95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Public Health , 01 July 2022

Sec. Health Economics

Volume 10 - 2022 | https://doi.org/10.3389/fpubh.2022.948964

Wenling Xiao1

Wenling Xiao1 Ran Tao2*

Ran Tao2*Asian countries have shown remarkable progress in financial inclusion and have become the world's fastest-growing regions. However, the financial inclusion-human health nexus has not received much attention. This study contributes to the empirical literature by examining the effect of financial inclusion on population health using panel data from Asian countries from 2007 to 2019. Population health is measured by death rate and life expectancy at birth. Our study finding shows that digital financial inclusion increases life expectancy but decreases the death rate in Asia. At the same time, financial inclusion positively impacts life expectancy and has a negative impact on the death rate in Asia. Finding also suggests that Internet users, GDP, and FDI have improved population health by increasing life expectancy and decreasing the death rate. The results suggest some essential policy implications.

Financial inclusion provides affordable, accessible, and beneficial products and financial services to individuals and businesses responsibly and sustainably (1, 2). Financial development denotes improvement in the size, stability, and efficiency of the financial system. While financial inclusion denotes those individuals and businesses are able to fulfill their requirements due to accessibility to affordable financial services and products (3). Recently, efforts to promote financial inclusion have enlarged. Financial inclusion is considered the fundamental tool that can be used to obtain social and economic development, especially in vulnerable societies (4). World Bank (1) declared financial inclusion as enabling most Sustainable Development Goals (SDGs). Access to finance simplifies daily activities and planning for long-term goals and emergencies for families and businesses.

United Nations Capital Development Fund (UNCDF) implies that financial account holders can access credit easily, enlarge and retain their businesses, invest in education and health, and handle financial shocks that enhance livelihoods' sustainability (5). Financial inclusion directly influences the health of people (6). Due to the occurrence of highly unpredictable diseases, financial inclusion can support individuals in bearing these treatment expenses through savings that lead to better health outcomes (7, 8). Furthermore, financial inclusion helps people afford better quality health inputs, such as a nutritious diet, clean energy, and improved sanitation (9). Besides these, financial inclusion reduces mental stress by providing financial stability that could end up in good quality health outcomes (10, 11). Various studies have explored the impact of financial inclusion on social and economic indicators (12–14), and very few studies have explored the impact of financial inclusion on human health (15, 16). Literature discloses that high mortality is considered a measure representing the bad quality of human health, and enlarged life expectancy is a measure of good quality of human health.

As far as the theoretical aspect of financial inclusion is concerned, literature provides two theories regarding financial inclusion: the vulnerable group theory and the public goods theory of financial inclusion (17). The vulnerable group theory implies that financial inclusion should consider a vulnerable population of society, including the poor, younger, older, and women (6). In contrast, the public goods theory claims that financial inclusion should be accessible to the whole society and no one should be left excluded (18). However, the theory of capability implies that financial inclusion enlarges the freedom of people in making choices for essential necessities such as good quality healthcare, education, clean water, and sanitation facilities that improve the health outcomes of people (19).

As long as the empirical aspect of the nexus between financial inclusion and health is concerned, Claessens and Feijen (20) found that credit to the private sector is positively linked with human health. In the case of South Africa, Sarma & Pais (21) found a strong association between financial development and life expectancy. Their study measures financial development by domestic credit as a percent of GDP, M3 as a percent of GDP, and domestic credit to the private sector as a percent of GDP (22). In the case of OECD economies, Gunakar (23) found that financial development enhances health outcomes by increasing the extent of life expectancy and reducing the rate of infant mortality. Financial development in this study is measured by liquid liabilities as a percent of GDP, credit to the private sector as a percent of GDP, and market capitalization as a percent of GDP (24). In the case of African economies, Chireshe (25) found that financial development increases life expectancy and reduces the child mortality rate. Gyasi et al. (15) explored the impact of financial inclusion on adult health in the case of Ghana. It is reported that financial inclusion is positively related to the health outcomes of adults (26). However, despite much effort, we cannot find any study exploring the impact of financial inclusion on human health in the case of Asian economies (27). This study provides us answer to the following question: Does financial inclusion lead to better health outcomes? To our knowledge, this is the first study of its kind that determines the nexus between financial inclusion and health outcomes (18).

