Guifu Chen

Guifu Chen Boyu Wei

Boyu Wei Ruoran Zhu

Ruoran Zhu

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 29 September 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.972328

This article is part of the Research Topic ESG Investment and Its Societal Impacts View all 28 articles

Corporate environmental responsibility (CER) has become a critical factor for measuring the competitiveness of firms in China, and environmental subsidies may be a catalyst for promoting firms’ CER. This study uses data from Chinese A-share listed firms during 2010–2020. Using the instrumental variable two-stage least squares (IV-2SLS) method, we found that environmental subsidies significantly improve corporate environmental performance but have no significant impact on the disclosure and governance of pollution emissions. We find that environmental subsidies are better for chemical and energy firms with high pollution levels, provide incentives for non-state-owned firms to improve CER and that their effect in western and eastern China is better than that in the central region. We also found that corporate social responsibility plays a moderating role in environmental subsidies that affect CER. Finally, this study finds that environmental subsidies may crowd out corporate investments to improve environmental performance. Based on the above results, we provide the corresponding policy suggestions.

China’s economic development model has shifted from rapid growth to high-quality growth. According to the World Development Indicators (2022), China’s GDP growth rate has gradually slowed since 2010. The growth rates of total and per capita carbon emissions have also decreased (World Development Indicator, 2022). However, serious environmental pollution caused by China’s rapid economic growth in the past, especially a series of “high pollution-high energy consumption-high emissions” during industrial development, has not been solved (Hanlon, 2020). Environmental issues have attracted considerable attention in recent years. In 2015, the Fifth Plenary Session of the 18th Central Committee of the Communist Party of China incorporated the construction of ecological civilization into the 13th Five-Year Plan. The concept of green development was considered essential to China’s economic development. The Ministry of Finance of China promulgated interim measures to manage energy conservation and emission reduction subsidy funds in 2015. In 2020, the Ministry of Finance revised the Interim Measures for the Management of Energy Conservation and Emission Reduction Subsidy Funds, added a performance management mechanism for energy conservation and emission reduction subsidy funds, and monitored the performance of firms applying for subsidies. Firms should also provide performance information and openly and actively accept social supervision. The continuous implementation of these regulations shows that government environmental subsidies have established a standardized mechanism in China.

From a micro perspective, corporate environmental responsibility (CER) and positive environmental, social responsibility, and corporate governance (ESG) information disclosure can show firms’ self-regulatory ability and business operations. This can help attract investment and achieve long-term development goals (Dyck et al., 2019). Firms that lack humanistic care and environmental governance are less attractive to consumers, whereas firms with better environmental performance are more competitive (Wenqi et al., 2022). However, the negative externalities of environmental pollution cause firms to lack the motivation to improve their green social responsibility. As an economic instrument, government environmental subsidies can internalize the positive externalities of firms to improve their environmental performance. These subsidies are compatible with firm incentives compared with administrative instruments and can improve firms’ environmental responsibility (Shi et al., 2015). In China, CER is different from other forms of social responsibility because environmental protection is a public management function of the government and is related to government officials’ performance and political promotion. Therefore, the Chinese government’s CER participation is higher than in other countries (Wang et al., 2020). Compared to Western countries, Chinese firms improve environmental responsibility to obtain government support, and the government can also benefit from improving environmental responsibility (Lee et al., 2017). Environmental subsidies, taxes, and regulations are government policy tools for improving the environment. Some studies have discussed the relationship between environmental subsidies and China’s CER (Lee et al., 2017; Qi et al., 2021; Wenqi et al., 2022).

This study obtains data for 2010–2020 for listed firms in China from the China Stock Market and Accounting Research (CSMAR) database and concludes similar to those in the existing literature. Based on this, we expand our empirical research. First, we introduce the two-stage least squares regression method of instrumental variables (IV-2SLS) to overcome endogeneity. Specifically, we consider a firm’s industry average environmental subsidy ratio (IV). Second, we distinguish between industries and state-owned or non-state-owned firms and find that environmental subsidies significantly improve CER in manufacturing and non-state-owned firms. Third, corporate social responsibility (CSR) plays a regulatory role. The higher the level of social responsibility, the more likely it is to use environmental subsidies to improve CER performance. Finally, we discuss the mediating mechanism of research and development (R&D) input. A mediating mechanism cannot exist, but we find that environmental subsidies may crowd out private R&D inputs. After summarizing the above findings, this study provides policy suggestions.

