94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Energy Res., 04 January 2023

Sec. Carbon Capture, Utilization and Storage

Volume 10 - 2022 | https://doi.org/10.3389/fenrg.2022.1087526

This article is part of the Research TopicThe Impact of Global Industrial Manufacturing and the Development Strategy of New Energy and New Technologies under the Action of Carbon ReductionView all 10 articles

Jie Wan1

Jie Wan1 Baochun Yu2*

Baochun Yu2*The concept of low-carbon economic development has led to changes in the business environment and financial environment of enterprises, leading to increased financial risks faced by enterprises. How to help enterprises better warn, prevent and control financial risks from the perspective of low-carbon economy has become a hot issue worth studying. Based on this, this paper is based on the perspective of low carbon economy, on the basis of analyzing the financing risk, investment risk, capital operation risk and growth risk faced by enterprises under the requirements of low carbon economy development. A set of financial risk management framework with clear hierarchy and strict vertical logic has been constructed. Ten financial early-warning indicators are constructed from four aspects. The risk prediction model of the indicator system is established using the research method of BPNN (Back Propagation Neural Network). The model is trained and simulated through the MATLAB neural network toolbox. After 10 indicators passed Bartlett’s correlation test, the BPNN financial early warning model was programmed using MATLAB software. The accuracy rate was 84.3%. The neural network training results show that when the layer node is 8, the best correct recognition rate can be obtained. Incorporate “low carbon” into the financial risk early warning indicator system that meets the requirements of low carbon economic development in the design of enterprise financial risk early warning indicators. This paper is expected to provide reference and reference for low-carbon economy enterprises to deal with financial risks under the new situation.

The core feature of developing a low-carbon economy is low carbon emissions. The so-called low carbon economy is an economic model based on low energy consumption, low pollution and low emissions, which corresponds to the high carbon economy characterized by high energy consumption, high pollution and high emissions. The essence of low carbon economy is to maintain economic and social development while realizing efficient utilization of resources and low-carbon or carbon free development of energy. Under the advocacy of green environmental protection and low-carbon development, all economic entities around the world actively assume environmental responsibility to promote low-carbon development. The financial market plays an important role in promoting the transition to a low-carbon economy. Low carbon green development will play a key role in helping the financial market in the process of transition to a low carbon economy (Louche et al., 2019). Under the impact of “economic globalization”, the market competition is intensifying, and enterprises are facing enormous pressure for survival and development. Among them, there are many cases of mismanagement caused by the financial crisis, which directly put these companies in trouble, or even led to their bankruptcy. Therefore, it is very practical to establish a scientific data model to analyze and forecast the financial data of enterprises. It can not only monitor the financial situation of enterprises in real time, but also play an effective role in financial early warning (Kuang et al., 2022). Several indicators and single variable ratios can be used to measure the robustness reflected in the company’s balance sheet (leverage, profitability, liquidity ratio, etc.). However, each indicator cannot measure the overall financial risk or financial distress level of a company separately (Colak, 2021). The combination of quantitative financial indicators with macroeconomic variables, industry factors and corporate non-financial standards can be used for robust and balanced risk analysis. Based on enterprise risk management (ERM) theory, it can be used as an important aspect of risk management to analyze the possibility of company failure (Tan et al., 2022). In a normal economic environment, the main predictor of financial failure is to distinguish between healthy and failed SMEs. Autonomous ratio, interest and sales, asset turnover, days of accounts receivable and period of accounts payable are variables that increase the probability of financial failure, while repayment ability and return on assets reduce the probability of failure (Zizi et al., 2020). The transition to a low-carbon economy will lead to large-scale structural changes. Some industries will have to expand their relative economic weight, while others, especially those directly related to fossil fuel production and consumption, will have to decline. This systemic change may have a significant impact on the stability of the financial system, including sudden asset revaluation, debt default and foam in emerging industries (Semieniuk et al., 2021). Traditional machine learning needs data representing feature target relationship, and relies on the development, maintenance and modification of handmade features, which are usually costly. Therefore, modeling highly variable heterogeneous patterns is a challenge. Deep learning is expected to remedy. The hierarchical and distributed representation of data is learned automatically, which reveals the generation features that determine the target, avoids artificial feature engineering, and is more robust to changes (Kim et al., 2020). The SEM model results show that risk management and tenure of CEO have a significant positive impact on financial performance and corporate capital. Through risk management, CEO duality and board size have a significant positive impact on financial performance (Hamid and Purbawangsa, 2022). We will actively fulfill our social responsibilities by establishing a low-carbon and environment-friendly business model, and build the green core competitiveness of enterprises.

Financing risk analysis of enterprises from the perspective of low-carbon economy financing risk refers to the lack of sufficient cash flow to pay the principal and interest, which makes enterprises suffer losses. During the financial crisis, the prediction ability of all traditional financial distress prediction models will decline. Therefore, it is necessary to develop a model by identifying variables that have a greater impact on the financial distress of companies operating in developed and developing markets (Ashraf et al., 2019). From the perspective of low-carbon economy, the impact on corporate financing risk is mainly manifested in two aspects: on the one hand, in order to respond to the requirements of national environmental protection policies, enterprises must update or even discard traditional high energy consumption and high pollution equipment or technologies. Traditional econometric models in economic forecasting mainly have the problem of understanding the model and using deviation. At present, there are many estimation methods in econometric modeling, especially under the guidance of machine learning ideas, new AI research has obtained more estimation methods. However, most of the errors caused by these algorithms and random interference errors are uncontrollable. The use and purchase of new environmental protection equipment forced the total debt of enterprises to increase, and the increase in the amount of financing naturally increased the risk and pressure of enterprise debt repayment. In order to detect and deal with the systematic risk of the increasing amount of data generated in financial markets and systems, many researchers have increasingly adopted machine learning methods. Machine learning methods are used to study the outbreak and contagion mechanism of systemic risks in financial networks and improve the supervision of current financial markets and industries (Kou et al., 2019). On the other hand, corporate debt is mainly used for energy-saving and environmental protection equipment or technology research and development, which cannot directly improve the economic benefits of enterprises. It also increases the operating costs of enterprises. Force the fund supplier to raise the enterprise financing threshold or financing cost under the influence of green credit. This also increases the constraints and difficulties of enterprise financing. To sum up, the environmental requirements of low-carbon economy on enterprises have increased the pressure on enterprises to raise funds and financial burden. The principle of financial risk control of small and medium-sized enterprises needs to conform to the general objective of the enterprise. The general objective of an enterprise is the starting point and destination of all business activities of the enterprise. The principle of combining local risk with overall risk prevention and control. The business results of an enterprise are the result of a number of interrelated business activities. Therefore, under the original financing risk management, enterprises should also focus on indicators such as carbon asset liability ratio and carbon current liability ratio, and timely reveal the financial risks related to carbon assets and liabilities. Establish a financial risk monitoring and prediction index system. It has a standardized, comprehensive, sensitive, complementary and operable financial risk monitoring and early warning indicator system. There should also be indicators reflecting changes in the financial system and the external environment of the region. Some financial relative quantity estimation indicators closely related to economic operation and reflecting changes in the financial system should be set.

