Junliang Liu

Junliang Liu Bolin Wang

Bolin Wang Xiaogang He

Xiaogang He

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 11 October 2024

Sec. Environmental Economics and Management

Volume 12 - 2024 | https://doi.org/10.3389/fenvs.2024.1469884

The impact of environmental, social, and governance (ESG) performance gaps on firm green innovation is examined in this paper by a panel database of A-share Chinese listed companies from 2011 to 2021. Using multiple linear regression and conducting a series of endogeneity tests and robustness checks, our empirical analysis shows that firm ESG performance gaps have significantly positive effect on green innovation. Both ESG performance below historical aspiration and social aspiration levels enhance a firm’s green innovation. Confucian culture negatively moderates the positive relationship between ESG performance gaps and green innovation, suggesting that firms more influenced by Confucian culture exhibit reduced green innovation than those less influenced. Additionally, firm digitalization positively moderates the positive relationship between ESG performance gaps and green innovation, indicating that firms with higher levels of digitalization are better equipped to improve green innovation when facing ESG performance shortfalls. This study extends the existing knowledge of firm ESG performance and motivation of green innovation. The research findings offer practical insights for leveraging the motivation and capabilities of green innovation to attain firm ESG objectives.

Firms face growing challenges and risks such as environment destruction, global economic downtown, and labor relation conflicts in recent years, threatening their sustainability. Firm’s outside stakeholders especially investors have increasing interest in the information disclosed related to the environmental, social, and governance (ESG) issues (Amel-Zadeh and Serafeim, 2018). Sustainability rating agencies evaluate firm’s ESG and provide ratings or scores as proxies of firm ESG performance (Busch et al., 2016; Clementino and Perkins, 2021). Existing studies have found that good ESG performance is usually associated with better financial performance (Wong et al., 2021) because ESG performance has informational value that enables to lower capital constraints and cost of capital, and improve analyst forecast accuracy and firm financial performance (Cheng et al., 2014; Dhaliwal et al., 2011; Dhaliwal et al., 2012). However, there exist firms with low ESG performance or experiencing ESG performance shortfalls, which may hurt investors’ confidence (Broadstock et al., 2021). These firms could have the pressure of ESG performance according to their ESG objectives. Therefore, how do these firms respond to the pressure of ESG performance should be an important issue to be further explored.

As a crucial strategy to gain firm competitive advantages, manage environmental issues, and ultimately achieve the goal of sustainability, green innovation has attracted growing attention from both academia and practices (Takalo et al., 2021). In addition to the goals mentioned above, firms are motivated to greenly innovate under the pressures as well. Studies mainly identified external pressures including environmental regulation and market turbulence (Qiu et al., 2020). Less attention has been paid to investigate how internal pressures motive firm’s green innovation. In this paper, we focus on the condition that the firm faces ESG performance shortfalls and regard it as a kind of firm’s (internal) pressure. We aim to investigate how ESG performance pressures motivate firm’s green innovation and further explore the boundary conditions.

Drawing on the behavioral theory of the firm (BTOF) and previous studies on organization aspirations, that is, financial performance aspiration and social performance aspiration, we define ESG performance aspiration including both historical and social aspiration. Using a sample of Chinese A-share firms from 2011 to 2021, we empirically examine how ESG performance gaps (below historical and social aspirations) influence firm green innovation, and how Confucian culture and firm digitalization moderate the above relationship. The empirical results demonstrate that ESG performance gaps as firm internal pressures motivate firms to do green innovation, showing the positive effect of ESG performance gaps on firm green innovation. Exploring the boundary conditions by examining the moderating roles of Confucian culture and firm digitalization, we find that Confucian culture decreases the firm’s motivation to greenly innovate and thus negatively moderates the positive relationship between ESG performance gap and green innovation, and firm digitalization increases a firm’s capability to take risks and positively moderates the positive relationship between ESG performance gap and green innovation. Further analyses including the endogeneity test and robustness test are adopted to further make sure the stability of empirical results.

This research makes three major theoretical contributions. First, we introduce ESG performance aspiration based on the studies of performance aspiration (Greve, 1998), which is not only an important firm ESG objective but also a reference point for firm to understand and interpret its ESG. This study extends current studies on ESG performance by paying attention to its aspiration level, which enables to better define and identify good/high or bad/low ESG performance. Second, we fill up the research gap wherein how firms respond to its ESG performance (Clementino and Perkins, 2021). Specially, we investigate how firms take such strategies as green innovation to respond to ESG performance gaps, that is, the ESG performance below its aspiration levels. It reveals how ESG performance shapes firm strategies. Finally, this research also contributes to existing green innovation studies by further exploring how internal pressures motive firms to take green innovation strategies. Different from existing studies on exploring the relationships between ESG performance and green innovation, we identify the circumstance when the firm faces ESG performance gaps and the impact on its green innovation. This study helps to avoid the causal inversion issue when exploring the relationship between ESG and green innovation as well. In addition, we also identify boundary conditions to investigate the motivation and capability of a firm to greenly innovate during the ESG performance gaps.

This paper is structured as follows. Section 2 provides the theoretical foundation of ESG performance and defines ESG aspiration, followed by theoretical analysis and hypothesis development. Section 3 states the research design including sample and data collection, variable definitions and measurements, and empirical model construction. Empirical analyses including model testing, endogeneity test, and robustness test are presented in Section 4. We conclude this study and discuss managerial implications in Section 5. Finally, limitation and future directions are discussed in Section 6.

Listed firm has been increasingly ESG-rated by third-party institutions (Shanaev and Ghimire, 2022). ESG performance is recognized as an important part of firm performance by the public as well. As an aggregated evaluation system on a firm’s responsibility taking, sustainable development, and ethical investment, ESG performance has attracted substantial attention from academia including the domains of finance, accounting, and management. Existing studies have mainly investigated the formation of ESG performance, the influence of ESG performance on firm performance, and the firm’s responses to its ESG performance.

ESG performance is generally evaluated by different agencies and measured by the ESG rating scores. ESG rating scores have been seen as the evaluation of a firm based on a comparative assessment of its performance on environmental, social, and governance issues (SustainAbility, 2018). The ESG rating provides a comparable data source of a wide range of CSR-related practices, policies, and performances (Crane et al., 2019), increasingly needed by the public especially investors to meet the information demand for the firm’s compliance to the ESG properties (Billio et al., 2021). Due to the rating scores provided by different agencies, a firm’s ESG ratings are usually disagreed. Increasing scholarly attention has been paid to the phenomenon of ESG rating disagreement (e.g., Avramov et al., 2022; Billio et al., 2021; Tsang et al., 2023). The ESG rating disagreement brings investors uncertainty to evaluate a firm’s true ESG performance, and therefore has impact on the firm’s risk-return trade-off, economic welfare, and social impact (Avramov et al., 2022). Billio et al. (2021) also provided evidence to show that heterogeneous rating criteria across agencies can lead ESG rating disagreement. The ESG rating disagreement disperses the effect of preferences of ESG investors on asset prices but has no impact on firm financial performance (Billio et al., 2021). Therefore, scholars criticize the ESG rating system for the lack of the reliable measurement of true ESG performance as well (Avramov et al., 2022).

In addition to the discussion and criticism on ESG performance, existing studies mainly focus on the consequences of ESG performance, especially how ESG performance influences firm’s financial performance and the sequential behaviors or actions. Based on the evidence from more than 2,000 empirical studies of ESG, Friede et al. (2015) found that nearly 90% of these studies report the non-negative relationship and there are still some studies that found the negative relationship between ESG performance and financial performance. ESG performance has been informational value (Dimson et al., 2020; Gyonyorova et al., 2023) with external and internal mechanisms of the positive effect on firm performance (e.g., Lian et al., 2023; Wong et al., 2021; Zhang et al., 2024). From external perspective, good ESG performance could lower a firm’s risk and information asymmetry, thus alleviating the concerns from investors. From internal perspective, ESG certification could lower a firm’s cost of capital and reduce the financial constraint. Good ESG performance is also beneficial for strengthening a firm’s stakeholder relationships, including improving employee and consumer loyalty, and gaining investor support (Clark et al., 2015). Furthermore, research has examined the relationship between ESG performance and firm’s actions or behaviors. Clementino and Perkins (2021) adopted a qualitative inquiry to investigate firm’s responses to ESG ratings. A two-dimensional topology, that is, active vs. passive, or conformity vs. resistance, has been proposed to capture how firms react to ESG ratings differently. Studies have also found that ESG performance has positive influence on firm innovation, especially green innovation (Lian et al., 2023; Wong et al., 2021; Zhang et al., 2024).

Based on the brief review on ESG performance, we identified two major research gaps. First, how a firm understands and interprets its ESG performance has been paid less attention. Existing studies mainly adopt stakeholder theory and take the perspective of outside stakeholders, to examine how a firm’s financial performance is affected by their evaluations. ESG ratings of a firm vary and disagree across agencies, which not only bring uncertainties to investors but also are not able to reflect true ESG performance. It is essential for a firm to deeply understand its ESG ratings and proactively respond to it, which benefits for shaping positive outside stakeholder’s attitude toward its ESG. Second, how firms respond to the ESG performance has been under-researched as well (Clementino and Perkins, 2021). Existing studies focus more on the informational value of ESG performance and investigate positive relationships between ESG performance and firm strategies such as digital transformation and (green) innovation (Lian et al., 2023; Wong et al., 2021; Zhang et al., 2024). However, these studies ignored how firms understand their ESG performance and proactively take strategies as responses. Furthermore, in the relationships between ESG performance and firm strategies, there may exist casual inversion issues. For example, green innovation could also inversely help a firm to gain better ESG certification (Zheng et al., 2022). Therefore, exploring how firms proactively take strategies to respond its ESG performance according to their understanding and interpretation helps to untangle accurate relationships between ESG performance and firm strategies.

In order to fill above research gaps, we propose ESG performance aspiration to help better understand ESG performance, especially how a firm understand and interpret its ESG performance. Firms always set various objectives as direction for their growth and development, including both financial and non-financial objectives (Xu and Zeng, 2020). Good financial performance and non-financial performance, that is, corporate social performance (hereafter CSP), demonstrate the reliability and responsibility of a firm. Therefore, firms may have their desired performance objectives, which help them to set goals and better understand their current performance. Existing studies have adopted the aspiration level as a type of objective, which indicates a reference point for decision-making (Kameda and Davis, 1990). Both financial performance and non-financial performance (CSP) aspiration have been proposed (e.g., Greve, 1998; Xu and Zeng, 2020). Accordingly, we define ESG performance aspiration as a firm’s desired ESG performance level in comparison with its historical level and other firms’ level, that is, historical aspiration and social aspiration levels. ESG performance aspiration could be seen as a goal or reference point of a firm on its ESG, enabling the firm to interpret and make sense of its current ESG performance and make responses to it as well.

In order to explore how ESG performance aspiration influences the firm’s green innovation, we draw on the behavioral theory of the firm (hereafter BTOF). In the existing BTOF literature, performance feedback has become an important context, and numerous scholarly attention has been paid to study its effect on the firm’s decision outcomes (e.g., Cyert and March 1963; Greve, 1998). Previous studies mainly focus on how performance relative to aspiration levels affects firm’s strategies and actions like organizational change, acquisitions, and innovation (e.g., Chen and Miller, 2007; Greve, 1998; 2003; Iyer and Miller, 2008). BTOF holds the view that performance feedback, especially performance below the aspiration level (negative attainment discrepancy), could lead to risk-takings. Performance below the aspiration level is always seen as performance shortfall or failure, which increases the probability of problematic searching to repair the performance gaps (Cyert and March 1963; Levinthal and March 1993; Greve, 1998). In addition, CSP below aspiration levels also motivates a firm to take actions for reputation repairing or even surviving (Xu and Zeng, 2020).

