Abdella K. Chebo

Abdella K. Chebo Shepherd Dhliwayo

Shepherd Dhliwayo Muhdin M. Batu3,4

Muhdin M. Batu3,4

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

REVIEW article

Front. Clim. , 07 June 2024

Sec. Climate and Economics

Volume 6 - 2024 | https://doi.org/10.3389/fclim.2024.1388444

Financial matters, corporate social responsibility (CSR), climate change, and other sustainable solutions all work in tandem. In order to provide a thorough understanding of the integration between various components during crises, it is necessary to provide knowledge of the interaction between financial, societal, and environmental aspects. In order to accomplish this, hundreds of papers were examined and presented using bibliometric analysis. The study demonstrated that, when examining financial crises in relation to CSR and climate change, sustainability issues were clearly examined. Sustainability, environmental economics, governance approaches, and sustainable development are some of the main issues in this comprehensive subject. Besides, the emerging topics that need more research include organizational resilience, global financial crises, and sustainable performance, while there are no specific themes developed in the subject matter that integrate financial crises, CSR, and climate change. Thus, future researchers need to provide new insights on the integration of these concepts.

Contrary to local crises, global crises (such as the COVID-19 pandemic, the climate change, and the 2008 financial collapse) have risen in frequency and severity (Davvetas et al., 2022). When institutions are disrupted by a financial or economic catastrophe, the organization’s future strategic course is uncertain (Lu et al., 2022). In addition, calls for a green transformation in times of crisis are not new to the COVID-19 era and were also a part of reviving the economy in the wake of the 2007–2008 Global Financial Crisis (GFC; Gunay et al., 2022). Regarding its interaction with CSR, proponents assert that it offers numerous advantages for the business, including a positive reputation; opponents counter that CSR is unable to shield a business from financial damage during difficult times (Davis, 1973). These demonstrate how climate and environmental factors are interconnected with the economic and financial crises.

Climate change is acknowledged as one of the most major sources of risk and opportunity facing the business sector in the foreseeable future as the economy emerges from the biggest financial crisis since the Great Depression (Brimble et al., 2011). Because economic growth, climate change mitigation, and other sustainable solutions do not conflict and instead support one another (Georgeson et al., 2017). Thus, it is expected that climate change will significantly alter the financial services industry (Brimble et al., 2011). Also, practically all organizations faced heightened volatility during the financial crisis, which results in high social performance being lower compared to enterprises with lower social performance. If the overinvestment theory is correct, the opposite should be seen (Bouslah et al., 2018). Then, the sustainable viability of businesses through crises becomes the main concern. Due to the fact that sustainability offers a kind of “insurance” against economic downturns (Lu et al., 2022).

Economic issues caused by COVID-19 resembled those of the 2008 financial crisis (Kaakeh and Gokmenoglu, 2022). Also, it can influence customers’ and investors’ preferences for green products, enabling businesses to transition to low-carbon production without suffering a decline in their financial performance (Guérin and Felix, 2021). At large US companies, the presence of emission reduction or climate change programs does not appear to be largely associated with financial performance, according to Petitjean (2019). They do not notice any obvious changes over time, whether or not they condition their analyses on the emergence of the financial crisis in 2008–2009.

In light of the connections between the outcomes of various crises, earlier investigations produced contentious results. For instance, during the financial crisis, companies that perform better in terms of sustainability have worse financial performance, but the marginal effects of profitability on sustainability are increased. However, sustainable businesses do better financially and are more robust during COVID-19, but the marginal effects of profitability on sustainability are reduced (Lu et al., 2022). Also, there is a good correlation between environmental performance and financial performance throughout recessions, therefore businesses must keep funding ecologically responsible and sustainable projects (Kaakeh and Gokmenoglu, 2022). Thus, strategic decisions must consequently place a high priority on understanding the nature of the relationship between environmental and financial performance during times of crisis (Petitjean, 2019) as well as social responsibilities.

Since the environmental component of CSR is frequently overlooked, Petitjean (2019) focuses on the connection between financial performance and environmental performance. However, companies now place a greater emphasis on ESG initiatives in order to rebuild their market reputation through socially responsible behavior following the GFC. The main factor behind the current financial instability worldwide is corporate scandal and accounting fraud (Dah and Jizi, 2018; Shakil et al., 2019). Given the economy’s state or when businesses are more financially strapped, CSR spending is likely to be lower since economic needs will take precedence over social ones during periods of low profitability (Bouslah et al., 2018). Besides, Bae et al. (2021) investigate the relationship between CSR and stock returns during the pandemic but find no proof of a connection. According to Branca et al. (2012), businesses invest less in CSR initiatives during adverse business cycles (such as the financial crisis; Bouslah et al., 2018). During the financial crisis, namely at times when demand for social initiatives was stronger than usual, Karaibrahimoğlu (2010) demonstrates that the number and scope of CSR projects significantly decreased (Petitjean, 2019). Similarly, according to Chiaramonte et al. (2021), participation in CSR activities was associated with greater stability (i.e., lower default risk) during the GFC. Also, Njoroge (2009) results show a clear trend in decreasing the CSR initiatives in times of crisis.

Selmi et al. (2021) claimed that investing in socially or ecologically responsible enterprises during the COVID-19 has positive outcomes, whereas Ding et al., 2021) suggested that firms with better sustainability scores are more robust. An ecologically friendly business model has a favorable impact on the firm’s financial structure even during times of crisis, like COVID-19, according to Kaakeh and Gokmenoglu (2022) extension of the current research. In this context, Demers et al. (2021) predict winning and losing stocks in the COVID-19 using a model created from data from the 2007–2008 financial crisis, but they find no proof that socially responsible businesses have better stock returns (Lu et al., 2022). These contentious findings call for more and comprehensive research.

Despite the importance of integrating GFC, CSR, and climate change, there is a scarcity of research on the integration of these concepts. For example, Jalles (2023) stated that the research on the impact of financial crises on climate change vulnerability and resilience indices is limited. Additionally, the analysis of the relationship between economic crises and CSR initiatives has been conducted separately, resulting in a gap between the two (Roman Pais Seles et al., 2018). These gaps underscore the necessity for further research and integration of GFC, CSR, and climate change to address the intricate challenges posed by these factors.

The study of the theoretical relationships between GFC, CSR, and climate change contributes to the comprehension of the difficulties encountered by companies in implementing guidelines and recommendations related to climate-related financial disclosures. It is observed that the degree of compliance with these recommendations is relatively low (Dias et al., 2023). Additionally, the impact of financial crises on climate change vulnerability and resilience indices is explored, revealing that such crises can result in a temporary deterioration in a country’s resilience to climate change, particularly in developing economies (Mandal, 2022). Furthermore, the relationship between CSR and climate risk is examined, showing that companies in countries with higher climate risks participate in more CSR initiatives, and that higher CSR reduces the impact of climate risk on performance, particularly in countries with high levels of religiosity and low levels of individualism (Jalles, 2023). Moreover, firms adjust their CSR standards upwards in response to climate change risk shocks, and the sensitivity of CSR performance to climate change risk increases after significant events such as the Stern Review and the Paris Agreement (Ozkan et al., 2022).

These study contributes to the theory in the following way. First, despite research attempting to examine the connections between the GFC, CSR, and climate change, there is no solid framework connecting these ideas. Studies are attempting to connect ideas like sustainability and sustainable development to the GFC, CSR, and climate change separately. Studies, however, could not make it clear how the combined idea of the GFC, CSR, and climate change affects these outcomes. Studying this relationship can also shed light on how CSR and climate change initiatives can influence financial stability or the reverse. This study demonstrates the possibility of connecting these ideas.

Secondly, the study highlights the significance of ideas like agro-ecology, which must be investigated in relation to the integrated idea of the GFC, CSR, and climate change. Thirdly, no other study has been conducted in these area to our knowledge. That is, the study is among the first to show significant data on the most influential sources, authors, institutions and countries. The study also identified key ideas on the topics of the GFC, CSR, and climate change as well as publication trends and thematic evolution.

Fourthly, to the practitioners, bibliometrically integrating GFC, CSR, and climate change is important since it allows for a comprehensive understanding of the relationship between these factors. The study helps in assessing the financial performance of companies in relation to their CSR practices and their ability to address climate change risks. Because, it provides a framework for evaluating the resilience of countries to climate change shocks and the effects of financial crises on their vulnerability (Bilbao-Terol et al., 2019). By integrating these three areas, policymakers, managers, investors, and stakeholders can make informed decisions and develop strategies that promote sustainable development and mitigate the adverse effects of climate change and financial crises.

Bibliometric methodologies, in contrast to conventional literature reviews, offer a comprehensive network portrayal of a study problem by scrutinizing an extensive corpus of articles within a meticulous database employing expert analysis (Miao et al., 2021). This approach facilitates the assessment of the effectiveness of the knowledge generation process and its impact on the scientific milieu (Ledesma and Malave González, 2022), ultimately leading to outcomes that are characterized by enhanced objectivity (van den Besselaar and Sandström, 2020). Thus, this study used bibliometric analysis since it aids in creating accurate and pertinent knowledge structures in a certain field (Fagerberg et al., 2012). This analysis is significant because it uses quantitative analysis to examine thousands of documents and present a comprehensive network picture of the topic under investigation (Miao et al., 2021). We will therefore examine and glean insights from the vast amounts of data we have taken from the Scopus data base.

The most influential sources and authors, most productive institutions and countries, intellectual structure, social structure, and conceptual mapping are all part of the main analysis that was conducted. So, in order to present a thorough review and trends on the topic of financial crises, CSR, and climate change, this study used these particular methodologies. The study specifically provides performance analysis in the form of productions per year, the most relevant affiliations, the most relevant publications, the most relevant authors, the most relevant countries, the most cited publications, and the most relevant sources. Also, the scientific mapping used to offer co-citation analysis, co-authorship analysis, links between research parts, bibliographic coupling, and keyword occurrences.

Choosing the most appropriate bibliographic database for a bibliometric review is of utmost importance for researchers conducting review studies. The selection of a database is influenced by various factors such as coverage, ownership, selection criteria, and employed metrics. In this regard, several databases have been compared. Among these databases, Web of Science and Scopus are commonly utilized by academics. A notable distinction lies in the number of journals available in the social sciences and humanities, where Scopus outperforms (Justesen et al., 2021). Additionally, Scopus surpasses Web of Science in terms of comprehensive and extensive journal coverage (Singh et al., 2021). Given that previous studies have indicated the superior coverage of Scopus compared to the Web of Science Core Collection, and our own data cross-validation confirmed this finding (Turzo et al., 2022). Thus, we have chosen Scopus as the primary database source for this study.

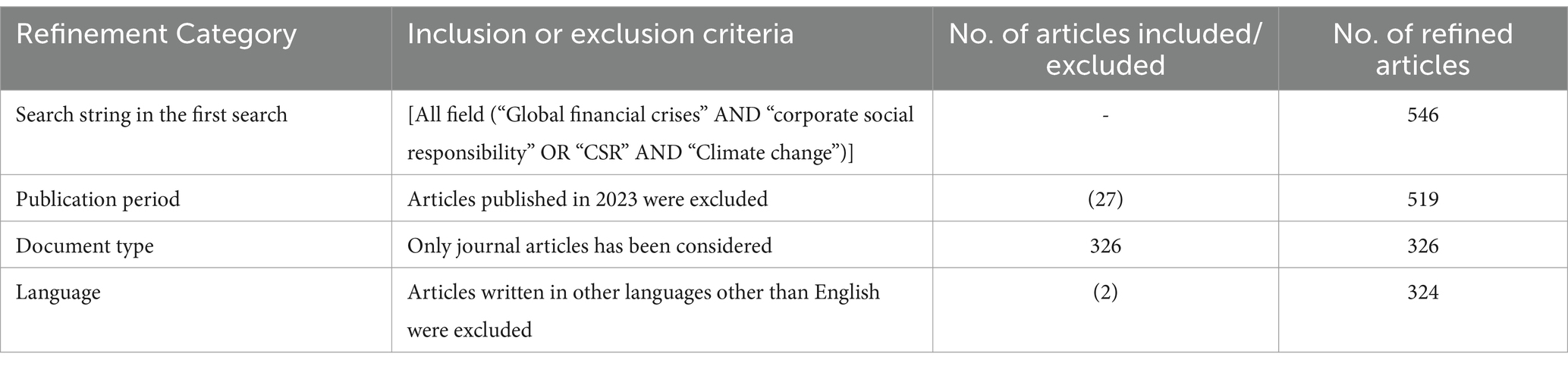

Following the selection of the Scopus data base, the search phrases “global financial crises” AND “corporate social responsibility” OR “CSR” AND “climate change” were inserted. The option to extract documents was then set to “all fields.” In general, the query is summarized as (ALL (“Global financial crises” AND “corporate social responsibility” OR “CSR” AND “Climate change”) AND (EXCLUDE (PUBYEAR, 2023)) AND (LIMIT-TO (DOCTYPE, "ar”)) AND (LIMIT-TO (SRCTYPE, “j”)) AND (LIMIT-TO (LANGUAGE, “English”))).

