Lei Wang

Lei Wang Jinzhe Yan

Jinzhe Yan

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 10 July 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1215866

This article is part of the Research Topic Sustainability of Digital Transformation for the Environment View all 16 articles

Introduction: In the digital economy, digital transformation (DT) is a deliberate decision to improve organizational procedures, alter production processes, introduce precision marketing, and more, ultimately impacting how well businesses innovate. This is why the current article investigates the effect of DT and the firm’s innovation performance and the boundary condition of corporate social responsibility (CRS).

Method: This study proposed a conceptual research model for the effect of DT on innovation performance and discussed the boundary condition of CRS. We collected China’s listed A-share firms’ data to examine the proposed hypotheses statistically. After Hausman test, the current study adopted fixed-effect regression, examined the heterogeneity issues resulting from different industry classifications, and robustness test for the correctness of the results.

Results and Implications: The following main conclusions are drawn: 1) DT can significantly enhance product innovation performance; 2) DT can significantly improve process innovation performance; 3) There is a time lag effect on the innovation performance (both product and process innovation performance) of the previous period on the innovation performance of the current period; 4) CSR positively moderates the role of DT on innovation performance; and 5) The impact of DT is heterogeneous across industries and patent. This study not only enriched the literature on DT and innovation performance but also provided the guidelines to promote digital transformation at the firm level.

Digital transformation (DT) is causing a wave of change in countries and industries worldwide. Digital technology is commonly used to transform corporate development and promote high-quality corporate development, especially concerning sustainability goals.

The literature on enterprise digitalization focuses on essential digitalization theory, digital capabilities, DT, the impact of digitalization on enterprise performance, and the underlying mechanisms of action. DT and digitalization are fundamentally different. Hess et al. (2016) hold that digitalization converts information from an analog to a digital format, whereas DT is the digital change that technology brings. Kim et al. (2011) believe that the digitization (capability) level reflects the ability of information-based technical facilities, human resources, and comprehensive management. DT is the use of recent digital technologies (e.g., social media, mobile technology, analytics, or embedded devices) by corporations to realize important business enhancements, improve client expertise, optimize operations, or create new business models (Fitzgerald et al., 2014). Within an enterprise, DT is outlined as an associate structure amendment toward big data analytics, cloud computing, social media platforms, and so on (Kane, 2017).

The current literature on DT focuses on three areas: 1) Business transformation, 2) technology as a driver of DT, and 3) institutional and social impact. Business transformation is the foundation of DT; it focuses on the effect of DT on business systems, where digital technology affects not only the transformation of merchandise, business processes, or sales but conjointly the whole business model (Hess et al., 2016). Research on business transformation covers two main areas: business combination and structure modification. Existing studies on business portfolios focus on strategy, and experimentation and implementation of digital technologies alone are insufficient to achieve transformation because a digital strategy must also be developed (Sebastian et al., 2017). The DT process must combine a company’s multiple practices with all its strategies, including digital, business, and information technology (IT) business strategies (A. Bharadwaj et al., 2013; Matt et al., 2015). The DT process for organizational change can be analyzed through the lens of resource theory. Liu et al. (2011) developed the resource matching theory by combining the resource base theory and strategic matching perspective. New technologies are the driving force behind DT, which profoundly affects the existing structures. IT investments are critical for business performance (Gerth and Peppard, 2016). Sebastian et al. (2017) consider how social technologies, mobile technologies, cloud computing, and IT are new digital technologies. White (2012) proposes four ideal digital technologies: mobile, big data, cloud computing, and search-based applications. In addition to new technologies and business models, DT depends on how society innovates and becomes more open, collaborative, and global (Bogers et al., 2018). Hinings et al. (2018) believe that the era of DT demands new theories that successively lead to institutional modification. Zhang et al. (2022) tested the relationship between digital transformation and corporate sustainability. Li and Fei (2023) suggested that DT is positively associated with a firm’s performance and network embeddedness plays a mediation role.

The idea of social responsibility was first introduced in the early 1950s. Bowen (1953) presents specific concepts concerning corporate social responsibility (CSR)—that business people’s choices and actions affect their stakeholders, employees, and customers, which in turn directly impacts the life standard in society as a whole. In the 1960s, mainstream academic thinkers argued that social, economic, and political changes pressured business people to reexamine their social roles and responsibilities. In the 1970s, social movements and new legislation influenced the understanding of CSR. In the 1980s, the international community became progressively conscious of environmental protection and property development and, indirectly, of company behavior. In the 1990s, major international events influenced the international community’s view on social responsibility and sustainable development. In celebration of the year 2000, the global organization called General Assembly was established, giving businesses a wider variety of responsibilities concerning human and labor rights, the environment, anti-corruption, and property development. In the 2010s, the Paris Agreement and the adoption of the “Property Development Goals” in 2015 ushered in a new accord. During this period, the literature on CSR focused on the impact on the performance of specific sectors, organizations, and industries that can be linked to the SDGs and generate shared values. Porter and Kramer (2011) claim that traditional, limited corporate methods, which frequently overlook the broad elements that affect their long-term success, are partly to blame for the need to produce shared value Based on the literature on greenhouse gas reduction (Sebos et al., 2020), carbon (Sebos, 2022), and air pollution (Progiou et al., 2023), we supposed that Greenhouse gas reduction is the outcome of digital transformation, a bridge linking digital transformation and CSR(Wu et al., 2023).

In academia, there are two main themes regarding CSR. One is that CSR has four dimensions: economic responsibility, obligation, moral responsibility, and philanthropic responsibility (Carroll, 1991). In addition, Elkington and Rowlands (1999) hold that CSR should include economic, social, and environmental responsibility; this is from a stakeholder perspective. Clarkson (1995) believes that all stakeholders (e.g., shareholders, employees, and consumers) must be involved in the business development process, meaning that companies are accountable to all stakeholders. The existing literature on the drivers and behavioral outcomes of CSR presents different research findings. Academics investigate the factors that drive CSR behavior from institutional, organizational, and individual levels. Campbell (2007) claims that CSR comes from the pressure of mandatory policies set by government departments and related organizations. Competition and learning among companies, the corporate mission, organizational culture and identity, the governance structure, business strategy, or trade orientation promote CSR (Khan et al., 2013; Schultz et al., 2013; Abhinav et al., 2017). Companies respond to increased malpractice risk by strategically increasing their investment in employee-related CSR (e.g., work and life wellbeing, health and safety policies, etc.; Flammer and Luo, 2017). For CSR to serve the interests of shareholders, important resources must be invested early on, as the benefits of CSR activities can only be collected once the CSR threshold has been met (Nollet et al., 2016). Cho and Tsang (2020) emphasize the importance of considering a company’s product strategy when evaluating CSR investments.

Drucker (1993) believes that innovation is a recombination of entrepreneurs’ production factors and conditions. Schumpeter (1982) proposes that innovation includes product innovation (manufacturing of new products or transformation of old products), technological innovation (adoption of new production processes), organizational or institutional innovation (adoption of new organizational forms), market innovation (exploration of new markets), and resource allocation innovation (search for new supply markets). Rochford and Rudelius (1997) consider that innovation performance (IP) is the degree of innovation of improved and new products resulting from a firm’s innovation activities. IP involves the entire process of generating a new concept, developing a new product from the new concept, and introducing the product to the market (Ernst, 2001). Sosik et al. (2012) consider the value of corporate innovation brought by corporate add-on products and pioneering product innovation as corporate IP. IP is also considered the result of the output and the improvement of production efficiency after the firm has invested certain resources in the innovation system, including product innovation performance (PDIP) and process innovation performance (PCIP; Guler and Nerkar, 2012).

Studies on the factors influencing IP have primarily been conducted from macro and micro perspectives. From a macro standpoint, Ahuja and Katila (2004) highlight that one effective factor for enhancing a firm’s IP is a good regional environment, as the regional setting has an important impact on the firm’s IP. Lindič et al. (2011) evaluate the factors that influence IP and conclude that government assistance could help SMEs improve their IP. From a micro perspective, Butlin and Carnegie (2001) delineate the antecedents of IP, namely, an ambitious business agenda, clear goals, rules-based forms, intimacy with customers, leadership, structure culture, infrastructure, and certain skills. In addition, Felin and Hesterly (2007) find that IP was associated with the knowledge and behavior of the people who manage this knowledge. Rouse and Daellenbach (2002) acknowledge that data, strategy, technology, structure, and culture are the main determinants of IP.

Prior research verified the DT effect on enterprise performance (Li and Fei, 2023; Ren et al., 2023), Corporate Social Performance (Meng et al., 2022), corporate sustainability (Zhang et al., 2022). However, few researchers investigated the effect on innovation performance. Chen and Kim (2023) verified the relationship between DT and innovation quantity and pointed out the mediation mechanism of knowledge flows and innovation awareness. Li et al. (2023) analyzed the influence of DT on innovation performance by adopting a fixed effect model with a total number of patents. This study presumed that DT could improve business capabilities, production, and management and help enterprises cross the “digital divide,” enabling them to operate efficiently and highlight their core competitiveness. White (2012) believes that economic integration could be achieved through digital processes and collaboration tools. Bouncken and Barwinski (2021) argue that DT should be incorporated into existing business views as this process involves technological amendments. Companies should not only rely on DT to enhance innovation capabilities but also take the initiative to assume greater social responsibility. Therefore, this study proposes that DT positively affects a firm’s IP and that CSR moderates the relationship between DT and IP.

This study provides the following potential contributions. Firstly, unlike DT literature, this study classified the innovation performance into product and process innovation performance, which enriched the literature on DT and innovation performance. Secondly, we introduced the CRS as a moderation variable. Finally, this study also investigated the multiplicative effect of DT and IP considering the heterogeneity of industry and ownership, using panel threshold regression, which is meaningful in constructing and improving the innovation theory of Chinese-listed companies.

According to Guler and Nerkar (2012), IP is the increase in productivity (including PDIP and PCIP) exhibited after the input of resource elements into the firm’s innovation system. We elaborate on both PDIP and PCIP below.

