94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci., 23 August 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.962409

This article is part of the Research TopicFinancial and Trade Globalization, Greener Technologies and Energy TransitionView all 46 articles

Zhihao Tian1,2*

Zhihao Tian1,2*Taking China’s A-share listed companies from 2014 to 2021 as the research sample, this article verifies the differential impact of executive equity incentive and employee stock ownership plan on enterprise performance and examines the economic consequences of their implementation under the influence of environmental uncertainty, the nature of property rights, and the quality of external audit. The results show that 1) there are significant differences between executive equity incentive and employee stock ownership plan on enterprise performance. 2) The effect of executive equity incentive is more significant when the environmental uncertainty is low, while the effect of employee stock ownership plan is more significant when the environmental uncertainty is high. 3) The equity incentive of state-owned listed companies cannot significantly improve enterprise performance when the environmental uncertainty is high. 4) High-quality external audit can significantly improve the effect of equity incentive on enterprise performance, and the effect is more obvious when the environmental uncertainty is high. The research conclusion confirms the necessity of reasonably selecting equity incentive objects under the influence of environmental uncertainty and also provides a useful reference for optimizing the reform of equity incentive system of state-owned enterprises and perfecting the external audit system.

Equity incentive has always been favored by enterprises. From the perspective of incentive object, equity incentive can be divided into two types: incentive to senior managers and incentive to lower managers and employees (Zhang et al., 2017). Among them, employee stock ownership plan (Esop) is an important form of income sharing plan. As a common incentive measure in modern enterprises, Esop, together with executive equity incentive, can alleviate the cash flow pressure of enterprises, fully mobilize the enthusiasm of all parties, and promote the rapid development of enterprises under the mechanism of “benefit sharing and risk sharing.” In recent years, relevant equity incentive policies have been issued. On 20 June 2014, the CSRC issued the “Guiding Opinions on the Implementation of the Pilot Employee Stock Ownership Plan by Listed Companies,” which further made clear requirements for enterprises to implement Esop. On 27 April 2020, the 13th meeting of the Central Comprehensive Deepening Reform Committee reviewed and approved the “General Implementation Plan for the Reform of the Growth Enterprise Market and the Pilot Registration System.” The plan once again took the reform of equity incentive system as one of the key points, hoping to provide reference for the comprehensive optimization of equity incentive system. The continuous introduction of relevant policies ensures the effective implementation of enterprise equity incentive, but it should also be noted that there are still a large number of cases of equity incentive failure due to the imprecision of incentive objects. The equity incentive plans of well-known enterprises such as Jiu Yang shares, Mei Hao group. and Zoomlion ended in failure because the relevant performance indicators did not meet the exercise standards. According to the statistics of Hejun equity incentive research center, more than 100 A-share listed companies terminated the equity incentive plan in 2021. It can be seen that there is still room for improvement in the application of equity incentive in China.

Properly implementing the equity incentive can achieve the incentive effect, and clarifying the incentive object is an important link. Executive equity incentive and employee stock ownership plan, which belong to the same category of equity incentive, have different system norms, policy positioning, and applicable objects, which cannot be generalized. Due to the heterogeneity of the incentive objects, giving incentive objects with equity as the target will lead to certain differences in their perception and behavior, and the results of this difference will eventually be reflected in enterprise performance. In addition, the interference of external factors on the implementation effect of equity incentive plan is also one of the necessary factors that cannot be ignored. Not only has the continuous spread of external challenges such as COVID-19 led to global economic instability, but also the external business environment of Chinese enterprises has become increasingly volatile. It is more urgent and necessary to explore the impact of environmental uncertainty on the effect of equity incentive in Chinese enterprises than ever before. So, will the uncertain environment have an impact on the economic consequences of equity incentive? In the face of different degrees of environmental uncertainty, what kind of equity incentive should enterprises implement to achieve the best effect? The above issues need to be discussed in depth, based on China’s background. Therefore, taking China’s A-share listed companies as a sample, this article discusses the difference between the impact of executive equity incentive and employee stock ownership plan on enterprise performance, introduces environmental uncertainty variables, and further tests the economic consequences of the two when considering environmental uncertainty, in order to provide reference for enterprises to clarify the incentive object, accurately implement the equity incentive plan, and ensure the realization of incentive objectives. At the same time, from the closed-loop perspective of internal and external factors that may affect the equity incentive effect of listed companies, this article takes the property right nature of the research sample and the quality of external audit as grouping variables for further investigation.

Contributions of this article include the following: 1) It verifies the different effects of executive equity incentives and employee stock ownership plans on corporate performance in listed companies in China and affirms the important position of clear incentive objects in the implementation of equity incentives. Compared with the research on the economic consequences of executive equity incentives, due to the difficulty of statistical work on the number of employee stock ownership, there are relatively few quantitative studies on the impact of employee stock ownership plans on corporate performance. At present, scholars mostly use the 0–1 variable to test the economic consequences of the implementation of equity incentive plans, but ignore the impact of the strength of employee stock ownership. In addition, there is still a big controversy on whether the two types of equity incentive plans can achieve the established goals of the enterprise. With the development of the economy and society and the continuous improvement of related systems, the object of equity incentives only focuses on the incentives of senior managers and gradually focuses on the incentives of lower-level managers and employees. However, there are few comparative studies on the economic consequences of the improvement of relevant systems and the transformation of equity incentive objects on enterprises. 2) This article incorporates environmental uncertainty into the consideration of listed companies’ implementation of equity incentives and provides a reference for Chinese listed companies to accurately implement equity incentive plans in combination with their own external business environment. Due to the individual differences in equity incentive objects, there must be differences in the perception and behavioral consequences of different incentive objects caused by the fluctuation of the external environment. Some scholars believe that considering the environmental uncertainty, equity incentives will enable managers and employees to fully play the role of stewards so that enterprises can gain advantages in future market competition. However, the existing literature has not conducted an in-depth comparative analysis for senior managers and ordinary employees on what kind of incentive objects companies should give equity to under what environmental uncertainty. 3) This article examines the different effects of the nature of property rights and the quality of external audit on the equity incentive effect of Chinese listed companies and provides new empirical evidence for the reform of the equity incentive system of Chinese state-owned enterprises and the optimization of external audit quality for listed companies.

Most of the existing studies believe that equity incentive will make the interests of executives and shareholders tend to be consistent and then improve enterprise performance (Jensen and Meckling, 1979; Holmstrom and Costa, 1986; Smith and Watts, 1992; Bizjak et al., 1993; Carpenter and Sanders, 2002; Morck and Yeung, 2005).The research of Yao and Wu (2014) showed that there is a positive correlation between enterprise performance and executive shareholding ratio. Wang (2015) found that equity incentive stimulated the growth of corporate profits, and the longer the validity period of equity incentive, the more conducive the realization of incentive effect. Wang and Huang (2020) believed that executive equity incentives can improve corporate performance by reducing agency costs. Fan and Liu (2020) believed that executive equity incentives can improve corporate performance, especially for state-owned manufacturing enterprises. Some scholars also came to the opposite conclusion that equity incentives are not always for incentive purposes, and they cannot promote enterprise performance and even damage corporate value (DeFusco et al., 1991; Lie, 2005; Heron and Lie, 2007). Xiao et al. (2012) examined the impact of equity concentration and equity incentives on enterprise performance from an endogenous perspective and found that there is no significant relationship among the three. Qiu et al. (2017) also found that executive equity incentives have a poor effect on enterprise performance. Xiao and Wang (2022) took academic spin-offs as a research sample and believed that executive equity incentives cannot significantly improve corporate performance. Li (2017) believed that equity incentives are a “double-edged sword”, and improper use may be harmful to companies.

Foreign research on the impact of employee stock ownership plans on enterprise performance was mainly reflected in changes in the capital market (Gordon and Pound, 1990; Chang and Mayers, 1992), corporate operating efficiency and productivity (Rosen and Quarrey, 1987; Pugh et al., 2000; Kim and Ouimet, 2014), and related information disclosure (Bova et al., 2015). Some scholars also found that after the implementation of the employee stock ownership plan, employees will pay more attention to the long-term development of the company and are willing to make more efforts for the company’s performance growth (Kumbhakar and Dunbar, 1993; Jones and Kato, 1995; Mauldin, 1999; Pugh et al., 2000; Kramer, 2010; Kim and Ouimet, 2014; Paterson and Welbourne, 2020). However, most domestic scholars only discussed from the qualitative perspective of whether the company implements employee stock ownership plans (Shen et al., 2018). For example, based on the background of the 2014 employee stock ownership system reform, it was found from a qualitative perspective that there was a significant positive correlation between the implementation of employee stock ownership plans and company performance, while few scholars analyzed the impact of employee stock ownership on enterprise performance from a quantitative perspective (Liu et al., 2019). Fang (2021) believed that the effective implementation of employee stock ownership plans can significantly enhance corporate value. On the contrary, some scholars believed that the relationship between employee stock ownership plans and enterprise performance is not significant or effective only in the short term and will encourage employees to “free ride” behavior. Giving employee shares does not necessarily motivate employees. Instead, they believed that is paying for major shareholders to reduce their holdings (Conte and Tannenbaum, 1978; Weitzman and Kruse, 1990).

