Jing Shao

Jing Shao Zhiwei He

Zhiwei He

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Ecol. Evol. , 04 August 2022

Sec. Environmental Informatics and Remote Sensing

Volume 10 - 2022 | https://doi.org/10.3389/fevo.2022.971077

This article is part of the Research Topic Social Media, Artificial Intelligence and Carbon Neutrality View all 10 articles

As public concern over global warming increases, there is a growing requirement for companies, as carbon emitters, to disclose (and work to reduce) their carbon emissions. Previous literature has neglected the role of social media as a source of legitimacy pressure to influence corporate carbon disclosure. Based on legitimacy theory, this study analyzed the impact of social media legitimacy pressure on corporate carbon disclosure using data from 3,656 Chinese listed companies from 2009 to 2019. We found that social media legitimacy pressure significantly enhances corporate carbon disclosure. Additionally, this positive relationship is weakened by substantive corporate internal carbon management measures (corporate green innovation and environmental management systems). Accordingly, in order to ensure consistent carbon management practices, companies should focus their efforts on substantive carbon management measures along with carbon disclosure.

Greenhouse gases are the leading cause of global climate change (Depoers et al., 2016), and reducing emissions is the primary way to address global warming and is the consensus of most countries. Either the Kyoto Protocol or the Paris Agreement encourages countries to reduce greenhouse gas emissions. Generally, businesses are a major source of greenhouse gas emissions, with nearly 90% of carbon dioxide emissions coming from production and operation activities. Therefore, transparent and objective disclosure of carbon information by enterprises is crucial for scientific emission reduction and establishing a carbon trading market. The level of carbon disclosure has improved in recent years; however, companies still have considerable discretion regarding whether, what, and how much carbon information they disclose as corporate carbon disclosure remains voluntary in the majority of countries around the world (He et al., 2022). Numerous researchers have expressed concerns about the quality of corporate carbon disclosure (Stanny, 2018), and some studies have even found no significant improvement in the quality of carbon disclosure (Comyns and Figge, 2015). How to improve the quality of corporate carbon information disclosure has become an essential stakeholder concern. With the development of internet technology and the advent of the digital economy, the monitoring and pressure facing companies have become more dynamic and complex. The social media created by the mobile internet is likely to become a vital information medium for people to monitor the activities of companies. It reduces the cost of monitoring by stakeholders and helps to establish a practical regulatory framework to improve the transparency of carbon information disclosure.

Existing literature on the determinants and motivations of carbon disclosure can be categorized into external pressures and internal characteristics. External pressures include environmental regulations, regulatory, economic, business, and financial market pressures [see reviews in Borghei (2021) and He et al. (2022)]. Internal characteristics of firms include corporate governance structures (e.g., board characteristics, management shareholding), financial characteristics (e.g., profitability, leverage, opportunities to increase), and managers’ attitudes and philosophies toward environmental protection [see reviews in Borghei (2021) and He et al. (2022)]. Regardless of the findings on carbon disclosure, social media has not been adequately discussed as an essential source of information and external pressure. The current research on social media and carbon information has focused on its impact on capital markets. For example, Albarrak et al. (2019) found that posting carbon information on Twitter reduced firms’ cost of equity. In contrast, the role of traditional media in corporate carbon disclosure is well understood, similar to that of social media (Guenther et al., 2016; Li L. et al., 2017; Li et al., 2018), but research has been limited to large companies or companies in heavily polluting industries. Contrary to social media, traditional media is “controlled by and for the elite” and may limit or control access to stakeholders. Companies are also adept at using traditional media to shape their reputations and public relations. As a result, stakeholders are limited in conveying their legitimate pressures through traditional media (Lyon and Montgomery, 2013). Social media provide a more accessible platform for stakeholders where content can be fully controlled, stakeholders can communicate, and a network effect of information can be created (Lyon and Montgomery, 2013), thus accelerating the dissemination of information and alleviating information asymmetries (Blankespoor et al., 2014). Given the unique attributes of social media, it is necessary to explore whether social media as an information medium can effectively monitor corporate carbon disclosure.

To address this issue, in this study, we highlighted the monitoring role of social media, arguing that the legitimacy pressure generated by social media comments is a crucial driver of corporate carbon reduction and disclosure. Social media has provided stakeholders with a forum to voice their concerns, which are widely discussed and quickly disseminated on social media platforms (Miller and Skinner, 2015), especially negative comments (Zhang and Yang, 2021). As a result of social media legitimacy pressures, corporate carbon disclosure serves as an effective tool to respond to stakeholders’ environmental demands and compensate for legitimacy deficits (Lee et al., 2016).

Furthermore, as carbon disclosure laws, regulations, and regulatory mechanisms are still insufficient, companies may manipulate corporate carbon disclosure (Li L. et al., 2017). Carbon disclosure is more of a symbolic response (Cho and Patten, 2007; Hrasky, 2012) when negative social media comments threaten companies’ legitimacy status (most companies’ carbon disclosure is insufficient). Therefore, it is necessary for companies to undertake substantial carbon management measures to close the expectation gap between stakeholders and managers and to avoid decoupling in carbon management measures (Herold and Lee, 2019). The implementation of environmental management systems (EMS), as well as the development of green technologies, are effective and substantive carbon management measures for companies. Substantial carbon management measures not only improve carbon performance but also prevent companies from being negatively impacted by social media legitimacy pressure.

To test our hypothesis, we examined the impact of social media legitimacy pressure on corporate carbon disclosure using data from 2009 to 2019 on stock forum comments on the Chinese Eastmoney website. This stock forum is China’s most popular and influential financial website for investors. Each listed company has its own forum where investors can post and exchange information as well as offer views on that company (Fan et al., 2021). We find strong evidence that social media legitimacy pressure significantly impacts corporate carbon disclosure. First, it has been shown that social media legitimacy pressures result in companies increasing carbon disclosure, with negative social media comments being the primary source of legitimacy pressures. Second, we observed that the positive relationship between social media legitimacy pressure and corporate carbon disclosure is weakened when firms have excellent green innovation levels and corporate EMS. Third, the legitimacy pressure conveyed by social media also impacts the structure of corporate carbon disclosure, with companies preferring to disclose non-financial carbon information over financial carbon information. In fact, disclosing non-financial carbon information can serve as a symbolic carbon management measure for companies.

There are three main contributions we have tried to make. First, we highlighted the critical role of social media legitimacy pressures in corporate carbon disclosure. It differs from previous studies that have examined the influence of mass media or government regulation on corporate carbon disclosure. Social media, especially in the modern age of intelligence, have a broader stakeholder base and stronger network information effect. Hence, they are superior at conveying legitimacy pressures. Second, we explored the relationship between corporate carbon disclosure and substantive carbon management measures in this study. We found that corporate carbon disclosure is primarily a symbolic carbon management measure for companies, while corporate green innovation and EMS serve as substantive carbon management measures that can reduce corporate social media legitimacy pressure to meet stakeholder regulatory requirements. Third, this study showed that social media could also be a powerful source of legitimacy pressure for businesses, which can affect companies to improve carbon information disclosure. Detailed evidence and insights on carbon information disclosure are provided to policymakers so they can improve the regulatory framework and develop policies or regulations.

Legitimacy has been widely recognized as an essential factor in corporate information disclosure (Li et al., 2018; Zhang and Yang, 2021). In accordance with previous research, we also analyze the impact of legitimacy pressure from social media on corporate carbon disclosure using legitimacy theory. Suchman (1995) defines corporate legitimacy as the general perception that corporate behavior is considered desirable, appropriate and rational within a socially constructed system of norms, values, beliefs and definitions. A “social contract” between business and society is the basis of legitimacy (Deegan and Deegan, 2007), and this contract is dynamic rather than fixed (Deegan and Blomquist, 2006). An organization’s legitimacy is the most valuable capital, allowing it to access the resources allocated by its stakeholders, gaining a competitive advantage, and increasing its long-term value. In China, under a regime of authoritarianism, it is even more important. Legitimacy theory suggests that firms should operate within social values; otherwise, they may breach the implicit contract between them and society (Cho and Patten, 2007), undermining their legitimacy (Luo, 2019). Stakeholders are ultimately responsible for determining the legitimacy of a business, and their views are reflected in the legitimization process. There is no doubt that social media plays an indispensable role in the process of public understanding and judging a business, as well as forming an evaluation of its legitimacy. Thus, legitimacy theory provides an appropriate framework for explaining corporate carbon disclosure behavior and carbon management practices when companies are under social media legitimacy pressure.

The interactive nature of social media provides accessible opportunities for stakeholders to process and disseminate information (Kent and Taylor, 2016), and companies have little control over the content posted by users, who may even exert pressure on management directly. Therefore, the legitimacy and prestige of a company will be undermined when negative comments from social media are widely spread through social media platforms, causing information contagion and influencing the opinions of other stakeholders (Miller and Skinner, 2015). Additionally, negative comments may also increase the possibility of a company being investigated by regulators and revealed to have been acting unethically, which may further undermine the company’s legitimacy (Zhang and Yang, 2021). The lack of legitimacy can result in limited resource access, higher financing costs, and regulatory penalties. Accordingly, it is essential for companies to bridge the gap between corporate and social values and move back within the boundaries of social appropriateness in order to minimize the adverse effects of a lack of legitimacy (Gray et al., 1995).

Corporate social responsibility (CSR) is widely regarded as a tool for enhancing and managing corporate legitimacy (Schultz and Wehmeier, 2010; Rankin et al., 2011), which means carbon disclosure, a component of CSR, can also be a powerful tool for companies to manage social media legitimacy pressures (Cho et al., 2006). With governments and the public increasingly concerned about climate change, their awareness of carbon emissions and expectations of companies to address climate change are rising (Li and Ding, 2013). The legitimacy pressure exerted by social media can drive companies to participate in carbon disclosure actively. Carbon disclosure can be an effective communication strategy between companies and the public. It can improve a company’s reputation, change social perceptions, and repair legitimacy deficits caused by negative comments. Additionally, legitimacy pressures from competitors may also force companies to provide additional carbon information to gain stakeholders’ Satisfaction (Hofer et al., 2012). By doing so, they can differentiate themselves from others who do less well in carbon disclosure. Conversely, if firms are under less pressure to be legitimate, they are subject to relatively little external scrutiny. The only thing they need to do is maintain the social legitimacy already granted to them by society (Ashforth and Gibbs, 1990). Therefore, companies under less legitimacy pressure from social media are likely to disclose less carbon information than companies under high legitimacy pressure. Thus, we propose the following hypothesis:

Hypothesis 1: There is a positive relationship between the social media legitimacy pressures and the carbon information disclosure.

