Vojtech Bocok

Vojtech Bocok Josef Abrham

Josef Abrham

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 14 September 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1272816

This article is part of the Research Topic Changes in the Approach to Energy Concerns and their Impact on the Economy and the Environment View all 6 articles

Goals: The paper aims to analyze the current development in the field of circular economy relating to the use of lease financing as possible environemental management’s tool.

Methods: The paper contains own research conducted on companies trading on the Prague Stock Exchange from 1993 to 2019, in which the influence of lease financing on market values of companies representing investor confidence and profitability ratios are examined. The research uses a regression model of panel data.

Results: The research confirms the fact that companies using leases are able to maintain investor confidence better. There has been an increase in their market value. It has been proved that lease financing does not harm the economic performance of companies and that, on the contrary, it is a possible way of financing companies, which would be more in line with sustainable development.

Conclusion: The presented article extended further quantitative research in the field of sustainability, circular economy, environmental management and the position of leasing as one of the possible instruments of these policies. It has been confirmed that the use of leases increases the value of Tobin’s Q. However, there has been a decrease in investor confidence expressed by the negative correlation of Tobin’s Q when comparing with the situation where the company invests in increasing its tangible assets in the standard way.

Leases can assist in the functioning of circular economy, i.e., an economy with a cycle of resources, which slows down resource flows or increases the productivity of resource use and thus help the application of environmental management principles. As the issue of circular economy is an extraordinarily complex topic, the authors want to contribute to it just by incorporating leases. To do this, however, it is first necessary to determine whether, or, more precisely under what circumstances the previous studies consider leases to be a means of circular economy, and then it is appropriate to begin to clarify whether or not the use of such leases is an obstacle for companies that have decided to apply the principles of environmental management.

Nowadays, the use of leasing can also be seen as one of the many tools by which it is possible to face the changing European business environment in particular. It happened so with the financial crisis in 2019, or it is also currently happening in the context of the topic of environmental protection environment. Global society is increasingly focusing on the issue of sustainability development and environmental protection. Many companies, states, but also the inhabitants themselves considers this topic increasingly important. That’s why more businesses are trying to apply instruments supporting their social responsibility, environmental friendliness and carbon achievement neutrality. It is in this area that leasing can be viewed as one of possibilities tools of environmental management.

Authors of this paper answer the question: How is the rate of leasing utilization related to the reported profitability values? Is this ratio direct of indirect? Aim of this article is create a regression model to evaluate the performance of companies using leasing financing. The resulting model will be created on the basis of literature research and already conducted studies. Model variables will be identified and data collection performed on the relevant sample of companies. Subsequently, the model will be calculated and interpretation and discussion of the results in the context of the environmental context issues.

The article is divided into 5 parts. Relevant source literature, including empirical findings on leases and circular economy, is summarized in part 2. The research methodology, including the description of the data sample, is explained in part 3. Part 4 presents the results of the regression model verifying the defined hypotheses. Concluding notes are given in part 5, inclusive of stating the area of further research.

The two main concepts, addressed in this paper, such as leases and circular economy, are extremely broad and their definition is not always clearly specified. According to Kopnina (2021), nowadays it seems that leases are widely used in all global markets. Leases of fixed assets are the main part of the financial strategy of many companies. Leases can be used to minimize risks, to increase cash flow, to reduce costs, or to improve financial reporting.

The definition of a lease can be based on that of the International Financial Reporting Standards (hereinafter referred to as the IFRS), which applied the new IFRS 16 standard dealing with leases on 1 January 2019. This standard refers to a lease as a contract that gives the lessee the right to use the underlying asset for a specified period in exchange for a consideration to the lessor (lease payments), with the lessee benefiting from and controlling the underlying asset for the duration of the lease. Therefore, the lessee uses the capitalization model for the vast majority of leases (Diaz et al., 2019).

The paper deals with the issues of lease position in circular economy. In the current state of research, circular economy is an interesting and still to some extent innovative approach of companies, especially in the European Union (EU) and the United States of America. This approach can be characterized as a model that focuses on the efficient use of resources, primarily through waste minimization, the retention of long-term values, the reduction of demands on primary resources, and closing the loop of products, parts of production or material within the environmental protection and socio-economic benefits (Kopnina, 2021). The purpose of circular economy is the path to sustainable development, which will also be separated from autotelic economic growth, which will lead to the negative consequences of depleting resources and environmental deterioration (Murray et al., 2017). Circular economy is often presented as a solution to the problems of the globalized economy in the form of resource overuse, climate change and environmental pollution (Srebalová et al., 2023). Therefore, circular economy is essentially linked to sustainable development, the use of natural resources and climatic changes. There are various government initiatives and programs at the EU level that promote the principles of circular economy in individual member states. Examples could be “A Zero Waste Programme for Europe” (European Commission, 2014), currently ongoing plastic waste initiatives (European Commission, 2018), energy recovery from waste (European Commission, 2017), or general programmes on renewable energy sources, eco-design, and energy efficiency (European Commission, 2015).

The relationship between accounting and ecology was reflected through the so-called “environmental accounting”, which is based on the combination of information on environmental costs based on different use of accounting methods, especially distribution procedures to record costs related to ecology, environmental costs and their breakdown into individual products and processes in the field of environment, environmental policy and specific strategies of individual companies (Ghosh and Wolf, 2021). This approach has recently been applied in the EU through using more data from different sources, procedures for making circular economy analyses and implementing individual managerial and accounting procedures in such a way that natural resources in production can be better and more accurately managed and a greener approach is ensured (Burritt et al., 2019). After the application of these tools, “Environmental management accounting,” a newer term, or EMA is used. Thanks to these principles, accounting can be further defined as an instrument for securing and managing relevant sources of information for monitoring the consequences resulting from the application of circular economy principles concerning operational planning, decision-making processes in aspects of material flows and waste management (Burritt et al., 2019).

In today´s globalized world, the approach of companies that have decided to apply not only EMA, but also other options of environmental behavior, is judged positively. These activities are associated with the concept of “Corporate Social Responsibility”, or CSR, which means a voluntary form of integration, social and environmental practices, and responsibilities within their business model (Andronie et al., 2019). However, CSR is not only about adhering to established rules, but also about willingness and practical investment in human and environmental capital within the civic, political, and social engagement that will benefit the entire community in the broadest sense (Dinu, 2011). In the globalized world and the atmosphere of western culture, it is more common for large companies to report environmental and social responsibility activities in their annual reports. Other partners (banks, investors, competitors, customers, the public, etc.) also draw on these sources. They are also used for academic purposes (Scarpellini et al., 2020). The interrelations between the principles of circular economy and CSR have been addressed by several other authors in their research (for example, Gupta et al., 2019), who described this connection as the so-called “triple bottom line of sustainability.” It is declared that mutual coordination and support of all stakeholders from the supply chain allow the creation of a quality basis for achieving the so-called triple bottom, i.e., the line of sustainability, which includes the economic, environmental, and social levels (Solovida and Latan, 2021).