Williamson (1975) believed that appropriate equity incentives can relieve employees’ anxiety and confusion caused by environmental uncertainty and enable them to strengthen their beliefs and work hard. Ezzamel (1990) believed that when environmental uncertainty increases, companies should pay more attention to the initiative of employees. Lewis (1990) believed that, with the increase of environmental uncertainty, the demand for flexible management of enterprises also increases. Since employees are closest to the changing environment, they need to be given greater incentives to deal with environmental uncertainty in a timely and effective manner. Fisher and Govindarajan (1992) believed that the uncertainty of the environment increases the degree of information asymmetry between managers and employees and makes the principal–agent problem within the enterprise more serious. In order to reduce agency costs, companies should pay more attention to the performance of employees, make their efforts consistent with the environment in which the company is located, and give employees certain equity incentives to improve enterprises performance. Domestic research on the impact of environmental uncertainty on equity incentives mainly focused on investment efficiency, accounting information governance effects, inefficient investment, and corporate innovation activities. Most scholars believed that taking into account environmental uncertainties, equity incentives will enable managers and employees to give full play to the role of stewardship, thereby gaining an advantage in future market competition (Shen et al., 2012; Shen and Wu 2012; Zhu, 2019). Gao (2021) believed that equity incentives can promote corporate innovation performance, but environmental uncertainty can inhibit this positive relationship. Li and Duan (2022) took heavily polluting enterprises as samples and believed that environmental uncertainty can inhibit technological innovation of enterprises and equity incentives can alleviate this negative relationship.

In summary, the research on the impact of executive equity incentives and employee stock ownership plans on enterprises performance is becoming more abundant, but the perspectives and conclusions are not consistent. As early as 1993–1998, China introduced measures related to employee stock ownership plans, but the plan eventually died due to other unfavorable factors. With the development of the economy and society and the continuous improvement of related systems, the object of equity incentives has shifted from focusing only on the incentives for senior managers, and tends to pay equal attention to the incentives for lower-level managers and employees. On 20 June 2014, the China Securities Regulatory Commission issued the “Guiding Opinions on the Pilot Implementation of Employee Stock Ownership Plans by Listed Companies,” which made clear requirements for the implementation of employee stock ownership plans. On 13 July 2016, the commission reviewed and approved the “Administrative Measures for Equity Incentives of Listed Companies,” which further clarified that the objects of equity incentives can include directors, senior management personnel, core technical personnel or core business personnel of listed companies, and other employees who have a direct impact on the company’s operating performance and future development. On 27 April 2020, the 13th meeting of the Central Committee for Comprehensively Deepening Reform reviewed and approved the “General Implementation Plan for the Reform of the Growth Enterprise Market and the Pilot Registration System,” which once again focused on the reform of the equity incentive system. The promulgation of the above policy bills not only shows the increasing importance of equity incentives in Chinese listed companies, but also provides a clearer basis for Chinese listed companies to formulate equity incentive plans and urges Chinese listed companies to continuously establish more scientific and reasonable equity incentive system. This not only proves that the research of this paper has important practical significance, but also provides a good research background and research opportunity for it.

In addition, compared with studies on the economic consequences of executive equity incentives, there are relatively few studies on the impact of employee stock ownership plans on enterprise performance in China, and they are still at a relatively early stage. Current scholars mostly study whether the company implements equity incentive plans as a 0–1 variable to test the economic consequences after implementation, ignoring the impact of shareholding intensity on enterprise performance. At the same time, whether executive equity incentives and employee stock ownership plans can improve enterprise performance is still a big controversy, and there are few obvious comparisons between the two based on the differences in equity incentive targets. Further, considering the environmental uncertainties, there are even fewer studies examining the impact of executive equity incentives and employee stock ownership plans on enterprise performance. According to the contingency theory, in the context of the ever-changing and turbulent external environment of today’s society, will environmental uncertainties have an impact on the economic consequences of equity incentives? In the context of different environmental uncertainties, will the economic consequences of equity incentives differ due to different incentive targets? Solving the above problems is of great significance to the successful implementation of equity incentive plan in Chinese enterprises.

The separation of ownership and management rights in modern enterprises leads to the information asymmetry between owners and managers, which makes managers to have the motivation to make decisions for their own goals, thus damaging the interests of owners. Equity incentive can change the role of managers into owners to a certain extent, let them make the best decision according to the maximization of shareholders’ interests, and promote the improvement of the overall performance of enterprises. According to the high-level echelon theory, people’s decision making is mainly affected by their psychological activities, and psychological perception will affect external behavior and lead to behavioral results. As a kind of incentive method, the mechanism of equity incentive is the process of influencing the individual’s psychological perception and ultimately affecting its external performance through external stimulus to people. However, it should also be noted that the executives and employees in the enterprise are different individuals in different positions on the functional chain. The same external stimulus will cause different psychological perception due to individual differences and eventually lead to different behavior results, and the different individual behavior results will eventually reflect the difference of enterprise performance. The motivator–hygiene theory also believes that hygiene factors and motivational factors are not completely separate and that the two are closely related and may be transformed into each other. Generally, in the environment of general shareholding of management, executives often regard equity incentives as part of their remuneration, representing the working environment and status, and most of them are hygiene factors. For ordinary employees at the bottom of the functional chain, Esop can better solve the more comprehensive problem of operator moral hazard by giving employees equity to motivate them in a wider range (Wang et al., 2019). At the same time, it also makes their work challenging and then stimulates employees’ sense of responsibility and achievement, which are mostly motivational factors. Only motivational factors can achieve the incentive purpose, and the satisfaction of hygiene factors can only eliminate people’s dissatisfaction and will not achieve the incentive effect. Therefore, the economic consequences of executive equity incentive and employee stock ownership plan are often different.

In addition, there are also differences between executive equity incentives and employee stock ownership plans in terms of functional positioning, stock sources, and funding channels. The implementation of the former focuses on executives and more on motivational attributes. It generally holds shares in the form of self-raised funds through channels, such as company grants and primary market issuance, so that the interests of senior management and shareholders are aligned, thereby reducing agency costs and improving enterprise performance. The latter is to expand the scope of equity incentive downward, including ordinary employees and senior executives. The employee stock ownership plan focuses more on benefit sharing. Generally, it holds shares in the form of self-financing or leveraged financing through channels, such as secondary market purchase and free gifts from major shareholders, which is part of the income sharing plan.

According to the above differences, this article uses the shareholding ratio of executives and ordinary employees as a measure of equity incentives, explores the differences in their economic consequences, and proposes hypothesis 1:

H1: There are significant differences between executive equity incentive and employee stock ownership plan on enterprise performance.

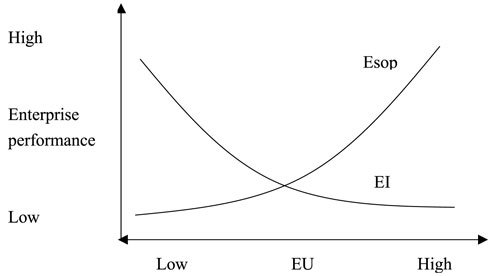

According to contingency theory, external environment is the most important contingency variable (Chenhall, 2003). It has a potential impact on the whole enterprise and a part of the enterprise. Furthermore, environmental uncertainty (EU) is an important performance characteristic of the external environment. Organizational theory believes that when the external environment is highly uncertain, it is the only reasonable goal of an enterprise to improve its own learning ability to adapt to the complex and changing environment (March, 1991). At this time, the enterprise is bound to decentralize and give employees certain incentives to give full play to its initiative, so as to enhance the effectiveness of business operations. The resource dependence theory also believes that the higher the environmental uncertainty, the more enterprises will strive to deal with the uncertainty. If the degree of environmental uncertainty expected by enterprises increases, enterprises will create a more open and decentralized atmosphere for themselves (Pfeffer and salancik, 1978). According to the above theories, environmental uncertainty will affect not only the centralization or decentralization of power and the behavior of the organization, but also the selection of equity incentive objects and their economic consequences. Therefore, in the increasingly turbulent external environment, there is no universally applicable equity incentive plan. Enterprises should consider the uncertain factors of their environment and select appropriate personnel as the object of equity incentive, so as to optimize their economic consequences. In conclusion, it can be inferred that when the degree of environmental uncertainty is low, enterprises can adopt a more centralized way and pay attention to the equity incentive for executives. When the degree of environmental uncertainty is high, enterprises should adopt a more decentralized way and pay attention to equity incentive for employees. Considering environmental uncertainty, the difference between executive equity incentive (EI) and employee stock ownership plan (ESOP) on enterprise performance is shown in Figure 1.

FIGURE 1. Impact of environmental uncertainty on economic consequences of equity incentive.

