Mithula Umakanth

Mithula Umakanth

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Sustain. , 11 September 2024

Sec. Sustainable Organizations

Volume 5 - 2024 | https://doi.org/10.3389/frsus.2024.1399509

This article is part of the Research Topic Green Finance & Carbon Neutrality: Strategies and Policies for a Sustainable Future View all 36 articles

This study aims to understand the impact of sustainability efforts on materiality or financial performance of insurers by accounting their risk coverage pattern in the Coal Mining Industry. 10 major insurance companies have been selected for this study and the focus has been to understand the stances and policies implemented by these companies between 2018 and 2023. Some of the firms like Hartford have officially declared that they have exited from this industry, while major players are still fueling the coal mining industry. Alternatively, companies themselves are looking to fund their risk mitigation plans so as to not rely on insurance firms. Studies by Hinshaw Law show that losses arising from climate change are rising at an alarming rate, the question then remaians, would insurance companies continue to fund activities that would put their existence in peril. Further research can be conducted on a larger time frame, new policies and frameworks implemented across this industry and to understand the risks of insuring activities that have increased the rate of climate change.

Global warming and climate change are increasingly affecting human life in today’s world. A US consensus shows that 3 in 4 Americans agree that it is human activity leading to this phenomenon (Thompson, 2019). The earliest studies on this phenomenon were done in the 19th century. Scientist Joseph Fourier hypothesized that carbon emissions would lead to global warming, as emitted CO2 remains within the atmosphere due to some gases creating a heat trap (Fleming, 1999). In another article, Foote (1856) was able to find how and what gasses were causing heating and predicted a higher temperature for earth. In 1988, modern work on climate change started garnering attention as NASA scientist Hanses addressed the Congress on discovering evidence that global warming has begun (Shabecoff, 1988).

In recent times many political and economic pacts and treaties have been formulated. However, these pacts have not effectively translated into reduced emissions and/or better synergies for businesses. A report from the National Bureau of Economic Research points out that it is difficult to note the effects of climate change as it is difficult to map the different effects of global warming which makes it difficult to plug into an economic analysis, CO2 emissions are a global phenomenon that have local effects and the consequences of which will only be seen in the distant future (Rossi-Hansberg, 2021). A recent report on global risks states that by 2034 long term potentially irreversible climate change would occur as a result of breaching the threshold and we would see a 3͘ degree world (WEF, Marsh McLennan and Zurich Insurance Group, 2024). Although, the economic impact cannot be accurately computed, businesses and their stakeholders today are exposed to all the effects of the environmental changes.

Practices to mitigate and address these risks have been put to use since years. In as early as 2004, a UN report titled “Who Cares wins” formalized ESG and encouraged its reporting (ABN Amro, Aviva, AXA Group, Banco do Brasil, Bank Sarasin, BNP Paribas, Calvert Group, CNP Assurances, Credit Suisse Group, Deutsche Bank, Goldman Sachs, Henderson Global Investors, HSBC, Innovest, ISIS Asset Management, KLP Insurance, Morgan Stan, 2004). Since then, awareness around sustainable practices have been increasing and businesses have come under a lot of pressure to ensure that they are sustainable, social and generally “good” for the society.

Financial institutions are pressured to invest only in sustainable practices as society believed that these stakeholders could make an impact on sustainable practices of businesses. In 2017, there was massive backlash against American insurance companies for insuring fossil fuel companies. Environmental groups believed that financial institutions underwriting these practices were one of the major reasons that these organizations continued their activities (Bosshard, 2017). Insurers also need to mitigate climate change to ensure that they remain financially relevant in the long run especially since 44% of world carbon emissions come from Coal, naturally insurance companies need to reconsider their exposure to the industry. A report from 2023 shows that AIG, Liberty Mutual, Lloyd’s of London, Swiss Re, and Zurich insure 41% of US Coal Mines (Mary Sweeters, 2023). Many insurers including Aviva and Alliance have limited their coal exposure while AXA promised a total exit from underwriting coal by 2030 (Distinguished, 2021).

There is a dearth of research that explores the area of sustainability practices of insurers and the financial impact on them. Therefore, this research aims to understand the impact of sustainability practice related coal underwriting by insurers and its impact on ESG scores. The study will further explore the impact on the financial performance of the insurers as coal underwriting make up to 1/3rd of the firm’s earnings today.

This research will be useful to insurance industry to understand the impact of sustainability initiative on ESG scores and on the firm’s financial performance. As several insurers stayed away from insuring new coal business which in turn created good corporate image for these insurers; it is important to see if that translated into better financial performance or materiality is impacted or not.