A total of 546 documents were found in the initial search after the key terms were entered into a database. Next, based on a set of criteria, documents are included or excluded to determine the actual size of the documents and summarized in Table 1. The year of publication is restricted to 2022 as the first exclusion condition, leaving 519 documents available until that year. Later, the search was restricted to journal articles, yielding 326 documents in total. Lastly, all publications in languages other than English have been excluded. In doing so, 324 articles remained for final analysis. Finally, this documents were extracted in a form of Bibtex (.bib) and comma-separated values (CSV) file formats in the form required for the software to undertake bibliometric analysis.

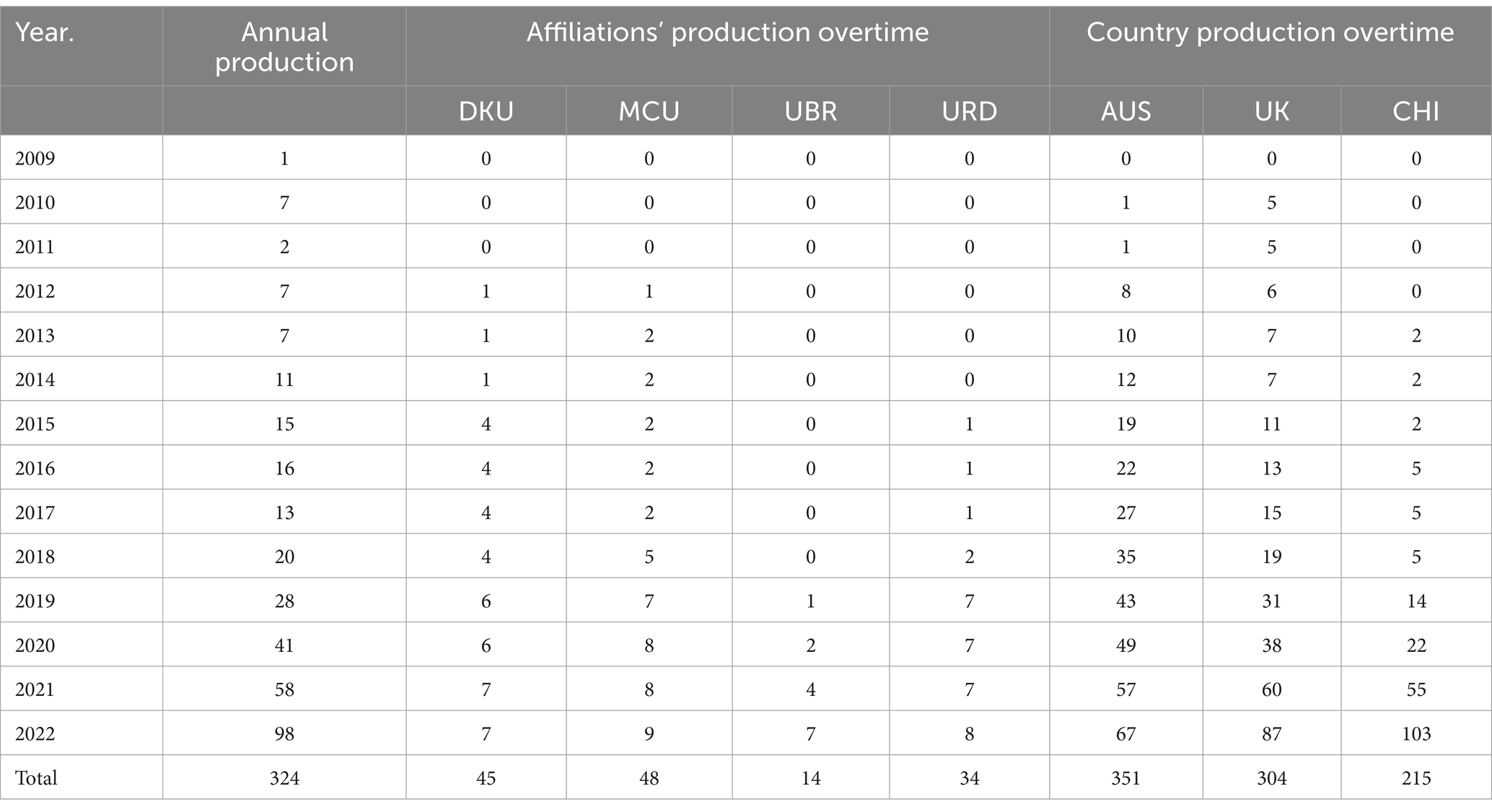

Table 1. Annual production, affiliations, and country productions overtime.

At the conclusion of the search operation, the final sample of articles was exported in the bib text and comma-separated values (CSV) file formats required by the R package software.

Both quantitative and qualitative analyses were done in this study. Many bibliometric indicators were used in this study to provide thorough understandings and insights. According to the findings of Donthu et al. (2021), bibliometric analysis employs the techniques of performance analysis and science mapping as its primary methods. This research also adopted bibliometric analysis in order to comprehensively understand the interconnected disciplines of GFC, CSR, and climate change. The performance analysis aspect of this study provides insights such as the number of publications by year, publishing productivity, influential publications, relevant affiliations, author contributions, and country of origin, as well as pertinent sources. On the other hand, the science mapping analysis encompasses co-authorship analysis, collaboration networks, and keyword co-occurrences, among other techniques.

For the purpose of conducting bibliometric analysis, the most widely used R package is bibliometrix, which has been increasingly adopted in numerous studies (Linnenluecke et al., 2020). The statistical software R studio was used to process the extracted data in order to do this. Using bibliometric coupling analysis, the R studio has been used to examine a number of features, including the conceptual framework, productivity, most important scientific actors, trending subjects, and thematic structure of the subject. To convert the dataset into R format, perform accurate bibliometric analysis, and create matrices for various characteristics, the “biblioshiny” package is specifically employed. Co-citation analysis, co-authorship analysis, keyword analysis, networking analysis, and conceptual analysis are generally included in the analysis conducted.

The finding in Table 2 shows that the study of financial crises in relation to CSR and climate change is a relatively new area that is rapidly growing. The first paper is released in 2009, in the wake of the financial crisis of 2008. After that time, there is a lot of interest in the subject. Yet, the number of scientific production is sufficient given the rising interest of researchers and the significant concerns on the topic of financial crises, CSR, and climate change. In the last 5 years, 75.62% of publications have been made, and 2022 will be a productive year for publications. This shows that, because to increased global uncertainty, the significance of studying financial crises in relation to CSR and climate change has grown. This trend is projected to continue in the future. Further understanding is still being sought by the researchers. Additionally, the relationship between financial crises and CSR as well as climate change is a new area of research that calls for in-depth comprehension and ground-breaking discoveries in the scientific community.

Table 2. Search strategy.

The top four affiliated institutions are University of Birmingham (n = 14), Macquarie University (n = 48), Deakin University (n = 45), and University of Reading (n = 34; Table 1). Recently, Macquarie University released the most documents among these institutions’ annual output, followed by University of Reading. In addition, Australia (n = 351), the United Kingdom (n = 304), and China (n = 215) are the top three most productive countries.

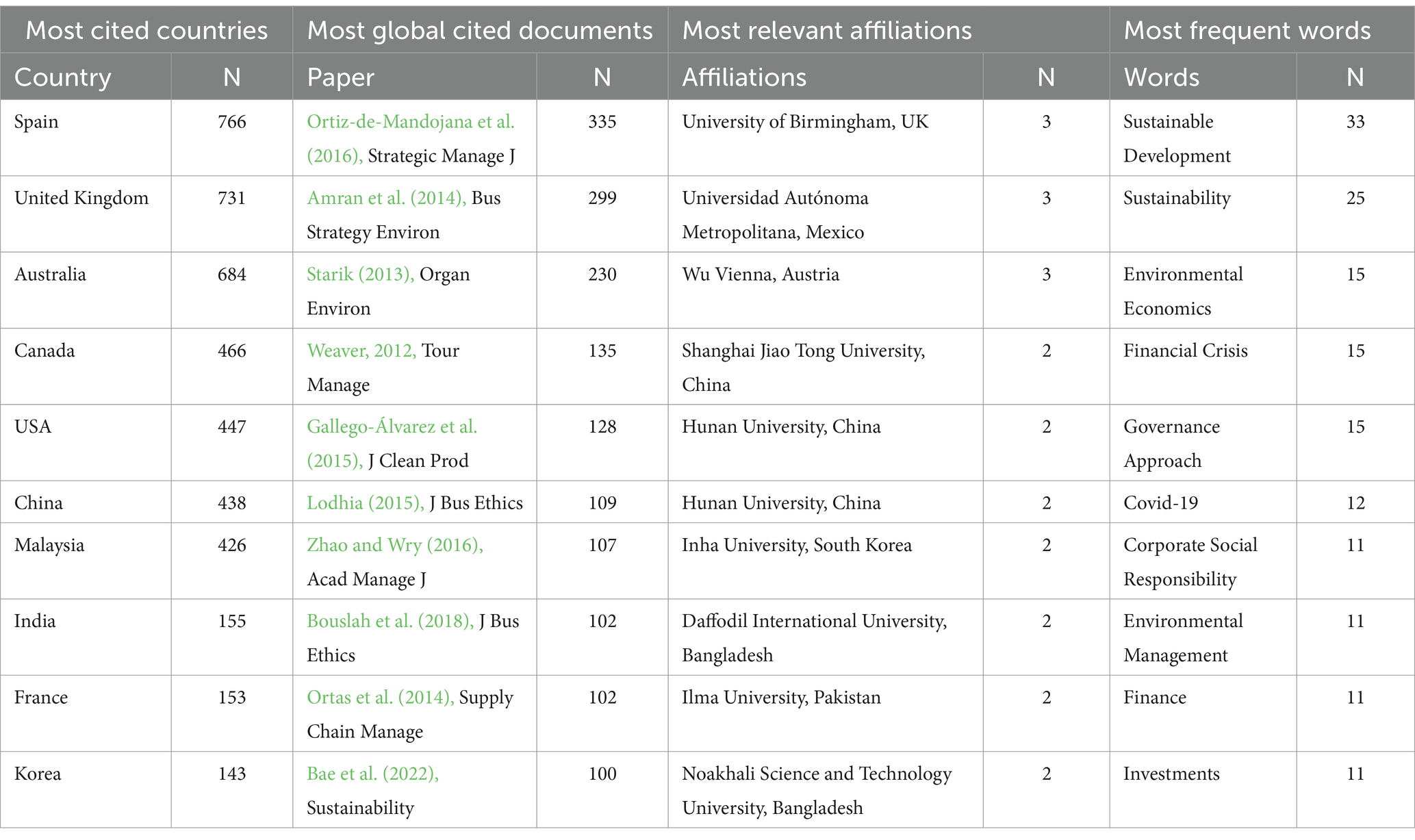

Table 3 showed that Spain, the United Kingdom, and Australia are the most productive nations in the field of combining financial crises with CSR and climate change, with total citation counts of 766, 731, and 648, respectively. The fact that European nations are the most frequently cited demonstrates the continent’s production of relevant literature on the topic. Yet, because western countries dominate the field, it is understudied in African and Asian countries. This shows that these countries are keen on finding out about financial crises in order to comprehend the topic and create effective strategies to deal with issues brought on by financial crises.

Table 3. Top 10 most relevant countries, documents, affiliations, and most frequent words.

