Jelle Strikwerda

Jelle Strikwerda Bregje Holleman

Bregje Holleman Hans Hoeken

Hans Hoeken- Department of Languages, Literature and Communication, Utrecht University, Utrecht, Netherlands

Introduction: Pension participants need appropriate support when making (complex) pension decisions. Grounded in Fuzzy-Trace Theory, we argue that suitable decisions require participants to (accurately) understand meaningful differences between decision alternatives. Based on this, we investigated the effectiveness of different types of decision support for the decision when to retire.

Methods: We conducted two experiments among participants of four Dutch pension funds (Study 1: N = 2,328, Study 2: N = 500) on the effectiveness of three different types of decision support: (a) a traditional pros and cons text, (b) a Value Clarification Method (VCM), and (c) testimonials.

Results: The studies showed mixed results. In the first study, we found an activating effect of the VCM and the testimonials: participants who received one of these two types of decision support were more likely to visit a web page with additional information. In the second study, we found no differences between the three types of decision support.

Conclusion: We discuss possible explanations for the effects found, as well as implications for future (research on) pension decision support.

1 Introduction

Pension participants face non-reversible decisions that involve complex intertemporal considerations with uncertain outcomes. One of these decisions is relevant for many older workers in different countries: the decision when to retire. In this study, we focus on this decision in the context of the Dutch pension system. In the Netherlands, participants retire by default at a retirement date set by their pension provider (i.e., a pension fund or insurance company), but they can choose to retire before or after this date. The monthly pension benefit decreases when retiring earlier, and increases when going later. A “wrong” decision (i.e., a decision that does not match participants' interests) can have undesirable consequences, such as a low or even insufficient pension benefit, or, alternatively an unhappy personal life. Therefore, appropriate support in making these decisions is needed and is even required by Dutch law (Pension Act 48a, 2023). This law also states that participants should be encouraged to take relevant action. Then, the question is what kind of decision support activates participants to take action and helps them to make an informed decision that best suits their interests.

1.1 Meaningful decisions

An interesting theory on decision making, is the Fuzzy-Trace Theory (FTT: e.g., Reyna, 2008, 2018; Broniatowski and Reyna, 2018; Reyna et al., 2022). This theory states that an individual represents decision alternatives in different ways. FTT assumes that when people receive specific information about decision alternatives (e.g., about probabilities or amounts related to the alternatives), they store such information in their memory as a verbatim representation and a gist representation. “Verbatim representations capture the exact words, numbers, or images included in the stimulus [e.g., pension information], whereas gist representations capture the essential, bottom-line meaning of the stimulus to the person, including its emotional meaning” (Blalock and Reyna, 2016, p. 781).

According to FTT, people prefer to make decisions based on gist representations. They take into account the consequences of the decision alternatives on the dimension(s) they consider important. Consequences on dimensions that are of little or no importance to them are considered irrelevant and are ignored when extracting the gist representation of the decision. If none of the dimensions become relevant, there is no reason for an individual to choose one of the decision alternatives (i.e., to deviate from the default option). On the dimension(s) that is (are) considered important, people try to boil the alternatives down to a qualitative difference between the decision alternatives.

FTT has mainly been applied to medical decision making and health (see Blalock and Reyna, 2016, for a review). For example, a patient is diagnosed with an illness and has only 2 years left to live, for the largest part in good condition. The patient can choose between (A) no treatment and (B) a clinical trial which will extend life by 2 years, but also with 50% chance of significantly lowering the quality of life for these remaining 4 years. The verbatim representation of this information would include the percentage and the quantitative differences between the two options. The gist representation may depend on what is important to the patient. For example, for some patients being in good health is important as they wish to travel around the world; option A may therefore be more attractive as option B brings the possibility of worsening their condition. Other patients may want to spend as much time as possible with their friends and family, regardless of their condition. To them, option B may be more attractive because it provides the certainty of a longer life. So, even though these patients may have the same verbatim representation of the two options, their gist representations may differ strongly because of what they consider important.

Research in the medical domain has shown positive effects on the quality of decision making when information about the decision provided cues to extract gist-related meaning from the options, in comparison to people who received equivalent, yet more numerical and detailed information. For example, if information enables people to determine qualitative differences between options, they more often make decisions in line with their values (Fraenkel et al., 2012)—“suitable”, in terms of Dutch law. Also, people report more often that they have sufficient knowledge to make the decision (Smith et al., 2015), and make objectively better decisions (in this case: better risk assessment and subsequent decisions) (Wolfe et al., 2015).

According to Strikwerda et al. (2022), decisions within the medical domain are comparable to decisions within the pension domain. In both domains people have to choose between alternatives whose consequences are often uncertain and whose (un)desirability can usually be determined on multiple dimensions (e.g., degree of certainty, financial maximization, standard of living). And in both domains, information about the decision alternatives is usually presented one-dimensionally. In the medical domain, the information provided to help patients make decisions is often numerical, focusing on the exact probabilities of positive and negative consequences of a certain treatment. In the pension domain, the focus is more on communicating exact monetary amounts associated with the decision alternatives (e.g., amount X when retiring at the set retirement date, amount Y when retiring 12 months earlier). As in the medical domain, we expect positive effects on the quality of decision making by providing cues to boil down the decision alternatives on multiple dimensions that may be relevant.

1.2 Relevant dimensions for the decision when to retire

Several studies in different countries have identified factors that determine the decision when to retire. In general, three factors have been uncovered: the need for (more) leisure time (see Beehr and Bennett, 2015; Eismann et al., 2017; Michaud et al., 2020), job satisfaction (see Van den Berg et al., 2010; Beehr and Bennett, 2015; Furunes et al., 2015; Fasbender et al., 2016; Zacher and Rudolph, 2017), and having sufficient income (see Beehr and Bennett, 2015; Van Solinge et al., 2021).

A recent interview study revealed these same dimensions for Dutch pension participants (Strikwerda et al., 2024), as did a qualitative study in Dutch pension practice by Nibud (2022), the Dutch National Institute for Family Finance Information. So, people's gist representations of the decision alternatives for when to retire will depend on people's financial perspective (whether the resulting pension benefit is sufficient for the desired standard of living), their work-life balance (whether there is need for more time for their personal life), and job satisfaction (whether a little or a lot of job satisfaction is experienced).

Cues about these dimensions can be placed on the website of the pension provider. This can be done in a more “traditional” way (i.e., in plain text about the pros and cons of the various alternatives), but also by using certain interventions that might help participants to consider to what extent the relevant dimensions apply to their situation. In the medical domain value clarification methods (VCMs) and testimonials are used. Our research will compare the effectiveness of these three types of interventions.

1.3 Value clarification methods

VCMs are interactive tools to help people determine which dimensions are relevant for a decision and how one's position on those dimensions aligns with the decision alternatives (Fagerlin et al., 2013). This prevents users from forgetting to take relevant dimensions into account when extracting gist representations of the decision alternatives. Several researchers regard VCMs as tools that are in line with FTT (Pieterse et al., 2013; Brust-Renck et al., 2016; Reyna et al., 2022).

Similar to FTT, VCMs have mainly been studied within the medical domain. A diverse array of VCMs are used across a range of health decisions (e.g., surrounding cancer treatments or reproductive health decisions) (Witteman et al., 2016b). Witteman et al. conducted a systematic review to identify design features of medical VCMs. The majority of VCMs in their review helps to identify what dimensions can be relevant to evaluate the desirability of the alternatives and how these dimensions play out for the users. Additionally, some VCMs allow people to infer the implications of relevant dimensions they expressed in relation to the different decision alternatives (e.g., by roughly comparing scores to the pros and cons of an option) or even explicitly show how different decision alternatives align with the expressed dimensions (e.g., by giving a recommended option or presenting scores to show how well or poorly each option fits with the user's responses) (Witteman et al., 2016b).

Witteman et al. (2016a) conducted a systematic review to explore the effects of VCM design features. Most of the studies included in their review focused on a comparison between the standard support provided for the decision (a description of all options and their associated pros and cons) and the standard decision support including a VCM. Although some studies reported positive outcomes of the inclusion of a VCM on decision making, Witteman et al. (2016a) stress that more research is needed, using direct experimental evaluations, to determine effects of different design features of VCMs in order to establish best practices in values clarification.

1.4 Testimonials

Another way to help people give meaning to the decision alternatives is by providing insight into how others have made this decision. For this, testimonials can be used.1 These are narrative examples of experiences of others who had to make the decision (Shaffer et al., 2021). As a result, those who have to make a decision can learn not only what others chose, but also what their considerations were to do so (Butow et al., 2005). People can use these experiences to see if similar considerations apply to their own situation.

