95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Appl. Math. Stat. , 03 January 2024

Sec. Mathematical Finance

Volume 9 - 2023 | https://doi.org/10.3389/fams.2023.1250227

This article is part of the Research Topic Applied Quantitative Methods for Corporate Finance and Investments View all 5 articles

Mohammad Salem Oudat1Basel J. A. Ali2

Mohammad Salem Oudat1Basel J. A. Ali2 Sameh Abdelhay1*Haziem M. Hazaimeh1Mohamed Saif Rashid Altalay3Attiea Marie1Magdi El-Bannany1

Sameh Abdelhay1*Haziem M. Hazaimeh1Mohamed Saif Rashid Altalay3Attiea Marie1Magdi El-Bannany1Risk management has emerged as a critical element across several economic sectors, with particular significance in the banking industry. The governing bodies of these industries encounter a multitude of threats stemming from the escalation of an unpredictable economic environment, the intricacy of transactions and big data, and several other concealed factors. The primary aim of the present research is to investigate the impact of certain financial risks, including capital risk, liquidity risk, and operational risk, on the financial performance of both commercial and Islamic banks operating within the banking sector of the United Arab Emirates. The study will focus on the time frame spanning from 2015 to 2022. The data used in this study was sourced from the annual reports of banks, which were acquired from the official websites of the Abu Dhabi Securities Exchange and the Dubai stock market. The most prevalent indicators used to assess a bank's financial performance are Return on Assets (ROA) and Return on Equity (ROE). In contrast, the financial risk metrics included three distinct categories of risk: capital risk, liquidity risk, and operational risk. The findings indicate that there is a statistically significant positive relationship between capital risk and both return on assets (ROA) and return on equity (ROE). However, it was observed that neither liquidity risk nor operational risk had a statistically significant impact on either of the financial performance metrics. Moreover, the size of a bank has a notable and favorable impact on both return on assets (ROA) and return on equity (ROE). The ramifications of the study's conclusions have significant importance for regulators, bank management, and investors. IPolicymakers need to prioritize the enhancement of the regulatory framework pertaining to caboutements in order to the financial stability of banks. Bank managers should give priority to the management of capital risk and the size of the bank in order to their financial performance. In order to optimize profits, it is important for investors to carefully evaluate and take into account the many risk considerations associated with their investment selections.

JEL: G20, G21

The rapid advancement of information and manufacturing technologies, together with the emergence of digital marketing, has given rise to an unprecedented corporate landscape. This new environment exposes economic sectors to a wider array of dangers that are both intricate and multifaceted compared to previous eras. The management of risk has gained increased significance across several sectors of the economy, necessitating the need for its identification, assessment, and control. Banks' business models are designed to assume financial risk and get profit from it. Nevertheless, non-financial risk, including regulatory failures, malfeasance, technological issues, and operational obstacles, is mostly associated with negative consequences. Financial risks pose significant issues for several firms, particularly those that are publicly traded and reliant on market conditions for their valuation. Credit risk, market risk, and liquidity risk are among the financial risks that are often encountered by firms. On the other hand, non-financial risks include model risk, solvency risk, operational risk, and legal risk [1, 2].

Financial institutions are used to assuming financial risk and deriving profit from it. Nevertheless, banks have a broad role since they function as financial middlemen, facilitators, and supports. Banks position themselves as a reliable institution for depositors, business partners, and investors. Liquidity risk might potentially emerge from these various activities since they bear complete responsibility for providing liquidity as required by the third party. Islamic banks face the need for further endeavors to enhance their liquidity management capabilities, owing to their distinct attributes and adherence to Sharia rules [3].

Over the last two decades, the global economy has encountered a multitude of crises. The crisis in 2008 showed the significance of risk management not just for industrial enterprises, but also for financial institutions. In recent times, there has been an increased focus on the implementation of risk management, both by governmental bodies and enterprises. This emphasis stems from the recognition that effective risk management is a crucial factor in enabling organizations to achieve more success and effectively navigate potential future risks. Basel I, II, and III have been implemented to structure the operations of financial institutions and enhance risk management practices within the global financial sector, particularly in the banking industry. These frameworks include the revision and enforcement of legislation and supervisory measures, which serve to mitigate financial risks. According to Hahm [4], there exists a considerable correlation between the performance of commercial banks and their level of pre-crisis exposure. This highlights the need to prioritize the enhancement of financial direction and risk management practices as a means to bolster financial liberalization.

The United Arab Emirates (UAE) has a comprehensive financial system that is characterized by its integration, with the system being organized and regulated by the central bank. The establishment comprises both domestic and foreign conventional banks, Islamic banks, insurance businesses, and money-changers, as well as entities facilitating the process of establishing bank accounts and providing financial services. The central bank assumes the responsibility of overseeing and controlling the monetary system and banking activities. The United Arab Emirates (UAE) has emerged as a prominent player in the global financial landscape via its strategic implementation and utilization of sophisticated technology. This approach has enabled the UAE to effectively navigate the financial industry and meet the evolving demands of customers by providing streamlined and effective financial goods and services.

The financial system performance in the United Arab Emirates (UAE) has been positively impacted by the COVID-19 epidemic in recent times. The global pandemic presented a crucial opportunity for private sector firms to expedite the process of digitizing financial services. Furthermore, the use of financial technology has been crucial in mitigating the risks associated with the pandemic and fostering the adoption of digital financial services among both businesses and people [5]. The primary objective in the contemporary financial sector is to attain sustainability as a fundamental effort via the use of digital advances and competitiveness. The use of novel technologies in the financial domain within the United Arab Emirates (UAE) facilitates the effective delivery of social goods and services to the government, corporations, and people while minimizing the associated time, effort, and expenses.

In addition to traditional banking institutions, the United Arab Emirates has developed Islamic banks that adhere to the principles of Sharia Law in their operations. As per UAE Federal Law No. 10 of 1980, Islamic banks have the authority to engage in various banking, conventional, investing, and financial services and activities. Individuals have the entitlement to partake in a comprehensive range of services and activities that are often conducted by financial institutions and fall within their purview. The United Arab Emirates (UAE) has implemented a division of services inside Islamic banks, including both local and international banking for individuals, local and foreign corporate banking, as well as specialized banking.

