Weida Wang

Weida Wang Shi Yin

Shi Yin

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 12 July 2024

Sec. Environmental Policy and Governance

Volume 12 - 2024 | https://doi.org/10.3389/fenvs.2024.1400725

Ecological accountability is an important means for the Chinese government to promote the development of green policies. In this study, a central environmental protection inspection was used as an exogenous shock event, China’s A-share-listed companies were selected as the research sample, and the impact of the central environmental protection inspection on the financialization behavior of heavily polluting enterprises was empirically tested. The research shows that the central environmental protection inspection significantly inhibited the financialization of heavily polluting enterprises. A mechanism analysis showed that the central environmental protection inspection mainly inhibited the financialization of enterprises by promoting green innovation, which shows that the implementation of a central environmental protection inspection can promote green innovation and transformation by forcing heavily polluting enterprises to return to their main business, produce a “crowding-out effect” on financial assets, and place a focus on sustainable and high-quality development. A heterogeneity test showed that the inhibitory effect of the central environmental protection inspection on enterprise financialization was more significant in the sample group of state-owned enterprises and areas with a higher level of development of green finance. This study provides a reference for evaluating the implementation effect and effectiveness of central environmental protection inspections and has significance for regulatory authorities in improving the revision of ecological accountability policies, promoting the green transformation of heavy pollution industries, and regulating the financial asset investment behavior of listed companies.

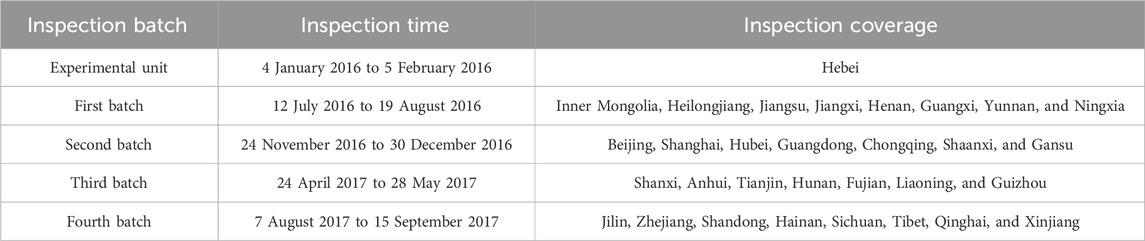

With the sustainable development of China’s economy, the problem of environmental pollution has become increasingly serious. Environmental regulation has become an inevitable choice for balancing high-level environmental protection and high-quality economic development (Xu et al., 2024). The report of the 20th National Congress of the Communist Party of China clearly pointed out that it is necessary to “further strengthen central government environmental inspection.” To this end, the Chinese government has continuously improved the top-level design of its environmental management system and has issued a number of environmental regulation policies and regulations, such as the new Environmental Protection Law and the Air Pollution Protection Law. However, due to the “high degree of decentralization” and the “administrative contracting system,” the implementation effect of environmental regulation by local governments is not ideal, and there are regulatory failures (Yin and Zhao, 2024a). The reason for this is closely related to the attempt to improve the GDP and competition among local governments (Cai et al., 2006; Zhou, 2007; Xia et al., 2020; Yin et al., 2024). In order to solve the plight of local governments’ failure in environmental inspection, the 14th Conference of the Central Leading Group for Comprehensively Deepening Reforms reviewed and approved the Environmental Protection Inspection Scheme (Trial), clearly established an environmental protection inspection mechanism that directly involved provincial and municipal Party committees, government departments, and polluting enterprises to avoid the weakening of regulatory policy implementations caused by the administrative level and territorial management in the past. This type of ecological accountability closely combines the assessment of officials for promotion with the assessment of environmental protection performance. Starting from the pilot work in Hebei in 2016, it has achieved full coverage of 31 provinces (autonomous regions and municipalities) and the Xinjiang Production and Construction Corps in four batches, as shown in Table 1. This means that China’s ecological inspection system has been reformed from “supervising enterprises” to “supervising government.” At the same time, the dual-carbon goal has become a solemn commitment by the Chinese government to building a community of human destiny. However, China’s transition from a carbon peak to carbon neutrality will require a tighter schedule and heavier energy and industrial transformation tasks, and it will be more difficult to achieve the nationally determined contribution goal in the second half of the emission reduction process (Jiang et al., 2022; Jiang et al., 2023; Yin and Zhao, 2024b). In this context, it is of certain practical significance to evaluate the implementation effect of central environmental protection inspection.

Table 1. Specific implementation of central environmental protection inspection.

In recent years, with the cost of land, raw materials, labor, and other factors of production rising year by year, the growth of China’s real economy has continued to slow down. However, as the financial market continues to expand and develop, the profit-seeking nature of capital drives non-financial enterprises to be more willing to invest in financial assets with strong profitability and fast liquidation speed (Zhang et al., 2016). As the backbone of China’s real economy, heavily polluting enterprises’ profits have decreased year by year due to multiple factors, such as environmental regulation, “shutdown and conversion,” and rising costs. This has forced some enterprises to reduce or even terminate their physical investments. For heavily polluting enterprises, financial investment not only occupies the funds needed to maintain the main business and green transformation, thus hindering long-term sustainable development, but also constantly pushes up the prices of financial assets, drives up the financial leverage of the whole society, exacerbates financial risks, and even causes serious economic crises (Dai et al., 2018). Therefore, effectively reducing the financialization of heavily polluting enterprises has become an important proposition that urgently needs to be discussed. Under the constraint of central environmental protection inspection, in order to achieve the goal of high environmental protection performance, local government officials must strengthen environmental governance and transfer the pressure of environmental protection layer by layer to heavily polluting enterprises (Kou et al., 2022). As key objects of inspection, heavily polluting enterprises have to adjust their investment and financing decisions, return to their main businesses, and allocate more funds to green projects for their survival and development; thus, they can have a “crowding-out effect” on financial asset investments and promote their own long-term sustainable and high-quality development. Can central environmental protection inspection restrain the financialization of heavily polluting enterprises and encourage them to return to their main businesses? It is necessary to bring central environmental protection inspection into the analytical framework of the factors affecting the financialization of enterprises. There is relatively rich discussion in the existing literature on the influencing factors of enterprise financialization, but few studies have discussed the relationship between central environmental protection inspection and enterprise financialization. Based on this, this study attempts to explore the impact of central environmental protection inspection on the financialization of heavily polluting enterprises. These findings are conducive to creating procedures that are applicable in business environments in other countries in the context of green transition. This will help developing countries coordinate and strengthen their capacity to cope with climate change and environmental protection.

The contributions and innovations of this study are as follows: First, ecological accountability is incorporated into the analytical framework of the factors influencing corporate financialization for the first time. There are abundant studies on the influencing factors of corporate financialization, but few have provided evidence of the causal relationship between ecological accountability and corporate financialization. Taking advantage of the exogenous impact of the policy of central environmental inspection, this study brings ecological accountability into the analytical framework of corporate financialization and complements the literature on the influencing factors thereof. Second, the effect of governance on ecological accountability is further explored from the perspective of corporate financialization. The previous literature mainly examined the impact of central environmental protection inspection on enterprises’ business performance and green innovation at the micro-level and found that central environmental protection inspection reduced air pollution (Wang et al., 2019; Deng et al., 2021; Li et al., 2021; Lin et al., 2021; Zeng et al., 2021), improved business performance (Chang and Sam, 2015; Bel and Joseph, 2018; Chen et al., 2019; Lv et al., 2020), promoted green innovation (Li et al., 2021), and promoted enterprise transformation and upgrading (Zhao et al., 2022). There is little literature on the effect of governance through central environmental inspection on corporate financialization. On the basis of previous work, this study analyzed the relationship between ecological accountability and corporate financialization, as well as its mechanism of action, and it further complements the research on the effects of governance on ecological accountability. Third, it expands the research perspectives of environmental finance, environmental management, and other disciplines. This study mainly explores the channel between central environmental protection inspection and corporate financial asset investment from the perspective of “green innovation,” providing an empirical exploration to understand how ecological accountability plays a role in green governance, which expands the research perspectives of the disciplines of environmental finance and environmental management.

