previous researchers by examining the role of CG as a moderator between firm performance and CSR in the Chinese energy sector firms. The sample was taken from the energy sector of the Shanghai stock exchange. Variables and their pattern in the study have rarely been studied before, i.e., Firm Performance (D.V), CSR (I.V), and CG (Mediator). The scope of the study is limited, as discussed in the earlier section, as previous studies mainly focused on developing economies while in this study we adopted a sample from energy sector listed firms at the Shanghai Stock Exchange, China. This study will be based on the following objectives: First, to examine the impact of FP on CSR. Secondly, to analyze the mediating role of sustainable CG between FP and CSR. Lastly, to investigate the interrelationships among FP, CSR, and sustainable CG. Furthermore, the study has the following research questions: first, does FP affect CSR? Second, does CG mediate between FP and CSR? Third, do interrelationships exist among FP, CSR and CG?

This study is important based on the reality that FP drives CSR practices while considering sustainable CG in developed economies. It is the need of the hour to provide a safe and sustainable environment with the help of a true CG mechanism.

The rest of the paper is organized as follows: section two discusses the literature review, section three discusses the research methodology, while section four and section five offer the results and discussion and conclude the paper.

The origin of CSR can be traced back to the 1920s; CSR was originally proposed by Sheldon in 1924, where the basic theme concept was that to protect society’s wellbeing is an enterprise’s primary responsibility when achieving the basic target of profit motive (Sheldon, 1923). Additionally, the occurrence of the 19th-century labor conflicts due to the industrial revolution, where individual artisan work was exchanged for mass production, uncovered a series of problems concerning society and its was a driving force to push companies to take necessary corrective actions that may be considered the root cause of CSR (Carrasco et al., 2016). Due to the recent tough competition among firms, it is very difficult for companies to survive and hold a strong position compared to their competitors. The firms, for this very purpose, aim to create a competitive advantage over their competitors, and will try their level best to adopt CSR practices. These competitive companies are caring about society in order to make it possible to be a pro-society firm in terms of their business location and activities. Therefore, corporate social responsibility (CSR) acts like a bridge integrating economic and environmental events, not only in their operations but also in their interactions with their anticipated stakeholders (Yang et al., 2019; Lu et al., 2020). The core objective of the capitalist model was centered on the promotion of profit maximization as well as self-regulation of markets in order to gain a monopoly during the 1950s and 1960s, resulting in neglectful behavior towards labor rights. Indeed, this was the main cause behind the rise of voices against such violations, with demands emerging for responsible business operations with the capacity to safeguard the social aspect along with the production and profit motives (Carrol & Shabana, 2010). Subjective evidence concluded that failure to manage an efficient corporate governance mechanism in corporations can be marked, among other considerable elements, as one of the noted factors in a financial crisis. Corporate growth is the outcome of timely and correct decisions through a well-structured corporate governance mechanism in the concerned decision-making (Aebi et al., 2012). Moreover, a severe economic crisis was witnessed in the 1970s, which also resulted in notable social movements. These movements paved an initial way for highlighting the most important issues concerning the environment and civil rights that were ignored by businesses and companies before (Carroll, 2015; Zhang et al., 2022). In essence, the corporations are guided and controlled through a system, called corporate governance. It is clear from previous research findings that a single variable, like board characteristics, ownership structure, and so on, cannot fully uncover and clarify the basic concept and quality of corporate governance Furthermore, these types of single concepts make the basic concept of corporate governance very ambiguous and questionable (Bhagat & Bolton, 2008). It is worth mentioning that corporate strategic decisions are significantly influenced by good governance practices and top management structures, including those firms who view their production and operations in light of activities that are environmentally friendly (Shahab et al., 2020). This is evident from various past studies that were focused mainly on analyzing the effect of board structure variables on Governance disclosures (Elmagrhi, Ntim, and Wang, 2016; Ntim, Soobaroyen, and Broad, 2017), and corporate social responsibility (Liao,Lin, and Zhang, 2018; McGuinness et al., 2017).

The majority of previously conducted studies examined the association between CSR and firm performance based on various approaches while the impact as well as the relationship between these two variables were re-analyzed. This study is based on a conceptual framework that amalgamated the impact of PF on CSR and CG mediation.

An indirect linkage is found and confirms between financial status and CSR practices in the sample firms of the study (Jiafeng, 2023). It is concluded that the company’s vision is positively and significantly influenced by CSR practices (Yang et al., 2019). CSR practices in the firms have a positive association with firm performance while various performance indicators like high growth increase in total assets, sound corporate position, and social contribution will boost CSR adaptation (Chawdhury et al., 2019). To encourage creativity to inspire and improve corporate social performance, companies use CSR and green business practices (Jesus, 2017). Another benefit of a good relationship between company performance and CSR is evidence that the direct costs incurred by the companies are not concealed fees for stakeholders. In other words, it, proves that firm performance and CSR have a positive linkage. Contrary to this, the benefits of CSR are big enough that considerable attention is given to the interest of the stakeholders and their social expectations, i.e., consumers, environment, and employees (Carroll, 1991). Thus, a serious consideration towards CSR practices in businesses, on one hand, raises the costs and, on the other hand, reduces the prices specifically concealed from the stakeholders. The popular three profitability proxies, namely, ROA, ROE, and ROS, measure the profitability of corporate financial performance (Low, 2016). Due to the required financial support needed to manage CSR practices, companies are facing hurdles in developing economies (Ying et al., 2021). For that very purpose, the relationship between financial performance and social responsibility of the firms are mutual and positive. In contrast to that, the causal relationships among these two, financial performance and social responsibility, have been analyzed to find out empirical results (Mc Williams, 2001). The results show that more liberal social responsibility does not produce better financial performance and, therefore, one can conclude that financial performance negatively impacts CSR. Furthermore, in the context of the meta-analytical investigation, it is proven that the relationship between corporate social and economic performance shows that corporate social performance positively impacts corporate financial performance (Muriithi et al., 2021). Similarly, the relationship between CSR and a firm’s performance has been examined with the help of accounting-based measurement tools like return on assets (ROA), total assets, and sales growth. It is concluded that a positive relationship between CSR and firms’ performance is obtained (Dartey-Baah & Amponsah-Tawiah, 2011).

The proxies of Returns on asset (ROA), return on equity (ROE), and return on sales (ROS) affect firms’ Performance (Khan et al., 2012). The size or volume of a firm has a substantial effect on the FP, as does the amount CSR practices require funds to invest in CSR practices (Khan et al., 2023). Better corporate financial performance can be obtained using a better understanding and usage of corporate financial social responsibility (European Commission, 2001). Contrary to the findings of Selcuk and Kiyma (2017), a negative relationship between CSR and financial performance is shown in companies that more frequently unveil information about CSR practices having a lower return on assets. The findings of the study also suggested that big companies have a high volume of profits subject to post-adjustment for their debt and size, whereas firms with higher leverage are less profitable. Further, the return on assets is negatively affected by the capital structure on the firm performance view, the short-term debt, the long-term debt, and the company leverage (Hermoningsih et al., 2020). There is a negative association between Return on equity (ROE) and capital structure variables; however, it is also insignificant as compared to the long-term debt and company leverage in order to provide the desired results. The performance of the firm is also negatively affected by the degree of liability on the capital structure. This discussion leads us to our first hypothesis.

Hypothesis H1. There is a positive and substantial impact of firm performance on corporate social responsibility practices.

