Yongbo Ge1

Yongbo Ge1 Qi Chen

Qi Chen

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 13 February 2023

Sec. Environmental Economics and Management

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1108508

This article is part of the Research Topic Environmental Risk and Corporate Behaviour View all 30 articles

Environmental performances have gained great prominence for firms in recent years. This paper empirically tests the relationship between environmental information disclosure and the risk of stock price crashes based on a sample of Chinese A-share listed firms from 2013–2018. The results show that environmental information disclosure has a significant negative correlation with stock price crash risk, with mechanism analysis showing that media coverage plays an intermediary role between them. Further analysis finds that: first, the inhibitory effect of environmental information disclosure on stock price crashes is more significant in companies with a lower proportion of independent directors, which reflects the supervision effect of environmental information disclosure. Second, the role of environmental information disclosure has a greater negative impact on the risk of stock price crashes in industries with low competition, indicating that environmental information disclosure is not a tool for enterprises to compete for resources. Third, the profit motivation of institutional investors restrains the negative impact of environmental information disclosure on price collapse risk. Forth, the level of government environmental governance is an important support for enterprise environmental information disclosure.

As the Chinese economy has entered a stage of high-quality development, it is crucial to continuously improve the capital market that serves the development of the real economy. However, along with high growth, China’s stock market also has the problem of vulnerability, especially the frequent crashes and collapses of the stock market after the 2008 financial crisis, which poses a challenge to China’s economic security and sustainable development. Regarding the causes of stock price crashes, based on principal-agent theory and information asymmetry theory, the relevant literature generally finds that company executives choose to hide the company’s “bad news” out of self-interested motives such as maintaining a reputation (Jin and Myers, 2006). As adverse news continues to accumulate until it is impossible to hide, it will suddenly explode in the capital market, leading to the rapid decline of individual stock prices and forming a so-called stock price crash. In this process, the lack of information disclosure leads to the decline of information transparency, regarded as an important factor in stock price crashes.

Information disclosure is not only a strong guarantee of improving the level of corporate governance but also the institutional cornerstone of the healthy development of capital markets. Information disclosure can be divided into financial information disclosure and non-financial information disclosure, although previous studies have focused more on financial information. For example, Hutton et al. (2009) showed that the lack of transparency in financial reports increased the risk of a company’s stock price crash; and (Zhu et al., 2020) argued that internet information interaction could improve the authenticity of corporate financial information, encourage investors to form reasonable expectations, and avoid the occurrence of stock price crashes. With the deepening of research, some scholars have turned to non-financial information disclosure, such as the impact of corporate social responsibility on stock price crashes (Kim et al., 2014), but the coverage of relevant non-financial information research is narrow, and the content in developing countries is deficient (Tao et al., 2022). As an important aspect of information disclosure, a consensus has been formed on the role of non-financial information disclosure in improving the information environment of capital markets (Hu and Tan, 2013). Therefore, it is necessary to combine different corporate internal governance and external environments to discuss from the perspective of non-financial information disclosure, which will help provide a comprehensive, in-depth understanding of the causes of stock price crash risk. From the perspective of environmental information disclosure, this paper attempts to answer the following questions: What is the relationship between environmental information disclosure and stock price crash risk? How can media coverage play a role in this relationship? Does firm heterogeneity significantly affect the relationship?

Accordingly, this paper uses unbalanced panel data of 2,446 listed firms from 2013–2018 to empirically test the relationship between environmental information disclosure and stock price crash risk. The main reasons for choosing the Chinese market are as follows. First, China has grown into the world’s second largest economy in recent years, but its capital market is still immature. There have been repeated stock price crashes in recent years, such as the financial crisis in 2008 and the 1,000-share crash in 2015. It means that the market is vulnerable to the impact of information shocks, and the stock price will have frequent ups and downs, with poor stability and self-correction ability. Second, as the world’s largest emerging capital market, its participants are mainly retail investors, and compared with developed markets, the information disclosure system is not perfect. China’s unique macro environment provides a good foundation for studying the impact of information disclosure. Therefore, Under the current economic downward pressure and the capital market is unstable, exploring the risk management mechanism of stock price crash in the Chinese market is helpful to maintain the stability of the capital market. At the same time, it can also provide reference for other emerging economies and developing countries with excess resource consumption to resolve enterprise risks through market-oriented means. Third, The accelerating climate change concerns highlight the importance of reducing fossil fuel consumption (Tian et al., 2022). China’s sustained high economic growth has accompanied the sharp increase in resources and energy consumption (Kang et al., 2022), environmental information disclosure can be regarded as an important symbol for enterprises to reduce energy consumption, therefore research on environmental information disclosure can contribute to energy transition.

The results show that environmental information disclosure is significantly negatively correlated with the risk of stock price crashes, which is still significant after using the instrumental variable method, propensity score matching (PSM) method, replacement variables and other robustness tests. The mechanism analysis shows that media coverage plays a mediating role in the inhibitory effect of environmental information disclosure on stock price crash risk. Further analysis shows that the characteristics of the board of directors, the pressure of industry competition, the shareholding ratio of institutional investors and the level of government environmental governance are important factors affecting the relationship.

The contributions of this paper are as follows. First, it expands the research on the influencing factors of stock price crash risk. Based on the perspective of financial information disclosure projects and supervision, existing studies have confirmed that the improvement of financial information quality significantly reduces the risk of stock price crashes, but the discussion on the influence of non-financial information disclosure on stock prices is still insufficient in developing countries (Tao et al., 2022). An analysis based on environmental information disclosure will undoubtedly enrich the research in related fields. Second, based on different market participants, this paper conducts an in-depth examination of the impact of environmental information disclosure on stock price crash risk. Most of the literature continues the research approach of Chen et al. (2001) to analyze the mechanism of stock price crash risk from the perspective of corporate governance (Song et al., 2017). In this paper, however, the possible market reaction to the company’s non-financial information is included in the research category of stock price crash risk mechanism analysis. It is useful to deepen and extend the understanding and analytical paradigm of the causes of stock price crash risk, which has profound theoretical and practical significance. Third, considering the macro background of China’s green development and ecological civilization construction, our paper attempts to explore the impact of corporate environmental information disclosure on the capital market to provide empirical evidence on the economic consequences of implementing the green development concept and actively fulfilling environmental responsibility for enterprises. In addition, the heterogeneity analysis results also provide support for the development of environmental information disclosure policies of relevant departments and the decision-making of enterprise environmental information disclosure.

Stock price crashes are an important topic in the field of asset pricing and corporate finance. Existing studies focus on the formation mechanism of stock price crashes and discuss the principal-agent problem and the corporate information environment. According to agency theory, the root cause of stock price crashes is that the company’s senior executives, motivated by self-interest, including the pursuit of higher salary, honor and status, use their authority to exercise opportunistic behavior and deliberately conceal the company’s adverse news, which eventually leads to the crash of the stock price (Jin and Myers, 2006). Kim et al. (2014) found that to maximize the value of short-term stock options, CEOs and CFOs are motivated to hide adverse news, leading to an increased risk of a stock price crash. Scholars have provided explanations from the perspective of corporate governance, including the number of shareholders, the proportion of major shareholders, the reduction of senior executives’ holdings, and the equity pledge of controlling shareholders. In terms of the information environment, Jin and Myers (2006) empirically tested the impact of information transparency differences between countries on stock prices using data at the national level and found that countries with lower information transparency had higher stock price crash risk. Hutton et al. (2009) turned the research subject to companies and found that corporate financial transparency significantly affected the probability of stock price crashes. The higher the transparency, the lower the probability of stock price crash risk. On this basis, Kim et al. (2014) conducted a more in-depth study. Based on the perspective of implied volatility, they found that the restatement of financial reports, earnings management and internal control defects would increase the occurrence of stock price crash risks. Other scholars have conducted research from the perspective of external supervision, including tax regulation (Kim et al., 2011; Chen et al., 2022), media reports (An et al., 2020; Hossain et al., 2022), institutional investors (Xiang et al., 2020), and investor sentiment (Fu et al., 2021).