There is a clear emotional bias in what is discussed or evaluated on social media platforms. According to social psychological research, the public is willing to spend more time thinking or seeking causal information when confronted with negative comments than with positive or neutral comments (Lange and Washburn, 2012; Kwahk and Kim, 2017). It can be assumed that negative comments on social media will increase the lack of legitimacy of companies to a greater extent, which will ultimately make companies more inclined to disclose carbon information publicly. Furthermore, in the context of enhanced investor protection, negative comments on social media spread more rapidly than positive comments (Lu et al., 2013), bringing more regulatory and public attention to companies and thus increasing the pressure on companies to be legitimate. However, when an organization has more positive than negative comments on social media platforms, it may be less motivated to disclose its carbon footprint since it is seen as more legitimate. Thus, we propose the following hypothesis:

Hypothesis 2a: There is a positive relationship between the negative comments on social media and the carbon information disclosure.

Hypothesis 2b: Positive comments on social media have no significant impact on corporate carbon disclosure.

Carbon disclosure often serves as an image management tool for companies when they face legitimate pressures (Cho and Patten, 2007). It should be noted, however, that prolonged symbolic disclosure rather than substantive carbon management activities may increase reputational risks and raise stakeholder concerns about opportunistic corporate behavior. In 2017, China FAW (First Automobile Works) Group disclosed its green factory and green industry chain projects in its CSR report. However, it was subsequently revealed that the company had mishandled pollutants and exceeded carbon emission standards. This opportunistic behavior was not only heavily resisted by the public but also criticized and punished by the regulators (Zhang and Yang, 2021). Likewise, the contradictory behavior of the fast-food giant in promoting its positive stories with farmers while negative events about McDonald’s food poisoning and low labor standards appear on social media created a hypocritical image for consumers (Lyon and Montgomery, 2013). The results suggest that when companies face legitimacy pressures, they may use the carbon disclosure tool as a symbolic carbon management tool without engaging in substantive carbon management. As a result, companies may become decoupled from their carbon management practices or suffer adverse economic consequences. Therefore, firms need a mix of substantive and symbolic legitimacy strategies of varying intensities to cope with legitimacy pressures or prevent the decoupling of firm practices (Ashforth and Gibbs, 1990).

The effectiveness of social media legitimacy pressure, which works as an informal external mechanism, depends on the substantive response from within the firm. It does not directly contribute to improving the carbon performance of firms (Li et al., 2018). In this study, we examined two substantive carbon measures, corporate green innovation and EMS, both of which are internal formal responses to legitimacy pressures within firms (Tachizawa and Wong, 2015).

Green innovation is characterized by the notion of sustainability and the reduction of environmental burdens. It is defined as innovation related to conserving resources and energy and improving technologies or processes to reduce environmental pollution (Saunila et al., 2018). Green innovation is essential for firms to achieve economic growth and environmental sustainability (Shao et al., 2021). It is a critical factor in maintaining firm competitiveness and improving the quality of life in society (Dangelico and Pujari, 2010). Specifically, for the firm itself, green innovation effectively improves resource efficiency and optimizes environmental performance during the product life cycle (Chen et al., 2006). It also helps ensure that the company complies with environmental requirements and avoids regulatory penalties (Chang, 2011). For society and external firms, green innovation has a “double externality”: in addition to benefiting firms that do not invest in green innovation by spreading knowledge (Berrone et al., 2013), green innovation can also be a quasi-public good that contributes to resource conservation, environmental protection, and reducing waste emissions, thus benefitting society (Li L. et al., 2017). Furthermore, green innovation sends a positive signal that a company is practicing carbon management, thus setting itself apart from competitor companies and enhancing its image and reputation (Barnett and Salomon, 2012). As a result, corporate green innovation can enhance corporate legitimacy from several perspectives.

When companies face social media legitimacy pressures, their ability to innovate green can cushion the impact of legitimacy pressures and thus minimize carbon-related risks. As public and government interest in corporate carbon disclosures increases and social media become more widely used, companies are subject to increased regulatory pressures. The sustainable nature of green innovation and its “double externality” not only satisfy the dynamically changing expectations of social legitimacy but also serve to bridge the gap between corporate and social values. Furthermore, as a substantive carbon management practice, green innovation is an effective strategy for repairing the legitimacy deficit caused by negative comments and easing regulatory pressure when the legitimacy status is under threat. Thus, we propose the following hypothesis:

Hypothesis 3: The positive relationship between the social media legitimacy pressures and corporate carbon disclosure is weaker for firms with a higher level of green innovation.

Similarly, corporate EMS are substantive carbon management practices that assist companies in organizing their internal processes, improving their environmental performance, as well as gaining legitimacy by meeting their environmental commitments to external stakeholders (Aravind and Christmann, 2011). Corporate EMS provide guidelines for corporate production, systematize and standardize a range of internal organizational procedures, and require managers to document production activities and processes, making a company’s environmental impact more transparent and manageable (King and Lenox, 2001). Corporate EMS also contribute to reducing the preparation costs of carbon information disclosure, including human resources, time, and financial costs (Ott et al., 2017). External stakeholders consider the establishment of EMS as a signal of the company’s environmental commitment to society, which helps to improve the company’s image and gain trust and support among stakeholders, thus increasing the company’s level of legitimacy (Boiral, 2007). External stakeholders view a company with an EMS as more credible and trustworthy than those without (Jiang and Bansal, 2003).

When companies face legitimacy pressures from social media, an environmental management system not only responds to increased regulatory demands and legitimacy expectations from stakeholders, but also sends a positive signal about a company’s carbon management practices. An environmental management system means that companies have standardized production processes, efficient production technologies and stringent emission standards, all of which effectively improve the relationship between companies and the public and alleviate social media legitimacy pressures. Based on the above discussion, we develop our third hypothesis:

Hypothesis 4: The positive relationship between the social media legitimacy pressures and corporate carbon disclosure is weaker for firms with the establishment of EMS.

For our research, we examined the impact of social media on corporate carbon information disclosure by using all Chinese companies listed on the Shanghai and Shenzhen Stock Exchanges between 2009 and 2019. Listed companies are the main subject of carbon information disclosure and are the main target of public discussion on social media platforms. In terms of the disclosure of corporate carbon information, we mainly gathered it manually from corporate social responsibility reports and corporate sustainability reports. The social media sentiment tendency data was obtained from the CNRDS database Eastmoney stock forum comment data, which had already collected and classified stock forum comments data daily, and we consolidate daily stock forum commentary data into annual data. In the Chinese securities market, which is dominated by small and medium-sized investors, the Eastmoney stock forum is the largest exchange platform in China. Obtaining data from this platform makes our data source more general. The rest of our data comes from the CSMAR database, which is one of the largest sources of data on listed companies in China.