Given this lacuna of existing literature, our study investigates the impact of financial inclusion on public health in the case of selected Asian economies. The sample of the study is selected based on data availability (28). Our study will make contributions to the existing literature in the following manners. Firstly, to the best of the authors' knowledge, this study is the first one exploring the nexus between financial inclusion and public health in the case of the Asian region. Secondly, the study will use 2 SLS and GMM approaches to explore this nexus from 2007 to 2019 (29). Thirdly, this is the first-ever study in the Asian region covering proxy health measures such as life expectancy and death rate. Lastly, most previous studies measure financial development through domestic credit to the private sector as a percent of GDP (26). However, our study measures financial inclusion using two proxy measures, namely ATMs and debit cards. This study tries to deal with the endogeneity issues and perform sensitivity analysis to check the robustness of the outcomes. The findings of the study will support policymakers in designing such policies that ease the involvement of individuals in financial activities to protect their health outcomes.

In recent years, financial inclusion has been supposed as a dynamic tool for attaining human development in advanced and developing countries (30). Financial inclusion also improves macroeconomic stability and inclusive economic growth (2). Our study is based on the vulnerable group theory (17). Theoretical developments have argued that financial inclusion improves human development. As such, we employ the following economic model that follows (31):

where is the population health (Healthit) that depend on financial inclusion (FI), internet users (Internet), health expenditure (HE), GDP growth (GDP), and foreign direct investment (FDI). Where λi refers to unobserved individual-country and εit is the error term. However, i(t) represents the country (year), and the remaining ηs are coefficients of the concerned explanatory variables. Financial inclusion can significantly improve human health outcomes. Thus, we expect an estimate of d to be positive. Following the research work of Immurana et al. (32), the control variables included in the health model include internet users, health expenditure, GDP growth, and FDI. The remaining explanatory variables have a favorable impact on population health; thus, estimates of η2, η3, η4, and η5 are expected to be positive. We estimate model (1) using the two-stage least squares (2 SLS) technique. This method is best suited because it can easily address the problem of endogeneity. The main sources of endogeneity are measurement errors, omitted variable bias, and reverse causality. These issues arise for different reasons; however, they can overcome the problem using instrumental variables. For estimation, this study employs the 2 SLS estimators to estimate the baseline outcomes. In our model, financial inclusion is a potential endogenous variable. The augmented panel model is:

while Healthit−1 is the first lag of health outcomes in equation (2), which is a dynamic term in the panel model. We estimate model (2) using the Blundell & Bond (33) system GMM technique. The system GMM approach has been used in many previous empirical health-related studies (32). Following Immurana et al. (31, 34), we use the dynamic panel-data model (2). This econometric specification is widely used in the empirical finance literature to examine the nexus between financial inclusion and human development. This approach is suitable as the number of countries (N = 18) is more than the number of years (T = 13), as in our study. Few diagnostics tests, such as the serial correlation test and the Sargan test statistic—are also used to demonstrate the validity of estimates.