Insurance cycles are an important factor that needs to be considered while understanding the operating decisions that these institutions tend to make (Doherty and Garven, 1993). Underwriting cycles tend to have an impact on the firm’s solvency as they are influenced by market forces (Trufin et al., 2009). As changes in interest rates have a significant impact on the insurer’s capital structure, the ripple effect will be seen on how the insurer would expose themselves to the different risks and the decisions they would partake to ensure a green bottom-line (Taylor, 1991).

With the gradually increasing environmental risks of the world reaching a point of no return and being catastrophic, there would be massive disruption of supply chain, manufacturing technologies and production cycles. Studies on SME activities have showed that uncertain environmental issues will disrupt their growth (Raar, 2015) and sustainable business practices need to be employed at the earliest (Morrad, 2020). The onus on ensuring that the world does not tip over lies with businesses and governments. Analysis by Brogi et al. (2022) reveals that the social and environmental pillars of ESG have a stronger impact on financial performance compared to the governance pillar in general. Additionally, firm-specific characteristics like solvency, profitability, and size are found to be significant determinants of ESG awareness (Bressan, 2023a,b). Incentivizing businesses to reduce their carbon footprint is essential and investors are making mindful decisions based on the disclosures and available ratings for said firms (Jinga, 2021). These decisions also impact the market sentiment towards financial institutions.

Incidentally, it is becoming increasingly important for insurance companies to communicate their stand on sustainability to ensure a positive reputation. Okhrimenko and Manaienko in their research on life insurance companies’ reputations in Ukraine (2019) proved that insurance firms need to strengthen their corporate social responsibility and provide high quality information to have the trust of stakeholders (Okhrimenko, 2019). ESG disclosures have shown a positive impact on a firm’s financial performance. Specifically, the environmental dimension is shown to have a positive relationship with a firm’s stock price and return on capital (Raisa Almeyda, 2019). In a study conducted by Khovrak (2020), 156 insurance companies were compared by the level of ESG risk they pose and their geographical affiliation. The study identified some common guidelines in framing a report and in companies’ approach to ESG components (Khovrak, 2020). However, it is also evident that a companies’ reputation and financial standing and have been impacted by other factors as well including but not limited to new product launches, price wars and marketing strategies. These have made it difficult to understand the impact of their sustainability practices on their financial performance.

Growing ESG concerns pose a looming threat to insurance companies across all operating domains. However, research connecting insurance to ESG values are few. A few studies have tested the relationship between ESG and an insurance firm’s financial indicators. Silvia Bressan in her research on the effects of ESG scores on P&C Insurance companies concludes that ESG scores have a significant impact, and a high ESG insurance firm is said to be financially stronger although exposed to the risks of underwriting (Bressan, 2023a,b). Another study focusing on American insurers between 2006 and 2018, provides evidence of a positive correlation. These studies demonstrate that higher ESG scores are associated with a decrease in financial distress, suggesting that sustainability practices contribute to enhanced financial stability for insurance companies (Chiaramonte et al., 2020).

Sustainable practices in the insurance industry have proven to be better for insurance companies specifically practicing in the life insurance sector. Insurers that adopt a more long-term approach and are conscious of their actions have better social scores, thereby increased trust amongst stakeholders (Chiaramonte et al., 2020). However, the nature and extent of understanding the impact of sustainability practices on a firm’s financial situation is considered to be complex and is debated about by many authors (Agnieszka Herdan, 2020).

A link is observed between sustainability and the purchase of reinsurance (Atz et al., 2023). As suggested in the research conducted by Atz companies with high ESG scores tend to be more profitable and engage in less reinsurance, suggesting they may have applied appropriate risk mitigation strategies leading to potential cost savings. The relationship between environmentally sustainable firms and their profitability is positive (Ki-Hoon Lee, 2016). However, the financial performance of a firm does not have any significant impact on a firm’s sustainability. For example, Berkshire Hathway, Starr and Liberty Mutual are amongst the biggest names in the insurance industry that are still underwriting new coal projects (Insure Our Future, 2022) even though there is significant research stating the enhanced environmental and financial risks of persistent support provided to the fossil fuel industry (El Safty and Siha, 2013).

Through these various research dimensions, we see the complexity of insuring coal businesses. Considering profits in the present or delayed gratification which is not guaranteed is the question that all investors face. We delve deeper into understanding the impact of insurance firms taking a stance on this dilemma mentioned and its effects on the financial performance and reputation of insurance firms.

Insurance companies that are currently operating in the American coal mining industry have been selected for this study. Of these there are few companies that have decided to phase out of underwriting coal projects in the coming years and ones that have no stance on whether they will be phasing out of the industry. Table 1 illustrates the companies chosen for this study.

Table 1. List of insurance companies.

