Anzi Han1

Anzi Han1 Yunqiang Liu

Yunqiang Liu

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 05 June 2024

Sec. Environmental Policy and Governance

Volume 12 - 2024 | https://doi.org/10.3389/fenvs.2024.1406577

This article is part of the Research Topic Green Finance & Carbon Neutrality: Strategies and Policies for a Sustainable Future View all 36 articles

Facing the double constraints of the “double carbon” target and high-quality economic development, carbon trading policy is an important tool for realizing the emission reduction commitment; based on the perspective of microenterprises, the specific mechanism and spatial effect of carbon trading policy still need to be evaluated. Taking China’s carbon emissions trading pilot as a quasi-natural experiment, this paper empirically investigates the impact of carbon trading policy on the carbon emission intensity of pilot enterprises and its mechanism of action, and its impact on the carbon emission intensity of neighboring enterprises, based on the multi-temporal double-difference model, moderating effect model, and spatial Durbin model with the A-share-listed enterprises in the period of 2009–2019 as the samples. It is found that: 1) Carbon trading policy will reduce the carbon emission intensity of enterprises to different degrees, and there are significant differences under different ownership types, degrees of marketization and the level of digitization. 2) Under the influence of environmental uncertainty, ESG disclosure will weaken the effectiveness of carbon emission reduction in the pre-pilot stage of the policy; with the gradual improvement of the carbon trading policy and ESG disclosure mechanism, ESG ratings will positively regulate the inhibitory effect of the carbon trading policy on the carbon emission intensity of enterprises through multiple paths. 3) Carbon trading policy effectively reduces multiple negative spillovers through the demonstration effect and competition effect of neighboring enterprises, driving the carbon emission reduction behavior of non-pilot enterprise. The research in this paper enriches the research paradigm of carbon emission intensity influencing factors, provides reference suggestions for the government to improve its policies, and better contributes to the realization of the “dual-carbon” vision in China as soon as possible.

In recent years, the climate problem caused by excessive carbon dioxide emissions has become a global issue affecting the survival and development of humanity (Cai et al., 2022a). Following the signing of the Paris Agreement, developed countries and regions such as the European Union, Japan, and Canada, which have already reached the peak of carbon emissions, have made a series of commitments to carbon neutrality (H. Wang et al., 2023), and will actively adopt the Clean Development Mechanism (CDM) and other policy instruments to reduce emissions (Sutter and Parreño, 2007). As a large carbon emitting country, China has taken the initiative to achieve carbon peak by 2030 and carbon neutrality by 2060, and set the “dual carbon” target as the national development strategy goal. However, the conflict between environmental protection and economic development is a major obstacle to China’s sustainable development: economic development will inevitably lead to a close demand for energy (Cai et al., 2022b), and the large amount of energy inputs will certainly exacerbate the climate problem (Mohmmed et al., 2019). At the same time, China’s traditional high-emission industries still account for a large proportion of the realization of carbon emission reductions will require China to accelerate the transformation of the industrial structure. In addition, urbanization and population growth brought out by economic development also make the implementation of carbon emission reductions difficult.

Under the ever-increasing pressure of resource and environmental constraints, how to reconcile the contradiction between the ecological environment and the improvement of the level of economic development has become a hot topic in today’s society. Environmental economics believes that environmental problems arise from the negative externalities of the production behavior of the economic sector, and if the property rights of environmental public goods can be clearly defined, the market mechanism can be used to cure its own inherent deficiencies. In order to solve the problem of “dilemma conflict” problem, the “Kyoto Protocol” for the first time proposed the carbon emissions trading system - carbon pricing-based market incentives for enterprises to choose the appropriate investment methods or technologies to reduce pollutant emissions. The carbon pricing-based market incentive mechanism provides greater flexibility for enterprises to choose appropriate investment methods or technologies to reduce pollutant emissions. To further promote carbon emission reduction measures, China has actively invested in the exploration of ETS research and the construction of voluntary emissions trading market. In October 2011, the National Development and Reform Commission issued the “Notice on Carbon Emission Trading Pilot Work”, which approved seven provinces and municipalities, including Beijing, Shanghai, Tianjin, Chongqing, Hubei, Guangdong and Shenzhen, and announced the opening of the national carbon trading market in June 2021. According to statistics, China’s carbon emission intensity has decreased significantly since 2013. By 2020, China’s carbon emission intensity will have decreased by 18.8 per cent compared with 2015 and 48.4 per cent compared with 2005, exceeding its international commitment targets. Carbon trading, as an economically effective and important policy system, can influence the carbon emission intensity of pilot enterprises and neighboring enterprises by adjusting industrial structure, optimizing energy structure and enhancing innovation.

To address the negative impact of the uncertain economic environment on business decisions and investment strategies, the inclusion of a public interest component in the corporate value system is more in line with current policy needs. As a result, companies’ environmental, social and corporate governance (ESG) performance has become an important criterion for measuring their level of sustainable development of enterprises. In 2008, the SSE and the SZSE successively required enterprises to disclose reports on their social responsibility performance as part of the annual report disclosure in the Circular. In recent years, the level of ESG disclosure domestic companies has improved, and the disclosure rate of A-share ESG reports will be 34% in 2022, an increase of 3% compared to 2021, and listed companies are increasingly becoming “activists” to help carbon reach the peak and become carbon neutral. Analysed from the perspective of political motivation, ESG can significantly improve corporate social responsibility and promote green transformation through market incentives and external monitoring mechanisms, thus promoting green and low-carbon development of enterprises. From the perspective of political motivation, (Ji et al., 2023) found that ESG disclosure can reduce the impact of financial risk on companies, and Dhaliwal et al. (2011) found that ESG disclosure can improve information transparency to reduce the transaction costs of enterprises and alleviate the problem of financing constraints. Analyzing from the perspective of investor motivation, there are cases of whitewashing and avoidance of shortcomings in traditional financial reports, from which investors are difficult to obtain effective information for deciding their investment intentions, and high-quality ESG reports are more helpful for their decision-making (Svanberg et al., 2022).

The marginal contributions of this paper are as follows: 1) Scholars mainly focus on the policy pilot regions, and pay less attention to the real policy intensity and governance effects on the first pilot enterprises (J. Hou et al., 2024; Xian et al., 2024). This paper takes the enterprise perspective as the starting point, providing reference basis for the carbon emission reduction of enterprises and the technological transformation of neighboring enterprises, further promoting the decarbonization and greening of industries, and allowing more enterprises to participate in the practice of realizing the “dual-carbon” strategic goal. 2) The analysis of the spatial effect of the carbon trading policy on pollution control is mostly focused on the region (Chang and Zhao, 2024; K. Li et al., 2024), and there is almost no research focusing on the flow of policy effects among micro enterprises, so a more accurate assessment of the actual policy effect among enterprises is lacking. This paper contributes to the analysis of the vertical and horizontal development of the policy’s carbon emission reduction effect of the policy, enriches the research paradigm about the influencing factors of carbon emission intensity in time and space effects, deepens the understanding of the impact of the carbon trading policy among enterprises and its path of action, and deepens the research on the evaluation system of environmental policies. 3) In the analysis on the effects of the carbon emissions trading policy, fewer studies have been conducted to deeply analyze the specific role path of the policy around the role of the mechanism of corporate ESG disclosure (Tian et al., 2024; Wan et al., 2024). This paper will provide a reference basis and feasible suggestions for the government to improve the policy and regulation of corporate ESG disclosure, draw the government’s attention to the correlation effect of the enterprise policy and put forward new ideas, and provide a clear guidance for China’s progress towards the goal of peaking carbon emissions. 4) In the testing the policy effects, a large number of studies have adopted double-difference models (Y. Chen and Mu, 2023; X. Feng et al., 2024a), and fewer studies have analyzed the spatial spillover effects of pilot policies by combining double-difference models, moderating effect models, and spatial econometric models. Therefore, this study examines the policy effects of the carbon trading policy on the carbon emission intensity of the first pilot enterprises over time and space from the perspectives of “between pilot enterprises - between government and enterprises - between enterprises and enterprises”; and examines the policy effects of the carbon trading policy on the carbon emission intensity of the first pilot enterprises over time and space with the help of the enterprises’ internal environmental management practices—ESG disclosure, in order to explore the specific path of carbon emissions trading, so as to enhance the carbon emission reduction capacity of enterprises, to achieve the construction of ecological civilization and sustainable economic and social development, and to better contribute to the realization of China’s vision of peaking carbon emissions by 2030.

With China’s increasing attention to corporate carbon emissions, the academic community has adopted various methods to measure the factors affecting carbon emission carbon intensity. By organizing and analyzing the existing research results, energy consumption and economic growth are the main driving factors of carbon emissions intensity (Esso and Keho, 2016; Nain et al., 2017; Rehman and Rashid, 2017; Osobajo et al., 2020). In tearms of energy consumption, (Zhang and Cheng, 2009) found a positive correlation between energy consumption and carbon emissions by using vector autoregression (VAR) and error correction model (ECM). Abdallh (2017) and others took the EKC approach, and further found that energy consumption is the main source of carbon emissions. Xiao et al. (2019)integrated the spatial lag model and spatial error model, and found that industrial structure, energy intensity, energy price and degree of openness are the main influencing factors of carbon emission intensity and carbon spillover. Zhao et al. (2018) used the LMDI method to decompose the influencing factors of carbon emission changes in six types of industries into emission factors, energy structure, energy intensity and industrial scale. Among them, energy structure plays a positive role in the process of carbon emission reduction in industries such as industry and construction, and plays a negative role in agriculture, transport and trade industries.

From the perspective of economic growth, Xu et al. (2021) concluded that gross product, research and development, foreign direct investment, and urban built-up area are the main factors influencing China’s CO2 emissions. Based on different regional panels, Wang (2017) suggested that: in terms of the cumulative effect at the national level, the effects of population, economic output, industrial structure, and energy structure have a positive impact on the increase in carbon emission intensity; at the provincial level, the economic output effect is the main positive factor driving the change in carbon emission intensity. In addition, Baiocch et al. (2010) showed that carbon emissions are positively correlated with income, controlling for lifestyle and other determinants. Some studies have further verified that the relationship between per capita income and carbon emissions is consistent with the EKC hypothesis that environmental quality may undergo an inverted U-shape transformation process as economic growth and per capita income increase. Combined with the new economic forms at the current stage, Li (2022c) and others used the SDM model and the panel threshold model for nonlinear analysis to conclude that the digital economy also has an inverted U-shaped relationship with carbon emissions.