Large financial and other resources require investments in the application of the principles of circular economy. Several authors have researched the model in terms of the interconnectedness of individual activities improving the environment and the social environment (Koraus et al., 2017). Another important part of this social and business responsibility is the relationship with customers, which has also been researched by some authors (Pauliuk, 2018). Nevertheless, no relevant research has been carried out on the specific microeconomic effects resulting from these market and customer pressures. A certain direction was indicated in the study (Scarpellini et al., 2020) focusing on Spanish companies with more than 50 employees that joined the Spanish government´s challenge and decided to innovate in the industrial, transport, logistics, waste, and energy sectors. The metrics used in the research were, for example, the rate of use of products or services modified in order to increase recyclability or the rate of use of products or services modified to extend life and others. In this study, several areas have been identified where there are links between economic performance and the application of circular economy principles in the given microeconomic conditions (Scarpellini et al., 2020). However, companies applied some principles of circular economy already in the past. An example could be Michelin, which, since 2007, has been selling its tires to road haulers up to a pre-determined mileage limit. In order to extend the life of these products, the company has built a network of mobile workshops, where repairs and cutting of returned tires, which could further be returned to service, are performed. A similar practice has been applied by the Swiss company named Elite to its products of hotel mattresses, uniforms or hotel and hospital textiles (Stahel, 2016).

In order to include leases in circular economy, it is necessary for companies to offer after-sales services and recycling or the re-use of the underlying asset in their comprehensive service, which brings new possibilities of use, which can be partial renewal, renovation, product reorganization, material recycling or subsequent ecological disposal after the termination of a lease (Ghisellini et al., 2016). For this reason, when looking at leases, two main components are considered: the ownership right of the supplier (lessor), who remains the owner of the underlying asset according to legal regulations; and the economic ownership of the operator (lessee), who acquires the right to use the underlying asset, and thus also uses most of the economic benefits for a prearranged consideration (Ionaşcu and Ionaşcu, 2018).

Using this model and financing options, lease financing can be considered to be an alternative to the traditional “Buy and own” model (Lewandowski, 2016). Ballardini, Kaisto and Simila (2021) emphasize the shortcomings of the traditional economic approach to utility in the private pillar of “ownership” when promoting the socially desirable development, such as sustainability, which is important in the context of circular economy (CE), and argue that repairs, reuses, and leases are necessary incentives to steer innovations and businesses towards more sustainable types of models. Innovative circular business models, such as the lease model or the after-sales service model with a focus on the regional context, are emphasized by Hoffmann, Morais and Teodoro (2020).

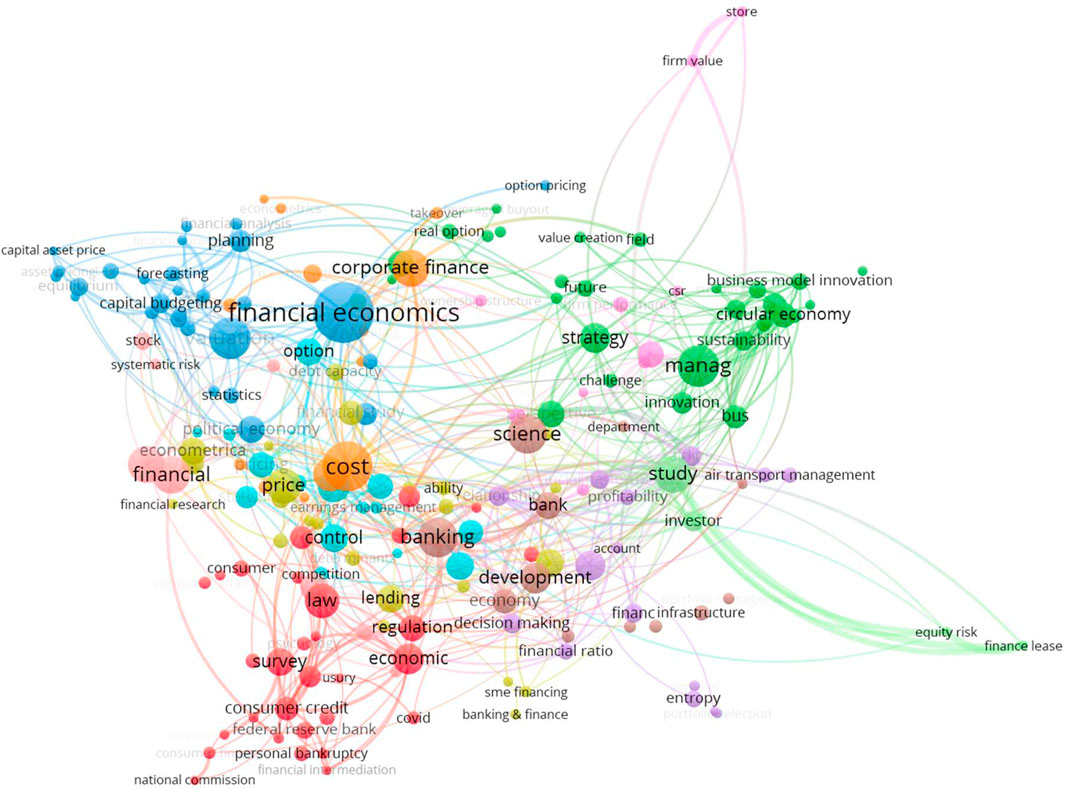

The scientific databases Web of Science and Scopus were primarily used for the literature search. The keywords used in the search were: leasing, efficiency, investor, evaluation. The overall selection of articles was processed using the PRISMA 2020 method (Prisma, 2022), and the main relevant sources found are listed and commented below. At the same sime, the main key links processed in the VOSviewer are visually presented in Figure 1.

FIGURE 1. Visualization of identified posts.

In presented visualization in Figure 1, it is possible to identify among other things, the main 3 colour areas created mutually related sections. In the blue part marked with the largest inscription of the visualization is financial economics, with which related terms such as capital, budgeting, planning, forecasting, etc. are interconnected. The second prominent area is those marked in red expressions related mainly to legislation, such as law, regulation, personal bankruptcy, etc. The fourth, the third and last commented area, which created a stronger area is green, from which management, strategies stand out as the main expressions, innovation, circular economy, business model or even financial leasing.

In one of the publications (Durkin et al., 2014), financing through leasing is analyzed in the context of substitution for classic unsecured bank loans. Another overview study (Lee, 2016) dealt with the position of leasing in alternative financial theories and implications for financial analysis, capital budgeting and interrelationships for short-term financial decision. An extensive analysis of the aviation industry was dealt with in his publication by Yu (2020), who analyzed the industry in the context of the high capital intensity of aircraft acquisition and leasing status. In other publications, in the form of overview studies, other authors analyzed corporate finance (Vishwanath, 2007), risk management (Tapiero, 2011) and, amont other things, the position of leasing in solving these topics or the influence of the top manager’s position on decisions about strategic financing and the ability to secure the necessary assets in optimal capital structure (Brooks et al., 2020). Or the possibility of obtaining an external form of financing in South Africa for small and medium-sized enterprises, whrere leasing plays a very small role in the current situation (Esho and Verhoef, 2022). Another study was devoted to the use of leasing financing in the case of an electric power supply system. Leasing has been shown to be a possible tool to achieve mutual satisfaction on the part of users and investors (Yao et al., 2020).

Other research linking lease transactions with financial performance includes a study by Romanian authors (Ionaşcu and Ionaşcu, 2018), which examined the economic and market performance of companies listed on the Bucharest Stock Exchange in the period from 2013 to 2016 and applied to these companies the monitoring of economic indicators related to market value, business profitability and the use of lease financing, while this study aimed to prove the fact that leases do not penalize companies that choose to use the principles of circular economy and to use more lease financing. However, this fact should not impact on their credibility for investors, profitability or overall performance. The research results discussed that lease transactions can be an illustrative model for the principles of circular economy (Ionaşcu and Ionaşcu, 2018). It was this result that led the authors to continue their research with a partial modification of the procedure that they applied in the conditions of the Czech Republic, namely, in order to strengthen their arguments (Ionaşcu and Ionaşcu, 2018).