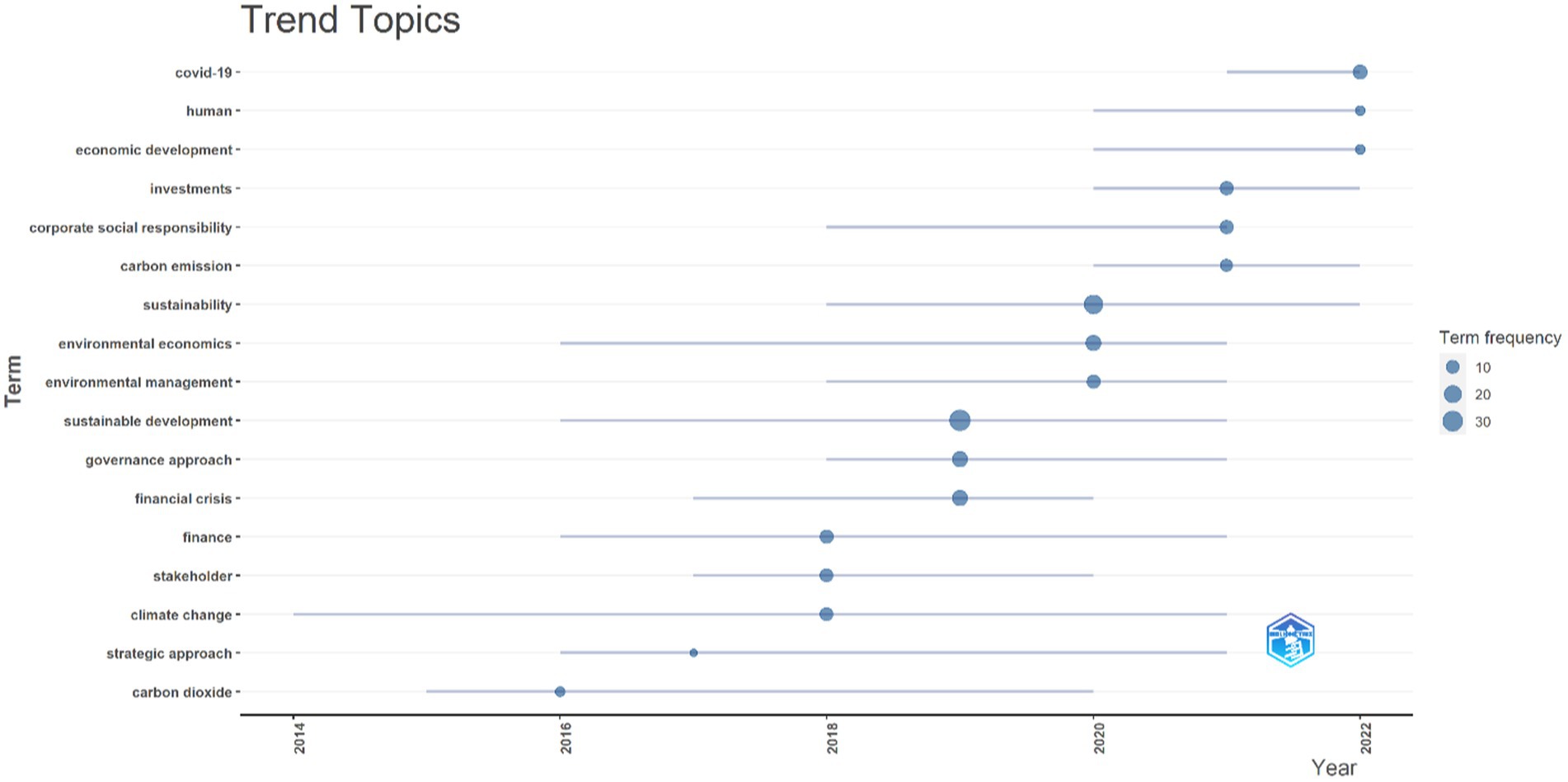

Table 3 analysis of the relevant documents reveals that Ortiz-de-Mandojana et al. (2016), which obtained 335 total citations, received the most. This was followed by Amran et al. (2014), which received 299 citations, and Starik (2013), which received 230 citations. While the next two documents were published in Business strategy and environment and Organization and environment, respectively, Ortiz-De-leading Mandojana’s publication is in the strategic management journal. Also shown in Table 1 are the most relevant affiliations. With a total of three papers each, the top three institutions are University of Birmingham, Universidad Autónoma Metropolitana, and Wu Vienna. Also, Table 1 showed the frequency of keyword occurrences. The most often used terms were Covid-19 (n = 12), Environmental Economics (n = 15), Financial Crisis (n = 15), Governance Approach (n = 15), Sustainable Development (n = 33), and Sustainability (n = 25). Besides, keywords such as Corporate Social Responsibility, Environmental Management, Finance, and Investments appeared 11 times each. They showed that experts give sustainability issues a lot of thought while researching financial crises in relation to CSR and climate change. Because sustainability and related issues will be the result of financial crises, climate change, and CSR. Financial crises have recently been closely related to COVID-19. Together with financial crises, CSR, and climate change, other issues discussed include the environment and economic factors like investment and financing.

The study’s main themes are terms like “sustainable development” and “sustainability.” As such, the research that incorporates GFC, CSR, and climate change is concentrating on how they relate to sustainability issues. The term financial crises are not sufficiently occurred. Contrarily, the financial markets, strategic approach, planning, and institutional framework are some of the terms that happen the least frequently. However, research on the financial crises, CSR, and climate change is required from both a micro and institutional perspective. This, there is a need to understand the integration of the above concepts.

The various scientific mapping analysis undertaken in this section includes co-citation network analysis, keywords co-occurrence network, and country collaboration network.

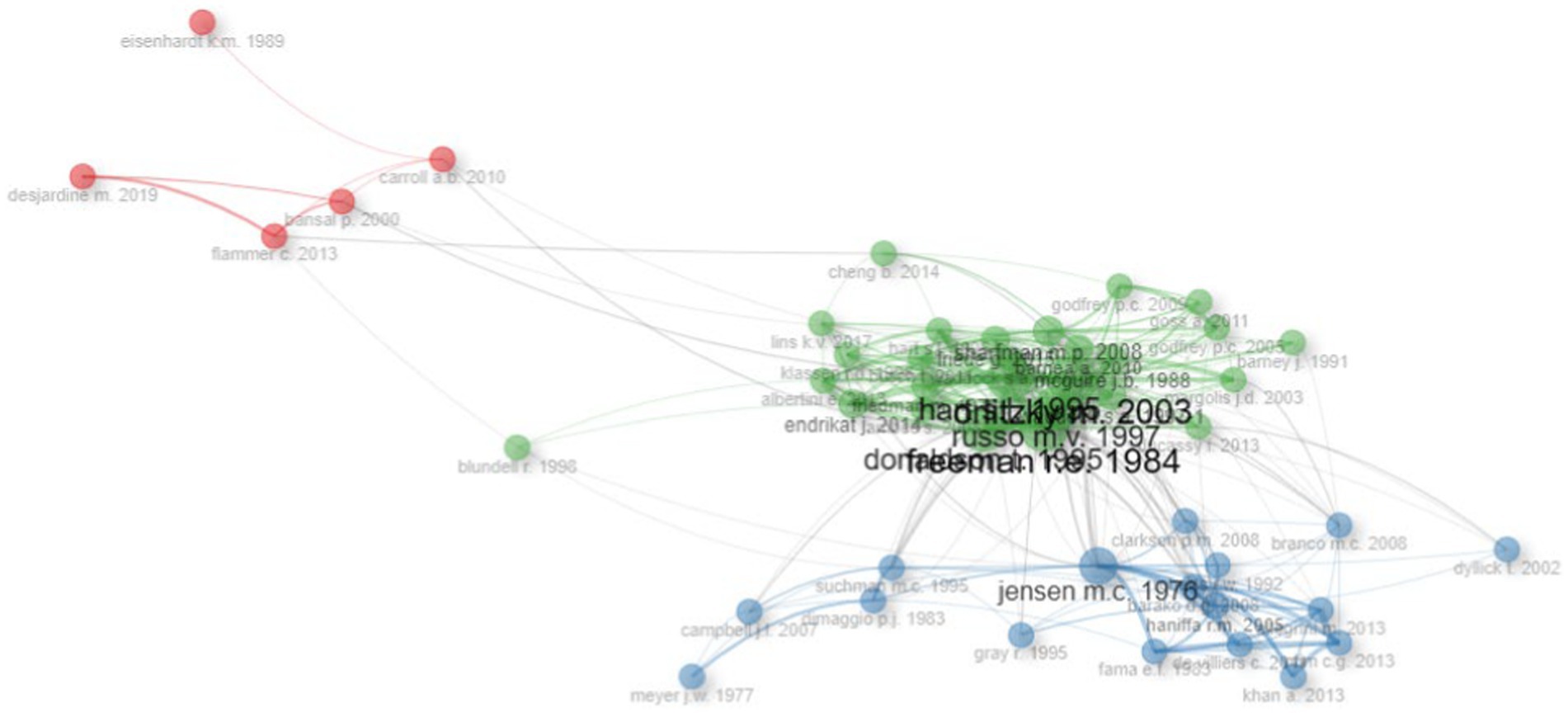

The co-citation analysis identifies three clusters, as shown in Figure 1. Carroll and Shabana (2010) anchor the first cluster, which has four co-authors and is highlighted in red. Carroll and Shabana (2010) give a succinct overview of the changing perspectives on CSR with a focus on business cases. They stated that when CSR programs yield direct and obvious links to corporate financial performance, a limited perspective of the business rationale justifies them. The business case is typically viewed narrowly, with an emphasis on immediate cost savings. Contrarily, when CSR programs result in both direct and indirect links to firm performance, the wide view of the business case validates them. From this cluster, Des Jardine et al. (2019) focused on investigation of the 2008 GFC impact on the development of resilience through social and environmental practices. They contend that strategic rather than tactical social and environmental initiatives have a greater impact on the organizational resilience. The second cluster, shown by the blue color, is anchored by Jensen et al. (1976), who looks into aspects of the theories of agency, property rights, and finance. Suchman (1995), from the same group, concentrates on combining institutional and strategic methods. The third and largest group, shown by the color green, is about strategic management with a stakeholder-focused approach, and it is centered by Freeman (1984). The other scholars from this cluster, Orlitzky et al. (2003), studied about Corporate Social and Financial Performance (Figure 2).

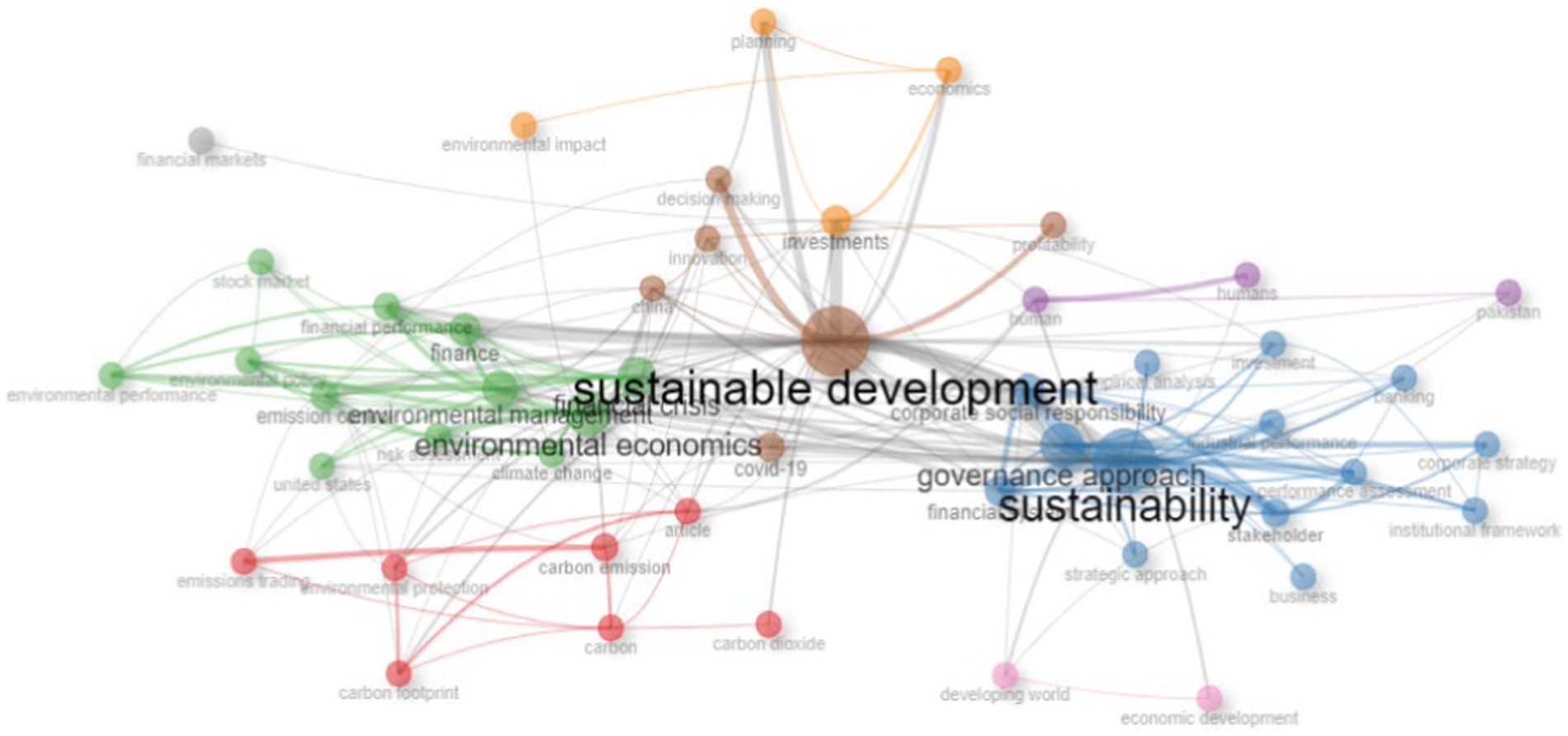

Figure 1. Word cloud of most relevant keywords.