The horizontal axis of Figure 1 represents the level of environmental uncertainty, the vertical axis represents the level of corporate performance, and the two curves represent the implementation of executive equity incentives and employee stock ownership plans. It can be seen from Figure 1 that environmental uncertainty can have a differential impact on the relationship between executive equity incentives, employee stock ownership plans, and corporate performance. In other words, as the degree of environmental uncertainty increases, the impact of executive equity incentives on corporate performance will be weakened, while the impact of employee stock ownership plans on corporate performance will be enhanced. In summary, this article uses environmental uncertainty (EU) as an adjustment variable to verify its impact on the economic consequences of executive equity incentives and employee stock ownership plans and proposes hypothesis 2:

H2(a): In the case of low environmental uncertainty, the positive impact of executive equity incentives on enterprise performance is more significant.

H2(b): In the case of high environmental uncertainty, the positive impact of employee stock ownership plans on enterprise performance is more significant.

In order to reduce the impact of the 2014 “Guiding Opinions on the Implementation of the Pilot Employee Stock Ownership Plan by Listed Companies” on this research, this article selects China’s A-share listed companies from 2014 to 2021 as the research sample and makes the following treatments: 1) Due to the lack of relevant data, those sample enterprises whose announcement date of the employee stock ownership plan is not in the same year as the implementation completion date are regarded, as the employee stock ownership plan is not implemented in the current year. 2) The shareholding ratio of the employee stock ownership plan in the renewal period is manually sorted out according to the contents of its announcement. Among them, the employee shareholding ratio is calculated after excluding the subscription part of the senior executives. 3) When calculating environmental uncertainty, this article needs 5 years of operating income, so the sample enterprises with operating income data less than 5 years are excluded. 4) Exclude the samples with changes in the nature of equity during this period. 5) Exclude ST, financial industry, and samples with missing data. In addition, in order to alleviate the influence of outliers, all continuous variables were reduced by 1%, and 8,384 sample observations from 1,048 enterprises were obtained. ESOP and related financial data are from WIND and CSMAR databases, respectively.

Referring to the research of existing scholars, Roa is selected as the explained variable to measure the enterprise performance.

Equity incentives mainly give managers and employees part of the shareholders’ rights and interests, so that they have a sense of ownership, so as to form a community of interests with the enterprise, promote the growth of the enterprise with them, and help the enterprise achieve the goal of stable development. According to China’s “Company Law,” the total capital of a listed company is divided into equal shares, each of which has a voting right, and shareholders enjoy rights and assume obligations with the shares they subscribe for. Therefore, the amount of company shares held by the incentive object represents the degree of equity incentives it receives. In order to make the equity incentives of each sample enterprise comparable, this article uses the ratio of the number of shares held by executives to the total number of shares, to measure the strength of executive equity incentives (EI); and the ratio of the number of employee stocks to the total number of stocks to measure the strength of the employee stock ownership plan (Esop).

Environmental uncertainty (EU_d) is selected as the adjustment variable. For the measurement of environmental uncertainty, the existing literature mainly adopts two indicators. One is the subjective index, which is obtained through the questionnaire method. It is more subjective and suitable for small sample research and the research conclusions are less universal. The other is objective indicators, including operating income and EBIT. Environmental uncertainty comes from the external environment, the change of the external environment will eventually lead to the fluctuation of the enterprise’s operating income (Dess and Beard, 1984; Bergh and Lawless, 1998), and the operating income is not easily affected by accounting policies and human manipulation. Therefore, environmental uncertainty is measured by its fluctuation degree (Tosi et al., 1973; Cheng and Kesner, 1997). Referring to the existing methods, this article uses the data of the past 5 years, taking operating income as the explained variable and taking the year as the explanatory variable to construct model (1) (Ghosh and Olsen, 2009; Shen et al., 2012; Shen and Wu 2012; Zhu, 2019). The standard deviation of the residual of model (1) divided by the mean value of the operating income in the past 5 years is used as an indicator of environmental uncertainty. At the same time, in order to avoid the influence of different industry characteristics, the above results are divided by the median of their sub-industry to eliminate the interference of industry characteristics, and the final results are sorted by small and large. If it is less than the median, the degree of environmental uncertainty is considered to be low and assigned a value of 0. If it is greater than or equal to the median, the degree of environmental uncertainty is considered to be high and assigned a value of 1.

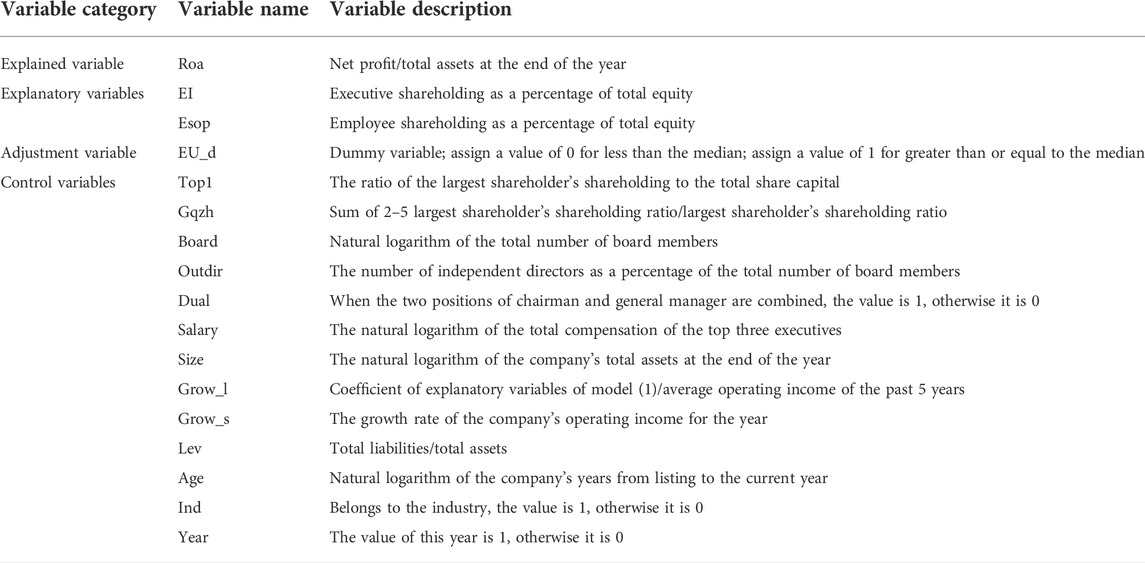

Drawing on the research of existing scholars (Shen and Wu, 2012; Li, 2017), this article controls the following variables: equity concentration (Top1), equity checks and balances (Gqzh), board size (Board), the proportion of independent directors (Outdir), combination of the two positions of chairman and general manager (Dual), total remuneration of the top three executives (Salary), company size (Size), company’s long-term growth (Grow_l), company’s short-term growth (Grow_s), debt-to-asset ratio (Lev), company age (Age), and dummy variables of industry (Ind) and year (Year). Table 1 lists the explained variables, explanatory variables, adjustment variables and control variables in detail.

TABLE 1. Variable definition.

The following regression was established to test hypothesis 1. If β1 and β2 are significant and there is a significant difference between the two, it means that the impact of executive equity incentives and employee stock ownership plans on corporate performance is significantly different. Therefore, hypothesis 1 is proved.

In order to test hypothesis 2, the groups are grouped according to EU_d. When EU_d = 0, it is the group with low degree of environmental uncertainty. When EU_d = 1, it is the group with high degree of environmental uncertainty. If when EU_d = 0, the β1 of models (2) and (4) are significantly positive, and when EU_d = 1, the significance disappears, then hypothesis 2(a) is proved. It means the positive impact of executive equity incentives on corporate performance is more significant in the case of low environmental uncertainty. If when EU_d = 1, β1 of model (3) and β2 of model (4) are significantly positive, and when EU_d = 0, the significance disappears, then hypothesis 2(b) is proved. It means the positive impact of Esop on enterprise performance is more significant in the case of high environmental uncertainty.

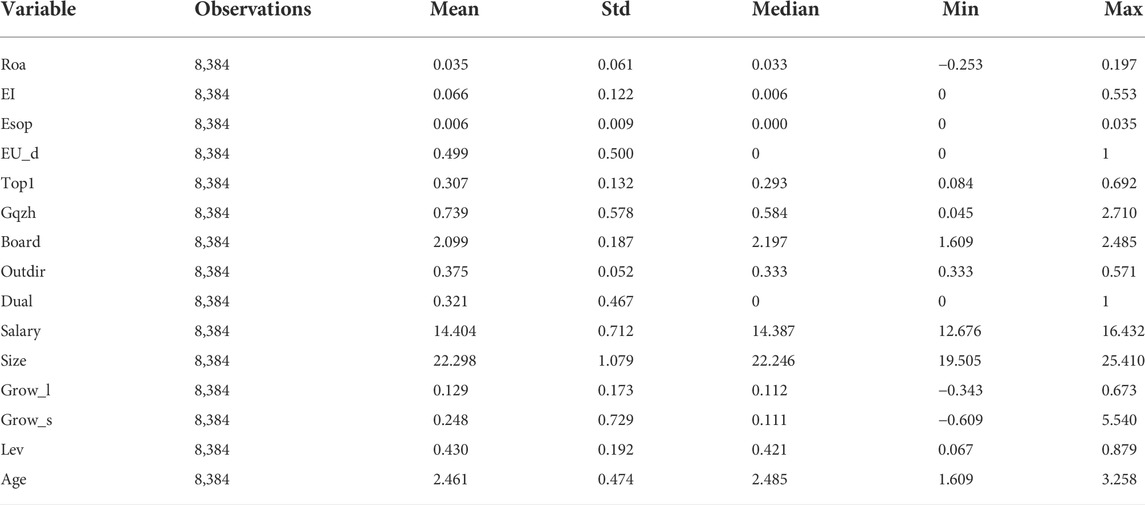

The descriptive statistical results of the main variables are shown in Table 2. It can be seen from Table 2 that the maximum and minimum values of Roa are 0.197 and −0.253, and their mean and median are 0.035 and 0.033, respectively. It shows that a small number of observation samples are in a state of loss, but most of the observation samples are in the state of profit. The median and mean values of Esop are less than the median and mean of EI, respectively, indicating that the employee ownership level of the sample enterprises is generally less than that of senior executives. The mean and median of environmental uncertainty are close to 0.5, indicating that the number of sample companies in the high group and low group of environmental uncertainty is roughly the same. The distribution of other variables is within a reasonable range and will not be repeated.

