Gongjin Hu1

Gongjin Hu1 Wadim Strielkowski

Wadim Strielkowski Junwei Xu

Junwei Xu

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 17 January 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1127380

This article is part of the Research TopicSustainable Economic Growth, Green Deal and Macroeconomic Recovery – Most Suitable Pathways to Recovering From the Actual Evolutionary HiatusView all 14 articles

Under the concept of green economy, discovering how to utilize the Green Credit Guidelines in a way that guides enterprises to focus on their industries and to promote sustainable development has become an important and urgent objective. It is also conducive to the successful implementation of the “double-carbon target”. This paper uses Chinese A-share listed enterprises from 2007–2018 as its research object to explore whether green credit policy is conducive to reducing the financialization behavior of heavily polluting enterprises to curb their transformation from real to virtual. It is found that the financialization of heavily polluting enterprises has significantly decreased since the implementation of the Green Credit Guidelines in 2012, and these results remain unchanged after a series of robustness tests. A heterogeneity analysis shows that state-owned enterprises are subject to stronger policy effects than non-state-owned enterprises; furthermore, the studied policy effects are stronger in the eastern regions of China than in its central and western regions, and these effects are stronger in green provinces than in polluting provinces. A mechanism study finds that credit constraints and corporate innovation play a partially mediating role in the effect of green credit policy on corporate financialization. Further studies find that both the level of internal corporate governance and external monitoring contribute to the disincentivizing effect of green credit policy on financialization. Moreover, through an exploration of the possible economic consequences of the examined policy, it is found that the green credit policy reduces corporate financialization in favor of reducing inefficient corporate investment and major shareholders’ tunneling so that the level of corporate investor protection is improved. The findings validate the effectiveness of the Green Credit Guidelines and provide empirical evidence and empirical support for reducing corporate financialization to curb enterprises’ transformation from real to virtual and thus promoting the development of sustainability.

Since its reform and opening up, China’s economy has developed rapidly and has become deeply integrated into internationalization and globalization processes; moreover, with the implementation of China’s registration system and the improvement of its capital market, corporate financialization has progressed, and the contribution of the financial sector to GDP has increased. This shows that the role of financial development in the country’s economic activities has also increased.

However, the frequent occurrence of environmental pollution and the decline in environmental quality have become important reasons for the sluggish economic development of real enterprises that have accompanied the new state of China’s economy. The development of sustainable energy technology and green economy are attracting more and more attention (Sansyzbayeva et al., 2020; Streimikiene, 2022). They are also paying more and more attention to practical issues, such as the energy poverty and impact of COVID-19 pandemics (Streimikiene, 2022) An important problem in China is green development and financial asset allocation. Specifically, heavily polluting enterprises are increasingly transferring real enterprise capital materials to the financial sector to develop the virtual economy; this behavior of allocating funds to financial assets with a high degree of virtualization is the phenomenon of corporate financialization (Demir, 2009). The development of real enterprises that feature excessive engagement in financial business leads to a lack of sufficient support for the development of the real economy, which certainly affects the healthy development of the national economy in the long run. Thus, ways to prevent heavily polluting enterprises from engaging in excessive financial business and to reduce enterprises’ transformation from real to virtual have become frequently discussed as key issues related to China’s economic development.

Numerous scholars have conducted rich research on corporate financialization. The studies on the economic consequences of corporate financialization include those on the differential impacts of financialized markets on management procedures and risk attitudes (Siepel & Nightingale, 2014), the possible positive impact of financialized markets on corporate governance (Matsumoto, 2020), the decline in entity investment due to financialization (Maria Diez-Esteban et al., 2016; Davis, 2017; Jin et al., 2022), the impact of the financialization of the non-financial sector on its economic growth (Tomaskovic-Devey et al., 2015), the decrease in the financialization of the functional income distribution (Kohler et al., 2018), the possibly negative effect of corporate financialization on corporate environmental responsibility (Li et al., 2020), and the possibility for financialization to lead to a decrease in the share of wages (Kohler et al., 2019). Thus, this demonstrates that the excessive engagement of non-financial capital enterprises in financial business development has certain negative effects on individuals, enterprises, and society, although the development of corporate financialization promotes the rapid development of enterprises to a certain extent; moreover, to curb corporate financialization, it is necessary to explore the reasons behind the influence of corporate financialization. The literature on the causes of corporate financialization mainly covers shareholder value creation pressures (Modell & Yang, 2018), technological and ideological changes (Davis & Kim, 2015), trust structures (Harrington, 2017), employee stock ownership plans (Feng et al., 2022a), business diversification (Feng et al., 2022b), multiple blockholders (Jiang et al., 2022), and increases in the cash holdings of non-financial firms, and it provides support for the possibilities that traditional non-financial firms are increasingly engaging in for-profit lending (Davis, 2018). While most of these influences have been studied only in terms of corporate behavior and social relations, few studies have explored how institutional reforms and related policy implementations can influence corporate financialization. A key factor that drives heavily polluting enterprises to make excessive investments in financial assets is the opportunity to increase free cash flows.

For this reason, the Chinese government has actively explored financial instruments that can be used to effectively manage the pollution and excessive financialization of heavily polluting enterprises in the pursuit of high-quality economic development. For example, on 24 February 2012, the China Banking Regulatory Commission (CBRC) implemented the Green Credit Guidelines, which clarify the standards and principles of green credit in the banking industry and provide effective guidance on how financial institutions can effectively utilize green credit, give full play to the resource allocation efficiency of the financial market, and promote the green transformation of traditional industries to encourage enterprises to improve their environmental quality and establish a low-carbon circular development system. Existing studies on green credit policy mainly focus on policy effects, but the relevant research findings have not been unanimously accepted. For example, on the commercial banking side, green credit has been shown to have a negative impact on commercial bank performance in some cases, but this impact continues to diminish over the long-term implementation of the policy; in contrast, studies conducted based on dynamic templates have found a significant positive impact of green credit policy on the aggregate performance of commercial outcomes (Luo et al., 2021; Yin et al., 2021; Li et al., 2022).

On the business side, some studies have found significant effects of green credit policy implementation in terms of its ability to increase the financing costs of high-pollution and high-energy consumption enterprises, reduce the maturity of debt financing, and thus reduce the environmental impact of the development of heavily polluting enterprises. However, other studies have concluded that the implementation of green credit policies has not achieved the expected effect, that green credit policies only have a restrictive effect on short-term loans and little impact on long-term loans and financing costs and that heavily polluting enterprises can easily still obtain credit (Xu & Li, 2020; Tan et al., 2022a; Li et al., 2022). Scholars have not reached a consensus on the implementation effect of green credit policy, and related issues still need to be further explored. The promulgation of the Green Credit Guidelines indicates the government’s determination to govern the financing behavior of heavily polluting enterprises through bank credit (Zhang et al., 2022a), which in turn will influence the financialization decisions of enterprises.

However, few existing studies have focused on the impact of green credit policy on the financialization of heavily polluting enterprises and the underlying mechanism of action. As an economic regulatory instrument of environmental regulation, does green credit policy curb the financialization of heavily polluting enterprises? If so, through what channels does green credit exert this influence on the financial investment behavior of enterprises? Does the impact of green credit on corporate financialization vary across different economic scenarios? The answers to these questions will not only help us further explore the important factors influencing corporate financialization at the macro policy level and gain a deeper understanding of the theoretical logic of the relationship between macroeconomic policy and micro enterprise behavior but will also provide theoretical references for the implementation of green credit policy to serve the real economy.

Based on this, this paper conducts a study on the relevant issues with a sample of Chinese A-share listed companies covering 2007 to 2018. The relevant findings show that the implementation of the Green Credit Guidelines policy significantly reduced the financialization behavior of heavily polluting enterprises, and these findings remain robust after a series of robustness tests. The relevant findings are more pronounced among state-owned enterprises, in the eastern regions of China and among enterprises in green provinces. The mechanism study finds that Green Credit Guidelines affect corporate financialization mainly through credit constraints and corporate innovation. Further study finds that both the level of internal corporate governance and external supervision enhance the disincentivizing effect of the Green Credit Guidelines on financialization and that the reduction in corporate financialization induced by this green credit policy is beneficial in terms of further reducing the inefficient investments of firms and reducing major shareholders’ tunneling.

The separation of power in modern enterprises into two components has caused a conflict of interest between managers and the owners of enterprises. Managers tend to excessively pursue short-term goals that benefit themselves, while owners seek to maximize long-term interests; this leads to the possibility that managers may use their management power to earn contractual compensation and excess profits at the expense of owners in the process of making relevant decisions to achieve performance goals or meet personal needs. Moreover, in corporate enterprises, major shareholders often tend to use their control power to disproportionately balance corporate decisions to benefit their personal self-interests against the detriment of the legitimate rights and interests of small and medium-sized shareholders. Among them, using free cash flow by executives to invest in financial products with the goal of obtaining transient high returns is an important means to seek personal gains (Li et al., 2020). Heavily polluting enterprises generally have significant fixed assets and can quickly obtain sufficient credit funds via tangible asset guarantees, which in turn may provide additional room for executives to make financial investments for personal gain.