Corporate financialization refers to the increasing involvement of companies in financial markets during their business activities, utilizing financial instruments and methods for capital operations and management, rather than solely focusing on their core business of production and sales. Arrighi (1994) argued that financialization means that profits are increasingly generated through financial channels rather than trade and commodity production. Dore (2002) stated that financialization is the domination of financial assets among the total assets, and various capital operations steadily replace physical production. Ozgur (2006) argued that financialization, in the narrow sense, refers to a change in the relationship between NFCs and financial markets, which can be an increase in financial investment in NFCs and the resulting financial returns. The above definition of corporate financialization reflects its connotation from two perspectives: first, corporate financialization means that enterprises invest more in or rely more on financial markets; second, the change in the source of corporate profits is caused by the above behavior. Based on this, and with reference to the definitions of Duchin et al. (2017); Xu and Zhu (2017); Xu and Deng (2019); Zhao and Su (2022); Valeeva et al. (2023), this study holds that the melting of enterprise entities is a behavior in which enterprises invest capital in the financial field and obtain profits through financial channels rather than their main business channels.

There are two theories about the motivation of enterprises to hold financial assets. Reservoir theory holds that the financial investment of enterprises is to avoid the operating risk caused by shortages of funds, and financial assets are highly liquid. When an enterprise suffers from a break in the capital chain, its financial crisis can be resolved by selling financial assets. Holding financial assets for precautionary motives can allow sudden business risks to be resisted and is conducive to the healthy and sustainable development of enterprises. According to the investment substitution theory, the purpose of holding financial assets is to obtain a high rate of return. In other words, when the profit rate of financial assets is higher than that of the real economy, enterprises will choose to invest in financial assets; otherwise, they are more willing to invest in entities. The decrease in entity investment return and the increase in financial investment return are important factors that lead to the financialization of enterprises. Based on these two theories, scholars have further discussed the influencing factors of corporate financialization from the macro-level in the context of the “Belt and Road” Initiative, interest rate liberalization, inflation, and policy uncertainty, in addition to the micro-level of digital transformation, the informal level of a board of directors, the financial nature of controlling shareholders, and entrepreneur confidence. However, there are few studies on the influencing factors of corporate financialization based on the perspective of central environmental protection inspection. In this study, central environmental protection inspection was used as an event with an exogenous impact, and the A-share-listed companies in Shanghai and Shenzhen, China from 2007 to 2022 were selected as research samples. By constructing a multi-period differential model, the influence of central environmental protection inspection on the financialization behavior of heavily polluting enterprises was empirically tested.

Real investment decisions are the fundamental factors affecting the financialization of enterprises. Increasing investment in entities can weaken the motivation for enterprises’ financialization and the ability to realize it, which is an effective way to restrain enterprises from “moving from real to virtual.” Therefore, this study demonstrates the impact of central environmental protection inspection on the allocation of financial assets of heavily polluting enterprises from the perspective of physical investment.

Central environmental protection inspection promotes green innovation and inhibits the allocation of the financial assets of heavily polluting enterprises. The investment substitution theory suggests that the survival and development of enterprises cannot be separated from resource support, but there are obvious boundaries between the resource constraints of enterprises, and there is an obvious substitutive relationship between financial investment and entity project investment (Demir, 2009; Du et al., 2017). The allocation of corporate financial assets is bound to crowd out physical projects that need long-term investment. Central environmental protection inspection closely combines the assessment of officials for promotion with the assessment of environmental protection performance, thus improving the determination and enthusiasm of local governments to control environmental pollution and strengthen environmental law enforcement. In inspections of environmental protection, inspection teams assess environmental pollution by investigating data, accepting reports, spot checking, conducting environmental protection interviews, and “looking back,” among other means. After receiving inspection feedback, local governments must punctually submit a rectification plan to the State Council, hold the relevant responsible persons accountable according to the law, and announce the implementation of this rectification to the public. It can be seen that central environmental protection inspection is bound to increase the intensity of environmental regulation for polluting enterprises in the jurisdiction. In order to alleviate the political pressure of ecological accountability and avoid the negative impact of environmental punishment on business activities, heavily polluting enterprises have to increase their green research and development and reduce the release, emission, leakage, overflow, or escape of pollutants through green technology innovations so as to reduce the probability of environmental pollution accidents and environmental punishment while meeting the rectification requirements. At this time, in order to reduce environmental risk, the polluting enterprises in the jurisdiction will invest more resources in their environmental governance. Green innovation locks up the occupation of resources in advance, crowding out financial asset investment, and the level of enterprise financialization also decreases. Therefore, with a strong political binding force, central environmental protection inspection forces the heavily polluting enterprises in a jurisdiction to carry out green innovation, thus inhibiting the allocation of corporate financial assets.

Based on this, this study puts forward the following research hypothesis:

H1:. Central environmental protection inspection significantly inhibits the financialization of heavily polluting enterprises.

In this study, China’s A-share-listed companies from 2007 to 2022 were selected as the research sample, and sample screening was carried out according to the following steps: first, eliminate the samples containing “St,” a suspension of a listing, delisting, or a new listing in that year were eliminated; second, the samples of financial, insurance, and real estate enterprises were eliminated; third, samples with an asset liability ratio of less than 0 or greater than 1 and with an operating revenue and operating cost of 0 were excluded; fourth, samples with serious data loss were eliminated. Finally, a total of 30,619 effective sample observations were obtained, including 6721 observations in the experimental group of heavily polluting enterprises and 23,898 observations in the control group of non-heavily polluting enterprises. The relevant information for central environmental protection inspection came from the official website of the Ministry of Ecological and Environmental Protection of China, and the data on each company’s financial characteristics and corporate governance characteristics were obtained from the CSMAR database, the WIND database, and the RESSET database. In order to alleviate the influence of outliers on the empirical results, the continuous variables were bilaterally winsorized by 1%.