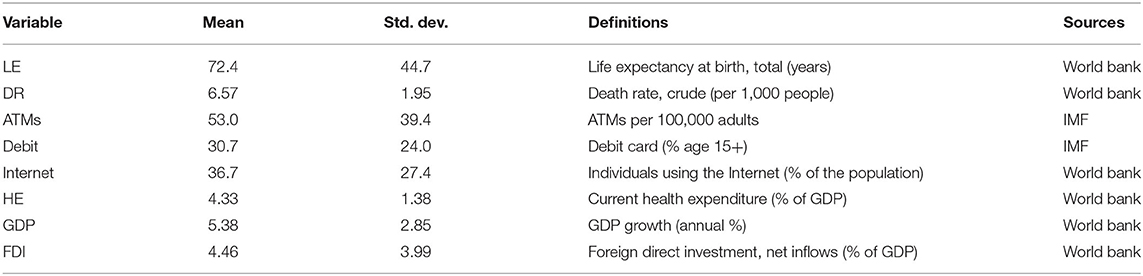

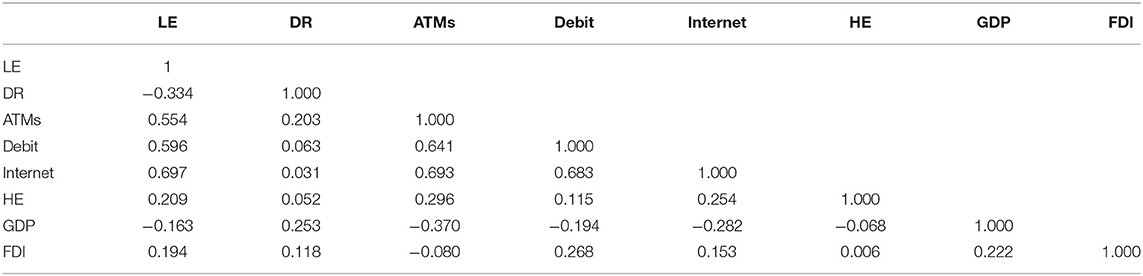

Table 1 displays the details of descriptive statistics of variables, definitions and symbols of variables, and sources of data series. The list of selected Asian countries is reported in Table 2. Asian Health in this study is measured by two indicators such as life expectancy and death rate. Two indicators also measure financial inclusion: ATMs per 1,000 adults and debit cards (% age 15+). Previous studies have used the same variables for financial inclusion (2, 35). The role of internet use, health expenditures, foreign direct investment, and GDP growth have been added as control variables. Internet use is measured as internet users in the percentage of the population. Health expenditures are measured as a percentage of GDP. GDP growth is taken in annual percentage. Net inflows determine FDI as a percent of GDP. The data for financial inclusion indicators have been taken from IMF, while the data for the remaining variables have been collected from the World Bank. Table 2 shows that the mean (standard deviation) for life expectancy is 72.4 (44.7), the death rate is 6.57 (1.95), ATMs is 53.0 (39.4), a debit card is 30.7 (24.0), the internet user is 36.7 (27.4), health expenditure is 4.33 (1.38), GDP growth is 5.38 (2.85), and FDI is 4.46 (3.99). While Table 3 shows that the correlation matrix and findings is free from multicollinearity problem.

Table 1. Descriptive statistics and definitions.

Table 2. List of countries.

Table 3. Matrix of correlations.