Accordingly, we focus on the conditions when ESG performance is below aspiration levels including both historical aspiration and social aspiration, that is, ESG performance gap. When ESG performance is below aspiration levels, a firm will attempt to make the change as a response due to the performance pressure. Good ESG performance could not only decrease the cost of capital to reduce financial constraint but also gain support from stakeholders, whereas ESG performance gap could threat a firm’s reputation and legitimacy. Therefore, firms are motivated to take risky actions or strategies to recover their ESG performance. Both historical aspiration and social aspiration levels are reference points (Greve, 1998), for a firm to make the change for attaining improvement in its ESG performance. When a firm’s ESG performance is lower than its peers (similar others), it could perceive pressure and take actions as responses. When a firm’s ESG performance is below its historical level, changes taken by the firm occur, as well from the learning perspective. Therefore, when ESG performance is below aspiration levels, a firm has motivation to take risky actions or strategies.

The BTOF literature has interest on exploring the influence of performance feedback on R&D expenditures and innovations (Gavetti et al., 2012). As a type of innovation, green innovation plays an important role in maintaining environmental management for organizations and communities (Aguilera-Caracuel and Ortiz-de-Mandojana, 2013; Arenhardt et al., 2016; Takalo et al., 2021; Wang et al., 2019; Yang et al., 2016). Green innovation generally includes both green product/service innovation and green process innovation (Ambec et al., 2013; Porter, 1991; Tang et al., 2018). It has been gradually regarded as a firm’s proactive and forward-looking strategy to achieve firm sustainability in the long run (Demirel and Danisman, 2019; Li C et al., 2023; Ren et al., 2023; Takalo et al., 2021). In addition, green innovation also enables a firm to improve legitimacy, get competitive advantage, support its strategic goals, and ultimately enhance organizational performance (Ren et al., 2023; Roy and Khastagir, 2016; Takalo et al., 2021; Yang et al., 2016).

Considering the long-term oriented purpose, investing in green innovation could lead to increase a firm’s cost and risk as well (Chen YS, 2008; Li et al., 2023a). Therefore, green innovation generally requires both external and internal forces to facilitate (Li et al., 2023b). Qiu et al. (2020) found that environmental regulation and market turbulence motive the firm to greenly innovate due to the pressures. For internal forces, Yuan and Cao (2022) summarized that resource and knowledge, and organization internal management can influence firm’s green innovation. To be specific, scholars have explored that the positive influence of ESG ratings on firm’s green innovation (He et al., 2022; Lian et al., 2023; Tan and Zhu, 2022). However, when a firm meets ESG performance gap, it also has motivation to do such risk-taking actions as green innovation for better ESG performance. Therefore, we propose the following hypotheses:

Hypothesis 1. ESG performance gap (when ESG performance is below historical aspiration level) enhances firm’s green innovation.

Hypothesis 2. ESG performance gap (when ESG performance is below social aspiration level) enhances firm’s green innovation.

The Confucian culture is generally described as a belief system, tradition, philosophy, or way of life, which has been founded by Confucius and his disciples for more than 2,000 years (Feng et al., 2021; Koczkas, 2023). Confucian culture involves such rich principles and virtues as ren (humaneness), yi (righteousness), li (propriety), zhi (wisdom), and xin (trust). Being as a dominant social value and logic, Confucian culture has rooted in societies of some Eastern Asia countries, especially China (Koczkas, 2023). Confucian culture plays an important role in understanding the behavioral logic of Chinese people (Li et al., 2020; Wang and Juslin, 2009) and is argued to influence organizations and their management practices (Hofstede and Bond, 1988).

Confucian culture has been explored to influence firm’s innovation including green innovation. However, the empirical results of existing studies are compound, which may be due to the different understandings or operations of Confucian culture and innovation (Koczkas, 2023). In this paper, we argue that Confucian culture could negatively impact on firm’s green innovation for several reasons. First, some specific principles in Confucian culture like high power distance and hierarchy have been seen as not enabling to provide proper atmosphere and environment for innovation (Koczkas, 2023). Second, some beliefs from Confucian culture may hinder people to take risks (Hilary and Hui, 2009). Li et al. (2024) found that the thoughts of “golden mean” and “peace is essential” in Confucian culture may lead to the organizations to be conservative, and therefore, they are reluctant to take risk for innovation. Third, Confucian culture emphasizes collectivism, in line with the characteristic of Chinese social environment. Collectivism has been found to reduce a firm’s risk-bearing capability and consequently to reduce to the motivation of a firm to make change (Li et al., 2013; Li et al., 2024). In addition, Weber (1958) also argued that Confucian culture is not beneficial for innovation and therefore negatively impacts on the economic development. Therefore, in the context of ESG performance gap, the firm which believes more in Confucian culture is more likely to be more conservative and not willing to take risks. So, we propose the following hypothesis:

Hypothesis 3. Confucian culture negatively moderates the positive relationship between ESG performance gap and firm’s green innovation. When a firm is more influenced by Confucian culture, it would reduce green innovation compared with those who are influenced by Confucian culture less.

As is required in digital economy for industrial development and national economic growth (Zheng et al., 2022; Guo et al., 2023), digitalization has become an increasingly important strategy for firms to gain sustainability and fit economic transformation. Digitalization refers to the application of digital technologies and digitalized information or resources to create values for firms in new approaches (Gobble, 2018; Guo et al., 2023). Existing studies have investigated that digitalization can elevate firm performance through reducing costs and improving operational efficiencies (Heredia et al., 2022; Gobble, 2018; Zhai et al., 2022). Innovation, especially green innovation, has been found as an important mechanism to unfold how digitilization improves firm performance (e.g., Guo et al., 2023; Peng and Tao, 2022).

Based on resource-based view including dynamic capability theory, scholars found that firm digitalization promotes firm green innovation (Guo et al., 2023; Li et al., 2023b; Ning et al., 2023). From this perspective, green innovation requires certain technological capabilities to facilitate (Tsai and Liao, 2017; Wu et al., 2020), and digitalization has been seen as an important technological capability that enables firms to apply digital technologies to improve their existing business operations (Heredia et al., 2022). Similarly, BTOF also holds the perspective that organizational change or risk-taking is jointly determined by motivation, capability, and opportunity (Greve, 1998; Miller and Chen, 1994). We have argued that the ESG performance gap motivates a firm to improve green innovation. In this context, when a firm is with a higher level digitalization, it has more capability to take risks or make the change, and therefore is more likely to improve green innovation. Therefore, we propose the following hypothesis:

Hypothesis 4. Firm digitalization positively moderates the positive relationship between ESG performance gap and firm’s green innovation. A firm with higher level digitalization is more likely to have capabilities to improve green innovation when facing ESG performance gap.

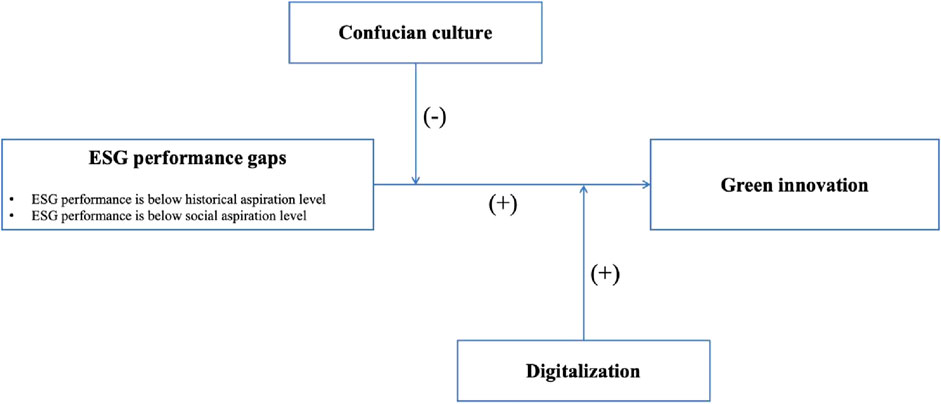

Figure 1 presents the research model and summarizes the hypotheses of this study. As the model shows, the main effect to be explored is the positive relationship between ESG performance gaps and firm green innovation. From both motivation and capability perspective, we aim to explore the negative moderating effect of Confucian culture and positive moderating effect of digitalization, respectively.

Figure 1. Research model and main hypotheses of this study.

We use a sample of A-share firms listed on the Shanghai and Shenzhen Stock Exchanges in China to test our hypotheses. The sources of data used in this paper are as follows. ESG-related data are from Sino-Securities Index Information Service (Shanghai) (www.chindices.com). Financial variables are collected from the Wind database and China Stock Market and Accounting Research (CSMAR) database. Data on patents and Confucian culture are from the Chinese Research Data Service (CNRDS).

The raw data are processed as follows: listed firms under special treatment (ST) or particular transferred (PT) are excluded, and sample firms from financial and insurance industries are also dropped, as well as excluding the firms with missing values of the main variables during the sample period. In order to minimize the effect of outliers on the regression results, all the continuous variables are winsorized at the upper and lower 1% quartiles. Finally, we obtain 3349 A-share listed firms with a total of 22,134 firm-year observations from 2011 to 2021.

The ESG performance gaps include both ESG performance below historical aspiration (HisGap) and social aspiration (SocGap). Based on the previous research, the commonly used method is to define industry expectation gaps through social comparison (Chen WR, 2008; Greve, 2003; Harris and Bromiley, 2007; Xu and Zeng, 2020). However, decision-makers may also compare with their “past selves.” So, some scholars have applied comparisons with historical expectations (Chrisman and Patel, 2012). Therefore, the ESG performance gap in this paper is measured by the difference between a company’s actual ESG performance and its ESG performance aspiration. The performance aspiration can be based on the average level of the company’s historical performance or the average level of the industry performance (Chen YS, 2008; Greve, 1998; Xu and Zeng, 2020). The greater the difference between actual performance and aspiration level, the more significant the gap.

For the historical aspiration level of ESG performance, we measured it by using the weighted average of the firm’s actual performance in period t-2 (weight of 0.4) and period t-1 (weight of 0.6). If the difference between the actual ESG performance and historical aspiration is negative, the firm is considered to be in a state of historical ESG performance gap. The same method is used to calculate the social aspiration level of ESG performance. The industry expectation level is the weighted average of the median performance of the industry in period t-2 (weight of 0.4) and period t-1 (weight of 0.6). If the difference between the actual ESG performance and social aspiration is negative, the firm is considered to be in a state of social ESG performance gap. The data processing for ESG performance gap uses a truncated dummy variable approach, where the absolute value of the actual difference is taken for the performance gap data, and values above the aspiration level are set to 0 (Chen WR, 2008; Xu and Zeng, 2020; Wang, 2024).

The ESG performance data in this paper comes from the Shanghai Huazheng Index (www.chindices.com), including environmental (E-score), social (S-score), and corporate governance (G-score), and the final comprehensive ESG evaluation score (Huang, 2023; Li and Wang, 2024). The Huazheng ESG rating assigns the evaluated entities a rating from “AAA” to “C” across nine levels. The total ESG score, primary indicators, secondary indicators, and tertiary indicators’ scores are all standard scores ranging from 0 to 100. Higher scores indicate better performance in the respective indicators.