It is a very common for the stakeholders to understand that PF is affected by the CG. Similarly it is considered the most basic issue by the stakeholders because it helps them to recognize and clarify these factors that influence performance while taking these elements into account as indicators for a firm’s success or failure. In this context, Fallatah and Dickins (Fallatah & Dickins, 2012) explore the association between corporate governance and a firm’s performance, while declaring that there is a considerable boost in the firm’s performance through corporate governance strategy in the given firms. At the opposite pole, Ahmed and Hamdan (Ahmed & Hamdan, 2015) conclude an unconnected association between corporate governance and firm performance while investigating the relationship between these two variables of interest. Though, Alsurayyi and Alsughayer (2021) observed a causal relationship between corporate governance and firm performance and established a strong and significant linkage of corporate governance to firm performance. In addition, Del Miras-Rodríguez and MartínezMartínez (2018) have taken into consideration publicly listed firms in order to find out the impact of good corporate governance on firm performance and concluded that those firms who have more strong corporate governance philosophy have sound performance. Similarly, the financial performance of firms can be improved with better corporate governance strategy and efficient CSR practices while CSR also plays a key role in better financial performance. According to (Mahrani & Soewarno, 2018) and (Akram et al., 2018), institutional regulation is also a considerable factor because it has a positive effect on both corporate governance and firm performance. The rise in corporate governance due to proper practices has a visible effect on company performance. Consequently, the above literature suggests that there is still room for the conduct of research work to further establish the relationship between corporate governance and firm performance. In this way, this study attempted to examine the same area of interest but with a unique aspect of the mediation role of corporate governance between firm performance and CSR practices.

Hypothesis H2. Firm Performance (FM) is positively and significantly influenced by Corporate Governance (CG).

Corporate governance, as a mediator between Firm Performance and CSR, has been found to have a significant positive relationship with a firm’s performance. In terms of board interaction, the relationship between CSR and firms’ performance demonstrated the same results. Furthermore, the management ownership and CSR interaction indicated a positive significant linkage with the firm’s performance whereas the firm’s performance is positively affected by the interaction between the ownership concentration and CSR practices in the firms. Moreover, the CSR initiatives are positively and significantly associated with the corporate governance practices subject to the level of CSR practices (Poudel, 2015). Indeed, it empowers the practicing organizations as well as statutory bodies to think through solid corporate governance practices that will augment CSR initiatives for better achievements of objectives.

There are many factors through which the strength of CSR engagement is determined at the firm level, including equity ownership structure, the composition of the board of directors, and corporate governance and CSR in terms of their regulatory framework (Crifo & Reberioux, 2016). CSR practices also depend on the firm because the larger the firms are, the more they tend towards utilizing more resources than small and medium firms in terms of capital and talent; hence, larger investments can be made in the head of CSR by the big firms and vice versa (Farooq et al., 2015). Similarly, there is positive and significant governance on CSR. It is concluded that firms’ corporate social responsibility practices can be improved through firms’ efficient corporate governance mechanisms that are associated in part with each other. The firm performance, financial performance, and CSR are positively and significantly affected by the mediating role of mechanism of good corporate governance and CSR. Besides, the key and visible role of government in motivating and influencing CSR practices is also worth mentioning (Park & Ghauri, 2015). This leads to our third hypothesis.

Hypothesis H3: There is a positive and significant CG mediation between FP and CSR.

The study is based on both quantitative and qualitative research approaches in order to get valid results, consistent with previous mixed studies (Kumar, 2011). As for as the nature of this study is concerned, the researcher’s rationality to pick a specified research design was due to the variety of characteristics like the type of data to be used, data collected, and valid analytical tools in order to get more authentic results. The applied research model in this study is adapted from previously examined studies (Sánchez-Infante et al., 2020). Due to the inclusion of mediators, the nature of variables as well as their measurement tools, the model specified, and differences in the methodology, to the researcher attempted to distinguish this research design study from the adapted one. Therefore, this study considered a research model that was designed to investigate the impacts of firms’ performance on CSR by using corporate governance as a mediator variable empirically while the indicators such as board, audit, and transparency are taken into account. Contrary, the indicator for firm performance is the liability on capital structure in the current study. Both primary and secondary sources of data have been considered in this study. The selected respondents like corporate boards, management, and staff members are considered in order to get relevant data from them. In this study, secondary data have been gathered from various sources such as annual reports, surveys, policy documents, and the official website of the Shanghai stock exchange. The data were collected through 50 standardized structured questionnaires out of a total of 80 questionnaires that were distributed via email to the respondents. The popular Likert scale with five points has been adapted (i.e. 1 = strongly disagree, 2 = disagree, 3 = neutral, 4 = agree, 5 = strongly agree) to measure the items of the questionnaire. In this study, the data have been collected from 25 energy sector listed companies out of a total of 77 firms from the energy sector listed on the Shanghai stock exchange for a period of 10 years, from 01.2010 to 12.2020, in order to evaluate firms’ performance (TIRET Corporate Business Enterprises Strategic Report, 2020).

At the end of the year 2020, there were a total of 1730 firms listed on the Shanghai stock exchange, which is one of the largest stock exchanges in China. This study has taken the energy sector which was comprised of 77 listed firms on the Shanghai stock exchange during the same period mentioned above. The sample size of this study, using a convenient sampling technique, is 25 energy firms out of a total of 77 listed firms in the same sector. A total of 500 questionnaires were distributed among the respondents via emails; 380 filled questionnaires were collected successfully (Ying et al., 2021).

There are 17 state-owned endowment firms as well as four firms shared by the private owners. The total sample size was 21 corporate business enterprises, from which a total of 357 individual respondents were chosen to collect data. Further, with the help of non-probability purposive sampling techniques in order to categorize the specified area and fix the respondents’ number, the researcher used valid sampling techniques for more generalized results (Palinkas et al., 2015).

This study used SPSS/AMOS to code, insert, and process the collected data. For the measurement of all instruments, nominal scales were used. Similarly, the firm performance results were evaluated by using the marketing-measurement approach. Further, the test of the hypotheses was done with the help of chi-square goodness-of-fit tests in order to get reliable results. Additionally, AMOS was used to estimate all latent variable coefficients on the structural equation model as well as using path diagram analysis (Ying et al., 2021).

In order to check the direct and mediating effect and the indirect impact on the direction, SEM is an excellent approach to get valid results. Therefore, it was designed to test a combined or single analysis model instead of separate regression analyses, which will be more able to analyze the required objectives of the study (Sobel, 1982). Various corporate governance indicators can better portray its linkage on the FP of the sample companies through SEM while also obtaining valuable findings in a more sophisticated manner (Oladeji, 2019; Li, Li and Wareewanich, 2021). Similarly, according to the findings of another study, it is concluded that the mediation of CG can be gauged nicely in between FP and CSR by using SEM. It provides ease of use and authenticity for the users (Alamgir, 2016; Zeng, Li and Huang, 2021). Therefore, based on the solid statements of the previous researchers regarding the use of SEM, this study adopted the same for valid results. There is a causal estimation for all the included variables in the study where one variable affects the second while that affects the next one, and so on. Consequently, the intervening variable between the independent and dependent is denoted by M, is the mediator whereas, this variable mediates their relationship. The association between explanatory variable X (i.e., firm performance) and Y, an explained variable (i.e., CSR) is examined. The following econometric model shows the above-mentioned discussion of variables of the study (Ying et al., 2021). First of all, the explained variable “Y” was in the following manner in order to estimate the impacts of firm performance on CSR.

In the second equation, the mediation role of CG has been taken into account between FP and CSR to predict it with the help of multiple regression analysis with the “X” and “M” predicting equation.

In the third step, CG as a mediator variable is predicted between the explanatory variable X and explained variable Y.

In the above equations, Y is the predicted variable, X is the explanatory variable, M denotes the mediator variable, α is the intercept, βs are the coefficients, and ei is the standard error of the model.