Green credit policies require financial institutions to fully examine the business scope of target enterprises when conducting credit operations, especially in terms of the environmental and social risks pertaining to the enterprises, and they are required to decline the authorization of credit for enterprises that are not friendly to the environment and social development or even those that have serious destructive effects with the objective of reducing their capital investment in polluting enterprises (He et al., 2019; Lyu et al., 2022; Peng et al., 2022; Wang et al., 2022). As environmental regulations become stricter and the “double-carbon target” is implemented, the increasing risk of environmental violations increases the chance that heavily polluting enterprises will not be able to repay their debts (Guo et al., 2022; Lian et al., 2022). Banks, as creditors, bear greater investment risks than shareholders, while corporate managers, in pursuit of their own interests or short-term interests, tend to reduce investment in real enterprises and tend to invest idle funds in financial products; however, investments in financial products entail great uncertainty, and once such an investment fails, a major debt crisis in terms of corporate funds may arise and harm the interests of creditors (Hu et al., 2020; Zhang et al., 2021; Zhu, 2022; Ge and Zhu, 2022). Therefore, banks apply credit rationing to heavily polluting enterprises to mitigate credit and environmental risks and safeguard their own credit quality. The introduction of a green credit policy means that heavily polluting enterprises face a stricter financing environment and that the available credit for heavily polluting enterprises is significantly reduced; this, in turn, reduces available cash flow (Liu & He, 2021; Tan et al., 2022b; Zhang & Zhou, 2022). A green credit policy can reduce the credit resources available to firms and decrease their disposable cash flow. This reduction in management’s disposable cash flow forces management to engage in less financial speculation, which helps reduce the financialization of heavily polluting enterprises and curb their transformation from real to virtual. In addition, the introduction of a green credit policy indicates that a greater proportion of limited resources will be allocated to green development enterprises (Liu et al., 2019; Zhang et al., 2022c). In turn, heavily polluting enterprises seeking green credit will actively improve their production processes, increase their R&D investments, and reduce pollution emissions by means of technological innovation (Liu et al., 2021; Zhang et al., 2022d; Gao et al., 2022). Moreover, a focus on technological innovation R&D is conducive to the development of the long-term goals of enterprises, as it reduces the crowding out of entity investment in enterprises and promotes the allocation of more funds to technological innovation, thus discouraging the financialization behavior of enterprises. It can be seen that, on the one hand, the introduction of a green credit policy can alleviate the corporate agency problem to a certain extent by reducing the discretionary cash flow of heavily polluting enterprises and thus reducing the self-interest motivation of executives and the tendency of enterprises to earn speculative profits by investing in financial products; on the other hand, a green credit policy guides heavily polluting enterprises to spend more funds on green technological innovation and transformative development and thus reduce their financial investment. Accordingly, this paper proposes the following hypothesis.

Hypothesis: After the implementation of a green credit policy, the financialization behavior of heavily polluting enterprises is significantly reduced, which curbs their transformation from real to virtual.

In this paper, Chinese A-share listed companies are selected as the research sample, and the chosen research interval spans from 2007 to 2018. The year 2007 is chosen because the new accounting standards of China were implemented in 2007; since new financial instrument standards were implemented after 2019, in order to ensure consistent measurement of variables in this paper, the sample was selected as of 2018; moreover, we exclude observations of financial companies, observations of ST and PT companies, observations of companies listed for less than 1 year, observations of companies with asset-liability ratios greater than 1, and observations with missing data. All continuous variables are winsorized at the 1% and 99% percentiles, and a final sample of 19,914 valid observations is obtained. This study utilizes financial data from the China Stock Market and Accounting Research Database (CSMAR), the RESSET financial research database, and the Chinese Research Data Services Platform (CNRDS).

Referring to existing scholars such as Demir (2009), the ratio of financial investment assets to total assets is chosen as a measure of financialization. Specifically, the sum of “trading securities,” “derivative instruments,” “available for sale securities,” “held-to-maturity securities,” “long-term equity investments,” and “investment properties” is used as a measure of financial investment assets, and the ratio of financial investment assets to total corporate assets is used as a measure of corporate financialization (FIN).

Based on existing scholarly studies (Wen et al., 2021; Zhang et al., 2022b), a relevant study design is used. POST×TREAT is the net effect of the green credit policy, and the dummy variable POST is created for the experimental period according to the difference-in-difference model. For the year 2012 or later years, the period after the promulgation of the Green Credit Guidelines, this variable is set to 1, while it is set to 0 for the years before 2012. In addition, the dummy variable TREAT denotes whether each sample enterprise is a heavily polluting enterprise. If the enterprise is a heavily polluting enterprise, TREAT takes the value of 1; otherwise, it takes the value of 0.

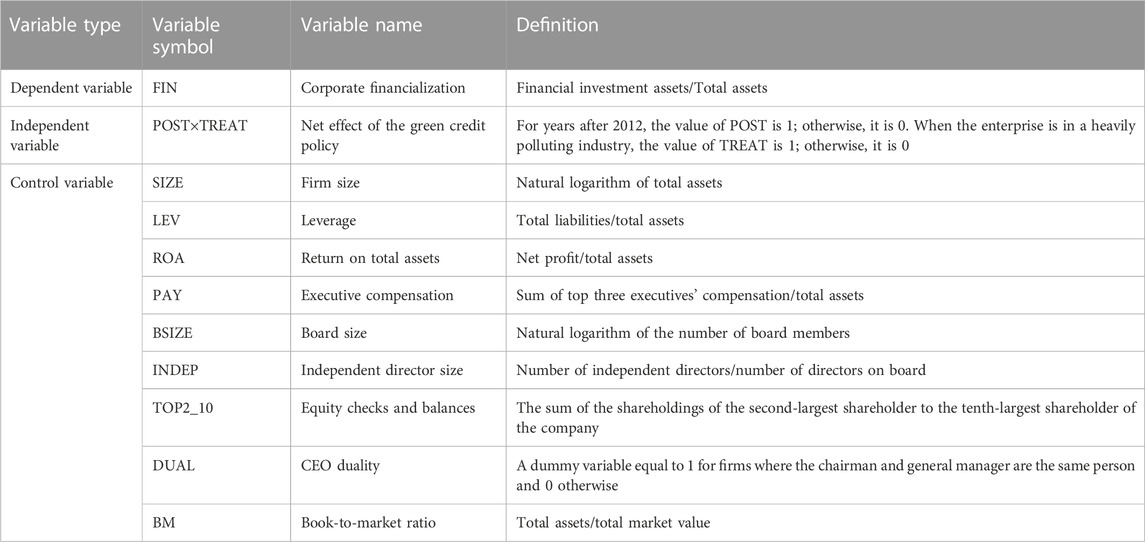

The control variables include firm size (SIZE), the gearing ratio (LEV), return on total assets (ROA), executive compensation (PAY), board size (BSIZE), independent director size (INDEP), equity checks and balances (TOP2_10), dual position (DUAL), and the book-to-market ratio (BM); moreover, annual and individual effects are controlled in the subsequent regression process. The relevant variables are defined in Table 1.

TABLE 1. Definition of variables.

To test hypothesis 1, the following model is constructed:

In the above equation,

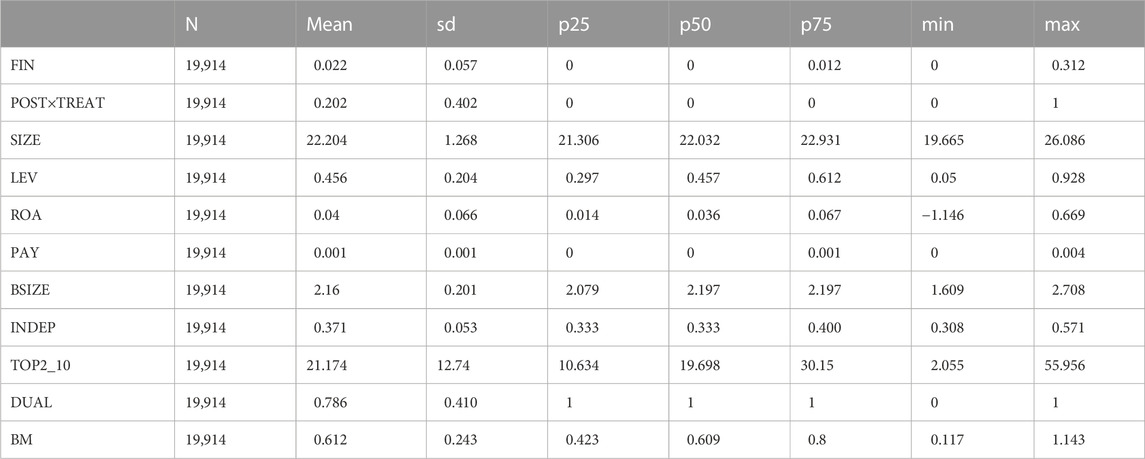

The descriptive statistics of the sample are shown in Table 2. According to this table, the mean value of FIN is 0.022, indicating that the ratio of financialized investment to the total assets of the sample enterprises reaches 2.22%; moreover, the standard deviation of FIN is 0.057, and the minimum and maximum values are 0.000 and 0.312, respectively, indicating that there is a certain degree of variation in the financialized investment of different enterprises. The distribution of the remaining control variables is basically consistent with the results of prior literature.

