Jianti Li

Jianti Li Xin Luo2*

Xin Luo2* Dawei Feng

Dawei Feng

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 03 April 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1120022

This article is part of the Research TopicEnvironmental Risk and Corporate BehaviourView all 30 articles

Avoiding the transfer of “carbon” and encouraging the digestion of “carbon” are essential to promote the green and low-carbon transformation of China’s economy. In accordance with the standpoint of off-site subsidiaries, this paper examines the transfer of “carbon” from high-carbon enterprises using the data of A-share listed companies from 2009 to 2018 using a DID approach and the 2013 China carbon emissions trading pilot as a quasi-natural experiment. As demonstrated by the reach findings: (1) Part of the effect of corporate “carbon reduction” is achieved by shifting high-carbon sectors. (2) As demonstrated in mechanism analysis, when high-carbon companies face the dual cost pressure of R&D expenditure and purchasing carbon trading rights, they will establish subsidiaries to avoid the parent company’s pressure to lessen emissions. As revealed in heterogeneity analysis. (3) companies with stronger R&D capabilities and higher success rates are more willing to respond to the impact of carbon trading policies with technological upgrades. Companies with weaker R&D capabilities and higher failure rates are more likely to choose to transfer “carbon” to avoid the “dual cost” of R&D failures. (4) Owing to the constraint of the migration threshold, the trajectory of “carbon” transfer is primarily domestic interregional transfer supplemented by cross-country transfer. (5) Larger enterprises emitting more “carbon”, are not only more likely to pay more “carbon” reduction costs in the face of carbon policy shocks, are but also more likely to shift “carbon”. This study not only provides a new perspective to explain the “carbon” transfer phenomenon in China, but also provides crucial policy implications for further strengthening environmental governance as well as regional joint prevention and control in China.

How to effectively cut down “carbon” emissions has become the focus of environmental policies in the world today, among which the carbon emissions trading system is considered to be a paramount tool for cutting down “carbon” emissions and mitigating climate warming. In 2013, China officially launched the carbon trading market in the pilot regions. As demonstrated by the research findings, implementing the carbon trading policies has not only promoted the R&D and innovation of green technologies in the pilot regions, but also has exerted a profound influence on the “emission reduction” of enterprises (Pan and Wang, 2022; Wu et al., 2022), but is there any “underhanded operation” in this? Is “carbon reduction” on the basis of enterprises’ own internal transformation or on the transfer of “carbon" (In this paper, the transfer of carbon emissions by enterprises across regions is uniformly referred to as “carbon” transfer)? There is little discussion in the literature.

As China’s environmental protection policy system continues to improve and the types of policies as well as instruments become more diverse, especially after the implementation of carbon trading policies, high-carbon companies will face pressure from both the quantity and intensity of environmental regulations. To avoid being closed down and banned, enterprises must either transform and upgrade or transfer “carbon”. The former is in line with policy expectations, using environmental regulation to “push” high-carbon enterprises to transform and upgrade, but the initial investment in this approach is large and slow. Apart from that, enterprises may face the dual cost of R&D expenditure and the cost of purchasing carbon emission rights arising from the failed transformation. The transfer of “carbon” can effectively avoid the disadvantageous influence of carbon trading policies. In terms of research on carbon transfer in China. Han et al. (2020) found that Jiangsu, Shandong, Inner Mongolia, Hebei and Liaoning have the largest carbon emission outflows, with more than 70.00 Mt to other domestic provinces. While Henan, Shanxi, Guangdong, Inner Mongolia and Yunnan are major importing regions, most of which with more than 60.0 Mt of domestic carbon emission inflows, this partly explains the shift in China’s carbon emissions. In recent years, this pollution transfer, or “pollution refuge”, hypothesis has been extensively discussed by domestic and foreign scholars (Brunnermeier and Levinson, 2004; Erdogan, 2014; Song et al., 2021; Shen et al., 2017). Most scholars have also confirmed the existence of this hypothesis. What’s more, most of these studies fix their attention on the overall transfer of firms, but the drawback is also more apparent, namely, the high cost of relocation. On this basis, scholars began to concentrate on the lower-cost and more concealed method of pollution transfer, i.e., transferring pollution through the intracompany group (Becker and Henderson, 2000; Keller and Levinson, 2002; List et al., 2003; Song et al., 2021; Dechezleprêtre et al., 2022). Aside from that, there are certain restrictions on such transfers: not only does it require the company to have an intragroup company in an off-site location, but it is also limited by the geographical influence of the intragroup company. On this basis, this paper probed deep into the transfer of high-carbon emitting sectors through the establishment of subsidiaries across regions under carbon trading policies. This transfer mode not only tremendously expands the market scale of the enterprise and cuts down transaction costs, but also makes full use of the local resource endowment through the rational distribution of subsidiaries, thus noticeably ameliorating the overall income of the enterprise. Meanwhile, it enables the parent company to avoid the carbon trading policy and alleviates the pressure on the parent company to “lessen emissions and carbon”. Even when the parent company shifts too much carbon emissions to cut down the amount of carbon emissions below the set amount of carbon trading, it can sell carbon trading rights to gain some revenue.

The carbon trading policy is originally intended to help enterprises “curtail carbon emissions” and force them to transform and upgrade, rather than inducing them to transfer “carbon”. This not only defeats the original intention of the state to “lessen carbon emissions” in general but also weakens the guiding role of carbon trading policy. It also cut downs the cost of carbon emissions, weakens the motivation of enterprises to “lessen emissions and decrease carbon”, and curbs the momentum of green technology innovation, transformation and upgrading of enterprises. Under this background, it is essential to probe deep into the intrinsic motivation and characteristics of the transfer of “carbon” by high-carbon enterprises. On this basis, to “prescribe the right medicine” to avoid the transfer of “carbon” by high-carbon enterprises, so as to ensure the effective implementation of carbon trading policy, which is crucial to promote the green and low-carbon transformation of China’s economy.

This paper is also bound up with the literature on carbon trading systems. Most scholars domestically and internationally have affirmed the role of carbon trading policies in upgrading regional industrial structures (Liu and Chen, 2022). On the enterprise side, carbon trading policy is advantageous for pushing R&D innovation ahead (Liu and Zheng, 2017), elevating the efficiency of corporate investment and ameliorating the short-term value of enterprises (Zhang and Wu, 2022). The most relevant paper examined the impact of carbon trading on OFDI and finds that regions heighten their OFDI on account of carbon trading policies (Guo and Xiao, 2022), which confirms that firms shift their “carbon” to cut down the pressure to lessen emissions after implementing carbon trading policies. Nevertheless, the above literature investigated nothing more than the impact of carbon trading policies at the provincial level. What’s more, it failed to explore the impact of carbon trading policies at the firm level. As a consequence, our paper is intended to examine the impact at the firm level to further fill the gap left in the above literature. Aside from that, the literature mentioned above investigated nothing but the impact of carbon trading policies on the transfer of carbon across borders. But it did not consider that most enterprises are unable to transfer carbon across borders as a result of their own business level and economic capacity. This paper further investigates the impact of carbon emissions trading policy on the transfer of pollution by enterprises not only in domestic cross-regional “carbon” transfer but also in the transnational transfer of enterprises.