The research on corporate environmental information disclosure mainly focuses on the following aspects: First, the content, mode and current situation of environmental information disclosure. Most scholars believe that the contents of environmental information disclosure should include environmental problems, impacts and corresponding countermeasures, as well as environment-related costs and benefits and environmental liabilities (Cho and Patten, 2007), and studied the status quo of environmental information disclosure of heavy polluting enterprises in China (Luo et al., 2019). Second, research on the influencing factors of environmental information disclosure. Most scholars have discussed the influencing factors of corporate environmental information disclosure from internal factors and external factors. Among them, external factors mainly include government policies and regulations, environmental control intensity, accounting responsibility and public opinion pressure, etc. (Liu and Anbumozhi, 2009; Wang et al., 2013; Fang and Guo, 2018), internal factors are mainly enterprise size, industry type, green commitment and corporate governance (Yan and Chen, 2017; Jacoby et al., 2019; Liu et al., 2022a). Third, the impact of environmental information disclosure. Some scholars believe that environmental information disclosure can have a positive impact on corporate value through reducing information asymmetry, improving corporate investment efficiency (Liu et al., 2022b), enhancing corporate governance (Earnhart and Lizal, 2006) and influencing financial markets (Wan et al., 2021).

According to the theory of externalities, enterprises show positive or negative externalities in the pursuit of profit maximization (Tirole, 2001), but the management of the company is often unsatisfactory in dealing with negative externalities. Therefore, undertaking social responsibility can be regarded as an effort by enterprises to reduce their negative externalities (Magill et al., 2015) and has gradually become an effective way for enterprises to balance their own interests with those of other stakeholders (Ferrell et al., 2016). As a reflection of the interaction between enterprises and other stakeholders, environmental information disclosure is an important indicator to measure the attitude and strength of enterprises toward social responsibility. In general, it can not only reflect the internal information of the enterprise to investors but also affect the external impression and reputation of the enterprise (Song et al., 2017), which has an important impact on the stock price of the enterprise. Specifically, environmental information disclosure can reduce the risk of stock price crashes in two ways: the information transfer effect and the reputation guarantee effect.

(1) Information transfer effect. Generally, when the degree of information asymmetry between internal and external companies is high, firm executives are more likely to hide adverse news out of self-interest, which is the root of stock price crashes (Habib et al., 2018). On the one hand, according to signaling theory, enterprises can transmit internal information to the outside world through environmental information disclosure behavior, alleviate the information disadvantage of outsiders to a certain extent, inhibit the occurrence of concealment behavior by increasing the cost of hiding “bad news” by company executives, and reduce the probability of stock price collapse from the root. On the other hand, since environmental information disclosure transmits the relevant information about the enterprise, investors know the financial health status of the enterprise (Lizzeri, 1999); based on this, reasonable investment decisions can be made so that the stock price fully reflects the real business situation of the enterprise, avoiding the formation of stock price bubbles due to asymmetric information and the occurrence of stock price crashes at a certain point.

(2) Reputation guarantee effect. According to the theory of reputation management, the influence of people’s perceptions of current news cannot be underestimated. Corporate reputation provides conditions for eliminating adverse situations with the help of the public’s mindset. Therefore, with the enhancement of public awareness of environmental protection, environmental information disclosure has gradually become an important means for enterprises to perform environmental protection duties and create a better image. Godfrey et al. (2009) pointed out that although this corporate reputation capital reflecting social morality could not directly bring benefits to the change in corporate capital stock and related transactions, it could play a role similar to insurance when enterprises are faced with adverse events. In other words, corporate reputation capital formed by environmental information disclosure can affect the public’s subjective judgment of negative corporate news (for example, that corporate executives are just “doing bad things with good intentions”), delay the time and impact of adverse corporate information entering stock prices, and be able to deal with current problems and reduce the degree of “sanctions” (massive stock selling) (Godfrey et al., 2009).

Hypothesis 1:. There is a significant negative correlation between environmental information disclosure and stock price crash risk.In the relationship between environmental information disclosure and stock price crash risk, both the ex ante information transmission effect and the ex post reputation guarantee effect include the process of information transmission from enterprises to capital markets (investors). In this process, the information intermediary plays a vital role. Existing studies show that the media (Fang and Peress, 2009) play important information intermediary functions in the capital market.Fang and Peress (2009) pointed out that the media have the function of information collection and dissemination, which improves the information available to investors. In the context of the extensive use of internet information technology in capital markets, media as information intermediaries play an increasingly critical role (Strycharz et al., 2018). In the process of continuous emphasis on and improvement of ecological civilization construction, enterprise-related environmental protection information has gradually become a hot topic of media reports. Therefore, it can be predicted that corporate environmental information disclosure will cause an increase in media attention; that is, corporate environmental information disclosure may be positively correlated with media attention. Existing studies show that the media can reduce the risk of stock price crashes from many aspects, including alleviating the internal and external information asymmetry of the company, improving the efficiency of the capital market, reducing the time and space for executives to hide negative news, and improving public opinion supervision to alleviate the executive agency problem. In conclusion, environmental disclosure may reduce the risk of stock price crashes by increasing media coverage.

Hypothesis 2:. In the relationship between environmental information disclosure and stock price crash risk, media coverage plays a mediating role.

This paper uses unbalanced panel data of 2,446 listed firms from 2013–2018. The shareholding data of institutional investors are obtained from the WIND database, media coverage is obtained from the Baidu News search index, and the remaining data are obtained from the CSMAR database. In November 2012, the 18th National Congress included ecological civilization construction in the “five-in-one” overall layout of the socialist cause with Chinese characteristics. Since then, enterprises’ participation in environmental protection has attracted wide attention. Drawing on his ideas, the samples selected in this paper started in 2013. As a rule, the research samples are processed as follows: 1) Abnormal samples such as