AIG, Chubb, Axis Capital, Zurich, The Hartford, Generali, Swiss Re, Travelers Insurance, and Allianz have issued statements on phasing out of underwriting coal projects. Careful study of the companies transcripts have been conducted (Gunnar Friede, 2015; Axis Capital, 2018, 2019, 2020, 2021, 2022, 2023; Chubb, 2018, 2019, 2020, 2021, 2022, 2023; Generali, 2018, 2019, 2020, 2021, 2022; Old Republic, 2018, 2019, 2020, 2021, 2022; AIG, 2018a,b, 2019a,b, 2020a,b, 2021a,b, 2022a,b, 2023; Allianz, 2018a,b,c, 2019a,b,c, 2020a,b,c, 2021a,b,c, 2022a,b,c; Hartford, 2018a,b, 2019a,b, 2020a,b, 2021a,b, 2022a,b; Swiss Re, 2018a,b, 2019a,b, 2020a,b, 2021a,b, 2022a,b, 2023; Agnieszka Herdan, 2020). However, there are many cases in recent past showcasing some of these companies underwriting major coal projects in the United States (Insure Our Future, 2023). Some big insurance firms that are part of a conglomerate, like Berkshire Hathway have businesses in fossil fuels including coal mining. Due to the complexity of their own structure and vested interests of the group; these companies have not taken a stance on underwriting coal projects (Berkshire Hathaway, 2024).

A comprehensive study of the sustainability practices of the companies in reference to coal underwriting and its impact on the financials of the firm is studied. Variables net written premium, net income, expense ratio, combined ratio, total risk (standard deviation), average returns and volatility of stock prices are considered. A qualitative analysis of the reports and latest ESG scores are analyzed to understand the underlying relationship between all the variables. All the data is collected from the annual reports of the firms and Yahoo Finance.

The net written premium is an indicator of the amount of business a company has done in the past year. It includes the sum of premiums written minus premiums ceded to reinsurance companies, plus any reinsurance assumed. The table shows us the net written premiums for the period between 2018 and 2022.

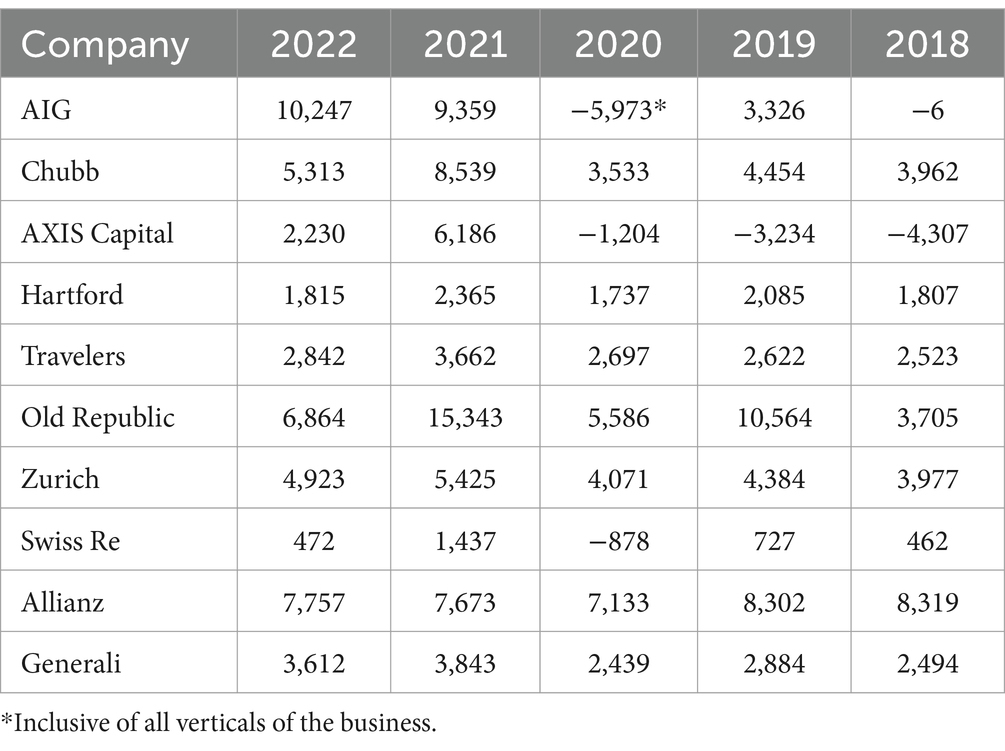

A firm’s net income indicates its true earnings for a given year. It is the amount that is available to shareholders after all expenses have been catered to. The expenses include interest, taxes and deductions. It shows how effectively a firm is able to manage all its expenses (operating and non-operating). The table shows the net income of all the selected companies for this study. We can see that on average that companies are not performing consistently. One of the major reasons for this is the COVID-19 pandemic, which had a huge impact in 2020 as reflected in Tables 2, 3.

Table 2. Net written premium.

Table 3. Net income.