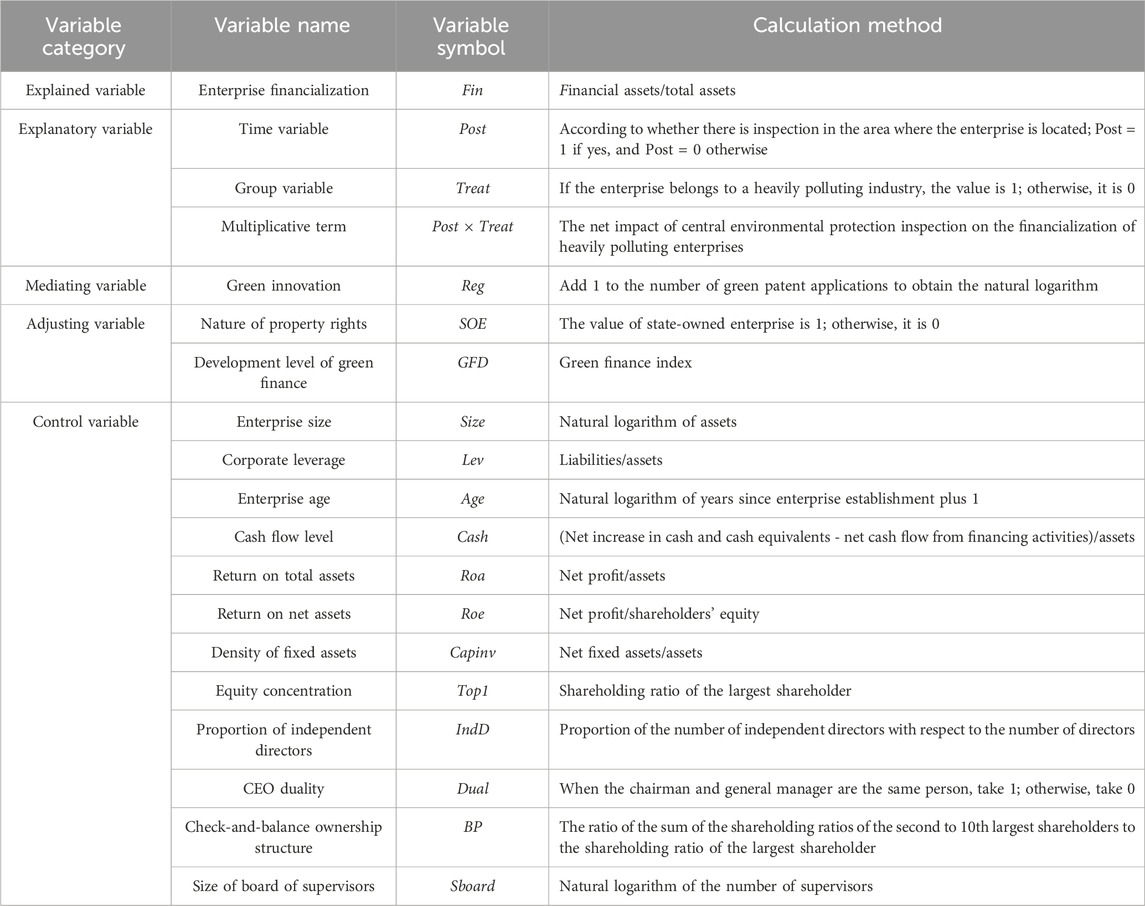

Referring to Demir (2009); Duchin et al. (2017); Xu and Zhu (2017); Xu and Deng (2019); Li et al. (2023), this study defined “trading financial assets,” “derivative financial assets,” “long-term equity investment,” “investment real estate,” “available-for-sale financial assets,” and “held-to-maturity investment” as financial assets, and it used the proportion of financial assets with respect to total assets to measure the degree of enterprise financialization (Fin). Since the new accounting standards in 2018 no longer used the two subjects of “held-to-maturity investment” and “available-for-sale financial assets,” after 2018 (including 2018), the total sum of “other debt investment,” “other noncurrent financial assets,” and “other equity instrument investment” replaced “available-for-sale financial assets,” and “held-to-maturity investment” was replaced with “debt investment.”

Drawing on the research of Zheng and Xu (2023); Wu and Chen (2023), this study set central environmental protection inspection (Post × Treat) as the core explanatory variable. Post was used as a time variable. According to the inspection coverage time shown in Table 1, it was observed whether an inspection team was stationed in the area where an enterprise was located. If yes, Post = 1; otherwise, Post = 0. Treat was used as a grouping variable. If an enterprise was a heavily polluting enterprise, Treat = 1; otherwise, Treat = 0. In this study, according to the Listed Companies Environmental Verification Industry Classification Management Directory issued by the Ministry of Ecology and Environment of China, 16 heavily polluting industries—the thermal power, steel, cement, electrolytic aluminum, coal, metallurgy, building materials, mining, chemical, petrochemical, pharmaceutical, brewing, paper-making, fermentation, textile, and leather industries—were selected. Drawing on the classification methods of Pan et al. (2021) and Liu and Liu (2015) and according to the Guidelines on Industry Classification of China’s Listed Companies, which were revised in 2012, B07 (oil and gas mining), B08 (ferrous metal mining), B09 (non-ferrous metal mining), C25 (petroleum processing, coking, and nuclear fuel processing), C26 (chemical raw material and chemical product manufacturing), C28 (chemical fiber manufacturing), C29 (rubber and plastic products), and C30 (non-metallic mineral products), C31 (ferrous metal smelting and rolling processing), C32 (non-ferrous metal smelting and rolling processing), and D44 (electricity and heat production and supply) were defined as heavily polluting industries.

The mediating variable in this study were green innovation (Reg). Referring to the practices of Zeng et al. (2022); Wang and Wang (2021); Zhang and Li. (2020), the natural logarithm of the number of green patent applications plus 1 was used to measure the green innovation of enterprises.

Referring to the existing research, this study also controlled the important variables affecting enterprise financialization, namely, enterprise size (Size), enterprise leverage (Lev), enterprise age (Age), cash flow level (Cash), return on total assets (ROA), return on net assets (ROE), fixed asset intensity (Capinv), equity concentration (Top1), proportion of independent directors (IndD), CEO duality (Dual), equity checks and balances (BP), and the size of the board of supervisors (Sboard). In addition, the fixed effects of time (Year), industry (Ind), and region (Region) were also controlled. The main variable definitions are shown in Table 2.

Table 2. Variable definitions.

The purpose of this study was to investigate the impact of central environmental protection inspection on the financialization of heavily polluting enterprises, that is, to determine whether and how central environmental protection inspection affects the financialization of heavily polluting enterprises. If it does, how does the relationship change in different economic situations? Firstly, a multi-period difference–difference model was established to explore the impact and mechanism of central environmental protection inspection on corporate financialization, and robustness tests were carried out using parallel trend tests, propensity score matching, replacement of explained variables, and other methods. Secondly, an intermediary effect model was used to test whether central environmental protection inspection had a negative impact on corporate financialization through the path of green innovation. Finally, grouping regression was used to investigate whether there were significant differences in the impact of central environmental protection inspection on corporate financialization with different levels of property rights and green financial development.

As an event with an exogenous impact, central environmental protection inspection is a means of macro-level environmental regulation by the government. Therefore, the multi-period double-difference model was used to investigate the impact of central environmental protection inspection on the financialization of heavily polluting enterprises. The specific model is as follows:

Here, subscripts i and t represent the enterprise and year, respectively, controlsi,t represent the set of control variables, and εi,t is a random disturbance term. The coefficient β3 is the focus of this study, as it reflects the net impact of central environmental inspection on enterprise financialization. If β3 is significantly negative, then central environmental protection inspection reduces the level of financialization of heavily polluting enterprises, assuming that H1 is true.

Secondly, this study draws on the intermediary effect model of Wen et al. (2004) to further test whether green innovation is the intermediary path for central environmental inspection’s effect on the level of financialization of heavily polluting enterprises. Specifically, Model (1) is used to examine the impact of central environmental inspection on the financialization of heavily polluting enterprises. Model (2) is used to examine the impact of central environmental inspection on green innovation (Reg). Model (3) is used to test whether there is an intermediary effect among central environmental inspection and green innovation (Reg). The specific model is as follows:

Here, Regi,t is the intermediary variable green innovation. Referring to the research of Zhang and Zhang (2024), the natural logarithm of the number of green patents +1 is adopted to represent the level of green innovation of an enterprise. Model (2) is a mechanism analysis that is used to identify potential channels affecting the level of financialization of firms, with λ1 as the core coefficient. Model (3) is consistent with Model (1) and is used to test the relationship between central environmental inspection and the financialization of heavily polluting enterprises, with γ1 as the core coefficient. If both λ1 and γ1 are significant, then the intermediation effect holds. The meanings of other variables are consistent with Model (1).

Finally, the whole sample was divided into a state-owned enterprise sample group and a non-state-owned enterprise sample group according to the nature of the enterprises’ property rights, and grouping regression was performed for Model (1). According to the mean value of the green financial development level, the whole sample was divided into a sample group with a high green financial development level and a sample group with a low green financial development level, and group regression was carried out for Model (1).