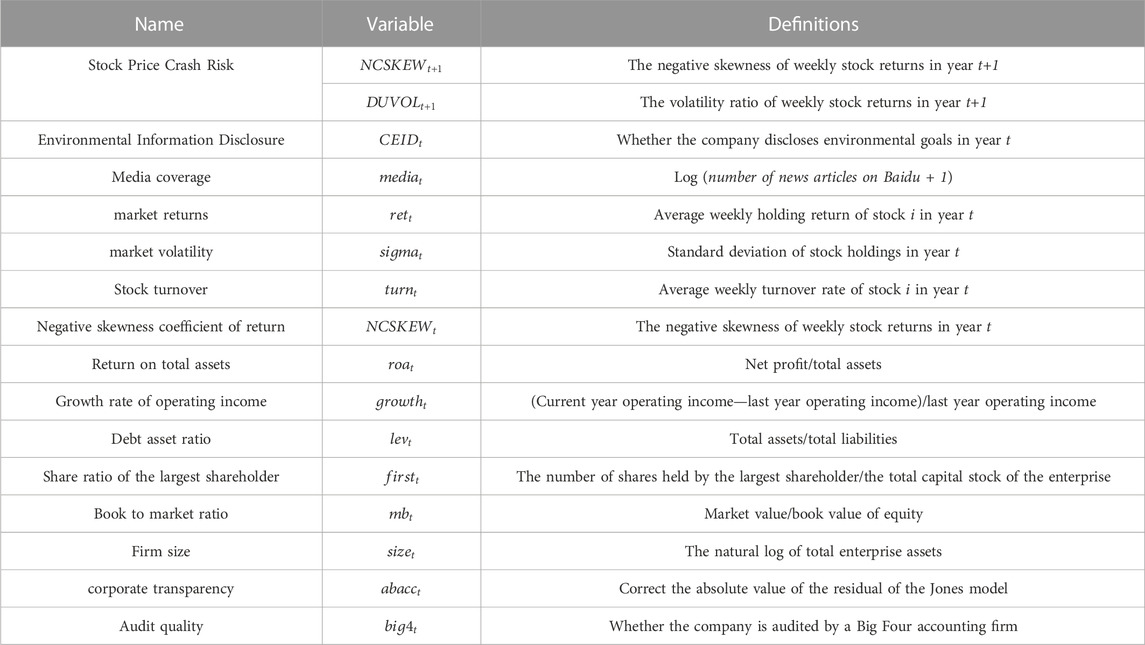

Stock Price Crash Risk. The calculation process is as follows:

The following regression is performed on the weekly return rate of stock i by year:

where

Based on the above indicators, the variables NCSKEW and DUVOL are constructed to reflect the crash risk of stock i in year t:

where n represents the number of weeks stock i was traded that year. In Eq. 3,

Environmental Information Disclosure. The disclosure of environmental protection targets in the Environmental Research Database of CSMAR China Listed Firms is selected as the proxy variable for environmental information disclosure. If the environmental protection targets are disclosed by enterprises, the value is 1; otherwise, it is 0. Hao and Su (2014) pointed out that whether to disclose important information is an important way to measure information in existing studies. In view of this, some scholars take the binary variable of whether to disclose relevant information as the measurement method of environmental information disclosure (Tao et al., 2020). This paper draws on its ideas and selects whether to disclose environmental protection goals as a proxy variable for environmental information disclosure.

Media coverage (

Based on the literature, the following variables are selected for control: market return (

TABLE 1. Variable definitions.

To explore the impact of information environmental disclosure on stock price crashes, this paper refers to the common practice of the literature of delaying all independent variables by one period and constructs the following model:

where the dependent variables are the negative skewness coefficient of the return rate (NCSKEW) and the fluctuation of the return rate (DUVOL) in period t +1. The higher the value, the higher the risk of stock price crashes. The right side shows the independent variables in period t. This paper focuses on the significance level of β. Controls include all the control variables in Table 1. Additionally, year and industry are controlled. In addition, considering that the environmental information disclosure of enterprises will be affected by the environmental quality status and environmental protection policies of different provinces, this paper also controls the province dummy variable.

To explore the mediating effect of analyst attention and media coverage, the following model was constructed by referring to the three-step method proposed by Baron and Kenny (1986):

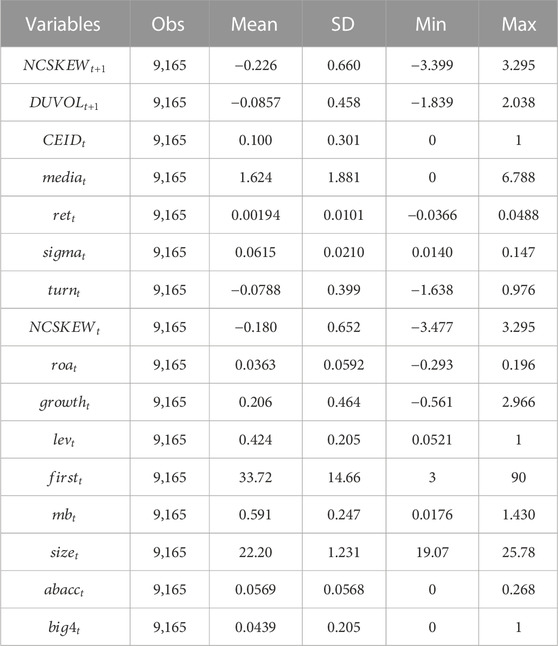

Table 2 reports descriptive statistics for the full sample. As shown in Table 2, the mean values of NCSKEW and DUVOL are −0.226 and −0.0857, and the standard deviations are 0.660 and 0.458, respectively. The mean value of the core explanatory variable Environmental Information Disclosure (CEID) is 0.1.

TABLE 2. Descriptive statistics.

