Huricha Bao

Huricha Bao Chibo Chen*

Chibo Chen*

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

POLICY AND PRACTICE REVIEWS article

Front. Environ. Sci., 08 November 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.990414

This article is part of the Research TopicEco-Innovation and Green Productivity for Sustainable Production and ConsumptionView all 47 articles

The green innovation (GI) of agriculture-related enterprises has been an important factor to the ecological and sustainable development of agriculture. This research integrates the eight elements of the internally and externally governing mechanisms in the innovative governance system (IGS), adopts the fuzzy-set qualitative comparative analysis (fsQCA) from the configuration perspective, taking the data of A-shares’ listed agricultural companies in Shanghai and Shenzhen stock markets from 2007 to 2019 as samples, and explores the configuration effects of highly green innovations (GIs) from the collaborative matching of various elements of the enterprises’ IGS. The research results showed that 1) a single element of this IGS was unable to become a requisite for agriculture-related enterprises to generate highly GIs, but government subsidies played a more universal role in such a process; 2) the “multiple synergies” of various elements in the enterprises’ IGS formed six different configurations to drive highly GIs, namely, three major models of internal and external supervision with an external incentive, internal supervision with internal and external incentives, and internal and external supervision with internal and external incentives; 3) there were five different paths for the IGS of agriculture-related enterprises to generate non-highly GIs, which were in asymmetry with the configuration paths to generate the highly GIs.

The establishment of ecological civilization has always been one of the most significant factors to the sustainable and healthy development of human society, and both academic and practical circles attach great importance to it. Enterprises are not only the users and takers of natural resources but also the key factor to coordinating economic, social, and ecological issues. In ecological governance, enterprises should assume a major role, and their GI has been an effective way to achieve the dual goals of economic and ecological benefits (Kong et al., 2016). However, the GI of agriculture-related enterprises not only possesses dual externalities but also faces uncertainties of agricultural production and operation. Its risk has been much higher than that of other industries (Wang et al., 2021a). The GI behaviors of its executives brought higher agency costs, and the economic benefits generated by the GIs of agriculture-related enterprises were often lower than their ecological and social benefits. This will dampen the enthusiasm of enterprises and withdraw their momentum for more GIs. Therefore, the synergy of internal and external governance mechanisms is needed to guide agriculture-related enterprises to actively carry out GIs.

Scholars have carried out significant research on the influences of GIs on enterprises and obtained fruitful results, but the conclusions were not always consistent and sometimes contrary to each other. As the most effective external governance mechanisms, environmental regulation and government subsidy policy have a significant effect on enterprises’ GIs. Research studies by scholars also showed that the subsidy policy would promote the GIs of enterprises, make up for the increased costs, and compensate for the short-term economic losses of producers (Wang et al., 2014). In contrast, it was believed that the subsidy policy would bring the crowding-out effect because sufficient government subsidies could replace a part of enterprises’ internal funds for research and development (R&D) (Herrer and Montmartin, 2015; Yu et al., 2016). Government subsidies or tax returns were deemed to mainly play an incentive role, while environmental regulation, as a mandatory regulatory policy, was considered to exert a more supervisory effect. The “Porter hypothesis” holds that appropriate environmental regulation could encourage enterprises to implement technological innovations and transformations. In contrast, it was believed that environmental regulation increased the cost of enterprises’ environmental governance, which would crowd out investments in technological innovations and product R&D and then impose a negative impact on the market competitiveness and performance of enterprises (Jaffe and Palmer, 1997; Kneller and Manderson, 2012). Effective implementation of external policies was directly related to the internal governance mechanism of enterprises. GIs require plenty of capital investments, policy support, and effective allocation of capital. As the carrier of the internal incentive and supervision mechanisms of enterprise innovations, internal governance played an important role in the process of GIs (Cheng et al., 2019), which would effectively reduce the agency behaviors of executives, promote their motivation for GIs, and improve the enterprise efficiency of resource allocation in a timely manner. Existing literature research studies demonstrated that increasing the cash incentives of executives would reduce their agency behaviors and lower their risk aversions (Benjamin et al., 2017). Increasing the proportion of independent directors would increase the transparency of enterprises and effectively control the major shareholders or internal staff, which might facilitate the improvement of the quality of innovative decision-making (Xu and Xu et al., 2021).

In general, the aforementioned research studies mainly evaluated and validated the influences of single governance systems and their mutual interactions on GIs, but the internal and external governance mechanisms exist in integration than in solitary, while there is a synergistic matching effect among their elements. Only the matching of diverse external policies and proper internal governance mechanisms can achieve encouraging enterprise innovation behaviors (Reichert et al., 2016). Future research should evaluate and validate the effectiveness of the IGS coordinately developed by internal and external governance elements.

Agricultural green innovation is the core of sustainable and high-quality development of the entire agriculture industry. Agricultural enterprises have not only been the most dynamic and vital subject, leading the activities of agricultural green innovation, but also a pivotal force in the industrialization of agricultural achievements from science and technologies (Hong and Li, 2020). However, research and development innovation activities are characterized by long cycles, high risks, and irreversibility, while enterprises have to bear the high governance costs when conducting these innovation activities (Wan et al., 2020). The production and operation activities of agricultural enterprises have already been influenced by uncontrollable factors such as biological growth cycle, natural environment, and epidemic situation; consequently, the technological innovation process and innovation result implementation cycle have become longer and riskier (Li and Li, 2015). In particular, green innovations of agricultural enterprises demand high-quality land; sufficient oxygen, moisture, and other natural environments; and abundant support of human and material resources. Unlike agricultural technology innovation or industrial enterprises’ green innovation, agricultural green technology innovation poses the dual characteristics of commonness of agricultural technology innovation and non-exclusivity of green technology innovation benefiting, which reflected its unique attribute of public goods (Chu, 2022). This feature enables the social and environmental benefits of agricultural green technology innovation to go far beyond its economic benefits. Enterprises and individuals seeking to maximize economic benefits are not willing to conduct agricultural green innovation. As a consequence, it becomes necessary to build supervision and incentive mechanisms for affecting the elements of agricultural green technology innovation to achieve the innovation objectives and eventually promote the green innovation behaviors of agricultural enterprises. It can be observed that establishing an effective system of innovation governance is quite significant to the green innovation of agricultural enterprises, but at present, few scholars have paid attention to the possible influence of an innovation governance system on the green innovations of agricultural enterprises.

This study integrates the eight elements of internal and external supervision and incentives of the IGS, takes the data of agricultural companies listed in Shanghai and Shenzhen stock markets from 2007 to 2019 as the research sample, and uses the method of fuzzy-set qualitative comparative analysis (fsQCA) to explore the synergistic matching of various elements of the IGS and the complex causality mechanism of GIs of agriculture-related enterprises. From the perspective of configuration, this method analyzes the different paths of highly GIs of agriculture-related enterprises generated by the synergistic matching of various elements of the governance system, like “all roads lead to Rome.” This study tries to answer the following questions: does a single element of the IGS constitute a necessary condition for highly GIs of agriculture-related enterprises? Which configurations of governance elements can generate highly GIs for agriculture-related enterprises? Also, which configurations of governance elements can generate non-highly GIs for agriculture-related enterprises?

Enterprise innovation brings high-quality resources to enterprises and is also an effective way to establish market competitiveness. It should become a natural selection process for enterprises, but in reality, not all companies actively implement innovations (Cheng et al., 2019). There are dual externalities in enterprises’ GI, which requires regulatory and subsidy policies to internalize the cost of enterprise environmental governance. As a mandatory environment from the external institution, environmental regulation will affect the investment scale and efficiency of enterprise GIs. The social costs from environmental pollution are higher than the benefits from GI, resulting in negative externalities. The government needs to implement mandatory constraints and market guidance to reduce the emission of pollutants from enterprises, thus stimulating enterprises’ technological transformation and GI. The “Porter hypothesis” holds that appropriate environmental regulation could encourage enterprises to carry out technological innovation and transformation so that enterprises’ core competitiveness and business performance are improved. Agriculture has been an industry with low-tech innovations (Pang and Liu, 2021), and agriculture-related enterprises rely more on resources, environments, and simple processing of regional agriculture-related products. Under increasingly strict environmental regulations, these enterprises now have to improve technology for green transformation. Moreover, the government mainly restricts pollution behaviors through mandatory requirements of directive environmental regulations and market supervision by pollution charging to stimulate the motivation for GIs.

From a macroscopic perspective, due to the positive externality of GI, innovative enterprises need to invest plenty of money and time, but they cannot monopolize their innovation results. The GIs of agriculture-related enterprises have long cycles, high risks, and low economic profits, which cause strong uncertainty in their investment returns. The contradiction between the weaknesses of agriculture and the profit-seeking nature of capital has severely restricted the financing of agriculture-related enterprises (Czarnitzki and Hussinger, 2004), leading to lack of GI momentum of listed agricultural companies. Other research studies showed that the government subsidy policy would promote the GI of enterprises, compensate for the increased costs, and make up for the short-term economic losses of innovators (Dong et al., 2021). First, government subsidies could solve the short-term financing problems of innovative enterprises, make up for the unexpected losses from early innovation failures, and reduce the uncertainty caused by financial problems to a certain extent (Czarnitzki and Hussinger, 2004). Second, later-stage compensations such as tax returns could offset the costs brought by the spillover of knowledge and technology to a certain degree, increase the efficiency of enterprise innovations’ compensation, and increase the enthusiasm of enterprise innovation (Cheng et al., 2019) so that the GI of enterprises is improved. The public production attribute of the agricultural industry causes its economic profits to be far below its social benefits, and the positive externality of GIs is more obvious, which makes the subsidy policy an important factor in the green and high-quality development of agricultural enterprises.

According to the agent theory, the agent problems hidden within enterprise innovative activities will restrict innovation efficiency. As the agents of entrepreneurs, executives are also the controllers and executors of enterprises’ GI strategies. Reasonable supervision and incentives to executives have been conducive to reducing agent costs and improving innovation efficiency (Xie et al., 2018). To pursue short-term interests, enterprise executives would often give up some long-term investments, especially when making highly risky investment decisions such as GIs. Thus, how to reduce the agent behaviors of executives and improve the enterprises’ enthusiasm for GI has been an important issue of internal governance. Improving the cash incentives to executives would reduce their agent behaviors and risk aversions (Xi and De, 2020), which is the most effective incentive in the short term. Moreover, equity incentives will enable them to tolerate short-term innovation failures and offer long-term returns, making executives consider more about the long-term development of the enterprise. However, due to binding the executive performance with equity, they would be affected by short-term market pressures and worries about the shrinkage of short-term wealth, before choosing investment projects with high economic returns to crowd out GI ones (Yu et al., 2020). Therefore, both internal and external supervision mechanisms must be adopted to restrict executives’ short-sighted behaviors.

Internal supervision is not only the core factor of internal governance but also an important element in the IGS. Research studies exhibited that governance mechanisms such as improving the proportion of independent directors and keeping the share balances could enhance the enterprise’s transparency and effectively implement internal control over major shareholders, which is conducive to improving the quality and efficiency of executives’ innovative decision-making (Xu and Xu, 2021). From the perspective of board governance, independent directors have no critical business connection with executives and can make decisions independently; therefore, they are expected to make more objective suggestions on the long-term development and environmental issues of the company, supervise the short-sighted behaviors of senior executives, and reduce the agent costs (Cheng et al., 2019). From the perspective of equity governance, the share balance divides the control among shareholders to supervise and restrict each other, alleviate their selfish behaviors, and reduce the agent cost between shareholders and executives to a certain extent (Yu et al., 2020). This could also restrict the short-sighted behaviors of executives so that the GI behaviors of enterprises are improved. Although the enterprise’s GIs endure high risk and a long return period, they remain the key factor to maintaining the enterprise’s core competitiveness and green sustainable development in the new era. As a result, for the sake of long-term interests, major shareholders and independent directors will become more inclined to improve the enterprise’s GI.

The governance of enterprise innovation is an integrated system composed of both internal and external governance systems (Cheng et al., 2019). The studies on the “net effects” of different internal and external governance systems on the GI of agriculture-related enterprises provided a basis for understanding the relationship between these IGSs and GIs. However, in such studies, the linear relationships between different government policies with different internal governance systems and GIs of agriculture-related enterprises were uncertain, and it was difficult to explain the configuration effects of more than three factors. It was impossible to clarify the necessary and sufficient causalities because the process of enterprise GI has been a loosely connected entity, relying on the values of “connection” and “aggregation” and the logic of re-creation (Wang et al., 2021b). Different internal and external governance systems are interdependent, interactive, and connected entities; hence, the single internal supervision and incentives cannot generate high GIs. There are complex causality relationships between multiple conditional variables of internal and external governance and enterprise GIs.

Scholars have also conducted substantial research on the complex causality among multiple factors with plentiful results, which laid a solid foundation for this study. Meyer et al. (1993) proposed that the environment, industry, technology, culture, belief, community, members, and other elements with results could be aggregated into distinct configurations at different dimensions. Ragin (2007) also believed in the existence of numerous reasons for various social phenomena, which were interdependent rather than independent of each other; therefore, the interpretation of these social phenomena requires the analysis ideology to rely on the abovementioned configurations. This ideology has also been widely applied in the display analysis of economic management, but the contingency theory remains preferred by traditional academic research, mainly to analyze the causal relationship between the two or the cross-relationship among the three, when controlling other conditions. This is primarily because of the mismatch between the research theories and methods. With the introduction of set theory and the QCA method, the dilemma of scholars in analyzing problems from the perspective of configurations was eventually resolved (Fiss, 2007). In recent years, numerous scholars have adopted the method of QCA to analyze the practical problems of economic management. For example, the study by Huang et al. (2021) has revealed that the performance by overseas subsidiaries of Chinese manufacturing enterprises was the result of the achievement of multiple factors. The research of Li et al. (2022) has demonstrated that the process of enterprise business model innovation is the output of multiple internal and external factors. Nonetheless, the existing literature on QCA lacks comprehensive consideration of the internal and external factors of the enterprises’ innovative governance systems.

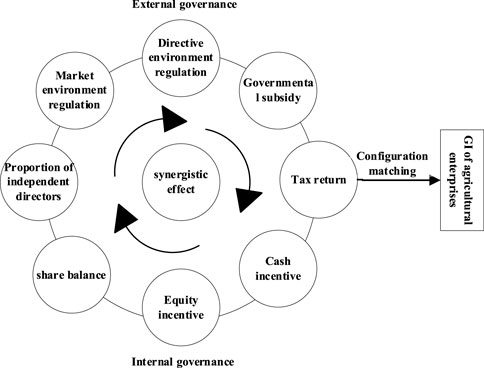

The relationships of symbiosis and competition among the elements of the enterprise IGS can only depend on the synergistic matchings between these elements to achieve effective governance, such as the matchings between the configuration effects of supervision and incentives, the configuration effects of long-term incentives and short-term incentives, and external policy and internal governance. Moreover, the green innovation process of agriculture-related enterprises is deemed to be a complex procedure that needs to integrate the natural, environmental, technological, and economic resources, while coordinating multiple stakeholders, including the government, farmers, related enterprises, and employees (Chu, 2022). These green innovations of enterprises demand the synergy between the combination policies of different departments and sophisticated internal governance (Cheng, 2019; Wang and Li, 2021). From the perspective of configuration, the organization is best understood as an interrelated structure rather than a unitized or loosely combined entity (Du and Jia, 2017), which is the same as the perspective of the enterprise IGS. Therefore, the configuration perspective is very suitable for analyzing the non-linearity, equivalence, and complexity of the enterprise IGS to the GI of agriculture-related enterprises. On one hand, the enterprise IGS restricts the agent behaviors of executives but encourages GI behaviors to improve the innovation enthusiasm of decision-makers. On the other hand, it optimizes the external policy and market environment to improve the efficiency of compensating the GI. To sum up, it remains an open question about how the elements of the IGS interact with each other to influence the GI of enterprises. Based on the configuration perspective, this study explores the complex causality mechanisms of the IGS affecting the GI of agriculture-related enterprises. The theoretical model is shown in Figure 1.

FIGURE 1. Research framework.

According to the aforementioned theoretical analyses, it was found that the GI of agriculture-related enterprises had a spillover effect, while the spillovers of technology and knowledge would reduce the enthusiasm of innovative enterprises. Therefore, it proved to be far from enough for the highly GI of agriculture-related enterprises to merely study the influences of the pairwise interactions between internal factors and external policies. It was necessary to explore the effects of the IGS with the multidimensional synergy of internal governance and external policies on the GI of agriculture-related enterprises.

The method of fuzzy-set qualitative comparative analysis (fsQCA) based on the set theory proposed by Ragin C C can well-solve the complexity of causality and identify different equivalent paths leading to the same result for evaluating the multiple synergistic causalities (Ragin, 1987). This method has been widely used in academia since Ragin proposed the QCA method. In the early days, scholars mainly used the QCA method in cross-case studies of small samples of complex problems in social sciences such as sociology and political science (Ragin, 1987; Ragin, 2007). In recent years, the QCA method has been widely used in the processing of large samples in management and the configuration analysis of complex problems (Du and Jia, 2017) and has become an important tool to solve the complexity of causality in management, marketing, and management information systems (Fiss, 2007; Fiss, 2011; Misangyi et al., 2017; Du and Ma, 2022). There are three reasons for choosing the fsQCA approach: first, the realization of highly GI of agriculture-related enterprises depends more on the joint supervision and incentive of external and internal governance. The fsQCA method can analyze the nonlinear relationship between different combinations of IGS elements and GI from the perspective of entirety and configuration. Second, this method can explore the different configuration paths of the IGS elements to realize the highly GI of listed agricultural companies, facilitating a better understanding of the multiple equivalent paths to realize the highly GI of agriculture-related enterprises. Third, the fsQCA method can also compare the asymmetric configuration path between highly and non-highly GIs generated by multiple synergy conditions.

This study took the GI of listed agricultural companies as the research object with a specific data source: the GI data of agriculture-related enterprises were retrieved by first querying the corresponding International Patent Clsassification (IPC) from the website of China’s State Intellectual Property Office based on all the innovation data of listed companies in the Guotai’an database. Then, these IPCs were compared with those published by the World Intellectual Property Organization (WIPO)1. Finally, according to the “Industry Classification Guide for Listed Companies” revised by the China Securities Regulatory Commission in 2012, this study selected the enterprises of agriculture, forestry, animal husbandry, fishery, and related agricultural product manufacturing2. The government’s work reports could be downloaded from the websites of Chinese provincial governments. The data for the pollutant discharge fee were obtained from the “China Environmental Statistics Yearbook,” in which the environmental protection tax was levied after 2018 without publishing the pollutant discharge fee any longer. In this article, the market-oriented environmental regulation in 2018 and 2019 was replaced by the environmental protection tax amount obtained from the “China Tax Statistics Yearbook.” Other data related to corporate governance and government subsidies were from the Guotai’an database.

Outcome variable: The GI of agriculture-related enterprises was measured by the number of green patent applications of listed agriculture-related companies, which could more accurately measure the output level of enterprise innovation activities (Li and Zheng, 2016), rather than the input in advance. Furthermore, the International Patent Clsassification (IPC) published by the State Intellectual Property Office could also clearly distinguish the technical characteristics of enterprise innovation activities: GI or non-GI.

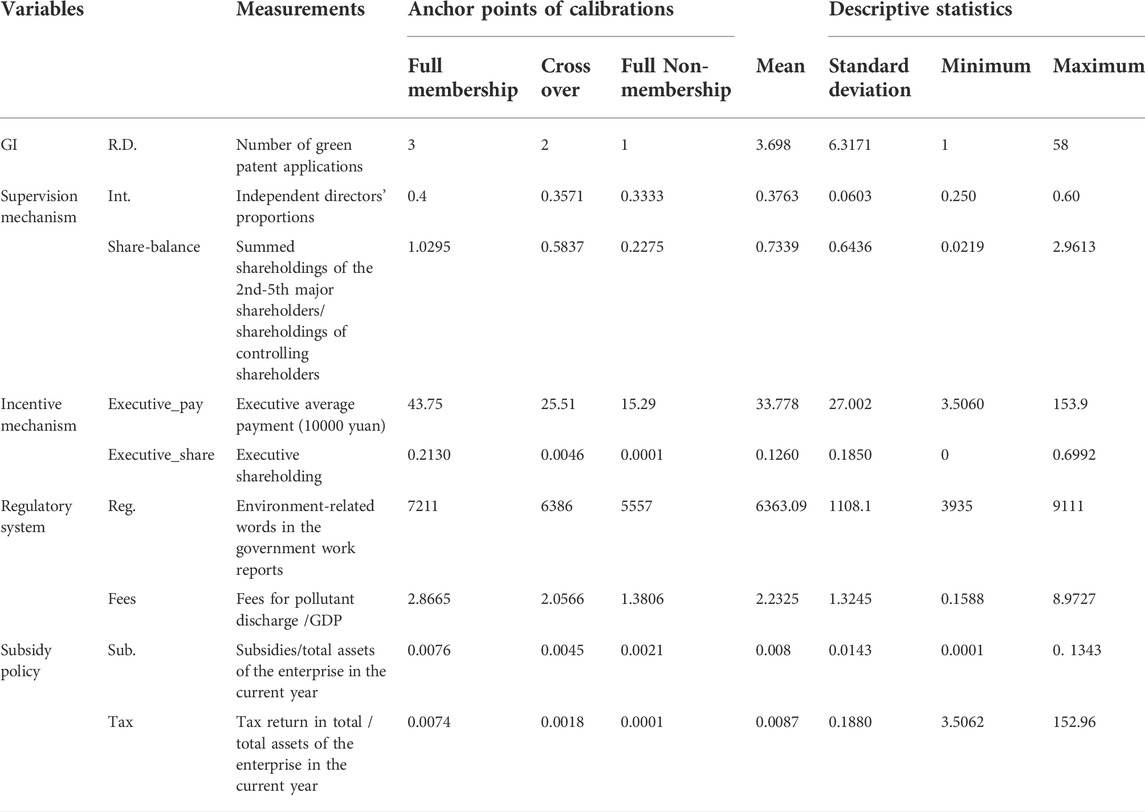

Conditional variables: We refer to the research studies of Benjamin et al. (2017) and Cheng et al. (2019) for selecting eight elements from four aspects of internal supervision, internal incentive, environmental regulation, and government subsidy, specifically including environmental regulation policy: directive environmental regulations and market-oriented environmental regulations; government subsidy policy: government subsidies and tax breaks; internal supervision: the proportion of independent directors and the degree of share balance; internal incentive: executive compensation incentive and executive equity incentive. Detailed measurements and descriptive statistics are listed in Table 1.

TABLE 1. Calibration values and descriptive statistics.

QCA data are usually numerical, and each type has its own specific format. All conditions in fsQCA must be calibrated as continuous values between 0 and 1. This study followed the mainstream research of QCA at home and abroad to use the direct method (the way of objective quantile value) to calibrate each variable as a fuzzy set. Referring to the research of Fiss (2011) and Greckhamer (2016), according to the characteristics of the sample data in this article, it can be observed from the descriptive statistics that there is a significant difference between the maximum value and the minimum value of the sample data, with the average value being closer to the minimum value. If 95%, 50%, and 5% are selected as the anchor points, it will be too extreme and affect the accuracy of the research results. Therefore, the 75%, 50%, and 25% quantiles of descriptive statistics of outcome variables and conditional variables were used as three qualitative anchor points of full membership, crossover, and full non-membership, respectively, This anchor is also widely used and recognized by scholars in economics and management (Fiss, 2011; Greckhamer, 2016; Du and Jia, 2017; Du and Ma, 2022). See Table 1 for details.

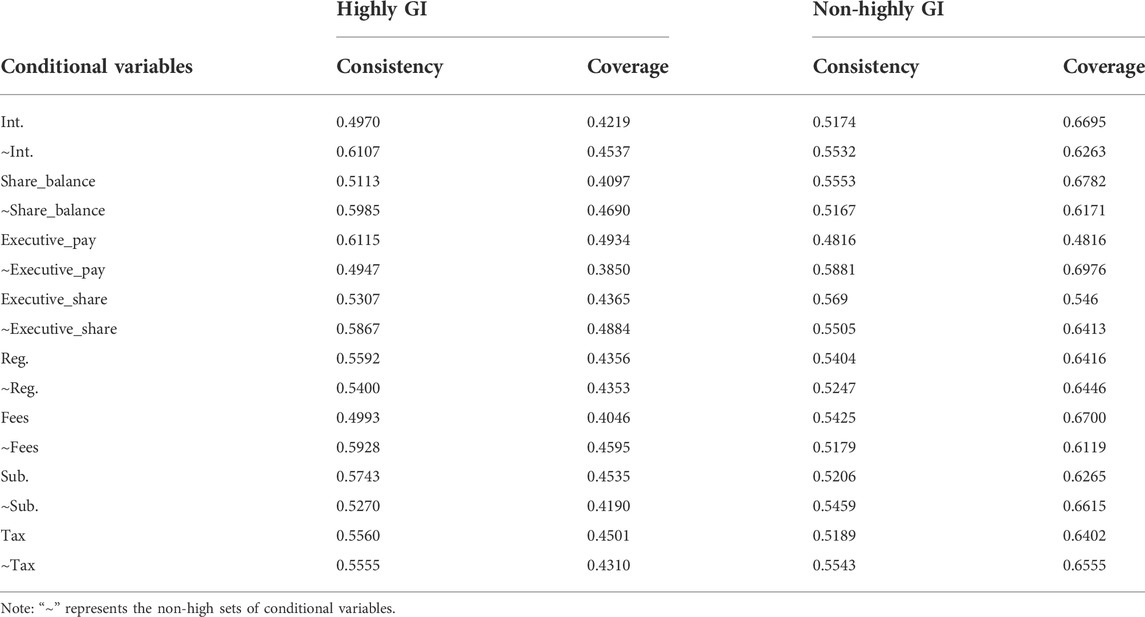

According to the existing QCA research practices, this study adopted the fsQCA software to test the requisites of all conditional variables and non-sets. Whether the elements of the IGS can constitute the requisites for highly GIs and non-highly GIs of agriculture-related enterprises is illustrated in Table 2. The consistencies of single variables were all below 0.7; thus, single conditions could not constitute the requisites for outcome variables (Du and Jia, 2017). The realization of highly GI of agriculture-related enterprises was proven to be a configuration system of synergy among the elements of the IGS, not driven by the single elements or the interactions between every two.

TABLE 2. Necessity test of single conditions.

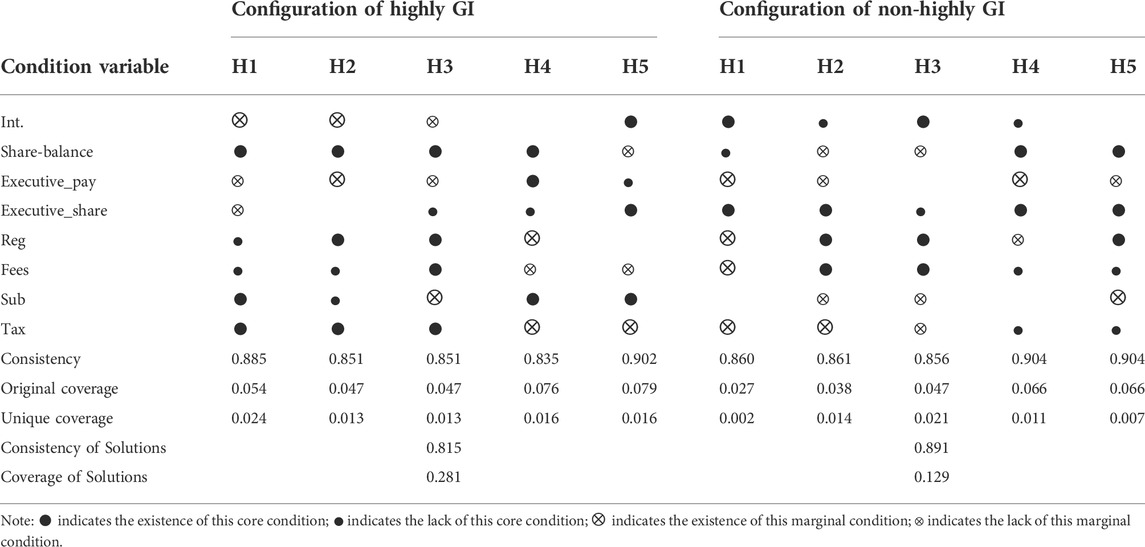

Referring to the research of Du and Jia (2017), considering that the sample cases and data feature frequency threshold and consistency threshold of this study were selected as 2 and 0.85, respectively, the results calculated by fsQCA software are listed in Table 3. This study distinguished the core condition or edge condition by comparing their simple solutions and the intermediate solutions (Fiss, 2011; Du and Jia, 2017). It could be observed from Table 3 that the overall consistency level of the intermediate solution was beyond 0.8 and the coverage was 0.258. According to the coverage index, each configuration had a substantive explanation for the GI of agriculture-related enterprises, while the six configurations jointly explained the coordination mechanism of internal and external governance of agriculture-related enterprises’ GIs. In five of the six configurations, government subsidy existed as the core condition, while the proportion of independent directors did not exist in three configurations, indicating that the highly GI of agriculture-related enterprises depended on the configuration system with synergistic effects of environmental regulation + internal supervision + government subsidies, government subsidies + internal incentive and internal supervision, and internal supervision + dual incentives of governments and enterprises. This study also analyzed the non-highly GIs' configuration system of agriculture-related enterprises and obtained five different configuration paths, as listed in Table 3. Each configuration is described in detail as follows.

(1) Configuration H1: a model of environmental regulation + government subsidy + share balance, in which sufficient government subsidies, insufficient environmental regulation or tax return, and the lack of share balance as the core condition would still generate highly GI of agriculture-related enterprises. In this configuration, whether there was an equity incentive had little effect on the GI of agriculture-related enterprises, while the marginal conditions of independent directors and executives’ cash incentives exist and lack. The possible reasons are that for listed agricultural companies, their competitiveness and scale have not been dominant at present. There are many financing constraints (Wang et al., 2021a), and more government subsidies are needed to offset short-term financial problems and generate a longer-term driving force for GI. Moreover, the regulatory effect of environmental regulation policy on agriculture-related enterprises has been insufficient. It is necessary to increase the regulatory intensity to improve the GI awareness of agriculture-related enterprises, simultaneously increase the shareholding ratios of minority shareholders, and strengthen the supervision over controlling shareholders. Configuration H1 is a typical traditional model of applying government support to promote GI.

(2) Configuration H2: a model of government subsidy + independent director supervision similar to H1, in which the synergistic effect of adequate government subsidies and strict supervision by independent directors would also generate highly GI of agriculture-related enterprises. Under this model, internal incentives, share balances, and tax returns all existed as marginal conditions. The possible reason was that government subsidies could compensate for the short-term costs of GI, but whether government subsidies were applied in GI required strict supervision by independent directors to improve the resource allocation efficiency of executives, with constraints of environmental regulation policy to guide the investment direction of agriculture-related enterprises. H2 belonged to the configuration path of highly GI generated by the synergistic effect of both internal and external supervision with sufficient government support.

(3) Configuration H3: a model of government regulation + share balance + tax return incentive, which was mainly a highly GI configuration formed by the synergy of strict internal and external supervision with internal and external long-term incentives. As long as the core conditions such as the directive-based and market-based environmental regulations and the share balances existed, irrespective of the presence of government subsidies or not, the long-term encouragement from executives’ equity incentives and tax returns would still generate highly GI of agriculture-related enterprises. The possible reason was that strict environmental regulation would increase the environmental awareness of decision-makers and bring an innovation compensation effect in the long run. Moreover, the supervision of market-based environmental regulation would improve the market reputation of enterprises, and the equity incentive would increase the ownership awareness of executives to pay more attention to the long-term development of the company, which would improve its GI. Under strict environmental regulation, only GI could bring market competitiveness to agriculture-related enterprises, but the existence of externalities and natural risks to agricultural enterprises required long-term and continuous incentives for executives to actively improve their GI enthusiasm.

(4) Configuration H4: a model of government subsidy + share balance + cash incentive, regardless of the supervision by independent directors, with environmental regulation policies as the marginal condition. As long as the lacked existence of sufficient government subsidies, executive payment incentives, share balances, and tax returns as core conditions could still generate highly GI of agricultural enterprises. This might be attributed to the following reasons: compared with other enterprises, agriculture-related enterprises suffered high operation risk and difficult financing; hence, sufficient financial support would effectively improve the innovation efficiency. Meanwhile, cash incentives would be given to executives for reducing the agent costs and increasing the efficiency of resource allocations, which would improve the GI enthusiasm of executives. This configuration belonged to a typical highly GI governance configuration generated by the synergistic effect of the internal and external short-term incentives and the supervision by minority shareholders.

(5) Configuration H5: a model of share balances + government and enterprise incentives. Whether there were independent director supervision and even directive-based and market-oriented government regulations have already been marginal conditions in this model, the existence of the supervision by minority shareholders as the core condition under sufficient government subsidies and enterprise incentives would still also generate highly GI of agriculture-related enterprises. The possible reason was that the operation risk of agriculture-related enterprises was relatively high and executives had more agent behaviors, but the strong internal and external support and encouragement could well-alleviate the negative feelings of executives, reduce their agent behaviors, and solve the financing problems. Furthermore, the internal supervision by minority shareholders over controlling shareholders would also promote the GI of enterprises. This configuration belonged to an IGS of synergy among government subsidies, long-term and short-term dual incentives for executives within the enterprise, and supervision by minority shareholders.

(6) Configuration H6: a model of internal dual supervision + share incentive + government subsidy. Whether it had command-based environmental regulation or not, when the existence of market-based environmental regulation and tax returns were both lacked as marginal conditions, as long as there was the existence of core conditions such as strict internal supervision, equity incentive, and government subsidy, the highly GI of agriculture-related enterprises will still be generated. The possible reason for this was that the current internal governance of China’s agriculture-related enterprises was imperfect. Hence, strict internal supervision would have obvious constraints on senior executives, and with the synergistic matching of government subsidies and long-term incentives, highly GI effects could be generated. This configuration belonged to the innovative governance configuration of synergy between strict internal supervision and internal and external dual incentives.

TABLE 3. Configuration analysis of GI of agriculture-related enterprises.

To sum up, the governance process of promoting GIs of agriculture-related enterprises has been a configuration system with the synergistic effect of internal and external supervision and internal and external incentives. It was neither generated by the supervision or incentive of a single party nor formed by the interactions between every two of them but by the entirety of the joint actions by the government, the market, and the enterprises themselves. Also, this configuration system was not symmetrical to that of non-highly GI, which was also analyzed in this study.

From Table 3, it could be observed that the existence of government subsidies had little effect on non-highly GI. Configuration H1 showed that only strengthening internal supervision and incentive without environmental regulation or government financial support was one of the main reasons for generating non-highly GI in agricultural enterprises; configuration H2 proved that only strict government policy regulation and internal incentives without internal supervision or government financial support would also generate non-highly GI of agriculture-related enterprises; configuration H3 indicated that strict internal and external supervision and internal incentives without government financial support would again generate non-highly GI of agriculture-related enterprises; configuration H4 revealed that the lacked existence of strict internal supervision, equity incentives, market-oriented environmental regulation, and tax returns also led to the non-highly GI of agriculture-related enterprises; configuration H5 demonstrated that the existence of core conditions such as strict directive-based environmental regulation, share balances, and tax returns, with the lack of core conditions such as equity incentives and market-oriented environmental regulation, would also generate non-highly GI of agriculture-related enterprises.

Moreover, it could be observed from Table 3 that government subsidies existed as a core condition in five of the six configurations of highly GI but as a marginal condition in only two of the five configurations of non-highly GI, which illustrated that government subsidies had a universal and important effect on the highly GIs of Chinese agriculture-related enterprises during their green transformation process. From the perspective of internal supervision, supervision by independent directors existed as a core condition in only two configurations of highly GI and in three configurations of non-highly GI, which indicated that the supervision role of independent directors of listed agricultural companies in GI decision-making had not been significant, as they might have colluded with other directors and senior executives to serve their personal interests.

Based on the research studies of Fiss (2011) and Du and Jia (2017), this study selected the frequency threshold and consistency threshold as 3 and 0.85, respectively, and tested the robustness of the configuration analysis on the GI of agricultural enterprises. Test results are shown in Table 4, It was found that the configurations of the new and the original models were basically consistent with each other, and there was a clear subset relationship between them, indicating that this research conclusion was relatively robust.

TABLE 4. Robustness test results.

This study analyzed the complex causality path of GI driven by various elements of enterprise IGS. First, a single governance element does not constitute a necessary condition for the highly GI of agriculture-related enterprises, which deepened the discovery of the positive role of environmental regulations, government subsidies, internal supervision, and internal incentives in promoting the GI of agriculture-related enterprises. Meanwhile, government subsidies played a more universal role and would influence the effects of other governance elements, which verified the compensation effect of government subsidies on the GI of Chinese agricultural enterprises at the current stage. Second, there were six and five types of internal and external synergy governance configurations that generated highly GI and non-highly GI of agriculture-related enterprises, respectively. This study not only revealed that the constraints of regulatory policies and government subsidies were complementary to each other, such as H1 and H2, but also included both the strict environmental regulations and high government subsidies, which promoted the compensation effect on GI, reduced the externalities, and complemented other governance factors to generate highly GI. It was also disclosed that environmental regulation policy and internal supervision exerted the substitution effects, such as H1 and H6, which both included the matching of high-level environmental regulation policy or high-level internal supervision with internal and external incentive mechanisms, which would generate highly GI and reduce externality and agent behavior. Finally, this study integrated different internal and external governance mechanisms, analyzed the complex matching relationship between various elements of the IGS, and improved the understanding of the synergies between the IGSs. From an overall perspective, this study discussed the influences of the synergistic configurations of various elements such as environmental regulations, government subsidies, internal supervision, and internal incentives on the GI of agriculture-related enterprises. It further proved that the internal and external governance mechanism of enterprises was an interdependent and synergistic entirety, and a single mechanism was difficult to become a necessary condition for generating highly GI. For agriculture-related enterprises, applying internal governance to increase the efficiency of resource allocation was also an important factor to GI improvement.

The study conclusion of this article puts forward the following three suggestions for improving the IGS of agriculture-related enterprises: first, optimizing the single enterprise governance mechanism is not the premise of improving the GI of agriculture-related enterprises. Their GI governance is a configuration system under the synergy of various elements of internal and external governance mechanisms, which cannot be limited to optimizing these single elements but expanded to the overall perspective of focusing on the synergistic matchings of internal and external governance elements and specifying the “combination” of optimizing the internal and external governance mechanisms. Second, while increasing their GI investments, agriculture-related enterprises could optimize the matching effect of their internal supervision and incentives and improve the efficiency of resource allocation. Agriculture-related enterprises can choose appropriate GI paths and targeted measures according to the development levels and their own innovative abilities and give full play to the incentive effects of the IGS on improving these abilities. Third, local governments should adopt measures to local conditions; formulate improvement policies for innovative governance in line with local agricultural development, environmental governance, and characteristics of agriculture-related enterprises; increase the efficiency of synergistic governance between governments and enterprises; and promote the green and high-quality development of these agriculture-related enterprises.

HB: manuscript writing and statistical analysis. CC significantly contributed in design of study and revise of the manuscript. YL: data collection and verification of submitted manuscripts.

This research was funded by The National Social Science Fund of China (grant number: 15AJY014).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1Bao Huricha (1988): Doctorate in Agricultural Economics, Zhongnan University of Economics and Law, China (Corresponding author); Email: U1VZRUJBT0BhbGl5dW4uY29t; Telephon:18204856757.

2Chen Chibo (1961): Professor, Doctoral Tutor, Zhongnan University of Economics and Law, China.

3Liu, Yuemin (1998): graduated from Bryant University with a bachelor’s degree and is currently studying for a master’s degree at Zhongnan University of Economics and Law, and her research field is agriculture management.

4Website: https://www.wipo.int/classifications/ipc/en/green_inventor/.

5Note: Including agricultural and sideline foods processing industry; food manufacturing; beverage manufacturing; textile industry; clothing, shoes, and hats manufacturing; leather, fur, feather (duvet), and their products industry; wood processing and bamboo, rattan, palm, and grass product industry; furniture manufacturing; paper-making and paper product industry; rubber product industry.

Benjamin, B., Lee, F., and Gustavo, M. (2017). Independent boards and innovation. J. Financial Econ. 123 (3), 536–557. doi:10.1016/j.jfineco.2016.12.005

Cheng, X., Zheng, H., and Zhao, M. (2019). A review on the mechanism of corporate governance influencing innovation. Nankai Journal (Philosophy, Literature Soc. Sci. Ed). 66 (06), 93–104. CNKI:SUN:LKXB.0.2019-06-010

Chu, D-J. (2022). Innovation mechanism of agricultural green technology based on public goods attributes. J. South China Agric. Univ. Sci. Ed. 21 (01), 23–32. doi:10.7671/j.issn.1672-0202.2022.01.003

Czarnitzki, D., and Hussinger, K. (2004). The link between R&D subsidies, R&D spending and technological performance. Soc. Sci. Electronic Publish, Discussion Paper No. 4–56. doi:10.2139/ssrn.575362

Dong, J., Zhang, W., and Chen, Y. (2021). The impact of environmental regulation tools and government support on green technology innovation. Industrial Econ. Res. 20 (03), 1–16. doi:10.13269/j.cnki.ier.2021.03.001

Du, Y., and Jia, L. (2017). Configuration perspective and qualitative comparative analysis (QCA): A new way of management research. Management World 33 (06), 155–167. doi:10.19744/j.cnki.11-1235/f.2017.06.012

Du, Y., and Ma, H. (2022). Research on innovation and entrepreneurship in the context of complexity:based on the QCA method. R&D Manag. 34 (03), 1–9. doi:10.13581/j.cnki.rdm.20220341

Fiss, P. C. (2011). Building better causal theories: A fuzzy set approach to typologies in organization research. Acad. Manage. J. 54 (2), 393–420. doi:10.5465/amj.2011.60263120

Fiss, P. C. (2007). A set-theoretic approach to organizational configurations. Acad. Manage. Rev. 32, 1180–1198. doi:10.5465/amr.2007.26586092

Greckhamer, T. (2016). CEO compensation in relation to worker compensation across countries: The configurational impact of country‐level institutions. Strateg. Manag. J. 37 (4), 793–815. doi:10.1002/smj.2370

Herrera, M., and Montmartin, B. (2015). Internal and external effects of R&D subsidies and fiscal incentives: Empirical evidence using spatial dynamic panel models. Res. Policy 44 (5), 1065–1079. doi:10.1016/j.respol.2014.11.013

Hong, T., and Li, B. (2020). Measurement and division of research and development efficiency of listed agricultural enterprises in China—empirical analysis based on SBM-malmquist model and enterprise life cycle. Inq. into Econ. Issues 41 (09), 65–77. CNKI:SUN:JJWS.0.2020-09-007

Huang, J., Yi, C., and Shen, H. (2021). On innovation performance driving mechanism of overseas subsidiaries of China’s multinational enterprises-configuration analysis based on QCA method. J. Huaqiao Univ. (Phil. Soc. Sci.) 39 (04), 77–90. doi:10.16067/j.cnki.35-1049/c.2021.04.007

Jaffe, A. B., and Palmer, K. L. (1997). Environmental regulation and innovation: A panel data study. Rev. Econ. Statistics 79 (4), 610–619. doi:10.1162/003465397557196

Kneller, R., and Manderson, E. (2012). Environmental regulations and innovation activity in UK manufacturing industries. Resour. Energy Econ. 34 (2), 211–235. doi:10.1016/j.reseneeco.2011.12.001

Kong, T., Feng, T. W., and Ye, C. M. (2016). Advanced manufacturing technologies and green innovation: The role of internal environmental collaboration. Sustainability 8 (10), 1056. doi:10.3390/su8101056

Li, W., Liu, S., and Mei, L. (2022). Research on the impact of business model innovation on enterprise performance based on QCA. J. Manag. Case Stud. 15 (02), 129–142. 10.7511/JMCS20220202

Li, Y., and Li, W. (2015). The mode, risk, problems and countermeasures of agricultural enterprise's scientific and technological innovation. Sci. Technol. Manag. Res. 35 (21), 7–12. doi:10.3969/j.issn.1000-7695.2015.21.002

Li, W., and Zheng, M. (2016). Is it substantive innotation or strategic innovatio?—impact of macroecomomic policies on mico-enterprises’ innovation. J. Econ. Res. 51 (04), 60–73. CNKI:SUN:JJYJ. .2016-04-005)

Meyer, A. D., Tsui, S., and Hinings, A. (1993). Configu-rational approaches to organationl analysis. Acad. Manag. J. 136, 1175–1195. doi:10.2307/256809

Misangyi, V. F., Greckhamer, T., Furnari, S., Fiss, P. C., Crilly, D., and Aguilera, R. (2017). Embracing causal complexity: The emergence of a neo-configurational perspective. J. Manag. 43 (01), 25–282.

Pang, Y., and Liu, Y. (2021). Research on market performances and reasons of listed agricultural companies in China. Rural. Econ. (03), 75–84.

Ragin, C. C. (1987). The comparative method: Moving beyond qualitative and quantitative strategies. Berkeley: University of California Press, 84.

Reichert, F. M., Torugsa, N. A., Zawislak, P. A., and Arundel, A. (2016). Exploring innovation success recipes in low-technology firms using fuzzy-set QCA. J. Bus. Res. 69 (11), 5437–5441. doi:10.1016/j.jbusres.2016.04.151

Wan, J., Zhou, Q., and Xiao, Y. (2020). Digital finance, financial constraint and enterprise innovation. Econ. Rev. 41 (01), 71–83. doi:10.19361/j.er.2020.01.05

Wang, F., Jiang, H., and Wang, C. (2014). The evolution of the control framework China’s central SOEs: Is it strategy determined, Institution Driven, or dependence on the path?—an attempt of a quality comparative analysis. Manag. World 30 (12), 92-114+187-188. doi:10.19744/j.cnki.11-1235/f.2014.12.009

Wang, L., Chen, M., and Niu, L. (2021a). Research on the construction and dynamic evolution of enterprise green innovation path. China Soft Sci. 36 (03), 141–154. doi:10.3969/j.issn.1002-9753.2021.03.013

Wang, L., Huo, Y., and Yang, Y. (2021b). Research on the policy combination mode of innovation and development of manufacturing SMEs: Based on QCA analysis of 31 provinces and cities. J. Technol. Econ. 40 (10), 90–97. doi:10.3969/j.issn.1002-980X.2021.10.008

Wang, P., and Li, G. (2021). Does policy uncertainty affect investment behavior ofAgricultural company? J. Agrotechnical Econ. 40 (08), 20–31. doi:10.13246/j.cnki.jae.2021.08.002

Xie, D., and Liao, K. (2018). Share pledging by controlling shareholders and real earnings management of listed firms. Accounting Res.39 (08), 21–27. doi:10.3969/j.issn.1003-2886.2018.08.003

Xi, Z., and De, L. (2020). Managerial equity incentives and R&D investments in emerging economies: Study based on threshold effects. Asian J. Technol. Innov. 29 (2), 1–24.

Xu, Y., and Xu, C. (2021). The influences of enterprise innovation and governance on its upgrading. Statistics Decis. 37 (11), 182–185. doi:10.13546/j.cnki.tjyjc.2021.11.04

Yu, F., Guo, Y., Le-Nguyen, K., Barnes, S. J., and Zhang, W. (2016). The impact of government subsidies and enterprises' R&D investment: A panel data study from renewable energy in China. Energy Policy 89, 106–113. doi:10.1016/j.enpol.2015.11.009

Yu, W., Zhang, L., Wang, J., Jiang, C., and Cao, L. (2020). Ownership Concentrations, Equity Balances and Financing Constraints: Empirical evidence from 102 listed companies in China's real estate industry from 2013 to 2017. BMC Chem. 41 (03), 46–54. doi:10.1186/s13065-020-00700-7

Zhang, L., Yu, W., and Chen, L. (2020). Guo Xiaohua. Can ownership concentration or equity balance ease the restraint of financing constraints on corporate performance? based on the data from listed companies of real estate industry. J Yunnan Univ. Finance Economics. 36 (070), 51–65. 10. 16537/j.cnki.jynufe.000607

Keywords: external governance, internal governance, synergistic matching, highly green innovations, fsQCA

Citation: Bao H, Chen C and Liu Y (2022) Innovative governance systems and green innovations of agriculture-related enterprises based on the approach of fuzzy-set qualitative comparative analysis. Front. Environ. Sci. 10:990414. doi: 10.3389/fenvs.2022.990414

Received: 10 July 2022; Accepted: 11 October 2022;

Published: 08 November 2022.

Edited by:

Munir Ahmad, Ningbo University of Finance and Economics, ChinaReviewed by:

Yunhui Zhao, Inner Mongolia University of Finance and Economics, ChinaCopyright © 2022 Bao, Chen and Liu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Huricha Bao, U1VZRUJBT0BhbGl5dW4uY29t; Chibo Chen, Y2hpYm9AYWx5dW4uY29t

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.