Within the research on the impact of leases on the business performance, studies interlinking lease transactions with financial performance in the air transport were identified. It is partly research at major USA airports, where there had been preconditions that the use of lease financing had helped to increase the performance efficiency of individual airports and airlines. The results identified links between the selected models of airport operation and the form of investment decisions of air carriers (Richardson et al., 2014). Furthermore, it is partly the research of Rahman and Dalimunthe, (2019), who analyzed the impact of decisions to use lease financing on the performance of 42 publicly listed airlines from 28 countries between 2015 and 2017. The aforementioned studies agree with the thesis that lease is a key element in creating good management related to market requirements. A regression analysis method was also used here, following financial analysis indicators and Tobin’s Q like at Ionascu and Ionascu, (2018). In the results, he points out, similar results, that leasing is related to the financial performance of companies, but no solid conclusions can be drawn from this. Leasing is only one of the possible causes of the observed differences and it is necessary to carry out further scientific quantitative research to obtain a sufficient number of other studies. Another study (Bourjade et al., 2017), also focused on the aviation industry, used regression analysis to monitor the effect of the age of the company on the use of leasing, the size of EBIT or the amount of turnover.

Hope and Vyas (2017) published an extensive review article on the possibilities of obtaining external financing by private companies. They report that leasing is the third most common external source of financing in the EU for SMEs. Another author (Pasirayi, 2020) used a regression model to process the use of rental/leasing for retail units that individual companies can provide to other users if they do not have full use for them. By applying this approach, companies can achieve an average incremental increase in company value of 1.06%. A macroeconomic study by Chinese authors (Zhang et al., 2019) looked at the impact of leasing on global economic growth. Using a dynamic threshold model, they compared the effect of the amount of bank loans and leasing on the growth of the world economy. In the results they interpreted that leasing financing has a positive effect on economic growth. Another study by Slovak author (Čajková and Bultoracova Sindleryouva, 2022) dealt with the interdisciplinary dimension within the macroeconomic perspective within the framework of sustainability and public budget planning and the use of external sources of financing, which can also be leasing.

The authors of further research (Ron van Kints and Louis Spoor, 2019) using the method of experiment and role-playing with 46 students of the master’s program at the Institute of Executive Master of Finance and Control observed investment decision-making after the application of the IFRS 16 standard. Namely, whether it will have the expected results on the investment decision-making of CFOs (roles of students). In the research, the authors present the results in such a was that the change of the standard to IFRS 16 has a positive effect on the quality of decision-making of professional users regarding investment decisions.

The interconnection between the circular economy and leases is also confirmed by Ghisellini, Cialani and Ulgiati (2016), namely, due to meeting the conditions, which include, in particular, the connection with after-sales services. One of the authors (Tukker, 2004) has formulated three mainstreams in the product-service system model defined by Mont (2002) as being a system of products and services of partner forces and infrastructure, meeting customer needs and at the same time having lesser impact on the environment. The three mainstreams as follows:

A model characterized by pressure to sell the final product, which is complemented by additional after-sales services (maintenance, consultancy, arranging financing–credit brokerage, etc.). In this model, repurchase is also provided, which is crucial for the purposes of circular economy and leases.

A model typical for leases and rentals, which are already classified in the same category in terms of the IFRS accounting and reporting after the application of IFRS 16. The final product is target, and only the right to use the asset is allowed. Ownership rights remain with the original owner. This model is often supplemented by the model mentioned above, with other after-sales services being added here, such as service, maintenance and possible repurchase. However, in case of this model it is also possible to encounter reusing by multiple users, the so-called “product pooling.”

The supplier and the customer agree in advance on the required final product or result, without specifying a particular product or using particular tools or practices. After that the supplier will ensure the delivery of the required ordered product or service. Typical examples of this model are outsourced services (accounting, cleaning, tax consultancy, call centers, but also leases).

It can be concluded from the authors’ statements above that leases with their characteristics fit in with the business models of circular economy, which can be expected to support sustainable development through recirculation of products, which will contribute to the slowdown in the flow of resources and to the increase in the productivity of using resources, which is accordance with the principles of the environmental management system.

Unlike the mainstream economy paradigm, where the aim is to increase the efficiency of extraction and use of resources in order to sustain growth, the ecological economy paradigm is aimed at achieving and ensuring a higher quality of life. The circular economy often seeks answers to deep ontological and epistemological questions that must be answered if we are to address the complex and interrelated environmental, economic, and social problems that society faces today (Temesgen et al., 2021). These authors argue that in order to achieve a lasting solution to the interconnected social, economic, and environmental problems, the circular economy must be integrated into the ontological, epistemological, and axiological foundations of the mainstream economy. This paper is based on just this thesis and aims to identify the links between the use of lease financing as a regular component of the economy and profitability and credibility for investors. Given the performed research part of the paper, the results will further be interpreted as hypothetical options of usability for companies that would decide to apply the principles of circular economy, respectively actively develop the environmental management system.

Other authors in their outputs presented leasing in the context of sustainability and the circular economy. The firs of them (Andriankaja et al., 2015) investigated the use of leasing in the context of PSS in urban freight transport and the monitoring of environmental impacts in comparison with models without the use of leasing. She found that with the use of leasing, increased efficacy is achieved and at the same time smaller impacts on the environment. Van Loon et al. (2020) focused on the leasing of automatic washing machines. He researched different model lines, customer demands and the use of the operational leasing and reuse model in the secondary market of used appliances. He found that this model is only sustainable when applied to premium product lines that can subsequently be used by up to three consumers in their life cycle. Based on IKEA customers questionnaires, Gullstrand et al. (2016) investigated long-term and short-term leasing models for household furniture or just for short-term occasions (garden parties, etc.). The rental model for these consumer goods had not proven to be sustainable. Positive results were demonstrated only for short-term rental, i.e., rather for borrowing.

Other authors demonstrated in their works the use and sustainability of leasing in the case of renting electric batteries for electric cars (Ahuja et al., 2020; Li et al., 2020). At the same time, other authors also confirmed that leasing is an important tool of environmental management for future use in automobile transport after the application of electromobility, which corresponds to the principles of sustainability and circular economy (Messagie et al., 2013; Lee et al., 2016; Hoogland et al., 2022).

The research part was inspired by the research conducted by Romanian authors (Ionaşcu and Ionaşcu, 2018), which examined the economic performance of companies traded on the Bucharest Stock Exchange. The presented research was applied to companies trading on the Prague Stock Exchange. The authors of this article methodically made adjustments compared to reference article in the area of data collection and the methodology itself. It was based on the total available sources from 1993 and not only from 2013 to 2016. At the same time, a selection of data was made in the event that companies were not publicly traded for the entire calendar year. For the sake of better comparison and further future research (even in an international comparison) the profit indicator EBIT and not Net Income was used at the same time. An important factor expanding the findings of the reference article is also the fact that the research presented here also includes observations after 2019, i.e., after the application of the new IFRS 16 standard.

The basic identification of companies was performed using the website of the Prague Stock Exchange, a.s. (Prague Stock Excange, 2023). Based on the trade volume realized in 2020, specific companies were identified. Investment funds and other market makers, which are mainly owned by commercial banks, were removed from the list.

Because of its applicability to companies in the normal market environment covering the manufacture of products or the provision of services, only one of the commercial banks, which has its shares listed on the Prague Stock Exchange, was included in the final selection of the research sample. Other banking institutions were excluded from the research (Bauer, 2004).

Companies that started trading on the Prague Stock Exchange during 2020 were subsequently excluded from the selected sample, as it would not be possible to obtain complete and published data for the entire calendar period of 2020. This selection also provided a better opportunity for the comparison with other companies and their results from previous periods.