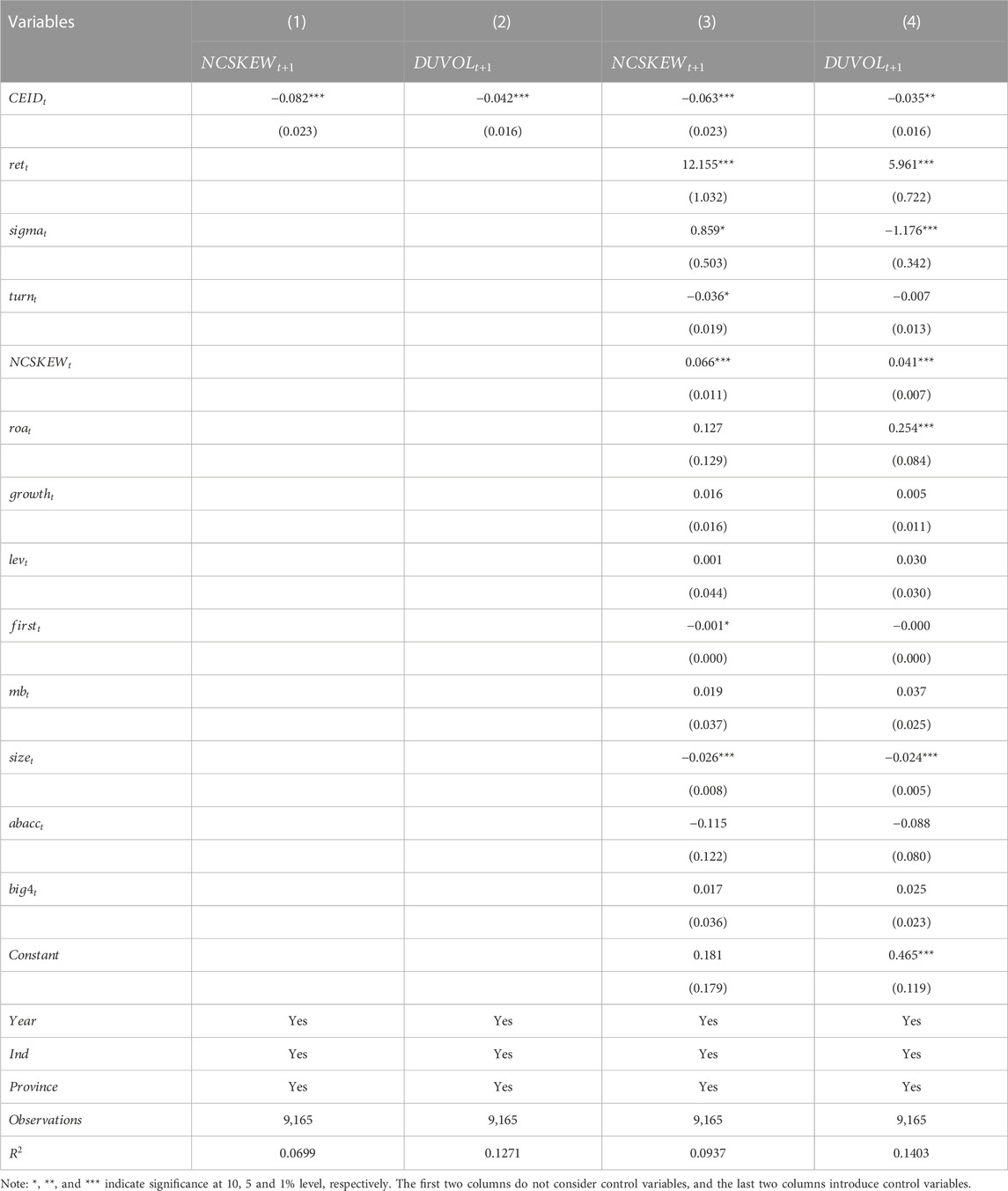

Table 3 reports the regression results of environmental disclosure and stock price collapse. Taking Column (3) and Column (4) as examples, regardless of whether

TABLE 3. Basic regression results.

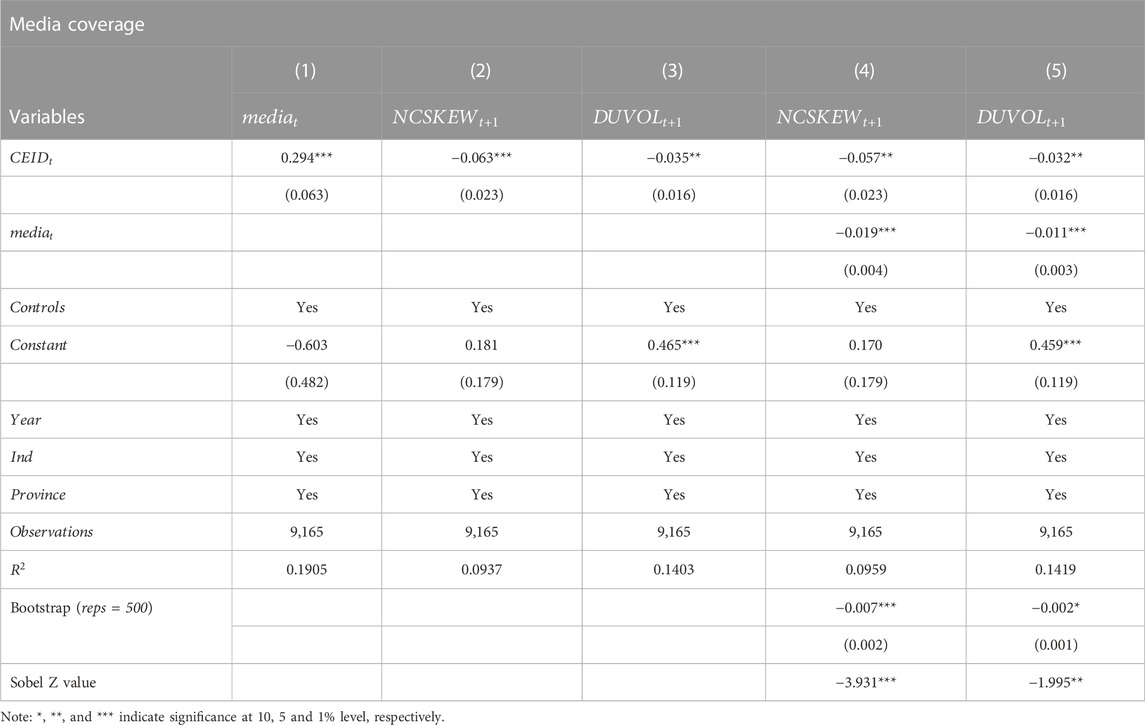

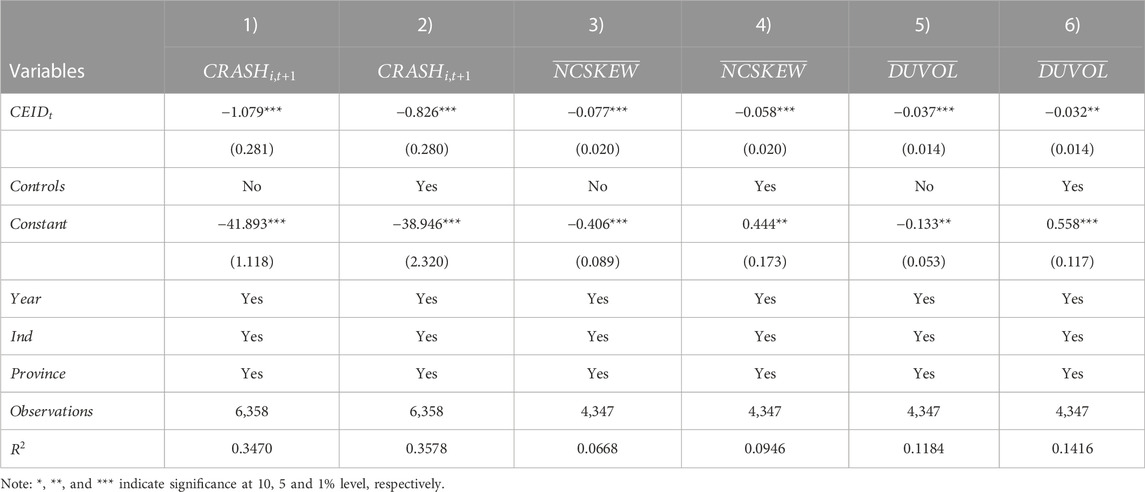

The empirical results above show that corporate information disclosure can reduce the risk of stock price crashes. Then, as the key information intermediaries in the capital market, what role do analysts and media play in the above effects? Therefore, this paper uses the three-step method to analyze whether corporate environmental information disclosure has an impact on stock price crash risk through the mediating role of analyst attention and media attention.

Table 4 reports the mediating effect test results of media coverage. Column 1) tests whether environmental information disclosure has a significant impact on the mediating variable media attention, and the coefficient of

TABLE 4. Mechanism analysis.