Scholars agree that to realize economic gains from process innovation, a mix of explicit and tacit new knowledge is necessary (Un and Asakawa, 2015). Un and Asakawa (2015) confirm that data should be rigorously embedded in a firm’s structure and technological systems to develop process innovation. Companies must acquire and assimilate internal and external information, reorganize existing and recently nonheritable information, and apply the remodeled information to their operations (Jansen et al., 2005). Theory of knowledge scholars expect firms to be able to assimilate external information (Zahra and George, 2002). A seamless flow of production-related details is generated through digitization, such as system access to external information, technology systems for enterprise resources coming up, offer chain management, or client relationship management. Data are generated to make production process issues visible in the manufacturing process and thereby improve the transparency of process operations and performance (Hendricks et al., 2007). PCIP can be positioned as a firm’s resource endowment (Sorescu et al., 2003). According to enterprise resource theory, in dynamic economic conditions, applying digital technologies in DT will improve the exploitation of resources, which would then enhance the ability of corporations to introduce and gain a proprietary competitive advantage (Henfridsson et al., 2018). According to process reengineering theory, companies improve their business performance by introducing digital information technology, which works backward within the organization and the workflow to help develop new products, organizational processes, and services (Scuotto et al., 2017). It simplifies corporate communication and organizational structure (Moeuf et al., 2020). A commitment to digitalization facilitates communication between companies and access to new kinds of information and related resources, which is believed to enhance firm IP (Parida et al., 2012). Liang and Li (2022) divided the innovation performance into PCIP and PDIP and verified DT promotes both PCIP and PDIP. Based on the analysis above, we propose the following:

H1:. DT positively affects PCIP.

Companies actively exploit the Internet, big data, artificial intelligence (AI), and alternative digital technology to innovate manufacturing processes and comprehensively improve product design, manufacturing practices, and management (Kang et al., 2016). In the digital economy, digitizing merchandise and services has become a serious means for corporations to achieve a competitive advantage. Companies that believe in digital products and services tend to maintain a good position in a competitive market (Frank et al., 2019). Regarding product–service innovation, companies provide advanced services, such as research and development (R&D), centered around a collaborative research process with customers to improve products and services to meet continuous customer needs through close interaction (Baines and Lightfoot, 2014). Kohtamäki et al. (2013) emphasize the tempering result of network capability (network management capability, network integration capability, and network learning capability) on product innovation. Strong information-learning capabilities allow firms to accumulate new skills and resources and integrate knowledge into internal capabilities to supply innovative merchandise, develop new product markets, cut R&D prices, and improve IP (Lew et al., 2013). According to stakeholder theory, for a company to achieve its product and service innovation goals, it must balance the conflicting interests of its contractual stakeholders as a whole, including management, general employees, shareholders, suppliers, regulators, and consumers. The government, as a regulator, requires companies to comply with environmental, policy, and regulatory requirements, which puts pressure on companies to innovate (Berchicci and King, 2007). Requests from customer provide information about their expectations for new merchandise and processes (Laforet, 2008). Suppliers and departments that are directly affected by the innovation can serve as co-creators or producers of the innovation (Yeniyurt et al., 2014). Liang and Li (2022) divided the innovation performance intwo PCIP and PDIP and verified DT promote both PCIP and PDIP Considering the studies discussed above, we propose the following:

H2:. DT has a significant positive impact on PDIP.

This study examines the differential impact of DT on IP from two perspectives: the nature of the firm’s equity and the type of industry.

Brynjolfsson (1993) finds that IT investment within the service sector had a considerably higher result on firm performance than that within the manufacturingsector. Tippins and Sohi (2003) believe that IT capabilities indirectly affect the performance of manufacturing companies. The ability to integrate the enterprise may generate important improvements in business performance with the IT chain (Rai et al., 2006). Parsons et al. (1990) believe that IT has an important contribution to the development of the banking industry. Franks (2012) consider that the emergence of mobile payment services has not significantly impacted financial markets and that the ease of payment has not led to an increase in the number of market investors. Previous studies indicated that the manufacturing industry typically uses digital technology to create digital production lines and digital factories to improve the efficiency of enterprise production and operation, and non-manufacturing enterprises strengthen their capabilities in areas such as predictive analytics and merchandising management through digital infrastructure, digital processes, and digital marketing.

According to the equity nature of enterprises in China, enterprises are categorized as state-owned enterprises (SOEs) or non-state-owned enterprises (NON-SOEs, including private enterprises, foreign-funded enterprises, and mixed enterprises). In China’s socialist market economy environment, the system is favorable to the development of SOEs (Zheng and Scase, 2013). SOEs are more likely to receive financial support through loan guarantees or government policies (Cui and Jiang, 2012). By contrast, NON-SOEs have limited access to financial aid and lack an intermediary for DT. In the process of digitalization, a big gap exists in the resources obtained by SOEs and NON-SOEs, and the resource difference determines the speed and level of their digitalization. In a socialist market economy, SOEs, which typically have more resources, have higher levels of digitization, whereas NON-SOEs may have lower levels. Accordingly, we propose the following:

H3:. The impact of DT on IP is heterogeneous across industries and state ownership.

According to the synergy effect, the interaction or cooperation of two things gives rise to a whole that is greater than the simple sum of its parts. Digitalization alone cannot successfully provide companies with a competitive advantage. Still, it can be useful in resource integration for purposes of CSR and sharing of business practices and specific resources, which gradually would help in forming an irreplaceable overall system and improving the IP of companies. Forcadell et al. (2020) note that corporate sustainability and digitalization are increasingly important to businesses, society, and policymakers worldwide. The combination of corporate sustainability and digitalization can enhance each other’s strengths, thereby producing better results. According to the theory of corporate resources, companies can increase their digital innovation investment and PCIP by continuously absorbing new knowledge regarding social responsibility, creating a corporate culture that actively fulfills social responsibility, and fostering an atmosphere and mechanism for continuous innovation (Carrasco-Monteagudo and Buendía-Martínez, 2013). According to stakeholder theory, the relationship between a company and its stakeholders can be better maintained through CSR, leading to a wide and deep social relationship network (Lončar et al., 2019). Access to information, skills, and resources that are necessary for digital activities can reduce innovation costs and facilitate DT (La Rosa et al., 2018). Based on the discussion above, we propose the following:

H4:. CSR positively moderates the relationship between DT and PCIP.

By engaging in socially responsible practices, companies could attract social and governmental capital and reduce the financing constraint of DT and maintain an honest image and establish products and production processes that satisfy market demand (Katmon et al., 2019). According to stakeholder theory, higher levels of investor social responsibility indicate that firms value communication with stakeholders and reduce the cost of developing innovative merchandise (Eccles et al., 2012). Management’s practices of social responsibility toward internal stakeholders will considerably affect funding constraints. By contrast, social responsibility toward external stakeholders will alleviate the pressure of funding constraints and allow the allocation of additional funds to digital product transformation (Jianfei and Yun, 2019). Moreover, shareholders’ fulfillment of social responsibility enhances the company name. This creates an honest company image, and the higher the company’s reputation, the lower the cost of equity capital the company faces, and thus, the more it invests in digitalization (Lin-Hi and Blumberg, 2018). By increasing the recognition and social involvement of the company’s employees, the firm would be able to attract the best employees and improve its level of digitalization, thereby enhancing its PDIP. Managers ought to specialize in coaching and recruiting staff with various business skills and a sense of responsibility (Groysberg and Lee, 2009). Strong learning capabilities and responsible practices help corporations accumulate new skills and resources and integrate them into internal capabilities to provide an innovative product, develop new product markets, cut back on R&D costs, and improve IP (Lew et al., 2013). How businesses operate is influenced by environmental, social, and economic trends, and DT will affect the business models (Chandola, 2015). DT considerably contributes to reducing waste emissions and enhancing environmental protection, leading individuals to unravel existing issues and address them in environmentally friendly ways (Feroz et al., 2021). Based on the analysis above, we propose the following:

H5:. CSR positively moderates the relationship between DT and PDIP.

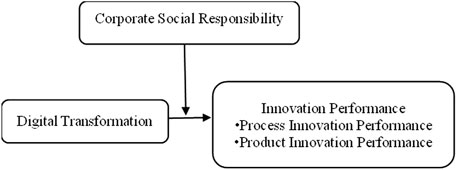

The research model is presented in Figure 1 below.

FIGURE 1. Research model.

We selected Chinese A-share listed enterprises from 2010 to 2019 and obtained their data from the China Stock Market and Accounting Research (CSMAR) database. The data for the DT variables came from the annual reports of enterprises from 2010 to 2019, collected through CNINF and examined using Python for keyword text analysis. The data for the CSR variable were obtained from the China Hexun database on professional measurements of listed companies. Subsequently, enterprises belonging to the ST, ST*, and finance sectors were excluded. Finally, to mitigate the influence of outliers on the regression results, this study winsorized all continuous variables at the 1% and 99% levels. Panel data for 950 sample companies were included in the analysis.

Innovation Performance (IP). According to the previous analysis, IP promotes technological innovation, including PCIP and PDIP. PCIP concerns the application of new or improved corporate manufacturing business processes, whereas PDIP involves developing and producing new products. Following Jimenez-Jimenez and Sanz-Valle (2008), we measured PCIP in terms of annual innovation investment as a percentage of operating revenue and PDIP in terms of the number of patent applications (including invention, utility model, and design patents). To highlight the innovation of invention patents, weightings of 30% for invention patents, 20% for utility model patents, and 10% for design patents were assigned, and the resulting values were then summed up.

Digital Transformation (DT). Following Chun et al. (2021a), we compiled the annual reports of A-share listed companies on the Shanghai and Shenzhen exchanges through a Python tool to search, match, and count the word frequency of feature words from the data, sum up the word frequencies of key technology directions, and construct an index system for DT. For robustness testing, drawing on Huaijin et al. (2020), the degree of annual change in the digital economy as a percentage of total intangible assets (DT_R) was used as a proxy variable to validate DT on PCIP. To validate DT on PDIP, we used the sum of the number of uses of DT (AI technologies, blockchain technologies, cloud computing technologies, big data technologies, digital technology applications) of listed companies from the CSMAR database (DT_RN) as a proxy variable.

Based on stakeholder theory and drawing on the research of Zuanyong and Dian (2021), we adopted the professional CSR measurement index system of China Hexun for listed companies to measure CSR fulfillment comprehensively.

Based on Zhu and Jin (2023) and Zuo et al. (2021), this study set business growth, enterprise scale, gearing ratio, cash flows from operating activities, scales cost ration, return on total assets, board, Corporate equity concentration, nature of shareholding, number of years in the market and industry as control variables.

Business growth (GRO). The purpose of company growth analysis is to observe the event of a company’s business capability exceeding an explicit amount. Therefore, the growth magnitude relation is a vital indicator of the company’s development rate.

Enterprise scale (SIZE). The growth of innovation activity tends to rise gradually with the firm’s size (Acemoglu and Linn, 2004). The size of an enterprise reflects its capability in product production or mounted assets for production and operation. We used the Napierian logarithm of total assets to measure this variable (Vij and Farooq, 2016).

Gearing ratio (GER). This indicator reflects the proportion of creditors’ assets in the enterprise’s total assets; it indicates the peril of using creditors’ credit facilities as well as the enterprise’s ability to boost debt.

Cash flows from operating activities (CFA). This indicator captures the cash flow generated from all the enterprise transactions and events other than investing and financing activities. We measured CFA by taking the Napierian logarithm of a company’s internet income from operations.