Compared with the above literature, the primary contributions of this paper are as follows.

First and foremost, this paper examines “carbon” transfer under a carbon trading policy in accordance with the viewpoint of off-site subsidiaries, which complements and enriches the “pollution refuge” hypothesis. Most of the existing studies on the pollution refuge hypothesis fix their attention on the way of transfer within the enterprise or group, but there are few papers that examine the transfer of pollution in the way of setting up subsidiaries.

Furthermore, this paper expands the issue of “carbon reduction” under a carbon trading policy in accordance with the viewpoint of “carbon” transfer. Most of the existing studies on carbon trading systems concentrate on the impact of carbon trading policies on the upgrading of regional industrial structure and technological innovation of enterprises. Nonetheless, is this on the basis of enterprises’ own internal transformation and upgrading, or is it in line with enterprises’ transformation and upgrading by transferring high “carbon” sectors? There is little explanation in existing studies. In this paper, we explain that the transformation and upgrading of enterprises or regions is partly in line with the transfer of high carbon sectors. This paper expands on the issue of “carbon reduction” under the carbon trading policy.

Finally, this paper provides policy ideas for promoting the green and low-carbon transformation of China’s economy. The original intention of carbon trading policy is to promote enterprises to “reduce carbon emissions” rather than to induce enterprises to transfer “carbon”. This not only goes against the country’s original aspiration of “reducing carbon emission” in total volume but also weakens the guiding role of carbon trading policy. It also reduces the cost of carbon emissions for enterprises, weakens the incentive for enterprises to “reduce carbon emissions”, and restrains the momentum of enterprises to carry out green technology innovation, transformation and upgrading. Based on an in-depth analysis of the internal motivation and characteristics of the transfer of “carbon” by high-carbon enterprises, this paper provides policy ideas for avoiding the transfer of “carbon” by high-carbon enterprises, ensuring the effective implementation of carbon trading policies, and promoting the green and low-carbon transformation of China’s economy.

Carbon trading is an economic instrument that uses market mechanisms to deal with the climate problem. It uses market forces to transform the environment into a factor of production and trade carbon emission rights as a valuable asset in the market. Since the Kyoto Protocol came into effect, carbon trading systems have developed rapidly. Aside from that, countries and regions have started to establish intraregional carbon trading systems to put their carbon emission reduction commitments into reality. Seventeen carbon trading systems were built across four continents in the decade from 2005 to 2015, and in recent years, the percentage of carbon emissions covered by carbon trading was more than two times higher than that covered by EU carbon trading when it was launched in 2005. China’s carbon emissions trading system started with the State Council’s Decision on Accelerating the Cultivation and Development of Strategic Emerging Industries issued in 2010. In October 2011, the National Development and Reform Commission issued the Notice on the Pilot Work of Carbon Emissions Trading, approving the pilot work of carbon emissions trading in seven provinces and cities, namely, Beijing, Tianjin, Shanghai, Chongqing, Hubei, Guangdong and Shenzhen. Since 2013, the seven pilot carbon markets have started online trading one after another, covering nearly 3,000 key emission units in more than 20 industries, such as electricity, steel and cement. As of 30 September 2021, the cumulative volume of allowances traded in the seven pilot carbon markets was 495 million tons of carbon dioxide equivalent, with a turnover of 11.978 billion yuan. The compliance rate of key emission units remained high. Furthermore, the total amount and intensity of carbon emissions within the market coverage have maintained a double downward trend, effectively promoting relevant enterprises to actively reduce GHG emissions. Nonetheless, is this in line with the inherent transformation of the enterprises themselves, or is it on the basis of the transfer of “carbon”? Further investigation is needed.

Since the connotation of regional carbon emission transfer is similar to carbon leakage, the carbon emission transfer can also be defined as the increase in emissions outside a region, as a direct result of the policy to cap emission in this region (Reinaud, 2008). There are three primary explanations for the formation mechanisms of carbon emission transfer. The first one is “free-rider leakage” (Carraro and Siniscalo, 1992). The second one is “supply side leakage” (Sinn, 2008). The third one is “specialization leakage”. Siebert (1979) and Copeland and Taylor (2005) pointed out that to reduce carbon emissions, unilateral introduction of carbon prices in developed countries would shift comparative advantage towards developing countries without climate policy, and lead to increased production of carbon intensive goods in those countries. Further, Song et al. (2021) find that when different firms within an enterprise group face different emission rates, firms located in areas with high emission rates shift their production, especially pollution-intensive production, to firms in areas with low emission rates, which in turn leads to pollution transfer within the enterprise group. Based on the above discussion, this paper argues that after the implementation of carbon trading policy, enterprises can reduce their carbon emissions through technology upgrading, but this practice is risky and enterprises may suffer from the double costs of R&D expenditures and purchasing carbon emission rights. Firms are more likely to shift their carbon emissions considering the uncertainty of technological upgrading. Specifically, when enterprises upgrade their green technologies, they will inevitably bring about an increase in R&D costs, and on the other hand, they may face the double cost of having to pay for the purchase of carbon emission rights even after their R&D fails. Even if an enterprise succeeds in research and development and obtains proceeds from the sale of carbon emission rights, the research and development process costs a lot, and after deducting various costs such as research and development, the actual proceeds that an enterprise can obtain are relatively small. In particular, for companies with poor R&D capabilities, reducing carbon emissions through technological upgrades exacerbates corporate costs. Rational companies will choose a less costly way to reduce their carbon emissions, i.e., by shifting their carbon emissions to a different location by establishing a subsidiary in a different location. This approach allows companies to avoid the various costs associated with carbon trading policies and alleviates the pressure on the parent company to reduce emission.

Aside from cost drivers, there are also benefits to be gained from transferring “carbon” by establishing subsidiaries across regions. From the viewpoint of transaction costs, enterprises trading in off-site markets will bring about an increment in transaction costs (Cao et al., 2019). Establishing off-site subsidiaries not only expands the market scale of enterprises but also strengthens cooperation with off-site enterprises and curtails the transaction costs of parent companies in off-site locations. Aside from that, through the reasonable layout of the geographical location of subsidiaries, enterprises are able to directly allocate the resource endowment of off-site locations to lessen the cost of acquiring raw materials (Cao et al., 2015).

In summary, this paper holds a standpoint that when confronted with carbon trading policies, companies will choose to establish subsidiaries to transfer “carbon” to avoid the costs of carbon trading policies and obtain certain benefits.

This paper selected the data of Chinese A-share listed companies in Shanghai and Shenzhen from 2009 to 2018 as the research object, and the firm-level data involved are predominantly from the Wind and CSMAR databases. To effectively examine the impact of carbon trading policies on the off-site “carbon” transfer of enterprises, this paper has conducted some screening of the sample. First, since the carbon trading policy primarily affects high-carbon industries, the full sample regression will give rise to biased policy estimation. For this reason, according to the data collected by the World Resources Institute (WRI), the emissions from the power generation and heating industry account for 41.6% of China’s total carbon emissions. Meanwhile, this paper draws lessons from Zhang and Wu (2022) to select extractive industries (B), manufacturing industries (C), and electricity, gas and water production and supply industries (D) as high-carbon industries as the predominant objects of investigation in accordance with the Industry Classification Guidelines for Listed Companies issued by the China Securities Regulatory Commission in 2012. Second, to avoid the impact of outliers on the regression, a 1% reduction in the continuous variables was conducted in this paper. Third, financial data outliers were excluded. Fourth, the sample whose parent company had migrated out of the original province from 2009 to 2018 was excluded.

