Rufeng Zhuo1

Rufeng Zhuo1 Yunhua Zhang

Yunhua Zhang Junwei Zheng

Junwei Zheng

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 05 March 2024

Sec. Environmental Economics and Management

Volume 12 - 2024 | https://doi.org/10.3389/fenvs.2024.1361576

Green innovation is an essential strategy for businesses to gain a competitive edge and attain long-term sustainable growth. It does, however, often run into money problems. The rapid advancement of digital technology provides organizations with potent tools to get external resources through digital transformation, surmount resource obstacles, and promote environmentally-friendly innovation. The impact mechanism, however, necessitates additional elucidation. This article analyzes the data of Chinese A-share listed firms from 2012 to 2022, using resource dependence theory and stakeholder theory. This study examines how digital transformation affects the ability of organizations to innovate in environmentally friendly ways by focusing on the acquisition of external resources. Research has shown that digital transformation may significantly improve the quantity and quality of green innovation in businesses. Moreover, the findings of the intermediate impact study indicate that digital transformation has the potential to enhance the green innovation capacity of businesses by improving their environmental, social, and governance (ESG) standards. Concurrently, we noticed that the level of openness in disclosing environmental information by corporations and the quality of partnerships between the government and enterprises play a positive role in influencing the effects of digital transformation on the ability to innovate in environmentally friendly ways. Based on the findings of our research, we provide fresh perspectives and policy suggestions to assist business managers and governments in fostering environmentally-friendly innovation in enterprises.

Recognizing the environmental crisis triggered by economic development, China and the United States, as the world’s largest economies, jointly issued a statement during the United Nations Climate Change Conference (COP26), pledging to further reduce carbon emissions in the coming decade (Li et al., 2023b). Short-term changes in China have a positive effect on the country’s medium- and long-term economy. However, these reforms also place significant pressure on existing enterprises to undergo significant transformations. Green innovation refers to the intentional and systematic efforts made by businesses to create and improve new products, processes, and technologies. The goal is to reduce the adverse effects, such as environmental hazards, pollution, and resource depletion, at every stage of a product’s life cycle (Ben Arfi et al., 2018). Green innovation is widely recognized as a crucial driver for facilitating the shift towards environmentally friendly practices in enterprises and enhancing overall environmental sustainability (Obobisa et al., 2022). While the benefits of green innovation are readily apparent, its inherent features of high risk, substantial investment, and prolonged return time frequently render it susceptible to resource constraints (Zhao and Wang, 2022).

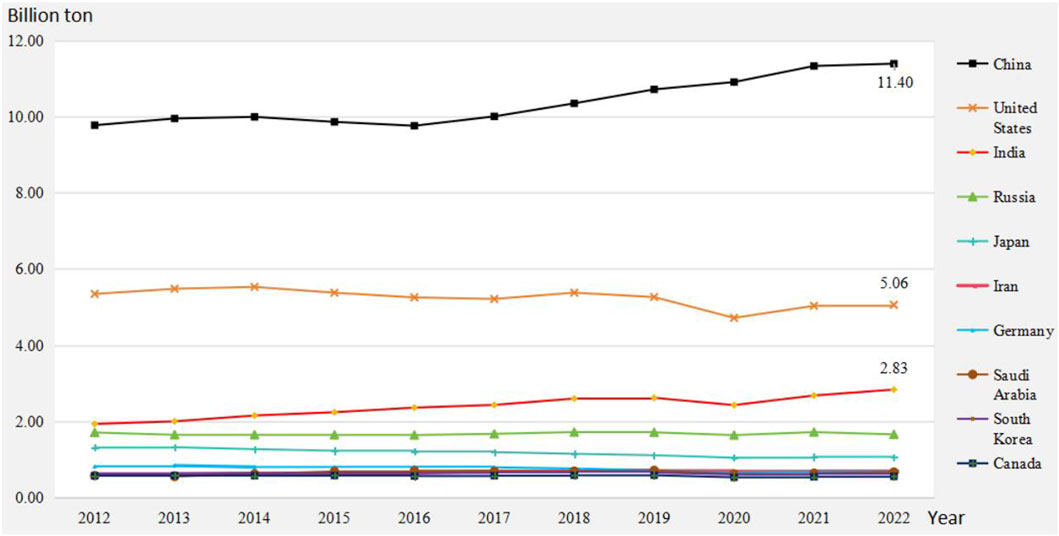

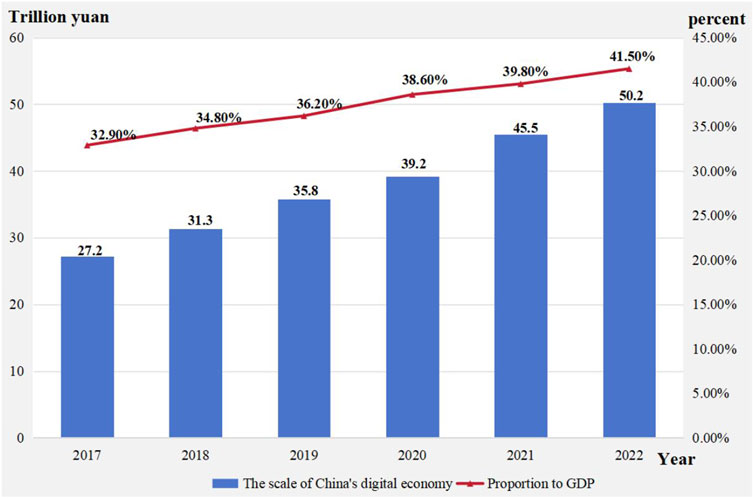

According to figures from the People’s Bank of China, green investment in China reached a total of 2.6 trillion yuan in 2022, accounting for approximately 2%–3% of the country’s gross domestic product (GDP). The government’s contribution accounted for approximately 10%–15% of the total investment, whereas social capital made up around 85%–90%. According to the Green Finance Professional Committee, China must devote a total of 487 trillion yuan towards green development over the next 3 decades in order to meet the “dual carbon” goal. According to the current investment ratio, there is a substantial deficit in funding for future development. In 2022, a majority of China’s environmental protection firms witnessed a decrease in their operational income and profits to different degrees, primarily owing to the influence of the economic climate and the pandemic. This circumstance has heightened the wariness of external investors and exacerbated the limitations on resources for environmentally-friendly innovation in firms. Therefore, it is crucial to increase investor interest in investing and enable the flow of social resources into the domain of sustainable development. China’s digital economy, seen in Figures 1, 2, has been steadily developing and reached a scale of 50.2 trillion yuan in 2022, reflecting a year-on-year rise of 10.3%. This is 41.5% of the country’s total GDP. Hence, in this particular context, it is essential to investigate if advanced digital technologies might contribute positively to the sustainable growth of businesses, aiming to strike a balance between economic progress and environmental preservation.

FIGURE 1. Carbon emission data of China in the past decade.

FIGURE 2. The magnitude of China’s digital economy.

Academics have thoroughly examined several methods of improving green innovation, acknowledging its substantial influence on sustainable development. Scholars conducted independent research to validate the influence of management ability, absorptive capacity, and leadership style on the capacity to innovate in green practices, considering the distinctive characteristics of organizations (Chen L. et al., 2023; Sun D. et al., 2023; Guang-lin and Tao, 2023). In addition, some scholars have demonstrated that environmental rules, government support, and economic conditions positively impact the promotion of corporate green innovation from an external environmental standpoint (Peng et al., 2021; Roh et al., 2021; Wang et al., 2022). Although earlier studies have produced significant findings, it is vital to highlight that only a restricted group of academics have established a correlation between digital transformation and green innovation. The main area of concentration for these academics is the reduction of carbon emissions (Yi et al., 2022), enhancement of manufacturing efficiency (Hao et al., 2023), and augmentation of investment (Liu et al., 2023) in research and development. Besides, the untapped advantages of digital transformation in fostering green innovation within organizations have not been thoroughly investigated.

Although there has been notable advancement in the examination of strategies that increase green innovation in companies, there are still unresolved concerns that require attention. Initially, companies must depend on ample external resources to foster innovation (Xiang et al., 2022). However, existing research on the influence of digital transformation on eco-friendly innovation has overlooked the advantages of digital transformation in facilitating companies’ access to external resources. Meanwhile, there is no consensus on the impact of digital transformation on green innovation in businesses. Although certain studies suggest that digital transformation can enhance sustainable business growth, an alternative perspective posits that it may deplete a company’s operational resources and impede its financial and environmental performance in the near future (Zhong and Ren, 2023). Consequently, it is necessary to elucidate the connection between digital transformation and green innovation in business. Furthermore, certain companies may seek to enhance their reputation by artificially inflating the quantity of green patent applications, thereby creating a facade of environmental friendliness (Han et al., 2024). However, these companies may not genuinely enhance their capacity for green innovation, thereby undermining the reliability of using the number of green patents as the sole indicator of their green innovation capability. Consequently, it is crucial to assess green innovation in a more comprehensive fashion. Finally, there is an increasing trend among financial institutions, external investors, governmental bodies, and other relevant parties to allocate financial resources towards initiatives that support sustainable development (Wan et al., 2022). Hence, more clarification is needed regarding the possible intermediary or regulating mechanisms in such cases.

The resource dependence theory posits that the viability and growth of enterprises hinge on their ability to acquire external resources. This theory is crucial for examining the resource movement between organizations and their external environment (Drees and Heugens, 2013). The stakeholder theory underscores the importance of enterprises taking into account the concerns and interests of all stakeholders during the development process. This theory has gained significant traction and has been extensively studied and applied to assist enterprises in acquiring external resources that yield profits in a competitive business environment (Barney, 2018). The resource dependence theory and stakeholder theory, from a resource perspective, synergistically offer a theoretical framework in this article to examine how digital transformation can facilitate enterprises in obtaining external resources and improving their green innovation capabilities. This study utilizes resource dependence theory and stakeholder theory to conduct regression analysis on the data of Chinese A-share listed businesses from 2012 to 2022, aiming to address the existing research gap. It intends to answer the following research questions: 1) Can digital transformation contribute to the advancement of green innovation in firms, particularly in terms of acquiring external resources? 2) Does the influence of digital transformation on green innovation differ according to the method of measurement? 3) Can we identify novel intermediary or regulatory methods to effectively control the influence of digital transformation on corporate green innovation, based on the viewpoint of this study?

This paper has the following research contributions: first, based on the resource dependence theory and stakeholder theory, this study links digital transformation with corporate green innovation from the perspective of resource acquisition, analyses why and how digital transformation affects corporate green innovation, and helps to supplement and expand the theoretical framework of current research; second, this paper divides corporate green innovation capacity into green innovation quantity and green innovation quality, and discusses the impact of digital transformation on these two dimensions separately, which makes up for the lack of comprehensiveness in the way green innovation capability is measured in traditional research; finally, this paper takes the level of corporate ESG as a potential mediating variable, and incorporates corporate environmental information transparency and government-enterprise relations into this process, which deepens our understanding of the nature of the relationship between digital transformation and green innovation and the boundary conditions. The findings of this study offer insights for managers seeking external resources to foster sustainable company expansion, as well as for regulators crafting legislation to attain the “dual-carbon goal.”