Testimonials are also frequently studied in health decision contexts. Shaffer and Zikmund-Fisher (2013) distinguish three types of testimonials. First, process testimonials focus on someone's decision-making process, that is, on how someone made a particular decision and which dimensions were taken into account to do so. An example of such a testimonial is: “I knew I needed to consider my appearance after both surgeries and how that would make me feel and how worried I would be about the cancer coming back” (Shaffer and Zikmund-Fisher, 2013, p. 8). Second, experience testimonials narrate about the experience of a disease or treatment. An example of such a testimonial is: “The surgery part was pretty much what I had expected. I was in some pain when I woke up from the surgery, but the pain medications made it tolerable” (Shaffer and Zikmund-Fisher, 2013, p. 7). Last, outcome testimonials describe the psychological or physical health outcomes associated with a decision (e.g., the consequences of undergoing a particular surgery). An example of such a testimonial is: “I really regret my choice to have a lumpectomy. I am constantly checking for new lumps and worrying about whether the cancer will return” (Shaffer and Zikmund-Fisher, 2013, p. 7).

Shaffer et al. (2021) conducted a literature review on the effectiveness of testimonials. The studies included predominantly focused on a comparison between the standard information on the decision and the same information plus one or more testimonials. Their review shows mixed effects between studies of testimonials on various variables (e.g., on knowledge, attitudes, intentions, behavior, feeling supported, decisional conflict): some studies demonstrate that testimonials are an effective method, other studies report no effects. They also looked specifically at the effectiveness of the three types of testimonials distinguished by Shaffer and Zikmund-Fisher (2013). Although process narratives have been shown to somewhat increase time spent searching for information and experience narratives can increase in some cases confidence in the decision and a greater sense of feeling informed, there is no clear pattern of effects. Shaffer et al. call for future research to study whether certain types of testimonials (i.e., outcome, process, experience) are more appropriate for certain purposes.

Regret seems an emotion that can be used to shape the various types of testimonials. According to Connolly and Zeelenberg (2002), the justifications people use to reduce the experienced regret from decisions made might be used to help people make better decisions. One of the most important justifications to reduce experienced regret is “that one made a careful, competent decision based on a wide range of input information” (Connolly and Zeelenberg, 2002, p. 215). This suggests that pointing out to people that others have not done this when making a decision, encourages them to make a thoughtful decision, “[which] could lead directly to improved decision making” (Connolly and Zeelenberg, 2002, p. 215). Shaffer et al. (2021) describe mixed effects of emotion-laden testimonials, among which regret-based testimonials.

In their conclusion, Shaffer et al. (2021) state that testimonials can have beneficial effects on decision making, but that in general, the evidence does not (yet) support a recommendation for implementation in decision support. They also point at a risk of using testimonials in decision support: people may be ‘pulled' into the direction of a certain decision alternative by the testimonials used (see also Ubel et al., 2001 or Winterbottom et al., 2008). That is, they may choose the same alternative as the person in the testimonial regardless of whether this person's situation and values are similar to theirs. One way to try to counter this is to develop a testimonial (of the same type) for each decision alternative so that information is presented in a balanced way.

1.5 Research questions

As argued before, insights from the medical domain regarding decision support can also be applied to the pension domain (Strikwerda et al., 2022). VCMs may have positive effects when assisting participants in sorting out their situation and what matters to them—such as, in the case of the decision when to retire, regarding the work-life balance and job satisfaction. Testimonials can also be used to help participants consider their work-life balance and job satisfaction. In a qualitative study on deciding when to retire, Nibud (2022, p. 24) argues that “stories from others and insight into what considerations they had and what values they considered important, help people with this [decision]”.

In this paper, we discuss two studies on the effectiveness of different types of decision support for the decision when to retire. We designed three types of decision support: (a) a traditional text with pros and cons of retiring earlier or later—comparable to standard information used in current practice, (b) a VCM that helps participants to get an impression of their work-life balance and of their job satisfaction, and (c) two testimonials that describe how other participants gave meaning to the decision alternatives and how they (partly) regretted their decision.

In the two studies, we compare the three types on their effectiveness as decision support. With effective decision support, we mean, in line with Dutch law (Pension Act 48a, 2023), decision support that activates participants to take relevant action (for example, to log in to their pension planner) and that helps them to make an informed and suitable decision (in this case, for participants facing the decision in the coming years: making them feel better prepared to make the decision). Therefore, the following questions are central to the two studies:

1) To what extent do the types of decision support activate participants to take a relevant follow-up action?

2) To what extent do the types of decision support contribute to the feeling of preparation of participants for making the decision when to retire?

In addition, it is also important that participants are satisfied with the decision support. Lourenço et al. (2020) show that satisfaction with a pension tool has a positive effect on the acceptance of advice generated by the tool. This emphasizes the importance of designing attractive and user-friendly decision support. The Dutch Federation of Pension Funds also states that, in addition to enabling participants to make a suitable decision, decision support can also aim to let the participant experience ease and simplicity. Therefore, we also focus on the following question in the two studies:

3) To what extent are the types of decision support appreciated by the participants?

2 Study 1

2.1 Materials

Besides the type-specific characteristics, discussed below, all three decision support interventions contained information about the relevance of work-life balance and job satisfaction (see Appendix A). Furthermore, each intervention mentioned the need to figure out the financial consequences of retiring earlier or later.

2.1.1 Text with pros and cons

The text with pros and cons of different retirement dates was based on standard materials pension providers use to inform their participants about the decision alternatives. The text also paid attention to the relevance of work-life balance and job satisfaction for the decision when to retire, mentioning the information from Appendix A. The text with pros and cons can be found in Appendix A.1.

2.1.2 Value clarification method

The VCM was an interactive tool that gave participants insight in and stimulated them to consider their current work-life balance and job satisfaction. For this, we incorporated two Dutch standardized and validated questionnaires in the VCM: the SWING (Survey Work-home Interaction—Nijmegen) and the UWES (Utrecht Work Engagement Scale).

The SWING is an instrument to measure the work-life balance (Geurts et al., 2005). We used nine items of the SWING on the negative influence of work on personal life, such as “How often does your work require time that you would rather spend with your partner/family/friends?” (see Appendix A.2 for a more detailed description of the questionnaire). The items constituted a reliable scale (Cronbach's α = 0.87).

The UWES is a validated instrument to measure the work engagement—we use the term “job satisfaction”—of individuals (Schaufeli and Bakker, 2004). We used a shortened version of the UWES, consisting of nine items, such as “I am enthusiastic about my job” (see Appendix A.2 for a more detailed description of the questionnaire). The scale was reliable (Cronbach's α = 0.95).

After completing both questionnaires, participants received information about the relevance of work-life balance and job satisfaction for the decision when to retire, mentioned in Appendix A. Furthermore, they received feedback on the two filled-out questionnaires, in the form of their median scores. For example, a participant with a median score of “Sometimes” on the SWING and “A few times a month” on the UWES received the following feedback: “Based on your answers to the questions on your work-life balance, your work sometimes hinders your personal life” and “Based on your answers to the statements on your job satisfaction, you experience (a lot of) satisfaction in your work a few times a month”. By displaying a summary of the participant's responses, the VCM helps participants to determine which dimensions are relevant to take into account and, in combination with the information about the relevance of work-life balance and job satisfaction for the decision, also allows them to infer by themselves how well or poorly the relevant dimensions they expressed align with the decision alternatives. The VCM can be found in Appendix A.2.

2.1.3 Testimonials

In the two testimonials, participants read how two fictitious participants diverged from the default date (one retiring early, the other retiring late), what their considerations were to do so, and how they (partly) regretted their decision afterwards (see Appendix A.3 for a more detailed description of the design of the testimonials).

We designed the testimonials in such a way that the participant regretted not having taken a certain dimension into account when making the decision. The participant who retired earlier regretted not taking job satisfaction sufficiently into account, but was satisfied with the current work-life balance. The participant who retired later regretted the work-life balance during continuing to work, but enjoyed the satisfaction work provided. Both mentioned the financial consequences about their decision, in a neutral manner. We highlighted two decision alternatives, aiming to present the information in a balanced way to counter a possible steering effect.2 We chose to highlight only the decision alternatives deviating from the default decision in the testimonials. By adding the partial regret, participants also gained insight into other considerations that could have been taken into account and might have led to choosing the default date.

After reading the testimonials, participants received information about the relevance of work-life balance and job satisfaction for the decision when to retire, mentioned in Appendix A. The testimonials can be found in Appendix A.3.

2.2 Questionnaire

Participants in the three conditions received the same questionnaire to measure effects of the decision support interventions (see Appendix B for a more detailed description of the questionnaire). We measured the extent to which a participant felt prepared for decision making due to the decision support with an adapted version of the Preparation for Decision Making Scale (Bennett et al., 2010), consisting of six items, such as “This information has helped me think about the pros and cons of the different moments to retire”. The items constituted a reliable scale (Cronbach's α = 0.93).