Sales cost ratio (SCR). The cost of goods sold ratio reflects a company’s cost of goods sold per unit of sales revenue and corresponds to the gross margin. An abnormally high cost of goods sold ratio indicates that a company is selling incorrectly or is in an unfavorable competitive position in the market. SCR = (Total profit/Total costs and expenses) × 100%.

Return on total assets (RTA). This indicator represents the listed company’s ability to use capital to generate profit, which may mirror aggressiveness, development ability, and comprehensive management ability.

Board size (BOS). Most studies indicate that the size of the board of directors has a vital impact on the company’s decision-making, access to external resources for development, the building of a decent company image, and effective management. We used the number of directors to capture this variable.

Corporate equity concentration (CEC). The concentration of equity is a quantitative indicator of whether the equity is concentrated or dispersed among shareholders. We measured this variable by taking the logarithm of the shareholding of the largest shareholder.

Nature of shareholding (NOS). The nature of equity denotes a company’s control through its shareholdings in a given company. The value is 1 if the enterprise is an SOE and 0 otherwise.

Number of years in the market (TIME). The number of years in the market is the period from the time of listing to the current time, which we measured by subtracting the present time from the listing time and taking the natural logarithm.

Industry (IND). The dummy variable for the industry is set as 1 for manufacturing and 0 for non-manufacturing.

To verify the hypotheses, we employed the economic models described below.

In Eq. 1, subscripts

To investigate the moderating role of CSR, we added the CSR and the interaction term of DT and CSR to the benchmark model.

In Eqs 2, 3, subscripts

The descriptive statistics analysis shows that the dependent variable PCIP has a maximum value of 0.244, a minimum value of 0, a mean value of 0.044, and a standard deviation of 0.042, indicating little difference in the PCIP of the sample of listed companies. The maximum value of the independent variable DT is 538; the minimum value is 1; the mean value is 66.118, and the standard deviation is 101.71, indicating a large gap in the degree of DT in the sample. From the robustness test, the maximum value of the proxy variable (DT_R) is 1; the minimum value is 0; the mean is 0.089, and the standard deviation is 0.182, indicating a wide variation in the percentage of the digital economy in the total intangible assets of listed companies. The maximum value of the moderating variable CSR is 76.015; the minimum value is −2.6; the mean is 25.928 and the standard deviation is 16.741, with some but no significant differences among samples (See Supplementary Table S1).

For an initial test of the role of DT on PCIP, Pearson correlation analysis was conducted on the key variables, and the results are shown in Supplementary Table S2. The dependent variable PCIP shows a positive relationship with the independent variable DT and the robustness test proxy variable (DT_R) and a negative relationship with the moderating variable CSR. To examine further the issue of multicollinearity among the main variables, the variance inflation factor (VIF) was tested for all explanatory and control variables, and we found that the maximum VIF value is 1.95 and the mean value is 1.36, suggesting no covariance problem in the model.

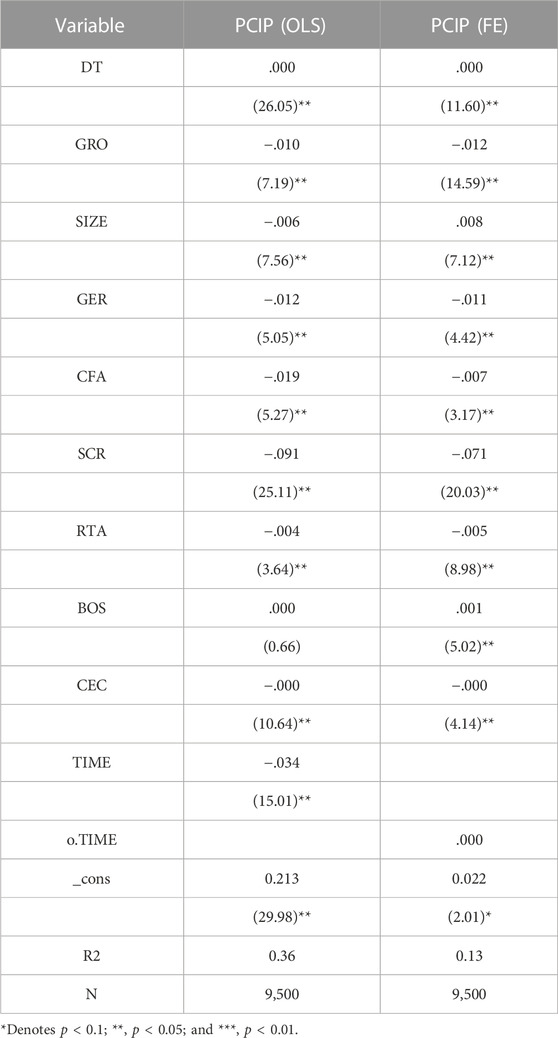

To test the role of DT on PCIP, a mixed ordinary least squares (OLS) regression approach and panel data regression were used for empirical testing. Before conducting the panel data regressions, we administered a Hausman test to determine whether to use a fixed or random effects model. As Prob > chi2 = 0.0000, the difference between the fixed and random effects was significant, favoring the fixed effects model. Table 1 combines the OLS and panel data regression results.

TABLE 1. OLS Regression vs. Fixed Effects Regression.

Table 3 shows that DT significantly positively affects PCIP in both the OLS and fixed effects regressions, thus verifying H1. However, in terms of the degree of explanation, the OLS regression (t = 26.05) surpassed the fixed effects regression (t = 11.6), indicating that a fixed effects model fixes some factors, thus giving a slight reduction in explanatory power. Nevertheless, both results are significant at the 5% level and do not reach the 1% level of significance, indicating that the degree of DT of Chinese listed companies needs further improvement.

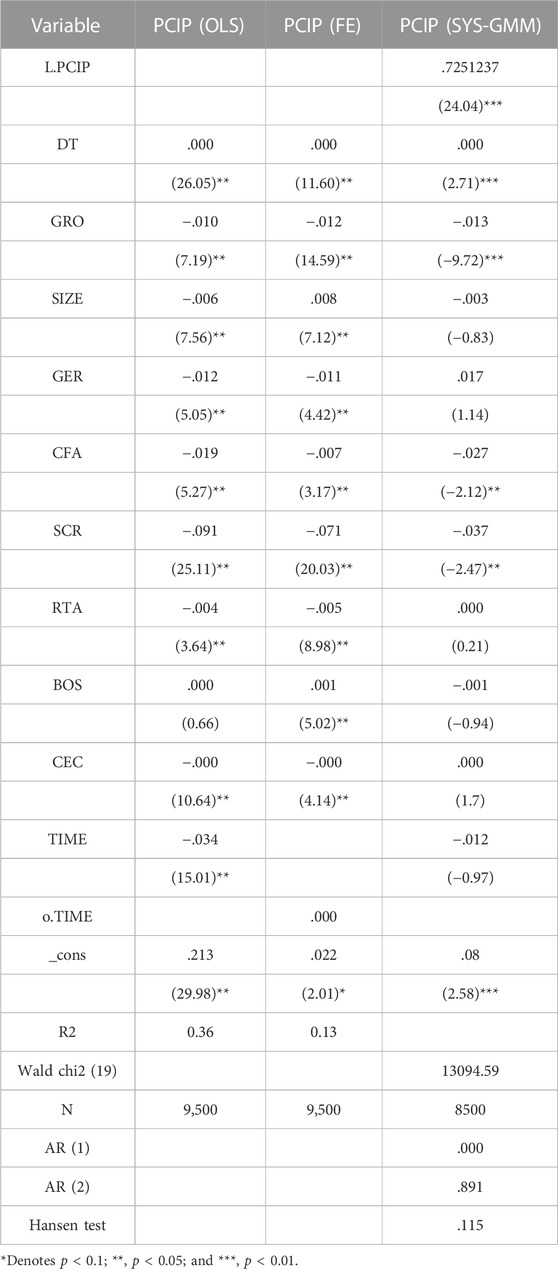

DT can significantly improve PCIP, and PCIP has a continuity feature; that is, the PCIP in the previous period may impact the PCIP in the current period. In addition, owing to the many factors that affect PCIP, the problem of omitted variables is inevitable when constructing the empirical model, which causes endogeneity issues. To deal with the aforementioned two endogeneity issues, we used the system generalized method of moments (SYS-GMM) to empirically test the relationship between prior- and current-period PCIP and then compare the results of the OLS, fixed effects, and SYS-GMM regressions. Table 2 displays the test results.

TABLE 2. Comparison of OLS, FE, and SYS-GMM.

In Table 4, the SYS-GMM results show that the PCIP lagged by one period has a significant positive effect on the current period and passes the 1% statistical significance level test. AR (1) = 0.000 < 0.05 and AR (2) = 0.891 > 0.1, which indicates a first-order autocorrelation and no second-order autocorrelation for the random disturbance term. The Hansen test value = 0.115 > 0.1 indicates that the model does not have an over-identification problem and that the overall model is well estimated. After controlling for endogeneity, DT still has a significant positive effect on PCIP; hence, H1 is further supported. The analysis above reveals that PCIP has a certain lag and long-term nature, which suggests that the benefits of PCIP are uncertain and that PCIP transmission requires some time.

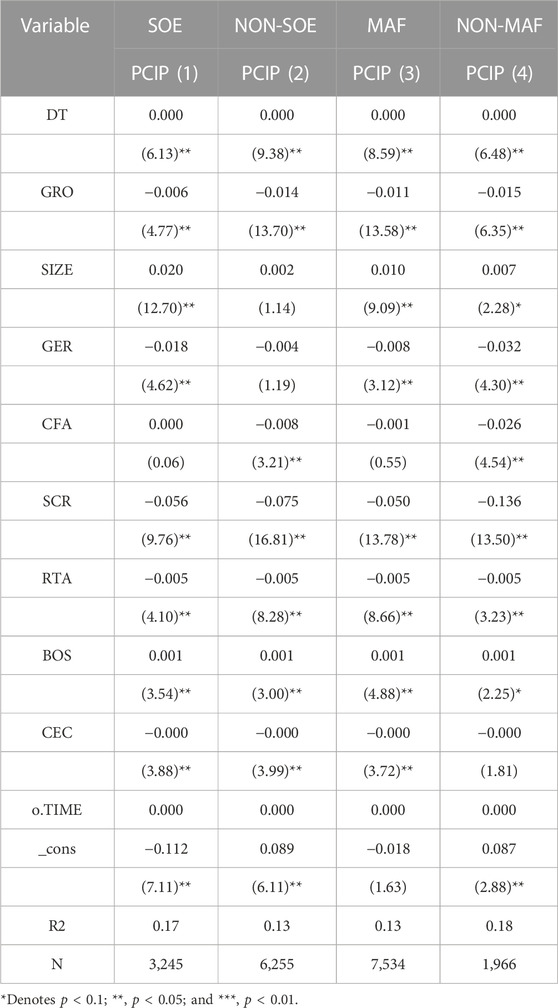

Are there differences in the performance of DT on PCIP across industries and by the nature of equity? Drawing on Lau et al. (2016), we divided the study sample into four subsamples: Manufacturing (MAF), non-manufacturing (NON-MAF), state-owned enterprises (SOE), and non-state-owned enterprises (NON-SOE), and used a panel fixed effects approach for group testing and likelihood uncorrelated estimation. We found significantly different random disturbance terms, allowing for coefficient comparisons. Table 3 shows the test results.