The subsequent portions of this work are structured in the following manner: Section 2 outlines the research hypotheses and theoretical framework. Section 3 provides an overview of the process for selecting and gathering data. Section 4 provides a comprehensive and thorough presentation of the outcomes. Section 5 focuses on discussion and implication. Section 6 is about the conclusion.

According to the resource dependence theory, organizations need to obtain resources for growth from the external environment to ensure their continued existence (Stern et al., 1979). This idea is founded on the assumption that organizations are incapable of attaining self-sufficiency in resources. This highlights the significant impact that obtaining essential external resources has on an organization’s competitive edge. Businesses have multiple challenges in obtaining the external resources necessary for innovation in a fiercely competitive market. Therefore, it is crucial for firms to recognize the advantages of aligning with the preferences of external stakeholders while acquiring external resources (Fleurbaey and Ponthière, 2023). According to the stakeholder hypothesis, the market value of a firm is primarily determined by its ability to fulfill the needs and expectations of stakeholders (Freeman, 2010). The fundamental principle of this theory states that, during the course of development and advancement, a corporation should give priority not just to the interests of shareholders but also make a concerted effort to fully address the needs of all stakeholders. This enables the firm to acquire external resources and strengthen its competitive advantage.

The introduction and utilization of emerging technologies such as big data, cloud computing, and artificial intelligence have significantly influenced the traditional company development model. Researchers have initiated an examination of the impact of digital transformation on aiding organizations in surmounting developmental challenges. Research has substantiated the positive impacts of digital transformation on the performance of relationships (Nasiri et al., 2020), the ability to absorb new knowledge (Zhuo and Chen, 2023), and the promotion of sustainable development in businesses (Yang and Shen, 2023). Simultaneously, certain experts have already discovered that digital transformation appears to have a beneficial impact on aiding businesses in overcoming limitations in resources. In their study, Cui and Wang (2023) discovered that digital transformation has the potential to mitigate operational risks and alleviate financial constraints, hence assisting in the resolution of financial difficulties. Li et al. (2023) verified that digital transformation can mitigate financial constraints and enhance the workforce composition in businesses. According to Wang et al. (2022), digital transformation has a beneficial impact on mitigating financial constraints and mitigating the adverse influence of bank concentration on business innovation. Hence, this article aims to examine the influence of digital transformation on the green innovation of firms from the standpoint of resource acquisition.

The level of green innovation in firms is contingent upon their capacity to efficiently handle and evaluate substantial quantities of information across the entirety of the production process (Barbieri et al., 2020). Digital technology has the ability to augment the internal information processing capability of businesses. Integrating digital technology into the green innovation process can greatly enhance the efficiency of resource utilization both within and outside of organizations (Li et al., 2021). The various avenues via which information is acquired simultaneously result in significant discrepancies in information among stakeholders in companies, hence amplifying investment risks and hindering enterprises from securing external investment (Akerlof, 1995). Digitization can mitigate information asymmetry between firms and external investors and lessen financial constraints by enhancing their abilities to gather, analyze, and communicate information (Kong et al., 2022). Moreover, the notion of digital human capital posits that digital transformation can effectively enhance employee engagement, optimize labor training outcomes, enhance staff proficiency, and have positive impacts on corporate human capital (Campanella et al., 2023). Consequently, this paper presents the following hypothesis:

Hypothesis 1: Digital transformation positively affects firms’ green innovation capabilities.

The inception of the ESG concept can be traced back to 1992, when the United Nations Environment Programme Financial Initiative (UNEP FI) suggested that businesses should comprehensively consider environmental, social responsibility, and corporate governance (ESG) factors when making investment decisions (Cadman, 2012). This suggestion initiated in-depth deliberations on environmental, social, and governance (ESG) issues within organizations. From the perspective of stakeholder theory, companies that prioritize environmental, social, and governance (ESG) factors attract a wider range of investors. This reduces investment risks and greatly enhances the organization’s capacity to obtain external resources for promoting environmentally friendly innovations (Zhai et al., 2022). Research has demonstrated that digital technology can assist businesses in consistently adjusting and adhering to ESG standards during the entire development process (Wang H. et al., 2023). This essay examines the possible function of the corporate Environmental, Social, and Governance (ESG) level as an intermediary between digital transformation and green innovation, drawing on the aforementioned study.

The implementation of digital transformation has the capacity to enhance the environmental, social, and governance (ESG) performance of businesses through multiple avenues. Implementing digital transformation can enhance resource allocation and data analytics skills, enabling organizations to efficiently control pollution emissions, minimize energy usage, and deter opportunistic actions such as environmental infractions and deceptive practices related to environmental, social, and governance (ESG) issues through transparent information sharing (Sun Z. et al., 2023). Consequently, this results in enhanced company environmental performance. Moreover, digital transformation tools can assist companies in cultivating the confidence of stakeholders, broadening their avenues for gathering information, and creating collaborative relationships through the exchange of developmental data. Consequently, this enhances the total social performance of the business (Ang et al., 2022). Ultimately, the utilization of digital technology has a positive impact on the performance of corporate governance as it enables companies to reduce production expenses and enhance their financial performance (Wang Y. et al., 2023). It is important to mention that ESG levels can, to some extent, serve as an indication of a company’s financial performance and operational skills. External stakeholders are increasingly viewing them as a crucial determinant for evaluating a company’s operational capabilities, forecasting future profitability, and evaluating credit risk (Chen S. et al., 2023). Enterprises with high environmental, social, and governance (ESG) standards are more likely to attract investor interest, allowing external capital to be injected into the enterprise’s development process. Accordingly, this paper puts forward the following hypothesis:

Hypothesis 2: Digital transformation facilitates corporate green innovation by improving corporate ESG levels.

We agree with Schnackenberg and Tomlinson (2016) that transparency is essential for establishing trust in organizations. From this standpoint, the market value of a firm is contingent upon the perception it cultivates among external stakeholders through the utilization of information transparency (BALAKRISHNAN et al., 2014). Environmental information transparency pertains to the extent to which a company willingly discloses its environmental data. This showcases the company’s efforts in the field of environmental sustainability (Li et al., 2022b). With the growing focus of the public on sustainable development, companies are realizing that environmental responsibility is essential for improving their intrinsic worth and acquiring resources. Companies with a strong degree of information openness can efficiently utilize digital technologies to convey eco-friendly information. This enables them to showcase their dedication to environmental preservation, cultivate a favorable corporate reputation, mitigate disparities in information, foster confidence with external parties, and facilitate the acquisition of external resources for the firm (Courtney et al., 2017). This paper puts forward the following hypothesis:

Hypothesis 3: Corporate environmental transparency positively moderates the impact of digital transformation on green innovation.

Green innovation is undeniably influenced by its external policy environment. The government, acting as both a market regulator and a significant external stakeholder in enterprises, can promote enterprise green innovation through encouragement and regulation. Stronger government relationships facilitate enterprises in obtaining policy support and inclination. This leads to enhanced information sharing and collaborative innovation between the government and enterprises. Consequently, enterprises can share innovation risks and strengthen the impact of digital transformation on their innovation capabilities (Luo et al., 2023). Moreover, Porter’s hypothesis posits that a specific level of environmental control can stimulate the advancement of technology within companies (Li B. et al., 2022). Research has demonstrated that implementing more stringent government regulations can bolster the capacity for digital transformation and mitigate the influence of regional disparities on enterprises’ resource limitations (Li et al., 2022c). Hence, this paper puts forward the following hypothesis:

Hypothesis 4: Government-Business Relationships Positively Regulate the Impact of Digital Transformation on Green Innovation.

From a resource acquisition standpoint, companies may possess some of the requisite resources for innovation, but the absence of crucial resources might impede the innovation process. Typically, external stakeholders, such as investors, government organizations, and customers, are responsible for managing these vital resources. Acquiring green innovation resources for enterprises can be viewed as a means to meet stakeholder demands and facilitate the influx of external resources for firm expansion. Stakeholders have shown a growing inclination to allocate their resources towards sustainable development in recent years (Zhang and Zhu, 2019). This creates an opportunity for companies to utilize digital technology tools to disseminate their environmentally friendly development information and acquire innovative resources. Previous studies have verified that digital transformation helps businesses foster amicable relationships with external stakeholders, facilitating connections and collaboration between enterprises and external stakeholders, and the positive influence of external stakeholder pressure on environmentally conscious innovation in enterprises (Li et al., 2021; Singh et al., 2022). This study investigates the potential influence of digital transformation on environmentally friendly innovation in companies by integrating resource dependence theory with stakeholder theory.

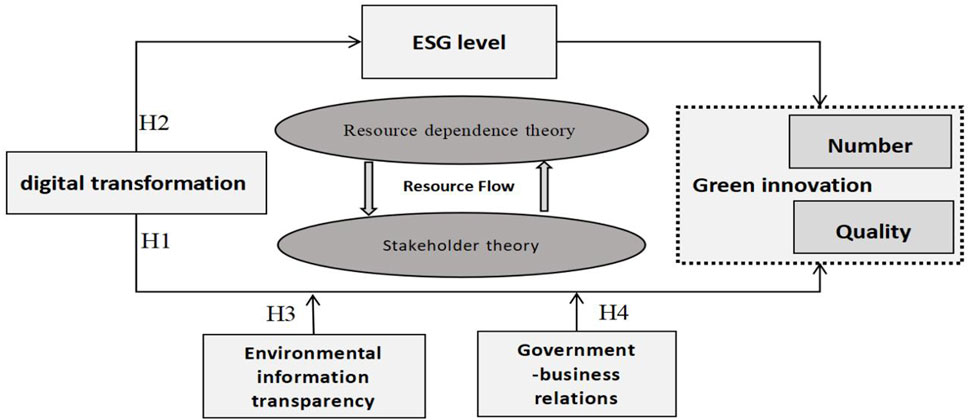

The study framework depicted in Figure 3 illustrates the correlation between the digital transformation of organizations and their capacity for green innovation. This framework is constructed around the four hypotheses put forward in this scholarly article. Digital transformation has the potential to impact the green innovation capabilities of enterprises in terms of both the quantity and quality of green innovation (H1). The level of environmental, social, and governance (ESG) within enterprises acts as a mediator in this process (H2). Moreover, the transparency of environmental information within enterprises (H3) and the character of the relationship between the government and enterprises (H4) play a moderating role in this process.

FIGURE 3. Conceptual framework.