The explained variable of the study is CSR measured by three dimensions, namely, economic, social, and environmental, used for measurements of the items in the questionnaires that have three parts (Yang et al., 2019; El-Garaihy et al., 2014; Hourneaux et al., 2018; Wu et al., 2018, Zhu et al., 2018; Otero-Gonzalez et al., 2021; Kai et al., 2022). There are nine measurement instrument indicators. The economic indicators include stakeholder involvement, the response of customers compliance, quality of products, customer satisfaction, maximizing profit, minimizing operating costs, monitoring employee productivity, and engaging in long-term business, while there are also six social dimensions: training and education, human rights, community development, health, safety in the workplace, employment and labor relation. There are six environmental dimensions: pollution, energy, waste, transport, ecological, and compliance. The primary data regarding CSR has been gathered from the respondents of the study in terms of the above-mentioned dimensions (Ying et al., 2021, Khan et., 2023 and Jiafeng 2023).

Different economic and financial indicator variables were used in this study to measure firm performance. The marketing approach of the performance indicator is also used to measure the predictor variable (Al-matari et al., 2014; Akomeah et al., 2018; Yuen et al., 2018; Yang et al., 2019). Thus, ROA, ROE, ROS, and liability on the capital structure are adapted to measure the independent variable FP. As a result, total sales, total assets, total liability, total capital, total equity, and financial strategic year results were taken into account in the study. These values will help the company to measure its internal performance (Ying et al., 2021) Furthermore, the mediator variable CG and its measurement items in this study were examined via the mediating variable indicator questionnaires that were used to evaluate the role of corporate governance on firm performance and CSR practices. Therefore, the measurement items for the mediator variable corporate governance are board, audit, ownership, and transparency.

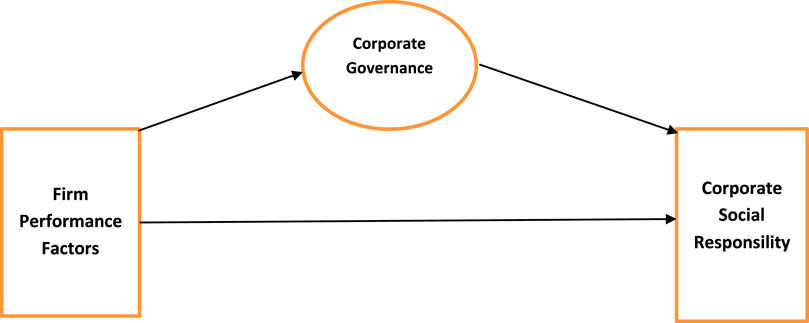

For any type of research study, it is necessary to have a conceptual model that guides the researchers to help in organizing, conceptualizing, and proceeding with their research (Grant & Osanloo, 2015; Rocco & Plakhotnik, 2009). Therefore, this study considered a research model that was designed to investigate the impacts of firms’ performance on CSR by using corporate governance empirically as a mediator variable.

The conceptual model includes the independent variable firm performance, the mediator variable corporate governance, and the dependent variable CSR practice. This study uses return on asset (ROA), return on equity (ROE), return on sales (ROS), and debt to equity (DTE) as indicators of firm performance. Likewise, the indicators of corporate governance are board, ownership, audit, and transparency. The outcome variable of the study is CSR practice, which has indicators such as the economic, social, and environmental dimensions (these are given in Figure 1).

FIGURE 1. Conceptual framework of the study.

As far as the demographic data of the respondents are concerned, out of the total sample size of 380 (100%), 233 (61.31%) were male whereas the remaining 147 (39.69%) were female. The mentioned gender data shows that developed nations give considerable opportunities to female employees as compared to developing nations. It proves that utilizing female employees can have a better effect on the overall productivity of the economy. Similarly, in terms of age of the respondents, there were four categories: 82 employees aged 21–30 years (21.57%), 98 employees aged 31–40 years (25.78%), 108 employees aged 40–50 years (28.42%), and 92 employees above 50 years of age (24.21%). This categorization proves that the majority of the respondents were from the most mature and productive categories, which is a sign of good sample selection in terms of accurate as well as valid answers to the questions.

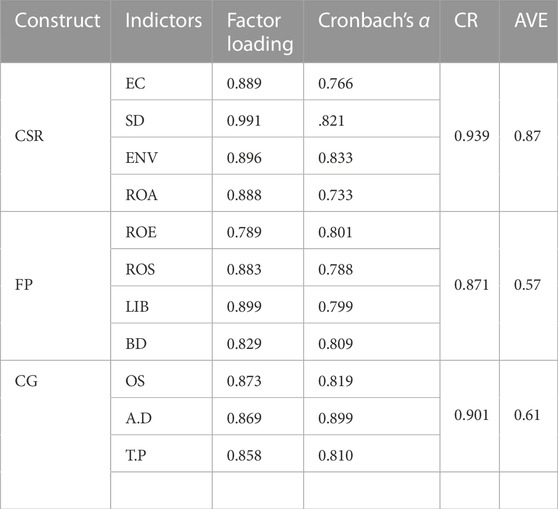

The study considered the key reliability analysis in order to ensure accurate and reliable data. For that very purpose, Cronbach’s alpha is used as the most valid and reliable measurement instrument. Alpha is the best choice among the given coefficients to test the reliability while the standard score for alpha shall be equal to or greater than 0.70 in order to meet the internal consistency preconditions (Cho et al., 2014).

In light of this principle, the values in Table 1 show the coefficient values of the alpha score with a range from 0.733 to 0.899, which itself proves that for the measurement of the predicted variable CSR all other included variables in this study are the best fit, reliable, and valid. Similarly, exploratory factor analysis (EFA) is adopted in this study to establish the validity of the instruments as well as to organize various items into constructs under the umbrella of one specifically defined variable (Chan & Idris, 2017). The range of the latent factors’ estimate of reliability under the composite reliability (CR) was from 0.871 to 0.939, which is an acceptable level in terms of the scale of CR level of reliability with a rational internal consistency in the given table. It is clear that a value greater than 0.70 of the C.R is accepted as a standard value (Bacon et al., 2015). Likewise, the recommended level of AVE shall exceed 0.50, therefore, as per given the standard, this study has an estimated (AVE) value for the given constructs ranging from 0.57 to 0.87 as indicated in Table 1, which fulfills the mentioned criteria of >0.50. Hence, it is very good as per the standardized value of the AVE (Henseler et al., 2015).

TABLE 1. Construct validity and reliability analysis.