After the identification of specific companies, for the purposes of the final research sample, data from the year when the companies started trading on the Prague Stock Exchange were used. We used data from the Prague Stock Exchange, the Commercial Register of the Czech Republic, the Ministry of Justice of the Czech Republic and the companies’ websites (Ministry of Justice, 2023). We examined the period from 1993 to 2019.

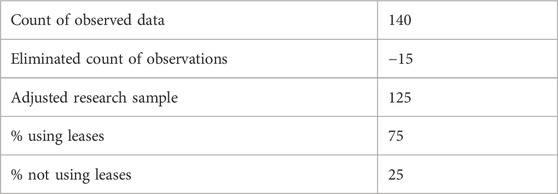

The resulting sample contained a total of 140 observations. Due to the possibility of using individual indicators in the research, a final adjustment was made, when 15 observations were excluded because of missing published data or unreliable leasing data. After the final selection, the research sample was shortened to 125 observations on 15 companies.

Table 1 below shows the distribution of companies in the resulting research sample by the line of business breakdown.

TABLE 1. Sectoral distribution of the research sample comprising 15 companies.

Table 1 shows that the largest number of observations was made at companies from the Production area. The second largest group of observations were companies from the service sector, especially IT, telecommunications or banking.

Table 2 shows the division of companies according to the individual parts of the stock market, where they are listed on the Prague Stock Exchange.

Table 2. Market distribution of the research sample comprising 15 companies.

As can be seen in Table 2, the largest number of observations included in the research was for companies listed on the Prague Stock Exchange in the PRIME category. The second most numerous category was STANDARD. From the point of view of represented companies, the FREE market category was more represented. However, these companies have been publicly traded for a short period of time and therefore it was not possible to obtain a higher number of observations for research purposes.

We used data on the market tradable price per share from the database of the Prague Stock Exchange as of December 31 of the analyzed year or the nearest possible date.

Where possible, financial ratios based on consolidated financial statements were used from the companies’ annual reports. For this reason (especially for foreign parent companies), the homepages of the companies in question had to be used as a source for obtaining the relevant annual reports.

Financial ratios obtained from the annual reports are as follows. From the balance sheet: net value of assets, net value of tangible assets, stockholders’ equity, and borrowed capital. From the profit and loss statement: turnover, total sales, and profit or loss before and after tax. From notes to financial statements: firm size and board size—to monitor the impact of company size on the quality of management - financial performance, number of shares forming the capital stock, and all information on the use of lease financing.

Since 2019, it has been necessary to capitalize lease contracts both on the assets side in the form of the measurable right of use and on the liabilities side in the form of the total lease liability in accordance with IFRS 16 (IFRS Foundation, 2016). In order to maintain continuity for subsequent comparisons, the research was always based on the value of lease liabilities, as these data were required to be provided by companies in the notes even before the application of IFRS 16.

After the data collection, the analytical part of the work was performed, where several derived indicators were used. They are listed below with the calculation formula because some variables are not always derived from the same variables in the professional literature.

In the resulting model, profitability ratios (ROA, ROS, ROE), which were complemented by two more ratios (Tobin´s Q and Market to Book), which represent the subjective perception of investors and financial analysts in the model, have been chosen as objective performance indicators of companies.

The variable could only take values of 0 or 1. When the examined year was classified in this variable as 1, the company used lease financing in the given year. When this was not the case, this variable had the value of 0.

The variable has been chosen in its simplified form as the product of the number of shares forming the share capital and the market value of one share traded on the Prague Stock Exchange always at the close of the given year (see above).

The “Profit before tax” variable was used in the calculations of profitability ratios. In case of these ratios, the professional literature is not always uniform. The variable chosen in this way was used mainly for the purpose of maintaining the possibility of comparing individual years and companies. In case that there were consolidated financial statements of foreign parent companies available, the use of the “Profit after tax” variable would distort the results due to the different tax rates in individual countries.

ROA–Return on assets

ROE–Return on equity

ROS–Return on sales

The ratio was used for the purposes of this research in its already modified modern form, which is used in measuring the market value of the company by the ratio between the market value and the book value of the company. The formula is given below (Herciu and Serban, 2018).

This ratio compares the market and book value of a share (Ionaşcu and Ionaşcu, 2018).

This ratio indicates the level of borrowed capital against the company´s net value of assets.

For the purposes of the examined issues, related to lease financing, the ratio between the net value of long-term assets and the total net value of assets of the company was monitored within this variable.

Lease Intensity was the last derived variable.

After the application of IFRS 16, this ratio should be modified to reflect the total value of capitalized rights to use - the value of assets capitalized by virtue of financial lease and discounted lease payments under the operating lease. However, this procedure can be applied only in the periods following 2019 (inclusive). Due to the fact that the research was conducted for the period from 1993 to 2019, there would be a discontinuous calculation for years other than for 2019, and for this reason the formula was applied as described above. It expresses the value of using lease financing in proportion to the company´s total fixed assets (tangible assets), whether or not they were capitalized directly in assets in the past. Prior to 2019, practically, data on only financial leases were required in the annual reports. After the application of the new IFRS 16, there was an increase in both total fixed assets (capitalization of the right of use) and the total value of leases (total lease liabilities). Prior to 2019, information on operating leases was not disclosed de facto and did not affect any variable in the aforementioned formula. In the past, operating leases were normally posted directly in operating costs (Giner and Pardo, 2018).

Based on the theoretical solutions, the following regression model for panel data with fixed effects is presented. This is an unbalanced panel because individual companies are monitored in different periods (they were not traded for the same length of time).

The hypotheses that will further be verified were formulated as follows:

H1. Financial performance is higher for companies traded on the Prague Stock Exchange using leases and rentals.

H2. Financial performance is directly proportional to the Lease Intensity variable.

The hypotheses were tested on the basis of the following regression models, where the explained variable, i.e., performancei,j is always changed to the monitored financial ratios: ROA, ROS, ROE, Tobin´s Q and Market to Book. The individual years of observation (i) and the individual companies (j) are used as indices:

The individual variables with comments are explained above in this chapter.

The second equation of the model contains the Lease Intensity2 variable. This adjustment was applied due to a possible non-linear relation between the leasing intensity and performance measured on the basis of accounting values (Bourjade et al., 2017). Its use is relevant only for observing the return on assets and the return on sales.

Industry Dummy and Year Dummy are only fictitious variables based on the observed individual years and the line of business of the given companies.

The resulting research sample is presented in Table 3, which shows the proportion of companies which used lease financing in the period from 1993 to 2019 and which, on the contrary, did not use it.

TABLE 3. The share of lease use in the observed sample of companies.

The non-use of leases has been identified mainly in large multinational companies or companies with the state ownership interest, which have sufficient capital to ensure self-financing (fields of business: banking services, production of tobacco products, electricity generation). Nevertheless, after the application of the new IFRS 16 standard, information on the capitalization of rights to use by virtue of operating leases was recorded even for these companies. Prior to 2019, all companies reported operating leases directly in operating costs and no additional information was provided on this type of financing in annual reports.