Figure 2. Co-citation network.

The keyword co-occurrence network indicates that there are eight clusters. The first cluster represented by red color contains terms such as carbon emission, carbon, environmental protection, emission trading. This cluster indicates the importance of environmental protection in the firms CSR and climate change. In the second group represented by blue color, the term sustainability is closely connected with governance approach, corporate social responsibility, stakeholder, financial system, and corporate strategy. The third cluster is about environmental economics. The top 5 keywords in this cluster are environmental economics, financial crisis, environmental management, finance, and climate change. Thus, this focus on the linkage of concepts such as financial crises and climate change with the economic benefits obtained from proper environmental management (Figure 3).

Figure 3. Co-occurrence network.

The fourth cluster is about the human side, while the top three keywords in cluster 5 includes investments, economics, and planning. On the other hand, in cluster 6 the term sustainable development is closely linked to covid-19, decision making, and profitability. The last two clusters cluster 7 and cluster 8 deals about economic development and financial markets, respectively.

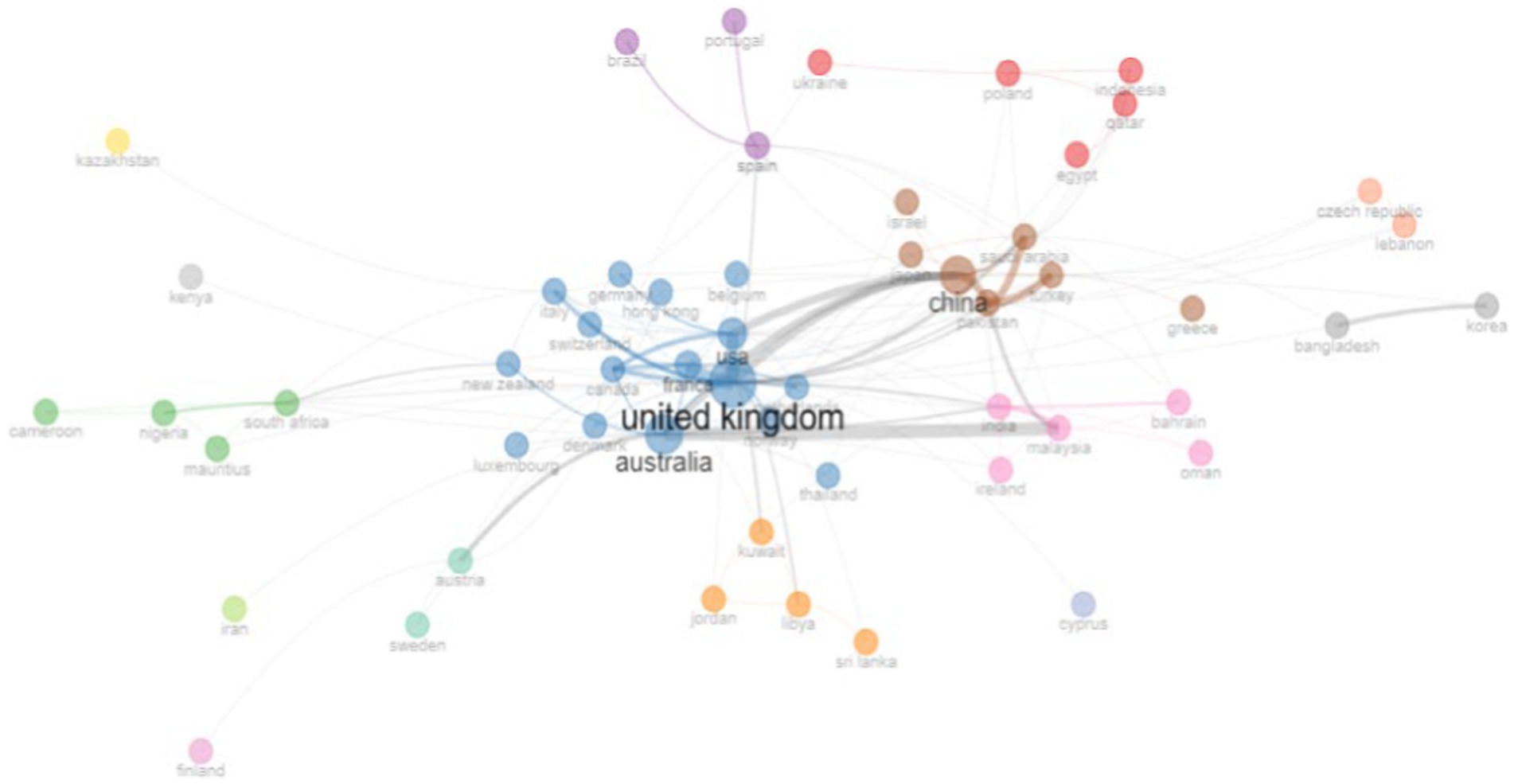

Figure 4. Country collaboration network.

Figure 4 shows the collaborative network between countries. The figure indicates that the highest collaboration which contains 16 countries is collaboration between western countries including United Kingdom, Australia, United States, France, Italy, Canada, Germany, and others. This is supported by a study by Zhang et al. (2022), who found that while existing research on corporate environmental protection behavior and corporate operation is more concentrated in developed economies, quantifying environmental disclosure in emerging markets can offer fresh perspective for global environmental governance given the growing involvement of developing countries in environmental issues. China is the leader of the second-highest collaboration among countries, which consists of seven developing countries, largely from Asia, including Saudi Arabia, Pakistan, Turkey, and China. Collaboration between nations like Indonesia, Poland, Ukraine, Egypt, and Qatar comes next. This is due to the rise in both the frequency and severity of global crises. Yet, the impact of these crises varies among nations, resulting in differences in the capacity of (inter)national crisis-regulating institutions to sustain public confidence and protect their constituents’ well-being (Davvetas et al., 2022).

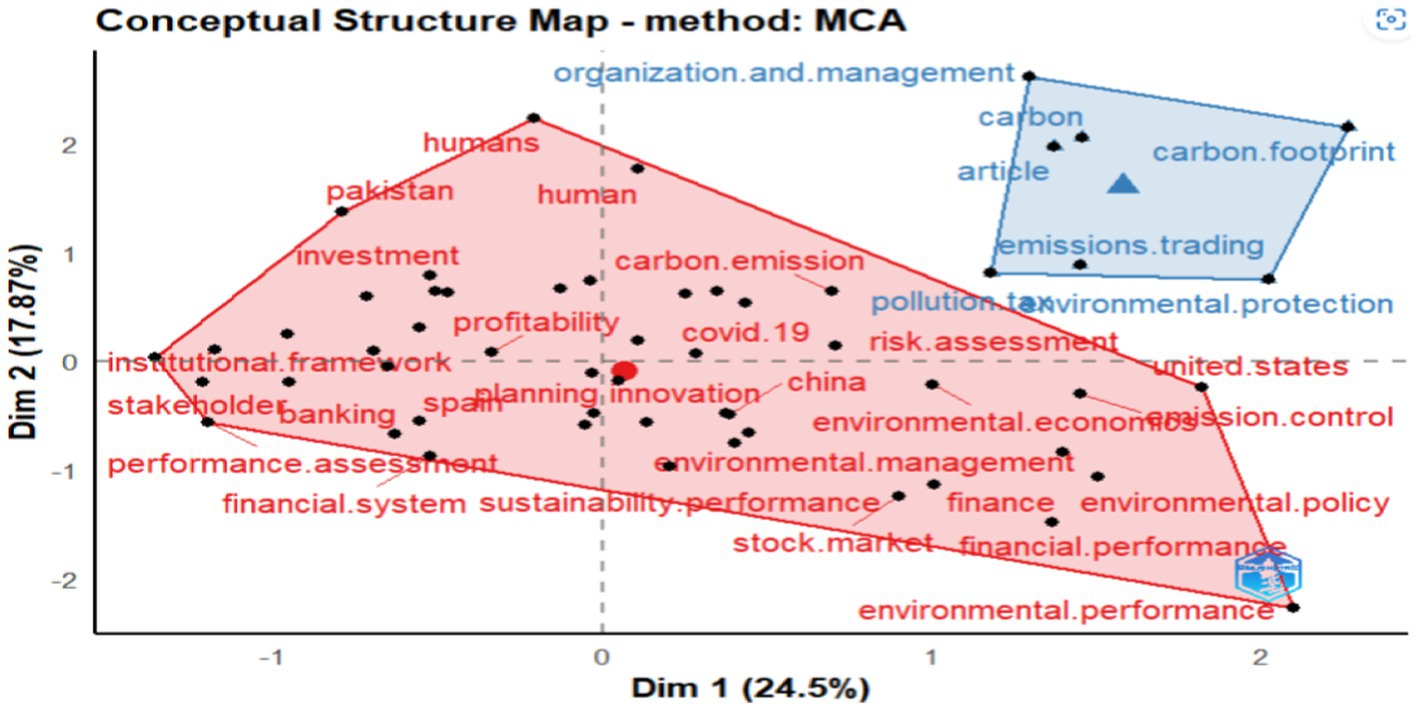

Figure 5. Conceptual structure map.

African nations including South Africa, Nigeria, Cameroon, and Mauritius are collaborating together. Also, there is cooperation among countries that speak the Latin, including Spain, Brazil, and Portugal, as well as Kuwait, Libya, Jordan, and Sri Lanka. Moreover, nations including India, Malaysia, Bahrain, Ireland, and Oman collaborated together. To sum up, the findings indicate that the collaboration is primarily regional. In other words, nations in the same region collaborate together. Although there is cooperation among developing countries of Asia and Africa, the developed western countries have the highest degree of collaboration. This might result from the developed nations’ significant financial and material investments in scientific research. The researchers form these advanced countries are also capable to collaborate and form network internationally than the developing countries.

Figure 5 presents the conceptual structure of main topics.

The conceptual structure in Figure 5 indicates that conceptually the subject that integrates financial crises with CSR and climate change is categorized to two clusters. The first strand with a high factor load contains concepts such as planning innovation, environmental economics, sustainability performance, profitability, and etc. The literature suggests that the incorporation of management activities within a company is positively related with economic and environmental performance, although there is inconsistent empirical evidence for the latter (Wagner, 2015). Integrating climate change and energy matters into the realm of business administration can be deemed as a sustainable and ecologically beneficial approach for the organization, particularly when tackled from the perspective of corporate social responsibility (CSR; Kim, 2008). To illustrate, leading companies adeptly handle the evolution pertaining to social and environmental accountability by means of amalgamating processes, management of change, fostering innovation, and devising corporate strategies (Sroufe, 2017). Particularly, innovation plays a crucial role in connecting sustainable management integration with economic and environmental performance (Hall and Wagner, 2012). Experts in the field stress the necessity for a fundamental shift in contemporary capitalism, where organizations allocate resources toward improving environmental and social performance alongside economic growth (Busch et al., 2011). Furthermore, sustainable manufacturing practices, which integrate environmental, economic, and social aspects into operational and business activities, result in improved economic sustainability, with innovation performance acting as a mediator in this relationship (Hami et al., 2015).

The second group contains concepts such as carbon footprint, environmental protection, emission trading, and etc. The second strand is more specific. Thus, it needs to be studied in integration with the first strand, in order to provide a full picture of specific issues in environmental, economic, innovation, and sustainability aspects.