Based on the innovation-driven theory, Porter believes that environmental regulation can force enterprises to take the initiative to carry out technological innovation in order to reduce production costs and improve carbon production efficiency. Among them, the cost of compliance effect usually occurs in the current period, while the innovation compensation effect has a certain time lag (M. Porter, 1996). Based on this, Acemoglu et al. (2012) consider the interaction between environmental policy and technological innovation, and through the construction of a dynamic model, they found that the strengthening of environmental policy will increase the demand for environmentally efficient technologies, and such technological innovation will further reduce the demand for environmental resources by enterprises, forming a feedback loop between the environment and technological innovation. The results also suggest that the direction of firms’ technological innovation will be influenced by environmental policy. In a further study, Dechezleprêtr (2017) constructs a balanced panel by collecting data on industrial sectors globally, and finds that strict environmental regulations can promote innovation activities of firms, especially in technology-intensive industries. Dechezleprêtre and (Wang et al., 2020) jointly show that technological innovation has a significant impact on the reducing carbon emissions in high-technology-intensive industries. Calel and Dechezleprêtre (2016) study the specific pathways and find that environmental regulations stimulate firms to undertake technological innovation and research and development in order to find environmentally friendly solutions; the study also finds that there is a certain degree of heterogeneity in the impact of environmental regulations on innovation, and the impact of environmental regulations on innovation is more pronounced in high-polluting industries and large firms. In summary, environmental regulation can be an effective policy tool to promote innovation. Governments can incentivize firms to innovate and promote environmentally friendly technologies and solutions by formulating and implementing environmental regulations.

Based on the cost-constraint theory, Coaserh (2012) and Tietenberg (1985) argue that when transaction costs are zero and property rights are clearly divided all firms will bear the same marginal abatement costs, and environmental regulation through market-based instruments rather thanthe command approach can achieve Pareto optimality. Among them, price constraints can induce economic agents to reduce emissions in areas with lower carbon abatement costs, while quantity constraints can ensure that overall carbon emission reduction target can be achieved. Pizer (2002) proposed that combining price control (e.g., carbon pricing) and quantity control (e.g., carbon quotas) can improve the effect of carbon emission reduction based on this. However, Abrell (2011) and others suggest that although the carbon trading system can help reduce carbon emissions, it has less impact on the performance of participating enterprises, and may even increase the management costs of enterprises. Goulder and Schein (2013) further point out that the implementation and regulation of carbon trading policies are more complex, and may face problems such as market manipulation and price volatility and have an impact on enterprise performance. However, the mainstream view in the academic community confirms the effectiveness of the carbon regulatory system to reduce emissions from the financing costs, decision-making costs, and agency costs: in terms of debt costs, carbon-intensive enterprises will bear a greater violation of the emission costs and the risk of default emissions (Ren et al., 2023); in terms of decision-making costs, carbon trading policy can be used to alleviate the constraints of innovative financing by improving the accuracy and transparency of information (Ferrer et al., 2019); in terms of agency costs, stakeholders can realize low-cost regulation of climate physical risks and governance performance through market signals (Rose et al., 2005), and the negative relationship between agency costs and trading prices will increase the incentives for firms to enter the carbon market (Zhu, 2017).

With regard to the emission reduction effect of carbon trading policy, some scholars take the opposite view: due to the existence of the “green paradox”, “bottoming out competition” and other phenomena, the carbon emission reduction effect of carbon trading policy may have a negative spillover. The “green paradox” refers to the idea that the restrictive effect of environmental regulations will have a crowding out effect on economic efficiency, leading to an increase in the supply and accelerated consumption of fossil energy, and ultimately leading to an increase in carbon emissions and a further deterioration of the environmental situation. On this basis, Van der Werf and Di Maria categorize the green paradox effect into two versions - weak and strong: the weak version emphasizes that imperfect climate policies increase carbon emissions in the short term, while the strong version emphasizes the increase in the net present value of future losses from climate change (Van der Werf and Di Maria, 2012). In terms of “bottom-up competition”, top-down Chinese scale competition will result in a series of forms of competition, such as spending competition, tax competition, environmental regulatory competition, etc. (Rudra, 2008), of which spending competition will squeeze out environmental protection inputs (G. Porter, 1999), This has led to the convergence of local governments’ policies of insufficient environmental protection investment; in this regard, Zhang utilized the environmental expenditure data of 284 prefectural-level cities in China to confirm that China’s environmental expenditures have been caught in the predicament of “competition at the bottom” (Z. Zhang et al., 2020a).

The above research shows that the carbon trading mechanism can effectively enhance the liquidity of the carbon market and the flexibility of carbon rights allocation, and realize the reduction of carbon emissions intensity while effectively enhancing the value of enterprises. Among other things, the key to policy design lies in balancing economic efficiency and emission reduction, and the establishment and operation of the carbon trading market requires a high degree of regulation and supervision to ensure the fairness and transparency of transactions.

Feng He (2022) and others believe that managers’ motives for ESG participation can be categorized into two types: self-interest motives and sustainable development motives. Among them, ESG disclosure strengthens the awareness of corporate value creation and sustainable development by influencing corporate financial performance, corporate social responsibility and managerial behavior. Based on the perspective of corporate financial performance, Henisz (2019) and others identified five main ways in which ESG is associated with corporate value creation: promoting revenue growth, reducing costs, minimizing regulatory and legal interventions, improving employee productivity, and optimizing investments and capital expenditures. Freeman (2010) demonstrated that investing in ESG activities can enable firms to gain a competitive market advantage and improve financial performance. performance.

Chen Meng-tao (2023) et al. further suggest that ESG disclosure can serve as an additional positive signal to improve stock liquidity through the institutional investor preference channel and the risk mitigation channel. However, results on the relationship between firms’ ESG performance and financial performance are mixed. Awaysheh (2021) et al. find that many of the higher scoring ESG portfolios underperform the market, while some of the lower scoring ESG portfolios outperform the market through the use of US market stocks. However, in the long run, Hui Wen (2022) used a baseline model of Tobin’s Q to confirm that the quality of ESG disclosure has a significant effect on increasing the market value and financial returns of firms as well as reducing the financial risk of firms. Meanwhile, Mario Testa found after empirical analysis that the relationship between financial performance and environmental performance is a mutual interaction and causality (Testa & D’Amato, 2017), so that the improvement of financial performance will further promote the attention of enterprises to environmental performance.

Based on the CSR theory, Feddersen (2001) and others found that companies with potential growth opportunities may receive more strategic investments and benefits from CSR activities, effectively increasing the demand for CSR activities. Minor (2010) and others argued that CSR activities can provide companies with goodwill and ethical capital, and will provide insurance-like protection in the event of adverse events. Berman et al. (1999) further suggest that reputation as a valuable resource reduces the severity of damage to firms in the event of business shocks and mitigates the likelihood of unfavorable regulatory, legislative, or fiscal action; meanwhile, while Waddock (1997) argues that firms need to offer the market a promise of quality and assurances of differentiation in order to create a competitive advantage. When analyzing the indirect effects, Mishra et al. (2017) used CSR as a mediator to demonstrated that innovative firms may enhance the value effect of their innovation efforts by promoting social responsibility, i.e., firms may seek higher ESG performance after innovation in order to develop valuable reputational resources and reduce capital constraints. In addition, there is no academic consensus on the stakeholder and resource base theories, which suggest a positive link between CSR and firm performance, and the neoclassical theory, which suggests that CSR imposes additional costs on firms and diverts funds from profitable investments.

Based on the theory of managerial behavior, more scholars focus on corporate governance and green innovation. Regarding the impact of ESG disclosure on corporate governance, Ren (2022), Zaman (2021) and others suggest that ESG performance has a substitution effect on internal and external corporate governance: high-quality ESG performance can inhibit managerial misbehavior by attracting the attention of analysts and brokers to create a good external monitoring environment. At the same time, ESG can strengthen internal governance by mobilizing independent directors and further regulating managerial behavior. However, some scholars hold opposite views: Jensen (2019) suggests that CSR practices based on opportunistic incentives to participate may mislead stakeholders’ perceptions of firm value and financial performance; Hemingway (2004) further suggests that managers may cover up their misbehavior by actively participating in ESG activities, and that in a high reputation insurance situation, managers are more likely to be involved in ESG activities, and in the case of higher levels of reputation insurance, managers are more likely to be involved in ESG activities. Situation, managers are more likely to adopt risky behaviors that satisfy the fraud triangle (Cressey, 2017). Regarding the impact of ESG on corporate innovation behavior, most studies show that ESG disclosure is positively correlated with corporate innovation. Now academic research on this facilitating effect mainly focuses on the following mechanisms: 1) External monitoring mechanism: Wang et al. (2023) suggest that ESG disclosure can force enterprises to carry out green innovation by reducing external monitoring costs. 2) Mitigating information asymmetry: ESG disclosure can incentivize firms to innovate by reducing innovation risk. 3) Increase resource availability: Wu et al. (2023) used the double-difference method to confirm that ESG disclosure mainly improves firms’ innovation level through the two paths of “patent-driven” and mitigating the “crowding-out effect”, using the financial constraint index as a mediating factor, found that ESG disclosure promotes green innovation by reducing corporate financing constraints, and this performance is more significant in non-green and high-tech industries dominated by strong technological motives (Bilyay-Erdogan, 2022; L. Chen et al., 2023a). However, some scholars, based on traditional agency theory, argue that excessive disclosure of ESG information is a resource crowding behavior motivated by the maintenance of managers’ reputation.

Carbon trading policy, as a flexible and efficient market-based emission reduction tool, privatizes carbon emissions through the establishment of a property rights system and uses carbon price signals to guide the optimal allocation of emission reduction resources in the economic system, thus achieving the dual goals of environmental and economic benefits. According to the data, since the launch of the carbon trading pilot in 2013, China’s carbon emission intensity has dropped significantly, and in 2017 China’s carbon emissions dropped by 5.1% compared with 2016. In addition, compared with 2005, carbon emissions in 2017 were reduced by about 46 percent. In the carbon trading market, enterprises are both the microscopic subjects of carbon emissions and the direct objects of the effects of carbon trading policies. Micro-enterprises are driven by interests to realize carbon emission reduction in two ways, namely, saving costs and increasing revenues.

