Nattavud Pimpa

Nattavud Pimpa

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Commun. , 28 February 2025

Sec. Organizational Communication

Volume 10 - 2025 | https://doi.org/10.3389/fcomm.2025.1543893

This article is part of the Research Topic Rethinking How Firms Communicate with Society View all articles

Introduction: Environmental, social, and governance (ESG) factors have become essential considerations for businesses seeking long-term sustainability and stakeholder trust. Effective ESG communication and disclosure practices are critical in demonstrating corporate commitment to sustainability. This study examines how the top 20 companies listed on the Thailand Stock Exchange communicate and disclose ESG-related information, with a focus on their integration of ESG metrics into business strategies.

Methods: This research employs a qualitative approach, utilizing secondary data from sustainability and ESG reports published by the selected companies. Thematic analysis is applied to identify and categorize key ESG activities and disclosure practices, providing a structured assessment of how businesses articulate their ESG commitments.

Results: The analysis identifies five key themes in ESG communication and disclosure: (1) comprehensive ESG disclosure and reporting, (2) environmental initiatives, (3) employee welfare, (4) governance and risk management, and (5) community development. These themes highlight the diverse approaches taken by companies to integrate ESG factors into their business models and public reporting.

Discussion: The findings underscore the importance of transparent ESG disclosure in enhancing corporate sustainability and stakeholder engagement. Companies that effectively integrate ESG considerations can mitigate risks, identify new business opportunities, and align with global sustainability standards. While the relationship between ESG practices and financial performance remains complex, existing literature suggests that strong ESG commitments can lead to long-term financial benefits. This study provides practical recommendations for Thai businesses to enhance their ESG communication strategies and strengthen their sustainability efforts.

Environmental, Social, and Governance (ESG) factors constitute a framework for evaluating companies based on their sustainability performance, extending beyond traditional financial metrics. This framework encompasses various considerations, including environmental impact, social responsibility, and corporate governance practices. The incorporation of ESG factors into business practices has become increasingly crucial as the global community grapples with pressing challenges such as climate change, social inequalities, and the need for more transparent and accountable corporate governance (Zaccone and Pedrini, 2020; Khalfaoui et al., 2021; Sugianto et al., 2022). The relationship between ESG performance and financial performance remains a subject of ongoing debate within academic and business circles. While a significant body of literature suggests a positive correlation, empirical evidence presents a nuanced picture. Some studies demonstrate no relationship or even negative associations, highlighting the complexity of this issue.

Furthermore, the impact of ESG initiatives on financial performance may not be uniform across all contexts. Ahmad et al. (2023) provide a scientometric review indicating a complex relationship between ESG factors and business investment sustainability. While investors may support effective ESG processes, their impact on business performance can vary significantly across different sectors and regions. Liu et al. (2023) found that in the context of the Yangtze River Delta in China, the initial stages of ESG practice development are positively associated with corporate financial performance. However, the extent of this impact varies considerably across different industries.

Conversely, some studies have observed negative or insignificant relationships. Barbosa et al. (2023) found that integrating ESG criteria can sometimes negatively impact corporate sustainability performance, particularly in sectors such as energy. Negara et al. (2024) reports that high levels of ESG disclosure do not significantly impact firm value, suggesting that companies may already possess a high level of transparency without the need for extensive ESG reporting. Liang et al. (2023) found a significant negative correlation between ESG and financial performance among environmentally sensitive enterprises. Similarly, Ponce and Wibowo (2023) observed a negative relationship between ESG and various financial performance indicators in the context of Indonesian banks. The influence of national culture and sector-specific risks further complicates the inconsistency in findings. Shin et al. (2023) highlight that the impact of ESG performance on financial outcomes can vary significantly across different cultural contexts. Similarly, Jasni and Zulkifli (2024) note that the financial impact of ESG practices is not uniform and can vary dramatically based on the risk profile of the sector in which a firm operates. Addressing these challenges requires excellent ESG reporting and communication standardization, improved data quality and transparency, and a deeper understanding of the complex interplay between ESG factors and financial performance and corporate sustainability in various contexts.

Communication of ESG processes and outcomes is pivotal as they showcase a company’s commitment to responsible practices and ethical behavior, influencing accounting performance and firm value (Siew et al., 2013). Stakeholders are increasingly urging companies to embed ESG goals into their strategic plans, practices, and value chains, emphasizing the importance of sustainability in business operations (Duan et al., 2023). Governance efforts within ESG can provide strategic advantages, particularly in high-risk sectors, by mitigating risks and attracting investors (Adu et al., 2022).

Additionally, Duan et al. (2023) and Zhang and Nedospasova (2024) demonstrate the positive influence of ESG factors on firm and corporate value, respectively. Moreover, integrating ESG principles into business models has been linked to increased operational efficiency, higher employee productivity, and enhanced corporate reputation (Cohen et al., 2024). A study by Shen (2023) also confirms that ESG, in the form of corporate governance, can positively impact a company’s performance in several ways: enhancing investment efficiency, fostering innovation, optimizing capital structure, and improving the concentration of ownership (Albarrak et al., 2019).

Given the increasing emphasis on sustainable business practices, companies must prioritize aligning their operations with ESG principles. When it comes to communicating ESG actions by corporations, sustainability reporting plays a central role in companies’ ESG communications. Sustainability reporting emphasizes ethical behavior and responsible practices, enabling businesses to share their ESG initiatives with stakeholders. This stakeholder theory and ESG reporting are closely related since they both emphasize how important it is for businesses to engage with internal and external stakeholders.

Effective ESG communication fosters transparency and accountability, essential for building trust with stakeholders. As organizations disclose their ESG practices, they provide stakeholders—such as investors, customers, and employees—with critical information that reflects their commitment to sustainable practices. Research indicates that companies with robust ESG disclosures tend to enjoy better reputations and lower capital costs, as stakeholders perceive them as more trustworthy and responsible (Sahin et al., 2022). This transparency mitigates risks associated with reputational damage and enhances the firm’s ability to attract investment, as investors increasingly favor companies that demonstrate strong ESG performance (Alsayegh et al., 2020). Moreover, integrating ESG factors into corporate reporting can significantly influence firm valuation. Studies have shown that firms that excel in ESG disclosures are better positioned to capture market benefits, as these disclosures enhance the positive impact of integrated reporting on firm value (Lokuwaduge and Heenetigala, 2016). This relationship aligns with stakeholder theory, which posits that companies that actively engage with their stakeholders through transparent communication are more likely to foster trust and loyalty, ultimately leading to improved financial performance. Furthermore, organizations that adopt a holistic approach to ESG reporting can pursue economic, environmental, and social objectives simultaneously, thereby achieving competitive advantages.

To comprehensively understand the challenges and opportunities associated with ESG practices and communication in the Thai business context, it is essential to analyze the specific drivers and barriers companies encounter. This study examines ESG activities implemented and reported by leading firms in Thailand, focusing on identifying opportunities for business organizations to integrate ESG principles effectively. The research aims to address the following key questions:

• What key elements do top companies in Thailand prioritize in their ESG communication and disclosure to the public?

• What are the emerging trends/areas for improvement that exist in the ESG communication practices of these companies?

Thematic analysis is adopted in this study to comprehend key ESG themes and trends for businesses to communicate ESG to stakeholders. It involves identifying, analyzing, and reporting patterns (themes) within data. This approach is particularly useful for examining ESG data, as it allows the author to uncover insights into how companies communicate their ESG practices and the implications of these communications for stakeholder engagement and corporate reputation. The analysis of ESG data through thematic analysis can reveal the complexities and nuances of corporate sustainability efforts, especially in contexts where regulatory frameworks and stakeholder expectations are rapidly evolving, such as in Thailand.

The concept of ESG has gained significant traction in recent years as a framework for assessing corporate responsibility and sustainability. However, ESG remains subjective, leading to considerable confusion among investors and stakeholders. One of the primary sources of this confusion is the lack of correlation among ESG ratings provided by different agencies. Research indicates that ESG ratings from various providers often show low consistency, with studies revealing that these ratings align only about 54% of the time, compared to nearly 99% for credit ratings (Billio et al., 2024). This divergence raises questions about the reliability and validity of ESG assessments as investors struggle to interpret conflicting ratings for the same companies (Liu et al., 2022).