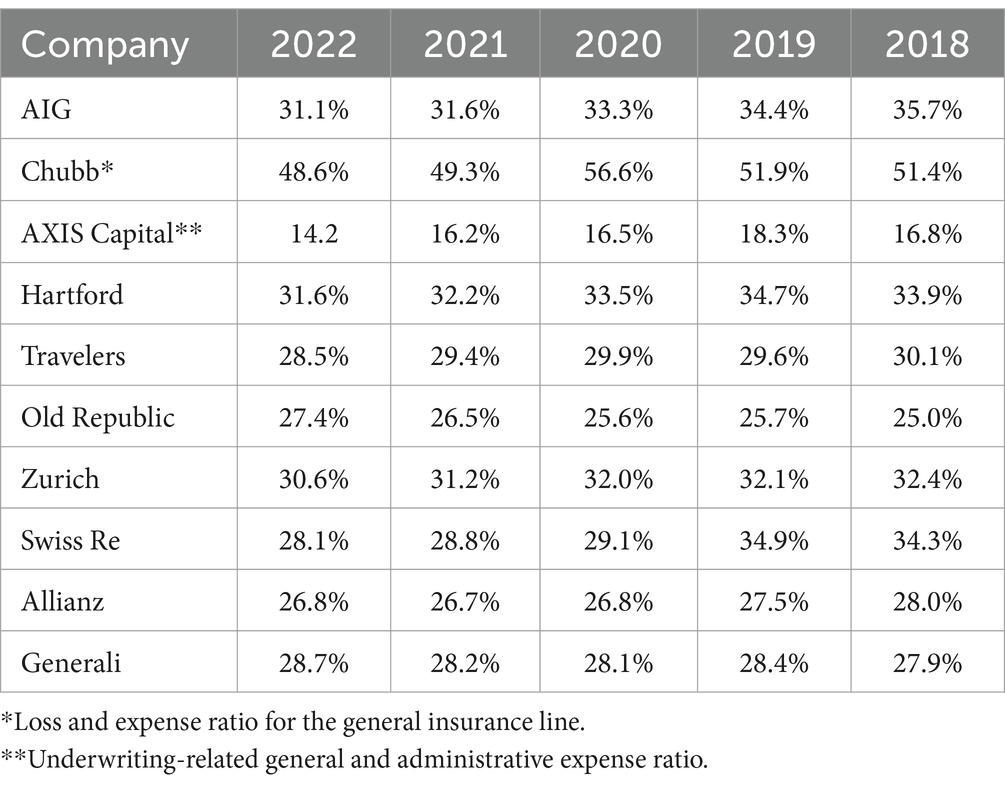

Table 4 showcases the expense ratio which is a percentage of premium used to pay for all the expenses towards acquiring, writing and servicing of insurance and reinsurance. It represents how efficiently a firm manages its operations. Smaller firm like Old Republic and Travelers have had a better control over their expenses in comparison to larger firms. On a trend we can see that all the companies have been reducing their expense ratios since its peak in 2020.

Table 4. Expense ratio.

Combined ratio evaluates the profitability of an insurance firm (Insurance Training Centre, 2024). It can be viewed as, for every unit of premium earned, the firm has lost or paid out “x” units. This is expressed as a percentage and as a general rule it is believe that a percentage between 75 and 90% is considered optimum for an insurance firm. From Table 5, we can see that all the insurance firms have been maintaining a good ratio since 2020.

Table 5. Combined ratio.

The stock prices for the same period have been considered to understand the perspective of the market on these stocks (see Supplementary Annexures). Tables 6–8 represent the annualized average returns, annualized total risk of the stock and volatility. These parameters help us in understanding how much these stocks have varied for the duration considered in the study, thereby how investors see the stock.