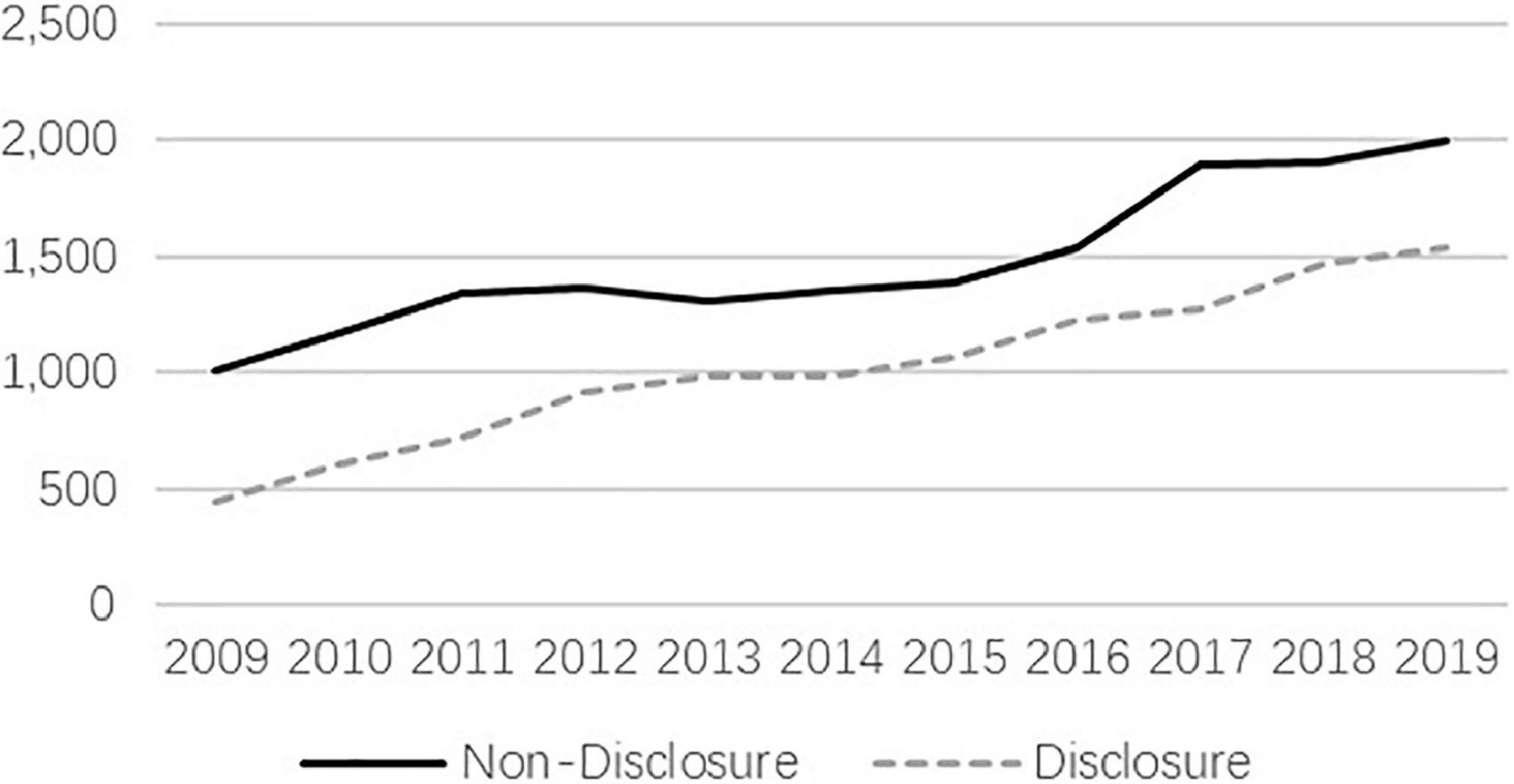

Using the data extracted from the above sources, we have collected an initial dataset of 35,532 observations from all listed companies. Then, we selected the sample by the following criteria (Liu et al., 2021). (a) Excluding all foreign capital shares (listed in the Shanghai and Shenzhen B-share markets); (b) Dropping observations that were specially treated (ST); and (c) Deleting all observations with missing variables. A total of 27,520 firm-year observations corresponding to 3,656 different companies were collected. Figure 1 shows the annual trend of corporate carbon disclosure. As shown in the graph, there has been a progressive increase in corporate carbon disclosure, with 448 companies disclosing carbon information in 2009 and 1,542 firms disclosing carbon information in 2019. A possible explanation for this graph might be that as government and public concern about climate change increases, companies face increasing regulatory pressure.

Figure 1. Number of companies disclosing carbon information versus those not disclosing carbon information.

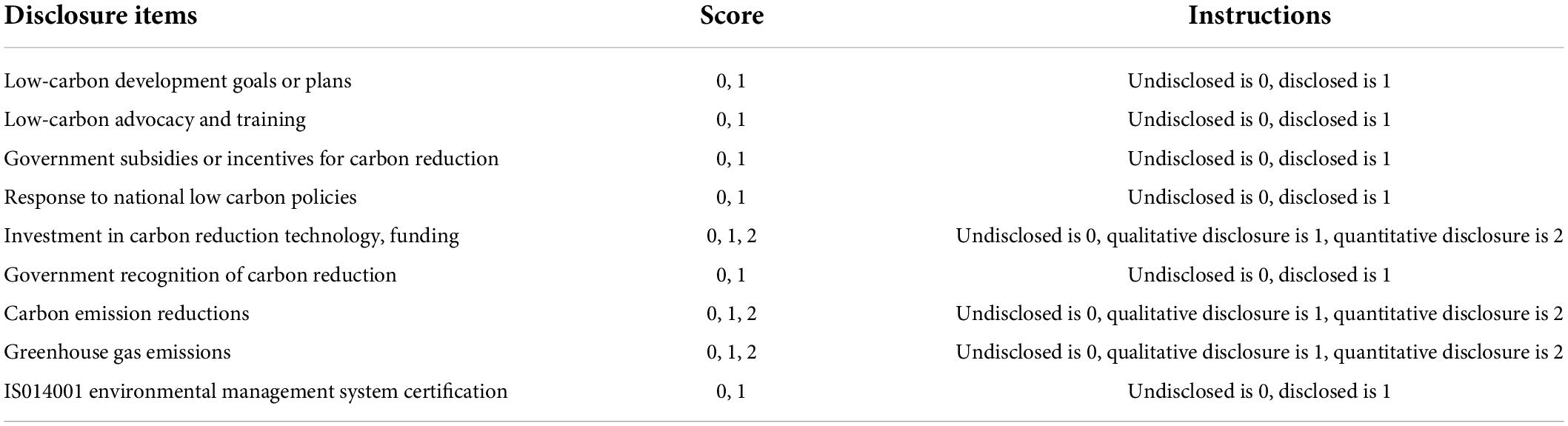

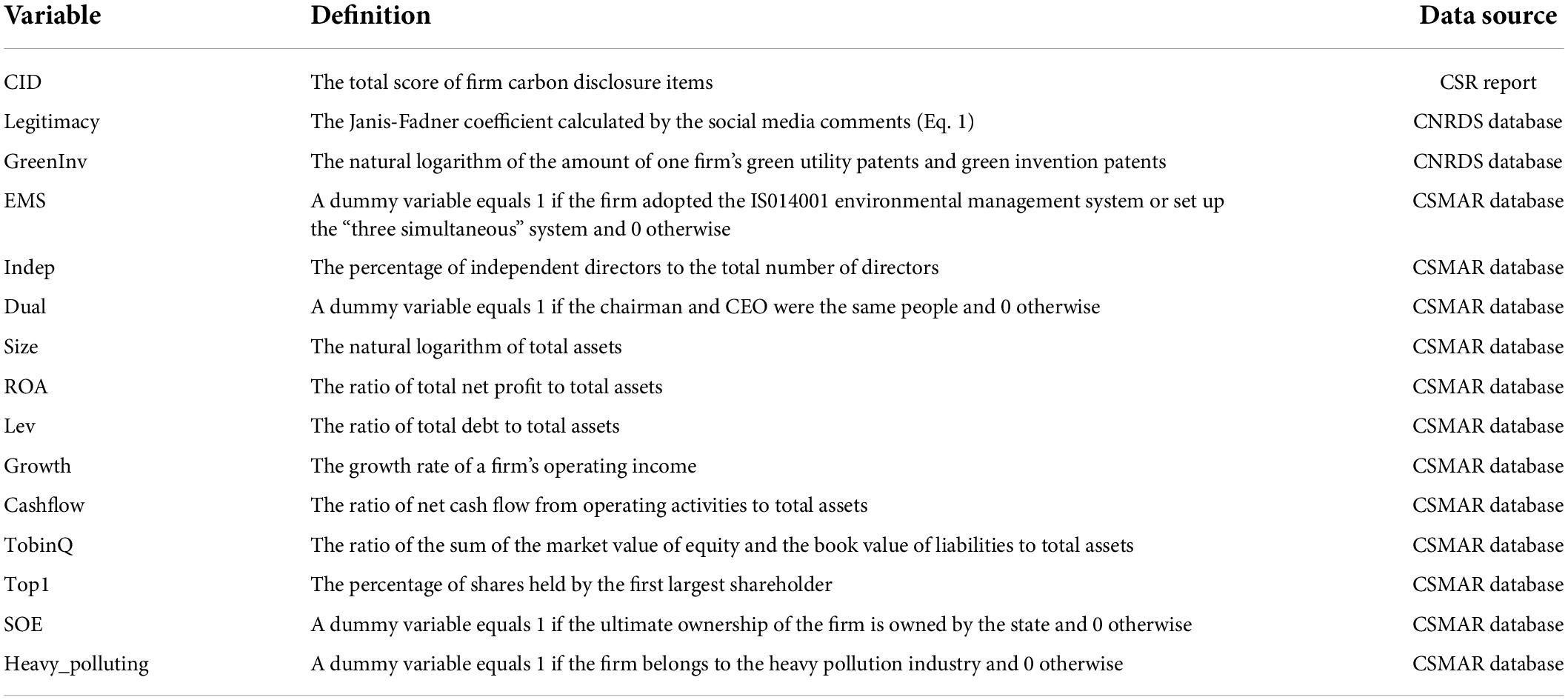

We used the corporate carbon information disclosure score (CID) as the dependent variable in this study (Li L. et al., 2017; Li et al., 2018). Following Aerts and Cormier (2009), we used content analysis to assess the level of disclosure of carbon information by corporations. Specifically, we assessed the level of corporate carbon information disclosure in nine items (Table 1) by referring to the Carbon Disclosure Project China Report and the characteristics of carbon disclosure in companies’ CSR and sustainability reports. The level of corporate carbon disclosure consists of the sum of the scores of the nine items. In addition, for robustness checking, two alternative measures of corporate carbon disclosure are applied. The CIDlogit dummy variable is coded 1 if the firm disclosed relevant carbon information in a specific year, 0 otherwise. The LnCID is the logarithm of the CID + 1.

Table 1. Specifications of carbon information disclosure.

Our independent variable is social media legitimacy pressure, and we collected data on the sentiment tendency of stock forum comments for each day of the Eastmoney website from 2009 to 2019. The sentiment of the comments is categorized as positive, neutral and negative. We used the Janis-Fadner coefficient (J-F) to measure social media legitimacy pressure (Legitimacy). This is a metric proposed by Janis and Fadner for content analysis methods, followed by Aerts and Cormier (2009), Li L. et al. (2017), Li et al. (2018), and others have used this coefficient to quantify legitimacy pressure. It is calculated as follows.

Where: e represents the number of positive comments, c represents the number of negative comments, and t is the sum of e and c. J-F coefficients have values ranging from −1 to 1. The more negative comments about a company, the closer the J-F coefficient is to −1 and the more legitimacy pressure the company faces. Moreover, in order to test hypotheses H2a and H2b, we consider the logarithm of the number of negative media posts as well as the number of positive comments (NLegitimacy/PLegitimacy) as independent variables.

In order to test hypotheses 3 and 4, we used the logarithm of the sum of green utility patents and green invention patents as a measure of green innovation (GreenInv). Further, we selected whether the company had implemented the IS014001 environmental management system and whether it had established a “three simultaneous” system to capture its environmental management system (EMS). The EMS is a dummy variable that is coded as 1 if the company has adopted the IS014001 environmental management system or set up the “three simultaneous” system, and 0 otherwise. Comparatively to the international standard environmental management system of IS014001, the “three simultaneous” system is a unique environmental management system in China. It is emphasized that environmental protection measures must be implemented simultaneously with the project, from design to construction through completion to commissioning (Li D. et al., 2017).