In this paper, we used the carbon trading pilot implemented in 2013 as a quasi-natural experiment to explore the impact of carbon trading policies on the behaviors of high-carbon firms in shifting “carbon” emissions using the Difference-in-Differences approach (DID). As Shenzhen belongs to Guangdong, for this reason the experimental group of this paper is Beijing, Tianjin, Shanghai, Chongqing, Guangdong, Hubei six provinces and cities, while Fujian Province joined the pilot in 2016. To avoid estimation bias, this paper will remove the sample of enterprises in Fujian Province. The other 25 provinces will be employed as the control group. The dummy variable Treat is whether the province is a pilot province for carbon emissions trading; in the event that the province is a pilot province for carbon emissions trading, then Treat = 1; conversely, providing that the province does not obtain pilot carbon emissions trading, then Treat = 0. The dummy variable period is the year in which pilot carbon emissions trading starts; in the event that it is in 2013 and later, then period = 1; conversely, before 2013, then period = 0. The model is constructed as follows.

where

Enterprise off-site transfer of “carbon” behavior:

The explanatory variable:

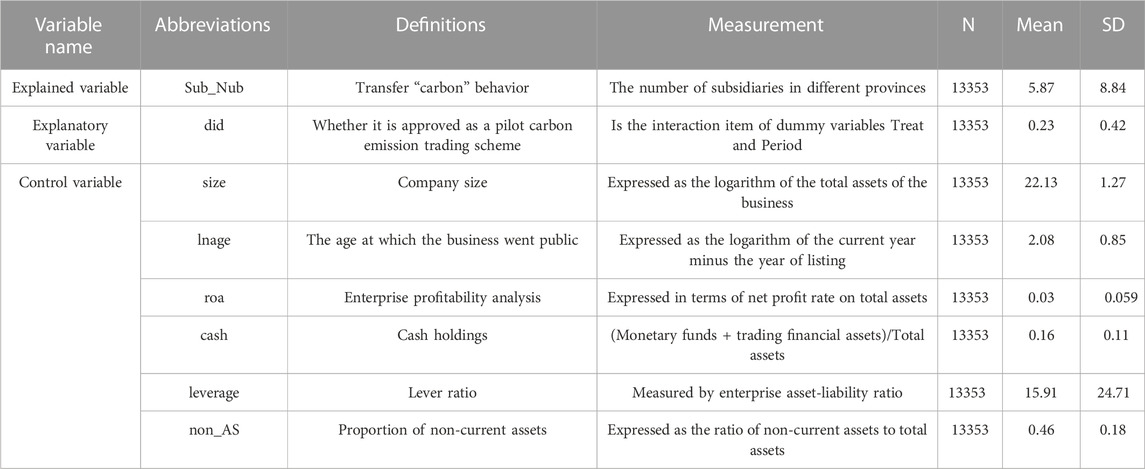

Apart from implementing carbon trading policies on enterprises’ transfer of “carbon” across regions, some factors at the enterprise level will also affect the transfer behavior of “carbon”, and the following control variables will be selected in this paper. (i)Firm size (size), expressed as the logarithm of the firm’s total assets. (ii) Year in which the company was listed (lnage) by subtracting the logarithm of the year in which it was listed from the current year. (iii) Corporate profitability (ROA), expressed as net profit margin on total assets. (iv) Cash holdings (CASH), cash holdings = (monetary funds + financial assets held for trading)/total assets. (v) leverage (leverage), measured by the firm’s gearing ratio. (vi) Noncurrent assets ratio (non_AS), expressed as the ratio of noncurrent assets to total assets. Descriptive statistics for the chief variables are given in Table 1.

TABLE1. Descriptive statistics.

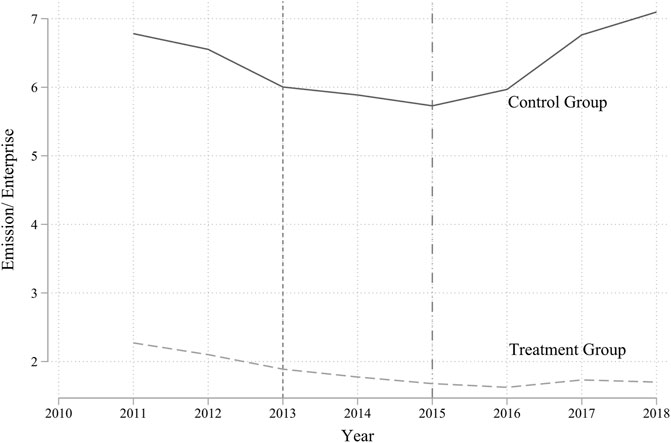

Before conducting the empirical analysis, this paper conducted a characteristic factual analysis of the trend of carbon emissions per firm in the experimental and control groups. The current energy mix in China is dominated by coal and oil consumption, accounting for 56% and 18.5% of total energy consumption, respectively, or a combined 74.5% (data from the National Bureau of Statistics 2021). For this reason, this paper fixes its attention on the amount of carbon dioxide produced by enterprises consuming coal and oil, where enterprise unit carbon emissions = total carbon emissions from coal and oil/total number of enterprises. As apparently revealed in the graph, in 2015, the carbon emissions per unit of relevant enterprises in the control group are progressively rising, and there is a lag of “carbon” migration. This is a preliminary reflection of the fact that enterprises are moving carbon. As in Figure 1.

FIGURE 1. Facts about the characteristics of “carbon” migration of enterprises.