The purpose of this paper is to investigate the causal relationship between environmental information disclosure and stock price crash risk. Although all explanatory variables are lagged by one period, the endogeneity problem may not be completely excluded. First, companies have the motivation to disclose environmental information for the purpose of improving their reputational capital and reducing the risk of stock price crashes, resulting in reverse causality. Second, the analysis of this paper may ignore some factors that are difficult to measure, such as system construction and policy support, which inevitably lead to the omission of variables. Therefore, this paper refers to the practice of (Ye et al., 2015) and chooses the industry mean (

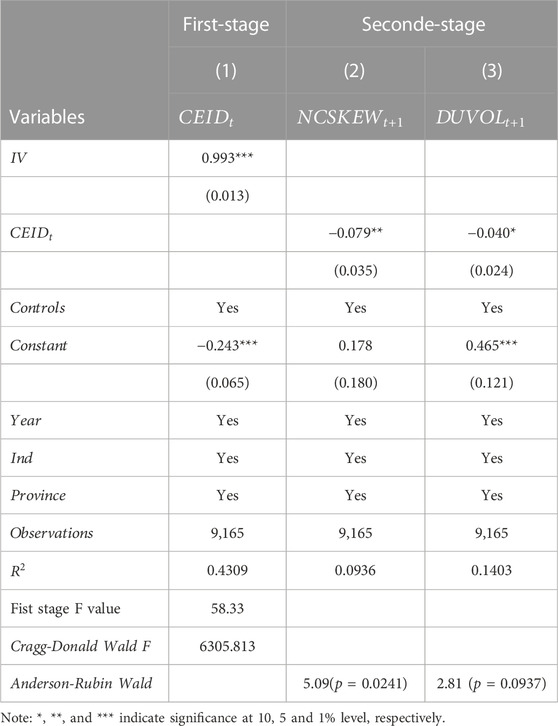

Table 5 reports the regression results of the instrumental variables. In the first-stage regression, the regression coefficient of the mean value of the environmental information disclosure industry is 0.993, which is significant at the 1% level, indicating that the instrumental variables are highly correlated with the endogenous explanatory variables. The F value in the first stage was 58.33, much greater than 10, which excluded the null hypothesis of “weak instrumental variables”. According to the two-stage regression results, the regression coefficient of environmental information disclosure is significantly negative, which is consistent with the basic regression, proving that the results of this paper are robust. In addition, this paper also reports a more stringent Anderson-Rubin Wald test, which rejects the null hypothesis that the sum of endogenous regression coefficients is equal to 0 at the significance level of 5% and 10%, respectively, which further illustrates the strong correlation between instrumental variables and endogenous explanatory variables.

TABLE 5. IV-test.

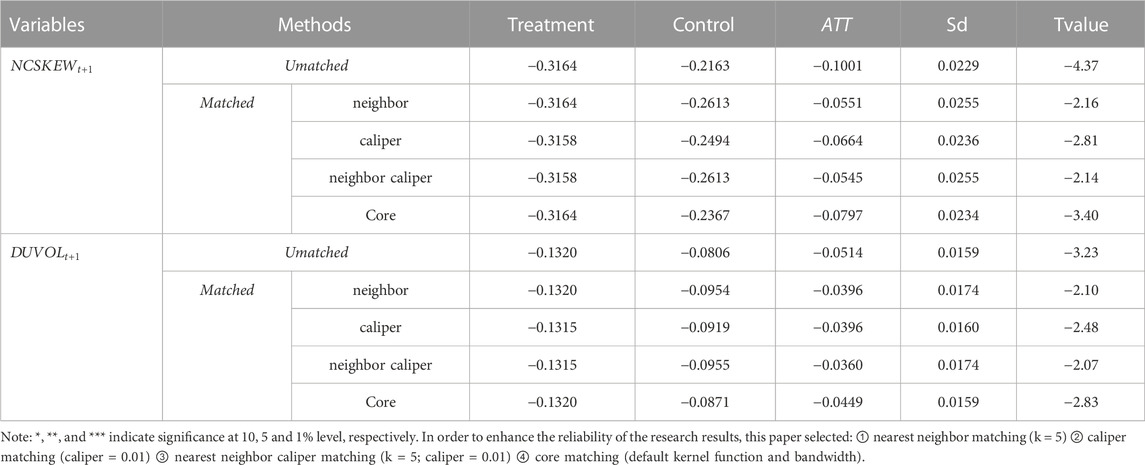

Due to the differences in the characteristics of different enterprises, it is impossible to exclude the possibility that the two types of samples (with and without environmental information disclosure) show different stock price crash risks due to the inherent characteristics of enterprises, resulting in sample selection bias. For example, the mean size (

In Table 6, the ATT results obtained by using the four matching methods are all negative, and the T values are all greater than 1.96 (5% significance level), indicating that environmental information disclosure still significantly inhibits the risk of stock price crashes after considering the sample selection bias, which proves that the results obtained in this paper are robust.

TABLE 6. PSM Results.

This paper uses the following two methods to measure the risk of stock price crash.

(1) Referring to the method of Callen and Fang (2015), the stock price crash risk is measured by the difference between the frequency of downward and upward occurrence of the weekly specific return rate of a company’s stock. The calculation process is as follows:

First, the weekly specific return rate in the downward phase is defined as:

where,

Similarly, the weekly specific rate of return in the upward phase is defined as:

Finally, the frequencies of

(2) Referring to the research of (Bennett B et al., 2020) the mean of the sum of the next three periods of the explained variables (

Columns (1) and (2) in Table 7 report the regression results of another calculation method

TABLE 7. Substitution variable.

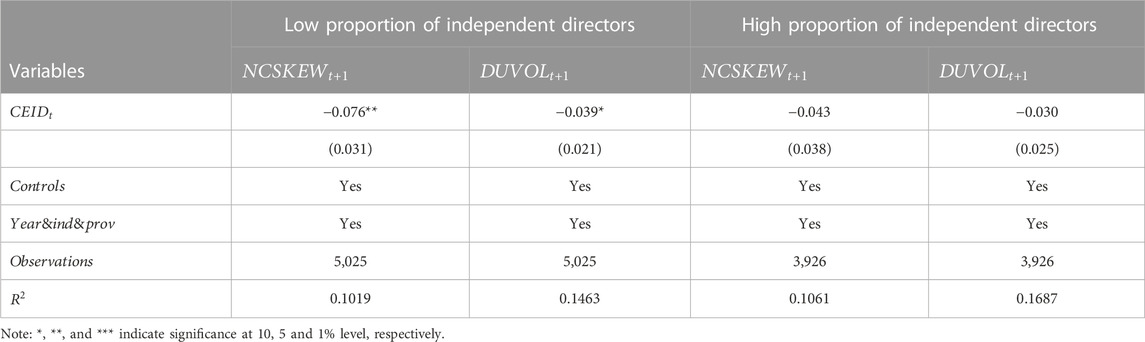

According to agent theory, if the internal supervision level of the enterprise is weak, there is a higher probability that management will negative news out of self-interest, exacerbating the risk of stock price crashes. Then, as a type of non-financial information disclosure, does environmental information disclosure have an inherent supervisory effect and reduce principal-agent problems? that is, does it play a role in reducing the risk of stock price crashes by reducing the likelihood that executives will hide negative news? To answer the above questions, we reference the ideas of Zhu et al. (2020), and the proportion of independent directors of a company is selected as a proxy variable for the characteristics of the board of directors for the group test. The logic is as follows: the board of directors system is the basis for the supervision of the management of listed companies. If the proportion of independent directors is low, it means that the company’s senior executives have more rights and less resistance to pursuing egotistical goals; in this case, the probability of hiding negative news increases, which leads to agency problems and increases the risk probability of stock price crashes. If environmental information disclosure has a supervisory effect on company executives, it should be a powerful supplement to the management of the company as independent directors. Therefore, we focus on whether environmental disclosure can play a complementary role when independent directors fail to implement effective supervision. In other words, does environmental information disclosure have a stronger effect on reducing the risk of stock price crashes for companies with a low supervision effect of independent directors?

According to whether the proportion of independent directors of listed firms is greater than the annual industry median, the samples are divided into two categories: a high proportion of independent directors and a low proportion of independent directors. According to Table 8, for firms with a high proportion of independent directors, the regression coefficients of stock price crash risk

TABLE 8. Environmental information disclosure and board characteristics.