To measure the appreciation and comprehensibility of the provided decision support, we formulated items based on items proposed by Maes et al. (1996, p. 208–209). For appreciation, we asked the participants what they thought of the provided decision support, with four items, such as “Uninteresting—Interesting”. The items constituted a reliable scale (Cronbach's α = 0.84). For comprehensibility, we also asked the participants what they thought of the provided decision support, with four items, such as “Cumbersome—Concise”. Again, the resulting scale was reliable (Cronbach's α = 0.91).

A well-considered decision for a retirement date requires participants to also know what the financial consequences are of those decision alternatives. To measure whether participants were activated to look for this information, we included an intention item and a behavioral measure.

As our research concerns decision support, we must also assess the behavioral intention for the decision when to retire, although we have no further expectations about this. The behavioral intention was measured with the item “Imagine that you had to make a decision now and that it is financially possible to retire earlier. What would you prefer?”.

The questionnaire also included control items. At the beginning of the questionnaire, we collected data from participants with one item on pension orientation and three items on self-efficacy regarding financial matters (constituting a reliable scale, Cronbach's α = 0.82). At the end of the questionnaire, we collected data from participants on age, gender, and highest level of education (see Appendix C). The questionnaire of this study also included various items that serve to answer another research question, which will be reported in a separate study. In the current study, we only use these items to determine the effect of the interventions as purely as possible, by controlling in the statistical analysis for the variables to which these items relate.

2.3 Pretest

Previous versions of the materials and questionnaire were critically evaluated by communication specialists of two Dutch pension funds and, where necessary, rewritten to safeguard the comprehensibility for a large and heterogeneous audience. The subsequent version of the study was pre-tested by four people from the target group (participants of one of the two pension funds) using the think-aloud protocol, via Microsoft Teams. In this method, participants perform a task—in this case, going through the survey, just as the actual participants do—while verbalizing their thoughts aloud (see Elling et al., 2012). The think-aloud protocol was followed by a short interview to discuss the participants' experience. The participants received a gift voucher worth 10 euros for their participation.

As a result of the pretest, some changes were made. These were mainly to clarify parts of both the material and the questionnaire. This resulted in the final design of the materials and questionnaire discussed above.

2.4 Procedure

Once ethical approval was obtained from the Faculty Ethics Assessment Committee Humanities of the Utrecht University (reference number: 22-136-01), two Dutch pension funds sent an invitation to participate in the study to their participants. The invitation email contained a link to the online survey, which was provided by an external research agency. Data were collected between October 6 and October 20, 2022.

The online survey started with an introduction in which the study was explained, as well as the possibility to win a gift voucher, the way the data were going to be handled, the rights of the participant, and the contact details of the researchers. This was followed by some of the items that serve to answer another research question (see Appendix B). Subsequently, the participants were randomly assigned to one of three conditions (the pros and cons text, the VCM, or the two testimonials). Within the testimonial condition, the order of the testimonials was also randomized—for some of the participants testimonial A was at the top, followed by B, for the other part it was the other way around—to control for a primacy or recency effect.3

After going through the decision support, the participants received the rest of the items from the questionnaire (see section “Questionnaire” above). Next, there was the opportunity for comments, the participant was thanked for participation and participants could leave their email address to participate in the raffle of one of 20 gift vouchers worth 25 euros. The survey ended with the behavioral measure (see section “Questionnaire” above).4 Participation in the entire study took an average of 10 min.

2.5 Participants

The primary target group for the decision support consists of workers who are approaching their retirement. Five to ten years before their set retirement date, participants appear to be the most concerned with their pension and search for pension information (Van Dalen and Henkens, 2022). Therefore, our target group consisted of actively pension-accruing participants—i.e., participants who were working at the time, aged 55 years or older, and for whom an email address was available. An invitation to participate in the survey for this study was sent out to a total of 40,334 participants of two Dutch pension funds who met these criteria. Of them, 2,328 participants completed the survey (5.8% response rate) (see Appendix C.1 for the demographic characteristics of the participants).5

We checked for differences between the three conditions on all control items. The three conditions did not differ.6

2.6 Results7

2.6.1 Preparation and appreciation

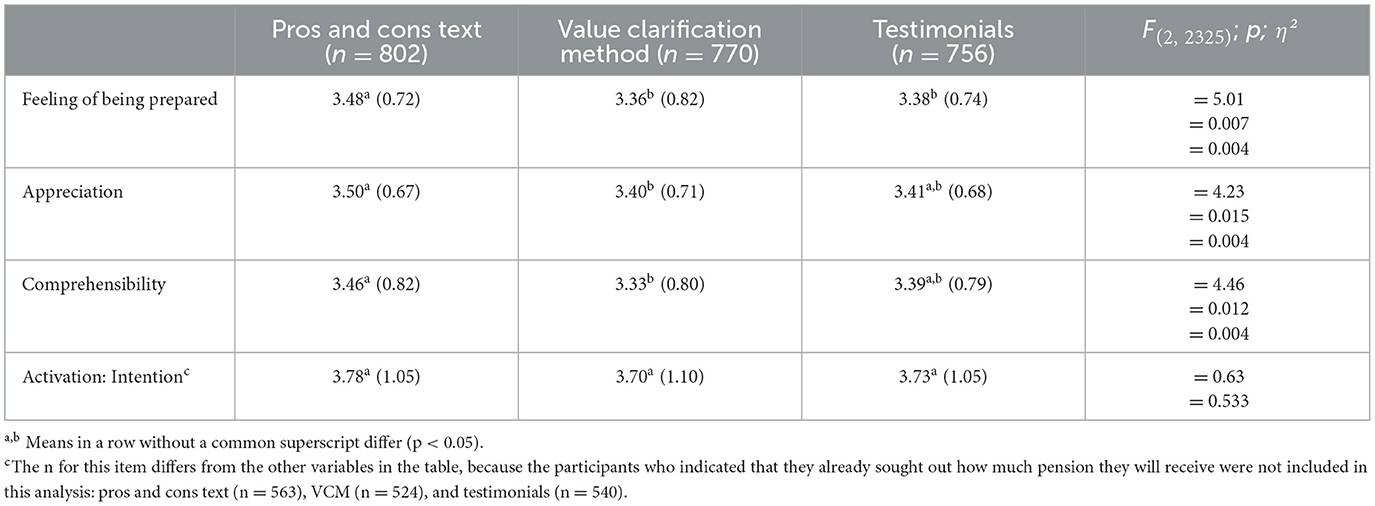

There was a significant difference between the conditions in the extent to which participants feel prepared to make the decision after using the decision support [F(2, 2325) = 5.01; p =0.007; η2 =0.004] (see Table 1). The post hoc Bonferroni test showed that participants who were shown the pros and cons text (M = 3.48, SD = 0.72) felt better prepared than the participants who received the VCM (M = 3.36, SD = 0.82) (p = 0.009) or the testimonials (M = 3.39, SD = 0.74) (p = 0.049).

Table 1. Participants' feeling of being prepared, appreciation of the provided decision support, and intention to explore the financial consequences, for each condition (1 = low, 5 = high).

There also was a significant difference in the average appreciation of the provided decision support between the three conditions [F(2, 2325) = 4.23; p =0.015; η2 =0.004] (see Table 1). The post hoc Bonferroni test showed that participants appreciated the pros and cons text (M = 3.50, SD = 0.67) more than the VCM (M = 3.40, SD = 0.71) (p =0.024).

Finally, there was a significant difference in the average comprehensibility of the provided decision support between the three conditions [F(2, 2325) = 4.46; p =0.012; η2 =0.004] (see Table 1). The post hoc Bonferroni test showed that participants found the pros and cons text (M = 3.46, SD = 0.82) more comprehensible than the VCM (M = 3.33, SD = 0.80) (p = 0.009).

Yet despite these comparisons being significant, the effect size was negligible and therefore practically irrelevant.

2.6.2 Activation

The participants in the three conditions did not differ significantly in the extent to which they intend to sometime soon seek out how much pension they will receive [F(2, 1624) =0.63, p =0.533] (see Table 1).

Subsequently, we assessed whether the next step of participants depended on the type of decision support: (i) visit the pension planner of the pension fund, (ii) visit a web page of the pension fund with additional information about the decision, or (iii) end the survey (see Appendix D.1 for the preferred next step of the participants).