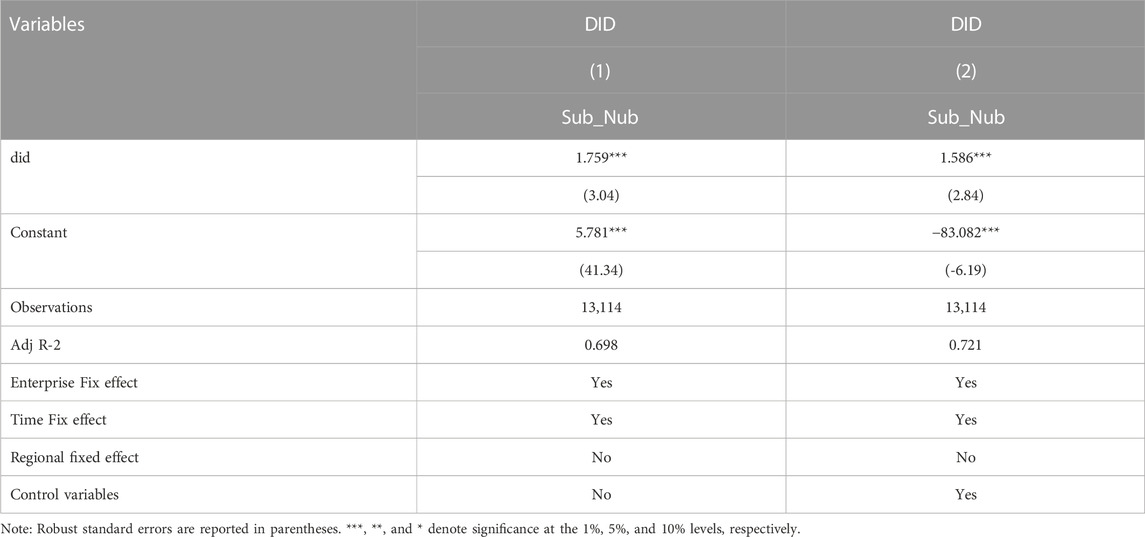

This paper empirically examines the association between carbon trading policies and enterprises’ off-site transfer of “carbon” behavior on the basis of model (1). To prevent the omission of firm-level factors that do not vary over time from biasing the regression results, firm fixed effects are included in all regressions; to exclude the effect of factors associated with year characteristics, all regression results include time fixed effects. The regression results are exhibited in Table 2, where column (1) does not include control variables. As demonstrated by the research findings, carbon trading policies significantly drive the transfer of “carbon” from high-carbon firms in China. In column (2), the coefficient is still noticeably positive after adding further control variables. The above results tentatively confirm the impact of carbon trading policy on the transfer of “carbon” by enterprises across regions.

TABLE 2. Baseline regression.

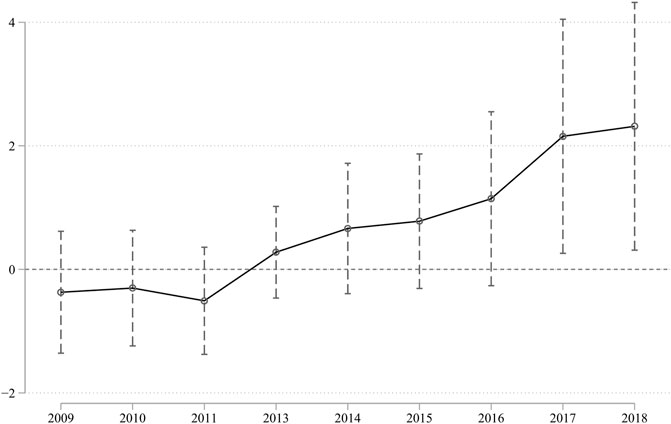

In the benchmark regression analysis, this paper identifies the causal effect of carbon trading policy on the cross-regional transfer of “carbon” behavior of high-carbon firms in China, but this requires a DID parallel trend test to verify the validity of these results. In accordance with this, this paper draws on Beck et al. (2010) for a parallel trend test. Figure 2 shows the parallel trend results of the Difference-in-Differences model of this paper. The findings of this paper pass the parallel trend test, and the impact of carbon trading policy on the cross-regional transfer of “carbon” behavior of high-carbon enterprises in China has progressively elevated after implementing carbon trading policies.

FIGURE 2. Parallel trend test.

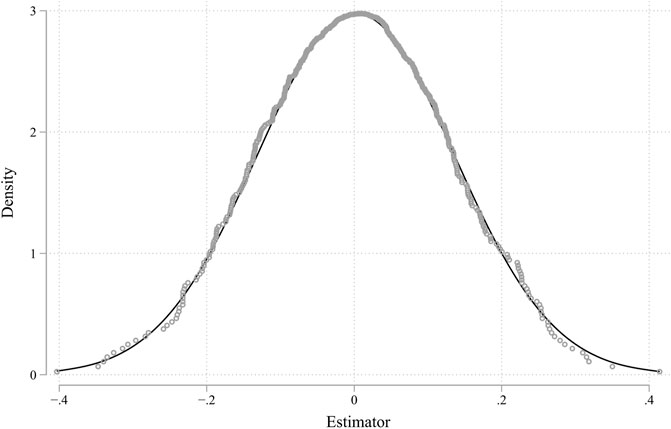

To further ensure the validity of the regression results, a placebo test with experimental group randomization was adopted to verify the robustness of the results. Randomizing the experimental group is a random sampling of the experimental group variables a certain number of times, and then observing whether the coefficients of the randomized DID are concentrated approximately 0 and whether the coefficients significantly deviate from their true values. In this paper, by using a placebo test with 500 random samples of the interaction term and plotting the distribution of regression coefficients (Figure 3), the majority of coefficients are concentrated approximately 0 and normally distributed, and the mean value is far from the true value, which means that the effect of carbon emissions trading policy on the transfer of “carbon” by enterprises across regions is not influenced by other unobserved factors and satisfies the placebo test.

FIGURE 3. Placebo test.

To better select the control group, this paper further adopts the propensity score matching method to test the causal correlation between carbon trading policy and the cross-regional transfer of “carbon” behavior of enterprises under other similar conditions. In this paper, we build a logit model for whether it is a carbon trading policy region, match Chinese provinces using the nearest 1:1 matching, and then employ the matched sample for regression. The estimation results of PSM-DID were obtained as illustrated in Table 3. As illustrated by the research findings obtained from Table 3, the estimated coefficient of the PSM-DID model is noticeably positive, and the magnitude of the coefficient is 1.693, which is approximately the same as the baseline estimation result of 1.586. The above analysis shows that endogeneity is mitigated to some extent by PSM-DID, and the results are roughly the same as the benchmark results, i.e., carbon trading policies promote the “carbon” transfer of enterprises across regions.

TABLE 3. Robustness test.

By combining relevant documents, it is found that the Green Credit Guidelines may interfere with the results of this paper during the sample period. For reference to the practice of Fan and Li (2022), this paper adds the Didm variable, Didm = Time*Post, into the benchmark regression. Where Time is the dummy variable of the year. If the number of years is greater than or equal to 2012, Time = 1; otherwise, Time = 0. Post is the dummy variable of a high-polluting enterprise. Post = 1 when it is a high-polluting enterprise; otherwise, Post = 0. The estimated results are shown in column (2) of Table 3. When Didm is added, the estimated coefficient is still significantly negative at the 1% level. After removing the interference of green credit policies, the results remain robust.

Since the characteristic variables at the provincial level may cause bias in the estimation results, this paper further adds the control variables at the provincial level, and the results are shown in Table 3. The variable of the per capita GDP coefficient (PerGDP) of each region was added into column (3) of Table 3, and the estimated coefficient of DID was still significantly positive at the 1% level. In addition, since regional labor income is an important factor affecting enterprise relocation, the variables of regional labor income (Lincome) are added into column (4) of Table 3, and it can be seen that the coefficient of did is still significantly positive at the 1% level. Finally, the regional fixed effect was further added into column (5), and the regional-level characteristic variables were further controlled to alleviate the interference of regional-level characteristic variables on the results. After the provincial fixed effect was added, the DID coefficient was still significantly positive.

As suggested by the above analysis, carbon trading policies have prompted high-carbon emitting enterprises to transfer “carbon” across regions. Nevertheless, the mechanisms involved still remains unclear and will be explored in this subsection.