TABLE 2. Descriptive statistics.

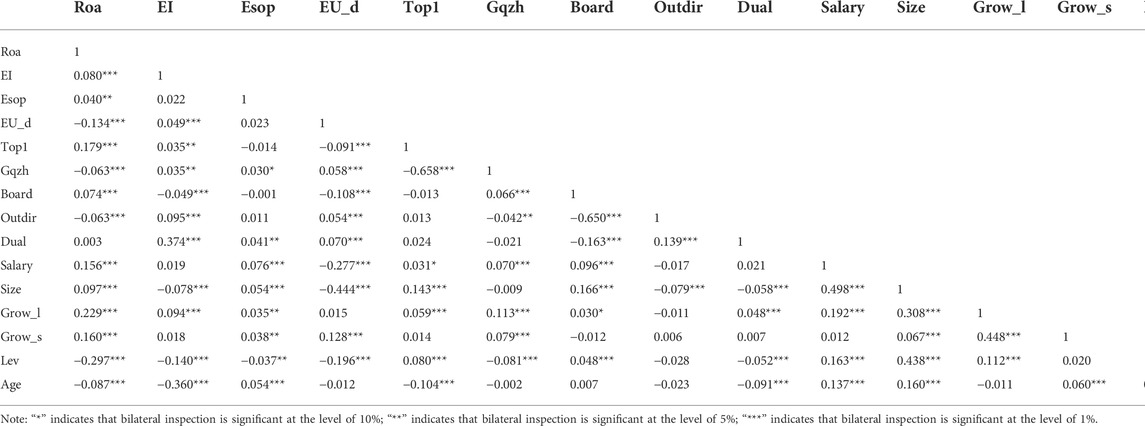

Table 3 shows the correlation coefficients between all variables. It can be seen from Table 3 that EI and Esop are significantly positively correlated with Roa, while EU_d was significantly negatively correlated. It preliminarily shows that executive equity incentive and employee stock ownership plan have a positive impact on enterprise performance, while the increase of environmental uncertainty weakens the enterprise performance. The correlation of other variables is roughly the same as that of existing studies, and there is no serious multicollinearity.

TABLE 3. Correlation coefficient.

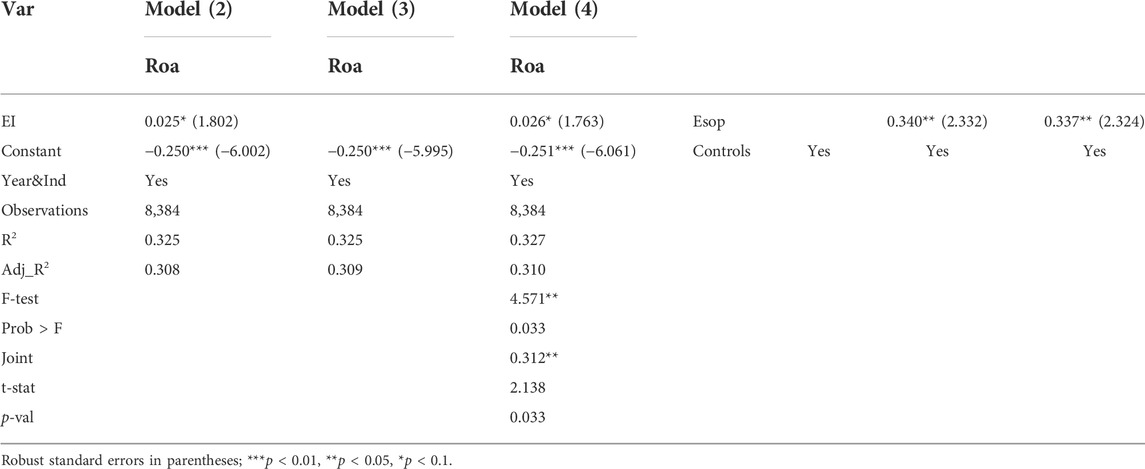

Table 4 lists the regression results of models (2)–(4). From Table 4, it can be seen that the coefficient of executive equity incentive in model (2) is 0.025 and that in model (4) is 0.026, both of which are significant at the 10% level, indicating that executive equity incentive can improve the enterprise performance. The coefficient of employee stock ownership plan in model (3) is 0.340 and in model (4) is 0.337, both of which are significant at the 5% level, which also confirms the positive effect of employee stock ownership plan on corporate performance. Through the coefficient difference test of EI and Esop of model (4), we can see that the F-value of the test is 4.571 and the Prob > F-value is 0.033. It shows that the influence of executive equity incentive and employee stock ownership plan on corporate performance is significantly different at the level of 5%. Further from Lincom test, its joint value is 0.312 and its p-value is 0.033, indicating that at the level of 5%, the economic consequences of employee stock ownership plans are better than the economic consequences of executive equity incentives. Hypothesis 1 is proved, that is, there is a significant difference in the impact of executive equity incentives and employee stock ownership plans on corporate performance.

TABLE 4. Regression results of models (2)–(4).

In addition, the coefficients of Top1, Salary, Size, Grow_l, and Grow_s are significantly positive. It shows that the higher the shareholding ratio of the largest shareholder of the sample company, the more the top three salary of executives, the larger the scale of the company, and the better the long-term and short-term growth, the better the performance of the sample company. The coefficients of Outdir and Lev are significantly negative, indicating that the more independent directors occupy the board of directors and the higher the company’s asset–liability ratio, the worse the company’s performance. The above results are basically consistent with existing research.

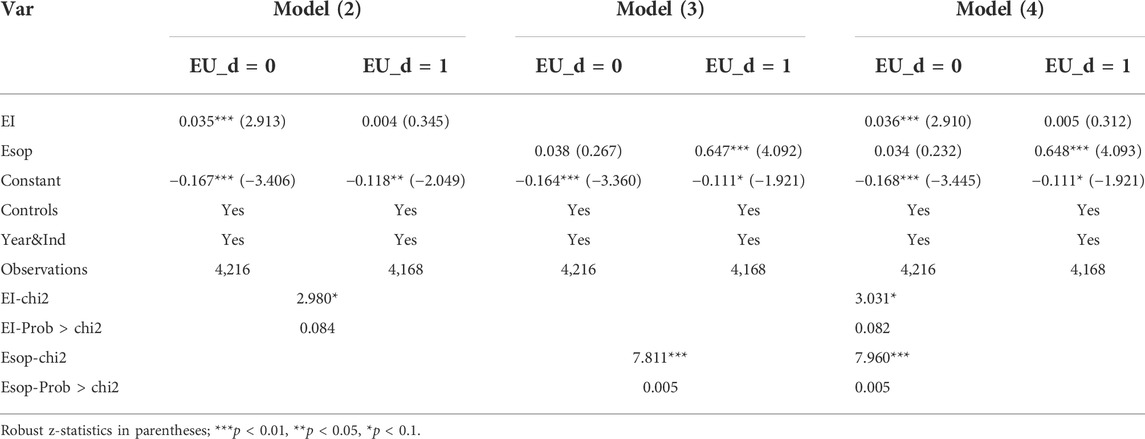

Further, in order to test the role of environmental uncertainty in the impact of executive equity incentive and employee stock ownership plan on enterprise performance, the group test is carried out according to the degree of environmental uncertainty. When EU_d = 0, the group is regarded as the group with low environmental uncertainty, and when EU_d = 1, the group is regarded as the group with high environmental uncertainty. The regression results are shown in Table 5.

TABLE 5. Grouping test of environmental uncertainty.