TABLE 3. Heterogeneity test results.

As shown in Table 3, the DT of both SOEs and NON-SOEs significantly positively affect PCIP. Furthermore, a comparison of the regression coefficients and t-values shows that the DT of NON-SOEs is more likely to promote PCIP than that of SOEs; hence, H3 is verified. Similarly, manufacturing firms show a significant positive effect on PCIP compared with non-manufacturing listed firms, and the comparison of regression coefficients and t-values shows that manufacturing firms are better able to promote PCIP than non-manufacturing firms, with a 5% statistical significance, thus verifying H3.

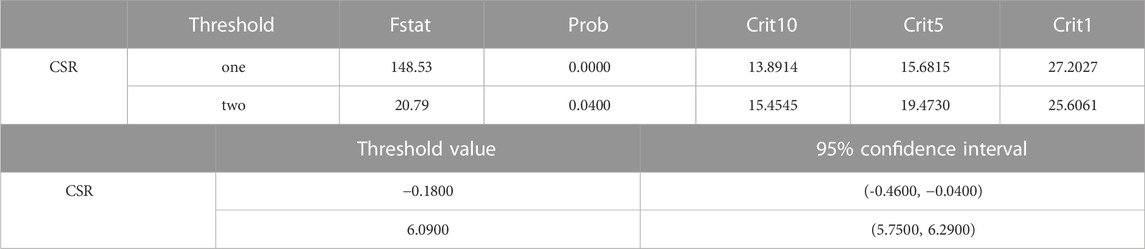

To drawing on Hansen (1999), we conducted Bootstrap sampling by iterating the estimation process 1,000 times to determine whether a threshold exists. Table 4 shows the results, from which the following conclusions can be drawn. The F-statistic is significant at the 5% level for both the one- and two-threshold models; that is, the p-value is less than 0.05, suggesting that there are two thresholds in the model. Table 4 presents the results of the specific threshold estimates, which are −0.18 and 6.09. That is, the moderating variables are treated in three segments in conjunction with the number-for-transformation, namely, the first segment: CSR ≤ −0.18; second segment: −0.18 < CSR ≤ 6.09; and third segment: CSR > 6.09.

TABLE 4. Threshold effect test.

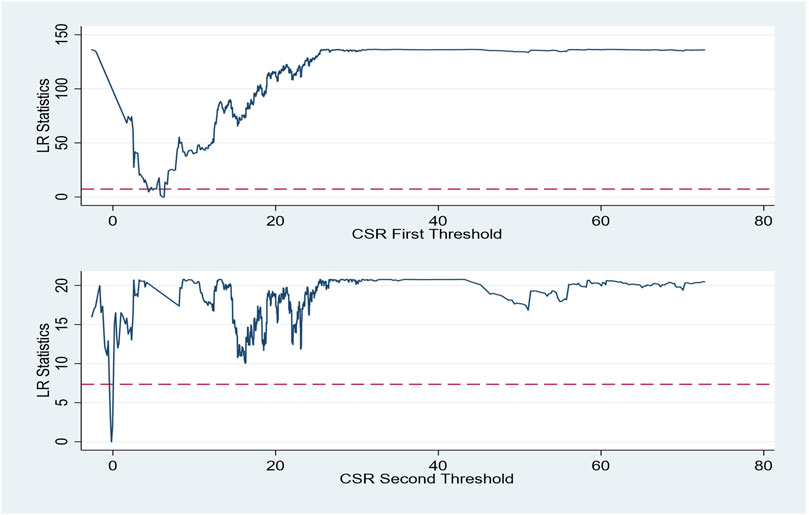

Figure 2 plots the existence of the two threshold estimates of CSR; it specifically shows the likelihood ratio function at a 95% confidence interval for the two thresholds of −0.18 and 6.09.

FIGURE 2. Threshold estimation chart.

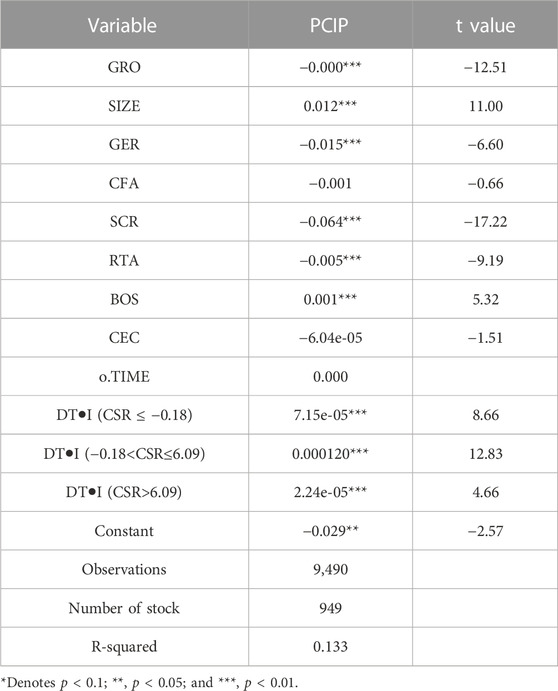

We further obtained the results of the panel threshold regressions along with the derived threshold values (see Table 5). Table 5 shows that the interaction between DT and CSR is split into three segments. In the first segment, the regression coefficient of DT•I (CSR ≤ −0.18) is 7.15e-05, and the t-value is 8.66, which is significant at the 1% level; that is, when CSR ≤ −0.18, the DT and CSR interaction has a significantly positive effect on PCIP. In the second segment, the regression coefficient of DT•I (−0.18 < CSR ≤ 6.09) is 0.000120, and the t-value is 12.83, which is significant at the 1% level; that is, when −0.18 < CSR ≤ 6.09, the effect of the interaction between DT and CSR on PCIP is also significantly positive. In the third segment, the regression coefficient of DT•I (CSR > 6.09) is 2.24e-05, and the t-value is 4.66, which is significant at the 1% level; that is, when CSR > 6.09, the effect of the interaction between DT and CSR on PCIP is still significantly positive. In addition, although the interaction of all three segments of CSR and DIT are significantly positive for both enterprise PCIP, the effects differ. From the magnitude of the regression coefficients and t-values, it can be judged that the interaction effect of the first segment is smaller than that of the second segment, and the interaction effect of the second segment is larger than that of the third segment. These results signify a process of first strengthening and then weakening. In summary, the interaction between DT and CSR is significantly positive on PCIP, which verifies H4.

TABLE 5. Panel threshold regression estimation.

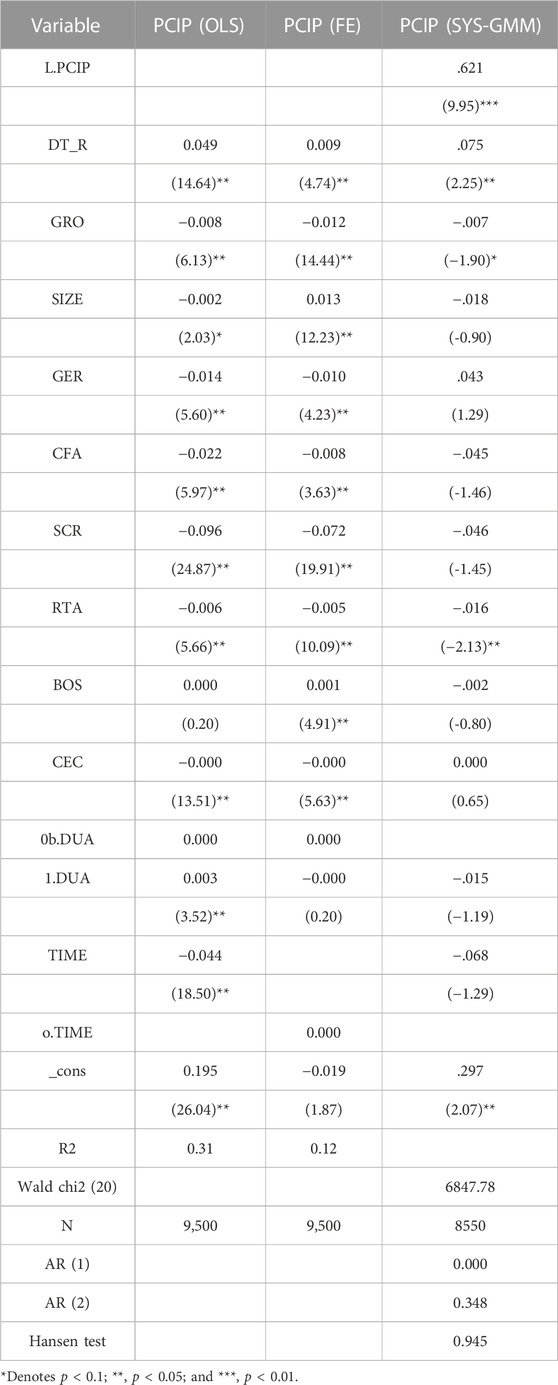

To examine the robustness of the study findings, we conducted robustness tests in two ways. The first was by replacing the explanatory variables. We replaced the independent variable DT with the proportion of the digital economy-related portion of the year-end intangible asset to total intangible assets (DT_R). The second was by adding a control variable (DUA), which indicates when one person is both a member of the board of directors and the general manager. After repeating the regression analysis discussed above, Table 6 shows that in the OLS and fixed effects regressions, the proportion of the digital economy-related component to the total intangible assets (DT_R) has a significant positive effect on PCIP. In the SYS-GMM model, the lagged one-period PCIP has a significant positive effect on the current period. Moreover, the proportion of the digital economy-related component to the total intangible assets ratio (DT_R) has a positive and significant effect on PCIP: AR (1) = 0.000 < 0.05; AR (2) = 0.348 > 0.1, which indicates the existence of first-order autocorrelation and no second-order autocorrelation for the random disturbance term. Furthermore, the Hansen test value equals 0.945 > 0.1, indicating that the model does not have an over-identification problem, and the previous findings still hold.

TABLE 6. Robustness check results.