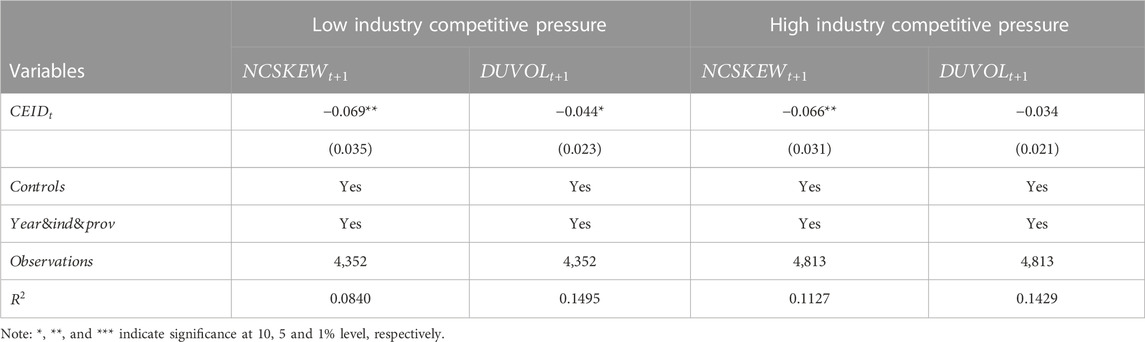

Although the above analysis does not distinguish between the motivations for environmental information disclosure, but the actual effect of environmental actions implemented by enterprises may vary greatly depending on the different motivations. Previous studies have shown that the motivations for enterprise information disclosure are restricted by industry competition (Stivers, 2004). In fierce market competition, enterprises will fully disclose information to compete for limited resources in the capital market, improve the transparency of corporate information and reduce the cost of capital. In this case, if the competition for resources as the motivation for a company to disclose environmental information is low compared to the competition in the industry, the company in the highly competitive industry will not only increase its environmental information disclosures but will also enrich the contents of the disclosure. Such improvements in the quality of the environmental information disclosure and increases in the transparency of information can effectively reduce stock crash events.

Based on the above considerations, the division is conducted according to the median Herfindahl-Hirschman index (

TABLE 9. Motivation of environmental information disclosure.

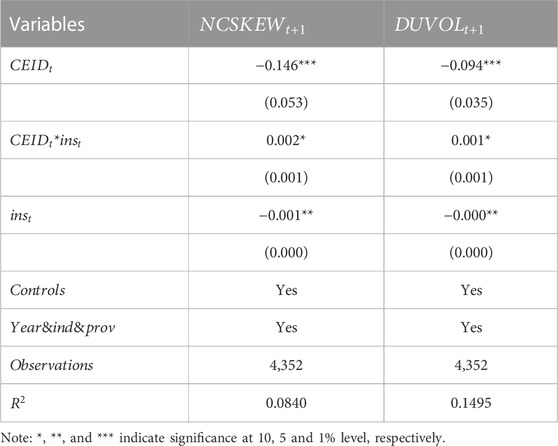

According to stakeholder theory, the enterprise is an institutional arrangement of specialized investment in intelligence and management. The survival and development of the enterprise depend on the quality of the enterprise’s response to the interest requirements of various stakeholders, not just on shareholders. The above analysis does not consider the reaction of other stakeholders to environmental information disclosure. As important shareholders of companies, institutional investors have attracted increasing attention regarding the impact of stock price crash risk. Therefore, this paper analyzes the impact of other stakeholders’ reactions on new environmental information disclosure from the perspective of institutional investors, which not only helps us understand the role of other stakeholders in “environmental information disclosure-stock price crash risk” from the theoretical level but also provides a reference for regulators to specify relevant decisions. The existing literature has shown that institutional investors affect the relationship between environmental information disclosure and stock price crashes from at least two paths. 1) The motivation of governance. With the increase in the shareholding ratio of institutional investors, the motivation of institutional investors to carry out active behaviors is enhanced, which makes institutional investors carry out supervision and governance behaviors to avoid the benefit loss caused by information asymmetry. Existing studies show that institutional investors have governance effects on the quality of corporate information disclosure (Aggarwal et al., 2011), which can improve the accuracy, timeliness and robustness of information disclosure, thereby increasing information transparency and reducing the risk of stock price crashes. Therefore, from the perspective of governance motivation, we believe that an increase in the shareholding ratio of institutional investors will promote the negative effect of new environmental information disclosure on the risk of stock price crashes. 2) Profit motive. Jiang and Kim (2015) pointed out that institutional investors in China have a significant short-term investment tendency. This means that environmental information disclosure may become a tool for institutional investors to make profits; that is, by increasing the number of disclosures or exaggerating positive news, investors will overreact to information and make wrong investment decisions, which will further promote short-term stock price bubbles. However, this type of bubble is not sustainable. As negative news enters the market, investors will panic, and the probability of stock prices falling sharply will increase, which eventually leads to a stock price crash. Therefore, from the perspective of profit motives, an increase in the shareholding ratio of institutional investors may inhibit the negative effect of environmental information disclosure on the risk of stock price crashes.

To verify the above problems, we introduce the interaction term between environmental information disclosure and the shareholding ratio of institutional investors, and Table 10 reports the results. It can be seen that the interaction term between the two is significantly positive, which is contrary to the sign of environmental information disclosure, reflecting that institutional investors’ shareholding inhibits the negative effect of environmental information disclosure on stock price crash risk; thus, the above profit-motive hypothesis is verified.

TABLE 10. Analysis based on the perspective of institutional investors’ shareholding ratio.

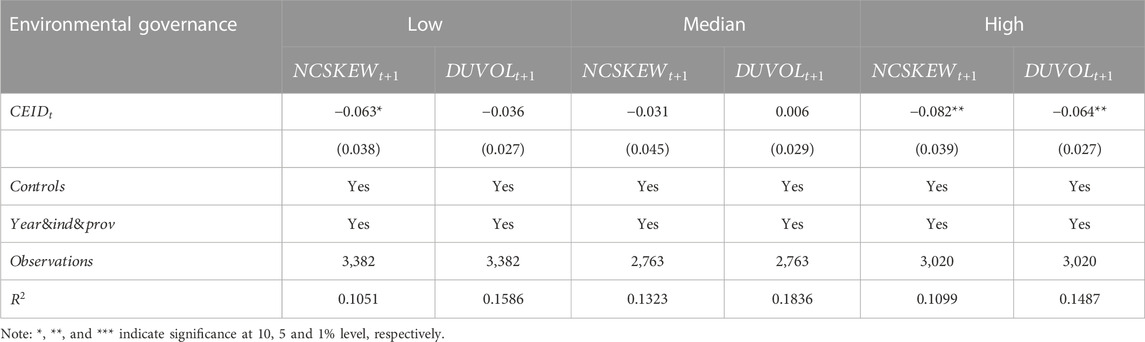

Finally, in view of the framework of “environmental information disclosure-stock price crash risk,” this part conducts research by embedding the environmental governance elements of the government from a macro perspective. Referring to the research of (Chen and Chen, 2018), the total frequency of environmental words in provincial government work reports and the total frequency of words in the report were used to measure the intensity of government environmental governance. Based on the intensity of environmental governance, group processing was conducted (adopting 3 quantiles), and the regression test of Eq. 4 was conducted again. The empirical results are shown in Table 11. In the interval where the government has a high level of environmental governance, environmental information disclosure has a good inhibitory effect on the risk of stock price crashes (the coefficient is negative, and both pass the 5% significance level test). Taking the last case as an example, in regions with higher levels of external governance, compared with enterprises without environmental information disclosure, the probability that enterprises with environmental information disclosure can reduce the risk of stock price crashes in the next year is 6.4%. In the group with low and medium levels of governance, only the regression coefficient of stock price crash risk, measured by

TABLE 11. Based on the perspective of government environmental governance.