In order to control for the potential impacts of corporate carbon disclosure, we selected control variables at the level of the top management team (TMT), as well as at the firm and industry levels. At the TMT level, corporate governance plays a significant role in influencing corporate carbon disclosure (Choi et al., 2013). Liao et al. (2015) also find that independent directors are likely to favor more transparent carbon disclosure since they have different backgrounds and have no financial interest in the company. Therefore, we controlled the independent directors’ ratio (Indep) and whether the chairman and CEO were the same people (Dual). We measured Indep by the number of independent directors as a proportion of the total. In addition, Dual was coded as 1 if the chairman and CEO were the same people and 0 otherwise.

In addition, we have considered a set of firm characteristics that may influence firms’ disclosure of carbon information. Firmsize was measured as the natural logarithm of total assets, because larger firms may experience more pressure from stakeholders (Berrone and Gomez-Mejia, 2009). ROA was measured by the ratio of total net profit to total assets, and Lev was measured by the ratio of total liabilities to total assets. Growth was measured as the growth rate of a firm’s operating income. Because these factors are closely related to corporate profitability, higher profitability increases the financial resources available to companies to invest in carbon reduction and disclosure (Ott et al., 2017). Cashflow was measured as the ratio of net cash flow from operating activities to total assets. TobinQ was measured by the ratio of the sum of the market value of equity and the book value of liabilities to total assets (Liu et al., 2022). Top1 was measured by the proportion of shares held by the first largest shareholder. SOE was measured by whether the ultimate ownership of the firm is owned by the state (Li L. et al., 2017; Li et al., 2018). At the industry level, we measured Heavy_polluting by whether a firm belongs to the heavy pollution industry (Luo, 2019). Finally, we controlled for year, industry, and province effects to capture changes in CID over time, industry, and province. A detailed definition for each variable used in this study is provided in Appendix A.

To test our Hypothesis 1, Hypothesis 2a, and Hypothesis 2b, we constructed the following test models. The models were estimated using least squares regression (OLS), controlling for year, industry, and province fixed effects (Li L. et al., 2017).

Where CID is the dependent variable and CIDit refers to firm i’s carbon disclosure score in year t. Legitimacy, NLegitimacy, and PLegitimacy are independent variables. Legitimacyit describes the social media legitimacy pressure faced by firm i in year t. Controls are a set of control variables.

To test for moderating effects Hypothesis 3 and Hypothesis 4, we estimated the following regression models, including the moderating variables and their interaction terms.

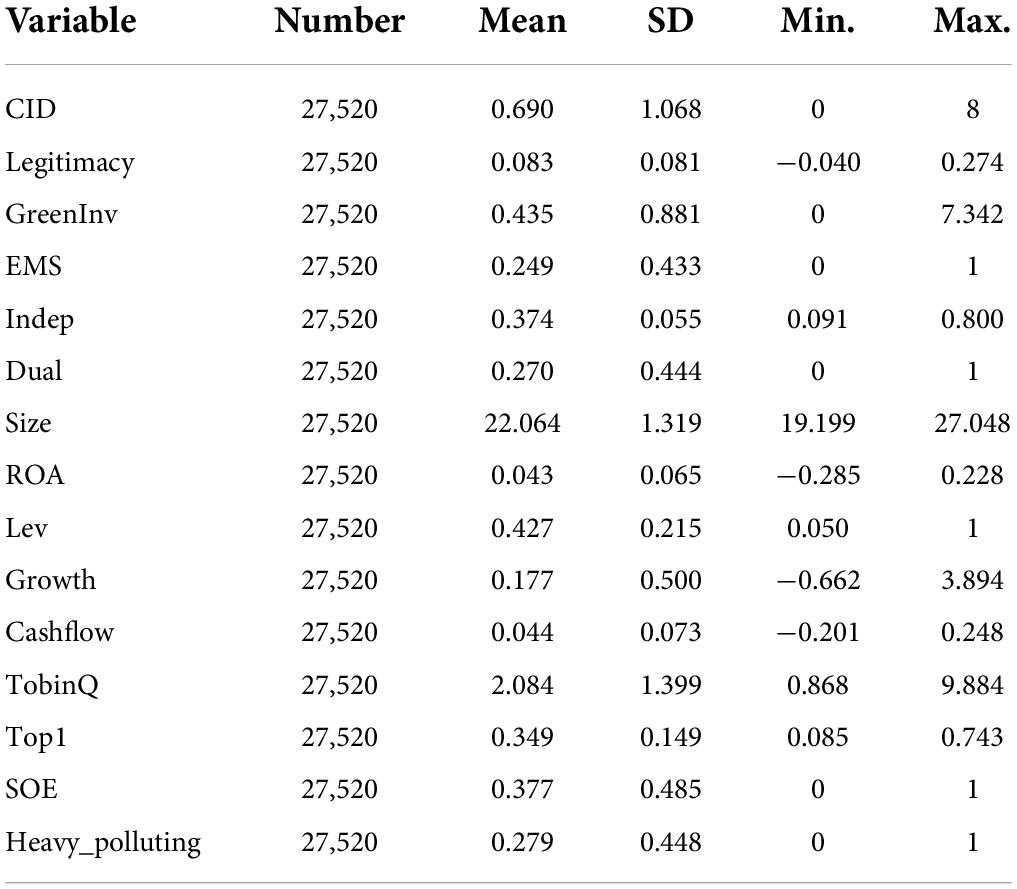

Table 2 summarizes the results of descriptive statistics for all variables. Accordingly, the mean value of the dependent variable carbon information disclosure (CID) is 0.69, indicating that the corporate carbon information disclosure level is not high. The results are similar to other relevant studies on corporate carbon information disclosure (Li L. et al., 2017). The mean values of GreenInv and EMS are 0.435 and 0.249, respectively, suggesting that most companies do not have substantial carbon management practices.

Table 2. Descriptive statistics.

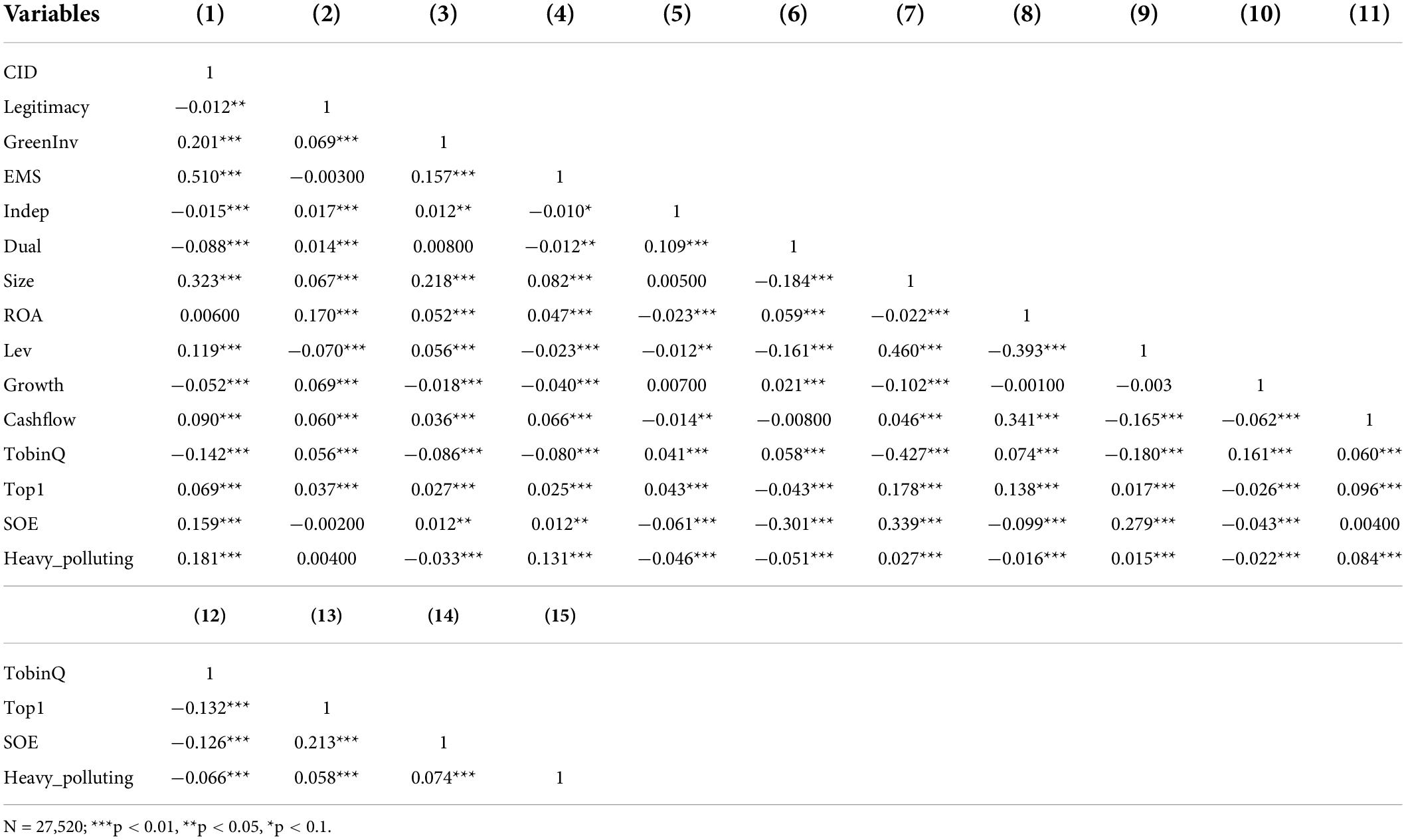

The Pearson correlation coefficient between variables is shown in Table 3. In line with expectations, social media legitimacy pressure (Legitimacy), reflected by the J-F coefficient, is positively correlated with corporate carbon information disclosure (CID). The higher the J-F coefficient, the lower the legitimacy pressure faced by the firm. The correlation coefficients between CID and the other variables are low. Additionally, we calculated the variance inflation factor (VIF) for each variable. We found that the maximum value was 1.88 and the mean value was 1.23, which is much smaller than the acceptable level, indicating that multicollinearity is not a serious issue.

Table 3. Pearson correlation matrix.