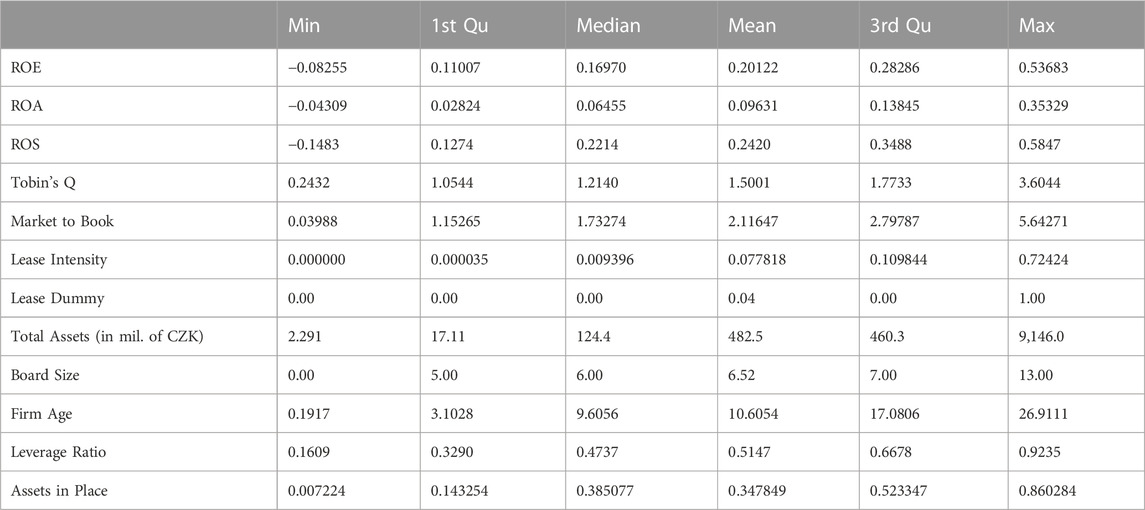

Table 4 shows the basic values of descriptive statistics on the adjusted research sample of 125 observed data. The Lease Intensity ratio shows the average value of 7.78%, which is interesting especially in comparison with its maximum value of 72.4%. The marked variability of this ratio is caused by including 15 observed companies, which were excluded from the research sample for regression models, and at the same time these were capital-strong companies operating on the Prague Stock Exchange. Nevertheless, thanks to the application of the new IFRS 16 standard and the need to publish information on operating leases already for 2018 and subsequently also for 2019, when the standard was applied, there is a noticeable increase in the average value of this ratio, which for these 2 years showed the value of 17.7%.

TABLE 4. Ratios of descriptive statistics on the adjusted research sample.

Table 5 gives an overview and comparison of the basic observed ratios and their average values for companies which used lease financing in the resulting research sample and which, on the contrary, did not use it.

TABLE 5. The comparison of basic observed ratios related to the use of leases.

The above comparison clearly shows that companies using lease financing achieve higher values in virtually all observed financial ratios.

The higher value of return on assets by +4.3 p.p. expresses the ability of companies using leases to make better use of their assets to achieve their profit. Likewise, their ability to use the resources of stock capital is better by +2.6 p.p., which may be associated with the fact that some resources are allocated to the use of lease financing.

In terms of return on sales, companies using leases achieved a worse result of −15.0 p.p. This is mainly caused by the fact that they are strong capital companies providing banking services and electricity generation and distribution, which reported lease financing only in 2019 (or more precisely in 2018), when there was a need for capitalization and disclosure due to the new IFRS 16. However, at the same time these are companies whose product has a generally high margin.

Companies with lease financing have significantly higher values in evaluating and measuring the company´s market value, i.e., the Tobin´s Q ratio, expressing investor confidence, or the Market to Book ratio, expressing the relation to the book value of their company.

This research aims to prove the fact that the use of lease financing is not an obstacle to investor confidence and the company´s overall market valuation. Chart 1 clearly illustrates the development of the three most important ratios. These derived variables are Tobin´s Q, Market to Book and Lease Intensity. Values related to Tobin´s Q and Market to Book are in the left part of y axis. The percentages related to the Lease Intensity variable are in the right part of y axis.

CHART 1. The development of key derived ratios over time.

At first glance, Chart 1 shows that over time, since 2001, companies have been focusing on the options of lease financing more and more. A large increase can be seen in 2019 and partly in 2018, which is related to the already mentioned application of the new IFRS 16 standard and the need to capitalize and disclose information on all lease contracts. In 2015, there was also a large increase in the use of lease financing, which was due to O2 Czech Republic, a.s., which separated CETIN, a.s. from its structure that year, and thus the value of Lease Intensity markedly increased, as the tangible assets decreased by −87%, but the value of total leases decreased by only −59%.