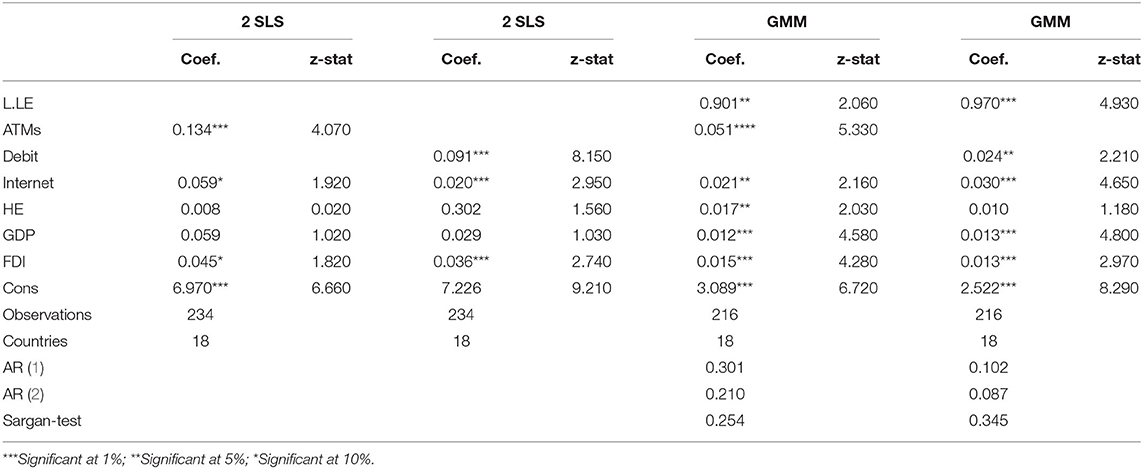

Table 4 reports the results of 2 SLS and GMM estimates for life expectancy models. It is found that ATMs and life expectancy are significantly and positively associated in both 2 SLS and GMM models. It reveals that a 1 percent upsurge in the number of ATMs improves life expectancy by 0.134 percent in the 2 SLS model and 0.051 percent in the GMM model. The findings further reveal that debit card and life expectancy are also significantly and positively associated in both 2 SLS and GMM models. It implies that a 1 percent upsurge in the number of credit cards improves life expectancy by 0.091 percent in the 2 SLS model and 0.024 percent in the GMM model. Hence, it is confirmed that both financial inclusion indicators contribute significantly to enhancing population health in selected 18 Asian economies. This finding is supported by Immurana (32), who noted that financial inclusion enhances health in Africa. This finding infers that digital financial inclusion easy financial services, enabling people to acquire health-related goods and services. This means that financial services boost human health. This finding is also backed by Ofosu-Mensah Ababio et al. (34), who reported that financial inclusion is an effective tool for achieving socio-economic development by reducing poverty and income inequality. The findings validate the study of Churchill et al. (36) that shows that financial inclusion has a strong poverty-reducing effect, improving population health. Another possible reason is that financial inclusion improves human health via income channels. Financial inclusion prompts the human development process in Asian economies. Findings infer that a well-performing digital financial system is an important factor in human development.

Table 4. Financial inclusion and life expectancy (2 SLS & GMM).

The impact of internet use on life expectancy is found to be significant and positive on life expectancy in all four models, displaying that the use of the internet tends to improve human health in the sample of selected Asian economies. This result is in line with Majeed & Khan (37), who found that internet development improves population health by increasing financial and health literacy, spreading health information, and health care services. This finding is also supported by Mushtaq & Bruneau (38), who noted that the composite impact of internet development and financial inclusion is an important factor for human development. The findings display that the nexus between health expenditures and life expectancy is significantly positive only in one model, confirming that current health expenditures are capable to improve health outcomes in Asian economies. The GDP and life expectancy association is found significantly positive in both GMM models, showing that an upsurge in GDP improves public health in Asian economies. Ordinarily, economic progress is found to improve human health by increasing positive externalities. For instance, Woodward et al. (39) found economic development to boost human health. The impact of FDI on life expectancy is found to be significantly positive in all four models confirming that FDI plays a prominent role in improving people's health in Asian economies. Thus, it is confirmed that financial inclusion, internet use, GDP, and FDI are significant indicators of human health in the case of Asian economies. Both GMM models are correctly specified, as confirmed by a statistically insignificant coefficient estimate of the Sargan test.