The issuance of the Green Credit Guidelines by the China Banking Regulatory Commission in 2012 heightened government support for green projects, improving the driving force of green innovation in enterprises (Tan et al., 2022). Consequently, considering the availability of data, we will use Chinese A-share listed companies from 2012 to 2022 as the research sample for analysis. In order to minimize the potential influence of extreme values, the initial samples undergo the following processing steps: First and foremost, it is advised to eliminate all samples that come from the financial industry. Furthermore, it is necessary to exclude samples that display financial irregularities, such as a sequential loss (ST) classification or a suspended listing (PT) classification. Furthermore, it is imperative to remove samples that have missing values for crucial variables. Finally, samples with values recorded before 2012 should be excluded from the dataset. To minimize the effect of extreme values, we apply winsorization to all numerical variables at the 1% and 99% percentiles. Upon the conclusion of the processing, a grand total of 28,448 annual observation reports were acquired for 4,409 listed enterprises.

This article utilizes several data sources to support the research perspective. The China Economic and Financial Research Database (CSMAR) delivers financial data and environmental information disclosure data for listed firms. Additionally, the China Research Database (CNRDS) provides information on the digital transformation of enterprises and green patents. Furthermore, the Huazheng ESG rating data is utilized to determine the ESG level of companies.

The explanatory variable examined in this study is enterprise green innovation. Many previous studies have categorized corporate green innovation into various forms, including green process innovation and green product innovation. However, green patents are widely regarded as the most prevalent and acknowledged indicator of green innovation, primarily because Chinese companies face challenges in obtaining green product labels (Brunnermeier and Cohen, 2003). In order to overcome the lack of accuracy in previous studies when measuring the capability of enterprise green innovation, the concept of green innovation capability is divided into two dimensions: green innovation number (GIN) and green innovation quality (GIQ), which include both quantitative and qualitative aspects. Studies have indicated that a company’s level of green innovation can be evaluated by counting the number of green patent applications, and the number of green patent citations can be used to gauge the quality of a green invention (Xu R. et al., 2023). As a result, this paper measures the volume and caliber of green innovation in businesses using this methodology.

The inclusion of keywords in a company’s annual reports can serve as an indicator of the company’s strategic attributes and future prospects. This practice can effectively reveal the company’s corporate philosophy and trajectory of growth (Guo et al., 2023). Prior research has presented ample data to demonstrate the viability of utilizing the frequency of digital transformation keywords as a metric for assessing digital transformation via text analysis (Zhou and Li, 2023). Thus, based on previous studies, we initially compiled the research findings and important terms related to the digital economy. Subsequently, we created a comprehensive dictionary of keywords pertaining to digital transformation. Furthermore, we acquired the frequency of digital transformation terms by doing text analysis on significant phrases and keywords found in the annual reports of publicly traded corporations. Subsequently, we applied the natural logarithm to this data in order to assess the level of digital transformation within these enterprises.

The Huazheng ESG Ratings have garnered substantial recognition for evaluating environmental, social, and governance (ESG) issues in the Chinese market. This grading system has been devised by integrating knowledge from current ESG frameworks in international jurisdictions and customizing it to suit the distinctive attributes of the Chinese market (Lu et al., 2023). The Huazheng ESG rating system is particularly notable for its robust alignment with the Chinese market, comprehensive coverage, and prompt evaluation capabilities. The study employed a hierarchical three-tier rating system, encompassing ratings that spanned from low to high. The ratings are denoted by the letters C, CC, AAA, and so forth. A company’s ESG level is determined by assigning a numerical value ranging from 1 to 9, which corresponds to its ESG grade. This article employs the rating method developed by Xu et al. (2023) to assess the ESG level of organizations.

Transparency of environmental information. Environmental disclosure information is a vital element for stakeholders to evaluate the degree to which a firm meets its environmental obligations. It functions as a gauge of the endeavors undertaken by corporations in the realm of environmental conservation (Su et al., 2022). Thus, this study utilizes the quality of corporate environmental information disclosure as a measure to assess the transparency of said information. A higher value on this indicator indicates a higher degree of transparency in the disclosure of corporate environmental information. This report employs existing research to construct an assessment system for evaluating the caliber of enterprise environmental information disclosure (Zhang et al., 2022). The system consists of thirty indicators that are divided into five aspects: environmental information disclosure, environmental management disclosure, environmental certification disclosure, environmental liability disclosure, and environmental governance disclosure. Utilizing the scoring methodology developed by Yang et al. (2023), the system categorizes enterprise environmental disclosure information into two distinct types: monetized information and non-monetized information. Monetized information is categorized based on disclosure levels. Non-disclosure is assigned a value of 0, qualitative disclosure is assigned a value of 1, and combined qualitative and quantitative disclosure is assigned a value of 2. Within the realm of non-monetary data, disclosure information is assigned a value of 1 point, while any other form of information is assigned a value of 0 points. Afterwards, the evaluation index system is utilized to combine and apply a logarithmic transformation to the scores allocated to each evaluation index, leading to the determination of corporate environmental information transparency (Eidq).

Relations between the government and businesses. Zhang et al. (2023) contend that the degree of government subsidies received by enterprises can serve as an effective gauge of the level of closeness between the government and such enterprises, hence indicating the strength of government-enterprise interactions. Thus, this article employs standardized government subsidies as a metric to assess government-business ties, with higher values indicating stronger relationships between the enterprise and the government.

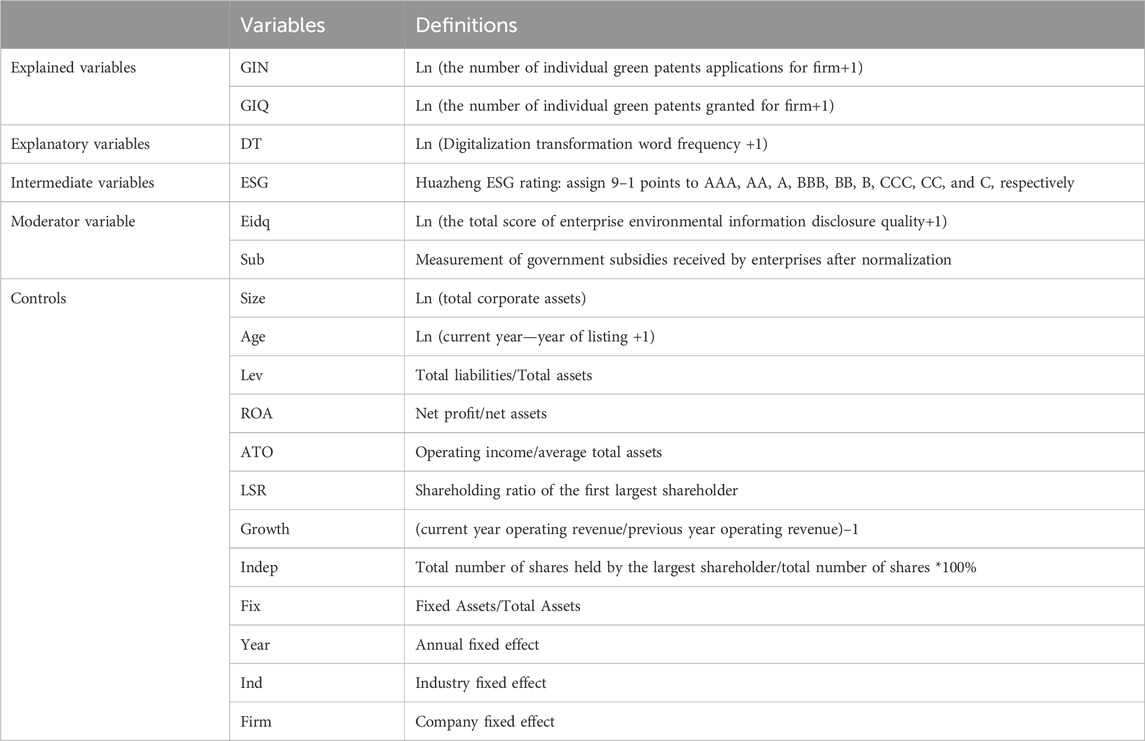

To ensure accuracy, it is important to manage the corporate characteristic elements that could potentially influence green innovation, as indicated by prior research (Lin and Ma, 2022). The control variables in this study encompass firm size (Size) and firm age (Age) (Xu A. et al., 2023). Financial considerations are further considered by controlling for variables such as the gearing ratio (Lev), return on assets (ROA), total asset turnover (ATO), and fixed assets (Fix) (Tan and Zhu, 2022). In addition, factors such as equity concentration (LSR), firm growth (Growth), and the number of independent directors (Index), among others, are taken into account (Xu et al., 2021; Shaheen and Luo, 2023). The model incorporates individual fixed effects (Firm), industry fixed effects (Ind), and time fixed effects (Year). Table 1 presents the definitions and descriptions of individual variables.

TABLE 1. Variables and explanations.

The article used a limited set of data over a short period of time for the study and applied a fixed effects model for regression analysis. To limit the impact of unobservable factors on the association between digital transformation and green innovation skills, we can incorporate year-fixed effects, industry-fixed effects, and firm-fixed effects into this model (Zhang and Chen, 2023). This methodology enables us to precisely quantify the significant correlation between the independent variable, digital transformation, and the dependent variable, green innovation capabilities. Based on the previous analysis and definitions of variables, we will utilize model (Eq. 1) to investigate Hypothesis 1.

Eq. 1 introduces the dependent variable

To examine the role of ESG as a mediator between digital transformation and corporate green innovation in hypothesis H2, we will draw upon the research conducted by Baron and Kenny (1986). A mediating effect model is developed based on model (Eq. 1) using the step-by-step procedure, as illustrated below: Model (Eq. 2) demonstrates the correlation between the level of ESG and digital transformation, while Model (Eq. 3) shows that, when controlling for digital transformation, the impact of ESG on green innovation can be determined by the significance of

Where

To examine the moderating impacts of corporate environmental information transparency and government-enterprise relations on H3 and H4, two additional models Eqs 4, 5 were constructed based on the fundamental regression model (Eq. 1), as described in Hao et al. (2023) research.

Let e

As the aforementioned analysis suggests, this study uses the fixed effect model to investigate the relationship between corporate green innovation and digital transformation. Firstly, this study establishes the usability of the research data by performing Fisher’s unit root test and VIF test. It then proceeds to verify the association between digital transformation and corporate green innovation through regression analysis. A mediation test model is created to verify the hypothesis that the ESG level of enterprises may act as a mediator in the process, using the basic regression model as a basis. Furthermore, the examination of previous research indicates that the transparency of corporate environmental information and the relationship between government and enterprises may also exert influence. Therefore, a moderating effect model is constructed to assess this impact, building upon the foundation of the basic regression model. Ultimately, this study is carried out by substituting the central variables, doing tests for endogeneity, and performing placebo tests to confirm the reliability and strength of the results presented in this research.