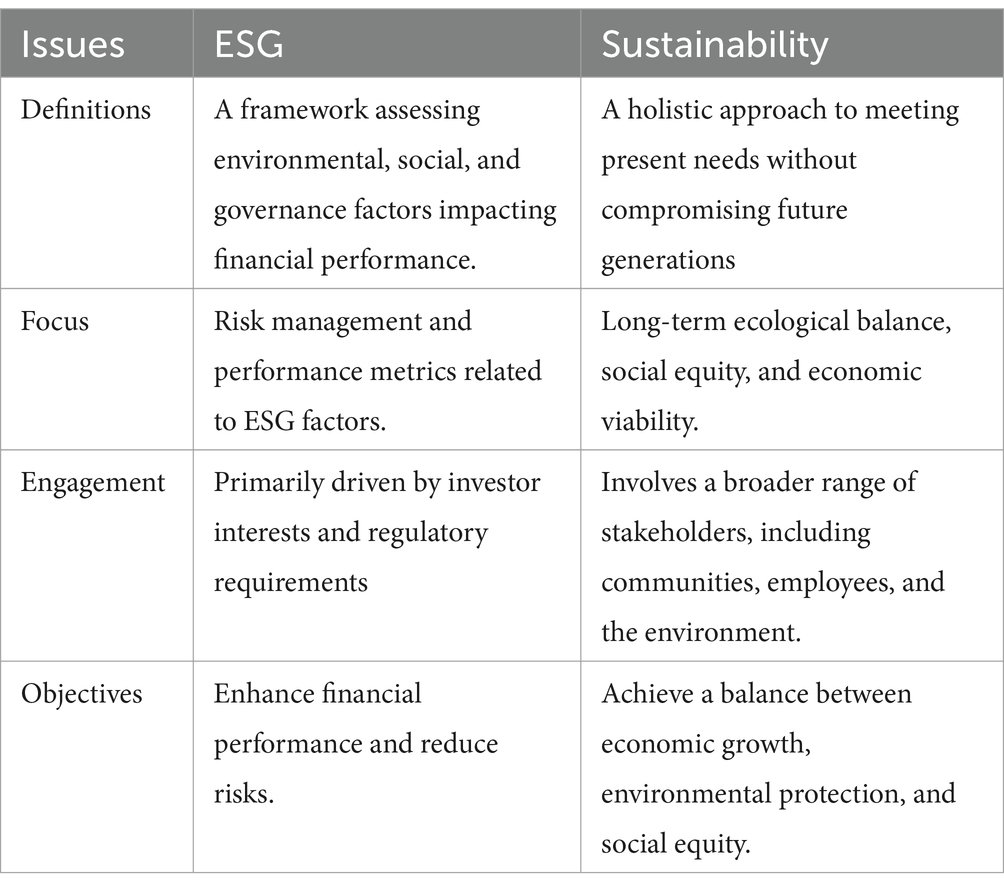

The misunderstanding that ESG criteria and sustainability are synonymous can significantly impact companies in various ways. This confusion often arises from the overlapping nature of the two concepts, leading organizations to conflate ESG practices with broader sustainability initiatives [Corporate Governance Institute (CGI), 2024]. While ESG factors are often framed within the sustainability narrative, they do not encompass the full spectrum of sustainability principles (van Zanten and Huij, 2022). This conflation can mislead stakeholders into believing that adherence to ESG criteria guarantees sustainable practices, which is not necessarily the case. The authors emphasize the need for a more apparent distinction between ESG metrics and broader sustainability goals to avoid misconceptions that could hinder genuine progress toward sustainable development. To illustrate the differences between ESG and sustainability, Table 1 compares key meanings and concepts associated with each:

Table 1. Comparison between ESG and sustainability.

The proliferation of ESG data providers has also contributed to the confusion surrounding ESG as a concept. Delgado-Ceballos et al. (2023) note that the increasing emphasis on the financial materiality of ESG factors has led to a surge in the number of metrics and ratings available to investors (Delgado-Ceballos et al., 2023). However, this has not been translated into a unified understanding of what constitutes effective ESG performance. The authors advocate for a double materiality approach, which recognizes that ESG factors can affect both financial performance and broader societal impacts, thus necessitating a more nuanced understanding of these metrics.

Moreover, the presumption that ESG is synonymous with sustainability further complicates the discourse. While ESG encompasses environmental, social, and governance factors, sustainability is a broader concept that includes economic viability and long-term ecological balance (Duan et al., 2023). This conflation can lead to misunderstandings about what ESG ratings truly represent. For instance, the ESG framework often emphasizes compliance and risk management rather than holistic sustainability practices, which can mislead stakeholders regarding a company’s overall impact on society and the environment (Liu et al., 2022). The ambiguity surrounding the definitions and metrics used in ESG assessments contributes to the perception that ESG ratings are subjective and inconsistent (Duan et al., 2023).

Additionally, the quality of ESG data has been criticized for being inadequate and irregular, further exacerbating the confusion surrounding ESG ratings (Ademi and Klungseth, 2022). The lack of standardized methodologies across rating agencies means that different firms may receive vastly different scores based on the same underlying data, leading to skepticism among investors regarding the credibility of these ratings (Billio et al., 2024). This skepticism is reflected in surveys indicating that a significant portion of institutional investors express distrust in companies’ commitments to ESG principles (Cohen et al., 2024).

In terms of relationship between ESG performance and corporate financial performance (CFP), this issue remains a complex and often debated topic in contemporary research. Despite a growing body of literature suggesting a positive correlation between ESG practices and financial outcomes, the evidence is not uniformly conclusive, leading to ongoing discussions about the nuances of this relationship. One significant aspect of the ESG-CFP relationship is the notion that companies with high ESG scores tend to exhibit greater financial stability. For instance, A study by Pimpa (2024) found that firms with elevated ESG performance often enjoy a slight advantage in financial performance, which contributes to their overall financial stability and growth. This suggests that companies investing in ESG initiatives may not only enhance their reputational capital but also secure a more stable financial future. Similarly, Liu et al. (2023) highlighted that in the context of the Yangtze River Delta in China, the initial stages of ESG practice development are positively associated with corporate financial performance, although the extent of this impact varies significantly across different sectors and regions.

Studies have highlighted the growing importance of ESG factors in Thailand’s corporate landscape, emphasizing the roles of transformative leadership and stakeholder engagement in driving ESG strategies in the Thai cultural context (Wichianrak et al., 2021; Suttipun and Dechthanabodin, 2022). The Stock Exchange of Thailand (SET) has played a pivotal role in promoting sustainability reporting among Thai-listed companies, requiring them to implement policies for environmental improvements in their reports (Petcharat and Zaman, 2019). Additionally, the integration of transformational leadership and ESG practices in Thai businesses, particularly in industries like the food sector, has been identified as essential for organizational transformation towards successful ESG and sustainability outcomes (Suttipun, 2023). Thai corporate environmental disclosures have been influenced by soft law and institutional signaling, indicating a shift towards greater environmental disclosures aligned with societal norms (Wichianrak et al., 2021).

In Thailand, local Thai firms increasingly recognize that strong ESG performance can lead to better financial resilience and competitive advantage. This can be a co-effort from the SET, Government, and international partners. However, the relationship between corporate ESG performance and financial return is not uniformly positive across all sectors or contexts in Thailand. Some studies have indicated that the costs associated with implementing ESG initiatives can initially detract from profitability, particularly in industries where margins are already thin (Wichianrak et al., 2021). This is echoed in findings that suggest the financial benefits of ESG investments may take time to materialize, leading to a temporary decline in performance metrics (Liu et al., 2023). In Thailand, where many companies are still in the early stages of integrating ESG into their business models, this lag can be particularly pronounced.

Despite the nuanced relationship between ESG performance and financial outcomes in Thailand, the adoption of ESG principles is steadily gaining traction across the corporate sector. The cultural and regulatory environment plays a crucial role in shaping the intersection of ESG and financial performance. Research suggests that national culture and governance structures moderate the effectiveness of ESG initiatives in Southeast Asian economies, including Thailand (Petcharat and Zaman, 2019). As ESG considerations continue to evolve, Thai businesses must navigate the complexities of regulatory compliance, stakeholder expectations, and financial sustainability to achieve long-term success in ESG implementation.

Additionally, the role of external factors, such as investor expectations and market conditions, cannot be overlooked. As investors increasingly prioritize ESG criteria in their decision-making processes, companies in Thailand that fail to meet these expectations may face challenges in attracting capital. This shift in investor sentiment underscores the importance of transparent and effective ESG reporting, which can enhance a company’s reputation and financial standing in the market.

The study of ESG practices in Thailand addresses the notion that firms operate within social systems by highlighting the interconnectedness between corporate actions and societal expectations. Firms do not exist in isolation; they are part of a broader social fabric that demands accountability and transparency. By analyzing how these companies communicate their ESG efforts, the research reveals how firms can build trust and legitimacy among stakeholders, thus reinforcing their social license to operate. This aligns with the idea that effective ESG communication is not merely a reporting obligation but a strategic tool for engaging with stakeholders and fostering a positive corporate reputation (Odriozola and Baraibar-Diez, 2017).

Having established that one of the critical aspects of ESG in Thailand is the relationship between corporate governance and ESG performance. Research indicates that many Thai listed companies struggle with the effective ESG disclosures and performance, due to weak governance structures, often exacerbated by the family ownership model prevalent in the region (Suttipun and Dechthanabodin, 2022). This relationship demonstrates the potential for ESG activities to improve operational efficiencies and business reputation, attracting investment. However, the challenge is to improve the quality and openness of ESG disclosures. Many companies engage in “greenwashing,” in which advertised ESG efforts do not match real practices, leading to stakeholder scepticism (Wang et al., 2023).

This governance issue is crucial as it directly impacts the ability of firms to implement robust ESG strategies that meet stakeholder expectations and regulatory requirements. Furthermore, the lack of a standardized framework for ESG reporting in Thailand has led to inconsistencies in how companies disclose their ESG activities, making it difficult for investors to assess their true sustainability performance (Suttipun and Dechthanabodin, 2022).

The communication of Environmental, Social, and Governance (ESG) information has become increasingly critical in the corporate landscape, driven by stakeholder demands and regulatory pressures. A key point in the discourse surrounding ESG communication is the emphasis on materiality assessment, which is essential for ensuring that companies disclose relevant information that meets stakeholder expectations. As highlighted by Sepúlveda-Alzate et al., the materiality of ESG information is underscored by organizations like the Global Reporting Initiative (GRI), which advocates for a robust disclosure of materiality analyses in sustainability reports. This practice not only enhances stakeholder engagement but also fosters informative and consultative relationships between companies and their stakeholders (Sepúlveda-Alzate et al., 2022).

