David Mhlanga

David Mhlanga

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

POLICY AND PRACTICE REVIEWS article

Front. Clim. , 15 September 2022

Sec. Climate and Economics

Volume 4 - 2022 | https://doi.org/10.3389/fclim.2022.949178

Individuals and enterprises have an increasing need for financial resources, which has led to the development of numerous financial instruments such as microfinance, insurance, and cash transfers, among other things. The number of development partners advocating for the use of these technologies to address disaster risks and climate change-related concerns is also increasing. With the rise in risk reduction needs and challenges associated with climate change, it's more important than ever to assess the effectiveness of various financial instruments (financial inclusion) in solving climate-related issues. The study used secondary data studied through document analysis to answer the question, what role does financial technology play in addressing the challenges or hazards associated with climate change in the Fourth Industrial Revolution? The results indicated that financial inclusion through FinTech could aid in the resilience of households, individuals, and companies in the case of a rapid climate event or the gradual effects of changing rainfall patterns, rising sea levels, or salter water incursion. Insurance, savings, credit, money transfers, and new digital distribution channels can all help victims of climate change and those in charge of dealing with the new environmental realities. As a result, the study advises that financial inclusion through FinTech be promoted as one of the channels that can aid in managing the risks of climate-related concerns and achieving sustainable development goals through development patterns, governments, and civil society.

Many central banks, financial regulators, and ministries of finance in emerging and developing economies are concerned about climate change and environmental challenges. The reality that central banks and financial regulators in emerging and developing countries have a policy mission that covers 85% of the world's unbanked population, or nearly 1.7 billion people, is one of the causes driving this worry (International Monetary Fund, 2019; Banna et al., 2021; Chenet, 2021). Environmental disasters are harming around 200 million people because of the detrimental effects of climate change, resulting in billions of dollars in annual costs to the worldwide economy (United Nations Environment Programme, 2019, 2022; Benni, 2021; NOAA National Centers for Environmental Information, 2021). Another severe issue is that climate change is displacing thousands of people every day, wreaking havoc on developing and rising economies (International Monetary Fund, 2019). Climate change is once again causing many people to become financially excluded, and it is one of the major barriers to financial stability and poverty reduction (IMF, 2019; Puschmann et al., 2020; Hansen, 2022).

Many scholars Hope (2009), Gasper et al. (2011), Shonkoff et al. (2011), Leichenko and Silva (2014), Levy and Patz (2015), Sethi and Acharya (2018) Umar (2020), Huang et al. (2021), Immurana et al. (2021) among many others believe that climate change disproportionately affects the poor and vulnerable, such as those living in low-lying coastal areas. Acute climatic calamities like floods, droughts, and storm surges have a significant impact on these people in the short term. Climate change is also thought to be causing an increase in poverty in a variety of ways around the world, with an estimated 132 million people falling into poverty because of the effects of climate change by 2030 (Jafino et al., 2020). According to the World Bank (2020), the greatest driver of rising poverty in the poorest regions, such as Sub-Saharan Africa, is rising food prices due to a loss in agricultural production. Poor people spend a large portion of their income on food, therefore a spike in food prices can significantly limit people's ability to meet their needs, pushing them into poverty. Malawian households, for example, spend 63% of their income on food and beverages. As a result, even a little adjustment in food prices has a significant impact on Malawians. As a result, it's also critical to ensure that agricultural production can adapt to climate change (World Bank, 2020).

Financial inclusion, according to Liu et al. (2021), can help with climate-related difficulties despite having detrimental effects on climate change. Financial inclusion is widely regarded to provide businesses and individuals with more beneficial and affordable financing, making green technology investments more accessible. The advances that are occurring as a result of the Fourth Industrial Revolution are even making it possible for financial companies to be able to deliver cheap financial solutions through the use of FinTech. In this context, inclusive financial systems improve the environment by increasing accessibility and affordability, as well as encouraging the adoption of good environmental measures to minimize climate change impacts (Ullah et al., 2022). Financial inclusion is vital in tackling climate change challenges, according to Liu et al. (2021), because many small enterprises and smallholder farmers may lack the financial muscle to invest in renewable energy. According to Baulch et al. (2015) in Ho Chi Minh City, Vietnam, financial constraints, a lack of funding from the government, and bank funding possibilities have all been recognized as important roadblocks to the implementation of solar household systems. Other scholars also believe that access to finance can have negative implications on climate change. For instance, Jensen (1996) argued that enhanced financial accessibility, on the other hand, assists and stimulates manufacturing and industrial activity, thereby increasing CO2 emissions and aggravating global warming. Frankel and Romer (1999) argued that Customers are more likely to buy energy-intensive consumer products such as autos, freezers, and air conditioning units, which constitute a severe environmental danger since they generate more greenhouse gases.

Economic activity is boosted by inclusionary financial institutions, which boosts demand for hazardous energy sources and hence raises Greenhouse gases. According to Alwi (2021), the growing use of personal mobile devices such as smartphones has enabled a slew of FinTech services to reach the most remote parts of developing countries. These services allowed consumers to conduct daily financial transactions using their mobile devices, increasing the flexibility of several consumer products. Even though much research has shown the consequences of financial development on CO2 emissions, such as Zhang et al. (2011), Shahbaz et al. (2013), and Charfeddine and Kahia (2019), the number of studies that evaluate FinTech's role in climate change is exceedingly limited. Alwi (2021) concentrated on identifying the factors that impact people's decision to use mobile e-wallets after the epidemic, whereas Pinshi (2021) examined the opportunities that FinTech presented to people throughout the pandemic's lifespan. Morgan (2022) examined the most recent advances in FinTech, as well as the challenges and benefits that they may bring to financial inclusion and financial literacy. Fu and Mishra (2020) studied the influence of the Covid-19 outbreak on digital finance and FinTech adoption, with an emphasis on mobile applications. Pinshi (2021) discovered that FinTech was one of the tools that assisted in rebalancing the global financial system during the Covid-disturbances and that it helped the financial sector become resilient and respond to the crisis by ensuring that the financial sector functioned while the virus's containment measures were followed. Many of the research conducted was biased toward evaluating financial inclusion and the factors of financial inclusion, rather than looking into the influence of FinTech on climate change, according to the empirical literature. Considering these considerations, the current paper investigates the role of FinTech for financial inclusion in tackling climate-related concerns in the Fourth Industrial Revolution and lessons learned for sustainable development goals. The rest of the document is organized as follows the next section will outline the background of the Fourth Industrial Revolution, financial inclusion, financial technology, sustainable development goals, and climate change. The study will also give the empirical literature review, the methodology and the discussion of the results responding to the research questions.

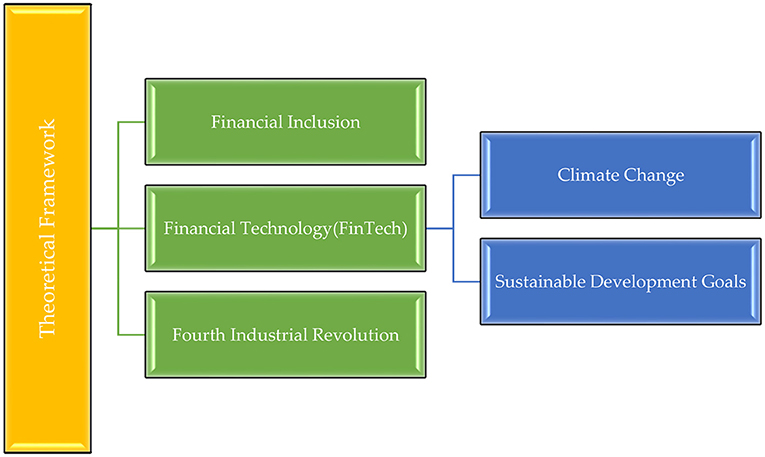

The theoretical framework will give the background information about the Fourth Industrial Revolution, financial inclusion, financial technology, sustainable development goals and climate change. Figure 1 below outlines the theoretical framework.

Figure 1. The theoretical framework. Source: The author's analysis.

Figure 1 above is outlining the theoretical framework. Financial inclusion, according to Li et al. (2021) is a crucial strategy for reaching the UN sustainable development goals on a global scale. According to Li et al. (2021) increasing feed costs and lower livestock selling prices brought on by economic globalization and climatic change posed a danger to herders' ability to support their families. It was shown in a study by Li et al. (2021) that herders with large grassland plot sizes who used their traditional ecological expertise to adjust through seasonal herd mobility benefited from financial inclusion loans. In this way, it is shown that financial inclusion has a huge impact on climate change. Liu et al. (2021) assert that financial inclusion can aid in resolving issues related to the environment. Financial inclusion is thought to offer people and businesses more advantageous and affordable financing, increasing access to green technology investments.

In the literature, the concept of “financial inclusion” has been defined in a number of different ways by different authors. To begin, “financial inclusion” is defined by Leeladhar (2005) as the practice of offering banking services to a large population of low-income and disadvantaged groups at a discounted rate. Thorat (2007) defined financial inclusion as the process of making the formal financial system's services available to underserved populations at cost. In this context, “access” refers to the ability to use a variety of financial services, such as making payments, sending money abroad, saving money, getting a loan, or getting insurance. The opposite of financial inclusion is financial exclusion. Sarma (2008) offers a different definition of financial inclusion as “the art of ensuring ease of access, availability, and utilization of the formal financial system to everyone in the economy.”