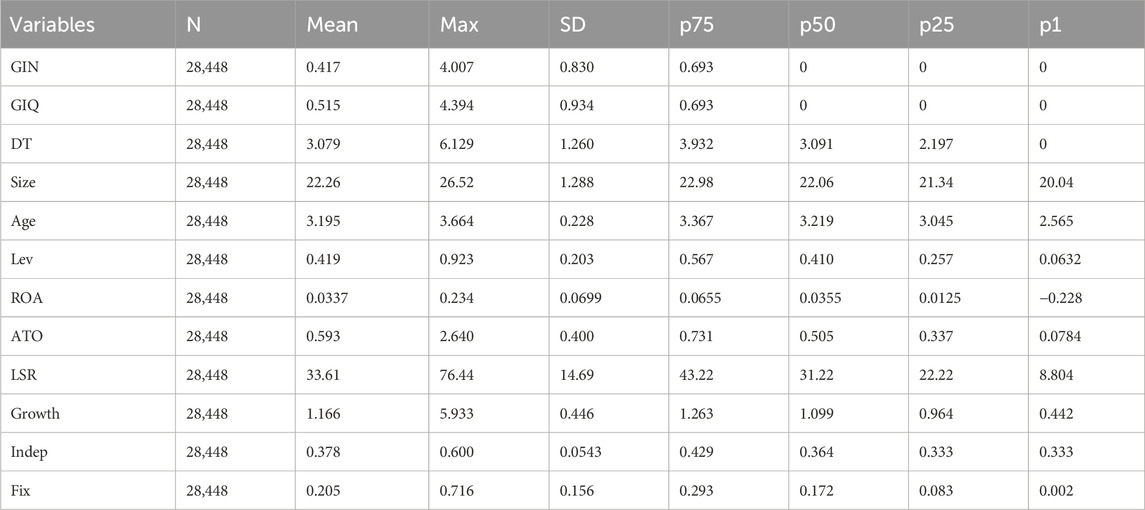

The descriptive statistical findings for the major variables are presented in Table 2. The sample of listed enterprises was analyzed, and it was found that the highest values for both the quantity and quality of green innovation were 4.007 and 4.394, respectively. Simultaneously, the minimum observed values were 0, with the median value similarly being 0. The standard deviations for the two variables are 0.830 and 0.934, respectively. By the end of 2022, only a small number of organizations will have adopted green innovation, and there will be significant differences in the scale and quality of these projects across different firms. Nevertheless, an examination of the digitalization of businesses indicates that the lower quartile of the listed companies in the sample is 2.197, indicating that most organizations have commenced the process of digital transformation. However, the computed average of 3.079 is accompanied by a standard deviation of 1.260. This indicates that there are significant differences in the extent of digital transformation among different publicly listed firms, highlighting substantial hierarchical inequities.

TABLE 2. Descriptive statistics.

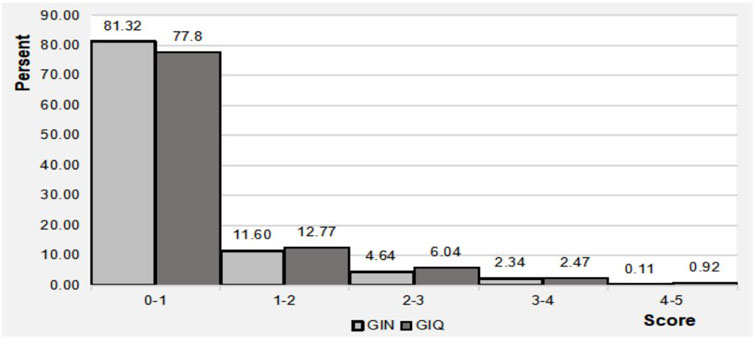

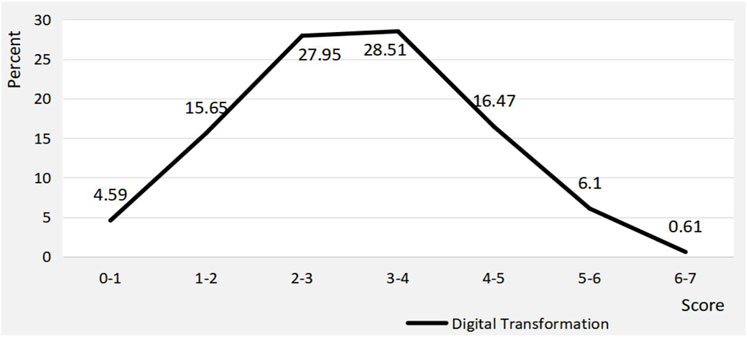

Figure 4 illustrates the descriptive distribution of firms’ green innovation capability, while Figure 5 shows the descriptive distribution of their digital transformation scores. Figure 4 reveals that a limited number of enterprises have engaged in green innovation activities. The majority of these enterprises possess a green innovation capability, measured in terms of quality or quantity of innovation, that falls within the range of 0–1 points (GIN = 81.32%; GIQ = 77.80%) and 1–2 points (GIN = 11.6%; GIQ = 12.77%). This indicates that the current green innovation capability of Chinese enterprises is deficient and requires further enhancement in the future. Figure 5 shows that nearly all listed companies in China are participating in the digital transformation process. The majority of these companies have digital transformation scores ranging from 2 to 3 (27.95%) to 3–4 (28.51%), with the highest score being 6.129. This suggests that most listed companies in China are currently undergoing digital transformation and have already made some progress. These findings align with the descriptive statistics presented in Table 2.

FIGURE 4. Green innovation score distribution.

FIGURE 5. Digital transformation score distribution.

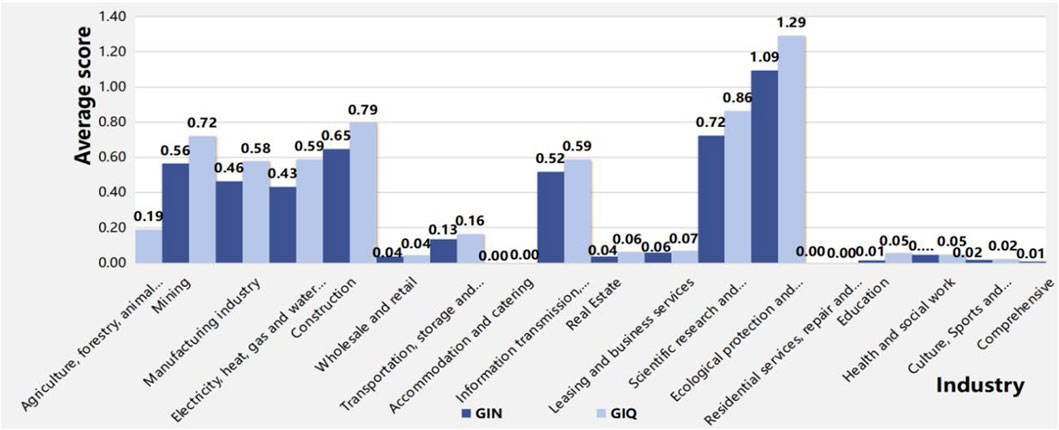

Figure 6 depicts the extent of green innovation capability across several industries. The industry of ecological protection and environmental governance has achieved remarkable success in terms of both the quality and quantity of green innovation. This sector is committed to the preservation of the environment and the management of ecological resources, in accordance with the fundamental tenets of sustainable innovation. Another area worth considering is the field of scientific research and technological services. This industry is dedicated to creating value for organizations through the utilization of scientific knowledge and technological breakthroughs. Green innovation, a type of technological advancement, has garnered significant interest within this sector. Industries with substantial environmental footprints, such as building, mining, manufacturing, and others, have achieved varying levels of high rankings in terms of their need for urgent green innovation. In addition, sectors such as social services, hotel, and food demonstrate a limited ability to engage in environmentally friendly innovation. This is likely because policy attention largely focuses on firms that are directly engaged in and have a substantial impact on green development. As a result, there is a lack of motivation to encourage green innovation in other industries.

FIGURE 6. Average green innovation score distribution by industry.

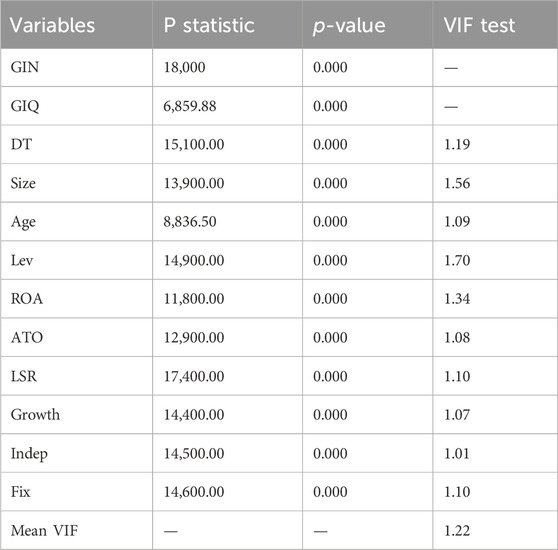

In order to prevent the development of pseudo-regression and maintain the accuracy of the regression results, this study first evaluates the reliability of the sample data. The current study utilizes unbalanced panel data and conducts Fisher’s unit root test to evaluate the stationarity of the sample data. Based on the data shown in Table 3, the statistical values related to the main variables offer enough evidence to reject the first hypothesis suggesting the existence of a unit root across panels. The p-values of 0.000 for all variables indicate that the sample data studied in this study do not display a unit root and can be deemed stable. In addition, the mean variance inflation factor (VIF) in this study is 1.22, which is lower than the threshold of 3. This indicates that there is no multicollinearity present among the variables.

TABLE 3. Data stationarity test.