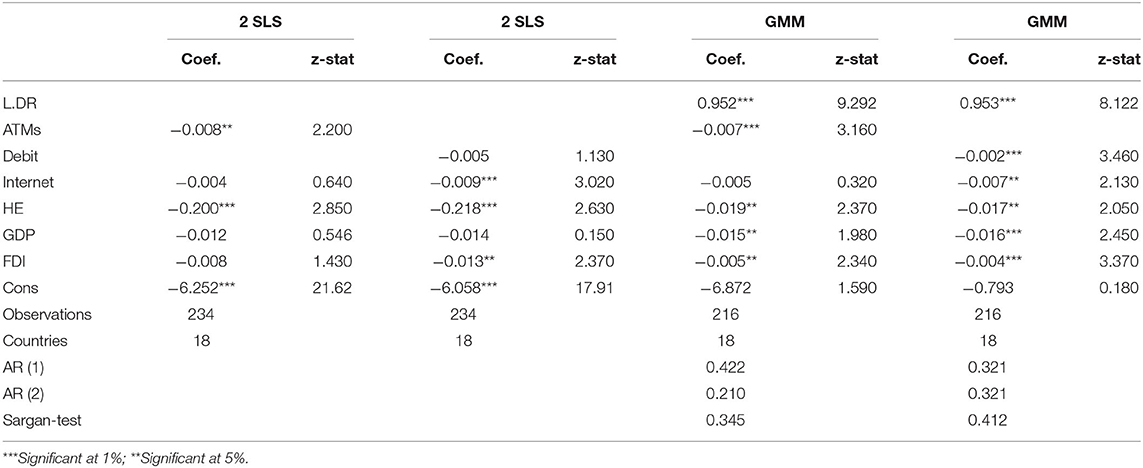

Table 5 reports the results of 2 SLS and GMM estimates for death rate models. It is reported that ATMs and death rates are significantly and negatively associated in both 2 SLS and GMM models. It implies that a 1 percent upsurge in ATMs users reduces the death rate by 0.008 percent in the 2 SLS model and 0.007 percent in the GMM model. The findings display that debit card and death rate are associated significantly and negatively in the GMM model only, while the association is found statistically insignificant in the case of the 2 SLS model. It displays that a 1 percent rise in the number of credit cards reduces the death rate by 0.002 percent in the GMM model. Thus, the findings of both 2 SLS and GMM models confirmed that both determinants of financial inclusion, ATMs and credit card, play a significant role in improving population health in Asian economies. The nexus between internet use and the death rate is found significant and negative in the case of two models, revealing that internet use plays a prominent role in improving human health in selected Asian economies. The nexus between health expenditures and the death rate is found significant and negative in all four models, displaying that current health expenditures play a fundamental role in improving population health in Asian economies. The nexus between GDP and death rate is significantly negative in the case of both GMM models, displaying that increase in GDP significantly improves public health in selected Asian economies. The association between FDI and death rate is significantly negative in the case of three models, inferring that FDI plays a key role in the improvement of population health in the case of Asian economies. Similar to the life expectancy model, financial inclusion, internet use, GDP, and FDI are significant determinants of human health in the sample of selected 18 Asian economies. The statistically insignificant coefficient estimate of the Sargan test confirms that both GMM models are correctly specified.

Table 5. Financial inclusion and death rate (2 SLS & GMM).

In this study, an effort is made to explore the nexus between financial inclusion and population health in the case of selected Asian economies over the time span of 1995–2020. Financial inclusion is measured through ATMs and debit cards in this study, while health is measured through death rate and life expectancy. For estimation purposes, the 2 SLS and GMM methods have been used. The obtained results are as follows. Both ATMs and credit cards positively affect population health, revealing that financial inclusion enhances population health in Asian economies. Other control variables such as GDP, current health expenditures, FDI, and internet use positively influence human health as described in most cases.

Thus, the study put forward some important policy implications for policymakers, stakeholders, and governments of Asian economies. It is suggested that the enlargement of financial inclusion should be the responsibility of governments, stakeholders, potential customers, service providers, financial supervisors, financial regulators, and development agencies. The promotion of financial inclusion should be embarked by the whole banking sector to further improves human health. New savings or deposit methods through branchless avenues and technological methods must be encouraged to support customers in accessing and depositing money. The governments should start initiatives that provide financial education and training to individuals about using branchless and digital avenues. Another suggestion is that there should be strong collaborations and linkages among financial service providers, financial regulations, and governments. The restrictions on inflows of FDI should be relaxed. Governments should establish strong regulatory and law enforcement organizations. Remote and backward areas should be modernized by establishing improved physical infrastructures such as telecommunication, electricity, and paved roads that provide mental peace to people, thus improving their health and livelihood. The stakeholders and governments should struggle to guarantee financial inclusion services to individuals from both supply and demand sides to enhance the health and wellbeing of people in Asian economies.

Besides these implications, the study also faces some limitations that must be considered in future studies. For instance, the study has used only two indicators to measure human health; however, there are several other health indicators that must be considered in future research, such as mental health, other chronic diseases, and maternal health. Our study is limited to the Asian region and adopts a linear method of estimation to explore the nexus between financial inclusion and human health. However, future studies can adopt non-linear methods of estimation to get more interesting results. Furthermore, future studies can also replicate these analyses for other regions and economies.

Publicly available datasets were analyzed in this study. This data can be found here: https://data.worldbank.org/.

WX: conceptualization, software, data curation, and writing—original draft preparation. RT: methodology and writing—reviewing and editing. WX and RT: visualization and investigation. Both authors contributed to the article and approved the submitted version.

This study was supported by High-level Talent Introduction Research Project of Shandong Women's University (Grant No. 2021RCYJ03) and Cultivation Fund for High-level Scientific Research Projects of Shandong Women's University (Grant No. 2021GSPSJ05).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1. Bank W. Poverty and Shared Prosperity 2018: Piecing Together the Poverty Puzzle. Northwest Washington, DC: The World Bank (2018).

