Tinghua Liu

Tinghua Liu Mengyuan Hu

Mengyuan Hu Ehsan Elahi

Ehsan Elahi Xiao Liu

Xiao Liu- 1School of Economics, Shandong University of Technology, Zibo, China

- 2Business School, Nanjing Xiaozhuang University, Nanjing, China

With the support of national policies and continuous emergence and innovation of emerging technologies, digital finance has developed rapidly in China. Can digital finance become a new driving force to promote quality development of economic growth? This study empirically examined the effect mechanisms of digital finance on the quality of economic growth. The study used the entropy weight and technique for order preference by similarity to an ideal solution method to construct a comprehensive index system of economic growth quality. From 2011 to 2019, the panel data of 272 cities in China were collected. The study found that digital finance can promote the quality of China’s economic growth in the long run; when digital finance development increases by one unit, the quality of economic growth will increase by 0.013%, and the effect is more significant in less developed regions. The digital finance coverage, depth of use, and degree of digitalization had a significant impact on the quality of economic growth. The mechanisms showed that digital finance can promote the quality of economic growth by promoting and upgrading the industrial structure. In addition, we used the threshold model to test the non-linear relationship between digital finance and the quality of economic growth. Furthermore, the results showed that when digital finance was at a low level, it had a negative effect on the quality of economic growth. As digital finance developed further, it had a significant effect on the quality of economic growth, and this effect gradually slowed down. Moreover, we found that digital finance played a more significant role in promoting the quality of economic growth in central and western regions and areas where traditional finance was underdeveloped. Based on this study, developing countries should strengthen the construction of digital infrastructure and give full play to the role of digital finance in improving the quality of economic growth, so as to promote sustainable and healthy economic development.

1 Introduction

For a long time, China has relied on the quantitative input of factors to drive rapid economic growth, and the economic aggregate has expanded substantially. China has become the second-largest economy in the world (Jin, 2018). However, the dividend brought by long-term extensive development will gradually disappear. At the same time, the way of high consumption, high input, and low output, and growing environmental pollution problems make the economic growth “unbalanced, uncoordinated, and unsustainable”. The speed of economic growth has also changed from high-speed development to medium- to high-speed development, and the benefits of economic growth have gradually declined. So the mode of economic development must change from scale and speed to quality and efficiency, which also means that the country begins to pay attention to the quality of economic growth. Therefore, it has become the focus of current scholars to explore new drivers of economic growth (Ren, 2020) and ensure that the quality of economic growth can be improved while economic development is fast.

As for the definition of the quality of economic growth, early foreign scholars regarded the quality of economic growth as a supplement to the growth rate (Barro and Lee, 2002). Later scholars expanded the connotation of the quality of economic growth from focusing only on the economic system to social welfare, resources and environment, people’s life, and other aspects (Hong, 1994; Ding, 2016), and it can be seen that efficiency, stability, and sustainability are the concentrated embodiment of the quality of economic growth. At the same time, finance is the core element of economic development (Teng and Ma, 2020). With the development of emerging technologies such as big data, cloud computing, Internet of Things, blockchain, artificial intelligence, and 5G communication, digital finance, as a product of the combination of traditional finance and digital technology innovation, can overcome the problems of poor access to traditional finance as well as low service quality and efficiency (Huang and Gao, 2020), in line with the needs of economic development for financial services. With the continuous integration of digital finance and economic and social fields, digital finance plays an important role in stimulating consumption, promoting innovation and entrepreneurship (Tang et al., 2020; Wan et al., 2020), and boosting exports (Jin and Zhang, 2022) and has become a new engine driving China’s economic growth. In addition, for example, in the COVID-19 outbreak, digital technology and digital finance have played an obvious role in supporting the fight against COVID-19 and restoring production and life. Digital finance is becoming a key force in restructuring global factor resources, reshaping the global economic structure, and changing the global competition pattern.

Although the aforementioned studies linked digital finance with economic development, most of them only focused on one aspect of the economic effect, without exploring the impact of digital finance on the quality of economic growth from the whole level. Then what is the impact of digital finance on the quality of economic growth? How does this effect differ across regions? What is the influence mechanism between them? This study explored the mechanism of digital finance on the quality of economic growth from the perspective of industrial structure upgradation and also explored the non-linear impact of digital finance on the economy. The aforementioned discussion is conducive to improving the allocation efficiency of resources, giving full play to the supporting role of finance in the benign and sustainable economic development, and is of great significance to the realization of high-quality economic development.

2 Literature review

To explores the influence of digital finance on the quality of economic growth, this study sorts out relevant literature from three aspects: the quality of economic growth, digital finance, and the economic effect of digital finance.

2.1 The definition of economic growth quality

The first type of research focuses on the definition of economic growth. Previous studies can be summarized into two perspectives: narrow and broad. From a narrow perspective, the connotation of growth quality is considered unitary. For example, growth quality was initially defined as growth efficiency, while Камаев (1983) believed that it was the use efficiency of input factors. In terms of measurement methods, the growth quality, in a narrow sense, is mostly measured by a single indicator, such as total factor productivity (Lucas, 1989; Xie et al., 1995), ratio of innovation to economic growth (Qian, 1996), and technological efficiency. From a broad perspective, the connotation of growth quality is considered to be diversified. For example, Belton (2017) studied the connotation and influence of economic development quality from the perspective of capital flow and openness. Other scholars extend the quality of growth from the single production level to the level of social life. For example, the quality of growth is extended from the economic system to the perspective of welfare related to the economic system (Hong, 1994; Mlachila et al., 2017), as well as political, social, and religious perfection (Barro and Lee, 2002). Studies emphasized that the quality should reflect the improvement of economic efficiency, stability, sustainability, economic structure, and social welfare. For example, Wang (2006) summarized the quality of growth as the sustainability of growth mode, coordination of the growth structure, harmony of growth benefits, and stability of growth. Chao and Ren (2011) measured the quality of China’s provincial growth by reducing the dimension of indicators from four aspects of growth structure: stability, welfare change, achievement distribution, and resources and ecology. Sui and Liu (2014) measured the growth quality of Asia-Pacific, Africa, and Latin America in terms of efficiency, stability, and sustainability of economic growth.

2.2 The connotation of digital finance

The second type of research focuses on the implications of digital finance. Digital finance as a new concept is derived from the development of finance, and the understanding of its meaning should be summarized from the development of the concept. Levine (2005) defines financial development as the ratio of the financial scale to the economic scale. Since the concept of financial inclusion was put forward, the academic circle has carried out a series of studies on it. Sarma and Pais (2011) defined the development level of inclusive finance from three dimensions. Van Rooij et al. (2012) believed that inclusive finance benefits various social groups and improves individual life quality. China’s digital finance is the product of the combination of Internet technology and finance. It is a financial service mode formed by the combination of digital technology and financial innovation. Specifically, it is the combination of financial services and digital technologies such as the Internet (mobile Internet and Internet of Things), big data, distributed technology (cloud computing and blockchain), artificial intelligence, and information security (biometrics and encryption). It is similar to the definition of Internet finance and fintech, and it can provide more economic subjects with “efficient, responsible, and commercially sustainable” financial services with lower capital costs and more convenient services (Teng and Ma, 2020). China’s digital finance started from the launch of the Alipay account system in 2004. After that, digital finance developed rapidly in China, mainly due to the shortage of supply of traditional financial services, relatively inclusive financial regulation, and rapid development of digital technology. But at the same time, a unified regulatory system for the digital finance industry should be established to effectively prevent and control risks (Huang and Huang, 2018).

2.3 Digital finance and the quality of economic growth

The third type of research focuses on the economic effects of digital finance. Can the development of digital finance significantly affect the quality of economic growth? In previous studies, most scholars focus on a certain aspect of its economic effect, for example, pollution reduction (Xu et al., 2021), technological innovation (Tang et al., 2020; Wan et al., 2020), urban–rural gap (Jeanneney and Kpodar, 2008; Fu et al., 2021), and entrepreneurship (Xie et al., 2018). In addition, digital finance also promotes inclusive growth (Fu et al., 2021) and stimulates household consumption (Li et al., 2020), alleviating financing constraints of enterprises (Beck et al., 2007) and improving the efficiency of banks (Du and Liu, 2022). Other scholars have studied the impact of digital finance on the quality of economic growth as a whole (Qian et al., 2020; Teng and Ma, 2020), and the results show that digital finance can promote the high-quality development of China’s economy.