CER refers to corporate responsibility for sustainable development (Wang et al., 2020). CER is a corporate social responsibility (CSR) branch, but CERs gradually separate from CSR to become independent concepts (Timpere, 2008). Fulfilling environmental responsibilities requires firms to pay additional costs and reduce their profits (Ganescu and Dindire, 2014). However, firms still have incentives to increase their investment in environmental research and improve their environmental performance. In recent years, consumers’ willingness to pay for green products has gradually increased, and firms have to respond promptly (DesJardins, 1998). Many factors affect firms’ environmental responsibility levels. First, firms of different sizes face varying environmental responsibility constraints. Larger firms usually have higher public awareness, leading to greater public and regulatory pressure; thus, they are more inclined to disclose CER information. They also have better management organizations and a stronger ability to deal with environmental responsibility issues (Brammer and Millington, 2006).

There is scant literature on the relationship between firm age and CER. Yang, (2009) found that the longer a firm’s business life, the more conducive it is to establishing a broad social network and a stable image of social responsibility, reducing information asymmetry between firms and investors. CER is also related to the corporate financial situation. Well-funded firms are willing to disclose CER-related information to attract more external investments and ensure that the firm is not undervalued (Chen and Hamilton, 2020). Specifically, some studies show a positive correlation between firms’ financial leverage and CER (Dimitropoulos and Koronios, 2021). However, some studies propose the opposite view that high financial leverage will become a burden on environmental investment (Meng et al., 2016). Another critical financial indicator affecting CER is a firm’s growth capacity. CER information disclosure can show external investors the sustainable development ability and prove their profitability and development prospects to improve access to financing (Crisóstomo et al., 2019). However, some studies find a negative correlation between financial performance and CER. Corporate executives and managers are more willing to invest in projects with higher short-term returns than in CER (Farag et al., 2015). Other studies show that companies with poor financial performance may disclose more CSR information and hide their poor financial performance, resulting in a negative correlation between financial performance and CER disclosure (Li et al., 2004). Although there are some differences in the current research on the influencing factors of CERs, it can be considered that corporate characteristics have a decisive impact on CER; therefore, we select the control variables for regression analysis based on the above research.

Subsidies are an effective way to solve externalities (Fogarty and Sagerer, 2016). Existing literature focuses on government subsidies, whereas there are few documents on the economic benefits of environmental subsidies. Environmental subsidies encourage firms to adopt clean technologies, implement energy conservation and emission reduction strategies, and innovate green technologies (Bai et al., 2018). As a policy tool opposed to environmental taxes, although environmental subsidies are less effective than environmental taxes in the short term, they can internalize the external economy in the long run (Li et al., 2004). The government can provide financial resources to ease financing constraints through environmental subsidies, and sufficient funds are invested in CER (Wu, 2019). Whether environmental subsidies or taxes are compatible with incentives, firms may still have room to allocate resources reasonably under the existing subsidies and tax frameworks. In administrative terms, the interests of governments and firms may be inconsistent, and firms’ actions may not maximize social welfare (Shi et al., 2015). In addition, government environmental subsidies can signal to the market that subsidized firms have been recognized by the government, conducive for firms to compete for resources to improve their CERs (Wei and Zuo, 2018).

Zhang et al. (2014) studied the role of subsidies in China’s renewable energy industry and found that government subsidies have increased the overall performance of renewable energy companies. However, the relationship between business executives and the government may weaken the role of subsidies. Therefore, we believe that environmental subsidies positively affect CER. However, some studies have proposed the opposite view, that subsidies are not conducive to improving CER performance. After receiving subsidies, firms may increase their dependence on subsidies and lack the motivation to actively use idle resources to improve CERs (Jia et al., 2021). Rent-seeking may also lead firms to reallocate resources to seek government support, negatively impacting environmental performance (Nilsson, 2017). To ensure future subsidies, firms prioritize R&D research projects that can produce results, leading to improper resource allocation and neglecting clean technologies conducive to improving CER performance (Hall and Harhoff, 2012). The above literature indicates that the relationship between environmental subsidies and CER performance may be more complex. Given China’s industrial transformation and upgradation, it is necessary to examine the heterogeneity of environmental subsidies in different industries and property rights. In addition, it is crucial to investigate the theoretical path through which environmental subsidies affect the CER. Therefore, we also check for a mediating effect between environmental subsidies and private R&D investments.