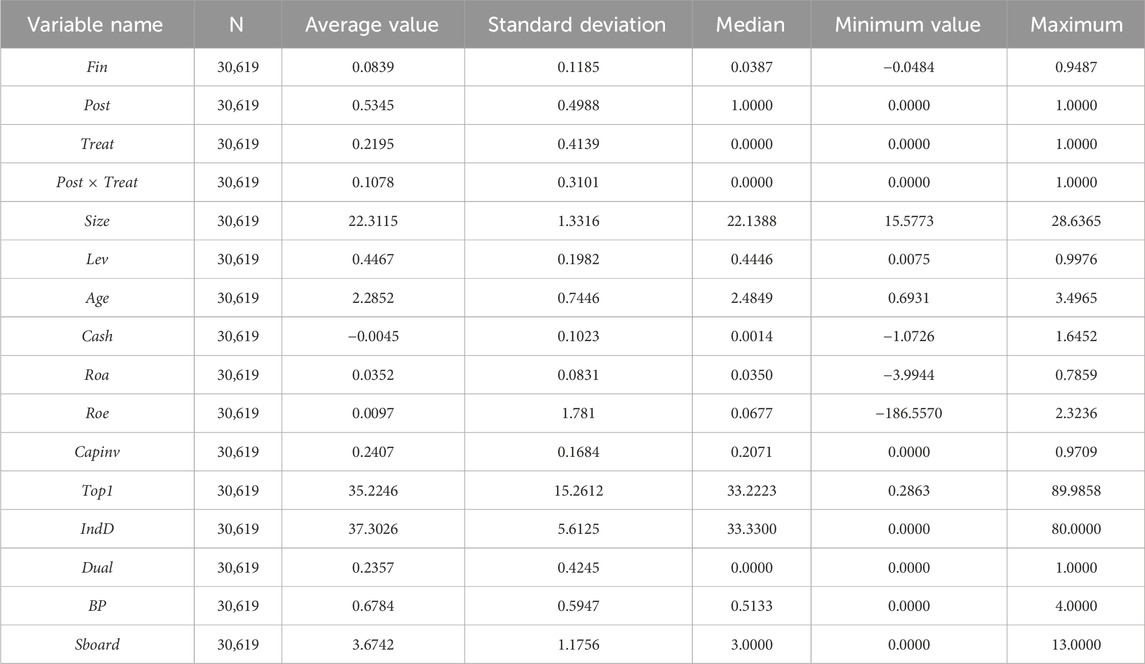

Table 3 shows the descriptive statistics of the variables. The average value of enterprise financialization (Fin) was 0.0839, the standard deviation was 0.1185, the minimum value was −0.0484, and the maximum value was 0.9487. Overall, the average proportion of financial assets of the sample enterprises with respect to their total assets was 8.39%, and there were great differences in the levels of financial asset allocation among the different listed companies. The average value of central environmental protection inspection (Post × Treat) was 0.1078, which meant that 10.78% of the heavily polluting listed companies were affected by central environmental protection inspection.

Table 3. Descriptive statistics.

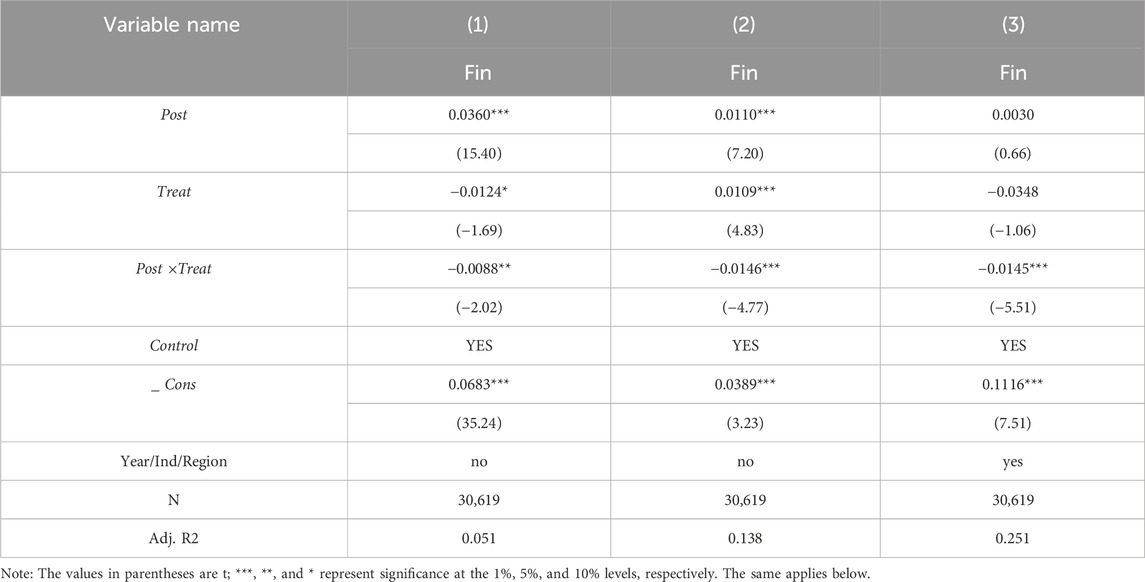

Table 4 reports the regression results for central environmental protection inspection and enterprise financialization. This paper uses model (Eq. 1) to examine the influence of central environmental supervision on the financialization behavior of heavy polluting enterprises. The results in Column (1) did not include any control variables, and the regression results for central environmental protection inspection with respect to enterprise financialization were investigated separately. For Column (2), multiple control variables were added, but the fixed effects of time, industry, and region were not controlled. For Column (3), all control variables were added. The results showed that the estimated coefficients of Post × Treat were −0.0088, −0.0146, and −0.0145, respectively, which were significantly negative at a statistical level of at least 5%, which meant that, compared with the situation for non-heavily polluting enterprises, central environmental protection inspection significantly reduced the level of financialization of heavily polluting enterprises, assuming that H1 was true.

Table 4. Basic regression results.

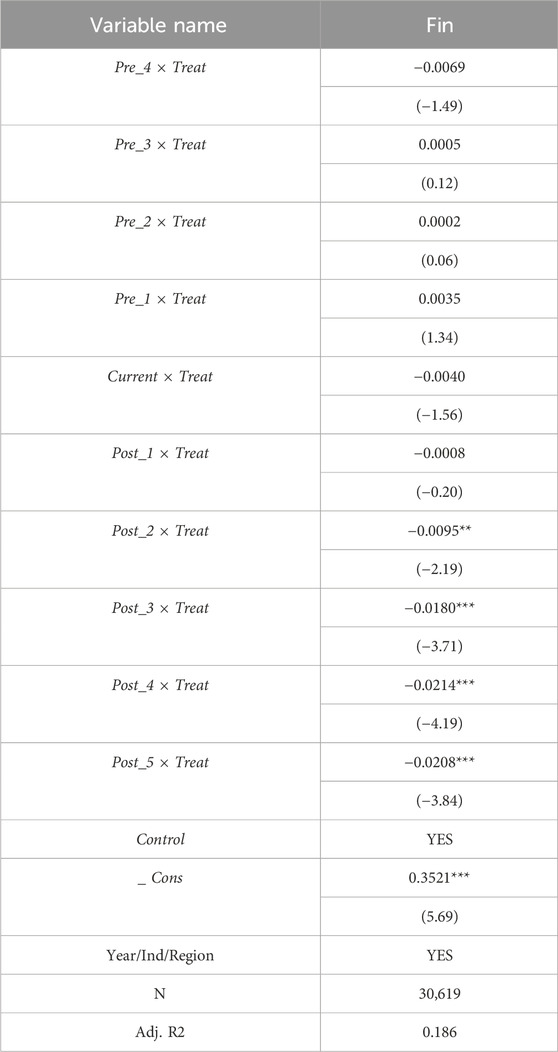

In order to ensure that the reduction in the level of financialization of heavily polluting enterprises was indeed a causal effect of the central environmental protection inspection policy, a parallel trend test was conducted. Table 5 shows the results of the parallel trend test. The coefficients of Pre_ 4 × Treat, Pre_ 3 × Treat, Pre_ 2 × Treat, and Pre_ 1 × Treat were not significant, which showed that before the implementation of central environmental protection inspection, there was no significant difference between the experimental group and the control group in terms of the impact on the level of financialization of enterprises, which was in line with an important premise of the double-difference parallel trend. The coefficients of Current × Treat and Post_1 × Treat were not significant, although the coefficients of Post_2 × Treat, Post_3 × Treat, Post_4 × Treat, and Post_5 × Treat were significantly negative at the level of at least 5%, indicating that after the implementation of central environmental protection inspection, the two groups of samples showed significant differences. This meant that, compared with the situation before the implementation of central environmental protection inspection, ecological accountability significantly inhibited the financialization of heavily polluting enterprises, thus further supporting Hypothesis 1.

Table 5. Results of the parallel trend test.