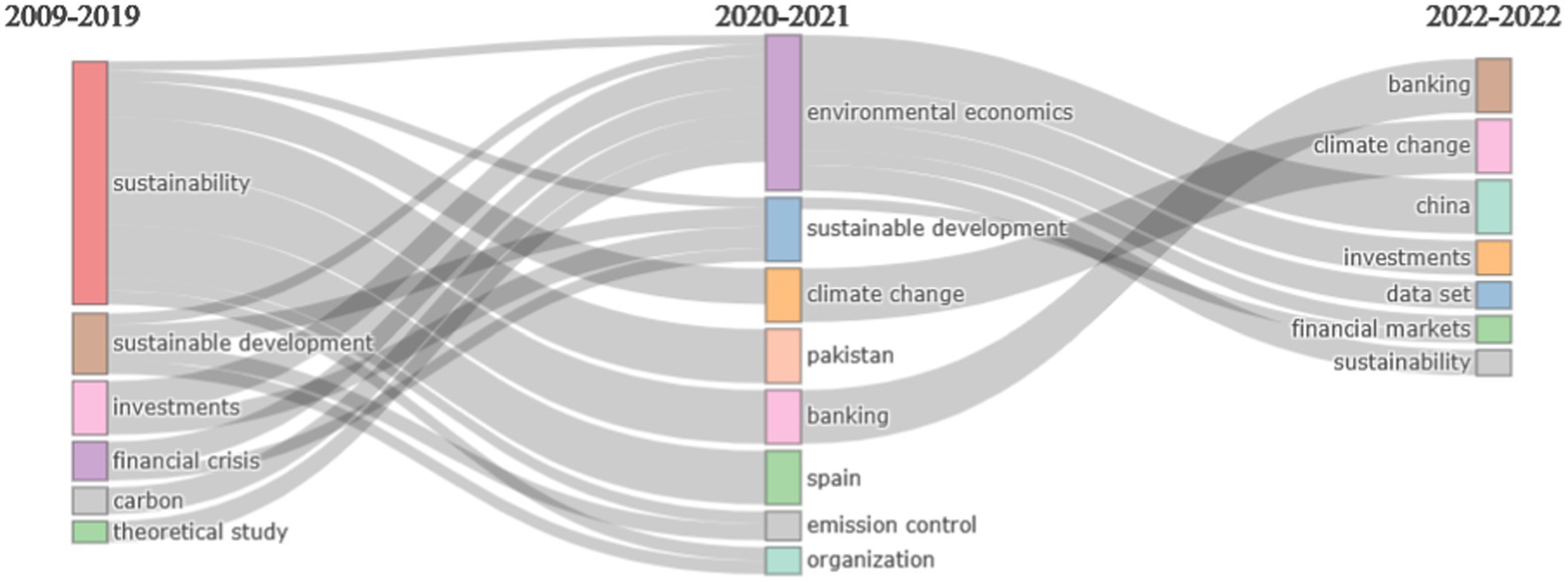

Figure 6 present the thematic evolution of topics while Figure 7 presents the trending topics in the subject.

Figure 6. Thematic evolution.

Figure 7. Thematic map.

The evolution of dominant terms were visualized in Figures 6, 7. The figure shows that the progress of topics overtime. In the discipline that integrates CSR with GFC and climate change, the previous studies mainly focused on the concepts such as sustainability, sustainable development, investment, and financial crises. To revisit this themes, the main concepts has been overviewed. For example, sustainable development endeavors to achieve a harmonious equilibrium among diverse needs while taking into account environmental, social, and economic constraints. Regrettably, prevailing development activities often disregard broader and future repercussions, resulting in severe financial crises prompted by reckless banking practices and shifts in the global climate (Jalles, 2021; Lentner and Zsarnóczai, 2022). Firms are increasingly acknowledging the imperative to disclose their influence on the economy, ecology, and society in order to foster sustainable development (Umantsiv, 2023). Sustainable management, inclusive of social and environmental responsibility, bears a significant sway on corporate performance, with customer and operational agility acting as intermediaries in this relationship (Jeon, 2023). Thus, the business strategies of the companies are reconfigured, the environment, social and governance issues being observed so that the interests of the stakeholders are promoted and not only the maximization of profit for the shareholders is pursued (Panait et al., 2023a). In essence, sustainable development, investment, and financial crises are intrinsically interconnected and necessitate focused attention and strategic approaches to ensure enduring sustainability. Additionally, CSR is intricately linked to sustainable development, particularly in addressing climate change and adopting environmentally conscious practices.

By incorporating the theme of sustainability into the study of the GFC, CSR, and climate change, it is plausible to cultivate responsible financial practices, promote sustainable business operations, and advance environmental and social well-being. For instance, the exploration of sustainability/sustainable development in financial crises entails scrutinizing the enduring consequences of economic practices on the environment, society, and future generations. Similarly, the integration of sustainability/sustainable development in CSR centers on how enterprises can conscientiously operate by incorporating sustainable practices into their strategic frameworks and considering the triple bottom line to contribute to the communities in which they operate. Moreover, integrating sustainability into climate change studies empowers us to construct a more resilient and sustainable future for both the planet and its inhabitants.

Financing and investment mechanisms are pivotal in supporting sustainability processes across various stages of development (Goodluck et al., 2022). Financial crises, including asset devaluation and debt deflation, present a notable risk to corporate sustainability, particularly among manufacturing firms (World investment report, 2023). Such crises have the potential to instigate transformative change and learning, yet short-term responses may inadvertently reinforce unsustainable practices rather than promote sustainability (Pahl-Wostl et al., 2023). The assessment of financial risks and investment development assumes utmost importance in ensuring enterprise sustainability, and a proposed methodology that incorporates contemporary and classical economic-statistical methods can contribute to informed investment decision-making (Tobisová et al., 2022). These findings underscore the significance of financing and investment in the study of GFC, CSR, and climate change. Incorporating the theme of financing and investment in these domains can foster responsible financial practices, facilitate sustainable investments, and drive positive environmental and social transformations.

Later, in 2020 and 2021 the concept of environmental economics has received a wide consideration than any other themes. Following environmental economics as the second most significant theme during the time period is climate change. This could be connected to COVID-19’s emergence. The theme of environmental economics holds significant importance in the examination of GFC, CSR, and climate change. Notably, CSR has been identified as a means to enhance corporate resilience against climate change risks at the firm level, thereby contributing to the augmentation of firm value (Mandal, 2022). Moreover, the fields of accounting and finance play a pivotal role in the integration of environmental factors into risk management frameworks and the evaluation of solutions for financing the transition toward a low-carbon and environmentally sustainable economy (Brooks and Schopohl, 2020). In a broader sense, the theme of environmental economics assumes a critical role in the exploration of financial crises, corporate social responsibility, and climate change. By incorporating the theme of environmental economics into the study of these subjects, we can promote the adoption of sustainable practices, encourage responsible business conduct, and address the multifaceted challenges presented by environmental concerns.

Recently in 2022, scholars tended to concentrate on particular fields and industries. Climate change is one of the primary themes, and the banking industry is the primary themes. As an illustration, Caby et al. (2022) noted that while many studies have examined the influence of environmental performance and, to a lesser extent, of green practices in various sectors, relatively few do so in the context of the banking business. The authors are also conducting research on other specific concepts, including investment, data set, financial crises, and sustainability. Since this themes are recent and new, there is a need to further discuss their integration in the study of GFC, CSR, and climate change.

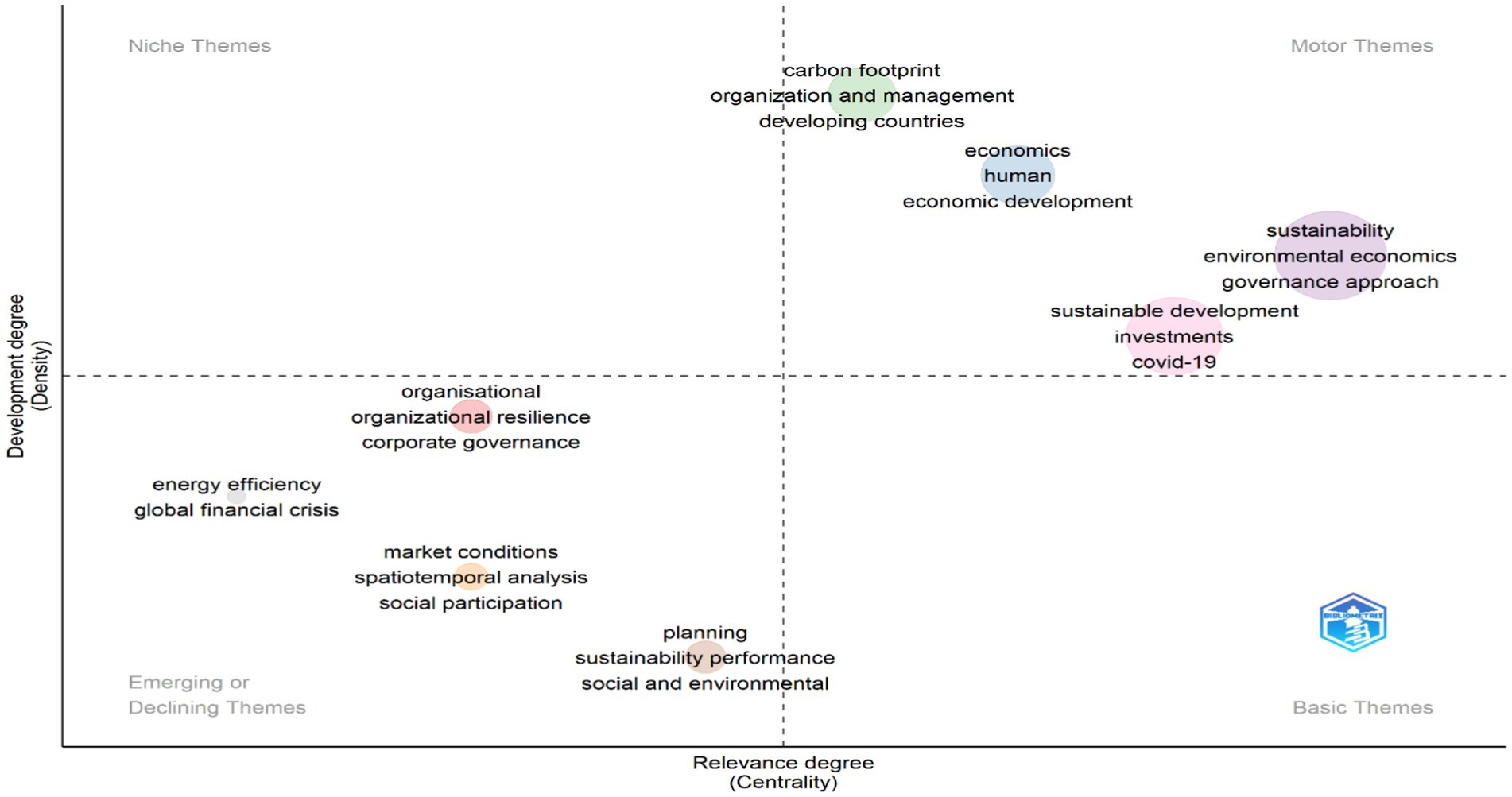

According to Esfahani et al. (2019), the field’s thematic map is essentially separated into four quadrants. Driving themes are represented in the upper right quadrant (Q1), underlying themes in the lower right quadrant (Q4), extremely specialized themes in the upper left quadrant (Q2), and emerging or fading themes in the lower left quadrant (Q3). As a result, Figure 8 shows that the primary driving themes in the study of financial crises, CSR, and climate change include sustainability, environmental economics, governance approach, sustainable development, and organization and management.

Figure 8. Trending topics.

Sustainability within the context of the GFC, CSR, and climate change is a multifaceted and interconnected matter. Crises have the potential to either catalyze transformative progress toward sustainability or perpetuate unsustainable practices (Pahl-Wostl et al., 2023). Additionally, the advent of the COVID-19 pandemic has presented an opportunity for corporations to align their operations and CSR initiatives with sustainability objectives. However, achieving equitable global accountability and fostering collaboration among multiple stakeholders are imperative. Consequently, prompt political action is critical in order to mitigate climate change and redirect financial markets toward sustainable investments, which will necessitate additional financial resources and the overcoming of various challenges.