Green innovation (GreenInno): as policy evaluation often requires an outcome perspective, the number of green patents serves as both the result of a firm’s green innovation activities and an indicator of a firm’s green innovation intensity. Therefore, this study uses the natural logarithm of the number of green patent applications plus one as a proxy variable for green technology innovation (Petruzzelli et al., 2011; Wang et al., 2019).

Two moderating variables are adopted in this paper, the Confucian culture of the region where the firm is located (Confu) and firm digitalization (Digital). This paper refers to the approach from previous research to construct an index of Confucian cultural intensity using a geographic proximity distance model (Li et al., 2020). By obtaining the latitude and longitude of the registered locations of listed companies and the historical number and coordinates of Confucian temples, we calculate the natural logarithm of the number of Confucian temples within a 200 km radius of the company’s registered location for the given year (Confu) as a proxy variable for the influence of Confucian culture (Li et al., 2020). The greater the number of Confucian temples per unit distance, the stronger the influence of Confucian culture on the firm. Referring to the study by Guo et al. (2023), firm digitalization (Digital) is measured in this paper by the digital investment component of a firm’s intangible assets. Specifically, when the detailed items of intangible assets include keywords related to digital transformation technologies such as software, network, client, management system, intelligent platform, and related patents, these detailed items are defined as digital technology intangible assets. The sum of multiple digital technology intangible assets for the same firm in the same year is used as a proxy variable for Digital (Song et al., 2022).

Referring to the previous research, a series of control variables are selected in this paper as firm-level determinants of firm innovation. Size is measured as the logarithm of total assets (Díaz-Díaz et al., 2008), and firms with substantial assets can allocate more resources to innovation (Wu et al., 2022). FirmAge is the natural logarithm of firm age, calculated by subtracting the year of incorporation from the current year. Leverage (Lev) is defined as the ratio of total debt to total assets in this paper (Benkraiem et al., 2023). We also control for return on equity (ROE) and firm ownership concentration (TOP1), which are crucial to corporate innovation (Wang et al., 2020), among which TOP1 is measured by the proportion of shares held by the largest non-CEO shareholder. Based on the prior research, audit quality positively affects a firm’s technological innovation (Nguyen et al., 2020). Therefore, we also control for related variables in this paper. If the listed firm is audited by one of the Big 4 audit firms (PricewaterhouseCoopers, Deloitte Touche Tohmatsu Limited, Ernst and Young, and Klynveld Peat Marwick Goerdeler), Big4 equals “1”; otherwise, it equals “0” (Li and Wang, 2024). Characteristics of the executive team, such as average age (TMTAge), environmental background (EP_Execu), and CEO duality (Dual), also influence their investment in green innovation (Wang et al., 2022; Pascariati and Ali, 2022; Sun et al., 2023). Table 1 presents the detailed definitions of all variables.

Table 1. Names of control variables and calculation methods.

In order to test the research hypothesis of this paper, we estimate the following ordinary least squares (OLS) specification with robust standard errors for firm i and year t. The fixed-effect regression model is constructed to investigate the impact of ESG performance gap on firm’s green innovation.

In Equation 1, β0 is the constant term added to the model, GreenInnoi,t-1 represents green innovation (GreenInno) of firm i in year t+1, GapESGi,t means historical ESG performance aspiration gap (HisGap) and industry ESG performance gap (SocGap) of firm i in year t, and Moderatorsi,t and Controlsi,t represent all moderators and control variables as explained in the previous section, respectively. Interactioni,t represents the interaction terms of the independent variable and moderators.

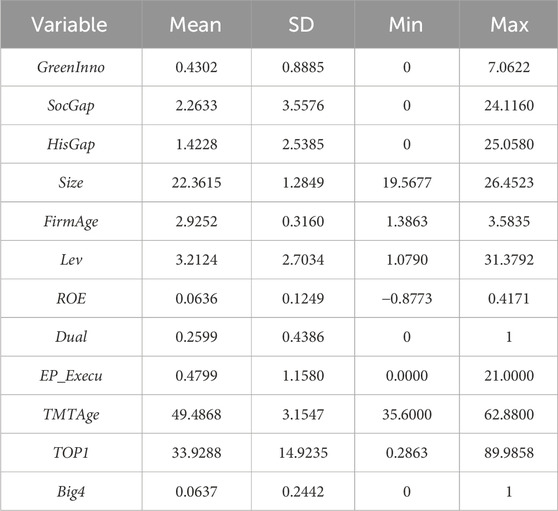

Table 2 presents the descriptive statistics for the main research variables in this study. The results indicate that the mean value of HisGap is 1.4228, and the mean value of SocGap is 2.2633. This suggests that the sampled companies perceive a greater gap in ESG performance than their industry peers. Regarding the control variables, the mean value of Big4 is 0.0637, indicating that 6.77% of the sampled companies are audited by one of the Big 4 accounting firms. Approximately 26% of the executives hold dual roles as both chairman and CEO, and about 48% of the executive teams have environmental experience.

Table 2. Descriptive statistics.

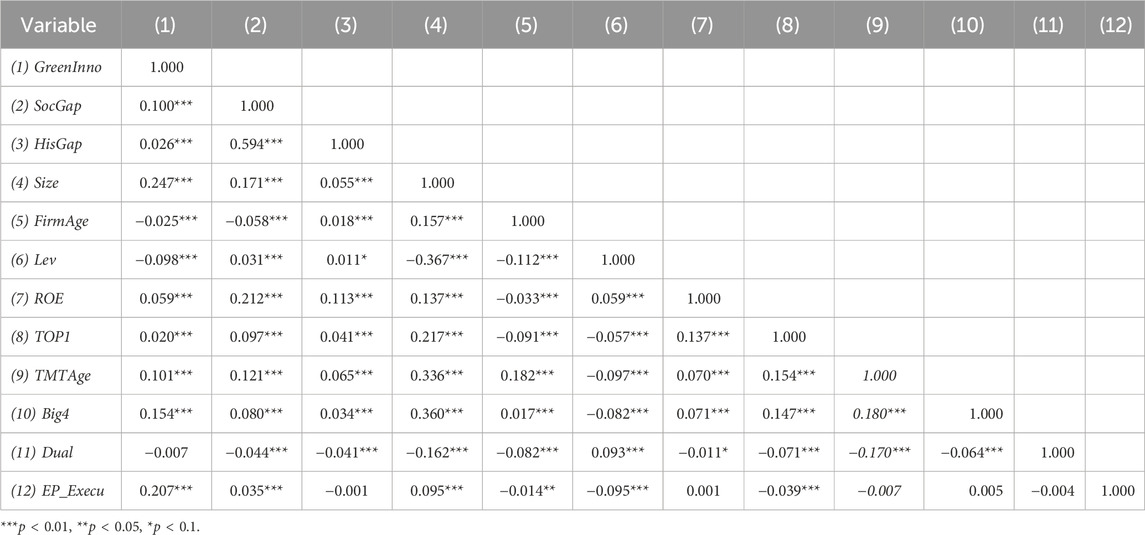

Table 3 shows the correlation results among the main variables. The results indicate that GreenInno has a significant positive correlation with both SocGap and HisGap (r = 0.100, p < 0.01; r = 0.026, p < 0.01). To further validate the research hypotheses of this study, the following sections will conduct statistical tests on the relationships among these variables.

Table 3. Correlation analysis.

In this paper, we perform variance inflation factor analysis to avoid the problem of multicollinearity among variables before formal regression (Dalal and Thaker, 2019), and the results show that the maximum and minimum values of VIF are 1.68 and 1.01, and the mean value is 1.22, which are all less than 10, so multicollinearity is not a major concern.

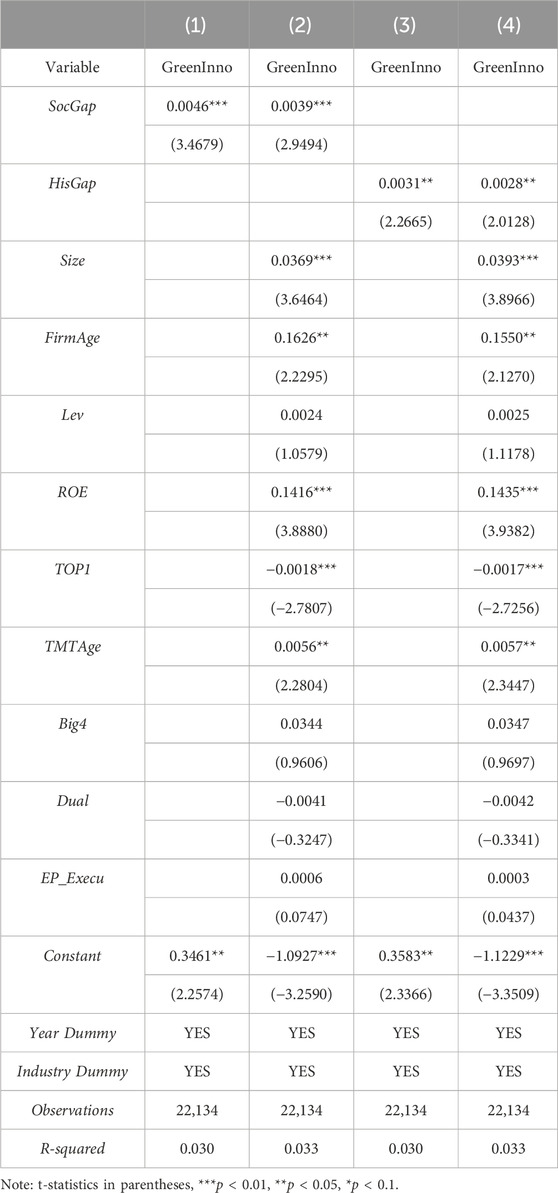

As shown in the first column of Table 4, the regression coefficient between GreenInno and SocGap is significantly positive (β = 0.0046, p < 0.01). The second column presents the regression results with control variables included, and the coefficient remains significantly positive (β = 0.0039, p < 0.01). The third and fourth columns show the regression results between GreenInno and HisGap (β = 0.0031, p < 0.05; β = 0.0028, p < 0.05). These findings support Hypothesis 1 and Hypothesis 2, indicating that ESG performance gaps, including ESG performance below both social aspiration and historical aspiration level, enhance a firm’s green innovation.

Table 4. Benchmark regression results.