The main contributions of this study are as follows: first, in terms of data selection, statistical data of 272 cities at the prefecture level and above in China from 2011 to 2019 are used in this study, compared with previous studies using provincial data (Qian et al., 2020; Teng and Ma, 2020). Therefore, the research conclusions are more authentic and reliable. Second, from the perspective of analysis, this study establishes a theoretical analysis framework of the influence of digital finance on the quality of economic growth based on the three perspectives of economic growth efficiency, economic growth stability, and sustainability to make the theoretical mechanism clearer. Third, in terms of research methods, most previous studies have studied the linear impact of digital finance on the quality of economic growth. In this study, the threshold effect model is used to explore the non-linear mechanism of digital finance on the quality of economic growth.

3 Theoretical analysis and research hypotheses

This part describes the theoretical mechanism and focuses on the research hypotheses from the perspective of the overall influence of digital finance and the mechanism influence of the industrial structure upgradation.

3.1 Digital finance and the quality of economic growth

Different from the high-speed growth period of the past three decades, China’s economy has entered a “new normal” stage, transforming from high-speed growth to high-quality growth. The reduction of factor supply efficiency, resource allocation efficiency, lack of innovation ability, and the enhancement of resource and environment constraints reflected in economic structural deceleration restrict China’s economic development in the new stage. At present, digital finance, as a combination of digital technology and financial innovation, is booming and has become new support and driving force for future economic development. Digital finance can complement the shortcomings of traditional financial services through scenarios, data, and financial innovative products; give full play to the advantages of “low cost, fast speed, and wide coverage”; and reduce the threshold of financial services and service costs (Huang and Huang, 2018), thus enhancing the convenience of financial services. This convenience not only promotes the economy of the traditional financially developed areas but also improves the financial service efficiency of the traditional financially less developed areas. From the perspective of the efficiency of economic growth, on the one hand, due to the small- and medium-sized enterprises is the long tail of the financial markets group; constrained by cost and technology, the traditional financial cannot efficiently implement to combine with this part of the group (Wan et al., 2020). Therefore, it makes the small- and medium-sized enterprise credit rationing problems to exist for a long time, but digital finance changes payment methods, greatly reducing search costs, evaluation of costs, and transaction costs (Li, 2015). It also improves the efficiency of the financial risks of enterprise identification and disposal efficiency to enrich the financial product supply and availability (Liu, 2021) and helps enterprises to overcome the internal and external conditions. Furthermore, digital finance reduces small- and medium-sized enterprise financing costs. Thus, the financing difficulties of enterprises are relieved, R&D costs of enterprises are guaranteed, technological innovation is facilitated, and the improvement of technological capability and total factor productivity of enterprises is ultimately promoted (Jiang and Jiang, 2021; Sun, 2021). On the other hand, the agricultural sector and agricultural producers are also in a weak position in the financial market. Therefore, it may affect negatively on the productivity of farms. The development of digital finance can also ease the credit constraints of farmers (Fu et al., 2021; Zheng and Li, 2022) and promote the improvement of agricultural total factor productivity, thus improving the efficiency of economic growth. From the perspective of the stability of economic growth, the prominent inclusive characteristics of digital finance not only expand the scope of financial services but also reduce financial costs. For example, “agriculture, rural areas” groups can obtain loans more easily and quickly through financial institutions, or agricultural production can be monitored and forecasted better through digitization. Digital finance also makes financial products more accessible to the “long tail group”, arouses their awareness of financial management (Fu et al., 2021), and provides them with better financial services to reduce the urban–rural income gap and stabilize economic growth. In addition, digital finance can promote inclusive economic growth (Fu et al., 2021), which plays a positive role in improving the urban–rural gap and balancing regional economic development (Zhou and Chen, 2022), thus promoting the stability of economic growth. From the perspective of the sustainability of economic growth, digital finance makes full use of digital technology to bring about the reform of residents’ consumption payment methods, especially the emergence of online payment methods such as Alipay and WeChat, which reduces the use of cash, transaction costs, and resource consumption (Xu et al., 2021). It is worth mentioning that Alipay launched the “Ant Forest” environmental protection service platform, which also promoted people’s awareness of green environmental protection and encouraged residents to carry out green consumption. In agricultural production, the application of digital technology can reduce the use of pesticides and make the production of crops shift in a cleaner and environmentally friendly direction. At the same time, the use of renewable energy in agricultural production relying on digital technology can reduce production risks, save production costs, and alleviate agricultural pollution emissions. Enterprises also use digital technology to improve the original production technology to promote its development in the direction of more energy conservation and emission reduction. All these reflect the green leading effect of digital finance (Liu et al., 2021) and promote the sustainability of economic growth. Thus, digital finance plays an effective role in the efficiency, stability, and sustainability of economic growth, ultimately acting on the quality of economic growth and promoting the improvement of economic growth quality.

3.2 A nexus between digital finance and quality of economic growth

Upgrading the industrial structure is one of the important factors of modern economic development and a key element to evaluate the level of economic development of a country or region. However, finance is an important driving force to promote the upgradation of the industrial structure (Levine, 1996). In the 14th Five-Year Plan period, China’s industrial structure change will go in a high-quality development of policy guidance in the new period, the requirement of high-quality development and upgrading industrial structure adjustment is consistent, are inadequate to solve the unbalanced development of contradictions, and satisfy the people to the important content of the growing demand for a better life. For a long time, China’s economic growth has depended on the structural acceleration benefits brought by the acceleration of industrialization. However, in recent years, China is in the transition period of industrial structure, which means that the “structural acceleration” benefits gradually disappear, leading to the decline of economic growth. China’s economy has entered the era of “structural deceleration” (Xie and Pan, 2018). Previous studies found that when the matching degree of financial and industrial structure upgradation becomes higher, it is conducive to improving the efficiency of resource allocation, thus promoting economic growth (Wang and Zhang, 2022). This means that financial development can promote economic growth through industrial structure upgradation (Chen and Zhang, 2017), which is a mechanism study on the role of industrial structure upgradation in financial development and economic growth. Digital finance is the product of the fusion of finance and digital technology and is also a part of finance in essence. Then what role does industrial structure upgradation plays in digital finance and the quality of economic growth? In view of this problem, the following will be sorted out from four aspects to achieve a clear understanding of the mechanism of this study. First, it can accelerate industrial differentiation and restructuring. Digital finance gains consumer data with the advantages of the digital technology and Internet trading platform through the market application of information technology and management innovation (Xu et al., 2021). Digital finance can speed up the industrial differentiation and reorganization, promote fusion and correlation between the industry and upstream and downstream industries that can be formed based on industrial convergence of new industries and new formats (Zhang, 2018; Zhang, 2019; Liang et al., 2021), and ultimately promote the upgradation of industrial structure. Second, it can reduce the financial service threshold and financing cost of industrial subjects. By increasing the coverage of financial services, digital finance reduces the threshold for industrial subjects to obtain financial services and the information cost of financing of industrial subjects and broadens financing channels (Li and Ran, 2021), thus achieving a more effective and accurate allocation of factors and promoting the upgradation of industrial structure. Therefore, the quality and efficiency of industrial development are further improved (Bruhn and Love, 2014). Third, it can improve the use efficiency of industrial funds. Through information-based selection technology, digital finance can guide the flow of idle financial resources in the society and make funds effectively enter the industrial fields with growth and sustainability (Li and Ran, 2021) to improve the efficiency of capital use, reshape the direction of industrial development, and promote the optimization and upgradation of industrial structure (Nie et al., 2021). Fourth, it can stimulate consumption and force the industrial chain to upgrade. Digital infrastructure makes residents’ transactions more convenient and improves the residents’ consumption demand; in addition, by using its universality, digital finance reduces rural financial exclusion, thus reducing the consumption cost, stimulating consumption, and increasing residents’ demand (Xu et al., 2021). Furthermore, it can force production enterprises to upgrade the industrial chain (Gao, 2019) and, finally, promote the optimization and upgradation of industrial structure. Through the role of the aforementioned aspects, digital finance promotes the upgradation of industrial structure. The upgradation of industrial structure can optimize the combination of production factors, make labor and human capital flow to efficient production departments, directly improve the production efficiency of related industries, improve social labor productivity and total factor productivity (Sui, 2017; Zhou et al., 2021), and realize the improvement of economic growth efficiency. In addition, the upgradation of industrial structure can promote the supply-side structural reform, promote inclusive economic growth, narrow the income gap between urban and rural areas, balance regional economic development, and finally achieve the stability of economic growth. At the same time, with the help of digital technology, the focus of industrial funds is transferred to green industries such as new energy, energy conservation, and environmental protection to transform the industrial structure from labor-intensive and heavy industry to high-tech and environmentally friendly and promote sustainable economic growth. Thus, digital finance can promote the efficiency, stability, and sustainability of economic growth by promoting the upgradation of industrial structure and ultimately promote the improvement of growth quality. Based on the aforementioned analysis, we have proposed the following hypotheses:

Hypothesis 1: Digital finance can effectively improve the quality of China’s economic growth.