Due to the emergence of the Fourth Industrial Revolution, the world is heading toward a cashless society because of numerous financial industry advances, the introduction of goods like credit and debit cards, as well as FinTech services, and the increased reliance of consumers on non-cash payment methods. Due to the availability of various technologies, virtual payments have grown in importance (Alwi, 2021). Electronic payment systems are gradually displacing conventional cash-based payment methods. According to the 2019 World Payment Survey, non-cash transactions increased by 12% between 2016 and 2017, totalling $539 billion, the greatest amount in the previous two decades (Alwi, 2021). In 2016–17, non-cash transactions rose by more than 32% in emerging economies like Asia. These various digital tools are increasing the levels of financial inclusion, especially among the smallholder farmers allowing them to invest more in climate-smart agriculture improving a lot on addressing the effects of climate change. According to Nicoletti et al. (2017), the term “FinTech,” which is also known as “Financial technology,” refers to a branch of the economy that offers financial services through the utilization of various softwares. FinTech refers to a new category of technologies developed to improve and automate the delivery and use of financial services. It describes the application of computer programs and algorithms to improve financial management for consumers, businesses, and financial institutions.

Al Nawayseh (2020) indicated that the global investment in FinTech technology is expected to exceed $40 billion in 2019 and despite increased FinTech investment, Al Nawayseh (2020) noted that the maturation and adoption of these technologies among low-income earners remains a challenge that requires immediate attention. It is believed that despite the increase in FinTech products and financial inclusion the technique of balancing the benefits and risks of FinTech advancements is critical, especially in developing countries. The problem is aggravated by the fact that people in developing nations with little socioeconomic resources lack access to the essential financial product expertise, even when they seek it. Many scholars such as Zaidi et al. (2021) and Hussain et al. (2022) believe that financial inclusion through FinTech can have a huge impact on climate change, especially on the impact of financial inclusion, energy use, and carbon emissions. The variables outlined in the theoretical framework will be defined in the next sections which include financial inclusion, financial technology, and the Fourth Industrial Revolution.

The Fourth Industrial Revolution also known as industry 4.0 has been described as a means of defining the “blurring of barriers between the physical, digital, and biological worlds” (Mhlanga, 2020; McGinnis, 2022). The Fourth Industrial Revolution is also described as a “combination of developments in artificial intelligence (AI), robots, the Internet of Things (IoT), 3D printing, genetic engineering, quantum computing, and other technologies” (McGinnis, 2022). The “Fourth Industrial Revolution, often known as Industry 4.0 or 4IR, builds on the first three industrial revolutions: the first, second, and third” (Mhlanga, 2020, 2021, 2022). The “invention of the steam engine in the eighteenth century ushered in the first industrial revolution, allowing for the first time the mechanization of industry, resulting in significant social change and urbanization.” The second industrial revolution occurred in the fourth millennium when electricity and other technological advances made mass production possible. With the advent of computer automation and digital technology, the third industrial revolution ended. As a result, “manufacturing has become increasingly automated, disrupting industries such as banking, energy, and communications” (McGinnis, 2022).

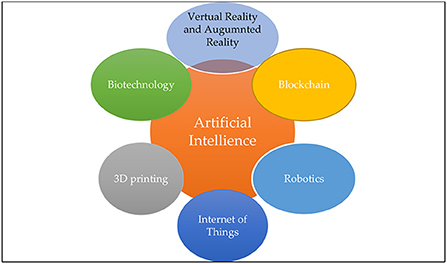

Klaus Schwab, “founder and executive chairman of the World Economic Forum and author of the book The Fourth Industrial Revolution, sees the Fourth Industrial Revolution as a new revolution. According to Schwab, the changes are so fundamental that there has never been a time of greater promise or potential hazard in human history” (McGinnis, 2022). Fourth Industrial Revolution is essentially distinct from its predecessors the First Industrial Revolution, the Second Industrial Revolution and the Third Industrial Revolution. The Fourth Industrial Revolution is distinguished by a variety of new innovations that are integrating the physical, digital, and biological worlds, touching all fields of study, economies, and businesses, and even questioning assumptions about what it is to be human. In other words, it is a time of technological convergence. The technologies that are fueling the Fourth Industrial Revolution are listed below.

Figure 2 depicts some of the technologies that are driving the Fourth Industrial Revolution's advancements. “Artificial intelligence, virtual reality, augmented reality, biotechnology, 3D printing, blockchain, robots, and the internet of things are examples of these technologies.”

Figure 2. Technologies driving change in the Fourth Industrial Revolution. Source: The analysis of the author.

The World Bank (2022) defines financial inclusion as “the process where individuals and businesses have access to useful and affordable financial products and services that meet their needs like transactions, payments, savings, credit and insurance.” These services should be delivered responsibly and sustainably (World Bank, 2022). Financial inclusion is also listed as a facilitator of eight of the 17 sustainable development goals, according to the World Bank (SDGs). The United Nations Capital Development Fund (2022) outlines these goals as “SDG one, eradicating poverty; SDG 2 on ending hunger, achieving food security, and promoting sustainable agriculture; SDG 3 on promoting health and wellbeing; SDG 5 on achieving gender equality and economic empowerment of women; SDG 8 on promoting economic growth and jobs; SDG 9 on supporting industry, innovation, and infrastructure; and SDG 10 on reducing inequality; and SDG 17 Strengthening the means of implementation and revitalize the global partnership for sustainable development.” Financial inclusion, according to the World Bank (2022), is a critical facilitator for reducing extreme poverty and increasing shared prosperity.

According to the World Bank (2022), great progress has been made in achieving global financial inclusion, with 1.2 billion adults having access to an account between 2011 and 2017. According to estimates, roughly 69% of individuals have a bank account in 2017. It is also believed that digital financial services, such as the use of mobile phones, have been introduced in more than 80 countries, and that “millions of previously excluded and underserved poor customers are transitioning from cash-based transactions to formal financial services via mobile phones or other digital technology” (Mhlanga, 2020; World Bank, 2022). According to the most recent Findex data, about one-third of individuals ~1.7 billion remained unbanked in 2017 (World Bank, 2022). About half of the unbanked people were women from low-income households in rural areas or who were unemployed (Mhlanga, 2020; World Bank, 2022).

FinTech stands for “financial technology” and refers to “all the technologies that are being utilized to enhance, digitize, or disrupt conventional financial services” (Stephanie Walden, 2020). FinTech refers to all “software, algorithms, and applications for both computer and mobile-based tools” (Philippon, 2016; Puschmann, 2017). FinTech isn't a new industry, but it's growing at a rapid pace. The introduction of credit cards and automated teller machines, among other technology, has been a component of the financial business. According to Puschmann (2017), FinTech is the “fusion of the Financial and Technology.” According to Puschmann (2017), the word FinTech was “originally suggested in the early 1990's by Citicorp's chairman John Reed in the context of a newly formed Smart Card Forum consortium, Speaking a language of cooperation across firms and industries.” FinTech, according to Puschmann (2017), is an “umbrella term that comprises new financial solutions enabled by technology, as well as start-up companies that supply those solutions, albeit it also includes traditional financial services providers such as banks and insurers.” FinTech, as the name implies, is the confluence of finance and technology, according to Goldstein et al. (2019). Goldstein et al. (2019) also stated that technology has always had an impact on the financial business, with innovations affecting how it runs. Again, the FinTech revolution is exceptional in that more of the change is coming from outside the financial industry, as young start-ups and large established technology firms try to disrupt incumbents by presenting new products and technologies, as well as supplying a substantial new dose of competitors in the market (Goldstein et al., 2019).

According to the United Nations (2022) SDGs, “are also known as the Global Goals, and they were approved by the United Nations in 2015 as a worldwide call to action to eradicate poverty, safeguard the planet, and ensure that by 2030, all people experience peace and prosperity,” These “17 sustainable development goals are interconnected because they recognize that actions in one area have an impact on outcomes in others, and that development must balance social, economic, and environmental sustainability” (Sustainable Development Goals, 2020; United Nations, 2022). These goals are aimed to “eliminate poverty, hunger, AIDS, and discrimination against women and girls” because of nations' strong commitment to giving priority to those who are far behind. It is also believed that “to realize the SDGs in whatever context, all of society's creativity, know-how, technology, and financial resources are required” (Sustainable Development Goals, 2020; United Nations, 2022).