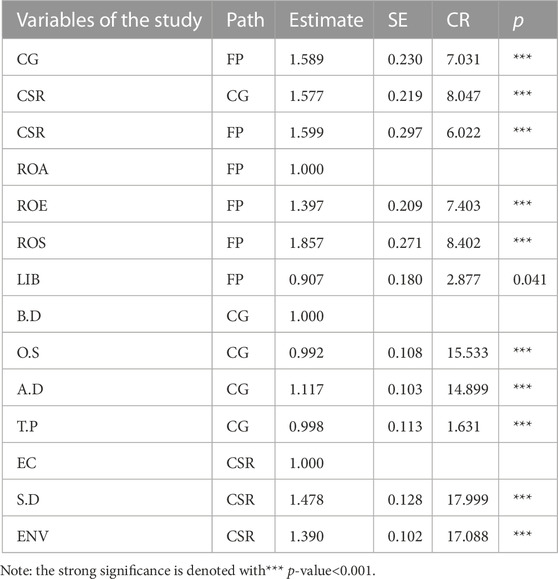

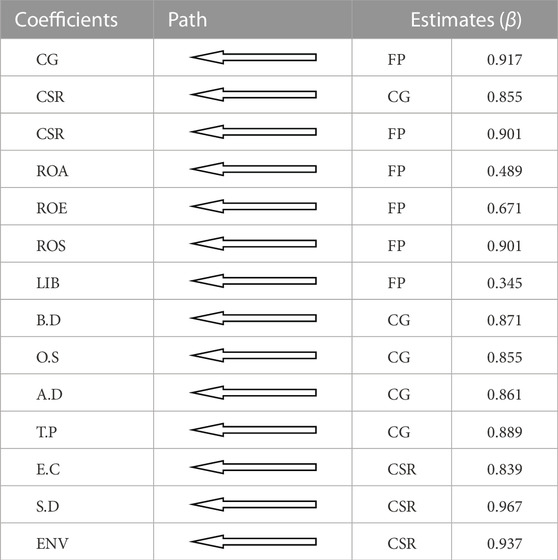

As per the results of the regression analysis in Table 2, the parameter estimate value is all positive and its range is from 0.992 for Corporate Governance to 1.857 for Firm Performance, which shows a significant trend in the table. The critical ratio is created by the separation of the estimates with their relevant standard error (SE). Similarly, the score of critical ratio values that exceeds the standardized value of 1.96 is considered to be significant at the p-value 0.05 level. Therefore, it is concluded that all the outcome values are significant at a level of p-value 0.05 because critical ratio (C.R) values exceeded the threshold value of 1.96. Furthermore, in order to be more valid in the results of the independent variable, the value for each of the variables were tested independently in order to check and verify the fitness of the model. Resultantly, the significance level of the independent variable firm performance is greater than the p-value, that is, 0.05 level of significance.

TABLE 2. Regression Analysis in terms of significance and CR

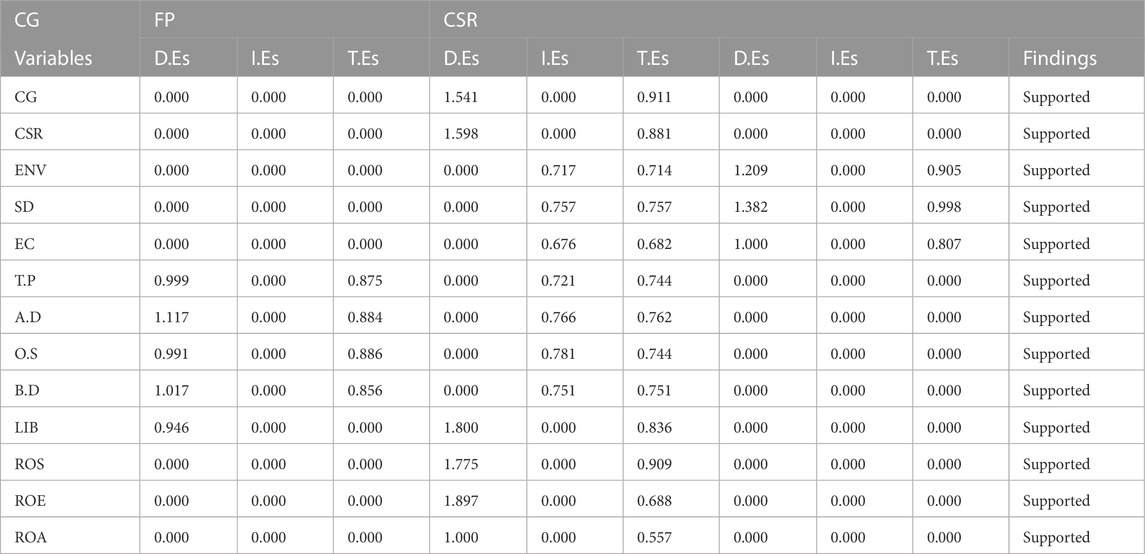

In Table 3 below, the role of CG as a mediator has been checked for the prediction of the direct effects (D.Es), indirect effects (I.Es), and total effects (T.Es). While based on the path model to examine the mediation effect, AMOS is used in this study. Similarly, there has been a comparison between the full mediation model and partial mediation model through the structural equation model (SEM). Similarly, direct paths from the independent variables were added to the dependent variable. Therefore, following the discussed procedure, the mediator variable is CG, and its direct, Indirect, and total effects have been specifically analyzed. The findings of the mediation effect are also specified in Table 3 in the last column. To sum up, there were two paths utilized in order to check the mediation effect of corporate governance between firm performances and CSR. The direction of the first path is from firms’ performance towards corporate governance. There were strong and positive significant mediating effects of corporate governance on firm performance with the value of 0.975*** for β. In other words, the role of CG is very visible in the determination of the firm’s performance of the sample firms while another link is between corporate governance and CSR. The β value stood at 0.986 *** which indicates the positive and significant effect of corporate governance involvement in the selected firms of the study. In terms of the influence of the variables of the study, the result shows the monitoring, controlling, andsupporting role of CG on CSR after the effect of FP in the next influential category. The result reveals a highly significant mediating effect of CG between FP and CSR in all of its dimensions. Furthermore, in the following Table 4, there has been a multiplier effect of CG as a mediator on both of the paths. While in order to support and implement CSR in the firms, the cumulative impact of CG has a double mediating legitimacy in the given variables of the study.

TABLE 3. The mediator, corporate governance, and its direct, indirect, and total effects.

TABLE 4. CG effect as mediator on FP and CSR.

Table 5 below indicates the coefficients and their outcome paths along with (β) values, standardized regression weights, and their R2 (explained variance) through which the SEM has been evaluated. The values of the standardized coefficient regression estimate values of the variables show the model fitness as the (R2) value stood at 0.890 or 89% and was significant at the given p-value. Similarly, the explanatory variable FP affects CSR with a β value of 0.901. The mediation effect of CG on CSR is 0.855 as a β value in the table below. Further, it is clear from the given outcome value in Table 5 that each of the indicators affected the mediator, and predicted variables of the current through the values of the β values. The predictor variable of the study, FP, has affected CSR as shown by the estimated coefficient in the model. The explanatory variable FP is affected by ROS with its 0.901 value of β estimate, ROA (β = 0.671), ROA (0.489), and Liability ratio of capital structure (0.345). As far as the role of CG as a mediator in the FP is concerned, the estimated factor β stood at 0.917. It is concluded that when the CSR determinants are changed by one unit, keeping other factors constant, the role of CG increases by one unit. Therefore, when the CG role increases, it also boosts the FP by the given estimated factor of 0.841 in terms of β value and it is significant at the specified p-value. Similarly, there is a noticeable effect of the positive and significant role of CG as a mediator on the CSR of the sample firms in the energy sector of the Shanghai stock exchange. When there is an increase in CG factors, there will also be a positive and significant increase in CSR assuming the other factors are constant. In simple words, one unit increase in CSR can be achieved through better involvement of CG, so CSR practice also improves by 0.855 when the estimated factor of β is significant at the stated p-value. It is concluded that the energy sector sample firms listed on the Shanghai stock exchange are highly affected by the FP as well as by the mediating role of CG. Similarly, FP is also considerably influenced.

TABLE 5. Structural (path) model analysis in light of standardized estimates regression.

Through the use of commonly used financial performance tools, such as total assets, total liabilities, total sales, and total capital as a collective investment, which shows the trend analysis growth path, the development of the sample firms has been examined and selected.

The company’s growth trend has been examined in connection with its strategic plan, and the aggregate growth trend analysis reveals an increase in the sample company’s total assets, sales, liabilities, and equity over the course of 7 years. The current study’s results revealed that the sample energy sector listed companies at the Shanghai Stock Exchange experienced an increase in FP appreciation to excellent CG mechanisms that captured stronger and stronger indicators. In light of this, we believe that accounting-based metrics, such as ROE, one of the performance metrics most frequently employed in corporate governance-related research and literature.

Unlike the previous studies on the same area of interest, this study explored how the liability of the sample firms is reasonable to manage because of the very high importance and demand for the products of the firms mentioned. In other words, there is little reliance on heavy debt financing in these firms. Therefore, CSR practices are a point of attraction which will also boost the sustainable FP of these firms as and create a thirst for more meaningful CG mechanism applications keeping in view the sustainability factors for long-term utility. Additionally, it is also observed, by comparing the previous findings in the developing economies, that developed nations are giving more attention and deploying larger resources to CSR practices in order to maintain sustainable FP, CG, and, ultimately, the CSR.