TABLE 2. Descriptive statistics of the variables.

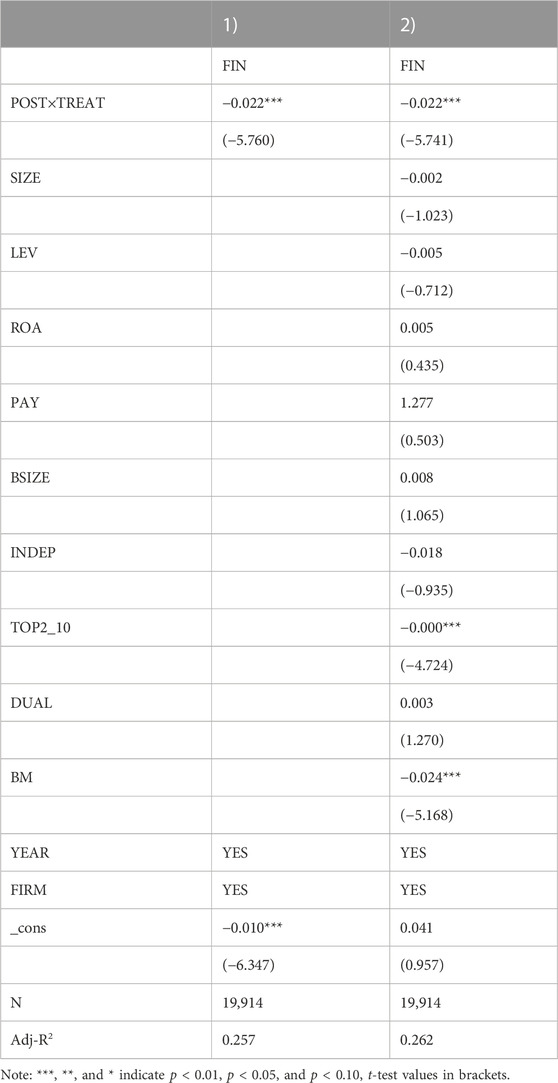

In this paper, the impact of the green credit policy on corporate financialization is tested based on model 1). Column (1) of Table 3 examines the effect of the green credit policy on corporate financialization with no addition of other variables, and the estimated coefficient of the green credit policy variable is −0.022 and significantly negative at the 1% level; column 2) further adds several control variables, and the coefficient of POST×TREAT remains unchanged at −0.022 and significant at the 1% level. This result indicates that the green credit policy significantly reduces the financialization of heavily polluting enterprises compared to that of non-heavily polluting enterprises, which in turn curbs these enterprises’ transformation from real to virtual. This validates hypothesis H1 of this paper.

TABLE 3. Main regression.

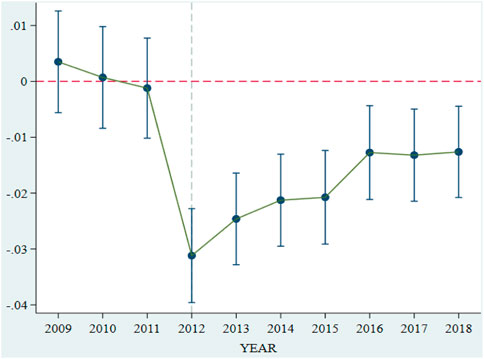

The use of a difference-in-difference model presupposes that the assumption of parallel trends is satisfied between the experimental and control groups. Specifically, for the context of this paper, before the introduction of the Green Credit Guidelines, the financialization of heavily polluting and non-heavily polluting enterprises should show essentially the same trend of change; however, after the introduction of the Green Credit Guidelines, the two should begin to show significant differences. That is, after the implementation of the green credit guidelines, the policy effects of heavily polluting enterprises and non-heavily polluting enterprises show different trends, and the reason for this change is the impact of policy implementation. Figure 1 reports the results of the parallel trend test of this paper. It can be seen that all the regression results before 2012 are non-significant, which shows that the changes in the trends of financialization for heavily polluting enterprises and non-heavily polluting enterprises are consistent and not significantly different before the introduction of the Green Credit Guidelines. From 2012 onward, the financialization of heavily polluting enterprises decreases significantly compared to that of non-heavily polluting enterprises. This difference is because the implementation of green credit policy has different effects on heavily polluted enterprises and non-heavily polluted enterprises, that is, the implementation of policy does have differences between the experimental group and the control group. Therefore, the sample passes the parallel trend test required for a difference-in-difference estimation.

FIGURE 1. Parallel trend test.

Considering that firm characteristic differences may vary across heavily and non-heavily polluting enterprises and that these differences may have an impact on the corporate financialization affected by the green credit policy, we attempt to mitigate endogeneity problems using the PSM method. The propensity scores are calculated according to observed characteristics influencing the policy operation, for the purpose of controlling selection bias (Lechner, 2002). Specifically, the nearest neighbor matching method is used to pair heavily and non-heavily polluting enterprises, and this is followed by DID regression; the corresponding regression results are shown in Table 4. From this table, it can be found that the coefficient of POST×TREAT remains significantly negative, and the conclusions of this paper remain unchanged.

TABLE 4. PSM-DID.

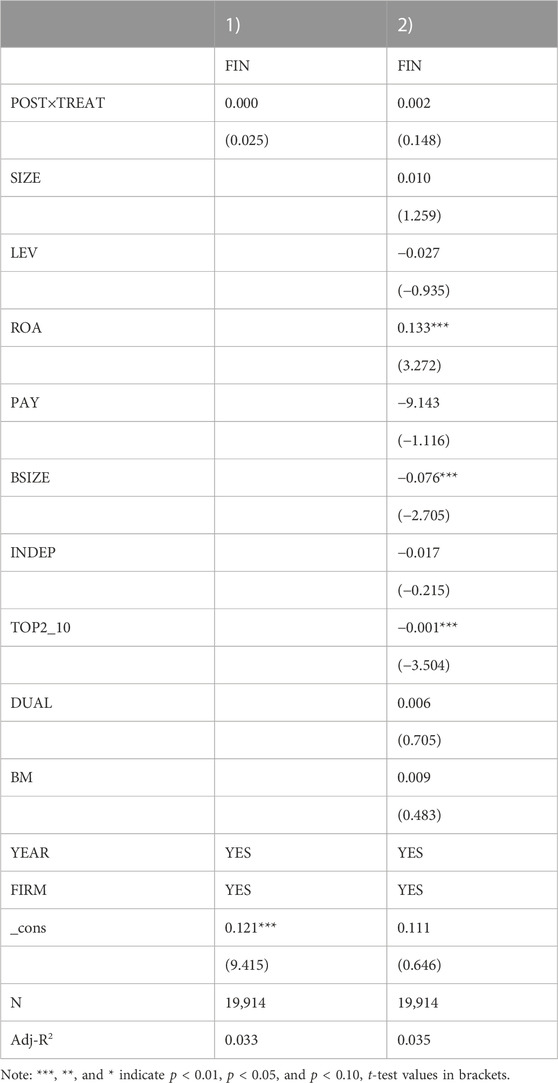

On the one hand, we conducted a time counterfactual test. To ensure that the core dependent variable of this study is affected by the introduction of the Green Credit Guidelines rather than other exogenous shocks, we advance the time when the sample is subjected to shocks by 2 years, i.e., we assume that 2010 is the year in which the virtual shock occurs, and hence, we set POST equal to 1 for the year 2010 and the following years, and we set POST equal to 0 for the years before 2010. If the above findings are due to unobservable inherent differences between heavily and non-heavily polluting enterprises caused by the time frame of the introduction of the Green Credit Guidelines, then the virtual time of the introduction of the Green Credit Guidelines should also be concluded invariantly. The specific regression results are listed in Table 5, and they show that the regression coefficient of POST×TREAT is no longer significant; thus, the hypothesis of this paper is further verified.

TABLE 5. Time counterfactual test, 2 years ahead.

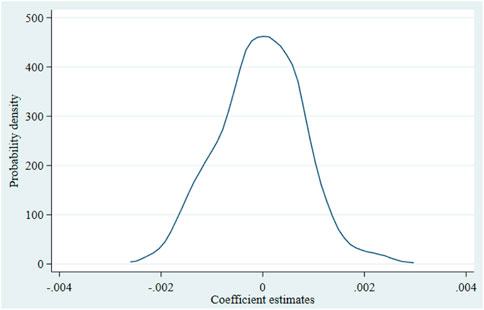

On the other hand, we conducted a placebo test in the randomized treatment group and the control group. To further exclude the influence of other unknown factors on firm selection and ensure the reliability of this paper’s conclusions, the original study findings are tested for robustness through a random selection of a number of dummy experimental groups from all the samples for a same-baseline regression, the results are shown in Figure 2. The regression coefficients of the fictitious cross-products are all concentrated around zero, indicating that the virtual treatment effect constructed in this paper does not exist and that the green credit policy has no effect on the choice of enterprises. The credit policy has no significant effect in any of the 500 random samples. That is to say, there is a clear correlation between the policy effect discussed in this paper and the implementation of green credit policy. The implementation of green credit policy is the real factor affecting the conclusion of this paper. Therefore, the inhibitory effect of the green credit policy on corporate financialization has little causal relationship with other unknown factors.