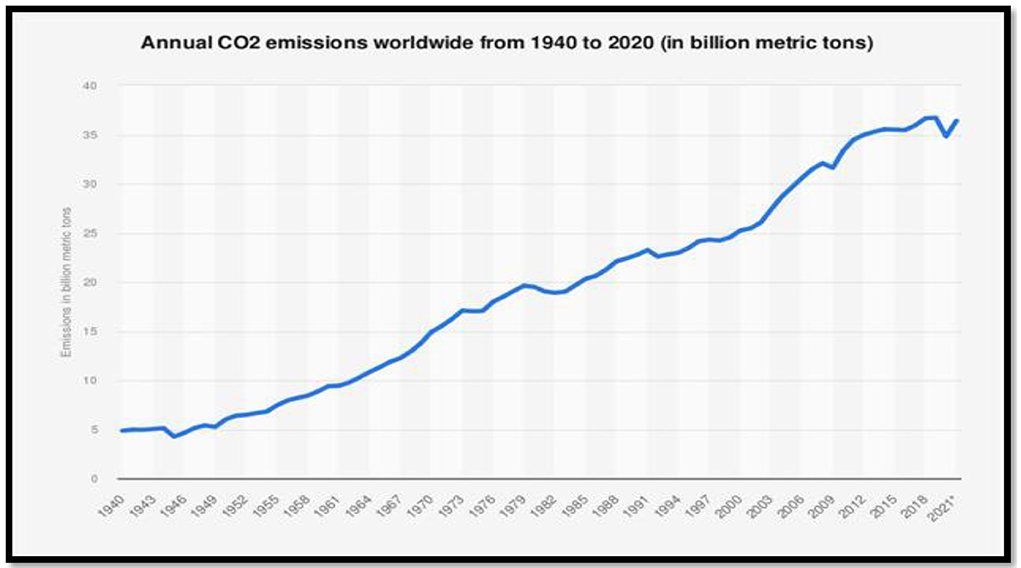

SDG's goal number 13 gives priority to climate change. The goal outlines that countries should “take urgent action to combat climate change and its impacts.” Climate change is affecting all the nations in all the continents of the world with disruptions in individual economies and affecting the lives of the people. There are “changes in weather patterns, rising sea levels and extreme weather events” (United Nations, 2022). For instance, in 2019 alone carbon dioxide (CO2) emissions rose to new records. Annual CO2 emissions worldwide from 1940 to 2020 are depicted in Figure 3.

Figure 3. Annual CO2 emissions in billion metric tons from 1940 to 2020. Source: Author's analysis, Statista (2022a) data.

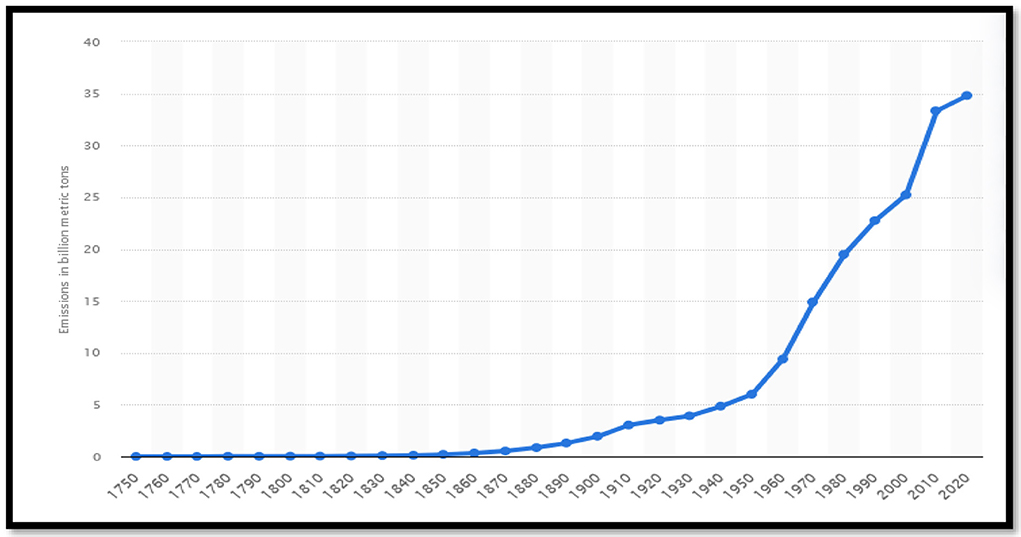

CO2 emissions worldwide have increased significantly since 2000, as seen in Figure 3. CO2 levels in the atmosphere reached a new high of 36.7 billion metric tons in 2019. However, CO2 levels fell by 5% to 34.81 billion metric tons because of the epidemic, but the lifting of lockdowns in 2021 caused CO2 levels to climb once more. Historically, huge worldwide events have resulted in significant reductions in emissions, such as the 2009 recession, which resulted in a global CO2 decrease of 460 metric tons (Statista, 2022a). This is like the year 2020 when countries were placed on rigorous lockdowns, with significant reductions in transportation and industrial activity. CO2 emissions in India, for example, fell for the “first time in four decades in the year ending March 2020” (Statista, 2022a). “Global CO2 emissions per capita also showed a significant reduction in 2020, decreasing to an average of 4.47 metric tons per person,” according to Statista (2022a). Statista (2022a) also reported that the “energy industry is the primary source of CO2 emissions, and worldwide energy demand is predicted to climb in the future decades as people and economies develop.” When we look at worldwide “fossil fuel combustion and industrial processes from 1750 to 2020” in Figure 4 below, we can see that CO2 emissions have been increasing as a testimony that industrial processes and fossil fuel combustion are the major causes of the rise in CO2 emissions.

Figure 4. Historical CO2 emissions from global fossil fuel combustion and industrial processes from 1750 to 2020. Source: Author's analysis, Statista (2022b) data.

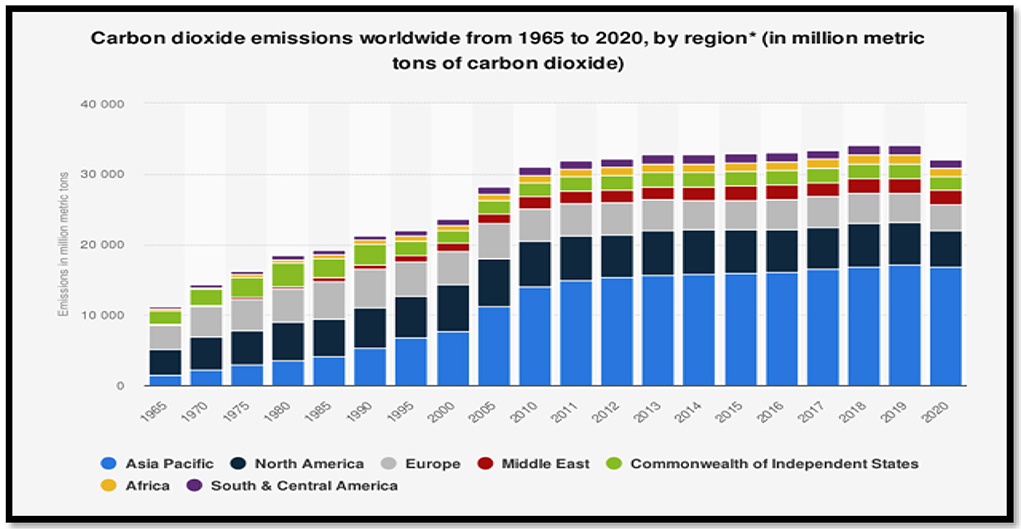

CO2 emissions from “fossil fuel burning, and industrial operations have been increasing since the beginning of the industrial revolution,” as illustrated in Figure 4. CO2 emissions began to climb sharply in 1950, according to Statista (2022b) and peaked at 25.23 billion metric tons in 2000. Again, Statista (2022b), reported that “emissions increased by 32% between 2000 and 2010, reaching 34.81 billion metric tons in 2020.” As previously stated, the Covid-19 epidemic reduced emissions by 5% in 2020. When it comes to regional emissions, Figure 5 shows that the Asia Pacific is the region contributing more to the emissions.

Figure 5. CO2 emissions worldwide by region from 1965 to 2020. Source: Author's analysis, Statista (2022c) data.

The Asia-Pacific area, as indicated in Figure 5, is the largest emitter of CO2. In 2020, “the Asia-Pacific area emitted 16.75 billion metric tons of carbon dioxide.” This was more than the total emissions of all other regions that year, according to Statista (2022c). China was responsible for 60% of emissions in the Asia-Pacific region and 31% of world emissions. The Asia-Pacific region was followed by North America, which released 5.3 billion metric tons in 2020. According to Statista (2022c), emissions in Europe and North America declined by over 12% in 2020 compared to 2019, while emissions in the Asia-Pacific area fell by about 2.5%. However, according to Statista (2022c), even though COVID-19 reduced annual emissions significantly, global CO2 concentrations in the atmosphere reached a new high in 2020, averaging more than 414 parts per million. CO2 levels in the atmosphere have risen dramatically in recent decades because of increased fossil fuel use, deforestation, and other human activities. Climate change is primarily caused by CO2 (Statista, 2022c). According to the United Nations (2022), “member States affirm their obligation to protect the earth from deterioration and take prompt action on climate change in the 2030 Agenda for Sustainable Development.” Climate change is also “identified as one of the greatest issues of our time in paragraph 14 of the agenda, with concerns about its negative consequences jeopardizing all countries' capacity to accomplish sustainable development.” Climate change consequences such as “rising global temperatures, sea-level rise, acidification of the oceans, and other effects are wreaking havoc on coastal areas and low-lying coastal countries, including many LDCs and Small Island Developing States. Many societies, as well as the planet's biological support systems, are in jeopardy.” While noting that the “United Nations Framework Convention on Climate Change is the principal international, intergovernmental venue for negotiating the global response to climate change, SDG 13 aspires to take urgent action to address climate change and its impacts” (United Nations, 2022). SDG 13's associated targets are “focused on integrating climate change mitigation, adaptation, impact reduction, and early warnings into national policies, as well as improving education, awareness-raising, and institutional capacity on climate change mitigation, adaptation, impact reduction, and early warnings. The alphabetical targets of SDG 13 also call for the implementation of the commitments made at the United Nations Framework Convention on Climate Change, as well as the promotion of mechanisms that can help LDCs and Small Island Developing States increase their capacity for effective climate change planning and management” (United Nations Capital Development Fund, 2022).