Sample data were obtained from the CSMAR database. Finally, this study determines the sample range of Chinese A-share listed firms during 2010–2020. All nominal variables in this study were reduced to 2010 as the base period. In addition, we winsorized all the variables at the 1% level to reduce the impact of extreme values. Referring to the model settings discussed (Ren et al., 2021; Wang et al., 2021), we used the following measurement model in the regression analysis:

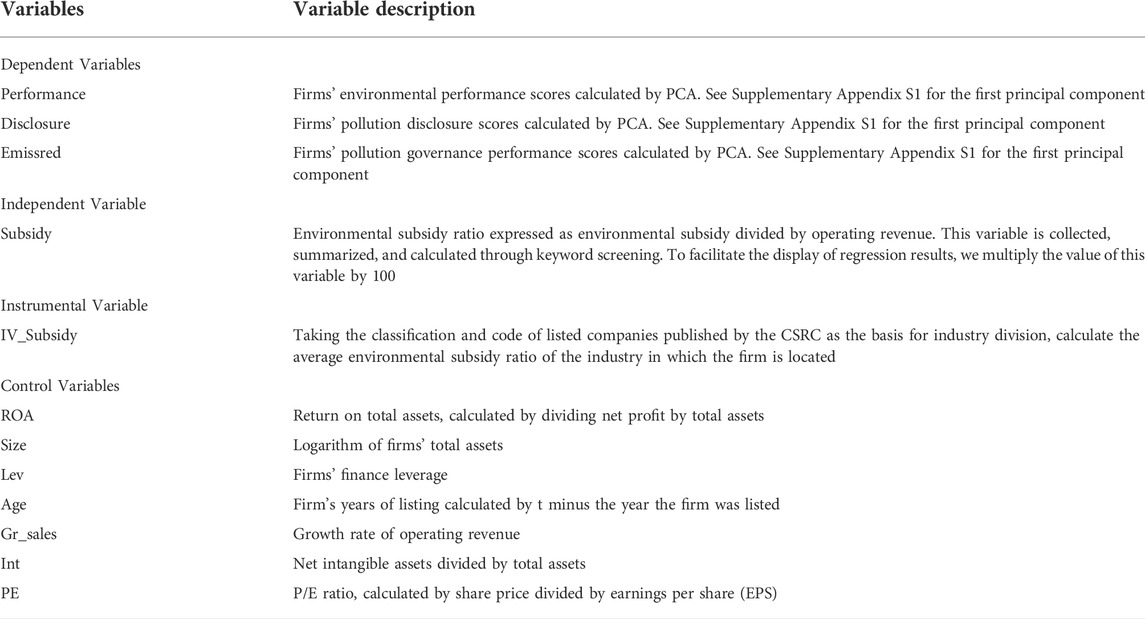

TABLE 1. Variable description.

The environmental protection decisions of listed firms may reflect and affect the trend of environmental protection and impact government policies. Both backward causality and sample selection biases exist. An effective treatment method is the use of IV to overcome the endogeneity problem. Therefore, the IV-2SLS method was used in these regression analyses. IV is the average of

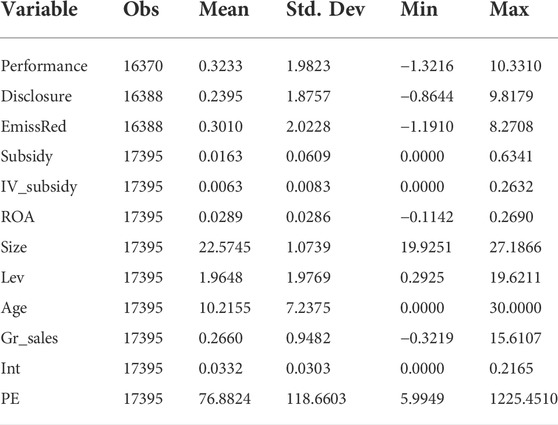

TABLE 2. Descriptive statistics

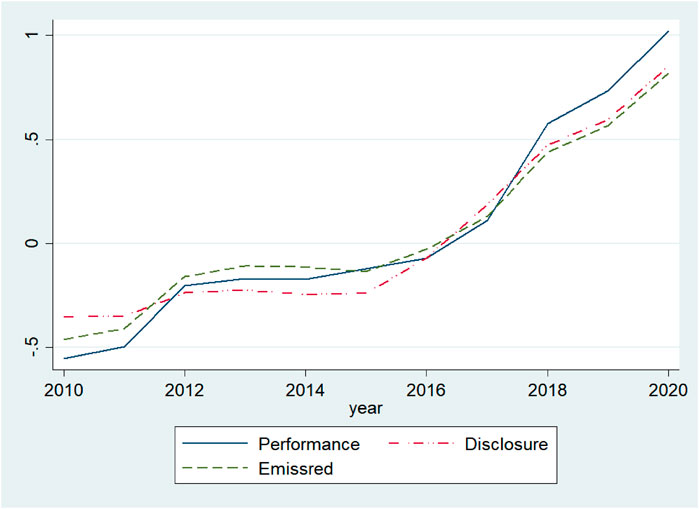

FIGURE 1. Time trend of the dependent variables.