It can be seen from Table 5 that when EU_d = 0, the coefficient of executive equity incentive in model (2) is 0.035 and that in model (4) is 0.036, both of which are significant at the 1% level, while when EU_d = 1, the significance of executive equity incentive coefficient disappears. The grouping of model (2) and model (4) was tested for seemingly unrelated regressions, and the chi2 values were 2.980 and 3.031, respectively, which were significant at the 10% level. The above shows that, in the case of low environmental uncertainty, the positive impact of executive equity incentives on enterprise performance is more significant. Therefore, hypothesis 2(a) is proved. When EU_d = 1, the coefficient of employee stock ownership plan in model (3) is 0.647 and that in model (4) is 0.648, both of which are significant at the 1% level, while when EU_d = 0, the significance of the employee stock ownership plan coefficient disappears. Similarly, the seemingly unrelated test is performed for the grouping of model (3) and model (4), and the chi2 values were 7.811 and 7.960, respectively, which were significant at the 1% level. The above shows that, in the case of high environmental uncertainty, the positive impact of the employee stock ownership plan on enterprise performance is more significant, and hypothesis 2(b) is proved. Other control variables are basically the same as in Table 4 and so will not be repeated here.

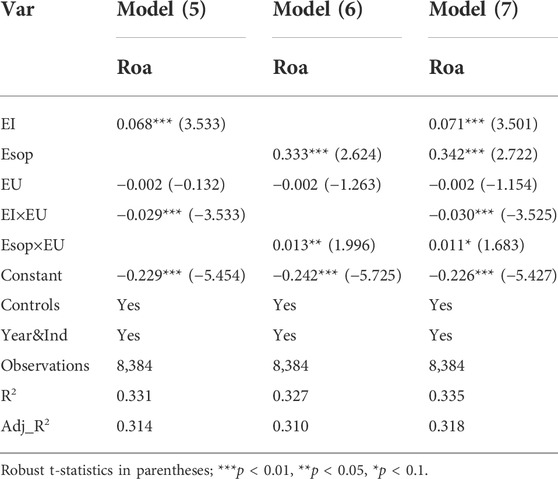

The above analysis mainly analyzes the 0–1 grouping based on the median of environmental uncertainty to test the impact of executive equity incentives and employee stock ownership plans on enterprise performance under different environmental uncertainties. Then, what impact will the intensity of environmental uncertainty (EU) have on the economic consequences of executive equity incentives and employee stock ownership plans? In order to test this problem, model (5), model (6), and model (7) were constructed for further analysis.

In models (5)–(7), the intensity of environmental uncertainty is measured by dividing the standard deviation of the residuals of model (1) by the mean value of operating income in the past 5 years and then dividing by the median of its sub-industry. The other variables are defined as above.

Table 6 lists the effects of EI and Esop on Roa under the influence of environmental uncertainty intensity. It can be seen from Table 6 that the coefficients of executive equity incentives in model (5) and model (7) are 0.068 and 0.071, respectively, both of which are significant at the 1% level. In the above two models, the multiplier coefficients of executive equity incentives and environmental uncertainty are −0.029 and −0.030, respectively, both of which are also significant at the 1% level. The above results mean that the more turbulent the external environment of the company, the weaker the impact of EI on Roa, which again confirms hypothesis 2(a), that is, in the case of low environmental uncertainty, executive equity incentives have a positive impact on corporate performance more significantly. The coefficients of employee stock ownership plans in model (6) and model (7) are 0.333 and 0.342, respectively, both of which are significant at the 1% level. In the above two models, the multiplier coefficients between the employee stock ownership plan and the external environment are 0.013 and 0.011, respectively, which are significant at the 5% and 10% levels, respectively, indicating that environmental uncertainty has enhanced the positive impact of Esop on Roa, which confirms hypothesis 2(b) again, that is, in the case of high environmental uncertainty, the positive impact of employee stock ownership plans on firm performance is more significant. Other control variables are basically the same as the above and will not be repeated here.

TABLE 6. Regression results of models (5)–(7).

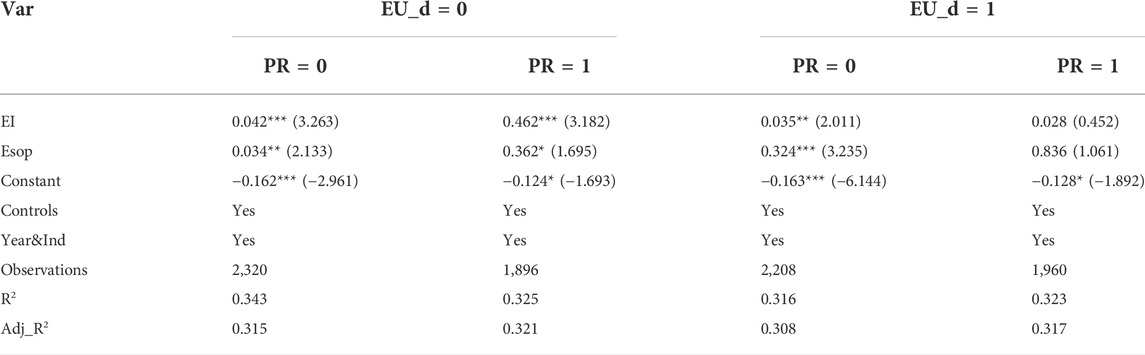

In view of the equity incentive of state-owned enterprises, in addition to improving enterprise performance, it also undertakes a certain degree of political objectives. It is inferred that the nature of property rights (PR), as the internal characteristic of enterprises, will inevitably have a certain impact on the economic consequences of the implementation of equity incentive. Therefore, this article further classifies according to the PR of the samples. When the property right of the enterprise belongs to the country, PR = 1, otherwise it is 0. Model (4) was group tested according to the level of environmental uncertainty. As shown on the left side of Table 7, the coefficients of executive equity incentive of state-owned listed companies and private listed companies are 0.042 and 0.462, respectively, which are significant at the level of 1%, and the coefficients of employee stock ownership plan are 0.034 and 0.362, respectively, which are significant at the level of 5% and 10%. It shows that when the environmental uncertainty is low, the impact of the nature of property rights on the effect of equity incentive is not different, but the effect of executive equity incentive is still better than that of employee stock ownership plan. As can be seen from the right side of Table 5, the significance of the coefficients of the executive equity incentive and the employee stock ownership plan of state-owned listed companies disappears, while the coefficients of executive equity incentive and employee stock ownership plan of private listed companies is 0.035 and 0.324, which are significant at the level of 5% and 1%, respectively. It shows that when the environmental uncertainty is at a high level, the equity incentive of state-owned listed companies cannot significantly improve enterprise performance. This shows that the more volatile the external environment, the greater the political task undertaken by state-owned listed companies. At this time, equity incentive is not the only goal to improve enterprise performance.

TABLE 7. Model 4) grouping test of property right nature.

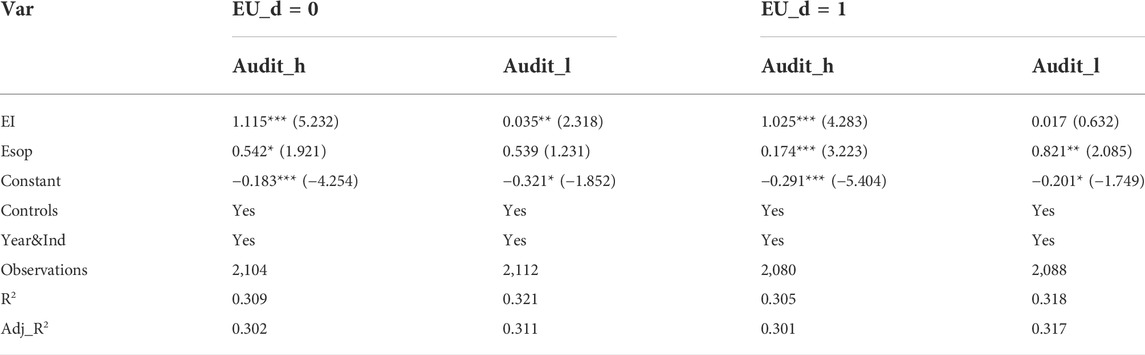

As an important supplementary mechanism of internal governance, external audit will inevitably have a certain impact on enterprise behavior. According to whether the audit institutions are “Big Four,” this article divides the research samples into two categories: high external audit quality (Audit_h) and low external audit quality (Audit_l), and tests model (4) according to the level of environmental uncertainty. It can be seen from Table 8 that when the environmental uncertainty is relatively stable, the coefficient of EI of the “Big Four” samples is 1.115, which is significant at the 1% level, the coefficient of Esop is 0.542, which is significant at the 10% level, and the coefficient of EI of the “non-Big Four” samples is 0.035, which is significant at the 5% level, and the significance level of the Esop coefficient disappears. When the environmental uncertainty is turbulent, the coefficient of EI of the “Big Four” samples is 1.025, which is significant at the 1% level, and the coefficient of Esop is 0.174, which is significant at the 1% level. The significance level of the EI coefficient of the “non-Big Four” samples disappeared, and the coefficient of Esop was 0.821, which was significant at the 5% level. It can be seen that, regardless of whether the external environment of the sample companies is stable or turbulent, the significance level of the EI and Esop coefficients of the “Big Four” samples is higher than that of the “non-Big Four” samples. Therefore, it can be inferred that high-quality external audit, as an important supplement to the company’s internal governance, can significantly improve the positive effect of executive equity incentives and employee stock ownership plans on corporate performance. At the same time, it can also be noted that when the external environment is in turmoil, the coefficient of the executive equity incentives in the Audit_h sample is less significant than that in the Audit_l sample, from 1% to insignificant. This shows that higher external audit quality not only can generally improve the effect of equity incentives of listed companies, but also has a more obvious improvement effect on the equity incentives of executives for listed companies in a turbulent external environment.