Hypothesis 2: Digital finance can improve the quality of economic growth by promoting the upgradation of industrial structure.

4 Materials and methods

4.1 Data source

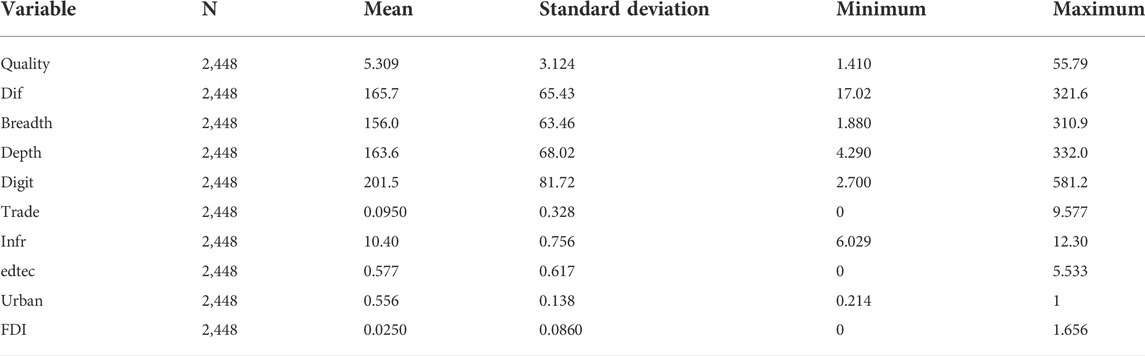

The data of proxy indicators and control variables in the quality index system of economic growth came from China Statistical Yearbook, local Statistical Yearbook, China Population and Employment Statistical Yearbook, and China Energy Statistical Yearbook, and the missing data were completed by the interpolation method. The digital finance index came from the China Digital Inclusive Finance Development Index released by the Digital Finance Research Center of Peking University. Considering the availability and uniformity of data, this study chose panel data of 272 cities in China from 2011 to 2019 as the research sample. The data in this study were deflated based on 2009. The descriptive statistics of our main variables are shown in Table 1.

TABLE 1. Summary of descriptive statistics.

4.2 Econometric model

Based on the aforementioned theoretical analysis, to study the impact of digital finance on the quality of economic growth, this study establishes the following regression model:

where

This study will test hypothesis 2 by using the mediating effect model. The mediation effect mainly includes three basic steps, and the model can be constructed as follows:

where the intermediary variable and the other variables have the same meanings as before. Function 1 is the regression function of the economic growth quality to digital finance. Function 2 is the regression function of the industrial structure upgradation to digital finance. Based on functions 1 and 3, we added the intermediary variable of industrial structure upgradation to regression digital finance with the quality of economic growth.

4.3 Selection and measurement of key indicators

4.3.1 Economic growth quality

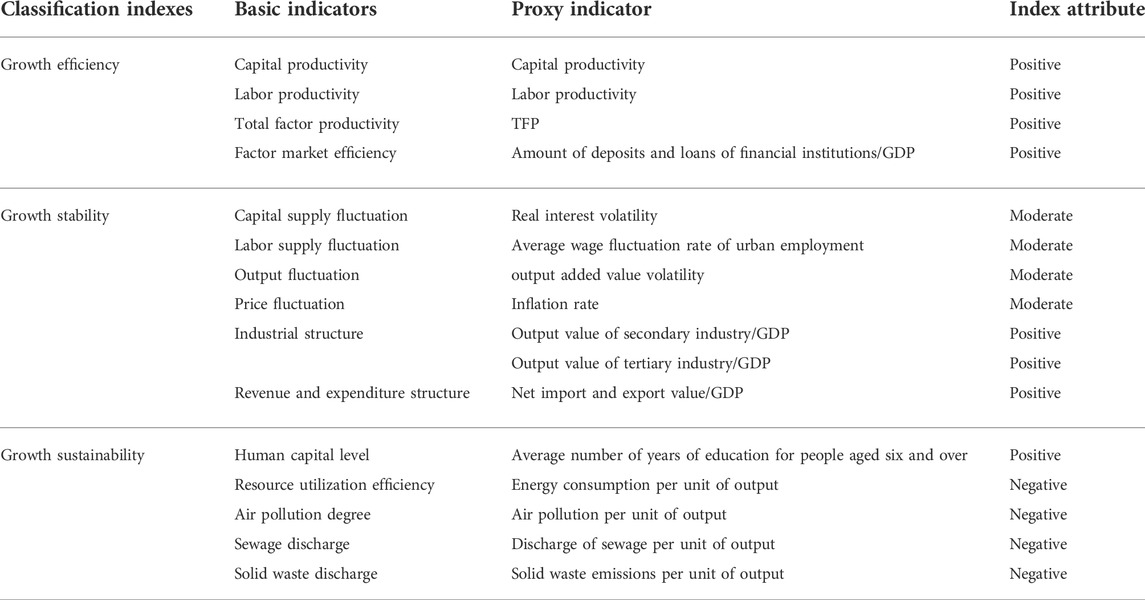

On the basis of existing studies, this study referred to the construction of ideas of economic growth quality indicators proposed by Sui et al. (2017). Moreover, it determined the quality of economic growth from three aspects: efficiency, stability, and sustainability of growth. Considering the availability of data, this study finally constructed an economic growth quality index system, including three classifications indexes and 15 basic indexes (Table 2).

TABLE 2. Comprehensive evaluation index system of economic growth quality.

As for the method of index construction, the previous studies mainly used the factor analysis method, analytic hierarchy process method, and principal component analysis method to measure economic growth or high-quality economic development. In this study, the entropy weight TOPSIS method was used to combine the entropy weight method with the TOPSIS method. On the one hand, the objective advantage of the entropy weight method in weight assignment can be brought into play. On the other hand, the TOPSIS method can make use of the ranking advantage of the best and the worst to measure the quality of economic growth in various regions in a more reasonable way. In the calculation process to eliminate the differences caused by different dimensions of indicators, the range method was used to standardize all indicators.

If

If

If

4.3.2 Digital finance index

A set of digital inclusive financial indexes jointly compiled by The Digital Finance Research Center of Peking University and Ant Financial Research Institute was adopted. The index establishes a digital inclusive financial index system including 24 secondary indicators from three dimensions: coverage, depth of use, and degree of digitalization. Since it is scientifically calculated by dimensionless quantification, weighting method of coefficient of variation, and exponential synthesis method, it has strong authenticity, authority, and credibility. Therefore, this study chose it as the core explanatory variable of the research content (Guo et al., 2020).

4.3.3 Intermediate variable

To measure the upgradation of industrial structure, this study used the method of Fu (2010) for reference and defined it as follows: first, GDP was divided into three parts according to the three industry divisions, and the proportion of the added value of each part in GDP was taken as a component of the space vector, thus forming a set of three-dimensional vectors. Then the angle

Then the function of the industrial advanced can be written as follows:

4.3.4 Control variable

Various control variables have been used in this study. In particular, the trade dependence variable represents trade, which is measured by the proportion of total imports and export in GDP. The urbanization rate represents urban, which is expressed as the proportion of the urban population in the total population. Infrastructure construction represents Infr, which is measured by regional per capita fixed asset investment. Science and education expenditure represents edtec, which is measured by the proportion of science and technology expenditure and education expenditure occupied by the municipal total financial expenditure. Similarly, foreign direct investment represents FDI, which is referred to the proportion of foreign direct investment in GDP.