Financial inclusion is gaining popularity in literature because of its direct and indirect links to several developmental features such as poverty reduction, financial system stability, firm growth, mental health, and gender equality, among many others. Financial inclusion has been proven to play a crucial role in driving economic growth and development in numerous studies.

According to Puschmann et al. (2020), the finance industry is going through a massive revolution, with automation and sustainability as the primary drivers. Puschmann et al. (2020) went on to explain that while these notions have indeed been studied in the past few years, their confluence, which is sometimes referred to as “green FinTech” is yet unknown. Puschmann et al. (2020) also argued that FinTech research is still in its infancy, is defined by a narrow concentration on discrete fields of green FinTech and doesn't yet include a holistic view on the subject. Financial technology (FinTech), according to Arner et al. (2020), is the principal determinant for financial intermediation, which in turn underpins sustainably balanced growth, as enshrined in the SDGs. Arner et al. (2020) also mentioned that the maximum capabilities of FinTech to assist the SDGs might be fulfilled with a gradual approach to the building of underpinning systems to accommodate online payments transformation. The ideal approach to conceive of such a plan, according to Arner et al. (2020), would be to pay attention to the following major pillars. The very first pillar necessitates the creation of a digital identity, which is backed by the second pillar of accessible interoperability of electronic payments. The third pillar, according to Arner et al. (2020), includes utilizing facilities of the first and second pillars to bolster the automated supply of public services and transactions, and the fourth pillar involves the configuration of an electronic financial system and infrastructure that supports broader access to credit and investment.

According to Puschmann et al. (2020), sustainability and digitization are the main forces driving the current significant transformation of the financial services sector. Puschmann et al. (2020) also argued that although both ideas have been studied separately in recent years, the intersection known as “green FinTech” has so far only drawn a small amount of research. However, the field is becoming more and more relevant as the financial system plays a crucial role in the greening of the global economy. In a different study, Cen and He (2018) made the case that it is difficult to implement sustainable development since there is not enough bond issuance to support the growth of the environmentally friendly sector. FinTech has altered financial service and pricing models while also promoting green financing and sustainable development. In addition, Cen and He (2018) argued that FinTech is inherently green and supports sustainable development, at least in the following ways: by guaranteeing green finance, lowering costs and information asymmetry, fostering efficiency, valuing nature's assets, and offering both a solution for sustainable finance and practical sustainable lifestyles. Additionally, Cen and He (2018) claimed that green finance and FinTech should coexist to address climate change and it matters for sustainable development.

Hinson et al. (2019)'s argument that the Agenda for Sustainable Development, FinTech, and the integration of these technologies with other (green) technologies as well as with digitized agriculture make the transformation of agribusiness crucial. When it comes to, for instance, SDG 12, specifically, responsible production, agriculture is crucial because it may reduce trade-offs, improve synergies between environmental and social SDGs, for instance, 1 and 15, and increase profitability without using more natural resources. For developing countries to fully profit from the potential that FinTech has in this context, however, major limits and hazards must be addressed, according to Hinson et al. (2019). Massive infrastructure investments and extensive capacity building are two of the many mitigating variables mentioned by Hinson et al. in their 2019 study. To make appropriate policy suggestions, it is necessary to conduct a thorough study on economic sustainability and the cost-effectiveness of more recent FinTech models. Tao et al. (2022) also made the case that the public has recently become aware of environmentalists' concerns about the excessive use of electricity, notably in cryptocurrency mining. According to Tao et al. (2022), stakeholders and regulators have been reassessing the costs and advantages of technology advancement in general, as well as those of FinTech, with a focus on restoring the environment. Tao et al. (2022) continued by arguing that now would be the right time to evaluate technology's genuine role in environmental protection, or rather, even destruction, given that it has long been seen as a double-edged sword for the environment. Tao et al. (2022) sought to answer the question of whether FinTech growth is assisting economies in a smooth transition to reduced levels of carbon and greenhouse gas emissions. After the proper control variables were added, Tao et al. (2022) confirmed that FinTech innovation can aid in the reduction of greenhouse gas emissions.

According to Chueca Vergara and Ferruz Agudo (2021), current environmental concerns have sparked several new trends in technology and financial management, to the point where FinTech has emerged as a rival to traditional financial institutions. These trends include digital transformation and sustainable finance. Chueca Vergara and Ferruz Agudo (2021) examined the relationship between FinTech and sustainability and the various areas of collaboration between FinTech and sustainable finance from both a theoretical and descriptive perspective while providing specific examples of contemporary technological platforms. They did this through a literature review and case study approach. Chueca Vergara and Ferruz Agudo (2021) found that green finance and sustainable finance have many characteristics and that FinTech can improve the sustainability of financial enterprises by supporting green finance. Additionally, this study emphasizes the significance of European and international regulation, particularly from the standpoint of consumer protection.

Matekenya et al. (2021) investigated the impact of financial inclusion on human development in Sub-Saharan Africa in another study. Financial inclusion has a good impact on human development, according to the findings of the study. Matekenya et al. (2021) concur with other scholars that access to, and use of financial services is advantageous for company start-ups, investment in health and education, risk management, and even the reduction of the impact of shocks. The result will be a boost in human development. Matekenya et al. (2021) concluded that policymakers should implement steps to help reduce the costs of accessing and using financial services, as well as improve awareness of their availability. Aside from its effects on economic growth and development, financial inclusion can also aid in poverty reduction. The impact of financial inclusion on poverty alleviation was investigated by Lal (2018). Lal (2018) found that financial inclusion through cooperative banks has a direct and significant influence on poverty reduction. Financial inclusion, according to Lal (2018), can assist people to escape poverty by providing access to various financial services such as credit, savings, and other financial services. In a similar line, Abor et al. (2018) studied whether the mobile telephone promotes pro-poor growth by supporting households in efficiently allocating consumption to escape poverty. The study also looked at whether having access to a wide range of financial services can help households create the capacity to live meaningful lives. The findings showed that when households have strong cell phone penetration and financial inclusion, the likelihood of being poor decreases.

Mobile penetration and financial inclusion have been found to assist enhance per capita household consumption of food and non-food goods. The welfare gains of financial inclusion are also more pronounced in female-headed households, according to Abor et al. (2018). Ouechtati (2020) looked at the impact of financial inclusion on poverty and income inequality in developing countries. The study's findings revealed that financial inclusion and poverty reduction had a negative association. Financial services like credit and access to commercial bank deposit accounts had a significant impact on poverty alleviation. The findings of Ouechtati (2020) support the idea that increased money supply and access to credit help to reduce poverty and improve the wellbeing of the poor. The findings were also in line with those of Abor et al. (2018), who concluded that a high bank penetration rate and credit enable poor households' access to financial services, which can help to reduce high levels of inequality. Park and Mercado (2018) looked at the global and Asian implications of financial inclusion. Following the discussion of numerous factors such as rule of law, per capita income, and demographic features as drivers of financial inclusion in Asia and the rest of the world. Financial inclusion was also associated with lower levels of poverty and income disparity in the samples, according to Park and Mercado (2018). However, the findings for developing Asia revealed no link between financial inclusion and income disparity. The impact of financial development through commercial banks on poverty reduction in India was also explored in another study by Inoue (2019). Financial inclusion and financial deepening exhibited a negative statistically significant link with the poverty ratio for public sector banks, but not for private sector banking institutions, according to the study's findings.

In most cases of public sector banks, the impact of financial inclusion and financial deepening on poverty reduction was considerable, implying that it is vital to promote the breadth and depth of public sector banks in India to have a synergistic influence on poverty reduction. Authors such as Park and Mercado (2018), Inoue (2019), and even Ouechtati (2020) agreed with Omar and Inaba (2020). Omar and Inaba (2020) investigated the impact of financial inclusion on poverty reduction and income inequality reduction in emerging countries. Financial inclusion reduces poverty rates and income inequality in developing countries, according to the findings. The findings of Omar and Inaba (2020) support the idea that promoting financial participation in neglected areas of society can help to maximize people's overall welfare. Koomson and Danquah (2021) looked at the effect of financial inclusion on energy poverty in Ghana once more. The study's findings showed that increasing financial inclusion can assist reduce energy poverty by 1.380 to 1.556 standard deviations. The findings of Koomson and Danquah (2021) revealed a higher level of consistency among rural male-headed households living in rural locations. According to the findings of the study, if financial inclusion improves, energy poverty will decrease by a wider margin, particularly among employees.

Financial inclusion can assist reduce energy poverty directly through the variables of home consumption poverty and household net income. Financial inclusion is critical in reducing poverty and inequality, according to all the research. Financial inclusion is crucial in addressing mental health, according to studies such as Aguila et al. (2016), Gyasi et al. (2019), and Ajefu et al. (2020). The Financial technology Implementation Plan and the Sustainable Finance Strategy, according to Macchiavello and Siri (2020), are both significant cornerstones of the current EU policy agenda. Nonetheless, according to Macchiavello and Siri (2020), the two fields have been considered different for several years, even though they share some similar characteristics and have a lot of promise when united. FinTech trying to address some of the present sustainable finance framework's flaws. The importance of the connection between sustainability, money, and innovation has also been highlighted by the COVID-19 pandemic problem, which has challenged all countries to rethink their existing methods and rely more on innovation and sustainable development, as explained by Macchiavello and Siri (2020).