Based on the cost constraint theory, in the tangible cost, if inefficient emitting enterprises do not explore ways to reduce emissions, the following three consequences will result. First, the excess carbon emissions under the established production target, inefficient emitting enterprises must bear the additional expenditure of purchasing carbon allowances from efficient emitting enterprises. Second, if enterprises in the pilot region make decisions to reduce production under the established carbon emission constraints, they will have to bear the loss of profits due to the decline in production. Third, if they emit more than they should, they run the risk of being penalized and paying the price for polluting the environment. But in either case, the tangible costs of inefficient emitters will rise, weakening their market competitiveness. At the same time in terms of intangible costs, inefficient emitters will receive lower valuations in the market compared to efficient emitters, which will be more favored by investors. Obviously, high-efficiency emitting enterprises will be more advantageous in terms of cost. Thus, it can be seen that the implementation of carbon trading policy makes high-emission enterprises face the problem of cost increase, which exerts economic pressure on them and forces them to explore the path of carbon emission reduction, so as to realize the overall effect of carbon emission reduction. Enterprises are forced to reduce their carbon emissions through technological innovation, industrial structure adjustment and improvement of resource utilization efficiency. Although technological innovation will bring new costs to enterprises, scholars have verified the weak Porter effect based on Porter’s hypothesis (M. E. Porter and Linde, 1995a): even if there is an increase in the cost of innovation, enterprises can still realize that the new benefits are greater than the new costs (Zhong et al., 2023). Therefore, rational enterprises will choose technological innovation to promote emission reduction instead of facing the problem of purchasing carbon allowances or paying fines for excessive emissions. The synthesis of the above analysis can be concluded that from the perspective of cost constraints, enterprises will be affected by the carbon trading policy to reduce their carbon emission intensity.

Based on the theory of environmental economics, firstly, enterprises that meet the carbon emission standards can avoid paying carbon taxes and penalties, thus reducing their operating costs. Second, the implementation of the carbon trading policy provides new business opportunities for enterprises, and the sale of surplus allowances allows them to increase the price of carbon trading in order to obtain excess profits and cash inflows (Veith et al., 2009). Furthermore, with the increasing demands for sustainable development, enterprises are gradually realizing the importance of reducing emissions: participating in carbon trading and reducing carbon emission intensity will help enterprises establish a good environmental image and improve their competitiveness in sustainable development. According to stakeholder theory, this will better maintain the relationship network between enterprises and stakeholders, create competitive advantages for enterprises and bring intangible benefits (X. Zhang and Zheng, 2024). Therefore, in order to increase revenue, enterprises will choose to actively pursue low-carbon production, carry out innovative activities of low-carbon technology and efficiently utilize energy so as to reduce carbon emissions. In addition, the increase in the cost of carbon emissions will increase social investment in low-carbon products and industries, improve the efficiency of enterprise resource allocation and optimize the industrial structure; (Nayyar et al., 2014) pointed out that the carbon trading policy can promote the faster transition to clean energy and upgrading of industrial structure by adjusting the demand structure. Therefore, carbon trading policy has the effect of carbon emission reduction in the perspective of promoting economy (X. Feng et al., 2024a).

Based on the above analysis, this paper puts forward the research hypothesis.

H1: Carbon trading policy has an inhibitory effect on carbon emission intensity in pilot regions.

With regard to the analysis of the policy mechanism, carbon trading policy is an effective policy tool to optimize the allocation of carbon emission resources, reduce the cost of carbon emission reduction, and control greenhouse gas emissions. However, in the quasi-natural experiment of the pilot policy, carbon trading still needs to be improved in terms of market effectiveness and the ability of coordinated management of regulatory resources (Yang, 2023), and the ESG disclosure system is still in an imperfect stage at the early stage of the pilot program, and the incompatibility between the carbon trading policy and the ESG disclosure mechanism may weaken the emission reduction effect of the policy. According to the signaling theory, the increase of environmental uncertainty will increase the difficulty of enterprises to formulate strategies. In this case, companies are more inclined to enter high-carbon fields with lower cost and technology thresholds, ignoring ESG concepts such as environmental governance and social responsibility. Driven by environmental uncertainty and lack of regulation, firms may implement a series of undesirable competitive strategies, such as commercial bribery, false public goods, and corporate greenwashing to reduce their environmental governance costs (Dhole et al., 2021; Hou et al., 2021), resulting in an asymmetry between economic and actual environmental benefits (Wang et al., 2023). Meanwhile, a high degree of environmental uncertainty will lead to an increase in investment waiting options and risk aversion, exacerbating the financing constraints of corporate green innovation and causing a downward trend in environmental performance (Z. Chen et al., 2022). In addition, the conflict between ESG performance and sustainability commitments will damage the market value of firms by affecting their goodwill, which in turn will cause disruptions to the operation of the carbon market (S. M. Fazzari and Athey, 1987).

With the gradual improvement of carbon trading policy and ESG disclosure mechanism, ESG disclosure policy can promote carbon information transfer and carbon market liquidity, while driving the fulfillment of corporate social responsibility from internal and external sources to further enhance the carbon emission reduction effectiveness of the policy. Specifically, ESG may promote policy emission reduction through paths such as reducing information asymmetry, improving carbon information quality, and enhancing monitoring pressure. Based on the signaling theory, companies communicate their organizational image, intentions, behaviors, and performance through signals, thus reducing information asymmetry and data authenticity issues in the carbon trading process (Karaman et al., 2020). It can be seen that more stringent carbon emission measurement methods and carbon accounting systems in ESG disclosure mechanisms can improve the carbon information disclosure system and quantitative norms, and enhance the transparency and bargaining power of carbon information. At the same time, according to the principal-agent theory, environmental regulation and managers will constrain the negative externality of enterprise operation through the formation of internal and external supervision system, thus positively promoting the carbon emission reduction effect of carbon trading policy. As a result, in the policy context of carbon trading, ESG disclosure can avoid the problem of “localized emission reduction, overall pollution diffusion and exacerbation pattern”, i.e., the “pollution paradise hypothesis”, by strengthening the regulatory constraints on synergistic emission reduction (S. Li et al., 2022). In addition, according to the theory of financing superiority, poor information is the key issue leading to corporate financing constraints, and ESG information disclosure can reduce the level of corporate financing constraints to promote innovation effects of carbon trading policiescorporate innovation by enhancing the willingness of investors to invest and confidence, which in turn improves corporate productivity and reduces the intensity of carbon emissions (H. Wen et al., 2022b). At the same time, lower financing constraints will also increase the willingness of enterprises to take risks to a certain extent, which will inhibit their risk aversion to green investment (Maaloul, 2018).

Based on the CSR theory, ESG disclosure may facilitate policy reductions through the paths of stakeholders, reputational capital, and green innovation: according to the theory of corporate social responsibility, economic, legal, ethical, and philanthropic responsibilities constitute the pyramid of corporate fulfillment of social responsibility (Carroll, 1991); furthermore, Bowen defines it as the obligation of a company to pursue desirable policies in terms of social goals and values (Azimli, 2023). Stakeholder theory suggests that enterprises will no longer be able to limit themselves to the perspective of shareholders’ interests, but will need to consider the legitimate needs of stakeholders, including the environment, society, and the economy; at the same time, corporate responsibility behavior is seen as a tool for its own reputation management and brand protection (Lewis, 2003), and a good corporate image can strengthen the stable relationship with external stakeholders, and obtain stable social capital. As a result, ESG disclosure is actually an incentive and penalty mechanism for corporate carbon emissions, which serves as an internal driver to improve corporate carbon emission reduction initiative and corporate value-innovation performance and environmental governance level, etc., and prompts corporate managers to set corporate development goals based on the concept of sustainability. In addition, the traditional agency theory and follow the cost theory that part of the environmental regulation will take away from the enterprise plan resource allocation (Y. Li et al., 2023), and ESG disclosure can amplify and promote the positive externalities of innovation for responsible innovation, providing new opportunities for the sustainable development of enterprises.

Based on the above analysis, this paper proposes the hypothesis.

H2: In the pre-pilot period of the policy, ESG disclosure plays a negative moderating role in the path of carbon trading policy on carbon emission intensity; in the late period of the policy pilot, ESG disclosure plays a positive moderating role in its path of action.

From the theory of externality, it can be seen that externality is a kind of spillover effect in economic activities, and the behavior and decisions of enterprises will have external effects on their surrounding environment. However, externalities are divided into positive and negative externalities, which leads to the diversity of spatial spillover effects, including both positive and negative spillover effects. Extending to the implementation of carbon trading policy, under the spatial perspective, it can be considered that the carbon trading policy acting on the pilot enterprises has spillover effects on the neighboring enterprises. Comprehensively, since the implementation of the carbon trading pilot policy, scholars have explored the spatial spillover effect at the provincial level and city level, and confirmed that the carbon trading policy generally shows more positive than negative spillover effects (Dhole et al., 2021; Hou et al., 2021). On this basis, this paper argues that based on the spatial spillover effect, neighboring enterprises are also affected by the carbon trading policy to produce carbon emission reduction effect, and the carbon emission reduction effect still exists when summed up to the overall perspective.

From the perspective of positive impacts, as the enterprises in the pilot area are regulated by the policy, they will spontaneously carry out low-carbon technological innovation, industrial structure adjustment, new energy application and other decisions (Z. Li et al., 2022), which will have demonstration effects and warning effects on the neighboring enterprises. The demonstration effect is mainly manifested in the technological spillover of low-carbon technologies, and neighboring enterprises can accumulate innovation and management experience from the technological innovation activities of the pilot enterprises, thus promoting carbon emission reduction of neighboring enterprises. The warning effect is mainly reflected in the long-term trend of the carbon trading policy, which is likely to be extended from the pilot region to the whole country. Neighboring enterprises will definitely consider the orientation of the policy when formulating development strategies, which will be manifested in their technological innovation and learning to adapt to the policy in advance, and consider the long-term interests and adaptability of their enterprises. In addition, based on the theory of linkage effect, regional linkage between regions or markets can generate induced investment and expand the whole industrial chain through expansion (Su et al., 2024); meanwhile, the difference in technological progress to promote the flow of production factors from low productivity to high productivity flow is conducive to the upgrading of industrial structure (Yan et al., 2024). Based on signaling theory, interregional information exchange can realize the spillover effect of policy emission reduction by reducing the cost of resource matching and increasing financial support (Y. Huang et al., 2022).