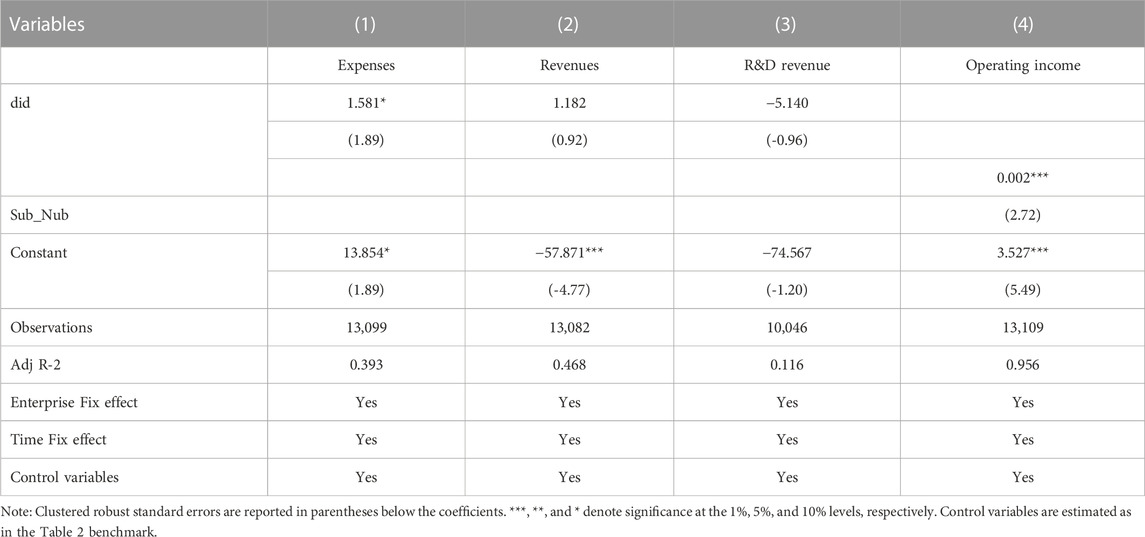

On the basis of the Interim Regulations on Accounting Treatment of Carbon Emission Trading issued by the Ministry of Finance, the carbon emission allowances sold and purchased by enterprises are recorded as “nonoperating income” and “nonoperating expense”, respectively; as a consequence, this paper will examine the impact of carbon trading policy on the nonoperating expense and nonoperating income of enterprises to examine the impact on enterprise cost. The results are displayed in Table 4. The coefficient of carbon trading policy on nonoperating expenses is remarkably positive, which means that carbon trading policy elevates the costs incurred by enterprises in the process of carbon trading (including the cost of purchasing carbon emission rights and the cost of participating in carbon emission rights trading). Column (2) of Table 4 examines the proceeds obtained by the sale of carbon emission rights by enterprises with lower than the required carbon emissions after implementing the carbon trading policies. As demonstrated in Table 4, the coefficient of (2) is positive but not significant, i.e., enterprises with lower than the required carbon emissions do not obtain corresponding returns from carbon emission rights trading. This is because, despite the fact that companies can gain from the sale of carbon credits, they also incur certain transaction costs during the sale process, and when carbon trading is first implemented, it's essential for companies to bear higher labor and material costs for preparation, which to some extent offsets the gains from the sale of carbon credits. As clearly revealed by the above results, the cost impact of carbon trading policy in the initial stage exceeds its benefit impact. Under such circumstance, rational companies will take initiatives to shift “carbon” to avoid the cost of carbon trading.

TABLE 4. Mechanism analysis.

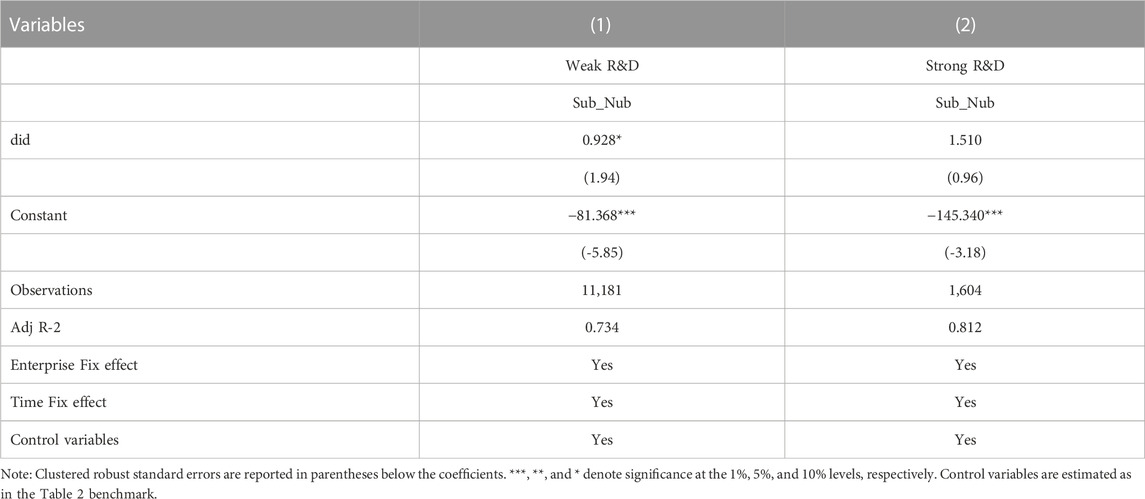

Second, this paper further examines the analysis of R&D benefits after implementing the carbon emissions trading policies, in which the explained variable is green technology R&D benefits (efficient), efficient = nonoperating income \ total R&D amount. The results are exhibited in column (3) of Table 4, and it is easy to see that the DID coefficient is insignificant, i.e., the enterprises have not gained the benefits of technological upgrading temporarily after implementing the carbon trading policies. This is because when enterprises upgrade their green technology, on the one hand, it will inevitably bring an augment in R&D costs, and on the other hand, they may face the dual cost of purchasing carbon emission rights even providing that the R&D fails. Even if an enterprise succeeds in R&D and obtains the proceeds from the sale of carbon emission rights, the R&D process still costs a lot. What’s more, the real proceeds that can be obtained are relatively small after deducting the R&D costs. For enterprises with relatively poor R&D capabilities, it would be more in their interest to avoid the above-mentioned dual costs by expending the dual costs of facing possible R&D expenses and purchasing carbon emission rights to obtain a small gain from the sale of carbon emission rights by shifting the high carbon emission sectors to an offsite location. In the following analysis of firm heterogeneity, Tables 5, 6 similarly corroborate the above arguments.

TABLE 5. Corporate R&D capabilities.

TABLE 6. Alternative energy response of enterprises to the policy.

Apart from being cost-driven, there are also certain benefits to be gained by establishing subsidiaries across regions. From the standpoint of transaction costs, a firm facing a foreign market will be accompanied by an augment in market transaction costs (Cao et al., 2019), and establishing a foreign subsidiary not only expands the market scale of that firm but also strengthens cooperation with foreign firms and lessens the transaction costs of the parent company in the foreign market. Apart from that, by rationalizing the geographical location of subsidiaries, companies are able to directly allocate off-site resource endowments to curtail the cost of acquiring raw materials (Cao et al., 2015). To argue the above statement, this paper regresses the logarithm of the parent company’s operating income on the heterogeneous subsidiaries. The results are displayed in column (4) of Table 4, and the coefficient of Sub_Nub is noticeably positive. From an economic point of view, the addition of a subsidiary in an offsite location by the parent company raises the parent company’s operating income by 0.2%. This confirms that it is beneficial for a parent company to establish a subsidiary in a foreign location.