Supplementary Table S3 shows that the maximum value of the dependent variable PDIP is 1,294.5; the minimum value is 0; the mean value is 78.542, and the standard deviation is 178.7, indicating large differences in the PDIP of the sample of listed companies, and the fractional places in the maximum and mean values are due to winsorization. From the robustness test, the maximum value of the proxy variable DT_RN is 115.5; the minimum value is 0; the mean is 7.826, and the standard deviation is 18.982, which still indicate a large variation among samples. The presence of fractional places in the maximum and mean values are also due to winsorization. The descriptive statistics of the independent variable DT and the control variables have been described in the discussion of the empirical evidence of DT on PCIP and will not be repeated in this section.

To examine the impact of DT on PDIP, we conducted a Pearson correlation analysis on the variables, the results of which are shown in Supplementary Table S4. The dependent variable PDIP has a positive relationship with the independent variable DT, the robustness test proxy variable DT_RN, and the moderating variable CSR. We also conducted the variance expansion factor test and passed it.

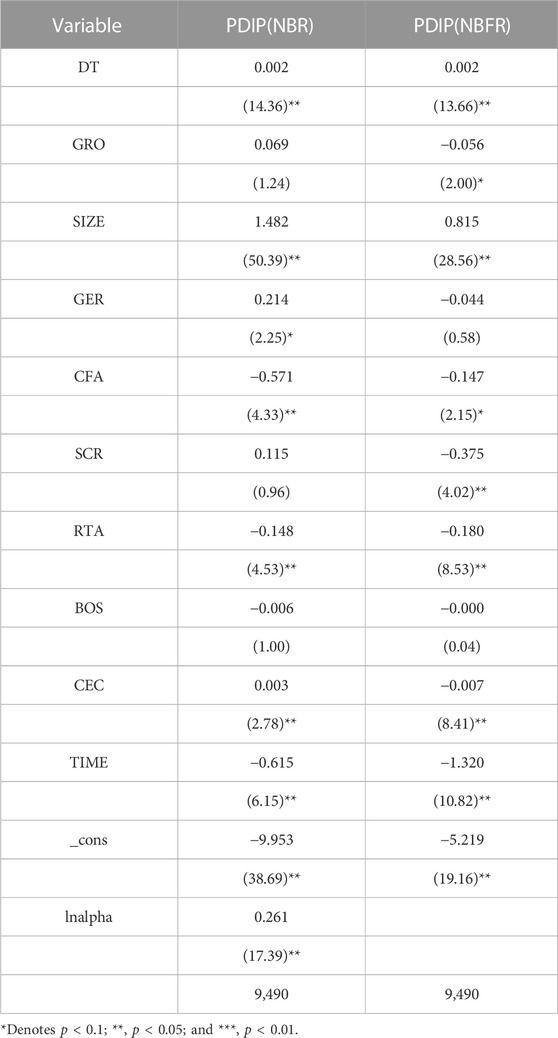

With reference to the previous study, we used negative binomial regression (NBR) and negative binomial panel regression for empirical testing. We initially conducted a Hausman test to determine whether to use negative binomial panel fixed effects regression (NBFR) or negative binomial panel random effects. As Prob > chi2 = 0.0000, the difference between fixed and random effects is significant, which favors the fixed effects model. The results of the two regressions are combined in Table 8.

Table 7 shows that in the NBR model, DT has a significant positive effect on PDIP with lnalpha = 0.261 and z = 17.39 ≠ 0; these results prove that the model is well structured. In the NBFR model, DT also significantly impacts PDIP, thus verifying H2. However, there is a difference in the degree of explanation, with z = 14.36 for DT in the NBR versus z = 13.66 for the NBFR.

TABLE 7. Comparison of regression results.

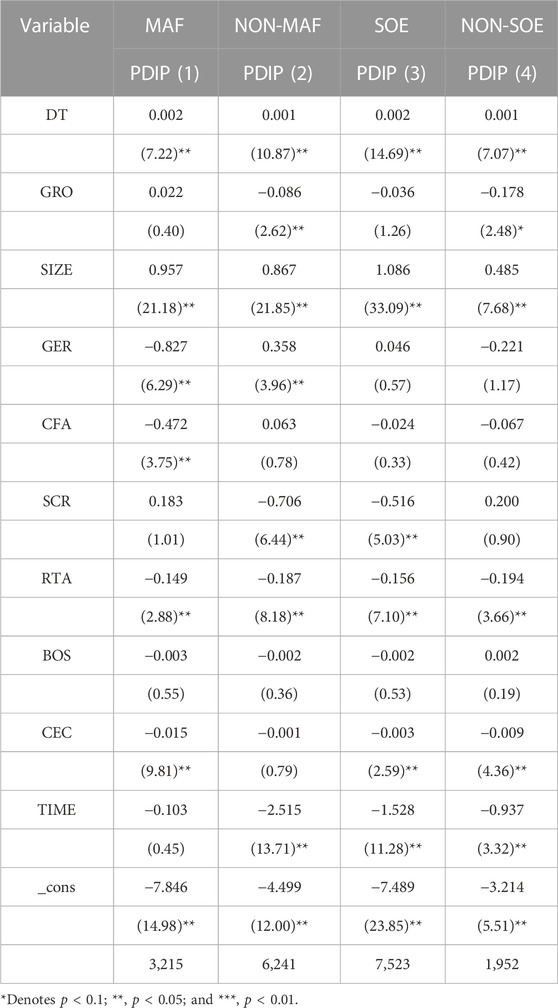

To explore the impact of DT on PDIP under different equity natures and industries, we divided the study sample into four subsamples: manufacturing (MAF), non-manufacturing (NON-MAF), state-owned enterprises (SOE), and non-state-owned enterprises (NON-SOE), following the procedures explained above. Grouping tests and seemingly uncorrelated estimation were performed using negative binomial stationary regression, and random disturbance terms were found to be considerably completely different, permitting constant comparisons. Table 8 shows the test results.

TABLE 8. Heterogeneity test.

As shown in Table 8, DT has a significant positive effect on PDIP for both SOEs and NON-SOEs, and from the comparison of regression coefficients and t-values, the DT of NON-SOEs is more effective than that of SOEs in promoting PDIP; hence, H3 is verified. In both MAF and NON-MAF classifications, DT has a significant positive effect on PDIP, which passes the statistical significance test of 5%. A comparison of the regression coefficients and t-values shows that the DT of MAF firms also promotes PDIP more than NON-MAF firms, thus verifying H3.

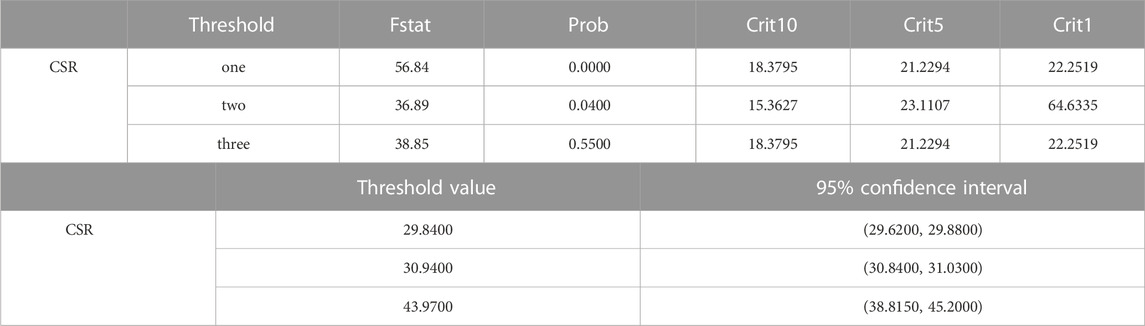

Following Hansen (1999), this study conducted Bootstrap sampling by iterating the estimation process 1,000 times to estimate three thresholds and two thresholds for CSR and determine whether a threshold impact exists. Table 9 shows the results, which lead to the following conclusions. The one-threshold F-statistic is significant at the 5% level; the two-threshold F-statistic is significant at the 10% level, and the three-threshold F-statistic is significant at the 1% level, which indicate that there are three thresholds in the model. Table 9 shows the results of the specific threshold estimates, which are 29.84, 30.94, and 43.97. The joint action of CSR and DIT is treated in four segments. For the first segment, CSR ≤ 29.84; for the second segment, 29.84 < CSR ≤ 30.94; for the third segment, 30.94 < CSR ≤ 43.97; and for the fourth segment, CSR > 43.97.

TABLE 9. Threshold effect test and threshold estimation.

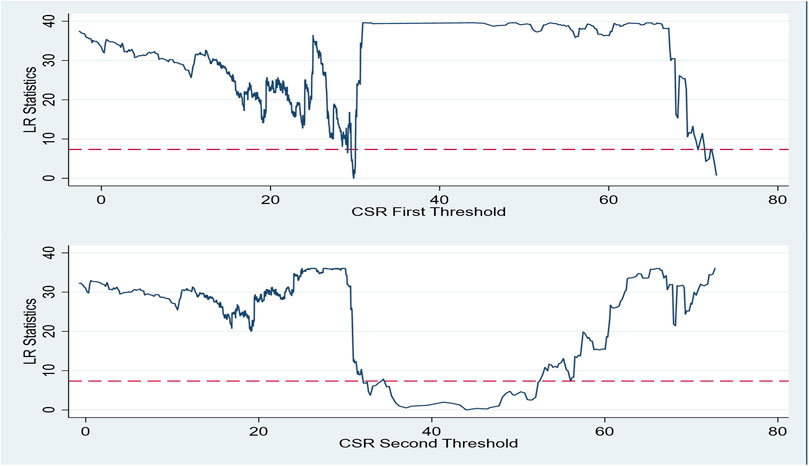

Figure 3 plots the likelihood ratio function at 95% confidence intervals for the three thresholds of 29.84, 30.94, and 43.97 and illustrates the presence of the three threshold estimates of CSR.

FIGURE 3. Threshold estimation chart.