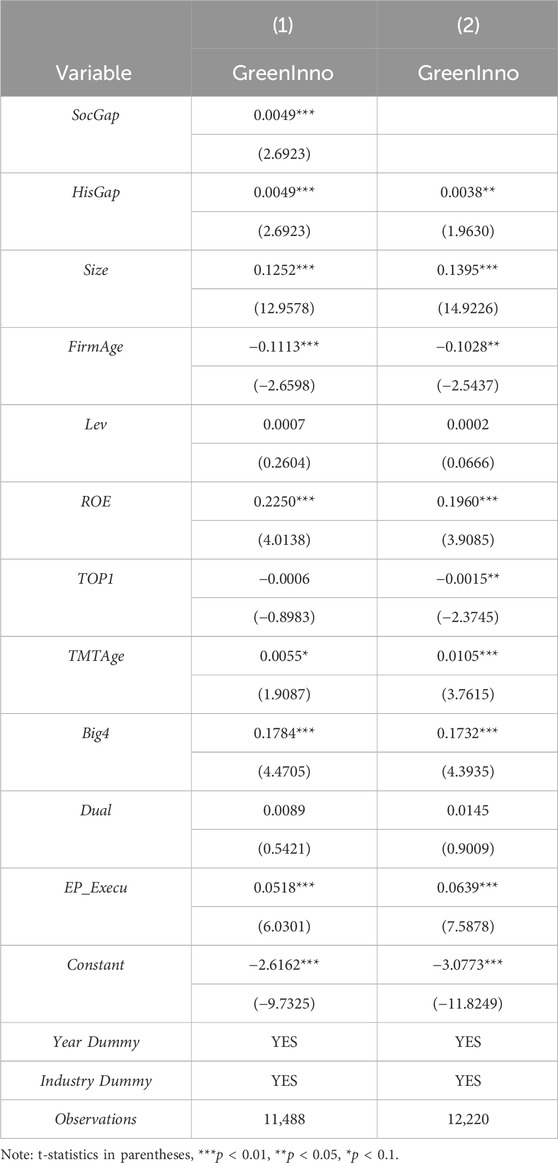

The propensity score matching (PSM) method is used in this paper to address potential issues of omitted variables and sample selection bias (Bai, 2011). To ensure comparability between the treatment and control groups, we group the samples based on the median values of HisGap and SocGap. We then use the nearest neighbor matching method within a caliper, matching samples at a 1:1 ratio. After matching, the sample sizes for the treatment and control groups are 11,488 and 12,220, respectively, indicating a good matching effect.

As shown in the first and second columns of Table 5, the results demonstrate that after using the PSM method to control for potential endogeneity issues, the regression coefficients of SocGap and HisGap with GreenInno are significantly positive (β = 0.0049, p < 0.01; β = 0.0038, p < 0.05), that is, H1a and H1b remain valid.

Table 5. PSM test results.

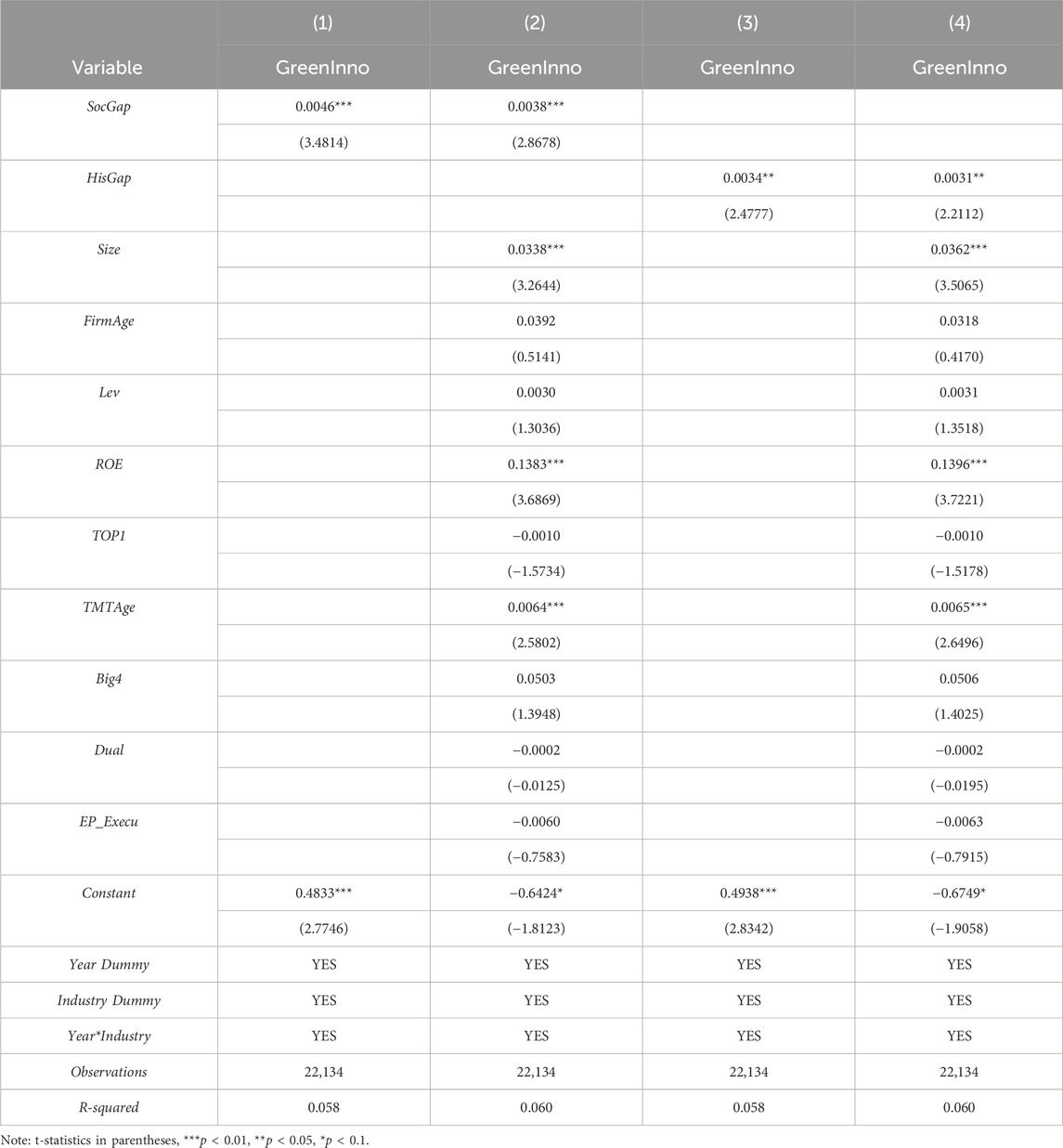

In the previous regression models, in this paper, time-fixed effects and industry-fixed effects are controlled for to account for their potential impact on the results. However, over time, the systemic structure of industries and their external environments undergoes dynamic changes (Amore et al., 2017), leading to differences in the development of various industries over time, which in turn affects firms’ green technology innovation. To mitigate the impact of this factor on the research conclusions, in this paper, the variations in different industries are further controlled for over time. The regression results are shown in Table 6. The results indicate that after considering this factor, the conclusions of this paper remain robust.

Table 6. Controlling for industry changes over time.

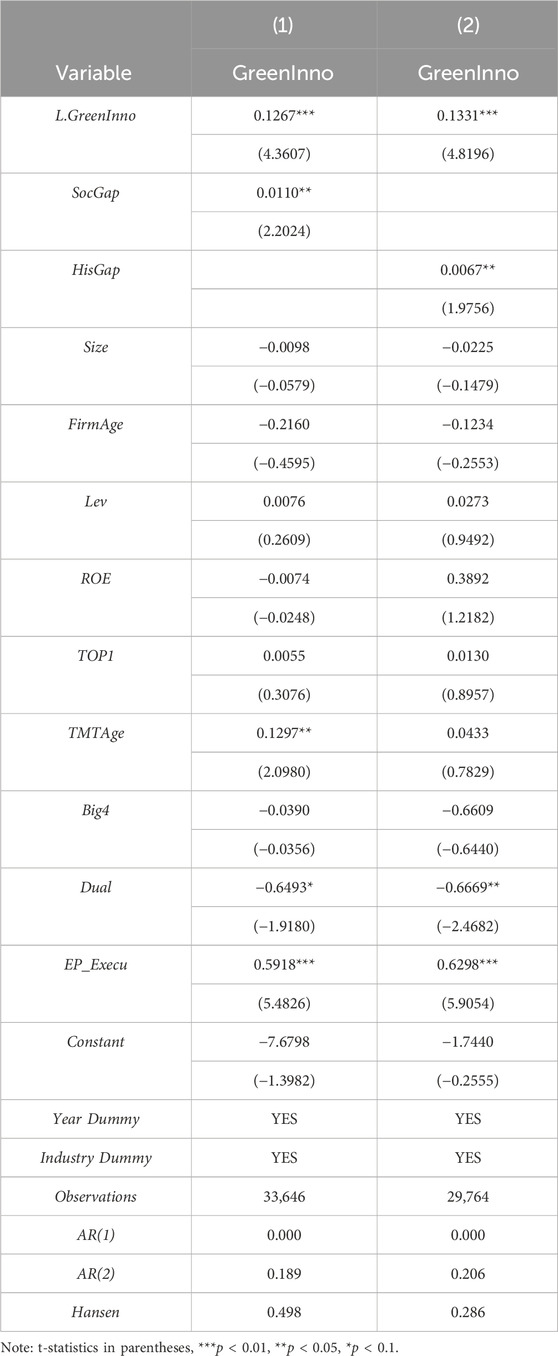

There are issues of serial correlation in firm-level green innovation. To address this, we further employ the system GMM regression to test the robustness of the previous conclusions (Khattak et al., 2022). The lagged dependent variable (L. GreenInno) is selected as the GMM instrument variable for regression estimation, with the results presented in Table 7. As the test statistics shown in Table 7, the AR (1) p-value is less than 0.1, and the AR (2) p-value is greater than 0.1, which indicates that there is only first-order autocorrelation in the disturbance term of the system GMM estimation, with no higher-order autocorrelation, thus meeting the conditions for using the system GMM. The Hansen p-value is greater than 0.1, indicating the validity of the instrumental variable. The regression results in the two columns of Table 7 show that the regression coefficients of SocGap and HisGap are both significantly positive at the 5% level (β = 0.0110, p < 0.05; β = 0.0067, p < 0.05), indicating that after considering the serial correlation characteristic of green technological innovation (controlling for L. GreenInno and its resulting endogeneity), the promoting effects of SocGap and HisGap on GreenInno still exist, confirming the robustness of the previous conclusions.

Table 7. GMM dynamic panel analysis.

Table 8 presents the results of the moderation tests. From the regression results in columns one to four, it can be observed that the regression coefficients of SocGap and GreenInno are consistently positive and significant, thus confirming Hypothesis 1 and Hypothesis 2. Columns two and three introduce the moderating variables Confu and Digital, along with the interaction terms interconfus and interdigitals with the independent variable SocGap. Column four represents the full model. The regression coefficients of the interaction terms (β = −0.0038, p < 0.01; β = 0.0006, p < 0.01) indicate that Confu negatively moderates the positive relationship between SocGap and GreenInno, whereas Digital positively moderates this relationship. Therefore, hypotheses 2 and 3 are supported. Confucian culture negatively moderates the positive relationship between ESG performance social gap and firm’s green innovation, and firm digitalization positively moderates the positive relationship between ESG social performance gap and firm’s green innovation.

Table 8. Examination of moderating effect-SocGap.