Because the neural network method can enable the model to have the self-learning ability with the changing complex environment, the BP neural network model is widely used to make the enterprise financial dynamic early warning possible. The basic idea of establishing the financial crisis early warning model with BP neural network is to take the financial evaluation index as the input value, and first give a weight. The output value is transferred to the output value through the hidden layer, and the output value after the function operation is compared with the expected value. If the error is large, the error will return along the original path in reverse, and the weight of each layer node will be modified for iterative calculation. After each operation, the weight distribution of the sample data is updated according to the error structure. After several iterations. When the error accuracy requirements are met, a group of optimal weights will be obtained, which are the parameters of the prediction model. In this paper, BP neural network is used as the financial early warning model, and the improved indicators are used as input variables. Compared with the traditional financial indicators as input variables, the low error rate shows that the improved input variables are more effective.

This paper first analyzes the types of enterprise risks, and then constructs an enterprise early warning model based on the basic principles of BPNN. Secondly, it points out the advantages of using BPNN to take advantage of enterprise financial risk early warning. The author believes that the biggest feature of early warning is pre control and quantitative management, and from the perspective of quantitative management, enterprise risk is more quantified from the perspective of financial risk. The enterprise dynamically monitors the important factors that affect the enterprise’s finance, makes statistical analysis of financial data, and through data statistics and analysis, reasonably and scientifically evaluates the company’s financial situation, and timely reflects the risks found. It can quickly respond to the operating conditions of the enterprise, especially the hidden risks of the enterprise. It is helpful for enterprise managers to allocate resources and analyze the causes of enterprise risks in combination with enterprise financial data. According to the early warning indicator system, obtain relevant data from the company’s external and enterprise information systems. The data are processed and condensed into independent principal component factors, which are used as input values of BPNN, and then used for early warning. Finally, according to the early warning results, send an alarm, return it to the enterprise information system, link it with the management procedures, analyze the reasons of the financial crisis, and propose control strategies for the financial crisis.

The contributions of this research and innovation are as follows:

1 The definition of rating results can reflect the financial situation of the institution more comprehensively and truly, and can improve the accuracy of the early warning model. Avoid blind low-carbon investment and reduce the economic benefits of enterprises.

2 Collect data in various ways and verify each other. The lost data shall be processed at different levels to ensure that the data can be mutually verified, so as to minimize information distortion.

3 Include non-financial indicators closely related to the financial status of green low-carbon enterprises into the selection range. So that the indicator system can more accurately reflect the actual financial situation of enterprises. It effectively warns against the investment risks brought by blind low-carbon investment.

This article is divided into six sections from the organizational structure.

The first section is the introduction. Firstly, it introduces the research background and significance of financial risk research. Secondly, it introduces the research status, the organizational structure and main content of this paper. It summarizes the research results from the perspective of financial early warning, and then puts forward the innovation in this research. The second section mainly introduce the research on financial management in various countries and the existing deficiencies. The third section introduces the types of enterprise financial risks and the functions of early warning system in detail, and the basic process of the financial early warning model based on BPNN. The fourth section introduces the algorithm. The fifth section is application of model design. The sixth section is the conclusion, which summarizes the results of the full text.

Traditional investment risk refers to the uncertainty of future investment income in the process of investment. The possibility of making enterprises suffer financial losses. From the perspective of low-carbon economy, enterprise investment risk refers to the transformation of enterprises from “high carbon” to “low carbon”. The cost of investment reconstruction or re purchase of operating equipment or technology is greater than the economic benefits of low-carbon investment in the future. Due to the large amount of operating funds required for the purchase of low-carbon equipment or newly developed environmental protection technologies by enterprises. And as a fixed asset or intangible asset, it needs to increase the economic benefits of the enterprise through value transfer for a long time in the future. Therefore, enterprises will carry out feasibility demonstration before upgrading or purchasing low-carbon equipment or technology, so as to avoid blind low-carbon investment to reduce the economic benefits of enterprises. That is to evaluate and calculate the initial cost of low-carbon investment and the economic benefits it will bring to the enterprise in the future. In order to effectively warn the investment risks arising from blind low-carbon investment, enterprises need to carry out targeted management of carbon investment under the original investment risk management. The hidden carbon investment risks of enterprises are revealed by measuring the economic benefits and cost rate of carbon investment in the future. The emergence of financial crisis is a gradual process and the result of deterioration of a series of factors. The reasons are divided into two categories: internal and external, namely, systematic risk and unsystematic risk. It is a common risk that changes in external risk factors of the company cause the uncertainty of the entire financial environment, thus affecting the financial operation of all companies in the whole society. In nature, systematic risk is environmental risk. The main factors that cause systematic risk are economic environment, legal environment and financial environment. The economic environment mainly includes: Economic cycle, economic development level and macroeconomic policies. The legal environment mainly includes: organizational form, relevant provisions of corporate governance and tax regulations; The financial environment is the most important external environmental influence factor of the company. At present, most models generally conduct financial early warning based on single type features, lacking early warning analysis based on multi type features. The accuracy and robustness of early warning of models also need to be further improved. On the premise that financial indicators and non-financial indicators are used to construct multiple types of financial features, Xuefeng et al. (2022) integrates multiple CART trees to construct CFW Boost by combining the causal relationship of features. It is found that CFW Boost has higher accuracy and more stable early warning performance than other models. The demonstration conforms to the market law, which can provide useful reference for enterprises and market supervision departments. Zeng analyzed the traditional financial risk early warning model based on accounting information. Based on this, an enterprise risk early warning model is proposed from the perspective of cash flow, and a financial risk early warning indicator system is established. After preprocessing, the data is input into the model according to the type of financial risk early warning indicators to obtain the company’s financial risk prediction results (Zeng, 2022). The concept of low-carbon development involves several interrelated tasks: improving energy efficiency, using renewable energy, etc. Kapitonov used statistical analysis, mathematical modeling and standard estimation methods to analyze the most important factors of development. It is the first time to put forward the sustainable development structure of energy security (Kapitonov, 2021). With the intensification of competition among enterprises, investors and enterprises pay more and more attention to the role of financial crisis early warning in enterprise management. Shang et al. (2021) selected multiple financial indicators based on big data mining of the Internet of Things. It is found that the rules among all financial indicators select more representative financial risk indicators. Then, FCM (fuzzy clustering method), parallel rules and parallel mining algorithm are used to determine frequent fuzzy option sets, so as to obtain fuzzy association rules satisfying the minimum fuzzy credibility. The financial risk of listed companies is a problem that needs attention. The financial crisis of e-commerce companies is a complex and gradual process, and its unique reasons may be many. E-commerce companies are facing financial risks or difficulties, and bankruptcy and liquidation are also increasing. Cao et al. (2022) studied from the perspective of establishing a financial early warning model based on deep learning and building an early warning mechanism for financial risks of e-commerce companies, and analyzed and predicted the financial risks of listed companies. Through the construction of the financial security early warning system, crisis signals can be diagnosed as early as possible, and crisis signals can be timely and effectively prevented and resolved. The traditional financial risk assessment is inaccurate, and the adaptive assessment ability is low. To solve this problem, Kang proposed a financial risk assessment model based on big data. The adaptive fuzzy weighted control method is used to fuse the information of financial risk assessment data and big data classification, and the asset return control and innovation assessment model are used to carry out linear programming and square fitting for financial risk. Based on the intervention factors of financial market participants, a quantitative regression analysis was conducted. According to the economic game theory, we have conducted big data analysis and prediction on financial risk assessment through regression analysis (Kang, 2019). The SME sector plays a crucial role in promoting economic growth in emerging countries. Buchdadi et al. (2020) tested the determinants of SME performance, namely the financial literacy of managers. Use financial product access and financial risk attitude as intermediary variables. Such studies use quantitative methods and use structural equation modeling (SEM) to analyze data. Through multiple regression analysis, Valaskova et al. (2018) determined significant predictive factors under specific economic environment conditions to estimate the prosperity and profitability of enterprises. The results obtained in the study are very important for the company itself, as well as its business partners, suppliers and creditors, to eliminate financial and other corporate risks related to the company’s unhealthy or adverse financial situation. He and Chen aims to study the application of the construction of the early warning model of the financing and financial risks of animal breeding enterprises in the economic transition period, and is conducive to the early warning of the financial risks of the animal breeding industry in this country in the economic transition period. This experimental study shows that building a financial risk early warning model can make the financing of animal breeding companies more clearly reflected in the economic transition period, and improve the financing probability of enterprises (He and Chen, 2020). Du and Shu proposed a credit scoring model based on deep learning network to solve the systemic risk problem caused by the lack of credit scoring in the existing financial market. Its purpose is to effectively manage the financial market and reduce the risk of financial enterprises. The bionic optimization algorithm is introduced, and an integrated deep learning model is proposed. Finally, a financial credit risk management system using integrated deep learning model is proposed (Du and Shu, 2022).