FIGURE 2. Placebo random sampling 500 times of green credit and financialization results.

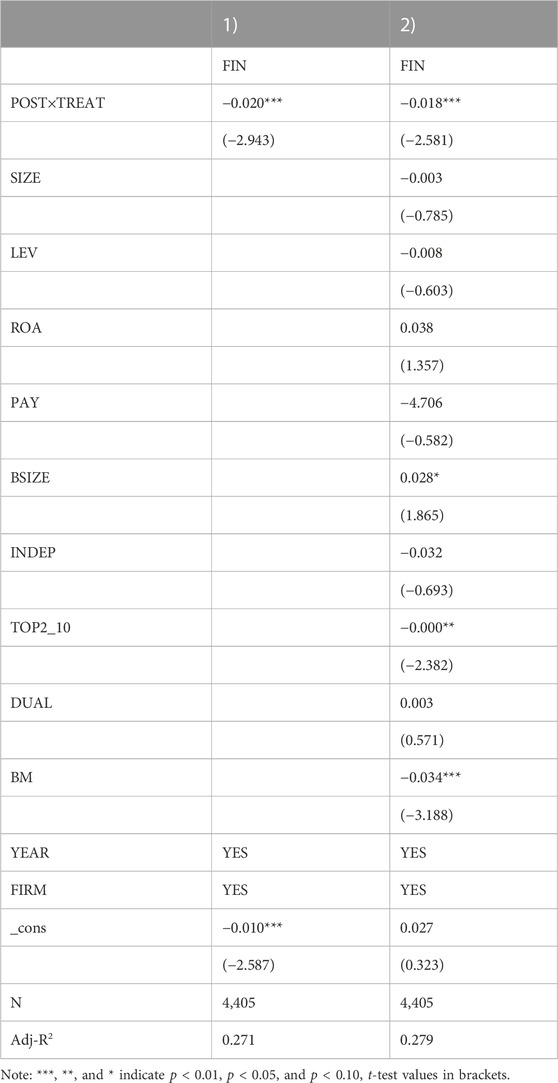

In addition to the aforementioned categories, financial assets should include five balance sheet accounts, namely, “other receivables”, “buying back the sale of financial assets”, “current portion of non-current assets”, “other current assets” and “other non-current assets” (Li et al., 2020). According to the results shown in Table 6, the regression coefficient of POST×TREAT is still negative and significant at the 1% level when the control variables are not included; moreover, the results are negative and significant at the 1% level when the control variables are included, and the relevant conclusions are still valid.

TABLE 6. Replacement of financialization measures.

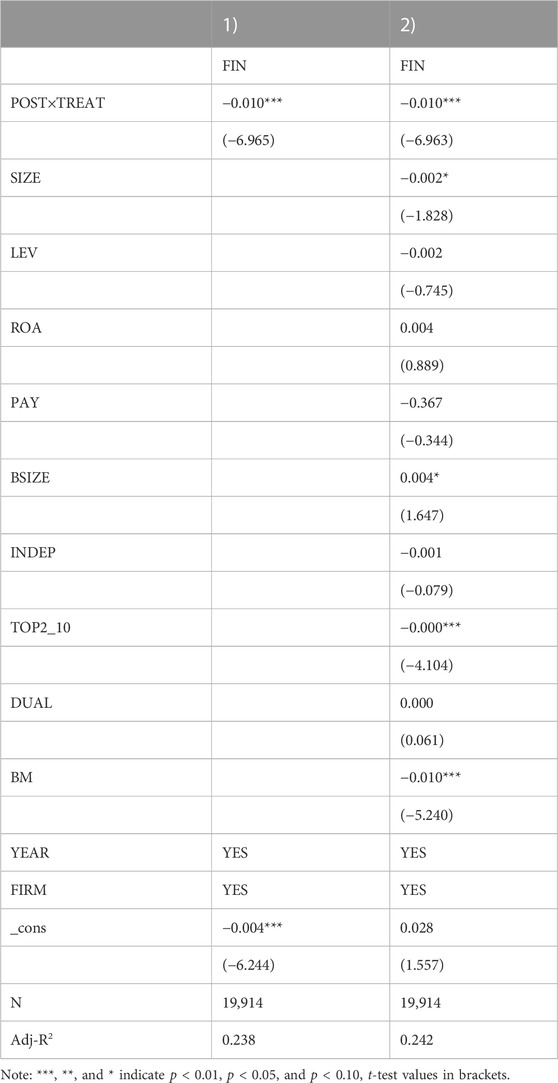

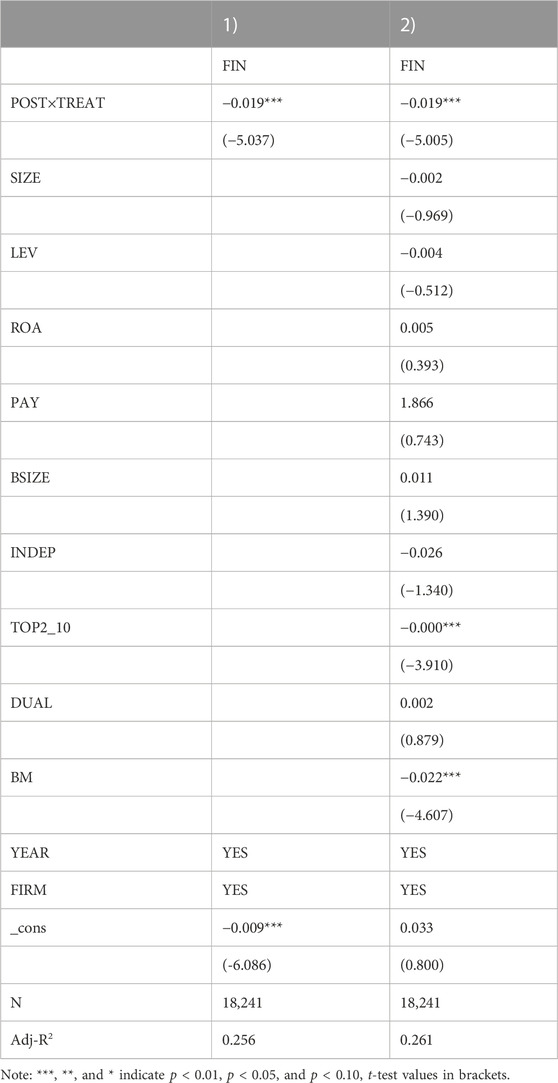

Since the Green Credit Guidelines were introduced in 2012, 2012 is excluded from the sample study interval to prevent possible measurement error problems. In other words, the portion of the sample corresponding to 2012 is excluded from the aforementioned research design, and the regression test is conducted again. The correlation results are presented in Table 7. The regression coefficient of POST × TREAT remains significantly negative at the 1% level, and the findings remain unchanged.

TABLE 7. Excluding the year of policy introduction.

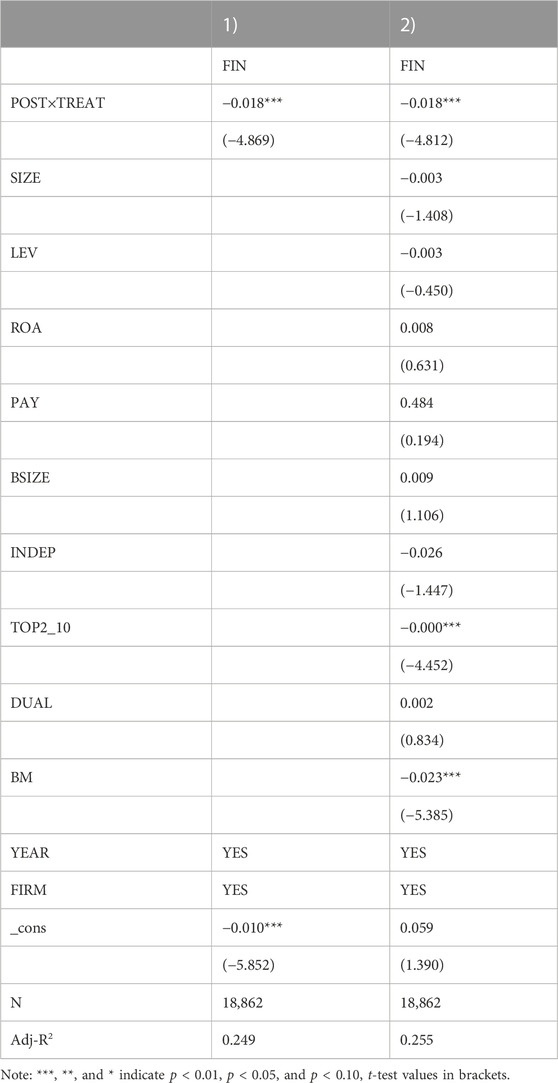

Considering that the real estate industry is recognized as a profitable industry, that the financialization of the corresponding commodities has shown an increasing trend in China, and that in a certain sense, real estate can be defined as a commodity with a high financialization level (Davis, 2017), all real estate industry observations in the original sample are removed and the regression test is conducted again; the results are presented in Table 8. The TREAT regression coefficient remains significantly negative at the 1% level, and the conclusion that the Green Credit Guidelines are conducive to reducing the financialization of heavily polluting enterprises and thus curbing their transformation from real to virtual remains unchanged.