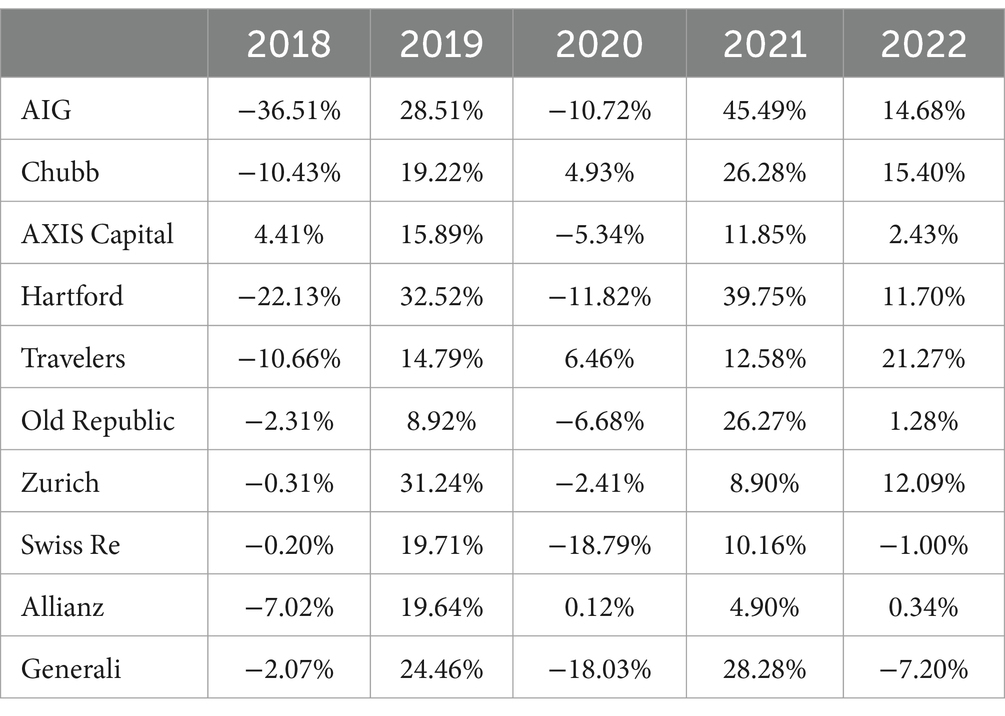

Table 6. Annualized average returns.

Table 7. Annualized total risk.

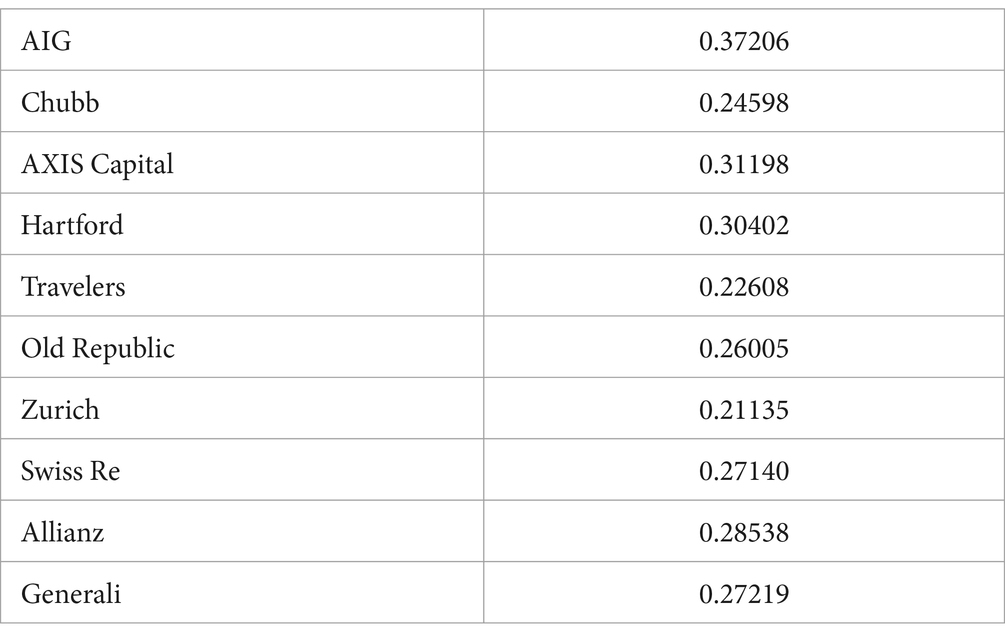

Table 8. Volatility.

The consolidated ESG scores show the overall impact that the firm has with respect to Environment, Social and Governance aspects of a business. They indicate how well the firm has managed to perform on all these parameters. This data is sourced from Sustainalytics. Table 9 shows us the latest ESG scores of all the firms considered for the study.

Table 9. ESG scores sourced from Sustainalytics.com.

Insurance companies may face catastrophic damage in the future due to climate change (Marcacci, 2019). As stakeholders increase their concerns over ESG practices, companies have become more conscious of their marketed solutions. Thereby inexplicably, shifting the risks of sustainable practices on insurers.

Based on the data collected, we understand that there has been no significant impact on the financial performance of the insurers even though they have brought in new policies for phasing out of the coal industry. All the companies listed in this study have policy rules which pertain to them not insuring firms that are making a certain percentage of their revenue from thermal coal and coal projects AIG (2018b, 2019b, 2020b, 2021b, 2022b, 2023), Allianz (2018c, 2019c, 2020c, 2021c, 2022c), Chubb reports (all 5), Genrali reports (all 5), Hartford (2018b, 2019b, 2020b, 2021b, 2022b, 2023), Old Republic reports (all 5), Travelers reports (all 5), Zurich Insurance reports (all 5). However, the commercial confidentiality clause makes it very difficult to identify which firms are actually implementing the policy (Wood, 2022).