The cost‒benefit analysis reveals that when confronted with carbon trading policies, companies are highly motivated to move their high carbon emitting sectors off-site to avoid the dual cost of having to pay for carbon emission rights even after facing R&D failures. Meanwhile, they are also able to obtain certain benefits by establishing off-site subsidiaries.

The green technology innovation ability of diverse enterprises will differ tremendously. Aside from that, this difference will affect the transfer of “carbon” across regions to a certain extent. For this reason, this paper measures the green technology innovation capability of enterprises by the number of green invention authorizations of listed companies and divides the full sample into two groups in accordance with whether the enterprises have green invention authorizations. Table 5 shows the results of the subsample regressions. As clearly revealed in Table 5, the carbon trading policy does not give rise to the transfer of “carbon” across regions when enterprises have strong R&D capability in green technology. This is because companies are able to cut down “carbon” emissions through R&D. When companies are less able to innovate in green technology, carbon trading policies will immensely facilitate the transfer of “carbon” from companies to ease the pressure of carbon emissions from parent companies.

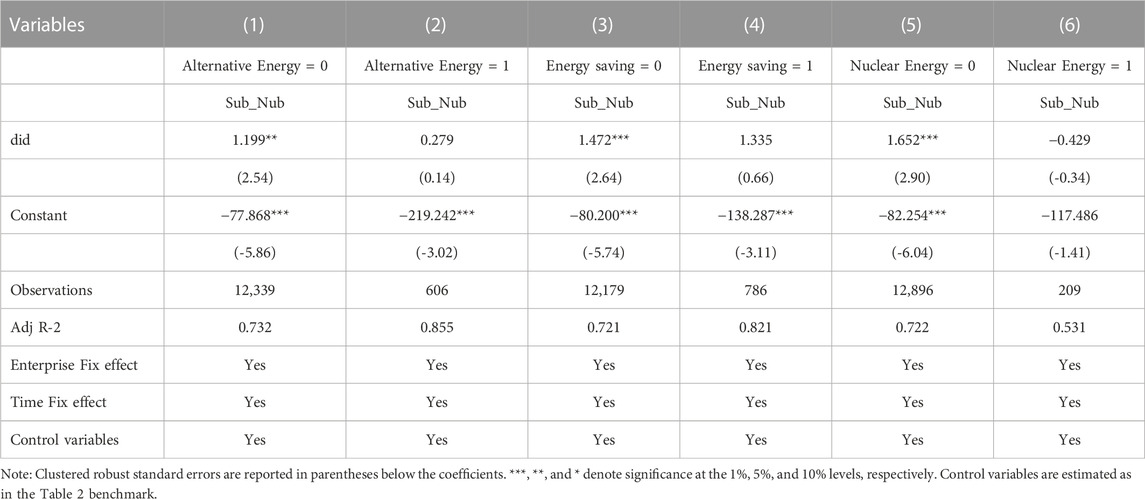

When a company has a new alternative energy source or the company consumes less energy, the company’s carbon emissions will also be lessened on that account. Under this circumstance, such companies will benefit from the carbon trading policy. As a result, such companies will be less likely to migrate “carbon”. To test the above conjecture, this paper further subdivides green technology innovation into three groups: whether the company possesses the licensed amount of alternative energy inventions, energy-saving inventions, core power generation inventions, respectively. The regression results are displayed in Table 6, in column (1) (2) of Table 6. What’s more, and the DID coefficient is strikingly positive when the firm has no alternative energy inventions and insignificant when the firm has alternative energy inventions. As displayed in Columns (3) and (4), the carbon trading policy does not affect the transfer of “carbon” when the company has an energy-saving invention. Nevertheless, when the company does not have a license for an energy-saving invention, the carbon trading policy will bring higher costs to the company, and the company will avoid it by transferring “carbon”. Finally, as exhibited in Columns (5) and (6), when a firm has clean nuclear energy to generate electricity, the firm’s carbon emissions are bound to be lower, and the firm will be able to sell carbon emission rights in the carbon trading market, thus gaining revenue. To put it in another way, the carbon trading policy will not affect the enterprises that own clean energy.

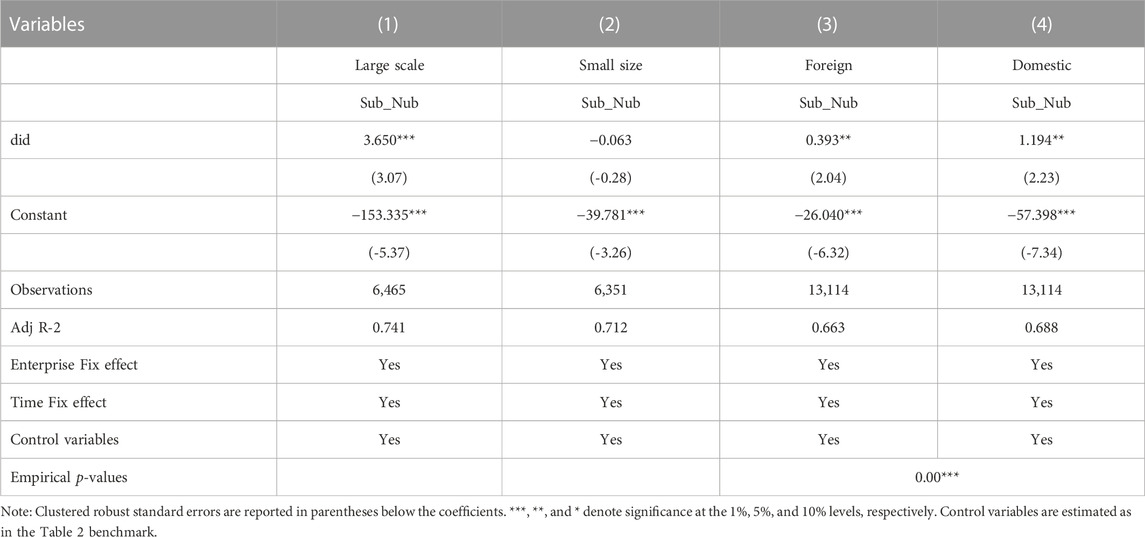

In this section, we further analyze the impact of the difference in enterprise size on the transfer of “carbon” from enterprises. On the contrary, small enterprises are less likely to shift their carbon emissions. To test the above arguments, this paper divided firms into larger and smaller firms by the median of their total assets and examines their responses to the policy separately. The results are exhibited in column (1) (2) of Table 7, from which it can be seen that the DID coefficient for large firms is markedly positive, while the DID coefficient for small firms is not significant, i.e., confirming the above conjecture.

TABLE 7. Analysis of firm size response to policy.

This paper further divides the geographical location of “carbon” transfer into two groups, domestic and foreign, and examines the distribution location of “carbon” transfer of enterprises. The results are exhibited in Table 7. As exhibited in columns (3) and (4) of Table 7, the DID coefficients are both remarkably positive, but the coefficient of group (2) is larger and passes the empirical p-test, i.e., the companies are more inclined to transfer “carbon” domestically owing to the influence of carbon trading policies. This is because it is easier and less costly to establish a subsidiary in China than abroad, and it also requires a higher level of expertise, i.e., a higher threshold for the transfer of “carbon” in a foreign country.

