Jinli Duan

Jinli Duan Feng Jiao

Feng Jiao Jicheng Xi3

Jicheng Xi3- 1School of Economics and Management, Sanming University, Sanming, Fujian, China

- 2School of Leadership and Managment, Arden University, Coventry, United Kingdom

- 3School of Economics and Management, Fuzhou University, Fuzhou, China

- 4School of Economics and Management, Yango University, Fuzhou, Fujian, China

Background: The National Health Commission and the other relevant departments in China have initiated testing of the Diagnosis Related Groups (DRGs) system in 30 pilot locations since 2019. In the process of DRG payment reform, accounting for the costs of diseases has become a highly challenging issue. The traditional method of disease accounting method overlooks the compensation for the knowledge capital value of medical personnel.

Objective: The primary objective of this study is to analyze the cost accounting scheme of China’s Diagnosis Related Groups (C-DRG), focusing on the value of knowledge capital.

Methods: The study initially proposes a measurement index system for the value of knowledge-based capital, including the difficulty of disease treatment, labor intensity of disease treatment, risk of disease treatment, and operation/treatment time for diseases. The Analytic Hierarchy Process (AHP) is then utilized to weigh the features of medical workers’ knowledge capital value. First, pairwise comparisons are conducted in this stage to develop a two-pair judgment matrix of the primary indicators. Second, the eigenvectors corresponding to the maximum eigenvalues of the matrix are calculated to generate the weight coefficient of each feature. The consistency test is carried out after this stage. An empirical analysis is conducted by collecting data, including the full costs of treating three types of diseases—hip replacement, acute simple appendicitis, and heart bypass surgery—from one public medical institution.

Results: The empirical analysis examines whether this DRG costing accounting can address the issue of neglecting the value of medical workers’ knowledge capital. The methods reconfigure the positive incentive mechanism, stimulate the endogenous motivation of the medical service system, foster independent changes in medical behavior, and achieve the goals of reasonable cost control.

Conclusion: In the cost accounting system of C-DRG, the value of medical workers’ knowledge capital is acknowledged. This acknowledgment not only boosts the enthusiasm and creativity of medical workers in optimizing and standardizing the diagnosis and treatment process but also improves the transparency and authenticity of DRG pricing. This is particularly evident in the optimization and standardization of the diagnosis and treatment processes within medical institutions and in monitoring inadequate medical practices within these institutions.

Introduction

Knowledge capital encompasses both explicit and implicit knowledge owned or controlled by an organization, capable of bringing value to it (1). This concept aligns with intangible assets (knowledge capitals) in traditional accounting practices (2) and aids in discerning disparities between an organization’s book value and market value. However, recent research has criticized practitioners and academics for being ensnared by the notion of ‘Quantification’, assuming that because some knowledge capital cannot be objectively and fairly measured, it should not be included in the cost element (3).

Furthermore, the measurement and disclosure of knowledge capital in real practice primarily concentrate on the static knowledge capital stock, neglecting the dynamic aspect of knowledge capital in ‘action’ (4). In this study, we propose a disease cost accounting method based on the value of knowledge capital within the DRG payment system.

Knowledge-based human capital constitutes the fundamental production factor in medical institutions. However, due to the scarcity of knowledge capital and ownership separation of knowledge capital, as well as the high acquisition costs associated with it, the cost accounting method for knowledge capital differs from the traditional costing accounting method (5). In addition, the organizational structure and service process management in medical institutions diverge significantly from those in traditional manufacturing industries (6). Consequently, specialized cost accounting and management models are necessary for medical institutions (7). The cost accounting system based on manufacturing costs is inadequate for the accounting system in medical institutions, as it cannot reflect the intrinsic logic of innovative behaviors of medical workers and the core value of innovative elements in medical institutions (8).

As integrated innovators, medical workers, particularly doctors who work on the frontlines, contribute valuable implicit knowledge accumulated from their long-term service (9). This knowledge enables them to manage uncertainties for patients and provide value-added services for medical institutions. According to Becker’s related theories, the time required to accomplish a task comprises two components: the time required to perform the task and the time needed to acquire the knowledge necessary to complete the task (10). Therefore, the time necessary for medical workers to execute the integration and coordination of medical services should encompass two aspects, including the time allocated for delivering basic services and the time dedicated to integrating and coordinating medical services. The former entails providing medical services to patients, such as the time spent on consultation, decision-making, and evaluating decisions around diagnostic and treatment activities. The latter involves accumulating activities essential for effectively innovating medical activities. In reality, the process of acquiring knowledge often requires more time than making and evaluating decisions.

Significant quantities of implicit knowledge demand extended periods for accumulation (11–15). This implicit knowledge requisite for medical integration activities encompasses disease-specific insights, patient-specific knowledge, medical diagnostic and treatment technologies, including drug treatment methodologies, and insights into the behavioral habits and foundational knowledge of relevant medical team members, essential for effectively navigating uncertainty (14, 16–19). This part of knowledge necessitates substantial accumulation in the initial education stage; meanwhile, it highly relies on the accumulation of doctors’ long-term clinical practice. Furthermore, doctors must consistently attend to patients to effectively apply relevant expertise. In this regard, current costing processes applied in medical institutions struggle to acknowledge the working time that medical workers invest in the abovementioned service, particularly the time required for medical workers to accumulate and complete tasks. The corresponding value of this time is rarely acknowledged (20, 21).

Full cost accounting of diseases considers the value of knowledge capital essential for medical workers to carry out medical service projects. The value of medical workers’ knowledge capital primarily manifests in the realization pathway, encompassing explicit and tacit knowledge (22–24). Explicit knowledge capital primarily pertains to the professional qualifications and other attributes of medical personnel, while tacit knowledge primarily pertains to their risk perception and ability to navigate uncertainty in medical service projects (25–28). Tacit knowledge is mainly evaluated through the difficulty and risk coefficients associated with medical services performed by medical workers for specific diseases (29, 30).

The rest of this article is organized as follows: Section 2 examines the evaluation of medical workers’ knowledge capital within the DRG cost accounting system. Section 3 provides an empirical analysis illustrating the cost accounting process based on knowledge of capital value. Section 4 applies the discussion to the cost accounting result. Finally, Section 5 offers a conclusion and proposes potential future research avenues.