In terms of negative impacts, because of the relatively lax policies of neighboring regions in the pilot areas, there is a risk that high-polluting and high-emission industries may evade policy regulations by moving to neighboring regions or outsourcing high-polluting production to neighboring enterprises (Dai et al., 2022a). At the same time, small and medium-sized enterprises (SMEs) face a more competitive environment, and SMEs in the pilot areas may face unfair competition, a factor that may also lead to the transfer of pollution to neighboring areas. Such pollution transfer will greatly reduce the effect of the policy and aggravate carbon emissions in neighboring areas, which is against the original purpose of the carbon trading pilot policy.

Based on the above analysis, this paper puts forward the hypothesis.

H3: The carbon trading policy has an inhibiting effect on the carbon emission intensity of neighboring enterprises in the pilot area.

Based on the above, the research framework is presented in Figure 1.

Figure 1. Theoretical model.

As a “quasi-natural experiment”, the carbon emissions trading policy pilot has randomness, so it is more suitable to use the method of Zhang (2021) to choose the double-difference model to analyze the effectiveness of the policy. The specific formula is shown in Eq. 1, where i, r, t represent enterprises, regions and time, respectively. The explanatory variables of the model are the cross-multiplication terms of the policy pilot time dummy variable and the policy pilot region dummy variable. Cbtradet denotes whether r region started the carbon emissions trading pilot work in year t. The year r region started the carbon emissions trading and the years thereafter take the value of 1, otherwise it takes the value of 0; Pilotr denotes the dummy variable of the pilot region, which takes the value of 1 if it is a policy pilot region and 0 otherwise; X is the ensemble of firm-level control variables; μi is the firm fixed effect; ηt is the time fixed effect; and ε is the randomized disturbance term.

In this paper, we adopt the approach of Feng (2022), which is based on the DID model with the addition of the moderating variable ESG and the interaction term between the moderating variable ESG and DID, and the specific model is shown in Eq. 2:

Before deciding to use the spatial panel model, this paper will use the Moran index I and construct a matrix geographic distance matrix to test the spatial autocorrelation of the carbon trading policy. Among them, the local Moran index is used to examine the spatial aggregation near the pilot area of the policy, and its formula is Eq. 3:

Where Ii represents the localized Moran index of the ith province, xi the carbon emission intensity of the ith province, μ is the mean of the carbon emission intensity of the 30 provinces, σ is the standard deviation of the carbon emission intensity of the 30 provinces, Wij is the value of spatial weights, and n is the total number of all the provinces, i.e. 30.

Based on the method of Amidi (2020), this paper further constructs the spatial error model (SEM), spatial autoregressive model (SAR) and spatial Durbin model (SDM) to evaluate the spatial spillover effect of the carbon trading pilot policy. At the level of research ideas, according to Perrox’s “growth nucleus” theory, regional development and enterprise development are not carried out at the same time, but through the enterprise’s own development and then spread to the surrounding areas, so this paper will be different from the existing research, from the enterprise micro perspective, extended to the macro-provincial perspective; at the same time, taking into account the possible impact on the results of the difference in latitude and longitude between units of enterprises is too small, this paper will be different from the established research, from the enterprise micro perspective to the macro-provincial perspective. At the same time, considering the possible influence of small latitude and longitude differences between enterprises, this paper sums up the enterprise panel data to the provincial level to establish a spatial geographic matrix, and conducts a regression on the panel data of a total of 30 provinces (excluding Hong Kong, Macao, Taiwan, and Tibet) in order to more comprehensively detect the policy effects of the carbon trading pilot. The specific formula is Eq. 4:

Where W is the weight matrix describing the spatial adjacency of the region; μ denotes obeying a normal distribution; λ and ρ denote the spatial correlation strength and the spatial correlation coefficient, respectively; and the rest of the variable definitions are consistent with each other.

(1) Explanatory variables: the cross-multiplier of the carbon emissions trading pilot policy and the dummy variable for pilot regions (DID or Cbtradet*Pilotr). Considering the differences in the time point of the implementation of the policy in each pilot region, this paper adopts the multi-period DID method for regression analysis, which divides Shenzhen into the beginning of 2013, Shanghai, Beijing, Guangdong, Tianjin, Hubei, and Chongqing into the beginning of 2014, and Fujian Province into the beginning of 2017 (Bian et al., 2024; Q. Wu, 2024).

(2) Explained variable: enterprise carbon emission intensity (CEI). According to the Intergovernmental Panel on Climate Change (IPCC) carbon emission accounting method to calculate the municipal panel carbon dioxide emissions, and combined with Jing Wu et al. (Wu et al., 2022; Wang et al., 2023)’s method to calculate the emission coefficient of each enterprise, so as to get the carbon emissions of each enterprise in the whole country, and finally divide the carbon emissions of the enterprise by the amount of its corresponding business income to get the enterprise carbon emission intensity, the specific formula is as follows:

① The carbon emission adjustment factor is first calculated for each prefecture-level city as in Eq. 5:

② Then the carbon emissions of i prefecture-level cities are calculated as in Eq (6):

③ Finally, the formula for the emissions of pollutant j from firm k in county i is Eq. 7:

Where Pi is the carbon emission of prefecture i, ∑Pi is the national total emission of carbon dioxide; Oi is the total industrial output value of prefecture i, ∑Oi is the national total industrial output value; Yi is the original emission of carbon dioxide of prefecture i; Ok is the industrial output of enterprise k, and ∑Ok is the total industrial output of the prefecture where the enterprise is located, and in this paper, we use the amount of business revenue of the enterprise as a proxy for the enterprise’s industrial output.

(3) Moderating variable: ESG disclosure level (ESG). Quantitative ESG scores are derived from three factors: environmental practices, social practices, and transparency and disclosure of corporate governance. Based on related literature (Liu et al., 2023; Gupta and Kashiramka, 2024), the annual composite score of ESG ratings is a common indicator of the level of ESG sustainability disclosure, and the score is proportional to the level of ESG disclosure. At present, the domestic ESG rating system shows a diversified development, mainly including CSI ESG rating, Shangdao Ronglv ESG rating, Runling Global ESG rating, etc. Compared with other rating systems, CSI ESG rating data has the advantage of being close to the Chinese market, covering a wide range of time-sensitive data. Compared with other rating systems, CSI ESG rating data has the advantages of being close to the Chinese market, covering a wide range of areas, and having a high degree of timeliness; at the same time, CSI has formulated corresponding indicator systems for different industries, which makes ESG evaluation more refined. As a result, this paper chooses the mainstream ESG rating system of A-share listed companies - CSI ESG rating data - as a proxy variable to measure the level of corporate ESG disclosure.

(4) Control variables: Referring to the studies of Xia. A (2023), Yang. S etc. (2023), the control variables in this paper mainly take the following factors into consideration: ① The number of years of listing (Listage): Ln (the current year year - the year of listing +1). ② Firm size (Size): the logarithm of the total assets of the firm at the end of the year. ③ Gearing ratio (Lev): total liabilities divided by total assets at the end of the period. ④ Equity concentration (Top1): the number of shares held by the first largest shareholder divided by the total number of shares. ⑤ Return on assets (Roa): net profit divided by ending assets. ⑥ asset turnover (Ato): operating income divided by the closing balance of total assets. ⑧ board size (Board): the number of board of directors. ⑨ level of economic development (Ln GDP): gross domestic product per capita. ⑩ industrial structure (Struct): secondary industry divided by gross regional product.

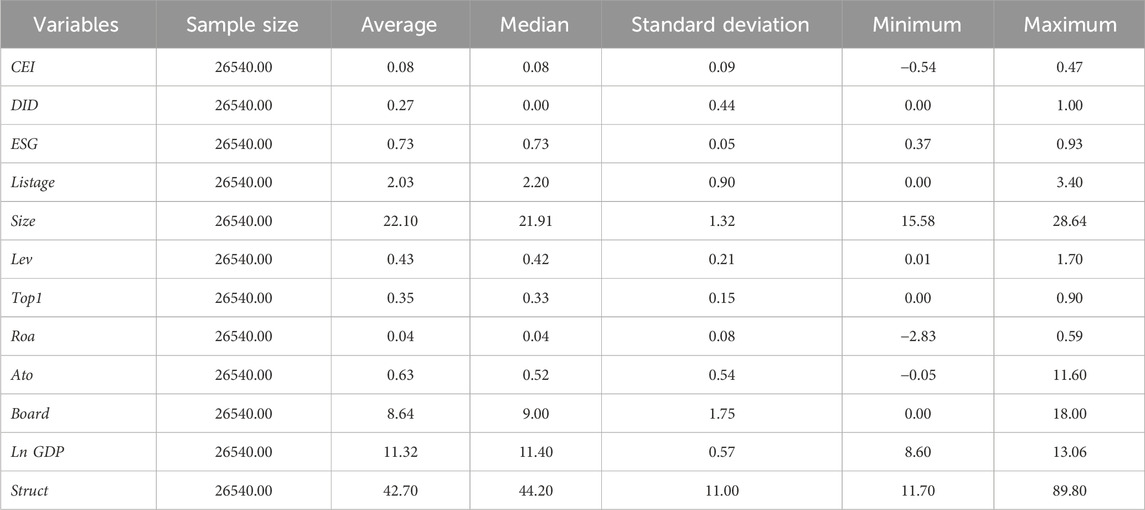

Considering the completeness, availability and timeliness of the data, this paper selects a total of 26,540 enterprises in China from 2009 to 2019 as samples for the study, and adopts the deletion method to clean the data from missing values and invalid values. All the data were obtained from China Statistical Yearbook, China Energy Statistical Yearbook and Wind database, Cathay Pacific database, etc. in previous years. In order to eliminate the effect of heteroskedasticity, this paper logarithmizes the variables with larger values before model estimation; at the same time, in order to avoid the effect of the magnitude on the regression coefficients, this paper standardizes the percentile ESG scores to the range of 0–1. Table 1 shows the descriptive statistics of all variables.

Table 1. Descriptive statistical analysis.