The reliance on voluntary ESG disclosures presents challenges in achieving consistency and comparability across firms. Robinson (2023) notes that corporate sustainability assessment tools primarily depend on publicly available sustainability reports, which are often disclosed voluntarily. This inconsistency results in disparities in the quality and reliability of ESG information, prompting calls for mandatory disclosure requirements to enhance transparency and accountability.

Despite the growing recognition of ESG factors in investment decisions, gaps remain in the effective communication of ESG information. For instance, Zhang points out that while ESG investment has gained traction in China, challenges persist in the quality and transparency of ESG disclosures (Zhang and Nedospasova, 2024). This lack of transparency can hinder stakeholder trust and engagement, as stakeholders may find it difficult to assess a company’s true ESG performance based on inadequate or unclear reporting. Furthermore, a study by Ademi and Klungseth (2022) emphasizes that while ESG performance reflects a firm’s commitment to sustainability, the actual communication practices may not adequately convey this commitment, leading to information asymmetry among stakeholders.

Most Thai companies focus on the communication in the form of ESG report as a critical component of corporate strategy, not a part of corporate culture. In fact, this form of communication is driven by increasing stakeholder expectations, regulatory pressures, and the recognition that ESG factors can significantly influence firm performance and valuation (Pimpa, 2020). Interestingly, most firms are interested in integrating of ESG Metrics into various environmental and social narratives by firms. MNCs, in particular, are increasingly incorporating the communication of ESG metrics into their overall corporate storytelling, particularly through social media platforms. This allows for more transparent and engaging communication with stakeholders.

An increasing number of Thai-listed firms are providing sustainability-related information, with 57% having released ESG reports in the past 2 years [Securities and Exchange Commission (SEC), 2021]. This trend is expected to continue as international regulatory pressures intensify. Thai companies are increasingly integrating environmental and social performance metrics into their business communication strategies to create sustainable value and strengthen their reputation among stakeholders. The establishment of ESG committees within Thai-listed firms further underscores a growing commitment to addressing ESG-related challenges, including conflicts of interest and information asymmetry. In response to the evolving ESG landscape, the Securities and Exchange Commission (SEC) of Thailand revised its regulatory framework in 2021, merging Form 56-2 (the annual report) and Form 56-1 (the annual registration statement) into a single comprehensive document known as Form 56-1 One Report [Securities and Exchange Commission (SEC), 2021]. This reform aims to streamline the reporting process for listed companies, reducing administrative burdens while improving the efficiency and transparency of ESG disclosures. The consolidated report includes corporate policies, objectives, and performance indicators related to environmental, social, and governance issues, covering aspects such as greenhouse gas emissions, human rights due diligence, and corporate initiatives aligned with the Sustainable Development Goals (SDGs) [Securities and Exchange Commission (SEC), 2021].

In the current situation in Thailand, the importance of ESG communication among listed companies is also underscored by the growing demand for standardized ESG metrics (Nation, 2024). As investors and stakeholders seek to assess corporate sustainability, the quality and consistency of ESG disclosures become paramount. Companies that proactively manage their ESG narratives and customize their metrics are better equipped to meet stakeholder expectations and enhance their market positioning. This proactive approach not only helps Thai organizations navigate the complexities of ESG data but also allows them to differentiate themselves in a local and international marketplaces.

Addressing sustainability issues is crucial for companies as it influences their approach to business opportunities and their overall progress towards achieving SDGs within Thailand and Southeast Asia. While not mandated by Thai law, many companies are voluntarily adopting SDG initiatives due to the long-term benefits they offer. Efforts to tackle global environmental challenges, energy concerns, diversity, and working conditions not only mitigate risks to business sustainability but also enhance corporate value and contribute to the attainment of SDGs [United Nations Global Compact (UNGC), 2020].

In Thailand, cultural and regulatory pressures significantly influence the adoption of ESG practices among companies. The Thai government has increasingly recognized the importance of ESG in promoting sustainable development and has implemented various regulatory frameworks to encourage corporate compliance. For instance, the Securities and Exchange Commission (SEC) of Thailand has introduced guidelines that require listed companies to disclose their ESG practices, thereby creating a regulatory environment that compels firms to prioritize ESG considerations in their operations. Furthermore, cultural factors, such as the growing awareness of social responsibility among Thai consumers and investors, have also driven companies to adopt ESG practices. This cultural shift is evident in the increasing demand for transparency and accountability from businesses regarding their environmental and social impacts.

According to the Securities and Exchange Commission (SEC) of Thailand, listed companies are required to disclose their Environmental, Social, and Governance (ESG) practices through the “One Report” (Form 56-1). This reporting framework operates on a “comply-or-explain” basis, meaning that companies must either provide relevant ESG disclosures or justify their omission. The disclosure requirements encompass a broad range of ESG-related factors, including climate change impact, environmental conservation initiatives, and corporate social responsibility programs, with a particular focus on labor practices and community engagement. While Thai companies are not mandated to adhere to specific international ESG standards, they are strongly encouraged to align with global best practices.

To enhance environmental sustainability, the SEC has urged companies to prioritize efforts aimed at reducing Thailand’s carbon footprint and promoting sustainable business practices. In the social dimension, Thai firms are expected to ensure fair labor practices, human rights protections, and active community engagement, in alignment with internationally recognized ESG standards. Key legal framework supporting social sustainability in Thailand is the Labor Protection Act B.E. 2541 (1998), which establishes minimum standards for employee welfare, including regulations on working hours, wages, and conditions for termination. Additionally, the Occupational Safety, Health, and Environment Act B.E. 2554 (2011) mandates that workplaces maintain safe and healthy working conditions for employees.

Governance plays a pivotal role in Thailand’s ESG regulatory framework, ensuring transparency, accountability, and ethical corporate conduct. The SEC of Thailand has been proactive in strengthening corporate governance standards, particularly for publicly listed companies. In 2017, the SEC introduced the Corporate Governance Code for Listed Companies, outlining best practices related to board structure, transparency in decision-making, and risk management. These governance guidelines aim to enhance corporate integrity and investor confidence in the Thai capital market.

Empirical studies have demonstrated the substantial impact of ESG initiatives on Thai firms. For example, a study by Suttipun and Yordudom (2022) analyzing the top 50 listed companies in Thailand found that higher levels of ESG disclosure positively influence market reactions, underscoring the role of ESG practices in enhancing corporate reputation and attracting investment. In the Thai business landscape, research has also indicated that the establishment of dedicated ESG committees within firms significantly enhances ESG performance. An analysis of the top 100 listed companies in Thailand revealed that those with active ESG committees tend to achieve higher ESG scores, demonstrating a direct correlation between governance structures and sustainability outcomes (Suttipun and Dechthanabodin, 2022). Furthermore, firms with higher levels of ESG disclosure have been shown to experience more favorable market responses, reinforcing the strategic importance of transparent ESG reporting (Suttipun and Dechthanabodin, 2022).

Among Thai corporations, stakeholder engagement and leadership strategies have emerged as key focal points for improving ESG performance. This emphasis is driven by the need for transformative leadership and stakeholder-centric approaches that enhance ESG integration within corporate strategies (Pimpa, 2024). The regulatory environment has further reinforced this focus. For instance, the Corporate Governance Code, issued by the Thailand Stock Exchange Commission in 2017, mandates publicly listed firms to enhance their ESG practices (Wang et al., 2023). This regulatory push is crucial in aligning corporate strategies with broader societal goals, particularly in addressing pressing environmental concerns such as energy consumption and carbon emissions (Lakkanawanit et al., 2022). The Stock Exchange of Thailand (SET) has actively promoted these efforts, supported by research indicating that companies with strong ESG frameworks tend to achieve better long-term performance, attracting greater investor interest.

Another significant development in Thailand’s ESG landscape is the increasing establishment of ESG committees within firms, a move strongly encouraged by the SET. Research has shown that companies with dedicated ESG committees demonstrate improved ESG performance metrics (Suttipun, 2023). These committees are responsible for overseeing the implementation of ESG strategies, ensuring accountability, and enhancing transparency in corporate reporting. The SET’s emphasis on such governance structures reflects a growing recognition of ESG’s critical role in investment decisions, as evidenced by the rising interest from institutional and retail investors in ESG-compliant firms (Zhao et al., 2018).

As Thailand continues to refine its ESG frameworks, corporate governance structures, and regulatory policies, integrating ESG principles into business operations will remain a key driver of corporate sustainability. The evolving regulatory landscape, combined with shifting cultural expectations, underscores the necessity for Thai businesses to adopt more comprehensive and transparent ESG strategies to maintain competitiveness in both domestic and global markets.

This study employed thematic analysis to systematically evaluate ESG disclosures in the sustainability reports of the top 20 Thai companies listed on the Stock Exchange of Thailand (SET) by market capitalization. Thematic analysis is helpful in the analysis of GRI data. By categorizing ESG practices into distinct themes, stakeholders can better understand how firms respond to sustainability challenges and opportunities. This is particularly relevant in contexts where ESG performance is increasingly scrutinized by investors and regulators alike. Thematic analysis is also adopted to identify trends and patterns in ESG practices over time (Savio et al., 2023). Such analyses can highlight how external events influence ESG priorities, enabling firms to adapt their strategies accordingly.