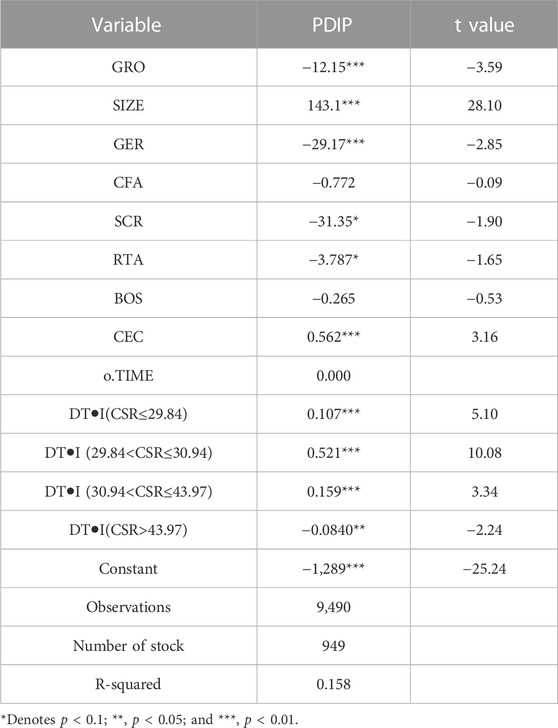

For further analysis, this study used panel threshold regression (see Table 10). Table 10 reveals that the interaction between DT and CSR is actually divided into four segments. For the first segment, the regression coefficient of DT·I (CSR ≤ 29.84) is 0.107, and the t-value is 5.10, which is significant at the 1% level; that is, when CSR ≤ 29.84, the DT and CSR interaction has a significantly positive effect on PDIP. For the second segment, the regression coefficient of DT·I (29.84 < CSR ≤ 30.94) is 0.521, and the t-value is 10.08, which is significant at the 1% level; that is, when 29.84 < CSR ≤ 30.94, the effect of the interaction between DT and CSR on PDIP is also significantly positive. For the third segment, the regression coefficient of DT·I (30.94 <CSR ≤ 43.97) is 0.159, and the t-value is 3.34, which is significant at the 1% level; that is, when 30.94 < CSR ≤ 43.97, the effect of the interaction between DT and CSR on PDIP is still significantly positive. For the fourth segment, the regression coefficient of DT·I (CSR > 43.97) is −0.0840, and the t-value is −2.24, which is significant at the 5% level, meaning that the interaction of DT and CSR has a significantly negative effect on PDIP when CSR > 43.97. Although in all three segments, CSR interacts with DT and has a significantly positive impact on PDIP, the effects differ. From the magnitude of the regression coefficients and t-values, it can be judged that the interaction of DT and CSR on PDIP is a process that first has positive effects, then the positive effects increase, and then gradually decreases until it finally becomes negative. Although the interaction between DT and CSR shows a significantly negative effect on PDIP when CSR > 43.97, its regression coefficient is equal to −0.084, whereas the interaction coefficients of the first three segments of DT are 0.107, 0.521, and 0.159, and the positive and negative effects are still neutralized after a positive effect. Therefore, in general, CSR positively moderates the role of DT on the PDIP, thus verifying H5.

TABLE 10. Panel threshold regression results.

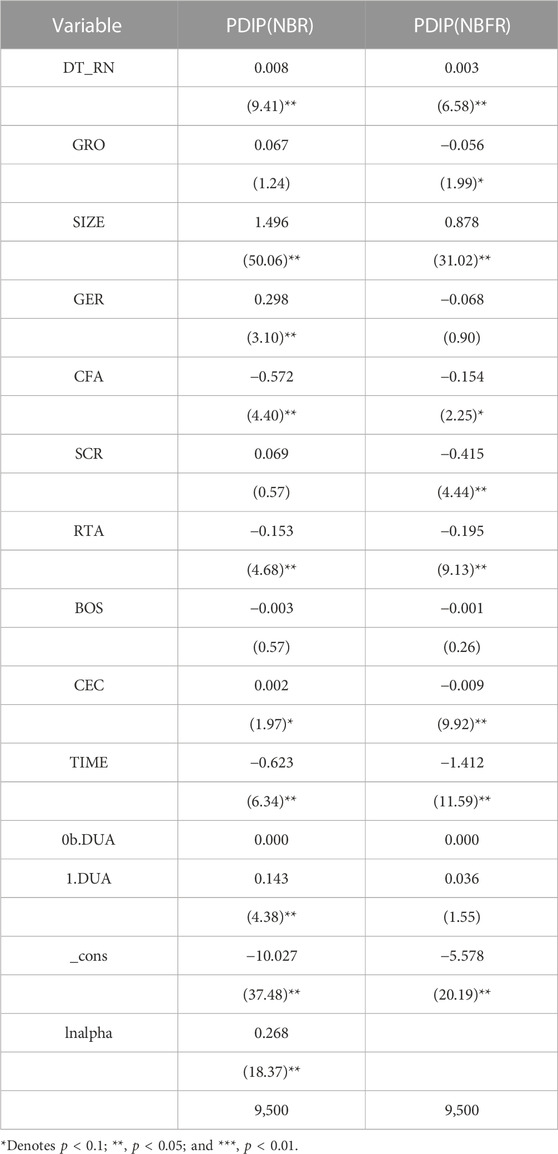

To examine the robustness of the findings, we conducted robustness tests by first replacing the independent variables. We replaced the independent variable DT with the sum of the number of times listed companies used the following: AI technology, blockchain technology, cloud computing technology, big data technology, and digital technology application, as indicated in the CSMAR database (DT_RN). Second, we added a control variable, DUA, which indicates when the same person holds the chairman and general manager positions. We then repeated the process described above and found that DT has a significant positive effect on PDIP in both NBR and NBFR; hence the previous findings still hold. The details are shown in Table 11.

TABLE 11. Robustness tests.

Based on resource theory, process reengineering theory, and stakeholder theory, this study investigated in depth the theoretical basis of DT, CSR, and IP. It analyzed the mechanism of DT’s impact on PCIP and PDIP, considering the role of DT on IP and the mechanism of CSR’s moderating effect on it. The inner logical relationships among DT, CSR, and IP were thus clarified. The impact mechanisms of DT, CSR, and IP were empirically tested using a combination of literature review and empirical testing using data from the CSMAR database and China Hexun data from 2010 to 2019. The following main conclusions are drawn: 1) DT can significantly enhance PCIP; 2) DT can significantly improve PDIP; 3) There is a time lag effect of the IP of the previous period on the IP of the current period; 4) CSR positively moderates the role of DT on IP; and 5) The impact of DT is heterogeneous across industries and ownership.

Li et al. (2023) measured the innovation performance using a total number of patents. This study not only measured the innovation performance at product and process level and used weight score (weightings of 30% for invention patents, 20% for utility model patents, and 10% for design patents). In line with Li et al. (2023), Chen and Kim (2023), our empirical finding suggested that the level of DT positively promotes innovation performance.

Regarding theoretical implications, by focusing on the impact of DT on IP, this study revealed the impact mechanisms, providing insight into the interaction and impact on IP. In addition, research on the dynamic effect of DT on IP is lacking, and this study filled this gap. This study also investigated the multiplicative effect of DT and IP considering the heterogeneity of industry and ownership, using panel threshold regression, which is meaningful in constructing and improving the innovation theory of Chinese-listed companies.

The results indicate that at the organizational level, the organizational structure should be re-optimized with the concept of digitalization to achieve a clear division of labor, clear functions, and authority and responsibility. First, the top management of the company should analyze the current industry in which it is located, including the characteristics of competitors and changes in the external environment, apply digital concepts, combine digital technology and the current business model of the company, and design an innovative ecology that is appropriate for the enterprise. Second, in the process of DT, enterprises should deploy and invest in the company’s organizational structure, business processes, and communication information technology. Finally, a relevant evaluation team should be established to assess the implementation plan and PCIP activities.

At the technical level, the leading innovation role of DT should be highlighted. Enterprises perform innovation activities, increase their investment in R&D, improve the investment mechanism of enterprise technology innovation, keep abreast with the advances in technology, modify the previous production mode, and make the production activities greener to realize environmental protection and higher efficiency. Emphasis should be placed on combining the interests of industries, academia, and the research environment, through the relationships among upstream, midstream, and downstream innovation to achieve a comprehensive application of technology, establish an open innovation system, focus on the set up of research platforms, promote high-quality scientific talent, update the configuration of production factors, and enhance the value of data applications.

At the market level, the first challenge is implementing balanced management of the inputs and outputs of digital transformation and minimizing the risks associated with digital transformation. Implement a goal management-oriented strategy, which means dividing the digital transformation into several projects, implementing the evaluation of the capital budget and goal achievement for each project, and confirming whether the set goals are completed after the project, and if they are completed, then a new extension project can be started, and if they are not completed, analyze the reasons for not completing them, and if necessary, terminate them. In addition, to take advantage of the zero-distance role between digitalization and market information, companies and consumers should maintain efficient communication, in-depth understanding of consumer habits, rapid response to customer needs, provide customized products and services for consumers, establish consumer value identity and brand identity of the product, and improve consumer loyalty.

Firstly, regarding the dimensional division of IP, this study examined the impact of DT on two dimensions, namely, PCIP and PDIP. According to Melville et al. (2004), organizational IP is also a dimension of corporate IP. However, this dimension was not studied here because it cannot be measured by the data published in the annual reports of listed companies and the existing literature does not provide much basis for it. However, in future studies, this dimension may be included in the model to explore further the association between DT, CSR, and this dimension.

Secondly, when exploring the moderating role of CSR in the model, only the moderating effect of the overall CSR was verified in this study. CSR has multiple dimensions. For example, according to Jamali et al. (2008), CSR is divided into mandatory economic responsibility, legal responsibility, ethical responsibility, strategic responsibility, and philanthropic responsibility. According to stakeholder theory, CSR is also categorized into corporate accountability to shareholders, employees, suppliers, consumers, customers, the environment, and society. Subsequent research can expand on the hierarchy to examine further the positive, negative, or insignificant effects of the different dimensions of CSR to provide a reference for theoretical research and corporate management Moreover, we will explore the environmental impact of digital processes based on the current study

Thirdly, the research methodology needs to be innovative. This paper uses OLS regression, panel fixed-effects regression, and SYS-GMM regression to analyze the data separately, but they do not reflect the dynamic changes of DT. DT is a complex and systematic process, and innovation input, learning capability, and entrepreneurial output may also change at different stages of DT, which leads to differences in the mechanism of action between different variables. In addition, this paper only uses property rights and industry as classification criteria to develop heterogeneity analysis, which is well represented but cannot fully show the full picture of heterogeneity. Therefore, the subsequent study can further examine the impact of dynamic changes of digital transformation on other variables, expand industry data sources, and investigate the dynamic impact of DT on firms’ IP through panel fixed-effects regression. The DID double difference method can also be incorporated into the study to explore the policy shock effects of DT on IP in different industries at different points in time.

Finally, stakeholder analysis is vital in assessing digital transformation’s impact on innovation and corporate social responsibility’s role, as it identifies key parties influencing the transformation and their power dynamics (Ioanna et al., 2022). We will extend current research by adding stakeholder analysis in further research.

In the digital economy, digital transformation is a deliberate decision to improve organizational procedures, alter production processes, introduce precision marketing, and more, ultimately impacting how well businesses innovate. Corporate social responsibility combines internal governance, environmental improvement, and social reputation. Companies that exhibit high levels of social responsibility are more likely to receive internal and external recognition and support and greater access to social resource allocation, thereby influencing the company’s innovative development. This paper analyzes the impact of digital transformation on both process and product innovation performance and examines the heterogeneity issues resulting from different industry classifications and property rights. The study also explores endogeneity problems arising from the lag period of enterprise innovation performance in the current period. Finally, this study verifies the positive moderating effect of corporate social responsibility on process and product innovation performance in the context of digital transformation.