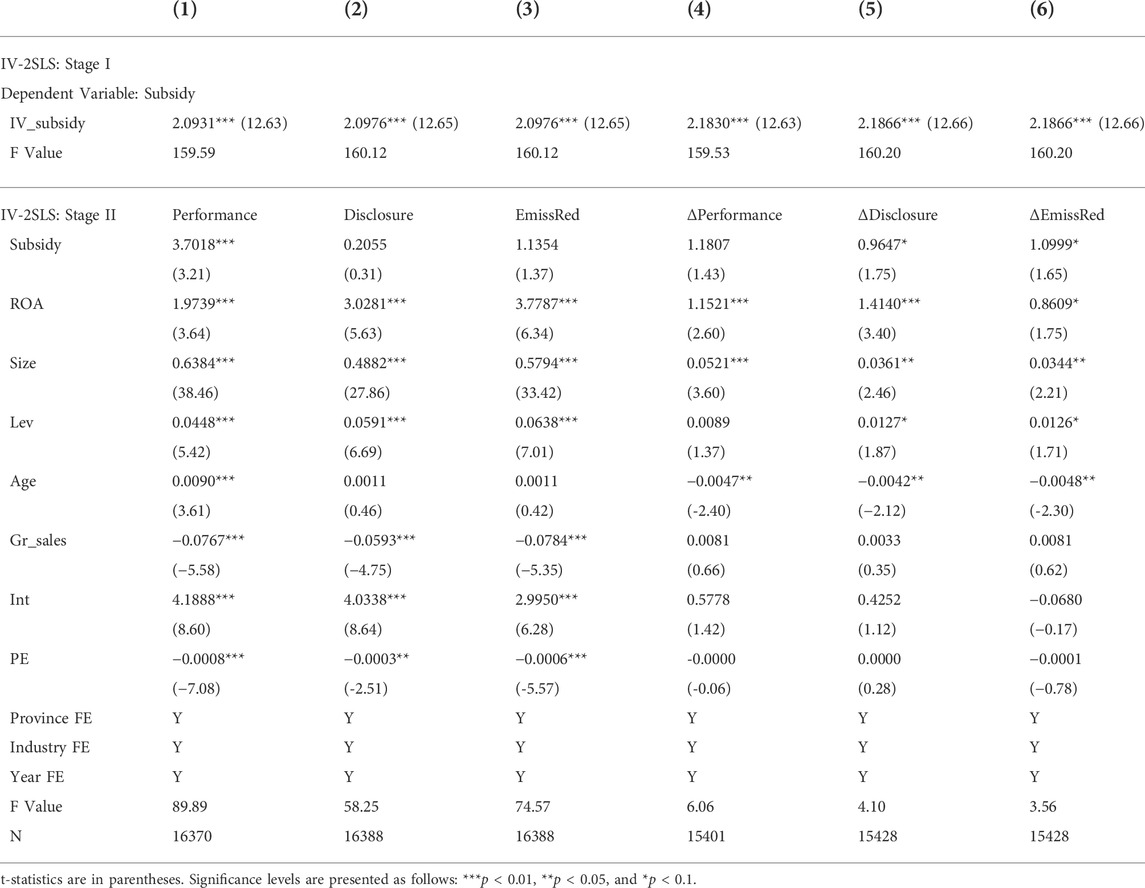

Table 3 shows the regression results for the IV-2SLS. Columns 1–3 show the regression results for the dependent variables of environmental performance, emission disclosure, and governance. The dependent variables in Columns 4–6 represent the first-order differences between the above three variables. According to the regression results of the first-stage IV regression in Table 3, the coefficients of