4.3.5 Instrumental variables

Although the relevant variables were controlled in this study, the endogeneity problem still exists. Endogenous sources mainly have two aspects. On the one hand, the digital reverses causality between financial and economic growth quality, namely, digital finance development promotes economic growth quality and the quality of economic growth, at the same time, it improves also makes the Internet progress toward more convenience and low cost to promote the development of digital finance. On the other hand, this study selected some variables as factors affecting the quality of economic growth and added them to the model. However, there are still some missing variables that are not taken into account. Therefore, in this study, we adopted the instrumental variable method to solve the estimation bias caused by endogenous problems. Referring to Zhang et al. (2020), this study selected the spherical distance between Hangzhou and other cities as instrumental variables. On the one hand, digital finance represented by Alipay originated in Hangzhou. Hangzhou is in a leading position in the development of digital finance. There will be better the development of digital finance if the area will close to Hangzhou. Therefore, this instrumental variable meets the requirements closely related to the explanatory variable. On the other hand, the distance from Hangzhou does not affect the quality of economic growth through other omitted variables, which can be used as an instrumental variable. In addition, since this instrumental variable does not change with time, we referred to the practice of Zhang et al. (2020) selection of instrumental variables with the mean value of the digital financial index in all cities (except Hangzhou), making it an instrumental variable with time effect.

5 Results and discussion

In this section, we empirically estimated the impact of digital finance on the quality of economic growth by using fixed effect and other measurement methods and also conducted heterogeneity and robustness tests.

5.1 Results of baseline regression

5.1.1 Digital finance development and quality of economic growth

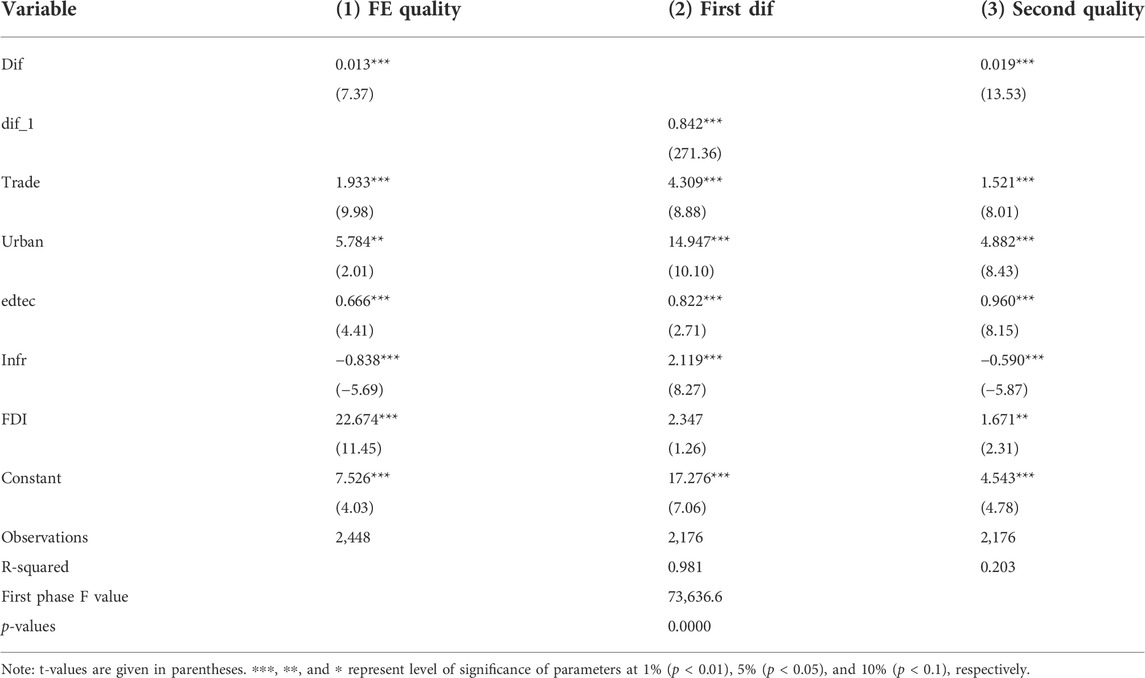

In the benchmark regression model, without considering endogeneity, this study used the fixed-effect model to explore the influence of digital finance on the quality of economic growth. Column 1 of Table 3 reports the impact of digital finance on the quality of economic growth. The results show that the coefficient of digital finance is positive at the significance level of 1%, indicating that the development of digital finance has a significant role in promoting the quality of economic growth. Considering the endogeneity problem, the digital finance lag value dif_1 was used as the instrumental variable, and the two-stage least squares (2SLS) estimation method was used to re-estimate the model. Column 2 of Table 3 reports the regression results in the first stage after the addition of instrumental variables. The probability value of the F statistic in the first stage is less than 0.05, indicating that the selected instrumental variables are valid. It means that there is no weak instrumental variable problem. Meanwhile, from the regression results, Durbin–Wu–Hausman results rejected the null hypothesis. This implies that there is no endogeneity at the 1% level. In addition, the coefficient of DIF was significantly positive at the 1% level, at 0.019. Therefore, the regression coefficient of DIF is significantly positive in both the benchmark regression and the regression-based on instrumental variables, and the conclusion is similar to the Qian et al.(2020) and Wang et al.(2021). However, their research uses provincial panel data, and Wang et al. ’s analysis of how digital finance affects the quality of economic growth as a whole is not clear and detailed, with a general perspective. This study analyzes the efficiency, stability and sustainability of economic growth from three aspects, and finally reaches a similar conclusion: digital finance has a significant role in promoting economic growth.

TABLE 3. Baseline regression results of digital finance to the quality of economic growth.

5.1.2 The subdimension of digital finance and the quality of economic growth

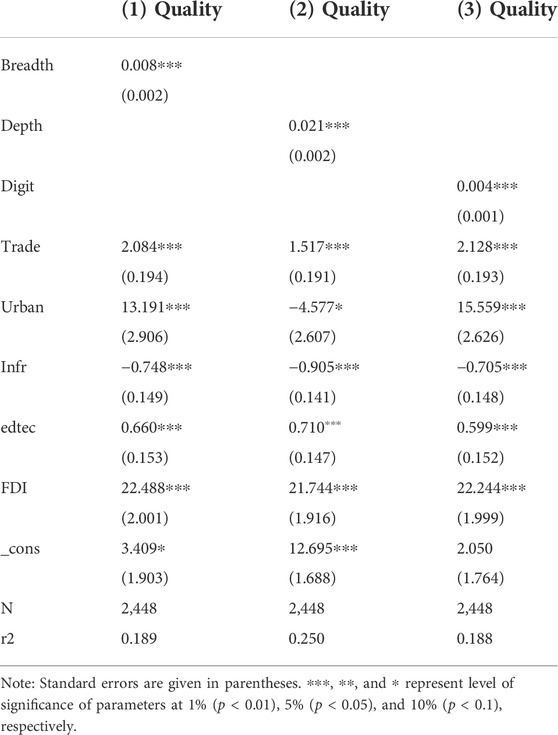

The digital finance index contains three subdimension indexes such as the coverage of digital finance, the depth of digital finance use and the degree of digitalization. Therefore, this study analyzed the impact of these subdimension indicators on the quality of economic growth. A fixed-effect model was used for estimation, and regression (Table 4). Digital finance covers a wide range of areas. Regression results showed that the coverage of digital finance significantly promotes the improvement of economic growth quality. As the coverage breadth of digital finance refers to expanding the scope of digital financial services and providing a sufficient amount of financial services, it plays a positive role in improving the quality of economic growth. Furthermore, results found that the depth of digital finance significantly promoted the improvement of economic growth quality. The use of digital finance deeply emphasizes the diversified services provided by digital finance, such as credit, insurance, and credit. These diversified services stimulate residents’ further demand for digital finance, which is conducive to the improvement of economic growth quality. Regarding the digital financial support service level digit, it is found that the degree of digital financial support can significantly improve the quality of economic growth. The degree of digital financial support emphasizes the convenience and low cost of obtaining financial services, which makes it more convenient for residents to obtain financial services, thus stimulating residents’ consumption demand, contributing to economic growth, and improving the quality of economic growth.