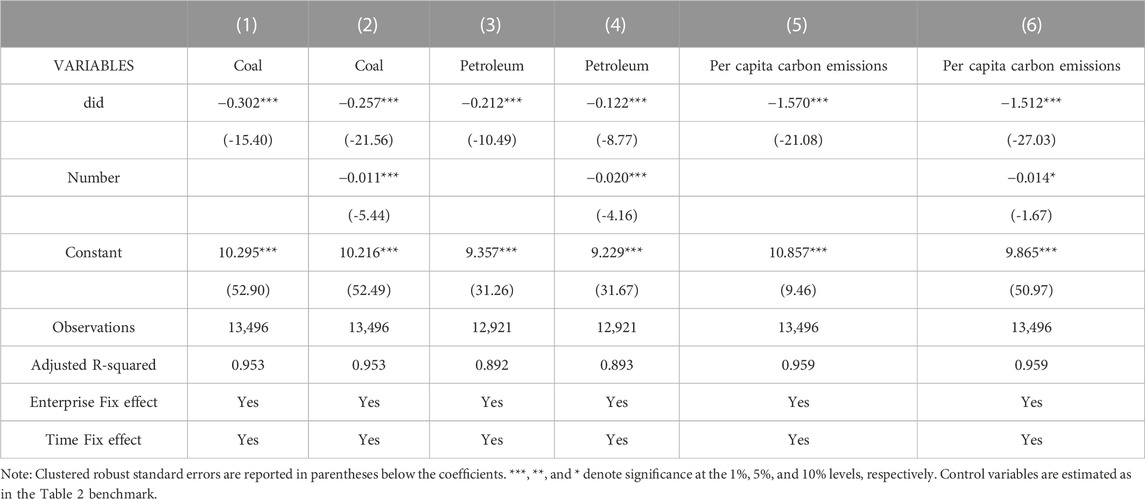

Finally, this paper verifies whether the establishment of subsidiaries in different places will lead to the transfer of carbon emissions. At present, China’s energy structure is mainly dominated by coal and oil consumption, which account for 56% and 18.5% of the total energy consumption, respectively, totalling 74.5% (data from the 2021 National Bureau of Statistics). To this end, this paper mainly investigates the carbon dioxide produced by the consumption of coal and oil by enterprises, and the results are shown in Table 8. Columns (1) and (2) in Table 8 investigate the CO2 produced by coal consumption by carbon trading policies in various regions. The DID coefficient in column (1) is significantly negative; that is, carbon trading policies significantly reduce the CO2 produced by coal. In column (2), add the Number (Number) of subsidiaries established across provinces by enterprises in different regions, whose coefficient is significantly negative and the DID coefficient decreases. This indicates that the establishment of subsidiaries in different places transfers carbon emissions to a certain extent. Similarly, columns (3) and (4) examined the effect of carbon trading policy on the amount of CO2 produced by oil consumption, and the DID coefficient was still significantly negative. After adding the “Number” variable, the size of the DID coefficient decreased, and “Number” was significantly negative, which further indicated that the enterprise transferred carbon emissions by establishing remote subsidiaries. Finally, in columns (5) and (6), per capita carbon emissions were investigated. The DID coefficient was significantly negative, and the DID coefficient decreased after adding Number. Through the above tests, it is confirmed that the enterprise transfers carbon emissions by establishing subsidiaries.

TABLE 8. Impact of carbon transfer on regional carbon emissions.

In this paper, the carbon emissions trading pilot in China in 2013 is treated as a quasi-natural experiment to examine the transfer of “carbon” from high-carbon enterprises using data from A-share listed companies from 2009 to 2018 using a Difference-in-Differences method. As revealed by the reach findings, (1) part of the effectiveness of “carbon reduction” by enterprises is achieved through the transfer of high “carbon” sectors. (2) As illustrated in mechanism analysis, when high-carbon firms face the dual cost pressure of R&D expenditures and purchasing carbon trading rights, they will avoid the parent company’s pressure to cut down emissions by establishing subsidiaries. As revealed in heterogeneity analysis, (3) companies with stronger R&D capability and higher success rates are more willing to upgrade their technology to cope with the impact of carbon trading policy. Companies with weaker R&D capabilities and higher failure rates are more likely to transfer carbon to avoid the “dual cost” of R&D failures. (4) Owing to the constraint of the migration threshold, the trajectory of “carbon” transfer is primarily domestic interregional transfer supplemented by cross-country transfer. (5) Larger enterprises emit more “carbon”, are more likely to pay more “carbon” reduction costs in the face of carbon policy shocks and are more likely to shift “carbon".

This paper offers multiple policy insights as follows. (1) Ex post facto subsidies for green technology R&D innovation to guide enterprises with weak R&D capability to progressively withdraw from the market. When enterprises upgrade their green technologies, on the one hand, they will certainly bring an increment in R&D costs, and on the other hand, they may face the pressure of “dual costs” when they still need to pay for the purchase of carbon emission rights after their R&D fails. This reinforces the transfer of “carbon” from enterprises with higher carbon emissions and weaker R&D capabilities. This requires law enforcers to ameliorate environmental enforcement and at the same time to do a good job of top-level design to progressively guide such enterprises out of the market. (2) Focused monitoring by region. The central government should strengthen the key monitoring of regions with more resource endowments and lower labor costs to avoid the dilemma of “polluting before getting rich” in such regions.

The original contributions presented in the study are included in the article/supplementary material further inquiries can be directed to the corresponding author.

XL: conceptualization, methodology, resources. JL: writing–review draft preparation,data curation, data analysis. DF: supervision, data analysis.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Beck, T., Levine, R., and Levkov, A. (2010). Big bad banks? The winners and losers from bank deregulation in the United States. J. Financ. 65 (5), 1637–1667. doi:10.1111/j.1540-6261.2010.01589.x

Becker, R., and Henderson, V. (2000). Effects of air quality regulations on polluting industries. J. Polit. Econ. 108 (2), 379421. doi:10.1086/262123

Bohringer, C., Balistreri, E. J., and Rutherford, T. F. (2012). The role of border carbon adjustment in unilateral climate policy: Overview of an energy modeling forum study (EMF 29). Energ Econ. 34 (2), 97–110. doi:10.1016/j.eneco.2012.10.003

Brunnermeier, S. B., and Levinson, A. (2004). Examining the evidence on environmental regulations and industry location. J. Environ. Dev. 13 (1), 6–41. doi:10.1177/1070496503256500

Cai, H., Chen, Y., and Gong, Q. (2016). Polluting thy neighbor: Unintended consequences of Chinas pollution reduction mandates. J. Environ. Econ. Manag. 6 (3), 86–104. doi:10.1016/j.jeem.2015.01.002

Cao, C., Xia, C., and Qian, C. (2019). Inter-regional trust and group off-site development - an empirical test based on firm boundary theory. Manag. World 35 (01), 179–191. doi:10.19744/j.cnki.11-1235/f.2019.0013