Methods

The full-cost accounting index system

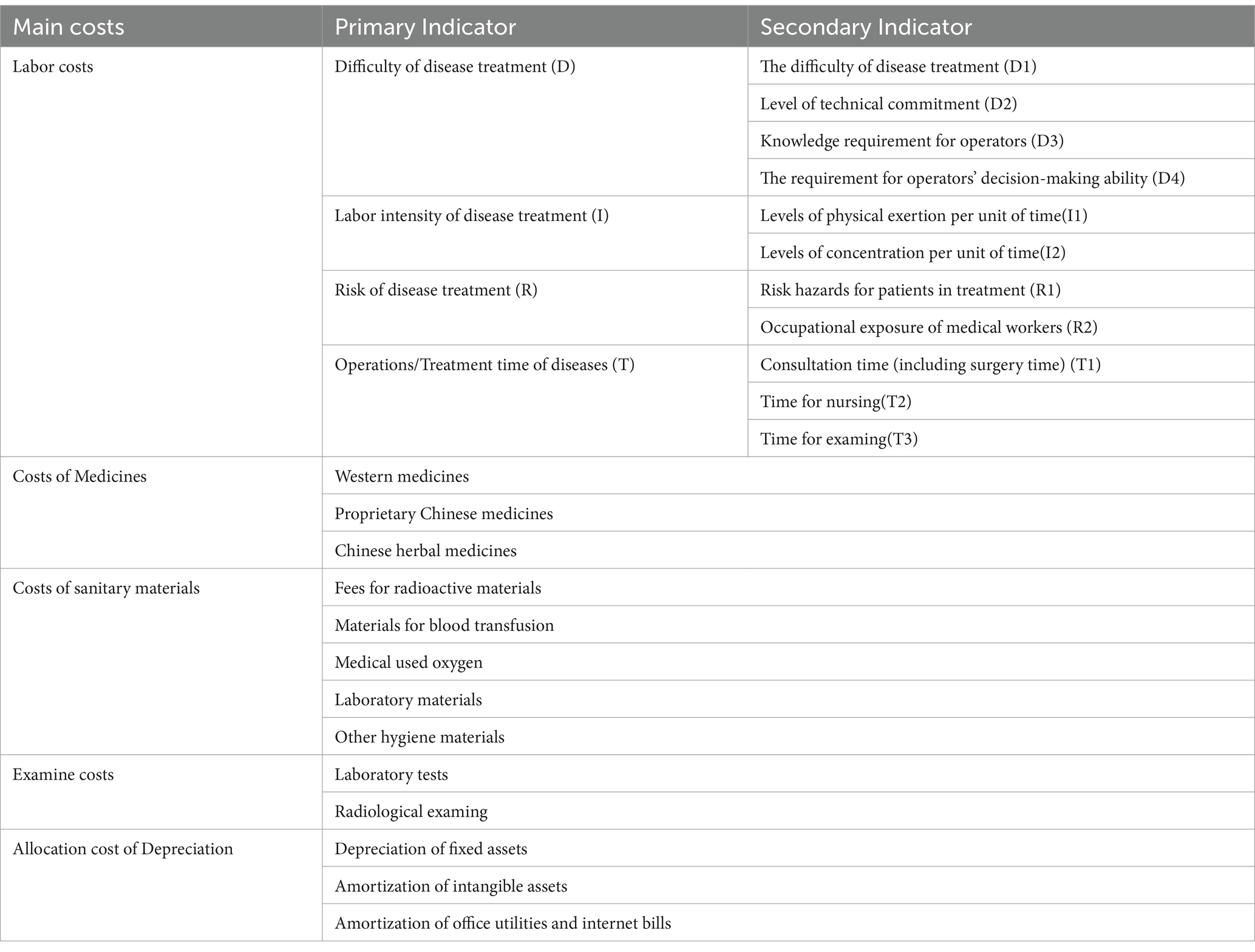

The disease cost index system includes labor costs, drug costs, health material costs, inspection costs, and depreciation and sharing costs (31). The calculation of labor costs is based on the evaluation model of the value of the knowledge capital of medical workers (32), including 4 primary indicators, namely the difficulty of the disease project, the labor intensity of the disease project, the risk degree of the disease project, and the operation time of the disease project, and 11 secondary indicators, which are the difficulty of disease treatment, level of technical commitment, knowledge requirement for operators, the requirement for operator’s decision - making ability, levels of physical exertion per unit of time, ability, levels of physical exertion per unit of time, levels of concentration per unit time, risk hazards for patients in treatment, occupational exposure of medical workers, consultation time (including surgery time), time for nursing and time for examining. These indicators are summarized and shown in Table 1.

Table 1. Disease cost accounting index system.

Determination of weight

In this study, the analytic hierarchy process (AHP) was used to determine the weight of medical workers’ knowledge of cost accounting indicators.

The establishment of a hierarchical framework

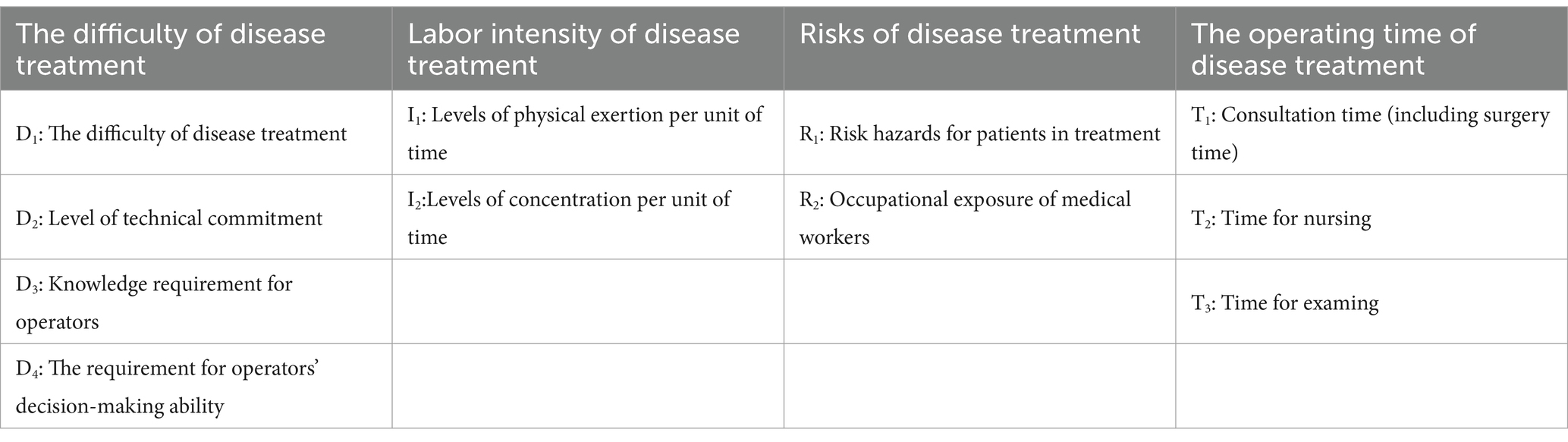

At the highest level of the hierarchy usually lies a single element, which is the decision goal. The intermediate level comprises criteria and sub-criteria, which may further branch into multiple layers. The criteria are guided by the decision-making goal, and the sub-criteria are influenced by the criteria at the preceding level, reflecting a top-down dominance relationship within the hierarchy. The knowledge capital value of costing indicators for medical workers is shown in Table 2.