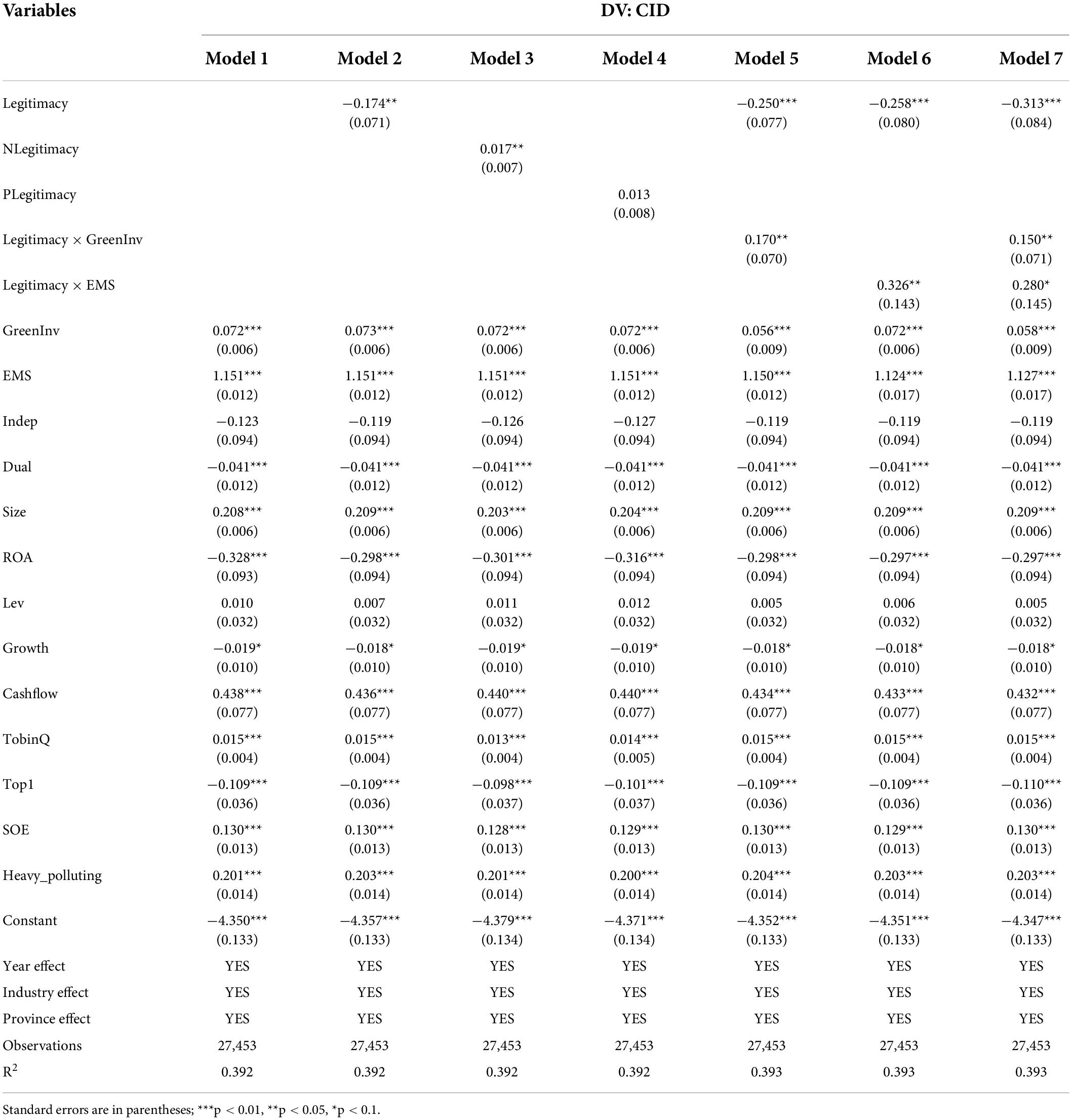

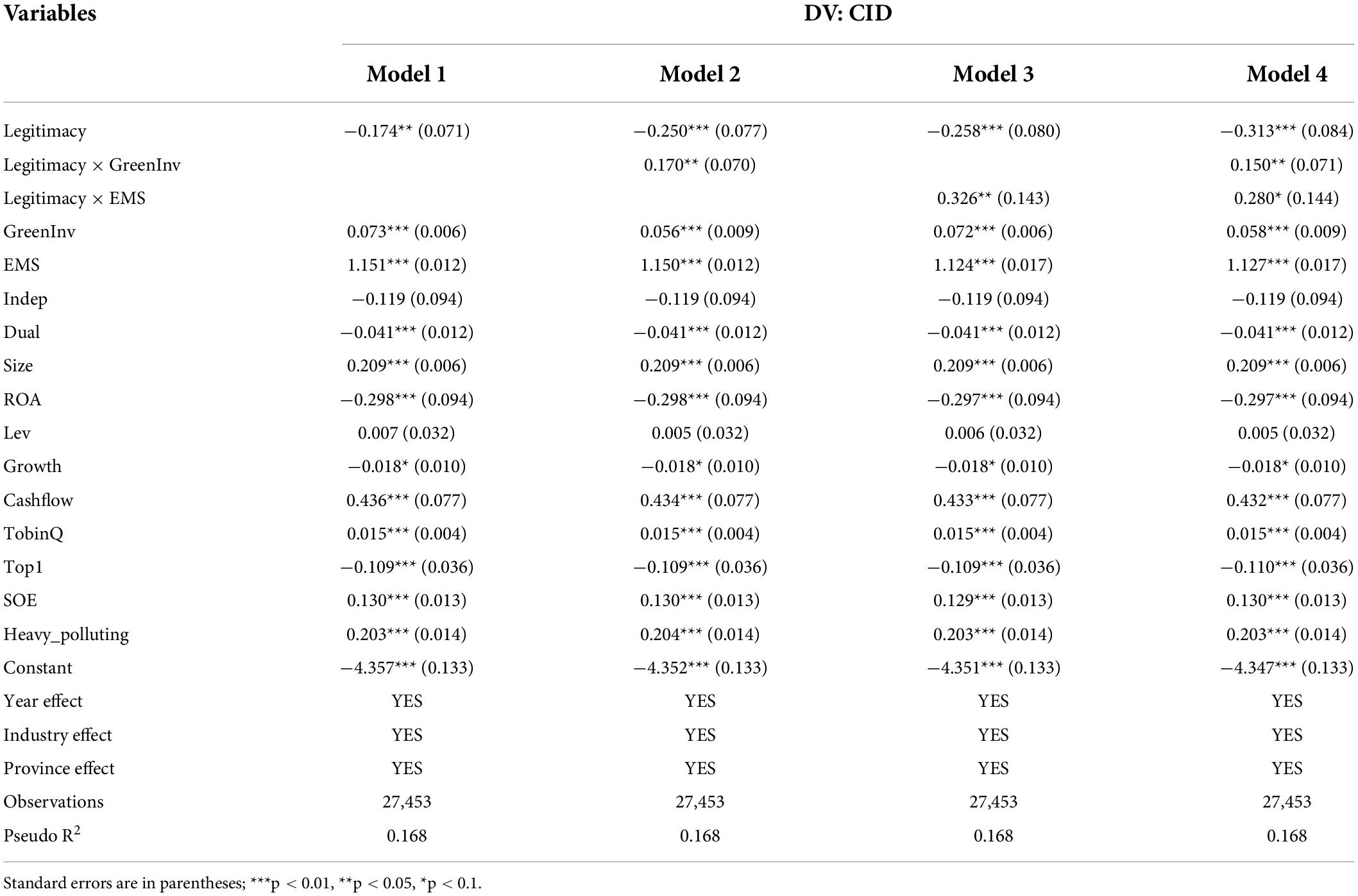

According to the research hypotheses, a multiple regression analysis of the relationship between social media legitimacy pressures and corporate carbon disclosure was performed. These results are presented in Table 4. Model 1 is the baseline model with control variables only. Legitimacy, a measure of social media legitimacy pressure, has been added to Model 2 to test Hypothesis 1. The results show that social media legitimacy pressure (the lower the Legitimacy, the higher the legitimacy pressure) has a positive and significant effect on corporate carbon disclosure at the 5% level (β = −0.174, ρ < 0.05). This strongly supports Hypothesis 1 and confirms that social media can effectively monitor corporate carbon information disclosures. The results in Table 4 allow us to calculate the economic significance of social media legitimacy pressure on corporate carbon disclosure, with a 100% increase in legitimacy pressure on companies increasing their carbon disclosure score by approximately 17.4%.

Table 4. Estimates for carbon information disclosure.

Models 3 and 4 examined the impact of negative and positive social media comments on corporate carbon disclosure, respectively. In model 3, NLegitimacy is positive and significant (β = −0.017, ρ < 0.05), but PLegitimacy is not significant (ρ > 0.1). This suggests that negative social media comments are the primary reason for the lack of corporate legitimacy and that companies are more likely to disclose carbon data under pressure from negative comments. However, positive evaluations do not encourage companies to disclose carbon information actively, thus confirming our expectation in Hypothesis 2a and Hypothesis 2b.

The results of the moderating effects are reported in Models 5 and 6. In Model 5, we added the interaction terms of Legitimacy and GreenInv to test the moderating effect of corporate green innovation. There is a positive and significant coefficient (β = 0.326, ρ < 0.05), which indicates that corporate green innovation (GreenInv) negatively moderates the relationship between social media legitimacy pressure and carbon disclosure, thus providing support for Hypothesis 3. Similarly, the coefficient of the interaction term between Legitimacy and EMS is positive and significant in Model 6 (β = 0.280, ρ < 0.1), suggesting that EMS also negatively moderates the relationship between legitimacy pressure and carbon disclosure. Collectively, these results suggest that substantive carbon management practices within firms (green innovation or EMS) can increase the level of legitimacy of firms and alleviate legitimacy pressures due to negative social media comments.

