Wei Zhang1

Wei Zhang1 Kaidi Yang

Kaidi Yang Yulei Li

Yulei Li

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 10 February 2023

Sec. Interdisciplinary Climate Studies

Volume 11 - 2023 | https://doi.org/10.3389/fenvs.2023.1045827

This article is part of the Research Topic Environmental Risk and Corporate Behaviour View all 30 articles

Using Chinese listed companies as the research setting, this study investigates the impact of climate risk on corporate precautionary cash holdings and further explores possible underlying channels. We first apply the text mining technique to construct the climate risk indicator. The regression results then show that climate risk has a significant and positive impact on corporate precautionary cash holdings. Such positive relationship is stronger for firms with small size and those located in central and eastern China. Further mechanism analysis indicates that risk taking and external financing play a mediating effect between climate risk and corporate precautionary cash holdings. Our findings have important practical implications for companies to make sustainability strategies against potential climate risks.

Climate risk should be highly concerned for it bringing increasing uncertainty to companies (Huang et al., 2018; Pinkse and Gasbarro, 2019; Kanagaretnam et al., 2022). Extreme weather events accelerate the depreciation of fixed assets of companies, even cause serious damage, and it also reduce labor productivity and adversely affect the sales and profitability of companies (Fuss, 2016; Hasegawa et al., 2016). From 2000 to 2019, there were more than 11,000 extreme weather events in the world, which directly caused 475,000 deaths and 2.56 trillion US dollars in economic losses (Eckstein et al., 2021). More importantly, in the process to a low-carbon economy, the climate risk causes that companies are negatively affected in finance and reputation because of changes in the aspects of relevant policies, laws, technologies and market (Huynh and Xia, 2021; Ren et al., 2021). For example, the transition of energy sources leads to that the utilization rate of traditional fossil energy declines, substantial financial and technical support are required for utilizing and developing renewable energy, and fossil fuel companies and energy intensive companies relying on fossil fuels face difficulties (Green and Newman, 2017; Zhang et al., 2022).

Climate risk not only brings uncertainty to companies, but also requires companies to implement appropriate risk prevention measures (Desing and Widmer, 2021). According to the preventive motivation theory, increasing precautionary cash holdings is an effective way to mitigate the uncertainty risks faced by companies (Han and Qiu, 2007). Precautionary cash can protect and buffer corporate investment and financing when companies face uncertainty. In terms of corporate investment, uncertainty increases the investment risk, thus corporate managers are more cautious about investment to reduce risks (Aghion et al., 2005; Bloom et al., 2007; Chatjuthamard et al., 2020). Cautious companies increase their precautionary cash holdings in order to meet future investment opportunities and reduce future financial distress (Bates et al., 2009). In terms of corporate finance, uncertain risks exacerbate information asymmetry. To reduce market and default risk, banks often reduce the scale of loans to companies or even suspend related business transactions, which causes a reduction in external financing of companies (Salas and Saurina, 2002). In order to mitigate the negative impact of the decline of external financing, companies tend to increase cash savings to ensure liquidity (Bliss et al., 2015). In addition, the dynamic trade-off theory shows that companies need to weigh between current investment and financing and future ones when facing future financing constraints (Almeida et al., 2004). When faced with external financing pressures, it is more expensive for a company to raise external funds than to use internal funds. At this point, it may be the best option for companies to hold some precautionary cash to meet the needs of investment (Opler et al., 1999).

Concern over the impact of climate risk on companies has grown over the past few years, and existing researches mainly focus on the direct impact of climate risk on corporate operation. For example, Hong et al., (2019) points out that climate change aggravates natural disasters, which causes serious damage to companies’ production and profits. Javadi and Masum (2021) found that the interest margin of bank loans paid by companies is significantly higher in areas with high climate risk. However, there are few studies about how companies strategically prevent climate risks, especially in China. In recent years, extreme weather events have occurred frequently in China, causing huge losses of economy. For example, the Wenchuan earthquake in 2008, the torrential rain in Beijing in 2012, the Typhoon Lichma in 2019 and the torrential rain in Henan in 2021 directly caused economic losses of 845.14 billion yuan, 11.64 billion yuan, 51.53 billion yuan and 114.269 billion yuan respectively. Moreover, as the largest carbon emitter globally, how to deal with the transformation risk is a major issue which is widely concerned by government, companies and the public (Tian et al., 2022a; Liu et al., 2022; Zhai et al., 2022). Therefore, this study is pioneering, which enriches research on precautionary cash holdings strategy adopted by Chinese listed companies to deal with climate risk. And Chinese listed companies pay close attention to climate risk, which provides an ideal research background.

Climate risk increases the uncertainty faced by companies (Barnett et al., 2020) and affects corporate strategies for cash holding. In the relevant research on influencing factors of corporate cash holdings, precautionary motivation, agency cost, transaction demand, and tax cost are all considered possible reasons for companies to maintain a high level of cash holdings (Bates et al., 2009). Among them, precautionary motivation is an important reason for companies to maintain a high level of cash holdings (Duchin, 2010; Mclean, 2011). This is because holding cash may help companies to better cope with liquidity risk and prevent operation uncertainty. As an important corporate operation decision, cash holding is affected by internal and external comprehensive factors of the company (Opler et al., 1999). Baum et al. (2009) and Pinkowitz et al. (2013) have studied the impact of macroeconomic fluctuations on corporate cash holdings. Others studied the impact of characteristics at the company level on cash holdings, such as company size, financial leverage, investment opportunities, ownership, and governance factors (Ferreira and Vilela, 2004; Ozkan and Ozkan, 2004; Kusnadi, 2011). However, most of the studies mentioned above focus on company the economic environment-level characteristics and discuss the impact of economic and internal factors on corporate cash holding strategies. The research on how climate risk affects corporate cash holdings is still insufficient. And this study explores the impact of climate risk on corporate precautionary cash holdings.

In this study, we investigate whether and how climate risk affects precautionary cash holdings with the data of Chinese listed companies during the period 2007–2020. Text mining is used to construct climate risk perception indexes to represent the climate risk faced by companies. And we use panel regression model and mediator model to test the impact of climate risk on precautionary cash holdings. According to the empirical analysis, the following three conclusions are drawn: 1) Climate risk has a positive impact on precautionary cash holdings. And the higher climate risk companies face, the more precautionary cash holdings companies hold. This conclusion remains valid under a series of robustness tests. 2) The positive impact of climate risk on the precautionary cash holdings is stronger for firms with small scale and those located in central and eastern China. 3) Risk taking and external financing are two important channels for climate risk to affect precautionary cash holdings.

This study contributes to the existing literature in at least three ways: First, the climate risk index constructed in our research provides a practical method for studying the impact of climate risk on companies (Huang et al., 2018; Kanagaretnam et al., 2022). The climate risk measurement index used in most existing literature is the Global Climate Risk index (CRI) prepared by German. Although this index can describe the climate risks among different countries, it lacks climate information in company level, which is difficult to quantify the relationship between climate risks and companies (Ren et al., 2022). Thus, we use text mining technology in the corporate management discussion and analysis (MD&A) disclosure to construct the corporate climate risk perception index which measures the climate risk faced by the companies. By this measurement, we can estimate the impact of climate risk on companies more accurately with a larger research sample. Moreover, our study extends the field of text mining using MD&A (Choi et al., 2020; Tian et al., 2022b). Second, this study enriches the research about the influence channels of climate risk on precautionary cash holdings (Chen et al., 2020; Xiao et al., 2020). We find that risk taking and external financing are two important channels for climate risk to affect precautionary cash holdings. When facing high climate risk, on the one hand, corporate managers are usually cautious about investment to reduce risk taking, and thus increase precautionary cash holdings; On the other hand, as banks reduce the supply of loans, the scale of corporate external financing decreases, which also result in the increase of precautionary cash holdings. Third, this study supplements the important factors affecting corporate cash holding behavior. Previous studies explain the level of cash holdings based on the characteristics of economic environment and company level (Ferreira and Vilela, 2004; Ozkan and Ozkan, 2004; Baum et al., 2009; Kusnadi, 2011; Pinkowitz et al., 2013). Compared with these studies, our study also provides additional evidence that climate risk affects corporate cash holdings. And our findings have important implications for companies to deal with climate risks with prevention behaviors.

Climate risk greatly increases the uncertainty faced by companies (Barnett et al., 2020). Climate risks are divided into physical risks and transition risks (Financial Stability Board, FSB; Task Force on Climate-related Financial Disclosure, TCFD). Physical risks refer to asset loss caused by extreme weather (such as drought, flood and hurricane) and long-term climate change (such as climate warming and sea level rise). In the short term, more frequent and severe extreme weather brings the risk of production facilities damage and value chain interruption to the companies; In the long term, global and regional long-term climate change lead to the reduction of output in agriculture, labor and material (Ebi et al., 2021; Meyer et al., 2022). Transition risks refer to the risks arising during the society transiting to a low-carbon and climate adaptive economy, including all risks caused by policies, laws, technologies, market sentiment, reputation, etc. For example, more or stricter policies transformation increases the operating costs of companies (Dunz et al., 2019; Zhang and Cheng, 2022). Facing the uncertainty caused by climate risk, companies usually take preventive measures (Desing and Widmer, 2021), such as adjusting companies’ precautionary cash holding strategies.

The attitude and ability of companies to deal with climate risks are crucial to mitigate uncertainty risks (Todaro et al., 2021). Risk taking reflects corporate managers’ risk preference and risk control (Li and Tang, 2010; Wen et al., 2021). Higher risk taking can stimulate corporate potential and help companies gain advantages in long-term competition, while lower risk taking can maintain stable growth of corporate performance. In the case of high climate risk, corporate managers are more likely to adopt conservative investment strategies to avoid investment risks. That is, companies facing high climate risk have low risk taking. Zhou D. et al. (2022a) found that the temperature rising significantly hinder corporate risk investment, thus reducing corporate risk-taking level. And the management’s trade-off between risk and return determines the cash holdings scale of a company. (Chen et al., 2012; Gao et al., 2013; Harford et al., 2014). As the value of cash is not easily affected by market price fluctuations and cash turnover is fast, cash holding has lower risk than other forms of assets (Lei et al., 2022). Based on this, cash, as a type of asset with high liquidity and low risk, is favored by risk averter. Although holding cash does not typically generate large profits for companies, it is unlikely to result in significant investment losses (Zhou M. et al., 2022b). Companies with cautious management and low risk taking would hold more cash for long-term stable development (Bates et al., 2009; Xu et al., 2016). Therefore, when faced with high climate risk, companies will reduce risk taking and thus increase precautionary cash holdings.

In addition, a company with higher climate risk is faced with the dilemma of costs rising, revenues falling and profits declining, which increases the possibility that the company cannot afford debts so that it threatens the stability and development of financial institutions (Cai et al., 2019). Considering own interests and social responsibilities, banks would control the loans scale to companies with high climate risk, which result in a decline in these companies’ external financing (Huang et al., 2022). For example, more than 30 major banks around the world indicate that they will no longer provide financing services for coal related projects or coal power companies. These companies with unfavorable financing constraints can only use their own funds for R&D activities. The decline in external financing causes companies to face the risk of bankruptcy liquidation due to capital chain rupture, thus companies need to make positive dynamic adjustments of cash holdings to deal with this risk (Denis and Sibilkov, 2010). Companies easy to obtain external financing are more likely to choose external financing rather than internal cash as a tool for market competition and access to investment opportunities. On the contrary, for companies that are not easy to obtain external financing, their cash holdings are more likely to play a competitive effect in the market (Beck and Demirguc-Kunt, 2006). Thus, in order to maintain liquidity and meet the needs of future investment, companies with external financing shortage would limit the current budget and increase cash holdings (Almeida et al., 2004). And when faced with high climate risk, corporate external financing decreases, and thus companies increase their precautionary cash holdings.

To sum up, companies would take preventive measures when facing uncertainty caused by climate risk, and adjusting precautionary cash holdings is the best measure to deal with the uncertainty. On the one hand, companies with higher climate risks would be more cautious, thus reducing risk taking. On the other hand, it is more difficult for companies to obtain bank loans when the climate risk increases, which means external financing of companies decreases. And precautionary cash can alleviate the shortage of investment and financing when companies face uncertain risks. Therefore, climate risk increases the uncertainty faced by companies, while increasing precautionary cash holdings can reduce this adverse effect. Therefore, we propose:

Hypothesis 1. Climate risk has a positive impact on precautionary cash holdings.

Based on the text analysis of MD&A disclosure, this study constructs a climate risk perception index to measure the climate risk faced by companies. Following to existing research (Choi et al., 2020; Tian et al., 2022a), we construct the climate risk index in three steps: First, we select the seed word set of climate risk in MD&A including the causes (such as global warming, air pollution), reflections (such as storms, soil erosion) and results (such as environmental governance, energy saving and emission reduction) of climate risk. Secondly, using the deep learning technology provided by the Wingo financial text data platform1, we select an expanded word set which has a similarity of 0.5 or more with the seed word set, and remove duplicate words. To remain objectivity, we invite three experts in academics and industry to triangulate the expanded word set, and finally determine the climate risk seed word set containing 271 seed words. Finally, we make word frequency statistics on the climate risk seed word set in each MD&A document and calculate the ratio of climate risk seed word’s frequency to MD&A’s total word frequency, then the climate risk perception index of the company is obtained. The larger the climate risk perception value of a company is, the higher climate risk the company faces.

Following Almeida et al. (2004), Sun and Wang (2015) and Su et al. (2020), the precautionary cash holdings (PreCashi,t) are measured by the ratio of the added value of cash and cash equivalents to the total assets minus the ending balance of cash and cash equivalents:

We quantify risk taking from the perspective of earnings volatility (VOL). Following John et al. (2008), corporate profitability is measured by the return on assets. Considering that the term of office of senior managers of listed companies in China is generally three years, we use the standard deviation of return on assets of a company within three years to measure its earnings volatility. The larger a company’s standard deviation of the return on assets is, the greater its earnings volatility is, and the higher risk taking the company faces.

Stock and bond markets are immature in China, and bank loans is the main source of external financing for companies. Thus, most Chinese companies rely on banks, and most of their loans are supported by bank loans (Firth et al., 2012; Liu et al., 2018). Following Su et al., (2020), we measure external financing (BLR) with the ratio of short-term loans plus long-term loans due in one year to total assets. The larger this value is, the larger the company’s external financing scale is.

Based on existing researches about precautionary cash holdings (Su et al., 2020; Xiong et al., 2021; Zhang and Cheng, 2022), we select total assets (Size), debt-to-asset ratio (Lev), company age (Age), Tobin’s Q (TobinQ), managements shareholdings ratio (Mshare) as the control variables. The definitions of variables used in this study are provided in Appendix.

Since 2007, China’s accounting standards have acted on international convention, and new “The Corporate Accounting Standards” has been implemented. To avoid the impact of differences in accounting standards before and after, we construct sample based on Chinese listed companies from 2007 to 2020. And we remove observations from initial samples as follows: 1) financial service and insurance industry, 2) firms with less than 2 years’ available data, and 3) special treatment (ST) and *ST companies. The information of corporate management discussion and analysis (MD&A) is collected from Cninfo website, and other data are acquired from the China Stock Market and Accounting Research (CSMAR) database. To avoid the influence of outliers, all continuous variables are winsorized at the upper and lower 1% levels. Finally, we obtain 25,889 firm-year observations from 3,377 Chinese listed companies.

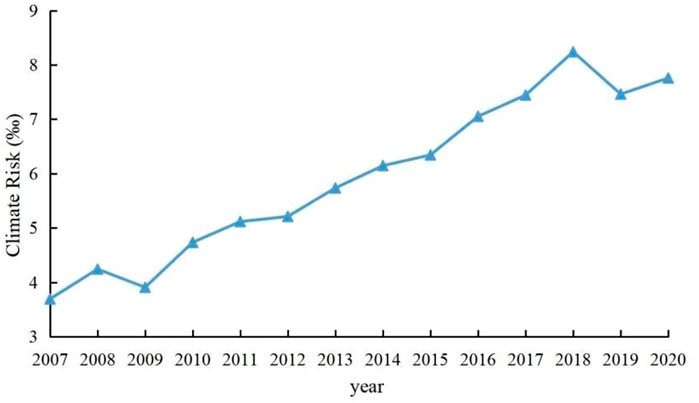

Figure 1 shows the change trend of average climate risk faced by companies from 2007 to 2020. The overall trend of climate risk faced by companies is on the rise, that is, companies’ climate risk is increasingly high. In addition, the climate risk index constructed in this study is significantly related to China’s climate risk score in the global Climate Risk Index (CRI) prepared by Germany at the 1% level, which indicates the reliability of our climate risk index.2

FIGURE 1. The trend of climate risk changes from 2007 to 2020.

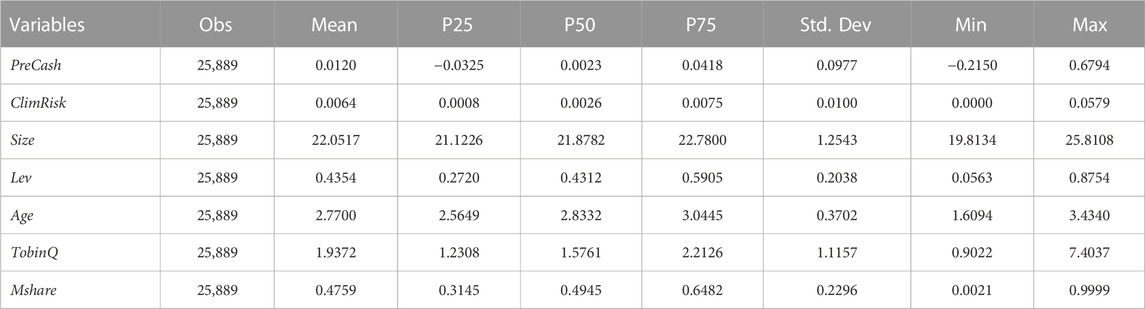

Table 1 provides a brief summary of descriptive statistics for main variables. Precautionary cash holdings (PreCash) have a mean of 0.0120, a standard deviation of 0.0977, a minimum of −0.2150 and a maximum of 0.6794. And climate risk (ClimRisk) has a mean of 0.0064, a standard deviation of 0.0100, a minimum of 0 and a maximum of 0.0579. It indicates that the key indicators fluctuate greatly within our study setting.

TABLE 1. Describes statistics.

This study examines the relationship between climate risk and precautionary cash holdings by the following panel regression model:

where PreCashi,t represents the precautionary cash holdings of company i in year t; ClimRiski,t represents the climate risk faced by company i in year t. Zi,t represents control variables, which includes total assets (Size), debt-to-asset ratio (Lev), company age (Age), Tobin’s Q (TobinQ), managements shareholdings ratio (Mshare). Year and industry fixed effects are controlled. And

Following Edwards and Lambert (2007), we examine the mediating effect of risk taking and external financing by the following models:

where Mi,t represents intermediate variable, which includes risk taking (VOL) and external financing (BLR). The definitions of other variables are identical to those of the Eq. 2.

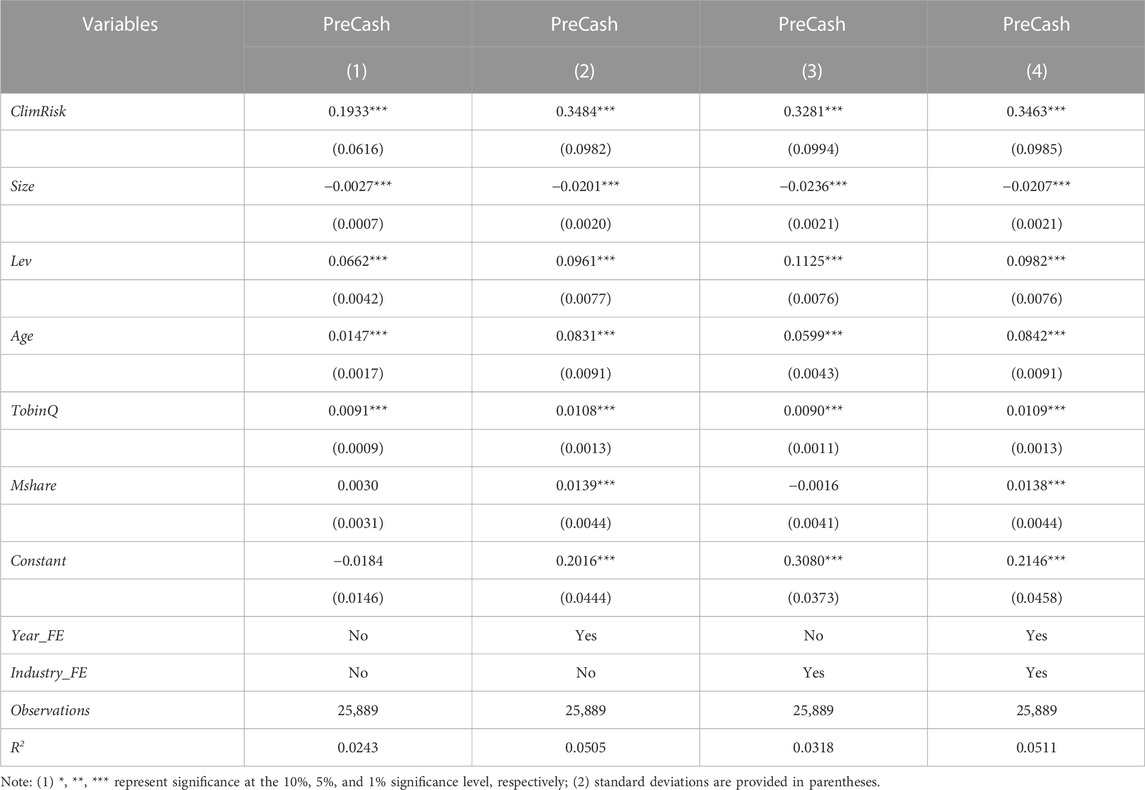

Table 2 shows the baseline regression results. Column (1) is the mixture regression result. Column (2) and column (3) show the results of regression with year fixed effect and that with industry fixed effect respectively. And column (4) shows the regression results with both year fixed effect and industry fixed effect. These results all show that the coefficient of ClimRisk is positive and significant at the 1% level, which is consistent with Hypothesis 1, meaning that a company would increase its precautionary cash holdings when the climate risk increases.

TABLE 2. Baseline regression results.

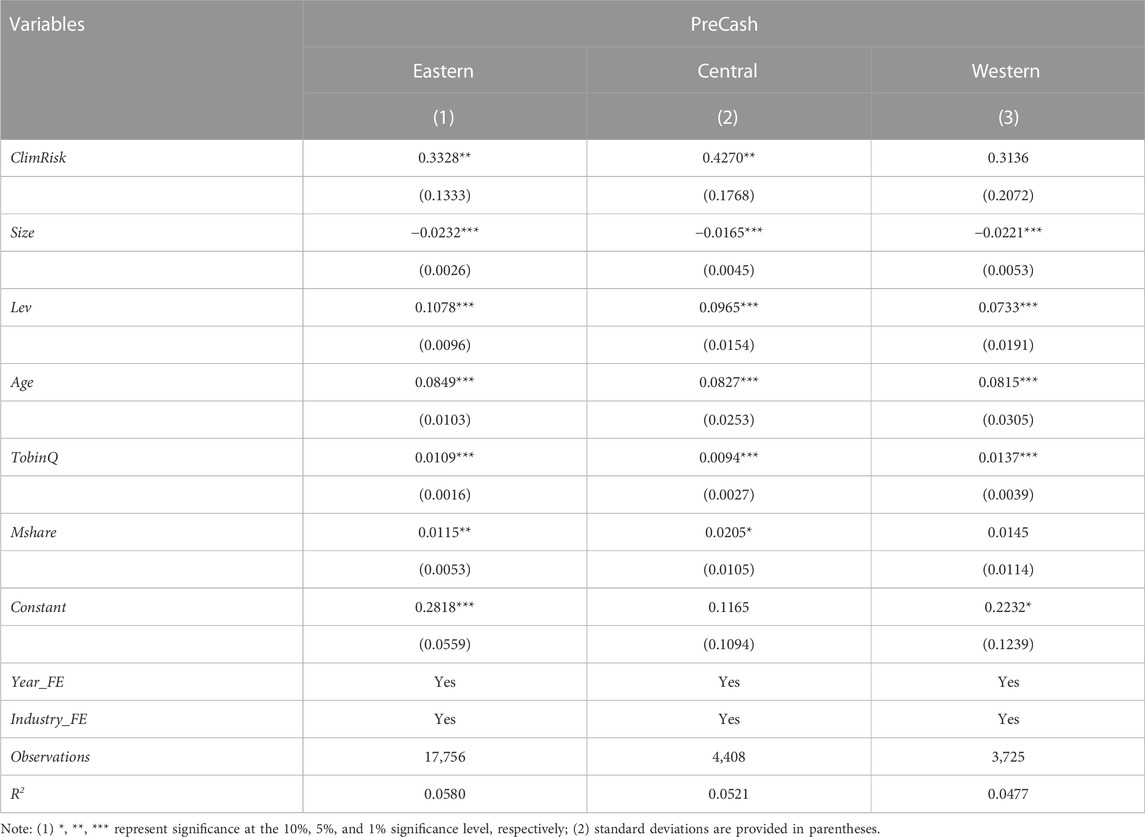

The climate risk faced by a company depends on the region where the company is located (Ginglinger and Moreau, 2019). Compared with the western region, the eastern and central regions of China face higher cost of environmental governance and more serious climate impacts. And the eastern and central regions of China have a higher degree of marketization and a better market system (Ren et al., 2022). Companies located in the eastern and central regions are more sensitive to climate change when they change their business and investment, and these companies enable adapt to the changing climate risks with various strategies. Thus, in order to catch the moderating effect of climate risk and precautionary cash holdings in the region where the company is located, we test the region heterogeneity of the impact of climate risk on precautionary cash holdings. Specifically, we conduct sub sample regression on the companies located in the eastern, central and western regions of China.

The regression results are shown in Table 3. Column (1) to column (3) respectively report the regression results of the climate risk of companies in eastern, central and western China on their precautionary cash holdings. Climate risk has a significant and positive impact on precautionary cash holdings for companies located in eastern and central China, while it is not significant for companies in western China.

TABLE 3. The regression results of region heterogeneity.

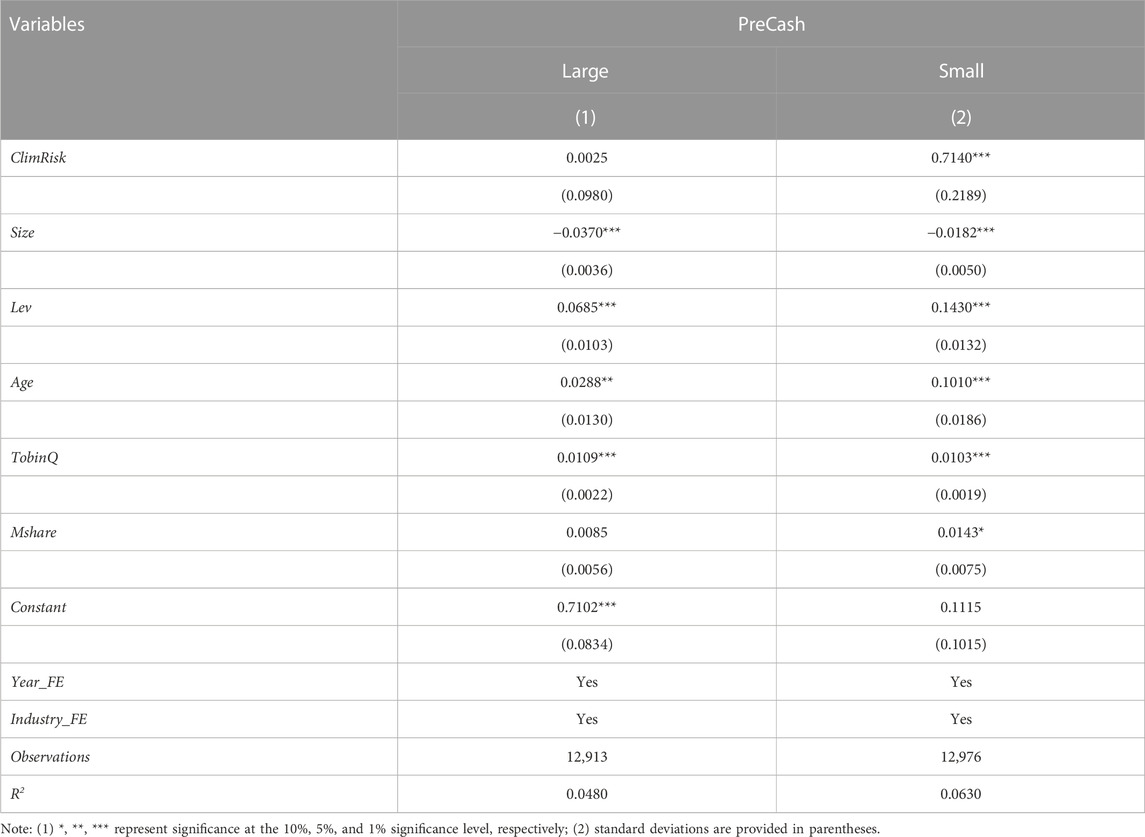

Corporate size is another important company-level consideration that affects precautionary cash holdings (Nguyen et al., 2016). Corporate scale reflects the overall capability and performance of the company. Due to China’s special institutional background, large-scale companies hold most bank credit, while limited credit funds from state-owned financial institutions is available for small-scale companies. Compared with large-scale companies, small-scale companies obtain external funds with stricter financing conditions and higher financing costs (Rostamkalaei and Freel, 2016). The uncertainty brought by climate risk further increases the difficulty for small-scale companies to achieve their financing goals. In order to effectively mitigate the possible adverse effects of climate risks and take potential market opportunities, small-scale companies would make decisions quickly to change conventional practices (Crick et al., 2018). Thus, we analyze scale heterogeneity to identify the moderating effect of corporate scale on climate risk and precautionary cash holdings. If the total assets of a company are above the median of the total assets of all companies, we regard this company as a large-scale company; otherwise, a small-scale company.

The regression results are shown in Table 4. Column (1) and column (2) in Table 4 respectively show the regression results of climate risk of large-scale companies and small-scale companies on precautionary cash holdings, suggesting climate risk has a significant and positive impact on precautionary cash holdings in small-scale companies. However, no significant impact is observed in large-scale companies.

TABLE 4. The regression results of scale heterogeneity.

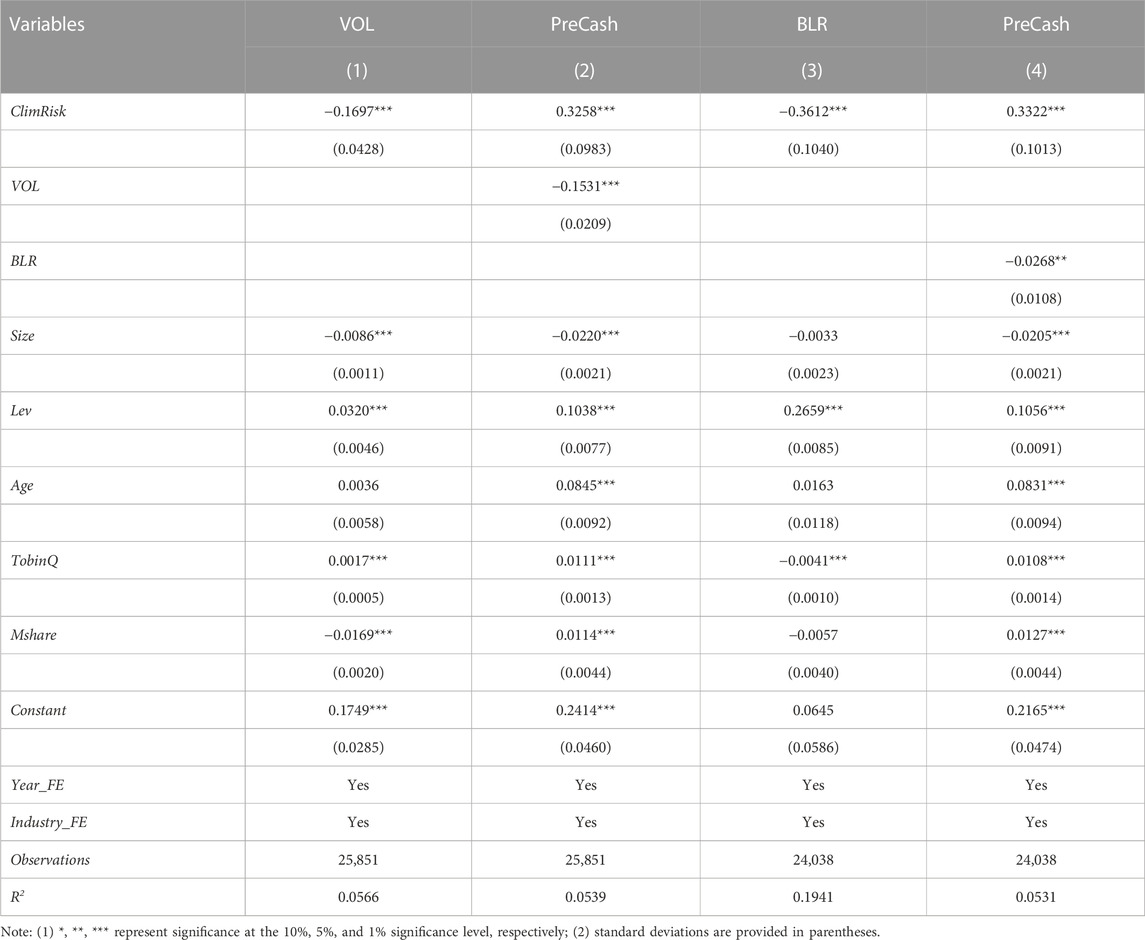

In this section, we examine the mediating effect of risk taking (VOL) and external financing (BLR) in the impact of climate risk on precautionary cash holdings. First, we examine whether the increase of companies’ climate risk leads to the reduction of their risk taking level and external financing. Second, we examine the impact of risk taking and external financing on precautionary cash holdings. Table 5 shows the results of the above analysis.

TABLE 5. The mediating effect of risk taking and external financing.

Columns (1) and (3) in Table 5 report the results about the impact of climate risk on risk taking and external financing respectively, suggesting that climate risk has a negative and significant impact on risk taking and external financing. It indicates that companies’ risk taking and external financing decrease with the increase of climate risk. Columns (2) and (4) respectively report the results about the impacts of risk taking and external financing on precautionary cash holdings, suggesting that risk taking and external financing both have a significantly negative impact on precautionary cash holdings. It indicates that the lower the risk taking is or the less the external financing is, the higher precautionary cash holdings a company has. Therefore, the climate risk faced by companies affects precautionary cash holdings through risk taking and external financing, that is, risk taking and external financing make a mediating effect between climate risk and precautionary cash holdings.

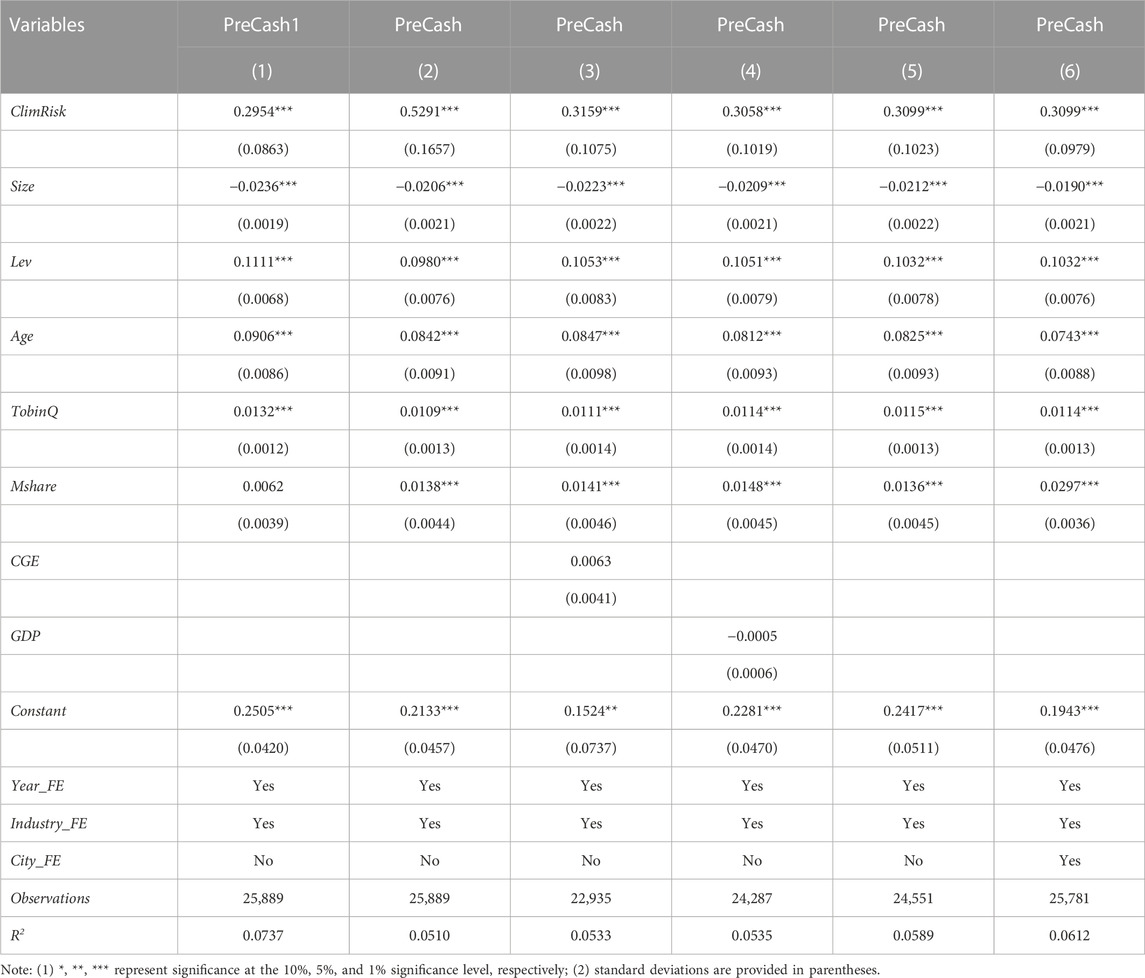

In this section, we conduct a battery of robustness checks. First, we re-estimate the baseline regression with another measure of precautionary cash holdings. Following the existing literature (Lin et al., 2021; Hasan et al., 2022; Seo and Han, 2022), we use the ratio of the increase in cash and cash equivalents to the total assets to measure the company’s precautionary cash holdings. The results are shown in column (1) of Table 6, which support our key findings that the impact of climate risk on precautionary cash holdings is significantly positive. Second, following Tian et al. (2022b), we select an expanded word set which has a similarity of 0.6 or more with the seed word set to construct climate risk indicators and then re-estimate the baseline regression. The results are shown in column (2) of Table 6, suggesting that the coefficient of ClimRisk is still positive and significant. Third, we consider eliminating the possible impact of macroeconomic factors on our research. Thus, we follow Su et al., (2020) to test the robustness of the baseline results by controlling local fiscal expenditure (CEG), per capita GDP (GDP) and urban fixed effects respectively. The results of these tests are given in columns (3) to (5), which shows that climate risk still has a significantly positive impact on precautionary cash holdings. Last, considering that sample period includes the global financial crisis period (GFC) (2008–2009), we follow Nguyen and Phan (2020) to exclude the GFC years from the sample period, which mitigates the impact of the financial crisis on the research results. Column (6) of Table 6 shows this result. And the oefficient of ClimRisk is still significantly positive at the level of 1%, suggesting our findings are robust and reliable3.

TABLE 6. Robustness tests.

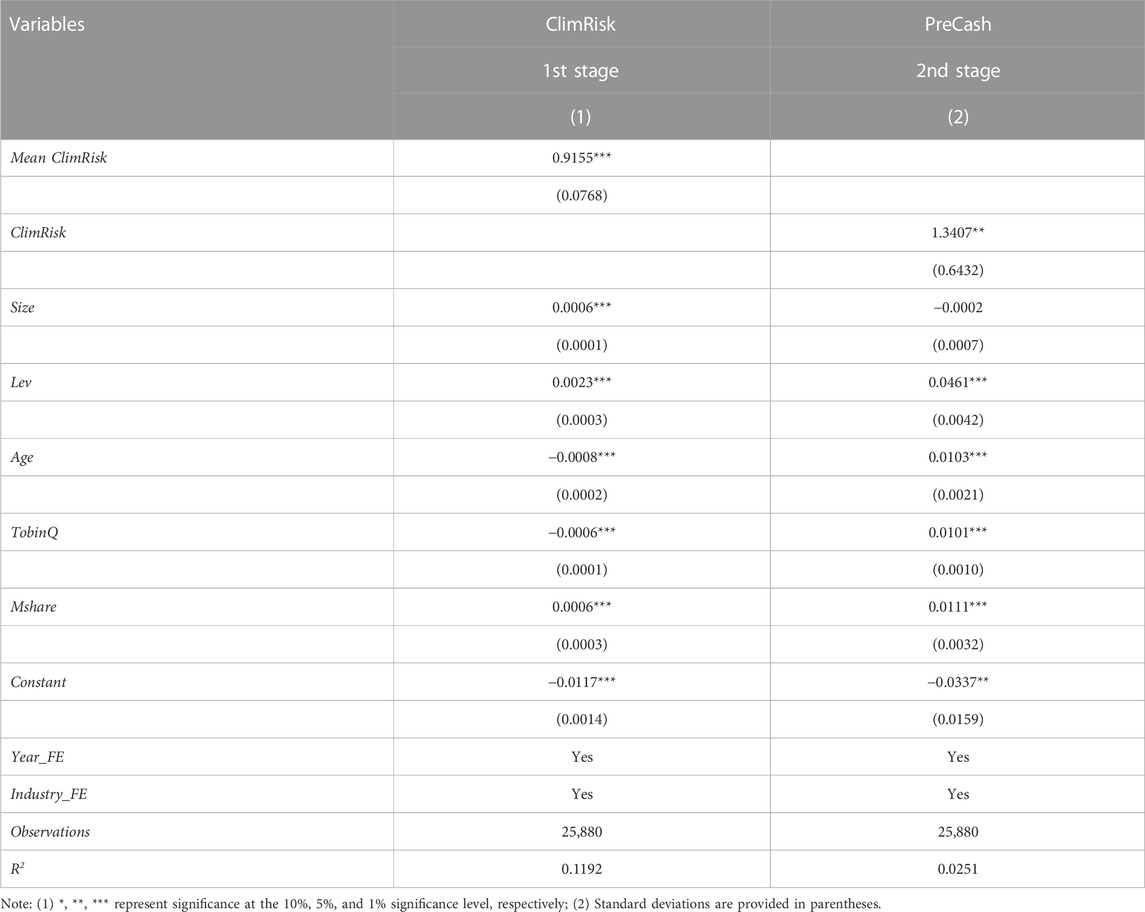

The baseline results of this study indicate that companies faced by high climate risk would increase precautionary cash holdings. And companies with high precautionary cash holdings are more likely to invest green projects, which affects their climate risk perception. Thus, the above studies may have endogenous problems. To solve these possible endogenous problems, we introduce instrumental variable. Inspired by Wintoki et al. (2012), we use the mean of all companies’ climate risk in the same industry over the years (Mean ClimRisk) as an instrumental variable for two-stage regression. The results of the two-stage regression are shown in Table 7. In the first stage of regression, we use the mean of climate risk in the industry where the company is in over the years and all control variables to explain the long-term level of climate risk. Column (1) is the result of the first stage. The coefficient of Mean ClimRisk is positive and significant and the F value is 119.28 which is far greater than 10, suggesting that there is a significant positive correlation between the mean of climate risk in the industry where the company is in over the years and the climate risk faced by the company. In the second stage of regression, we analyze the regression relationship between the precautionary cash holdings and the fitting value of climate risk in the first stage, and control variables are added. Column (2) of Table 7 shows the result that the coefficient of ClimRisk is still positive and significant. This test alleviates the endogenous problem to a certain extent. Moreover, the results of two-stage regression also support our baseline results, that is, climate risk has a significantly positive impact on precautionary cash holdings.

TABLE 7. Instrumental variable analysis.

This study takes China’s listed companies from 2007 to 2020 as the research setting and uses text mining technology to measure corporate climate risk perception which represents the level of climate risk faced by companies. We then use panel regression model and mediator model to respectively test the impact and impact channels of climate risk on corporate precautionary cash holdings. The results indicate that there is a significant and positive relationship between climate risk and corporate precautionary cash holdings. That is, the higher climate risk a company faces, the more precautionary cash holdings the company holds. We further explore the heterogeneous effects of region and scale. In terms of region heterogeneity, climate risk has a significantly positive impact on precautionary cash holdings of companies in eastern and central China, but no significant impact is observed in companies in Western China. In terms of scale heterogeneity, climate risk has a significantly positive impact on precautionary cash holdings of large-size companies, while has no significant impact on that of small-size companies. In addition, risk taking and external financing have mediating effects between climate risk and precautionary cash holdings. In other words, the climate risk faced by companies affects corporate precautionary cash holdings through affecting companies’ risk taking and external financing.

Based on the research conclusions, we make the following three suggestions for companies to cope with climate risks. First, while sensing climate risks, the company should develop reasonable preventive strategies and adjust precautionary cash holdings in time to meet the need of sustainable development. Second, in the case of high climate risk, changing environmental policies will increase companies’ investment risk. Companies need sharp risk awareness and control force to weight between risk and return. And companies should reasonably estimate its risk-taking level and select projects with low risk and stable income. Third, climate risk intensifies the information asymmetry in the capital market, which leads to the decrease of corporate external financing. On the one hand, banks should carefully identify corporate risk information and conduct credit risk assessment on specific projects, so as to avoid relying on industry attributes to make credit decisions which cause financial difficulties for company transformation. On the other hand, companies should enhance comprehensive strength to meet the investment requirements of financial institutions and investors.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

WZ: Methodology, validation, supervision. KY: Methodology, formal analysis, software, writing—review and editing YL: Data curation, writing—original draft preparation. KY: Software, formal analysis, writing—original draft preparation. YL: Software, writing—review and editing. All authors have read and agreed to the published version of the manuscript.

This research is supported by the National Social Science Foundation of China (Grant No. 21BTJ064) and the National Natural Science Foundation of China (Grant No. 72272018).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

2Details of this result can be obtained from the author.

3We also tested the robustness not only with using the explanatory variable lagged for one period, but also using one-period lagged explanatory variable and one-period lagged control variables. The results did not change and can be obtained from the author.

Aghion, P., Bloom, N., Blundell, R., Griffith, R., and Howitt, P. (2005). Competition and innovation: An inverted-U relationship. Q. J. Econ. 120 (2), 701–728. doi:10.1162/0033553053970214

Almeida, H., Campello, M., and Weisbach, M. S. (2004). The cash flow sensitivity of cash. J. Finance 59 (4), 1777–1804. doi:10.1111/j.1540-6261.2004.00679.X

Barnett, M., Brock, W., and Hansen, L. P. (2020). Pricing uncertainty induced by climate change. Rev. Financial Stud. 33 (3), 1024–1066. doi:10.1093/rfs/hhz144

Bates, T. W., Kahle, K. M., and Stulz, R. M. (2009). Why do US firms hold so much more cash than they used to? J. Finance 64 (5), 1985–2021. doi:10.1111/j.1540-6261.2009.01492.x

Baum, C. F., Caglayan, M., and Ozkan, N. (2009). The second moments matter: The impact of macroeconomic uncertainty on the allocation of loanable funds. Econ. Lett. 102 (2), 87–89. doi:10.1016/j.econlet.2008.11.019

Beck, T., and Demirguc-Kunt, A. (2006). Small and medium-size enterprises: Access to finance as a growth constraint. J. Bank. Finance 30 (11), 2931–2943. doi:10.1016/j.jbankfin.2006.05.009

Bliss, B. A., Cheng, Y., and Denis, D. J. (2015). Corporate payout, cash retention, and the supply of credit: Evidence from the 2008–2009 credit crisis. J. Financial Econ. 115 (3), 521–540. doi:10.1016/j.jfineco.2014.10.013

Bloom, N., Bond, S., and Van Reenen, J. (2007). Uncertainty and investment dynamics. Rev. Econ. Stud. 74 (2), 391–415. doi:10.1111/j.1467-937x.2007.00426.X

Cai, H., Wang, X., and Tan, C. (2019). Green credit policy, incremental bank loans and environmental protection effect. Acc. Res. 3, 88–95.

Chatjuthamard, P., Wongboonsin, P., Kongsompong, K., and Jiraporn, P. (2020). Does economic policy impertinty influence executive risk-taking incentives? Finance Res. Lett. 37 (101), 101385. doi:10.1016/j.frl.2019.101385

Chen, Q., Chen, X., Schipper, K., Xu, Y., and Xue, J. (2012). The sensitivity of corporate cash holdings to corporate governance. Rev. Financial Stud. 25 (12), 3610–3644. doi:10.1093/rfs/hhs099

Chen, R. R., Guedhami, O., Yang, Y., and Zaynutdinova, G. R. (2020). Corporate governance and cash holdings: Evidence from worldwide board reforms. J. Corp. Finance 65, 101771. doi:10.1016/j.jcorpfin.2020.101771

Choi, J., Suh, Y., and Jung, N. (2020). “Predicting corporate credit rating based on qualitative information of MD&A transformed using document vectorization techniques,” in Data technologies and applications. doi:10.1108/DTA-08-2019-0127

Crick, F., Eskander, S. M., Fankhauser, S., and Diop, M. (2018). How do african SMEs respond to climate risks? Evidence from Kenya and Senegal. World Dev. 108, 157–168. doi:10.1016/j.worlddev.2018.03.015

Denis, D. J., and Sibilkov, V. (2010). Financial constraints, investment, and the value of cash holdings. Rev. Financial Stud. 23 (1), 247–269. doi:10.1093/rfs/hhp031

Desing, H., and Widmer, R. (2021). Reducing climate risks with fast and complete energy transitions: Applying the precautionary principle to the paris agreement. Environ. Res. Lett. 16 (12), 121002. doi:10.1088/1748-9326/ac36f9

Duchin, R. (2010). Cash holdings and corporate diversification. J. Finance 65 (3), 955–992. doi:10.1111/j.1540-6261.2010.01558.x

Dunz, N., Naqvi, A., and Monasterolo, I. (2019). Climate transition risk, climate elements, and financial stability in a stock-flow consistent approach. SSRN Electron. J 65. doi:10.2139/ssrn.3520764

Ebi, K. L., Vanos, J., Baldwin, J. W., Bell, J. E., Hondula, D. M., Errett, N. A., et al. (2021). Extreme weather and climate change: Population health and health system implications. Annu. Rev. Public Health 42, 293–315. doi:10.1146/annurev-publhealth-012420-105026

Eckstein, D., Künzel, V., and Schäfer, L. (2021). “Global climate risk index 2021,” in Who suffers most from extreme weather events, 2000–2019.

Edwards, J. R., and Lambert, L. S. (2007). Methods for integrating moderation and mediation: A general analytical framework using moderated path analysis. Psychol. Methods 12 (1), 1–22. doi:10.1037/1082-989x.12.1.1

Ferreira, M. A., and Vilela, A. S. (2004). Why do firms hold cash? Evidence from EMU countries. Eur. Financ. Manag. 10 (2), 295–319. doi:10.1111/j.1354-7798.2004.00251.x

Firth, M., Malatesta, P. H., Xin, Q., and Xu, L. (2012). Corporate investment, government control, and financing channels: Evidence from China's Listed Companies. J. Corp. Finance 18 (3), 433–450. doi:10.1016/j.jcorpfin.2012.01.004

Fuss, S. (2016). Substantial risk for financial assets. Nat. Clim. Change 6 (7), 659–660. doi:10.1038/nclimate2989

Gao, H., Harford, J., and Li, K. (2013). Determinants of corporate cash policy: Insights from private firms. J. Financial Econ. 109 (3), 623–639. doi:10.1016/j.jfineco.2013.04.008

Ginglinger, E., and Moreau, Q. (2019). Climate risk and capital structure. Paris: Université Paris-Dauphine Research Paper, 3327185.

Green, J., and Newman, P. (2017). Disruptive innovation, stranded assets and forecasting: The rise and rise of renewable energy. J. Sustain. Finance Invest. 7 (2), 169–187. doi:10.1080/20430795.2016.1265410

Han, S., and Qiu, J. (2007). Corporate precautionary cash holdings. J. Corp. Finance 13 (1), 43–57. doi:10.1016/j.jcorpfin.2006.05.002

Harford, J., Klasa, S., and Maxwell, W. F. (2014). Refinancing risk and cash holdings. J. Finance 69 (3), 975–1012. doi:10.1111/jofi.12133

Hasan, M. M., Habib, A., and Zhao, R. (2022). Corporate reputation risk and cash holdings. Account. Finance 62 (1), 667–707. doi:10.1111/acfi.12803

Hasegawa, T., Fujimori, S., Takahashi, K., Yokohata, T., and Masui, T. (2016). Economic implications of climate change impacts on human health through undernourishment. Clim. Change 136 (2), 189–202. doi:10.1007/s10584-016-1606-4

Hong, H., Li, F. W., and Xu, J. (2019). Climate risks and market efficiency. J. Econ. 208 (1), 265–281. doi:10.1016/j.jeconom.2018.09.015

Huang, H. H., Kerstein, J., and Wang, C. (2018). The impact of climate risk on firm performance and financing choices: An international comparison. J. Int. Bus. Stud. 49 (5), 633–656. doi:10.1057/s41267-017-0125-5

Huang, H. H., Kerstein, J., Wang, C., and Wu, F. (2022). Firm climate risk, risk management, and bank loan financing. Strategic Manag. J. 43, 2849–2880. doi:10.1002/smj.3437

Huynh, T. D., and Xia, Y. (2021). Climate change news risk and corporate bond returns. J. Financial Quantitative Analysis 56 (6), 1985–2009. doi:10.1017/s0022109020000757

Javadi, S., and Masum, A. A. (2021). The impact of climate change on the cost of bank loans. J. Corp. Finance 69, 102019. doi:10.1016/j.jcorpfin.2021.102019

John, K., Litov, L., and Yeung, B. (2008). Corporate governance and risk-taking. J. Finance 63 (4), 1679–1728. doi:10.1111/j.1540-6261.2008.01372.X

Kanagaretnam, K., Lobo, G., and Zhang, L. (2022). Relationship between climate risk and physical and organizational capital. Manag. Int. Rev. 62, 245–283. doi:10.1007/s11575-022-00467-0

Kusnadi, Y. (2011). Do corporate governance mechanisms matter for cash holdings and firm value? Pacific-Basin Finance J. 19 (5), 554–570. doi:10.1016/j.pacfin.2011.04.002

Lei, X. T., Xu, Q. Y., and Jin, C. Z. (2022). Nature of property right and the motives for holding cash: Empirical evidence from Chinese listed companies. Manag. Decis. Econ. 43 (5), 1482–1500. doi:10.1002/mde.3469

Li, J., and Tang, Y. I. (2010). CEO hubris and firm risk taking in China: The moderating role of managerial discretion. Acad. Manag. J. 53 (1), 45–68. doi:10.5465/amj.2010.48036912

Lin, C., Schmid, T., and Weisbach, M. S. (2021). Product price risk and liquidity management: Evidence from the electricity industry. Manag. Sci. 67 (4), 2519–2540. doi:10.1287/mnsc.2020.3579

Liu, H., Jiang, J., Xue, R., Meng, X., and Hu, S. (2022). Corporate environmental governance scheme and investment efficiency over the course of COVID-19. Finance Res. Lett. 47, 102726. doi:10.1016/j.frl.2022.102726

Liu, Q., Pan, X., and Tian, G. G. (2018). To what extent did the economic stimulus package influence bank lending and corporate investment decisions? Evidence from China. J. Bank. Finance 86, 177–193. doi:10.1016/j.jbankfin.2016.04.022

McLean, R. D. (2011). Share issuance and cash savings. J. Financial Econ. 99 (3), 693–715. doi:10.1016/j.jfineco.2010.10.006

Meyer, A., Bresson, H., Gorodetskaya, I. V., Harris, R. M., and Perkins-Kirkpatrick, S. E. (2022). Extreme climate and weather events in a warmer world. Front. Young Minds 10, 1–10. doi:10.3389/frym.2022.682759

Nguyen, J. H., and Phan, H. V. (2020). Carbon risk and corporate capital structure. J. Corp. Finance 64, 101713. doi:10.1016/j.jcorpfin.2020.101713

Nguyen, T. L. H., Nguyen, L. N. T., and Le, T. P. V. (2016). Firm value, corporate cash holdings and financial constraint: A study from a developing market. Aust. Econ. Pap. 55 (4), 368–385. doi:10.1111/1467-8454.12082

Opler, T., Pinkowitz, L., Stulz, R., and Williamson, R. (1999). The determinants and implications of corporate cash holdings. J. Financial Econ. 52 (1), 3–46. doi:10.1016/S0304-405X(99)00003-3

Ozkan, A., and Ozkan, N. (2004). Corporate cash holdings: An empirical investigation of UK companies. J. Bank. Finance 28 (9), 2103–2134. doi:10.1016/j.jbankfin.2003.08.003

Pinkowitz, L., Stulz, R. M., and Williamson, R. (2013). Is there a US high cash holdings puzzle after the financial crisis? Georgetown: Fisher College of Business. (2013-03), 07. doi:10.2139/ssrn.2253943

Pinkse, J., and Gasbarro, F. (2019). Managing physical impacts of climate change: An attentional perspective on corporate adaptation. Bus. Soc. 58 (2), 333–368. doi:10.1177/0007650316648688

Ren, X., Cheng, C., Wang, Z., and Yan, C. (2021). Spillover and dynamic effects of energy transition and economic growth on carbon dioxide emissions for the European union: A dynamic spatial panel model. Sustain. Dev. 29 (1), 228–242. doi:10.1002/sd.2144

Ren, X., Li, Y., Shahbaz, M., Dong, K., and Lu, Z. (2022). Climate risk and corporate environmental performance: Empirical evidence from China. Sustain. Prod. Consum. 30, 467–477. doi:10.1016/j.spc.2021.12.023

Rostamkalaei, A., and Freel, M. (2016). The cost of growth: Small firms and the pricing of bank loans. Small Bus. Econ. 46 (2), 255–272. doi:10.1007/s11187-015-9681-x

Salas, V., and Saurina, J. (2002). Credit risk in two institutional periods: Spanish commercial and savings banks. Journal of. Financial Serv. Res. 22 (3), 203–224. doi:10.1023/A:1019781109676

Seo, D. W., and Han, S. H. (2022). Corruption and corporate cash holdings. Emerg. Mark. Finance Trade 58 (5), 1441–1515. doi:10.1080/1540496x.2021.1890022

Su, X., Zhou, S., Xue, R., and Tian, J. (2020). Does economic policy emeritus raise corporate precursory cash holdings? Evidence from China. Account. Finance 60 (5), 4567–4592. doi:10.1111/acfi.12674

Sun, Z., and Wang, Y. (2015). Corporate precautionary savings: Evidence from the recent financial crisis. Q. Rev. Econ. Finance 56, 175–186. doi:10.1016/j.qref.2014.09.006

Tian, J., Cao, W., Cheng, Q., Huang, Y., and Hu, S. (2022a). Corporate matching culture and environmental investment. Front. Psychol. 12, 6709. doi:10.3389/fpsyg.2021.774173

Tian, J., Yu, L., Xue, R., Zhuang, S., and Shan, Y. (2022b). Global low-carbon energy transition in the post-COVID-19 era. Appl. Energy 307, 118205. doi:10.1016/j.apenergy.2021.118205

Todaro, N. M., Testa, F., Daddi, T., and Iraldo, F. (2021). The influence of managers' awareness of climate change, perceived climate risk exposure and risk tolerance on the adoption of corporate responses to climate change. Bus. Strategy Environ. 30 (2), 1232–1248. doi:10.1002/bse.2681

Wen, F., Li, C., Sha, H., and Shao, L. (2021). How does economic policy impertinty effect corporate risk-taking? Evidence from China. Finance Res. Lett. 41 (101), 101840. doi:10.1016/j.frl.2020.101840

Wintoki, M. B., Linck, J. S., and Netter, J. M. (2012). Endogeneity and the dynamics of internal corporate governance. J. financial Econ. 105 (3), 581–606. doi:10.1016/j.jfineco.2012.03.005

Xiao, T., Sun, R., and Yuan, C. (2020). The preventive value of corporate cash holdings under the impact of the outbreak of the new crown pneumonia. Bus. Manag. J. 42 (4), 175–191. doi:10.19616/j.cnki.bmj.2020.04.011

Xiong, F., Zheng, Y., An, Z., and Xu, S. (2021). Does internal information quality impact corporate cash holdings? Evidence from China. Acc. Finance 61, 2151–2171. doi:10.1111/acfi.12657

Xu, N., Chen, Q., Xu, Y., and Chan, K. C. (2016). Political uncertainty and cash holdings: Evidence from China. J. Corp. Finance 40, 276–295. doi:10.1016/j.jcorpfin.2016.08.007

Zhai, X. Q., Xue, R., He, B., Yang, D., Pei, X. Y., Li, X., et al. (2022). Dynamic changes and convergence of China's regional green productivity: A dynamic spatial econometric analysis. Adv. Clim. Change Res. 13 (2), 266–278. doi:10.1016/j.accre.2022.01.004

Zhang, C., and Cheng, J. (2022). Environmental regulation and corporate cash holdings: Evidence from China's new environmental protection law. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.835301

Zhang, W., Liu, Y., Zhang, F., and Dou, H. (2022). Green credit policy and corporate stock price crash risk: Evidence from China. Front. Psychol. 13, 891284. doi:10.3389/fpsyg.2022.891284

Zhou, D., Zhou, H., Bai, M., and Qin, Y. (2022a). The COVID-19 outbreak and corporate cash-holding levels: Evidence from China. Front. Psychol. 13, 942210. doi:10.3389/fpsyg.2022.942210

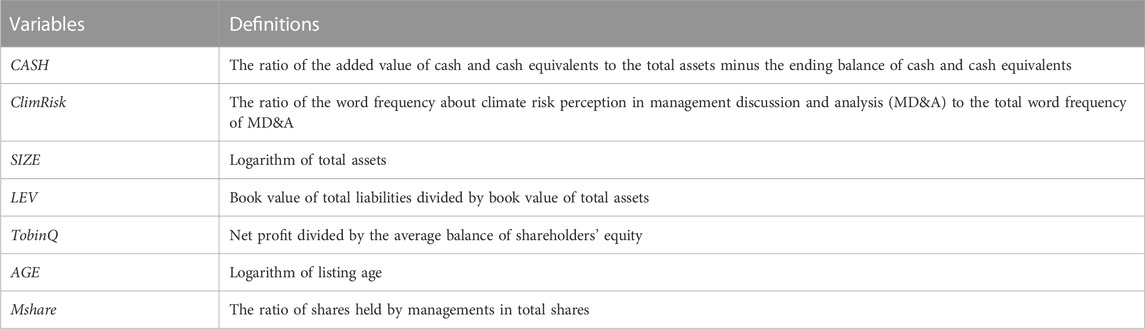

TABLE A1. Variable definitions.

Keywords: climate risk, precautionary cash holdings, text mining, risk taking, external financing, panel regression model

Citation: Zhang W, Yang K and Li Y (2023) Climate risk and precautionary cash holdings: Evidence from Chinese listed companies. Front. Environ. Sci. 11:1045827. doi: 10.3389/fenvs.2023.1045827

Received: 16 September 2022; Accepted: 26 January 2023;

Published: 10 February 2023.

Edited by:

Guojie Wang, Nanjing University of Information Science and Technology, ChinaReviewed by:

Abeeb Olaniran, Centre for Econometrics and Applied Research, NigeriaCopyright © 2023 Zhang, Yang and Li. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Yulei Li, MjY5MzY0MTI2NEBxcS5jb20=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.