Table 2. Knowledge capital value costing indicators for medical workers.

The construction of a two-pair judgment matrix

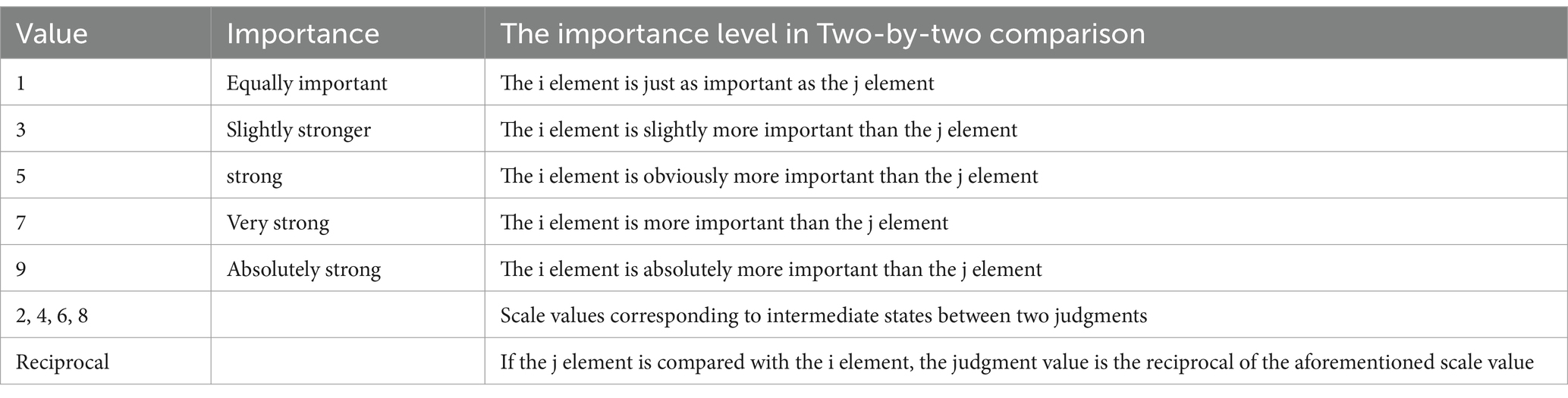

Once the hierarchical framework is established, the connection between the upper and lower elements becomes apparent. The expert group conducts an in-depth analysis of the accounting book data. Simultaneously, they invite cost accountants, clinicians, nurses, and medical technicians from the public hospitals where DRG trials are taking place. These participants are tasked with comparing the importance of indicators and constructing a two-by-two comparison matrix. The analytic hierarchy method typically employs the 9-level scale method to assign values to the elements of the judgment matrix, as shown in Table 3.

Table 3. Scale explanation on value 1 to 9.

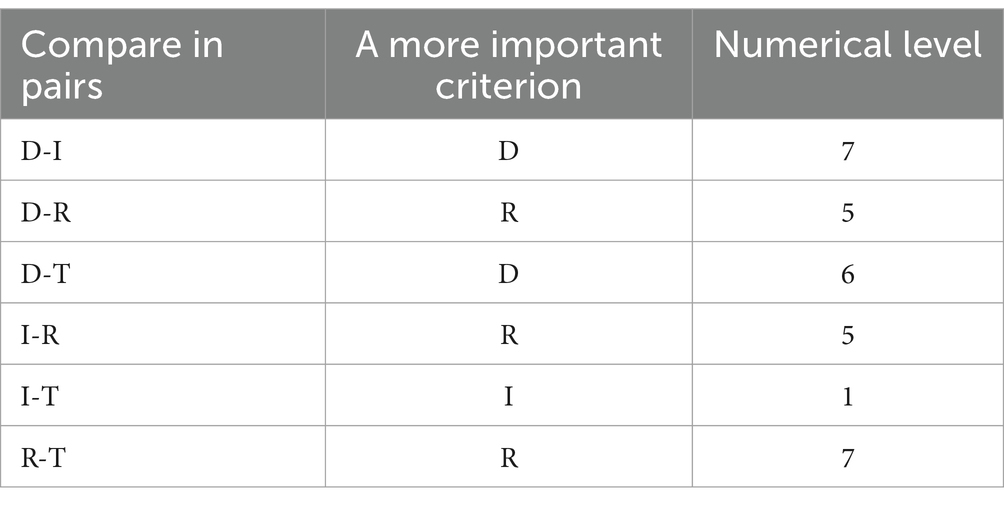

Table 3 shows that a value of 9 means “absolutely important,” a value of 7 means “very important,” and a value of 5 means “important,” so a median rating such as “the degree of importance is between very important and important” is awarded 6 points. The experts evaluated and weighed four primary indicators of the cost of knowledge for medical workers, and the resulting pairwise matrix is scored as shown in Table 4.

Table 4. Pairwise comparison of expert scores on decision criteria.

According to the scoring table provided by the decision expert, a pairwise comparison judgment matrix A of the primary indicators can be constructed:

The calculation of the weight coefficient

In brief, the eigenvectors corresponding to the maximum eigenvalues of matrix A can be calculated by approximate calculation methods such as the square root method and normalized to the weight of each evaluation index. The calculation of the weight coefficient is divided into three steps, using the square root method. The specific steps to adopt the square root method are as follows:

(1) calculate the product of all elements of each row of the judgment matrix A.

(2) calculate the root of

(3) Normalization of vectors

Then, the vector is the desired feature vector, and the weight of the primary index is obtained .