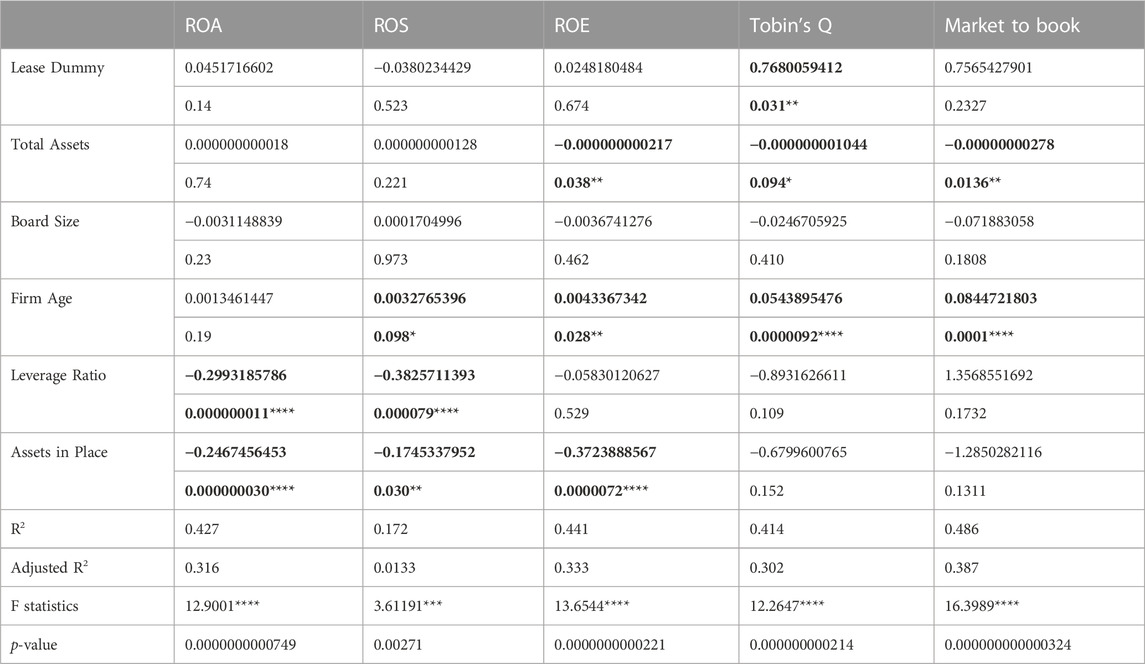

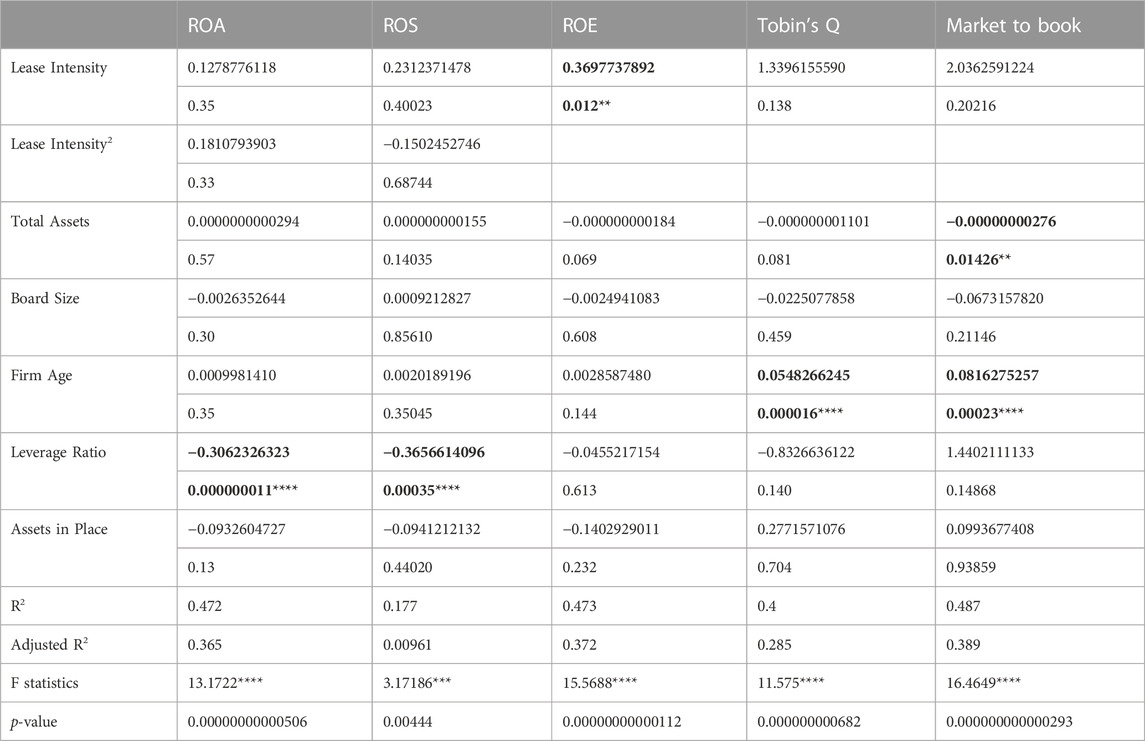

The following table, i.e., Table 6 presents the results of the regression model on the adjusted research sample according to the first equation shown above. The equation follows up with the first hypothesis observing the relation between the use of lease financing and the financial performance of companies trading on the Prague Stock Exchange. The significance levels are indicated as follows: **** 0.001; *** 0.01; ** 0.05; * 0.1. The value of the β coefficient is shown on the first line for each variable. The test criterion Pr(>|t|) is on the second line.

TABLE 6. The results of the regression model according to the first equation.

The fact whether the company uses the possibility of lease financing was statistically significant for observing the value of Tobin´s Q, which expresses investor confidence and the company´s valuation in the market. The use of lease financing is not perceived by external investors as a penalizing parameter leading to a lower market valuation (positive correlation). The value of Total Assets with negative correlations for the values of ROE, Tobin´s Q and also Market to Book has also proved to be a statistically significant variable when monitoring the market valuation. The increasing amount of total net assets does not lead to an increase in the return on stock capital or an increase in the market value of companies.

The statistically significant negative correlation was also recorded for Assets in Place. Likewise, this negative correlation has been proved for derived indicators expressing investor confidence. The examined companies have failed to improve profitability values in the long-term investment and to convince external investors of maintaining the market value of the company. The possible solution is just the greater use of leases to ensure investment needs of companies, and thus maintaining the return on assets as well as the investor confidence.

The number of years for which the company is present at the Prague Stock Exchange has been identified as another statistically significant factor in the company´s market valuation. Investor confidence increases with the increasing number of years (positive correlations with Tobin´s Q and Market to Book) and companies have also improved their return on equity.

So far, the fact whether companies use lease financing or not at all has been examined in the regression model. For this reason, the research has therefore been widened to include the fact whether such lease financing really occurs and also to include its intensity rate. The results of the regression model (based on the second hypothesis reflected in the second equation) are shown in Table 7. The significance levels are indicated as follows: **** 0.001; *** 0.01; ** 0.05; * 0.1. The value of the β coefficient is shown on the first line for each variable. The test criterion Pr(>|t|) is on the second line.

TABLE 7. The regression model results of the second equation.

Compared with the results of the first regression model, Lease Intensity has become the statistically significant variable only for the return on equity. Thanks to the positive correlation, it can be expected that companies using leases will achieve higher appreciation of their equity for their stockholders. The results of the second regression model have also identified a positive correlation for the market valuation of companies, which was quite close to the statistical significance, namely, the value of for Tobin’s Q, expressing the fact that increasing leases in proportion to the long-term net assets does not lead to a negative perception of investors.

Other variables and their positive or negative correlations have already been commented on in case of the first equation results of the regression model. As in the first case, the number of years of trading on the Prague Stock Exchange has proved to be a statistically significant variable for market valuation.

Resulting from the above facts, it was thus possible to accept both hypotheses.

The literature review part of this article has shown that the issue of leases as part of the circular economy and even the model of business behavior itself corresponding to the principles of the environmental management is still basically an innovative approach. For this reason, the standard methods of scientific research have not been defined yet. Therefore, leases were applied as an illustrative method corresponding to the principles of circular economy (as an environmentally, socially and economically sustainable approach).

Some areas of identical results can be identified when comparing the results presented by this research with the Romanian authors (Ionaşcu and Ionaşcu, 2018). The Romanian authors examined the total of 266 samples in their study (vs. 125 in this study). They found that companies using leases are represented in the examined sample by 72% (vs. 75%). Some adjustments were made in the research presented in this paper in order to ensure a better possibility of comparing individual samples, which were explained and described in the methodology (such as reporting the value of leases in the amount of total lease liability due to the inclusion of 2019, etc.). However, essentially the same linear regression models were used to examine the dependences.

As in the case of research by Romanian authors, relationships supporting the increase in the market valuation of companies through the use of leasing have been identified. The negative correlation has also been identified for the return on assets.

However, unlike Romanian companies, it has been shown that the number of years of public trading improves the market value of companies traded on the Prague Stock Exchange. As stated in the Romanian research (Ionaşcu and Ionaşcu, 2018), the companies traded on the Bucharest Stock Exchange were largely companies from the previous communist era. Therefore, most Romanian investors preferred and trusted newer companies with more potential. This research, examining the sample from the Prague Stock Exchange, has proved the exact opposite, when the better market valuation occurring with the increasing number of years of public trading. This fact is caused mainly by the presence of foreign companies on the Prague Stock Exchange or publicly traded Czech companies, which were established after the fall of the communist regime and have been built in the market economic environment.

From the aforementioned facts, the Romanian authors also believe that the business model based on the use of lease financing increases the business performance measured by market values, and investors value leases as a business model that has the potential to increase the company´s value (Ionaşcu and Ionaşcu, 2018).

The principles of circular economy, supporting sustainable development and corresponding environmental behavior in today´s globalized world, are becoming increasingly important and companies are increasingly being pushed by their visions, strategies, but also by customers and the public to behave more socially and economically responsibly. So that they actively apply the environmental management system and thus prevent environmental threats. Yet, the application of these models should take place in such a way so that the economic performance of companies and confidence for investors and business partners can be maintained.

The possibility to use lease financing is one of the many models that can be considered to comply with these principles. The research examined the links between companies using leases and the achieved level of their profitability as well as of their market valuation by investors. The results were compared both with companies that do not use leases in their business model, and the links between the amount of leases and the achieved economic and market performance of companies were analyzed.

It has been proved that companies using leases are able to maintain investor confidence better. Their market value has increased, or their overall results measured by financial ratios have been better. It has been confirmed that lease financing does not harm the economic performance of companies and that, on the contrary, it is an alternative way of financing companies, which would serve as a tool for support and further development of the environmental management system.