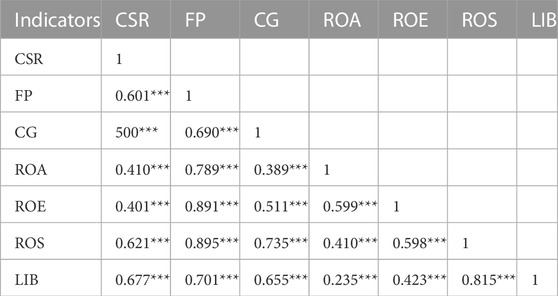

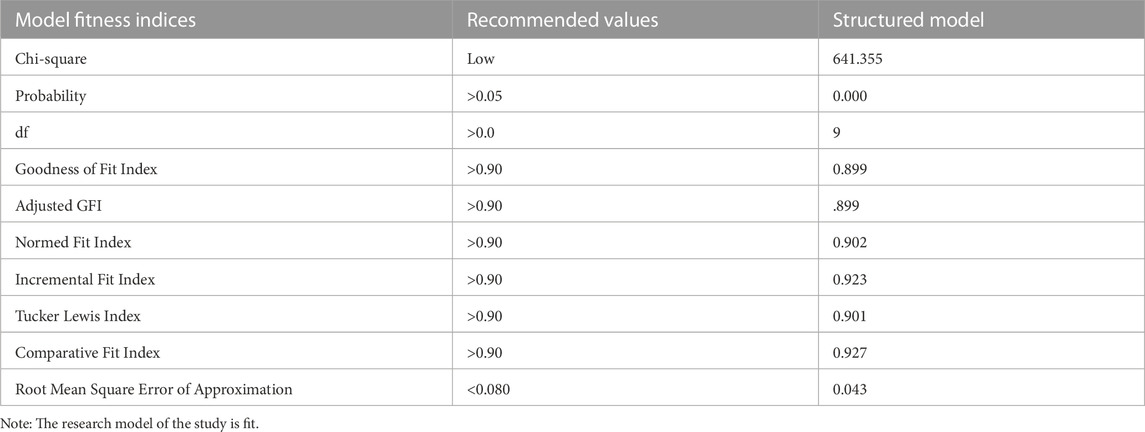

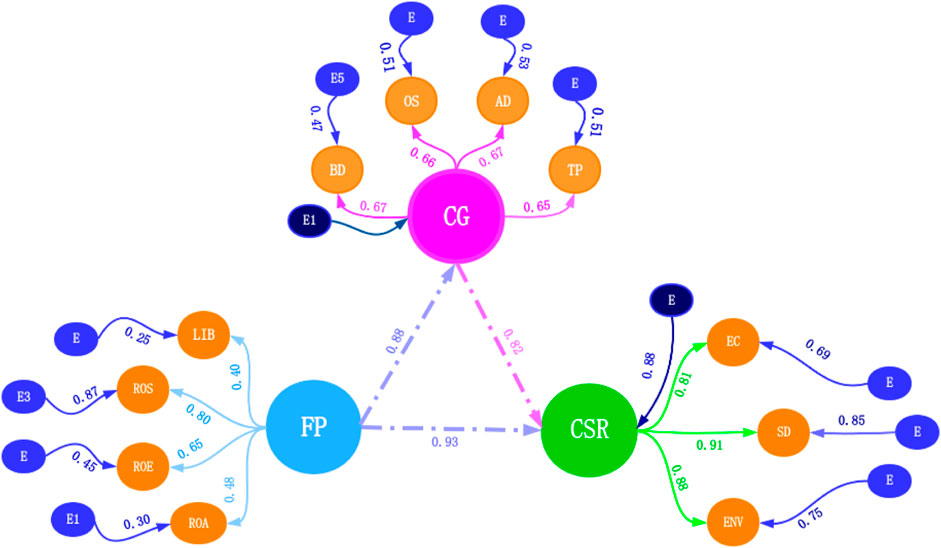

In the correlation matrix Table 6 above, it is observed that FP indicators (ROA, ROS, ROE, and LIB) have positive as well as significant effects on CG and CSR practices in the sample energy sector listed firms at the Shanghai stock exchange in the given sample period of study (2011–2020). It is concluded from the results that firms in developed economies are more sustainability conscious than firms in developing countries in terms of CG and CSR practices and the remaining 30% of the total capital is acquired from debt financing. Table 7 shows the fitness of the research model of the study. The estimated results show that the model was a good fit. Furthermore, it is also confirmed in the structural equation model analysis shown in Figure 2, that ROA, ROE, ROS, and debt-ratio affect firm performance of energy sector in our sample data. Due to this, the result of the path modeling analysis also shows that there is a positive as well as significant effect of FP on CSR practices in the sample firms with a β value of 0.93***.

TABLE 6. Correlation coefficient matrix of latent construct and ratio analysis.

TABLE 7. Summary of model fit indices.

FIGURE 2. Structure model on CSR with parameter estimates.

The results generated from the financial ratio analysis show that all its indicators have favorable outcomes that considerably contribute to the sample firms’ overall performance. It is observed from the 0.39 value of ROA that companies are more efficient in utilizing their total assets in order to generate more reasonable profit or income. Simply put, for every US Dollar of assets there is 39 cents of revenue generated by the firms. In the same way, another indicator of the financial ratios is the ROE which means how much return a firm generates on every Dollar in equity shares investment. This ratio also shows a strong position of the sample firms of the study, that is, ROE equals 0.69, which means that the firms are efficiently utilizing the investments of their shareholders by generating 69 cents for every dollar of equity investments. Furthermore, the next indicator under the umbrella of ratios analysis is the ROS which implies the efficiency of the firm to manage its operating expenses incurred in generating the sales revenues. Therefore, the ROS value stood at 0.52 which is also very good. It means that for every US Dollar in sales revenue, 52 cents remain after the deduction of operating expenses. In other words, these 52 cents out of 1 US Dollar sales revenue are the operating income of the sample firms.

The last and equally important indicator of the firm performance is the debt ratio which indicates the portion of total debts in the total capital utilized in the production and operations to produce goods or services. In this context, the debt ratio of the sample firms of the study is 0.30, that is out of every 1 US Dollar of the total capital, the sample firms raised 30 cents from the creditors. Therefore, the debt ratio is also very favorable, showing that out of 100% capital, the firms are relying 70% on equity financing and the remaining 30% of the total capital is acquired from debt financing.

As a whole, there is due attention given to the sustainability factor in terms of FP, CG, and CSR practices in the firms operating in the developed economies of the globe. This can be attributed to many factors like a well-established system, defined corporate rules and regulations, a more sophisticated education system to educate the young generation about sustainability factors, a collectivism approach which is created to improve the national economy and future favorable conditions for the upcoming generations, and willingness of the corporate sector to follow the rules specified by the government. In contrast, developing nations are following the developed nations in order to create long-term value in the form of sustainability in their corporate sectors. It is worth mentioning that, due to the abundance of resources, the developed nations of the world should provide a solid plan not only to safeguard their long-lived future but to cooperate and help the developing nations of the globe as well. Ultimately, we are all human beings and therefore, every human being has the right to leave a secured and prosperous future for all.