TABLE 4. Results of the digital finance subdimension test.

5.2 Heterogeneity test

5.2.1 Regional heterogeneity

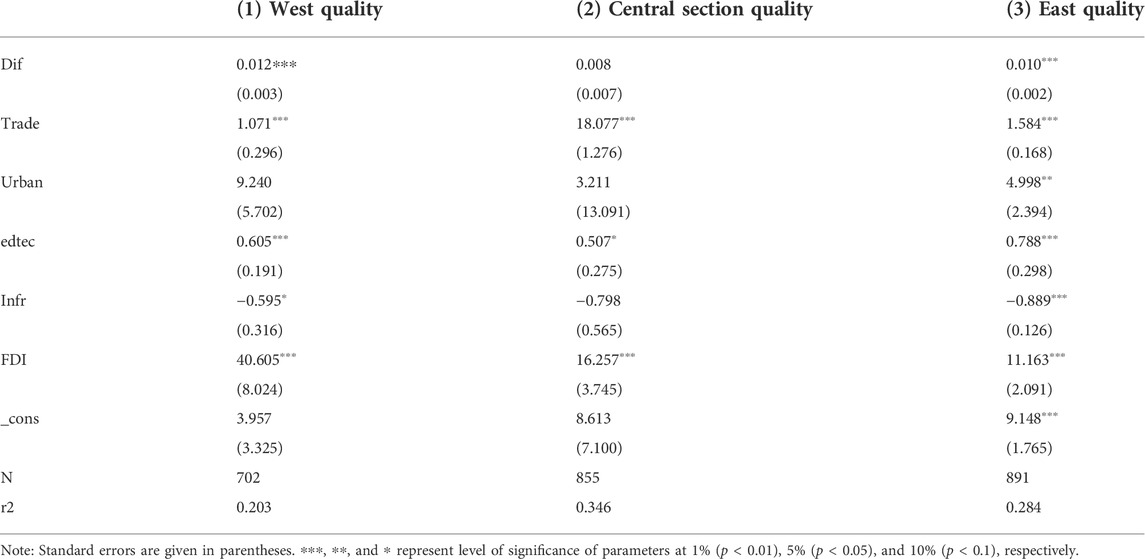

Previous studies have shown that regional differences are one of the factors affecting the development level of digital finance. Therefore, the 272 cities were divided into three regions of eastern, central and western regions for regression. It is found that the coefficient of DIF is 0.012 is significant at the statistical level of 1%, indicating that the development of digital finance in western China can promote the improvement of the quality of economic growth (Table 5). Column 2 of Table 5 showed the regression result of the influence of digital finance on the quality of economic growth in central China. The coefficient of DIF is 0.008, indicating that the influence of digital finance development in central China on the quality of economic growth is positive but not significant. The given results in column 3 of Table 5 found that digital finance on the quality of economic growth in eastern China. The coefficient of DIF is 0.010, which is significant at the statistical level of 1%, indicating that digital finance development in eastern China plays a role in promoting the quality of economic growth. In general, the development of digital finance in western China plays the strongest role in promoting the quality of economic growth. For the less developed areas in western China, digital finance can play a more inclusive role, make up for the deficiency of traditional financial services, and reduce the threshold and cost of financial services for residents and enterprises. As the traditional financial services in the eastern region are more complete than those in the western region, digital financial services attract more entrepreneurs. Therefore, compared with developed areas, digital finance plays a greater role in promoting the quality of economic growth in less developed areas.

TABLE 5. Results of the regional heterogeneity test.

5.2.2 Differences in levels of financial development

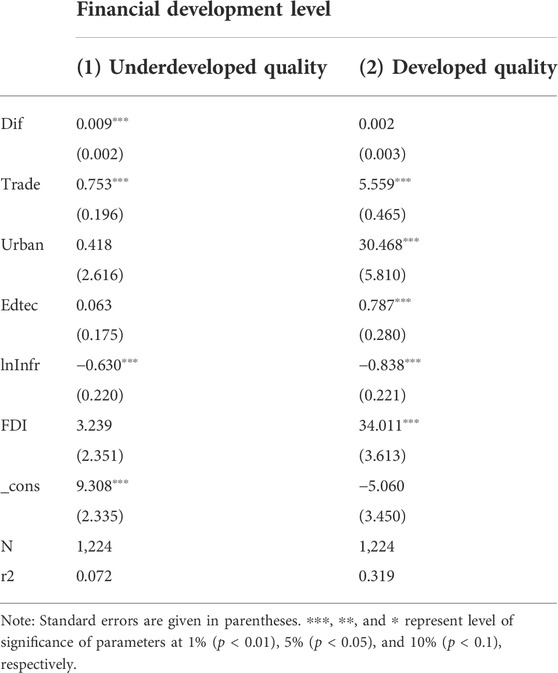

The development level of traditional finance can also have an impact on the development of digital finance. Therefore, according to the median development level of traditional finance in cities (loan balance of urban financial institutions/urban GNP), 272 cities were divided into developed and underdeveloped financial cities. The grouped empirical results are shown in columns 1 and 2 of Table 6. Results found that the coefficient of cities with a high level of financial development is 0.002, which does not pass the significance test. Cities with a low level of financial development have a coefficient of 0.009, passing the significance test at a confidence level of 1%. The possible explanation is that the development of digital finance only plays a role of “icing on the cake” in areas with a high level of traditional financial development. It plays a role based on the originally developed financial system. In cities with a low development level of traditional finance, digital finance reduces the threshold of financial services, broadens the scope of financial coverage, and plays a role in “delivering charcoal in the snow”. Therefore, it has a significant impact on the quality of economic growth.

TABLE 6. Results of the heterogeneity test of the financial development level.

5.3 Robustness test

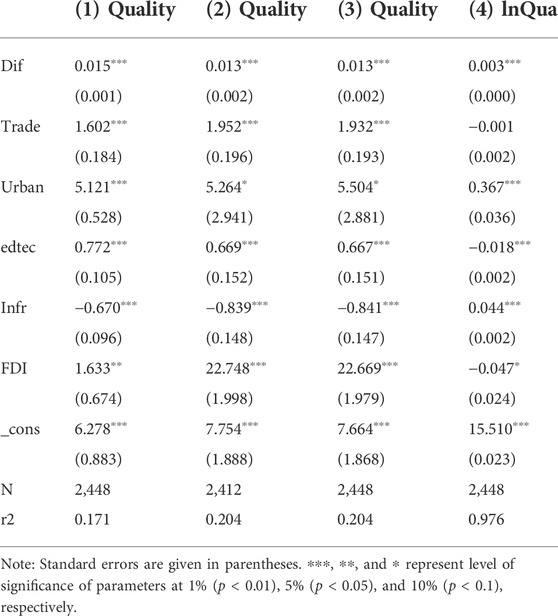

It found that digital finance improved the quality of economic growth from various dimensions. To ensure the reliability of the results, we have followed the method of Teng and Ma (2020) for checking the robustness.

The measurement method was changed. The distance between each city and Hangzhou was taken as the instrumental variable, and the instrumental variable passed both the “unrecognizable” test and the “weak instrumental variable” test, which verified the validity of the results of the instrumental variable. The regression results are given in column 1 of Table 7. There is still a positive promoting relationship between digital finance and the quality of economic growth, and the parameters and significance of explanatory variables did not change significantly. It indicated that the results of this study are robust.

TABLE 7. Results of robustness tests.

Municipalities were excluded. To verify the robustness of the results, this study excluded the more developed municipalities directly under the central government to avoid the impact of regional economic development imbalance on the empirical results and then carried out regression. The results are shown in column 2 of Table 7. The parameters and significance of explanatory variables do not change significantly, indicating the results are robust.

The panel regression of fixed effects was carried out in this study after reduction of tail reduction at 1% level for the main explanatory variable. The results are shown in column 3 of Table 7. It is found that the parameter estimation and level of significance did not change. It indicates the results are robust.