Consistency test

Upon obtaining the judgment matrix of the primary indicators, a consistency test is conducted. Due to the considerable number of pairwise comparisons, achieving complete consistency can be challenging. In reality, some inconsistency is inevitable in any pairwise comparison. To mitigate this issue, AHP offers a method to gauge the consistency of decision-makers when making such comparisons. If the desired level of agreement is not met, decision-makers should reassess the pairwise comparisons and make necessary adjustments before proceeding with the AHP analysis to minimize bias in subjective judgment. The consistency of pairwise comparisons is measured through a consistency metric (Table 5). The consistency check is conducted in three steps:

Table 5. The corresponding R.I value.

The first step is to calculate the maximum eigenroot in the pairwise comparison matrix A

Then,

which calculated .

Step 2: Calculate consistency indicator C.I

Step 3: Calculate the consistency ratio C.R

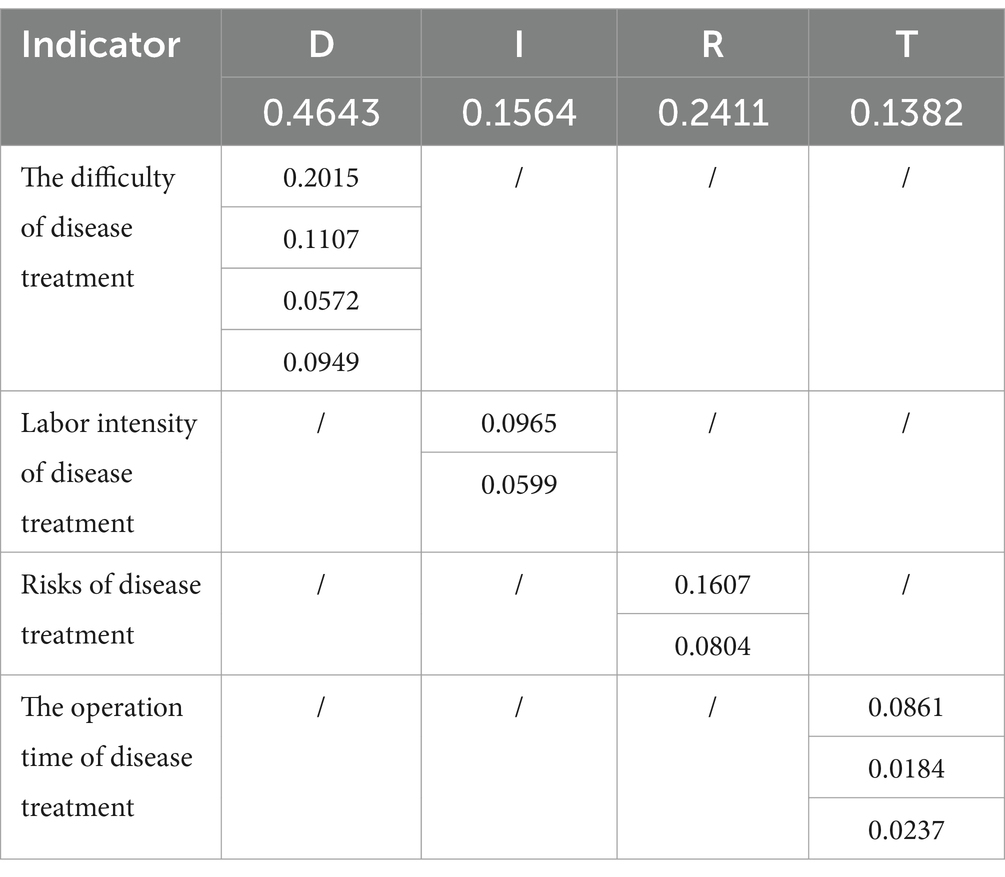

Since and , it is acceptable to compare the inconsistencies of matrix A, that is, the obtained weight–weight coefficients are valid. Similarly, the weights of secondary indicators can be obtained, and the summary table of the weights of primary and secondary indicators is shown in Table 6.

Table 6. Weight of knowledge capital value of accounting indicators for medical workers.