The long-term sustainability of enterprises is due to the backup provided by stakeholders in the form of resource supply. However, the stakeholders also expect those enterprises to provide a satisfactory level of value proposition. It is said that for the safe and long-term sustainability of a car, the skills of a driver are more important than the quality of that car. So, in the case of corporate matters too, the researchers have focused their attention on the key role of corporate governance in terms of various factors that jointly constitute a huge inter disciplinary coalition. There is an association between how a company governs and its effects on various aspects of the business ventures and a visible effect on how to survive in such a tough competitive environment. The concept of “Responsible Innovation” is proposed by the European Commission’s Horizon 2020 Framework Plan. The aim of Responsible innovation should not compromise on moral, social, ethical, and sustainable desirability; instead, the focus shall be given, in the first place, to the fulfillment of future needs via collective-based management which suggests that there should be cooperation between society and technological innovations. The concept of “balance” thought is included in responsible innovation and, therefore, it has been introduced in business management research and stands as a new management paradigm. Over the last few decades, corporate social responsibility (CSR) has been introduced, grown, and emerged as an excellent sustainable corporate strategy. There are various reasons behind the popularity and significance of CSR like governmental regulations, demand from consumers, and market conditions which consistently play a key role in the international economic slump.

Thus, the findings of previous studies are inconsistent; some outcomes seem reasonable, while many of them are contradicting one another and, therefore, there is a mismatch in their conclusions (Ying et al., 2021; Khan et al., 2023 and Jiafeng, 2023). Some studies have focused on data from a specific state/region of a country by using panel data while some have used survey data.

In light of the results and its relevant discussions, this study concludes that, as a whole, there is due attention given to the sustainability factor in terms of FP, CG, and CSR practices in the firms operating in the developed economies of the globe. This can be attributed to many factors like a well-established system, defined corporate rules and regulations, a more sophisticated education system to educate the young generation about sustainability factors, collectivism approach which is created to improve the national economy and future favorable conditions for the upcoming generations and willingness of the corporate sector to follow the rules specified by the government in a true letter and spirit. In the correlation matrix table above, it is observed that FP indicators (ROA, ROS, ROE, and LIB) have positive as well as significant effects on CG and CSR practices in the sample energy sector listed firms on the Shanghai stock exchange in the given sample period of study (2011–2020). It is concluded from the results that firms in the developed economies are more sustainability conscious than the developing countries’ firms in terms of CG and CSR practices. Therefore, this study has more valid results as compared to various previous studies (Ying et al., 2021). Furthermore, it is also confirmed in the structural equation model analysis shown in Figure 2, with the obtained values of βs for ROA (0.48), ROE (0.65), ROS (0.80), and debt-ratio (0.40) that considerably affects FP in the sample firms of the energy sector. This ratio also shows a strong position of the sample firms of the study, that is, ROE equals 0.69, which means s that the firms are efficiently utilizing the investments of their shareholders by generating 69 cents for every dollar of equity investments. Furthermore, the next indicator under the umbrella of ratio analysis is the ROS that implies the efficiency of the firms to manage their operating expenses that are incurred in generating the sales revenues. Therefore, ROS value stood at 0.52, which is also very good. It means that for every US Dollar in sales revenue, 52 cents remain after the deduction of operating expenses. In other words, these 52 cents out of 1 US Dollar sales revenue are the operating income of the sample firms. These results present a strong relationship among the variables as compared to the previous studies of (Ying et al., 2021) and (Khan et al., 2023). The policy implications of the study states that top management should give proper attention to the sustainability factor in terms of FP, CG, and CSR practices at firm level in developed and developing economies.

Every research study is limited within a specified scope because it is difficult to cover all aspects under one area of interest. This study is based on a sample taken from the energy sector firms of the Shanghai Stock Exchange for a period of 10 years. Therefore, future studies can be conducted by considering more sectors among the listed sectors of the Shanghai stock exchange. Similarly, the data period may also be extended to more than the sample period of this study which will increase the further validity of the future results and generalize these results in a more efficient way.

The proposed directions of this study for future expected research include considering other advanced economies of the globe which will multiply the worth of the present study. Furthermore, apart from energy sector, which was the focus of the current study, one could examine other sectors of the economy of China while other variables could also be included.

The significance of the present study is valuable because of the large sample size and longer period of time as compared to the previous studies in the same area of expertise. Therefore, the study contributes a considerable amount of quality literature in order to benefit the researchers, students, policymakers, board of directors, and other stakeholders to make better decisions for a better and safe future (Gu, 2023).

Publicly available datasets were analyzed in this study. This data can be found here: From Shanghai Stock Exchange.

All authors listed have made a substantial, direct, and intellectual contribution to the work and approved it for publication.

The authors acknowledge the support of the editorial team and reviewers for their insightful suggestions during the review process. The authors also acknowledge the financial support of the Information Research Institute, Qilu University of Technology (Shandong Academy of Sciences), Jinan, People’s Republic of China.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Aebi, V., Sabato, G., and Schmid, M. (2012). Risk management, corporate governance, and bank performance in the financial crisis. J. Bank. Finance 36 (12), 3213–3226. doi:10.1016/j.jbankfin.2011.10.020

Ahmed, E., and Hamdan, A. (2015). The impact of corporate governance on firm performance: Evidence from Bahrain bourse. Int. Manag. Rev. 11, 21.

Akomeah, E., Bentil, P., and Musah, A. (2018). The impact of capital structure decisions on firm performance: The case of listed NonFinancial institutions in Ghana. Int. J. Acad. Res. Acc. Financ. Manag. Sci. 8, 1–15. doi:10.6007/ijarafms/v8-i4/5050

Akram, F., Abrar-Ul-Haq, M., and Raza, S. (2018). A role of corporate governance and firm’s environmental performance: A moderating role of institutional regulations. Int. J. Manag. Stud. 25, 19–37.

Al-Matari, E. M., Al-Swidi, A. K., and Fadzil, F. H. B. (2014). The measurements of firm performance’s dimensions. Asian J. Financ. Acc. 6, 24. doi:10.5296/ajfa.v6i1.4761

Alamgir, M., and Alam, M. (2016). The mediating role of corporate governance and corporate image on the CSR-FP link. Evidence from a developing country. J. Gen. Manag. 41, 33–51. doi:10.1177/030630701604100303

Alexander, G. J., and Buchholz, R. A. (1978). Corporate social responsibility and stock market performance. Acad. Manag. J. 21, 479–486. doi:10.5465/255728

Ali, R., Sial, M. S., Brugni, T. V., Hwang, J., Khuong, N. V., and Khanh, T. H. T. (2020). Does CSR moderate the relationship between corporate governance and Chinese firm’s financial performance? Evidence from the Shanghai stock exchange (SSE) firms. Sustainability 12, 149. doi:10.3390/su12010149

Alsurayyi, A. I., and Alsughayer, S. A. (2021). The relationship between corporate governance and firm performance: The effect of internal audit and enterprise resource planning (ERP). Open J. Acc. 10, 56–76. doi:10.4236/ojacct.2021.102006

Ayalew, B. M. (2018). Corporate social responsibility practices, determinants and challenges: Theoretical and empirical lesson for effective and successful engagement. J. Investig. Manag. 7, 157–165.

Bacon, D. R., Sauer, P. L., and Young, M. (2015). Composite reliability in structural equations modeling. J. Educ. Psychol. Meas. 55, 394–406. doi:10.1177/0013164495055003003

Barney, J. B. (1986). Strategic factor markets: Expectations, luck, and business strategy. Manag. Sci. 32, 1231–1241. doi:10.1287/mnsc.32.10.1231

Bhagat, S., and Bolton, B. (2008). Corporate governance and firm performance. J. Corp. finance 14 (3), 257–273. doi:10.1016/j.jcorpfin.2008.03.006

Bimir, M. N. (2016). Corporate social responsibility learning in the Ethiopian leather and footwear industry. Int. J. Sci. Eng. Res. 7, 224–236.

Carrasco, P. G., Saorin, E. G., and Osma, B. G. (2016). The illusion of CSR: Drawing the line between core and supplementary CSR. Sustain. Acc. Manag. Policy J. 7, 125–151. doi:10.1108/sampj-12-2014-0083

Carroll, A. B. (2015). A history of corporate social responsibility: Concepts and practices. J. Corp. Soc. Responsib. 1, 19–45.