From the perspective of low-carbon economy, the growth risk of enterprises mainly refers to that the continuous growth of carbon investment of enterprises fails to effectively promote the growth of economic benefits of enterprises. That is, the growth rate of carbon investment is greater than the growth rate of enterprise economic benefits. This risk reveals that the enterprise carbon investment fails to give full play to its benefits, and there are blind investment and waste of investment. From the current research results, the selection of early warning indicators and early warning theory are still not perfect. Moreover, at present, there are few classified models for the same industry in China. Due to the different characteristics among industries, the factors affecting the formation of financial crisis are also different. Therefore, we need to design and establish a financial management model from a new perspective, and use new methods and means to improve the rationality and accuracy of financial management. For example, the combination of statistical methods and computer software, and the combination of statistical models and artificial neural networks can complement each other.

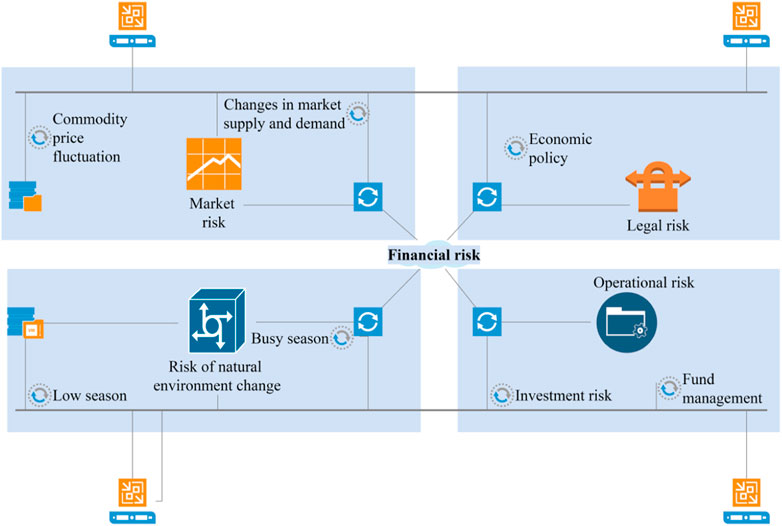

From the perspective of financial management, small and medium-sized enterprises can interpret the causes of bankruptcy or failure of small and medium-sized enterprises in two aspects: First, the operating income of enterprises is decreasing until losses occur. Secondly, the enterprise is short of funds and cannot effectively pay off the due debts. This is also the realistic background of the research on the financial risk prediction of SMEs. A sound and efficient financial early warning system can help small and medium-sized business owners to understand the changes in the business operation and financial situation, predict the risk of business failure, and leave time and space for small and medium-sized business owners to deal with this crisis. The integrity principle means that the indicators designed should cover all risk early warning financial indicators related to low-carbon economy. We should not only consider the actual economic indicators of enterprises, but also consider the resources that may be wasted in economic activities and the damage to the ecological environment after wasting resources. The principle of comparability means that the expected users can use these financial early warning indicators to compare with the financial information of other enterprises. That is, the indicator design cannot only consider the low-carbon economy. It is also necessary to consider the financial situation of the enterprise, so as to achieve the comparison with the financial statements when the low carbon indicators were not designed before. Business risk mainly refers to the possibility of adverse impact on the Company’s objectives due to production and operation reasons. For example, the supply risks caused by the changes in the political and economic conditions of the raw material supply place, the emergence of new materials and other factors. Production risks caused by unreasonable production organization. Sales risks caused by sales decision-making mistakes. If a company’s equity capital is insufficient, or it blindly pursues economies of scale and financial leverage benefits and becomes excessively indebted, it will increase its burden of repaying debt principal and interest. At the same time, the owners and creditors of the company will demand to increase the distribution of investment income and increase the interest rate due to the increased investment risk, which will further increase the financial burden. The solvency was further reduced. If the structure of the company’s assets or liabilities is unreasonable and the cash flow is poor, which causes difficulties in short-term debt repayment or turnover, it will also lead to financial crisis. Modern enterprises are faced with the various business pressures and risks, the inconsistency between owners and operators and asymmetric information. In addition, we are faced with the ever-changing market and the ever-changing international and environment. Coupled with a series of changes in politics, economy and society, risks are inevitable. Financial risk is the final embodiment of many risks. Early warning system can help enterprises to prevent crises and carry out strategic management. The main financial risks faced by the company can be splited into the following categories (Figure 1).