TABLE 8. Model (4) grouping test of external audit quality.

The above results show that there are significant differences in the impact of executive equity incentives and employee stock ownership plans on enterprise performance. In the case of low environmental uncertainty, the positive impact of executive equity incentives on enterprise performance is more significant; in the case of high environmental uncertainty, the positive impact of employee stock ownership plans on enterprise performance is more significant. But in order to alleviate reverse causality, for example, companies with good performance are more inclined to implement equity incentive plans. This article adopts the following methods to alleviate endogenous problems.

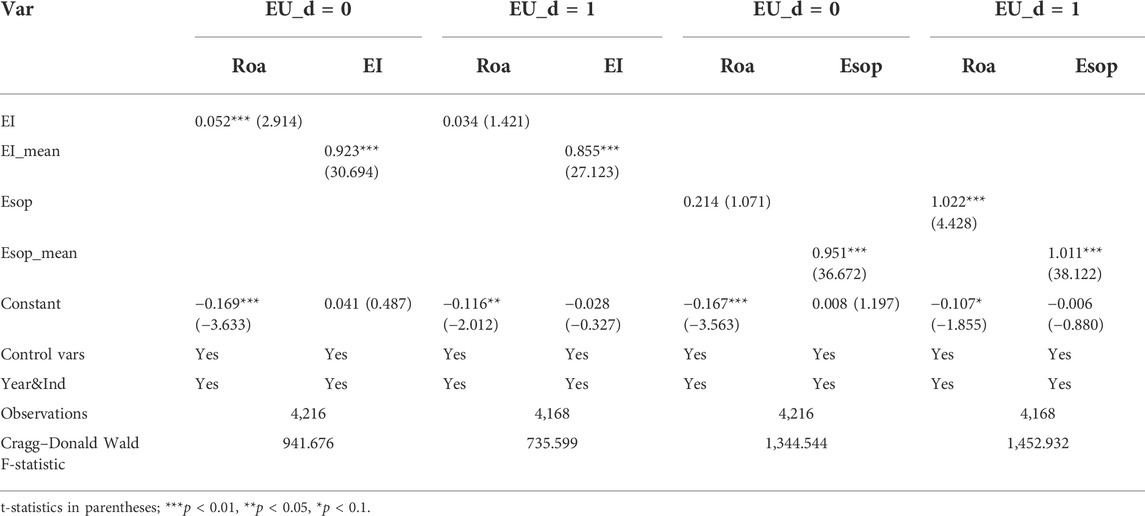

Based on the research methods of existing works (Hochberg and Lindsey, 2010; Chang et al., 2015; Wang et al., 2019), the mean values of EI and Esop of sample enterprises in the same province and industry are taken as the instrumental variables of EI and Esop of the sample enterprises, respectively. Due to the close geographical distance of enterprises in the same province and industry, there is an imitation behavior in equity incentive (Kedia and Rajgopal, 2009), but the performance of the company cannot directly affect the average level of executive equity incentive and employee stock ownership plan in the same province and industry. Therefore, EI_mean and Esop_mean are ideal as instrumental variables.

It can be seen from Table 9 that whether EU_d = 0 or EU_d = 1, EI_mean and EI are significantly positively correlated at the level of 1%. It shows that the implementation of equity incentives for executives in the sample enterprises will be affected by the average level of the same province and the same industry, and the F-statistics of the weak instrumental variable test are 941.676 and 735.599, respectively, which rejects the hypothesis of weak instrumental variables. Similarly, whether EU_d = 0 or EU_d = 1, Esop_mean and Esop are significantly positively correlated at the 1% level. It shows that the implementation of the employee stock ownership plan of the sample enterprises will be affected by the average level of the same province and the same industry, and the F-statistics of the weak instrumental variable test are 1,344.544 and 1,452.932, respectively, which also rejects the hypothesis of weak instrumental variables. It can be seen from the above that it is reasonable to use the mean of EI and Esop of sample enterprises in the same province and the same industry as the instrumental variables of EI and Esop of the sample enterprises. In addition, when EU_d = 0, the coefficient of EI is 0.052, which is positively correlated at the 1% level, while when EU_d = 1, the significance of the EI coefficient disappears. It shows that in the case of low environmental uncertainty, the positive impact of executive equity incentives on corporate performance is more significant. When EU_d = 1, the coefficient of Esop is 1.022, which is positively correlated at the 1% level, while when EU_d = 0, the significance of the Esop coefficient disappears. It shows that in the case of high environmental uncertainty, the positive impact of employee stock ownership plan on corporate performance is more significant. It can also be seen that there is a significant difference in the impact of executive equity incentives and employee stock ownership plans on corporate performance. This result verifies hypothesis 1 and hypothesis 2(a) and 2(b) again, indicating that the conclusions of this article are robust.

TABLE 9. Instrumental variables of models (2)–(3) (grouping).

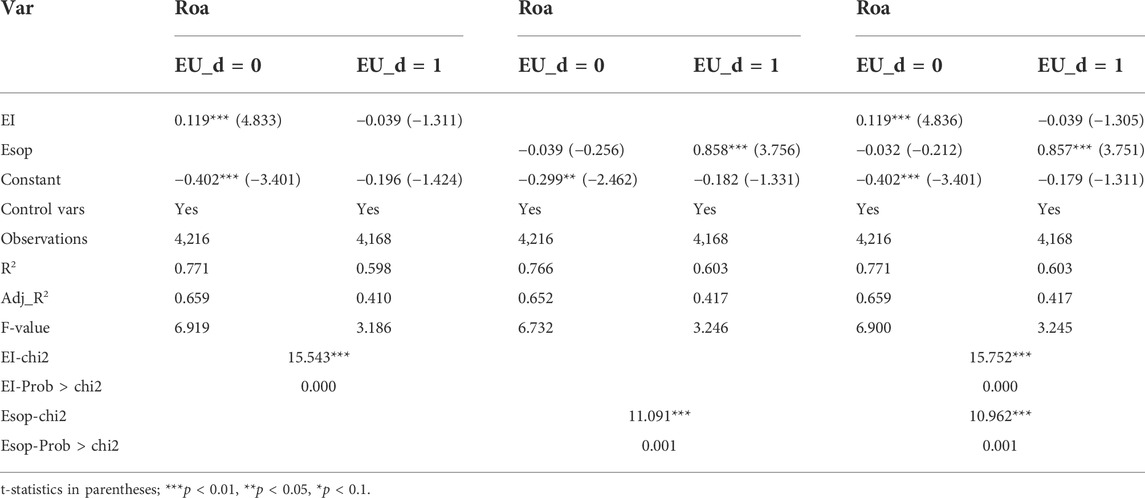

This article uses a fixed-effects model to test the robustness of the research results. The fixed-effects model can control the characteristics of the sample companies, so as to exclude the possibility that the research results are reverse causality. The test results are shown in Table 10.

TABLE 10. Fixed-effects of models (2)–(4) (grouping).

It can be seen from Table 10 that when EU_d = 0, the coefficient of EI is 0.119, which is positively correlated at the 1% level, while when EU_d = 1, the significance of the EI coefficient disappears. It shows that in the case of low environmental uncertainty, the positive impact of executive equity incentives on corporate performance is more significant. When EU_d = 1, the coefficient of Esop is 0.857, which is positively correlated at the 1% level, while when EU_d = 0, the significance of the Esop coefficient disappears. It shows that in the case of high environmental uncertainty, the positive impact of employee stock ownership plan on corporate performance is more significant. It can also be seen that there is a significant difference in the impact of executive equity incentives and employee stock ownership plans on corporate performance. This result verifies hypothesis 1 and hypothesis 2(a) and 2(b) again, indicating that the conclusions of this article are robust.