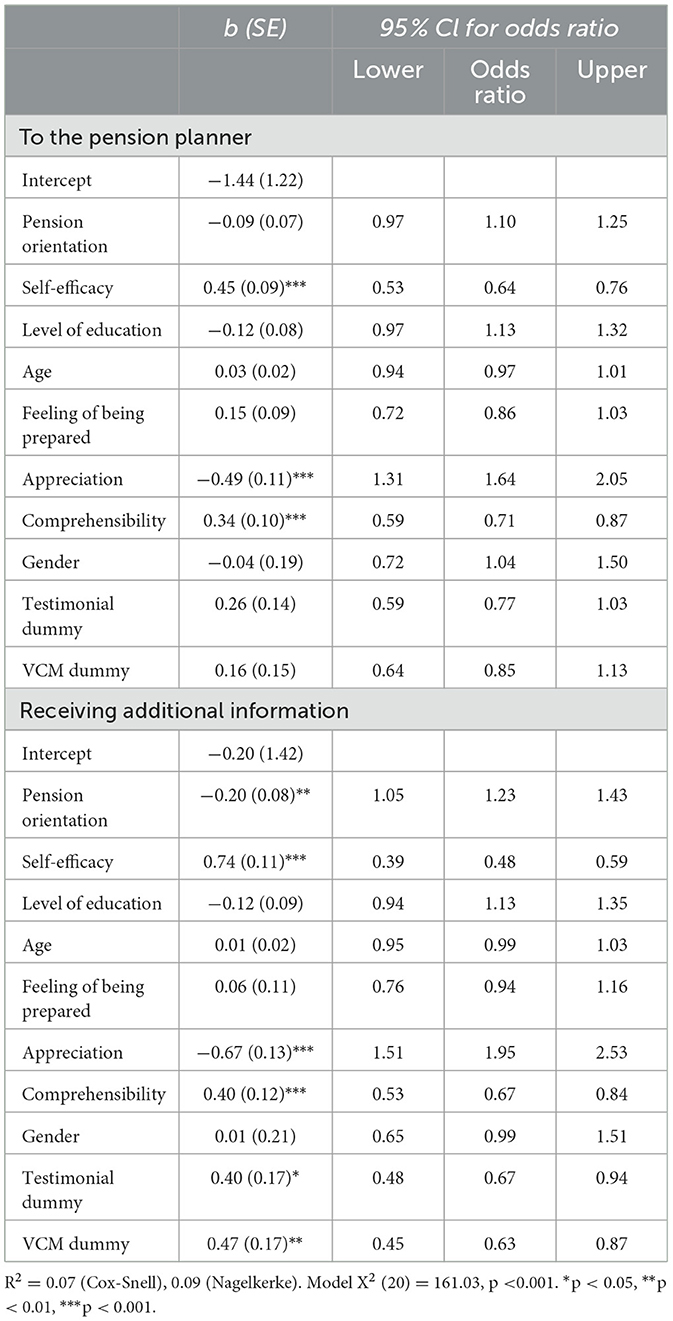

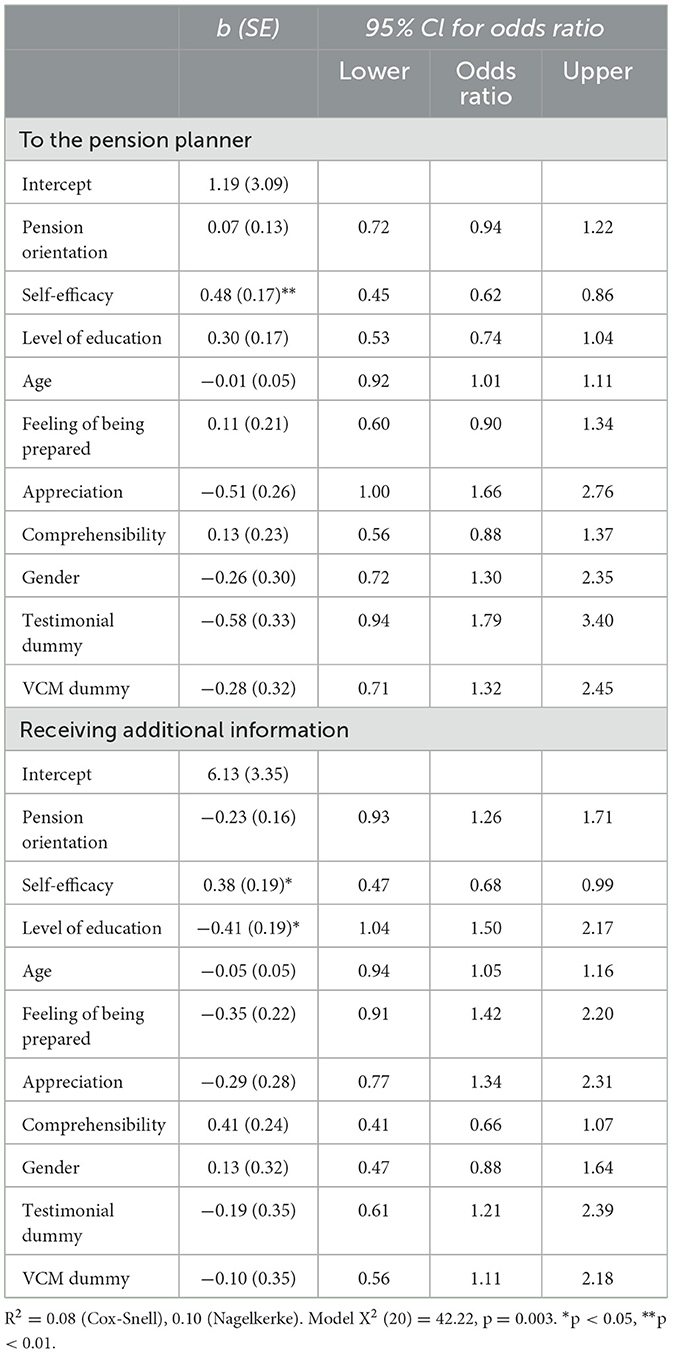

We analyzed these data through a multinomial logistic regression. This way, we could also control for the extent to which participants felt prepared to make the decision, for the intervention's appreciation and comprehensibility, and for several other participant characteristics we measured as control variables, such as self-efficacy regarding financial matters and level of education. We created two dummy variables, for the testimonials and the VCM. The multinomial logistic regression showed that the model is significant, with several significant predictors (see Table 2). Self-efficacy regarding financial matters was a significant predictor of both visiting the pension planner and visiting a web page with additional information. This means that participants who felt more able to deal with financial matters, were more likely to visit the pension planner and a web page with additional information. The same applies to appreciation and comprehensibility: those who considered the decision support more comprehensible, were more likely to visit the pension planner and a web page with additional information. However, those who appreciated the decision support more, were less activated: they were less likely to visit the pension planner or go to a web page with additional information. Furthermore, pension orientation was a significant predictor of visiting a web page with additional information: those who had oriented themselves more on the pension decision, were less likely to visit a web page with additional information. Finally, the testimonials dummy and the VCM dummy were significant predictors of visiting a web page with additional information about the decision. This means that participants who received the testimonials or the VCM were more likely to visit a web page with additional information as next step.8

Table 2. Results multinomial logistic regression (Study 1).

Finally, an unexpected result was that the three conditions differed significantly in the number of participants who dropped out during the intervention [χ2(2) = 42.19, p < 0.001; Cramer's V = 0.121]. With the pros and cons text, significantly fewer people (n = 26) dropped out than expected (p < 0.001). With the VCM, significantly more people (n = 90) dropped out than expected (p < 0.001).

2.6.3 Intention for the decision when to retire

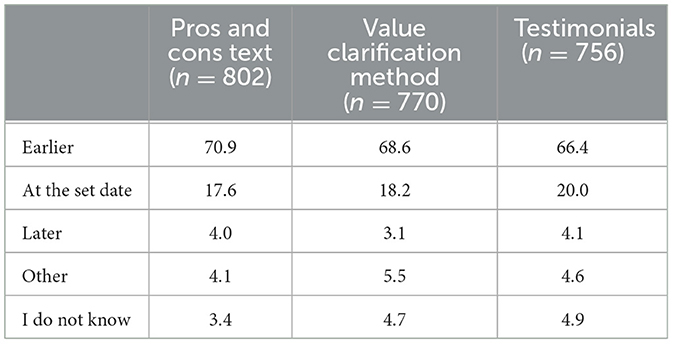

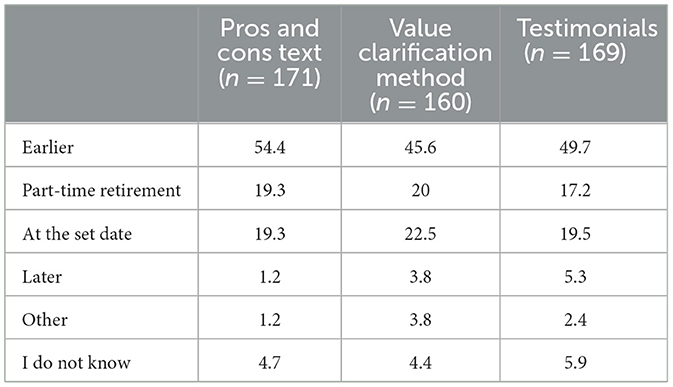

The participants in the three conditions did not differ significantly (χ2 (8) = 7.67, p =0.466) with respect to the decision alternative they would currently prefer, assuming that it is financially possible to retire earlier (see Table 3). The types of decision support did not lead to different decisions.