FIGURE 1. Types of corporate financial risks.

Enterprises may involve a variety of commodities. The prices of these commodities fluctuate with the fluctuation of market prices, and their uncertain changes make enterprises face the uncertainty of losses.

China’s macro-economic policies often change, and the pressure of inflation makes the price rise, the project cost increase, and also brings risks to the company’s operation. In addition, the relevant regulations formulated by state institutions or industry organizations to regulate the financial behavior of enterprises and coordinate the financial relations between different financial entities will also implicate enterprises.

The company faced problems in planning and managing the operation of investment projects, which led to the return rate of investment funds being far lower than the borrowing rate, and even brought debt problems to institutions.

The nature is always in a kind of movement and change, which often has a certain impact on economic activities. Seasonal changes will produce “off season” and “peak season” of commodity sales, while natural disasters often have a destructive impact on the normal operation of enterprises, which will ultimately be reflected in the financial results of enterprises.

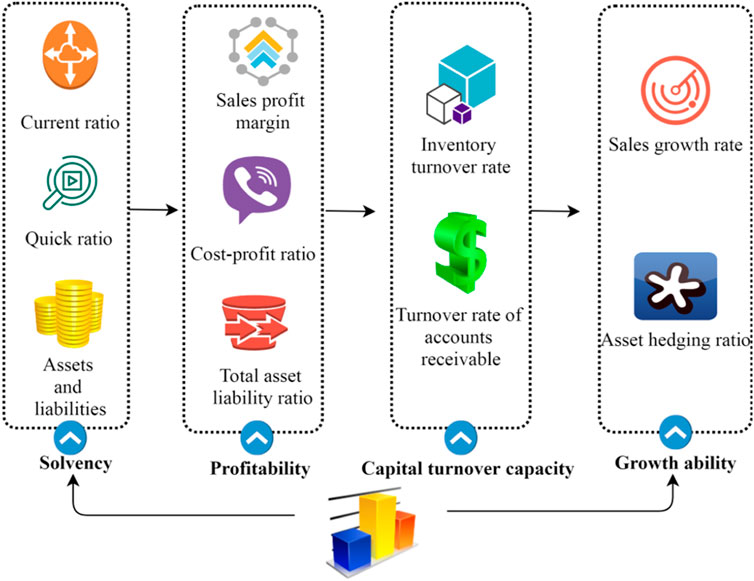

The establishment of the index system is the most important link in the whole financial risk early warning system. Early warning indicators should be the most representative financial indicators. They should not be too many and should comprehensively reflect the financial situation and operating results of the enterprise, so they should not be less. Select indicators that are highly related to risk early warning to form an indicator system. The index diagnosis for all aspects of the enterprise mainly includes the following contents: business diagnosis, production diagnosis, organizational diagnosis, and technical diagnosis. In order to help find or judge the main problems and causes in enterprise management, propose targeted measures to improve the level of enterprise management. The indicator system should not only consider the particularity of each enterprise, but also be designed in combination with the different characteristics of modern enterprises. In terms of the selection of specific indicators, considering that the indicators should complement each other without duplication and give expression to the financial situation of the company as comprehensively and comprehensively as possible, each early warning module takes several representative indicators. Figure 2 shows the warning indicator system studied in this paper.

FIGURE 2. Financial risk early warning indicator system.

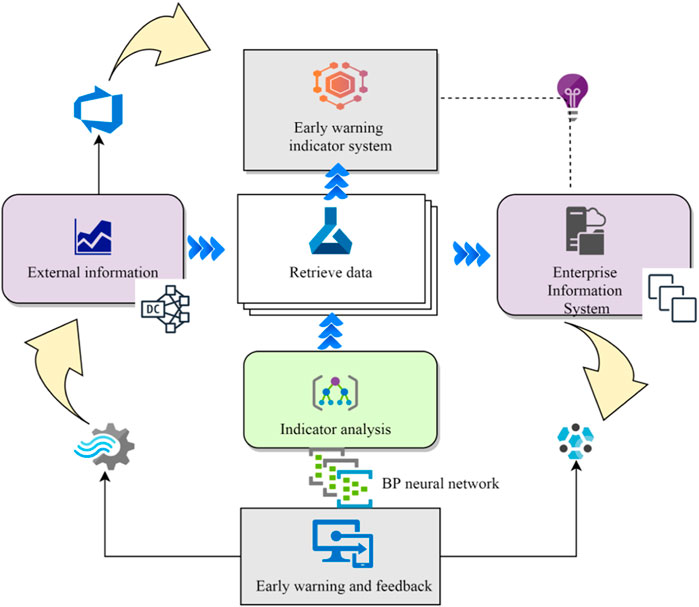

BPNN has excellent error correction ability and learning ability. It play a significant role to apply it to enterprise financial early warning. Its basic principle is that the input layer is responsible for importing data samples and sending sample data to the hidden layer. Secondly, the hidden layer processes data in real time according to the activation function, and transfers the calculation results to the next layer. Finally, the output layer is responsible for output. After training, the network deviation gradually reduces to achieve the desired value. Therefore, we can establish an expectation function, put all indicators into the function, and use the discriminant method to score and classify. Figure 3 shows the basic process of the financial early warning model based on BPNN.

FIGURE 3. Basic process of financial early warning model based on BPNN.

The establishment steps are as follows: 1) Select an appropriate analysis mode. To establish a financial early warning model, the most fundamental thing is to choose an appropriate analysis mode, that is, first analyze and judge whether the research object is suitable for single variable model or multi variable model. 2) Determine the appropriate sample for analysis. For a discriminant function, it is very important to focus the discriminant values on two or more intervals to achieve the effect of discrimination. This requires starting from the analysis of samples and dividing them into several obvious categories. 3) Design and further screen out appropriate financial indicators or financial indicator combinations. 4) Use the analysis software to calculate the model parameters (assuming SPSS system is selected to complete the analysis model). 5) Results inspection. There are two main aspects to test the results: One is the accuracy test, the other is the predictive test.

The implementation steps of the financial early-warning comprehensive index measurement system. The implementation steps of the financial early-warning comprehensive index measurement system are generally as follows: 1) Design the core indicators and auxiliary indicators that should be monitored in the financial early-warning comprehensive index; 2) Measure the “early warning critical indicator value” of various financial monitoring indicators; 3) Measure the “actual index value” of various financial monitoring indicators; 4) According to the “early warning critical value” and “actual indicator value” of each financial monitoring indicator, measure the early warning composite index of each financial monitoring indicator and predict the warning degree; 5) Analyze and evaluate the financial early-warning comprehensive index. The efficiency coefficient method refers to comparing each index to be evaluated with its own standard according to the principle of multi-objective planning, and according to the weight of each index. The power function is transformed into measurable evaluation scores, and then the individual index scores of each index are summed up to obtain the comprehensive evaluation scores. The efficiency coefficient method is used to convert financial indicators into single efficiency coefficients. In fact, the influencing factors of different industries have been removed, which should improve the risk prediction.

The first step is to set variables and parameters. Assuming that the number of input and output neurons is

Standardization before data input can effectively improve the convergence speed and effect. This paper analyzes some of the motivations. If our activation function is sigmoid or TAH, the maximum gradient interval is around 0. When the input value is large or small, the change of sigmoid or TAH is basically flat. That is to say, the gradient tends to zero while the optimization speed is very slow. The simplest and most useful method is to carry out z-score, PCA whitening and other standardization methods, scaling the input to 0 mean and standard variance.

Because of the non-linear dynamics of neural networks, it is difficult to obtain a simple and general formula to identify hidden layer units in theory. However, some qualitative conclusions obtained through extensive and long-term application process will help to reasonably arrange the number of hidden layer units. Therefore, the number of hidden layer units can be determined by referring to the following formula.

Among them,

The second step is to initialize the connection right and threshold value.

After the training, use the test sample to test the network accuracy, compare the actual output with the expected output of the test sample, and select the number of hidden layer nodes with the highest alert accuracy as the final number of hidden layer nodes of the alert model in this paper. If the set accuracy requirements are met, that is, the error is within the allowable range, the algorithm is terminated and the BPNN model is obtained. If the error fluctuation exceeds the limited range, assess the error of the hidden layer node, calculate the error gradient, adjust the weight and threshold, and adjust the relevant parameters if essential until the error meets the set standard.

The output curve of Sigmoid function is relatively flat at both ends, with sharp changes in the middle part, which is closer to the signal output form of biological neurons. Generally, the differentiated S-ray function is continuously defined as the activation function in the hidden layer node, namely:

In the reverse iteration process of error, determine whether the adjacent calculation cells need to be iterated in the orthogonal direction, which will lead to zigzag jump near the extreme value. Although this can reduce the value of the network performance function as quickly as possible, it slows down the convergence calculation of the network and makes the calculation result easy to approach the local minimum.

For the input layer neurons of the model, the input and output are the same. The calculation rules for the neurons of the middle hidden layer and the output layer are as follows:

In the above formula,

The output value at the

The actual output value in the

In order to save the time of training network, partial connection mode can be used to obtain better accuracy in a reasonable time, the update amount

Take the probability analysis method to measure the degree of investment risk. The probability analysis method calculates the standard deviation according to the probability rate of return, expected rate of return and probability analysis of the investment scheme under various economic conditions. The standard deviation refers to the deviation degree between the expected yield rate and the yield rate. The standard deviation formula is:

Among them,

For cost index, that is, the smaller the index value, the better, let:

Moderate indicators require that the indicator value is determined to be a fixed value as the best, so that:

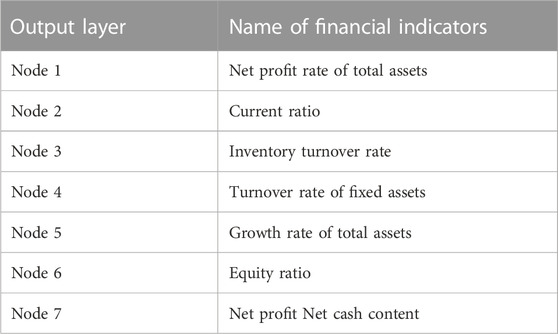

The purpose of back propagation is to achieve optimization without repeating derivative steps. It refers to a multilayer neural network that uses error back propagation (BP algorithm for short) to solve the weight correction problem in the training of artificial neural network. An algorithm for training some given feedforward neural networks for a given input pattern when the classification is known. When each segment of the sample set is displayed to the network, the network will see its output response to the sample input mode. Then, the measurement output response is compared with the expected output and the error value. Then, we adjust the connection weight according to the measured error value. In order to train the BP neural network, it is necessary to calculate the weighted input vector, network output and error vector of the network, and then calculate the sum of squares of the errors. When the sum of error squares of the training vector is less than the error target, the training stops. In this paper, by increasing the training times and observing the simulation results to find the best training times, the network has the best generalization ability. According to the above research results, it can be seen that the early warning of enterprise financial risk under the low-carbon perspective has certain particularity, and the principles, indicator setting and weight of each indicator must be considered when establishing. Therefore, this paper proposes the following suggestions for establishing a low carbon economy enterprise financial risk early warning system. First, multiple principles should be considered in the design. When designing the financial risk early warning system, enterprises should consider the principles of integrity, comparability and systematization; Scientific principle, etc. as shown in Table 1.

TABLE 1. Corresponding indicators of the input layer.

This paper determines the weight of financial risk early warning indicators. In the criteria layer, the carbon profitability index has the highest weight, followed by the carbon debt repayment index, carbon development index and carbon operation index. It shows that experts believe that under the perspective of low-carbon economy, enterprises still aim to make profits, that is, to make profits by using carbon equipment, carbon inventory, etc. The important indicator of bank loans to enterprises is the debt repayment indicator, so we should still pay attention to the carbon debt repayment indicator when developing the carbon economy, that is, the indicator is still important. However, the ultimate goal of carbon development indicators and carbon operation indicators is to promote the rise of carbon profitability indicators, which may be the reason why experts give a lower score. Among the financial factors of an enterprise, profitability and solvency have the greatest impact on the financial crisis in, while growth ability, capital structure and operating ability and non-financial factors have relatively little impact. In the final analysis, profitability and solvency are the ability of enterprises to obtain funds. It is the blood of a capital enterprise, and the profitability is an important factor to determine whether the capital is sufficient. The business activities of an enterprise cannot be separated from financial support, just as the human body cannot live without blood. But practice shows that the lack of funds has become an important factor hindering the survival and development of enterprises.

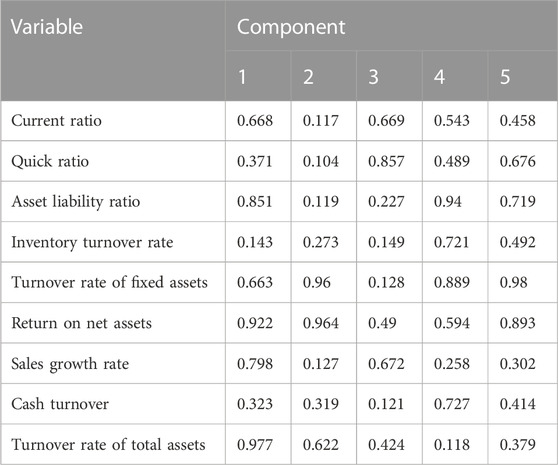

The samples selected in this paper are manufacturing companies listed in Shenzhen and Shanghai stock exchanges, and the original data are all from Huatai Securities website www.htzq.com cm. Among them, Bankruptcy companies selected refer to those specially treated by the stock market in 2017 (There are 27 ST companies in total. The base date is the earliest occurrence date of financial anomalies. The financial statement data of these companies before the base date are selected. In this paper, the same company in different years is also considered as different companies. After removing the companies with missing financial data, the total number of samples used in the final empirical analysis is 138. Among them, the total number of training samples is 10, and the total number of generalized tests is 56. For the selected sample data, the equal scale example is used to reduce In this way, the financial data can fall into the range [0, 1], so that the neural network can process the data. K-S test is adopted to test the normality of basic financial early-warning indicators. S-W inspection and K-S inspection: S-W inspection is recommended for small samples (less than 50), and K-S inspection is recommended for large samples (more than 50). It will be used when using software to solve statistical problems. If the financial early warning indicators meet the normal distribution, perform a t-test on the selected basic financial early warning indicators. If the financial early warning indicators do not meet the normal distribution, Kruskal Wallis non-parametric test is performed on the selected basic financial early warning indicators to obtain the component matrix in Table 2.

TABLE 2. Rotated composition matrix.

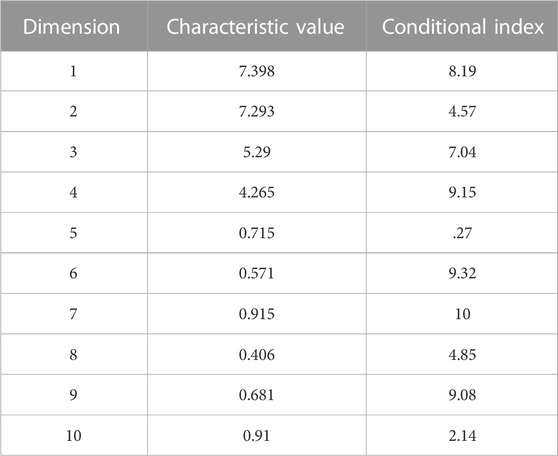

Through the significance test of the initial variables, we know that 10 indicators such as the cash recovery rate of assets have obvious correlation with the financial situation of the enterprise. However, some of these indicators have strong collinearity and contain repeated information, which will have a certain impact on the accuracy of the experiment. Therefore, continue to use factor analysis to screen the 10 indicators for the second time to eliminate the collinearity between indicators, as shown in Table 3.

TABLE 3. Collinearity diagnosis.

From the results of collinearity diagnosis, the eigenvalues of the first few principal components are larger, while the latter ones are smaller. At the same time, the conditional index of the latter principal components far exceeds 8, which also indicates that there is serious multicollinearity among these variables. We need to filter the independent variables.

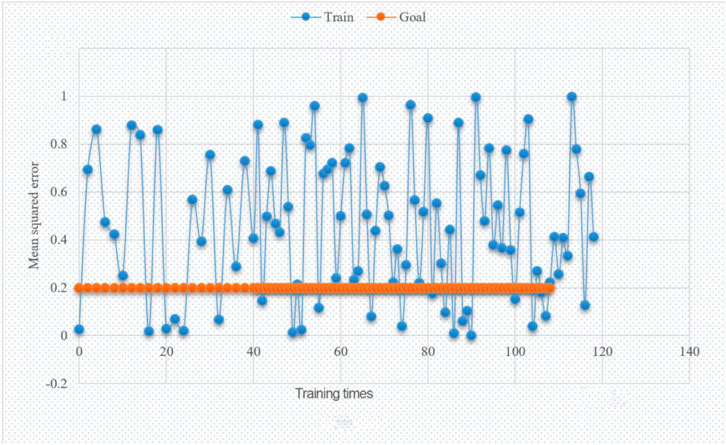

Use the weight of financial risk early warning indicators of low-carbon economy enterprises studied in this paper. This paper uses AHP method to calculate the weight of financial risk early warning indicators. Among them, collect the survey results of each respondent, and finally take the comprehensive results of three opinions to scale the importance. It can be seen that this weight is very effective, so it is recommended that enterprises use this financial risk early warning indicator weight to warn their financial risks. At the same time, the consistency check table of financial risk early warning indicators from the perspective of low-carbon economy also shows that the weights designed in this paper are appropriate. In addition, the smaller the final comprehensive weight value of the research setting, the smaller the contribution to the enterprise. The weight reflects the importance of each early warning indicator to the overall evaluation target. The determination of index weight is an important link in the early warning of SMEs’ financial risk. It can be said that the determination of indicator weight can affect the effective play of early warning system functions to some extent. Comparing 100 randomly selected test results, it is found that the simulation error of .9984 using the optimized weight and threshold is far less than the simulation error of 2.13 using the random weight and threshold (Figure 4).

FIGURE 4. Number of training steps and mean squared error.

A single-layer neural network has no hidden layer (input directly maps to output). For the output layer, which is also different from other layers in the neural network, neurons in the output layer generally do not have an activation function (or they can be considered as having a linear equivalent activation function). This is because the final output layer is mostly used to represent the classification score value, so it is a real number of any value. Compared with a single hidden layer, neural network training with two hidden layers does not help to improve the accuracy of prediction. This has actually given us a basic principle for designing BP neural network. The improvement of error accuracy can also be achieved by increasing the number of neurons in the hidden layer, and the training effect is easier to observe and adjust than increasing the number of layers. Therefore, in general, using a single hidden layer can meet the research needs, and the key consideration is to determine the number of neurons in the hidden layer. The most important input mode should be determined from a large number of raw test data. If the two inputs have strong correlation, just take one of them as the input, which requires statistical analysis of the original data, test the correlation between them, carry out correlation analysis, and find out the most important quantity as the input.

The critical value of early warning indicators includes the determination of satisfactory value, impermissible value and upper and lower limit value. 1) Positive type variable. The average value of the industry is selected as the satisfaction value, but the selection of values is not allowed to be different. 2) Inverse variable. Its standard value is determined in the opposite way to the positive variable. The satisfactory value is 0, and the disallowed value is .3. 3) Stable variable. Add 10 percentage points above the average value of the industry as the satisfaction value, and take - times and half of the satisfaction value as the upper and lower limit of the unacceptable value. 4) Moderately optimal variable. According to the industry average value of the ratio, the increase and decrease of 10 percentage points on the basis of the average value is taken as the upper and lower limit of the satisfactory range of the ratio. The upper and lower limits of the disallowed range are doubled and halved on the average value. Establish an early warning indicator system that can reflect the risk characteristics of the enterprise, including indicators reflecting five dimensions of debt repayment, operation, development, profitability and cash flow. In order to improve the convergence speed and stability of the model, SPSS25.0 is used to conduct factor analysis on these five dimensions, select financial indicators that meet the requirements of the model, and take the extracted main factors as the input data of the model.

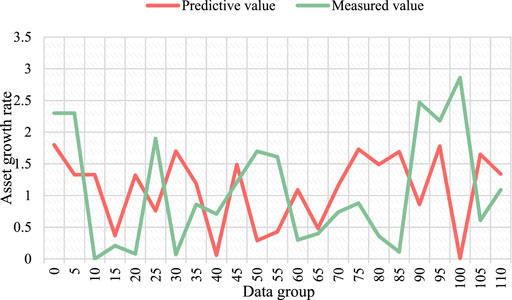

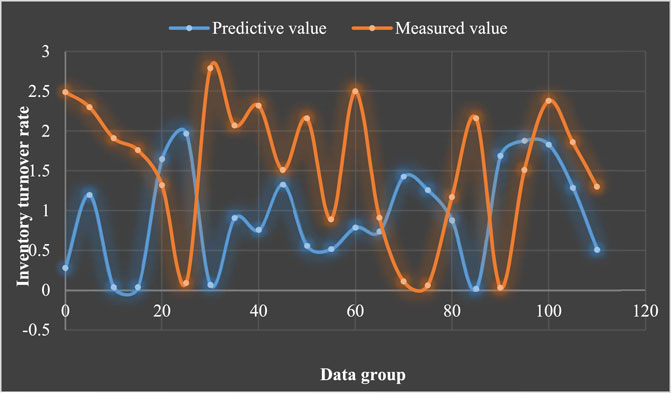

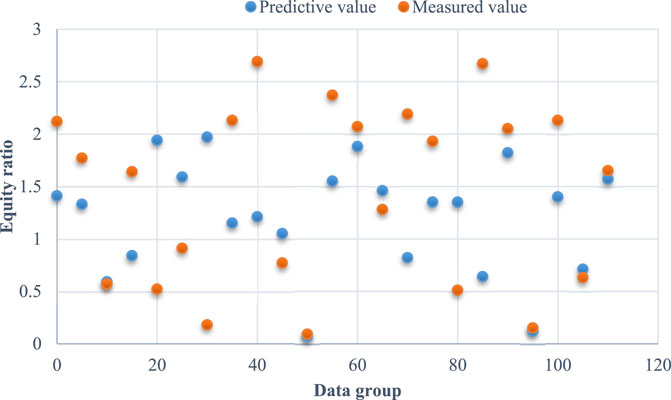

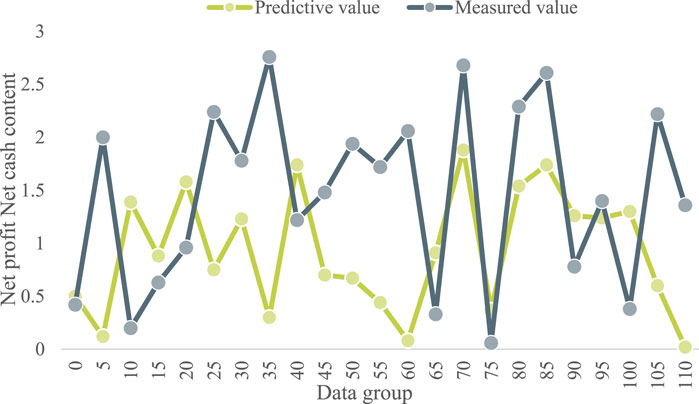

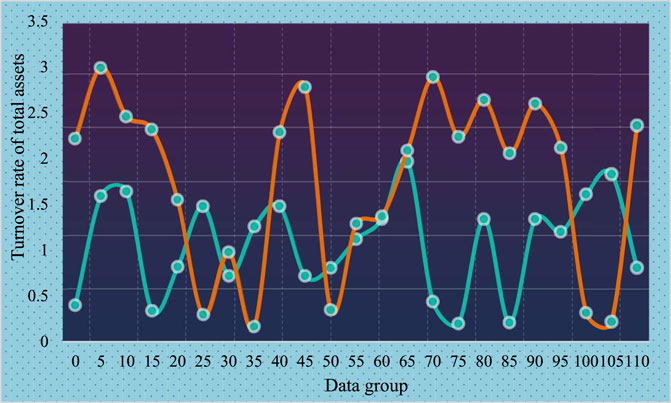

It can be seen from Figures 5, 6, 7, 8, 9 that the model has a good prediction result on the operating capacity index, with the average prediction error less than 3%, the average prediction error on the solvency index between 5% and 10%, and the average prediction error on the crude fatty acid value of soybeans between 1.3% and 2.9%. Since the training data of the model comes from the same enterprise, and each indicator factor has a similar change law, the prediction error of the five dimensions of the model is reduced by 12.8%, 6.4%, 8.4%, 8.0%, and 8.1% respectively, and the prediction effect is better. The ideal situation is that the network output is equal to the expected output. Generally speaking, the R value is above .9, which indicates that the BPNN has good performance. The solid line in the figure is the actual fitting situation, while the dotted line is the ideal fitting situation. It can be seen that the neural network is very close to the ideal fitting condition.

FIGURE 5. The training results of the solvency index.

FIGURE 6. Training results of operational capability indicators.

FIGURE 7. Profitability index training results.

FIGURE 8. Training results of cash flow capability indicators.

FIGURE 9. Training results of developmental ability indicators.

Through repeated experiments, it is proved that when the number of hidden nodes is small, the network has poor ability to obtain knowledge from the samples, and cannot quickly find the internal laws in the samples, resulting in slow convergence speed and low accuracy of the model. Increasing the number of hidden nodes can speed up the convergence of the model and improve the accuracy of the model. When the number of hidden layer nodes is 8, the optimal correct recognition rate can be achieved. After 10 indicators passed the KMO and Bartlett correlation test, MATLAB software was used to program and establish the BPNN financial early warning model. The accuracy rate was 84.3% after verification.