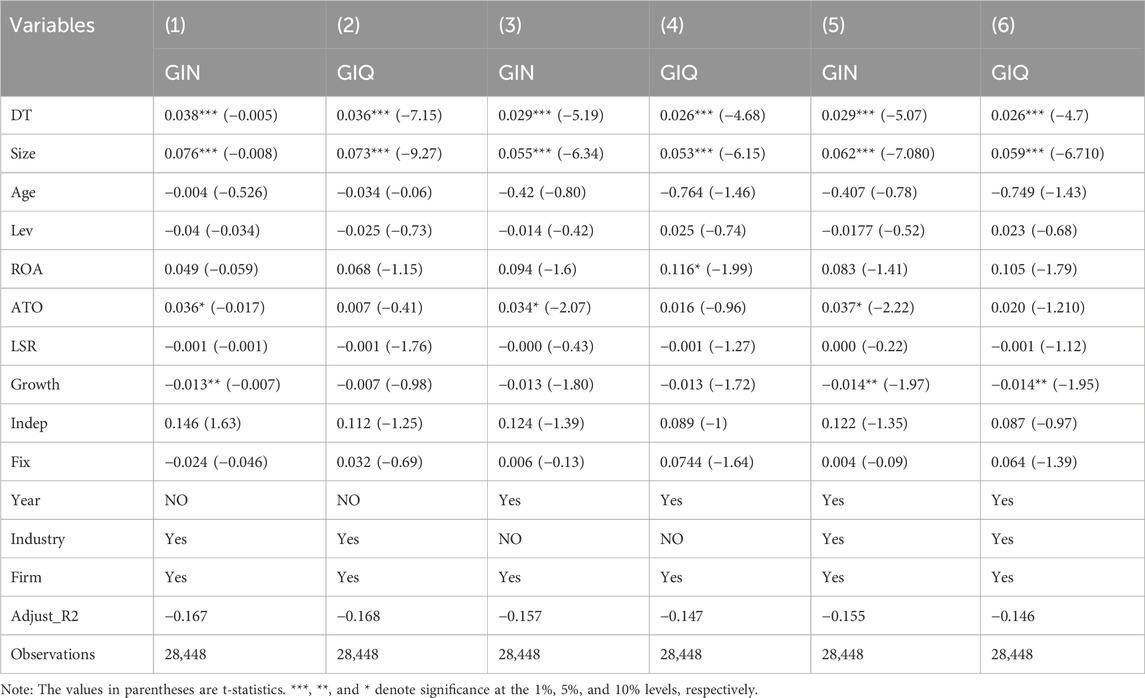

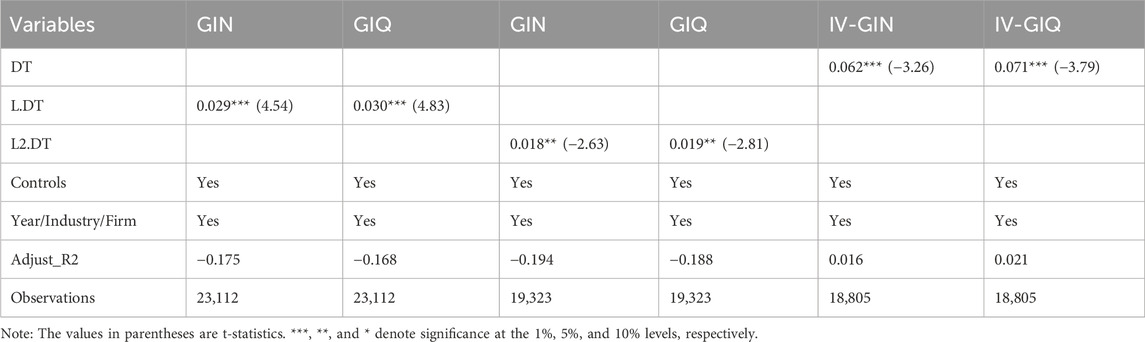

The regression results presented in Table 4 demonstrate the impact of digital transformation on the quality and quantity of green innovation capabilities. Specifically, when controlling for industry and firm factors, it is observed that digital transformation has a positive and statistically significant effect on both the quality and quantity of green innovation capabilities at the 1% level in columns (1) and (2). Similarly, when controlling for year and firm factors, columns (3) and (4) reveal that digital transformation significantly and positively influences both the quantity and quality of green innovations at the 1% level. Furthermore, when considering the combined effects of year, industry, and firm factors, columns (5) and (6) indicate that the digital transformation of firms continues to have a significant and positive impact on both the quantity (

TABLE 4. Baseline regression results.

Subsequently, we investigated the role of firms’ ESG levels as a mediator and assessed the existence of a “digital transformation-ESG level-green innovation” pathway. The data displayed in Table 5 depicts the regression analysis carried out to investigate the mediating influence of enterprise ESG level on the connection between digital transformation and green innovation capability. The regression coefficient (

TABLE 5. Regression results for mediating mechanisms.

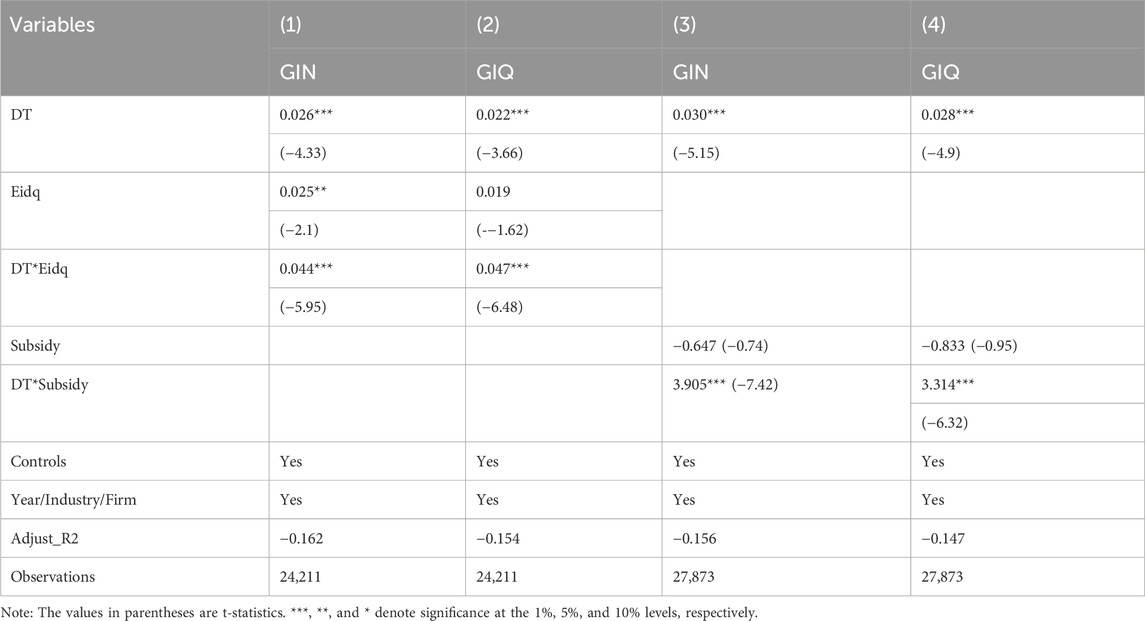

The regression results, presented in columns (1)–(2) of Table 6, demonstrate that the coefficients of the interaction term (DT*Eidq) between digital transformation of enterprises and environmental information transparency have a significant positive impact on both the quantity and quality of green innovations. Specifically, the coefficients are found to be 0.044 and 0.047, respectively, and are statistically significant at the 1% level. These findings suggest that the positive influence of digital transformation on firms’ green innovation capability is more pronounced in firms that exhibit a higher quality of environmental information disclosure. As a result, Hypothesis 3 is confirmed.

TABLE 6. Regression results for moderating effects.

The regression results presented in columns (3)–(4) of Table 6 indicate that the regression coefficients of the interaction term (DT*Sub) between the enterprise’s digital transformation and the government relationship have significant positive effects on both the quantity and quality of green innovation. Specifically, the coefficient for the quantity of green innovation is 3.905, while the coefficient for the quality of green innovation is 3.314. These coefficients are statistically significant at the 1% level. These findings suggest that the relationship between the government and the enterprise plays a positive moderating role in the impact of digital transformation on green innovation. This supports Hypothesis 4.

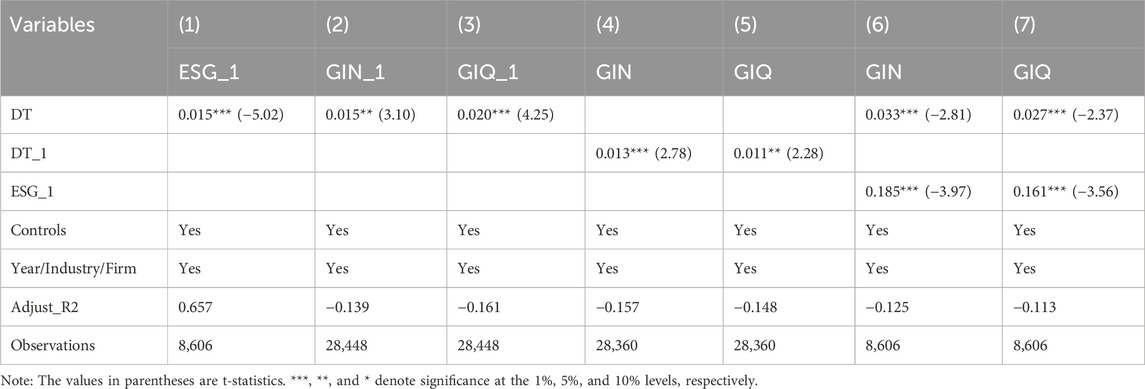

During the robustness test phase, the quantification of green innovation (GIN_1) is established by tallying the quantity of green patents that have been awarded to companies, The assessment of the quality of green innovation (GIQ_1) is based on the quantity of green invention patents, as assessed by Lin and Ma (2022) study. Furthermore, several studies indicate that the Executive Discussion and Analysis (MD&A) section of a company’s annual report is the predominant section that provides the most precise depiction of a company’s present advancement and future strategies (Fang et al., 2023). Hence, in the phase of robustness testing, this article utilizes this part to assess the extent of digital transformation within organizations. To evaluate the strength of the mediating influence, we utilized a logarithmic transformation on the Bloomberg ESG score, which ranges from 0 to 100 points, to gauge the company’s ESG level, as recommended by Husted and Sousa (2019). This approach was adopted to tackle the previous challenges related to accurately measuring ESG levels. The regression results are presented in Table 7 below. The regression results obtained by replacing the core variables show consistency with the initial base regression, thereby validating the reliability of the regression findings in this study.

TABLE 7. Regression results for replacing core variables.

To mitigate endogeneity concerns stemming from omitted variables and reverse causation, it is important to consider that organizations with greater levels of green innovation may have a stronger inclination to employ digital tools in order to enhance their environmental performance and communicate green information. This work utilizes the research completed by Sun et al. (2023b) and conducts regressions on digital transformation with a lag of one period (L1. DT) and two periods (L2. DT), respectively. The findings suggest that, to some extent addressing the issue of endogeneity, digital transformation can still have a substantial positive impact on both the quantity and quality aspects of business green innovation capabilities. Furthermore, this work utilizes the research completed by Wu et al. (2022a) and adopts the instrumental variable approach (LV-GMM) to evaluate endogeneity. The delay in implementing digital transformation by one period (L1. DT) and two periods (L2. DT) is used as a tool to measure and address the potential influence of endogeneity in digital transformation (DT). The findings showed that the LM statistical value was 984.97, which was statistically significant at the 1% level and passed the instrumental variable non-identification test. The Wald F-value of 632.54 surpassed the 10% criterion of 19.93, indicating that the weak instrumental variable validity test was passed. In addition, the Sargan-Hansen statistical value of 0.233 suggests that there is no evidence to reject the hypothesis that all instrumental factors are exogenous. The outcomes of the three tests provide evidence of the efficacy of the instrumental variables used in this article. After addressing the problem of endogeneity, the results shown in Table 8 are consistent with the benchmark regression findings. Digital transformation may greatly improve both the amount and quality of green innovation in businesses, thereby confirming the effectiveness of the research findings presented in this article.