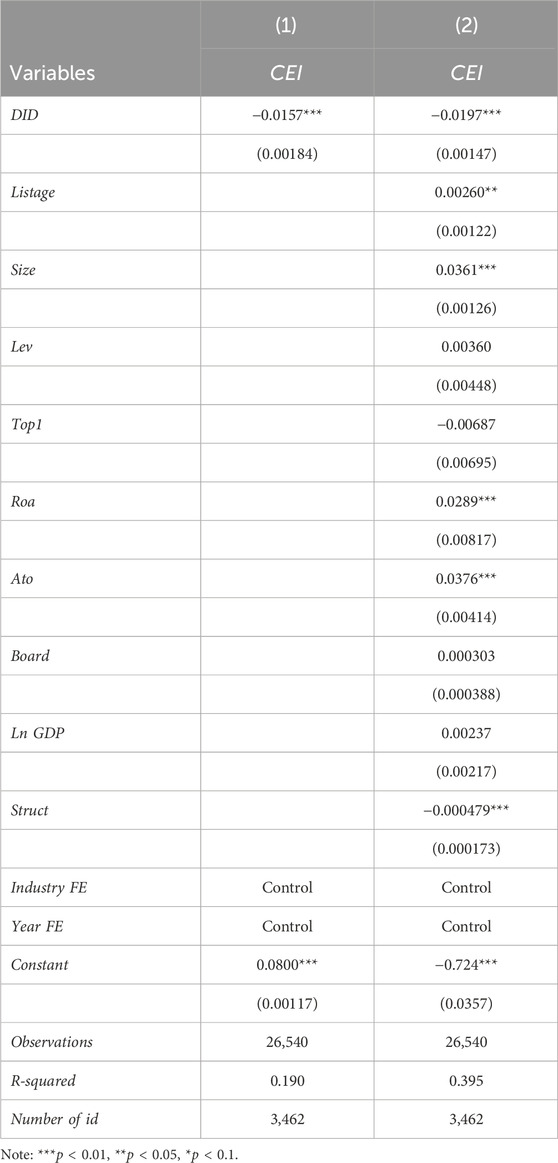

This paper first examines the impact of carbon emissions trading pilot policy on the carbon emissions intensity of enterprises, and Table 2 summarizes the results of the benchmark regression. According to Model 1, the DID - policy time interaction term is the core explanatory variable of interest in this paper. The results show that the coefficient of the core explanatory variable DID is negative with or without control variables and passes the significance test at the 1% level. The absolute value of the correlation coefficients between the variables in general is less than 0.5, ruling out the problem of multicollinearity, and the result is in agreement with Li, Xian (K. Li et al., 2024; Xian et al., 2024) et al. However, some researchers have pointed out that the emission reduction effect of carbon trading policy is not significant, which may be caused by the sample differences between sub-sectors and regions (X. Feng et al., 2024b; G. Huang et al., 2015).

Table 2. Benchmark regression results.

This paper provides the following interpretation of the results based on existing studies:s: from the perspective of the action pathway, China’s carbon trading pilot policy focuses on reducing carbon intensity through technological innovation, industrial structure upgrading and improving resource allocation efficiency (C. J. Zhang et al., 2021); from the perspective of energy consumption and supply chain, carbon trading policy may indirectly affect carbon emission intensity of enterprises through influencing the consumption structure of the “consumption side” and the output scale of the “production side” (Wang et al., 2023); from the perspective of enterprise risk taking, carbon trading policy may make enterprises pay more attention to the downside risk of creditors risk premium requirements (Ni et al., 2022), but the establishment and operation of the emission rights trading market will bring positive expectations to participating enterprises that the level of corporate risk taking of participating enterprises will be significantly increased (Wang et al., 2023). However, the current carbon trading system still lacks macro-control and integrated supervision, resulting in a lack of flexibility in the adjustment of carbon price and carbon allowances, so some scholars hold the opposite view. According to (Kerr and Duscha, 2014), the uneven degree of marketization of the carbon market may cause market price distortion, reduce the efficiency of market resource allocation and lead to the overall cost of emission reduction; the rebound effect suggests that the “carbon rebound” caused by technological advances may undermine the effectiveness of incentives for innovation. Combining the regression results with the above analysis, with the promotion and improvement of carbon trading policy, the incentive-driven and cost-constraint effects of carbon trading policy can reduce the carbon emission intensity of pilot enterprises, and hypothesis 1 is valid. At the same time, according to the joint effect of environment and economy, carbon trading policy can improve the productivity and market competitiveness of enterprises through the paths of energy structure, technological innovation, industrial structure (Deryugina et al., 2021; F. Li et al., 2021) and cash flow (Chan et al., 2013; Duan et al., 2024), leading to the transformation of enterprises into a low-carbon economy.

As for the control variables, the impacts of the number of years of listing, enterprise scale, return on assets, and asset turnover on carbon emission intensity are positive, mainly because the expansion of financial scale and efficiency improvement are conducive to the growth of carbon emissions (H. Xu et al., 2023); while the industrial structure inhibits the carbon emission intensity, mainly because the industrial structure can significantly inhibit the carbon emissions through the change of factor allocation and technological change through the rationalization of industrial structure (Z. Li and Wang, 2022a); in addition, enterprise size, return on assets, equity concentration, board size and economic development level do not affect carbon emission intensity.

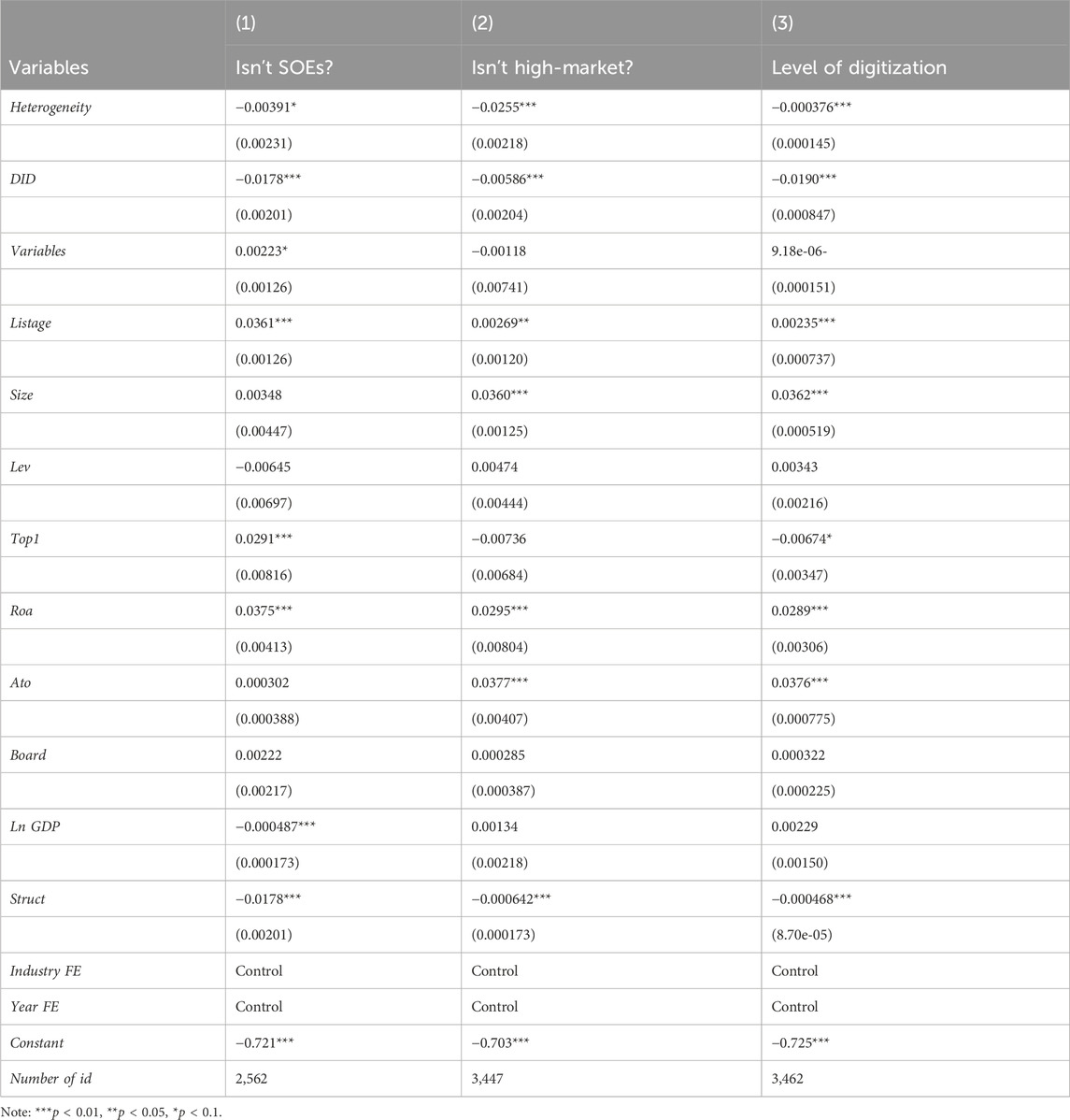

Due to the obvious differences in the economic, technological and social functions of enterprises of different ownership types, as well as the level of digitization of enterprises and the degree of inter-regional marketization, which have created imbalances in the level of economic development, resource endowment, and carbon emission reduction potentials, the effects of the policy implementation in pilot enterprises may vary. This paper will further explore the effects of enterprise ownership, degree of marketization, and digital transformation on the relationship between carbon trading pilots and the carbon emission intensity of enterprises, so as to further clarify the heterogeneity of the results of the role of carbon trading policies on carbon emission reduction of enterprises (Coad, 2007).,

(1) Heterogeneity of ownership categories

According to institutional theory, institutional pressure is an important driver of corporate carbon emission reduction (F. Wang et al., 2019). In China, the management of state-owned enterprises (SOEs) consists of government officials, and their assessment system focuses more on the implementation of government policies compared to corporate profitability (Yen and Abosag, 2016). Prior studies have shown regulatory discrimination between SOEs and non-SOEs(Yen and Abosag, 2016). The public generally expects SOEs to behave more in line with social preferences than private firms (Guan et al., 2021). Based on the social responsibility perspective and the “spotlight effect”, large state-owned enterprises (SOEs), which dominate economic growth, employment, and social distribution, have unique social identities and reputations, and will be subject to greater pressure for organizational legitimacy (Liu et al., 2023); at the same time, the differences in business objectives and financing constraints between enterprises of different ownership systems make it inevitable for SOEs to assume more social responsibility (Wang, Ma, et al., 2023b). Based on the power allocation theory, information advantage (Bilal et al., 2022) and closer social network relationships (X. Chen, 2017) facilitate SOEs’ access to government resources, and better business environment and financial efficiency make it easier for SOEs to enter the debt market and obtain (Herbohn et al., 2019) government subsidies (Lee et al., 2017). Based on the green innovation theory, imitation, norms and coercive pressure are important factors in the adoption of new technologies (Ma et al., 2023), while greater institutional pressure can help firms to realize process innovation and green products thus improving resource efficiency (Berrone et al., 2013). Therefore, state-owned enterprises are more likely to actively participate in carbon emission reduction than non-state-owned enterprises. This paper divides the sample into state-owned and non-state-owned parts and assigns the value of 1 to state-owned enterprises, otherwise 0. The results in Table 3 are consistent with the results of existing studies, i.e., state-owned enterprises are more conducive to strategic change and green governance due to their social nature and financing advantages.

(2) Heterogeneity of the degree of marketization.

Table 3. Results of heterogeneity analysis.

Market-oriented reform plays an important role in optimizing the business environment and enhancing the vitality of enterprises’ independent innovation (Cole and Elliott, 2003), and can improve the allocation efficiency of innovation resources by reducing the “crowding out effect” of government intervention, improving the mobility of factors and the enthusiasm for external financing (Hansen, 1999; Liu et al., 2020). At the same time, the diffusion of technology effects and the improvement of energy technology will further enhance the effectiveness of policies and the efficiency of enterprise carbon emission reduction (Flammer, 2018). Based on the perspective of social responsibility, the degree of marketization is positively correlated with the rule of law, the level of economic development and the degree of public concern, so the enterprises in regions with a higher level of marketization are more prominent in the strength and effectiveness of their policy implementation (Krugman, 1991). In addition, the high marketization level of the region’s market signal quality is higher, which is conducive to enterprises to a greater extent to avoid information asymmetry and obtain the optimal allocation of capital (Buera et al., 2011); market profit-seeking will lead to the flow of factor resources from the underdeveloped regions to the developed regions with high allocation efficiency, the formation of the “center - periphery pattern”, exacerbating the heterogeneity of the effect of carbon emission reduction between regions (L. Chen et al., 2021). In summary, the uneven degree of marketization will lead to the heterogeneity of carbon emission intensity changes in different regions. According to the marketization index report, Shanghai, Zhejiang, Jiangsu, and Guangdong provinces are classified as high marketization regions, and the rest are low marketization regions. The results in Table 3 show that the emission reduction effect of carbon trading policy is affected by the degree of regional marketization: the degree of marketization plays a positive moderating role in the relationship between the role of carbon trading policy on carbon emission reduction of enterprises, and all of them are significant at the 1% level. This result is consistent with the results of existing studies, that is, the emission reduction effect of carbon trading is more significant in regions with higher levels of marketization, indicating that market-oriented reforms can effectively enhance the effectiveness of the policy and achieve the goal of low-carbon development (Wang et al., 2023; Yao et al., 2023).

(3) Heterogeneity of the level of digitization

As the digital economy continues to run at an accelerating pace, the level and development of digital technology in Chinese enterprises is constantly improving. Digital transformation has become an important strategic goal to promote the high-quality development of enterprises and an urgent need to address climate change in China. In the context of carbon trading policy, whether or not the level of digitization may cause heterogeneity of carbon reduction effectiveness among enterprises. Based on the green innovation perspective, the impact of the digital economy on enterprise-generated technology is divided into spillover effect and impact effect, which reduces enterprise costs while improving the overall operational efficiency of the company (Tian et al., 2024); at the same time, enterprises can increase the sharing of information in the carbon market through digitization to promote the development of green technology (Peng and Tao, 2022), and attract more financial support and government subsidies (Geng et al., 2023). Based on the theory of value creation, digital transformation can expand the scale of production and achieve economies of scale with high total factor productivity through paths such as reducing marginal production costs and optimizing labor factor allocation (Liu et al., 2023); at the same time, digital technology, as a tool for resource management, can reduce production time and maximize energy consumption (Awan et al., 2021). In addition, An and Zhang et al. demonstrated a positive correlation between the level of enterprise digitization and carbon emission reduction (An and Shi, 2023; W. Zhang et al., 2022). Referring to the approach of Qi et al. (Qi et al., 2020), this paper constructs a comprehensive measure of digital transformation by standardizing core enterprise technologies such as artificial intelligence, blockchain, cloud computing, and big data, as well as basic inputs such as digital capital, human resources, and infrastructure investment. The results in Table 3 show that the level of digitization plays a positive regulating role in the relationship between the role of carbon trading policy on carbon emission reduction of enterprises, and all of them are significant at the level of 1%, that is, the carbon trading policy has a greater impact on carbon emission intensity of high digitalized enterprise, which indicates that the digital transformation can effectively enhance the effectiveness of the policy.

In order to ensure that the results are not affected by potential endogeneity issues, this study employs different methods to mitigate these issues, such as the propensity score matching method, the log-linear instrumental variables method, and the lagged change model.

Policy implementation is by nature a non-randomized experiment, so the double-difference method used for policy effect assessment inevitably suffers from self-selection bias, whereas the use of the propensity score matching (PSM) method allows for each treatment group sample to be matched to a specific control group sample, making the quasi-natural experiment approximately randomized, and thus checking whether the results of the study are interfered with by the influence of other potential factors. For Hypothesis 1, in order to alleviate the endogeneity problem that may be caused by omitted variables, this paper uses the PSM-DID method to correct it. After the test, the coefficients of the explanatory variables are still significantly negative, and the coefficients of the remaining control variables are also in line with expectations, which indicates that the benchmark regression results remain robust when the selection bias problem is taken into account (e.g., Table 4).

Table 4. PSM-DID test results.

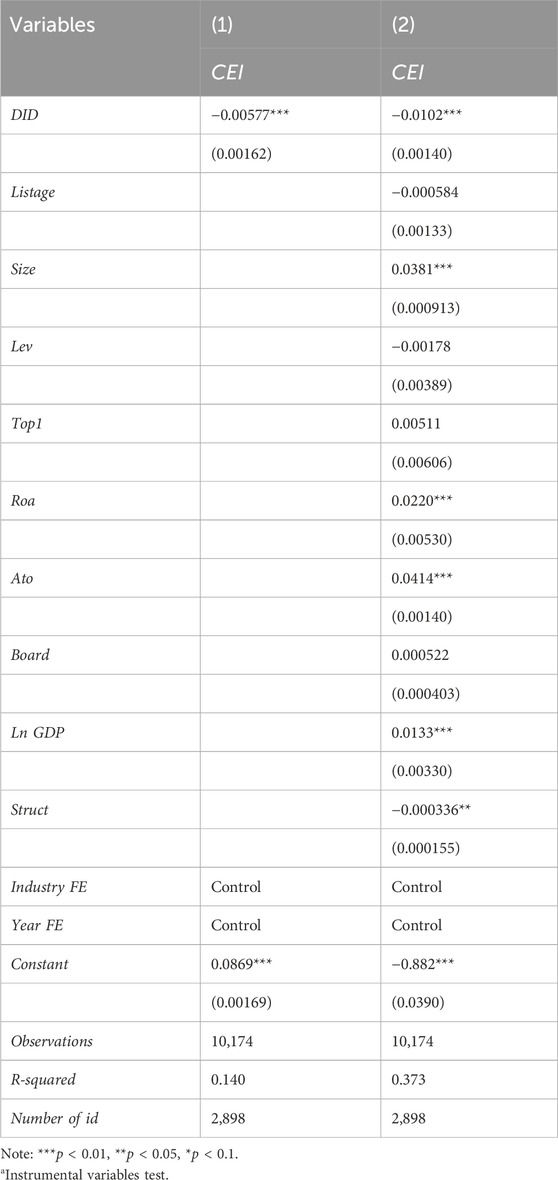

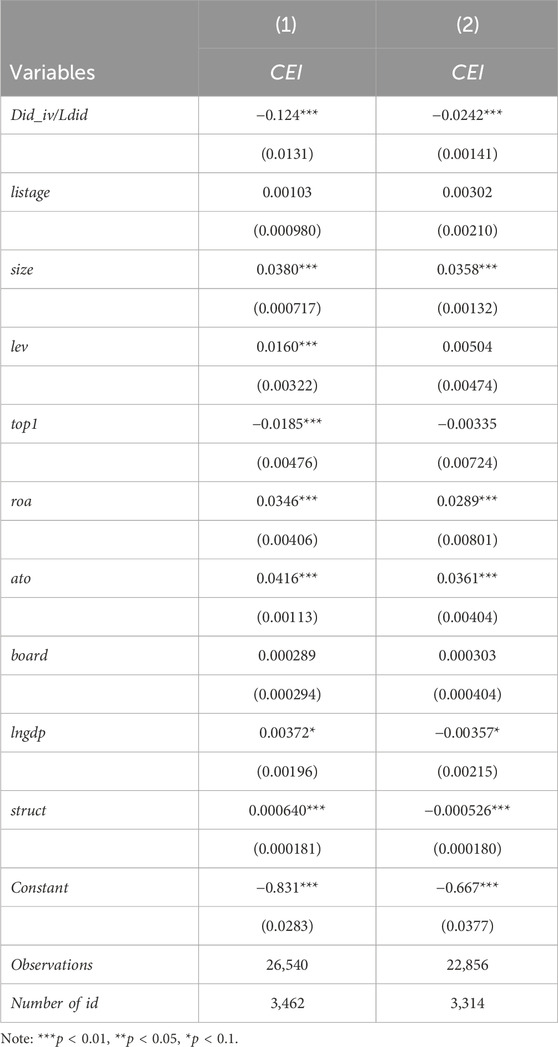

In order to address the endogeneity problem due to possible omitted variables and reverse causality, this paper draws on the research ideas of Hering et al. (Hering and Poncet, 2014), who used the Air Mobility Coefficient (ACR) to measure environmental policies. Specifically, cap-and-trade policies affect the rate of air pollution dispersion by controlling Greenhouse Gas (GHG) emissions, and thus the rate of air pollution dispersion. In the standard box model of air pollution, the ventilation coefficient is identified as a determinant of air pollution dispersion rate (Jacobson, 2002). Meanwhile, since the air mobility coefficient is determined by large-scale weather systems, it can be regarded as an exogenous characteristic of local economic activities (Jacobson, 2002; Yu et al., 2022). Therefore, in this section, the air mobility coefficient of the city where the sample firms are located is chosen as an instrumental variable, which is calculated as the product of unit wind speed and boundary layer height, and the relevant data are obtained from the China Meteorological Yearbook and provincial statistical yearbooks. The results in column (1) of Table 5 show that the estimated coefficient of the interaction term is still significantly negative. Therefore, after further mitigating the potential endogeneity problem, the carbon trading policy is still effective in reducing emissions.