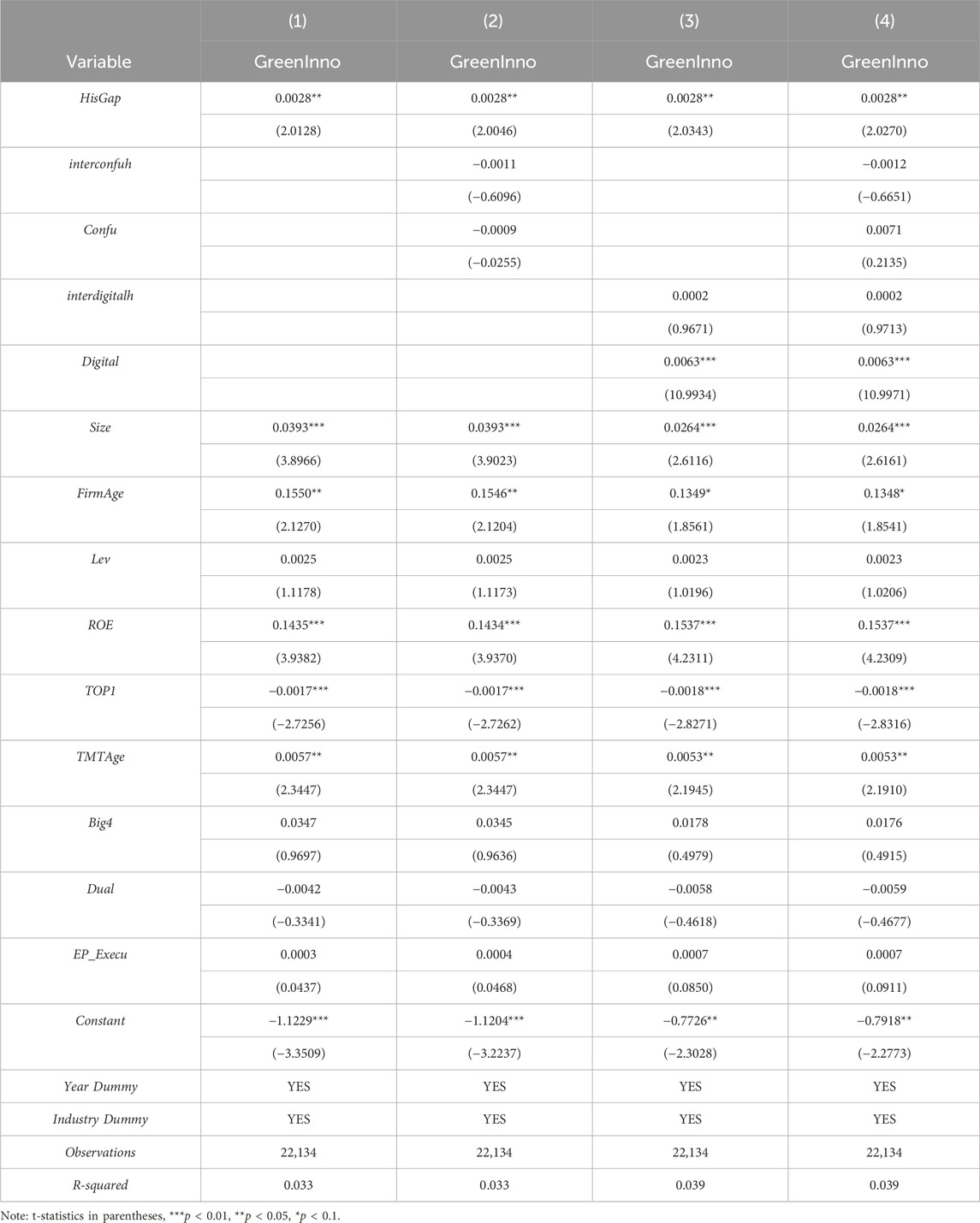

From the regression results in columns one to four of Table 9, it can be observed that the regression coefficients of HisGap and GreenInno are consistently positive and significant, thus confirming H1a and H1b. Columns two and three introduce the moderating variables Confu and Digital, along with the interaction terms interconfuh and interdigitalh with the independent variable HisGap. Column four represents the full model consisting all variables. The regression coefficient of the interaction term interconfuh is negative but not significant (β = −0.0012, p > 0.1) and that of interdigitalh is positive but not significant (β = 0.0002, p > 0.1), indicating that for ESG performance historical gap, Hypothesis 3 and Hypothesis 4 are not supported.

Table 9. Examination of moderating effect-HisGap.

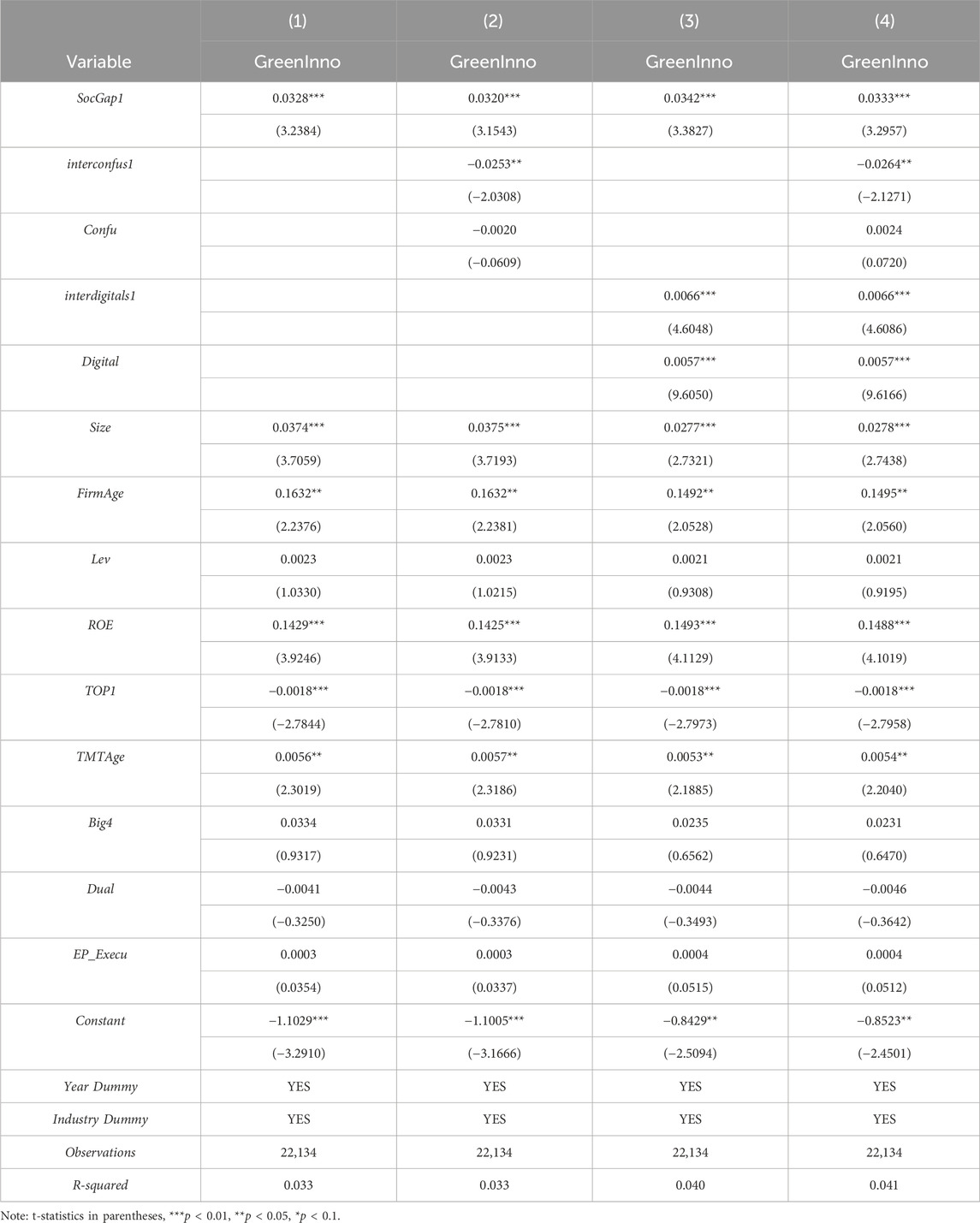

Based on the study by Gao et al. (2022), when the ESG performance rating is C-CCC, ESG performance is assigned a value of 1; when the rating is B-BBB, ESG performance is assigned a value of 2; and when the rating is A-AAA, it is assigned a value of 3. Accordingly, the social gap for ESG performance SocGap1 is recalculated, interconfus1 and interdigitals1 represent the interaction terms between Confu and Digital with SocGap1, respectively. The regression results in Table 10 indicate that all hypotheses are validated.

Table 10. Changing the measurement of the independent variable SocGap1.

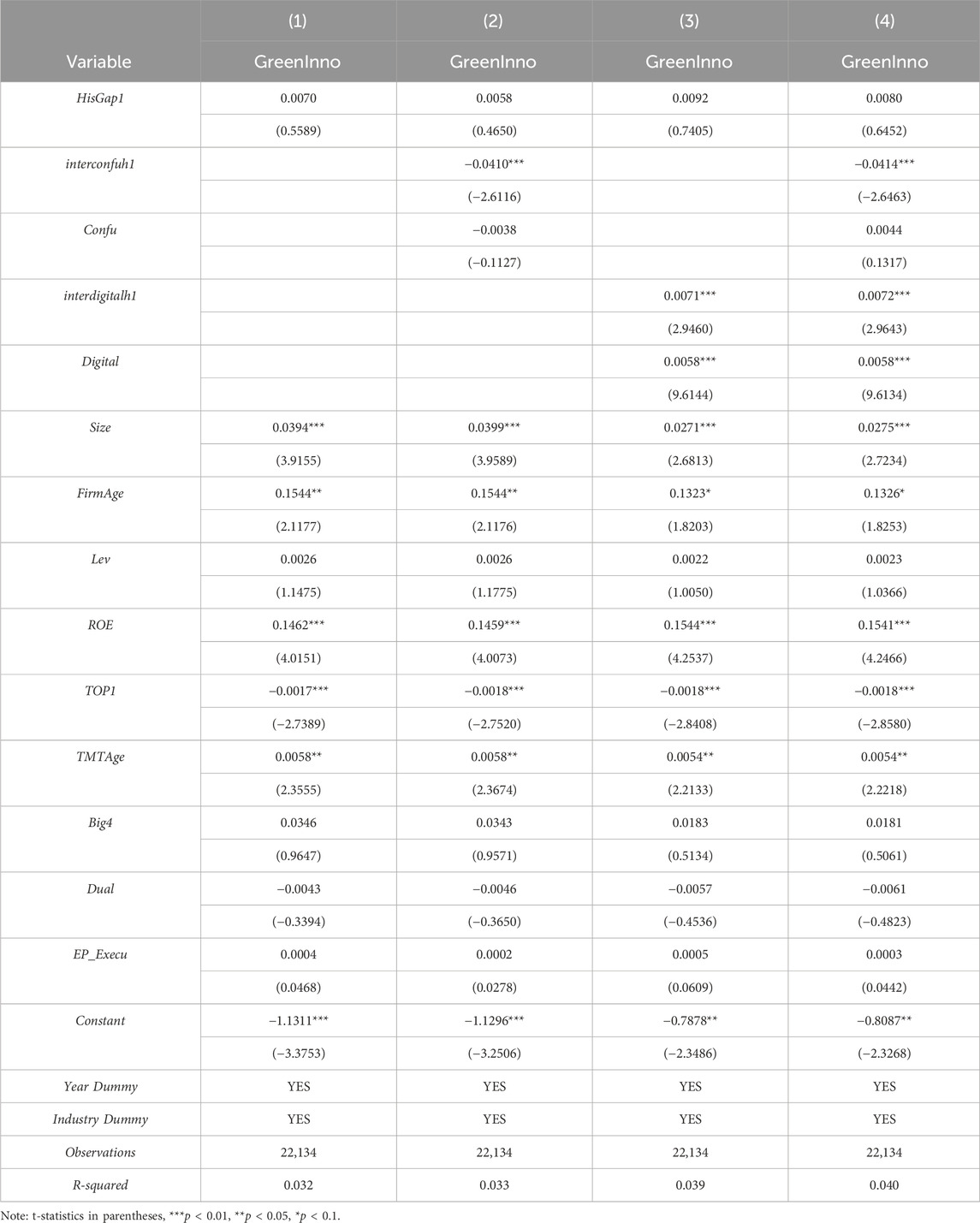

Similarly, Table 11 recalculates HisGap1, interconfuh1, and interdigitalh1. The regression results in Table 9 also indicate that the previous conclusions are robust.