TABLE 8. Lag test for digital transformation.

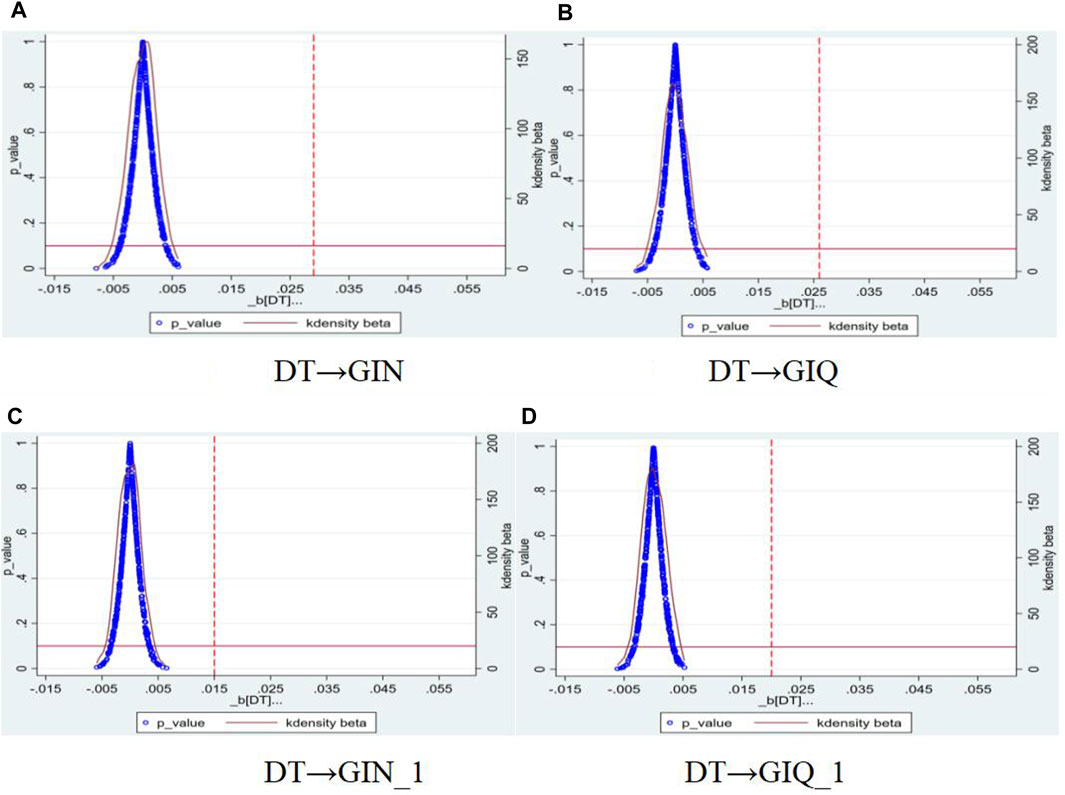

To ensure that the observed effects of enterprise digital transformation on green innovation capacity are not influenced by extraneous factors, this study employs a placebo test, as described by Zhang and Chen (2023). The outcomes of this analysis are presented in Figure 7. Based on the obtained test results, it is evident that the estimated coefficients of the randomly sampled samples exhibit a distribution that closely resembles a normal distribution with a mean of 0. These coefficients are comparatively smaller than the baseline regression coefficients. Furthermore, a majority of the coefficients possess p-values exceeding 0.10, indicating a lack of statistical significance at the 10% level. Hence, the test outcomes effectively eliminate the potential influence of unobservable variables on the relationship between enterprise digital transformation and green innovation capacity, thereby affirming the robustness and credibility of the findings presented in this research.

FIGURE 7. Placebo test. (A) DT→GIN. (B) DT→GIQ. (C) DT→GIN_1. (D) DT→GIQ_1.

This study integrates digital transformation into the research framework of enterprise green innovation. Drawing on resource dependence theory and stakeholder theory, it conducts a comprehensive analysis of the influence of digital transformation on enterprise green innovation. Research has shown that companies that have achieved higher degrees of digital transformation also demonstrate stronger quantities and qualities of green innovation. The research findings validate that digital transformation has a substantial positive impact on green innovation within firms. The findings of this study provide support for Hypothesis 1, aligning with the research undertaken by Liu et al. (2023). Hao et al. (2023) argue that the digital economy hinders technical progress in manufacturing, particularly in relation to the analysis of green total factor productivity decomposition. Nevertheless, this essay emphasizes how digital transformation positively influences organizations’ ability to acquire resources and enhance their green innovation capabilities. The discrepancy can be attributed to differences in research perspectives and industries. Furthermore, our research indicates that digital transformation can indirectly enhance corporate green innovation by improving environmental, social, and governance (ESG) levels. Referring to existing research, this may be due to the positive impact of digital transformation on environmental performance, social performance, and organizational governance, ultimately leading to improved corporate ESG levels. Meanwhile, higher levels of ESG practices have the potential to alleviate financial constraints and increase management’s environmental awareness (Li J. et al., 2023; Yang and Han, 2023). This article investigates the influence of corporate environmental information transparency and government-enterprise relations on the connection between the effects of digital transformation and corporate green innovation. Additionally, the results indicate that the positive impact of digital transformation on firms’ ability to innovate in environmentally friendly ways is stronger in firms that have higher levels of transparency in sharing environmental information. This could be because these organizations are more adept at utilizing digital platforms to promote their green initiatives and attract external resources and support (Ding et al., 2022). Simultaneously, the symbiotic connection between the government and businesses can bolster the influence of digital transformation in augmenting the capacity for green innovation. Utilizing digital tools to establish a positive reputation and facilitate the exchange of information with the government can assist firms in securing policy support and financial subsidies, thereby expediting their green innovation endeavors (Luo et al., 2023).

This work presents three novel contributions to existing theoretical knowledge. Prior research has predominantly concentrated on the advantages of digital transformation for sustainability in China, taking into account the restricted accessibility of green innovation resources and the swift progress of digital developments. The advantages encompass minimizing resource use, strengthening pollution control, and optimizing resource utilization efficiency. Nevertheless, the overlooked advantages of digital transformation in enabling companies to access external resources for long-term growth have been common. Simultaneously, existing research on the impact of digital transformation on firms’ innovation has yielded inconclusive findings. Some studies indicate that digital transformation may have an adverse effect on firms’ financial performance and does not facilitate creativity (Zhong and Ren, 2023). However, these studies struggle to elucidate why certain firms with a greater level of digital transformation possess more abundant innovation resources (Zhou and Li, 2023). This article is based on the theory of resource dependence and stakeholder theory. From the perspective of enterprise resource acquisition, the two theories complement each other, emphasizing the limited innovative resources of enterprises and the role of digital tools in promoting the acquisition of external resources. It demonstrates that digital transformation has a positive impact on improving a company’s ability to innovate in environmentally friendly ways. This finding contributes to the existing research on the factors that influence corporate green innovation and adds to our understanding of how digital transformation affects green innovation.

Furthermore, organizations gain greater legitimacy when their structures and behaviors align with social norms and principles (Suchman, 1995). By adhering to various norms, standards, and values, these organizations are able to meet the expectations of important resource providers, thus alleviating their resource constraints (Fisher et al., 2016). The provision of government subsidies to encourage innovation in businesses has unintentionally resulted in certain entities exploiting green innovation for fraudulent purposes, such as making false claims for subsidies (Zhang et al., 2023). This has given rise to a phenomenon known as “greenwashing” or “green patent bubbles,” which ultimately diminishes the credibility and impact of the number of green patents held by businesses (Xia et al., 2023). Hence, enhancing the accuracy of measuring green innovation is crucial. This research categorizes corporate green innovation into two aspects: the quantity of green innovation and the quality of green innovation. This approach addresses the limitations of the conventional assessment of green innovation and enhances the reliability of the study’s findings.

This report thoroughly examines the underlying mechanisms involved in the influence of digital transformation on corporate green innovation. The idea of information asymmetry posits that the disparity in information between firms and external investors is a significant factor contributing to the challenges faced by enterprises in obtaining external resources (Dye, 2001). The implementation of digital transformation can expedite the dissemination of environmental, social, and governance (ESG) information, thereby significantly enhancing the credibility and authenticity of businesses (Drempetic et al., 2020). Meanwhile, ESG levels are increasingly becoming a crucial factor influencing investor investment decisions. A higher ESG score can enhance investors’ confidence in the company for investment (Jin et al., 2024). Hence, this paper posits the hypothesis that the level of environmental, social, and governance (ESG) factors partially mediates the relationship between digital transformation and green innovation, specifically in terms of resource acquisition. It also establishes the causal pathway of “digital transformation-ESG level-green innovation” and provides empirical evidence to support the validity of this hypothesis. Additional investigation reveals that digital transformation can enhance the internal control of businesses, enhance the level of information disclosure, and assist businesses in establishing a market image (Wu K. et al., 2022). Therefore, this study examines the moderating effects of environmental information transparency and government-enterprise relationships on the influence of digital transformation on businesses’ green innovation. The findings indicate that higher environmental information transparency and a stronger government-enterprise relationship can amplify the positive impact of digital transformation on businesses’ green innovation. This study elucidated the underlying process by which digital transformation affects green innovation in firms, focusing on the acquisition of resources.

The findings of our study establish a theoretical framework that may inform many parties involved in digital transformation, including company executives, governmental entities, regulatory bodies, and consumers. Companies can enhance their green innovation capabilities and achieve dual advantages in terms of environmental and financial performance by actively investing in technologies such as artificial intelligence, information technology, and blockchain. These technologies not only contribute to increased productivity and cost reduction, leading to improved economic performance, but also facilitate the adoption of sustainable practices and environmental stewardship.

Businesses should be strongly encouraged by the government to undergo digital transformation, since this can boost their capacity for green innovation while also increasing production efficiency. In addition, this research demonstrates the favorable regulatory function of government-business partnerships in supporting green innovation in digital transformation. By enacting policies like innovation subsidies or regulatory fines, the government can fortify its relationship with businesses, hasten the process of digital transformation within businesses, and promote green innovation within businesses.

Regulatory bodies should proactively establish a comprehensive repository of corporate environmental data and enhance the accessibility and clarity of such information. According to research findings, the implementation of digital transformation has the potential to facilitate green innovation and enhance the environmental, social, and governance (ESG) performance of enterprises. Consequently, it is advisable for regulatory bodies to include the degree of digital transformation within their oversight purview. This approach would enable the simultaneous achievement of the dual objectives of environmental preservation and economic development.