2. Liu D, Zhang Y, Hafeez M, Ullah S. Financial inclusion and its influence on economic-environmental performance: demand and supply perspectives. Environ Sci Pollut Res. (2022) 1–10. doi: 10.1007/s11356-022-18856-1

3. Siddik M, Alam N, Kabiraj S. Digital Finance for Financial Inclusion and Inclusive Growth. Digital Transformation in Business and Society. Cham: Springer (2020). p. 155–168.

4. Niaz MU. Socio-Economic development and sustainable development goals: a roadmap from vulnerability to sustainability through financial inclusion. Econ Res-Ekon IstraŽivanja. (2021) 1–33. doi: 10.1080/1331677X.2021.1989319

5. Ajefu JB, Demir A, Haghpanahan H. The impact of financial inclusion on mental health. SSM Popul Health. (2020) 11:100630. doi: 10.1016/j.ssmph.2020.100630

6. Su C-W, Xi Y, Umar M, Oana-Ramona L. Does technological innovation bring destruction or creation to the labor market? Technol Soc. (2022) 101905. doi: 10.1016/j.techsoc.2022.101905

7. Lashitew AA, van Tulder R, Liasse Y. Mobile phones for financial inclusion: what explains the diffusion of mobile money innovations? Res Policy. (2019) 48:1201–15. doi: 10.1016/j.respol.2018.12.010

8. Pazarbasioglu C, Mora AG, Uttamchandani M, Natarajan H, Feyen E, Saal M. Digital financial services. World Bank Group. (2020) 54. Available online at: https://pubdocs.worldbank.org/en/230281588169110691/Digital-Financial-Services.pdf

9. Wang Q-S, Su C-W, Hua Y-F, Umar M. How can new energy vehicles affect air quality in China?—From the perspective of crude oil price. Energy Environ. (2021) 0958305X211044388. doi: 10.1177/0958305X211044388

10. Patwardhan A. Financial Inclusion in the Digital Age. Handbook of Blockchain, Digital Finance, and Inclusion, Volume 1. Singapore: Elsevier (2018). p. 57–89.

11. Chen J, Rojniruttikul N, Kun LY, Ullah S. Management of green economic infrastructure and environmental sustainability in one belt and road enitiative economies. Environ Sci Pollut Res. (2022) 29:1–11. doi: 10.21203/rs.3.rs-811001/v1

12. Koomson I, Villano RA, Hadley D. Effect of financial inclusion on poverty and vulnerability to poverty: evidence using a multidimensional measure of financial inclusion. Soc Indic Res. (2020) 149:613–39. doi: 10.1007/s11205-019-02263-0

13. Polloni-Silva E, da Costa N, Moralles HF, Sacomano Neto M. Does financial inclusion diminish poverty and inequality? A panel data analysis for Latin American countries. Soc Indic Res. (2021) 158:889–925. doi: 10.1007/s11205-021-02730-7

14. Dar SS, Sahu S. The effect of language on financial inclusion. Econ Model. (2022) 106:105693. doi: 10.1016/j.econmod.2021.105693

15. Gyasi RM, Adam AM, Phillips DR. Financial inclusion, health-Seeking behavior, and health outcomes among older adults in Ghana. Res Aging. (2019) 41:794–820. doi: 10.1177/0164027519846604

16. Matekenya W, Moyo C, Jeke L. Financial inclusion and human development: evidence from Sub-Saharan Africa. Dev South Afr. (2021) 38:683–700. doi: 10.1080/0376835X.2020.1799760

17. Ozili PK. Theories of Financial Inclusion. Uncertainty and Challenges in Contemporary Economic Behaviour. Munich: Emerald Publishing Limited (2020).

18. Su C-W, Li W, Umar M, Lobont O-R. Can green credit reduce the emissions of pollutants? Econ Anal Policy. (2022) 74:205–19. doi: 10.1016/j.eap.2022.01.016

19. Alkire S, Deneulin S. Introducing the human development and capability approach. Introd Hum Dev Capab Approach Lond Earthscan. (2009). doi: 10.4324/9781849770026

20. Claessens S, Feijen E. Finance and Hunger: Empirical Evidence of the Agricultural Productivity Channel. Holland, MI: World Bank Publications (2006).