Table 3. Intention for the decision when to retire, for each condition (in %).

2.7 Conclusion and discussion

The results of Study 1 show that the VCM and the testimonials lead to a lower feeling of being prepared for the decision when to retire than the pros and cons text. Also, the VCM is appreciated less than the pros and cons text and scores lower on comprehensibility. However, these differences are hardly relevant in practice because the effect sizes are very small. On the other hand, the VCM and the testimonials show an activating effect: participants who receive one of these two types of decision support are more likely to visit a web page with additional information about the decision when to retire. This effect is present even after controlling for the extent to which participants felt (less) prepared to make the decision and the intervention's (lower) appreciation and comprehensibility.

The VCM was appreciated less than the pros and cons text, and led to more participants dropping out. This might be explained by the fact that the VCM is a new type of decision support for pension participants, while the pros and cons text is comparable to texts used in current practice. A second possible explanation lies in the feedback participants received in the VCM, that might not been informative enough. Participants received feedback on the filled-out questionnaires on work-life balance and job satisfaction in the form of their median scores. We would have preferred to give feedback on how they scored compared to a benchmark, for example, ‘only 30 out of 100 people have a worse work-life balance than you'.9 We believe, this provides participants with a more meaningful interpretation of their scores on the work-life balance and job satisfaction questionnaires.

The activating effect that we observed from the VCM and the testimonials and the possible explanations for the other results found, provide good reasons to optimize the decision support and further investigate the effects of these types of pension decision support. Therefore, we conducted a second study.

3 Study 2

In the second study, we made some adjustments to the materials and the questionnaire to investigate whether the VCM and the testimonials would be appreciated more and made participants feel better prepared for decision making, while keeping the positive effects on activation. Below, we describe the main adjustments we made for the second study.

3.1 Adjustments

3.1.1 Explicit introduction as “decision support”

We now introduced all three types of decision support more explicitly as information that can help participants make the decision when to retire, because the VCM and the testimonials can be considered a new type of decision support that participants may not always recognize as such. We also explicated this in the questionnaire by introducing the items regarding decision support (i.e., preparation for decision making, appreciation and comprehensibility of the decision support) with respectively: (a) You have just received information about the pros and cons of retiring earlier or later, (b) You have just received information about the extent to which your work hinders your personal life and how much you enjoy your work. That information may be important in weighing the pros and cons of retiring earlier or later, and (c) You have just received information about how other people have considered the pros and cons of retiring earlier or later, followed by “We will now ask you a number of questions about how you experienced that information”.

3.1.2 Benchmark feedback VCM

As in the first study, participants in the VCM condition received feedback on their work-life balance scores and job satisfaction scores. In this second study, we used the scores obtained from the first study as a benchmark. We did this as follows:

“You have answered questions on your work-life balance. Your answers give an impression of the extent to which your work hinders your personal life.

Out of 100 people aged 55 years and older, 20 indicate that their work hinders their personal life less often than you and 71 indicate that their work hinders their personal life more often.”

And:

“You have answered questions on your job satisfaction. Your answers give an impression of the extent to which you enjoy your work.

Out of 100 people aged 55 years and older, 21 indicate that they experience more job satisfaction than you and 73 experience less job satisfaction.”

3.1.3 Other adjustments

In addition to the main adjustments described above, several other modifications were made based on advancing insights from the first study.

First, as we did not provide feedback in the VCM in the form of a median score, we did no longer needed an uneven number of items in the questionnaires (see Appendix A.2). Therefore, we used the original eight SWING items (and the nine UWES items). The reliability of both scales remained good (Cronbach's α = 0.85 and Cronbach's α = 0.94, respectively).

Second, we included a filter question at the beginning of the questionnaire in which we asked the participants whether they had already finalized the decision when to retire, because in that case, the decision support is no longer relevant to them. Participants who agreed to this question, were excluded from the study (see Note 10).

Third, we added the answer option “Retire part-time (continue to work partly and retire partly)” in the questionnaire to the item about the intention for the decision when to retire, assuming it is financially possible to retire earlier. This was suggested by several participants in the open comments in the first study, and part-time retirement also appears an interesting option in the broader Dutch context: two-thirds of employees and three-quarters of employers are positive about part-time retirement, even though it is still not commonly used (Van Solinge et al., 2020).

Finally, we shortened the questionnaire used in Study 1 by removing the items that serve to answer the other research question. This means that, in the same way as in the first study, participants received a questionnaire with the following items: one control item on pension orientation and three control items on self-efficacy regarding financial matters (Cronbach's α = 0.88) before the decision support, the intention item for activation, intention for the decision when to retire, six items on preparation for decision making (Cronbach's α = 0.93), four items on appreciation (Cronbach's α = 0.93), four items on comprehensibility (Cronbach's α = 0.89), control items on demographic characteristics (age, gender, education level), opportunity for open comments, opportunity to leave e-mail to participate in raffle of one of 15 gift vouchers worth 25 euros, and the behavioral measure after the decision support.

Other parts of the materials and the questionnaire remained unchanged.

3.2 Participants and procedure

Once ethical approval was obtained from the Faculty Ethics Assessment Committee Humanities of the Utrecht University (reference number: 23-078-02), two pension funds—different from those in the first study—sent an invitation to participate in the study to their actively pension-accruing participants aged 55 years or older and for whom an email address was available (same criteria as in the first study). A reminder to participate in the study was sent out 3 weeks after the initial invitation. Data were collected between June 23 and July 31, 2023.

A total of 6,486 participants were invited. Of them, 500 participants completed the survey (7,7% response rate) (see Appendix C.2 for the demographic characteristics of the participants).10 Participation in the entire study took an average of 8 min.

We checked for differences between the three conditions on all control items. The three conditions did not differ.11

3.3 Results

3.3.1 Preparation and appreciation

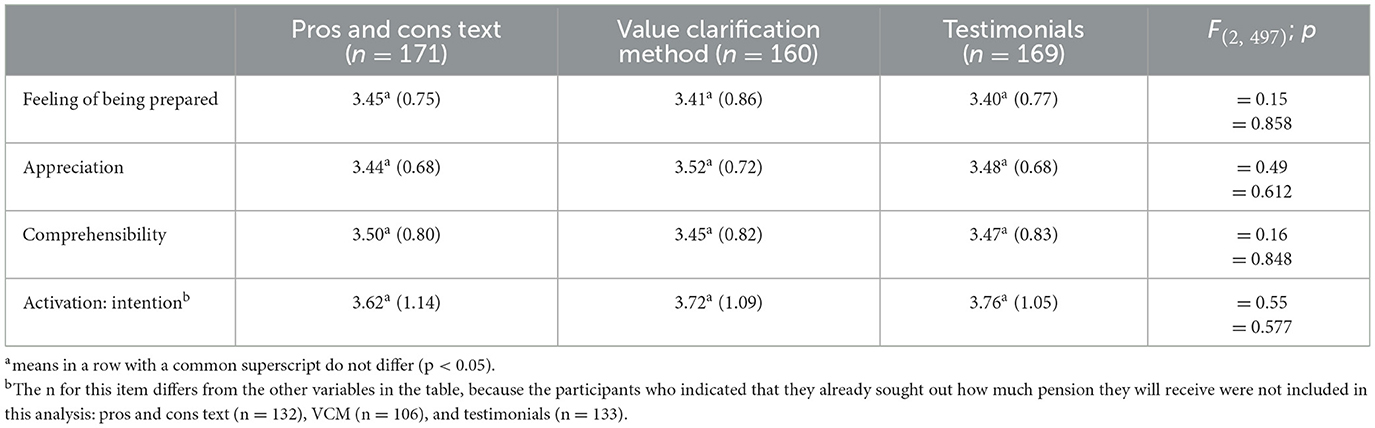

Table 4 displays the mean preparation for decision making and appreciation scores. There were no significant differences between the conditions [feeling of being prepared: F(2, 497) = 0.15; p = 0.86; Appreciation: F(2, 497) = 0.49; p =0.61; Comprehensibility: F(2, 497) = 0.16; p = 0.85].

Table 4. Participants' feeling of being prepared, appreciation of the provided decision support, and intention to explore the financial consequences, for each condition (1 = low, 5 = high).

3.3.2 Activation

The participants in the three conditions did not differ significantly in the extent to which they intend to sometime soon seek out how much pension they will receive [F(2, 368) =0.55, p =0.577] (see Table 4).

Subsequently, we assessed whether the next step of participants depended on the type of decision support: (i) visit the pension planner of the pension fund, (ii) visit a web page of the pension fund with additional information about the decision, or (iii) end the survey (see Appendix D.2 for the preferred next step of the participants).