Empirical analysis

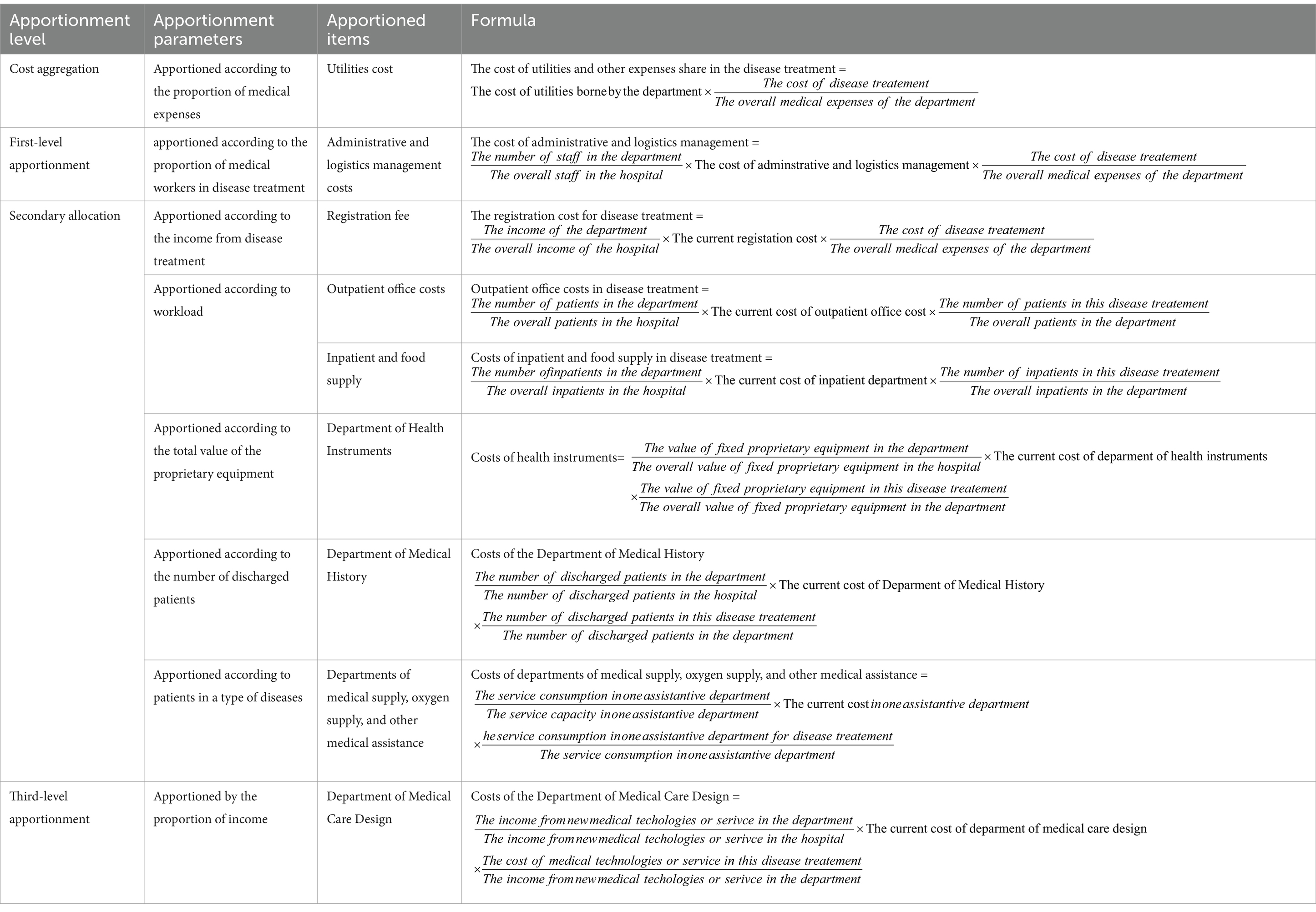

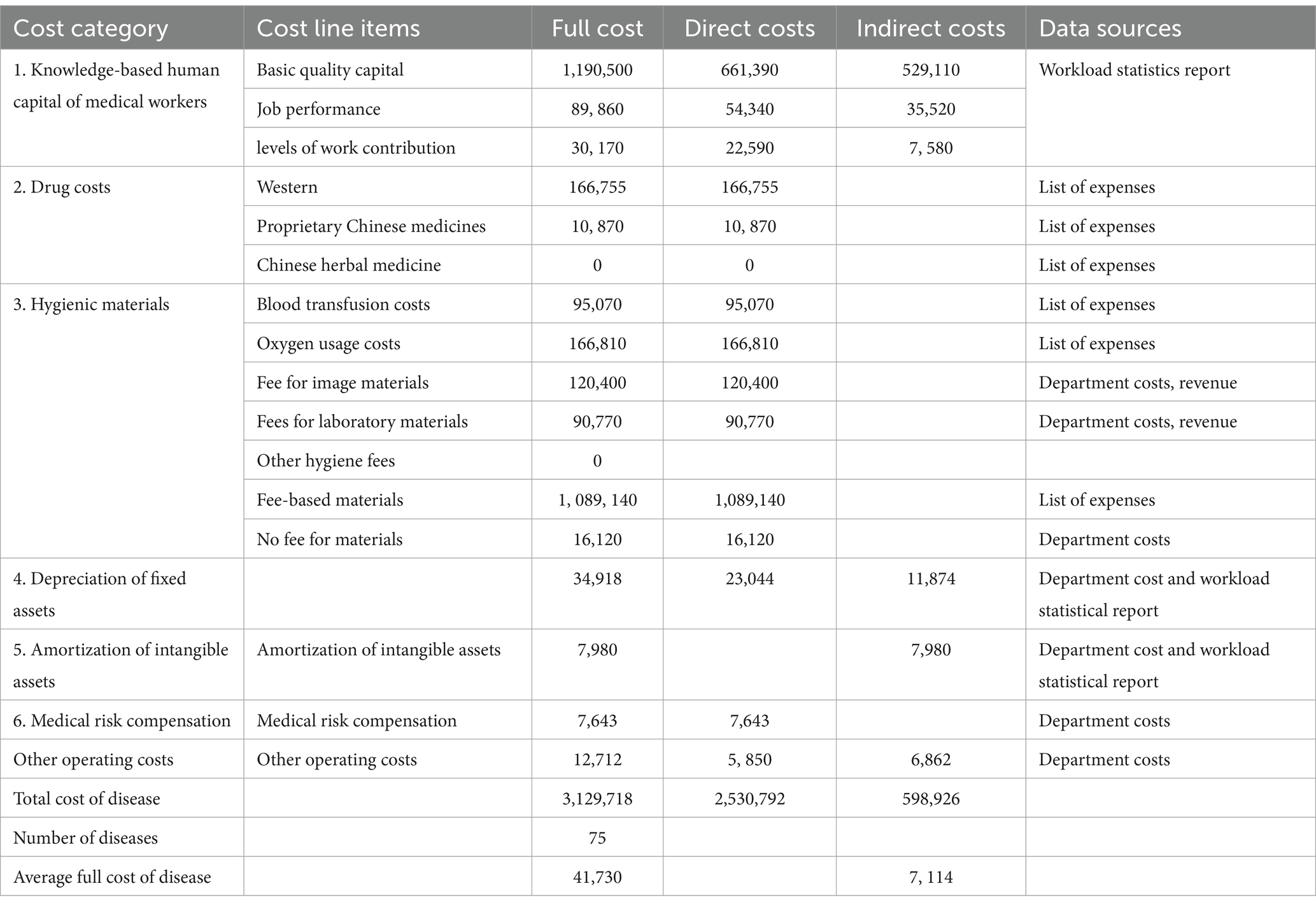

This study collects data on the full costs of treating three types of diseases: hip replacement, acute simple appendicitis, and heart bypass surgery. The dataset includes a patient settlement list, the first page of medical records, and the knowledge costs of medical workers, all sourced from a single public hospital. Specifically, the components of full cost within DRG encompass the knowledge capital of medical workers, sanitary material costs (blood transfusion cost, oxygen usage cost, costs of imaging materials, and costs of laboratory materials), drug costs, depreciation expense of fixed assets, amortization expense of intangible assets, withdrawal of medical risk fund, and other operating expenses (office expenses, utility costs, costs of postage and telecommunications, internet bills, official car operation and maintenance fees and travel expenses, training fees, union funds, and other expenses) (33).

The depreciation expenses of fixed assets and office expenses, salaries of management staff, and utilities and Internet bills that need to be apportioned in disease treatment are shown in Table 7.

Table 7. Calculation table of disease sharing costs.