21. Sarma M, Pais J. Financial inclusion and development. J Int Dev. (2011) 23:613–28. doi: 10.1002/jid.1698

22. Usman A, Ozturk I, Hassan A, Zafar SM, Ullah S. The effect of ICT on energy consumption and economic growth in South Asian economies: an empirical analysis. Telemat Inform. (2021) 58:101537. doi: 10.1016/j.tele.2020.101537

23. Bhatta G. Financial Development Health Capital Accumulation (2018). Available online at: https://digitalcommons.wayne.edu/cgi/viewcontent.cgi?article=1637&context=oa_dissertations

24. Su C-W, Pang L, Umar M, Lobont O-R. Will gold always shine amid world uncertainty? Emerg Mark Finance Trade. (2022) 1–14. doi: 10.1080/1540496X.2022.2050462

25. Chireshe J. Finance and renewable energy development nexus: evidence from Sub-Saharan Africa. Int J Energy Econ Policy. (2021) 11:318. doi: 10.32479/ijeep.10417

26. Umar M, Farid S, Naeem MA. Time-frequency connectedness among clean-energy stocks and fossil fuel markets: comparison between financial, oil and pandemic crisis. Energy. (2022) 240:122702. doi: 10.1016/j.energy.2021.122702

27. Hao L-N, Umar M, Khan Z, Ali W. Green growth and low carbon emission in G7 countries: how critical the network of environmental taxes, renewable energy and human capital is? Sci Total Environ. (2021) 752:141853. doi: 10.1016/j.scitotenv.2020.141853

28. Su C-W, Yuan X, Tao R, Umar M. Can new energy vehicles help to achieve carbon neutrality targets? J Environ Manage. (2021) 297:113348. doi: 10.1016/j.jenvman.2021.113348

29. Yu B, Li C, Mirza N, Umar M. Forecasting credit ratings of decarbonized firms: comparative assessment of machine learning models. Technol Forecast Soc Change. (2022) 174:121255. doi: 10.1016/j.techfore.2021.121255

30. Li L. Financial inclusion and poverty: the role of relative income. China Econ Rev. (2018) 52:165–91. doi: 10.1016/j.chieco.2018.07.006

31. Immurana M. Does population health influence FDI inflows into Ghana? Int J Soc Econom. (2021) 48:334–47. doi: 10.1108/IJSE-05-2020-0288

32. Immurana M. How does FDI influence health outcomes in Africa? Afr J Sci Technol Innov Dev. (2021) 13:583–93. doi: 10.1080/20421338.2020.1772952

33. Blundell R, Bond S. Initial conditions and moment restrictions in dynamic panel data models. J Econom. (1998) 87:115–43. doi: 10.1016/S0304-4076(98)00009-8

34. Ofosu-Mensah Ababio J, Attah-Botchwey E, Osei-Assibey E, Barnor C. Financial inclusion and human development in frontier countries. Int J Finance Econ. (2021) 26:42–59. doi: 10.1002/ijfe.1775

35. Jing R, Ma Y, Zhang L, Hafeez M. Does financial technology improve health in Asian economies? Front Public Health. (2022) 107:1–8. doi: 10.3389/fpubh.2022.843379

36. Churchill SA, Marisetty VB. Financial inclusion and poverty: a tale of forty-five thousand households. Appl Econ. (2020) 52:1777–88. doi: 10.1080/00036846.2019.1678732

37. Majeed MT, Khan FN. Do information and communication technologies (ICTs) contribute to health outcomes? An empirical analysis. Qual Quant. (2019) 53:183–206. doi: 10.1007/s11135-018-0741-6

38. Mushtaq R, Bruneau C. Microfinance, financial inclusion and ICT: implications for poverty and inequality. Technol Soc. (2019) 59:101154. doi: 10.1016/j.techsoc.2019.101154

Keywords: human health, financial inclusion, FDI, GDP, Asian

Citation: Xiao W and Tao R (2022) Financial Inclusion and Its Impact on Health: Empirical Evidence From Asia. Front. Public Health 10:948964. doi: 10.3389/fpubh.2022.948964

Received: 20 May 2022; Accepted: 06 June 2022;

Published: 01 July 2022.

Edited by:

Chi Wei Su, Qingdao University, ChinaReviewed by:

Meng Qin, Central Party School of the Communist Party of China, ChinaCopyright © 2022 Xiao and Tao. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Ran Tao, dGFvdGFvMDIxMkAxNjMuY29t

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.