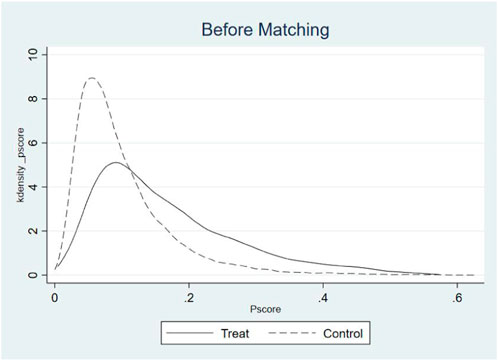

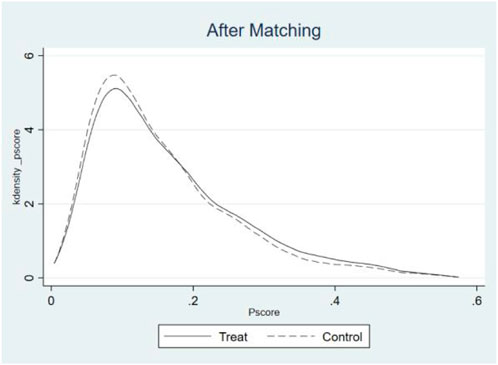

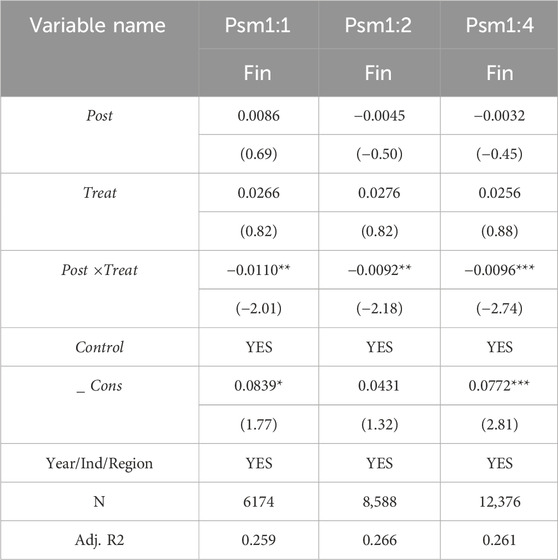

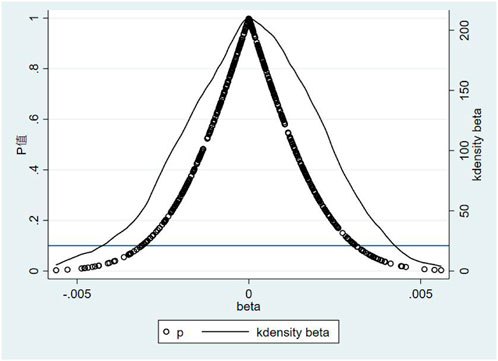

The propensity score matching method was used to control the systematic differences between the experimental group and the control group, and regression was performed again. First, the enterprise size, enterprise leverage, enterprise age, cash flow level, return on total assets, return on net assets, fixed asset intensity, equity concentration, proportion of independent directors, CEO duality, check-and-balance ownership structure, and size of the board of supervisors were selected as matching variables, and 1:1 no-return-sampling nearest neighbor matching was carried out to screen out effective samples for heavily polluting enterprises in the control group. Finally, Model (1) was used to test the matched samples again. Figures 1, 2 show the distribution of the kernel density before and after matching. After matching, the probability density distribution of the two groups of samples tended to be consistent, and the matching quality was good. Table 6 reports the regression results for the PSM samples. In Column (1), Post × Treat had a coefficient of −0.0110, which was significantly negative at the 5% level. In addition, the 1:2 and 1:4 nearest neighbor sampling methods were used to match. The results are shown in Columns (2) and (3) of Table 7, where the coefficients of Post × Treat were all significantly negative. This supports the research hypothesis of this study.

Figure 1. Kernel density map before matching.

Figure 2. Kernel density map after matching.

Table 6. PSM test results.

Table 7. Redefinition of heavily polluting enterprises.

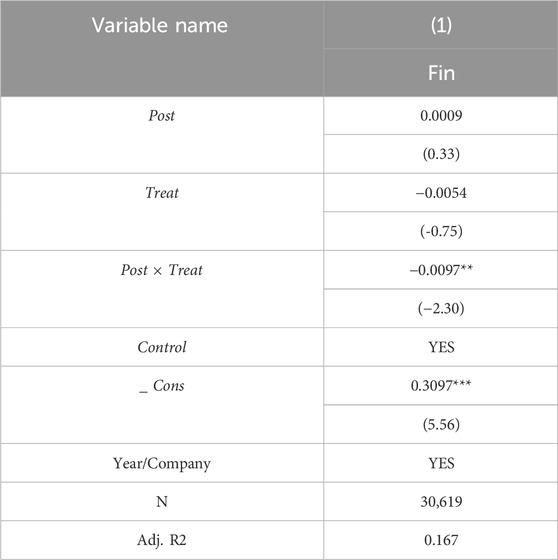

Referring to the practice of Jiang and Cui (2019), the industry classification codes of the CSRC were listed as B (mining industry), C0 (food and beverage), C1 (textile, clothing, fur), C3 (papermaking, printing), C4 (petroleum, chemistry, plastics), C6 (metal and non-metal), C8 (medicine and biological products), and D (electricity, gas, and water production and supply industry); Model (1) was reused for regression, and the test results are shown in Column (1) of Table 7. The coefficient of Post×Treat1 was −0.0083, which was significantly negative at the 5% level, consistently with the main conclusion.

The previous research results showed that central environmental protection inspection significantly reduced the degree of financialization of heavily polluting enterprises, but in order to ensure that this result was not caused by other missing variables or other unobservable variables, a placebo test was used as a robustness test. Referring to the practice of Li and Xiao (2023), central environmental protection inspection (Post × Treat) was randomly selected 500 times to check if the coefficient was significantly different from that in the results of the basic regression. It can be seen in Figure 3 that the estimated coefficients were mostly concentrated near the value of 0, which was far from the true regression coefficient. This showed that central environmental protection inspection failed to pass the significance test with 500 iterations of sampling. The reduction in the level of financialization of heavily polluting enterprises was caused by central environmental protection inspection.

Figure 3. Placebo test chart.

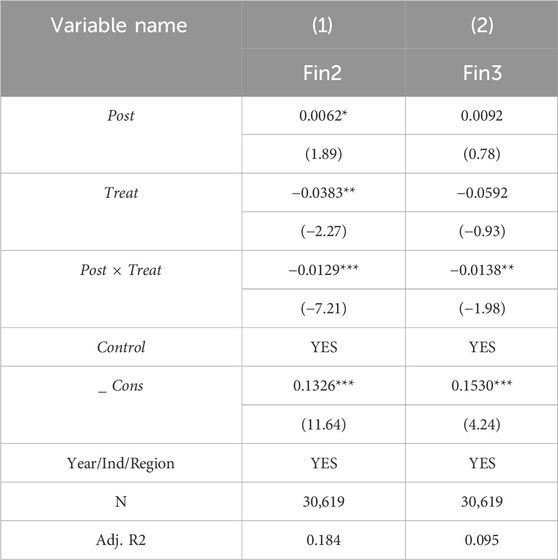

In order to rule out the possible influence of the differences in the measurement methods for the explained variable on the conclusion of this research, the measurement method for the explained variable Post × Treat was adjusted, and Model (1) was re-regressed. First, based on the research of Du et al. (2017); Cai et al. (2021), the Fin2 index was constructed, and enterprise financialization was defined as (trading financial assets + derivative financial assets + available-for-sale financial assets + held-to-maturity investment + loans and advances issued + investment real estate)/total assets. The regression results are shown in Column (1) of Table 8. The coefficient of Post×Treat was −0.0129, which was significant at the 1% level. Secondly, using the research of Wang et al. (2017) for reference, the Fin3 index was constructed. If an enterprise allocated financial assets, Fin3 was set to 1; otherwise, it was set to 0. The regression results are shown in Column (2) of Table 10, and the coefficient of Post×Treat was −0.0138, which was significantly negative. This showed that the conclusion of this research is robust.

Table 8. Replacement of the explained variables.