As in the first study, in order to predict this, we conducted a multinomial logistic regression with two dummy variables, for the testimonials and the VCM. The multinomial logistic regression showed that the model is significant, with several significant predictors (see Table 5). Self-efficacy regarding financial matters was a significant predictor of both visiting the pension planner and visiting a web page with additional information. This means that participants who felt more able to deal with financial matters, were more likely to visit the pension planner and a web page with additional information. Furthermore, level of education was a significant predictor of visiting a web page with additional information: participants with a higher level of education were less likely to visit a web page with additional information. Finally, the testimonial dummy and the VCM dummy were no significant predictors of a next step.12

Table 5. Results multinomial logistic regression (Study 2).

Finally, we checked whether the drop-out of participants varied between the three conditions. The number of participants who dropped out during the intervention [χ2(2) = 11.40, p = 0.003; Cramer's V = 0.136] varied significantly. With the pros and cons text, significantly fewer people (n = 7) dropped out than expected (p < 0.05). With the VCM, significantly more people (n = 24) dropped out than expected (p < 0.05).

3.3.3 Intention for the decision when to retire

The participants in the three conditions did not differ significantly [χ2(10) = 9.31, p =0.503] with respect to the decision alternative they would currently prefer, assuming that it is financially possible to retire earlier (see Table 6). The types of decision support did not lead to different decisions.

Table 6. Intention for the decision when to retire, for each condition (in %).

3.4 Conclusion

The results of Study 2 show that participants who received the VCM or the testimonials, compared to participants who received the pros and cons text, no longer feel less prepared for decision making, appreciate the decision support less, or find the decision support less comprehensible. However, the activation effect was not replicated and despite (small) changes in the setup of the second study, the VCM still led to more participants dropping out than the pros and cons text.

4 General discussion

In this paper, we examined the impact of various interventions supporting pension participants in making (complex) decisions. Grounded in FTT, we argued that suitable decisions require participants to understand meaningful differences between decision alternatives. In the medical domain, VCMs and testimonials appear to be particular suitable to help people with this—although that is not a consistent finding across all studies. Therefore, research is called for to examine which VCM and testimonial designs are effective decision support for which type of decisions and in which contexts (see Witteman et al., 2016b; Shaffer et al., 2021). As such, we considered VCMs and testimonials as potentially effective interventions to explore for pension decision support. In this paper, we have discussed two studies on the effectiveness of these types of decision support for the decision when to retire. We compared: (a) a traditional text with pros and cons of retiring earlier or later, (b) a VCM that helps participants to get an impression about their work-life balance and their job satisfaction, and (c) two testimonials that describe how other participants gave meaning to the decision alternatives and how they (partly) regretted their decision.

The two studies showed mixed results. In the first study, we found an activating effect of the VCM and of the testimonials: participants who received one of these two types of decision support were more likely to visit a web page of the pension fund with additional information about the decision. However, on other variables for effective decision support, the VCM (feeling of being prepared to make the decision, appreciation, and comprehensibility) and the testimonials (feeling of being prepared to make the decision) were less effective than the pros and cons text. In the second study, we found no differences between the three types of decision support for any of these variables for effective decision support. Finally, in both studies, the VCM led to more participants dropping out, the pros and cons text to fewer. After the first study, we thought this might be explained by the fact that the VCM can be considered a new type of decision support that participants may not recognize as such. Therefore, in the second study we introduced the intervention more explicitly as information that can help participants make the decision when to retire. However, the VCM still led to more participants dropping out. We now think it might be attributed to the VCM requiring a larger time investment (Study 1: 12 min, Study 2: 10 min) than the testimonials (Study 1: 10 min, Study 2: 7 min) and the pros and cons text (Study 1: 9 min, Study 2: 7 min).

We can conclude that the two studies conducted in this research did not yield unambiguous results on whether a particular type of decision support is more suitable to support participants in making the decision when to retire. Therefore, it is too early to make recommendations for the implementation of one of the new types of decision support.

One possible explanation for the lack of differences in effects between the three interventions is that the content of the three interventions was to some extent comparable. All addressed the relevance of work-life balance and job satisfaction for the decision when to retire. The way these dimensions were communicated differed, but it is possible that the effectiveness of the different interventions was mainly driven by their (comparable) content—ergo the lack of differences.

The lack of differences in effects between the three interventions might also be attributed to the content of all three having been suboptimal in providing effective decision support. While all three addressed the relevance of work-life balance and job satisfaction, the dimension ‘(in)sufficient income' was not included in the interventions. The pros and cons text discussed the financial consequences of the decision alternatives, the testimonials described how two other participants considered and experienced the financial consequences of the options, and the VCM, like the other two interventions did as well, only stressed the need to seek out the financial consequences of the decision alternatives. But none of the interventions provided insight into whether the decision alternatives provided sufficient income for the desired standard of living, which is obviously an essential question.

Due to privacy issues, it was not possible to communicate personal monetary amounts with the interventions. However, even if it had been possible to provide participants with the exact monetary amounts associated with the decision alternatives, it is questionable whether this would have solved the problem. The exact monetary amounts on themselves are not really meaningful; the main question is whether the amount is sufficient for the desired standard of living. This is a subjective measure that is difficult to determine. Participants need help to gain insight into which amounts are sufficient for which standard of living. Communicative initiatives are being developed to address this need; Barrett (2024), for example, examined evaluative labels (descriptions classifying the future pension benefit on a scale from “minimum” to “comfortable”) and consumption baskets (descriptions specifying consumption possibilities with different pension benefits, such as the possibilities for gifts, travel, and housing) in a pension decision-making context as additional supportive information to numerical amounts.

Finally, the specific lack of superior effects of the VCM as pension decision support might be attributed to the possibly suboptimal design of the intervention. The VCM only provided participants with feedback on their scores on the work-life balance questionnaire and the job satisfaction questionnaire. This had to help them to determine how they fare on these dimensions. In the second study, we tried to make these results more informative by providing specific information on how the participants' scores on work-life balance and job satisfaction compared to those of their peers. However, it still remained up to the participant to explicitly relate his or her scores to the different decision alternatives. Some medical VCMs explicitly show how different decision alternatives align with the expressed dimensions (e.g., scores of a user's current situation on or personal importance of dimensions), for example by giving a recommended option or presenting scores to show how well or poorly each option fits with the user's responses (Witteman et al., 2016b). The systematic review by Witteman et al. (2016a) suggests that relating expressed relevant dimensions to decision alternatives may lead to better outcomes (greater decision readiness, more positive post-decision effects) compared to VCMs that do not (e.g., only ranking the current situation on or personal importance of dimensions). It seems that VCMs “may be more helpful when they are designed not only to assist people in sorting out what matters to them, but also in seeing how what matters to them determines which option may be best for them” (Witteman et al., 2016a, p. 774). According to Witteman et al. (2020), these type of VCMs indeed seem to be the most effective (i.e., in reducing decisional conflict and in encouraging decisions in line with people's values). Integrating this feature into a pension VCM could be beneficial for pension decision support. For example, such a VCM could indicate that for a participant with little job satisfaction and whose work often hinders the personal life, early retirement appears to be the more suitable option (and vice versa). However, this would be difficult to implement, for example because it also requires an alignment of the decision alternatives with counteracting scores on work-life balance and job satisfaction (e.g., work that often hinders private life, but also offers a lot of job satisfaction).

Moreover, future research should consider to measure participants' evaluations and (actual) decisions after a delay. Feldman-Stewart et al. (2012) studied the effectiveness of a VCM including follow-up measurements, showing that relevant effects of the VCM were more pronounced at later dates (i.e., a few months after completing the treatment and a year or more later) than immediately after the actual decision had been made. Witteman et al. (2016a) also state that longer-term outcomes are likely for VCMs and therefore encourage researchers to conduct follow-up measurements (although they warn that these may be influenced by the outcome of the decision rather than by the decision support). It is conceivable that longer-term outcomes are also likely for testimonials.

Future studies on the effectiveness of pension decision support should also be conducted amongst different populations. The participants who joined our two studies were probably more motivated and involved with pensions than the average pension participant and therefore may not be representative of the general Dutch 55+ population. However, the response rates of 5.8% and 7.7% for our two studies are quite comparable to other studies in the pension domain (see, for example, Dinkova et al., 2018, 2022; Eberhardt et al., 2022) and the studies were conducted with a large sample of actual participants, which is beneficial to the external validity of the research. In addition, although there was strong variation in the education level of the participants who joined the studies, gender and age varied less (attributable to respectively the predominantly male population of the pension funds and to the inclusion criteria of our studies) (see Appendix C). Moreover, a study by Bruine de Bruin et al. (2017) shows that people with lower numeracy may be more affected by testimonials when making a decision. Although numbers were not a major component of our material, it is a factor we did not control for. This means that any results from our studies should be interpreted cautiously.