TABLE 8. Removing real estate industry samples.

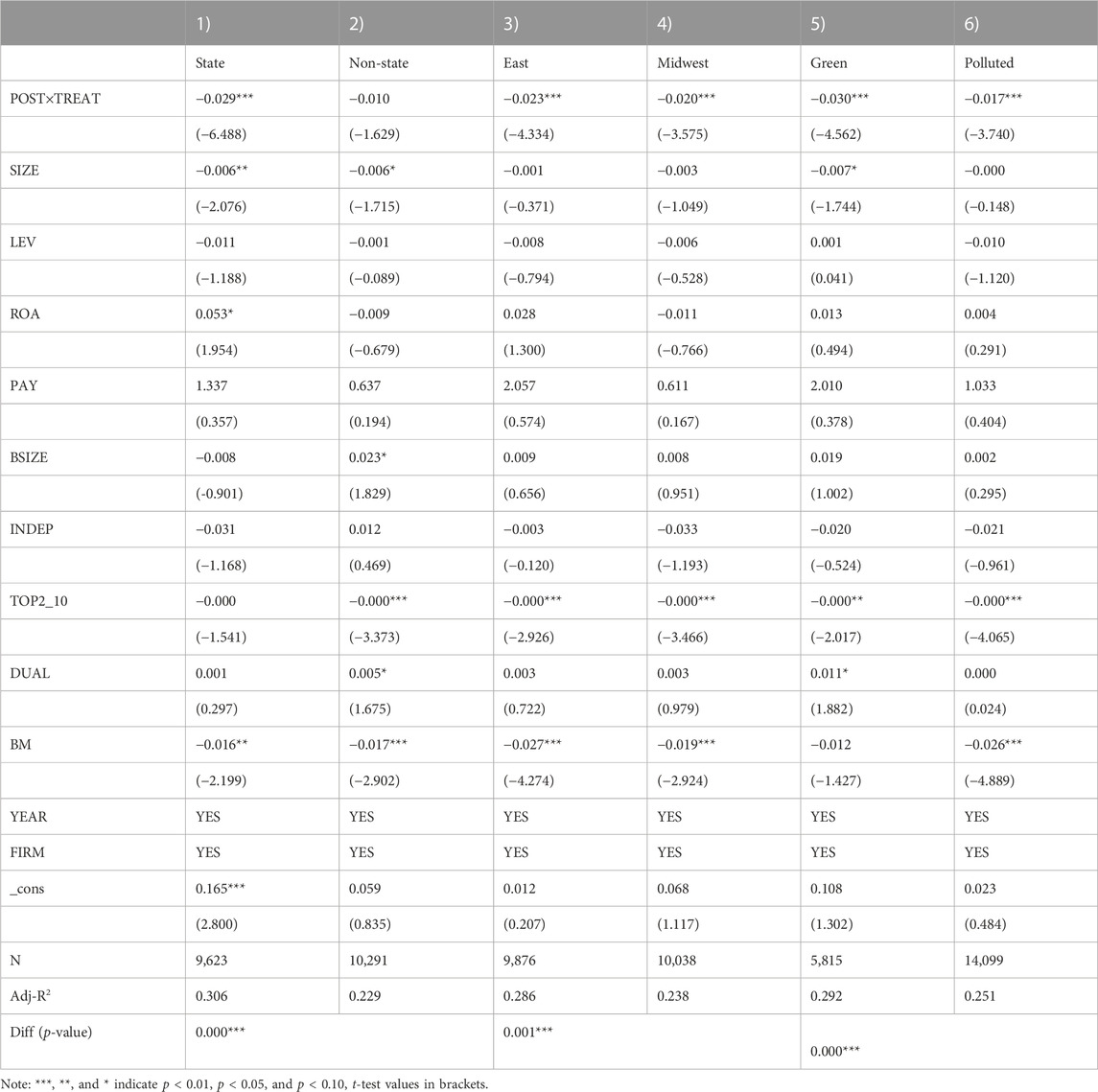

The first is the analysis of the heterogeneity of Nature of ownership. Due to the special nature of state-owned enterprises, government policy support tends to favor these firms; moreover, even if state-owned enterprises make financial investments and suffer unaffordable losses, due to the existence of soft budget constraints, the government tends to provide state-owned enterprises with support in the form of subsidies and tax cuts to ensure their stability. Furthermore, compared to non-state-owned enterprises, state-owned enterprises have a lower degree of financing constraints (Wang et al., 2020), which leads state-owned enterprises to make more financial investments. However, green credit has a stronger punitive effect on heavily polluting state-owned enterprises, and heavily polluting state-owned enterprises face stronger constraints on credit financing than non-heavily polluting state-owned enterprises. Thus, green credit policies may lead to restrictions on available liquidity for heavily polluting state-owned enterprises and may reduce their financialized investments. For this reason, the sample of this paper is divided into a sample group of state-owned enterprises and a sample group of non-state-owned enterprises for regression purposes, and the regression results are presented in columns (1) and (2) of Table 9. The regression coefficient of POST×TREAT is −0.029, which is significant at the 1% level in the sample group of state-owned enterprises; however, in the sample group of non-state-owned enterprises, the regression coefficient is −0.010, and it fails the significance test, and the empirical p-value is 0, with a significant difference in coefficients between groups. This indicates that the inhibitory effect of the green credit policy on corporate financialization is more pronounced among heavily polluting state-owned enterprises than among heavily polluting non-state-owned enterprises.

TABLE 9. Heterogeneity: nature of ownership.

The second is the analysis of regional heterogeneity. Due to the wide geographical dispersion of Chinese enterprises, the eastern region of China tends to have better economic development and a higher level of legal management and enforcement than the central and western regions. Considering the lack of economic development in the central and western regions, the environmental governance and protection of these areas may be lower, and enterprises may face looser environmental regulation. Therefore, the credit constraints generated by the green credit policy may have different impacts on enterprises in different regions. In this paper, the full sample of firms is divided into two groups corresponding to the eastern and central-western regions according to the provinces where the firms are registered for testing, and the results are presented in columns (3) and (4) of Table 9. In the eastern region sample, the regression coefficient of POST×TREAT is −0.023, which is significant at the 1% level, while in the central and western region sample, the regression coefficient of POST×TREAT is −0.020, which is significant at the 1% level; moreover, the empirical p-value of the two groups is 0.001, indicating that the phenomenon of decreased financialization among heavily polluting enterprises was significantly reduced after the implementation of the green credit policy. In particular, this phenomenon is more obvious for heavily polluting enterprises located in the eastern region.

Finally, the heterogeneity analysis between green provinces and polluted provinces Similarly, there are differences in environmental pollution across provinces with different environmental attributes due to the common influence of factors such as the natural environment and the industry layouts of different regions. Therefore, the sample is divided into a green province group and a polluting province group. The governments of green provinces tend to pay more attention to every move of polluting enterprises to maintain their existing environmental achievements, and the management and requirements of heavily polluting enterprises are stricter. Therefore, the green credit policy may have a greater impact on heavily polluting enterprises in green provinces. The results of the subsequent grouped regressions are presented in columns (5) and (6) of Table 9. The regression coefficient of POST×TREAT for the green provinces is −0.030, which is significant at the 1% level, while in the polluting provinces, the regression coefficient of POST×TREAT is −0.017, which is significant at the 1% level; both samples have an empirical p-value of 0 and a significant difference in coefficients between groups, indicating that the suppressive effect of the green credit policy on the financialization of heavily polluting enterprises in both green and polluting provinces can have an effect but that it is more pronounced among heavily polluting enterprises in green provinces.

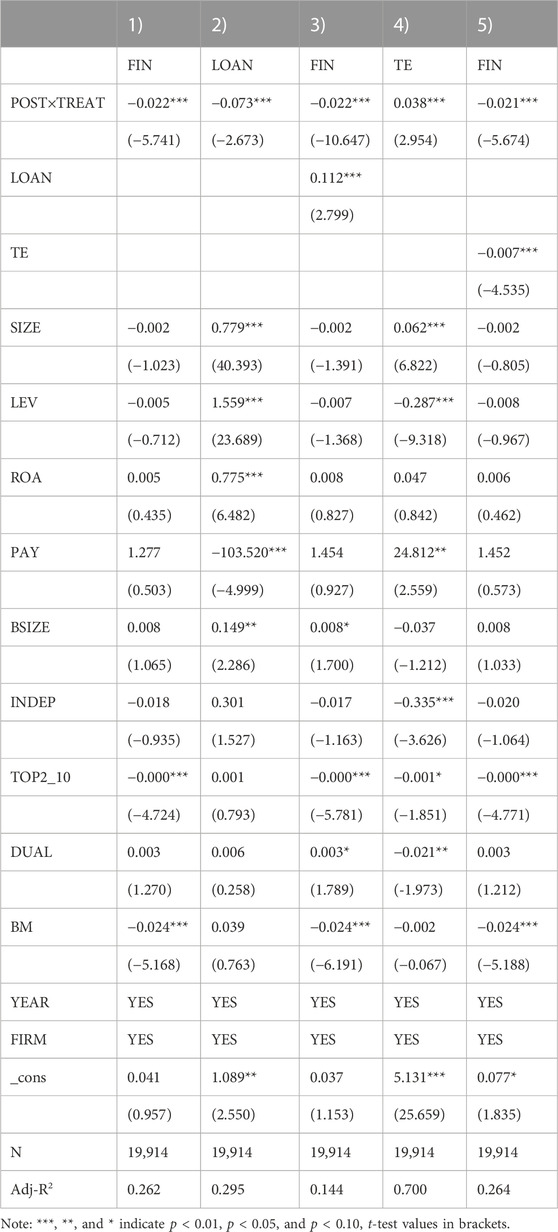

On the one hand, the previous section finds that the green credit policy increases the cost of access to credit for heavily polluting enterprises and, on the other hand, forces firms to undertake green technological innovation to reduce their idle capital and thus their financial investment. Therefore, there is an increase in the cost of credit and technological innovation, which may be the mediating variable impacting the effect of green credit policy on heavily polluting enterprises. To this end, the following model is designed for specific testing:

where MED is the mediating variable, which is the cost of credit and technological innovation, respectively, and the cost of credit is expressed by the loan constraint LOAN, which is the ratio of the sum of long-term and short-term borrowing to the total assets of the enterprise; TE is the technological innovation measured by the number of patents granted to the enterprise for inventions. Referring to Baron and Kenny (Baron & Kenny, 1986) regarding the intermediation effect, an analysis is carried out in conjunction with model 1); specifically, if

TABLE 10. Mediation: Loan constraints and the number of patents granted for inventions.

The previous section verifies that the studied green credit policy helps reduce the financial investment of heavily polluting enterprises and thus curbs their transformation from real to virtual. Since the financialization behavior of firms largely stems from management’s self-interest motivation, finding effective measures to reduce management’s self-interest motivation may enhance the effectiveness of the green credit policy in terms of curbing the financialization of heavily polluting enterprises. In view of this, this paper continues to verify the internal governance level, INGOV, and the external supervision level, EXSUP, and we design the following model:

where

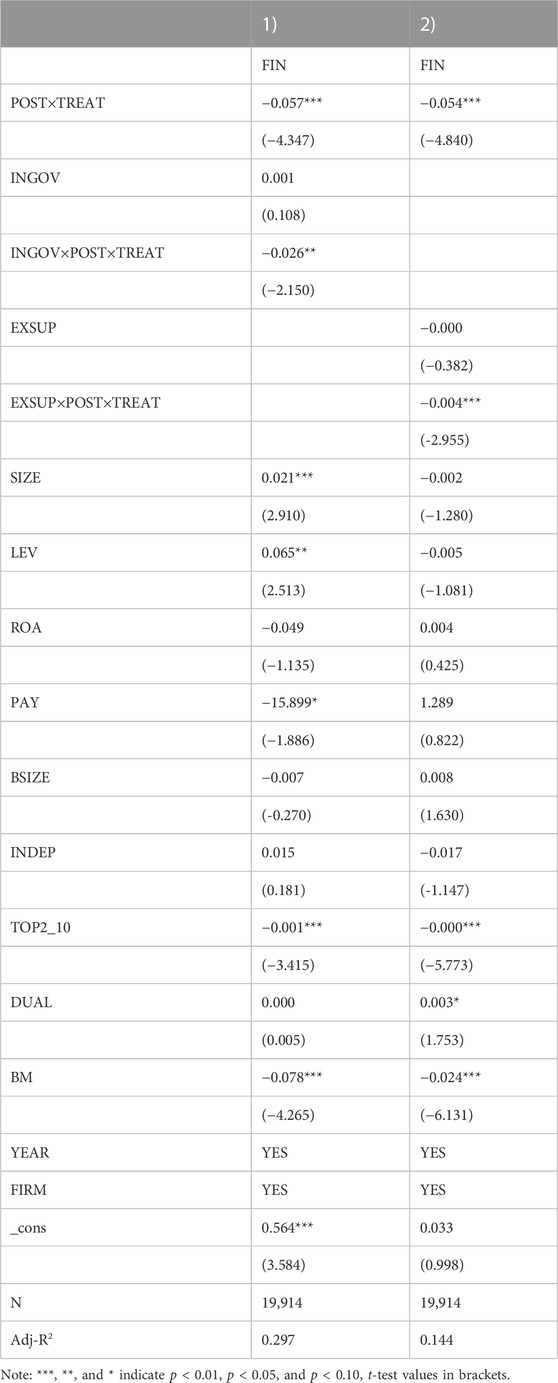

The regression test results corresponding to model (4) are presented in Table 11. According to column (1) of the table, it can be seen that the coefficient of INGOV×POST×TREAT is −0.026, which is significant at the 5% level, showing that an effective level of internal corporate governance can strengthen the inhibitory effect of the green credit policy on the financialization of heavily polluting enterprises. Similarly, the regression coefficient of EXSUP×POST×TREAT in column (2) is −0.004, which is significant at the 1% level, indicating that external government environmental supervision can also further enhance the inhibitory effect of the green credit policy on the financialization of heavily polluting enterprises.

TABLE 11. Interaction effect.

On the one hand, we conducted an analysis of inefficient investment. Since excessive investment in financial assets by enterprises will, to a certain extent, limit the development of normal entity investment and because a good green credit policy is conducive to reducing this adverse behavior, such a policy may promote the efficiency of enterprise investment. To verify this view, the following model is constructed for regression testing:

Model (5) mainly refers to the work of Richardson (Richardson, 2006) and other practices to measure inefficient investment.

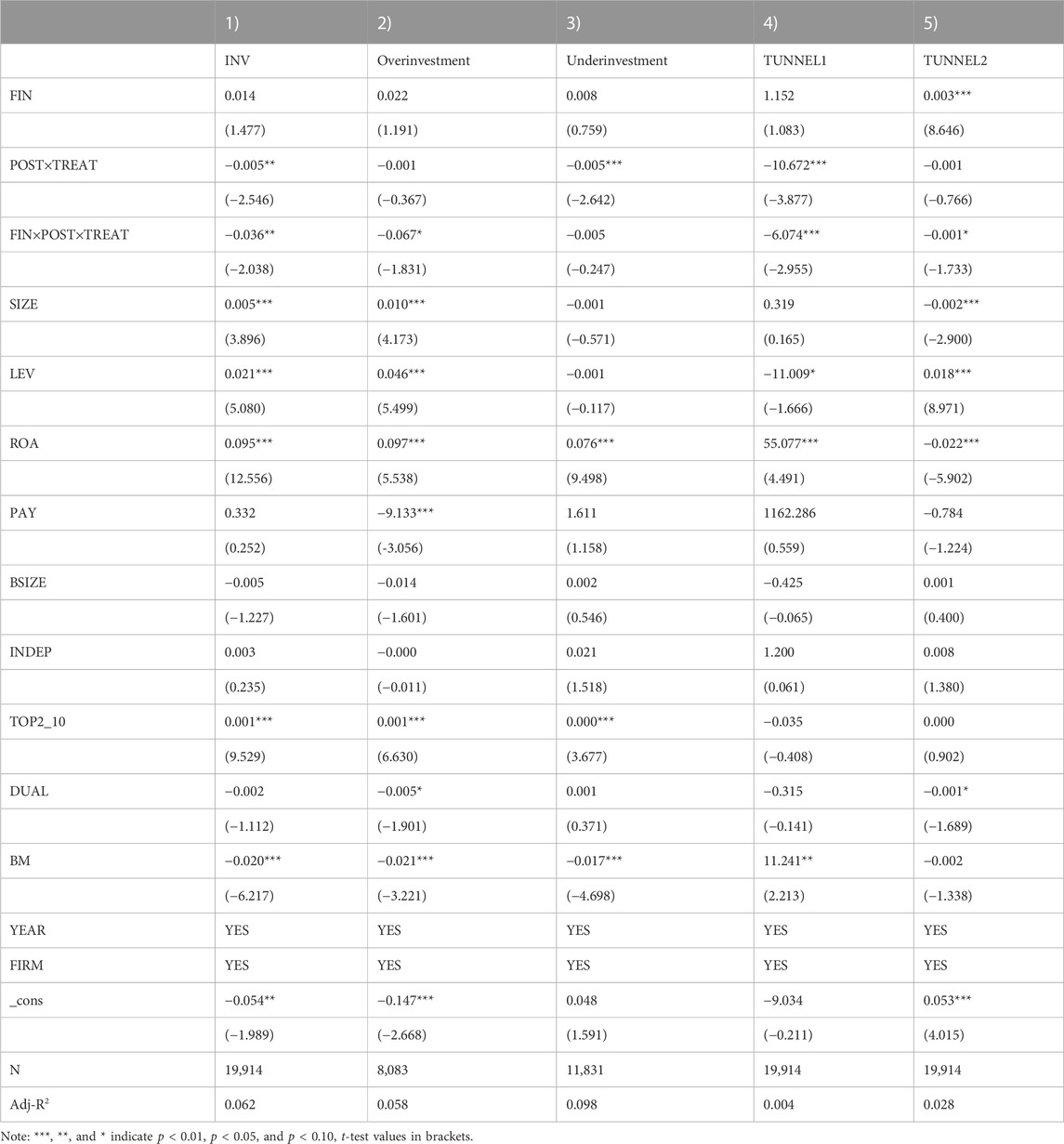

In model (6), INV denotes inefficient investment, and a correlation regression between overinvestment and underinvestment is conducted. The specific results are listed in columns (1), (2) and (3) of Table 12. The regression coefficient of FIN×POST×TREAT in Table 12 is −0.036 for the full sample, which is significantly negative at the 5% level, indicating that the green credit policy reduces the inefficient investment caused by the financialization behavior of heavily polluting enterprises. The regression coefficient of FIN×POST×TREAT is −0.067 for the overinvestment group and −0.005 for the underinvestment group; however, the results are significant only at the 10% level for the overinvestment group. These results indicate that the green credit policy reduces the inefficient investment caused by overinvestment mainly by reducing the financialization of heavily polluting enterprises.