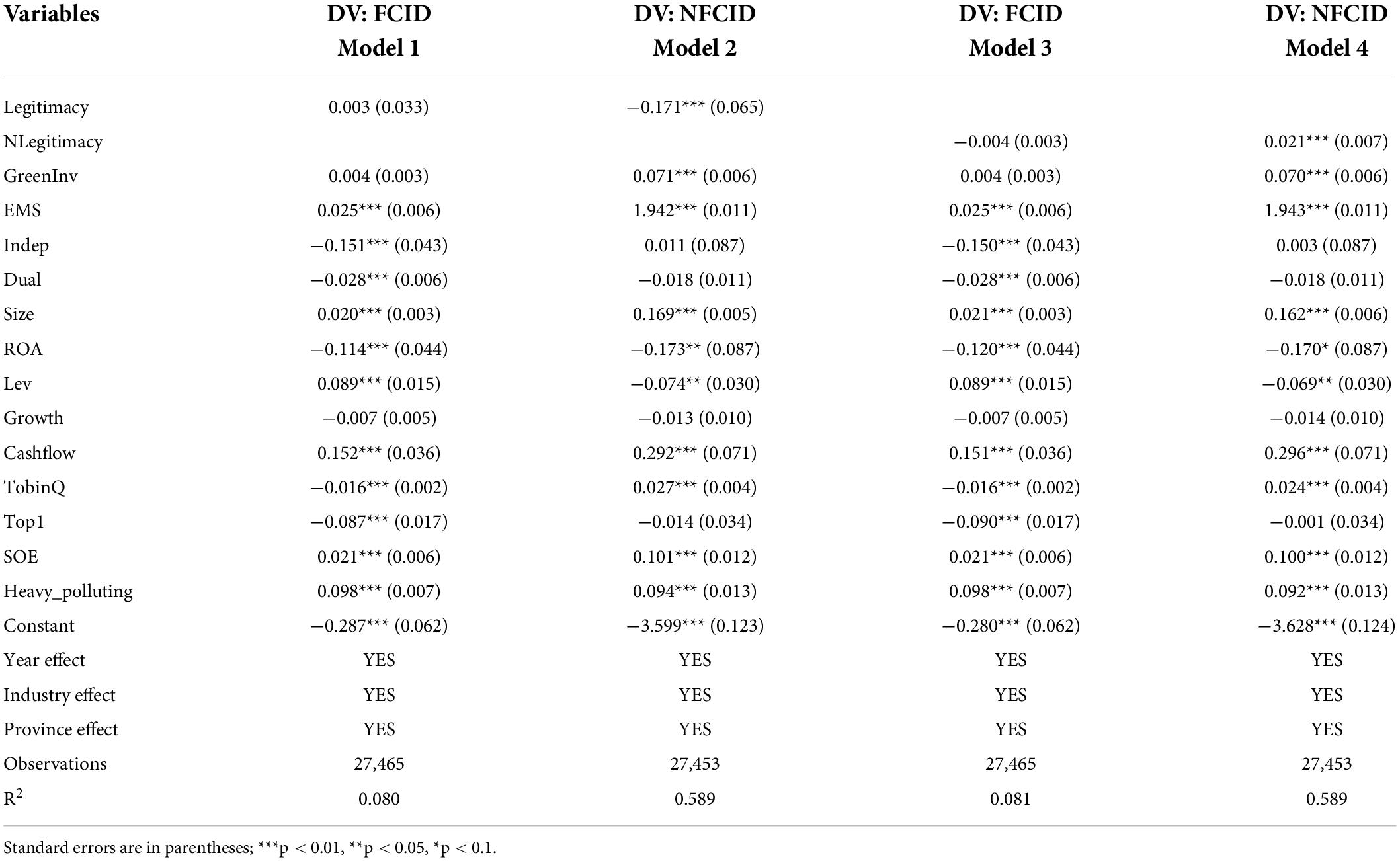

Corporate carbon information disclosure can be divided into two categories: financial carbon information disclosure (FCID) and non-financial carbon information disclosure (NFCID) (Li L. et al., 2017). The main difference between them is whether they are measured in monetary terms. Following Li L. et al. (2017), the scores of “government subsidies or incentives for carbon emission reduction” as well as “investments in carbon emission reduction technologies and funds” are utilized to assess the FCID of enterprises. The remaining seven items were used as NFCID.

To test the structural impact of social media legitimacy pressure on corporate carbon information disclosure, we further examined the relationship between social media legitimacy pressure (Legitimacy/NLegitimacy) and financial or non-financial carbon information (FCID/NFCID). Table 5 reports the regression results. Models 1 and 3 report the impact of social media legitimacy pressures on corporate FCID, whereas Models 2 and 4 report the impact of social media legitimacy pressures on corporate NFCID. Both Legitimacy and NLegitimacy are insignificant in Model 1 and Model 3, but both Legitimacy and NLegitimacy in Model 2 and Model 4 are significant at the 1% level (β = −0.172, ρ < 0.01; β = 0.021, ρ < 0.01). This suggests that under the pressure of social media legitimacy, firms are more inclined to disclose non-financial carbon information rather than financial carbon information. This finding is in line with the study by Li L. et al. (2017).

Table 5. Estimates for FCID and NFCID.

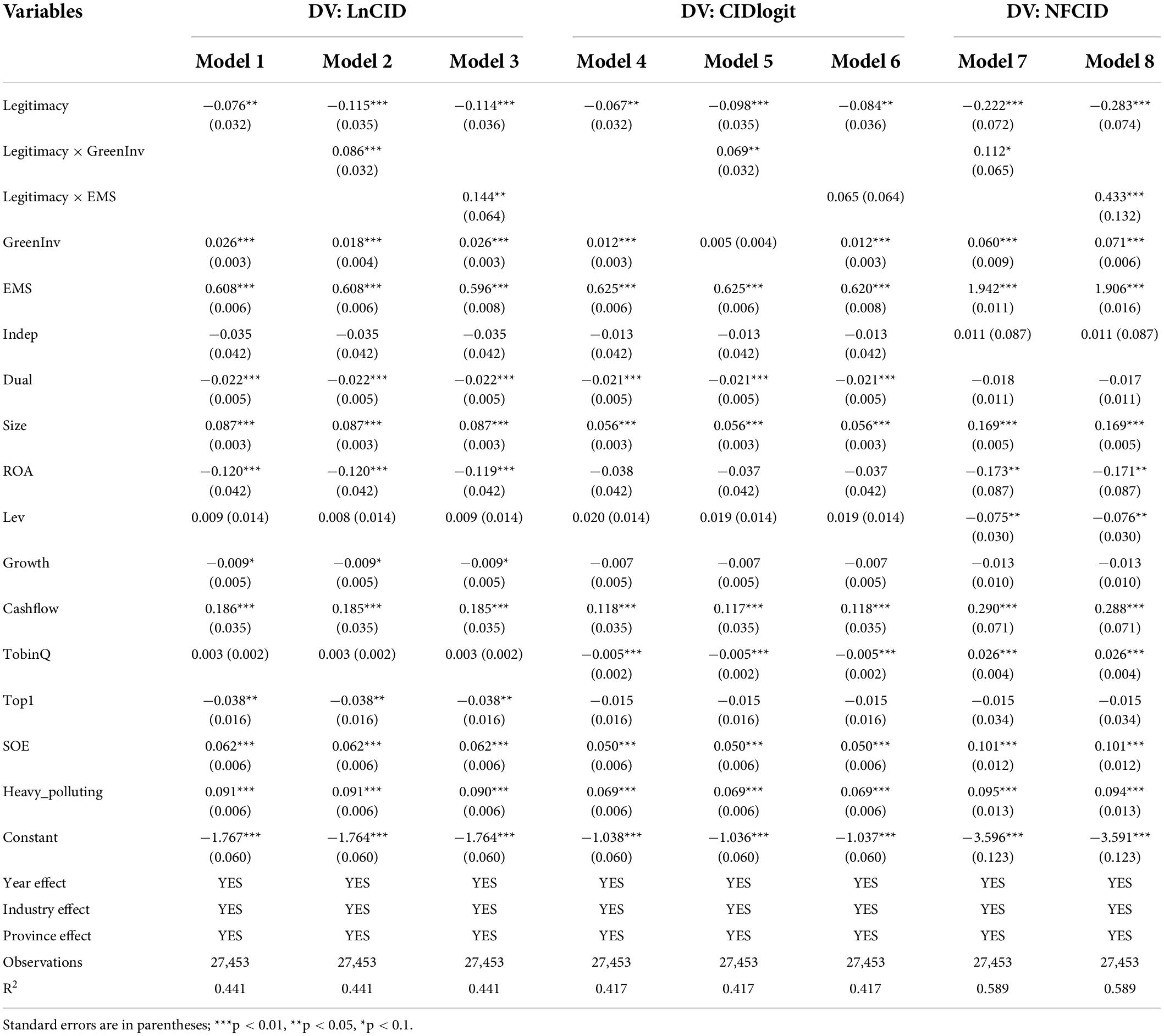

We tested the robustness of our results through a set of robustness checks. First, we adopted an alternative measure of the dependent variable. Referring to Li et al. (2018), we used the natural logarithm of a firm’s carbon disclosure score (LnCID), whether or not carbon information is disclosed (CIDlogit), and NFCID as dependent variables for robustness tests. All results are reported in Table 6. For the dependent variable LnCID, Model 1–Model 3 show that the coefficients on Legitimacy, Legitimacy × GreenInv and Legitimacy × EMS are significant (β = −0.076, ρ < 0.05; β = 0.086, ρ < 0.01 and β = 0.144, ρ < 0.05). Similarly, in Model 4–Model 8, the results are similar to those of previous analyses, except for the non-significant moderating effect of corporate EMS in Model 5. These results are consistent with the main findings in Table 4, suggesting the robustness of our results.

Table 6. Robustness check using alternative dependent variables.