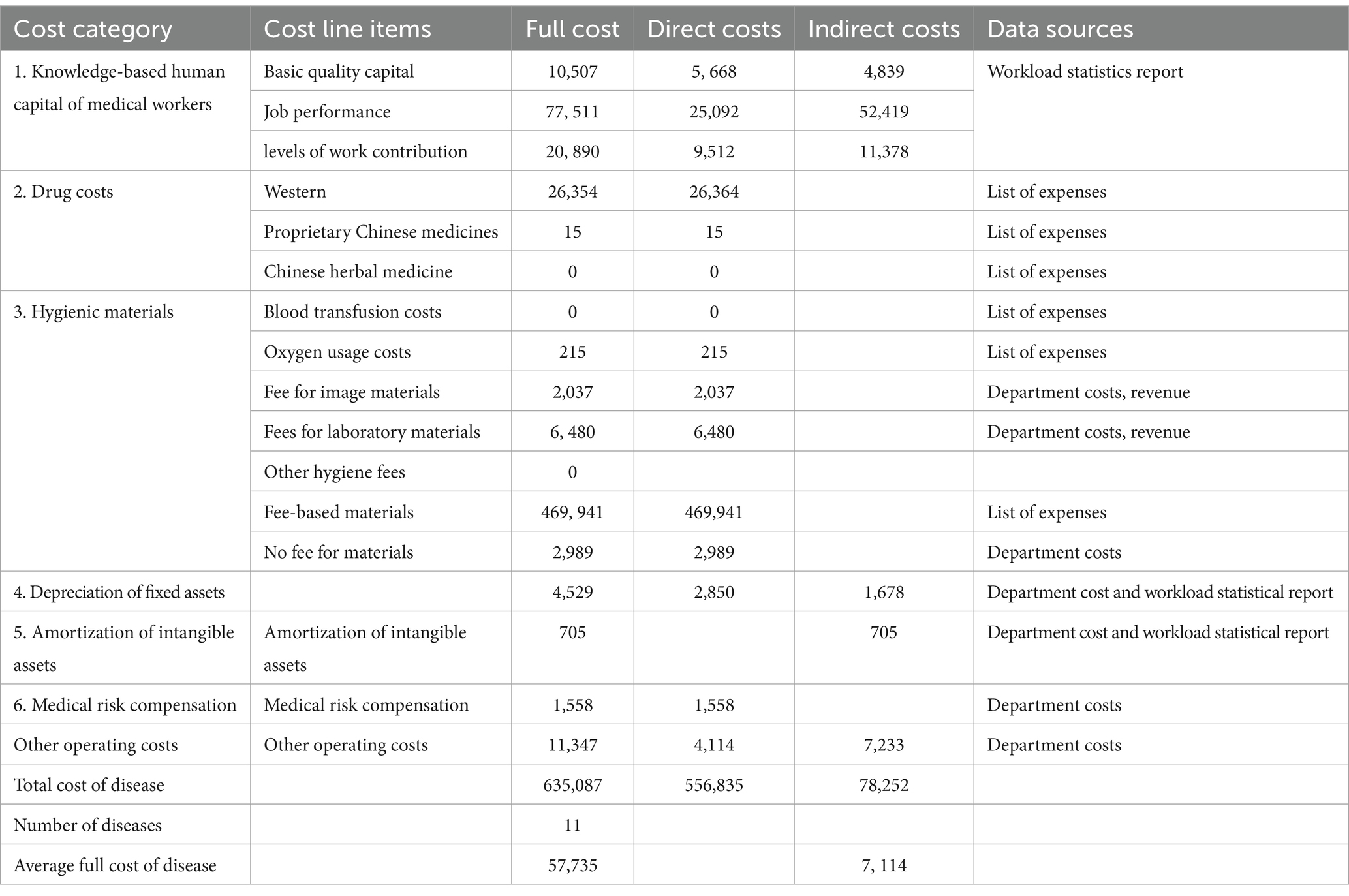

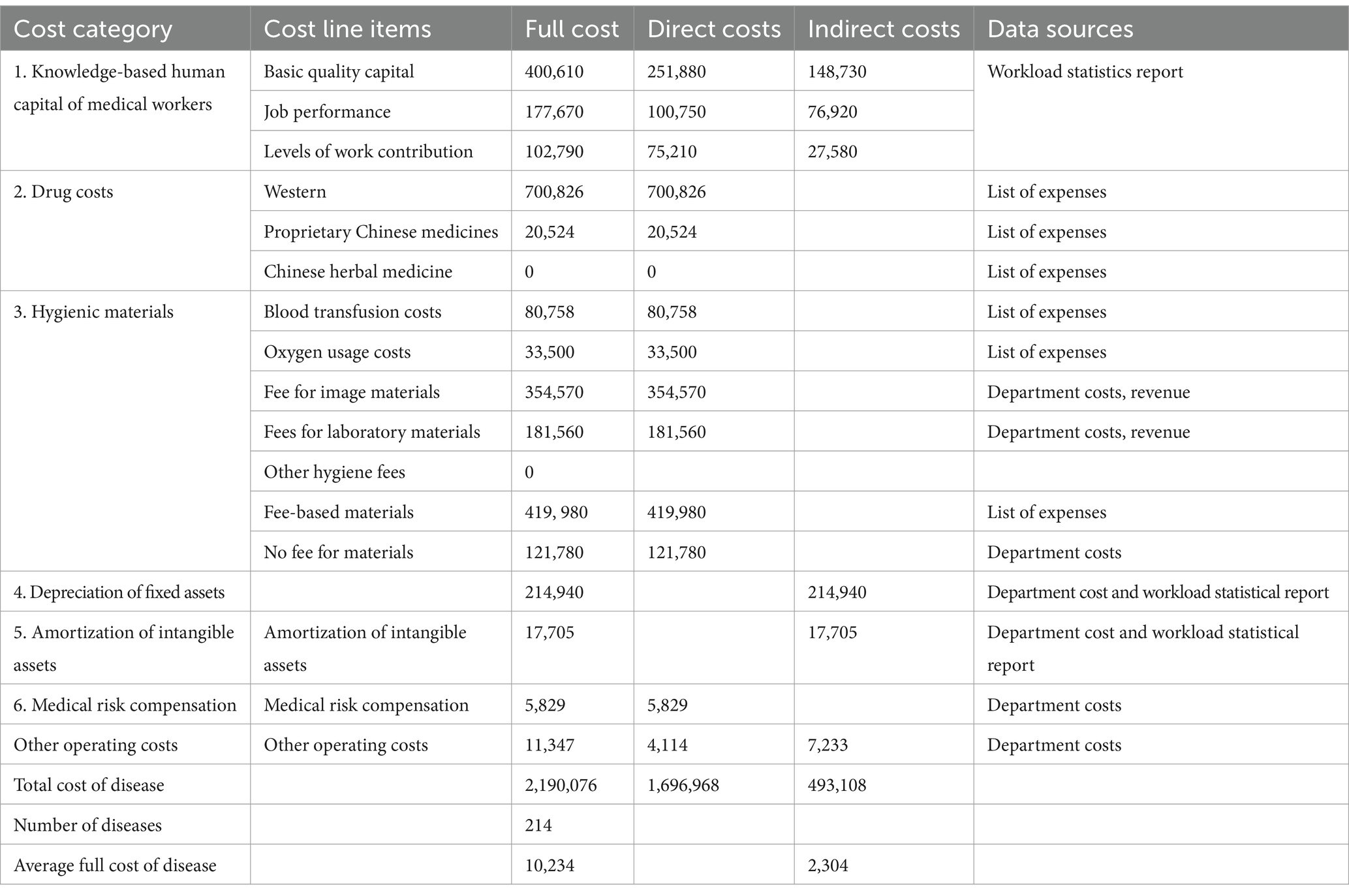

Taking the data from hip replacement, acute simple appendicitis, and heart bypass surgery as examples, the full cost accounting results are shown in Tables 8–10.

Table 8. DRG costing results for “Hip Replacement.”

Table 9. DRG costing results for “acute simple appendicitis.”

Table 10. Cost accounting results of DRG disease “Heart bypass surgery.”

Discussion

In this study, considering the compensation of the value of the intellectual capital of medical workers, the cost of DRG diseases was calculated. This calculation is achieved by considering four primary indicators: technical difficulty, labor intensity, risk degree, and operation time of the disease project. In addition, factors such as the complexity of the operation steps, knowledge requirements, decision-making ability, physical exertion, concentration levels, and the likelihood of potential safety hazards to patients and occupational exposure to medical workers are taken into account. Through the refinement of eight secondary-level indicators related to service item operation time, the study calculates the knowledge capital value compensation for the disease and establishes a comprehensive cost accounting model. This endeavor addresses a longstanding issue in China’s disease cost accounting, which historically neglected the value of medical workers’ knowledge-based capital. The study has successfully redefined the positive incentive mechanism, stimulated endogenous motivation within the medical service system, instigated independent changes in medical behavior, and achieved goals of cost control and rational expenditure. Ultimately, this study provides decision-makers with valuable insights and a viable policy pathway for reforming the implementation of DRG payment systems.

Conclusion

This study establishes a framework for compensating the knowledge capital value in cost accounting of DGR diseases, with the objective of promoting recognition of medical workers’ knowledge capital. The initiative serves a dual purpose: first, it incentivizes medical workers, fostering enthusiasm and creativity in optimizing and standardizing the diagnosis and treatment process; second, acting as a guiding mechanism for values, it addresses existing behaviors among medical workers, such as excessive prescriptions and examinations, thereby reducing disease costs in support of DRG payment reform. Subsequently, hospitals conduct disease cost accounting based on the knowledge value compensation of medical workers, thereby enhancing the transparency and authenticity of DRG pricing; furthermore, this strategy facilitates the monitoring of medical institutions’ inadequacies through DRG cost accounting.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Author contributions