Taking Chinese A-share listed firms from 2013–2018 as the sample, this paper empirically tests the impact of environmental information disclosure on stock price crash risk. It is found that environmental information disclosure is significantly negatively correlated with estimated crash risk, and this result is still significant after using instrumental variables, propensity score matching (PSM), substitution variables and a series of other robustness tests. The mechanism analysis shows that media coverage has a mediating effect on the relationship between the two. Further analysis indicates that the characteristics of the board of directors, multilevel capital market, industry competition pressure, institutional investors’ shareholding ratio and the level of government environmental governance are important factors affecting the relationship between “environmental information disclosure and stock price crash risk”. This paper further opens the black box of non-financial information disclosure to improve the market information environment. The results also show that positive enterprise environmental information disclosure is not only beneficial to the construction of socialist ecological civilization but also has the effect of reducing the risk of stock price crash “icing on the cake”. It is of great practical significance to improve the information disclosure system, strengthen corporate governance, strengthen government environmental governance, and prevent systemic financial risks for regulatory departments and investors.

(1) Improve the information disclosure system. It is necessary to further improve the effective and feasible standards for the public disclosure of environmental information, including the release of disclosure guidelines covering the content range and format of environmental information, and put forward more targeted and refined requirements for environmental information disclosure to provide reference standards for enterprises to implement environmental information disclosure. Strengthen the supervision of environmental disclosure, establish and improve the punishment mechanism, and avoid the occurrence of “more talk than action” in the aspect of environmental responsibility of enterprises, which is conducive to improving the integrity, authenticity and comparability of corporate information, facilitating the selection of stakeholders, and effectively playing the role of participants in the capital market with active concern motivation in information intermediaries.

(2) News, newspapers and other media should be proactive and give full play to their role as an information intermediary. On the one hand, it is necessary to continuously explore and pay attention to the environmental information disclosed by enterprises, increase the exposure of enterprises’ environmental protection behaviors, attract the attention of external stakeholders to give enterprises greater pressure on environmental responsibility, and urge enterprises to disclose more valuable information. On the other hand, we should consider increasing the publicity of enterprises that earnestly fulfill their environmental responsibility, enhancing investors’ perception of such enterprises, providing potential impetus for enterprises to continue to implement environmental protection behaviors, making full use of the power of public opinion to form an environmental atmosphere in the whole society, and laying a solid foundation for the construction of ecological civilization.

(3) Regulatory authorities should focus on strengthening financial supervision, standardizing the financial supervision system, effectively improving the quality of environmental information disclosure of enterprises, and alleviating the adverse impact of the accumulation of stock price crash risk caused by the concealment of “bad news” by senior executives. On the one hand, it is necessary to continuously strengthen functional financial supervision, attach importance to and standardize the content and system of non-financial information disclosure of enterprises, take non-financial information disclosure systems as an effective supplement to the total loss absorption capacity supervision system, and jointly serve the stability construction of the Chinese capital market. On the other hand, for different market sectors and industry types, regulatory authorities can implement differentiated management policies. The results of this paper show that the impact of environmental information disclosure on stock price crash risk varies by sectors and industries under different competitive pressures, indicating that the “one-size-fits-all” regulatory scheme does not reflect the actual needs of different types of enterprises, so specific regulatory measures should be formulated for enterprises with different attributes. We should ensure that the capital market can better serve the development of the real economy through appropriate forecasting and classified intervention.

(4) For the government, it is necessary to continuously improve the level of environmental governance, lay a good foundation for enterprises to assume environmental responsibility and timely disclosure, make reasonable use of administrative means, and form a scientific, environmental governance system dominated by the government and enterprises. It is necessary to make good use of market-oriented means to give publicity, tax and preferential policies to those enterprises that actively undertake environmental protection responsibilities, send positive signals to the market, attract the attention of investors in the capital market and bring capital inflow, and provide a potential impetus for enterprises to actively undertake environmental protection responsibilities and improve environmental protection information disclosure.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

Conceptualization, YG and QC; methodology, YG, QC, and SQ; formal analysis, YG, QC, and SQ; writing—original draft preparation, YG, QC, and SQ; writing—review and editing, YG, QC, SQ and XK. All authors have read and agreed to the published version of the manuscript.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Aggarwal, R., Erel, I., Ferreira, M., and Matos, P. (2011). Does governance travel around the world? Evidence from institutional investors. J. Financial Econ. 100 (1), 154–181. doi:10.1016/j.jfineco.2010.10.018

An, Z., Chen, C., Naiker, V., and Wang, J. (2020). Does media coverage deter firms from withholding bad news? Evidence from stock price crash risk. J. Corp. Finance 64, 101664. doi:10.1016/j.jcorpfin.2020.101664

Baron, R., and Kenny, D. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personality Soc. Psychol. 51 (6), 1173–1182. doi:10.1037/0022-3514.51.6.1173

Bennett, B., Stulz, R., and Wang, Z. (2020). Does the stock market make firms more productive? J. Financial Econ. 136 (2), 281–306. doi:10.1016/j.jfineco.2019.09.006

Callen, J. L., and Fang, X. (2015). Religion and stock price crash risk. J. Financial Quantitative Analysis 50 (1-2), 169–195. doi:10.1017/s0022109015000046

Chen, J., Hong, H., and Stein, J. C. (2001). Forecasting crashes: Trading volume, past returns, and conditional skewness in stock prices. J. Financ. Econ. 61 (3), 345–381.

Chen, S. Y., and Chen, D. K. (2018). Air pollution, government regulations and high-quality economic development. Econ. Res. J. 53 (2), 20–34.

Chen, S., Ye, Y., and Jebran, K. (2022). Tax enforcement efforts and stock price crash risk: Evidence from China. J. Int. Financial Manag. Account. 33 (2), 193–218. doi:10.1111/jifm.12145

Cho, C. H., and Patten, D. M. (2007). The role of environmental disclosures as tools of legitimacy: A research note. Account. Organ. Soc. 32 (7-8), 639–647. doi:10.1016/j.aos.2006.09.009

Earnhart, D., and Lizal, L. (2006). Effects of ownership and financial performance on corporate environmental performance. J. Comp. Econ. 34 (1), 111–129. doi:10.1016/j.jce.2005.11.007

Fang, L., and Peress, J. (2009). Media coverage and the cross-section of stock returns. J. Finance 64 (5), 2023–2052. doi:10.1111/j.1540-6261.2009.01493.x

Fang, Y., and Guo, J. (2018). Is the environmental violation disclosure policy effective in China: Evidence from capital market reactions. Econ. Res. J. 53 (10), 158–174.