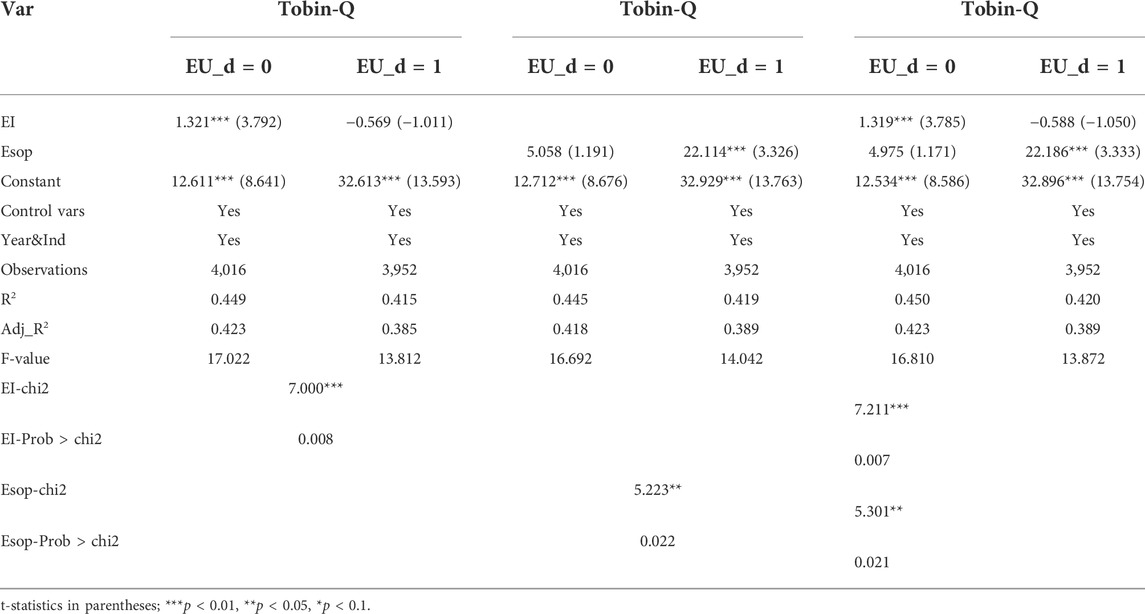

In order to further verify the robustness of the research results, this article changes the measurement indicators of the explained variables and also the return on total assets (Roa) to Tobin-Q to measure the performance of the sample companies. Tobin-Q is measured by the market value/asset replacement cost of the sample companies. Tobin-Q reflects the company’s expected future profits, while Roa only measures the company’s past performance level. Furthermore, because a firm’s market value is affected by the variance of expected profits, Tobin-Q includes an automatic adjustment for risk. Therefore, Tobin-Q is mostly considered to be a better surrogate index for Roa, and the test results after changing the explained variables are shown in Table 11.

TABLE 11. Tobin-Q of models (2)–(4) (grouping).

It can be seen from Table 11 that when EU_d = 0, the coefficient of EI is 1.319, which is positively correlated at the 1% level, while when EU_d = 1, the significance of the EI coefficient disappears. It shows that in the case of low environmental uncertainty, the positive impact of executive equity incentives on corporate performance is more significant. When EU_d = 1, the coefficient of Esop is 22.186, which is positively correlated at the 1% level, while when EU_d = 0, the significance of the Esop coefficient disappears. It shows that in the case of high environmental uncertainty, the positive impact of employee stock ownership plan on corporate performance is more significant. It can also be seen that there is a significant difference in the impact of executive equity incentives and employee stock ownership plans on corporate performance. This result verifies hypothesis 1 and hypothesis 2(a) and 2(b) again, indicating that the conclusions of this article are robust.

Taking China’s A-share listed companies from 2014 to 2021 as a sample, this article verifies the differential impact of executive equity incentive and employee stock ownership plan on enterprise performance and examines the economic consequences of their implementation under the consideration of environmental uncertainty. In addition, in view of the possible impact of the nature of property rights and the quality of external audit, this article makes a further grouping test on the implementation effect of equity incentive of listed companies. The results show the following. 1) There are significant differences between executive equity incentive and employee stock ownership plan on enterprise performance. 2) The effect of executive equity incentive is more significant when the environmental uncertainty is low, while the effect of employee stock ownership plan is more significant when the environmental uncertainty is high. 3) The equity incentive of state-owned listed companies cannot significantly improve enterprise performance when the environmental uncertainty is high. 4) High-quality external audit can significantly improve the effect of equity incentive on enterprise performance, and the effect is more obvious when the environmental uncertainty is high.

The research of this article affirms the positive effect of executive equity incentive and employee stock ownership plan on enterprise performance improvement, finds that the economic consequences of equity incentive are different due to different incentive objects and environmental uncertainty, and further analyzes the impact of the nature of property rights and the quality of external audit on the research results, which provides a useful reference for Chinese enterprises to accelerate the realization of the goal of equity incentive, specifically. 1) There are differences in the psychological perception of different individuals due to the same external stimulus, which will determine the consequences of individual behavior and ultimately be reflected in enterprise performance. Therefore, clarifying the equity incentive object and deeply analyzing the psychological needs of the incentive object are the premise for enterprises to successfully implement the equity incentive plan. Only by clarifying the psychological needs of equity incentive objects and meeting their needs can they fully mobilize their enthusiasm and make their best efforts to create value for the enterprise. 2) In addition to considering the internal factors of the enterprise, the turbulence level of the external environment also determines which incentive objects the enterprise should prefer to give equity incentive. Especially in today’s unpredictable external environment, there is no “universal” equity incentive plan. Enterprises should choose the appropriate incentive object in combination with the uncertainty of their own environment in order to achieve the best effect. 3) For state-owned enterprises with high environmental uncertainty, improving enterprise performance is not the only goal of equity incentive. Therefore, in order to ensure the rapid development of state-owned enterprises, we should further improve the equity incentive system and support other corresponding incentive measures, which have important enlightenment significance for accelerating the reform of equity incentive system of state-owned enterprises. 4) As an important part of corporate governance, high-quality external audit can not only supervise and restrict the enterprise management to a certain extent, but also play an important supplementary role in the successful implementation of equity incentive plan. Therefore, relevant departments should constantly improve the external audit system to provide institutional guarantee for the rapid development of enterprises.

The existing literature lacks quantitative analysis of the economic consequences of the intensity of employee stock ownership plans, comparative research on the economic consequences of the heterogeneity of equity incentive objects, and research on the impact of environmental uncertainty on the effect of equity incentives. Although the research of this article supplements the above gaps to a certain extent, due to the limitation of the author’s time and ability, this article still has certain research limitations, which need to be further improved in the follow-up research. Specifically the following need to be included: 1) The measurement of employee stock ownership plans. The announcement date of the employee stock ownership plan of a small number of listed companies is not in the same year as the completion date of its implementation. Since these sample companies lack relevant data in the database, in accordance with academic research conventions, this article treated these sample companies as having not implemented employee stock ownership plans in the year on which the announcement was made. In the future, for the missing data in the database, questionnaires can be used to obtain relevant data as supplements. 2) The measurement of environmental uncertainty. This article adopts the common practice in academia, considers the availability of relevant data, and replaces the environmental uncertainty with the fluctuation degree of the operating income of the sample enterprises. However, environmental uncertainty is a relatively complex factor, and a more accurate indicator system can be considered to measure environmental uncertainty for further in-depth research.

The original contributions presented in the study are included in the article/Supplementary Material; further inquiries can be directed to the corresponding author.

Ethics review and approval/written informed consent were not required as per local legislation and institutional requirements.

This thesis was completed by the independent author ZT.

This work was supported by the Key Projects of National Social Science Foundation of China (19AGL014).

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Bergh, D. D., and Lawless, M. W. (1998). Portfolio restructuring and Limits to Hierarchical Governance: The Effects of Environmental Uncertainty and Diversification Strategy. Organ. Sci. 9 (1), 87–102. doi:10.1287/orsc.9.1.87

Bizjak, J. M., Brickley, J. A., and Coles, J. L. (1993). Stock-based incentive compensation and investment behavior. J. Account. Econ. 16 (1), 349–372. doi:10.1016/0165-4101(93)90017-a

Bova, F., Dou, Y., and Hope, O. K. (2015). Employee Ownership and firm disclosure. Contemp. Acc. Res. 32 (2), 639–673. doi:10.1111/1911-3846.12084

Carpenter, M. A., and Sanders, W. M. G. (2002). Top management team compensation: The missing link between CEO pay and firm performance? Strat. Mgmt. J. 23 (4), 367–375. doi:10.1002/smj.228

Chang, S., and Mayers, D. (1992). Managerial vote ownership and shareholder wealth. J. Financial Econ. 32 (1), 103–131. doi:10.1016/0304-405x(92)90027-u

Chang, X., Fu, K., Low, A., and Zhang, W. (2015). Non-executive employee stock options and corporate innovation. J. Financial Econ. 115 (1), 168–188. doi:10.1016/j.jfineco.2014.09.002

Cheng, J. L. C., and Kesner, I. F. (1997). Organizational Slack and response to Environmental Shifts: The impact of resource Allocation Patterns. J. Manag. 23 (1), 1–18. doi:10.1177/014920639702300101

Chenhall, R. H. (2003). Management control systems design within its Organizational context: Findings from contingency based research and Directions for the future. Account. Organ. Soc. 2 (8), 127–168. doi:10.1016/s0361-3682(01)00027-7

Conte, M., and Tannenbaum, A. S. (1978). Employee-owned companies: Is the difference measurable?[J]. Acad. Manag. Rev. 101 (7), 97–102.

DeFusco, R. A., Zorn, T. S., and Johnson, R. R. (1991). The Association between Executive stock Option plan changes and managerial decision making. Financ. Manag. 20 (1), 36. doi:10.2307/3666095

Dess, G., and Beard, D. (1984). Dimensions of Organizational Environments[J]. Adm. Sci. Q. 29 (1), 313–327. doi:10.2307/2393080

Ezzamel, M. (1990). The impact of environmental uncertainty, managerial autonomy and size on budget characteristics. Manag. Account. Res. 1, 181–197. doi:10.1016/s1044-5005(90)70057-1

Fan, Z., and Liu, Z. (2020). Research on the influence of executive incentives on business performance[J]. J. Hangzhou Dianzi Univ. Soc. Sci. 16 (01), 26–32.