Some firms like Hartford have exited all existing insurance relationships and investments in publicly traded securities in companies that exceed coal and tar sands related policy thresholds (Hartford, 2023). However, this has not had any significant impact on its financials nor in the stock market. The total risk of the stock remains high and returns average. AIG, Zurich, Chubb and Swiss Re which are some of the biggest insurers of US coal also do not see any significant negative impact because of these practices. This phenomenon, shows that there are no incentives for businesses to phase out of coal in the immediate timeline.

The combined ratio and expense ratios are in the same range for all the companies- they are profitable regardless of whether they insure coal or not. Expense ratios indicate the firm’s expenses on acquiring a premium, the lower the number the more profitable a company is. This ratio in included in calculating the combined ratio as well, however for this particular study we have taken this (expense ratio) separately to indicate that regardless of the implementation of policies and a global pandemic all these companies have maintained their profitability. The companies also seem to have similar risk profiles and similar combined ratios. Interestingly so these insurance firms even in times of extreme duress across the world have not reported losses, which leads to question if they really implemented policies on phasing out of the industry. It will be impertinent to watch the outputs derived from these actions in the near future.

The stocks of all these companies too illustrate similar volatility. AIG’s stock is more volatile than the rest but a direct connection between insuring coal and this volatility cannot be established. Especially since there are a lot of external factors that play a huge role in determining it. However, it can be inferred that this volatility shows investor and markets do not know how to react to the changing landscape and are eagerly awaiting more information.

On closely examining the sustainability reports of each of the firms, we see a consistent nod towards sustainability practices, but there is little to no mention about coal and related insurance in their recent reports. Out of the 10 firms selected in this study, 9 of them (as mentioned previously) have put restrictions on coal in the period under examination (2018–2020). There has been some impact of these restrictions as insurers are backing away from underwriting new coal projects and coal miners are forced to set aside millions of dollars to cover their risks (Mcfarlane, 2023). This development just shows that money is not moving out of the industry rather is being circulated through different means. It is also important to note that there is still a large amount of insurance coverage for the coal industry and as seen in the data collected, there is no incentive for these companies to phase out completely.

Although, there is no incentive for firms to exit this sector immediately, there is rising concern over the increased risk of calamities. The Geneva Association Task Force in its report has outlined that if climate change is left unmitigated, the negative impacts will significantly increase and severity and frequency of various “perils” (earthquakes, hurricanes, viruses, wildfires etc) will also significantly increase (The Geneva Association Task Force, 2021). This will lead to newer challenges including population shifts - which is already visible in states like Arizona and Florida, where people are shifting for more affordable housing, lesser cost of living and more job opportunities at the risk of their security. Strategically, it is not viable for insurance firms to completely exit this sector for this decade too. They benefit from the increased premiums, predictable risk profile and volatility in the political landscape. Many countries are undergoing elections this year, and increasingly the sentiment is positive towards political parties that are “far right.” Meaning, people would like leaders who are more selfish in the policies that they make for the nation, leaders that are more nationalists than globalists.

There is a growing sense of urgency amongst all stakeholders to address climate change issues. Many believe that the continued support from the financial industry is what is still boosting climate change. While this maybe true, the shift from fossil fuel energy to more modern and ecofriendly energy resources needs to be supported by all stakeholders. Insurance firms need to change priorities and be more agile in adapting to the changing ecological landscape of today’s world.

Companies like AIG, Swiss Re and Zurich are some of the biggest insurers of coal in the US despite net zero promises. Reports by Insure our future show that AIG is the biggest insurer, insuring about 28.1% of coal in the US, Zurich about 4.9% and Swiss Re insurers about 3% of the total output. Mary Sweeters of Insure our future is quoted saying “This damning report perfectly illustrates the problem: insurers are publicly committing to net zero emissions and restrictive fossil fuel policies, yet behind closed doors they continue to underwrite dirty fossil fuel projects, violating their own policies or exploiting loopholes. They are fuelling the climate crisis and profiting from it, while greenwashing their business with empty promises” (Insure Our Future, 2023).

From the research, we understand that there seem to be no impact on the companies’ financials even after they came out with policies on phasing out. The volatility of their stocks were high and there seems to be no significant impact on their ESG scores. (ESG scores include social and governance factors which could be driving the scores as well). Given that there is no immediate benefit that is tangible, insurance firms in their truest nature must be socialists to survive in the world, and for that to sustain and continue, immediate action is required.

However, in the current circumstances and market forces it is clear that insurance firms are not going to completely phase out as there seems to be no financial or reputational incentive to do so. Therefore, the stances taken and the measures adopted may be a way to put society at ease, while the firm continues to maintain its balance sheets. Also given the current research is limited in scope, there may be a few other factors that are influencing profitability to the business, this could be new market opportunities (the rise of climate change has exponentially increased the threat to property, life and casualty), cost cutting, and or changes in the market dynamics. The rise of climate change has invariably increased the risk to traditional business models and thereby to businesses, supply chains and operations continues. It is also predicted that an increased threat to the environment will cause higher losses for insurance firms. Therefore, their continued presence in the fossil fuel sector is counterintuitive to their sustainability. How long could this model continue to work is a question that only time can answer.