Ferrell, A., Liang, H., and Renneboog, L. (2016). Socially responsible firms. J. Financial Econ. 122 (3), 585–606. doi:10.1016/j.jfineco.2015.12.003

Fu, J., Wu, X., Liu, Y., and Chen, R. (2021). Firm-specific investor sentiment and stock price crash risk. Finance Res. Lett. 38, 101442. doi:10.1016/j.frl.2020.101442

Godfrey, P. C., Merrill, C. B., and Hansen, J. M. (2009). The relationship between corporate social responsibility and shareholder value: An empirical test of the risk management hypothesis. Strategic Manag. J. 30 (4), 425–445. doi:10.1002/smj.750

Habib, A., Hasan, M. M., and Jiang, H. (2018). Stock price crash risk: Review of the empirical literature. Account. Finance 58, 211–251. doi:10.1111/acfi.12278

Hao, X. C., and Su, Z. X. (2014). Can primary risk disclosure mitigate IPO underpricing? Evidence from text analysis. J. Finance Econ. 40 (5), 42–53.

Heckman, J. J., Ichimura, H., and Todd, P. E. (1997). Matching as an econometric evaluation estimator: Evidence from evaluating a job training programme. Rev. Econ. Stud. 64 (4), 605–654. doi:10.2307/2971733

Hossain, M. M., Mammadov, B., and Vakilzadeh, H. (2022). Wisdom of the crowd and stock price crash risk: Evidence from social media. Rev. Quantitative Finance Account. 58 (2), 709–742. doi:10.1007/s11156-021-01007-x

Hu, Y. M., and Tan, Y. C. (2013). Non-financial information disclosure: Literature review and future prospects. Acc. Res. 3, 20–26.

Hutton, A. P., Marcus, A. J., and Tehranian, H. (2009). Opaque financial reports, R2, and crash risk. J. Financial Econ. 94 (1), 67–86. doi:10.1016/j.jfineco.2008.10.003

Jacoby, G., Liu, M., Wang, Y., Wu, Z., and Zhang, Y. (2019). Corporate governance, external control, and environmental information transparency: Evidence from emerging markets. J. Int. Financial Mark. Institutions Money 58, 269–283. doi:10.1016/j.intfin.2018.11.015

Jiang, F., and Kim, K. A. (2015). Corporate governance in China: A modern perspective. J. Corp. Finance 32, 190–216. doi:10.1016/j.jcorpfin.2014.10.010

Jin, L., and Myers, S. C. (2006). R2 around the world: New theory and new tests. J. Financial Econ. 79 (2), 257–292. doi:10.1016/j.jfineco.2004.11.003

Kang, J., Yu, C., Xue, R., Yang, D., and Shan, Y. (2022). Can regional integration narrow city-level energy efficiency gap in China? Energy Policy 163, 112820. doi:10.1016/j.enpol.2022.112820

Kim, J. B., Li, Y., and Zhang, L. (2011). Corporate tax avoidance and stock price crash risk: Firm-level analysis. J. Financial Econ. 100 (3), 639–662. doi:10.1016/j.jfineco.2010.07.007

Kim, Y., Li, H., and Li, S. (2014). Corporate social responsibility and stock price crash risk. J. Bank. Finance 43, 1–13. doi:10.1016/j.jbankfin.2014.02.013

Liu, H., Jiang, J., Xue, R., Meng, X., and Hu, S. (2022a). Corporate environmental governance scheme and investment efficiency over the course of COVID-19. Finance Res. Lett. 47, 102726. doi:10.1016/j.frl.2022.102726

Liu, H., Wang, Y., Xue, R., Linnenluecke, M., and Cai, C. W. (2022b). Green commitment and stock price crash risk. Finance Res. Lett. 47, 102646. doi:10.1016/j.frl.2021.102646

Liu, X., and Anbumozhi, V. (2009). Determinant factors of corporate environmental information disclosure: An empirical study of Chinese listed companies. J. Clean. Prod. 17 (6), 593–600. doi:10.1016/j.jclepro.2008.10.001

Lizzeri, A. (1999). Information revelation and certification intermediaries. RAND J. Econ. 30, 214–231. doi:10.2307/2556078

Luo, W., Guo, X., Zhong, S., and Wang, J. (2019). Environmental information disclosure quality, media attention and debt financing costs: Evidence from Chinese heavy polluting listed companies. J. Clean. Prod. 231, 268–277. doi:10.1016/j.jclepro.2019.05.237

Magill, M., Quinzii, M., and Rochet, J. C. (2015). A theory of the stakeholder corporation. Econometrica 83 (5), 1685–1725. doi:10.3982/ecta11455

Song, X. Z., Hu, J., and Li, S. H. (2017). Corporate social responsibility disclosure and stock price crash risk: Based on information effect and reputation insurance effect. J. Financial Res. 4, 161–175.

Stivers, A. E. (2004). Unraveling of information: Competition and uncertainty. BE J. Theor. Econ. 4 (1). doi:10.2202/1534-598x.1151

Strycharz, J., Strauss, N., and Trilling, D. (2018). The role of media coverage in explaining stock market fluctuations: Insights for strategic financial communication. Int. J. Strategic Commun. 12 (1), 67–85. doi:10.1080/1553118x.2017.1378220

Tao, H., Zhuang, S., Xue, R., Cao, W., Tian, J., and Shan, Y. (2022). Environmental finance: An interdisciplinary review. Technol. Forecast. Soc. Change 179, 121639. doi:10.1016/j.techfore.2022.121639

Tao, K. T., Guo, X. Y., and Sun, N. (2020). Research on the relationship between corporate environmental information disclosure and corporate performance from the perspective of green governance—Evidence from 67 heavily polluted listed companies in China. China Soft Sci. (02), 108–119.

Tian, J., Yu, L., Xue, R., Zhuang, S., and Shan, Y. (2022). Global low-carbon energy transition in the post-COVID-19 era. Appl. Energy 307, 118205. doi:10.1016/j.apenergy.2021.118205

Wan, D., Xue, R., Linnenluecke, M., Tian, J., and Shan, Y. (2021). The impact of investor attention during COVID-19 on investment in clean energy versus fossil fuel firms. Finance Res. Lett. 43, 101955. doi:10.1016/j.frl.2021.101955

Wang, X., Xu, X., and Wang, C. (2013). Public pressure, social reputation, inside governance and firm environmental information disclosure: The evidence from Chinese listed manufacturing firms. Nankai Bus. Rev. 16 (2), 82–91.

Xiang, C., Chen, F., and Wang, Q. (2020). Institutional investor inattention and stock price crash risk. Finance Res. Lett. 33, 101184. doi:10.1016/j.frl.2019.05.002

Yan, H., and Chen, B. (2017). Climate change, environment regulation and the firm value of carbon emissions disclosure. J. Financial Res. (6), 142–158.

Ye, C. G., Wang, Z., Wu, J. F., and Li, H. (2015). External governance, environmental information disclosure and the cost of equity financing. Nankai Bus. Rev. 18 (5), 85–96.

Keywords: environmental information disclosure, nonfinancial information disclosure, media coverage, stock price crash risk, corporate governance

Citation: Ge Y, Chen Q, Qiu S and Kong X (2023) Environmental information disclosure and stock price crash risk: Evidence from China. Front. Environ. Sci. 11:1108508. doi: 10.3389/fenvs.2023.1108508

Received: 26 November 2022; Accepted: 30 January 2023;

Published: 13 February 2023.

Edited by:

Rui Xue, Macquarie University, AustraliaReviewed by:

Yongping Li, Qilu University of Technology, ChinaCopyright © 2023 Ge, Chen, Qiu and Kong. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Qi Chen, MTU4MDY2Nzg5ODBAMTYzLmNvbQ==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.