The analysis was guided by the Global Reporting Initiative (GRI, 2021) standards, ensuring a structured evaluation of disclosures across three primary dimensions:

• Economic Factors (e.g., anti-corruption, governance, economic contributions).

• Environmental Factors (e.g., energy consumption, carbon footprint, water use, waste management).

• Social Factors (e.g., employee well-being, diversity and inclusion, community engagement).

The data set consisted of 148 GRI disclosures categorized according to Universal and Topic-Specific Standards. The focus was on identifying how frequently companies reported specific ESG indicators and the qualitative depth of their communication, including goals, performance outcomes, and narratives about challenges and progress. In the context of sustainability reporting, the ESG framework has been adopted. It is clear to identify firms’ performance on environmental and social (including economic) actions. In this study, the “G” primarily refers to governance-related disclosure. Under the GRI standards, governance disclosures are encapsulated within the GRI’s governance-related indicators, the GRI universal standard, which focus on the organization’s governance structure, practices, and policies that influence its sustainability performance.

The author adopted the thematic analysis process to analyze and define key themes from the sustainability reports of the top 20 Thai listed companies. The data analysis is structured into six distinct yet iterative phases. This approach allows for a comprehensive understanding of the ESG themes and trends emerging from the data. Each phase is critical in ensuring a thorough and nuanced analysis of the sustainability disclosures.

The first phase involves immersing oneself in the data collected from the annual ESG and sustainability reports. This process begins during data collection, where the author reads and re-reads the reports to gain a deep understanding of the content. This initial engagement is crucial as it helps the author identify preliminary insights and familiarize themselves with the context of the sustainability data. The aim is to become intimately acquainted with the nuances of the reports, which sets the foundation for subsequent analysis phases. Note that reports from different companies and industries can differ in format and presentation. The author focuses on the content, which is GRI data.

At this stage, the author systematically analyzed ESG disclosures and the details from company reports, identifying key activities and priorities. Then, the author generated initial codes by tracking ESG-related terms such as “carbon footprint,” “employee benefits,” “board diversity,” and “community investment” to assess reporting trends. Each disclosure was either explicit (quantifiable data and commitments) or implicit (narrative-driven statements). Codes were assigned based on specific ESG indicators, such as carbon reduction initiatives, employee well-being programs, governance policies, and community investments. This coding process allowed for the structured extraction of ESG disclosure patterns, laying the groundwork for identifying broader themes.

Building on the coded data, the author grouped related codes into five overarching themes that encapsulated ESG reporting priorities among companies. These themes emerged based on disclosure trends, activities, and companies’ relative emphasis on sustainability. For instance, codes related to detailed ESG reporting frameworks, standardized metrics, and external assurance were consolidated under Theme One: Comprehensive ESG Disclosure and Reporting. Similarly, codes linked to climate action, emissions reduction, and renewable energy adoption were clustered into theme two: Enhancement of Environmental Initiatives. Under these three, Employee Welfare and Social Well-being Initiatives, the author focuses on codes related to employee benefits, workplace safety, and community engagement programs. It highlights the importance of fostering a supportive work environment and addressing the social impacts of corporate operations. Codes related to the governance of the company and leadership are grouped as theme four, Governance and ethics. Finally, in theme five, Promotion of Community and Economic Development, the author selected codes related to community investment, social responsibility initiatives, and partnerships with local stakeholders.

To ensure the themes accurately represented the dataset, the author revisited the data to refine and validate each theme. The author assessed whether each theme was well-supported by the codes and distinct from the others. The review process also assessed whether the themes captured key ESG trends across organizations, leading to minor refinements such as expanding Theme Three to include employee welfare and social well-being initiatives. This iterative review ensured the themes were robust and reflective of corporate ESG disclosure practices.

In the final phase, the author clearly defined and named each theme, ensuring they captured the core aspects of ESG disclosure trends. The author names each theme as Theme 1: Comprehensive ESG Disclosure and Reporting, Theme Two: Enhancement of Environmental Initiatives, Theme Three: Social Well-being and Employee Welfare, Theme Four: Strengthening Governance and Risk Management, and Theme five: Promotion of Community and Economic Development.

It is crucial to carefully filter the data and examine its validity to ensure a robust and meaningful analysis of the data regarding ESG communication and practices from the top 20 companies in Thailand. The process involves several steps to ensure that the study’s data is relevant and reliable.

The filtering process involves selecting the relevant data (GRI items) from the annual sustainability reports to focus on the specific ESG issues being analyzed. The following steps outline the filtering process:

• Identify Relevant ESG Indicators: The author began by determining which ESG indicators are most relevant to the study’s objectives. This may include metrics related to environmental impact (e.g., carbon emissions, energy usage), social responsibility (e.g., employee welfare, community engagement), and governance (e.g., board diversity, anti-corruption measures).

• Remove Redundant or Irrelevant Data: The author excluded any data not directly related to the key ESG indicators identified. For example, financial performance metrics that do not link directly to ESG factors would be excluded. This ensures that the focus remains on sustainability-related information.

• Ensure Consistency Across Companies: The author then standardized the data by comparing similar metrics across all 20 companies. This might involve recalculating or normalizing specific values to make them comparable, such as converting different units of measurement or aligning different reporting periods.

• Exclude Outdated or Unreliable Data: At this stage, the author focused on the most recent and comprehensive reports, as ESG practices can evolve significantly yearly. Exclude older data unless it is necessary to identify long-term trends or patterns.

After filtering the data, the author examined its validity to ensure the conclusions were based on accurate and trustworthy information. This involves the following steps:

• Source Credibility Assessment: At this stage, the author evaluates the credibility of the data sources, which in this case are the sustainability reports from the companies themselves. Check if these reports are independently verified by third-party auditors or certification bodies, such as the Global Reporting Initiative (GRI) or the Sustainability Accounting Standards Board (SASB). Reports with external verification are typically more reliable.

• Cross-Verification with Multiple Sources: Where possible, the author cross-checked the data reported (style, format, and content) by companies with data from other credible sources, such as industry benchmarks, non-governmental organizations (NGOs), or government databases. This helps to validate the accuracy and consistency of the information provided.

Most companies in this study operate domestically within Thailand (60%) and have been in business for over a decade. Approximately half of the companies analyzed are classified as being in pollution-intensive “dirty industries,” according to the classification by Mani and Wheeler (1998).

In this section, the author focuses on the results from the thematic analysis of the data from the sustainability report. This section provides an in-depth examination of the ESG (Environmental, Social, and Governance) opportunities identified in the sustainability reports of 20 companies. The analysis focuses on uncovering key patterns, insights, and emerging trends that can guide firms in enhancing their ESG performance and aligning with industry standards. Five main themes emerged from the data: comprehensive ESG disclosure, enhancement of environmental initiatives, focus on social well-being and employee welfare, strengthening governance and risk management, and promotion of community and economic development.

The thematic analysis reveals that companies increasingly recognize the importance of comprehensive ESG practices. The trends identified in the report—ranging from enhanced ESG disclosure and environmental initiatives to a focus on social well-being—demonstrate a commitment to sustainability that aligns with stakeholder expectations and global standards.

A significant number of companies (Company 1, 2, 3, 4, 5, 6, 8, 9, 10, 11, 13, 14, 16, 17, 19, 20) identified opportunities to enhance their ESG disclosures by fully covering all relevant topics under each disclosure category. This reflects a broader trend toward achieving greater transparency and accountability in sustainability reporting. Indeed, Thai companies in this study are increasingly aligning their disclosures with industry best practices.

Apart from disclosing governance structure, nomination of the governance body, list of material topics, and other universal aspects, companies also include economic disclosures such as direct economic value generated and distributed (Economic Disclosure 201-01) and confirmed incidents of corruption and actions taken (Economic Disclosure 205-03). The trend toward more transparency and comprehensive reporting suggests that companies are aiming to improve stakeholder confidence and align with international standards such as the Global Reporting Initiative (GRI) and the Sustainability Accounting Standards Board (SASB).

Integration of ESG Disclosures into Financial Reports: The integration of ESG (Environmental, Social, and Governance) disclosures into traditional financial reports is becoming a significant trend among companies. This approach provides a more unified and comprehensive view of a company’s overall performance by combining financial metrics with non-financial sustainability data. By embedding ESG information into financial reporting, companies can demonstrate how sustainability initiatives impact financial health, risk management, and long-term value creation. This integration helps investors, stakeholders, and regulators understand a company’s holistic performance, including its environmental impact, social responsibility, and governance practices. It aligns with the growing demand for transparency and accountability, enabling stakeholders to make more informed decisions. Moreover, integrated reporting supports the transition towards sustainable and responsible investment by highlighting how ESG factors contribute to the company’s strategic goals and financial stability.

Companies adopting integrated reporting increasingly align their practices with global frameworks such as the International Integrated Reporting Council (IIRC) and the Global Reporting Initiative (GRI). These frameworks encourage organizations to disclose how their governance, strategy, and prospects lead to value creation over the short, medium, and long term. As a result, integrated reporting is becoming a vital tool for companies to articulate their sustainability story, connect ESG performance with financial outcomes, and enhance their reputation among socially conscious investors and consumers.