JD: Conceptualization, Data curation, Funding acquisition, Investigation, Methodology, Validation, Visualization, Writing – original draft, Writing – review & editing. FJ: Data curation, Formal analysis, Writing – review & editing. JX: Data curation, Formal analysis, Writing – review & editing. QZ: Conceptualization, Funding acquisition, Writing – review & editing.

Funding

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. This study received funding from the Fujian Province Social Science Planning Project “Policy Research on Promoting High Quality Recycling of Resources from the Perspective of Utility Matching” (FJ2021B035).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

1. Zhu, Y. Practice of cost accounting for DRG disease types in hospitals. Administrative Assets and Finance. (2023) 9:119–21. doi: 10.3969/j.issn.1674-585X.2023.09.042

2. Yang, H. Disease cost calculation and hospital operation management. Chinese Chief Accountant. (2023) 6:117–9. doi: 10.3969/j.issn.1672-576X.2023.06.040

3. Wu, Y. Exploration of disease cost accounting based on department full cost. Chinese Chief Accountant. (2022) 3:112–5. doi: 10.3969/j.issn.1672-576X.2022.03.041

4. Zhu, J, Zhang, Y, and Jin, L. Exploration of cost accounting methods for disease types in public hospitals. China's health industry. (2021) 18:98–101. doi: 10.16659/j.cnki.1672-5654.2021.15.098

5. Yang, J, Deng, Y, and He, J. Comparative study on disease cost accounting methods based on DRG payment model. Bus Econ. (2023) 1:174–6. doi: 10.3969/j.issn.1009-6043.2023.01.051

6. Song, X, and Liu, Y. Comparative study on disease cost accounting methods based on DRGs. Chinese Hospitals. (2020) 24:5–8. doi: 10.19660/j.issn.1671-0592.2020.05.02

7. Song, X. Application of cost to expense ratio method in disease cost accounting. New Accounting. (2019) 8:62–4. doi: 10.3969/j.issn.1674-5434.2019.08.017

8. Chen, Y. Analysis of payment by disease type and cost accounting management. Finance Account Learn. (2021) 9:18–20. doi: 10.3969/j.issn.1673-4734.2021.09.011

9. Huang, J, He, Y, and Di, H. Research on disease cost accounting and management based on service unit superposition method. Chinese Hospitals. (2023) 27:74–7. doi: 10.19660/j.issn.1671-0592.2023.06.20

10. Ileanu, BV, and Tanasoiu, OE. Factors of the earning functions and their influence on the intellectual Capital of an Organization. J App Quantitative Methods. (2008) 4:366–74. doi: 10.1016/j.ydbio.2011.05.504

11. Sun, S. Research on hospital project cost, disease cost, and cost control. Chinese Market. (2019) 7:108–9. doi: 10.13939/j.cnki.zgsc.2019.07.108

12. Chen, J, and Wu, D. Construction of disease cost accounting system based on clinical pathway. Chinese Chief Accountant. (2019) 11:110–1. doi: 10.3969/j.issn.1672-576X.2019.11.050

13. Liu, Y, and Song, X. Research on the application of disease cost accounting method based on cost expense ratio. Chinese Hospitals. (2020) 24:9–12. doi: 10.19660/j.issn.1671-0592.2020.05.03