Furthermore, after taking the logarithm of the comprehensive index of economic growth quality, panel regression of fixed effect was carried out in this study (Table 7). The results are shown in column 4 of Table 7. Parameter estimation and level of significance did not change, indicating the results are robust.

In the next step, we used the mediation model to verify the existence of the mediation effect of industrial structure, and the threshold model was used to verify the non-linear effect of digital finance.

5.4 Mediation effect

Table 8 is the inspection of the industrial structure upgrade ACTS as an intermediary variable. According to the aforementioned principle, the results found that the empirical results of column (1) figures in the financial significantly the quality of economic growth is positive, column (2) of the digital finance have significant positive effects on industrial structure upgrade, column (3) for the upgradation of the industrial structure of the quality also has a significant positive influence on economic growth, at the same time compared to the column (1), The fitting coefficient of digital finance in column (3) becomes smaller, indicating that the upgradation of the industrial structure plays a partial intermediary effect in the impact of digital finance on the quality of economic growth. So hypothesis 2 was tested.

TABLE 8. Results of mediation mechanism testing.

5.5 Threshold effect

It is found that the advanced industrial structure plays an intermediary role and digital finance can effectively improve the quality of economic growth. However, due to the different development levels of digital finance, the intensity of its impact on the quality of economic growth may be different. Therefore, this study further studied whether there was a non-linear effect of such promotion. The panel threshold model proposed by Hansen (2000) was used to test whether the aforementioned non-linear relationship is valid. We have followed the given model.

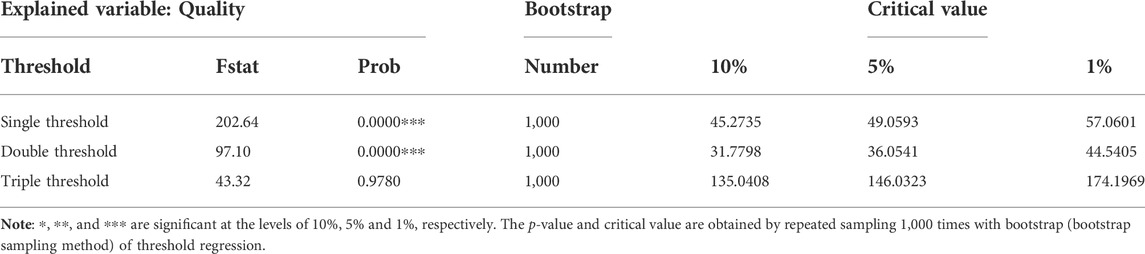

where I (∙) is the indicator function, and the other variables have already been explained. Firstly, the bootstrap method was used to judge whether there was a digital financial threshold effect. The given results in Tables 9, 10 found that both single and double thresholds of digital finance passed the significant test.

TABLE 9. Results of the threshold effect test.

TABLE 10. Result of threshold estimation.

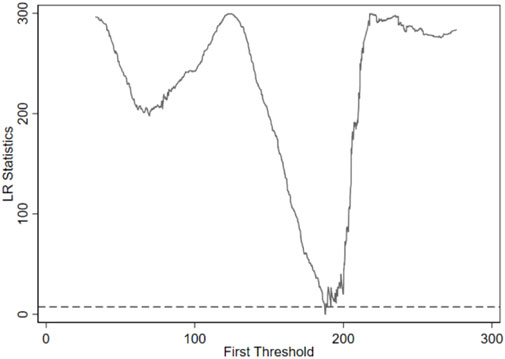

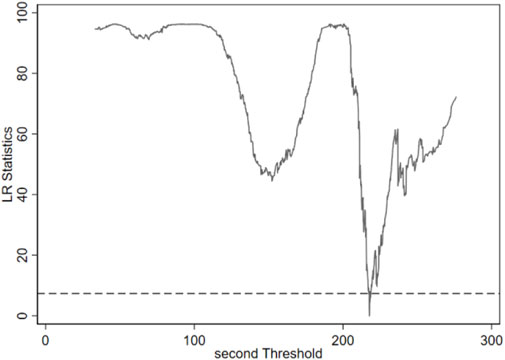

According to the principle of the threshold model, the threshold estimation value is the corresponding γ value when the likelihood ratio statistic LR approaches 0 (Table 10). Figure 1 and Figure 2 are the diagrams of the likelihood ratio function of the two threshold estimation values 187.90 and 217.74 of digital finance under a 95% confidence interval. The lowest point of LR statistics is the corresponding real threshold value.

FIGURE 1. Results of the first round estimate of the threshold variable dif.

FIGURE 2. Results of the second round estimate of the threshold variable dif.

The results of the double threshold estimation of digital finance are given in Table 11. It is found that when the development level of digital finance is lower than the first threshold value of 187.90, the estimation coefficient of digital finance on the quality of economic growth is relatively small and negative −0.001036, indicating that when the development of digital finance is in the initial stage, it inhibits the improvement of the quality of economic growth. This can be explained by the high cost of digital infrastructure construction and intangible asset investment in the early stage, which makes the marginal revenue brought by the development of digital finance lower than the marginal cost. When the number of financial development in the first threshold value between 187.90 and the second threshold value of 217.74, the digital finance estimate of the economic growth quality coefficient was 0.014, indicating that the digital finance with big data, cloud computing, such as the development of information technology, reduces the threshold of the financial services, optimize the allocation of resources, and promote the economic growth quality of ascension. When digital finance passes the second threshold value of 217.74, the estimated coefficient of digital finance on the quality of economic growth is 0.0072, less than 0.014, indicating that when the development level of digital finance reaches a certain height, the promotion effect of digital finance on the quality of economic growth begins to slow down.

TABLE 11. Result of threshold model regression.

6 Discussion

Digital finance, as a new form of business produced by the combination of digital technology and finance, has an important impact on economic growth. Previous studies have discussed the impact of digital finance on the quality of economic growth, but the research data are relatively rough, mainly using panel data at the provincial level (Qian et al., 2020; Teng and Ma, 2020). In order to draw more reliable conclusions, this study adopts city-level data for empirical analysis. The development of digital technology promotes industrial differentiation, reorganization, or integration, and some new industrial forms also come into being. How does the industrial structure play a role in the process of digital finance affecting the quality of economic growth? Although there have been previous studies, there are few analysis perspectives (Wang et al., 2021). This study analyzes the mechanism of industrial structure upgradation in detail from three perspectives: efficiency, stability, and sustainability of economic growth. It more clearly shows how digital finance can improve the quality of economic growth by promoting the upgradation of industrial structure. In addition, this study further studies the non-linear influence of digital finance. When digital finance develops to different degrees, it has different effects on the quality of economic growth. Compared with the previous linear perspective, this study enriches the research in this field.

7 Conclusion

Based on the development of digital finance in China, this study used the data of 272 cities in China from 2011 to 2019 to construct an index system of economic growth quality from three aspects of economic growth, efficiency, stability, and sustainability, by using entropy weight and technique for order preference by similarity to an ideal solution method and empirically tested the impact of digital finance on economic growth quality. The study found that in the long run, digital finance can significantly promote the improvement of the quality of economic growth. When digital finance is at a low level, it had a negative effect on the quality of economic growth. It will significantly promote the quality of economic growth and this promotion will gradually slow down with the further development of digital finance. The coverage of digital finance, depth of use, and degree of digitalization can promote the quality of economic growth. Regarding the performance of the regional sample, compared with the eastern region, digital finance plays a more significant role to promote the quality of economic growth in the western region. While for the central region, the effect of digital finance is positive but not significant. In the subsample of financial development levels, digital finance plays a more significant role in promoting the quality of economic growth in cities with low financial development levels compared with cities with high financial development levels. Therefore, it is found that digital finance plays a more significant role in promoting the quality of economic growth in less developed cities compared with developed regions. The upgradation of the industrial structure plays a mediating effect in the impact of digital finance on the quality of economic growth, that is, the upgradation of industrial structure strengthens the promoting effect of digital finance on the quality of economic growth, and digital finance can improve the quality of economic growth by promoting the upgradation of industrial structure.