Finally, more research should be conducted on the use of new, non-traditional types of decision support such as VCMs and testimonials for other pension decisions. In the two studies discussed in this paper, we focused on one pension decision: when to retire. In the Netherlands, pension participants face several other non-reversible decisions that involve complex intertemporal considerations with uncertain outcomes. For example, the decision to exchange accrued pension between their own pension and the pension benefit that is reserved for their spouse in case they die first (partner's pension), or the decision how to allocate the pension over time (evenly, or in a high/low construction).

Despite the aforementioned shortcomings and the lack of clear effects of the VCM and the testimonials, we have conducted insightful research: a unique, repeated field study with large samples (ensuring sufficient statistical power to find effects) of real-life participants who are actually facing the decision, with no alternative explanations for the lack of effects (e.g., in case the participants in the different conditions would not be comparable), and of which the design is strongly substantiated in collaboration between science and practice. Therefore, this research provides insight into the contexts in which certain types VCMs and testimonials are (not) effective as decision support.

Furthermore, the landscape of (Dutch) pension communication is changing and it becomes increasingly important for pension providers to encourage participants to take relevant action and to adequately support them in making suitable decisions. This research contributes to the knowledge about the use of decision support for these purposes and expands the arsenal of communication options to support participants on the pension provider's general website, before logging into the personal pension dashboard.

Data availability statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

Ethics statement

The studies involving humans were approved by Faculty Ethics Assessment Committee Humanities of the Utrecht University. The studies were conducted in accordance with the local legislation and institutional requirements. The participants provided their written informed consent to participate in this study. Written informed consent was obtained from the individual(s) for the publication of any potentially identifiable images or data included in this article.

Author contributions

JS: Conceptualization, Data curation, Formal analysis, Investigation, Methodology, Validation, Writing – original draft, Writing – review & editing. BH: Conceptualization, Methodology, Supervision, Validation, Writing – review & editing. HH: Conceptualization, Data curation, Formal analysis, Methodology, Project administration, Supervision, Validation, Writing – review & editing.

Funding

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. This project was funded by Netspar, Network for Studies on Pensions, Aging and Retirement, grant number 2018.1.

Acknowledgments

We thank TKP, PME pension fund, BPL Pension, Pension Fund UWV, Pension Fund PostNL, and all participants for their indispensable contribution to this study. We also thank the editor and the reviewers of Frontiers in Behavioral Economics for their valuable comments on earlier versions of this manuscript.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher's note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/frbhe.2024.1369500/full#supplementary-material

Footnotes

1. ^In the literature, different terms are used sometimes where the same concept is meant. For example: “narratives”, “personal stories”, and “testimonials”. In this paper we use the term “testimonials”, as a form of narratives and personal stories.

2. ^We also check for this with the item on the intention for the decision when to retire, see section “Questionnaire”.

3. ^In that case, the first or last testimonial respectively has more impact.

4. ^The options to receive a link to (1) the pension planner or (2) additional information were also randomized to control for a primacy or recency effect.

5. ^753 participants started the survey, but did not complete it. In addition, 38 participants left an open comment at the end of the survey in which they indicated that it was not clear to them which ‘provided information' the questions from the survey related to (for example, the decision support intervention of this study, or the information communicated by the pension funds in the past). The data of these two groups of participants were not included in the analysis.

6. ^We also checked for differences between the two groups of participants who received the different order of testimonials (see the section ‘Procedure' above), on preparation for decision making, appreciation of the decision support, activation, and the intention for the decision when to retire. We found significant differences for the behavioral measure [χ2(2) = 6.70, p = 0.035; Cramer's V = 0.094], which disappeared if we specified for the next step (looking at the standardized residuals), and for the extent to which participants intend to sometime soon seek out how much pension they will receive [F(1, 754) = 4.15; p =.042; η2 = 0.005], which are hardly relevant in practice.

7. ^In this results section, in the main text we only specify significant differences between conditions. Non-effects can be found in the tables.

8. ^We conducted the same analysis including a dummy variable for whether participants already sought out how much pension they will receive. The analysis showed no different results with respect to the key variables (see Appendix E.1).

9. ^Benchmark data existed for both scales, but these were outdated (collected in 2013 and between 1999 and 2003, respectively) and collected among Dutch employees from various age groups. We only wanted to use recent benchmark data and to give specific feedback (relevant to our target group of 55 and older), and therefore, we chose not to use these benchmark data.

10. ^92 participants started the survey, but were filtered out with the filter question because they already finalized a decision when to retire. In addition, 145 participants started the survey, but did not complete it. Finally, five participants left an open comment at the end of the survey in which they indicated that it was not clear to them which ‘provided information' the questions from the survey related to. The data of these groups of participants were not included in the analysis.

11. ^We also checked for differences between the two groups of participants who received the different order of testimonials, on preparation for decision making, appreciation of the decision support, activation, and the intention for the decision when to retire. We found no differences.

12. ^As in the first study, we also conducted the same analysis including a dummy variable for whether participants already sought out how much pension they will receive. The analysis showed no different results with respect to the key variables (see Appendix E.2).

References

Barrett, A. M. (2024). Money Matters: Understanding and Improving Financial Well-Being (Doctoral Thesis) Maastricht University, Maastricht, Netherlands.

Beehr, T. A., and Bennett, M. M. (2015). Working after retirement: features of bridge employment and research directions. Work Aging Retirem. 1, 112–128. doi: 10.1093/workar/wau007

Bennett, C., Graham, I. D., Kristjansson, E., Kearing, S. A., Clay, K. F., and O'Connor, A. M. (2010). Validation of a preparation for decision making scale. Patient Educ. Couns. 78, 130–133. doi: 10.1016/j.pec.2009.05.012

Blalock, S. J., and Reyna, V. F. (2016). Using fuzzy-trace theory to understand and improve health judgments, decisions, and behaviors: a literature review. Health Psychol. 35, 781–792. doi: 10.1037/hea0000384

Broniatowski, D. A., and Reyna, V. F. (2018). A formal model of fuzzy-trace theory: variations on framing effects and the Allais paradox. Decision 5, 205–252. doi: 10.1037/dec0000083

Bruine de Bruin, W., Wallin, A., Parker, A. M., Strough, J., and Hanmer, J. (2017). Effects of anti-versus pro-vaccine narratives on responses by recipients varying in numeracy: a cross-sectional survey-based experiment. Med. Deci. Making 37, 860–870. doi: 10.1177/0272989X17704858

Brust-Renck, P. G., Reyna, V. F., Wilhelms, E. A., and Lazar, A. N. (2016). “A fuzzy-trace theory of judgment and decision-making in health care: explanation, prediction, and application,” in Handbook of Health Decision Science (New York, NY: Springer), 71–86.

Butow, P., Fowler, J., and Ziebland, S. (2005). “Section E: using personal stories,” in IPDAS Collaboration Background Document, eds. A. O'Connor, H. Llewellyn-Thomas & D. Stacey, 24–27. Available online at: http://ipdas.ohri.ca/ipdas-chapter-e.pdf (accessed January 12, 2024).

Connolly, T., and Zeelenberg, M. (2002). Regret in decision making. Curr. Dir. Psycho. 11, 212–216. doi: 10.1111/1467-8721.00203

Dinkova, M., Elling, S., Kalwij, A., and Lentz, L. (2022). You're invited–RSVP! The role of tailoring in incentivising people to delve into their pension situation. J. Pens. Econ. Finance 21, 38–55. doi: 10.1017/S1474747220000141

Dinkova, M., Elling, S. K., Kalwij, A. S., and Lentz, L. R. (2018). The effect of tailoring pension information on navigation behaviour. Netspar Design Paper 38, 1–29.