Considering that we still do not have a sustainable alternative for fossil fuels, and that there seems to be no immediate change in the climate landscape; at least for the short-term business landscape, this is even more reason for insurers to not move away from insuring coal businesses. Therefore, the evidence we find in this research and the risk profile for the short-term business landscape prove why these businesses are not moving away from this sector just yet.

The original contributions presented in the study are included in the article/Supplementary material, further inquiries can be directed to the corresponding author.

MU: Conceptualization, Data curation, Formal analysis, Investigation, Methodology, Writing – original draft, Writing – review & editing.

The author(s) declare that no financial support was received for the research, authorship, and/or publication of this article.

I would like to thank my guide Prof. Sachin Mohan of Ramaiah Institute of Management for guiding me throughout this project. I would also like to thank late Prof. Varadharajan for his inputs to the research I conducted. I would like to thank Kim Byungwook of University of California, Irvine for sharing his thoughts and ideas to make this a better project.

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/frsus.2024.1399509/full#supplementary-material

ABN Amro, Aviva, AXA Group, Banco do Brasil, Bank Sarasin, BNP Paribas, Calvert Group, CNP Assurances, Credit Suisse Group, Deutsche Bank, Goldman Sachs, Henderson Global Investors, HSBC, Innovest, ISIS Asset Management, KLP Insurance, Morgan Stan. (2004). Who cares wins: the global compact.

Agnieszka Herdan, L. N. (2020). Sustainable business and financial performance. Evidence from the UK. Zeszyty Teoretyczne Rachunkowości 109, 33–42. doi: 10.5604/01.3001.0014.4340

AIG. (2023). AIG earnings call transcripts. Seeking Alpha. Availabe at: https://seekingalpha.com/symbol/AIG/earnings/transcripts

Atz, U., Van Holt, T., Liu, Z., and Bruno, C. (2023). Does sustainability generate better financial performance? Review, meta-analysis, and propositions. J. Sustain. Financ. Invest. 13, 802–825. doi: 10.1080/20430795.2022.2106934

Axis Capital. (2023). Axis Capital Earnings call transcripts. Seeking Alpha. Available at: https://seekingalpha.com/article/4666838-axis-capital-holdings-limited-axs-q4-2023-earnings-call-transcript

Berkshire Hathaway. (2024). Official home page. Berkshire Hathaway. Available at: https://www.berkshirehathaway.com/

Bressan, S. (2023a). Effeccts of ESG scores on P&C insurers. Sustainability (Sustainable Finance and Risk Management). Available at: https://www.mdpi.com/2071-1050/15/16/12644#B6-sustainability-15-12644

Bressan, S. (2023b). Reinsurance and sustainability: evidence from international insurers. J. Appl. Finance Bank, 153–184. doi: 10.47260/jafb/1368

Brogi, M., Cappiello, A., Lagasio, V., and Santoboni, F. (2022). Determinants of insurance companies’ environmental, social, and governance awareness. Corp. Soc. Respon. Environ. Manag. 29, 1357–1369. doi: 10.1002/csr.2274

Chiaramonte, L., Dreassi, A., Paltrinieri, A., and Piserà, S. (2020). Sustainability practices and stability in the insurance industry. Sustain. For. 12. doi: 10.3390/su12145530

Chubb. (2023). Chubb earnings call transcripts. Seeking Alpha. Available at: https://seekingalpha.com/article/4666382-chubb-limited-cb-q4-2023-earnings-call-transcript

Distinguished (2021). Insurers limiting their coal exposure. Market Insights. Available at: https://distinguished.com/insurers-backing-away-from-coal-amid-climate-change/#:~:text=In%20addition%20to%20stepping%20up%20efforts%20to%20raise,their%20Environmental%2C%20Social%2C%20and%20Corporate%20Governance%20%28ESCG2920strategy.

Doherty, N., and Garven, J. (1993). Interest rates, financial structure and insurance cycles. University of Pennsylvania Working Paper: University of Pennsylvania.

El Safty, A., and Siha, M. (2013). Environmental and health impact of coal use for energy production. Egypt. J. Occup. Med., 181–194.

Fleming, J. R. (1999). Joseph Fourier, the ‘greenhouse effect’, and the quest for a universal theory of terrestrial temperatures. Endeavour 23, 72–75. doi: 10.1016/S0160-9327(99)01210-7

Gunnar Friede, T. B. (2015). ESG and financial performance: aggregated evidence from more than 2000 empirical studies. J. Sustain. Fin. Invest. 5.