It has been confirmed that the use of leases increases the value of Tobin´s Q. However, there has been a decrease in investor confidence expressed by the negative correlation of Tobin´s Q when comparing with the situation where the company invests in increasing its tangible assets in the standard way (using own or borrowed capital).

Nevertheless, the view of lease financing as part of the circular economy is still innovative. Therefore, there are considerable opportunities for further research, especially after the application of new IFRS 16. Data on the use of this form of financing operating needs of companies in relation to their results and market valuation will be increasingly available in the future (due to the application of IFRS 16).

The presented article extended further quantitative research in the field of sustainability, circular economy, environmental management and the position of leasing as one of the possible instruments of these policies. Methodologically, it was different from other authors in that it offered better possibilities for international comparison by using profit at the EBIT level. At the same time, data were analysed over a longer period than is the case with other authors.

However, the possibilities of obtaining the necessary information about leasing financing from public sources are very complicated and limited. For this reason, the authors recommend in further research to focus future attention on specific areas of individual business activities (transport, banking, construction, retail, services, etc.) so that a quantitative comparison can be made. Further future research carried out in this way will serve to obtain sufficient scientific background for any generalization and possible evaluation of the position of leasing supporting the economic performance of companies. Further research can be expanded especially after the application of the new IFRS 16 standard, when leasing contracts (primarily also operational leasing) were capitalized and the level of detail disclosed in annual reports increased.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

VB: Conceptualization, Data curation, Formal Analysis, Funding acquisition, Investigation, Methodology, Project administration, Resources, Software, Supervision, Validation, Visualization, Writing–original draft, Writing–review and editing. JH: Conceptualization, Data curation, Formal Analysis, Funding acquisition, Investigation, Methodology, Project administration, Resources, Supervision, Validation, Writing–original draft, Writing–review and editing. JA: Conceptualization, Funding acquisition, Investigation, Project administration, Resources, Supervision, Validation, Visualization, Writing–original draft, Writing–review and editing.

This article was supported by the Internal Grant Agency, number 2020A0008 - Leases in the circular and shared economy.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2023.1272816/full#supplementary-material

Ahuja, J., Dawson, L., and Lee, R. (2020). A circular economy for electric vehicle batteries: Driving the change. J. Prop. Plan. Environ. Law 12, 235–250. doi:10.1108/JPPEL-02-2020-0011

Andiankaja, D., Gondran, N., and Gonzalez-Feliu, J. (2015). Assessing the environmental impacts of different IPSS deployment scenario for the light commercial vehicle industry. 7thIndustrial Product-Service_Systems Conf. – IPSS, Industry Transformation Sustain. Bus. 30, 281–286. doi:10.1016/j.procir.2015.02.159

Andronie, M., Simion, V. E., Gurgu, E., Dijmărescu, A., and Dijmărescu, I. (2019). Social responsibility of firms and the impact of bio-economy in intelligent use of renewable energy source. Amfiteatru Econ. 21, 520–535. doi:10.24818/EA/2019/52/520

Ballardini, R. M., Kaisto, J., and Simila, J. (2021). Developing novel property concepts in private law to foster the circular economy. J. Clean. Prod. 279, 123747. doi:10.1016/j.jclepro.2020.123747

Bauer, P. (2004). Determinants of capital structure: Empirical evidence from the Czech republic. Czech J. Econ. Finance 54, 159–175. doi:10.18267/j.pep.237

Bourjade, S., Hucm, R., and Muller-Vibes, C. (2017). Leasing and profitability: Empirical evidence from the airline industry. Transp. Res. 97, 30–46. doi:10.1016/j.tra.2017.01.001

Brooks, M., Hairston, S., and Harter, C. (2020). Does manager ability influence the classification of lease arrangements? J. Appl. Account. Res. 21, 19–37. doi:10.1108/JAAR-02-2019-0028

Burritt, R. L., Herzig, C., Schaltegger, S., and Viere, T. (2019). Diffusion of environmental management accounting for cleaner production: Evidence from some case studies. J. Clean. Prod. 224, 479–491. doi:10.1016/j.jclepro.2019.03.227

Čajková, A., and Bultoracová Šindleryová, I. (2022). Usability of municipal performance-based budgets within strategic planning in Slovakia: Perception of elected local representatives. Nisp. J. Public Adm. Policy 15, 17–37. doi:10.2478/nispa-2022-0002

Diaz, J. M., Hernandez, M. A. V., and Voicila, F. I. (2019). Lease accounting: An inquiry into the origins of the capitalization model. De. Computis-Revista Espanola De. Hist. De. La Contab. 16, 160–187. doi:10.26784/issn.1886-1881.v16i2.357

Dinu, V. (2011). Corporate social responsibility – opportunity for reconciliation between economical interests and social and environmental interests. Amfiteatru Econ. 13, 6–7.

Durkin, T. A., Elliehausen, G., Staten, M. E., and Zywicki, T. J. (2014). Consumer credit and the American economy. Consumer Credit Am. Econ. 2014, 1–736. doi:10.1093/acprof:oso/9780195169928.001.0001

Esho, E., and Verhoef, G. (2022). SME funding-gap and financing: A comprehensive literature review. Int. J. Glob. Small Bus. 13 (2022), 164–191. doi:10.1504/ijgsb.2022.127226

European Commission (2018). A European strategy for plastics in a circular economy. Brussels: European Commission, 18.

European Commission (2015). Closing the loop - an EU action plan for the Circular Economy. Brussels: European Commission, 34.

European Commission (2017). The role of waste-to-enerty in the circular economy. Brussels: European Commission, 34.

European Commission (2014). Towards a circular economy: A zero waste programme for Europe. Brussels: European Commission, 34.

Ghisellini, P., Cialani, C., and Ulgiati, S. (2016). A review on circular economy: The expected transition to a balanced interplay of environmental and economic systems. J. Clean. Prod. 114, 11–32. doi:10.1016/j.jclepro.2015.09.007

Ghosh, R., and Wolf, S. (2021). Hybrid governance and performances of environmental accounting. J. Environ. Manag. 284, 111995–112011. doi:10.1016/j.jenvman.2021.111995

Giner, B., and Pardo, F. (2018). The value relevance of operating lease liabilities: Economic effects of IFRS 16. Aust. Account. Rev. 28, 496–511. doi:10.1111/auar.12233

Gullstrand, E. E., Lehner, M., and Mont, O. (2016). Exploring consumer attitudes to alternative models of consumption: Motivations and barriers. J. Clean. Prod. 4, 5–15. doi:10.1016/j.jclepro.2015.10.107

Gupta, S., Chen, H., Hazen, B. T., Kaur, S., and Gonzalez, E. D. S. (2019). Circular economy and big data analytics: A stakeholder perspective. Technological Forecasting and social change. Technol. Forecast. Soc. Change 144, 466–474. doi:10.1016/j.techfore.2018.06.030

Herciu, M., and Serban, R. A. (2018). Measuring firm performance: Testing a proposed model. Stud. Bus. Econ. 13, 103–114. doi:10.2478/sbe-2018-0023

Hoffmann, B. S., Morais, J. D., and Teodoro, P. F. (2020). Life cycle assessment of innovative circular business models for modern cloth diapers. J. Clean. Prod. 249, 1–16. doi:10.1016/j.jclepro.2019.119364

Hoogland, K., Chakraborty, D., and Hardman, S. (2022). To purchase or lease: Investigating the finance decision of plug-in electric vehicle owners in California. Environ. Res. Commun. 4 (2022), 095005–095015. doi:10.1088/2515-7620/ac8397

Hope, O. K., and Vyas, D. (2017). Private company finance and financial reporting. Account. Bus. Res. 47, 506–537. doi:10.1080/00014788.2017.1303963

IFRS Foundation (2016). IFRS 16 leases. Available at: https://www.ifrs.org/-/media/project/leases/ifrs/published-documents/ifrs16-effects-analysis.pdf (Accessed March 20, 2023).