Growing Adoption of Digital Tools for ESG Data Management and Reporting: The adoption of digital tools and technologies for ESG data management and reporting is accelerating, driven by the need for enhanced data accuracy, consistency, and real-time stakeholder engagement. Digital platforms, including cloud-based systems, AI-powered analytics, and blockchain technology, are increasingly being used to automate the collection, verification, and reporting of ESG data. These tools enable companies to streamline the ESG data management process, reduce the risk of human error, and ensure that the reported data is reliable and verifiable.

By leveraging advanced digital tools, companies can gain deeper insights into their ESG performance, identify areas for improvement, and make data-driven decisions to enhance sustainability efforts. For instance, AI and machine learning algorithms can analyze vast datasets to uncover trends, predict future risks, and optimize resource allocation for sustainability initiatives. On the other hand, Blockchain technology offers enhanced transparency and traceability of ESG data, helping to prevent greenwashing and build trust among stakeholders.

Furthermore, digital tools facilitate more dynamic and interactive ESG reporting, enabling companies to communicate their sustainability performance more effectively to various stakeholders, including investors, customers, employees, and regulators. Real-time dashboards, interactive reports, and data visualization tools allow stakeholders to explore ESG data more engaging and meaningfully, fostering a deeper understanding and commitment to sustainability goals. The growing use of digital tools for ESG management transforms the sustainability landscape, enabling companies to operate more efficiently, enhance stakeholder trust, and achieve better sustainability outcomes.

Most companies have identified opportunities to improve their environmental impact by adopting energy-efficient technologies and practices. Examples include using LED lighting and R32 refrigerants for air conditioning, participating in the Earth Hour project, and adopting work-from-anywhere arrangements to reduce office energy consumption (Company 1, 15, 20).

The focus on disclosing direct (Scope 1), indirect (Scope 2), and other indirect (Scope 3) GHG emissions (Company 7, 18) indicates a growing emphasis on carbon footprint reduction and climate action. Companies are considering measures like purchasing carbon credits, using renewable energy sources and implementing eco-friendly office supplies. Waste management and recycling have also emerged as key areas, with companies exploring initiatives to sort waste, recycle paper, and use recyclable packaging (Company 2, 10, 16).

This shift is driven by a growing recognition of the critical role that environmental sustainability plays in a company’s long-term viability and societal impact. Companies are moving beyond compliance with environmental regulations and proactively integrating sustainable practices that contribute to a low-carbon economy, resource efficiency, and climate resilience. One major trend is the adoption of comprehensive strategies to reduce greenhouse gas (GHG) emissions across Scope 1 (direct emissions), Scope 2 (indirect emissions from energy consumption), and Scope 3 (other indirect emissions, such as those from supply chains and business travel). Companies are increasingly setting ambitious targets to achieve net-zero emissions and are implementing innovative solutions, such as transitioning to renewable energy sources, optimizing energy efficiency in operations, and investing in carbon offset projects like reforestation and carbon capture. This trend reflects a broader commitment to aligning corporate strategies with global climate goals, such as those outlined in the Paris Agreement.

Another significant focus is on enhancing waste management and promoting a circular economy. Companies are looking at innovative ways to reduce waste generation, recycle materials, and upcycle by-products into valuable resources. For example, many firms are adopting zero-waste-to-landfill goals, investing in recycling and composting infrastructure, and collaborating with suppliers and customers to minimize waste throughout the product lifecycle.

Additionally, there is a growing emphasis on designing products and packaging that are recyclable, biodegradable, or made from recycled materials, thereby reducing the environmental footprint of products and services. Biodiversity and ecosystem restoration are increasingly recognized as critical components of corporate environmental strategies. Companies are taking steps to minimize their impact on natural habitats and ecosystems by adopting sustainable land-use practices, supporting conservation efforts, and restoring degraded ecosystems. This may involve initiatives like reforestation, marine conservation, and creating green spaces around company facilities. The goal is to mitigate environmental harm and enhance ecosystem services that are vital for business continuity and community well-being.

The analyses show that companies from all sectors in this study increasingly focus on enhancing employee welfare and social well-being. Many firms (i.e., Company 3, 5, 6, 14, 16, 19) are considering providing additional benefits to full-time employees that are not available to temporary or part-time employees. These benefits may include course fees, rental allowances, work-from-home allowances, leave for religious activities, transportation services, and facilities for working parents.

Health and safety management is a critical focus area, with initiatives like annual health checks, digital platforms for health advice, and occupational health services such as online medical consultations and fitness programs (Company 1, 2, 10, 13). Besides, Thai companies also invest in employee skills development through talent development programs, upskilling grants, job rotation, and digital/mobile learning platforms (Company 4, 16).

Increasing reliance on digital health and wellness platforms to enhance employee well-being and provide remote health services. A significant emerging trend in employee well-being is the growing reliance on digital health and wellness platforms. These platforms are transforming how companies deliver health services and promote wellness among employees, especially in a more distributed and remote workforce. Digital health platforms offer various services, including virtual consultations with healthcare professionals, mental health support through apps and online counseling, fitness tracking, stress management programs, and personalized wellness plans. By leveraging technology, companies can create a more engaging and personalized approach to employee well-being, ultimately leading to higher satisfaction, reduced absenteeism, and increased productivity.

Another key trend is the growing emphasis on fostering inclusive workplaces that accommodate the diverse needs of all employees, including those working part-time, on a contractual basis, or in remote settings. Companies recognize that inclusivity is not just about diversity in terms of gender, race, or ethnicity but also about creating an environment where all employees feel valued, respected, and supported, regardless of their work arrangements or personal circumstances.

To achieve inclusion in the workplace, some organizations are implementing comprehensive diversity, equity, and inclusion (DEI) strategies that address various dimensions of diversity, such as age, disability, sexual orientation, and family status. This involves revisiting policies and practices to ensure they are inclusive and equitable. Companies from energy, banking and finance, and manufacturing industries are introducing flexible work arrangements that accommodate employees’ needs, such as remote work options, flexible hours, job-sharing, and extended parental leave. These policies help employees balance work and personal responsibilities more effectively, fostering a sense of belonging and engagement. Inclusive workplaces also focus on providing equal access to professional development opportunities and career growth. Companies offer targeted training and mentorship programs for underrepresented groups, ensuring that all employees have the tools and support they need to advance in their careers. Creating safe spaces and support networks within the organization, such as employee resource groups (ERGs) and diversity councils, enables employees to voice their concerns and contribute to an inclusive culture.

Strengthening governance practices is a key opportunity area identified by many companies in this study. This includes establishing ethics and risk management frameworks, such as policies, procedures, whistleblowing channels, and awareness programs (Company 8, 9, 17, 19). Companies in this study also focus on supplier screening using social and environmental criteria, which involve assessing material risks, establishing supplier codes of conduct, and initiating supplier change management programs (Company 6, 9, 17).

Managing corruption and ensuring transparency in actions taken remain priorities for many Thai firms in this study. This involves setting up committees, developing anti-corruption policies, and creating reporting channels (Company 2, 8, 9, 16).

A significant trend in ESG governance is developing and implementing comprehensive governance frameworks that align with international standards and best practices. Companies are increasingly adopting frameworks such as the United Nations Global Compact (UNGC), the OECD Principles of Corporate Governance, the International Integrated Reporting Framework, and the Global Reporting Initiative (GRI) to ensure that their governance practices meet global expectations. These frameworks guide critical governance areas, including board composition and diversity, executive compensation, anti-corruption measures, stakeholder engagement, ethical conduct, and transparency in reporting.

By aligning with these global standards, companies can establish a solid governance foundation that promotes ethical behavior, accountability, and transparency. This alignment helps in setting clear policies, procedures, and controls that govern the organization’s conduct, including its decision-making processes, risk management, and stakeholder interactions. For example, companies are increasingly setting up dedicated committees at the board level, such as audit, risk, and sustainability committees, to oversee specific governance areas and ensure alignment with best practices.

Moreover, comprehensive governance frameworks encourage organizations to adopt a stakeholder-centric approach, moving beyond shareholder primacy to consider the interests of all stakeholders, including employees, customers, suppliers, communities, and regulators. This shift enhances corporate accountability and fosters stronger relationships with stakeholders, leading to improved reputation, investor confidence, and social license to operate.

Another emerging trend is the integration of sustainability considerations into risk management frameworks. Companies are moving beyond traditional risk management approaches that primarily focus on financial and operational risks to incorporate a broader range of environmental, social, and governance risks. This integrated approach recognizes that sustainability-related risks, such as climate change, resource scarcity, regulatory changes, and social inequality, can have profound impacts on a company’s operations, reputation, and financial performance.

Companies are embedding sustainability into their enterprise risk management (ERM) processes to enhance resilience and long-term value creation. This involves identifying, assessing, and mitigating sustainability-related risks alongside conventional risks. For instance, companies are increasingly conducting climate risk assessments to evaluate the potential impacts of physical risks (such as extreme weather events) and transition risks (such as policy shifts toward a low-carbon economy) on their business operations and supply chains. These assessments help companies develop strategies to mitigate risks, such as investing in climate-resilient infrastructure, diversifying supply chains, or transitioning to renewable energy sources.

In addition to risk assessments, companies also incorporate scenario analysis and stress testing into their risk management practices to evaluate how different ESG-related scenarios could affect their business. This forward-looking approach allows companies to prepare for various possible futures, ensuring they remain agile and adaptive in the face of uncertainty.

More than half of the companies in this study have highlighted opportunities to invest in community in conjunction with economic development. This includes supporting infrastructure investments and services for local businesses or groups, such as start-up incubation, social entrepreneurship, and community services (Company 5, 8, 14, 18, 19).

It is quite common for business organizations in this study to recognize the value of managing significant indirect economic impacts by engaging in public education seminars and informal activities, providing products and services to disadvantaged groups, and supporting community development programs (Company 10, 11, 13, 18). Companies are also exploring initiatives to promote local economic development by spending on local suppliers and engaging in habitat protection and restoration efforts (Company 11, 14).

Promoting community and economic development reveals a significant alignment between corporate investment strategies and local community needs. A notable trend is the increasing recognition among businesses of the importance of investing in community infrastructure and services to foster economic development. This includes start-up incubation, social entrepreneurship, and community services, which are essential for nurturing local businesses and enhancing economic initiatives’ resilience. Companies are increasingly viewing these investments not merely as corporate social responsibility (CSR) efforts but as integral components of their business models that can lead to sustainable economic growth. Enhanced focus on creating shared value by aligning business strategies with societal needs, such as inclusive growth and community resilience. Growing participation in collaborative initiatives with non-governmental organizations (NGOs) and other stakeholders to drive sustainable development.

Another significant trend is the focus on local economic development through the support of local suppliers and engagement in habitat protection and restoration efforts. This trend reflects a growing awareness of the interconnectedness of local economies and the broader ecological context in which they operate. By prioritizing local sourcing and environmental sustainability, companies contribute to the local economy and enhance their supply chain resilience. This approach aligns with global sustainability goals and reflects a broader commitment to responsible business practices considering environmental and social impacts alongside economic outcomes.

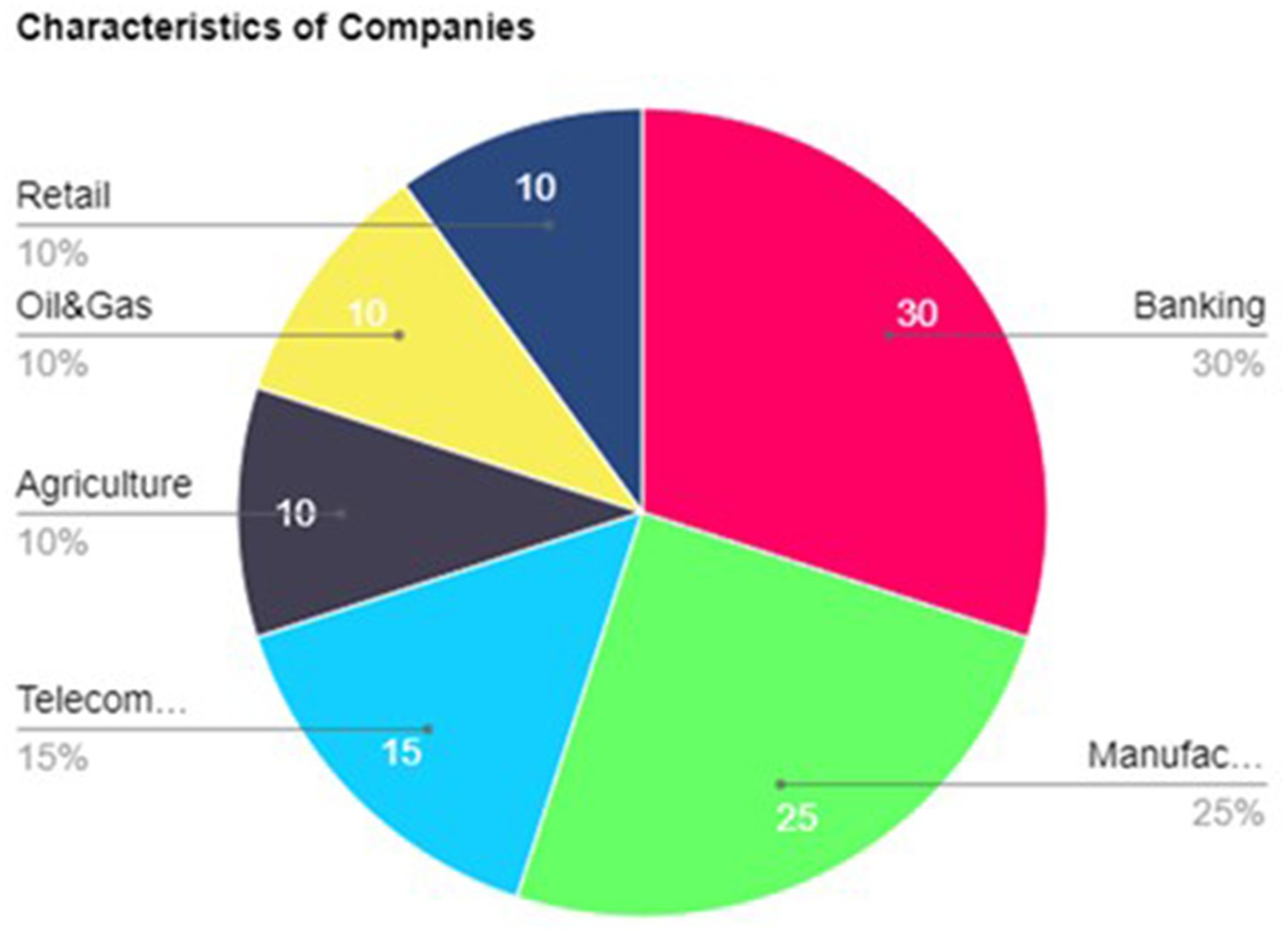

In recent years, companies in Thailand have increasingly prioritized Environmental, Social, and Governance (ESG) practices, with a strong focus on transparency and accountability in their reporting. According to recent data, leading Thai companies, on average, reported 93 disclosures, covering 63% of the 148 disclosures specified in the Global Reporting Initiative (GRI) 2020 standards. This indicates a significant commitment to adhering to global ESG standards and ensuring comprehensive disclosure across various areas of their operations. Chart One identifies the industry’s characteristics selected for study in this project.

Companies in this study are from the banking and finance sector (30%), followed by manufacturing (25%) and telecommunication (15%) sectors. The average years in business are 55 years. Figure 1 illustrates the characteristics of companies (by industry) in this study. In ESG reporting, the “G” pertains specifically to governance-related disclosures critical for stakeholders assessing an organization’s sustainability performance. The Global Reporting Initiative (GRI) Universal Standards, exceptionally GRI 102, provide a structured framework for organizations to disclose governance-related information, enhancing transparency and accountability. GRI 102 is a foundational standard that outlines the general disclosures required from organizations, including those related to governance. This standard encompasses essential information about the organization’s governance structure, such as the board’s composition, the governance bodies’ roles and responsibilities, and the processes employed to manage economic, environmental, and social impacts. Including these disclosures is vital, as they allow stakeholders to evaluate how governance practices influence the organization’s sustainability efforts and overall accountability.

Figure 1. Characteristics of companies.

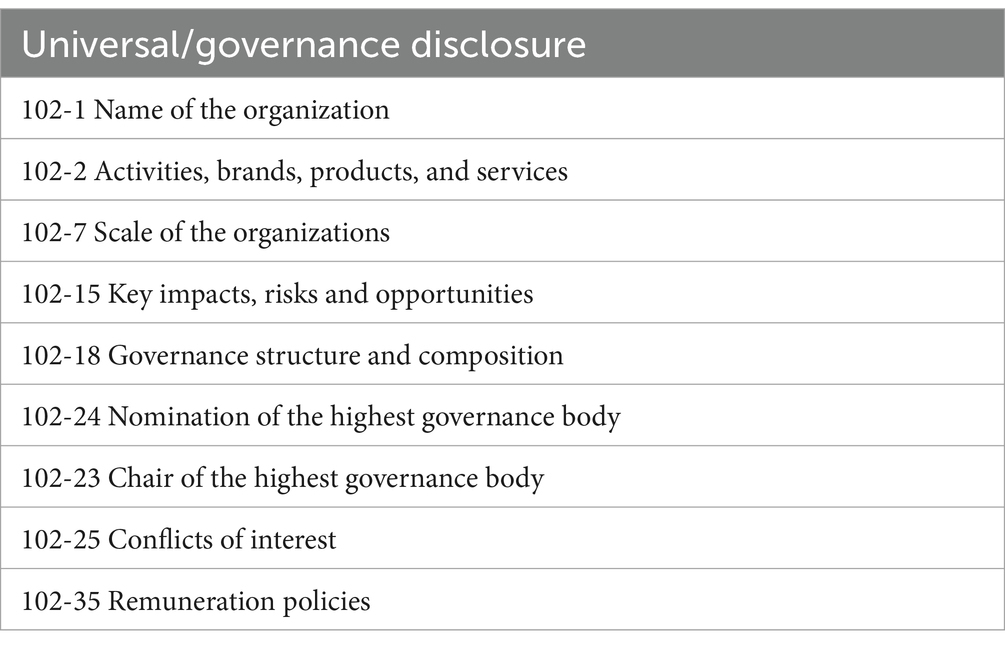

Regarding universal topic (100), some disclosures related to key business functions and activities are reported by all companies (e.g., organization activities, brands, products, and services) or the majority (e.g., key impacts, risks, and opportunities). The last reported disclosure is 102-34: Nature and a total number of critical concerns (only reported by 15%). This section (GRI 102) clarifies the governance structure, composition, roles, and remuneration. This information is crucial to ensure the accountability of governance bodies and senior executives regarding sustainable development and the organization’s impact on the economy, environment, and people, including human rights.

Regarding the governance of the organizations (along with universal topic[100]), some disclosures related to key business functions and activities are reported by all companies (e.g., organization activities, brands, products, and services) or the majority (e.g., key impacts, risks, and opportunities). All companies in this study focus on GRI 102. This standard includes information about the organization’s governance structure, including the board’s composition, governance bodies’ roles, and the processes for managing economic, environmental, and social impacts. This part is important in communication since these disclosures encompass the organization’s governance structure, practices, and policies, which are critical for stakeholders to evaluate the organization’s sustainability performance and commitment to responsible governance.

Furthermore, key governance activities were examined in relation to firms’ ESG actions. These governance mechanisms are critical in ensuring the accountability of senior executives and corporate boards regarding sustainable development and the organization’s overall impact on the economy, environment, and society. By analyzing governance disclosures, the author can assess how firms integrate ESG principles into their decision-making processes, corporate policies, and risk management frameworks.

Table 2 presents key governance and universal topics reported by all companies (100%) in this study. This structured approach enhances transparency and provides valuable insights into corporate governance practices, ensuring that ESG commitments translate into measurable actions rather than symbolic compliance.

Table 2. Key universal/governance disclosure by Thai firms.

The key theme under universal and governance disclosure is the necessity for transparency in reporting governance structures and practices. The disclosures related to governance, such as the composition of boards, roles, and remuneration, are essential for stakeholders to understand how decisions are made within organizations.

Interestingly, among the various disclosures outlined in GRI 102, the least reported is 102-34, which pertains to the nature and total number of critical concerns faced by the organization, with only 15% of companies reporting this information. This low reporting rate highlights a potential gap in transparency regarding the governance challenges organizations encounter, which could be crucial for stakeholders seeking a comprehensive understanding of governance dynamics.

The necessity for transparency in reporting governance structures and practices emerges as a key theme within both universal and governance disclosures. Disclosures related to governance, such as board composition, roles, and remuneration, are essential for stakeholders to understand how decisions are made within organizations. This transparency not only enhances stakeholder trust but also ensures that ESG commitments translate into measurable actions rather than mere symbolic compliance.

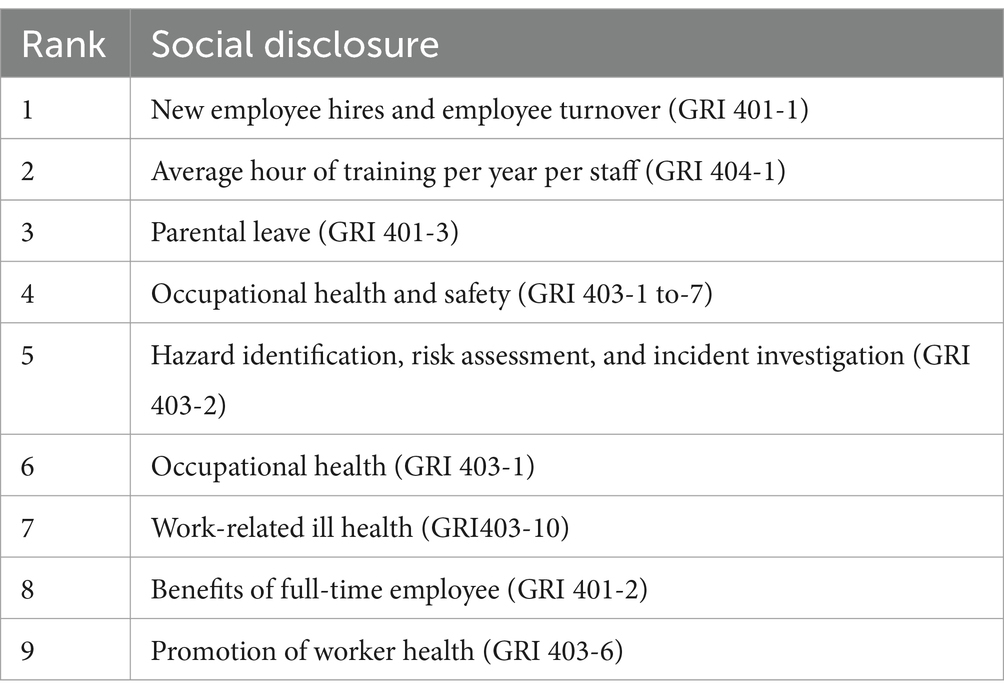

Table 3 illustrates ranking of GRI social disclosures among top Thai companies. It highlights key areas of workforce and workplace reporting. The most frequently disclosed topics focus on employee management, training, and workplace safety, reflecting corporate priorities in human capital development and occupational health and safety. Companies emphasize workforce stability through reporting on new hires, turnover (GRI 401-1), and parental leave (GRI 401-3), while also investing in employee growth by disclosing average training hours per staff (GRI 404-1). Workplace health and safety remain central, with disclosures on occupational health policies (GRI 403-1 to 403-7), hazard identification (GRI 403-2), and work-related ill health (GRI 403-10). Additionally, businesses report on employee welfare through benefits for full-time staff (GRI 401-2) and initiatives promoting worker health (GRI 403-6), though these areas receive comparatively less attention.

Table 3. Key social disclosure by Thai Firms.

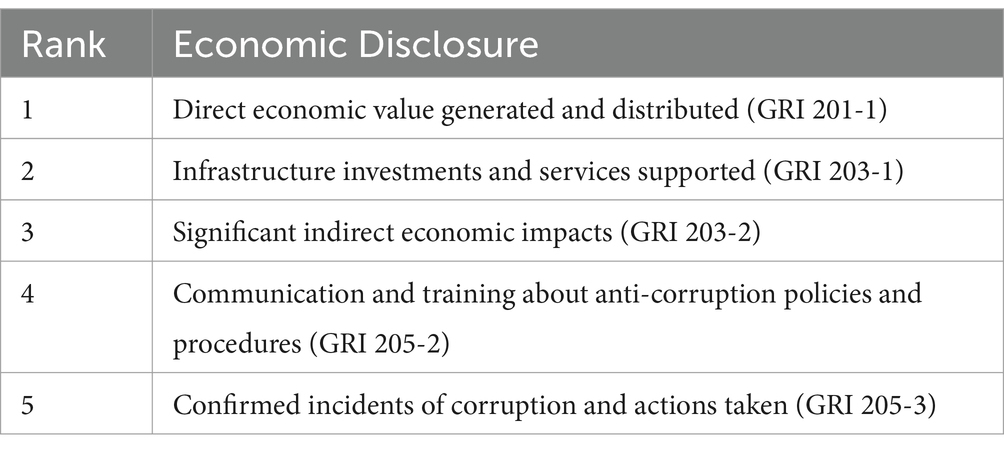

Conversely, economic topics received the least attention, with only 38.24% of relevant disclosures being covered. Despite this, certain economic disclosures, such as anti-corruption training (205-02) and direct economic value generated and distributed (201-01), were widely reported by the majority of leading companies, underscoring the ongoing efforts to address critical economic issues like corruption and economic impact. Table 4 illustrates key economic issues among Thai firms in this study. Table 4 illustrates top economic disclosure.

Table 4. Key economic disclosure by Thai firms.

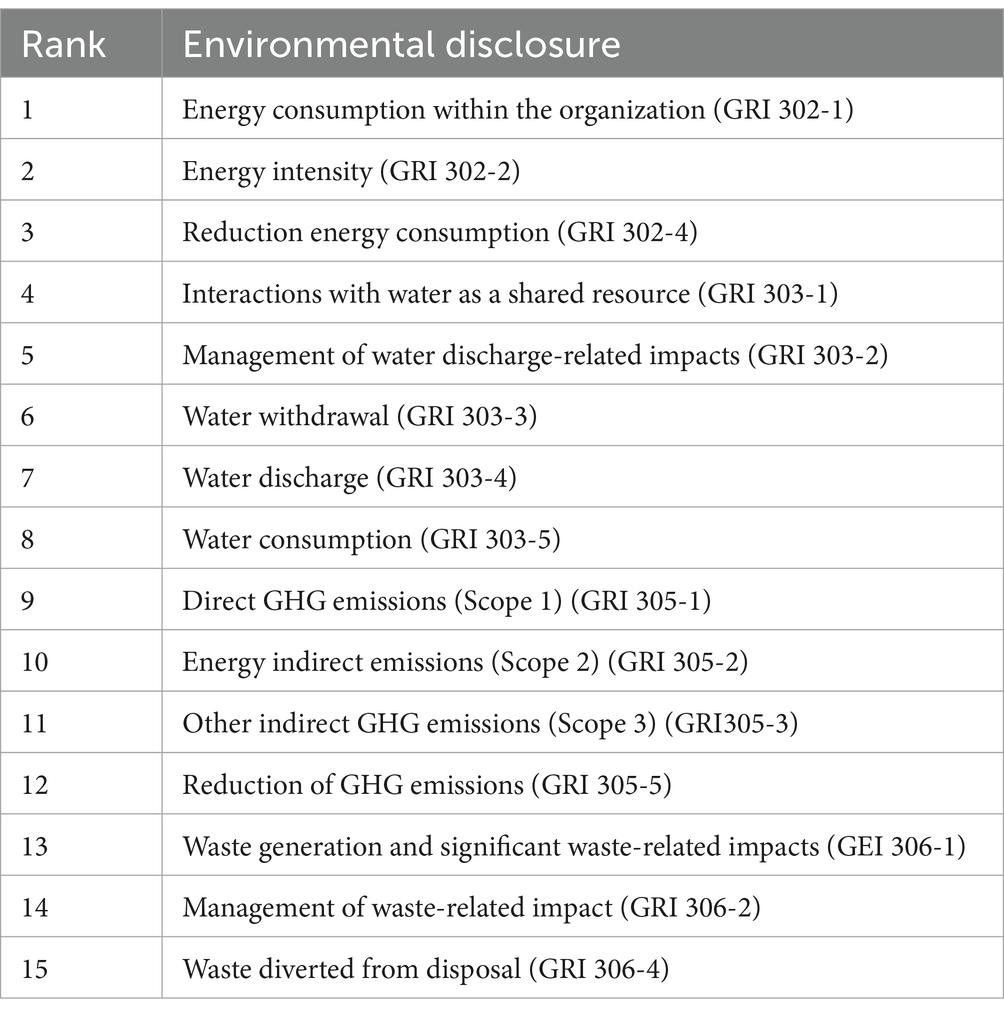

Environmental topics also saw a robust reporting trend, particularly regarding energy consumption and greenhouse gas emissions. The most commonly issues reported disclosures included energy consumption within the organization (302-01) and energy indirect (Scope 2) GHG emissions (305-02), covered by 95 and 90% of leading companies, respectively. However, certain areas, such as the impact on endangered species and habitats (304-04), saw significantly lower reporting rates, indicating areas where further attention and transparency may be needed. Table 5 illustrates the environmental aspects among Thai firms in this study.

Table 5. Key environmental disclosure by Thai firms.

In this study, Thai companies demonstrate a clear preference for selecting specific ESG activities to communicate to stakeholders. This tendency can be understood through the lens of agenda-setting theory, which suggests that organizations shape stakeholder perceptions by emphasizing particular topics in their communication.

The significant focus on social topics (55.75% of relevant disclosures) highlights Thai companies’ efforts to showcase their commitment to workforce development, diversity, and customer privacy. These areas resonate with growing societal concerns around equality, inclusion, and corporate responsibility in Thailand. Examples such as “average hours of training per year per employee” (404-01) and “diversity of governance bodies and employees” (405-01) illustrate a deliberate attempt to align corporate messaging with societal values and expectations.

In contrast, economic topics, reported at the lowest rate (38.24%), appear underemphasized despite their relevance to promoting economic growth. This strategic omission might reflect an effort to avoid highlighting areas where companies could face criticism or where stakeholder interest is relatively lower, such as direct financial metrics. By selectively prioritizing certain disclosures, companies manage the narrative and influence the issues stakeholders perceive as most important.

When analyzing ESG reporting across different industries in Thailand, significant variations emerge, reflecting the diverse priorities and challenges faced by each sector. Among the six industries analyzed, the manufacturing and construction sectors stand out for their comprehensive approach to ESG disclosures, reporting the most significant number of disclosures across all categories: Universal, Economic, Environmental, and Social. This indicates a strong commitment within these industries to transparency and adherence to ESG standards, likely driven by the high-impact nature of their operations and the corresponding regulatory and stakeholder scrutiny.

Manufacturing and construction lead in the total number of disclosures and surpass other industries in Universal Disclosures. These disclosures, which cover fundamental aspects such as organizational activities and governance structures, are crucial for establishing a baseline of corporate transparency. In contrast, the agriculture industry reports the fewest Universal Disclosures, suggesting that companies in this sector may face challenges or prioritize differently when it comes to foundational ESG reporting.

Regarding Economic, Environmental, and Social Topics, the telecommunications industry lags, reporting the least number of disclosures across these categories. This reflects the telecommunications sector’s unique operational and regulatory environment, where other factors take precedence over comprehensive ESG disclosure. On the other hand, industries like agriculture, banking, and financial services, and retail demonstrate a stronger focus on Environmental Disclosures. This emphasis likely stems from the direct environmental impact these sectors can have, whether through resource use, emissions, or other ecological footprints.

Interestingly, while these industries prioritize environmental reporting, others, particularly manufacturing, construction, and potential services, place a greater emphasis on social disclosures. These disclosures often relate to workforce issues, diversity, and community impact, where these industries might have more direct and immediate responsibilities. The disparities in ESG disclosure practices across industries highlight the importance of sector-specific strategies when it comes to ESG reporting. The norms and expectations within each industry provide a valuable guide for companies seeking to align with industry standards and improve their ESG performance. Companies should consider these norms as benchmarks, helping them prioritize disclosures that are most relevant to their industry while striving for comprehensive coverage across all ESG topics.

While the annual report does not explicitly address ESG communication challenges, the author draws on insights from Thai literature (Suttipun and Dechthanabodin, 2022) to understand these issues.

Since the culture of ESG reporting is still in its infancy in Thailand, companies face several key barriers and challenges that hinder their ability to provide accurate and meaningful disclosures. One of the most significant challenges is the lack of standardization in ESG reporting frameworks and methodologies. This absence of uniformity complicates the comparison and evaluation of companies’ ESG performance, making it difficult for investors and stakeholders to assess the actual sustainability efforts of firms (Zaccone and Pedrini, 2020). The author examined the structure of the top 20 companies, and they followed the traditional Global Reporting Initiative (GRI). Some of them (13 companies) also adopted the Sustainability Accounting Standards Board (SASB). The literature in this area confirms that this can lead to confusion and inconsistency in the data reported, further complicating the landscape for companies attempting to comply with these varying requirements (Lokuwaduge and Heenetigala, 2016).

Moreover, the complexity and cost associated with collecting, processing, and analyzing ESG data present substantial hurdles for companies (Suttipun and Dechthanabodin, 2022). Many organizations struggle with integrating ESG metrics into their existing reporting systems, leading to fragmented and incomplete disclosures (Chen, 2024; Matuszak-Flejszman et al., 2023). This challenge may not be as prominent for the top 20 companies. This issue, however, can be exacerbated for small and medium-sized enterprises (SMEs) in Thailand, which often lack the resources and expertise necessary to navigate the intricacies of ESG reporting. As a result, the quality of ESG data can be highly variable, undermining the credibility of the reports produced (Darnall et al., 2022).

ESG disclosure in Thailand is still voluntary, which can lead to a lack of accountability and transparency (Samborski, 2024). Companies may choose to disclose only favorable information, obscuring potential risks and challenges associated with their ESG practices.

It is important to recognize this study’s limitations, especially when using techniques such as thematic analysis and incorporation with the Global Reporting Initiative (GRI) data analyses. These restrictions are caused by methodological limitations, problems with the quality of the data, and contextual elements that may affect the results. The lack of standardized definitions and metrics for ESG assessments complicates the analysis, as different researchers may prioritize different aspects of ESG, leading to inconsistent conclusions.

Another significant drawback is the cultural setting in which ESG methods are applied. The success of ESG activities can be greatly impacted by sector-specific hazards and national culture, which can have differing effects on financial performance across various businesses. For example, although some research indicates that business financial success and ESG policies are positively correlated, other studies show that the two are negatively correlated, especially in ecologically sensitive industries. This discrepancy emphasizes the need for caution when extrapolating results from one environment to another.

Lastly, the presumption that ESG is synonymous with sustainability can also lead to misunderstandings about the true nature of ESG ratings and their implications for corporate performance.

The analysis of ESG disclosures among leading Thai companies highlights progress and significant improvement opportunities, particularly in less-reported areas. The least disclosed aspects of ESG reporting, such as critical concerns, ozone-depleting emissions, and biodiversity impacts, present opportunities for Thai companies to enhance transparency and fully address key environmental, social, and governance material topics. Leveraging tools like the S2 Sustainability Intelligence System©, Thai companies can align their reporting with global standards, ensuring they meet the rising expectations of shareholders, stakeholders, and regulators.

Since disclosing ESG activities and impacts is new to many Thai business organizations, they often report such activities in a modest, conventional way. Adopting tools such as SASB (Sustainability Accounting Standards Board) or TCFD (Task Force on Climate-Related Financial Disclosures) remains in its infancy. Regarding barriers, it is common for most organizations not to detail these challenges despite encouragement from the Stock Exchange of Thailand (SET). Future research should focus on exploring these underreported areas in greater detail, investigating the barriers Thai companies face in disclosing ESG metrics.

The study highlights significant opportunities for Thai companies to improve their ESG communication and disclosures, particularly in underreported areas. By addressing these gaps, companies can enhance their transparency and stakeholder accountability. This improvement in reporting practices aligns with global standards and fosters trust among shareholders and stakeholders. Thai firms must regularly review and update their ESG strategies in response to stakeholder feedback and emerging trends, demonstrating adaptability and responsiveness.

Several phases were undertaken in conducting the thematic analysis for this study. Initially, data was collected from various ESG disclosures to identify recurring themes and patterns. Subsequently, the data was coded to categorize the information into relevant themes, focusing on areas such as governance practices, environmental impacts, and social responsibilities. Finally, the themes were analyzed to draw insights and conclusions regarding the current state of ESG reporting among Thai companies and to identify specific areas for improvement.