TABLE 12. Economic consequences.

It has been verified that the green credit policy can reduce the financialization of heavily polluting enterprises and thus curb their transformation from real to virtual. Under this premise, is the implementation of green credit policy conducive to reducing the tunneling behavior of major shareholders and effectively protecting the legitimate rights and interests of small and medium-sized investors? Based on this, we study the impact of the green credit policy on short selling by major shareholders after the further implementation of the green credit policy for heavily polluting enterprises. The following model is designed for regression analysis:

Green financial policies, as management tools to guide enterprises toward green development, continuously influence their investment and business decisions. This paper uses Chinese A-share listed enterprises from 2007–2018 as research subjects to explore whether green credit policies are conducive to reducing heavily polluting enterprises’ transformation from real to virtual. It is found that 1) the implementation of the Green Credit Guidelines significantly reduced the financialization behavior of heavily polluting enterprises and curbed their transformation from real to virtual firms, and the results are unchanged after a series of robustness tests. It is also found that 2) state-owned enterprises are subject to stronger policy effects than non-state-owned enterprises, that the identified policy effects are stronger in the eastern regions of China than in the central and western regions, and that the policy effects are stronger in green provinces than in polluting provinces. Moreover, 3) credit constraints and corporate innovation play a partly mediating role in the effect of green credit policy on corporate financialization. Additionally, 4) both the level of internal corporate governance and external supervision contribute to the disincentivizing effect of green credit policy on corporate financialization. 5) Green credit policy reduces corporate financialization, the inefficient investment of heavily polluting enterprises and the tunneling behavior of the major shareholders of heavily polluting enterprises, thus improving investor protections. These findings verify the effectiveness of the Green Credit Guidelines and enrich the research on the influencing factors of corporate financialization.

The main possible contributions of this paper are as follows. 1) Based on the social context of corporate green development, we study the impact of green credit policy on corporate financialization from the perspective of credit policy changes pertaining to commercial banks, which enriches the research content regarding the framework of the relationship between macroeconomic policy and micro corporate behavior. 2) The existing studies on green credit mainly focus on defining concepts and the current status of implementation, and the studies on the impact of green credit mainly focus on financing; however, this paper is devoted to an in-depth study of the relationship between green credit and corporate financialization and to the relevant internal mechanism and possible economic consequences, thus enriching the research on the impact of green credit. 3) The national institutional design of the Green Credit Guidelines is used to study their inhibitory effect on the financialization of heavily polluting enterprises, enriching the research on the impact factors of corporate financialization.

The above findings have the following policy implications for further improving green credit policies to play a more effective governance role. 1) Green credit policies have certain effects, and the government needs to provide effective institutional support for the further improvement of the green financial market, give full play to the positive effects of green credit policies, and urge heavily polluting enterprises to proactively pursue new development models and give attention to real business development. 2) For banks and other financial institutions, due to differences in the nature of ownership, the regions in which they are located and the overall environmental regulations of different enterprises, these policy effects vary; thus, the relevant financial institutions should be firmly in compliance with the green development policy, they should comprehensively consider the development difficulties faced by different enterprises, and develop differentiated measures to promote the green, high-quality development of enterprises. 3) Heavily polluting enterprises should also actively adapt to the new trend of green development and actively transform their development to better promote the implementation effect of the green credit policy, reduce their corporate financial investment and allocate more funds to technological innovation and reform and other real business development to initiate a virtuous cycle of sustainable development.

Specifically, on the one hand, we need to improve the green financial information disclosure system by referring to the international prevailing standards and information disclosure methods, effectively solve the problem of green financial information asymmetry, improve the construction of financial infrastructure, and improve the operating efficiency of green financial services.

On the other hand, the government, enterprises and banks need to effectively cooperate and communicate, improve the efficiency of financial resource allocation, ensure the stability and long-term nature of green credit policies, actively prevent and resolve local debt risks, and guide the sustainable development of green economy.

In a word, the green credit policy is of great significance to the development of enterprises, the performance of government functions and the maintenance of social green health. All sectors of society should work together to promote the sound implementation of green credit policy and achieve the stable development of green economy.

When discussing the effectiveness of green credit policies, this study only compares the differences between heavily polluted enterprises and non-heavily polluted enterprises, ignoring that there may be different policy differences between heavily polluted enterprises and heavily polluted enterprises, as well as between non-heavily polluted enterprises and non-heavily polluted enterprises. Subsequent studies can be detailed from this perspective to further clarify the differences in the effectiveness of green credit policies, it provides a new theoretical reference for policy formulation and implementation. In addition, selecting appropriate methods to unify the variable measurement after 2018 and expanding the research sample to the latest year is also the thinking direction for future research.

Publicly available datasets were analyzed in this study. This data can be found here: https://cn.gtadata.com/, http://www.resset.cn/, https://www.cnrds.com/.

Writing-original draft, Methodology, Resources, Writing-review and editing GH; Conceptualization, Data curation WS; Formal analysis, Investigation HL; Supervision, Validation, Visualization SZ; Project administration, Software, Funding acquisition JX.

This work was supported the Philosophy and Social Sciences Research Project of Colleges and Universities in Anhui Province (Grant No. 2022AH050552).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Baron, R. M., and Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personality Soc. Psychol. 51 (6), 1173–1182. doi:10.1037/0022-3514.51.6.1173

Davis, G. F., and Kim, S. (2015). Financialization of the economy. Annu. Rev. Sociol. 41, 203–221. doi:10.1146/annurev-soc-073014-112402

Davis, L. E. (2017). Financialization and investment: A survey of the empirical literatur. J. Econ. Surv. 31, 1332–1358. doi:10.1111/joes.12242

Davis, L. (2018). Financialization, shareholder orientation and the cash holdings of US corporations. Rev. Political Econ. 30 (1), 1–27. doi:10.1080/09538259.2018.1429147

Demir, F. (2009). Financial liberalization, private investment and portfolio choice: Financialization of real sectors in emerging markets. J. Dev. Econ. 88 (2), 314–324. doi:10.1016/j.jdeveco.2008.04.002

Feng, Y., Yao, S., Wang, C., Liao, J., and Cheng, F. (2022a). Diversification and financialization of non-financial corporations: Evidence from China. Emerg. Mark. Rev. 50, 100834. doi:10.1016/j.ememar.2021.100834

Feng, Y., Yu, Q., Nan, X., and Cai, Y. (2022b). Can employee stock ownership plans reduce corporate financialization? Evidence from China. Econ. Analysis Policy 73, 140–151. doi:10.1016/j.eap.2021.11.002

Gao, D., Mo, X., Duan, K., and Li, Y. (2022). Can green credit policy promote firms' green innovation? Evidence from China. Sustainability 14 (7), 3911. doi:10.3390/su14073911

Ge, Y., and Zhu, Y. (2022). Boosting green recovery: Green credit policy in heavily polluted industries and stock price crash risk. Resour. Policy 79, 103058. doi:10.1016/j.resourpol.2022.103058

Guo, L., Tan, W., and Xu, Y. (2022). Impact of green credit on green economy efficiency in China. Environ. Sci. Pollut. Res. 29 (23), 35124–35137. doi:10.1007/s11356-021-18444-9

Harrington, B. (2017). Trusts and financialization. Socio-Economic Rev. 15 (1), 31–63. doi:10.1007/s11577-018-0537-7

He, L., Zhang, L., Zhong, Z., Wang, D., and Wang, F. (2019). Green credit, renewable energy investment and green economy development: Empirical analysis based on 150 listed companies of China. J. Clean. Prod. 208, 363–372. doi:10.1016/j.jclepro.2018.10.119

Hu, Y., Jiang, H., and Zhong, Z. (2020). Impact of green credit on industrial structure in China: Theoretical mechanism and empirical analysis. Environ. Sci. Pollut. Res. 27 (10), 10506–10519. doi:10.1007/s11356-020-07717-4

Jiang, F., Shen, Y., and Cai, X. (2022). Can multiple blockholders restrain corporate financialization? Pacific-Basin Finance J. 75, 101827. doi:10.1016/j.pacfin.2022.101827

Jin, X. M., Mai, Y., and Cheung, A. W. K. (2022). Corporate financialization and fixed investment rate: Evidence from China. Finance Res. Lett. 48, 102898. doi:10.1016/j.frl.2022.102898

Kohler, K., Guschanski, A., and Stockhammer, E. (2018). Verteilungseffekte von Finanzialisierung. Kolner Z. Soz. Sozpsychol. 70 (1), 37–63. doi:10.1007/s11577-018-0537-7

Kohler, K., Guschanski, A., and Stockhammer, E. (2019). The impact of financialisation on the wage share: A theoretical clarification and empirical test. Camb. J. Econ. 43 (4SI), 937–974. doi:10.1093/cje/bez021

Lechner, M. (2002). Program heterogeneity and propensity score matching: An application to the evaluation of active labor market policies. Rev. Econ. Statistics 84 (2), 205–220. doi:10.1162/003465302317411488

Li, S., Liu, Q., Lu, L., and Zheng, K. (2022). Green policy and corporate social responsibility: Empirical analysis of the Green Credit Guidelines in China. J. Asian Econ. 82, 101531.