Banks may encounter many categories of hazards. Financial hazards are a category of risks that have the potential to substantially increase the overall risk profile of a bank according to Abdelhay S, El-Bannany MAGDI [6]. For example, a financial institution engaged in international currency transactions often has exposure to foreign currency risk. However, it also faces credit risk, liquidity risk, interest rate risk, and repricing risks if it maintains imbalances or open positions in its forward book. Moreover, the bank is confronted with operational risks that are linked to its organizational structure and operational processes. Technologies, particularly those about computers, that adhere to the laws and procedures of financial institutions, including safeguards and methodologies to combat fraudulent activities and instances of mismanagement. The risks associated with the company are interconnected with the banking business environment, including various macroeconomic factors, legal and regulatory considerations, policy implications, and the overall structure of the financial system according to Matar and Eneizan [7]. This includes elements such as auditing professionals and payment systems. Financial hazards are not limited just to conventional banks; they also pose a danger to Islamic banks and other financial institutions, hence impacting the whole economy of any given nation. In general, it can be posited that risk management is often regarded as a pivotal factor influencing the outcomes of many economic sectors, determining both their achievements and shortcomings according to Musah and Kong [8].

Numerous scholarly inquiries have been conducted to explore the correlation between financial risks and financial outcomes. However, it is worth noting that the majority of these investigations primarily focus on countries with distinct economic, social, and legislative contexts that differ from those of the United Arab Emirates (UAE). Consequently, caution must be exercised when attempting to extrapolate these findings to the specific circumstances of the UAE. Prior research has also indicated a deficiency in the examination of various categories of financial risks. For instance, Shamas et al. [9] demonstrated a decline in the number of studies investigating financial risks, including liquidity, as well as a decrease in the number of studies conducted in the Arabian Gulf region. This study aims to address the existing research gap by examining several financial risk factors, including capital risk, exchange rate risk, liquidity risk, and operational risk. The objective is to investigate the potential influence of these risks on the financial performance, namely the return on assets (ROA) and return on equity (ROE), of the banking institutions listed in the United Arab Emirates (UAE) stock markets to Panda and Nanda [10].

The primary aim of the present research is to investigate the influence of financial risks, namely capital, liquidity, and operational risks, on the performance of both conventional and Islamic banks in the context of the United Arab Emirates. The study focuses on a period spanning from 2015 to 2022 and includes a sample of 10 banks. This research aims to provide empirical data about the influence of specific risks on the financial performance of both conventional and Islamic banks. The study will examine many alternative indicators of financial performance and financial risks, focusing on current periods. Additionally, this research will provide a multitude of advantages for the bank's management and supervisory board, as well as for present and prospective investors of the publicly traded institutions in the stock market. The use of this approach enables the bank's management to enhance their comprehension of the impact of these risks on the financial performance of the institution. Furthermore, stakeholders may get advantages from the findings of the research by effectively incorporating the primary suggestions into their practices, therefore mitigating or averting the potential consequences of these hazards in subsequent instances.

The subsequent sections of the current research are organized as follows: Section 2 provides an overview of the existing empirical literature, highlighting relevant studies and their key results. Section 3 outlines the data collection process and research methods used in this study. Finally, Section 4 presents the analysis of the collected data and offers a comprehensive discussion of the findings. Lastly, the paper addresses the conclusion and provides suggestions.

Several theories have examined the impact of financial risk on the financial performance of a corporation. The firm's management may effectively implement suitable financial risk management practices by demonstrating a comprehensive understanding and recognition of these ideas. One prominent hypothesis in the field is known as the “Finance Distress Theory,” as posited by Baldwin and Mason [[11], p. 505]. According to this theory, when a company's value declines to a point where it becomes unable to fulfill its financial obligations, it enters a state of financial distress. Consequently, the first indication of financial trouble often manifests as a violation of debt obligations, which may be accompanied by a deviation from the firm's stated objective or a reduction in dividend payments. This phenomenon refers to a situation in which companies are unable to earn profits or revenue, and therefore, they are unable to fulfill financial responsibilities. In this particular scenario, the banking sector's inability to fulfill deposit withdrawals and loan disbursements gives rise to liquidity risk. Similarly, the occurrence of credit risk is seen when financial institutions own a multitude of non-performing loans inside their financial records due to borrowers' failure to repay or their delayed repayment of loans. Therefore, banks need to prioritize and closely oversee all financial risks to prevent or mitigate any financial turmoil in the future. The financial distress hypothesis has relevance in the present research about the influence of financial risk on the financial performance of banks according to Mohamed [12].

Financial risk is a significant factor that has a direct impact on the profitability of a firm. It leads to increased fluctuations in returns and encompasses various types of risks, including capital, liquidity, credit, and operational risks. These risks collectively contribute to the volatility of a firm's financial performance [13–15]. Additionally, the theory posited that inadequate management of financial risk is a contributing factor to the decline in a firm's financial performance. The financial performance of enterprises is a crucial factor in shaping the strategy, operational leverage, and investment choices of the organization, with the ultimate goal of attaining the desired degree of financial stability. Banks are widely regarded as a fundamental component of the financial system, assuming a significant role in fostering the economic development of nations by offering a range of financial services to people, organizations, and governmental entities. Consequently, the occurrence of any vulnerabilities in the operational efficiency of banks may result in the destabilization of the domestic financial system, potentially precipitating a financial crisis that can profoundly impact the functioning of financial markets. This was notably exemplified by the 2008 financial crisis, particularly the collapse of Lehman Brothers Bank.

Financial ratios, such as profitability, liquidity, assets utilization, and debt utilization, are frequently employed to assess the financial performance of firms. To utilize these ratios effectively, it is necessary to analyze historical financial statement data to make informed predictions about the performance of the firm. This information can then be used to make appropriate decisions. However, existing literature has explored several studies that investigate the correlation between financial risks and financial performance in both the banking industry and other firms. Nonetheless, conflicting findings have emerged, particularly within the banking industry, when comparing conventional banks to Islamic banks. The present research aims to investigate the subject matter by using recently acquired financial data pertaining to botaboutl and Islamic banks, obtained from a dynamic financial market in the United Arab Emirates, covering the time spaperiod15 to 2022. The following discourse addresses many relevant empirical studies that have investigated the influence of financial risks on financial performance, using identical research characteristics but yielding divergent outcomes.