Fang, K. (2021). Research on the relationship between employee stock ownership plan, agency cost and enterprise value. Price Theory & Pract. 12, 118–121. doi:10.19851/j.cnki.cn11-1010/f.2021.12.435

Fisher, J., and Govindarajan, V. (1992). Profit center manager compensation: An examination of market, political and human capital factors. Strat. Mgmt. J. 13 (3), 205–217. doi:10.1002/smj.4250130304

Gao, X. (2021). Research on the Influence of management ability on enterprise Innovation efficiency: Based on the moderating role of equity Incentive and environmental uncertainty[D]. Kunming: Yunnan University of Finance and Economics.

Ghosh, D., and Olsen, L. (2009). Environmental uncertainty and managers' use of discretionary accruals. Account. Organ. Soc. 34 (2), 188–205. doi:10.1016/j.aos.2008.07.001

Gordon, L. A., and Pound, J. (1990). ESOPs and corporate control. J. Financial Econ. 27 (2), 525–555. doi:10.1016/0304-405x(90)90066-9

Heron, R. A., and Lie, E. (2007). Does backdating explain the stock price pattern around executive stock option grants? J. Financial Econ. 83 (2), 271–295. doi:10.1016/j.jfineco.2005.12.003

Hochberg, Y. V., and Lindsey, L. (2010). Incentives, targeting, and firm performance: An analysis of non-executive stock Options. Rev. Financ. Stud. 23 (11), 4148–4186. doi:10.1093/rfs/hhq093

Holmstrom, B., and Costa, J. R. (1986). Managerial incentives and capital management. Q. J. Econ. 101 (4), 835. doi:10.2307/1884180

Jensen, M. C., and Meckling, W. H. (1979). Theory of the firm: Managerial behavior, agency costs, and ownership structure[M]. Springer Netherlands: Economics Social Institutions.

Jones, D. C., and Kato, T. (1995). The productivity Effects of Employee stock-Ownership plans and Bonuses: Evidence from Japanese Panel data[J]. Am. Econ. Rev. 85 (3), 391–414.

Kedia, S., and Rajgopal, S. (2009). Neighborhood matters: The impact of location on broad based stock option plans. J. Financial Econ. 92 (1), 109–127. doi:10.1016/j.jfineco.2008.03.004

Kim, E. H., and Ouimet, P. (2014). Broad-based Employee stock Ownership: Motives and Outcomes. J. Finance 69 (3), 1273–1319. doi:10.1111/jofi.12150

Kramer, B. (2010). Employee ownership and participation effects on outcomes in firms majority employee-owned through employee stock ownership plans in the US1. Econ. Industrial Democr. 31 (4), 449–476. doi:10.1177/0143831x10365574

Kumbhakar, S. C., and Dunbar, A. E. (1993). The elusive ESOP-productivity link. J. Public Econ. 52 (2), 273–283. doi:10.1016/0047-2727(93)90024-n

Li, X. (2017). An Empirical study on the influence of stock incentive intensity on the performance of listed companies[J]. J. Soc. Sci. Hunan Normal Univ. 05, 126–132. doi:10.19503/j.cnki.1000-2529.2017.05.017

Li, X., and Duan, J. (2022). Environmental uncertainty, executive incentives and corporate technological innovation: Empirical data from heavily polluting companies[J]. Friends Account. 04, 88–95.

Lie, E. (2005). On the timing of CEO stock Option Awards. Manag. Sci. 51 (5), 802–812. doi:10.1287/mnsc.1050.0365

Liu, Y., Su, G., and Wang, S. (2019). Research on the impact of Employee stock Ownership plans on the value of listed companies--based on the Empirical data of Chinese listed companies[J]. J. Yunnan Univ. Finance Econ. 11, 91–99. doi:10.16537/j.cnki.jynufe.000508

March, J. G. (1991). Exploration and Exploitation in Organizational learning. Organ. Sci. 2 (1), 71–87. doi:10.1287/orsc.2.1.71

Mauldin, E. G. (1999). Systematic differences in employee stock ownership plan contributions: Some evidence. J. Account. Public Policy 18 (2), 141–163. doi:10.1016/s0278-4254(98)10016-9

Morck, R., Wolfenzon, B., and Yeung, B. (2005). Corporate Governance, Economic Entrenchment, and Growth. J. Econ. Literature 43 (3), 655–720. doi:10.1257/002205105774431252

Paterson, T. A., and Welbourne, T. (2020). I am therefore I own: Implications of organization‐based identity for employee stock ownership. Hum. Resour. Manage. 59 (2), 175–183. doi:10.1002/hrm.21985

Pugh, W. N., Oswald, S. L., and Jahera Jr., J. S. (2000). The effect of ESOP adoptions on corporate performance: Are there really performance changes? Manage. Decis. Econ. 21 (5), 167–180. doi:10.1002/mde.971

Qiu, Y., Yu, X., and Yao, Y. (2017). Management incentives, R&D investment and corporate performance: An Empirical analysis based on state-owned listed companies[J]. Friends Account. 12, 85–89.

Rosen, C., and Quarrey, M. (1987). How well is Employee Ownership working[J]. Harv. Bus. Rev. 65 (5), 126–132.

Salancik, J., and Pfeffer, G. R. (1978). A social information processing approach to job attitudes and task design. Adm. Sci. Q. 23, 224–253.

Shen, H., Linghao, H., and Xu, J. (2018). The operating performance of state-owned enterprises implementing employee stock ownership plans: Incentive compatibility or insufficient incentives[J]. Manag. World 11, 121–133. doi:10.19744/j.cnki.11-1235/f.2018.0010

Shen, H., Peng, Y., and Wu, L. (2012). State-owned equity, environmental uncertainty and investment efficiency[J]. Econ. Res. 7, 113–126.

Shen, H., and Wu, L. (2012). The nature of equity, environmental uncertainty and the governance effect of accounting information[J]. Account. Res. 8, 8–16.

Smith, C. W., and Watts, R. L. (1992). The investment opportunity set and corporate financing, dividend, and compensation policies. J. Financial Econ. 32 (3), 263–292. doi:10.1016/0304-405x(92)90029-w

Tosi, H., Aldag, R., and Storey, R. (1973). On the measurement of the Environment: An Assessment of the Lawrence and Lorsch Environmental Uncertainty Subscale. Adm. Sci. Q. 18 (1), 27. doi:10.2307/2391925

Wang, C., and Huang, Q. (2020). Research on the impact of executive equity incentives on corporate performance[J]. Friends Account. 3, 89–96.

Wang, T., and Hu, M. (2015). Research on the impact of Equity incentives on financial performance[J]. Statistics Decis. 4, 168–172. doi:10.13546/j.cnki.tjyjc.2015.04.045

Wang, Y., Sheng, M., and Sun, H. (2019). Research on Substitution Effect of large shareholder supervision and Employee stock Ownership plan: Based on Empirical data of 2014 Employee stock Ownership system reform[J]. Finance Trade Res. 11, 94–110. doi:10.19337/j.cnki.34-1093/f.2019.11.009

Weitzman, M. L., and Kruse, D. L. (1990). Profit sharing and productivity[M]. Washington: Brookings Institution.

Williamson, O. E. (1975). Markets and Hierarchies: Analysis and Antitrust Implication[M]. New York: Free Press. DiMaggio.

Xiao, J., and Wang, R. (2022). Salary, equity and promotion, which executive incentive model is more effective for scientific research organization spin-off companies? Manag. Rev. 3401, 79–91. doi:10.14120/j.cnki.cn11-5057/f.2022.01.023

Xiao, S., Tian, J., and Liu, Y. (2012). Equity incentives, Equity concentration and corporate performance[J]. J. Beijing Inst. Technol. 14 (3), 24–32. doi:10.15918/j.jbitss1009-3370.2012.03.020

Yao, G., and Wu, Q. (2014). Research on the relationship between equity incentives, agency costs and company performance[J]. Statistics Decis. 24, 173–175. doi:10.13546/j.cnki.tjyjc.2014.24.051

Zhang, X., Chi, G., Jia, X., and Cui, Y. (2017). Innovation and application expansion of management control theory with Chinese characteristics [M]. China finance and Economics Press.

Keywords: executive equity incentive, employee stock ownership plan, enterprise performance, environmental uncertainty, empirical evidence

Citation: Tian Z (2022) Executive equity incentives, employee stock ownership plans, and enterprise performance: Empirical evidence based on environmental uncertainty. Front. Environ. Sci. 10:962409. doi: 10.3389/fenvs.2022.962409

Received: 06 June 2022; Accepted: 29 June 2022;

Published: 23 August 2022.

Edited by:

Magdalena Radulescu, University of Pitesti, RomaniaReviewed by:

Yawei Qi, Jiangxi University of Finance and Economics, ChinaCopyright © 2022 Tian. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Zhihao Tian, ODA3MzU2NDQ4QHFxLmNvbQ==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.