Climate governance encompasses a wide range of social, economic, and political actors across various sectors and scales. Its primary objective is to ensure the resilience of the global socio-ecological system in the face of unpredictability and transformation (Nielsen, 2022). Within the domain of climate finance, there is a pressing need for novel funding mechanisms to address the climate crisis, with a specific emphasis on attracting private capital toward financially viable climate-related projects. Nonetheless, the existing global governance architecture has faced criticism for its inherent shortcomings in regulatory mechanisms and crisis response capabilities, thus demanding adaptations to effectively confront new challenges and risks (Broome et al., 2012). The potential of the financial sector to leverage positive changes in response to climate change through socially responsible investment has been hindered by inadequate governance frameworks and the sector’s abandonment of its ethical agenda (Richardson, 2009).

Research has demonstrated that CSR initiatives can serve as effective strategies for companies to navigate economic crises by enhancing operational efficiency and fostering stronger relationships with stakeholders and markets (Roman Pais Seles et al., 2018). In addition, the GFC has presented an opportunity for contemplation and the development of novel organizational models aimed at advancing the well-being of worldwide stakeholders (Shrivastava and Statler, 2012). This serves to underscore the critical nature of integrating CSR, corporate governance, and climate governance in order to address these pressing social challenges. Consequently, it is imperative to conduct further studies on the convergence of climate governance with the GFC, CSR, and climate change themes.

Moreover, emerging topics that need more research include organizational resilience, global financial crises, sustainable performance, and others in quadrant 3. Because, these themes are not strongly developed since they have lower centrality and low density. The study of Benn et al. (2014) proposes a comprehensive strategy to facilitate transformative change within organizations and its integrated approach to corporate sustainability. It combines global concerns regarding ecological sustainability, strategic human resource management, organizational change, CSR, leadership, and community renewal. Currently, the majority of climate-related disclosures are encompassed within broader corporate reports, predominantly found within ecological, social responsibility, and sustainable development reports. However, it is imperative to recognize the materiality of information pertaining to the impact of climate change on the financial position, performance, and cash flows of companies within the context of financial statements (Efimova and Rozhnova, 2020).

Further, there are no themes in Q4 which considered as a fundamental and important theme in the subject. This is because of the fact that there are no specific themes developed in the subject matter that integrates financial crises, CSR, and climate change. Thus, there is a need to research further in order to provide comprehensive understanding and developing basic foundations in the subject matter. There is also no very specialized (niche) themes. Thus, the future researchers have to undertake a research that links this concept with specialized topics.

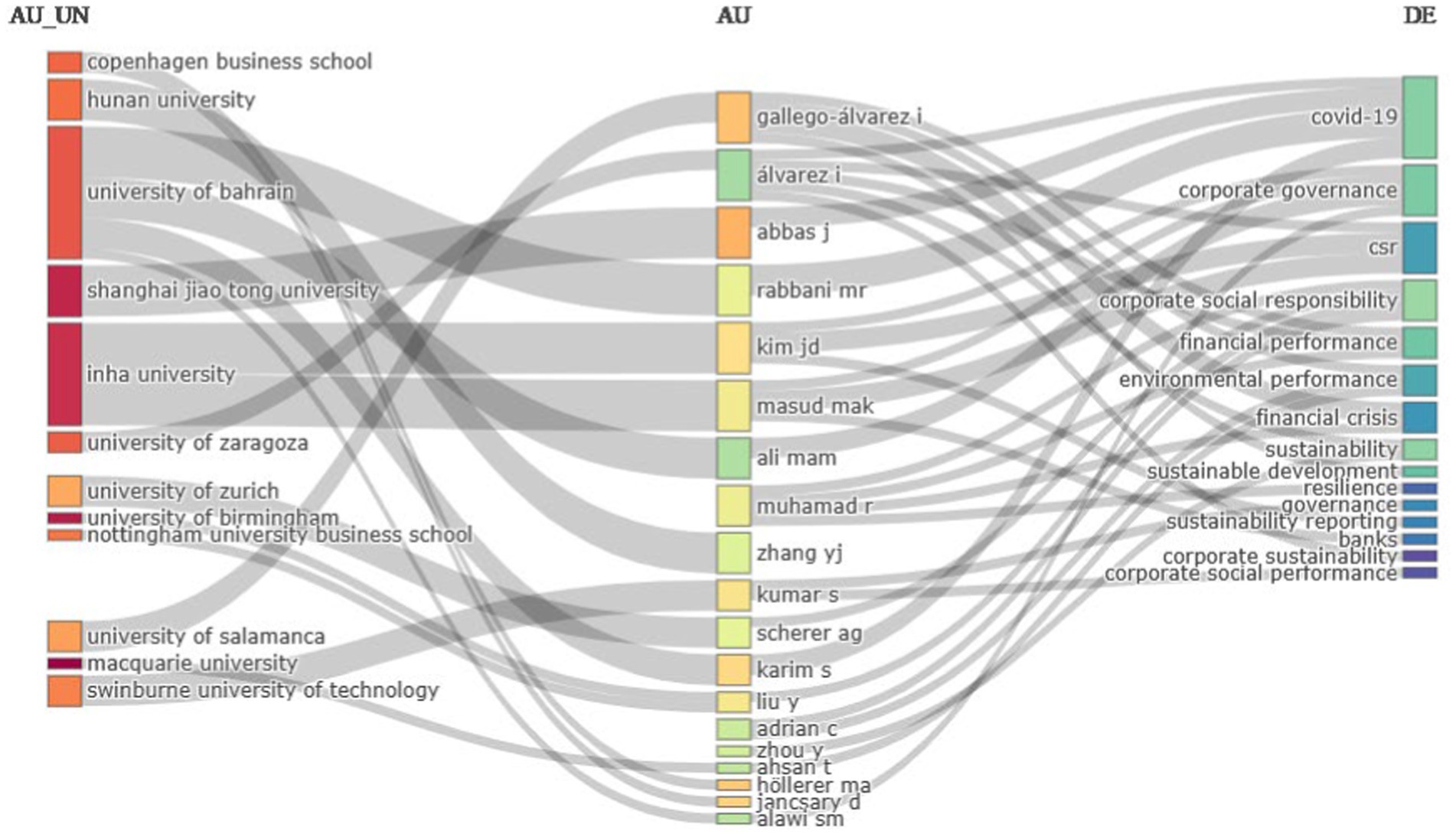

Figure 9 depicted the most active institutions are presented in the left field, active authors in the middle, and keywords at the right. Accordingly, the University of Bahrain, Inha University, and Shangai Jiao Tong University are just a few of the institutions currently conducting study on the interconnected ideas of the GFC, CSR, and Climate Change. Researchers from the University of Bahrain, including Rabbani MR, investigated the topic and made a connection between it and COVID-19, while Ali Mam from the same institution made a connection between the concept and corporate governance. Shangai Jiao Tong University’s Abbas J also connected the concept to COVID-19. Saini et al. (2022) claim that institutional investors are turning away from profit-making and toward sustainable and ethical investment as a result of the Covid-19 pandemic. Researchers have looked at scholars from Inha University including Masud Mak and Kim JD by relating the GFC to CSR.

Figure 9. Three field plot.

Since the first release in 2009, a sizable advancement has been seen in the field of GFC, CSR, and climate change. This is due to the fact that the severity and frequency of global crises have increased (Davvetas et al., 2022), which has changed the scope of CSR and the way people are responding to climate change. Following this, at times of crisis, such as the COVID-19 period and the 2007–2008 GFC, appeals for a green transition are made (Gunay et al., 2022). Companies now place more of an emphasis on ESG initiatives to rebuild their market reputation through socially responsible behavior in the wake of the GFC (Shakil et al., 2019). Several variables contributed to the global crisis, necessitating the simultaneous consideration of numerous factors. For instance, lesser CSR spending can be anticipated at times of economic hardship or when businesses are under more financial pressure (Bouslah et al., 2018). Due to their interdependence, the GFC, CSR, and climate change components must all be integrated. Yet, research on the connection between CSR and financial performance during times of crisis is scarce (Petitjean, 2019). So, amid financial crises, it is necessary to take into account the financial performance in relation to CSR and climate change.

The most frequently cited article examined the long-term advantages of organizational resilience through sustainable business practices (Ortiz-De-Mandojana et al., 2016). They contend that business sustainability measures related to social and environmental factors also increase organizational resilience, including reduced financial volatility, sales growth, and survival rates. Consequently, during crises like financial crises and pandemics, it is important to take into account sociological and environmental factors. The second-most-cited article, Amran et al. (2014), discovered that improving sustainability reporting quality is made possible by institutionalizing the idea of CSR within a business. Further, the third most cited document by Starik (2013) is about uncovering and integrating a theory of sustainability management. Also, in order for an organization to endure through times of global crisis and climate change, CSR and sustainable management practices must be internalized and integrated.

Regarding the keyword analysis, sustainable development” and “sustainability” are the central themes of the study. These is followed by terms such as, financial markets, strategic approach, planning, and institutional framework. These showed how closely related the issues of FC, CSR, and climate change are to sustainability and sustainable development. Since financial institutions play a crucial part in guaranteeing the steady expansion of the economy, the concept of sustainability is essential for all organizations (Galletta et al., 2022). The first cluster in the co-occurrence network is specifically focused on environmental protection through carbon emission reduction, emission trading, carbon footprint reduction, and similar methods. This demonstrates why environmental preservation and pollution reduction are essential in light of the GFC and climate change, and why they should be incorporated into business CSR frameworks. The most significant factors influencing bank stability are environmental transparency and emissions reduction, according to Azmi et al. (2021). Because of the demand from governments to minimize high carbon emissions, corporations are compelled to significantly alter their business practices. However, Petitjean (2019) finds that there is no evidence of a general relationship between financial performance and the existence of emission reduction or climate change policies in significant US corporations. They do not notice any obvious changes over time, whether or not we condition the analysis on the existence of the 2008–2009 financial crisis.

The second cluster is about the integration of CSR in the institutional framework and strategic approach toward industrial performance and sustainability. It also demonstrates how important it is to take into account CSR when choosing investments and the financial system. Georgeson et al. (2017) claimed that given this relevance, economic recovery, climate change, and other sustainable actions are not at odds with one another, but rather support one another. That is, it is expected that aspects of the economy, such as financial performance, will be merged with environmental factors, such as climate change. This demonstrates that both organizational internal factors and environmental external factors must be taken into account when making strategic decisions. Because, the company’s future operations and maintenance of stable financial performance and growth depend on sound corporate governance (Shakil et al., 2019). Further, engagement in CSR activities, according to Chiaramonte et al. (2021), was associated with greater stability during the GFC (Galletta et al., 2022). Njoroge (2009) and Karaibrahimoğlu (2010) do, however, demonstrate a strong pattern of declining CSR activity during times of crisis (Petitjean, 2019). However, more research needs to be done in order to clarify this controversial findings and to determine the cause of this trend.

The theme emerged from the third cluster links the financial crises with environmental policy, environmental economics and management, and environmental performance as well as climate change, financial performance and stock market. During the financial crisis, businesses that perform better in terms of sustainability have worse financial performance, but profitability’s marginal effects on sustainability are increased (Lu et al., 2022). At times of economic difficulty, environmental performance and financial performance have a good relationship, according to Kaakeh and Gokmenoglu (2022). The claim that there is a correlation between financial performance and environmental performance that is unique to times of low trust, according to Petitjean (2019), is only partially supported by the research. Thus, future research has to take this tension into account. Because it is anticipated that investments in community well-being will help businesses perform sustainably. However, it is expected that the contribution’s scope would be made clear. Besides, according to Galletta et al. (2022), initiatives taken by financial institutions like banks and new regulations put in place by supervisory bodies will help to improve the estimation of climate risk impacts and lay the groundwork for efforts to reduce climate-related financial risks. These initiatives will also help to improve relations between the community and stakeholders.

The fifth cluster linked terms such as investments, economics, planning, and environmental impact, while the sixth cluster linked terms such as sustainable development, Covid-19, decision making, profitability, innovation. This shows that the study of GFC, CSR, and climate change is required to be liked with environmental effects, sustainable economic development, and crises such as Covid-19. For instance, Van Duuren et al. (2016) stated that investors have started to match their investment choices with societal norms and the value system as a result of the COVID-19 outbreak and the 2008 Global Financial Crisis. Institutions may be disrupted by a financial or economic crises like the COVID-19, which may leave them unsure of their future strategic course. For instance, the global energy sector has encountered difficulties as a result of the COVID-19 epidemic (Panait et al., 2023b). However, current research indicates that COVID-19 has a smaller impact on businesses with higher sustainability performance (Lu et al., 2022). Furthermore, stock prices and sustainability are related concepts. For instance, Ding et al. (2021) find that companies with greater sustainability efforts experience reduced stock price declines during pandemics, while Garel and Petit-Romec (2021) demonstrate that external investors favor businesses that prioritize environmental responsibility.