8 Policy implications

Compared with developed countries, the development of digital finance in China still needs to be improved. Therefore, the study suggests the following policy implications. First, we should continue to promote the construction of digital finance. The government should focus on developing digital finance by further deepening the research and development and application of modern information technologies such as big data, cloud computing, and artificial intelligence; accelerating the cultivation of digital industries; enhancing the depth and coverage of digital finance; and promoting the coordinated development of digital finance among regions. Also, the government should make full use of digital technology, build industrial cloud platform, promote big data sharing, break information asymmetry, and promote the transformation of industrial form.

Second, we should speed up the deep integration of digital technology with traditional industries, strengthen the integration of digital technology with real industries, fully release the capacity enlargement effect of digital technology, vigorously promote the transformation of traditional industries, and tap the development potential of more industries. The government should issue relevant policies to fully guide leading enterprises to carry out industrial transformation, thus driving the transformation and upgradation of the upstream and downstream industrial chain, and finally enabling the quality improvement of economic growth. At the same time, the driving effect of digital finance on the quality of economic growth should be released according to the differences between different regions and cities. In addition, the government should correctly view the coordinated development relationship between various industries to prevent excessive virtualization of economic development.

Third, we should strengthen the cultivation of digital talents. Digital technology has emerged as a new high-end technology, and the cultivation and use of talents are crucial for its development. The government should introduce relevant policy support and provide funds and tax subsidies to enterprises in cultivating digital talents. At the same time, the government, enterprises, colleges, and universities should play a role to jointly build digital talent training, use, reserve, and evaluation system. Also, it is necessary to build a number of training bases for digital technology professionals by relying on key universities, enterprises, and industrial parks and strengthen the training of high-end digital talents.

Fourth, we should strengthen financial supervision, advance reform of the financial system, and effectively prevent and control financial risks. The essence of digital finance is finance. Digital finance not only brings positive influence to the economy but also exposes its potential risks. Therefore, on the one hand, the government should perfect the financial system and establish consent regulation rules and long-term supervision mechanism of digital finance industry; on the other hand, the government should improve the regulatory rules and regulations of digital finance and refine the regulatory rules. In addition, modern technology should be used to strengthen regulatory tools to deal with increasingly complex and hidden financial risks. However, attention should also be paid to striking a balance between financial regulation and financial development, so as to avoid financial regulation restricting the development of digital finance. In this regard, sandbox mechanism can be implemented to evaluate the development of digital finance, so as to obtain the optimal regulatory status.

Data availability statement

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

Author contributions

TL: conceptualization, supervision, validation, project administration, funding support, and writing—review. MH: formal analysis and writing—original draft, review, and editing. XL: providing original data and constructing growth quality index. EE: writing—review and language polishing.

Funding

This research was supported by the Project of Nature Science Found of Shandong Province (Project Title: Trade credit and TFP of Shandong Manufacturing Enterprises: A study from the Perspective of Enterprises and Clusters, No. ZR2020MG037), key Project of Shandong University Humanities and Social Sciences (Project Title: the Mechanism of Trade Credit Influencing Technological Innovation: an Empirical Study of Shandong Enterprises, No. J17RZ005) and Taishan Young Scholar Program (tsqn202103070), Taishan Scholar Foundation of Shandong Province, China.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors, and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Barro, R. J., and Lee, J. W. (2002). IMF programs: Who is chosen and what are the effects? Cambridge, Massachusetts, United States: NBER Working Papers.

Beck, T., Demirguc-Kunt, A., and Martinez Peria, M. S. (2007). Reaching out: Access to and use of banking services across countries. J. Financial Econ. 85, 234–266. doi:10.1016/j.jfineco.2006.07.002

Belton, P. (2017). Why doesn't capital flow rich to poor countries? Am. Econ. Rev. 80 (2), 92–96. doi:10.4324/9781912281152

Bruhn, M., and Love, I. (2014). The real impact of improved access to finance: Evidence from Mexico. J. Finance 69, 1347–1376. doi:10.1111/jofi.12091

Chao, X., and Ren, B. (2011). Time series change and regional difference analysis of China's economic growth quality. Econ. Res. J. 46 (04), 26–40. In Chinese. doi:10.3969/j.issn.1673-5889.2014.27.032

Chen, X., and Zhang, Y. (2017). Research on the dynamic relationship between financial development, industrial upgrading and economic growth -- Panel VAR analysis based on inter-provincial data. Finance Trade Res. 28 (10), 19–25. In Chinese. doi:10.19337/j.cnki.34-1093/f.2017.10.002

Ding, R. (2016). A political economy analysis of supply-side structural reform. Economist 03, 13–15. In Chinese. doi:10.16158/j.cnki.51-1312/f.2016.03.006

Du, L., and Liu, Z. (2022). Impact of digital finance on credit risk constraint and operational efficiency of commercial banks. Stud. Inter. Fin. 41 (06), 75–85. In Chinese. doi:10.16475/j.cnki.1006-1029.2022.06.004

Fu, L. (2010). An empirical study on the relationship between advanced industrial structure and economic growth in China. Stat. Res. 27 (08), 79–81. In Chinese. doi:10.3969/j.issn.1002-4565.2010.08.011

Fu, L., Li, J., Fang, X., and Wei, H. (2021). Mechanism and effectiveness test of digital inclusive finance promoting inclusive Growth. Stat. Res. 38 (10), 62–75. In Chinese. doi:10.19343/j.cnki.11-1302/c.2021.10.006

Gao, Y. (2019). Research on the upgrading of enterprise value chain under the mode of international fragmentation. Beijing: People's Publishing House.

Guo, F., Wang, J., Wang, F., Kong, T., Zhang, X., and Cheng, Z. (2020). Measuring the development of digital inclusive 561 finance in China: Index compilation and spatial characteristics. China Econ. Q. 19 (4), 1401–1418. doi:10.13821/j.cnki.ceq.2020.03.12

Hansen, B. E. (2000). Sample splitting and threshold estimation. Econometrica 68 (3), 575–603. doi:10.1111/1468-0262.00124

Hong, J. E. (1994). Converging processes toward "statement of cash flows. U.S.A. Annu. Rep. Econ. Soc. tohoku Univ. 56, 141–158.

Huang, T., and Gao, B. (2020). Financial development, financing constraints and enterprise innovation. Mod. Econ. Res. 39 (3), 11. In Chinese. doi:10.13891/j.cnki.mer.2020.03.004

Huang, Y., and Huang, Z. (2018). Digital finance development in China: Present and future. China Econ. Q. 17 (04), 1489–1502. In Chinese. doi:10.13821/j.cnki.ceq.2018.03.09

Jeanneney, S. G., and Kpodar, K. (2008). Financial development and poverty reduction: Can there Be a benefit without a cost? J. Dev. Stud. 08 (62), 143–163. doi:10.1080/00220388.2010.506918

Jiang, H., and Jiang, P. (2021). Can digital finance improve enterprise total factor productivity? -- empirical evidence from Chinese listed companies. J. Shanghai Univ. Finance Econ. 23 (03), 3–18. In Chinese. doi:10.16538/j.cnki.jsufe.2021.03.001

Jin, B. (2018). Economic research on high quality development. China Ind. Econ. 35 (04), 5–18. In Chinese. doi:10.19581/j.cnki.ciejournal.2018.04.001

Jin, X., and Zhang, W. (2022). Does digital finance boost Chinese companies’ exports? - Theoretical mechanisms and Chinese evidence. Nankai Econ. Studies 38 (4), 81–99. doi:10.14116/j.nkes.2022.04.005

Камаев, В·Д·. (1983). The speed and quality of economic growth. Wuhan: Hubei People's Publishing. In Chinese.