14. Xu, Z, Qiu, H, and Yao, Y. Research progress and reflection on cost accounting methods for disease types under the background of payment by disease type. Health Soft Sci. (2021) 35:43–6. doi: 10.3969/j.issn.1003-2800.2021.01.011

15. Hou, L. DRGs prepayment system and hospital disease cost analysis. Chinese Chief Accountant. (2018) 9:57–9. doi: 10.3969/j.issn.1672-576X.2018.09.023

16. Huang, A, Chen, J, and Lin, Z. Exploration of cost accounting for hospital disease groups based on DRG. Modern Hospitals. (2022) 22:1893–6. doi: 10.3969/j.issn.1671-332X.2022.12.025

17. Reyes, C, Engel-nitz, N, and Dacosta, B. Cost of disease progression in patients with chronic lymphocytic leukemia, acute myeloid leukemia, and non-Hodgkin's lymphoma. Oncologist. (2019) 24:1219–28. doi: 10.1634/theoncologist.2018-0019

18. Hulme, C. The cost of health care resources in cardiovascular disease. Resuscitation. (2013) 84:865–6. doi: 10.1016/j.resuscitation.2013.04.018

19. Anna, N, Johan, B, and Jan, W. Cost of healthcare utilization associated with incident cardiovascular and renal disease in individuals with type 2 diabetes: a multinational, observational study across 12 countries. Diabetes Obes Metab. (2022) 24:1277–87. doi: 10.1111/dom.14698

20. Wimo, A, Reed, C, Dodel, R, Belger, M, Jones, RW, Happich, M, et al. The GERAS study: a prospective observational study of costs and resource use in community dwellers with Alzheimer's disease in three European countries-study design and baseline findings. J Alzheimer's disease: JAD. (2013) 36:385–99. doi: 10.3233/JAD-122392

21. Bijlmakers, L, Cornelissen, D, Cheelo, M, Nthele, M, Kachimba, J, Broekhuizen, H, et al. The cost of providing and scaling up surgery: a comparison of a district hospital and a referral hospital in Zambia. Health Policy Plan. (2018) 33:1055–64. doi: 10.1093/heapol/czy086

22. Warwick, M, Fernando, SM, Aaron, SD, Rochwerg, B, Tran, A, Thavorn, K, et al. Outcomes and resource utilization among patients admitted to the intensive care unit following acute exacerbation of chronic obstructive pulmonary disease. J Intensive Care Med. (2021) 36:1091–7. doi: 10.1177/0885066620944865

23. Boswell, K, Cameron, H, West, J, Fleming, C, Ibbotson, S, Dawe, R, et al. Narrowband ultraviolet B treatment for psoriasis is highly economical and causes significant savings in cost for topical treatments. Br J Dermatol. (2018) 179:1148–56. doi: 10.1111/bjd.16716

24. Standaert, B, Sauboin, C, Leclerc, QJ, and Connolly, MP. Comparing the analysis and results of a modified social accounting matrix framework with conventional methods of reporting indirect non-medical costs. PharmacoEconomics. (2021) 39:257–69. doi: 10.1007/s40273-020-00978-4

25. Francisci, S, Guzzinati, S, Capodaglio, G, Pierannunzio, D, Mallone, S, Tavilla, A, et al. Patterns of care and cost profiles of women with breast cancer in Italy: EPICOST study based on real world data. Eur J Health Econ. (2020) 21:1003–13. doi: 10.1007/s10198-020-01190-z

26. Tejal, P, and Feng, C. Parkinson's disease guidelines for pharmacists. Canadian pharmacists J: CPJ. (2014) 147:161–70. doi: 10.1177/1715163514529740

27. Mareova, P, and Zahalkova, V. The economic burden of the care and treatment for people with Alzheimer's disease: the outlook for the Czech Republic. Neurol Sci. (2016) 37:1917–22. doi: 10.1007/s10072-016-2679-6

28. Holowachuk, S, Zhang, W, Gandhi, SK, Anis, AH, Potts, JE, and Harris, KC. Cost savings analysis of early Extubation following congenital heart surgery. Pediatr Cardiol. (2019) 40:138–46. doi: 10.1007/s00246-018-1970-0

29. Viljugrein, H, Hopp, P, Benestad, SL, Nilsen, EB, Våge, J, Tavornpanich, S, et al. A method that accounts for differential detectability in mixed samples of long-term infections with applications to the case of chronic wasting disease in cervids. Methods Ecol Evol. (2019) 10:134–45. doi: 10.1111/2041-210X.13088

30. Davidsen, JR, Miedema, J, Wuyts, W, Kilpeläinen, M, Papiris, S, Manali, E, et al. Economic burden and Management of Systemic Sclerosis-Associated Interstitial Lung Disease in 8 European countries: the BUILDup Delphi consensus study. Adv Ther. (2021) 38:521–40. doi: 10.1007/s12325-020-01541-5

31. Gidwani-Marszowski, R, Owens, DK, Lo, J, Goldhaber-Fiebert, JD, Asch, SM, and Barnett, PG. The costs of hepatitis C by liver disease stage: estimates from the veterans health administration. Appl Health Econ Health Policy. (2019) 17:513–21. doi: 10.1007/s40258-019-00468-5

32. Trickey, A, Hiebert, L, Perfect, C, Thomas, C, el Kaim, JL, Vickerman, P, et al. Hepatitis C virus elimination in Indonesia: epidemiological, cost and cost-effectiveness modelling to advance advocacy and strategic planning. Liver Int. (2020) 40:286–97. doi: 10.1111/liv.14232

Keywords: knowledge capital value, cost accounting, diagnosis related groups, medical workers, analytic hierarchy process

Citation: Duan J, Jiao F, Xi J and Zhang Q (2024) Based on knowledge capital value for disease cost accounting of diagnosis related groups. Front. Public Health. 12:1269704. doi: 10.3389/fpubh.2024.1269704

Edited by:

Georgios Tagarakis, Aristotle University of Thessaloniki, GreeceReviewed by:

Sokratis Tsagkaropoulos, University General Hospital of Thessaloniki AHEPA, GreeceFani Tsolaki, Aristotle University of Thessaloniki, Greece

Copyright © 2024 Duan, Jiao, Xi and Zhang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Jinli Duan, NzgzMDg3NzZAcXEuY29t; Qichun Zhang, MjM1NzU1OTdAcXEuY29t