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.

WL: Formal analysis, writing—original draft preparation, and supervision. JY: Visualization and project administration. Both authors contributed to the conceptualization, methodology, validation, data curation, writing—review, and editing, and read and agreed to the published version of the manuscript. All authors contributed to the article and approved the submitted version.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2023.1215866/full#supplementary-material

Abhinav, G., Forrest, B., and C, H. D. (2017). Red, blue, and purple firms: Organizational political ideology and corporate social responsibility. Strategic Manag. J. 38 (5), 1018–1040. doi:10.1002/smj.2550

Acemoglu, D., and Linn, J. (2004). Market size in innovation: Theory and evidence from the pharmaceutical industry. Q. J. Econ. 119 (3), 1049–1090. doi:10.1162/0033553041502144

Ahuja, G., and Katila, R. (2004). Where do resources come from? The role of idiosyncratic situations. Strategic Manag. J. 25 (8-9), 887–907. doi:10.1002/smj.401

Baines, T., and Lightfoot, H. W. (2014). Servitization of the manufacturing firm: Exploring the operations practices and technologies that deliver advanced services. Int. J. Oper. Prod. Manag. 34 (1), 2–35. doi:10.1108/ijopm-02-2012-0086

Berchicci, L., and King, A. (2007). 11 postcards from the edge: A review of the business and environment literature. Acad. Manag. Ann. 1 (1), 513–547. doi:10.5465/078559816

Bharadwaj, A., El Sawy, O. A., Pavlou, P. A., and Venkatraman, N. v. (2013). Digital business strategy: Toward a next generation of insights. MIS Q. 37 (2), 471–482. doi:10.25300/misq/2013/37:2.3

Bogers, M., Chesbrough, H., and Moedas, C. (2018). Open innovation: Research, practices, and policies. Calif. Manag. Rev. 60 (2), 5–16. doi:10.1177/0008125617745086

Bouncken, R., and Barwinski, R. (2021). Shared digital identity and rich knowledge ties in global 3D printing—a drizzle in the clouds? Glob. Strategy J. 11 (1), 81–108. doi:10.1002/gsj.1370

Bowen, H. R. (1953). in Social responsibilities of the businessman (Iowa City, IA: University of Iowa Press). 2013.

Brynjolfsson, E. (1993). The productivity paradox of information technology. Commun. ACM 36 (12), 66–77. doi:10.1145/163298.163309

Butlin, M., and Carnegie, R. (2001). “Developing innovation in a medium business: A practical approach,” in Innovation and imagination at work, 107–131.

Campbell, J. L. (2007). Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 32 (3), 946–967. doi:10.5465/amr.2007.25275684

Carrasco-Monteagudo, I., and Buendía-Martínez, I. (2013). Corporate social responsibility: A crossroad between changing values, innovation and internationalisation. Eur. J. Int. Manag. 7 (3), 295–314. doi:10.1504/ejim.2013.054327

Carroll, A. B. (1991). The pyramid of corporate social responsibility: Toward the moral management of organizational stakeholders. Bus. Horizons 34 (4), 39–48. doi:10.1016/0007-6813(91)90005-g

Chandola, V. (2015). Digital transformation and sustainability: Study and analysis. Cambridge: Havard University.

Chen, P., and Kim, S. (2023). The impact of digital transformation on innovation performance-The mediating role of innovation factors. Heliyon 9 (3), e13916. doi:10.1016/j.heliyon.2023.e13916

Cho, E., and Tsang, A. (2020). Corporate social responsibility, product strategy, and firm value. Asia-Pacific J. Financial Stud. 49 (2), 272–298. doi:10.1111/ajfs.12291

Chun, Y., Tusheng, X., Chunxiao, G., and Yu, S. (2021a). Digital transformation and division of labor: Specialization or vertical integration. China’s Ind. Econ. (09), 137–155.

Clarkson, M. E. (1995). A stakeholder framework for analyzing and evaluating corporate social performance. Acad. Manag. Rev. 20 (1), 92–117. doi:10.2307/258888

Cui, L., and Jiang, F. (2012). State ownership effect on firms’ fdi ownership decisions under institutional pressure: A study of Chinese outward-investing firms. J. Int. Bus. Stud. 43 (3), 264–284. doi:10.1057/jibs.2012.1

Eccles, R. G., Ioannou, I., and Serafeim, G. (2012). The impact of a corporate culture of sustainability on corporate behavior and performance, 17950. Cambridge, MA, USA: National Bureau of Economic Research.

Elkington, J., and Rowlands, I. H. (1999). Cannibals with forks: The triple bottom line of 21st century business. Altern. J. 25 (4), 42.

Ernst, H. (2001). Patent applications and subsequent changes of performance: Evidence from time-series cross-section analyses on the firm level. Res. Policy 30 (1), 143–157. doi:10.1016/s0048-7333(99)00098-0

Felin, T., and Hesterly, W. S. (2007). The knowledge-based view, nested heterogeneity, and new value creation: Philosophical considerations on the locus of knowledge. Acad. Manag. Rev. 32 (1), 195–218. doi:10.5465/amr.2007.23464020

Feroz, A. K., Zo, H., and Chiravuri, A. (2021). Digital transformation and environmental sustainability: A review and research agenda. Sustainability 13 (3), 1530. doi:10.3390/su13031530

Fitzgerald, M., Kruschwitz, N., Bonnet, D., and Welch, M. (2014). Embracing digital technology: A new strategic imperative. MIT sloan Manag. Rev. 55 (2), 1.

Flammer, C., and Luo, J. (2017). Corporate social responsibility as an employee governance tool: Evidence from a quasi-experiment. Strategic Manag. J. 38 (2), 163–183. doi:10.1002/smj.2492

Forcadell, F. J., Aracil, E., and Úbeda, F. (2020). The impact of corporate sustainability and digitalization on international banks’ performance. Glob. Policy 11, 18–27. doi:10.1111/1758-5899.12761

Frank, A. G., Mendes, G. H., Ayala, N. F., and Ghezzi, A. (2019). Servitization and industry 4.0 convergence in the digital transformation of product firms: A business model innovation perspective. Technol. Forecast. Soc. Change 141, 341–351. doi:10.1016/j.techfore.2019.01.014

Franks, B. (2012). Taming the big data tidal wave: Finding opportunities in huge data streams with advanced analytics. John Wiley and Sons.

Gerth, A. B., and Peppard, J. (2016). The dynamics of CIO derailment: How CIOs come undone and how to avoid it. Bus. Horizons 59 (1), 61–70. doi:10.1016/j.bushor.2015.09.001

Groysberg, B., and Lee, L.-E. (2009). Hiring stars and their colleagues: Exploration and exploitation in professional service firms. Organ. Sci. 20 (4), 740–758. doi:10.1287/orsc.1090.0430

Guler, I., and Nerkar, A. (2012). The impact of global and local cohesion on innovation in the pharmaceutical industry. Strategic Manag. J. 33 (5), 535–549. doi:10.1002/smj.957

Hansen, B. E. (1999). Threshold effects in non-dynamic panels: Estimation, testing, and inference. J. Econ. 93 (2), 345–368. doi:10.1016/s0304-4076(99)00025-1

Hendricks, K. B., Singhal, V. R., and Stratman, J. K. (2007). The impact of enterprise systems on corporate performance: A study of ERP, SCM, and CRM system implementations. J. Oper. Manag. 25 (1), 65–82. doi:10.1016/j.jom.2006.02.002

Henfridsson, O., Nandhakumar, J., Scarbrough, H., and Panourgias, N. (2018). Recombination in the open-ended value landscape of digital innovation. Inf. Organ. 28 (2), 89–100. doi:10.1016/j.infoandorg.2018.03.001

Hess, T., Matt, C., Benlian, A., and Wiesböck, F. (2016). Options for formulating a digital transformation strategy. MIS Q. Exec. 15 (2), 123–139. doi:10.7892/boris.105447/

Hinings, B., Gegenhuber, T., and Greenwood, R. (2018). Digital innovation and transformation: An institutional perspective. Inf. Organ. 28 (1), 52–61. doi:10.1016/j.infoandorg.2018.02.004

Huaijin, Q., Xiuqin, C., and Yanxia, L. (2020). The impact of digital economy on corporate governance: From the perspective of information asymmetry and managers’ irrational behavior. Reform (04), 50–64.

Ioanna, N., Pipina, K., Despina, C., Ioannis, S., and Dionysis, A. (2022). Stakeholder mapping and analysis for climate change adaptation in Greece. Euro-Mediterranean J. Environ. Integration 7 (3), 339–346. doi:10.1007/s41207-022-00317-3

Jamali, D., Safieddine, A. M., and Rabbath, M. (2008). Corporate governance and corporate social responsibility synergies and interrelationships. Corp. Gov. Int. Rev. 16, 443–459.

Jansen, J. J., Van Den Bosch, F. A., and Volberda, H. W. (2005). Managing potential and realized absorptive capacity: How do organizational antecedents matter? Acad. Manag. J. 48 (6), 999–1015. doi:10.5465/amj.2005.19573106

Jianfei, L., and Yun, G. (2019). The quality and innovation sustainability of corporate social responsibility information disclosure under financing constraints--data analysis of small and medium-sized board enterprises. Sci. Technol. Prog. Countermeas. 36 (11), 8.

Jimenez-Jimenez, D., and Sanz-Valle, R. (2008). Could HRM support organizational innovation? Int. J. Hum. Resour. Manag. 19 (7), 1208–1221. doi:10.1080/09585190802109952

Kane, G. C. (2017). Digital innovation lights the fuse for better health care outcomes. MIT sloan Manag. Rev. 59 (1).

Kang, H. S., Lee, J. Y., Choi, S., Kim, H., Park, J. H., Son, J. Y., et al. (2016). Smart manufacturing: Past research, present findings, and future directions. Int. J. Precis. Eng. Manuf. Green Technol. 3 (1), 111–128. doi:10.1007/s40684-016-0015-5

Katmon, N., Mohamad, Z. Z., Norwani, N. M., and Farooque, O. A. (2019). Comprehensive board diversity and quality of corporate social responsibility disclosure: Evidence from an emerging market. J. Bus. ethics 157 (2), 447–481. doi:10.1007/s10551-017-3672-6

Khan, A., Muttakin, M. B., and Siddiqui, J. (2013). Corporate governance and corporate social responsibility disclosures: Evidence from an emerging economy. J. Bus. ethics 114 (2), 207–223. doi:10.1007/s10551-012-1336-0

Kim, G., Shin, B., Kim, K. K., and Lee, H. G. (2011). Journal of the association for information IT capabilities, process-oriented dynamic capabilities, and firm financial performance.