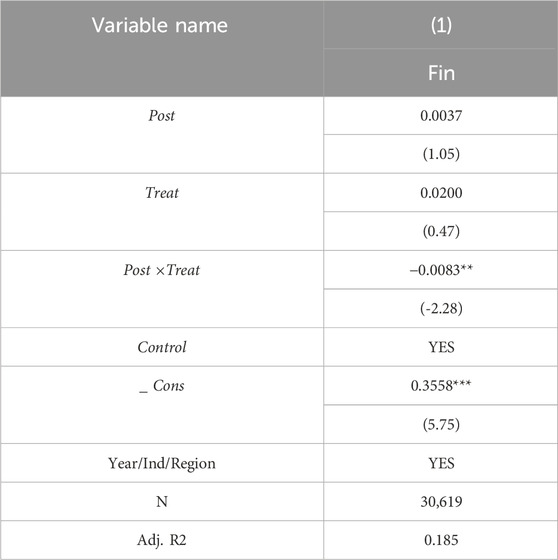

In order to control the other exogenous factors in the sample interval and unobservable factors at the individual level of the company, a two-way fixed effect model was used for regression. Table 9 shows the regression results of the fixed effect model. The coefficient of Post × Treat was significantly negative at the 5% level, which again proved the robustness of the conclusion.

Table 9. Results of the fixed effect test.

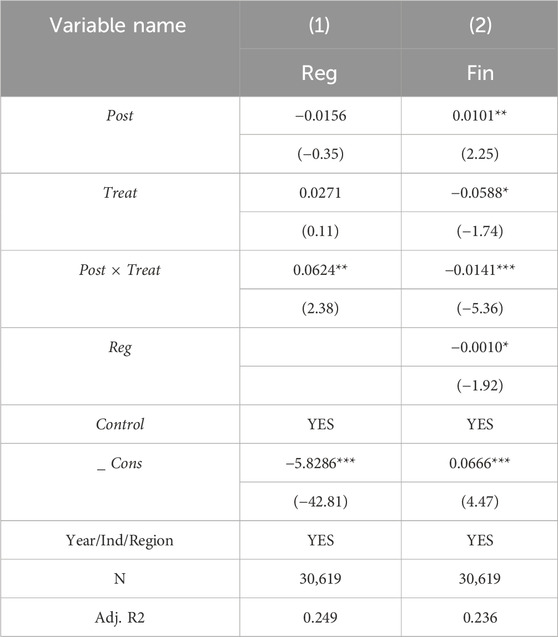

With the central environmental protection inspection system, heavily polluting enterprises have to improve their green technology innovation and actively implement environmental governance in order to avoid the business risks brought by environmental punishment. Green innovation requires enterprises to invest significant amounts of money, and under the condition of limited funds, they are bound to reduce their investments in financial assets. However, central environmental protection inspection may reduce the level of financialization of heavily polluting enterprises by promoting their green innovation. In order to test whether central environmental protection inspection affects the financialization behavior of heavily polluting enterprises through the path of influencing green innovation, Models (2) and (3) were regressed, and the results are shown in Columns (1) and (2) of Table 10. In Column (1), the coefficient of Post × Treat was 0.0624, which was significantly positive at the 5% level, indicating that central environmental protection inspection significantly promoted the green innovation of the supervised enterprises. In Column (2), the coefficient of Post × Treat was −0.0141, which was significantly negative at the 1% level. The coefficient of Reg was −0.0010, which was significantly negative at the 10% level, indicating that central environmental protection inspection reduced the financialization of heavily polluting enterprises by promoting green innovation, and green innovation played a mediating role in the impact of central environmental protection inspection on the financialization of enterprises.

Table 10. Results of the test on mediating effect.

It was confirmed that central environmental protection inspection inhibited the financialization of heavily polluting enterprises, and the relationship between these two aspects may have been affected by objective conditions. Based on this, this study examined whether there were significant differences in the impact of central environmental protection inspection on enterprise financialization in different economic situations. A cross-sectional test was carried out from the perspectives of the nature of property rights and the development level of green finance.

The impact of central environmental protection inspection on the financialization of heavily polluting enterprises was closely related to the implementation of the policy. As local pillar enterprises, the managers of state-owned enterprises are appointed directly by the government. The government internalizes its political objectives into the development strategies and daily operation of state-owned enterprises so that they can serve the implementation of policies in their respective jurisdictions. Central environmental protection inspection links environmental protection performance with official promotion, and government officials who fail to complete assessment tasks will be directly dismissed. For the sake of their own political careers, the executives of state-owned enterprises can take timely action to comprehensively and vigorously rectify polluting projects and prevent backlash. Therefore, compared with that for non-state-owned enterprises, the impact of central environmental protection inspection on the financialization of state-owned enterprises may be more obvious. To this end, the whole sample was divided into state-owned enterprises and non-state-owned enterprises according to the nature of their property rights, and a grouping regression was performed on Model (1). The results are shown in Columns (1) and (2) of Table 11. In the sample group of state-owned enterprises, the Post × Treat coefficient was −0.0064, which was significantly negative at the 10% level. In the sample group of non-state-owned enterprises, the Post × Treat coefficient was −0.0089, which was not significant. This showed that central environmental protection inspection mainly reduced the level of financialization of heavily polluting state-owned enterprises.

Table 11. Results of the cross-sectional test.

With the rapid development of green finance, banks and other financial institutions are more inclined to provide sufficient and lower-cost funds for green enterprises and green projects, thus increasing the financing difficulty for heavily polluting enterprises. In areas with a high level of green financial development, it is difficult for heavily polluting enterprises to obtain sufficient funds due to the production and consumption of highly polluting products, which weakens the motivation for financialization. Therefore, compared with regions with a low level of green financial development, the impact of central environmental protection inspection on the financialization of heavily polluting enterprises in regions with a high level of green financial development may be more obvious. Therefore, the whole sample was divided into a sample group with a high level of green financial development and a sample group with a low level of green financial development according to the average level, and grouping regression was performed on Model (1). The results are shown in Columns (3) and (4) of Table 11. In the high green financial development sample group, the estimated coefficient of Post × Treat was −0.0174, which was significantly negative at the 1% level; in the low green financial development sample group, the estimated coefficient of Post × Treat was −0.0046, which failed the significance test. This showed that the inhibitory effect of central environmental protection inspection on the level of financialization of heavily polluting enterprises was more significant in enterprises in areas with a higher level of development of green finance.

An ecological accountability system, which is the key to promoting the construction of a green policy for China, is an important starting point for promoting the high-quality development of heavily polluting enterprises. Based on the perspective of central environmental protection inspection, this study examined the inhibitory effect, path of action, and cross-sectional differences in ecological accountability with respect to the level of financialization of heavily polluting enterprises by taking A-share-listed companies in Shanghai and Shenzhen as research samples. First, the results showed that central environmental inspection is significantly negatively correlated with the financialization of heavily polluting enterprises. This shows that central environmental inspection is conducive to curbing the financialization of heavily polluting enterprises. Inhibiting the heavy pollution enterprises “from real to virtual,” and maintaining the stability of the financial system has become an important issue that the Chinese government urgently needs to solve. Ecological accountability puts forward clear requirements for local governments’ environmental rectification and is linked to officials’ performance. Under the compulsory constraints of central environmental protection inspection, the pressure of environmental governance is shifted from administrative departments for supervision to enterprises. In order to reach environmental performance goals, local government officials are bound to increase environmental governance efforts and strongly deter heavily polluting enterprises in their jurisdictions. In order to meet the rectification requirements and restore normal production, heavily polluting enterprises have to adjust their investment and financing decisions and allocate more funds to green projects so as to alleviate the crowding out of real investment by financialization with the incentive of enterprise entity substitutions and to inhibit financialization.

Second, the mechanism analysis showed that central environmental protection inspection mainly inhibits financial asset allocation by promoting green innovation. Central environmental inspection places a rigid constraint on the environmental governance behavior of local governments and passes the pressure of environmental protection to heavily polluting enterprises. Central environmental protection inspection is bound to increase the intensity of environmental regulations on polluting enterprises in their jurisdictions. On the one hand, in order to ease the political pressure of ecological accountability and avoid the negative impact of environmental penalties on corporate business activities, heavy polluters have to increase their green research and development, which inhibits the allocation of corporate financial assets. On the other hand, for the sake of their own careers, members of the management must invest more funds in corporate environmental governance, improve their environmental performance, reduce their environmental pollution, and form a long-term investment mechanism that focuses on the main business of each entity. This can discourage management from investing in financial assets. This shows that the implementation of central environmental protection inspection can force heavily polluting enterprises to return to their main businesses, promote green innovation and transformation, have a “crowding-out effect” on financial assets, and weaken their motivation for pursuing short-term profit instead of focusing on sustainable and high-quality development.