TABLE 3. Results of IV-2SLS regression

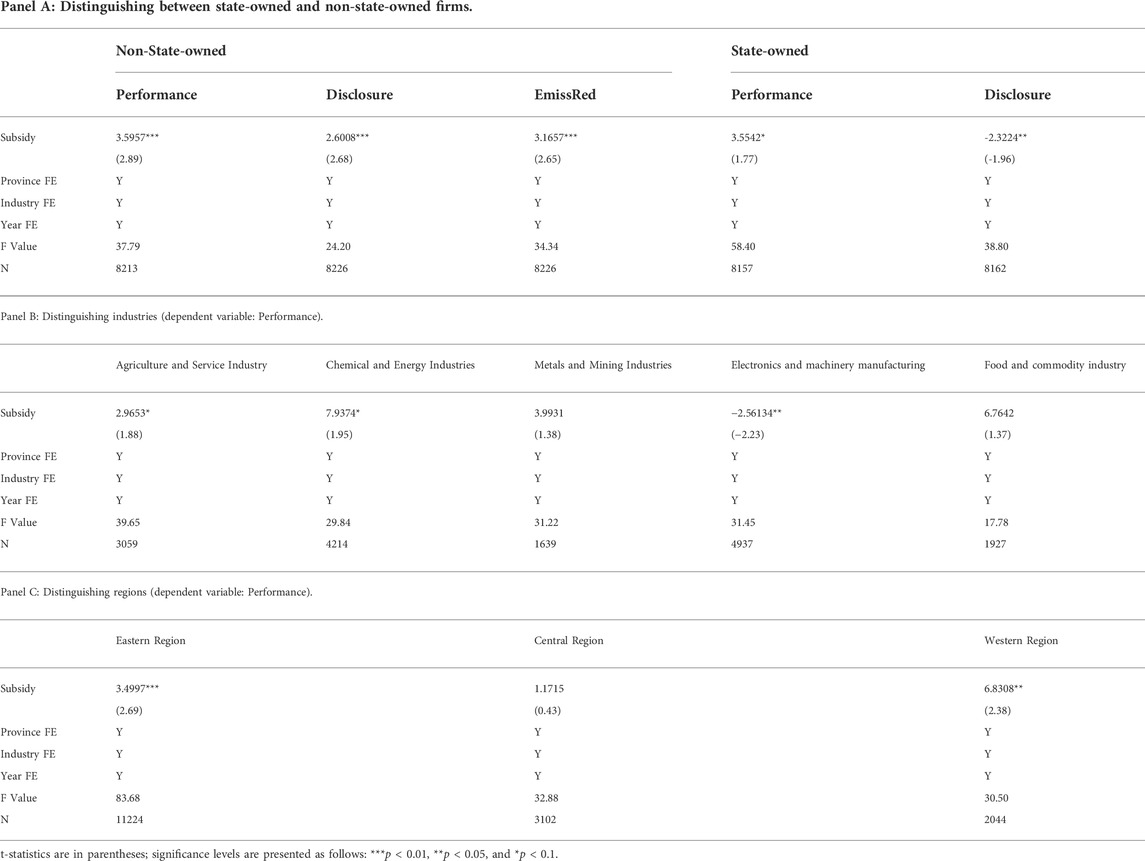

This study conducted a subsample regression considering the large heterogeneity of firms in the sample. We adopt two classification bases to distinguish between industries and property rights: state-owned and non-state-owned. In Panel A, we regress according to the sample of state-owned and non-state-owned firms, and the classification is based on the list of state-owned listed firms provided by CSMAR. Although the CER level of Chinese firms is significantly higher than that of non-state-owned firms, the regression results show that environmental subsidies have a stronger incentive to improve the CER of non-state-owned firms, consistent with Lee et al. (2017). For state-owned firms, the coefficient of Subsidy is less significant. When disclosure is the dependent variable, the coefficient is significantly negative. Owing to the natural political ties from state-owned equity, state-owned firms can obtain more long-term debt financing and policy preferences. Non-state-owned firms are more likely to cater to policies and adopt corresponding political strategies (Zhang and Zhang, 2005). Therefore, non-state-owned firms are more likely to use government subsidies to improve CER performance. Panel B in Table 4 presents the regression results for distinguishing industries according to the classifications and codes of listed companies. Notably, the regression coefficients of the different subsamples are not comparable due to different samples. However, environmental subsidies had a higher regression coefficient for chemical and energy industries, agriculture, and services. In contrast, the regression coefficients of firms in the food and commodity industries, metals, and mining industries were not significant. The coefficient of the electronics and machinery manufacturing industry is significantly negative. Therefore, we believe that because firms in the chemical and energy industries have relatively higher pollution levels and greater environmental governance pressure, environmental subsidies incentivize such firms to improve their CER. Finally, in Panel C, we conduct a subsample regression according to the regional division criteria of Eastern, Central, and Western China provided by the National Development and Reform Commission. The results indicate that environmental subsidies play a more significant role in the eastern region. They effectively improve the environmental performance of enterprises in Western China, but the effect of environmental subsidies in Central China is not significant.

TABLE 4. Sub-sample regression

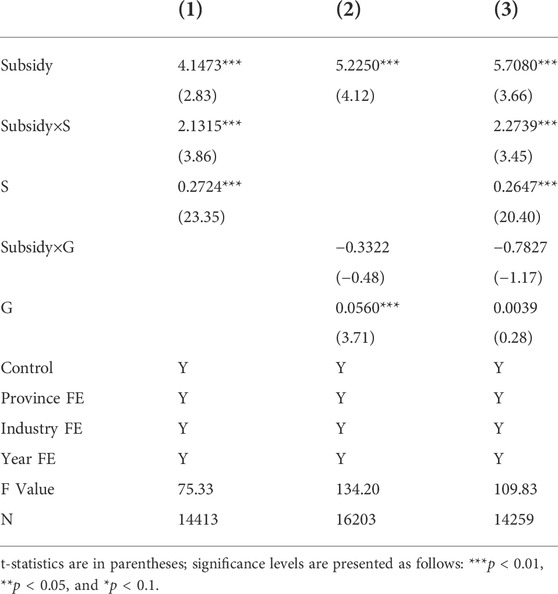

CSR may be related to entrepreneurship, and responsible entrepreneurs are more willing to actively implement technological innovation, achieve green development, and fulfill social and environmental responsibilities (Chen et al., 2021). Some studies illustrate the relationship between corporate governance structures and CSR or the sustainability of firm development (Aras and Crowther, 2009; Wang, 2016). Referring to Qiu and Yin (2019), this study calculates firms’ social responsibility and corporate governance scores using the CSMAR database and PCA, which are represented as