Cao, C., Zhou, D., Wu, C., and Zhan, T. (2015). The market segmentation and the distribution of nonlocal subsidiaries. Manag. World, 92–103+169+187188. doi:10.19744/j.cnki.11-1235/f.2015.09.008

Carraro, C., and Siniscalco, D. (1992). Environmental innovation policy and international competition. Environ. Resour. Econ. 2, 183–200. doi:10.1007/BF00338242

Copeland, B. R., and Taylor, M. S. (2005). Free trade and global warming: A trade theory view of the Kyoto protocol. J. Environ. Econ. Manag. 49 (2), 205–234. doi:10.1016/j.jeem.2004.04.006

Dechezleprêtre, A., Gennaioli, C., Martin, R., Muûls, M., and Stoerk, T. (2022). Searching for carbon leaks in multinational companies. J. Environ. Econ. Manag. 112, 102601. doi:10.1016/j.jeem.2021.102601

Erdogan, A. M. (2014). Foreign direct investment and environmental regulations a survey. J. Econ. Surv. 28 (5), 943–955. doi:10.1111/joes.12047

Fan, Y., and Li, J. (2022). Research on the impact of green credit policy on labor income share: Based on the perspective of human capital and credit constraint reallocation. Econ. Rev. (3), 22–38. doi:10.19361/j.er.2022.03.02

Gao, C., Tao, S., He, Y., Su, B., Sun, M., and Isaac, A. M. (2021). Effect of population migration on spatial carbon emission transfers in China. Energy Policy 156, 112450. doi:10.1016/j.enpol.2021.112450

Guo, L., and Xiao, Y. (2022). Have carbon emissions trading pilots promoted OFDI? China Popul. Resour. Environ. 32 (01), 42–53.

Han, M., Yao, Q., and Lao, J. (2020). China’s intra- and inter-national carbon emission transfers by province: A nested network perspective. Sci. China Earth Sci., 63, 852–864. doi:10.1007/s11430-019-9598-3

Keller, W., and Levinson, A. (2002). Pollution abatement costs and foreign direct investment inflows to U. S. states. Rev. Econ. Stat. 84 (4), 691–703. doi:10.1162/003465302760556503

List, J. A., McHone, W., and Millimet, D. L. (2003). Effects of air quality regulation on the destination choice of relocating plants. Oxf. Econ. Pap. 55 (4), 657–678. doi:10.1093/oep/55.4.657

Liu, M., and Chen, S. (2022). Does the carbon emission trading scheme promote the optimization and upgrading of regional industrial structure? Manag. Comment 34 (07), 33–46. doi:10.14120/j.cnki.cn11-5057/f.2022.07.015

Liu, Y., and Zhang, X. (2017). Carbon emission trading system and enterprise R&D innovation: An empirical study based on triple difference model. Econ. Sci. 39 (03), 102–114. doi:10.19523/j.jjkx.2017.03.008

Moore, N. A. D., Grosskurth, P., and Themann, M. (2019). Multinational corporations and the EU Emissions Trading System: The specter of asset erosion and creeping deindustrialization. J. Environ. Econ. Manag. 94, 1–26. doi:10.1016/j.jeem.2018.11.003

Pan, M., and Wang, C. (2022). Research on the corporate reduction effect of the carbon emission trading pilot. Econ. Rev. 38 (10), 73–81. doi:10.16528/j.cnki.22-1054/f.202210073

Reinaud, J. (2008). Climate policy and carbon leakage: Impacts of the European emissions trading scheme on aluminium. Paris: International Energy Agency. Available at: https://www.osti.gov/etdeweb/servlets/purl/21589331.

Ren, D., and Zhen, J. (2019). Does emissions trading system improve firm’s total factor productivity: Evidence from Chinese listed companies. China Ind. Econ. 37 (05), 5–23. doi:10.19581/j.cnki.ciejournal.2019.05.001

Shen, H., and Huan, N. (2019). Will the carbon emission trading scheme improve firm value? Financ. Trade Econ. 40 (01), 144–161. doi:10.1371/journal.pone.0253460

Shen, K., Jin, G., and Fang, X. (2017). Does environmental regulation cause pollution to transfer nearby? J. Finan Res. 52 (05), 44–59.

Siebert, H. (1979). Environmental policy in the two-country-case. Zeitschr F. Natl. 39 (3), 259–274. doi:10.1007/BF01283630

Sinn, H. W. (2008). Public policies against global warming: A supply side approach. Int. Tax. Public Financ. 15 (4), 360e394. doi:10.1007/s10797-008-9082-z

Song, D., Zhu, W., Wang, B., and Ding, H. (2021). Are there “pollution havens” within the business conglomerate. China Ind. Econ. 39 (10), 156–174. doi:10.19581/j.cnki.ciejournal.2021.10.008

Wu, S., Lei, Y., and Li, S. (2017). Provincial carbon footprints and interprovincial transfer of embodied CO2 emissions in China. Nat. Hazards 85, 537–558. doi:10.1007/s11069-016-2585-5

Wu, S., Qu, Y., Huang, H., and Xia, Y. (2022). Carbon emission trading policy and corporate green innovation: Internal incentives or external influences. Environ. Sci. Pollut. Res. 181, 1–23. doi:10.1007/s11356-022-24351-4

Xun, Z., Ying, X., and Wang, X. (2020). Polluting firms’ location and survival. J. World Econ. 43 (07), 122–145. doi:10.19985/j.cnki.cassjwe.2020.07.007

Yang, L., Li, F., and Zhang, X. (2022). Chinese companies’ awareness and perceptions of the emissions trading scheme (ETS): Evidence from a national survey in China. Energ Policy 98 (3), 254–265. doi:10.1016/j.enpol.2016.08.039

Zhan, T., and Wu, M. (2022). Can carbon emission rights trading affect enterprise investment efficiency? Zhejiang Soc. Sci. 38 (01), 39–47+157158. doi:10.14167/j.zjss.2022.01.004

Zhang, C., and Guo, Y. (2015). Can pollution-intensive industry transfer achieve win-win development in economy and environment? From the perspective of environmental regulation. J. Financ. Econ. 60 (10), 96–108.

Zhang, C., Shi, D., and Li, P. (2017). Potential effects of inter-provincial carbon permit trading in China. Financ. Trade Econ. 38 (02), 93–108. doi:10.1515/cfer-2018-070302

Zhang, Z. (2012). Competitiveness and leakage concerns and border carbon adjustments. Int. Rev. Environ. Resour. Econ. 6 (3), 225–287. doi:10.2139/ssrn.2187207

Keywords: pollution transfer, carbon emission transfer, carbon emissions trading, green development, offsite subsidiaries

Citation: Li J, Luo X and Feng D (2023) “Black box operation” in carbon reduction: Based on empirical evidence of carbon transfer by subsidiaries of Chinese enterprises. Front. Environ. Sci. 11:1120022. doi: 10.3389/fenvs.2023.1120022

Received: 09 December 2022; Accepted: 20 January 2023;

Published: 03 April 2023.

Edited by:

Shiyang Hu, Chongqing University, ChinaReviewed by:

Yu Chen, Zhongnan University of Economics and Law, ChinaCopyright © 2023 Li, Luo and Feng. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Xin Luo, NTY5MzYzMTQ5QHFxLmNvbQ==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.