The increased prevalence of short videos, short messages, and social platforms has effectively fostered enhanced openness in corporate environmental disclosures. As a result, consumers now have the ability to access and comprehend corporate environmental governance measures through such information. Furthermore, the utilization of digital technology tools enables consumers to report and oppose instances of corporate environmental harm, as well as to promote and endorse environmentally responsible practices. Consequently, this fosters increased awareness regarding the importance of sustainable development within corporations, encourages independent green innovation, and helps consumers act as external monitors of corporate behavior.

The study is subject to the following constraints: Firstly, this article solely focuses on the influence of digital transformation on green innovation within enterprises. Indeed, the combined impact of several elements might result in varying outcomes for green innovation during the process of digital transformation. As has been confirmed by scholars, in high-volatility market environments, the higher the degree of digital transformation, the lower the firm’s environmental performance (Li, 2022). Hence, future studies should thoroughly examine the influence of digital transformation on eco-friendly innovation in businesses across various internal and external contexts. Secondly, this article exclusively utilizes text analysis to assess the extent of enterprise digital transformation without taking into account enterprise digital assets. A future study can investigate diverse methodologies for quantifying digital transformation. Finally, the research scope of this article encompasses all industries, with the exception of the finance sector. The influence of digital transformation on green innovation may vary across different industries due to the differing demands for green innovation. Hence, forthcoming research endeavors can engage in focused deliberations pertaining to particular sectors.

Utilizing digital technology tools is essential for promoting environmentally friendly innovation in businesses. This article utilizes a dataset consisting of 4,409 publicly traded companies in China from 2012 to 2022 to investigate the impact of digital transformation on corporations’ capacity to innovate in environmentally sustainable manners. This article also examines whether there are variations in the impact of digital transformation on different types of green innovation. This study also investigates the role of ESG levels in mediating this process, as well as the moderation effect of disclosing corporate environmental information and government enterprise connections. The study found that: 1) Digital transformation has a noteworthy positive influence on the quantity and quality of green innovation capabilities in businesses. 2) The digital transformation of businesses can indirectly enhance their green innovation capabilities by enhancing their environmental, social, and governance (ESG) level, with the ESG level acting as a partial intermediary. 3) The transparency of corporate environmental information and the quality of government enterprise relationships can amplify the positive impact of digital transformation on the green innovation capability of businesses.

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

RZ: Formal Analysis, Writing–original draft. YZ: Supervision, Writing–review and editing. JZ: Supervision, Validation, Writing–review and editing. HX: Funding acquisition, Writing–review and editing.

The author(s) declare financial support was received for the research, authorship, and/or publication of this article. This research is supported by the National Natural Science Foundation of China (Grant nos 72161021 and 72162026), and Applied Basic Project of Yunnan Province (Grant no. 202101AT 070088).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Akerlof, G. (1995). “The market for ‘lemons’: quality uncertainty and the market mechanism,” in Essential readings in economics (London: Macmillan Education UK), 175–188. doi:10.1007/978-1-349-24002-9_9

Ang, R., Shao, Z., Liu, C., Yang, C., and Zheng, Q. (2022). The relationship between CSR and financial performance and the moderating effect of ownership structure: evidence from Chinese heavily polluting listed enterprises. Sustain Prod. Consum. 30, 117–129. doi:10.1016/j.spc.2021.11.030

Balakrishnan, K., Billings, M. B., Kelly, B., and Ljungqvist, A. (2014). Shaping liquidity: on the causal effects of voluntary disclosure. J. Finance 69, 2237–2278. doi:10.1111/jofi.12180

Barbieri, N., Marzucchi, A., and Rizzo, U. (2020). Knowledge sources and impacts on subsequent inventions: do green technologies differ from non-green ones? Res. Policy 49, 103901. doi:10.1016/j.respol.2019.103901

Barney, J. B. (2018). Why resource-based theory’s model of profit appropriation must incorporate a stakeholder perspective. Strategic Manag. J. 39, 3305–3325. doi:10.1002/smj.2949

Baron, R. M., and Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Pers. Soc. Psychol. 51, 1173–1182. doi:10.1037/0022-3514.51.6.1173

Ben Arfi, W., Hikkerova, L., and Sahut, J.-M. (2018). External knowledge sources, green innovation and performance. Technol. Forecast Soc. Change 129, 210–220. doi:10.1016/j.techfore.2017.09.017

Brunnermeier, S. B., and Cohen, M. A. (2003). Determinants of environmental innovation in US manufacturing industries. J. Environ. Econ. Manage 45, 278–293. doi:10.1016/S0095-0696(02)00058-X

Cadman, T. (2012). “The legitimacy of ESG standards as an analytical framework for responsible investment,” in, 35–53. doi:10.1007/978-90-481-9319-6_3

Campanella, F., Serino, L., Battisti, E., Giakoumelou, A., and Karasamani, I. (2023). FinTech in the financial system: towards a capital-intensive and high competence human capital reality?. J. Bus. Res. 155, 113376. doi:10.1016/j.jbusres.2022.113376

Chen, L., Yuan, M., Lin, H., Han, Y., Yu, Y., and Sun, C. (2023a). Organizational improvisation and corporate green innovation: a dynamic capability perspective. Bus. Strategy Environ. 32, 5686–5701. doi:10.1002/bse.3443

Chen, S., Song, Y., and Gao, P. (2023b). Environmental, social, and governance (ESG) performance and financial outcomes: analyzing the impact of ESG on financial performance. J. Environ. Manage 345, 118829. doi:10.1016/j.jenvman.2023.118829

Courtney, C., Dutta, S., and Li, Y. (2017). Resolving information asymmetry: signaling, endorsement, and crowdfunding success. Entrepreneursh. Theory Pract. 41, 265–290. doi:10.1111/etap.12267

Cui, L., and Wang, Y. (2023). Can corporate digital transformation alleviate financial distress? Financ. Res. Lett. 55, 103983. doi:10.1016/j.frl.2023.103983

Ding, X., Appolloni, A., and Shahzad, M. (2022). Environmental administrative penalty, corporate environmental disclosures and the cost of debt. J. Clean. Prod. 332, 129919. doi:10.1016/j.jclepro.2021.129919

Drees, J. M., and Heugens, P. P. M. A. R. (2013). Synthesizing and extending resource dependence theory. J. Manage 39, 1666–1698. doi:10.1177/0149206312471391

Drempetic, S., Klein, C., and Zwergel, B. (2020). The influence of firm size on the ESG score: corporate sustainability ratings under review. J. Bus. Ethics 167, 333–360. doi:10.1007/s10551-019-04164-1

Dye, R. A. (2001). An evaluation of “essays on disclosure” and the disclosure literature in accounting. J. Account. Econ. 32, 181–235. doi:10.1016/S0165-4101(01)00024-6

Fang, M., Nie, H., and Shen, X. (2023). Can enterprise digitization improve ESG performance? Econ. Model. 118, 106101. doi:10.1016/j.econmod.2022.106101

Fisher, S., Kotha, S., and Lahiri, A. (2016). Changing with the times: an integrated view of identity, legitimacy, and new venture life cycles. Acad. Manage Rev. 41, 383–409. doi:10.5465/amr.2013.0496

Fleurbaey, M., and Ponthière, G. (2023). The stakeholder corporation and social welfare. J. Political Econ. 131, 2556–2594. doi:10.1086/724318

Freeman, R. E. (2010). Strategic management. Cambridge University Press. doi:10.1017/CBO9781139192675

Guang-lin, X., and Tao, M. (2023). How can management ability promote green technology innovation of manufacturing enterprises? Evidence from China. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.1051636

Guo, X., Li, M., Wang, Y., and Mardani, A. (2023). Does digital transformation improve the firm’s performance? From the perspective of digitalization paradox and managerial myopia. J. Bus. Res. 163, 113868. doi:10.1016/j.jbusres.2023.113868

Han, M., Lin, H., Sun, D., Wang, J., and Yuan, J. (2024). The eco-friendly side of analyst coverage: the case of green innovation. IEEE Trans. Eng. Manag. 71, 1007–1022. doi:10.1109/TEM.2022.3148136

Hao, X., Wang, X., Wu, H., and Hao, Y. (2023). Path to sustainable development: does digital economy matter in manufacturing green total factor productivity? Sustain. Dev. 31, 360–378. doi:10.1002/sd.2397

Husted, B. W., and Sousa-Filho, J. M. de (2019). Board structure and environmental, social, and governance disclosure in Latin America. J. Bus. Res. 102, 220–227. doi:10.1016/j.jbusres.2018.01.017

Jin, Y., Yan, J., and Yan, Q. (2024). Unraveling ESG ambiguity, price reaction, and trading volume. Financ. Res. Lett. 61, 104972. doi:10.1016/j.frl.2024.104972

Kong, T., Sun, R., Sun, G., and Song, Y. (2022). Effects of digital finance on green innovation considering information asymmetry: an empirical study based on Chinese listed firms. Emerg. Mark. Finance Trade 58, 4399–4411. doi:10.1080/1540496X.2022.2083953

Li, B., Lei, Y., Hu, M., and Li, W. (2022a). The impact of policy orientation on green innovative performance: the role of green innovative capacity and absorptive capacity. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.842133

Li, C., Huo, P., Wang, Z., Zhang, W., Liang, F., and Mardani, A. (2023a). Digitalization generates equality? Enterprises’ digital transformation, financing constraints, and labor share in China. J. Bus. Res. 163, 113924. doi:10.1016/j.jbusres.2023.113924

Li, C. J., Razzaq, A., Irfan, M., and Luqman, A. (2023b). Green innovation, environmental governance and green investment in China: exploring the intrinsic mechanisms under the framework of COP26. Technol. Forecast. Soc. Change 194, 122708. doi:10.1016/j.techfore.2023.122708

Li, G., Xue, Q., and Qin, J. (2022b). Environmental information disclosure and green technology innovation: empirical evidence from China. Technol. Forecast Soc. Change 176, 121453. doi:10.1016/j.techfore.2021.121453

Li, G., Zhang, R., Feng, S., and Wang, Y. (2022c). Digital finance and sustainable development: evidence from environmental inequality in China. Bus. Strategy Environ. 31, 3574–3594. doi:10.1002/bse.3105

Li, H., Wu, Y., Cao, D., and Wang, Y. (2021). Organizational mindfulness towards digital transformation as a prerequisite of information processing capability to achieve market agility. J. Bus. Res. 122, 700–712. doi:10.1016/j.jbusres.2019.10.036

Li, J., Lian, G., and Xu, A. (2023b). How do ESG affect the spillover of green innovation among peer firms? Mechanism discussion and performance study. J. Bus. Res. 158, 113648. doi:10.1016/j.jbusres.2023.113648