Financial performance is a quantifiable evaluation of the effectiveness with which a company utilizes its resources to create income. Furthermore, this word is often used as a standard metric for assessing the total fiscal wellbeing within a specific time frame of precisely 12 months. The existing literature indicates that there is significant variation in both the components and ratios of bank profitability across different nations and regions [16]. Consistent with prior research conducted by Grier [17], profitability ratios such as Return on Assets (ROA), Return on Equity (ROE), and Earnings per Share (EPS) are often used as metrics for assessing the profitability of a company. Furthermore, according to Grier [17], the bank's profitability is regarded as a significant indication of the bank's credit analysis due to its direct correlation with management performance results. The performance of a bank serves as an indicator of its ability to create long-term, consistent returns. The management of banks always endeavors to safeguard their profitability against unforeseen losses. This is because a robust capital position of a bank enhances the efficacy of investment choices payout retained profits, hence fostering heightened future profitability. Hence, the present study aligns with prior research that assessed bank profitability via the use of key performance indicators such as Return on Assets (ROA), Return on Equity (ROE), and Earnings per Share (EPS).

Capital risk refers to the bank's ability to absorb fluctuations in the value of its assets [18, 19]. Furthermore, capital risk refers to the disparities seen between the market values of an asset and its equity obligations. The capital of a bank assumes a crucial function in mitigating potential risks, particularly in cases when the level of protection is inadequate inside banking institutions according to Abdelhay et al. [20]. The primary responsibility of the central bank is to augment the capital in banks to safeguard stakeholders, particularly depositors, by maintaining the desired level of protection ratio [21]. The Basel Committee has placed significant emphasis on capital risk in order to mititoimize its influence on the financial performance of banks. The literature has extensively examined the relationship between capital risk and financial performance, yielding noteworthy findings. Notably, several studies [22–28] have reported a positive impact of capital risk on financial performance. In contrast, prior research findings, such as those presented by Mousa et al. [18], have shown a detrimental effect.

According to Kimondo et al. [29], it is essential to consider the influence of liquidity on financial performance due to its significant role in shaping several aspects of a firm's growth and advancement. The effective management of resources by a business is of utmost importance, as it ensures the maintenance of sufficient liquidity levels to satisfy all financial commitments without incurring any danger of default. However, as shown by Goodhart's [30] research, liquidity risk may be seen as including two primary dimensions. The two key concepts under discussion are maturity transformation, which refers to the alignment of the maturity of a bank's obligations and assets, and integral liquidity of assets, which pertains to the ability of a bank to sell its assets without incurring any value losses, regardless of prevailing market conditions. Nevertheless, it is important for banks not to be too preoccupied with the change of maturity provided they own sufficient liquid assets that may be readily sold without suffering any detrimental financial losses. According to the findings of Ahmed [31], banks that own assets with shorter maturity periods may exhibit less reliance on liquid assets. The scholarly literature has extensively examined the relationship between liquidity risk and financial performance, yielding varying findings. Notably, prior studies conducted by Lake [32], and Ejike and Agha [33] have reported a negative association between liquidity risk and financial performance. In contrast, previous studies conducted by Huong et al. [34] have reported a detrimental effect on financial performance.

According to Sun [35], operational risks may be described as hazards that are linked to a firm's strategy, internal systems and operations, technology, and mismanagement. The Basel Committee defines operational risk as the set of hazards arising from people operations, internal procedures, systems, and external activities. However, the Basel Committee asserts that banks have to establish their specific definition of operational risks based on factors such as their unique characteristics, scale, and business operations. It is recommended that banks should not rely only on a generic definition of operational risks. Nevertheless, the committee contends that a deficiency in comprehending the definition of operational risks, their impact, and the methods for their management is a matter of concern. This is particularly significant given that most banks encounter operational risks across their various activities and transactions. By neglecting to address these risks, the bank may find itself unable to mitigate or exercise control over certain aspects of these risks. Previous studies [24, 36, 37] have shown favorable association between operational risks and financial performance. In contrast, prior studies conducted by Wasiuzzaman and Gunasegavan [38] and Al-Tamimi et al. [39] have shown a discernible inverse correlation between operational risks and financial success. Furthermore, prior research has shown that operational risks do not have a statistically significant effect on financial performance, as demonstrated by Aruwa and Musa [40].

The Market-Power theory posits that the expansion of a firm's scale has a considerably favorable influence on its financial success, as elucidated by Athanasoglou et al. [41]. According to Clarke [42], there is a claim that larger firms tend to be more lucrative and efficient compared to smaller firms, which might be attributed to the associated efficiency hypothesis. According to Abdelhay et al. [43], the potential consequence of corporate expansion is the potential for a separation between ownership and management/control, particularly if the firm's size has increased. The separation of ownership from control inside a firm may be exacerbated by the firm's size, particularly if the size of the firm reaches a certain threshold. According to Fama and French [44], it is observed that above a certain threshold company size, the influence of firm size on the financial performance of the business might become negative. Nevertheless, many prior empirical investigations have shown that the financial performance of enterprises and banks, as quantified by the natural logarithm of total assets, is adversely affected [45–47]. In contrast, other research has shown that the financial success of enterprises is positively influenced by their size [48]. The present investigation is anticipated to provide novel data that may provide support for one of the aforementioned conclusions.

The primary aim of this research is to investigate the impact of several financial risks, including capital risk, liquidity risk, and operational risk, on the financial performance of both commercial and Islamic banks operating within the banking industry of the United Arab Emirates.

Drawing on the aforementioned literature review and the particular aims of the present research, the following hypotheses have been formulated:

Hypothesis 1: The presence of capital risk has a statistically significant negative impact on the financial performance of banks in the United Arab Emirates, as measured by indicators such as return on assets (ROA) and return on equity (ROE).

Hypothesis 2: The presence of liquidity risk has a statistically significant negative impact on the financial performance of banks in the United Arab Emirates, as measured by indicators such as return on assets (ROA) and return on equity (ROE).

Hypothesis 3: The impact of operational risk on the financial performance (measured by ROA and ROE) of banks in the United Arab Emirates is statistically significant and negative.

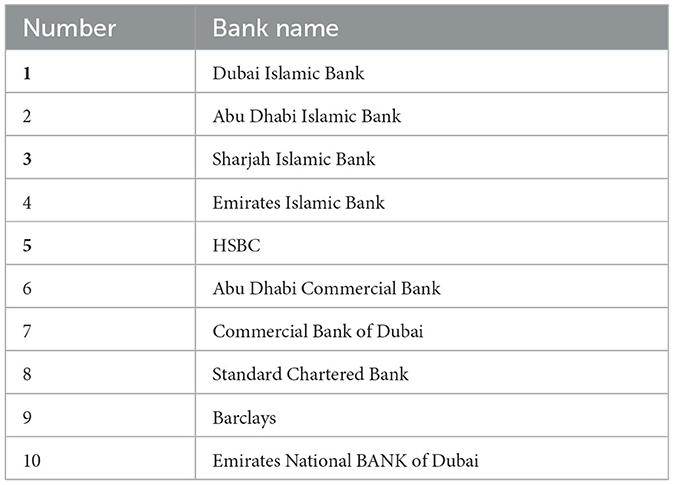

The present study employs a hypothesis test to investigate the influence of specific dependent variables, namely capital risk, liquidity risk, and operational risk, on the financial performance of both conventional and Islamic banks. This examination utilizes return on assets, return on equity, and earnings per share as proxies for the independent variables. The research utilizes secondary data sourced from the annual reports of financial institutions listed in the public exchanges of the United Arab Emirates, covering the time frame from 2015 to 2022. There is a total of 10 banks that are listed in the stock markets of the United Arab Emirates, and this has been the case for the last seven years. With a sample size of 70 observations, as shown in Table 1.

Table 1. Banking listed in UAE stock markets.

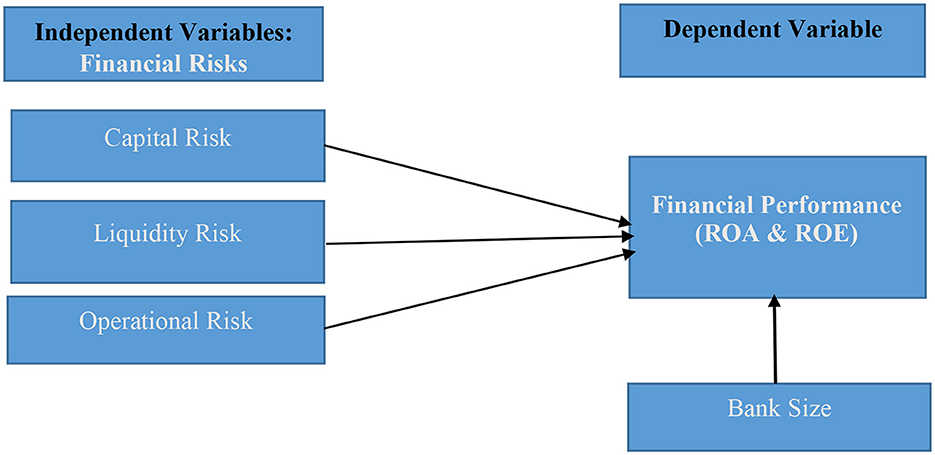

The present study aims to analyze or scrutinize the given subject matter. This study examines the impact of financial risk, namely capital risk, liquidity risk, and operational risk, on the financial performance of banks. Additionally, the study considers bank size as a control variable.

As shown in Figure 1, there is one independent variable with its three factors, such as capital risk, liquidity risk and operational risk, and the study aims to investigate its influence on the dependent variable, which is financial performance with its two factors, which are return of earnings and return of assets. The bank size is the moderator variable in this study to examine the results of the study will vary according to the bank size on not.

Figure 1. Conceptual Framework of the study. Source: Prepared by the researcher 2023.

The present research aims to demonstrate the influence of financial risk on bank performance via the use of a regression analysis model applied to the banking sector companies listed on the stock exchange marketplaces in the United Arab Emirates. The data will be processed with the SPSS program. Moreover, the following equation will be used to assess the correlation between the variables in the present investigation:

Where:

Yit: represents financial performance (Returns on Asset and, Return on Equity).

β0: denotes time-invariant intercept.

β11 CAP: represents capital expense risk exposure.

β21 LIQ: liquidity expense risk exposure.

β31 OPE: denotes operation expense risk exposure.

β41 Siz: is the bank size.

εit = refers to an error term.

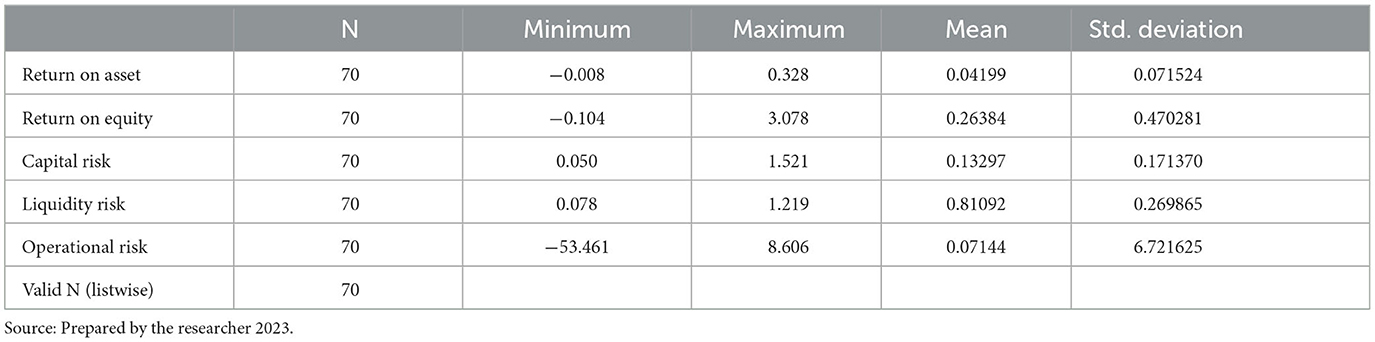

Table 2 presents the descriptive statistics for the variables used in the present analysis, including return on assets (ROA), return on equity (ROE), capital risk, liquidity risk, and operational risk. The average return on assets (ROA) for the selected banks in the sample was 0.04, accompanied by a standard deviation of 0.07. The average return on equity (ROE) was calculated to be 0.26, accompanied wily standard deviation of 0.47. The average capital risk was found to be 0.13, accompanied by a standard deviation of 0.17. Similarly, the average liquidity risk was determined to be 0.81, with a standard deviation of 0.27. In conclusion, the average operational risk was determined to be 0.07, accompanied wily standard deviation of 6.72. The aforementioned descriptive statistics provide a comprehensive portrayal of the variable distribution within the sample. An examination of the data reveals that the range of values observed for the Return on Assets (ROA) metric spans from −0.008 to 0.328. Furthermore, it is noteworthy that the standard deviation associated with these values is rather modest, measuring at 0.07.

Table 2. Descriptive statistics.

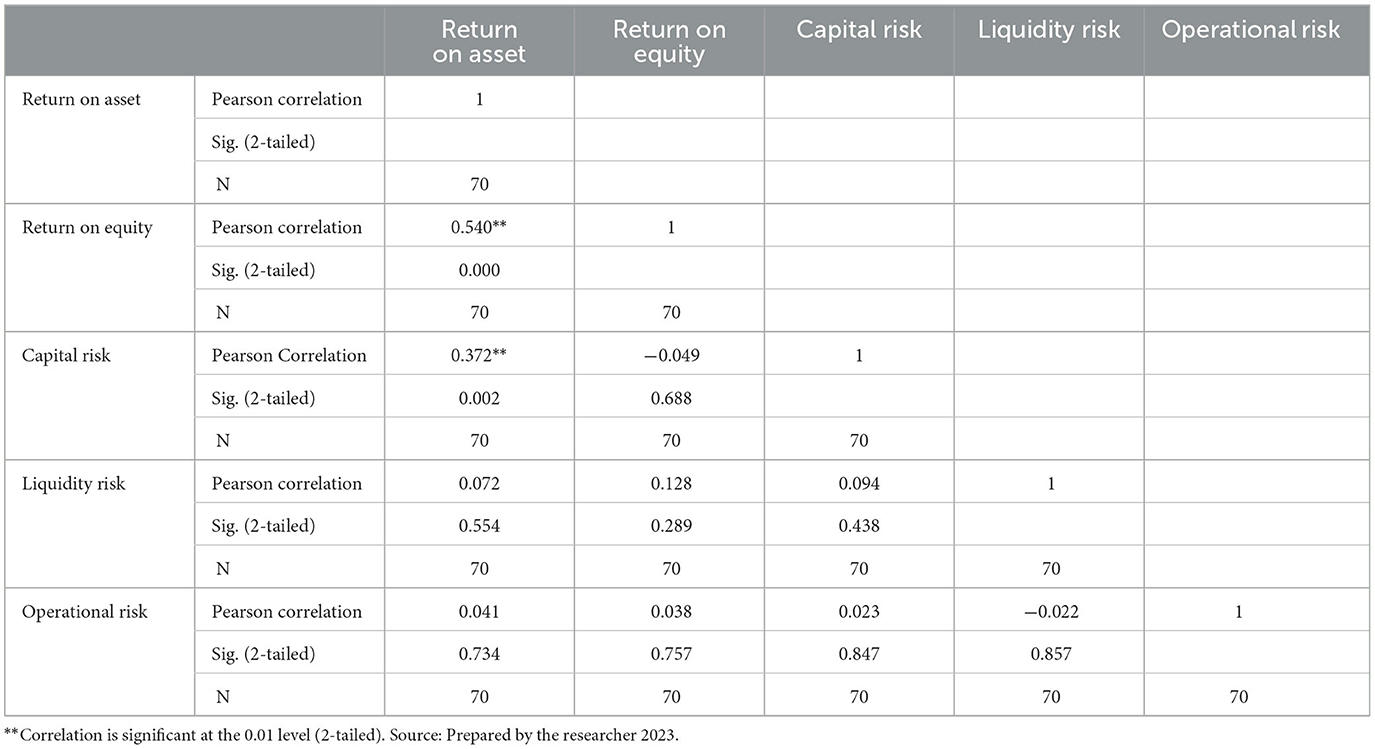

Table 3 presents the Pearson correlation coefficients among the variables. The correlation coefficient between Return on Assets (ROA) and Return on Equity (ROE) demonstrates a statistically significant positive link at the 0.01 level (r = 0.54, p < 0.01), demonstrating a robust association between these two variables. This implies that banks exhibiting a high return on assets (ROA) are also expected to have a correspondingly high return on equity (ROE).

Table 3. Correlations.

The correlation coefficient between return on assets (ROA) and capital risk is positive, although it lacks statistical significance (r = 0.37, p = 0.002). This suggests that there is no substantial association between these two variables. This implies that the influence of capital risk on the return on assets (ROA) of banks in the United Arab Emirates (UAE) may not be substantial.

In a similar vein, the statistical analysis reveals that the connection between the return on assets (ROA) and liquidity risk is not deemed to be statistically significant (r = 0.07, p = 0.554). This finding indicates that there is no substantial association between these two variables. This suggests that the influence of liquidity risk on the return on assets (ROA) of banks in the United Arab Emirates (UAE) may not be substantial.

In conclusion, the statistical analysis reveals that the correlation coefficient between return on assets (ROA) and operational risk is not statistically significant (r = 0.04, p = 0.734). This finding suggests that there is no substantial association between these two variables. This implies that the influence of operational risk on the return on assets (ROA) of banks in the United Arab Emirates (UAE) may not be substantial.

It is essential to acknowledge that the correlation coefficients do not establish causality between the variables; instead, they provide valuable insights into the direction and magnitude of their association.

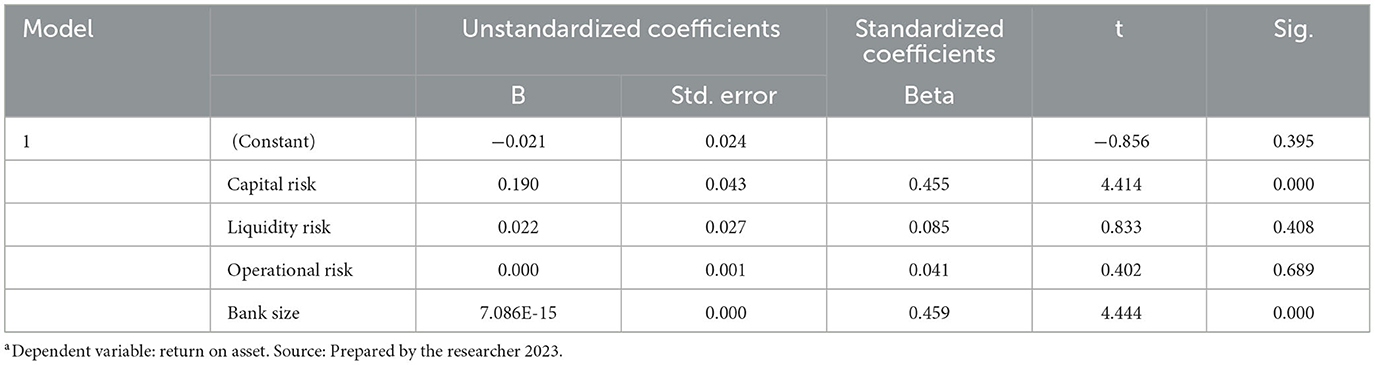

The findings of the multiple regression analysis, using return on assets (ROA) as the dependent variable, are shown in Table 4. The model incorporates four distinct factors that are considered independent: capital risk, liquidity risk, operational risk, and bank size. The findings indicate that of the factors examined, namely capital risk and bank size, only these two exhibit statistical significance in predicting the return on assets (ROA). The association between capital risk and return on assets (ROA) is found to be positive and statistically significant. The beta coefficient for capital risk is estimated to be 0.455, indicating the magnitude of the effect. The p-value associated with this coefficient is 0.000, suggesting a high level of confidence in the observed relationship. This observation suggests that there is a positive relationship between capital risk and return on assets (ROA), indicating that when capital risk grows, ROA tends to increase as well. There exists a positive and statistically significant association between the size of a bank and its return on assets (ROA). The beta coefficient of 0.459 and the p-value of 0.000 provide evidence that bigger banks generally exhibit greater levels of ROA.

Table 4. Coefficients.a

The model summary for the regression analysis with the dependent variable of Return on Assets (ROA) is shown in Table 5. The model's R-squared value is 0.341, suggesting that about 34.1% of the variability in ROA can be accounted for by the independent variables used in the model. The obtained adjusted R-squared value of 0.300 indicates that there is potential for enhancing the model fit by including supplementary variables. The standard error of the estimate, calculated to be 0.059820, is the mean discrepancy between the projected and observed values of return on assets (ROA). In summary, the findings of this study indicate that both capital risk and bank size play significant roles in predicting the return on assets (ROA) within the banking sector. Nevertheless, the model might be enhanced by including other factors.

Table 5. Model summary.

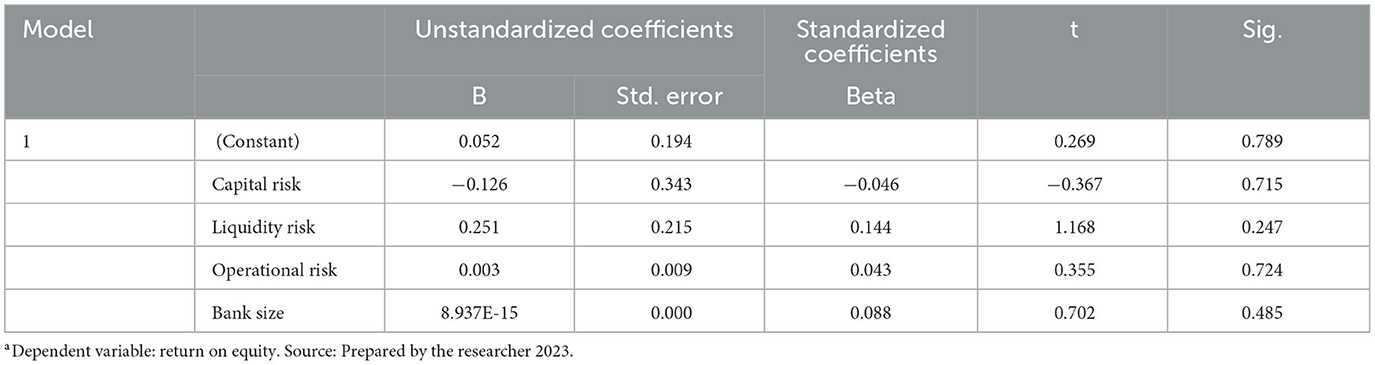

The findings of a regression study examining the variables influencing Return on Equity (ROE) are shown in Table 6. The table displays the coefficients of the independent variables together with their corresponding statistical significance. The model incorporates four distinct independent variables, namely Capital Risk, Liquidity Risk, Operational Risk, and Bank Size. The findings reveal that of the variables examined, only Liquidity Risk has a statistically significant positive impact on Return on Equity (ROE). The beta coefficient for Liquidity Risk is calculated to be 0.144, and the corresponding t-value is 1.168. However, the p-value of 0.247 suggests that this relationship is not statistically significant at the conventional significance level of 0.05.

Table 6. Coefficients.a

The other factors, namely Capital Risk, Operational Risk, and Bank Sie, do not have a statistically significant impact on Return on Equity (ROE). The coefficient for Capital Risk is −0.046 with a corresponding t-value of −0.367, suggesting a little negative influence on Return on Equity (ROE). However, it is important to note that this relationship lacks statistical significance. The coefficient of Operational Risk is 0.043 with a corresponding t-value of 0.355. This suggests a marginal positive effect on Return on Equity (ROE), but, it lacks statistical significance. The coefficient of Bank Size is 0.088 with a t-value of 0.702, suggesting a marginal positive effect on Return on Equity (ROE). However, this relationship lacks statistical significance. In general, the model provides a limited explanation for the variability seen in return on equity (ROE), as shown by an R-squared value of just 0.171. Nevertheless, the model might be enhanced by including other factors.

It is clear in Table 7 that R is 0.171a, R-square is 0.029, Adjusted R-Square is −0.030 and standard error of the Estimate is 0.477363. This suggests a marginal positive effect on Return on Equity (ROE). The obtained adjusted R-squared value of 0.029 indicates that there is potential for enhancing the model fit by including supplementary variables. The standard error of the estimate, calculated to be 0.477363, is the mean discrepancy between the projected and observed values of return on assets (ROA). In summary, the findings of this study indicate that both capital risk and bank size play significant roles in predicting the return on assets (ROA) within the banking sector. Nevertheless, the model might be enhanced by including other factors.

Table 7. Model summary.

The objective of this research was to examine the correlation between several categories of risks, namely capital, liquidity, and operational risks, and the financial performance indicators of return on assets and return on equity. Additionally, the study sought to assess the influence of bank size on this connection. The data was obtained from a sample of 10 banks located in the United Arab Emirates, spanning a duration of 7 years. The examination of the risk and performance of banks in the United Arab Emirates (UAE) for the period spanning from 2015 to 2021 has yielded some significant discoveries. To begin with, it is observed that a positive correlation exists between the size of a bank and its return on equity, indicating that bigger banks tend to create greater returns. Furthermore, it was shown that capital risk had a noteworthy positive influence on return on assets, although liquidity and operational risks did not have any meaningful effect. In addition, the findings from the multiple regression analysis indicate that both capital risk and bank size exhibit substantial predictive power about return on asset. However, the investigation did not find any significant predictive relationship between liquidity risk, operational risk, and bank size with return on equity. The aforementioned results include significant significance for the strategic management of banks operating inside the United Arab Emirates.

Based on the empirical evidence, it is advisable for banks operating in the United Arab Emirates to prioritize the effective management of capital risk as a means to enhance their return on assets. This objective might be attained by enhancing risk management practices, including portfolio diversification, enhancing credit risk evaluation, and enforcing more stringent capital requirements. Moreover, banks should contemplate the expansion of their activities as a means to augment their scale since empirical evidence suggests a positive correlation between scale and returns on equity. Nevertheless, individuals need to possess an understanding of the various hazards that may arise in conjunction with the expansion, including amplified operational and liquidity concerns.

This research makes a valuable contribution to the existing body of knowledge on the risk and performance of banks by offering novel insights into the banking system of the United Arab Emirates. This study contributes to the expanding literature on the effects of risk management practices on bank performance, as well as the correlation between bank size and performance. The outcomes of this research may be used by policymakers and bank executives to formulate policies aimed at enhancing the efficiency and viability of the banking industry in the United Arab Emirates.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Conceptualization and writing-review and editing: MO. Methodology, software, and validations: HH. Formal analysis and writing-original draft preparation: ME-B. Investigation: MA. Writing-review and resources: SA. Curation: AA. Visualization: AA and EA. Supervision: AM.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1. Kassi DF, Rathnayake DN, Louembe PA, Ding N. Market risk and financial performance of non-financial companies listed on the Moroccan stock exchange. Risks. (2019) 7:20. doi: 10.3390/risks7010020

2. Oudat MS, Ali BJ. The underlying effect of risk management on banks' financial performance: an analytical study on commercial and investment banking in Bahrain, In: Ilkogretim Online. (2021) p. 20. Available online at: http://ilkogretim-online.org

3. Akhtar MF, Ali K, Sadaqat S. Factors influencing the profitability of conventional banks in Pakistan. Int Res J Finance Econ. 66:117–24.

4. Hahm JH. Interest rate and exchange rate exposures of banking institutions in pre-crisis Korea. Appl Econ. (2004) 36:1409–19. doi: 10.1080/0003684042000206979

5. Oudat MS. The COVID-19 Pandemic and the Performance of the Stock Exchange Market: Evidence From The Bahrain Stock Exchange Indexes. (2022).

6. Abdelhay S, El-Bannany MAGDI. Intellectual Capital Impact On The Performance Of Banks In Egypt During The Pandemic COVID 19. The Seybold (2022).

7. Matar A, Eneizan B. Determinants of financial performance in the industrial firms: evidence from Jordan. Asian J Agric Extens Econ Sociol. (2018) 22:1–10. doi: 10.9734/AJAEES/2018/37476

8. Musah M, Kong Y. The relationship between liquidity and the financial performance of non-financial firms listed on the Ghana stock exchange (GSE). Int J Adv Res Manage Soc Sci. (2019) 8:1–34.

9. Shamas G, Zainol Z, Zainol Z. The impact of bank's determinants on liquidity risk: Evidence from Islamic banks in Bahrain. J Busin Manage (COES&RJ-JBM). (2018) 6:1–22. doi: 10.25255/jbm.2018.6.1.1.22

10. Panda AK, Nanda S. Working capital financing and corporate profitability of Indian manufacturing firms. Manage Decis. (2018) 56:441–57. doi: 10.1108/MD-07-2017-0698

11. Baldwin CY, Mason SP. The resolution of claims in financial distress the case of Massey Ferguson. J Finan. (1983) 38:505–16. doi: 10.1111/j.1540-6261.1983.tb02258.x

12. Mohamed SM. Employee Performance as affected by the digital Training, the digital Leadership, and subjective wellbeing during COVID-19. J Posit School Psychol. (2022) 6:540–53.

14. Tafri FH, Hamid Z, Meera AKM, Omar MA. The impact of financial risks on profitability of Malaysian commercial banks: 1996-2005. Int J Econ Manage Eng. (2009) 3:1320–34.

15. Dimitropoulos PE, Asteriou D, Koumanakos E. The relevance of earnings and cash flows in a heavily regulated industry: evidence from the Greek banking sector. Adv Account. (2010) 26:290–303. doi: 10.1016/j.adiac.2010.08.005

16. Doliente JS. Determinants of bank net interest margins in Southeast Asia. Appl Financ Econ Letters. (2005) 1:53–7. doi: 10.1080/1744654042000303629

17. Grier WA. Credit analysis of financial institutions. In: Euromoney Books. books.google.com (2007).

18. Mousa M, Judit S, Zeman Z. The impact of credit and capital risk on the banking performance: evidence from Syria. Management. (2018) 32:1.

19. Harban FJMJ, Ali BJ, Oudat MS. The effect of financial risks on the financial performance of banks listed on bahrain bourse: an empirical study. Informat Sci Lett. (2021) 10:71–89. doi: 10.18576/isl/10S105

20. Abdelhay SM, Korany H, Elsawy M. The impact of demographic diversity in egyptian banks on management board performance. J Posit School Psychol. (2022) 6:4397–411.

21. Saunders A, Cornett MM. Financial Markets and Institutions: An introduction to the Risk Management Approach. (2007).

22. Aymen BMM. Impact of capital on financial performance of banks: the case of Tunisia. Banks Bank Syst. (2013) 8:47–54.

23. Ukinamemen AA, Ozekhome HO. Does capital adequacy influence the financial performance of listed banks in Nigeria. Oradea J Busin Econ. (2019) 4:69–80. doi: 10.47535/1991ojbe079

24. Ali BJ, Oudat MS. Financial risk and the financial performance in listed commercial and investment banks in Bahrain bourse. Int J Innovat Creat Change. (2020) 13:160–80.

25. Ismail AO, Mahmood AK, Abdelmaboud A. Factors influencing academic performance of students in blended and traditional domains. Int J Emerg Technol Learn. (2018) 13:170. doi: 10.3991/ijet.v13i02.8031

26. Ahmad S, Wasim S, Irfan S, Gogoi S, Srivastava A, Farheen Z. Qualitative v/s. quantitative research-A summarized review. J Evid Based Med Healthc. (2019) 6, 282832. doi: 10.18410/jebmh/2019/587

27. Agu SA, Nwankwo BE. Influence of religious commitment, intentionality in marriage and forgiveness on marital satisfaction among married couples. IFE Psychol Int. J. (2019) 27:121–33.

28. Cahyaningtyas I, Utama KW, Sukmadewi Y. Judicial bureaucratic reform in the Indonesian Fisheries Court. AACL Bioflux. (2020) 13:1422–7.

29. Kimondo CN, Irungu M, Obanda M. The impact of liquidity on the financial performance of the nonfinancial firms quoted on the Nairobi Securities Exchange. J Account. (2016) 4:1–12.

30. Goodhart C. Liquidity risk management. Banque de France. Financial Stability Rev. (2008) 11:39–44.

31. Ahmed L. The effect of foreign exchange exposure on the financial performance of commercial banks in Kenya. Int J Scientific Res Pub. (2015) 5:115–20.

32. Lake E. Financial risks and profitability of commercial banks in Ethiopia (Doctoral dissertation). Addis Ababa: University Addis Ababa, Ethiopia. (2013).

33. Ejike SI, Agha NC. Impact of operating liquidity on profitability of pharmaceutical firms in Nigeria. Int J Acad Res Account Financ Manag. (2018) 8:73–82. doi: 10.6007/IJARAFMS/v8-i3/4466

34. Huong TTX, Nga TTT, Oanh TTK. Liquidity risk and bank performance in Southeast Asian countries: a dynamic panel approach. Quant Financ Econ. (2021) 5:111–33. doi: 10.3934/QFE.2021006

35. Wang Y, Sun S. Assessing beliefs, attitudes, and behavioral responses toward online advertising in three countries. Int Bus Rev. (2010) 19:333–44. doi: 10.1016/j.ibusrev.2010.01.004

36. Al-Tamimi HAH, Al-Mazrooei FM. Banks' risk management: a comparison study of UAE national and foreign banks. J Risk Finan. (2007) 8:394–409. doi: 10.1108/15265940710777333

37. Oudat MS, Ali BJ. Effect of bad debt, market capitalization, operation cost capital adequacy, cash reserves on financial performance of commercial banks in Bahrain. Int J Psychosocial Rehabilitat. (2020) 24:5979–86.

38. Wasiuzzaman S, Gunasegavan UN. Comparative study of the performance of Islamic and conventional banks: the case of Malaysia. Humanomics. (2013) 29:43–60. doi: 10.1108/08288661311299312

39. Hassan Al-Tamimi HA, Miniaoui H, Elkelish W. Financial risk and Islamic banks' performance in the Gulf Cooperation Council countries. Int J Busin Finance Res. (2015) 9:103–12.

40. Aruwa SA, Musa AO. Risk components and the financial performance of deposit money banks in Nigeria. Inr J Social Sci Entrepreneurs. (2014) 1:514–22.

41. Athanasoglou PP, Brissimis SN, Delis MD. Bank-specific, industry-specific and macroeconomic determinants of bank profitability. J Int Financial Markets, Institut Money. (2008) 18:121–36. doi: 10.1016/j.intfin.2006.07.001

42. Clarke R, Davies S, Waterson M. The profitability-concentration relation: market power or efficiency? J Ind Econ. (1984) 32:435–50. doi: 10.2307/2098228

43. Abdelhay S, Haider S, Abdulrahim H, Marie A. Employees performance as affected by monetary and psychological incentives (the field of study the commercial banks in UAE) a comprehensive review study. J Law Sustain Dev. (2023) 11:e733–e733. doi: 10.55908/sdgs.v11i3.733

44. Fama EF, French KR. Financing decisions: who issues stock? J Financ Econ. (2005) 76:549–82. doi: 10.1016/j.jfineco.2004.10.003

45. Cortese M, Papal S, Pisciottano F, Elgoyhen AB, Hardelin JP, Petit C, et al. Spectrin βV adaptive mutations and changes in subcellular location correlate with emergence of hair cell electromotility in mammalians. Proc Natl Acad Sci USA. (2017) 114:20549. doi: 10.1073/pnas.1618778114

46. Amraoui F, Pain A, Piorkowski G, Vazeille M, Couto-Lima D, de Lamballerie X, et al. Experimental adaptation of the yellow fever virus to the mosquito Aedes albopictus and potential risk of urban epidemics in Brazil, South America. Sci Rep. (2018) 8:14337. doi: 10.1038/s41598-018-32198-4

47. Bayoud NS, Kavanagh M, Slaughter G. An empirical study of the relationship between corporate social responsibility disclosure and organizational performance: evidence from Libya. Int J Manage Market Res. (2012) 5:69–82. doi: 10.5539/ijef.v4n5p37

Keywords: capital risk, return on assets (ROA), return on equity (ROE), financial performance, Islamic banks, conventional banks, liquidity risk, operational risk

Citation: Oudat MS, Ali BJA, Abdelhay S, Hazaimeh HM, Altalay MSR, Marie A and El-Bannany M (2024) The effect of financial risks on the performance of Islamic and commercial banks in UAE. Front. Appl. Math. Stat. 9:1250227. doi: 10.3389/fams.2023.1250227

Received: 29 June 2023; Accepted: 03 November 2023;

Published: 03 January 2024.

Edited by:

Stefan Cristian Gherghina, Bucharest Academy of Economic Studies, RomaniaReviewed by:

Jumadil Saputra, University of Malaysia Terengganu, MalaysiaCopyright © 2024 Oudat, Ali, Abdelhay, Hazaimeh, Altalay, Marie and El-Bannany. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Sameh Abdelhay, ZHJzYW1laC5hQHVhcXUuYWMuYWU=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.