TABLE 5. Moderating effect (dependent variable: Performance)

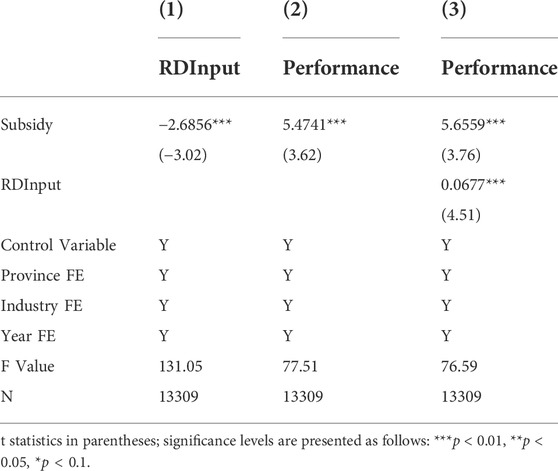

As environmental R&D investment can improve CER performance, we speculate a mediating mechanism between environmental subsidies and environmental R&D investment. After collecting the R&D input data of each firm and taking logarithmic processing after flattening in 2010, this study determines the mediating mechanism of R&D investment through a step-by-step regression method. Based on the regression results in Table 6, we find that the regression coefficient of environmental subsidies for R&D inputs in Column 1 is significantly negative, the coefficients of R&D inputs and environmental subsidies in Column 3 are significantly positive, and the coefficients of Subsidy in Column 3 are larger than those in Column 2. As the direct effect (i.e., the coefficient of

TABLE 6. Mechanism analysis.

China is in a transition period of industrial structure optimization and upgradation, and improving the performance of CER is a challenge for Chinese firms in the transformation process. To reasonably guide firms to optimize resource allocation and use idle resources, a series of economic means, represented by environmental subsidies and taxes, have entered the public view and play an important role. Based on the background of the gradual improvement of China’s environmental subsidy system and the rising social influence of the CER concept, this study collected samples of listed firms in China from 2010 to 2020 using the CSMAR database. Through IV-2SLS regression, this study examines whether environmental subsidies have a significant positive effect on CER. We found that significantly increasing environmental subsidies has indeed improved the performance of firms in CERs, but it has no significant impact on pollution emissions and controls. In the analysis, we distinguish between industries and property rights. Environmental subsidies can play a critical role in the more seriously polluting chemical and energy industries and non-state-owned firms with greater survival pressure. The effect of environmental subsidies in western and eastern China is significant but not in the central region. We also find that a firm’s sense of social responsibility can play a moderating role in the path of environmental subsidies to improve CER performance. Finally, through mechanism analysis, we find a crowding-out effect between environmental subsidies and private R&D investment.

The empirical results can provide policy guidance. When formulating an environmental subsidy mechanism, the government must follow the principle of adapting to local conditions. Simultaneously, policymakers can further strengthen the supervision of corporate behavior by the public and media to play a coupling effect with environmental policies and promote firms to improve environmental performance. Finally, the government should actively promote the diversification of environmental subsidy mechanisms to ensure that subsidies and environmental R&D investments have complementary effects. The limitations of this study are as follows. Due to the lack of data related to environmental subsidies and environmental performance, more sample sizes have been lost, so there will be certain errors in estimating the effect of environmental subsidies on Chinese listed firms. However, there is still room for improvement in this study’s calculation method for the CER performance. However, there are few indicators related to the environmental behavior of Chinese firms in the existing database, and there is no agreement on the estimation of CER performance in empirical studies. With the deepening of the concept of CER and the improvement of the relevant database, the measurement dimensions of CER will be further expanded.

Publicly available datasets were analyzed in this study. This data can be found here: The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

GC conceived and designed the research method; RZ conceived and designed the research method with GC and provided financial support; BW analyzed the data, wrote, and finalized the manuscript. All authors have read and agreed to the published version of the manuscript.

This work was supported by the 2021 Undergraduate Education and Teaching Reform Research Project of Fujian Province (grant no. FBJG20210010) and the Key Research Institutes of Humanities and Social Sciences of the Ministry of Education of China (Grant No. 17JJD790014). The remaining errors were our own.