Studies that directly link the GFC to the CSR and climate change are scarce. Even if this study offers comprehensive analysis, the relationship and integration between these concepts still need to be empirically tested. So, this issue will be taken into account in future studies. That is, it is necessary to examine the impact of the GFC, CSR, and climate change on business success. There are, however, few research on the link between CSR and financial performance during difficult times. According to Petitjean (2019), no studies have examined how the integrated idea relates to both financial and environmental performance. This requires the clarification of the conceptual relationship in the subject matter.

The literature on how companies change their CSR attitude and strategy in times of crisis is still very limited. While discussing CSR, the environmental dimensions are frequently ignored; therefore, the relationship between financial performance and environmental performance should be taken into account (Petitjean, 2019). Moreover, Souto and Fernández (2009) believe that financial crises are indicators for enterprises to temporarily stop investing in CSR in order to survive the financial shock or to reduce their CSR spending when the business cycle is negative (Bouslah et al., 2018). Also, during the financial crisis, companies that perform better in terms of sustainability have weaker financial performance, but the marginal benefits of profitability on sustainability are increased (Lu et al., 2022). Thus, future scholars should provide further clarification on these contentious conclusions. Also, it is anticipated that additional research will be done on the impact of lowering carbon emissions on financial performance.

The term financial markets, strategic approach, planning, and institutional framework are some of the terms that happen the least frequently. This shows that the institutional dimensions of financial crises are not given as much attention as the macro aspects in the study of financial crises. Thus, future researchers need to provide new insights on the integration of these concepts. Besides, developing models that integrate public-private efforts, support sustainable financial management with an emphasis on environmental and social factors, and take intergenerational equity into consideration to improve operational sustainability and crisis mitigation are all part of the process of integrating management practices with financial crises, CSR, and climate change. Future academics must, in particular, connect the study of GFC, CSR, and climate change with managerial and organizational concepts like learning organizations and organizational culture.

This study is not without limitation; first, the scope of this study is global in focus. Future scholars should, however, thoroughly examine the unique circumstances of different countries in order to offer detailed information and specifics that may vary from country to country. The study’s materials are journal articles that have only been published in English. It is more significant, though, if some strong non-journal papers and materials published in languages other than English have been thoroughly reviewed and added to the research. This study also made use of the Scopus database. In addition to Scopus, we advise future scholars to utilize other databases like Web of Science.

The objective of this study was to offer an in-depth comprehension of GFC, CSR, and climate change. The study of financial crises in relation to CSR and climate change is a rapidly growing area, especially in the last 5 years. The most commonly cited countries are those in Europe, which indicates that the continent has produced significant research on the subject. However, research on African and Asian countries is lacking. Policymakers and practitioners in developing Asian and African countries will learn from this to incorporate the subject of climate change into their CSR efforts and financial decisions. The terms COVID-19, environmental economics, financial crisis, governance approach, sustainable development, and sustainability are used the most in the study. The primary themes of the study are “sustainability” and “sustainable development,” with an emphasis on the connections between these topics and sustainability-related problems. In light of its significance, practitioners and policymakers should engage in environmental economics and evaluate their governance strategy in relation to sustainability rather than concentrating only on financial rewards.

The keyword co-occurrence network consists of eight clusters, with the first cluster highlighting the importance of environmental protection in CSR and climate change. The second cluster focuses on sustainability, with the third cluster focusing on environmental economics and the linkage of financial crises and climate change with economic benefits. The fourth cluster focuses on the human side, with the fifth cluster focusing on investments, economics, and planning. The last two clusters deal with economic development and financial markets. The literature also suggests that incorporating innovation and management activities within a company is positively related to economic and environmental performance. That is, sustainable manufacturing practices integrate environmental, economic, and social aspects into operational and business activities, resulting in improved economic sustainability. These are the important concepts that need to be considered by company managers when setting corporate policies and strategies.

The study revealed that integrating sustainability into climate change studies can help construct a more resilient and sustainable future for both the planet and its inhabitants. Financing and investment mechanisms are crucial for supporting sustainability processes, especially in the context of financial crises. These crises can instigate transformative change, but short-term responses may reinforce unsustainable practices. Thus, the company managers should think big by considering the long term and sustainable future. Furthermore, the GFC presents an opportunity for contemplation and the development of novel organizational models to advance global stakeholders’ well-being. Thus, it is recommended that companies should have a comprehensive strategy for transformative change within organizations, combining global concerns with ecological sustainability, strategic management initiatives, and CSR activities.

AC: Writing – review & editing, Writing – original draft, Visualization, Validation, Supervision, Software, Resources, Project administration, Methodology, Investigation, Funding acquisition, Formal analysis, Data curation, Conceptualization. SD: Writing – review & editing, Writing – original draft, Visualization, Validation, Supervision, Software, Resources, Project administration, Methodology, Investigation, Funding acquisition, Formal analysis, Data curation, Conceptualization. MB: Writing – review & editing, Writing – original draft, Visualization, Validation, Supervision, Software, Resources, Project administration, Methodology, Investigation, Funding acquisition, Formal analysis, Data curation, Conceptualization.

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. The publication of this article is financial supported by University of Johannesburg.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Amran, A., Lee, S. P., and Devi, S. S. (2014). The influence of governance structure and strategic corporate social responsibility toward sustainability reporting quality. Bus. Strateg. Environ. 23, 217–235. doi: 10.1002/bse.1767

Azmi, W., Hassan, M. K., Houston, R., and Karim, M. S. (2021). ESG activities and banking performance: International evidence from emerging economies. J. Int. Financ. Mark. Inst. Money 70:101277. doi: 10.1016/j.intfin.2020.101277

Bae, K.-H., El Ghoul, S., Gong, Z., and Guedhami, O. (2021). Does CSR matter ysisysin times of crisis? Evidence from the COVID-19 pandemic. J. Corp. Finan. 67:101876. doi: 10.1016/j.jcorpfin.2020.101876

Bae, S. M., Masud, M. A. K., Rashid, M. H. U., and Kim, J. D. (2022). Determinants of climate financing and the moderating effect of politics: evidence from Bangladesh. Sustain. Account. Manag. Policy J. 13, 247–272. doi: 10.1108/SAMPJ-04-2019-0157

Benn, S., Edwards, M., and Williams, T. (2014). Organizational Change for Corporate Sustainability, (3rd ed.). London: Routledge.

Bilbao-Terol, A., Arenas-Parra, M., Álvarez-Otero, S., and Cañal-Fernández, V. (2019). Integrating corporate social responsibility and financial performance. Manag. Decis. 57, 324–348. doi: 10.1108/MD-03-2018-0290

Bouslah, K., Kryzanowski, L., and M'Zali, B. (2018). Social Performance and Firm Risk: Impact of the Financial Crisis. J. Bus. Ethics 149, 643–669. doi: 10.1007/s10551-016-3017-x

Branca, A. S., Pina, J., and Margarida Catala O-Lopes, M. (2012). Corporate giving, competition and the economic cycle : School of Economics and Management, Technical Lisbon: University of Lisbon.

Brimble, Mark, Stewart, Jenny, and DeZwann, Laura, (2011). Climate Change and Financial Regulation: Challenges for the Financial Sector Following the Global Financial Crisis (July 12, 2011). Griffith Law Review. Available at: https://ssrn.com/abstract=1884046

Brooks, C., and Schopohl, L. (2020). Green Accounting and Finance: Advancing Research on Environmental Disclosure, Value Impacts and Management Control Systems. Br. Account. Rev. doi: 10.2139/ssrn.3741193

Broome, A., Clegg, L., and Rethel, L. (2012). Global Governance and the Politics of Crisis. Glob. Soc. 26, 3–17. doi: 10.1080/13600826.2011.629992

Busch, T., Stinchfield, B. T., and Wood, M. S. (2011). “Rethinking Sustainability, Innovation, and Financial Performance” in Cross-Sector Leadership for the Green Economy. eds. A. Marcus, P. Shrivastava, S. Sharma, and S. Pogutz (New York: Palgrave Macmillan).

Caby, J., Ziane, Y., and Lamarque, E. (2022). The impact of climate change management on banks profitability. J. Bus. Res. 142, 412–422. doi: 10.1016/j.jbusres.2021.12.078

Carroll, A. B., and Shabana, K. M. (2010). The business case for corporate social responsibility: A review of concepts, research and practice. Int. J. Manag. Rev. 12, 85–105. doi: 10.1111/j.1468-2370.2009.00275.x

Chiaramonte, L., Dreassi, A., and Girardone, C. (2021). Do ESG strategies enhance bank stability during financial turmoil? Evidence from Europe. Eur. J. Financ. 28, 1173–1211. doi: 10.1080/1351847X.2021.1964556

Dah, M. A., and Jizi, M. I. (2018). Board independence and the efficacy of social reporting. J. Int. Account. Res. 17, 25–45. doi: 10.2308/jiar-51952

Davis, K. (1973). The Case For and Against Business Assumption of Social Responsibility. Acad. Manag. J. 16, 312–322. doi: 10.2307/255331

Davvetas, V., Ulqinaku, A., and Abi, G. S. (2022). Local Impact of Global Crises, Institutional Trust, and Consumer Well-Being: Evidence from the COVID-19 Pandemic. J. Int. Mark. 30, 73–101. doi: 10.1177/1069031X211022688

Demers, E., Hendrikse, J., Joos, P., and Lev, B. (2021). ESG did not immunize stocks during the COVID-19 crisis, but investments in intangible assets did. J. Bus. Financ. Acc. 48, 433–462. doi: 10.1111/jbfa.12523

Des Jardine, M., Bansal, P., and Yang, Y. (2019). Bouncing back: building resilience through social and environmental practices in the context of the 2008 global financial crisis. J. Manag. 45, 1434–1460. doi: 10.1177/0149206317708854

Dias, A. I., Baptista Fernandes, S. R., and Pinheiro, P. (2023). Climate-Related Financial Disclosures and Corporate Social Responsibility: Evidence from European companies. In F. Albuquerque and P. Santosdos (Eds.), Accounting and Financial Reporting Challenges for Government, Non-Profits, and the Private Sector (pp. 24–57). IGI Global.

Ding, W., Levine, R., Lin, C., and Xie, W. (2021). Corporate immunity to the COVID-19 pandemic. J. Financ. Econ. 141, 802–830. doi: 10.1016/j.jfineco.2021.03.005

Donthu, N., Kumar, S., Mukherjee, D., Pandey, N. B., and Lim, W. M. (2021). How to conduct a bibliometric analysis: an overview and guidelines. J. Bus. Res. 133, 285–296. doi: 10.1016/j.jbusres.2021.04.070

Efimova, O., and Rozhnova, O. (2020). Financial Reporting and Climate-related Disclosures. J. Digit. Sci. 2, 67–75. doi: 10.33847/2686-8296.2.1_6

Esfahani, H., Tavasoli, K., and Jabbarzadeh, A. (2019). Big data and social media: A scientometrics analysis. Int. J. Data Network Sci. 3, 145–164. doi: 10.5267/j.ijdns.2019.2.007

Fagerberg, J., Fosaas, M., and Sapprasert, K. (2012). Innovation: Exploring the knowledge base. Res. Policy 41, 1132–1153. doi: 10.1016/j.respol.2012.03.008

Freeman, R. E. (1984). Strategic Management: A Stakeholder Approach. Business and Public Policy Series, Pitman series in business and public policy : Pitman, 1984.