However, according to Macchiavello and Siri (2020), FinTech still creates legal challenges that must be resolved for it to fulfill its goals and possibilities in the responsible finance industry. The purpose of this article is to initiate a discussion on “Green FinTech” to successfully integrate the two sectors and stimulate research in this exciting new field. According to Nassiry (2019), the sustainable development goals (SDGs) and the Paris Agreement's implementation will necessitate major new investment and innovative finance technologies. Blockchain, the Internet of Things (IoT), and big data, which were created around the same time as the Paris Agreement and the SDGs, have the potential to be unlocked by FinTech.n Anshari et al. (2021) also made the case that FinTech, namely the Digital Wallet initiative, has the power to influence public opinion in favor of sustainable development and green growth. Using the Digital Wallet platform, Anshari et al. (2021) suggested a framework for raising the number of recycling initiatives and activities and rewarding public engagement. According to Anshari et al. (2021), a digital wallet unites all stakeholders on a single platform and may provide financial incentives to encourage more public participation in activities that promote socioeconomic and environmental conditions.

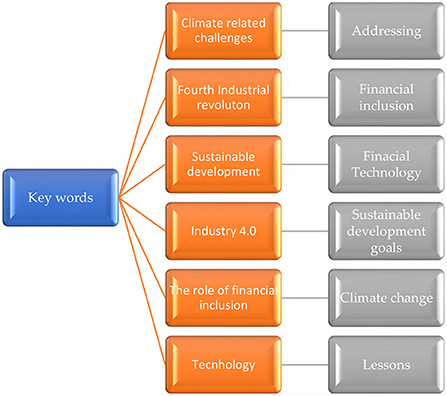

The current study looks at the role of FinTech in tackling climate-related concerns in the Fourth Industrial Revolution, as well as the implications for sustainable development goals. Secondary data was employed in the study, which was conducted unobtrusively. “Unobtrusive research is defined by Elo et al. (2014) as data gathering techniques in which the researcher does not interact with the subjects being studied.” This is because the procedures aren't too obtrusive (Colorado State University, 1997). Qualitative data was used in the study through content Analysis. Content analysis is the study where researchers look for information in texts, media, or physical items. While investigating a social phenomenon, content analysis has the advantage of being non-invasive (Colorado State University, 1997). Traditional, guided, and summative content analysis are the three main types of content analysis. The three approaches, according to Elo et al. (2014), facilitate the interpretation of meaning from text data content, and so fit into the naturalistic paradigm. The current study made extensive use of summative content analysis, which entails counting and comparing keywords, reading the context in the keywords or material, and then analyzing the underlying context (Colorado State University, 1997). Figure 6 is outlining the keywords used in the summative content analysis.

Figure 6. Keywords used in the summative content analysis. Source: Author's analysis.

In Figure 6 the keywords that were used in the summative content analysis are outlined which include climate change-related challenges, financial conclusion, financial technology, climate change, and lessons among others which were not listed in the figure. The keywords were picked in accordance with Hsieh and Shannon (2005) claims that a summative content analysis entails comparing and counting keywords or other information, typically, before interpreting the underlying context. According to Hsieh and Shannon (2005), research interests or literature reviews are the source of keywords. Key words in this study are drawn from the literature and the researcher's areas of interest.

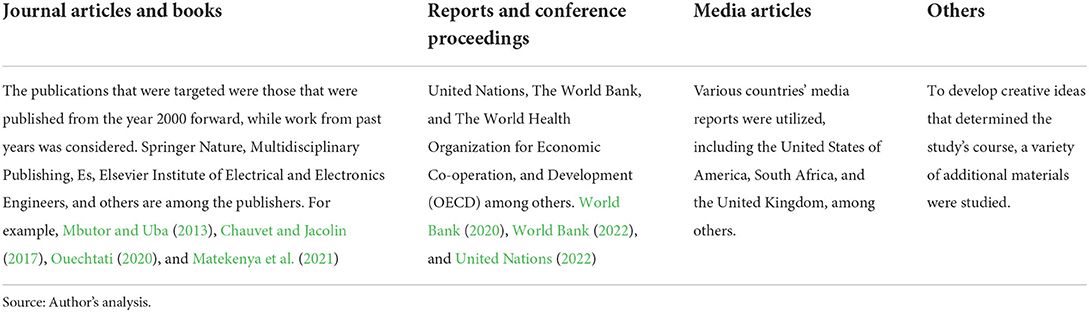

The table below outlines the documents that were used in the summative content analysis.

Table 1 summarizes all the sources used throughout the content analysis. Journal articles from various publications, as well as reports, are among the papers.

Table 1. The main documents used in summative content analysis.

The role of FinTech for financial inclusion in addressing climate-related challenges in the Fourth Industrial Revolution and lessons for sustainable development goals is the focus of this study. Though climate change worsens poverty, a substantial body of data indicates that financial inclusion can assist individuals to become a little more resilient, either too frequent or severe weather events or the steady effects of shifting rainfall patterns, sea-level rise, or saltwater intrusion. Persons dealing with changing environmental conditions can benefit from “savings, credit, insurance, money transfers, and new digital distribution methods. Because most people have access to a cell phone, digital financial services have the potential to reach more unbanked people, notably women, the poor, and those living in rural areas.” Following natural disasters, mobile banking accounts allow poor people to receive money transfers as well as provide a quick, focused, and cost-effective way to help impacted populations.

According to comprehensive research, “greater accessibility to formal financial services can assist the poor manage with income shocks, whether they are weather-related such as drought or floods, health and wellbeing threats, or other unforeseen impediments” (Poverty Action, 2017). Everything hinges on whether efficient financial goods and services can be designed to suit the specific requirements of farmers and others whose livelihoods are being disturbed by changing climate, make these products more accessible to the poor, and promote the adoption of these products and services. According to Arner et al. (2020), “financial inclusion entails providing financial products and services to all members of society at a reasonable cost, and it enables people to effectively manage their financial obligations, lowers poverty, and promotes overall economic growth.” Arner et al. (2020) also argued that financial inclusion reduces people's susceptibility through facilitating saving, for example, allowing people to weather economic downturns and invest in their education, health, and microbusinesses. Again, financial inclusion improves everyday efficiency, bills may be paid electronically without taking time off from work and financial inclusion allows people's financial risks to be socialized and diversified through the financial system (Arner et al., 2020). An example given by Arner et al. (2020) was breadwinner insurance which can help people avoid falling back into poverty. Finally, financial inclusion promotes economic growth by expanding financial resources available to support real-world activities, especially for individuals and small and medium-sized businesses (SMEs).

Cohen (2021) contended that mobile payments are the lifeblood of the FinTech sector, but a new breed of agriFinTech companies is emerging in nations where agriculture accounts for most of the economic output and employment. These companies' services are essential for fostering resilience among small-scale farmers. Cohen (2021) suggested that e-commerce and business-to-business software applications that focus on food systems have used algorithms to optimize logistics and cut out expensive intermediaries, cutting prices while increasing the wealth of farmers, supporting the small-holder farming business model. For instance, the Japanese company Secai Marche stands out because it directly links ASEAN farmers with the Japanese restaurant and food business using AI-based algorithms that forecast demand and route orders to the most effective mode of transportation. According to Kass-Hanna et al. (2022), a large portion of the world's 1.7 billion adults still live in South Asia and Sub-Saharan Africa without access to formal financial services. The latest financial inclusion strategies give these at-risk groups access to a variety of financial services to construct extra inclusive and financially resilient communities. Digital financial literacy is on the rise because of the FinTech trend and the fact that over 67% of people worldwide own smartphones. In their study, Kass-Hanna et al. (2022) demonstrate that promoting inclusion and financial resilience requires both digital and financial literacy. Kass-Hanna et al. (2022) concluded that traditional financial literacy needs to be redefined to include digital literacy. This has significant ramifications for nations that are considering combining financial literacy with digital literacy as a dual strategy to increase households' long-term financial resilience.

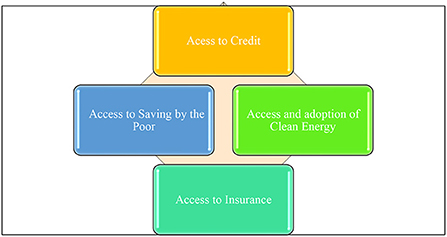

In Figure 7 below some of the Channels Through Which Financial Inclusion Can Help to Address Climate-related Challenges are presented which include access to saving by the poor, and access to credit and insurance.

Figure 7. Channels through which financial inclusion can help to address climate-related challenges. Source: Author's analysis.

In Figure 6 above some of the Channels Through Which Financial Inclusion Can Help to Address Climate-related Challenges are presented which include access to saving by the poor, and access to credit and insurance.

Poor households may be able to protect themselves against the harmful effects of climate change if they have access to financing (Calderone et al., 2019). Whilst also poor households could find it very hard to afford expensive initial costs of low-carbon technology solutions as well as other investments that safeguard against the unexpected and slow but steady effects of climate change, the availability of credit can spread out these costs in the long run, according to Innovation for Product Action (2017). The Innovation for Product Action (2017) provided instances of how this might play out. Extending loans to smallholder farmers, according to Innovation for Product Action (2017), allows them to invest in agricultural inputs that boost resiliency, like improved seed varieties, irrigation, fertilizer, and insecticides. In addition, it is believed that Farmers could save during harvest and planting cycles by tailoring loan disbursement and repayment terms to their seasonal cash flow, increasing agricultural yields and revenue while reducing the risk of potential droughts, floods, and other climatic changes (Innovation for Product Action, 2017; Stage and Thangavelu, 2019).

Furthermore, comprehensive research has demonstrated that climate-resistant inputs like hybrid seeds can boost smallholder farmers' resilience in the face of climate-related shocks. Increased access to credit, according to research, helps farmers invest in technology that raises crop production and productivity, such as improved seeds, irrigation, fertilizer, and insecticides (Bryan et al., 2009; Le et al., 2020; Ojo et al., 2021). In Kenya, for instance, researchers discovered that asset-collateralized loans increased the uptake of rainwater collection tanks, allowing dairy farmers to have more consistent and easy access to water while also increasing their output (Jack et al., 2015, 2016; Innovation for Product Action, 2017). Another example is Mumuadu Rural Bank in Ghana extended credit with crop price insurance to farmers who were chosen at random. The loan stated “specifically that if crop prices during harvest fell below a set level, the bank will forgive half of the loan and interest payments. Farmers who received the loan spent much more on inputs, primarily fertilizer, than farmers who did not receive the loan and did not receive crop price protection” (Karlan et al., 2011). In other studies, from Kenya, “researchers discovered that giving farmers the choice to purchase fertilizer when they got their harvest money improved fertilizer use by 14 percentage points on a 23-point baseline.” These effects were “like those obtained with a 50% price subsidy. Increasing credit availability during the lean season can also assist farming households in better allocating labor, resulting in increased production and wellbeing” (Innovation for Product Action, 2017).

Another example is where Farmers in Mali saw a large rise in farm investments and expenditures, as well as fertilizer, insecticides, and herbicides, after receiving an innovative loan product tailored to their seasonal cash flow (Beaman et al., 2014; Innovation for Product Action, 2017). Again, Farmers' communities in Zambia with access to credit supplied at the beginning of the lean season and reimbursed after harvesting produced 5.6% more on average than comparator households. During the lean season, they were also about 40% less likely to face food insecurity. Clients who are faced with natural catastrophes or other unforeseen circumstances may benefit from credit solutions that offer flexible repayment plans. While combining credit and insurance products may aid clients who are exposed to climate-related risk, the outcomes of research examining this method are varied (Fink et al., 2014). As revealed by these studies, poor households with access to money may be able to protect themselves from the detrimental effects of climate change. What this research shows is that if poor households have access to money, they may be able to defend themselves from the negative effects of climate change. As financial markets expand and become more inclusive in the Fourth Industrial Revolution, FinTech presents potential to promote financial stability and access by vulnearable groups which can allow themselves to fight the negative effects of climate change. Despite numerous policy initiatives to improve climate adaptation in this context, Batung et al. (2022) argued that smallholders' lack of access to credit constitutes one of the crucial dimensions of extreme climate vulnerability. While climate change is a huge occurrence, it really has substantially constrained agricultural output in the Developing World caused by changes of crucial atmospheric elements such as temperature extremes and unexpected weather patterns over the last fifty years. FinTech services must be used to guarantee that smallholder farmers may obtain loans that will enable them to withstand the detrimental consequences of climate change. According to Batung et al. (2022) informal credit sources may be able to give smallholder farmers access to the more flexible financial loan options they require to improve rural agricultural output and climate change resilience.

Many researchers believe that increased savings rates can assist the poor in smooth consumption after unanticipated shocks and endure the burden of gradual cost rises (Meng, 2003; Ganong et al., 2020). According to estimates, “boosting savings alone might minimize the effects of climate change on wellbeing by 4.5–7.6% in Guatemala, Mauritania, Angola, Peru, Gabon, Morocco, Zambia, Colombia, Kyrgyz Republic, Democratic Republic of Congo, Mongolia, Niger, and El Salvador.” Savings accounts with banking institutions, rather than informal savings in the form of livestock or homes, give the most resilience because they allow the poor to diversify risks, gain access to credit, and speed up recovery and reconstruction. In Malawi, for example, farmers using savings accounts increased agricultural input investments by 13% and agricultural productivity by 21%. Karlan et al. (2014) concur that saving is critical in mitigating the effects of climate change. Savings, according to Karlan et al. (2014), are another financial tool that might help the poor smooth consumption in times of unforeseen setbacks or support investments in climate-resilient technologies. It's also thought that formal savings accounts are a better way of saving money than informal savings in livestock or other items that could be harmed by climate change. Various digital financial inclusion tools can help people save more by resources allocation “for specific purchases using labeling, where a client labels finances as they set them aside for a clear objective, or commitment devices, where a saver chooses to restrict access to his or her funds to save toward a goal.” These technologies can also assist users in directing investment toward agriculture, which is the most sensitive to climate change's consequences.

Brune et al. (2016) conducted a “randomized intervention among Malawian farmers intending to encourage formal financial savings for agricultural inputs in Malawi. Farmers in the treated group were given the option of having their cash crop harvest revenues transferred directly into new bank accounts in their names, whilst those in the control group were paid in cash. The experiment resulted in increased savings in the months leading up to the next agricultural planting season, as well as increased agricultural input utilization during that season.” The study also discovered that the therapy had a positive impact on subsequent crop sale revenues and household spending. In another study, Stage and Thangavelu (2019) reproduced and reanalyzed data from a randomized controlled trial of a program designed by Brune et al. to help Malawian tobacco farmers save formal money. According to the findings, giving farmers access to personal savings accounts increased their banking activities and improved their household's wellbeing. As a result of these findings, we can deduce that “higher savings rates can help the poor smooth consumption after unexpected shocks and bear the burden of steady cost increases when a disaster occurs.” This view is supported by another study from Bastian et al. (2018). In an experiment with and without business training, women microentrepreneurs in Tanzania were encouraged to register for a mobile savings account. The results showed that 6 months after the intervention, women were saving significantly more using the mobile wallet and that the business training aided this effect. The findings also found that women receive more microloans through the product's mobile account, which is an additional feature. As a result, financial inclusion measures must be stepped up, particularly in areas vulnerable to climate change disasters.

Improving poor people's access to different forms of insurance can safeguard them from a range of climate-related dangers, such as persistent droughts, rising sea levels, disease transmission, and a rise in pests that threaten crops and the spreading of diseases. According to Innovation for Product Action (2017), “parametric insurance or weather index insurance for farmers, as well as microinsurance for individuals without traditional insurance, provide a cushion from severe weather events and volatility. Insurance gives smallholder farmers the confidence to undertake the investment options and production decisions that boost agriculture production. In Ghana, the availability of rainfall index insurance encouraged farmers to make larger investments, resulting in higher returns” (Innovation for Product Action, 2017). Research points out that farmers who are granted subsidized insurance are more likely to invest in increasing agricultural productivity and in some circumstances, insurance products may be a better financial tool for supporting growth than cash or credit (Vigani and Kathage, 2019; Sibiko and Qaim, 2020). Small-scale farmers for instance are extremely sensitive to the risk associated with their investment, and in the absence of proper insurance solutions, they will make decisions to reduce risk while also reducing profitability. Investments can be facilitated by providing capital in the form of credit or cash, but such investments may increase risk because they are not guaranteed to pay off. They also can't provide the same level of protection against weather-related risks as insurance can. One of the reasons why the poor are most in danger is because they lack the resources to deal with the issues that climate change poses to their health and livelihood. Access to “formal financial institutions, such as insurance, savings, and loans, can help the poor smooth consumption when they encounter unanticipated setbacks, according to rigorous evidence.” Therefore, financial services are acting as a tool for building resilience in the face of climate change-related shocks. Financial services as a means of increasing the availability, cost, and adoption of green technologies that minimize greenhouse gas emissions impacts. Specially tailored financial services may enable the poor to participate in environmentally friendly practices at a lower cost, reducing environmental impact. The next section will give a more detailed explanation of how financial inclusion can help to address climate change-related problems.

Financial inclusion is widely acknowledged to benefit the environment by encouraging the use of renewable energy sources (Feng et al., 2022). In China, Feng et al. (2022) looked at whether financial inclusion has any impact on renewable energy use and environmental quality. The findings revealed that an increase in the number of “ATMs and overall insurance had a long-term favorable impact on renewable energy use in China. Financial inclusion promotes renewable energy usage and lowers CO2 emissions in China, according to the findings.” As a result, it's critical to redirect resources toward ecologically sustainable consumption and manufacturing. FinTech companies can indeed enable the poor to make a reasonable investment in other, greener technology, as well as stimulate the development of good environmental practices that reduce greenhouse gas emissions and may improve individual wellbeing. Current study into these innovative solutions indicates that there is a market for them, but more research is needed to determine how best to create and promote goods that stimulate the adoption of cleaner technologies and better environmental behaviors (Innovation for Product Action, 2017). Payments for ecosystem services, in which individuals or businesses are compensated for doing ecologically beneficial services, is one method that financial products might aid in the implementation of the best environmental practices. In Uganda, Jayachandran et al. (2016) found that encouraging landowners to not chop trees led to lower tree cover reduction in villages where the incentive was given. The program was a successful and cost-effective strategy to reduce carbon dioxide emissions, and it resulted in much-reduced deforestation in the villages targeted. Although there is an indication that farmers can be enticed to invest in environmentally friendly processes if, given the correct incentives, more innovation about how to integrate such incentive schemes into conventional financial products and services is needed.

The Innovation for Product Action (2017) reported that green loans, for example, give customers finance to buy ecologically friendly items like solar panels, better-insulated homes, and organic seeds and fertilizers. These loans, however, must be thoroughly analyzed because they are new, to determine whether they can encourage the adoption of ecologically beneficial behaviors and lower the population's carbon footprint (Innovation for Product Action, 2017). “Solar energy microgrids are an example of a sustainable energy technology that may be integrated into financial services to benefit clients, service providers, and the environment. These grids are designed to be cost-effective for users, and they have the potential to improve disadvantaged communities' resilience to power outages due to weather disasters while also decreasing carbon emissions by burning fewer fossil fuels” (Innovation for Product Action, 2017). Customers can use “pay-as-you-go (PAYGO) services to get access to environmentally friendly technology like solar microgrids and other alternative energy sources. A client can take out a small loan to purchase power from an off-grid solar panel and then pay it back in installments through mobile money accounts that are simple to maintain.” If a client fails to make a payment, the devices might be turned off to serve as a reminder. These platforms are not only handy for clients, who may purchase as much electricity as they require, but they are also less hazardous for suppliers, who can terminate service if payment is not received. Consumers in South Africa, according to an observational study, take advantage of the flexibility that prepaid power meters allow when this technology is accessible. According to preliminary findings from an IPA study done in Kenya, providing shopkeepers in Nairobi with PAYGO solar lamps resulted in lower kerosene use (Adwek et al., 2020; Ndiritu and Engola, 2020). What can be concluded from this discussion is that, if implemented successfully, financial inclusion can be a mechanism for addressing climate change and achieving Goal 13 goals.

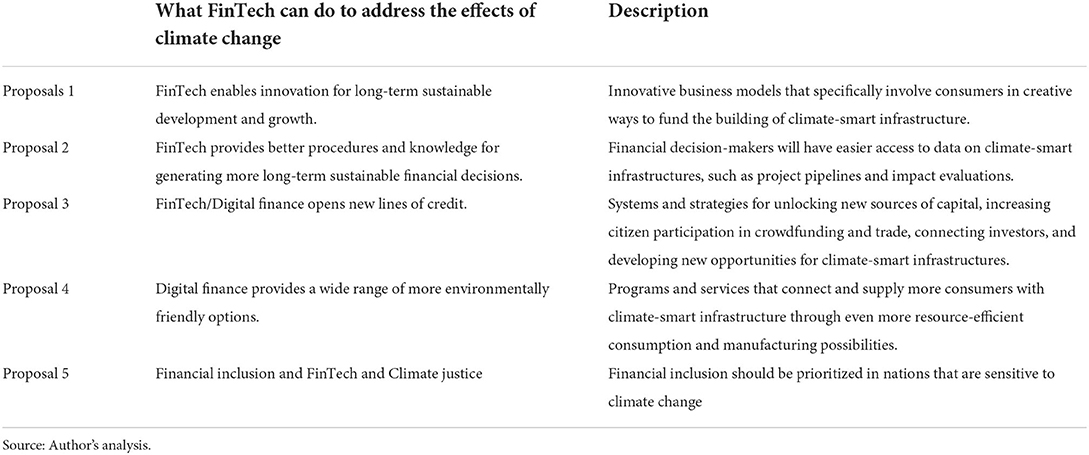

The table below summarizes how FinTech and digital finance can help citizens to support climate-smart infrastructure in their daily activities which can help in addressing the negative effects of climate change (United Nations Environment Programme, 2019; Macchiavello and Siri, 2020; Benni, 2021).

Table 2 shows some of the concepts for FinTech and digital money that can assist citizens in supporting climate-smart infrastructure in their daily activities, thereby reducing the negative effects of climate change. These include, FinTech enables innovation for long-term sustainable development and growth, FinTech provides better procedures and knowledge for generating more long-term sustainable financial decisions, FinTech /Digital finance opens new lines of credit, and Digital finance provides a wide range of more environmentally friendly options as well as financial inclusion and FinTech and Climate justice.

Table 2. How FinTech allows citizens to support climate-smart infrastructure.

Since its inception, the United Nations Framework Convention on Climate Change (UNFCCC) has evolved to emphasize climate change as a fundamental concern of human rights and global justice (Gach, 2019; Ranganathan and Bratman, 2021). Being financially savvy as well as having access to inclusive financial products and services can help many individuals, families, and micro-businesses during times of natural disasters (Jafry et al., 2019; McArdle, 2021). Increasing access to microfinance can help promote community-level environmental and climate action, and this will have a positive impact on local economies. In fact, it is vital to link locals with capital that is open to all especially using various FinTech products and services. Long-term financial and technical requirements can be met through the utilization of revolving funds. Households and small enterprises without access to traditional banking can benefit from microfinance. Environmentally friendly lifestyles and assisting communities at high risk from the effects of climate change are two of the main aims of green finance. Governments and regulatory bodies are increasingly focusing on this type of financing. Investment and financing for growth must be balanced with conservation of the environment in green finance. To execute international agreements and goals, such as the sustainable development goals (SDGs), vulnerable populations must have easy access to financial resources. To enhance green finance, regulatory frameworks, fiscal incentives, and appropriate price changes must be developed in tandem with financial system transformation. It is possible to lessen the effects of climate change and the need for post-disaster rehabilitation by using green financing and various FinTech products. There is a pressing need for capital mobilization because these vulnerable people are underserved and unbanked.

The growing need for greater access to financial resources by individuals and businesses, lead to the development of various financial instruments like microfinance, insurance, and cash transfers among other developments. There is also a rise in the number of development partners who are advocating for the use of these tools to address disaster risks and climate change-related challenges. With the increase in risk reduction needs and challenges related to climate change, there is a need to evaluate the efficacy of the various financial instruments (financial inclusion) in addressing climate-related challenges. Using secondary data analyzed through document analysis, the study sought to answer the following question, what is the role of financial technology in addressing the problems or risks related to climate change. Through content analysis of secondary sources of data, the results of the study indicated that financial inclusion through FinTech could help in building the resilience of households, individuals, and businesses when there is either a sudden climate event or even gradual implications of different rainfall patterns, the rise in sea level or salter water intrusion. Insurance, savings, credit, money transfers and the new digital delivery channels can assist in the provision of critical support for the victims of climate change and those who manage the new environmental realities. Therefore, the study recommends that it is very important for development patterns, governments, and civil society to promote financial inclusion through FinTech as one of the channels that can help in addressing the risks of climate-related challenges and the achievement of sustainable development goals.

DM: conceptualization and writing of the paper.

This study was supported by the University of Johannesburg.

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Abor, J. Y., Amidu, M., and Issahaku, H. (2018). Mobile telephony, financial inclusion, and inclusive growth. J. Afri. Bus. 19, 430–453. doi: 10.1080/15228916.2017.1419332

Adwek, G., Boxiong, S., Ndolo, P. O., Siagi, Z. O., Chepsaigutt, C., Kemunto, C. M., et al. (2020). The solar energy access in Kenya: a review focusing on Pay-As-You-Go solar home system. Environ. Dev. Sustainabil. 22, 3897–3938. doi: 10.1007/s10668-019-00372-x

Aguila, E., Angrisani, M., and Blanco, L. R. (2016). Ownership of a bank account and health of older Hispanics. Econ. Lett. 144, 41–44. doi: 10.1016/j.econlet.2016.04.013

Ajefu, J. B., Demir, A., and Haghpanahan, H. (2020). The impact of financial inclusion on mental health. SSM-Popul. Health 11, 100630. doi: 10.1016/j.ssmph.2020.100630

Al Nawayseh, M. K. (2020). Fintech in COVID-19 and beyond: what factors are affecting customers' choice of fintech applications?. J. Open Innov: Technol. Market Complex. 6, 153. doi: 10.3390/joitmc6040153

Alwi, S. (2021). Fintech as financial inclusion: Factors affecting behavioral intention to accept mobile e-wallet during Covid-19 outbreak. Turkish J. Comput. Math. Educ. 12, 2130–2141. Available online at: https://www.proquest.com/openview/5d08fb73ccb0f77df48378a8b925a58c/1?pq-origsite=gscholar&cbl=2045096

Anshari, M., Almunawar, M. N., Masri, M., Hamdan, M., Fithriyah, M., and Fitri, A. (2021). “Digital wallet in supporting green FinTech sustainability,” in 2021 Third International Sustainability and Resilience Conference: Climate Change (Piscataway, NJ: IEEE), 352–357. doi: 10.1109/IEEECONF53624.2021.9667957

Arner, D. W., Buckley, R. P., Zetzsche, D. A., and Veidt, R. (2020). Sustainability, FinTech and financial inclusion. Eur. Bus. Org. Law Rev. 21, 7–35. doi: 10.1007/s40804-020-00183-y

Banna, H., Hassan, M. K., and Rashid, M. (2021). Fintech-based financial inclusion and bank risk-taking: evidence from OIC countries. J. Int. Fin. Market. Instit. Money 75, 101447. doi: 10.1016/j.intfin.2021.101447

Bastian, G., Bianchi, I., Goldstein, M., and Montalvao, J. (2018). Short-Term Impacts of Improved Access to Mobile Savings, With and Without Business Training: Experimental Evidence From Tanzania. Documents de travail. Washington, DC: World Bank. 478.

Batung, E. S., Mohammed, K., Kansanga, M. M., Nyantakyi-Frimpong, H., and Luginaah, I. (2022). Credit access and perceived climate change resilience of smallholder farmers in semi-arid northern Ghana. Environ. Dev. Sustain. 2022, 1–30. doi: 10.1007/s10668-021-02056-x

Baulch, B., Do, T. D., and Le, T. H. (2015). Solar Home Systems in Ho Chi Minh City: A Promising Technology Whose Time Has Not Yet Come. Munich: The Munich Personal RePEc Archive (MPRA) University Library Geschwister-Scholl-Platz 1 D-80539.

Beaman, L., Karlan, D., Thuysbaert, B., and Udry, C. (2014). Self-Selection Into Credit Markets: Evidence From Agriculture in Mali (No. w20387). Cambridge, MA: National Bureau of Economic Research. doi: 10.3386/w20387

Benni, N. (2021). Digital Finance and Inclusion in the Time of COVID-19: Lessons, Experiences and Proposals. Rome: Food & Agriculture Org.

Brune, L., Giné, X., Goldberg, J., and Yang, D. (2016). Facilitating savings for agriculture: field experimental evidence from Malawi. Econ. Dev. Cult. Change 64, 187–220. doi: 10.1086/684014

Bryan, E., Deressa, T. T., Gbetibouo, G. A., and Ringler, C. (2009). Adaptation to climate change in Ethiopia and South Africa: options and constraints. Environ. Sci. Pol. 12, 413–426. doi: 10.1016/j.envsci.2008.11.002

Calderone, M., Weingärtner, L., and Kroessin, M. R. (2019). Investing in Financial Inclusion for Climate Resilience and Adaptation. The Role of Islamic Financial Services. London: ODI.

Cen, T., and He, R. (2018). “Fintech, green finance and sustainable development,” in 2018 International Conference on Management, Economics, Education, Arts and Humanities (MEEAH 2018) (Atlantis Press), 222–225. doi: 10.2991/meeah-18.2018.40

Charfeddine, L., and Kahia, M. (2019). Impact of renewable energy consumption and financial development on CO2 emissions and economic growth in the MENA region: a panel vector autoregressive (PVAR) analysis. Renew. Energy 139, 198–213. doi: 10.1016/j.renene.2019.01.010

Chauvet, L., and Jacolin, L. (2017). Financial inclusion, bank concentration, and firm performance. World Dev. 97, 1–13. doi: 10.1016/j.worlddev.2017.03.018

Chenet, H. (2021). “Climate change and financial risk,” in Financial Risk Management and Modeling (Cham: Springer), 393–419. doi: 10.1007/978-3-030-66691-0_12

Chueca Vergara, C., and Ferruz Agudo, L. (2021). Fintech and sustainability: do they affect each other? Sustainability 13, 7012. doi: 10.3390/su13137012

Cohen, A. (2021). FinTech Can Help Fill Climate Resilience Gaps In Emerging Markets. Available online at: https://www.forbes.com/sites/arielcohen/2021/09/30/fintech-can-help-fill-climate-resilience-gaps-in-emerging-markets/?sh=31db7d0961c8

Colorado State University (1997). An Introduction to Content Analysis Writing@CSU: Writing Guide. Available online at: http://writing.colostate.edu/references/research/content/pop2a.cfm (accessed January 4, 2022).

Elo, S., Kääriäinen, M., Kanste, O., Pölkki, T., Utriainen, K., and Kyngäs, H. (2014). Qualitative content analysis. SAGE Open 4, 522633. doi: 10.1177/2158244014522633

Feng, J., Sun, Q., and Sohail, S. (2022). Financial inclusion and its influence on renewable energy consumption-environmental performance: the role of ICTs in China. Environ. Sci. Poll. Res. 9, 1–8. doi: 10.1007/s11356-022-19480-9

Fink, G., Jack, B. K., and Masiye, F. (2014). Seasonal Credit Constraints and Agricultural Labour Supply: Evidence From Zambia (No. w20218). Cambridge, MA: National Bureau of Economic Research. doi: 10.3386/w20218

Frankel, J. A., and Romer, D. (1999). Does trade cause growth? Am. Econ. Rev. 89, 379–399. doi: 10.1257/aer.89.3.379

Fu, J., and Mishra, M. (2020). The Global Impact of COVID-19 on FinTech Adoption. Swiss Finance Institute Research Paper No. 20–38. Available online at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3588453

Gach, E. (2019). Normative shifts in the global conception of climate change: the growth of climate justice. Soc. Sci. 8, 24. doi: 10.3390/socsci8010024

Ganong, P., Jones, D., Noel, P. J., Greig, F. E., Farrell, D., and Wheat, C. (2020). Wealth, Race, and Consumption Smoothing of Typical Income Shocks (No. w27552). Cambridge, MA: National Bureau of Economic Research. doi: 10.3386/w27552

Gasper, R., Blohm, A., and Ruth, M. (2011). Social and economic impacts of climate change on the urban environment. Curr. Opin. Environ. Sustainabil. 3, 150–157. doi: 10.1016/j.cosust.2010.12.009

Goldstein, I., Jiang, W., and Karolyi, G. A. (2019). To FinTech and beyond. Rev. Fin. Stud. 32, 1647–1661. doi: 10.1093/rfs/hhz025

Gyasi, R. M., Adam, A. M., and Phillips, D. R. (2019). Financial inclusion, Health-Seeking behavior, and health outcomes among older adults in Ghana. Res. Aging. 41, 794–820. doi: 10.1177/0164027519846604

Hansen, L. P. (2022). Central banking challenges are posed by uncertain climate change and natural disasters. J. Monetary Econ. 125, 1–15. doi: 10.1016/j.jmoneco.2021.09.010

Hinson, R., Lensink, R., and Mueller, A. (2019). Transforming agribusiness in developing countries: SDGs and the role of FinTech. Curr. Opin. Environ. Sustainabil. 41, 1–9. doi: 10.1016/j.cosust.2019.07.002

Hope, K. R. (2009). Climate change and poverty in Africa. Int. J. Sustain. Dev. World Ecol. 16, 451–461. doi: 10.1080/13504500903354424

Hsieh, H. F., and Shannon, S. E. (2005). Three approaches to qualitative content analysis. Qualitat. Health Res. 15, 1277–1288. doi: 10.1177/1049732305276687

Huang, R., Kale, S., Paramati, S. R., and Taghizadeh-Hesary, F. (2021). The nexus between financial inclusion and economic development: comparison of old and new EU member countries. Econ. Anal. Policy 69, 1–15. doi: 10.1016/j.eap.2020.10.007

Hussain, M., Ye, C., Ye, C., and Wang, Y. (2022). Impact of financial inclusion and infrastructure on ecological footprint in OECD economies. Environ. Sci. Pollut. Res. 29, 21891–21898. doi: 10.1007/s11356-021-17429-y

IMF (2019). Fiscal Monitor: How to Mitigate Climate Change. Available online at: https://www.imf.org/en/Publications/FM/Issues/2019/09/12/fiscal-monitor-october-2019 (accessed April 10, 2022).

Immurana, M., Iddrisu, A. A., Boachie, M. K., and Dalaba, M. A. (2021). Financial inclusion and population health in Africa. J. Sustain. Fin. Invest. 2021, 1–16. doi: 10.1080/20430795.2021.1953929

Innovation for Product Action (2017). Climate Change and Financial Inclusion. Available online at: https://www.poverty-action.org/publication/climate-change-and-financial-inclusion

Inoue, T. (2019). Financial inclusion and poverty reduction in India. J. Fin. Econ. Policy 2018, 12. doi: 10.1108/JFEP-01-2018-0012

International Monetary Fund (2019). Climate Change and Financial Risk. Available online at: https://www.imf.org/external/pubs/ft/fandd/2019/12/climate-change-central-banks-and-financial-risk-grippa.htm (accessed March 10, 2022).

Jack, W., Kremer, M., de Laat, J., and Suri, T. (2015). Joint Liability, Asset Collateralization, and Credit Access: Evidence From Rainwater Harvesting Tanks in Kenya. Chicago, IL: University of Illinois.

Jack, W., Kremer, M., De Laat, J., and Suri, T. (2016). Borrowing Requirements, Credit Access, and Adverse Selection: Evidence From Kenya (No. w22686). Cambridge, MA: National Bureau of Economic Research. doi: 10.3386/w22686

Jafino, B. A., Walsh, B., Rozenberg, J., and Hallegatte, S. (2020). Revised Estimates of the Impact of Climate Change on Extreme Poverty by 2030. Washington, DC: World Bank. doi: 10.1596/1813-9450-9417

Jafry, T., Helwig, K., and Mikulewicz, M. (2019). Routledge Handbook of Climate Justice. Routledge, Taylor & Francis Group, Earthscan from Routledge. doi: 10.4324/9781315537689