The authors thank the editors, two anonymous reviewers for their helpful comments and suggestions for improving this paper, and Jiajun Yuan for providing lab support.

The authors declare that this research was conducted without any commercial or financial relationships construed as potential conflicts of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2022.972328/full#supplementary-material

Aras, G., and Crowther, D. (2009). Corporate sustainability reporting: A study in disingenuity? J. Bus. Ethics 87, 279–288. doi:10.1007/s10551-008-9806-0

Bai, Y., Hua, C., Jiao, J., Yang, M., and Li, F. (2018). Green efficiency and environmental subsidy: Evidence from thermal power firms in China. J. Clean. Prod. 188, 49–61. doi:10.1016/j.jclepro.2018.03.312

Brammer, S., and Millington, A. (2006). Firm size, organizational visibility and corporate philanthropy: An empirical analysis. Bus. Ethics. 15, 6–18. doi:10.1111/j.1467-8608.2006.00424.x

Chen, G., Wei, B., and Dai, L. (2022). Can ESG-responsible investing attract sovereign wealth funds’ investments? Evidence from Chinese listed firms. Front. Environ. Sci. 10. doi:10.3389/fenvs.2022.935466

Chen, S., Chen, Y., and Jebran, K. (2021). Trust and corporate social responsibility: From expected utility and social normative perspective. J. Bus. Res. 134, 518–530. doi:10.1016/j.jbusres.2021.05.045

Chen, Z., and Hamilton, T. (2020). What is driving corporate social and environmental responsibility in China? An evaluation of legacy effects, organizational characteristics, and transnational pressures. Geoforum 110, 116–124. doi:10.1016/j.geoforum.2020.02.004

Crisóstomo, V. L., de Souza Freire, F., and de Oliveira Freitas, M. F. (2019). Determinants of corporate sustainability performance: Evidence from Brazilian panel data. SRJ 16, 1053–1072. doi:10.1108/SRJ-04-2018-0102

DesJardins, J. (1998). Corporate environmental responsibility. J. Bus. Ethics 17, 825–838. doi:10.1023/A:1005719707880

Dimitropoulos, P., and Koronios, K. (2021). Literature review on corporate environmental responsibility. Cham: Springer International Publishing. doi:10.1007/978-3-030-72773-4_3

Dyck, A., Lins, K. V., Roth, L., and Wagner, H. F. (2019). Do institutional investors drive corporate social responsibility? International evidence. J. Financ. Econ. 131, 693–714. doi:10.1016/j.jfineco.2018.08.013

Farag, H., Meng, Q., and Mallin, C. (2015). The social, environmental and ethical performance of Chinese companies: Evidence from the shanghai stock exchange. Int. Rev. Financial Analysis 42, 53–63. doi:10.1016/j.irfa.2014.12.002

Fogarty, J. J., and Sagerer, S. (2016). Exploration externalities and government subsidies: The return to government. Resour. Policy 47, 78–86. doi:10.1016/j.resourpol.2016.01.002

Ganescu, C., and Dindire, L. (2014). Corporate environmental responsibility – A key determinant of corporate reputation. Comp. Methods Soc. Sci. 2, 48.

Hall, B. H., and Harhoff, D. (2012). Recent research on the economics of patents. Annu. Rev. Econ. 4, 541–565. doi:10.1146/annurev-economics-080511-111008

Hanlon, W. W. (2020). Coal smoke, city growth, and the costs of the Industrial Revolution. Econ. J. 130, 462–488. doi:10.1093/ej/uez055

Jia, L., Nam, E., and Chun, D. (2021). Impact of Chinese government subsidies on enterprise innovation: Based on a three-dimensional perspective. Sustainability 13, 1288. doi:10.3390/su13031288

Lee, E., Walker, M., and Zeng, C. (2017). Do Chinese state subsidies affect voluntary corporate social responsibility disclosure? J. Account. Public Policy 36, 179–200. doi:10.1016/j.jaccpubpol.2017.03.004

Li, X., He, G. j., Yi, X. h., and Kaplan, A. P. (2004). The influence of dexamethasone on the proliferation and apoptosis of pulmonary inflammatory cells in bleomycin-induced pulmonary fibrosis in rats. Respirology 2, 25–32. (in Chinese). doi:10.1111/j.1440-1843.2003.00523.x

MacKinnon, D. P., Lockwood, C. M., Hoffman, J. M., West, S. G., and Sheets, V. (2002). A comparison of methods to test mediation and other intervening variable effects. Psychol. Methods 7, 83–104. doi:10.1037/1082-989X.7.1.83