Levine, R. (2005). Chapter 12 finance and growth: Theory and evidence. Handb. Econ. Growth 1 (2), 865–934. doi:10.1016/S1574-0684(05)01012-9

Levine, R. (1996). Financial development and economic growth: Views and agenda. J. Econ. Literature 35 (2), 688–726. doi:10.1596/1813-9450-1678

Li, J. (2015). Thinking about internet finance. Manag. World 31 (07), 1–7+16. In Chinese. doi:10.19744/j.cnki.11-1235/f.2015.07.002

Li, J., Wu, Y., and Xiao, J. J. (2020). The impact of digital finance on household consumption: Evidence from China. Econ. Model. 86, 317–326. doi:10.1016/j.econmod.2019.09.027

Li, X., and Ran, G. (2021). Digital finance development, capital allocation efficiency and industrial structure upgrading. J. Southwest Minzu Univ. Humanit. Soc. Sci. 43 (07), 152–162. In Chinese. doi:10.3969/j.issn.1004-3926.2021.07.019

Liang, Q., Xiao, S., and Li, M. (2021). Development of digital economy, Spatial spillover and improvement of regional innovation quality -- Also on the threshold effect of marketization. Shanghai J. Econ. 38 (09), 44–56. In Chinese. doi:10.19626/j.cnki.cn31-1163/f.2021.09.004

Liu, T. (2021). Study on the influence of trade credit on technological innovation of enterprises. Beijing: China Social Sciences Press, 37. doi:10.3969/j.issn.1003-3947.2021.06.008

Liu, W., Dai, B., and Liu, W. (2021). Can digital finance drive high-quality economic development? -- empirical analysis based on Chinese provincial panel data from 2011 to 2017. Comp. Econ. Soc. Syst. 37(6), 13. In Chinese. doi:10.3969/j.issn.1003-3947.2021.06.008

Lucas, R. (1989). On the mechanics of economic development. J. Monetary Econ. 22, 3–42. doi:10.1016/0304-3932(88)90168-7

Mlachila, M., Tapsoba, R., and Tapsoba, S. (2017). A quality of growth index for developing countries: A proposal. Soc. Indic. Res. 134, 675–710. doi:10.1007/s11205-016-1439-6

Nie, X., Jiang, P., Zheng, X., and Wu, Q. (2021). Research on digital finance and regional technology innovation level. J. Financial Res. 64 (3), 19. In Chinese. doi:10.13253/j.cnki.ddjjgl.2021.12.011

Qian, H., Tao, Y., Cao, S., and Cao, Y. (2020). Theory and demonstration of China's digital finance development and economic growth. J. Quantitative Tech. Econ. 37 (06), 26–46. In Chinese. doi:10.13653/j.cnki.jqte.2020.06.002

Qian, J. (1996). Theoretical thinking on the reform of distribution system. J. Shanxi Univ. Finance Econ. 17 (001), 3–5. In Chinese.

Ren, B. (2020). Major practical problems in accelerating the implementation of high-quality development in China during the 14th Five-Year Plan period. Finance Trade Res. 31 (11), 1–9. In Chinese. doi:10.19337/j.cnki.34-1093/f.2020.11.001

Sarma, M., and Pais, J. (2011). Financial inclusion and development. J. Int. Dev. 23 (5), 613–628. doi:10.1002/jid.1698

Sui, H., Duan, P., Gao, H., and Zhou, J. (2017). Financial intermediation and the quality of economic growth: An empirical study based on a provincial sample in China. Econ. Rev. 38 (05), 64–78. In Chinese. doi:10.19361/j.er.2017.05.06

Sui, H., and Liu, T. (2014). Whether FDI improves the quality of economic growth in developing host countries: Empirical evidence from Asia Pacific, Africa and Latin America. J. Quantitative Tech. Econ. 31 (11), 3–20. In Chinese. doi:10.13653/j.cnki.jqte.2014.11.001

Sui, H. (2017). Study on the influence of foreign direct investment on the quality of economic growth: Mechanism, effect and structural evolution. Beijing: Post and Telecom Press.

Sun, L. Y. (2021). Research on financing of enterprises, technological innovation. Beijing: China Social Sciences Press.

Tang, S., Wu, X., and Zhu, J. (2020). Digital Finance and enterprise technological innovation: Structural characteristics, mechanism identification and effect differences under financial supervision. Manag. World 36 (05), 52–66+9. In Chinese. doi:10.19744/j.cnki.11-1235/f.2020.0069

Teng, L., and Ma, D. (2020). Can digital finance promote quality development? Stat. Res. 37 (11), 80–92. In Chinese. doi:10.19343/j.cnki.11-1302/c.2020.11.007

Van Rooij, M., Annamaria, L., and Alessie, R. J. (2012). Financial literacy, retirement planning, and household wealth. Econ. J. 122 (560), 449–478. doi:10.1111/j.1468-0297.2012.02501.x

Wan, J., Zhou, Q., and Xiao, Y. (2020). Digital finance, financing constraints and enterprise innovation. Econ. Rev. 221 (01), 71–83. In Chinese. doi:10.19361/j.er.2020.01.05

Wang, Y. (2006). How to establish our country economy growth quality evaluation index system. Econ. Manag. J. 28 (13), 32–35. In Chinese. doi:10.19616/j.cnki.bmj.2006.13.008

Wang, M., Li, Z., and Lu, H. (2021). Digital finance and high-quality economic growth: Mechanism, effect and heterogeneity analysis. J. Harbin Univ. Commer. Soc. Sci. Ed. 39 (03), 18–34. In Chinese. doi:10.3969/j.issn.1671-7112.2021.03.002

Wang, W., and Zhang, Y. (2022). Financial structure, industrial structure upgrading and economic growth -- from the perspective of technological progress based on different characteristics. Economist 34 (02), 118–128. In Chinese. doi:10.16158/j.cnki.51-1312/f.2022.02.013

Xie, Q., Luo, S., and Zheng, Y. (1995). Estimation and reliability analysis of the trend of China's industrial productivity since the reform. Econ. Res. J. 12, 10–22. (In Chinese): CNKI:SUN:JJYJ.0.1995-12-001.

Xie, T., and Pan, Y. (2018). Financial agglomeration, industrial structure upgrading and China's economic growth. Econ. Surv. 35 (4), 8. In Chinese. doi:10.15931/j.cnki.1006-1096.20180606.005

Xie, X., Shen, Y., Zhang, H., and Guo, X. (2018). Can digital finance boost entrepreneurship? -- evidence from China. China Econ. Q. 17 (04), 1557–1580. In Chinese. doi:10.13821/j.cnki.ceq.2018.03.12

Xu, Z., Gao, Y., and Huo, Z. (2021). The pollution reduction effect of digital finance. Finance Econ. 65 (04), 28–39. In Chinese. doi:10.3969/j.issn.1000-8306.2021.04.003

Zhang, X., Yang, T., Wang, C., and Wang, G. (2020). Digital finance development and consumer consumption growth: Theory and practice in China. Manag. World 36 (11), 48–63. In Chinese. doi:10.19744/j.cnki.11-1235/f.2020.0168

Zhang, Y. (2018). Development ideas and main tasks of digital economy driving industrial structure to the middle and high end. Econ. Rev. J. 34 (9), 7. In Chinese. doi:10.16528/j.cnki.22-1054/f.201809085

Zhang, Z. (2019). Research on rural labor transfer and government supporting policies based on urban-rural overall development. Beijing: People’s Publishing House.

Zheng, H., and Li, G. (2022). The impact of digital inclusive finance development on agricultural total factor productivity growth at county level: Based on heterogeneity. Contemp. Econ. Manag. 44, 10–10. In Chinese. doi:10.13253/j.cnki.ddjjgl.2022.07.011

Zhou, L., and Chen, Y. (2022). Digital financial inclusion and the income gap between urban and rural residents: Theoretical mechanisms, empirical evidence and policy options. Word Econ. Stud. 41 (05), 117–134+137. In Chinese. doi:10.13516/j.cnki.wes.2022.05.004

Keywords: digital finance, quality of economic growth, upgrading of industrial structure, growth efficiency, growth stability, sustainability of growth

Citation: Liu T, Hu M, Elahi E and Liu X (2022) Does digital finance affect the quality of economic growth? Analysis based on Chinese city data. Front. Environ. Sci. 10:951420. doi: 10.3389/fenvs.2022.951420

Received: 24 May 2022; Accepted: 19 July 2022;

Published: 06 September 2022.

Edited by:

Larisa Ivascu, Politehnica University of Timisoara, RomaniaReviewed by:

Sibghat Ullah, Beijing University of Posts and Telecommunications (BUPT), ChinaMuhammad Saad Khan, Bahauddin Zakariya University, Pakistan

Copyright © 2022 Liu, Hu, Elahi and Liu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Ehsan Elahi, ZWhzYW5lY29Ab3V0bG9vay5jb20=