Finally, the heterogeneity test showed that the inhibitory effect of central environmental inspection on enterprise financialization was more significant in the sample group of state-owned enterprises and areas with a higher level of development of green finance. This indicated that the nature of property rights and the level of development of green finance were important moderating variables affecting the relationship between central environmental inspection and corporate financialization. On the one hand, unlike in non-state-owned enterprises, managers of state-owned enterprises are directly appointed by the government. For the sake of their own political careers, executives of state-owned enterprises act in a timely manner to comprehensively rectify polluting projects and forcefully regulate them to prevent backlash. Therefore, compared with the effect on non-state-owned enterprises, central environmental protection inspection mainly reduces the level of financialization of heavily polluting state-owned enterprises. On the other hand, in areas with a high level of green financial development, heavily polluting enterprises have difficulty in obtaining sufficient funds due to the production and consumption of highly polluting products, thus weakening the motivation for financialization. Therefore, compared with the effect in areas with a low level of green financial development, central environmental protection inspection mainly reduces the level of financialization of heavily polluting enterprises in areas with a high level of green financial development.

Based on the above conclusions, this study puts forward the following policy recommendations.

First, we will continue to promote the regular development of central environmental protection inspection. This study found that central environmental inspection has a restraining effect on the financialization behavior of heavily polluting enterprises, which verifies the effectiveness of this supervision policy. In the future, the regulatory authorities should focus on how to scientifically and reasonably deepen the central environmental inspection system, establish a regular operation mechanism, effectively play the role of external supervision, improve the enthusiasm of local officials in governance, and promote coordinated economic development with green policies so as to promote the construction of green policies in China.

Second, we will increase support for green innovation projects in heavily polluting enterprises. The conclusion of this study indicates that central environmental inspection can reduce the level of financialization of heavily polluting enterprises by improving their green innovation. Therefore, the regulatory authorities should not only inspect environmental performance but also fully consider the status quo and quality of the green innovation of heavily polluting enterprises, select enterprises with remarkable green transformation results as typical examples, and give certain financial subsidies. Heavily polluting enterprises should consider a long-term perspective, rationally allocate their financial assets, reduce their dependence on financial assets, focus on their physical business, and actively look for promising physical investment projects.

Third, environmental supervision should be carried out in accordance with local conditions. From the cross-sectional analysis, it was seen that listed companies and state-owned enterprises in areas with higher levels of development of green finance are more sensitive to environmental protection supervision and are more able to restrain their corporate financialization behavior. Therefore, the regulatory authorities should flexibly adjust the time and intensity of supervision for enterprises with different types of property rights and levels of green financial, list enterprises in areas with low levels of green financial development as key inspection enterprises, and strengthen the intensity of supervision of non-state-owned enterprises in order to promote the transformation of heavily polluting industries into green industries through “precise” inspectors.

Based on a large sample, this study empirically examined the impact of ecological accountability on corporate financialization by using central environmental inspection as a quasi-natural experiment. However, there are great differences in practice among different companies. Therefore, typical cases can be selected in future research, and the case study method can be used to conduct analyses of specific companies. From the perspective of the research content, when local environmental protection departments exert environmental regulation pressure on heavily polluting enterprises in their jurisdiction, they will also provide certain policy support to these enterprises in order to mobilize their enthusiasm for environmental governance. In our future research, we will study the synergistic effect of environmental protection incentive policies and central environmental inspection on the financial behavior of heavily polluting enterprises. This will contribute to a more in-depth assessment of the effectiveness of the implementation of central environmental protection inspection.

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

WW: Investigation, Software, Writing–original draft, Writing–review and editing. CZ: Formal Analysis, Methodology, Project administration, Writing–original draft, Writing–review and editing. JN: Conceptualization, Project administration, Resources, Visualization, Writing–original draft, Writing–review and editing. SY: Formal Analysis, Funding acquisition, Investigation, Writing–review and editing. DZ: Supervision, Validation, Writing–original draft, Writing–review and editing.

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. This research received funding from the Hebei Provincial Department of Education University Humanities and Social Sciences Research Project “Research on Evaluation of Green Governance Effect of Environmental Pollution Liability Insurance for Listed Companies under the “Double Carbon” Goal” (BJS2022003) and Hebei Agriculture Research System (HBCT2024020301).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2024.1400725/full#supplementary-material

Arrighi, G. (1994). The long twentieth Century.Money,Power and the origins of our times. London,New York: Verso.

Bel, G., and Joseph, S. (2018). Policy stringency under the European Union Emission trading system and its impact on technological change in the energy sector. Energy Policy 117, 434–444. doi:10.1016/j.enpol.2018.03.041

Cai, H., and Treisman, D. (2006). Did government decentralization cause China's economic miracle? World Polit. 4, 505–535. doi:10.1353/wp.2007.0005

Cai, H. J., Xie, Q. X., and Zhang, H. M. (2021). Contingency or profit seeking: institutional logic of entity enterprise financialization from the perspective of environmental regulation. Account. Res. 4, 78–88.

Chang, C. H., and Sam, A. G. (2015). Corporate environmentalism and environmental innovation. J. Environ. Manag. 153, 84–92. doi:10.1016/j.jenvman.2015.01.010

Chen, R. J., Xiao, Q. L., Lan, S. Q., and Liu, J. Q. (2019). Can the central environmental protection inspector improve enterprise performance -- Take listed industrial enterprises as an example. Econ. Rev. 5, 36–49. doi:10.19361/j.er.2019.05.03

Dai, S., Peng, Y. C., and Ma, S. C. (2018). Understanding the "Disenchantment" of economy from a micro perspective -- a review of relevant studies on enterprise financialization. Foreign Econ. Manag. 11, 31–43. doi:10.16538/j.cnki.fem.2018.11.003

Demir, F. (2009). Capital market impacts and financing of real sectors in emerging markets: private investment and cash flow relationship revised. World Dev. 5, 953–964. doi:10.1016/J.WORLDDEV.2008.09.003

Demir, F. (2009). Financial liberalization, private investment and portfolio choice: financing of real sectors in emerging markets. J. Dev. Econ. 2, 314–324. doi:10.1016/j.jdeveco.2008.04.002

Deng, H., Gan, T. Q., and Tu, Z. G. (2021). China's road to atmospheric environment governance -- Based on the exploration of the central environmental protection inspection system. Econ. Q. 5, 1591–1614. doi:10.13821/j.cnki.ceq.2021.05.05

Du, Y., Zhang, H., and Chen, J. Y. (2017). The impact of financialization on the main business development of real enterprises in the future: promotion or inhibition. China Ind. Econ. 12, 113–131. doi:10.19581/j.cnki.ciejournal.20171214.007

Duchin, R., Gilbert, T., Harford, J., and Hrdlicka, C. (2017). Precautionary savings with risky assets: when cash is not cash. J. Finance 2, 793–852. doi:10.1111/jofi.12490

Jiang, H. D., Purohit, P., Liang, Q. M., Dong, K., and Liu, L. J. (2022). The cost-benefit comparisons of China's and India's NDCs based on carbon marginal abatement cost curves. Energy Econ. 109, 105946. doi:10.1016/j.eneco.2022.105946

Jiang, H. D., Purohit, P., Liang, Q. M., Liu, L. J., and Zhang, Y. F. (2023). Improving the regional deployment of carbon mitigation efforts by incorporating air-quality co-benefits: a multi-provincial analysis of China. Energy Econ. 204, 107675. doi:10.1016/j.ecolecon.2022.107675

Jiang, Y. B., and Cui, G. H. (2019). Research on the impact of environmental protection industrial policies on environmental pollution -- Based on the perspective of environmental protection investment of heavily polluting enterprises. South. Econ. 9, 51–68. doi:10.19592/j.cnki.scje.360944

Kou, P., Han, Y., and Qi, X. (2022). The operational mechanism and effectiveness of China's central environmental protection inspection: evidence from air pollution. Soc. Econ. Plan. Sci. 81, 101215. doi:10.1016/j.seps.2021.101215

Li, T., and Xiao, Y. (2023). Environmental regulation and financing constraints of heavily polluting enterprises–a quasi natural experiment based on the central environmental protection inspection. J. Harbin Univ. Commer., Soc. Sci. Ed. 3, 72–86.