Kohtamäki, M., Partanen, J., Parida, V., and Wincent, J. (2013). Non-linear relationship between industrial service offering and sales growth: The moderating role of network capabilities. Ind. Mark. Manag. 42 (8), 1374–1385. doi:10.1016/j.indmarman.2013.07.018

La Rosa, F., Liberatore, G., Mazzi, F., and Terzani, S. (2018). The impact of corporate social performance on the cost of debt and access to debt financing for listed European non-financial firms. Eur. Manag. J. 36 (4), 519–529. doi:10.1016/j.emj.2017.09.007

Laforet, S. (2008). Size, strategic, and market orientation affects on innovation. J. Bus. Res. 61 (7), 753–764. doi:10.1016/j.jbusres.2007.08.002

Lau, C., Lu, Y., and Liang, Q. (2016). Corporate social responsibility in China: A corporate governance approach. J. Bus. ethics 136 (1), 73–87. doi:10.1007/s10551-014-2513-0

Lew, Y. K., Sinkovics, R. R., and Kuivalainen, O. (2013). Upstream internationalization process: Roles of social capital in creating exploratory capability and market performance. Int. Bus. Rev. 22 (6), 1101–1120. doi:10.1016/j.ibusrev.2013.03.001

Li, Y., and Fei, G. Z. (2023). Network embeddedness, digital transformation, and enterprise performance—the moderating effect of top managerial cognition. Front. Psychol. 14, 1098974. doi:10.3389/fpsyg.2023.1098974

Li, S., Gao, L., Han, C., Gupta, B., Alhalabi, W., and Almakdi, S. (2023). Exploring the effect of digital transformation on Firms’ innovation performance. J. Innovation Knowl. 8 (1), 100317. doi:10.1016/j.jik.2023.100317

Liang, S., and Li, T. (2022). Can digital transformation promote innovation performance in manufacturing enterprises? The mediating role of R&D capability. Sustainability 14 (17), 10939. doi:10.3390/su141710939

Lindič, J., Baloh, P., Ribière, V. M., and Desouza, K. C. (2011). Deploying information technologies for organizational innovation: Lessons from case studies. Int. J. Inf. Manag. 31 (2), 183–188. doi:10.1016/j.ijinfomgt.2010.12.004

Lin-Hi, N., and Blumberg, I. (2018). The link between (not) practicing CSR and corporate reputation: Psychological foundations and managerial implications. J. Bus. Ethics 150 (1), 185–198. doi:10.1007/s10551-016-3164-0

Liu, D. Y., Chen, S. W., and Chou, T. C. (2011). Resource fit in digital transformation: Lessons learned from the CBC Bank global e-banking project. Manag. Decis. 49 (10), 1728–1742. doi:10.1108/00251741111183852

Lončar, D., Paunković, J., Jovanović, V., and Krstić, V. (2019). Environmental and social responsibility of companies cross EU countries–Panel data analysis. Sci. Total Environ., 657, 287–296. doi:10.1016/j.scitotenv.2018.11.482

Matt, C., Hess, T., and Benlian, A. (2015). Digital transformation strategies. Bus. Inf. Syst. Eng. 57 (5), 339–343. doi:10.1007/s12599-015-0401-5

Melville, N., Kraemer, K., and Gurbaxani, V. (2004). Review: Information technology and organizational performance: An integrative model of IT business value. MIS Q. 28 (2), 283–322. doi:10.2307/25148636

Meng, S., Su, H., and Yu, J. (2022). Digital transformation and corporate social performance: How do board independence and institutional ownership matter? Front. Psychol. 13, 915583. doi:10.3389/fpsyg.2022.915583

Moeuf, A., Lamouri, S., Pellerin, R., Tamayo-Giraldo, S., Tobon-Valencia, E., and Eburdy, R. (2020). Identification of critical success factors, risks and opportunities of Industry 4.0 in SMEs. Int. J. Prod. Res. 58 (5), 1384–1400. doi:10.1080/00207543.2019.1636323

Nollet, J., Filis, G., and Mitrokostas, E. (2016). Corporate social responsibility and financial performance: A non-linear and disaggregated approach. Econ. Model. 52, 400–407. doi:10.1016/j.econmod.2015.09.019

Parida, V., Westerberg, M., and Frishammar, J. (2012). Inbound open innovation activities in high-tech SMEs: The impact on innovation performance. J. small Bus. Manag. 50 (2), 283–309. doi:10.1111/j.1540-627x.2012.00354.x

Parsons, D., Gotlieb, C., and Denny, M. (1990). Productivity and computers in Canadian banking. University of Toronto—Department of Economics.

Porter, M. E., and Kramer, M. R. (2011). Creating shared value: Harvard business review. From the Magazine (January–February 2011).

Progiou, A., Liora, N., Sebos, I., Chatzimichail, C., and Melas, D. (2023). Measures and policies for reducing PM exceedances through the use of air quality modeling: The case of thessaloniki, Greece. Sustainability 15 (2), 930. doi:10.3390/su15020930

Rai, A., Patnayakuni, R., and Seth, N. (2006). Firm performance impacts of digitally enabled supply chain integration capabilities. MIS Q. 30, 225–246. doi:10.2307/25148729

Ren, Y., Li, B., and Liang, D. (2023). Impact of digital transformation on renewable energy companies’ performance: Evidence from China. Front. Environ. Sci. 10, 2702. doi:10.3389/fenvs.2022.1105686

Rochford, L., and Rudelius, W. (1997). New product development process: Stages and successes in the medical products industry. Ind. Mark. Manag. 26 (1), 67–84. doi:10.1016/s0019-8501(96)00115-0

Rouse, M. J., and Daellenbach, U. S. (2002). More thinking on research methods for the resource-based perspective. Strategic Manag. J. 23 (10), 963–967. doi:10.1002/smj.256

Schultz, F., Castelló, I., and Morsing, M. (2013). The construction of corporate social responsibility in network societies: A communication view. J. Bus. ethics 115 (4), 681–692. doi:10.1007/s10551-013-1826-8

Schumpeter, J. A. (1982). The theory of economic development: An inquiry into profits, capital, credit, interest, and the business cycle (1912/1934), 1. Transaction Publishers, 244.

Scuotto, V., Santoro, G., Bresciani, S., and Del Giudice, M. (2017). Shifting intra-and inter-organizational innovation processes towards digital business: An empirical analysis of SMEs. Creativity Innovation Manag. 26 (3), 247–255. doi:10.1111/caim.12221

Sebastian, I., Mocker, M., Ross, J., Moloney, K., Beath, C., and Fonstad, N. (2017). How big old companies navigate digital transformation. MIS Q. Exec. 42, 150–154.

Sebos, I., Progiou, A. G., and Kallinikos, L. (2020). “Methodological framework for the quantification of GHG emission reductions from climate change mitigation actions,” in Strategic planning for energy and the environment, 219–242.

Sebos, I. (2022). Fossil fraction of CO2 emissions of biofuels. Carbon Manag. 13 (1), 154–163. doi:10.1080/17583004.2022.2046173

Sorescu, A. B., Chandy, R. K., and Prabhu, J. C. (2003). Sources and financial consequences of radical innovation: Insights from pharmaceuticals. J. Mark. 67 (4), 82–102. doi:10.1509/jmkg.67.4.82.18687

Sosik, J. J., Gentry, W. A., and Chun, J. U. (2012). The value of virtue in the upper echelons: A multisource examination of executive character strengths and performance. Leadersh. Q. 23 (3), 367–382. doi:10.1016/j.leaqua.2011.08.010

Tippins, M. J., and Sohi, R. S. (2003). IT competency and firm performance: Is organizational learning a missing link? Strategic Manag. J. 24 (8), 745–761. doi:10.1002/smj.337

Un, C. A., and Asakawa, K. (2015). Types of R&D collaborations and process innovation: The benefit of collaborating upstream in the knowledge chain. J. Prod. Innovation Manag. 32 (1), 138–153. doi:10.1111/jpim.12229

Vij, S., and Farooq, R. (2016). Moderating effect of firm size on the relationship between IT orientation and business performance. IUP J. Knowl. Manag. 14 (4), 34–52.

White, M. (2012). Digital workplaces: Vision and reality. Bus. Inf. Rev. 29 (4), 205–214. doi:10.1177/0266382112470412

Wu, Z., Wang, X., Liao, J. Y., Hou, H., and Zhao, X. (2023). Evaluation of digital transformation to support carbon neutralization and green sustainable development based on the vision of “channel computing resources from the east to the west”. Sustainability 15 (7), 6299. doi:10.3390/su15076299

Yeniyurt, S., Henke, J. W., and Yalcinkaya, G. (2014). A longitudinal analysis of supplier involvement in buyers’ new product development: Working relations, inter-dependence, co-innovation, and performance outcomes. J. Acad. Mark. Sci. 42 (3), 291–308. doi:10.1007/s11747-013-0360-7

Zahra, S. A., and George, G. (2002). The net-enabled business innovation cycle and the evolution of dynamic capabilities. Inf. Syst. Res. 13 (2), 147–150. doi:10.1287/isre.13.2.147.90

Zhang, C., Chen, P., and Hao, Y. (2022). The impact of digital transformation on corporate sustainability-new evidence from Chinese listed companies. Front. Environ. Sci. 10, 1047418. doi:10.3389/fenvs.2022.1047418

Zheng, P., and Scase, R. (2013). The restructuring of market socialism in China: The contribution of an “agency” theoretical perspective. Thunderbird Int. Bus. Rev. 55 (1), 103–114. doi:10.1002/tie.21526

Zhu, Y., and Jin, S. (2023). COVID-19, digital transformation of banks, and operational capabilities of commercial banks. Sustainability 15 (11), 8783. doi:10.3390/su15118783

Zuanyong, Y., and Dian, W. (2021). “One belt, one road” corporate social responsibility, financing constraints and investment efficiency. Finance Econ. (02), 45–55.

Keywords: CSR, digital transformation (DT), product innovation performance, process innovation performance, innovation performance

Citation: Wang L and Yan J (2023) Effect of digital transformation on innovation performance in China: corporate social responsibility as a moderator. Front. Environ. Sci. 11:1215866. doi: 10.3389/fenvs.2023.1215866

Received: 02 May 2023; Accepted: 28 June 2023;

Published: 10 July 2023.

Edited by:

Grigorios L. Kyriakopoulos, National Technical University of Athens, GreeceReviewed by:

Ahmad Ibrahim Aljumah, Al Ain University, United Arab EmiratesCopyright © 2023 Wang and Yan. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Jinzhe Yan, eWFuanpAZ2FjaG9uLmFjLmty

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.