Gallego-Álvarez, I., Segura, L., and Martínez-Ferrero, J. (2015). Carbon emission reduction: the impact on the financial and operational performance of international companies. J. Clean. Prod. 103, 149–159. doi: 10.1016/j.jclepro.2014.08.047

Galletta, S., Mazzù, S., and Naciti, V. (2022). A bibliometric analysis of ESG performance in the banking industry: From the current status to future directions. Res. Int. Bus. Financ. 62. doi: 10.1016/j.ribaf.2022.101684

Garel, A., and Petit-Romec, A. (2021). Investor rewards to environmental responsibility: Evidence from the COVID-19 crisis. J. Corp. Finan. 68:101948. doi: 10.1016/j.jcorpfin.2021.101948

Georgeson, L., Maslin, M., and Poessinouw, M. (2017). The global green economy: a review of concepts, definitions, measurement methodologies and their interactions. Geo: Geography and Environ. 4:e00036. doi: 10.1002/geo2.36

Goodluck, H. C., Iliemena, R. O., and Islam, M. M. (2022). Financial Crises as a Threat to Corporate Sustainability: Evaluating the Implications of Asset Devaluation and Debt Deflation in the Pursuit of Sustainable Development. Int. J. Account. Finance Rev. 13, 35–41. doi: 10.46281/ijafr.v13i1.1854

Guérin, P., and Felix, Suntheim F. (2021). Firms’ Environmental Performance and the COVID-19 Crisis. IMF, WP/21/89. Accessed from: file: ///C: /Users/Inspiron%205567/Downloads/wpiea2021089-print-pdf%20(1).pdf

Gunay, S., Muhammed, S., and Elkanj, N. (2022). Risk transmissions between regional green economy indices: Evidence from the US, Europe and Asia. J. Clean. Prod. 379. doi: 10.1016/j.jclepro.2022.134752

Hall, J., and Wagner, M. (2012). Integrating Sustainability into Firms' Processes: Performance Effects and the Moderating Role of Business Models and Innovation. Bus. Strateg. Environ. 21, 183–196. doi: 10.1002/bse.728

Hami, N., Muhamad, M. R., and Ebrahim, Z. (2015). The Impact of Sustainable Manufacturing Practices and Innovation Performance on Economic Sustainability. Procedia CIRP 26, 190–195. doi: 10.1016/j.procir.2014.07.167

Jalles, J.T. (2021). Financial Crises and Climate Change, 12 April 2021, PREPRINT (Version 1) available at Research Square:. doi: 10.21203/rs.3.rs-299516/v1

Jalles, J. T. (2023). Financial Crises and Climate Change. Comp. Econ. Stud. 2023, 166–190. doi: 10.1057/s41294-023-00209-7

Jensen, M. C., William, H., and Meckling, W. H. (1976). Theory of the firm: Managerial behavior, agency costs and ownership structure. J. Financ. Econ. 3, 305–360. doi: 10.1016/0304-405X(76)90026-X

Jeon, B. (2023). The Impact of Sustainability Management of Social Economy Enterprises on Corporate Performance: Focusing on the mediating effect of organizational agility. Korea Career Entrepreneurship Manag. Res. 7, 35–50.

Justesen, T., Freyberg, J., and Schultz, A. N. (2021). Database selection and data gathering methods in systematic reviews of qualitative research regarding diabetes mellitus - an explorative study. BMC Med. Res. Methodol. 21:94. doi: 10.1186/s12874-021-01281-2

Kaakeh, M., and Gokmenoglu, K. K. (2022). Environmental performance and financial performance during COVID-19 outbreak: Insight from Chinese firms. Front. Environ. Sci. 10, 1–14. doi: 10.3389/fenvs.2022.975924

Karaibrahimoğlu, Y. Z. (2010). Corporate social responsibility in times of financial crisis. Afr. J. Bus. Manag. 2, 382–389.

Kim, C. H. (2008). “Climate Change: Business Challenge or Opportunity?” in EKC2008 Proceedings of the EU-Korea Conference on Science and Technology. Springer Proceedings in Physics. ed. S. D. Yoo, vol. 124 (Berlin, Heidelberg: Springer).

Ledesma, F., and Malave González, BE. (2022). Bibliometric indicators and decision making. Data and Metadata. Accessed at 2024 May 25. Available from: https://dm.saludcyt.ar/index.php/dm/article/view/9

Lentner, C., and Zsarnóczai, S. J. (2022). Some Aspects of Fiscal and Monetary Tools of the Environmental Sustainability: Through the Case of Hungary. Public governance, administration and finances law review 7, 63–76. doi: 10.53116/pgaflr.2022.1.5

Linnenluecke, M. K., Marrone, M., and Singh, A. K. (2020). Conducting systematic literature reviews and bibliometric analyses. Aust. J. Manag. 45, 175–194. doi: 10.1177/0312896219877678

Lodhia, S. (2015). Exploring the Transition to Integrated Reporting Through a Practice Lens: An Australian Customer Owned Bank Perspective. J. Bus. Ethics 129, 585–598. doi: 10.1007/s10551-014-2194-8

Lu, J., Rodenburg, K., Foti, L., and Pegoraro, A. (2022). Are firms with better sustainability performance more resilient during crises? Bus. Strateg. Environ. 31, 3354–3370. doi: 10.1002/bse.3088

Mandal, G. C. (2022). Rethinking Corporate Social Responsibility in the Arena of Climate Change: A Study in Socio-Legal Aspect. J. climate change 8, 17–24. doi: 10.3233/JCC220026

Miao, S., Peng, H., and Li, S. (2021). A visualized bibliometric analysis of mapping research trends of machine learning in engineering (MLE). Expert Syst. Appl. 186:115728. doi: 10.1016/j.eswa.2021.115728

Nielsen, H. O. (2022). “Climate change and sustainable development governance” in Handbook on the Governance of Sustainable Development. eds. D. Russel and N. Kirsop-Taylor, Cheltenham, Edward Elgar Publishing 30–47.

Njoroge, J. (2009). Effects ofthe Global Financial Crisis on Corporate Social Responsibility in Multinational Companies in Kenya. Geneva: Africa Nazarene University (Kenya), Covalence Intern Analyst Papers.

Orlitzky, M., Schmidt, F. L., and Rynes, S. L. (2003). Corporate Social and Financial Performance: A Meta-Analysis. Organ. Stud. 24, 403–441. doi: 10.1177/0170840603024003910

Ortas, E., Moneva, M., and Álvarez, I. (2014). Sustainable supply chain and company performance: A global examination. Supply Chain Manag. 19, 332–350. doi: 10.1108/SCM-12-2013-0444

Ortiz-de-Mandojana, N., Aguilera-Caracuel, J., and Morales-Raya, M. (2016). Corporate governance and environmental sustainability: the moderating role of the national institutional context. Corp. Soc. Responsib. Environ. Manag. 23, 150–164. doi: 10.1002/csr.1367

Ozkan, A., Temiz, H., and Yıldız, Y. (2022). Climate Risk, Corporate Social Responsibility, and Firm Performance. Br. J. Manag. 1791–1810. doi: 10.1111/1467-8551.12665

Pahl-Wostl, C., Odume, O. N., and Scholz, G. (2023). The role of crises in transformative change towards sustainability. Ecosystems and people 19, 1–17. doi: 10.1080/26395916.2023.2188087

Panait, M., Gigauri, I., Hysa, E., and Raimi, L. (2023a). “Corporate Social Responsibility and Environmental Performance: Reporting Initiatives of Oil and Gas Companies in Central and Eastern Europe” in Corporate Governance for Climate Transition. eds. C. Machado and J. Paulo Davim (Cham: Springer).

Panait, M., Ionescu, R., Gigauri, I., and Palazzo, M. (2023b). Maintaining Green Goals in Disruptive Times: Evidences from the European Energy Sector. In: L. Chivu, I. Los Ríos CarmenadoDe, and J.V. Andrei (eds) Crisis after the Crisis: Economic Development in the New Normal. ESPERA 2021. Springer Proceedings in Business and Economics. Springer, Cham.

Petitjean, M. (2019). Eco-friendly policies and financial performance: Was the financial crisis a game changer for large US companies? Energy Econ. 80, 502–511. doi: 10.1016/j.eneco.2019.01.028

Richardson, B. J. (2009). Climate Finance and its Governance: Moving to a Low Carbon Economy through Socially Responsible Financing. Int. Comparative Law Q. 58, 597–626. doi: 10.1017/S0020589309001213

Roman Pais Seles, B. M., Lopes de Sousa Jabbour, A. B., Chiappetta Jabbour, C. J., and Jugend, D. (2018). In sickness and in health, in poverty and in wealth?: Economic crises and CSR change management in difficult times. J. Organ. Chang. Manag. 31, 4–25. doi: 10.1108/JOCM-05-2017-0159

Saini, N., Antil, A., Gunasekaran, A., Malik, K., and Balakumar, S. (2022). Environment-Social-Governance Disclosures nexus between Financial Performance: A Sustainable Value Chain Approach. Resour. Conserv. Recycl. 186:106571. doi: 10.1016/j.resconrec.2022.106571

Selmi, R., Hammoudeh, S., Errami, Y., and Wohar, M. E. (2021). Is COVID-19 related anxiety an accelerator for responsible and sustainable investing? A sentiment analysis. Applied Econ. 53, 1528–1539. doi: 10.1080/00036846.2020.1834501

Shakil, M. H., Mahmood, N., Tasnia, M., and Munim, Z. H. (2019). Do environmental, social and governance performance affect the financial performance of banks? A cross-country study of emerging market banks. Manag. Environ. Quality: Int. J. 30, 1331–1344. doi: 10.1108/MEQ-08-2018-0155

Shrivastava, P., and Statler, M. (2012). Learning from the global financial crisis: creatively, reliably, and sustainably. Redwood City, CA: HAL.

Singh, V. K., Singh, P., Karmakar, M., et al. (2021). The journal coverage of Web of Science, Scopus and Dimensions: A comparative analysis. Scientometrics 126, 5113–5142. doi: 10.1007/s11192-021-03948-5

Souto, F., and Fernández, B. (2009). Crisis and corporate social responsibility: threat or opportunity? Int. J. Econ. Sci. Appl. Res. 2, 36–50. https://hdl.handle.net/10419/66605

Sroufe, R. (2017). Integration and organizational change towards sustainability. J. Clean. Prod. 162, 315–329. doi: 10.1016/j.jclepro.2017.05.180

Starik, M. (2013). Organization & Environment: Present, Past, and Future. Organ. Environ. 26, 239–240. doi: 10.1177/1086026613499233

Suchman, M. C. (1995). Managing legitimacy: Strategic and institutional approaches. Acad. Manag. Rev. 20, 571–610. doi: 10.2307/258788

Tobisová, A., Seňová, A., Ižaríková, G., and Krutakova, I. (2022). Proposal of a Methodology for Assessing Financial Risks and Investment Development for Sustainability of Enterprises in Slovakia. Sustain. For. 14:5068. doi: 10.3390/su14095068

Turzo, T., Marzi, G., Favino, C., and Terzani, S. (2022). Non-financial reporting research and practice: Lessons fromthe last decade. J. Clean. Prod. 345:131154. doi: 10.1016/j.jclepro.2022.131154

Umantsiv, H. (2023). Reporting on sustainable development in the context of corporate social responsibility. F scientia fructuosa 2023 3, 59–71. doi: 10.31617/1.2023(149)05

van den Besselaar, P., and Sandström, U. (2020). Bibliometrically disciplined peer review: On using indicators in research evaluation. Scholarly Assessment Reports 2, 1–13. doi: 10.29024/sar.16

Van Duuren, E., Plantinga, A., and Scholtens, B. (2016). ESG integration and the investment management process: Fundamental investing reinvented. J. Bus. Ethics 138, 525–533. doi: 10.1007/s10551-015-2610-8

Wagner, M. (2015). The link of environmental and economic performance: Drivers and limitations of sustainability integration. J. Bus. Res. 68, 1306–1317. doi: 10.1016/j.jbusres.2014.11.051

Weaver, D. B. (2012). Organic, incremental and induced paths to sustainable mass tourism convergence. Tour. Manag. 33, 1030–1037. doi: 10.1016/j.tourman.2011.08.011

World investment report (2023). Capital markets and sustainable finance. World investment report, 97–138.

Zhang, Z., Su, Z., Wang, K., and Zhang, Y. (2022). Corporate environmental information disclosure and stock price crash risk: Evidence from Chinese listed heavily polluting companies. Energy Econ. 112. doi: 10.1016/j.eneco.2022.106116

Keywords: financial crises, CSR, climate change, sustainability, scientific mapping, thematic

Citation: Chebo AK, Dhliwayo S and Batu MM (2024) The linkage between global financial crises, corporate social responsibility and climate change: unearthing research opportunities through bibliometric reviews. Front. Clim. 6:1388444. doi: 10.3389/fclim.2024.1388444

Edited by:

Mirela Panait, Petroleum & Gas University of Ploieşti, RomaniaReviewed by:

Iza Gigauri, St. Andrew First-Called Georgian University of the Patriarchate of Georgia, GeorgiaCopyright © 2024 Chebo, Dhliwayo and Batu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Abdella K. Chebo, YWJkaWtvc2FAZ21haWwuY29t

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.