Carroll, A. B., and Shabana, K. M. (2010). The business case for corporate social responsibility: A review of concepts, research and practice. Int. J. Manag. Rev. 12, 85–105. doi:10.1111/j.1468-2370.2009.00275.x

Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horiz. 34, 39–48. doi:10.1016/0007-6813(91)90005-g

Chan, L. L., and Idris, N. (2017). Validity and reliability of the instrument using exploratory factor analysis and Cronbach’s alpha. Int. J. Acad. Res. Bus. Soc. Sci. 7, 400–410. doi:10.6007/ijarbss/v7-i10/3387

Cherian, J., Umar, M., Thu, P., Nguyen-Trang, T., Sial, M., and Khuong, N. (2019). Does corporate social responsibility affect the financial performance of the manufacturing sector? Evidence from an emerging economy. Sustainability 11, 1182. doi:10.3390/su11041182

Cho, E., and Kim, S. (2014). Cronbach’s coefficient alpha: Well known but poorly understood. Organ. Res. Methods 18, 207–230. doi:10.1177/1094428114555994

Chowdhury, R. H., Choi, S., Ennis, S., and Chung, D. (2019). Which dimension of corporate social responsibility is a value driver in the oil and gas industry? Can. J. Adm. Sci. 36, 260–272. doi:10.1002/cjas.1492

Crifo, P., and Reberioux, A. (2016). Corporate governance and corporate social responsibility: A typology of oecd countries. J. Gov. Regul. 5, 14–27. doi:10.22495/jgr_v5_i2_p2

Crifo, P., and Vanina, D. F. (2015). The economics of corporate social responsibility: A firm-level perspective survey. J. Econ. Surv. 29, 112–130. doi:10.1111/joes.12055

Dartey-Baah, K., and Amponsah-Tawiah, K. (2011). Exploring the limits of western corporate social responsibility theories in africa. Int. J. Bus. Soc. Sci. 2, 126–137.

Del Miras-Rodríguez, M. M., Martínez-Martínez, D., and Escobar-Pérez, B. (2018). Which corporate governance mechanisms drive CSR disclosure practices in emerging countries? Sustainability 11, 61. doi:10.3390/su11010061

El-Garaihy, W. H., Mobarak, A. K. M., and Albahussain, S. A. (2014). Measuring the impact of corporate social responsibility practices on competitive advantage: A mediation role of reputation and customer satisfaction. Int. J. Bus. Manag. 9, 109–124. doi:10.5539/ijbm.v9n5p109

European Commission, (2001). Green paper—promoting a European framework for CSR; COM. Brussels, Belgium: European Commission, 366.

Eyasu, A. M., and Endale, M. (2020). Corporate social responsibility in agro-processing and garment industry: Evidence from Ethiopia. Cogent Bus. Manag. 7, 1720945. doi:10.1080/23311975.2020.1720945

Fallatah, Y., and Dickins, D. (2012). Corporate governance and firm performance and value in Saudi arabia. Afr. J. Bus. Manag. 6, 10025–10034.

Farooq, S. U., Ullah, S., and Kimani, D. (2015). The relationship between corporate governance and corporate social responsibility (CSR) disclosure: Evidence from the USA. Abasyn J. Soc. Sci. 8, 197–212.

Gereziher, B., and Shiferaw, Y. (2020). Corporate social responsibility practice of multinational companies in Ethiopia: A case study of heineken brewery, S.C. Br. J. Arts Humanit. 2, 36–55. doi:10.34104/bjah.020036055

Grant, C., and Osanloo, A. (2015). Understanding, selecting, and integrating a theoretical framework in dissertation research: Creating the blueprint for your house. Adm. Issues J. Educ. Pract. Res. 4, 12–26. doi:10.5929/2014.4.2.9

Gu, J. (2023). Firm performance and corporate social responsibility: Spatial context and effect mechanism. SAGE Open 13 (1), 215824402311521. doi:10.1177/21582440231152123

Henseler, J., Ringle, C. M., and Sarstedt, M. (2015). A New criterion for assessing discriminant validity in variance-based structural equation modeling. J. Acad. Mark. Sci. 43, 115–135. doi:10.1007/s11747-014-0403-8

Hermuningsih, S., Kusuma, H., and Cahyarifida, R. A. (2020). Corporate governance and firm performance: An empirical study from Indonesian manufacturing firms. J. Asian Financ. Econ. Bus. 7, 827–834. doi:10.13106/jafeb.2020.vol7.no11.827

Hirigoyen, G., and Poulain-Rehm, T. (2015). Relationships between corporate social responsibility and financial performance: What is the causality? J. Bus. Manag. 4, 18–43. doi:10.12735/jbm.v4i1p18

Hourneaux, F., Gabriel, M. L., Da, S., and Gallardo-Vázquez, D. A. (2018). Triple bottom line and sustainable performance measurement in industrial companies. Emerald 13, 1–18.

Hung, R. Y., Yang, B., Lien, B. Y., McLean, G. N., and Kuo, Y. M. (2010). Dynamic Capability: Impact of process alignment and organizational learning culture on performance. J. World Bus. 45, 285–294. doi:10.1016/j.jwb.2009.09.003

Imran, M. (2021). Company fundamentals as determinants of firm-level equity premiums: Evidence from an emerging economy. Panoeconomicus 68 (5), 681–697. doi:10.2298/pan180404006i

Javeed, S. A., and Lefen, L. (2019). An analysis of corporate social responsibility and firm performance with moderating effects of CEO power and ownership structure: A case study of the manufacturing sector of Pakistan. Sustainability 11, 248. doi:10.3390/su11010248

Jesus, M. F. (2017). Sustainability as an object of corporate social responsibility. Int. J. Archit. Technol. Sustain. 2, 13–23.

Kai, R., Kong, Y. S., Imran, M., and Bangash, A. K. (2022). The impact of the voluntary environmental agreements on green technology innovation: Evidence from the prefectural-level data in China. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.833724

Khan, I., Jia, M., Lei, X., Niu, R., Khan, J., and Tong, Z. (2023). Corporate social responsibility and firm performance. Total Qual. Manag. Bus. Excell. 34 (5-6), 672–691. doi:10.1080/14783363.2022.2092467

Khan, N. A. K., Ahmed, S., and Ali, M. (2012). Corporate social responsibility (CSR)—definition, concepts and scope (A review). Univers. J. Manag. Soc. Sci. 2, 41–52.

Kumar, R. (2011). Research methodology a step-by-step guide for beginners. New Delhi, India: SAGE Publications Ltd.

Lee, S., Seo, K., and Sharma, A. (2013). Corporate social responsibility and firm performance in the airline industry: The moderating role of oil prices. Tour. Manag. 38, 20–30. doi:10.1016/j.tourman.2013.02.002

Li, B., Li, R. Y. M., and Wareewanich, T. (2021). Factors influencing large real estate companies competitiveness: A sustainable development perspective. Land 10 (11), 1239. doi:10.3390/land10111239

Low, M. P. (2016). Corporate social responsibility and the evolution of internal corporate social responsibility in 21st century. Asian J. Soc. Sci. Manag. Stud. 3, 56–74. doi:10.20448/journal.500/2016.3.1/500.1.56.74

Lu, J., Imran, M., Haseeb, A., Saud, S., Wu, M., Siddiqui, F., et al. (2020). Nexus between financial development, FDI, globalization, energy consumption and environment: Evidence from BRI countries. Front. Energy Res. 9. doi:10.3389/fenrg.2021.707590

Mahrani, M., and Soewarno, N. (2018). The effect of good corporate governance mechanism and corporate social responsibility on financial performance with earnings management as mediating variable. Asian J. Acc. Res. 3, 41–60. doi:10.1108/ajar-06-2018-0008

Manning, B., Braam, G., and Reimsbach, D. (2019). Corporate governance and sustainable business conduct—E ffects of board monitoring effectiveness and stakeholder engagement on corporate sustainability performance and disclosure choices. Corp Soc Responsib Environ Manag. 26 (2), 351–366. doi:10.1002/csr.1687

Martinuzzi, A., Krumay, B., and Pisano, U. (2011). Focus CSR: The new communication of the EU commission on CSR and national CSR strategies and action plans. Eur. Sustain. Dev. Netw. 23, 103.