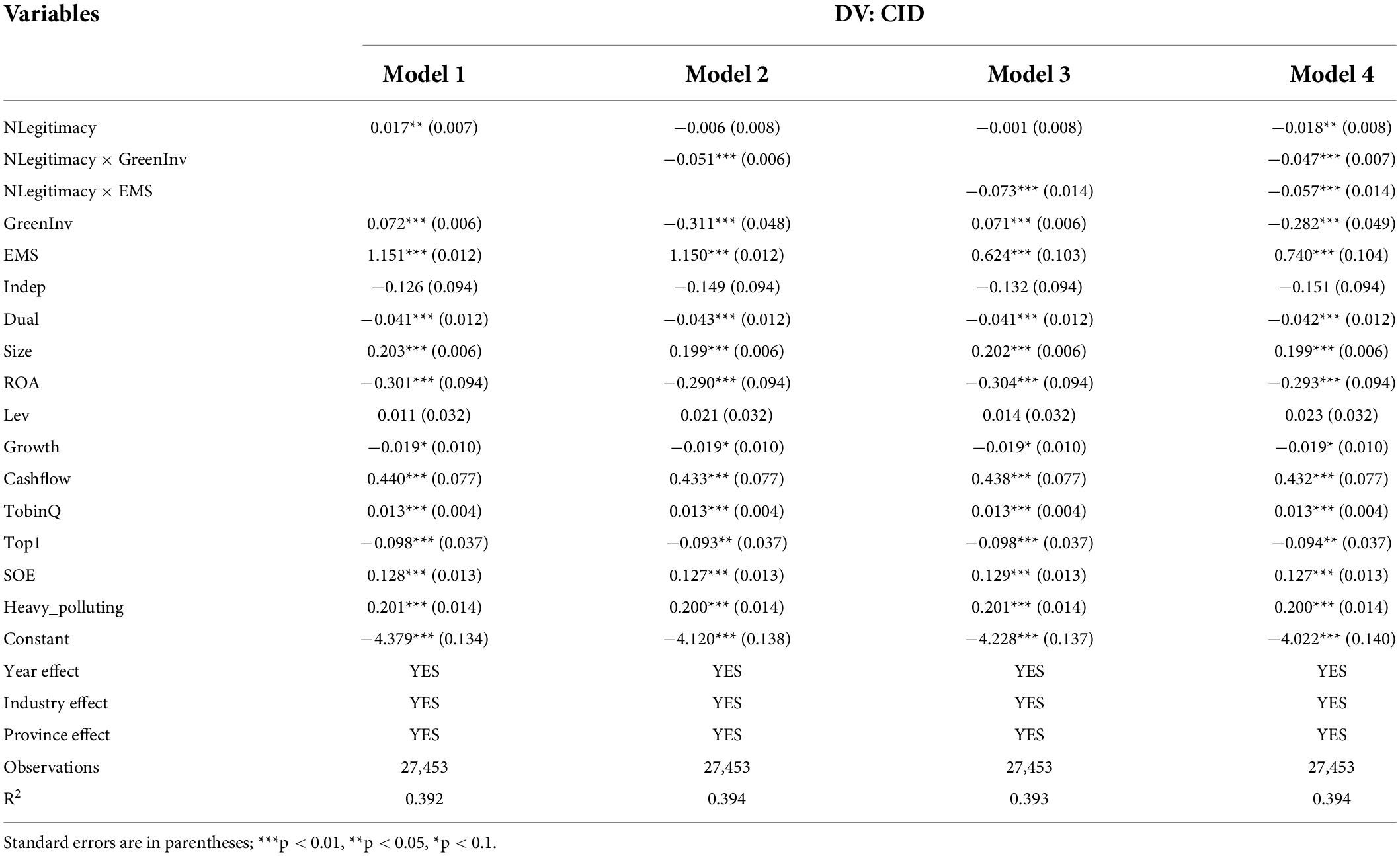

Second, we used an alternative measure of the independent variable. Previously, we discovered that social media legitimacy pressures are primarily a result of negative comments on social media platforms. Therefore, we try to examine the moderating effect of corporate green innovation (GreenInv) and EMS by utilizing NLegitimacy as an independent variable. All results are reported in Table 7. In model 1, the coefficient on NLegitimacy is positive and significant (β = 0.017, ρ < 0.05). In models 2 and 3, the coefficients for GreenInv × NLegitimacy and GreenInv × EMS are negative and significant (β = −0.051, ρ < 0.01; and β = −0.073, ρ < 0.01). These results are consistent with our previous, suggesting that our results are robust.

Table 7. Robustness check using alternative independent variables.

Third, most Chinese companies do not disclose their carbon emissions; that is, they have a carbon information disclosure score of 0 (CID = 0). Thus, the dependent variable is truncated at 0. In our study, they account for 59.17%. We, therefore, considered a robustness test using the Tobit model. All the results are reported in Table 8. From the reported results, all the findings remain consistent with the previous analysis, which further indicates the robustness of our results.

Table 8. Robustness check using Tobit model.

As countries in the world continually implement measures to address climate and environmental change, corporate carbon information disclosure is becoming increasingly important to stakeholders. Social media offers the public a convenient and effective platform to voice their concerns about climate change. As a result, we examined the impact of social media legitimacy pressure on corporate carbon disclosures, using the largest listed Chinese stock exchange platform as a data source. We provide strong evidence that social media legitimacy pressure has a significant positive impact on corporate carbon disclosures. Furthermore, we find that substantive carbon management measures have a moderating effect on corporate legitimacy pressure, and corporate green innovation and EMS alleviate the legitimacy pressure faced by enterprises.

This study makes two main contributions to the existing literature. First, using social media as a means of generating corporate legitimacy pressure, we validated the effectiveness of social media monitoring of corporate carbon disclosure, which contributes to the application of legitimacy theory to information disclosure. Earlier literature has concentrated on institutional pressure from the government (Luo, 2019), mass media (Li L. et al., 2017; Li et al., 2018), and most studies have focused on heavily polluting industries or large companies. However, our study sample includes a significant number of small and medium-sized enterprises as well as businesses located in non-heavy polluting industries. Using a more comprehensive sample, we found that legitimacy pressure not only enhanced corporate disclosure but also impacted the structure of corporate disclosure. Second, we contribute to the carbon management literature by considering corporate carbon disclosure as a symbolic carbon management measure and emphasizing the interaction between symbolic and substantive carbon management measures. We find that both symbolic and substantive carbon management measures alleviate the legitimacy pressure on companies.

More practically, in the context of the carbon-neutral, carbon-cycling era, this study provides evidence and insights for policymakers to formulate regulatory policies better. First, corporate carbon disclosure is a response strategy to threats to corporate legitimacy. However, it is likely to be a symbolic management measure. Governments need to establish appropriate regulations to make it mandatory that companies disclose substantive carbon management practices in order to prevent companies from trying to “bleach” themselves by using such low-cost measures. Second, our research has proved the appropriateness of social media as a strong regulator of corporate carbon disclosure. Social media is a potent regulator of corporate carbon disclosure. In other words, when companies disclose additional carbon information on their social media platforms voluntarily, this will increase their credibility and differentiate them from companies in the same industry that make low-quality disclosures. Consequently, it is crucial that companies use substantive carbon management practices to improve their carbon performance. Third, although both substantive and symbolic carbon management measures can effectively alleviate the legitimacy pressure of social media, if companies engage in only symbolic carbon management behaviors rather than substantive carbon management behaviors for a long time. This will inevitably lead to decoupling companies’ carbon management practices and consequent stakeholder penalties. Therefore, it is necessary for companies to maintain consistency between carbon disclosure and carbon management activities.

Our study has several limitations. Firstly, due to data availability, only nine carbon information disclosure items were selected in this article to calculate enterprises’ carbon information disclosure score, and this measurement method may not be authoritative. When the quality of corporate carbon information disclosures is further enhanced, additional carbon information disclosure items will have to be selected to calculate the corporate carbon information disclosure scores. Second, although the stock forum has the characteristics of social media, it is still different from popular social media such as Facebook and Twitter. A further investigation needs to be conducted into whether stakeholders expressing their legitimacy expectations on social media platforms such as Facebook and Twitter enhance corporate carbon disclosure.

The original contributions presented in this study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

JS completed the logical structure of the study as well as the data collection. ZH completed the empirical research in the study. Both authors contributed to the article and approved the submitted version.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Aerts, W., and Cormier, D. (2009). Media legitimacy and corporate environmental communication. Account. Org. Soc. 34, 1–27. doi: 10.1016/j.aos.2008.02.005

Albarrak, M. S., Elnahass, M., and Salama, A. (2019). The effect of carbon dissemination on cost of equity. Bus. Strat. Env. 28, 1179–1198. doi: 10.1186/s12889-015-2540-5

Aravind, D., and Christmann, P. (2011). Decoupling of standard implementation from certification: does quality of ISO 14001 implementation affect facilities’ environmental performance? Bus. Ethics Q. 21, 73–102. doi: 10.5840/beq20112114

Ashforth, B. E., and Gibbs, B. W. (1990). The double-edge of organizational legitimation. Org. Sci. 1, 177–194. doi: 10.1287/orsc.1.2.177

Barnett, M. L., and Salomon, R. M. (2012). Does it pay to be really good? Addressing the shape of the relationship between social and financial performance. Strat. Manag. J. 33, 1304–1320. doi: 10.1002/smj.1980

Berrone, P., Fosfuri, A., Gelabert, L., and Gomez-Mejia, L. R. (2013). Necessity as the mother of ‘green’ inventions: institutional pressures and environmental innovations. Strat. Manag. J. 34, 891–909. doi: 10.1002/smj.2041

Berrone, P., and Gomez-Mejia, L. R. (2009). Environmental performance and executive compensation: an integrated agency-institutional perspective. Acad. Manag. J. 52, 103–126. doi: 10.5465/amj.2009.36461950

Blankespoor, E., Miller, G. S., and White, H. D. (2014). The role of dissemination in market liquidity: evidence from firms’ use of Twitter™. Account. Rev. 89, 79–112. doi: 10.2308/accr-50576

Boiral, O. (2007). Corporate greening through ISO 14001: a rational myth? Org. Sci. 18, 127–146. doi: 10.1287/orsc.1060.0224

Borghei, Z. (2021). Carbon disclosure: a systematic literature review. Account. Fin. 61, 5255–5280. doi: 10.1111/acfi.12757

Chang, C.-H. (2011). The influence of corporate environmental ethics on competitive advantage: the mediation role of green innovation. J. Bus. Eth. 104, 361–370. doi: 10.1007/s10551-011-0914-x

Chen, Y.-S., Lai, S.-B., and Wen, C.-T. (2006). The influence of green innovation performance on corporate advantage in Taiwan. J. Bus. Ethics 67, 331–339. doi: 10.1007/s10551-006-9025-5

Cho, C. H., and Patten, D. M. (2007). The role of environmental disclosures as tools of legitimacy: a research note. Account. Org. Soc. 32, 639–647. doi: 10.1016/j.aos.2006.09.009

Cho, C. H., Patten, D. M., and Roberts, R. W. (2006). Corporate political strategy: an examination of the relation between political expenditures, environmental performance, and environmental disclosure. J. Bus. Ethics 67, 139–154. doi: 10.1007/s10551-006-9019-3

Choi, B. B., Lee, D., and Psaros, J. (2013). An analysis of Australian company carbon emission disclosures. Pacific Account. Rev. 25:1. doi: 10.1016/j.heliyon.2021.e07505

Comyns, B., and Figge, F. (2015). Greenhouse gas reporting quality in the oil and gas industry: a longitudinal study using the typology of “search”,“experience” and “credence” information. Account. Aud. Account. J. 28, 403–443. doi: 10.1108/AAAJ-10-2013-1498

Dangelico, R. M., and Pujari, D. (2010). Mainstreaming green product innovation: why and how companies integrate environmental sustainability. J. Bus. Eth. 95, 471–486. doi: 10.1007/s10551-010-0434-0

Deegan, C., and Blomquist, C. (2006). Stakeholder influence on corporate reporting: an exploration of the interaction between WWF-Australia and the Australian minerals industry. Account. Org. Soc. 31, 343–372.