Ionaşcu, I., and Ionaşcu, M. (2018). Business models for circular economy and sustainable development: The case of lease transactions. Amfiteatru Econ. 20, 356–372. doi:10.24818/EA/2018/48/356

Kopnina, H. (2021). Towards ecological management: Identifying barriers and opportunities in transition from linear to circular economy. Philosophy Manag. 20, 5–19. doi:10.1007/s40926-019-00108-x

Koraus, A., Simionescu, M., Bilan, Y., and Schönfeld, J. (2017). The impact of monetary variables on the economic growth and sustainable development: Case of selected countries. J. Secur. Sustain. 6, 383–390. doi:10.9770/jssi.2017.6.3(5

Lee, A. C., Lee, J. C., and Lee, C. F. (2016). Financial analysis, planning and forecasting: Theory and application. Financial Analysis, Plan. Forecast. Theory Appl. 2016, 1–1136. doi:10.1142/6416

Lee, S. H. (2016). A study of servitization strategy for electric vehicles. J. Distribution Sci. 14, 5–13. doi:10.15722/jds.14.9.201609.5

Lewandowski, M. (2016). Designing the business models for circular economy-towards the conceptual framework. Sustainability 8, 43–28. doi:10.3390/su8010043

Li, M., Ye, H., Liao, X., Ji, J., and Ma, X. (2020). How Shenzhen, China pioneered the widespread adoption of electric vehicles in a major city: Implications for global implementation. Wiley Interdiscip. Rev. Energy Environ. 9, 1–15. doi:10.1002/wene.373

Messagie, M., Lebreau, K., Coosemans, T., Macharis, C., and van Mierlo, J. (2013). Environmental and financial evaluation of passenger vehicle technologies in Belgium. Sustain. Switz. 5, 5020–5033. doi:10.3390/su5125020

Ministry of Justice (2023). Public register of legal entities. Available at: https://or.justice.cz/ias/ui/rejstrik-$firma (Accessed March 15, 2023).

Mont, O. K. (2002). Clarifying the concept of product-service system. J. Clean. Prod. 10, 237–245. doi:10.1016/S0959-6526(01)00039-7

Murray, A., Skene, K., and Haynes, K. (2017). The circular economy: An interdisciplinary exploration of the concept and application in a global context. J. Bus. Ethics 140 (3), 369–380. doi:10.1007/s10551-015-2693-2

Pasirayi, S. (2020). Stock market reactions to store-in-store agreements. Ind. Mark. Manag. 91, 455–467. doi:10.1016/j.indmarman.2020.09.010

Pauliuk, S. (2018). Critical appraisal of the circular economy standard BS 8001:2017 and a dashboard of quantitative system indicators for its implementation in organizations. Resour. Conservation Recycl. 129, 81–92. doi:10.1016/j.resconrec.2017.10.019

Prague Stock Exchange (2023). Prague stock exchange. Available at: https://www.pse.cz/ (Accessed March 15, 2023).

Prisma (2022). Prisma. Available at: http://prisma-statement.org/ (Accessed November 16, 2022).

Rahman, T. A., and Dalimunthe, Z. (2019). Does aircraft leasing strategy increase airline performance? In proceedings of conference: 33rd international-business-information-management-association (IBIMA). Spain: Granada, pp. 7579–7587.

Richardson, C., Budd, L., and Pitfield, D. (2014). The impact of airline lease agreements on the financial performance of US hub airports. J. Air Transp. Manag. 40, 1–15. doi:10.1016/j.jairtraman.2014.04.004

Ron van Kints, R. E. G. A., and Louis Spoor, L. L. (2019). Leases on balance a level playing fiels? Adv. Account. 44, 3–9. doi:10.1016/j.adiac.2018.11.001

Scarpellini, S., Marín-Vinuesa, L. M., Aranda-Usón, A., and Portillo-Tarragona, P. (2020). Dynamic capabilities and environmental accounting for the circular economy in businesses. Sustain. Account. Manag. Policy J. 11, 1129–1158. doi:10.1108/SAMPJ-04-2019-0150

Solovida, G. T., and Latan, H. (2021). Achieving triple bottom line performance: Highlighting the role of social capabilities and environmental management accounting. Manag. Environ. Qual. 32, 596–611. doi:10.1108/MEQ-09-2020-0202

Srebalová, M., Peráček, T., and Mucha, B. (2023). “Nuclear waste potential and circular economy: Case of selected European country,” in Developments in information and knowledge management systems for business applications. Studies in systems, decision and Control. Editors N. Kryvinska, M. Greguš, and S. Fedushko (Cham: Springer), Vol. 462. doi:10.1007/978-3-031-25695-0_13

Tapiero, C. S. (2011). Risk finance and asset pricing: Value, measurements, and markets. Risk Finance Asset Pricing Value, Meas. Mark. 2011, 1–456. doi:10.1002/9781118268155

Temesgen, A., Storsletten, V., and Jakobsen, O. (2021). Circular economy - reducing symptoms or radical change? Philosophy Manag. 20, 37–56. doi:10.1007/s40926-019-00112-1

Tukker, A. (2004). Eight types of product–service system: Eight ways to sustainability? Experiences from SusProNet. Bus. Strategy Environ. 13, 246–260. doi:10.1002/bse.414

Van Loon, P., Delegarde, C., Van Wassenhove, L. N., and Mihelič, A. (2020). Leasing or buying white goods: Comparing manufacturer profitability versus cost to consumer. Int. J. Prod. Res. 58 (2020), 1092–1106. doi:10.1080/00207543.2019.1612962

Vishwanath, S. H. (2007). Corporate finance: Therory and practice. Corp. Finance Theory Pract. 2007, 1–763. doi:10.4135/9788132111801

Yao, Z., Chen, W., Jin, Q., Guo, M., and Feng, Y. (2020).Service pattern for premium power supply based on combination of leasing and property transfer, IEEE 4th Conference on Energy Internet and Energy System Integration: Connecting the Grids Towards a Low-Carbon High-Efficiency Energy System, Nov-1-2020, China, 9346. IEEE, 3558–3563. doi:10.1109/EI250167.2020.9346962

Yu, D., Boughton, B. A., Hill, C. B., Feussner, I., Roessner, U., and Rupasinghe, T. W. T. (2020). Aircraft valuation: Airplane investments as an asset class. Aircr. Valuat. Airpl. Investments as Asset Cl. 2020, 1–332. doi:10.3389/fpls.2020.00001

Keywords: environmental management, IFRS 16, leases, tangible assets, fixed assets, company’s market value

Citation: Bocok V, Hinke J and Abrham J (2023) Leasing from the perspective of environmental management and its influence on business performance. Front. Environ. Sci. 11:1272816. doi: 10.3389/fenvs.2023.1272816

Received: 04 August 2023; Accepted: 30 August 2023;

Published: 14 September 2023.

Edited by:

Erginbay Uğurlu, İstanbul Aydın University, TürkiyeReviewed by:

Andrea Cajkova, University of St. Cyril and Methodius, SlovakiaCopyright © 2023 Bocok, Hinke and Abrham. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Josef Abrham, YWJyaGFtakBwZWYuY3p1LmN6

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.