Zi-Rui Chen

Zi-Rui Chen Yuan Yuan

Yuan Yuan Xu Xiao

Xu Xiao- 1School of Marxism, South China Normal University, Guangzhou, China

- 2School of Mathematical Sciences, South China Normal University, Guangzhou, China

- 3School of Economics and Management, Beihang University, Beijing, China

The Resource Tax Law was officially implemented on September 1, 2020, in China. This law presents the “Fee-to-Tax” reform of water resources. This article compares the effects of the “Fee-to-Tax” reform under asymmetric duopoly conditions with perfect information. The mechanisms of the two policies are different when all firms simultaneously respond to water resources: the water resource fee affects output by reducing market size, while the water resource tax reduces output by amplifying the weighted cost difference effects between companies. Water resource taxes work better than fees for eliminating backward production capacity. A comparison of the situation when companies respond sequentially is also carried out. When a low-cost firm is in the leading position, the collection of fees actually reduces the output difference, whereas the tax improves it. When a high-cost firm acts as a leader, the effects depend on the cost difference. When the cost difference between firms is small, the first-move advantage of high-cost firms dominates the cost advantages of low-cost firms. Therefore, a higher tax rate yields a smaller output difference. When cost differences are relatively larger, the cost advantage of low-cost firms dominates the first-move advantage of high-cost firms. As the operational cost for reducing water consumption increases, the reduced water consumption first increases and then decreases.

Introduction

On August 26, 2019, after the twelfth meeting of the Standing Committee of the Thirteenth National People’s Congress, the Resource Tax Law was officially adopted and was officially implemented on September 1, 2020. For the first time, the Resource Tax Law explicitly levies water resource taxes on a trial basis for industries and individuals who use surface water or groundwater. As the water resource tax is levied, the collection of water resource fees will cease. China’s water resources are very scarce, and the per capita water resources are only one-fourth of the world average. Water resources are unevenly distributed in space and time, and there are problems such as water pollution, waste, the excessive exploitation of groundwater, and weak citizen protection awareness. With the development of the construction of an ecological civilization, the importance of water resources to human society is constantly increasing; therefore, a general trend is to include water resources in the scope of resource tax collection.

China began collecting water resource fees in 1980. In 1988, China officially promulgated and implemented the “Water Law of the People’s Republic of China”, which explicitly included the collection of water resource fees into the legal scope. The collection of water resource fees has serious problems, such as multisector collection, low actual collection rates, and irregular use management. To promote the construction of resource-saving and environmentally friendly cities, increase citizens’ awareness of water resource protection and water efficiency, and improve water resources, China has included water resources in the scope of resource tax collection.

Although country characteristics must necessarily shape practical policy advice, theory provides some fairly specific guidance. This paper aims to analyze the theoretical basis that underlies the Fee-to-Tax reformation of water resources.

When studying the effect of the reform of water resource fees and taxes, scholars hold different opinions. Mushtaq et al. (2008) questioned the effectiveness and feasibility of a water Fee-to-Tax reform and noted that this reform is likely to cause serious difficulties in agricultural production. Ma, Zhao and Ni (2018) indicated that tax reform is conducive to reducing not only arbitrary charges but also the burden on enterprises, and the collection and use of a water resource tax is more reasonable and transparent, which is helpful for the state to control the source and use of the water resource tax and to reduce corruption. Some researchers established the computable general equilibrium model (CGE) of the economy with water as an explicit factor of production. Qin et al. (2012) used the CGE model to assess the economic impact of water pricing in China. Li et al. (2019) calculated a reasonable tax rate of water resources in Yunnan Province with the CGE model; Tian (2021) also calculated the optimal tax rate of water resources in Hebei Province. Beyond these studies, there are few articles on the economic principles of water resource tax fee shifting.

To avoid increasing the corporate tax burden, a general rule is presented that the tax fee after the reform equals the original water resource fee in the Fee-to-Tax reform. In this particular situation, the collection of water resource fees can be seen as a special type of unit tax before the Fee-to-Tax reform. Considering this, the model that studies ad valorem and unit taxes can be adapted to analyze the effect of the Fee-to-Tax reform on water resources.

The comparison between these two types of taxes is a classic topic that has been the subject of ongoing discussion and development in public finance (Skeath, 1994; Blackorby and Murty, 2007; Vetter, 2017). The study of differentiated duopolies or oligopolies was developed by Dixit (1979), Singh and Vives (1984), Häckner (1999) and other scholars. Wang and Zhao (2007) compared the welfare effects of cost reductions in differentiated Bertrand and Cournot oligopolies but did not take taxation into account. It was indicated that in asymmetric and differentiated oligopolies, unit taxation could be welfare-superior to ad valorem taxation if the goods are sufficiently differentiated under either Cournot or Bertrand competition (Wang and Zhao, 2009). Lapan and Hennessy (2011) extended the analysis to multimarket oligopolies. For a linear demand system, it is also demonstrated that the marginal cost of public funds for ad valorem taxes is generally lower than that for unit taxes (Häckner and Herzing, 2016). Arguably, policy designers favor the use of ad valorem taxes over unit taxes in oligopolies. However, the anticompetitive effects of the two taxes on firms’ strategic interactions favor unit taxes over ad valorem taxes (Vetter, 2014). Given decreasing returns to scale, an ad valorem tax regime unambiguously Pareto dominates a unit tax regime (Hoffmann and Runkel, 2016). Griffith and Nesheim et al. (2018) noted that by considering the use of tax policy, utility is linear in the consumption of the outside good. A specific tax results in larger reductions than an ad valorem tax but at a greater cost to consumers.

The vast majority of applications focus on how these theories help us to explain economic situations in real life (Nie and Chen, 2012; Nie et al, 2018; Tao et al, 2018). Such theories are also applied to discuss clean and dirty technology competition (Chen et al, 2015; Acemoglu et al, 2016), the impacts of subsidies and taxation (Chen et al, 2017; Golosov et al, 2014; Wang et al, 2017; Yang et al, 2018; Dong et al, 2018), and other related social economic issues (Bloch and Demange, 2018; Fuest et al, 2018; Wang and Wright, 2017).

In this paper, the model of ad valorem and unit taxes is further developed to study the effect of the Fee-to-Tax reform under an asymmetric duopoly by investigating the total outputs and the difference in the outputs in the two collection regimes.

The remainder of this paper is organized as follows. Model Establishment introduces the model. The model is discussed in Model Analysis under two different circumstances: (1) all firms simultaneously respond to the policy; (2) different firms respond to policy change sequentially. Finally, concluding remarks are presented in Concluding Remarks.

Model Establishment

By taking water resource policy into account, a duopoly model is adopted for the following study. In an industry, two asymmetric firms exist (the marginal production costs are different) that compete in quantity. For convenience, denote the two firms as

In Eq. 1,

In Eq. 2,

In the following section, the above model is used to analyze the economic and environmental effects of the Fee-to-Tax reform in the situation when all firms respond to the policy change simultaneously and sequentially.

Model Analysis

Firms Respond to the Policy Simultaneously

First, we are concerned with the case in which all firms respond to the policy simultaneously, and then the model is discussed under Cournot competition.

When the water resource fee is collected, Eq. 2 is also concave, and the unique equilibrium is determined by the first-order optimal condition. The equilibrium is outlined by the following equations:

The equilibrium is

When water resource fees are collected, both firms reduce outputs, and the two firms reduce output identically. The output gap and corresponding price and profits are

Before the Fee-to-Tax reform, the water resource fee reduced the total outputs and producer surplus. The corresponding price increases with the fee collection intensity. The output difference remains constant regardless of the amount of payment per unit, which means that such a policy places an identical effect on the outputs of the two firms. From Eq. 4, we have

When the water resource tax is collected, the payment is

The equilibrium is

To measure the cost difference, we refer to the definition of WCD (weighted cost difference) combined with product substitutability.

Definition 1. WCD (weighted cost difference) is defined as

The corresponding price and profits are given as follows:

From Eq. 9, we have

Proposition 1. When all firms respond to the policy change simultaneously, (1) The water resource fee does not change the output difference. (2) The water resource tax reduces total outputs and increases the output gap. (3) With small cost differences, the water resource tax reduces the outputs and profits of both firms. (4) Under large cost differences, the water resource tax improves the outputs and profits of high-efficiency firms while reducing the outputs and profits of low-efficiency firms.

Proof. See in Supplementary Appendix SA.

Remarks. Based on the above analysis, we argue that the implementation of water resource taxes improves prices while reducing total output and product surplus. Higher taxes mean higher prices and lower outputs.

Obviously, product substitutability increases the opponent’s costs in the WCD. When

Based on Definition 1, we can intuitively draw the following conclusions. Under Cournot competition, collecting the water resource fee affects equilibrium by reducing the market size, while collecting the water resource tax affects equilibrium by amplifying the effects of the WCD. Both the water resource fee and tax affect the market equilibrium, and the affecting mechanisms differ. Water resource fees reduce the market size and then reduce firms’ outputs and profits. In contrast, collecting a tax amplifies the effects of the WCD and then affects the output difference and profits. The above conclusions capture the action mechanism of the different taxes.

When conducting the Fee-to-Tax reform, a general rule is assumed that the amount of payment remains unchanged during the reform. Thus, a comparison of the outputs is conducted under this basic rule. That is,

Eq. 13 is restated as

For the output effects of the two types of policy, we have the following relationship:

Under a fixed total amount of payment, we draw the following conclusions. Proposition 2 (1)

Proof. See Supplementary Appendix SB.

Remarks. This proposition demonstrates that low-cost firms experience a larger loss in outputs than high-cost firms experience. After the reform, it is more advantageous to phase out backward production capacity. By levying water resource taxes, the government participates in the distribution of benefits from the development of state-owned water resources, can also adjust the distribution of benefits between resource occupiers and nonresource occupiers, and at the same time promote equal competition among water companies.

Interestingly, the distinguishing effects on the output difference are the result of the two policies’ action mechanisms. Collecting the water resource fee affects the equilibrium by reducing the market size. Such a tax affects outputs by amplifying the effects of the WCD. After using tax leverage to increase the cost of water use, companies will naturally adjust their production behavior to promote water conservation.

Firms Respond to the Policy Sequentially: Low-Cost Firm as the Leader

Next, this article discusses the second case: assuming that not all firms respond to the policy synchronously, then the model is discussed under Stackelberg competition. Once the outputs are obtained, the analysis of prices and profits under Stackelberg competition is similar to that under Cournot competition. Thus, in the following section, we mainly focus on outputs. We first address the case in which the low-cost firm plays the leading position, and the high-cost firm acts as a follower.

By taking a backward induction approach, we immediately obtain the following equilibrium when the water fee is collected.

The output gap of the two firms is

Under Stackelberg competition, collecting the water resource fee affects the output gap, which is different from the result under Cournot competition. Moreover,

After the Fee-to-Tax reform, the equilibrium is given as follows.

Similarly, the output gap is

Based on the above analysis, we have the following conclusions.

Proposition 3. Collecting the water resource fee reduces the output difference between firms. When a low-cost firm acts as the leader, the output difference is larger than that under the circumstance when the water resource fee is collected. Based on the above conclusion, high-cost firms may prefer water resource fees, and low-cost firms may favor water resource taxes.

Proof. See Supplementary Appendix SC.

Remarks. The output difference when not all firms respond simultaneously is larger than the output difference under the Cournot game. Accordingly, when low-cost firms respond first to the policy reform, these firms possess both cost and first-move advantages. These advantages yield larger output differences than those when firms act at the same time. First, on the basis of their own cost advantages, the first mover has the opportunity to limit its competitor to achieve sales and achieve cost advantages through economies of scale and learning effects. Second, the forerunner creates switching costs for customers who use it, and it is difficult for the latecomer to seize it from the forerunner. Third, the first-move company can build important brand loyalty, but the latter is difficult to break. In all, when firms do not respond simultaneously, the effects of the policy reform that supports phasing out of backward production capacity are strengthened.

Furthermore, an analysis of the environmental benefits of the “Fee-to-Tax” reform will be discussed. For the ith firm under consideration:

To measure the reducing water consumption, we introduce the definition of

When the low-cost firm (firm A) plays the leading position, its production cost increases:

By taking a backward induction approach, we immediately obtain the following equilibrium when the water fee is collected.

After the tax reform, the water tax was collected.

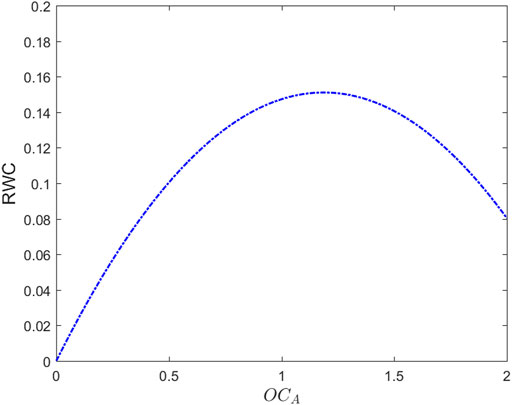

Proposition 4. As the operational cost for saving water consumption increases, the reducing water consumption increases at first, and then decreases.

Remarks. The first-move company invests in water saving technology. Thus, the actual cost of its product includes the original cost and the increased operational cost for reducing water consumption. As a company increases its investment in saving water, the reduced water consumption increases as well. However, when the operational cost increases beyond the extreme point, the actual cost will become so high that it will cause the sales of the product to decline dramatically, hinder the company’s commercial competition, and thus eventually decrease the reducing water consumption. Figure 1 shows numerical simulations of

FIGURE 1. Numerical simulations of

Firms Respond to the Policy Sequentially: High-Cost Firm as the Leader

Then, we consider the other case in which the high-cost firm leads, while the low-cost firm follows.

When a high-cost firm (firm

The output gap is

Similar conclusions to those drawn in Concluding Remarks also hold. That is,

Moreover, a small cost difference between the two firms implies that

Apparently,

In the situation when the water resource tax is collected, the equilibrium is given as follows:

Similarly, the output gap is

Based on Eq. 26, we have the relationships

Based on the above analysis, we obtain the following conclusions:

Proposition 5. When the high-cost firm leads the investment in water savings according to the “Fee-to-Tax” reform, the output of the high-cost firm is higher than its output under the situation when two firms respond simultaneously. The outputs of the latecomer are lower than the outputs under other circumstances. The total output of two firms is higher than the output when two firms respond simultaneously. More specifically, the proposition can be delivered in the following inequality:

Proof. See Supplementary Appendix SD.

Remarks. Under the Stackelberg game, firm

Accordingly, the implementation of the tax reduces the outputs of both firms. The tax reduces the outputs of high-cost firms more than the outputs of low-cost firms. When two firms respond at the same time, collecting water resource fees reduces outputs symmetrically. However, the implementation of a water resource tax has an asymmetric reduction effect on firms’ output. In other cases, when two firms do not respond to the policy reform simultaneously, both policies have an asymmetric reduction effect on firms’ outputs. However, the effect of taxes on the leading firm in such situations is more severe than the effect of taxes on the corresponding firm when they respond simultaneously.

Concluding Remarks

This article addresses the effects of the “Fee-to-Tax” reform of China’s water resources under asymmetric duopoly conditions. The impacting mechanisms of water resource taxes and water resource fees differ. Collecting water resource fees reduces the market size, while taxes amplify the WCD (weighted cost difference) effects between industries. When all firms in the market respond to the policy simultaneously, the water resource fee reduces firms’ outputs identically, while the water resource tax affects high-cost firms more than low-cost firms. Furthermore, when firms respond sequentially, the implementation of fees asymmetrically affects the equilibrium of firms. However, the tax affects the leading firm more than it affects the corresponding firm when all firms act synchronously. Additionally, the effect of the tax is more severe for leading firms than for followers. Surprisingly, it is also proven that the outputs are higher under Stackelberg competition than under Cournot competition because the leading firm under Stackelberg produces more than the leading firm under Cournot produces to hinder entrants. As the operational cost for reducing water consumption increases, the reduced water consumption first increases and then decreases. Therefore, the “Fee-to-Tax” reform provides some benefits to maintain the environmental development of some water mining or related industries.

Based on the above analysis, taxes can act as an efficient regulative tool to support and shape industrial development. Some policy implications can be proposed according to the findings in this analysis. Specifically, the adoption of special taxes in some industries can help to eliminate backward production capacity. Because the collection of taxes has asymmetric effects on output, it works better to phase out backward production capacity than the collection of fees. Additionally, when the government decides on a tax pattern, the market characteristics of different firms should be fully considered.

In this article, the effect of the “Fee-to-Tax” reform under asymmetric duopoly conditions with perfect information is discussed. Some further research topics arise. On the one hand, the market response under incomplete information is worth discussing. Incomplete information deters both government and industry decisions, and it is also important to study the mechanisms in such situations. On the other hand, in analyzing tax reforms, it is worth considering deterring the different production characteristics of different industries. In this way, an optimal tax regime can be proposed. It is crucial to design a tax regime that considers the long-term effects for some industries with externalities that involve energy, the environment and food safety. Chen and Nie, 2016.

Data Availability Statement

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding authors.

Author Contributions

XX and Z-RC conceived the idea and supervised the project. Z-RC designed the model and wrote the manuscript. YY performed the mathematical studies. All authors approved the manuscript before submission to the journal.

Funding

This work is partially supported by the Guangdong Planning Office of Philosophy and Social Science (GD20YYJ01).

Conflict of Interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s Note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Acknowledgments

Z-RC especially wishes to thank Mr. Jun Gong, whose song brought her joy and delight.

Supplementary Material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenrg.2021.752592/full#supplementary-material

References

Acemoglu, D., Akcigit, U., Hanley, D., and Kerr, W. (2016). Transition to Clean Technology. J. Polit. Economy 124 (1), 52–104. doi:10.1086/684511

Blackorby, C., and Murty, S. (2007). Unit versus Ad Valorem Taxes: Monopoly in General Equilibrium. J. Public Econ. 91 (3-4), 817–822. doi:10.1016/j.jpubeco.2006.10.003

Bloch, F., and Demange, G. (2018). Taxation and Privacy protection on Internet Platforms. J. Public Econ. Theor. 20 (1), 52–66. doi:10.1111/jpet.12243

Chen, Y.-h., He, Q., and Paudel, K. P. (2018a). Quality Competition and Reputation of Restaurants: the Effects of Capacity Constraints. Econ. Research-Ekonomska Istraživanja 31 (1), 102–118. doi:10.1080/1331677x.2017.1421996

Chen, Y.-h., Huang, S.-j., Mishra, A. K., and Wang, X. H. (2018b). Effects of Input Capacity Constraints on Food Quality and Regulation Mechanism Design for Food Safety Management. Ecol. Model. 385, 89–95. doi:10.1016/j.ecolmodel.2018.03.011

Chen, Y.-h., Wen, X.-w., Wang, B., and Nie, P.-y. (2017). Agricultural Pollution and Regulation: How to Subsidize Agriculture? J. Clean. Prod. 164, 258–264. doi:10.1016/j.jclepro.2017.06.216

Chen, Y. H., Nie, P. Y., and Wang, X. H. (2015). Asymmetric Doupoly Competition with Innovation Spillover and Input Constraints. J. Business Econ. Manage. 16 (6), 1124–1139. doi:10.3846/16111699.2013.823104

Chen, Z.-y., and Nie, P.-y. (2016). Effects of Carbon Tax on Social Welfare: A Case Study of China. Appl. Energ. 183, 1607–1615. doi:10.1016/j.apenergy.2016.09.111

Dixit, A. (1979). A Model of Duopoly Suggesting a Theory of Entry Barriers. Bell J. Econ. 10, 20–32. doi:10.2307/3003317

Dong, B., Wei, W., Ma, X., and Li, P. (2018). On the Impacts of Carbon Tax and Technological Progress on China. Appl. Econ. 50 (4), 389–406. doi:10.1080/00036846.2017.1316826

Fuest, C., Peichl, A., and Siegloch, S. (2018). Do higher Corporate Taxes Reduce Wages? Micro Evidence from Germany. Am. Econ. Rev. 108 (2), 393–418. doi:10.1257/aer.20130570

Golosov, M., Hassler, J., Krusell, P., and Tsyvinski, A. (2014). Optimal Taxes on Fossil Fuel in General Equilibrium. Econometrica 82 (1), 41–88. doi:10.3982/ecta10217

Griffith, R., Nesheim, L., and O'Connell, M. (2018). Income Effects and the Welfare Consequences of Tax in Differentiated Product Oligopoly. Quantitative Econ. 9 (1), 305–341. doi:10.3982/qe583

Häckner, J. (1999). A Note on Price and Quantity Competition in Differentiated Oligopolies. J of Econ, 15, 546-554. doi:10.1006/jeth.2000.2654

Häckner, J., and Herzing, M. (2016). Welfare Effects of Taxation in Oligopolistic Markets. J. Econ. Theor. 163, 141–166. doi:10.1016/j.jet.2016.01.007

Hoffmann, M., and Runkel, M. (2016). A Welfare Comparison of Ad Valorem and Unit Tax Regimes. Int. Tax Public Finance 23 (1), 140–157. doi:10.1007/s10797-015-9355-2

Lapan, H. E., and Hennessy, D. A. (2011). Unit versus Ad Valorem Taxes in Multiproduct Cournot Oligopoly. J. Public Econ. Theor. 13 (1), 125–138. doi:10.1111/j.1467-9779.2010.01495.x

Li, M., Liu, C., and Xu, S. (2019). “Simulation and Analysis on the Optimal Tax Rate of Water Resources in Yunnan Province. IOP Conf. Ser. Earth Environ. Sci. 267, 062034. doi:10.1088/1755-1315/267/6/062034

Ma, Z., Zhao, J., and Ni, J. (2018). Green Tax Legislation for Sustainable Development in China. Singapore Econ. Rev. 63 (04), 1059–1083. doi:10.1142/s0217590817420103

Mushtaq, S., Khan, S., Dawe, D., Hanjra, M. A., Hafeez, M., and Asghar, M. N. (2008). Evaluating the Impact of Tax-For-Fee Reform (Fei Gai Shui) on Water Resources and Agriculture Production in the Zhanghe Irrigation System, China. Food Policy 33 (6), 576–586. doi:10.1016/j.foodpol.2008.04.004

Nie, P.-y., and Chen, Y.-h. (2012). Duopoly Competitions with Capacity Constrained Input. Econ. Model. 29 (5), 1715–1721. doi:10.1016/j.econmod.2012.05.022

Nie, P.-y., Wang, C., Chen, Z.-y., and Chen, Y.-h. (2018). A Theoretic Analysis of Key Person Insurance. Econ. Model. 71, 272–278. doi:10.1016/j.econmod.2017.12.020

Qin, C., Jia, Y., Su, Z., Bressers, H. T. A., and Wang, H. (2012). The Economic Impact of Water Tax Charges in China: a Static Computable General Equilibrium Analysis. Water Int. 37 (3), 279–292. doi:10.1080/02508060.2012.685554

Singh, N., and Vives, X. (1984). Price and Quantity Competition in a Differentiated Duopoly. RAND J. Econ. 15, 546–554. doi:10.2307/2555525

Skeath, S. E., and Trandel, G. A. (1994). A Pareto Comparison of Ad Valorem and Unit Taxes in Noncompetitive Environments. J. Public Econ. 53 (1), 53–71. doi:10.1016/0047-2727(94)90013-2

Tao, A., Wang, X. H., and Yang, B. Z. (2018). Duopoly Models with a Joint Capacity Constraint. J. Econ., 125, 1–14. doi:10.1007/s00712-018-0597-1

Tian, G.-l., Wu, Z., and Hu, Y.-c. (2021). Calculation of Optimal Tax Rate of Water Resources and Analysis of Social Welfare Based on CGE Model: a Case Study in Hebei Province, China. Water Policy 23 (1), 96–113. doi:10.2166/wp.2020.118

Vetter, H. (2014). Ad Valorem versus Unit Taxes in Oligopoly and Endogenous Market Conduct. Public Finance Rev. 42 (4), 532–551. doi:10.1177/1091142113496129

Vetter, H. (2017). Commodity Taxes and Welfare under Endogenous Market Conduct. J. Econ. 122 (2), 137–154. doi:10.1007/s00712-017-0538-4

Wang, C., Nie, P.-y., Peng, D.-h., and Li, Z.-h. (2017). Green Insurance Subsidy for Promoting Clean Production Innovation. J. Clean. Prod. 148, 111–117. doi:10.1016/j.jclepro.2017.01.145

Wang, X. H., and Zhao, J. (2009). On the Efficiency of Indirect Taxes in Differentiated Oligopolies with Asymmetric Costs. J. Econ. 96 (3), 223–239. doi:10.1007/s00712-008-0046-7

Wang, X. H., and Zhao, J. (2007). Welfare Reductions from Small Cost Reductions in Differentiated Oligopoly. Int. J. Ind. Organ. 25 (1), 173–185. doi:10.1016/j.ijindorg.2006.02.003

Wang, Z., and Wright, J. (2017). Ad Valorem Platform Fees, Indirect Taxes, and Efficient price Discrimination. RAND J. Econ. 48 (2), 467–484. doi:10.1111/1756-2171.12183

Keywords: fee-to-tax reform, policy effect, asymmetric duopoly, water resource tax, water consumption

Citation: Chen Z-R, Yuan Y and Xiao X (2021) Analysis of the Fee-to-Tax Reform on Water Resources in China. Front. Energy Res. 9:752592. doi: 10.3389/fenrg.2021.752592

Received: 03 August 2021; Accepted: 27 September 2021;

Published: 13 October 2021.

Edited by:

Yong-Cong Yang, Guangdong University of Foreign Studies, ChinaReviewed by:

Minxing Jiang, Nanjing University of Information Science and Technology, ChinaYou-Hua Chen, South China Agricultural University, China

Copyright © 2021 Chen, Yuan and Xiao. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Yuan Yuan, eXl1YW4yMTAyQG0uc2NudS5lZHUuY24=; Xu Xiao, eHV1X3hpYW9AMTYzLmNvbQ==