Hartford,. (2023). The Hartford Coal and Tar Sands Policy. Available at: https://ewcstatic.thehartford.com/thehartford/the_hartford/files/Comm/coal-tar-sands-policy.pdf

Insurance Training Centre. (2024). Underestanding combined ratio. Insurance Training Centre. Available at: https://insurancetrainingcenter.com/resource/understanding-combined-ratio/

Insure Our Future. (2022). The coal insurers of last resort. Solutions for our climate. Available at: https://global.insure-our-future.com/wp-content/uploads/sites/2/2022/05/IOF-KEPCO-Briefing.pdf

Insure Our Future. (2023). Leading European insurers underwrite 30% of U.S. coal despite net zero pledges. Insure Our Future. Available at: https://global.insure-our-future.com/leading-european-insurers-underwrite-30-of-u-s-coal-despite-net-zero-pledges/

Jinga, P. (2021). The increasing importance of environmental, social and governance (ESG) investing in combating climate change. Environ. Manag.

Khovrak, I. (2020). ESG driven approach to companies sustainable development. Insur. Mark. Comp. 11, 42–52. doi: 10.21511/ins.11(1).2020.05

Ki-Hoon Lee, B. C. (2016). Environmental responsibility and firm performance: the application of an environmental, social and governance model. Bus. Strateg. Environ., 40–53.

Marcacci, S. (2019). The Global Insurance Industry's $6 Billion Existential Threat: Coal Power.. Available at: https://www.forbes.com/sites/energyinnovation/2019/05/22/the-global-insurance-industrys-6-billion-existential-threat-coal-power/?sh=7c67d44f63c1Forbes

Mary Sweeters, K. W. (2023). Covering coal: the top insurers of U.S. coal mining. Insure our future. Available at: https://us.insure-our-future.com/wp-content/uploads/sites/3/2023/09/Insurers-of-US-Coal-Report-Final-web.pdf

Mcfarlane, C. D. (2023). Insight: coal miners forced to save for a rainy day by insurance snub : Reuters.

Morrad, D. (2020). SME leaders’ drivers to embrace environmental uncertainty and develop their sustainable business model strategy. Environ. Manag. Available at: https://www.semanticscholar.org/paper/SME-leaders-%E2%80%99-drivers-to-embrace-environmental-and-Morrad/4133f9d0fb75cb5eb0ecd1301cbd5ad6224c1510

Okhrimenko, O. (2019). Forming the life insurance companies reputaion in Ukranian realities. Insur. Mark. Comp. 10, 49–60. doi: 10.21511/ins.10(1).2019.05

Raar, J. (2015). SMEs, environmental management and global warming: a fusion of influencing factors? J. Small Bus. Enterp. Dev., 528–548.

Raisa Almeyda, A. D. (2019). The influence of environmental, social, and governance (ESG) disclosure on firm financial performance. IPTEK J. Proc. Series.

Rossi-Hansberg, K. D. (2021). The economic impact of climate change over time and space. The Reporter Available at: https://www.nber.org/reporter/2021number4/economic-impact-climate-change-over-time-and-space.

Swiss Re. (2023). Earnings call transcripts. Seeking Alpha. Availabe at: https://seekingalpha.com/symbol/SSREF/earnings/transcripts

Taylor, G. (1991). An analysis of underwriting cycles and their effects on insurance solvency. Huebner international series on risk, insurance, and economic security.

The Geneva Association Task Force (2021). Climate change risk assessment for the insurance industry : The Geneva Association Available at: https://www.genevaassociation.org/sites/default/files/research-topics-document-type/pdf_public/climate_risk_web_final_250221.pdf.

Thompson, C. (2019). How 19th century scientists predicted global warming. JStor. Available at: https://daily.jstor.org/how-19th-century-scientists-predicted-global-warming/

Trufin, J., Albrecher, H., and Denuit, M. (2009). Impact of underwriting cycles on the solvency of an insurance company. N. Am. Actuar. J. 13, 385–403. doi: 10.1080/10920277.2009.10597564

WEF, Marsh McLennan and Zurich Insurance Group (2024). The global risks report 2024 : World Economic Forum.

Wood, D. (2022). Leaked information reveals global insurers’ coal power projects. Insurance Business Magazine. Available at: https://www.insurancebusinessmag.com/au/news/environmental/leaked-information-reveals-global-insurers-coal-power-projects-409407.aspx

Keywords: ESG, insurance, sustainability, coal industry, climate change

Citation: Umakanth M (2024) Sustainability materiality of insuring coal businesses for insurers. Front. Sustain. 5:1399509. doi: 10.3389/frsus.2024.1399509

Edited by:

Tian Tang, Florida State University, United StatesReviewed by:

Izabela Jonek-Kowalska, Silesian University of Technology, PolandCopyright © 2024 Umakanth. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Mithula Umakanth, bXVtYWthbnRAdWNpLmVkdQ==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.