Li, Y., Gao, D., and Wei, P. (2021). Can the central environmental protection inspection induce enterprises' green innovation? Sci. Res. 8, 1504–1516. doi:10.16192/j.cnki.1003-2053.20210202.004

Li, Y. M., Hu, J. F., and Huang, Q. H. (2023). Financialization of real enterprises and total factor productivity: reservoir effect or crowding out effect? Contemp. Financial Res. 11, 88–107. doi:10.20092/j.cnki.ddjryj.2023.11.007

Li, Z. C., Liu, S. D., and Yang, F. (2021). Environmental protection inspection, the relationship between government and business and the effect of air pollution control -- a quasi experimental study based on the central environmental protection inspection. Public Manag. Rev. 4, 105–131.

Lin, J., Long, C., and Yi, C. (2021). Has central environmental protection inspection improved air quality? Evidence from 291 Chinese cities. Environ. Impact Assess. Rev. 90, 106621. doi:10.1016/j.eiar.2021.106621

Liu, Y. G., and Liu, M. N. (2015). Does haze affect earnings management of heavily polluting enterprises -- an investigation based on the political cost hypothesis. Account. Res. 3, 26–33.

Lv, X., Qi, Y., and Dong, W. (2020). Dynamics of environmental policy and firm innovation: asymmetric effects in Canada's oil and gas industries. Sci. Total Environ. 712, 136371. doi:10.1016/j.scitotenv.2019.136371

Ozgur, O. (2006). Financialization of the U.S. Economy and its Effects on Capital Accumulation: a Theoretical and Empirical Investigation. Ph.D. Thesis (Amherst: University of Massachusetts Amherst).

Pan, A. L., Zhang, G. Z., and Qiu, J. L. (2021). Will two-way performance feedback affect the timing of green M&A for heavily polluting enterprises? Econ. Manag. Res. 3, 64–82. doi:10.13502/j.cnki.issn1000-7636.2021.03.005

Sun, Y., Wu, S., and Wang, Z. Q. (2023). The impact of green credit policy on heavily polluting enterprises. China Popul. Resour. Environ. 3, 91–101.

Valeeva, D., Klinge, T. J., and Aalbers, M. B. (2023). Shareholder payouts across time and space: an internationally comparative and cross-sectoral analysis of corporate financialisation. New Polit. Econ. 02, 173–189. doi:10.1080/13563467.2022.2084522

Wang, H. J., Cao, Y. Q., Yang, Q., and Yang, Z. (2017). Does the financialization of real enterprises promote or inhibit enterprise innovation -- Based on the empirical study of listed companies in China's manufacturing industry. Nankai Manag. Rev. 1, 155–166.

Wang, L., Liu, X. F., and Xiong, Y. (2019). Central environmental protection inspection and air pollution control -- an empirical analysis based on micro panel data of prefecture level cities. China Ind. Econ. 10, 5–22.

Wang, X., and Wang, Y. (2021). Research on the green innovation effect of environmental information disclosure -- a quasi natural experiment based on the ambient air quality standard. Financial Res. 10, 134–152.

Wen, Z. L., Zhang, L., Hou, J. T., and Liu, H. Y. (2004). Mediation effect test procedure and its application. Acta Psychol. Sin. 5, 614–620.

Wu, X., and Chen, X. (2023). Central Environmental protection inspection, local government competition and enterprise environmental protection investment. Audit Econ. Res. 2, 97–106.

Xia, W., Li, B., and Yin, S. (2020). A prescription for urban sustainability transitions in China: innovative partner selection management of green building materials industry in an integrated supply chain. Sustainability 12 (7), 2581. doi:10.3390/su12072581

Xu, G., and Zhu, W. D. (2017). Financialization, market competition and R&D investment crowding out -- Empirical evidence from non-financial listed companies. Sci. Res. 5, 709–719. doi:10.16192/j.cnki.1003-2053.2017.05.008

Xu, J., Tong, B., Wang, M., and Yin, S. (2024). Does environmental pollution governance contribute to carbon emission reduction under heterogeneous green technological innovation? Empirical evidence from China’s provincial panel data. Environ. Dev. Sustain. 15, 1–30. doi:10.1007/s10668-024-04655-w

Xu, Z. Y., and Deng, C. (2019). Research on the impact of financialization on corporate social responsibility information disclosure from the perspective of conflict of interest. China Soft Sci. 5, 168–176.

Yin, S., Yu, Yu, and Zhang, N. (2024). The effect of digital green strategic orientation on digital green innovation performance: from the perspective of digital green business model innovation. SAGE Open 14 (2), 1–23. doi:10.1177/21582440241261130

Yin, S., and Zhao, Y. (2024a). An agent-based evolutionary system model of the transformation from building material industry (BMI) to green intelligent BMI under supply chain management. Humanit. Soc. Sci. Commun. 11 (1), 468–515. doi:10.1057/s41599-024-02988-5

Yin, S., and Zhao, Y. (2024b). Digital green value co-creation behavior, digital green network embedding and digital green innovation performance: moderating effects of digital green network fragmentation. Humanit. Soc. Sci. Commun. 11 (1), 228–312. doi:10.1057/s41599-024-02691-5

Zeng, C. L., Liu, L., Li, J. T., and Li, L. (2022). Environmental protection assessment and enterprise green innovation -- a quasi natural experiment based on the pilot audit of leading cadres' natural resource assets. Account. Res. 3, 107–122.

Zeng, H., Dong, B., Zhou, Q., and Jin, Y. (2021). The capital market reaction to central environmental protection inspection: evidence from China. J. Clean. Prod. 279, 123486. doi:10.1016/j.jclepro.2020.123486

Zhang, C. S., and Zhang, B. T. (2016). The mystery of the decline of China's industrial investment rate: from the perspective of economic financialization. Econ. Res. 12, 32–46.

Zhang, W., and Li, G. (2020). Environmental decentralization, environmental protection investment, and green technology innovation. Environ. Sci. Pollut. Res. 12, 12740–12755. doi:10.1007/s11356-020-09849-z

Zhao, H. F., Li, S. Y., and Wu, Z. W. (2022). The impact of central environmental protection inspection on the transformation and upgrading of manufacturing enterprises -- a test of the intermediary effect based on the process of marketization. Manag. Rev. 6, 3–14. doi:10.14120/j.cnki.cn11-5057/f.20210623.002

Zhao, Y., and Su, K. (2022). Economic policy uncertainty and corporate financialization: evidence from China. Int. Rev. Financial Analysis 82, 102182. doi:10.1016/j.irfa.2022.102182

Zheng, Z. Y., and Xu, Y. B. (2023). Central environmental protection inspection, second generation involvement and ESG responsibility rating of family enterprises. Econ. Manag. 6, 30–39.

Keywords: ecological accountability, central environmental protection inspection, enterprise financialization, heavily polluting enterprises, green transformation

Citation: Wang W, Zhao C, Ning J, Yin S and Zhang D (2024) Does ecological accountability restrain the financialization of heavily polluting enterprises? Evidence from China. Front. Environ. Sci. 12:1400725. doi: 10.3389/fenvs.2024.1400725

Received: 22 March 2024; Accepted: 26 June 2024;

Published: 12 July 2024.

Edited by:

Jinxin Zhu, Sun Yat-sen University, ChinaReviewed by:

Hong-Dian Jiang, China University of Geosciences, ChinaCopyright © 2024 Wang, Zhao, Ning, Yin and Zhang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Jinhui Ning, bmluZ2ppbmh1aTExMjBAMTYzLmNvbQ==; Shi Yin, c2h5c2hpMDMxNEAxNjMuY29t

†ORCID: Shi Yin, orcid.org/0000-0001-6885-7412

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.