Table 11. Changing the measurement of the independent variable HisGap1.

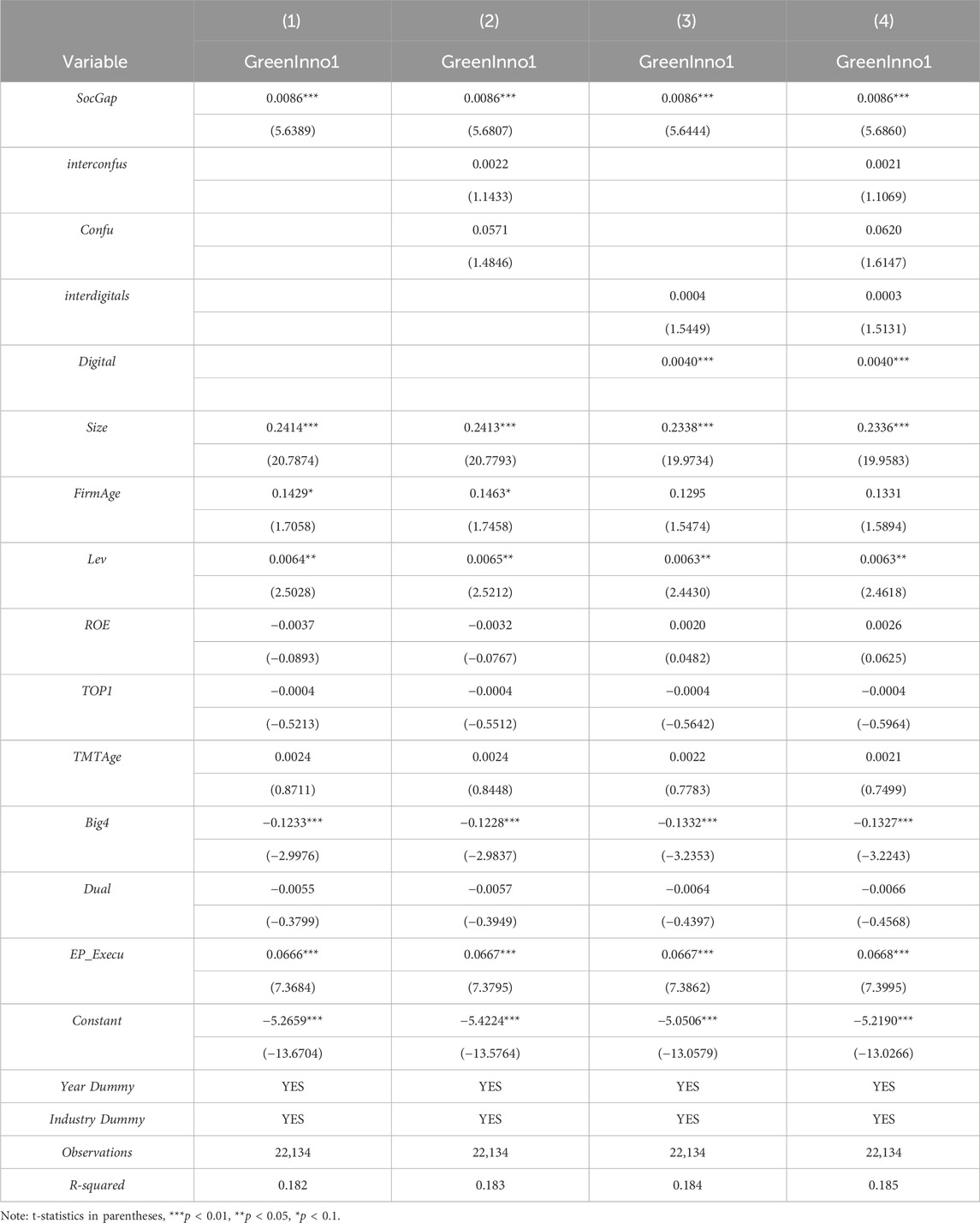

According to Chang et al. (2015) and Lian et al. (2023), green innovation can also be measured by the number of green patents granted to a company within 1 year. This metric is considered to more accurately reflect the firm’s actual innovation capabilities during the current period. Table 12 re-examines the relationship using the natural logarithm of the number of patents granted (GreenInno1) as the dependent variable and SocGap as the independent variable. The results remain consistent with previous findings.

Table 12. Changing the measurement of the dependent variable SocGap.

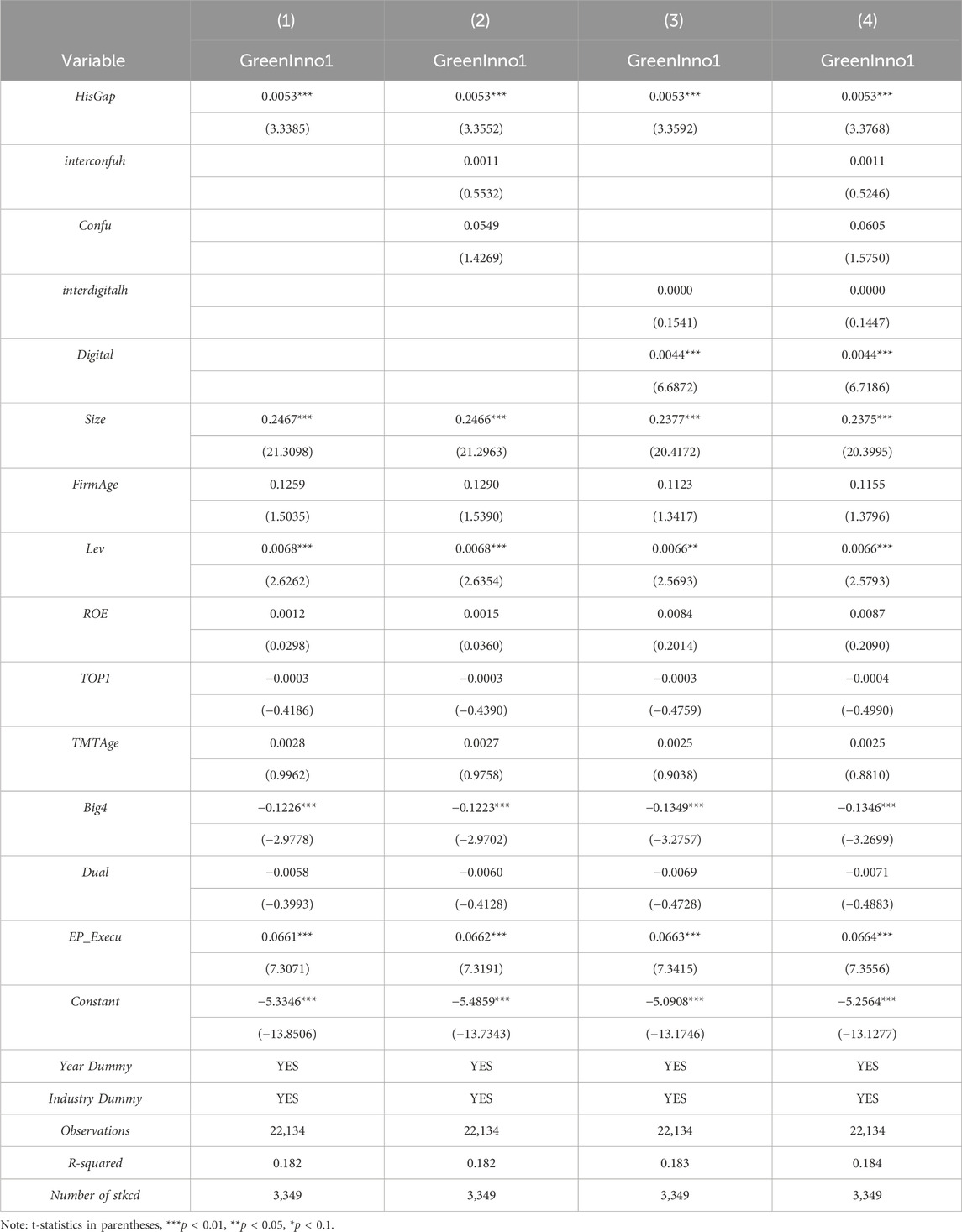

Table 13 represents the relationship using the natural logarithm of the number of patents granted (GreenInno1) as the dependent variable and SocGap as the independent variable. The results remain consistent with previous findings.

Table 13. Changing the measurement of the dependent variable HisGap.

In order to effectively resolve issues of heteroskedasticity, autocorrelation, and cross-sectional correlation in panel data, the Driscoll–Kraay fixed-effect regression model is adopted in this study for the estimation of long-term coefficients (Driscoll and Kraay, 1998; Beylik et al., 2022). The regression results remain consistent with previous findings.

Additionally, the fixed-effect regression may be too strong for our analysis. As such, we conducted the robustness test using the random-effect regression (Xu and Zeng, 2020). The findings are consistent with those from the fixed-effect models.

Firms are motivated to pursue better ESG ratings for building positive impression on stakeholders and demonstrating their sustainability. Good ESG performance could not only lower the capital constraint and cost of capital but also alleviate information asymmetry and improve firm reputation. On the contrary, a firm with low ESG performance or ESG performance gap is more likely to be doubted for its growth and sustainability by stakeholders. An important issue arises that how firms take actions or strategies as responses to ESG performance gaps. Based on BTOF, in this study, how the firm ESG performance gaps motivate its green innovation in a Chinese listed firm context is empirically examined. The empirical results show that the firm tends to greenly innovate more when its ESG performance is below both historical aspiration and social aspiration levels, that is, ESG performance gaps. The results also indicate that ESG performance pressure could be a motivation of firm’s green innovation. Following the logic of BTOF, we further explore boundary conditions from the perspective of firm motivation and capability, and testify the roles of Confucian culture and digitalization. It is found that Confucian culture could reduce firm’s motivation to take risks, which means that firms are less likely to greenly innovate when facing ESG performance gaps. However, digitalization demonstrates firm’s capability, which enables the firm to take more risks and facilitates green innovation during the ESG performance gaps.

Implications for managerial practices are also provided in this study. First, firms are supposed to make sense of their ESG performance based on the ESG ratings or scores provided by third-party institutions. Firms may face ESG performance shortfalls or failures, which bring them with pressures. Both historical aspiration and social aspiration levels provide reference points, shaping firms’ ESG objectives and helping firms to evaluate their current ESG performance. Accordingly, firms could adjust their strategic priorities and take actions as responses to attain their ESG performance aspirations and meet their ESG objectives. Second, green innovation could be a proper strategy or action for firms to improve their ESG performance, especially dealing with ESG performance gaps. Green innovation is not only a response strategy under external pressures such as environmental regulation and market turbulence but also a proactive choice of internal management purpose when facing internal pressures such as ESG performance gap. Third, firms should leverage their motivation and capabilities of risk-takings under ESG performance pressures. It is essential to identify and evaluate how factors like cultures and capabilities impact risk-takings. In addition to organizational culture, local culture such as Confucian culture could shape a firm’s risk preference and behaviors as well (Du, 2017). Firms should emphasize the role of culture when making risk-taking decisions under ESG performance gaps while also evaluating their owned resources and capabilities. A firm’s digitalization demonstrates its technological capability and would facilitate firm’s take risks.

Although significant contributions are made in this study to existing ESG and green innovation research, there still exist several limitations, providing direction for future studies. First, as we stated in the literature review part, existing measurements of corporate performance, that is, the ESG rating scores of a firm, vary across different third-party evaluation institutions. Future research could benefit from a comparative analysis of ESG ratings provided by multiple agencies, such as SynTao Green Finance and RKS ESG rating, to ensure the consistency and reliability of these assessments. Second, we measure ESG by using the rating score, which is an aggregated evaluation of firm ESG performance. The ESG performance contains multiple dimensions to evaluate, that is, environmental (E), social (S), and governance (G) dimensions. Future studies could empirically investigate each dimension, especially the performance gaps, to explore how they have influence on corporate strategies. Furthermore, we have tried to explore the boundary conditions that impact the relationship between ESG performance gaps and corporate green innovation from the perspective of motivation and capability. Subsequent research could further explore contextual mechanisms that may exist, such as corporate culture, regulatory environments, or other industry-specific factors. It would be helpful for broadening the applicability of the findings shown in this study.

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

JL: Conceptualization, methodology, writing–original draft, and writing–review and editing. BW: Data curation, formal analysis, writing–original draft, and writing–review and editing. XH: Writing–review and editing.

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. This research was funded by the National Natural Science Foundation of China (grant numbers: 71972121 and 72272096).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Aguilera-Caracuel, J., and Ortiz-de-Mandojana, N. (2013). Green innovation and financial performance: an institutional approach. Organ. and Environ. 26 (4), 365–385. doi:10.1177/1086026613507931

Ambec, S., Cohen, M. A., Elgie, S., and Lanoie, P. (2013). The Porter hypothesis at 20: can environmental regulation enhance innovation and competitiveness? Rev. Environ. Econ. Policy 7 (1), 2–22. doi:10.1093/reep/res016

Amel-Zadeh, A., and Serafeim, G. (2018). Why and how investors use ESG information: evidence from a global survey. Financial Analysts J. 74 (3), 87–103. doi:10.2469/faj.v74.n3.2

Amore, M. D., Miller, D., Breton-Miller, I. L., and Corbetta, G. (2017). For love and money: marital leadership in family firms. J. Corp. Finance 46, 461–476. doi:10.1016/j.jcorpfin.2017.09.004

Arenhardt, D. L., Battistella, L. F., and Grohmann, M. Z. (2016). The influence of the green innovation in the search of competitive advantage of enterprises of the electrical and electronic Brazilian sectors. Int. J. Innovation Manag. 20 (01), 1650004. doi:10.1142/S1363919616500043

Avramov, D., Cheng, S., Lioui, A., and Tarelli, A. (2022). Sustainable investing with ESG rating uncertainty. J. Financial Econ. 145 (2), 642–664. doi:10.1016/j.jfineco.2021.09.009

Bai, H. (2011). A comparison of propensity score matching methods for reducing selection bias. Int. J. Res. and Method Educ. 34 (1), 81–107. doi:10.1080/1743727x.2011.552338

Benkraiem, R., Dubocage, E., Lelong, Y., and Shuwaikh, F. (2023). The effects of environmental performance and green innovation on corporate venture capital. Ecol. Econ. 210, 107860. doi:10.1016/j.ecolecon.2023.107860

Beylik, U., Cirakli, U., Cetin, M., Ecevit, E., and Senol, O. (2022). The relationship between health expenditure indicators and economic growth in OECD countries: a Driscoll-Kraay approach. Front. Public Health 10, 1050550. doi:10.3389/fpubh.2022.1050550

Billio, M., Costola, M., Hristova, I., Latino, C., and Pelizzon, L. (2021). Inside the ESG ratings:(Dis) agreement and performance. Corp. Soc. Responsib. Environ. Manag. 28 (5), 1426–1445. doi:10.1002/csr.2177

Broadstock, D. C., Chan, K., Cheng, L. T., and Wang, X. (2021). The role of ESG performance during times of financial crisis: evidence from COVID-19 in China. Finance Res. Lett. 38, 101716. doi:10.1016/j.frl.2020.101716

Busch, T., Bauer, R., and Orlitzky, M. (2016). Sustainable development and financial markets: old paths and new avenues. Bus. and Soc. 55 (3), 303–329. doi:10.1177/0007650315570701

Chang, X., Fu, K., Low, A., and Zhang, W. (2015). Non-executive employee stock options and corporate innovation. J. Financial Econ. 115 (1), 168–188. doi:10.1016/j.jfineco.2014.09.002

Chen, W. R. (2008). Determinants of firms' backward-and forward-looking R&D search behavior. Organ. Sci. 19 (4), 609–622. doi:10.1287/orsc.1070.0320

Chen, W. R., and Miller, K. D. (2007). Situational and institutional determinants of firms' R&D search intensity. Strategic Manag. J. 28 (4), 369–381. doi:10.1002/smj.594

Chen, Y. S. (2008). The driver of green innovation and green image–green core competence. J. Bus. Ethics 81, 531–543. doi:10.1007/s10551-007-9522-1

Cheng, B., Ioannou, I., and Serafeim, G. (2014). Corporate social responsibility and access to finance. Strategic Manag. J. 35 (1), 1–23. doi:10.1002/smj.2131

Chrisman, J. J., and Patel, P. C. (2012). Variations in R&D investments of family and nonfamily firms: behavioral agency and myopic loss aversion perspectives. Acad. Manag. J. 55 (4), 976–997. doi:10.5465/amj.2011.0211

Clark, G. L., Feiner, A., and Viehs, M. (2015). From the stockholder to the stakeholder: how sustainability can drive financial out-performance. SSRN 2508281.

Clementino, E., and Perkins, R. (2021). How do companies respond to environmental, social and governance (ESG) ratings? Evidence from Italy. J. Bus. Ethics 171 (2), 379–397. doi:10.1007/s10551-020-04441-4

Crane, A., Matten, D., Glozer, S., and Spence, L. J. (2019). Business ethics: managing corporate citizenship and sustainability in the age of globalization. (USA: Oxford University Press).

Cyert, R., and March, J. (1963). Behavioral theory of the firm. (Englewood Cliffs, NJ: Prentice-Hall).

Dalal, K. K., and Thaker, N. (2019). ESG and corporate financial performance: a panel study of Indian companies. IUP J. Corp. Gov. 18 (1), 44–59.

Demirel, P., and Danisman, G. O. (2019). Eco-innovation and firm growth in the circular economy: evidence from European small-and medium-sized enterprises. Bus. Strategy Environ. 28 (8), 1608–1618. doi:10.1002/bse.2336

Dhaliwal, D. S., Li, O. Z., Tsang, A., and Yang, Y. G. (2011). Voluntary nonfinancial disclosure and the cost of equity capital: the initiation of corporate social responsibility reporting. Account. Rev. 86 (1), 59–100. doi:10.2308/accr.00000005

Dhaliwal, D. S., Radhakrishnan, S., Tsang, A., and Yang, Y. G. (2012). Nonfinancial disclosure and analyst forecast accuracy: international evidence on corporate social responsibility disclosure. Account. Rev. 87 (3), 723–759. doi:10.2308/accr-10218

Díaz-Díaz, N. L., Aguiar-Díaz, I., and De Saá-Pérez, P. (2008). The effect of technological knowledge assets on performance: the innovative choice in Spanish firms. Res. Policy 37 (9), 1515–1529. doi:10.1016/j.respol.2008.06.002

Dimson, E., Marsh, P., and Staunton, M. (2020). Divergent ESG ratings. J. Portfolio Manag. 47 (1), 75–87. doi:10.3905/jpm.2020.1.175

Driscoll, J. C., and Kraay, A. C. (1998). Consistent covariance matrix estimation with spatially dependent panel data. Rev. Econ. Statistics 80 (4), 549–560. doi:10.1162/003465398557825

Du, X. (2017). Religious belief, corporate philanthropy, and political involvement of entrepreneurs in Chinese family firms. J. Bus. Ethics 142, 385–406. doi:10.1007/s10551-015-2705-2

Feng, X., Jin, Z., and Johansson, A. C. (2021). How beliefs influence behaviour: confucianism and innovation in China. Econ. Transition Institutional Change 29 (3), 501–525. doi:10.1111/ecot.12277

Friede, G., Busch, T., and Bassen, A. (2015). ESG and financial performance: aggregated evidence from more than 2000 empirical studies. J. Sustain. Finance and Invest. 5 (4), 210–233. doi:10.1080/20430795.2015.1118917

Gao, J., Chu, D., Zheng, J., and Ye, T. (2022). Environmental, social and governance performance: can it be a stock price stabilizer? J. Clean. Prod. 379, 134705. doi:10.1016/j.jclepro.2022.134705

Gavetti, G., Greve, H. R., Levinthal, D. A., and Ocasio, W. (2012). The behavioral theory of the firm: assessment and prospects. Acad. Manag. Ann. 6 (1), 1–40. doi:10.5465/19416520.2012.656841

Gobble, M. M. (2018). Digitalization, digitization, and innovation. Res. Technol. Manag. 61 (4), 56–59. doi:10.1080/08956308.2018.1471280

Greve, H. R. (1998). Performance, aspirations, and risky organizational change. Adm. Sci. Q. 43 (1), 58–86. doi:10.2307/2393591

Greve, H. R. (2003). A behavioral theory of R&D expenditures and innovations: evidence from shipbuilding. Acad. Manag. J. 46 (6), 685–702. doi:10.5465/30040661

Guo, X., Li, M., Wang, Y., and Mardani, A. (2023). Does digital transformation improve the firm’s performance? From the perspective of digitalization paradox and managerial myopia. J. Bus. Res. 163, 113868. doi:10.1016/j.jbusres.2023.113868

Gyonyorova, L., Stachoň, M., and Stašek, D. (2023). ESG ratings: relevant information or misleading clue? Evidence from the S& Global 1200. J. Sustain. Finance and Invest. 13 (2), 1075–1109. doi:10.1080/20430795.2021.1922062

Harris, J., and Bromiley, P. (2007). Incentives to Cheat: the influence of executive compensation and firm performance on financial misrepresentation. Organ. Sci. 18 (3), 350–367. doi:10.1287/orsc.1060.0241

He, F., Yan, Y., Hao, J., and Wu, J. G. (2022). Retail investor attention and corporate green innovation: evidence from China. Energy Econ. 115, 106308. doi:10.1016/j.eneco.2022.106308

Heredia, J., Castillo-Vergara, M., Geldes, C., Gamarra, F. M. C., Flores, A., and Heredia, W. (2022). How do digital capabilities affect firm performance? The mediating role of technological capabilities in the “new normal”. J. Innovation and Knowl. 7 (2), 100171. doi:10.1016/j.jik.2022.100171

Hilary, G., and Hui, K. W. (2009). Does religion matter in corporate decision making in America? J. Financial Econ. 93 (3), 455–473. doi:10.1016/j.jfineco.2008.10.001

Hofstede, G., and Bond, M. H. (1988). The Confucius connection: from cultural roots to economic growth. Organ. Dyn. 16 (4), 5–21. doi:10.1016/0090-2616(88)90009-5

Huang, X. (2023). The Impact of green stock indices and ESG considerations on Sustainable Finance—a Study of Chinese green indices. Financial Eng. Risk Manag. 6 (10). doi:10.23977/ferm.2023.061019

Iyer, D. N., and Miller, K. D. (2008). Performance feedback, slack, and the timing of acquisitions. Acad. Manag. J. 51 (4), 808–822. doi:10.5465/amr.2008.33666024

Kameda, T., and Davis, J. H. (1990). The function of the reference point in individual and group risk decision making. Organ. Behav. Hum. Decis. Process. 46 (1), 55–76. doi:10.1016/0749-5978(90)90022-2

Khattak, S. I., Khan, M. K., Sun, T., Khan, U., Wang, X., and Niu, Y. (2022). Government innovation support for green development efficiency in China: a regional analysis of key factors based on the dynamic GMM model. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.995984

Koczkas, S. (2023). Confucianism: ancient ideology or driving force of the future? A scoping review on the effect of Confucian culture on innovation. Soc. Econ. 45 (4), 411–431. doi:10.1556/204.2023.00021

Levinthal, D. A., and March, J. G. (1993). The myopia of learning. Strategic Manag. J. 14 (S2), 95–112. doi:10.1002/smj.4250141009

Li, K., Griffin, D., Yue, H., and Zhao, L. (2013). How does culture influence corporate risk-taking?. Journal of Corporate Finance 23, 1–22. doi:10.1016/j.jcorpfin.2013.07.008

Li, C., Huo, M., Jiang, Y., and Liu, R. (2024). Confucian culture and enterprise strategic change from a perspective of the golden mean ethics. Strateg. Change 33 (4), 311–327. doi:10.1002/jsc.2581

Li, C., Huo, M., Li, C., Li, G., and Liu, R. (2023). Economic policy uncertainty and enterprise strategic change: evidence from China. Strateg. Change 32 (4-5), 125–137. doi:10.1002/jsc.2549

Li, J., Lian, G., and Xu, A. (2023a). How do ESG affect the spillover of green innovation among peer firms? Mechanism discussion and performance study. J. Bus. Res. 158, 113648. doi:10.1016/j.jbusres.2023.113648

Li, J., Wang, L., and Nutakor, F. (2023b). Empirical research on the influence of corporate digitalization on green innovation. Front. Environ. Sci. 11, 1137271. doi:10.3389/fenvs.2023.1137271

Li, W., and Wang, Y. (2024). Does state capital equity affect ESG performance of private firms? based on the perspective of sustainable development of Chinese enterprises. Front. Environ. Sci. 12, 1342557. doi:10.3389/fenvs.2024.1342557

Li, W., Xu, X., and Long, Z. (2020). Confucian culture and trade credit: evidence from Chinese listed companies. Res. Int. Bus. Finance 53, 101232. doi:10.1016/j.ribaf.2020.101232

Lian, Y., Li, Y., and Cao, H. (2023). How does corporate ESG performance affect sustainable development: a green innovation perspective. Front. Environ. Sci. 11. doi:10.3389/fenvs.2023.1170582

Miller, D., and Chen, M. J. (1994). Sources and consequences of competitive inertia: a study of the US airline industry. Adm. Sci. Q. 39 (1), 1–23. doi:10.2307/2393492

Nguyen, L., Vu, L., and Yin, X. (2020). The undesirable effect of audit quality: evidence from firm innovation. Br. Account. Rev. 52 (6), 100938. doi:10.1016/j.bar.2020.100938

Ning, J., Jiang, X., and Luo, J. (2023). Relationship between enterprise digitalization and green innovation: a mediated moderation model. J. Innovation and Knowl. 8 (1), 100326. doi:10.1016/j.jik.2023.100326

Pascariati, P. S., and Ali, H. (2022). Literature review factors affecting decision making and career planning: environment, experience and skill. Dinasti. Int. J. Digital Bus. Manag. 3 (2), 219–231. doi:10.31933/dijdbm.v3i2.1121

Peng, Y., and Tao, C. (2022). Can digital transformation promote enterprise performance? from the perspective of public policy and innovation. J. Innovation and Knowl. 7 (3), 100198. doi:10.1016/j.jik.2022.100198

Petruzzelli, A. M., Dangelico, R. M., Rotolo, D., and Albino, V. (2011). Organizational factors and technological features in the development of green innovations: evidence from patent analysis. Innovation 13 (3), 291–310. doi:10.5172/impp.2011.13.3.291

Porter, M. E. (1991). Towards a dynamic theory of strategy. Strategic Manag. J. 12 (S2), 95–117. doi:10.1002/smj.4250121008

Qiu, L., Hu, D., and Wang, Y. (2020). How do firms achieve sustainability through green innovation under external pressures of environmental regulation and market turbulence? Bus. Strategy Environ. 29 (6), 2695–2714. doi:10.1002/bse.2530

Ren, X., Xia, X., and Taghizadeh-Hesary, F. (2023). Uncertainty of uncertainty and corporate green innovation—evidence from China. Econ. Analysis Policy 78, 634–647. doi:10.1016/j.eap.2023.03.027

Roy, M., and Khastagir, D. (2016). Exploring role of green management in enhancing organizational efficiency in petro-chemical industry in India. J. Clean. Prod. 121, 109–115. doi:10.1016/j.jclepro.2016.02.039

Shanaev, S., and Ghimire, B. (2022). When ESG meets AAA: the effect of ESG rating changes on stock returns. Finance Res. Lett. 46, 102302. doi:10.1016/j.frl.2021.102302

Song, M., Tao, W., and Shen, Z. (2022). The impact of digitalization on labor productivity evolution: evidence from China. J. Hosp. Tour. Technol. doi:10.1108/jhtt-03-2022-0075

Sun, H., Cappa, F., Zhu, J., and Peruffo, E. (2023). The effect of CEO social capital, CEO duality and state-ownership on corporate innovation. Int. Rev. Financial Analysis 87, 102605. doi:10.1016/j.irfa.2023.102605

Takalo, K. T., Tooranloo, H. S., and Parizi, S. Z. (2021). Green innovation: a systematic literature review. J. Clean. Prod. 279, 122474. doi:10.1016/j.jclepro.2020.122474

Tan, Y., and Zhu, Z. (2022). The effect of ESG rating events on corporate green innovation in China: the mediating role of financial constraints and managers' environmental awareness. Technol. Soc. 68, 101906. doi:10.1016/j.techsoc.2022.101906

Tang, M., Walsh, G., Lerner, D., Fitza, M. A., and Li, Q. (2018). Green innovation, managerial concern and firm performance: an empirical study. Bus. strategy Environ. 27 (1), 39–51. doi:10.1002/bse.1981

Tsai, K. H., and Liao, Y. C. (2017). Innovation capacity and the implementation of eco-innovation: toward a contingency perspective. Bus. Strategy Environ. 26 (7), 1000–1013. doi:10.1002/bse.1963

Tsang, A., Frost, T., and Cao, H. (2023). Environmental, social, and governance (ESG) disclosure: a literature review. Br. Account. Rev. 55 (1), 101149. doi:10.1016/j.bar.2022.101149

Wang, F., Feng, L., Li, J., and Wang, L. (2020). Environmental regulation, tenure length of officials, and green innovation of enterprises. Int. J. Environ. Res. Public Health 17 (7), 2284. doi:10.3390/ijerph17072284

Wang, L., and Juslin, H. (2009). The impact of Chinese culture on corporate social responsibility: the harmony approach. J. Bus. Ethics 88, 433–451. doi:10.1007/s10551-009-0306-7

Wang, M. (2024). Negative performance aspiration gap and stock price crashes: based on Behavioral Theory and agency Theory perspective. Asia-Pacific J. Financial Stud. 53 (1), 60–86. doi:10.1111/ajfs.12462

Wang, Q., Qu, J., Wang, B., Wang, P., and Yang, T. (2019). Green technology innovation development in China in 1990–2015. Sci. Total Environ. 696, 134008. doi:10.1016/j.scitotenv.2019.134008

Wang, Y., Su, Q., and Sun, W. (2022). CEO relational leadership and product innovation performance: the roles of TMT behavior and characteristics. Front. Psychol. 13, 874105. doi:10.3389/fpsyg.2022.874105

Weber, M. (1958). The Protestant Ethic and the Spirit of Capitalism: the relationships between religion and the economic and social life in modern culture. New York, NY: Charles Scribner’s Sons.

Wong, W. C., Batten, J. A., Mohamed-Arshad, S. B., Nordin, S., and Adzis, A. A. (2021). Does ESG certification add firm value? Finance Res. Lett. 39, 101593. doi:10.1016/j.frl.2020.101593

Wu, S., Sun, H., and Liu, M. (2022). Research on the influencing factors of green technology innovation in manufacturing enterprises. Manuf. Serv. Operations Manag. 3 (1), 1–8. doi:10.23977/msom.2022.030101

Wu, Y., Gu, F., Ji, Y., Guo, J., and Fan, Y. (2020). Technological capability, eco-innovation performance, and cooperative R&D strategy in new energy vehicle industry: evidence from listed companies in China. J. Clean. Prod. 261, 121157. doi:10.1016/j.jclepro.2020.121157

Xu, Y., and Zeng, G. (2020). Corporate social performance aspiration and its effects. Asia Pac. J. Manag. 38 (4), 1181–1207. doi:10.1007/s10490-020-09706-0

Yang, L. R., Chen, J. H., and Li, H. H. (2016). Validating a model for assessing the association among green innovation, project success and firm benefit. Qual. and Quantity 50, 885–899. doi:10.1007/s11135-015-0180-6

Yuan, B., and Cao, X. (2022). Do corporate social responsibility practices contribute to green innovation? The mediating role of green dynamic capability. Technol. Soc. 68, 101868. doi:10.1016/j.techsoc.2022.101868

Zhai, H., Yang, M., and Chan, K. C. (2022). Does digital transformation enhance a firm's performance? Evidence from China. Technol. Soc. 68, 101841. doi:10.1016/j.techsoc.2021.101841

Zhang, X., Li, W., Ji, T., and Xie, H. (2024). The impact of ESG performance on firms’ technological innovation: evidence from China. Front. Environ. Sci. 12, 1342420. doi:10.3389/fenvs.2024.1342420

Keywords: ESG performance aspiration, green innovation, behavioral theory of the firm (BTOF), Confucian culture, digitalization

Citation: Liu J, Wang B and He X (2024) How are firms motivated to greenly innovate under the pressure of ESG performance? Evidence from Chinese listed firms. Front. Environ. Sci. 12:1469884. doi: 10.3389/fenvs.2024.1469884

Received: 24 July 2024; Accepted: 25 September 2024;

Published: 11 October 2024.

Edited by:

Otilia Manta, Romanian Academy, RomaniaReviewed by:

Laeeq Razzak Janjua, WSB Universities, PolandCopyright © 2024 Liu, Wang and He. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Bolin Wang, d2JsMDIyMUBzYnMuZWR1LmNu

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.