Enterprises should pay attention to carbon profitability indicators and carbon debt repayment indicators when conducting low carbon financial early warning. It is found that the carbon profitability index has the highest weight in the criteria layer, followed by the carbon debt repayment index, carbon development index and carbon operation index. It can be seen that experts believe that under the perspective of low-carbon economy, enterprises are still for profit, that is, to use carbon equipment, carbon inventory, etc. to make profits for enterprises. The important indicator of bank loans to enterprises is the debt repayment indicator, so we should still pay attention to the carbon debt repayment indicator when developing the carbon economy. This paper constructs 10 financial early warning indicators from four aspects, uses the research method of BPNN to complete the establishment of the risk prediction model of the indicator system, and conducts training and simulation experiments on the established model through the MATLAB neural network toolbox. The results show that the early warning management of enterprise financial risk is conducive to strengthening the internal control level of enterprises, helping enterprises to solve the problems in management, thereby promoting the development of enterprises and enhancing their competitiveness. As the lifeblood of enterprise development, financial management directly determines the future development trend of the enterprise. How to improve the sustainable development ability of the enterprise based on meeting both the economic development and the enterprise’s own development is what the current workers need to pay attention to. Therefore, business operators need to change their core concepts and improve the working level and efficiency of financial personnel. However, the study lacks correlation analysis of the original variables. The correlation coefficient matrix between calculated variables needs to be statistically tested. Further analysis is needed in future research. However, the analysis of differences in asset structure, business characteristics and human capital level in this paper is insufficient. BP neural network has no strict requirements on data distribution. Therefore, further analysis is needed in the future research.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

JW wrote the manuscript, BY contributed to manuscript revision. They contributed to the article and approved the submitted version.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Ashraf, S., Gs Félix, E., and Serrasqueiro, Z. (2019). Do traditional financial distress prediction models predict the early warning signs of financial distress?[J]. J. Risk Financial Manag. 12 (2), 55. doi:10.3390/jrfm12020055

Buchdadi, A. D., Sholeha, A., and Ahmad, G. N. (2020). The influence of financial literacy on SMEs performance through access to finance and financial risk attitude as mediation variables[J]. Acad. Account. Financial Stud. J. 24 (5), 1–15.

Cao, Y., Shao, Y., and Zhang, H. (2022). Study on early warning of E-commerce enterprise financial risk based on deep learning algorithm. Electron. Commer. Res. 22 (1), 21–36. doi:10.1007/s10660-020-09454-9

Colak, M. S. (2021). A new multivariate approach for assessing corporate financial risk using balance sheets. Borsa İstanbul Rev. 21 (3), 239–255. doi:10.1016/j.bir.2020.10.007

Du, P., and Shu, H. (2022). Exploration of financial market credit scoring and risk management and prediction using deep learning and bionic algorithm[J]. J. Glob. Inf. Manag. (JGIM) 30 (9), 1–29. doi:10.4018/jgim.293286

Hamid, N., and Purbawangsa, I. B. A. (2022). Impact of the board of directors on financial performance and company capital: Risk management as an intervening variable. J. Co-op. Organ. Manag. 10 (2), 100164. doi:10.1016/j.jcom.2021.100164

He, H., and Chen, X. (2020). Animal Farming Enterprise Financing and Financial Risk Early Warning Model Construction in Economic Transition Period[J]. Rev. Científica Fac. Ciencias Veterinarias 30 (2), 992–1003.

Kang, Q. (2019). Financial risk assessment model based on big data. Int. J. Model. Simul. Sci. Comput. 10 (04), 1950021. doi:10.1142/s1793962319500211

Kapitonov, I. A. (2021). Development of low-carbon economy as the base of sustainable improvement of energy security. J]. Environ. Dev. Sustain. 23 (3), 3077–3096. doi:10.1007/s10668-020-00706-0

Kim, A., Yang, Y., Lessmann, S., Ma, T., Sung, M. C., and Johnson, J. E. (2020). Can deep learning predict risky retail investors? A case study in financial risk behavior forecasting[J]. Eur. J. Operational Res. 283 (1), 217–234. doi:10.1016/j.ejor.2019.11.007

Kou, G., Chao, X., Peng, Y., Alsaadi, F. E., and Herrera, V. E. (2019). Machine learning methods for systemic risk analysis in financial sectors[J]. Technol. Econ. Dev. Econ. 25 (5), 716–742. doi:10.3846/tede.2019.8740

Kuang, J., Chang, T. C., and Chu, C. W. (2022). Research on Financial Early Warning Based on Combination Forecasting Model. Sustainability 14 (19), 12046. doi:10.3390/su141912046

Louche, C., Busch, T., Crifo, P., and Marcus, A. (2019). Financial Markets and the Transition to a Low-Carbon Economy: Challenging the Dominant Logics. Organ. Environ. 32 (1), 3–17. doi:10.1177/1086026619831516

Semieniuk, G., Campiglio, E., Mercure, J. F., Volz, U., and Edwards, N. R. (2021). Low-carbon transition risks for finance. Wiley Interdiscip. Rev. Clim. Change 12 (1), e678. doi:10.1002/wcc.678

Shang, H., Lu, D., and Zhou, Q. (2021). Early warning of enterprise finance risk of big data mining in internet of things based on fuzzy association rules. Neural Comput. Appl. 33 (9), 3901–3909. doi:10.1007/s00521-020-05510-5

Tan, M. M., Xu, D. L., and Yang, J. B. (2022). Corporate Failure Risk Assessment for Knowledge-Intensive Services Using the Evidential Reasoning Approach. J. Risk Financial Manag. 15 (3), 131. doi:10.3390/jrfm15030131

Valaskova, K., Kliestik, T., Svabova, L., and Adamko, P. (2018). Financial Risk Measurement and Prediction Modelling for Sustainable Development of Business Entities Using Regression Analysis. Sustainability 10 (7), 2144. doi:10.3390/su10072144

Xuefeng, Z. A. O., Weiwei, W. U., Xu, G. U. O., and Huining, S. H. I. (2022). CFW-Boost Model for Cause-and-effect Analysis in Enterprise Financial Risk Warning[J]. J. Syst. Manag. 31 (2), 317.

Zeng, H. (2022). Influences of mobile edge computing-based service preloading on the early-warning of financial risks. J. Supercomput. 78 (9), 11621–11639. doi:10.1007/s11227-022-04329-2

Keywords: back propagation neural network, financial risk, enterprise, early warning model, low-carbon economy

Citation: Wan J and Yu B (2023) Early warning of enterprise financial risk based on improved BP neural network model in low-carbon economy. Front. Energy Res. 10:1087526. doi: 10.3389/fenrg.2022.1087526

Received: 02 November 2022; Accepted: 16 December 2022;

Published: 04 January 2023.

Edited by:

Wen-Tsao Pan, Hwa Hsia University of Technology, TaiwanReviewed by:

Zhe Song, Yantai University, ChinaCopyright © 2023 Wan and Yu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Baochun Yu, MjEwMDAzN0Bnbm51LmVkdS5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.