Table 5. Results of Instrumental variables test and Lag test.

Since the impact of carbon trading policy on corporate carbon emission intensity may have a time lag, this study refers to the method of Si Pu (Pu and Ouyang, 2023), lagging all explanatory variables by one cycle and then re-evaluating the regression model. Column (2) of Table 5 shows that 1 year after the implementation of carbon trading policy, the carbon emission reduction of enterprises is still significantly advanced.

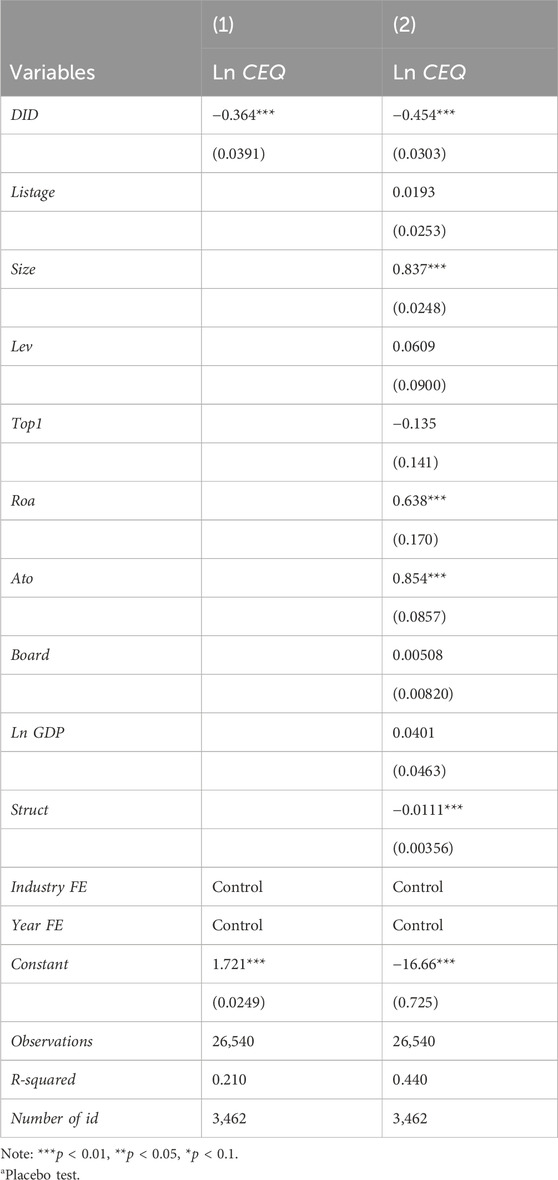

In this paper, the carbon emissions (CEQ) of enterprises are used to replace the explanatory variable carbon emissions intensity in the original model, as shown in Table 6. It is found that the sign and significance of the estimated coefficients of DID are basically consistent, which further supports the robustness of hypothesis 1.

Table 6. Robustness regression results.

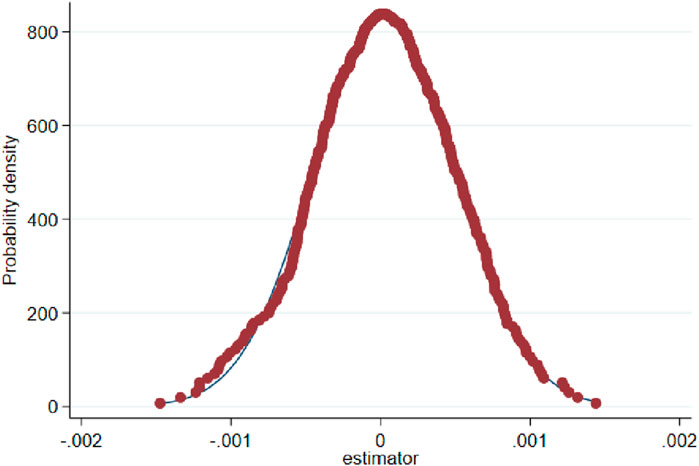

In order to further test whether the impact of carbon trading policy on the carbon emission intensity of enterprises is generated by other unobservable factors, this paper conducts a placebo test by randomly assigning carbon trading pilots, and at the same time, in order to enhance the effectiveness of the placebo test, the above experimental process is repeated 500 times. The results are shown in Figure 2, the estimated coefficients are basically around the value of 0, and most of them are not significant at the 10% level, so the influence of other unobservable factors other than carbon trading policy on the empirical results can be excluded.

Figure 2. Placebo test.

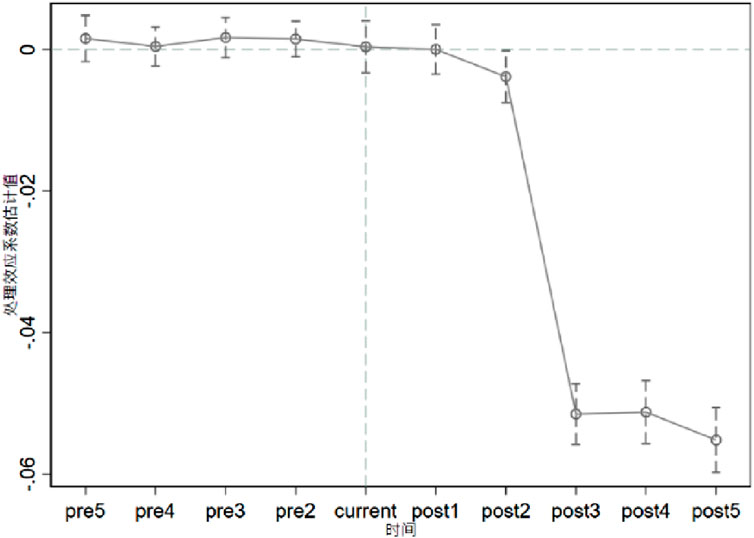

It is an important prerequisite for the use of the double-difference method that the experimental and control groups satisfy the parallel trend assumption, i.e., before the implementation of the carbon trading policy, the carbon emission intensity of each region maintains a relatively stable trend of change. Figure 3 shows the estimation results of the coefficient α and the corresponding 95% confidence intervals at different time points of the policy implementation. Before the implementation of the policy, there is no significant difference between the pilot regions and non-pilot regions. After the implementation of the policy, the carbon emission reduction effect is gradually and significantly negative, which satisfies the parallel trend hypothesis.

Figure 3. Parallel trend test.