Li, L. (2022). Digital transformation and sustainable performance: the moderating role of market turbulence. Ind. Mark. Manag. 104, 28–37. doi:10.1016/j.indmarman.2022.04.007

Lin, B., and Ma, R. (2022). How does digital finance influence green technology innovation in China? Evidence from the financing constraints perspective. J. Environ. Manage 320, 115833. doi:10.1016/j.jenvman.2022.115833

Liu, X., Liu, F., and Ren, X. (2023). Firms’ digitalization in manufacturing and the structure and direction of green innovation. J. Environ. Manage 335, 117525. doi:10.1016/j.jenvman.2023.117525

Lu, Y., Xu, C., Zhu, B., and Sun, Y. (2023). Digitalization transformation and ESG performance: evidence from China. Bus. Strategy Environ. 33, 352–368. doi:10.1002/bse.3494

Luo, Y., Cui, H., Zhong, H., and Wei, C. (2023). Business environment and enterprise digital transformation. Financ. Res. Lett. 57, 104250. doi:10.1016/j.frl.2023.104250

Nasiri, M., Ukko, J., Saunila, M., and Rantala, T. (2020). Managing the digital supply chain: the role of smart technologies. Technovation 96–97, 102121. doi:10.1016/j.technovation.2020.102121

Obobisa, E. S., Chen, H., and Mensah, I. A. (2022). The impact of green technological innovation and institutional quality on CO2 emissions in African countries. Technol. Forecast Soc. Change 180, 121670. doi:10.1016/j.techfore.2022.121670

Peng, H., Shen, N., Ying, H., and Wang, Q. (2021). Can environmental regulation directly promote green innovation behavior?— based on situation of industrial agglomeration. J. Clean Prod. 314, 128044. doi:10.1016/j.jclepro.2021.128044

Roh, T., Lee, K., and Yang, J. Y. (2021). How do intellectual property rights and government support drive a firm’s green innovation? The mediating role of open innovation. J. Clean. Prod. 317, 128422. doi:10.1016/j.jclepro.2021.128422

Schnackenberg, A. K., and Tomlinson, E. C. (2016). Organizational transparency. J. Manage 42, 1784–1810. doi:10.1177/0149206314525202

Shaheen, R., and Luo, Q. (2023). Green innovation and political embeddedness in China’s heavily polluted industry: role of environmental disclosure, gender diversity, and enterprise growth. Environ. Sci. Pollut. Res. 30, 97498–97517. doi:10.1007/s11356-023-29339-2

Singh, S. K., Del Giudice, M., Chiappetta Jabbour, C. J., Latan, H., and Sohal, A. S. (2022). Stakeholder pressure, green innovation, and performance in small and medium-sized enterprises: the role of green dynamic capabilities. Bus. Strategy Environ. 31, 500–514. doi:10.1002/bse.2906

Stern, R. N., Pfeffer, J., and Salancik, G. (1979). The external control of organizations: a resource dependence perspective. Contemp. Sociol. 8, 612. doi:10.2307/2065200

Su, X., Pan, C., Zhou, S., and Zhong, X. (2022). Threshold effect of green credit on firms’ green technology innovation: is environmental information disclosure important? J. Clean. Prod. 380, 134945. doi:10.1016/j.jclepro.2022.134945

Sun, D., Zeng, S., Lin, H., Yu, M., and Wang, L. (2023a). Is green the virtue of humility? The influence of humble CEOs on corporate green innovation in China. IEEE Trans. Eng. Manag. 70, 4222–4232. doi:10.1109/TEM.2021.3106952

Suchman, M. C. (1995). Managing legitimacy: strategic and institutional approaches. Acad. Manage Rev. 20, 571. doi:10.2307/258788

Sun, Z., Sun, X., Wang, W., and Wang, W. (2023b). Digital transformation and greenwashing in environmental, social, and governance disclosure: does investor attention matter? Bus. Ethics, Environ. Responsib. doi:10.1111/beer.12585

Tan, X., Yan, Y., and Dong, Y. (2022). Peer effect in green credit induced green innovation: an empirical study from China’s Green Credit Guidelines. Resour. Policy 76, 102619. doi:10.1016/j.resourpol.2022.102619

Tan, Y., and Zhu, Z. (2022). The effect of ESG rating events on corporate green innovation in China: the mediating role of financial constraints and managers’ environmental awareness. Technol. Soc. 68, 101906. doi:10.1016/j.techsoc.2022.101906

Wan, X., Wang, Y., Qiu, L., Zhang, K., and Zuo, J. (2022). Executive green investment vision, stakeholders’ green innovation concerns and enterprise green innovation performance. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.997865

Wang, C., Chen, P., Hao, Y., and Dagestani, A. A. (2022). Tax incentives and green innovation—the mediating role of financing constraints and the moderating role of subsidies. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.1067534

Wang, H., Jiao, S., Bu, K., Wang, Y., and Wang, Y. (2023). Digital transformation and manufacturing companies’ ESG responsibility performance. Financ. Res. Lett. 58, 104370. doi:10.1016/j.frl.2023.104370

Wang, Q., and Du, Z.-Y. (2022). Changing the impact of banking concentration on corporate innovation: the moderating effect of digital transformation. Technol. Soc. 71, 102124. doi:10.1016/j.techsoc.2022.102124

Wang, Y., Jiang, Z., Li, X., Chen, Y., Cui, X., and Wang, S. (2023). Research on antecedent configurations of enterprise digital transformation and enterprise performance from the perspective of dynamic capability. Financ. Res. Lett. 57, 104170. doi:10.1016/j.frl.2023.104170

Wu, G., Xu, Q., Niu, X., and Tao, L. (2022a). How does government policy improve green technology innovation: an empirical study in China. Front. Environ. Sci. 9. doi:10.3389/fenvs.2021.799794

Wu, K., Fu, Y., and Kong, D. (2022b). Does the digital transformation of enterprises affect stock price crash risk? Financ. Res. Lett. 48, 102888. doi:10.1016/j.frl.2022.102888

Xia, F., Chen, J., Yang, X., Li, X., and Zhang, B. (2023). Financial constraints and corporate greenwashing strategies in China. Corp. Soc. Responsib. Environ. Manag. 30, 1770–1781. doi:10.1002/csr.2453

Xiang, X., Liu, C., and Yang, M. (2022). Who is financing corporate green innovation? Int. Rev. Econ. Finance 78, 321–337. doi:10.1016/j.iref.2021.12.011

Xu, A., Zhu, Y., and Wang, W. (2023a). Micro green technology innovation effects of green finance pilot policy—from the perspectives of action points and green value. J. Bus. Res. 159, 113724. doi:10.1016/j.jbusres.2023.113724

Xu, J., Yu, Y., Zhang, M., and Zhang, J. Z. (2023b). Impacts of digital transformation on eco-innovation and sustainable performance: evidence from Chinese manufacturing companies. J. Clean. Prod. 393, 136278. doi:10.1016/j.jclepro.2023.136278

Xu, Q., Lu, Y., Lin, H., and Li, B. (2021). Does corporate environmental responsibility (CER) affect corporate financial performance? Evidence from the global public construction firms. J. Clean. Prod. 315, 128131. doi:10.1016/j.jclepro.2021.128131

Xu, R., Yao, D., and Zhou, M. (2023c). Does the development of digital inclusive finance improve the enthusiasm and quality of corporate green technology innovation? J. Innovation Knowl. 8, 100382. doi:10.1016/j.jik.2023.100382

Yang, Y., and Han, J. (2023). Digital transformation, financing constraints, and corporate environmental, social, and governance performance. Corp. Soc. Responsib. Environ. Manag. 30, 3189–3202. doi:10.1002/csr.2546

Yang, Z., and Shen, Y. (2023). The impact of intelligent manufacturing on industrial green total factor productivity and its multiple mechanisms. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.1058664

Yang, J., Shi, Y., Zhang, L., and Hu, S. (2023). The influence of environmental information transparency of green bond on credit rating. Finance Res. Lett. 58, 104410. doi:10.1016/j.frl.2023.104410

Zhai, Y., Cai, Z., Lin, H., Yuan, M., Mao, Y., and Yu, M. (2022). Does better environmental, social, and governance induce better corporate green innovation: the mediating role of financing constraints. Corp. Soc. Responsib. Environ. Manag. 29, 1513–1526. doi:10.1002/csr.2288

Zhang, C., and Chen, D. (2023). Do environmental, social, and governance scores improve green innovation? Empirical evidence from Chinese-listed companies. PLoS One 18, e0279220. doi:10.1371/journal.pone.0279220

Yi, M., Liu, Y., Sheng, M. S., and Wen, L. (2022). Effects of digital economy on carbon emission reduction: New evidence from China. Energy Policy 171, 113271. doi:10.1016/j.enpol.2022.113271

Zhang, F., and Zhu, L. (2019). Enhancing corporate sustainable development: stakeholder pressures, organizational learning, and green innovation. Bus. Strategy Environ. 28, 1012–1026. doi:10.1002/bse.2298

Zhang, S., Zhang, M., Qiao, Y., Li, X., and Li, S. (2022). Does improvement of environmental information transparency boost firms’ green innovation? Evidence from the air quality monitoring and disclosure program in China. J. Clean. Prod. 357, 131921. doi:10.1016/j.jclepro.2022.131921

Zhang, W., Qin, C., and Zhang, W. (2023). Top management team characteristics, technological innovation and firm’s greenwashing: evidence from China’s heavy-polluting industries. Technol. Forecast Soc. Change 191, 122522. doi:10.1016/j.techfore.2023.122522

Zhao, L., and Wang, Y. (2022). Financial ecological environment, financing constraints, and green innovation of manufacturing enterprises: empirical evidence from China. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.891830

Zhong, X., and Ren, G. (2023). Independent and joint effects of CSR and CSI on the effectiveness of digital transformation for transition economy firms. J. Bus. Res. 156, 113478. doi:10.1016/j.jbusres.2022.113478

Zhou, M., Govindan, K., Xie, X., and Yan, L. (2021). How to drive green innovation in China’s mining enterprises? Under the perspective of environmental legitimacy and green absorptive capacity. Resour. Policy 72, 102038. doi:10.1016/j.resourpol.2021.102038

Zhou, Z., and Li, Z. (2023). Corporate digital transformation and trade credit financing. J. Bus. Res. 160, 113793. doi:10.1016/j.jbusres.2023.113793

Keywords: digital transformation, green innovation, ESG, information transparency, sustainable development

Citation: Zhuo R, Zhang Y, Zheng J and Xie H (2024) Digitalization transformation and enterprise green innovation: empirical evidence from Chinese listed companies. Front. Environ. Sci. 12:1361576. doi: 10.3389/fenvs.2024.1361576

Received: 26 December 2023; Accepted: 20 February 2024;

Published: 05 March 2024.

Edited by:

Rongrong Li, China University of Petroleum (East China), ChinaReviewed by: