Xin Ma

Xin Ma Raheel Akhtar

Raheel Akhtar Adeel Akhtar

Adeel Akhtar Raema Abdullah Hashim3

Raema Abdullah Hashim3 Muhammad Sibt-e-Ali

Muhammad Sibt-e-Ali

94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 04 August 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.972555

This article is part of the Research TopicEconomic Development, Social Consequences, and Technological Innovation Under Climate Change COVID-19 Pandemic ConditionsView all 48 articles

Pakistan is an agricultural country that uses a huge number of pesticide chemicals and is confronting environmental and economic issues. Firms need to comprehend the integration of green supply chain management (GSCM) practices in their supply chain. The current study intends to analyze the mediation effect of environmental performance (ENP) in the relationship between GSCM practices, institutional pressures (IP), and financial performance (FNP). Therefore, GSCM-IP-ENP-FNP model was developed with the help of an extensive literature review and then proved with the help of data collected from pesticide chemical firms working in Pakistan. Data were collected through a questionnaire from 500 senior-level managers of the pesticide firms of Pakistan. However, 468 responses were retained for analysis keeping in view the limitations of the current study. SPSS version 22 and SmartPLS 3.0 were used for data analysis. Results of the study indicated strong relationships among all variables. It was also concluded that GSCM practices, IP, and ENP have a positive and statistically significant relationship with a firm’s FNP. This study is an important contribution to theory and practice. The study is unique and has significant contributions because it developed and proved the GSCM-IP-ENP-FNP model. The model helped to prove the mediation effect of ENP in the relationship between GSCM practices, IP, and FNP in the pesticide sector of Pakistan, which would be highly beneficial for the managers of pesticide firms as well as for the government to understand the importance of GSCM practices for improving the ENP as well as the FNP of pesticide firms in Pakistan as well as worldwide, especially in developing countries. This study recommends that the management of firms should implement GSCM practices to protect the environment. Government, consumers, and other institutions should exert pressure and the government should provide subsidies, if necessary, to the firms for successful implementation of GSCM practices. Furthermore, it is recommended to conduct further studies in other countries by using the mixed methodology in the pesticide sector as well as in other sectors of the economy to increase the generalizability of the current study.

Over the last decade, firms, as well as governments of various countries, have been highly concerned regarding environmental issues (Zelazna, Bojar and Bojar, 2020). The growing trend of implementing green supply chain management (GSCM) practices is highly stimulated by institutional pressures to achieve the target of greening the industrial operations (Tseng et al., 2019). GSCM practices from supplier to customer encompass the whole value chain as organizations try to reduce the negative impacts of their operations on the natural environment (Ahmed et al., 2020). Pressure from the global industry is to implement the GSCM practices to become competitive in the global market, which also provides export opportunities for manufacturers (Al-Ghwayeen and Abdallah, 2018). The institutional pressures accompanying globalization have prompted enterprises to improve their environmental and financial performance (Helm, 2020). The pressure on businesses to increase environmental performance also comes from globalization (Tang et al., 2020). Increasing environmental concern has become a part of the pesticides sector as well. GSCM practices including internal and external practices have a positive and significant effect on the firm’s financial growth (Liao and Zhang, 2020).

Firms implementing GSCM practices under institutional pressures can be assessed on environmental and firm’s financial performance. All over the world, global warming and environmental change is an important issue (Ali et al., 2021; Rehman et al., 2021). The recent studies suggest that further investigations are required to find the relationship between environmental practices and financial performance, which may include reduced use of toxic materials and reduced wastage of water, materials, and electricity and firm’s financial growth, especially in the developing countries (Vanalle et al., 2017). Most of the studies are carried out in developed countries, so a research gap exists in developing countries (Geng, Mansouri and Aktas, 2017). Most of the GSCM studies included single informants from each organization, but future researchers must include multiple responses from each organization from different levels of employees (Habib et al., 2020). Therefore, this study aims to analyze the relationship between GSCM practices, institutional pressures, environmental and firm’s financial performance in the Pakistani pesticide sector by having multiple responses from each organization from different levels of employees. This research has a vital contribution to the existing literature because it has proved the mediation effect of environmental performance in the relationship between GSCM practices, institutional pressures, and financial performance in the pesticide sector of Pakistan, which would be helpful for the managers of pesticide firms as well as for the government to understand the importance of GSCM practices for improving the environmental as well as the financial performance of pesticide firms in Pakistan as well as worldwide, especially in developing countries. Moreover, it is one of the rare studies, which includes GSCM practices; internal (IGSCM) practices like eco-design (ECD) of product and internal environmental management (IEM), and external (EGSCM) practices like green purchasing (GP), cooperation with customers (CWC) and reverse logistics (RL), institutional pressures (IP), environmental (ENP) and firm’s financial performance (FNP).

This research is conducted using the resource-based view (RBV) theory and the institutional theory. The RBV theory emphasizes that the resources and capabilities always play important role in achieving competitive advantage (Bu et al., 2020). Adoption of GSCM practices may also be one of the competitive advantages. RBV theory focuses on a firm’s internal and external strategies to improve the firm’s financial performance (Kamasak, 2017). IP plays an important role in the adoption of GSCM practices to improve environmental performance (Chu et al., 2017), which is linked with institutional theory. Institutional theory dimensions clear the boundaries of best GSCM practices (Dedoulis, 2016). The institutional theory theoretically supports explaining the GSCM practices (internal GSCM practices and external GSCM practices). The institutional theory also supports the relationship between institutional pressures and environmental performance (Yang, 2018).

Pakistan’s agricultural sector has a great contribution to the GDP of Pakistan. Pakistani farmers use large amounts of pesticide chemicals for improving agricultural outputs, whereas pesticide producers are adopting effective GSCM practices for improving their environmental and financial performance (Akhtar and Soratana, 2021). Most of the farmers in Pakistan use pesticides for growth in agricultural production. Pesticides have many negative effects on the environment (Hakeem et al., 2016). More use of pesticides and fertilizers harms the environment and is becoming a major challenge for the improvement of environmental performance (Hakeem et al., 2016; Dagar et al., 2020). The agriculture sector, which contributes 18.9% of Pakistani GDP, can benefit from China Pakistan Economic Corridor (CPEC) by upgrading the nexus of the backward and forward supply chain (Yar et al., 2021). CPEC is one of the flagship projects of China’s Belt and Road Initiative, which had an initial worth of $47 billion and currently has $62 billion (Ali et al., 2020). CPEC is one of the major FDIs in the history of Pakistan (Ali et al., 2020). Due to CPEC projects, hundreds of companies are doing investments in Pakistan and many more companies are willing to invest; most of those companies are implementing green practices but still, the environmental threat should not be ignored (Khan, 2020). FDI was criticized for the rise in environmental pollution through unsustainable production practices due to a lack of environmental regulations by host countries (Asif et al., 2020). More regulations (institutional Pressures) are required to improve the environmental performance of Pakistani firms (Kouser, Subhan and Abedullah, 2020). Thus, the current study aims to analyze the mediation effect of environmental performance in the relationship between GSCM practices, institutional pressures, and financial performance in the pesticide sector of Pakistan through the lens of RBV theory and institutional theory.

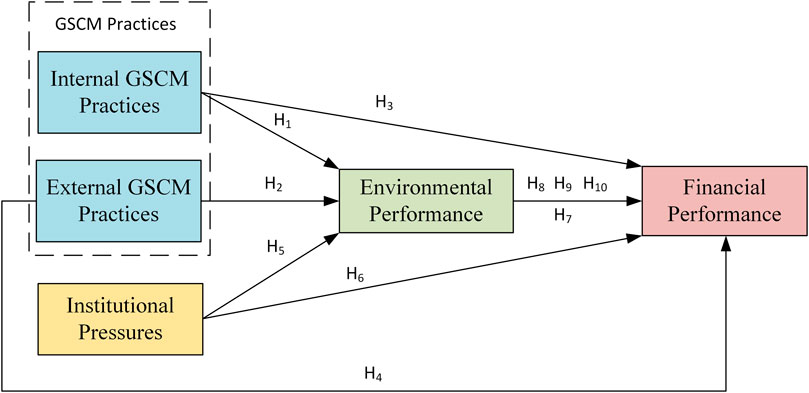

A detailed examination of the literature was conducted with particular attention paid to GSCM practices, institutional pressures, firm’s environmental and financial performance. A model GSCM-IP-ENP-FNP (Figure 1) was developed after an extensive literature review. The literature review findings are given below:

FIGURE 1. GSCM-IP-ENP-FNP model.

RBV theory focuses on indispensable, rare, valuable, and non-sustainable firms’ capabilities and resources to attain sustainable and competitive advantage in the form of environmental improvement (green and better quality products) and competitive financial performance (resources optimization) as compared to competing firms (Barney, 1991). Tangible assets and intangible assets both include the firm’s important resources like GSCM practices, environmental and financial performances (Vitorino Filho and Moori, 2020). A temporary competitive advantage is provided by tangible resources because competitors can copy these resources easily. Although, the competitors cannot copy the intangible resources because it is gained by the experience (Kamasak, 2017). It is difficult to copy the GSCM practices of the competitors because it gains from the experience. For example, competitors cannot easily copy the positive reputation of firms that is earned by the successful implementation of GSCM practices (Yildiz Çankaya and Sezen, 2019). Therefore, RBV is one of the most appropriate theories for the investigation of the relationship between GSCM practices, environmental and financial performances.

Institutional theory is utilized to comprehend the many external variables that compel any firm to launch or implement any new practice. The pressure which firms put on one another in the adoption of more sustainable green practices in the supply chain is known as institutional pressures (Saeed et al., 2018). External pressures which can influence organizational activities are known as institutional pressures (DiMaggio and Powell, 1983). This theory can be used to examine and explain the cause and extent of implementing the firm’s green practices (Touboulic and Walker, 2015).

GSCM practices are implemented to improve environmental performance (Zhu, Sarkis and Lai, 2012). A sustainable environment can be achieved by adopting innovative environmental-related technologies like GSCM practices (Khan M. K. et al., 2022). The Implementation of GSCM (internal and external) practices causes a reduction in environmental accidents, which improves the firm’s performance as well as society’s well-being (Das, 2018). The environmental performance of the firm demonstrates its ability to reduce hazardous components, environmental accidents, pollution, and solid waste. (Esfahbodi, Zhang and Watson, 2016). GSCM practices cover internal GSCM practices and external GSCM practices (Ming Heng et al., 2018). Internal GSCM practices include deliberate performance-related activities, which means these practices have a valuable contribution to a firm’s performance (Vanalle et al., 2017). Internal GSCM practices include the practices like eco-design (ECD) and internal environmental management (IEM) (Choi, Min and Joo, 2018; Al-Sheyadi, Muyldermans and Kauppi, 2019). External GSCM covers practices like green purchasing (GP), cooperation with customers (CWC) and reverse logistics (RL) have a significant relationship with the environmental performance of the firm (Zaid, Bon and Jaaron, 2019). Internal and external GSCM practices have a significant relationship with environmental performance (Marhamati and Azizi, 2017). GSCM (Internal and external) practices have a significant relationship with environmental performance (Al-Sheyadi, Muyldermans and Kauppi, 2019). Therefore, the following hypotheses are proposed:

H1: Internal GSCM practices have a significant effect on the firm’s environmental performance.

H2: External GSCM practices have a significant effect on the firm’s environmental performance.

Financial performance includes an increase in return on investment, increase in earnings per share, increased profit margin, raise in product price, raise in sales, and enhanced market share (Golicic and Smith, 2013). In previous studies, limited research was conducted to investigate the relationship between GSCM (internal and external) practices and financial performance (Siddiqui and Siddiqui, 2020). Recent studies find a direct and significant relationship between GSCM (internal and external) practices and organizational performance (Chin, Tat and Sulaiman, 2015). If GSCM practices are combined with the supply chain of a firm, they will lead to an increase in profit and competitive advantage (Chan, He and Wang, 2012). The overall change in financial performance is due to indicators related to GSCM practices (Shahzad et al., 2022). A study conducted on the supply chain situation paradox collected data from 284 individuals from each firm and concluded that GSCM (internal and external) practices have a significant and positive effect on a firm’s financial performance (Schmidt, Foerstl and Schaltenbrand, 2017). There are mixed results found in the previous studies indicating the relationship between GSCM (internal and external) practices and a firm’s financial performance (Geng, Mansouri and Aktas, 2017). Adoption of GSCM (internal and external) practices is vital for the top management to achieve a competitive advantage (Banasik et al., 2017). Effective GSCM practices cause an improvement in financial performance (Golicic and Smith, 2013). Therefore, the following hypotheses are proposed:

H3: Internal GSCM practices have a significant effect on the firm’s financial performance.

H4: External GSCM practices have a significant effect on the firm’s financial performance.

Institutional pressures from governments, competitor firms, customers, and other pressure groups have a significant impact on firms for the successful implementation of GSCM practices (Zhang et al., 2020). GSCM practices can be influenced by institutional pressures, which include pressure from domestic regulatory bodies, government regulations, stakeholders, customers, competitors, non-government organizations, and employees (Zhang et al., 2020). Pressure from competing firms encourages organizations to implement GSCM practices as it allows the firms to compete by delivering green products and staying agile with improvements in environmental commitments (Choi, Min and Joo, 2018). Institutional pressures from governments and other pressure groups have a positive and significant effect on a firm’s environmental performance (Phan and Baird, 2015). Environmental regulations play an important role in the improvement of environmental performance (Murshed et al., 2021). Research conducted on 248 enterprises concluded that the institutional pressures had a significant impact on a firm’s environmental and financial performance (Aharonson and Bort, 2015). Environment and financial performance have a negative relationship, so the government needs to provide subsidies and tax exemptions to encourage eco-friendly products (Ullah and Ali, 2022). Effective governance may improve environmental performance (Nadeem et al., 2022). Institutional pressures have a significant and noteworthy relationship with GSCM (internal and external) practices (Mitra and Datta, 2014). Therefore, we proposed the following hypotheses:

H5: Institutional pressures have a significant and noteworthy effect on the firm’s environmental performance.

H6: Institutional pressures have a significant and noteworthy effect on the firm’s financial performance.

Environmental performance includes environmental compliance improvement, a decrease in consumption of energy and water, minimum use of hazardous material and environmental accidents, and a decrease in carbon emissions (Yook, Choi and Suresh, 2018). Firms implementing GSCM practices minimize firm costs and improve environmental performance by protecting the environment (Shafique, Asghar and Rahman, 2017). A firm’s GSCM practices cause environmental improvement and have a significant and noteworthy effect on a firm’s financial performance (Yang, 2018). Change in a climate affects the industrial financial performance (Ali et al., 2021). Environmental concerns to achieve firm performance have an important impact on society (Luo, Ullah and Ali, 2021). Earlier studies have clear evidence of a remarkable relationship among the environmental and firm’s financial performance (Al-Sheyadi, Muyldermans and Kauppi, 2019; Weimin et al., 2022). A firm’s financial performance improvement can happen through the successful implementation of GSCM (internal and external) practices (Al-Sheyadi, Muyldermans and Kauppi, 2019). Therefore, we proposed the following hypothesis:

H7: Firm’s environmental performance has a significant and noteworthy effect on the firm’s financial performance.

Environmental performance can be measured by waste reduction, prevention of pollution, or other items related to environmental performance (Tseng et al., 2019). Firms should adopt GSCM practices, but how they can improve environmental and financial performance is not clear yet (Zhu, Sarkis and Lai, 2019). Internal GSCM practices like ECD and IEM can reduce the use of toxic materials, energy, and water waste, which has a remarkable role in minimizing environmental impacts and enhancing firm financial performance by cost-cutting (Al-Ghwayeen and Abdallah, 2018). Financial performance improves as the firms successfully implement GSCM practices (Zailani et al., 2012). According to a study done in China on 126 automobile manufacturers, the indirect influence of GSCM practices on a firm’s financial performance might be mediated by a firm’s environmental performance (Feng et al., 2018). The rise in environmental performance minimizes pollution due to the successful implementation of GSCM (internal and external) practices, which results in the improvement of financial performance because of a reduction in costs (Esfahbodi et al., 2017). Environmental practices have a remarkable relationship with institutional pressure and green practices (Jianguo et al., 2022). The green growth objective cannot be achieved without the sustainable use of material resources (Xie et al., 2022). A firm’s environmental performance mediates the relationship among GSCM practices and financial performance in manufacturing companies (Al-Ghwayeen and Abdallah, 2018). A firm’s environmental performance also mediates the relationship among the institutional pressures and a firm’s financial performance (Gupta and Gupta, 2021). Future studies should be conducted to investigate the direct influence of institutional pressures on the environment and the indirect effect on firm financial performance (Yang, 2018). More studies are required to examine the impact of environmental performance, GSCM (internal and external) practices, institutional pressures, and financial performance in manufacturing firms (Saeed et al., 2018). Therefore, based on the above-stated studies we proposed the following hypotheses:

H8: Firm’s environmental performance has a mediating role between internal GSCM practices and a firm’s financial performance.

H9: Firm’s environmental performance has a mediating role between external GSCM practices and a firm’s financial performance.

H10: Firm’s environmental performance has a mediating role between institutional pressures and a firm’s financial performance.

After an extensive literature review, Figure 1, GSCM-IP-ENP-FNP Model was developed. The model shows that internal GSCM, external GSCM, and institutional pressures have a significant, direct as well as indirect effect, on a firm’s financial performance having the mediating role of environmental performance. The rationale for the GSCM-IP-ENP-FNP model is inspired by recent studies (Saeed et al., 2018), (Ahmed, Najmi and Khan, 2019; Marri, Sarwat and Aqdas, 2021).

The Figure 1 indicates that internal GSCM, external GSCM, and institutional pressures have a significant, noteworthy, direct, and indirect, effect on financial performance with mediating role on environmental performance.

It is a quantitative study and a survey questionnaire was utilized to collect data. Multi-stage sampling was done. In the 1st stage, purposive sampling was applied for the selection of firms and at 2nd stage, convenient sampling was used to get responses from senior employees of the selected firms. Cross sectional design was followed for data collection due to time and cost constraints. There are 52 corporate-level pesticide chemical firms registered with Pakistan Crop Protection Association (PCPA). Out of those 52 firms, 22 firms are located in district Multan, Punjab, which accounts for 44% of the total corporate-level firms. Therefore, Multan is considered a hub for the pesticide chemical firms operating in Pakistan. That’s why 22 corporate-level pesticide chemical firms, located in district Multan, were selected for the collection of data by using the purposive sampling method.

Sampling is the process of selecting a subset from a defined sampling frame or the complete population. Sampling can be used to draw conclusions about a population or to make generalizations on current theory (Taherdoost, 2016). Generally, sampling is divided into two categories; probability sampling and non-probability sampling. By using probability sampling, every item in the population has an equal chance of being included in the sample. One method for doing probability sampling would be for the researcher to first create a sampling frame and then use a random number generating computer program to choose a sample from the sampling frame (Taherdoost, 2016). Probability sampling includes; simple random, systematic sampling, stratified random, and cluster sampling. Probability sampling is not appropriate for the current study because it is not possible to list down all the employees working in pesticide chemical firms in a short time and low budget.

Non-probability sampling techniques such as convenience sampling and purposive sampling are used by researchers to choose a sample of subjects/units from a population. Although non-probability sampling has several drawbacks owing to the subjective nature of sample selection, it is beneficial when randomization is difficult, such as when the population is very massive (Etikan, 2016). It can be beneficial when the researchers’ resources, time, and labor are limited. So, the non-probability sampling is appropriate for the current study.

This study has five variables with 39 items to evaluate the conceptual framework of the study. Internal GSCM practices were measured with 10 items (Al-Sheyadi, Muyldermans and Kauppi, 2019), External GSCM Practices were measured with 09 items (Yildiz Çankaya and Sezen, 2019), Institutional Pressures was measured with 07 items (Chu et al., 2017; Kalpande and Toke 2020), Environmental performance was measured with 06 items (Pinto, 2020), (Banasik et al., 2017) and Financial performance was measured with 07 items (Flynn et al., 2010; Zhang et al., 2020). According to (Israel, 1992) for the selection of sample size where the population is greater than 100,000 and the level of confidence is 95% with a p-value = 0.05 sample size should be 400 (Singh and Masuku, 2014). Researchers suggests that at least the 05 to 01 ratio should be taken (Memon et al., 2020). In another study, the “10-times rule” is stated as a favorite for data collection due to its simple application (Kock, 2018) its most widely used in PLS-SEM studies (Kock and Hadaya, 2018). This rule is based on that the sample size should be greater than 10 times the maximum number of items in the scale. The requirement for a sufficient sample size is 5–20 responses against one item (Maurischat, 2006). Based on these studies the targeted sample for the current study was 390 respondents from 22 Pesticide firms located in district Multan, Pakistan.

Data were collected using Google Forms. An online link was shared with respondents through WhatsApp, Facebook, email, and personal visits. The link was sent to senior executives of the companies and they further forwarded it to their senior-level colleagues. Responses were collected from 10 July 2021 to 10 November 2021. The minimum required sample size was 390 by using the 10 times rule for data collection (Kock, 2018), which is a suitable technique for using SmartPLS (Kock and Hadaya, 2018). However, to ensure quality, a total of 500 responses were collected. 468 responses were retained for further analyses, whereas 32 responses were eliminated due to study limitations (responses from firms having less than 100 employees or the firm’s age was not more than 10 years). Descriptive analysis was conducted using SPSS version 22. Other statistical analyses including reliability and validity, discriminant validity, multicollinearity, correlation analysis, and hypothesis testing were performed by using Partial Least Square Structural Equation Modelling through SmartPLS 3.

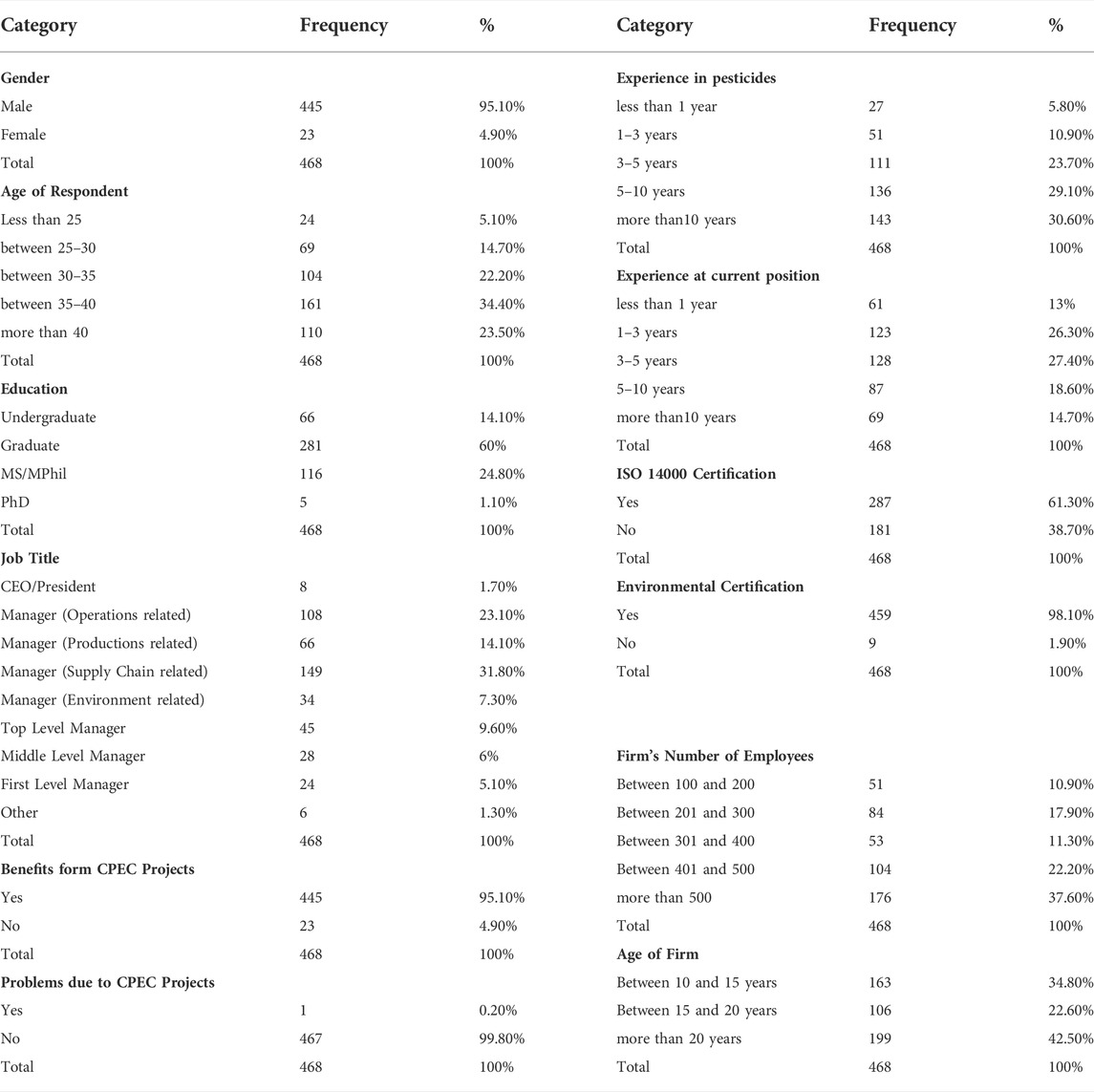

Demographic analysis was conducted to generalize and check the study limitations (Table 1), and the bold text is the subsection of demographics using SPSS version 22. As the study was limited to corporate-level pesticide chemical firms, having more than 10 years of firm age along with more than 100 employees. 500 responses for the current study were received from which 32 responses were excluded because those responses belonged to firms, which had less than 100 employees or the firm’s age was not more than 10 years. There were 445 male (95.1%) and 23 female (4.9%) participants. 161 (34.4%) respondents had an age between 35–40. 402 (85.9%) respondents were having at least graduate or higher-level educational qualifications. 143 (30.6%) respondents had more than 10 years of experience in pesticide firms, whereas 128 respondents (27.4%) had working experience at their current job. 287 (61.3%) respondents belonged to such firms, which were having ISO 14000 certification. 459 (98.1%) respondents belonged to those firms, which were having ISO 14000 certification and/or any other environmental certification. 445 (95.1%) respondents indicated that pesticide firms had benefited from CPEC projects and 467 (99.8%) respondents indicated that pesticide firms in Pakistan did not have any problems due to CPEC projects as shown in Table 1.

TABLE 1. Demographics analysis.

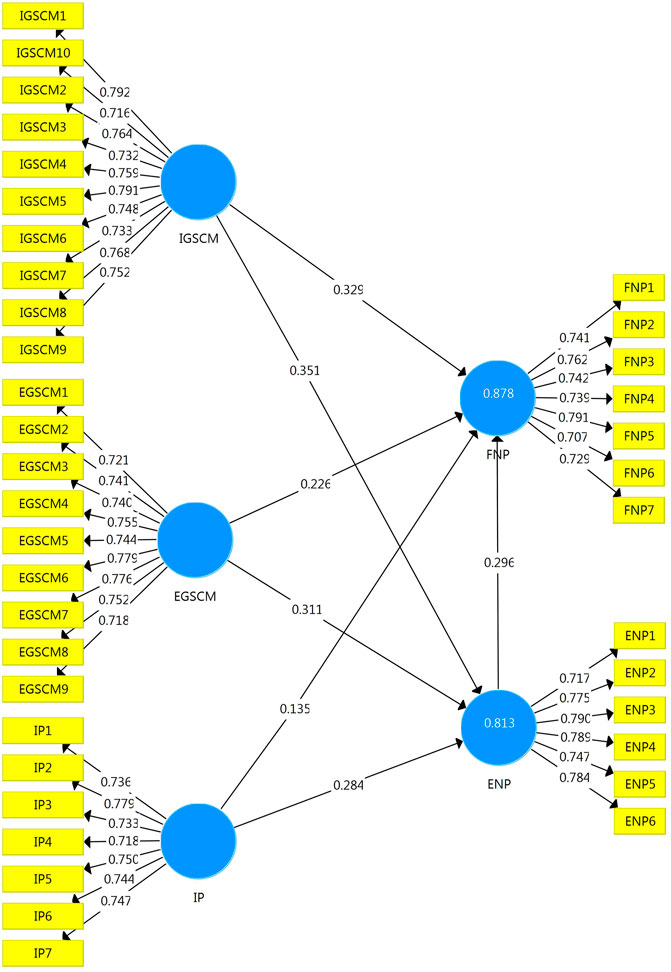

This section encompasses two parts. 1st part, Figure 2, shows the measurement/outer model, whereas, the 2nd part, Figure 3, depicts the structural (inner model). Association between variables is indicated in the measurement/outer model (Xiang et al., 2022). For the determination of the constructs’ reliability and validity, it is necessary to estimate the outer model at 1st stage (Ringle et al., 2015). To examine the validity as well as reliability of constructs, an analysis of the outer model was performed to confirm that the items of the survey questionnaire were measuring what they were supposed to measure.

FIGURE 2. Measurement model.

FIGURE 3. Structural model (GSCM-IP-ENP-FNP).

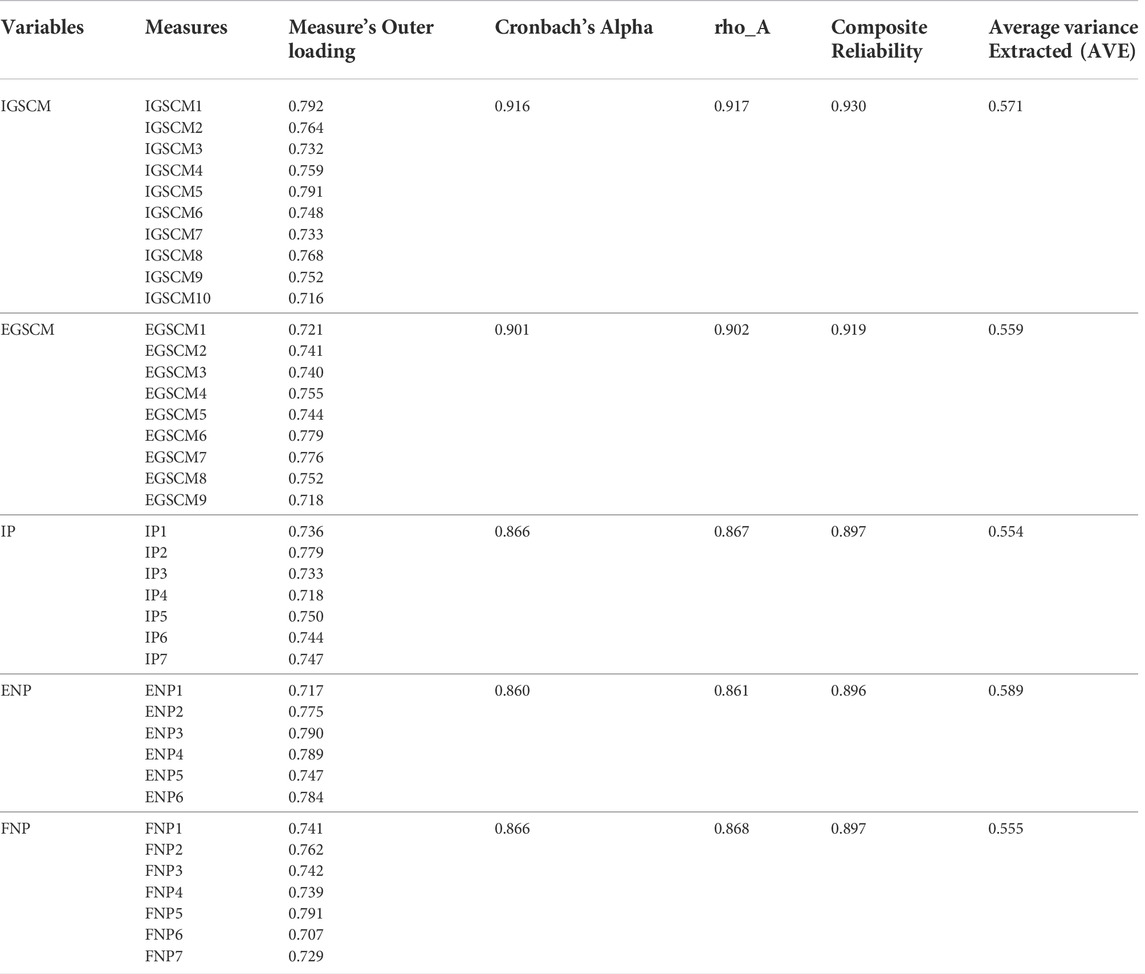

To estimate the validity as well as reliability of the constructs and items, outer model analysis is used as the “Quality Criteria for Measuring Instrument” (Henseler, Hubona and Ray, 2016). Cronbach’s Alpha values were >0.70 and Composite Reliability values also were >0.70, which confirmed the reliability of the outer model (Table 1). In the current study convergent validity was ensured by using average variance extracted (AVE) measuring >0.50 as the rule of thumb (Henseler, Hubona and Ray, 2016). As the outer loadings of all items were >0.70 (Table 1), therefore, further analyses were conducted to test the study hypotheses.

One of the important methods to evaluate discriminant validity is cross-loading analysis (Khan M. T. et al., 2022), which confirms that the items measuring the variable are measuring what they are intended to measure (Hair et al., 2014), (Vanalle et al., 2017). The cross-loading analysis yielded sufficient data for discriminant validity in the current investigation as shown in Table 2.

TABLE 2. Quality criteria for measuring instrument.

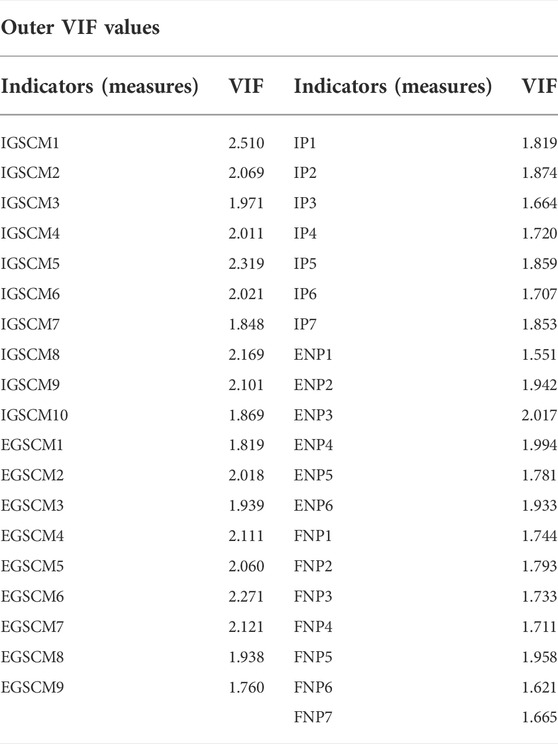

Multicollinearity of the data should be checked before the analysis of the structural model of the study (Hair et al., 2017). Table 3 shows the maximum multicollinearity value of 2.510, which is within the normal range. That’s why multicollinearity is not the problem of the current study (Henseler, Hubona and Ray, 2016).

TABLE 3. Cross loadings.

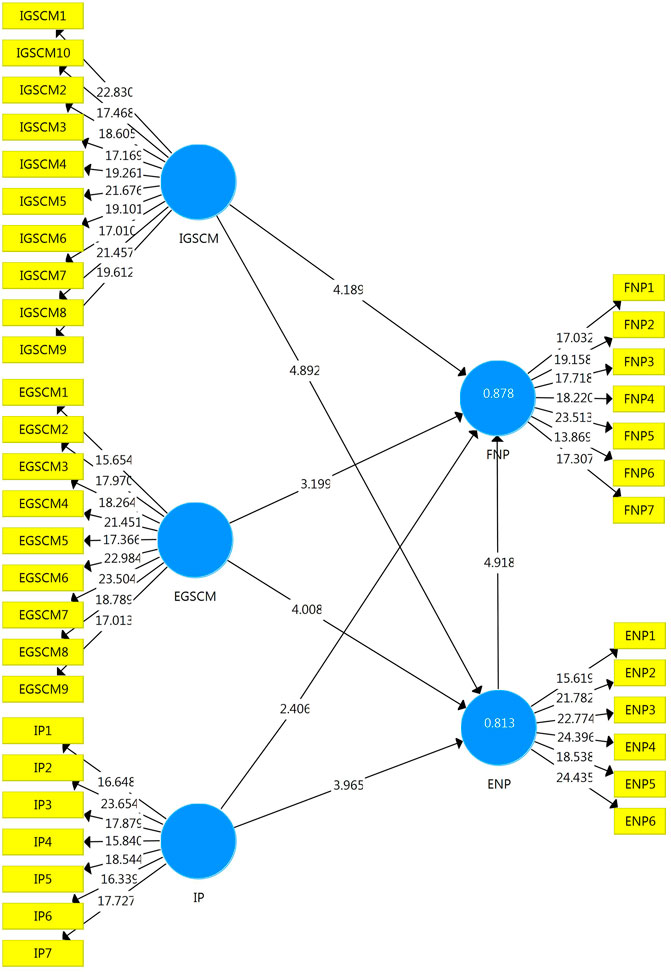

Because of recommended bootstrap samples of 5000 (Vanalle et al., 2017), the current study conducted bootstrap analysis at 5000 samples. The relationship was examined between independent variables (IGSCM, EGSCM, institutional pressures), mediating variable (environmental performance), and dependent variable (financial performance). The bootstrapping method was used to measure the path coefficients, significance, t-value, and standard error through SmartPLS 3. Bootstrapping results are presented in Figure 3.

Results in Figure 3 show that all measures had a t-value > 1.96 and a p-value < 0.05 therefore, all the measures were statistically significant (Marri, Sarwat and Aqdas, 2021).

All items of financial performance were highly correlated with GSCM practices (internal as well as external practices), institutional pressures, and environmental performance, which means that GSCM practices (internal and external), institutional pressures, and environmental performance have a strong relationship with firm’s financial performance as shown in Table 4, and the value of IGSCM1= 2.510 is highest value and ENP1=1.551 is the lowest value.

TABLE 4. Collinearity statistics (VIF).

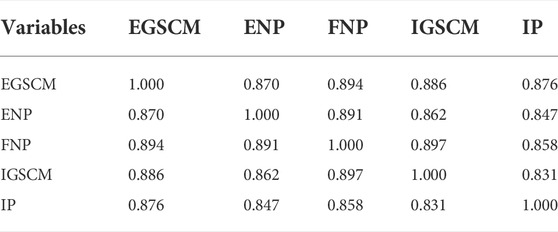

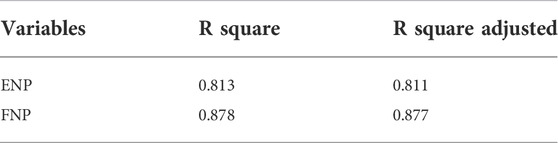

To estimate the adequacy of the model it is necessary to calculate the “coefficient of determination (R2)” (Marri, Sarwat and Aqdas, 2021). The coefficient of determination (R2) was used to evaluate and measure the structural model. R2 values of 0.75 indicate strong, 0.50 indicates moderate and 0.25 indicates the weak effect of the independent variable(s) on the dependent variable (Akter, Fosso Wamba and Dewan, 2017). The variance in the dependent variable due to the independent variable is measured with R2. Results of R2 for environmental performance and financial performance are shown in Table 5, and the value =1.000 shows the perfect correlation. Results showed that environmental performance had R2 = 0.813, whereas Financial Performance had R2 = 0.878, which indicated that there was a strong effect on environmental performance and financial performance due to GSCM (internal and external) Practices and institutional pressures (see Table 6).

TABLE 5. Latent variable correlations.

TABLE 6. R square.

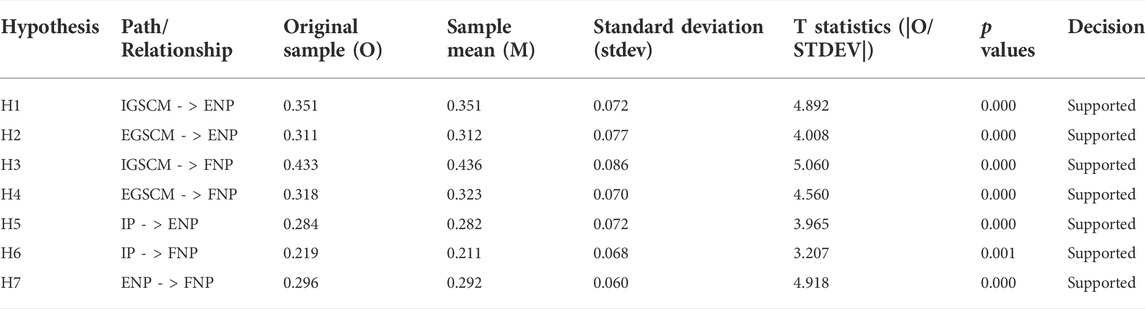

This study tested the hypotheses using SmartPLS 3. Hypotheses testing and final decision for internal green supply chain management (IGSCM) practices, external green supply chain management (EGSCM) practices, institutional pressures (IP), environmental performance (ENP), and financial performance (FNP) result shows in Table 7.

TABLE 7. Hypotheses testing results and decision.

H1 results (Internal GSCM Practices - > Environmental Performance) indicated a “Relationship coefficient” (β) = 0.351, “T-statistics” = 4.892 with “p-value” = 0.000. So, our H1 is supported with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, there was a “positive and significant relationship proved between internal GSCM practices and environmental performance”. H2 results (External GSCM Practices - > Environmental Performance) indicated a “Relationship coefficient” (β) = 0.311, “T-statistics” = 4.008 with “p-value” = 0.000. So, our H2 is accepted with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, there was a “positive and significant relationship proved between external GSCM practices and environmental performance”. H3 results (Internal GSCM Practices - > Financial Performance) indicated a “Relationship coefficient” (β) = 0.433, “T-statistics” = 5.060 with “p-value” = 0.000. So, our H3 was accepted with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, there was a “positive and significant relationship proved between internal GSCM and firm’s financial performance”. H4 results (External GSCM Practices - > Financial Performance) indicated a “Relationship coefficient” (β) = 3.18, “T-statistics” = 4.560 and “p-value” = 0.000. So, our H4 was accepted with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, there was a “positive and significant relationship proved between external GSCM practices and firm’s financial performance”. H5 results (Institutional Pressure - > Environmental Performance) indicated a “Relationship coefficient” (β) = 0.284, “T-statistics” = 3.965 with “p-value” = 0.000. So, our H5 is supported with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, there was a “positive and significant relationship proved between institutional Pressure and environmental performance”. H6 (Institutional Pressure - > Financial Performance) indicated a “Relationship coefficient” (β) = 0.219, “T-statistics” = 3.207 with “p-value” = 0.001. So, our H6 was accepted with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Therefore, a “significant and positive relationship between institutional pressures and firm’s financial performance was proved”. H7 results (Environmental Performance - > Financial Performance) indicated a “Relationship coefficient” (β) = 0.296, “T-statistics” = 4.918 and “p-value” = 0.000. So, our H7 was accepted with “T-statistics > 1.96 with p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, there was a “positive and significant relationship proved between firm’s environmental performance and firm’s financial performance”.

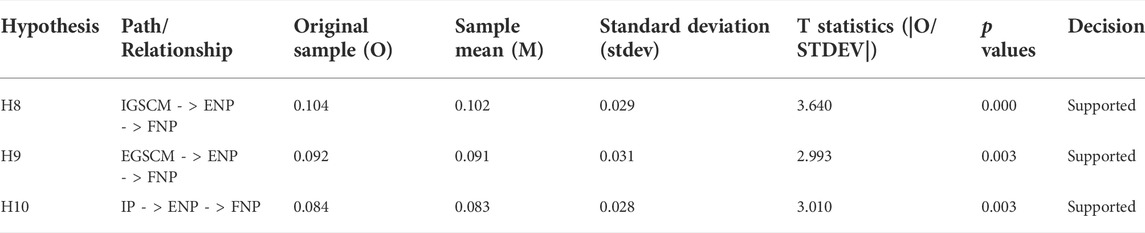

This study tested the mediation effect of environmental performance using SmartPLS 3. Table 8 shows the results of the mediation analysis and final decision on mediating role of a firm’s environmental performance between GSCM (IGSCM and EGSCM) practices, institutional pressure, and the firm’s financial performance.

TABLE 8. Mediation testing results and decision.

H8 results (Internal GSCM Practices - > Environmental Performance - > Financial Performance) indicated a “Relationship coefficient” (β) = 0.104, “T-statistics” = 3.640 with “p-value” = 0.000. Therefore, our H8 was accepted with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, “environmental performance had a positive mediating role between GSCM (internal practices) and firm’s financial performance”. H9 results (GSCM External Practices - > Environmental Performance - > Financial Performance) indicated a “Relationship coefficient” (β) = 0.092, “T-statistics” = 2.993 with “p-value” = 0.003. So, our H9 was accepted with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, “environmental performance had a mediating role between external GSCM practices and firm’s financial performance”. H10 results (Institutional Pressures - > Environmental Performance - > Financial Performance) indicated a “Relationship coefficient” (β) = 0.084, “T-statistics” = 3.010 with “p-value” = 0.003. So, our H10 was accepted with “T-statistics > 1.96 and p-value < 0.05” (Akter, Fosso Wamba and Dewan, 2017), (Akhtar and Soratana, 2021). Hence, “environmental performance had a mediating role between institutional pressures and firm’s financial performance”.

According to the findings of the study, the strong, positive, and statistically significant association between GSCM (IGSCM and EGSCM) practices, institutional pressures, environmental performance, and a firm’s financial performance was established. GSCM (IGSCM and EGSCM) practices and institutional pressures had a significant relationship with the environmental as well as with the firm’s financial performance (Wei, Ayub and Dagar, 2022). As implementing the GSCM practices there is a visible decline in consumption of natural resources. Consumption of natural resources and energy has a significant effect on environmental performance (Dagar et al., 2022). There was a mediating role of environmental performance in the relationship between GSCM practices, institutional pressure, and financial performance. Moreover, the environmental performance had also a significant positive effect on a firm’s financial performance.

The current study has a great contribution to theory and practice. The GSCM-IP-ENP-FNP model was developed with the help of an extensive literature review and then proved with the help of data collected from pesticide chemical firms working in Pakistan. The resource-based view (RBV) theory and institutional theory were used to prove the mediation effect of a firm’s environmental performance in the relationship between GSCM (IGSCM and EGSCM) practices, institutional pressures, and financial performance in the pesticide sector of Pakistan (Khan M. T. et al., 2022). These findings would be helpful for the managers of pesticide firms as well as for the government to understand the importance of GSCM practices for improving the environmental as well as the financial performance of pesticide firms in Pakistan as well as worldwide, especially in developing countries. More specific rules and government guidelines are needed for environmental improvement (Choi, Min and Joo, 2018). In terms of application, this research helps pesticide chemical firm executives to better grasp the significance of GSCM practices and institutional pressures in improving environmental and financial performance. The conclusions of this study are important for the government and other stakeholders to keep pressure on pesticide firms and other businesses to adopt GSCM practices.

This study has some limitations also. The study included pesticide chemical firms because Pakistan is an agricultural country and the use of pesticide chemicals is necessary for the improvement of agriculture production (Akhtar and Soratana, 2021). The study included only corporate-level firms having 10 years of firm age and a minimum of 100 employees because small firms do not have enough resources to adopt GSCM practices in their business operations (Geng, Mansouri and Aktas, 2017). The study is limited to GSCM practices, institutional pressures, environmental performance, and financial performance. Government, consumers, media, and other pressure groups have emphases on implementing GSCM practices and improving environmental performance; on the other hand, firms have concerns regarding financial performance (Ullah and Ali, 2022). The quantitative research approach is followed because the quantitative method is suitable for theory testing by examining the relationship among variables of the study (Ming Heng et al., 2018). A quantitative approach is used because it helps collect larger data in a short time. Future research may be conducted using a mixed research methodology including questionnaires as well as in-depth interviews to get further insights.

The current study recommends that GSCM practices (internal and external) should be adopted and implemented by the management of the firms to protect the atmosphere and improve the environmental and financial performance. GSCM-related practices like energy-efficient use, and minimum fossil fuel consumption can lead to improvement in environmental and financial performance (Ullah and Nadeem, 2022). To eliminate unsustainable activities and improve environmental quality, policymakers are advised to raise public pressure on political leadership (Zhang et al., 2022). Government, consumers, media, and other institutions should exert pressure on pesticide chemical firms and other firms to adopt the GSCM (internal and external) practices for the improvement of environmental performance. Government should also pay attention to facilitating and providing subsidies, if necessary, to the firms for the successful implementation of GSCM practices for environmental protection.

The results may be generalized to the pesticide firms and other firms operating in other countries with similar features. The findings of this study can be applied in developing countries as well as in developed countries. The current study is limited to the variables of the study due to particular emphasis on the mediation effect of environmental performance, whereas financial performance is a major concern of firms. Data collection was also limited to Pakistan only. It is recommended for future researchers to conduct more studies in other countries by focusing on additional variables like technological shift, innovation, and social performance. It is strongly recommended that future studies may be conducted using a mixed methodology. The study concludes that a firm’s environmental and financial performances are affected by the GSCM (internal and external) practices as well as by institutional pressures, moreover, environmental performance mediates the relationship between GSCM practices, institutional pressures, and financial performance.

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

For this research article, four authors have their contributions. The contributions from authors include “Conceptualization, XM, RA, and AA; methodology, RA and AA; software use, validation, formal analysis, RA, AA, and RH; investigation, resources, data curation, writing—original draft preparation, RA; supervision, project administration, funding acquisition, XM; writing-review and editing, XM, AA, RH, and MS. All authors have read and agreed with the terms to the published version of the manuscript. Authorship is limited to those who have contributed substantially to the work reported.”

This research was funded by the National Social Science Fund of China, grant number 13BJL076, and also was funded by the Key Soft Science Projects in Henan Province, China, grant number 222400410010.

This original study is extracted from the PhD thesis of the second author. We are thankful to Shakil Akthar and Muhammad Hassaan for useful discussions. We are also thankful to the senior level managers of pesticide chemical firms, operating in district Multan, Pakistan, for their cooperation in data collection.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Aharonson, B. S., and Bort, S. (2015). Institutional Pressure and an Organization’s Strategic Response in Corporate Social Action Engagement: The Role of Ownership and media Attention. Strateg. Organ. 13 (4), 307–339. doi:10.1177/1476127015598306

Ahmed, W., Ashraf, M. S., Khan, S. A., Kusi-Sarpong, S., Arhin, F. K., Kusi-Sarpong, H., et al. (2020). Analyzing the Impact of Environmental Collaboration Among Supply Chain Stakeholders on a Firm’s Sustainable Performance. Oper. Manag. Res. 13 (1–2), 4–21. doi:10.1007/s12063-020-00152-1

Ahmed, W., Najmi, A., and Khan, F. (2019). Examining the Impact of Institutional Pressures and green Supply Chain Management Practices on Firm Performance. Manage. Environ. Qual. Int. J. 31 (5), 1261–1283. doi:10.1108/MEQ-06-2019-0115

Akhtar, A., and Soratana, K. (2021). Importance of Triple-A and GSCM Practices for Organizational Performance : Qualitative Insights from a Developing Country. Int. J. Disaster Recovery Business Continuity 12 (1), 107–116. Available at: http://sersc.org/journals/index.php/IJDRBC/article/view/35550.

Akter, S., Fosso Wamba, S., and Dewan, S. (2017). Why PLS-SEM Is Suitable for Complex Modelling? an Empirical Illustration in Big Data Analytics Quality. Prod. Plann. Control. 28 (11–12), 1011–1021. doi:10.1080/09537287.2016.1267411

Al-Ghwayeen, W. S., and Abdallah, A. B. (2018). Green Supply Chain Management and export Performance: The Mediating Role of Environmental Performance. J. Manufacturing Techn. Manage. 29 (7), 1233–1252. doi:10.1108/JMTM-03-2018-0079

Al-Sheyadi, A., Muyldermans, L., and Kauppi, K. (2019). The Complementarity of green Supply Chain Management Practices and the Impact on Environmental Performance. J. Environ. Manage. 242 (October 2018), 186–198. doi:10.1016/j.jenvman.2019.04.078

Ali, K., Bakhsh, S., Ullah, S., Ullah, A., and Ullah, S. (2021). Industrial Growth and CO2 Emissions in Vietnam: the Key Role of Financial Development and Fossil Fuel Consumption. Environ. Sci. Pollut. Res. 28 (6), 7515–7527. doi:10.1007/s11356-020-10996-6

Ali, Y., Saad, T. B., Sabir, M., Muhammad, N., Salman, A., and Zeb, K. (2020). Integration of green Supply Chain Management Practices in Construction Supply Chain of CPEC. Manage. Environ. Qual. Int. J. 31 (1), 185–200. doi:10.1108/MEQ-12-2018-0211

Asif, M. S., Lau, H., Nakandala, D., Fan, Y., and Hurriyet, H. (2020). Adoption of green Supply Chain Management Practices through Collaboration Approach in Developing Countries – from Literature Review to Conceptual Framework. J. Clean. Prod. 276, 124191. doi:10.1016/j.jclepro.2020.124191

Banasik, A., Kanellopoulos, A., Claassen, G. D. H., Bloemhof-Ruwaard, J. M., and van der Vorst, J. G. A. J. (2017). Assessing Alternative Production Options for Eco-Efficient Food Supply Chains Using Multi-Objective Optimization. Ann. Oper. Res. 250 (2), 341–362. doi:10.1007/s10479-016-2199-z

Barney, J. (1991). Firm Resources and Sustained Competitive Advantage. J. Manage. 17 (1), 99–120. doi:10.1177/014920639101700108

Bu, X., Dang, W. V., Wang, J., and Liu, Q. (2020). Environmental Orientation, Green Supply Chain Management, and Firm Performance: Empirical Evidence from Chinese Small and Medium-Sized Enterprises. Int. J. Environ. Res. Public Health 17 (4), 1199. doi:10.3390/ijerph17041199

Chan, H. K., He, H., and Wang, W. Y. C. (2012). Green Marketing and its Impact on Supply Chain Management in Industrial Markets. Ind. Marketing Manage. 41 (4), 557–562. doi:10.1016/j.indmarman.2012.04.002

Chin, T. A., Tat, H. H., and Sulaiman, Z. (2015). Green Supply Chain Management, Environmental Collaboration and Sustainability Performance’. Proced. CIRP 26, 695–699. doi:10.1016/j.procir.2014.07.035

Choi, S.-B., Min, H., and Joo, H.-Y. (2018). Examining the Inter-relationship Among Competitive Market Environments, green Supply Chain Practices, and Firm Performance. Int. J. Logistics Manage. 29 (3), 1025–1048. doi:10.1108/IJLM-02-2017-0050

Chu, S., Yang, H., Lee, M., and Park, S. (2017). The Impact of Institutional Pressures on Green Supply Chain Management and Firm Performance: Top Management Roles and Social Capital. Sustainability 9 (5), 764. doi:10.3390/su9050764

Dagar, V., Bhattacharjee, M., Ahmad, F., Pawariya, V., and Jit, P. (2020). Stochastic frontier analysis for measuring technical efficiency of neem coated urea : evidence from North India. Int. J. Agric. Stat. Sci. 16 (1), 361–371. doi:10.5281/ZENODO.4027114

Dagar, V., Khan, M. K., Alvarado, R., Rehman, A., Irfan, M., Adekoya, O. B., et al. (2022). Impact of Renewable Energy Consumption, Financial Development and Natural Resources on Environmental Degradation in OECD Countries with Dynamic Panel Data. Environ. Sci. Pollut. Res. 29 (12), 18202–18212. doi:10.1007/s11356-021-16861-4

Das, D. (2018). The Impact of Sustainable Supply Chain Management Practices on Firm Performance: Lessons from Indian Organizations. J. Clean. Prod. 203, 179–196. doi:10.1016/j.jclepro.2018.08.250

Dedoulis, E. (2016). Institutional Formations and the Anglo-Americanization of Local Auditing Practices: The Case of Greece. Account. Forum 40 (1), 29–44. doi:10.1016/j.accfor.2015.11.003

DiMaggio, P. J., and Powell, W. W. (1983). The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields. Am. Sociological Rev. 48 (2), 147. doi:10.2307/2095101

Esfahbodi, A., Zhang, Y., and Watson, G. (2016). Sustainable Supply Chain Management in Emerging Economies: Trade-Offs between Environmental and Cost Performance. Int. J. Prod. Econ. 181, 350–366. doi:10.1016/j.ijpe.2016.02.013

Esfahbodi, A., Zhang, Y., Watson, G., and Zhang, T. (2017). Governance Pressures and Performance Outcomes of Sustainable Supply Chain Management – an Empirical Analysis of UK Manufacturing Industry. J. Clean. Prod. 155, 66–78. doi:10.1016/j.jclepro.2016.07.098

Etikan, I. (2016). Comparison of Convenience Sampling and Purposive Sampling. Am. J. Theor. Appl. Stat. 5 (1), 1. doi:10.11648/j.ajtas.20160501.11

Feng, M., Yu, W., Wang, X., Wong, C. Y., Xu, M., and Xiao, Z. (2018). Green Supply Chain Management and Financial Performance: The Mediating Roles of Operational and Environmental Performance. Bus. Strategy Environ. 27 (7), 811–824. doi:10.1002/bse.2033

Flynn, B. B., Huo, B., and Zhao, X. (2010). The Impact of Supply Chain Integration on Performance: A Contingency and Configuration Approach. J. Operations Manage. 28 (1), 58–71. doi:10.1016/j.jom.2009.06.001

Geng, R., Mansouri, S. A., and Aktas, E. (2017). The Relationship between green Supply Chain Management and Performance: A Meta-Analysis of Empirical Evidences in Asian Emerging Economies. Int. J. Prod. Econ. 183, 245–258. doi:10.1016/j.ijpe.2016.10.008

Golicic, S. L., and Smith, C. D. (2013). A Meta-Analysis of Environmentally Sustainable Supply Chain Management Practices and Firm Performance. J. Supply Chain Manag. 49 (2), 78–95. doi:10.1111/jscm.12006

Gupta, A. K., and Gupta, N. (2021). Environment Practices Mediating the Environmental Compliance and Firm Performance: An Institutional Theory Perspective from Emerging Economies. Glob. J. Flex. Syst. Manag. 22 (3), 157–178. doi:10.1007/s40171-021-00266-w

Habib, M. A., Bao, Y., and Ilmudeen, A. (2020). The Impact of green Entrepreneurial Orientation, Market Orientation and green Supply Chain Management Practices on Sustainable Firm Performance. Cogent Business Manage. 7 (1), 1743616. doi:10.1080/23311975.2020.1743616

Hair, F., Matthews, L. M., Matthews, R. L., and Sarstedt, M. (2017). PLS-SEM or CB-SEM: Updated Guidelines on Which Method to Use. Int. J. Multivariate Data Anal. 1 (2), 107. doi:10.1504/IJMDA.2017.087624

Hair, J. F., Hult, T. M. J, Ringle, C. M, and Sarstedt, M (2014). A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). Thousand Oaks, CA: SAGE Publications. Available at: https://books.google.com.pk/books?id=IFiarYXE1PoC.

Hakeem, K. R., Akhtar, M. S., and Abdullah, S. N. A. (2016). Effects of pesticides on environment. Cham: Springer International Publishing, 253–269. doi:10.1007/978-3-319-27455-3_13

Helm, D. (2020). The Environmental Impacts of the Coronavirus. Environ. Resour. Econ. (Dordr). 76 (1), 21–38. doi:10.1007/s10640-020-00426-z

Henseler, J., Hubona, G., and Ray, P. A. (2016). Using PLS Path Modeling in New Technology Research: Updated Guidelines. Ind. Manage. Data Syst. 116 (1), 2–20. doi:10.1108/IMDS-09-2015-0382

Israel, G. (1992). Sampling the Evidence of Extension Program Impact. Program Evaluation and Organizational Development. Gainesville, FL: University of Florida. PEOD-5. Available at: https://www.psycholosphere.com/DeterminingsamplesizebyGlenIsrael.pdf.

Jianguo, D., Ali, K., Alnori, F., and Ullah, S. (2022). The Nexus of Financial Development, Technological Innovation, Institutional Quality, and Environmental Quality: Evidence from OECD Economies. Environ. Sci. Pollut. Res. Int. doi:10.1007/s11356-022-19763-1

Kalpande, S. D., and Toke, L. K. (2020). Assessment of green Supply Chain Management Practices, Performance, Pressure and Barriers Amongst Indian Manufacturer to Achieve Sustainable Development. Int. J. Productivity Perform. Manage. 70, 2237–2257. ahead-of-p(ahead-of-print). doi:10.1108/IJPPM-02-2020-0045

Kamasak, R. (2017). The Contribution of Tangible and Intangible Resources, and Capabilities to a Firm’s Profitability and Market Performance. Eur. J. Manage. Business Econ. 26 (2), 252–275. doi:10.1108/EJMBE-07-2017-015

Khan, M. K., Babar, S. F., Oryani, B., Dagar, V., Rehman, A., Zakari, A., et al. (2022). Role of Financial Development, Environmental-Related Technologies, Research and Development, Energy Intensity, Natural Resource Depletion, and Temperature in Sustainable Environment in Canada. Environ. Sci. Pollut. Res. 29 (1), 622–638. doi:10.1007/s11356-021-15421-0

Khan, M. T., Idrees, M. D., Rauf, M., Sami, A., Ansari, A., and Jamil, A. (2022). Green Supply Chain Management Practices’ Impact on Operational Performance with the Mediation of Technological Innovation. Sustainability 14 (6), 3362. doi:10.3390/su14063362

Khan, S. A. R. (2020). The Critical Success Factors of Green Supply Chain Management in Emerging Economies. Beijing, China: Springer International Publishing (EAI/Springer Innovations in Communication and Computing. doi:10.1007/978-3-030-42742-9

Kock, N. (2018). “Chapter 1 Minimum Sample Size Estimation in PLS-SEM: An Application in Tourism and Hospitality Research,” in Applying Partial Least Squares in Tourism and Hospitality Research (Emerald Publishing Limited), 1–16. doi:10.1108/978-1-78756-699-620181001

Kock, N., and Hadaya, P. (2018). Minimum Sample Size Estimation in PLS-SEM: The Inverse Square Root and Gamma-Exponential Methods. Info. Syst. J. 28 (1), 227–261. doi:10.1111/isj.12131

Kouser, S., Subhan, A., and Abedullah, A. (2020). Uncovering Pakistan’s Environmental Risks and Remedies under the China-Pakistan Economic Corridor. Environ. Sci. Pollut. Res. 27 (5), 4661–4663. doi:10.1007/s11356-019-07428-5

Liao, Z., and Zhang, M. (2020). The Influence of Responsible Leadership on Environmental Innovation and Environmental Performance: The Moderating Role of Managerial Discretion. Corp. Soc. Responsib. Environ. Manag. 27 (5), 2016–2027. doi:10.1002/csr.1942

Luo, R., Ullah, S., and Ali, K. (2021). Pathway towards Sustainability in Selected Asian Countries: Influence of Green Investment, Technology Innovations, and Economic Growth on CO2 Emission. Sustainability 13 (22), 12873. doi:10.3390/su132212873

Marhamati, A., and Azizi, I. (2017). The Impact of Green Supply Chain Management on Firm’s Performance. Int. J. Supply Chain Manage., 9. Available at: http://excelingtech.co.uk/.

Marri, M. Y. K., Sarwat, N., and Aqdas, R. (2021). Exploring the Nexus Among Green Supply Chain Management, Environmental Management, and Sustainable Performance: The Mediating Role of Environmental Management. J. Contemp. Issues Business Government 27 (02). doi:10.47750/cibg.2021.27.02.201

Maurischat, C. (2006). [Exploratory and Confirmatory Factor Analysis]. Rehabilitation 45 (4), 243–248. doi:10.1055/s-2006-940029

Memon, M. A., Ting, H., Cheah, J. H., Thurasamy, R., Chuah, F., and Cham, T. H. (2020) ‘Sample Size for Survey Research: Review and Recommendations’, J. Appl. Struct. Equation Model., 4(2), pp. i, xx, –xx. doi:10.47263/JASEM.4(2)01

Ming Heng, Y., Zakiyuddin Ahmad Rashid, Z., and Riazi Mehdi Riazi, S. (2018). Significance of Regulations in Driving Internal Environmental Management Among Contractors for GSCM Application. Int. J. Eng. Technol. 7 (438), 1025. doi:10.14419/ijet.v7i4.38.27632

Mitra, S., and Datta, P. P. (2014). Adoption of green Supply Chain Management Practices and Their Impact on Performance: an Exploratory Study of Indian Manufacturing Firms. Int. J. Prod. Res. 52 (7), 2085–2107. doi:10.1080/00207543.2013.849014

Murshed, M., Rahman, M. A., Alam, M. S., Ahmad, P., and Dagar, V. (2021). The Nexus between Environmental Regulations, Economic Growth, and Environmental Sustainability: Linking Environmental Patents to Ecological Footprint Reduction in South Asia. Environ. Sci. Pollut. Res. 28 (36), 49967–49988. doi:10.1007/s11356-021-13381-z

Nadeem, M., Lou, S., Wang, Z., Sami, U., Ali, S. A., Abbas, Q., et al. (2022). Efficiency of Domestic Institutional Arrangements for Environmental Sustainability along the Way to Participate in Global Value Chains: Evidence from Asia. Econ. Research-Ekonomska Istraživanja 0 (0), 1–20. doi:10.1080/1331677X.2022.2077793

Phan, T. N., and Baird, K. (2015). The Comprehensiveness of Environmental Management Systems: The Influence of Institutional Pressures and the Impact on Environmental Performance. J. Environ. Manage. 160, 45–56. doi:10.1016/j.jenvman.2015.06.006

Pinto, L. (2020). Green Supply Chain Practices and Company Performance in Portuguese Manufacturing Sector. Bus. Strategy Environ. 29 (5), 1832–1849. doi:10.1002/bse.2471

Rehman, A., Radulescu, M., Ma, H., Dagar, V., Hussain, I., and Khan, M. (2021). The Impact of Globalization, Energy Use, and Trade on Ecological Footprint in Pakistan: Does Environmental Sustainability Exist? Energies 14 (17), 5234. doi:10.3390/en14175234

Ringle, C. M., Wende, S., and Becker, J.-M. (2015). ‘SmartPLS 3’. Boenningstedt: SmartPLS GmbH. Available at: http://www.smartpls.com.

Saeed, A., Jun, Y., Nubuor, S., Priyankara, H., and Jayasuriya, M. (2018). Institutional Pressures, Green Supply Chain Management Practices on Environmental and Economic Performance: A Two Theory View. Sustainability 10 (5), 1517. doi:10.3390/su10051517

Schmidt, C. G., Foerstl, K., and Schaltenbrand, B. (2017). The Supply Chain Position Paradox: Green Practices and Firm Performance. J. Supply Chain Manag. 53 (1), 3–25. doi:10.1111/jscm.12113

Shafique, M., Asghar, M., and Rahman, H. (2017). The Impact of Green Supply Chain Management Practices on Performance: Moderating Role of Institutional Pressure with Mediating Effect of Green Innovation. Business, Manage. Educ. 15 (1), 91–108. doi:10.3846/bme.2017.354

Shahzad, U., Madaleno, M., Dagar, V., Ghosh, S., and Dogan, B. (2022). Exploring the Role of export Product Quality and Economic Complexity for Economic Progress of Developed Economies: Does Institutional Quality Matter? Struct. Change Econ. Dyn. 62, 40–51. doi:10.1016/j.strueco.2022.04.003

Siddiqui, M. I. A., and Siddiqui, D. A. (2020). Impact of Green Supply Chain Management on Economic and Organizational Performance of Food Industry in Sindh and Punjab. cenraps 2 (3), 439–455. doi:10.46291/cenraps.v2i3.42

Singh, A. S., and Masuku, M. B. (2014). Sampling Techniques & Determination of Sampel Size in Applied Statistics Reseaech: An Overview, United Kingdom. Internatioonal J. Econ. Commerce Manageemnt II (11), 22. Available at: http://ijecm.co.uk/.

Taherdoost, H. (2016). Sampling Methods in Research Methodology; How to Choose a Sampling Technique for Research. SSRN J. 5 (2), 18–27. doi:10.2139/ssrn.3205035

Tang, S., Wang, Z., Yang, G., and Tang, W. (2020). What Are the Implications of Globalization on Sustainability?-A Comprehensive Study. Sustainability (Switzerland) 12 (8), 3411. doi:10.3390/SU12083411

Touboulic, A., and Walker, H. (2015). “Theories in Sustainable Supply Chain Management: a Structured Literature Review,” in International Journal of Physical Distribution & Logistics Management. Editors P. Maria Jesus Saenz, and D. Xenophon Koufteros, 1/2, 45, 16–42. doi:10.1108/IJPDLM-05-2013-0106

Tseng, M.-L., Islam, M. S., Karia, N., Fauzi, F. A., and Afrin, S. (2019). A Literature Review on green Supply Chain Management: Trends and Future Challenges. Resour. Conservation Recycling 141 (October 2018), 145–162. doi:10.1016/j.resconrec.2018.10.009

Ullah, S., Ali, K., Shah, S. A., and Ehsan, M. (2022). Environmental Concerns of Financial Inclusion and Economic Policy Uncertainty in the Era of Globalization: Evidence from Low & High Globalized OECD Economies. Environ. Sci. Pollut. Res. 29 (24), 36773–36787. doi:10.1007/s11356-022-18758-2

Ullah, S., Nadeem, M., Ali, K., and Abbas, Q. (2022). Fossil Fuel, Industrial Growth and Inward FDI Impact on CO2 Emissions in Vietnam: Testing the EKC Hypothesis. Manage. Environ. Qual. Int. J. 33 (2), 222–240. doi:10.1108/MEQ-03-2021-0051

Vanalle, R. M., Ganga, G. M. D., Godinho Filho, M., and Lucato, W. C. (2017). Green Supply Chain Management: An Investigation of Pressures, Practices, and Performance within the Brazilian Automotive Supply Chain. J. Clean. Prod. 151, 250–259. doi:10.1016/j.jclepro.2017.03.066

Vitorino Filho, V. A., and Moori, R. G. (2020). RBV in a Context of Supply Chain Management. Gest. Prod. 27 (4), 1–20. doi:10.1590/0104-530x4731-20

Wei, R., Ayub, B., and Dagar, V. (2022). Environmental Benefits from Carbon Tax in the Chinese Carbon Market: A Roadmap to Energy Efficiency in the Post-COVID-19 Era. Front. Energ. Res. 10. doi:10.3389/fenrg.2022.832578

Weimin, Z., Sibt-e-Ali, M., Tariq, M., Dagar, V., and Khan, M. K. (2022). Globalization toward Environmental Sustainability and Electricity Consumption to Environmental Degradation: Does EKC Inverted U-Shaped Hypothesis Exist between Squared Economic Growth and CO2 Emissions in Top Globalized Economies. Environ. Sci. Pollut. Res. Int. doi:10.1007/s11356-022-20192-3

Xiang, H., Chau, K. Y., Iqbal, W., Irfan, M., and Dagar, V. (2022). Determinants of Social Commerce Usage and Online Impulse Purchase: Implications for Business and Digital Revolution. Front. Psychol. 13, 837042. doi:10.3389/fpsyg.2022.837042

Xie, M., Irfan, M., Razzaq, A., and Dagar, V. (2022). Forest and mineral Volatility and Economic Performance: Evidence from Frequency Domain Causality Approach for Global Data. Resour. Pol. 76, 102685. doi:10.1016/j.resourpol.2022.102685

Yang, C. S. (2018). An Analysis of Institutional Pressures, green Supply Chain Management, and green Performance in the Container Shipping Context. Transport. Res. Part D Transport Environ. 61, 246–260. doi:10.1016/j.trd.2017.07.005

Yar, P., Khan, S., Ying, D., and Israr, M. (2021). Understanding CPEC’s Role in Agriculture Sector Development in Pakistan: Issues and Opportunities. Sarhad J. Agric. 37 (4). doi:10.17582/journal.sja/2021/37.4.1211.1221

Yildiz Çankaya, S., and Sezen, B. (2019). Effects of green Supply Chain Management Practices on Sustainability Performance. J. Manufacturing Techn. Manage. 30 (1), 98–121. doi:10.1108/JMTM-03-2018-0099

Yook, K. H., Choi, J. H., and Suresh, N. C. (2018). Linking green Purchasing Capabilities to Environmental and Economic Performance: The Moderating Role of Firm Size. J. Purchasing Supply Manage. 24 (4), 326–337. doi:10.1016/j.pursup.2017.09.001

Zaid, A. A., Bon, A. T., and Jaaron, A. A. M. (2019). The Impact of Implementing External and Internal GSCM Practices on Organizational Performance: Evidence from Manufacturing Firms in Palestine. Int. J. Recent Techn. Eng. 8 (2S7), 62–70. doi:10.35940/ijrte.B1013.0782S719

Zailani, S., Jeyaraman, K., Vengadasan, G., and Premkumar, R. (2012). Sustainable Supply Chain Management (SSCM) in Malaysia: A Survey. Int. J. Prod. Econ. 140 (1), 330–340. doi:10.1016/j.ijpe.2012.02.008

Zelazna, A., Bojar, M., and Bojar, E. (2020). Corporate Social Responsibility towards the Environment in Lublin Region, Poland: A Comparative Study of 2009 and 2019. Sustainability (Switzerland) 12 (11), 4463. doi:10.3390/su12114463

Zhang, C., Khan, I., Dagar, V., Saeed, A., and Zafar, M. W. (2022). Environmental Impact of Information and Communication Technology: Unveiling the Role of Education in Developing Countries. Technol. Forecast. Soc. Change 178, 121570. doi:10.1016/j.techfore.2022.121570

Zhang, J., Zhang, X., Wang, Q., and Ma, Z. (2020). “Relationship between institutional pressures, green supply chain management practices and business performance: an empirical research on automobile industry,” in Advances in intelligent systems and computing (Cham: Springer International Publishing), 430–449. doi:10.1007/978-3-030-21255-1_33

Zhu, Q., Sarkis, J., and Lai, K. (2019). Choosing the Right Approach to green Your Supply Chains. Mod. Supply Chain Res. Appl. 1 (1), 54–67. doi:10.1108/mscra-02-2019-0006

Keywords: green supply chain management, institutional pressures, environmental performance, financial performance, pesticide firms

Citation: Ma X, Akhtar R, Akhtar A, Hashim RA and Sibt-e-Ali M (2022) Mediation effect of environmental performance in the relationship between green supply chain management practices, institutional pressures, and financial performance. Front. Environ. Sci. 10:972555. doi: 10.3389/fenvs.2022.972555

Received: 18 June 2022; Accepted: 04 July 2022;

Published: 04 August 2022.

Edited by:

Vishal Dagar, Great Lakes Institute of Management, IndiaReviewed by:

Ali Junaid Khan, Islamia University of Bahawalpur, PakistanCopyright © 2022 Ma, Akhtar, Akhtar, Hashim and Sibt-e-Ali. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Raheel Akhtar, bWlhbnJhaGVlbDE5QGdtYWlsLmNvbQ==; Adeel Akhtar, YWRlZWwuYWtodGFyQGJ6dS5lZHUucGs=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.