McWilliams, A., and Siegel, D. (2001). Corporate social responsibility: A theory of the firm perspective. Acad. Manag. Rev. 26, 117–127. doi:10.2307/259398

Miglani, S., Ahmed, K., and Henry, D. (2020). Corporate governance and turnaround: Evidence from Australia. Aust. J. Manag. 45 (4), 549–578. doi:10.1177/0312896220902225

Mortazavi, H., Pirmouradi, N., Soltaninejad, A., and Pormosa, H. (2013). Corporate social responsibility (CSR). J. Behav. Sci. Asia 4, 63–77.

Muriithi, S. G., Walters, B. A., McCumber, W. R., and Robles, L. R. (2021). Managerial entrenchment and corporate social responsibility engagement: The role of economic policy uncertainty. J. Manag. Gov. 27, 621–640. doi:10.1007/s10997-021-09569-7

Oladeji, S. W., and Agbesanya, E. O. (2019). Corporate governance indicators and their effects on firms’ value. Int. J. Res. Innov. Soc. Sci. 3, 545–552.

Otero-Gonzalez, L., Dur, P., Rodriguez-Gil, L., and Lado-Sestayo, R. (2021). Does company’s profitability influence the level of CSR development? Sustainability 13, 3304. doi:10.3390/su13063304

Palinkas, L. A., Horwitz, S. M., Green, C. A., Wisdom, J. P., Duan, N., and Hoagwood, K. (2015). Purposeful sampling for qualitative data collection and analysis in mixed method implementation research. Adm. Policy Ment. Health 42, 533–544. doi:10.1007/s10488-013-0528-y

Park, B., and Ghauri, P. N. (2015). Determinants influencing CSR practices in small and medium sized mne subsidiaries: A stakeholder perspective. J. World Bus. 50, 192–204. doi:10.1016/j.jwb.2014.04.007

Poudel, R. L. (2015). Relationship between corporate governance and corporate social responsibility: Evidence from Nepalese commercial banks. J. Nepal. Bus. Stud. 9, 137–144. doi:10.3126/jnbs.v9i1.14603

Sen, R. (2017). Corporate social responsibility with socio-economic development. Int. J. Manag. IT Eng. 7, 119–124.

Sánchez-Infante Hernández, J. P., Yañez-Araque, B., and Moreno-García, J. (2020). Moderating effect of firm size on the influence of corporate social responsibility in the economic performance of micro-small- and medium-sized enterprises. Technol. Forecast. Soc. Chang. 151, 119774. doi:10.1016/j.techfore.2019.119774

Selcuk, E. A., and Kiymaz, H. (2017). Corporate social responsibility and firm performance: Evidence from an emerging market. Acc. Financ. Res. 6, 42–51. doi:10.5430/afr.v6n4p42

Shahab, Y., Ntim, C. G., Chen, Y., Ullah, F., Li, H. X., and Ye, Z. (2020). Chief executive officer attributes, sustainable performance, environmental performance, and environmental reporting: New insights from upper echelons perspective. Bus. Strategy Environ. 29 (1), 1–16. doi:10.1002/bse.2345

Sheldon, O. (1923). The philosophy of management: Pitman’s business handbooks. London, UK: Sir Isaac Pitman And Sons, Ltd, 1–336.

Sial, M. S., Zheng, C., Khuong, N. V., Khan, T., and Usman, M. (2018). Does firm performance influence corporate social responsibility reporting of Chinese listed companies? Sustainability 10, 2217. doi:10.3390/su10072217

Smith, A. D. (2010). Growth of corporate social responsibility as a sustainable business strategy in difficult financial times. Int. J. Sustain.Econ. 2, 59–79. doi:10.1504/ijse.2010.029941

Sobel, M. E. (1982). “Asymptotic confidence intervals for indirect effects in structural equation models,” in Sociological methodology. Editor S. Leinhardt (Washington, DC, USA: American Sociological Association), 290–312.

Tiret, (2020). Five years TIRET corporate business enterprises strategic report. The growth path of TIRET corporate. Available online: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/320239/ipostrategy.pdf.

Wang, Y. G., Hsu, W. H. L., and Chang, K. W. (2012). The impact of fulfilling corporate social responsibility on firm performance—a stakeholder’s approach. Int. J. Model. Simul. 32, 206–215. doi:10.2316/journal.205.2012.3.205-5731

Wei, A., Peng, C., Huang, H., and Yeh, S. (2020). Effects of corporate social responsibility on firm performance: Does customer satisfaction matter? Sustainability. 12, 7545. doi:10.3390/su12187545

Wu, W., Liu, Y., Chin, T., and Zhu, W. (2018). Will green CSR enhance innovation? A perspective of public visibility and firm transparency. Int. J. Environ. Res. Public Health 15, 268. doi:10.3390/ijerph15020268

Yang, M., Bento, P., and Akbar, A. (2019). Does CSR influence firm performance indicators? Evidence from Chinese pharmaceutical enterprises. Sustainability 11, 5656. doi:10.3390/su11205656

Ying, M., Tikuye, G. A., and Shan, H. (2021). Impacts of firm performance on corporate social responsibility practices: The mediation role of corporate governance in Ethiopia corporate business. Sustainability 13 (17), 9717. doi:10.3390/su13179717

Yuen, K. F., Thai, V. V., and Wong, Y. D. (2018). An investigation of shippers’ satisfaction and behaviour towards corporate social responsibility in maritime transport. Transp. Res. Part A 116, 275–289. doi:10.1016/j.tra.2018.06.027

Zeng, L., Li, R. Y. M., and Huang, X. (2021). Sustainable Mountain-based health and wellness tourist destinations: The interrelationships between tourists’ satisfaction, behavioral intentions, and competitiveness. Sustainability 13 (23), 13314. doi:10.3390/su132313314

Zhang, T. J., Zhou, J. Y., Wang, M., Ren, K., Imran, M., and Wang, R. (2022). Cultivation mechanism of green technology innovation in manufacturing enterprises under environmental regulations in China. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.926896

Zheng, Q., Luo, Y., and Maksimov, V. (2015). Achieving legitimacy through corporate social responsibility: The case of emerging economy firms. J. World Bus. 50, 389–403. doi:10.1016/j.jwb.2014.05.001

Keywords: sustainability, corporate governance, firm performance, CSR, energy sector, shanghai stock exchange

Citation: Imran M, Liu X, Arif M, Rahman SU, Manan F, Khattak SR and Wang R (2023) Sustainable corporate governance mediates between firm performance and corporate social responsibility using structural equation modelling. Front. Energy Res. 11:1121853. doi: 10.3389/fenrg.2023.1121853

Received: 12 December 2022; Accepted: 07 July 2023;

Published: 26 July 2023.

Edited by:

Otilia Manta, Romanian Academy, RomaniaReviewed by:

Nandita Mishra, Linköping University, SwedenCopyright © 2023 Imran, Liu, Arif, Rahman, Manan, Khattak and Wang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Muhammad Imran, aW1yYW5Ac2Rhcy5vcmc=; Shams Ur Rahman, c2F5ZWRzaGFtc0BhdXAuZWR1LnBr

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.