Deegan, C. M., and Deegan, C. (2007). Australian financial accounting. Sydney NSW: McGraw-Hill Sydney.

Depoers, F., Jeanjean, T., and Jérôme, T. (2016). Voluntary disclosure of greenhouse gas emissions: Contrasting the carbon disclosure project and corporate reports. Journal of Business Ethics 134, 445–461. doi: 10.1007/s10551-014-2432-0

Fan, X., Wang, Y., and Wang, D. (2021). Network connectedness and China’s systemic financial risk contagion——An analysis based on big data. Pacific-Basin Fin. J. 68:101322. doi: 10.1016/j.pacfin.2020.101322

Gray, R., Kouhy, R., and Lavers, S. (1995). Corporate social and environmental reporting: a review of the literature and a longitudinal study of UK disclosure. Account. Audit. Accountab. J. 1995:09513579510146996.

Guenther, E., Guenther, T., Schiemann, F., and Weber, G. (2016). Stakeholder relevance for reporting: explanatory factors of carbon disclosure. Busin. Soc. 55, 361–397. doi: 10.1177/0007650315575119

He, R., Luo, L., Shamsuddin, A., and Tang, Q. (2022). Corporate carbon accounting: a literature review of carbon accounting research from the kyoto protocol to the paris agreement. Account. Fin. 62, 261–298. doi: 10.1111/acfi.12789

Herold, D. M., and Lee, K.-H. (2019). The influence of internal and external pressures on carbon management practices and disclosure strategies. Austral. J. Env. Manag. 26, 63–81. doi: 10.1080/14486563.2018.1522604

Hofer, C., Cantor, D. E., and Dai, J. (2012). The competitive determinants of a firm’s environmental management activities: evidence from US manufacturing industries. J. Operat. Manag. 30, 69–84. doi: 10.1016/j.jom.2011.06.002

Hrasky, S. (2012). Carbon footprints and legitimation strategies: symbolism or action? Account. Audit. Accountab. J. 2012, 0951–3574.

Jiang, R. J., and Bansal, P. (2003). Seeing the need for ISO 14001. J. Manag. Stud. 40, 1047–1067. doi: 10.1111/1467-6486.00370

Kent, M. L., and Taylor, M. (2016). From Homo Economicus to Homo dialogicus: rethinking social media use in CSR communication. Public Relat. Rev. 42, 60–67. doi: 10.1016/j.pubrev.2015.11.003

King, A. A., and Lenox, M. J. (2001). Lean and green? An empirical examination of the relationship between lean production and environmental performance. Product. Operat. Manag. 10, 244–256. doi: 10.1111/j.1937-5956.2001.tb00373.x

Kwahk, K.-Y., and Kim, B. (2017). Effects of social media on consumers’ purchase decisions: evidence from Taobao. Serv. Bus. 11, 803–829. doi: 10.1007/s11628-016-0331-4

Lange, D., and Washburn, N. T. (2012). Understanding attributions of corporate social irresponsibility. Acad. Manag. Rev. 37, 300–326. doi: 10.5465/amr.2010.0522

Lee, K. H., Herold, D. M., and Yu, A. L. (2016). Small and medium enterprises and corporate social responsibility practice: a Swedish perspective. Corp. Soc. Responsib. Env. Manag. 23, 88–99. doi: 10.1002/csr.1366

Li, D., Huang, M., Ren, S., Chen, X., and Ning, L. (2018). Environmental legitimacy, green innovation, and corporate carbon disclosure: evidence from CDP China 100. J. Bus. Ethics 150, 1089–1104. doi: 10.1007/s10551-016-3187-6

Li, D., Zheng, M., Cao, C., Chen, X., Ren, S., and Huang, M. (2017). The impact of legitimacy pressure and corporate profitability on green innovation: evidence from China top 100. J. Clean. Prod. 141, 41–49. doi: 10.1016/j.jclepro.2016.08.123

Li, F., and Ding, D. Z. (2013). The effect of institutional isomorphic pressure on the internationalization of firms in an emerging economy: evidence from China. Asia Pacific Bus. Rev. 19, 506–525. doi: 10.1080/13602381.2013.807602

Li, L., Liu, Q., Tang, D., and Xiong, J. (2017). Media reporting, carbon information disclosure, and the cost of equity financing: evidence from China. Env. Sci. Pollut. Res. 24, 9447–9459. doi: 10.1007/s11356-017-8614-4

Liao, L., Luo, L., and Tang, Q. (2015). Gender diversity, board independence, environmental committee and greenhouse gas disclosure. Br. Account. Rev. 47, 409–424. doi: 10.1016/j.bar.2014.01.002

Liu, W., De Sisto, M., and Li, W. H. (2021). How does the turnover of local officials make firms more charitable? a comprehensive analysis of corporate philanthropy in China. Emerg. Mark. Rev. 46:100748. doi: 10.1016/j.ememar.2020.100748

Liu, Y., Liu, W., and Xu, Y. (2022). Donation or advertising? the role of market and non-market strategies in corporate legitimacy. Front. Psychol. 13, 943484–943484. doi: 10.3389/fpsyg.2022.943484

Lu, X., Ba, S., Huang, L., and Feng, Y. (2013). Promotional marketing or word-of-mouth? evidence from online restaurant reviews. Inform. Syst. Res. 24, 596–612. doi: 10.1287/isre.1120.0454

Luo, L. (2019). The influence of institutional contexts on the relationship between voluntary carbon disclosure and carbon emission performance. Account. Fin. 59, 1235–1264. doi: 10.1111/acfi.12267

Lyon, T. P., and Montgomery, A. W. (2013). Tweetjacked: the impact of social media on corporate greenwash. J. Bus. Ethics 118, 747–757. doi: 10.1007/s10551-013-1958-x

Miller, G. S., and Skinner, D. J. (2015). The evolving disclosure landscape: how changes in technology, the media, and capital markets are affecting disclosure. J. Account. Res. 53, 221–239. doi: 10.1111/1475-679X.12075

Ott, C., Schiemann, F., and Günther, T. (2017). Disentangling the determinants of the response and the publication decisions: the case of the carbon disclosure project. J. Account. Public Policy 36, 14–33. doi: 10.1016/j.jaccpubpol.2016.11.003

Rankin, M., Windsor, C., and Wahyuni, D. (2011). An investigation of voluntary corporate greenhouse gas emissions reporting in a market governance system: australian evidence. Account. Audit. Accountab. J. 2011, 951–3574.

Saunila, M., Ukko, J., and Rantala, T. (2018). Sustainability as a driver of green innovation investment and exploitation. J. Clean. Prod. 179, 631–641. doi: 10.1016/j.jclepro.2017.11.211

Schultz, F., and Wehmeier, S. (2010). Institutionalization of corporate social responsibility within corporate communications: combining institutional, sensemaking and communication perspectives. Corp. Comm. 2010, 9–29. doi: 10.1108/13563281011016813

Shao, X., Zhong, Y., Liu, W., and Li, R. Y. M. (2021). Modeling the effect of green technology innovation and renewable energy on carbon neutrality in N-11 countries? Evidence from advance panel estimations. J. Env. Manag. 296:113189. doi: 10.1016/j.jenvman.2021.113189

Stanny, E. (2018). Reliability and Comparability of GHG Disclosures to the CDP by US Electric Utilities. Soc. Env. Account. J. 38, 111–130. doi: 10.1080/0969160X.2018.1456949

Suchman, M. C. (1995). Managing legitimacy: strategic and institutional approaches. Acad. Manag. Rev. 20, 571–610. doi: 10.2307/258788

Tachizawa, E. M., and Wong, C. Y. (2015). The performance of green supply chain management governance mechanisms: a supply network and complexity perspective. J. Supply Chain Manag. 51, 18–32. doi: 10.1111/jscm.12072

Zhang, Y., and Yang, F. (2021). Corporate social responsibility disclosure: responding to investors’ criticism on social media. Internat. J. Env. Res. Public Health 18:7396. doi: 10.3390/ijerph18147396

Appendix A. Variable definition.

Keywords: social media, legitimacy pressure, carbon disclosure, green innovation, environmental management systems

Citation: Shao J and He Z (2022) How does social media drive corporate carbon disclosure? Evidence from China. Front. Ecol. Evol. 10:971077. doi: 10.3389/fevo.2022.971077

Received: 16 June 2022; Accepted: 07 July 2022;

Published: 04 August 2022.

Edited by:

Xuefeng Shao, University of Newcastle, AustraliaReviewed by:

Young-Chan Lee, Dongguk University Gyeongju, South KoreaCopyright © 2022 Shao and He. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Zhiwei He, MTc3ODA2NjQ4MDFAMTYzLmNvbQ==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.