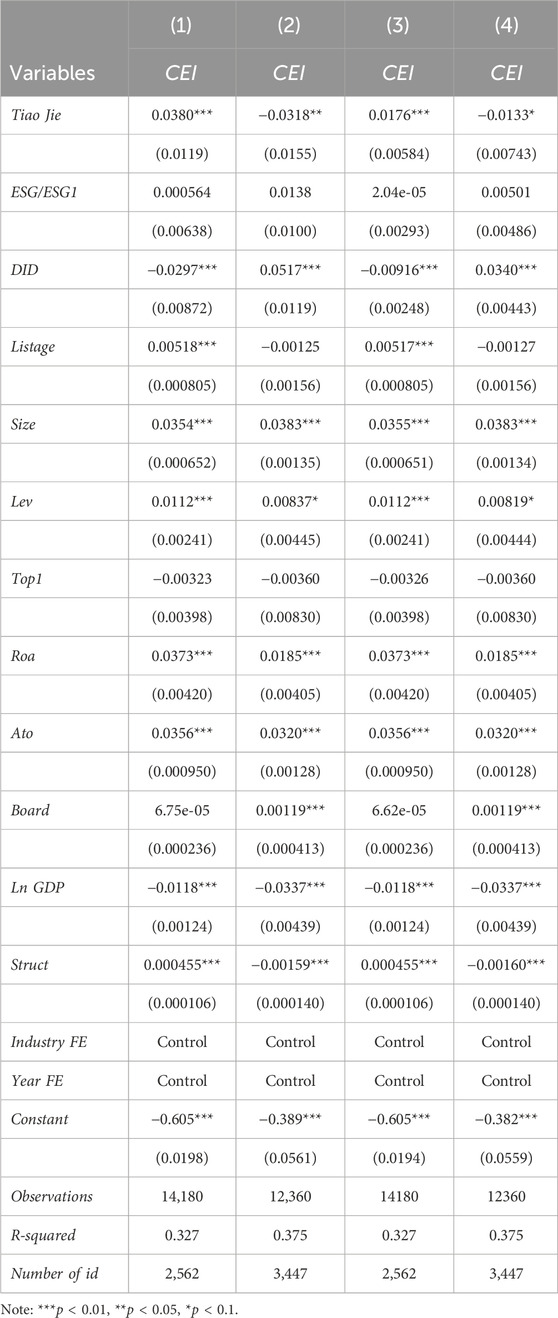

The basic framework of China’s carbon emissions market was initially harmonized at the end of 2014; successively, the Hong Kong Stock Exchange upgraded the “recommended disclosure” to “explanation for non-compliance” in the ESG Guidelines in 2015, marking an increasingly mature policy environment. This paper will take 2015 as the cut-off point. In this paper, we will take 2015 as the cut-off point and use staged regression to explore the specific role effect of ESG disclosure level during the policy pilot period, and classify 2009–2015 as the pre-pilot period of the carbon trading policy and 2016–2019 as the post-pilot period of the policy. The model results show (Table 7) that the regression coefficient of the cross term in the pre-pilot period is 0.0380, while the coefficient in the post-pilot period is −0.0318, and both of them are significant at the 5% significance level, with a high degree of fit, which confirms the existence of the moderating effect of ESG disclosure level. For the sign difference of the coefficients in the stage before and after the pilot of the policy, this paper intends to explain as follows: the environmental and social responsibility information of Chinese enterprises has only entered the stage of combining voluntary disclosure and mandatory disclosure since 2008, and the maladaptation between the carbon trading policy and ESG disclosure mechanism will weaken the policy effect of carbon trading: the theory of overinvestment argues that ESG will increase the management cost of the enterprise and reduce the profit of the enterprise in the short term The theory of over-investment suggests that ESG will increase corporate management costs and reduce corporate profits in the short term, crowding out other productive investments and leading to a reduction in carbon productivity (Gao and Liu, 2023a) In addition, if the purpose of managers’ behavior is not shareholder welfare, but self-interest, such as seeking to improve their personal reputation, the market for their trading will take a negative attitude (Bilyay-Erdogan et al., 2023). However, with the gradual improvement of ESG disclosure mechanism and carbon trading market, ESG disclosure level plays a positive moderating role in the carbon emission reduction effect of carbon trading policy: ESG can provide favorable conditions for the ecological construction of carbon trading market, avoiding the carbon hiding behavior of the companies with weak sustainability performance as much as possible. At the same time, ESG can improve the effectiveness of the policy and perfect the financing constraints by circumventing the asymmetry of information, improving the performance of corporate responsibility and innovation, and alleviating the financing constraints, thus promoting the carbon emission reduction effect of the carbon trading policy (Naeem et al., 2022). According to the legitimacy theory, a social contract will be established between the enterprise and the society, and the enterprise should act according to the beliefs, expectations, norms, standards, and values of the latter in order to achieve “legitimacy” and “social license to operate” (Gao and Liu, 2023b). Related research further confirms that the management of enterprises with ESG ratings is more likely to avoid the short-sighted behavior of only looking at immediate interests and pay more attention to the long-term development goals of enterprises, which is conducive to the green transformation of enterprises (Rahman et al., 2023). Summarizing the above analysis and empirical test results, ESG disclosure level weakens the policy effect in the early stage of carbon trading policy implementation, and positively moderates the degree of carbon trading policy’s impact on carbon emission intensity in the later stage, and Hypothesis 2 is established.

Table 7. Regression analysis of moderating effects.

In order to test the robustness of the results, this paper replaces the measurement of ESG disclosure level, drawing on Su Jingzeng’s (Zeng et al., 2024) method of assigning values to ESG scores, and assigns the nine grades of C, CC, CCC, B, BB, BBB, A, AA and AAA of the composite results to be from 1 to 9, respectively, and the regression results are shown in columns (3) and (4), which do not change the original conclusions, so the original conclusions are robust. (ESG in the table is the percentage score of CSI ESG, and ESG1 is the score of the assignment method.)

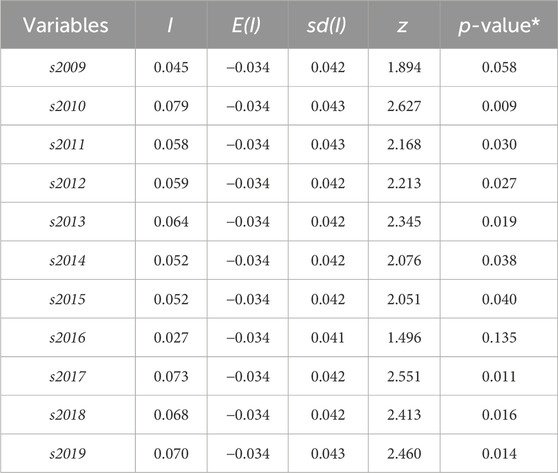

This paper introduces the geographic distance matrix to test the autocorrelation of the spatial panel data of carbon emission intensity, as shown in Table 8, except for 2016, which is not significant, the Moran’ I of carbon emission intensity from 2009 to 2019 is significantly positive at the 10% level, indicating that the spatial and temporal distributions of the carbon intensity of China’s 30 provinces are not completely random but This indicates that the spatial and temporal distribution of carbon emission intensity in the 30 provinces of China is not completely random, but there is a significant positive spatial correlation, i.e., the trend of the carbon emission intensity of each province and city will be affected by the carbon emission intensity of its neighboring provinces and cities.

Table 8. Statistical results of spatial autocorrelation test of carbon emission intensity.

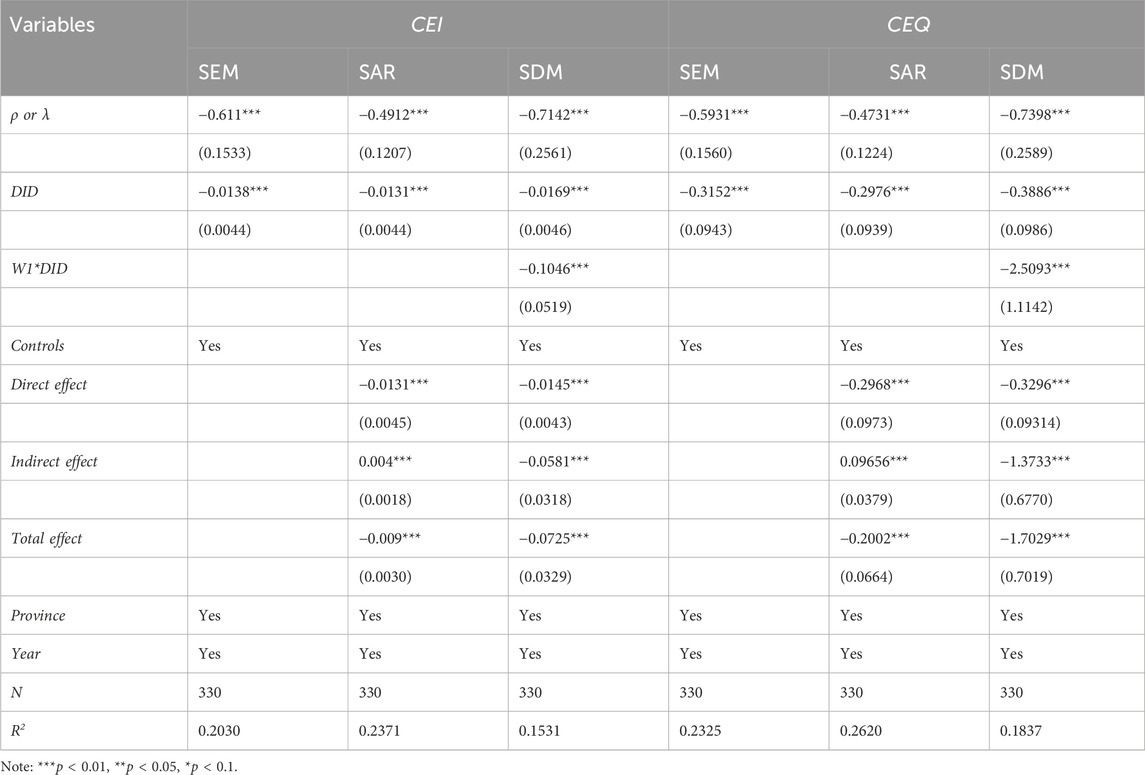

Table 9 shows the results of the spatial spillover effect of the carbon trading policy on carbon emission intensity, and the autocorrelation test is conducted on the spatial panel data of carbon emission intensity by constructing the geographic distance matrix as well. The spatial correlation coefficients ρ or λ of the three models are all significantly negative, and the estimates of DID are also significantly negative, indicating that there is a significant spatial spillover effect of the impact of the policy on carbon emission intensity. This paper further uses partial differential estimation to analyze the direct, indirect and total effects of the carbon trading pilot policy on carbon emission intensity. The regression results show that the indirect effect of the pilot carbon trading policy on carbon emission intensity is larger than the direct effect, indicating that the effect of the policy has a strong mobility between the pilot enterprises and the neighboring enterprises. In order to further enhance the credibility and accuracy of the conclusions, this paper uses the method of replacing the dependent variable, and after replacing the explanatory variable with the logarithm of the carbon emissions of the enterprises, the empirical results are basically the same in general, which indicates that the model has a certain degree of robustness. The result is in agreement with Lai, Dai et al. (Dai et al., 2022a; Lai and Chen, 2023a). However, some scholars hold the opposite view, possibly because under imperfect policies, productivity differences across firms may cause heterogeneity in carbon spillover outcomes (Lai and Chen, 2023b). Based on the empirical results, this paper analyzes the driving and inhibiting effects of carbon trading policies on carbon emission reduction from the perspective of spatial spillovers and the perspective of enterprises. The demonstration effect and competition effect among enterprises will encourage enterprises to develop new products or master new technologies, and force other enterprises to improve their productivity and competitiveness (S. Fazzari et al., 1987); meanwhile, Porter’s hypothesis suggests that the “innovation compensation” effect brought by environmental regulation can offset the “compliance cost” of enterprises to a certain extent (L. Chen et al., 2023b). In this regard, the international academic community has put forward contradictory theories, such as Sinn’s “green paradox hypothesis”: in order to avoid the adverse impacts of environmental regulations, fossil energy producers will advance the extraction of fossil fuels, exacerbating climate deterioration (M. E. Porter and Linde, 1995b); and China’s regional club effect: the presentation of the large enterprises in situ “green innovation”, medium-sized enterprises “pollution transfer” of medium-sized enterprises, and closure of small enterprises. However, with the increase of pilot regions, the joint effect of environmental regulation can weaken the “green paradox” effect of individual environmental regulation variables (Dai et al., 2022b). At the same time, with the diversification of performance evaluation systems and the increase of environmental indicators, enterprises will gradually move from the “GDP only” mode of “bottom-up competition” to “bottom-up competition” mode of “GDP only.” (Z. Zhang et al., 2020b). To summarize, the driving role in the spillover effect of carbon trading policy is dominant. In terms of economic benefits, China’s gradient development model enhances spatial agglomeration effects and exhibits strong spatial dependence and convergence (G. Huang et al., 2015). However, interregional capital flows caused by carbon trading policies may increase the value and market competitiveness of neighboring firms through paths such as narrowing regional economic gaps, thus realizing Pareto optimality for the whole society (Fan et al., 2016).

Table 9. Results of spatial spillover effects.

Starting from the perspective of enterprises, this paper uses a quasi-natural experiment based on the panel data of Chinese enterprises from 2009 to 2019, using the double-difference method, to comprehensively assess the impacts of carbon trading policies on carbon emission intensity in pilot and non-pilot regions, and to explore the mechanism role of ESG disclosure level in it. The research conclusions of this paper are as follows.