Li, W., Cui, G., and Zheng, M. (2022). Does green credit policy affect corporate debt financing? Evidence from China. Environ. Sci. Pollut. Res. 29 (4), 5162–5171. doi:10.1007/s11356-021-16051-2

Li, Z., Wang, Y., Tan, Y., and Huang, Z. (2020). Does corporate financialization affect corporate environmental responsibility? An empirical study of China. Sustainability 12 (9), 3696. doi:10.3390/su12093696

Lian, Y., Gao, J., and Ye, T. (2022). How does green credit affect the financial performance of commercial banks? --Evidence from China. J. Clean. Prod. 344, 131069. doi:10.1016/j.jclepro.2022.131069

Liu, L., and He, L. (2021). Output and welfare effect of green credit in China: Evidence from an estimated DSGE model. J. Clean. Prod. 294, 126326. doi:10.1016/j.jclepro.2021.126326

Liu, S., Xu, R., and Chen, X. (2021). Does green credit affect the green innovation performance of high-polluting and energy-intensive enterprises? Evidence from a quasi-natural experiment. Environ. Sci. Pollut. Res. 28 (46), 65265–65277. doi:10.1007/s11356-021-15217-2

Liu, X., Wang, E., and Cai, D. (2019). Green credit policy, property rights and debt financing: Quasi-natural experimental evidence from China. Finance Res. Lett. 29, 129–135. doi:10.1016/j.frl.2019.03.014

Luo, S., Yu, S., and Zhou, G. (2021). Does green credit improve the core competence of commercial banks. Based on quasi-natural experiments in China. Energy Econ. 100, 105335. doi:10.1016/j.eneco.2021.105335

Lyu, B., Da, J., Ostic, D., and Yu, H. (2022). How does green credit promote carbon reduction? A mediated model. Front. Environ. Sci. 10, 531. doi:10.3389/fenvs.2022.878060

Maria Diez-Esteban, J., Farinha, J. B., and Diego Garcia-Gomez, C. (2016). The role of institutional investors in propagating the 2007 financial crisis in Southern Europe. Res. Int. Bus. Finance 38, 439–454. doi:10.1016/j.ribaf.2016.07.006

Matsumoto, A. (2020). Considerations on inequality, corporate governance, and financialization. J. Econ. Issues 54 (2), 334–340. doi:10.1080/00213624.2020.1743141

Modell, S., and Yang, C. (2018). Financialisation as a strategic action field: An historically informed field study of governance reforms in Chinese state-owned enterprises. Crit. Perspect. Account. 54, 41–59. doi:10.1016/j.cpa.2017.09.002

Peng, B., Yan, W., Elahi, E., and Wan, A. (2022). Does the green credit policy affect the scale of corporate debt financing? Evidence from listed companies in heavy pollution industries in China. Environ. Sci. Pollut. Res. 29 (1), 755–767. doi:10.1007/s11356-021-15587-7

Richardson, S. (2006). Over-investment of free cash flow. Rev. Account. Stud. 11 (2-3), 159–189. doi:10.1007/s11142-006-9012-1

Sansyzbayeva, G., Temerbulatova, Z., Zhidebekkyzy, A., and Ashirbekova, L. (2020). Evaluating the transition to green economy in Kazakhstan: A synthetic control approach. J. Int. Stud. 13 (1), 324–341. doi:10.14254/2071-8330.2020/13-1/21

Siepel, J., and Nightingale, P. (2014). Anglo-Saxon governance: Similarities, difference and outcomes in a financialised world. Crit. Perspect. Account. 25 (1), 27–35. doi:10.1016/j.cpa.2012.10.004

Streimikiene, D. (2022). Energy poverty and impact of Covid-19 pandemics in Visegrad (V4) countries. J. Int. Stud. 15 (1), 9–25. doi:10.14254/2071-8330.2022/15-1/1

Streimikiene, D. (2022). Renewable energy technologies in households: Challenges and low carbon energy transition justice. Econ. Sociol. 15 (3), 108–120. doi:10.14254/2071-789x.2022/15-3/6

Tan, X., Xiao, Z., Liu, Y., Taghizadeh-Hesary, F., Wang, B., and Dong, H. (2022a). The effect of green credit policy on energy efficiency: Evidence from China. Technol. Forecast. Soc. Change 183, 121924. doi:10.1016/j.techfore.2022.121924

Tan, X., Yan, Y., and Dong, Y. (2022b). Peer effect in green credit induced green innovation: An empirical study from China's Green Credit Guidelines. Resour. Policy 76, 102619. doi:10.1016/j.resourpol.2022.102619

Tomaskovic-Devey, D., Lin, K., and Meyers, N. (2015). Did financialization reduce economic growth? Socio-Economic Rev. 13, 525–548. doi:10.1093/ser/mwv009

Wang, H., Qi, S., Zhou, C., Zhou, J., and Huang, X. (2022). Green credit policy, government behavior and green innovation quality of enterprises. J. Clean. Prod. 331, 129834. doi:10.1016/j.jclepro.2021.129834

Wang, Y., Lei, X., Long, R., and Zhao, J. (2020). Green credit, financial constraint, and capital investment: Evidence from China's energy-intensive enterprises. Environ. Manag. 66 (6), 1059–1071. doi:10.1007/s00267-020-01346-w

Wen, H., Lee, C., and Zhou, F. (2021). Green credit policy, credit allocation efficiency and upgrade of energy-intensive enterprises. Energy Econ. 94, 105099. doi:10.1016/j.eneco.2021.105099

Xu, X., and Li, J. (2020). Asymmetric impacts of the policy and development of green credit on the debt financing cost and maturity of different types of enterprises in China. J. Clean. Prod. 264, 121574. doi:10.1016/j.jclepro.2020.121574

Yin, W., Zhu, Z., Kirkulak-Uludag, B., and Zhu, Y. (2021). The determinants of green credit and its impact on the performance of Chinese banks. J. Clean. Prod. 286, 124991. doi:10.1016/j.jclepro.2020.124991

Zhang, A., Deng, R., and Wu, Y. (2022a). Does the green credit policy reduce the carbon emission intensity of heavily polluting industries? -Evidence from China's industrial sectors. J. Environ. Manag. 311, 114815. doi:10.1016/j.jenvman.2022.114815

Zhang, K., Wang, Y., and Huang, Z. (2021). Do the green credit guidelines affect renewable energy investment? Empirical research from China. Sustainability 13 (16), 9331. doi:10.3390/su13169331

Zhang, K., and Zhou, X. (2022). Is promoting green finance in line with the long-term market mechanism? The perspective of Chinese commercial banks. Mathematics 10 (9), 1374. doi:10.3390/math10091374

Zhang, W., Liu, Y., Zhang, F., and Dou, H. (2022b). Green credit policy and corporate stock price crash risk: Evidence from China. Front. Psychol. 13, 891284. doi:10.3389/fpsyg.2022.891284

Zhang, Y., Li, X., and Xing, C. (2022c). How does China's green credit policy affect the green innovation of high polluting enterprises? The perspective of radical and incremental innovations. J. Clean. Prod. 336, 130387. doi:10.1016/j.jclepro.2022.130387

Zhang, Z., Duan, H., Shan, S., Liu, Q., and Geng, W. (2022d). The impact of green credit on the green innovation level of heavy-polluting enterprises-evidence from China. Int. J. Environ. Res. Public Health 19 (2), 650. doi:10.3390/ijerph19020650

Keywords: green credit policy, corporate financial investment, green economy, sustainability, inefficient corporate investment, major shareholders’ tunneling

Citation: Hu G, Strielkowski W, Li H, Zenchenko S and Xu J (2023) Can green credit policy under the concept of green economy curb corporate financialization to promote sustainable development?. Front. Environ. Sci. 11:1127380. doi: 10.3389/fenvs.2023.1127380

Received: 19 December 2022; Accepted: 09 January 2023;

Published: 17 January 2023.

Edited by:

Muhammad Zahid Rafique, Shandong University, ChinaReviewed by:

Magdalena Radulescu, University of Pitesti, RomaniaCopyright © 2023 Hu, Strielkowski, Li, Zenchenko and Xu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Junwei Xu, eHVqdW53ZWkwNDIwQDEyNi5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.