Eberhardt, W., Post, T., Hoet, C., and Brüggen, E. (2022). Exploring the first steps of retirement engagement: a conceptual model and field evidence. J. Serv. Manag. 33, 1–26. doi: 10.1108/JOSM-11-2020-0402

Eismann, M., Henkens, K., and Kalmijn, M. (2017). Spousal preferences for joint retirement: evidence from a multiactor survey among older dual-earner couples. Psychol. Aging 32, 689–697. doi: 10.1037/pag0000205

Elling, S., Lentz, L., and De Jong, M. (2012). Combining concurrent think-aloud protocols and eye-tracking observations: an analysis of verbalizations and silences. IEEE Trans. Prof. Commun. 55, 206–220. doi: 10.1109/TPC.2012.2206190

Fagerlin, A., Pignone, M., Abhyankar, P., Col, N., Feldman-Stewart, D., Gavaruzzi, T., et al. (2013). Clarifying values: an updated review. BMC Med. Inform. Decis. Mak. 13, S8. doi: 10.1186/1472-6947-13-S2-S8

Fasbender, U., Wang, M., Voltmer, J. B., and Deller, J. (2016). The meaning of work for post-retirement employment decisions. Work Aging Retirem. 2, 12–23. doi: 10.1093/workar/wav015

Feldman-Stewart, D., Tong, C., Siemens, R., Alibhai, S., Pickles, T., Robinson, J., et al. (2012). The impact of explicit values clarification exercises in a patient decision aid emerges after the decision is actually made: evidence from a randomized controlled trial. Med. Deci. Mak. 32, 616–626. doi: 10.1177/0272989X11434601

Fraenkel, L., Peters, E., Charpentier, P., Olsen, B., Errante, L., Schoen, R. T., et al. (2012). Decision tool to improve the quality of care in rheumatoid arthritis. Arthritis Care Res. 64, 977–985. doi: 10.1002/acr.21657

Furunes, T., Mykletun, R. J., Solem, P. E., de Lange, A. H., Syse, A., Schaufeli, W. B., et al. (2015). Late career decision-making: a qualitative panel study. Work, Aging Retirem. 1, 284–295. doi: 10.1093/workar/wav011

Geurts, S. A., Taris, T. W., Kompier, M. A., Dikkers, J. S., Van Hooff, M. L., and Kinnunen, U. M. (2005). Work-home interaction from a work psychological perspective: development and validation of a new questionnaire, the SWING. Work Stress 19, 319–339. doi: 10.1080/02678370500410208

Lourenço, C. J., Dellaert, B. G., and Donkers, B. (2020). Whose algorithm says so: the relationships between type of firm, perceptions of trust and expertise, and the acceptance of financial robo-advice. J. Inter. Market. 49, 107–124. doi: 10.1016/j.intmar.2019.10.003

Maes, A., Ummelen, N., and Hoeken, H. (1996). Instructieve teksten: Analyse, ontwerp en evaluatie [Instructional Texts: Analysis, Design, and Evaluation]. Bussum: Uitgeverij Coutinho.

Michaud, P. C., Van Soest, A., and Bissonnette, L. (2020). Understanding joint retirement. J. Econ. Behav. Organiz. 173, 386–401. doi: 10.1016/j.jebo.2019.07.013

Nibud (2022). Blik op pensioen: De klantreis [A look at retirement: The customer journey]. Available online at: https://www.nibud.nl/nieuws/onderzoek-nibud-pensioentool/ (accessed January 12, 2024).

Pension Act 48a (2023). Pension Act 48a. Available online at: https://wetten.overheid.nl/BWBR0020809/2023-07-01 (accessed January 12, 2024).

Pieterse, A. H., de Vries, M., Kunneman, M., Stiggelbout, A. M., and Feldman-Stewart, D. (2013). Theory-informed design of values clarification methods: a cognitive psychological perspective on patient health-related decision making. Soc. Sci. Med. 77, 156–163. doi: 10.1016/j.socscimed.2012.11.020

Reyna, V. (2018). When irrational biases are smart: a fuzzy-trace theory of complex decision making. J. Intellig. 6, 29. doi: 10.3390/jintelligence6020029

Reyna, V. F. (2008). A theory of medical decision making and health: Fuzzy Trace Theory. Med. Decis. Making 28, 850–865. doi: 10.1177/0272989X08327066

Reyna, V. F., Edelson, S., Hayes, B., and Garavito, D. (2022). Supporting health and medical decision making: findings and insights from fuzzy-trace theory. Med. Decis. Making 42, 741–754. doi: 10.1177/0272989X221105473

Schaufeli, W. B., and Bakker, A. B. (2004). Bevlogenheid: een begrip gemeten [Engagement: a concept measured]. Gedrag & Organisatie 17:2. doi: 10.5117/2004.017.002.002

Shaffer, V. A., Brodney, S., Gavaruzzi, T., Zisman-Ilani, Y., Munro, S., Smith, S. K., et al. (2021). Do personal stories make patient decision AIDS more effective? An update from the International Patient Decision Aids Standards. Med. Decis. Making 41, 897–906. doi: 10.1177/0272989X211011100

Shaffer, V. A., and Zikmund-Fisher, B. J. (2013). All stories are not alike: a purpose-, content-, and valence-based taxonomy of patient narratives in decision aids. Med. Decis. Making 33, 4–13. doi: 10.1177/0272989X12463266

Smith, S. G., Raine, R., Obichere, A., Wolf, M. S., Wardle, J., and von Wagner, C. (2015). The effect of a supplementary (‘gist-based') information leaflet on colorectal cancer knowledge and screening intention: a randomized controlled trial. J. Behav. Med. 38, 261–272. doi: 10.1007/s10865-014-9596-z

Strikwerda, J., Holleman, B., and Hoeken, H. (2022). Designing pension communication: Lessons from the medical domain. Inform. Design J 26, 260–281. doi: 10.1075/idj.21011.str

Strikwerda, J., Holleman, B., and Hoeken, H. (2024). Relevant dimensions to give meaning to pension decisions. Work Aging Retirem. doi: 10.1093/workar/waae001 [Epub ahead of print].

Ubel, P. A., Jepson, C., and Baron, J. (2001). The inclusion of patient testimonials in decision aids: effects on treatment choices. Med. Decis. Making 21, 60–68. doi: 10.1177/0272989X0102100108

Van Dalen, H., and Henkens, K. (2022). Zoeken naar pensioeninformatie als de finishlijn in zicht komt [Searching for pension information as the finish line approaches]. Pensioen Magazine. 27, 12–14.

Van den Berg, T. I., Elders, L. A., and Burdorf, A. (2010). Influence of health and work on early retirement. J. Occup. Environm. Med. 52, 576–583. doi: 10.1097/JOM.0b013e3181de8133

Van Solinge, H., Damman, M., and Hershey, D. A. (2021). Adaptation or exploration? Understanding older workers' plans for post-retirement paid and volunteer work. Work, Aging Retirem. 7, 129–142. doi: 10.1093/workar/waaa027

Van Solinge, H., Van Dalen, H., and Henkens, K. (2020). “Deeltijdpensioen: belangstelling en belemmeringen op de werkvloer [Part-time retirement: interest and obstacles in the workplace],” in Netspar Design Paper, 162. Available online at: https://www.netspar.nl/assets/uploads/P20201106_Netspar-Design-Paper-162-WEB.pdf (accessed January 12, 2024).

Winterbottom, A., Bekker, H. L., Conner, M., and Mooney, A. (2008). Does narrative information bias individual's decision making? A systematic review. Soc. Sci. Med. 67, 2079–2088. doi: 10.1016/j.socscimed.2008.09.037

Witteman, H. O., Gavaruzzi, T., Scherer, L. D., Pieterse, A. H., Fuhrel-Forbis, A., Chipenda Dansokho, S., et al. (2016a). Effects of design features of explicit values clarification methods: a systematic review. Med. Deci. Making 36, 760–776. doi: 10.1177/0272989X16634085

Witteman, H. O., Julien, A.-S., Ndjaboue, R., Exe, N. L., Kahn, V. C., Fagerlin, A., et al. (2020). What helps people make values-congruent medical decisions? eleven strategies tested across 6 studies. Med. Deci. Making 40, 266–278. doi: 10.1177/0272989X20904955

Witteman, H. O., Scherer, L. D., Gavaruzzi, T., Pieterse, A. H., Fuhrel-Forbis, A., Chipenda Dansokho, S., et al. (2016b). Design features of explicit values clarification methods: a systematic review. Med. Deci. Making 36, 453–471. doi: 10.1177/0272989X15626397

Wolfe, C. R., Reyna, V. F., Widmer, C. L., Cedillos, E. M., Fisher, C. R., Brust-Renck, P. G., et al. (2015). Efficacy of a web-based intelligent tutoring system for communicating genetic risk of breast cancer: a fuzzy-trace theory approach. Med. Deci. Making 35, 46–59. doi: 10.1177/0272989X14535983

Keywords: pension communication, decision support, Fuzzy-Trace Theory, value clarification methods, testimonials, activation, feeling of preparation, appreciation

Citation: Strikwerda J, Holleman B and Hoeken H (2024) Supporting pension decisions with value clarification methods or testimonials: two studies showing mixed effects on activation and feeling of preparation. Front. Behav. Econ. 3:1369500. doi: 10.3389/frbhe.2024.1369500

Received: 12 January 2024; Accepted: 17 May 2024;

Published: 05 June 2024.

Edited by:

Thomas Post, Maastricht University, NetherlandsReviewed by:

Minou Van Der Werf, Maastricht University, NetherlandsGerrit Antonides, Wageningen University and Research, Netherlands

Copyright © 2024 Strikwerda, Holleman and Hoeken. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Jelle Strikwerda, ai5zdHJpa3dlcmRhQHV1Lm5s