Meng, X. H., Zeng, S. X., Xie, X. M., and Qi, G. Y. (2016). The impact of product market competition on corporate environmental responsibility. Asia Pac. J. Manag. 33, 267–291. doi:10.1007/s10490-015-9450-z

Nilsson, P. (2017). Productivity effects of CAP investment support: Evidence from Sweden using matched panel data. Land Use Policy 66, 172–182. doi:10.1016/j.landusepol.2017.04.043

Qi, Y., Chai, Y., and Jiang, Y. (2021). Threshold effect of government subsidy, corporate social responsibility and brand value using the data of China’s top 500 most valuable brands. PLOS ONE 16, e0251927. doi:10.1371/journal.pone.0251927

Qiu, M., and Yin, H. (2019). Construction and empirical analysis of environmental cost early-warning model for manufacturing enterprises based on fishbone diagram. FMR 3, 108–123. (in Chinese). doi:10.22606/fmr.2019.33002

Rajan, R. G., and Zingales, L. (1998). Financial dependence and growth. Am. Econ. Rev. 88, 559–586. doi:10.3386/w5758

Ren, S., Sun, H., and Zhang, T. (2021). Do environmental subsidies spur environmental innovation? Empirical evidence from Chinese listed firms. Technol. Forecast. Soc. Change 173, 121123. doi:10.1016/j.techfore.2021.121123

Shi, G., Zhou, L., Zheng, S., and Zhang, Y. (2015). Environmental subsidy and pollution abatement: Evidence from the power industry. China Econ. Q. 15, 1439–1462. (in Chinese). doi:10.13821/j.cnki.ceq.2016.03.07

Wang, S. (2016). A study of the influence of management background characteristics on corporate social responsibility: Empirical evidence from Chinese A-share listed companies. Acc. Res. 11, 53–60 + 96. (in Chinese). doi:10.3969/j.issn.1003-2886.2016.11.008

Wang, W., Zhao, C., Jiang, X., Huang, Y., and Li, S. (2020). Corporate environmental responsibility in China: A strategic political perspective. SAMPJ 12, 220–239. doi:10.1108/SAMPJ-12-2019-0448

Wang, Y., Yang, Y., Fu, C., Fan, Z., and Zhou, X. (2021). Environmental regulation, environmental responsibility, and green technology innovation: Empirical research from China. PLOS ONE 16, e0257670. doi:10.1371/journal.pone.0257670

Wei, J., and Zuo, Y. (2018). The certification effect of R&D subsidies from the central and local governments: Evidence from China. R&D Manag. 48, 615–626. doi:10.1111/radm.12333

Wenqi, D., Khurshid, A., Rauf, A., and Calin, A. C. (2022). Government subsidies’ influence on corporate social responsibility of private firms in a competitive environment. J. Innovation Knowl. 7, 100189. doi:10.1016/j.jik.2022.100189

World Development Indicators (2022). World development indicators. Available at: https://datatopics.worldbank.org/world-development-indicators [Accessed June 1, 2022].

Wu, Y. (2019). Financial subsidies and financing constraints of small and medium-sized enterprises: Research on heterogeneity effect results and mechanisms. Commun. Res. 8, 14–24. (in Chinese). doi:10.13902/j.cnki.syyj.2019.08.003

Wu, Z., Fan, X., Zhu, B., Xia, J., Zhang, L., and Wang, P. (2022). Do government subsidies improve innovation investment for new energy firms: A quasi-natural experiment of China’s listed companies. Technol. Forecast. Soc. Change 175, 121418. doi:10.1016/j.techfore.2021.121418

Yang, C., Betti, C., Singh, S., Toor, A., and Vaughan, A. (2009). Impaired NHEJ function in multiple myeloma. Mutat. Res. 1, 66–73. (in Chinese). doi:10.1016/j.mrfmmm.2008.10.019

Zhang, H., Li, L., Zhou, D., and Zhou, P. (2014). Political connections, government subsidies and firm financial performance: Evidence from renewable energy manufacturing in China. Renew. Energy 63, 330–336. doi:10.1016/j.renene.2013.09.029

Keywords: corporate environmental responsibility, environmental subsidies, panel data, IV-2SLS, China

Citation: Chen G, Wei B and Zhu R (2022) The impact of environmental subsidy on the performance of corporate environmental responsibility: Evidence from China. Front. Environ. Sci. 10:972328. doi: 10.3389/fenvs.2022.972328

Received: 18 June 2022; Accepted: 30 August 2022;

Published: 29 September 2022.

Edited by:

Lu Yang, Shenzhen University, ChinaReviewed by:

Li Yue, Guangdong University of Foreign Studies South China Business College, ChinaCopyright © 2022 Chen, Wei and Zhu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Ruoran Zhu, enJyQGh4eHkuZWR1LmNu

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.