Zhimeng Wang

Zhimeng Wang Zumian Xiao

Zumian Xiao

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 08 June 2022

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.928434

This article is part of the Research Topic Advances in Co-benefits of Climate Change Mitigation View all 12 articles

Formulating policies under the dual policy objectives of environmental protection and carbon neutrality in China is essential. This paper utilizes enterprise-level data to construct a panel model. Our empirical test indicates that increasing China’s pollutant discharge fee can effectively reduce industrial pollutants, including wastewater and exhaust gas. The empirical results indicate that in terms of enterprises, pollutant discharge fees can not only directly reduce carbon emissions but also indirectly by reducing coal assumption. This paper also constructs a threshold model of the carbon emission reduction effect of population size. It has been proved that when the population size does not exceed the threshold, the utility of the pollutant discharge fee is apparent. According to this study’s heterogeneity test, the carbon emission reduction effect of the pollutant discharge fee is more evident in large- and medium-sized enterprises and heavy pollution enterprises.

The economic growth and human activities continue to expand carbon emissions, increasing the risk of environmental deterioration. Many researchers have begun to emphasize the importance of the carbon neutrality (Ji et al., 2021). Since the 2015 Paris Agreement, various member countries of the United Nations Climate Change Conference (21st Conference of the Parties, or COP21) are working on policies and strategies to control the problem of carbon dioxide (CO2) emissions (Zhang and Wang, 2017). Sustainable environmental development is becoming a global consensus. Many countries strive to develop policies to control environmental degradation and reduce environmental pollution.

Among many environmental regulations in China, the pollutant discharge fee has an extensive history. At the corporate level, the most common way to protect the environment is to charge pollutant discharge fees. This paper establishes a model of pollutant discharge fees and other variables to explore the impact of charges on industrial pollutants and carbon emissions. The Chinese government promulgated the regulation for pollutant discharge fees in 1979. But there are two problems, lack of motivation for corporate pollution control and significant differences in charging standards in different areas. In 2003, the Chinese government issued the second edition of the regulation and implemented it at the end of 2017. However, as the environment is a non-exclusive public good, many enterprises did not pay the fee as stipulated, leading to low resource allocation efficiency and environmental problems (Hu et al., 2020; Li et al., 2021).

The purpose of charging the pollutant discharge fee is to reduce pollutant emissions. There is evidence demonstrates that it does achieve this purpose. However, it is unclear whether the policy’s implementation has played an important role in reducing carbon emissions. To fill this gap, this paper establishes a panel regression model and analyzes the role of pollutant discharge fees. We find that pollutant discharge fees also can reduce carbon emissions. With different population sizes, the carbon emission reduction effect of pollutant discharge fees is different. Further, the type and scale of enterprises also affect the emission reduction effect of the fees.

In addition to the direct effect, we also find that pollutant discharge fees can indirectly influence carbon emissions by reducing the use of coal. The consumption of fossil fuels such as coal is an important source of CO2. China’s current industrial sector requires coal to operate power plants, steel plants, and chemical plants and create electricity, steel, ammonia, methanol, urea, and agricultural fertilizer (Jia and Lin, 2021). Coal is China’s major energy source and the most prominent contributor to the country’s GHG emissions. The Chinese government attaches great importance to reducing GHG emissions. Energy conservation and emission reduction is the most critical step for China to address global climate change and other environmental issues in the present and future (Zhou et al., 2020). Reducing carbon emissions also have a positive impact on the Chinese government’s proposal at the 75th UN General Assembly to achieve carbon neutrality by 2060.

Amid a critical time of global warming, it is effective for China to adopt new policies to reduce carbon emissions, but this will have significant costs. Utilizing existing systems to achieve the goal of reducing carbon emissions is a more efficient approach. In theory, there is a large overlap between the sources of environmental pollutants and CO2 emissions. This paper uses data at the enterprise level to provide empirical evidence that there is also a negative correlation between the number of emission fees and carbon emissions.

This article provides the following contributions to the existing literature. First, in terms of this paper’s research perspective, the pollutant discharge fee is a considerable part of Chinese environmental protection law. Charging for polluters is also a common practice throughout the world. Such regulation is of great significance for reducing environmental pollution and improving environmental quality (Wang et al., 2014a). Studying the actual emission reduction effect of the pollutant discharge fee has great reference value for decision makers to establish more suitable regulatory policies. However, the existing research only focuses on the promoting effect of pollutant discharge fees on environmental pollution, air pollution, and exhaust emission. Few literatures mentioned the effect of this policy on carbon emissions. This paper fills this research gap and studies the dual function of the pollutant discharge fee in China. While having a great inhibitory effect on air pollutants, the pollutant discharge fee also has a significant abatement effect on carbon emissions. Second, from the perspective of research objects, rather than the studying the impact of policies at the provincial or macro level, this paper quantitatively studies the reverse relationship between pollutant discharge fees and carbon emissions at the enterprise level to study the impact of Chinese government procurement of coal substitutions.

The remainder of this study is arranged as follows: Section 2 presents the related literature review and hypotheses. Section 3 describes the data and methodology. Section 4 discusses the empirical results. Section 5 carries out the heterogeneity analysis. The last section concludes.

Since Arthur C. Pigou first proposed environmental tax in his externality theory, academia has not reached a unified conclusion on the governance effect of environmental tax. China adheres to the policy of the pollutant discharge fee, while other countries implement the environmental tax. Previous studies mainly focus on the role of environmental tax. Many literatures can prove that the implementation of environmental tax has the effects of reducing industrial pollution, strengthening green economies, and inhibiting environmental degradation (Lin and Li, 2011). used the Differences-in-Differences (DID) model to comprehensively evaluate the impact of carbon tax on environmental governance in five Nordic countries (Denmark, Finland, Sweden, the Netherlands, and Norway) and found that environmental taxes had a negative effect on CO2 emissions in Finland. However, this effect was weak in the other four countries. For the first time (Han and Li, 2020), quantified the impact of environmental taxes on the PM2.5 emissions in China’s provinces and noted that clean air policies and environmental taxes could significantly reduce its pollution (Chien et al., 2021). Also proved that environmental taxes and ecological innovation have a positive impact on reducing carbon emissions and haze formation in Asian countries.

There is substantial evidence in various countries that charging taxes is an effective means of reducing environmental damage (Meng et al., 2013). Collated data and noted that carbon taxes can effectively reduce CO2 emissions. For example, Australia has imposed environmental taxes since 2012 to meet Copenhagen targets for its CO2 emission reductions. In Europe and China, environmental taxes also have a negative impact on GHG emissions (Yang et al., 2014; Onofrei et al., 2017), indicating that environmental taxes have an important role in reducing environmental pollution (Vallés-Giménez and Zárate-Marco, 2020). Reported that the GHG emissions in Spain are spatially dependent, spatially persistent and temporally. In this case, taxes that aim at reducing emissions have a slight inhibiting effect. However, sometimes environmental taxes have a negative impact on economic development (Floros and Vlachou, 2005). Assessed the impact of environmental tax and found that carbon tax in the Greek manufacturing industry has been an effective environmental policy to alleviate global warming. But it has proved to be expensive and detrimental to the economic development (Gao and Chen, 2002; Lu et al., 2010). Also illustrated that the implementation of environmental taxes in China will reduce carbon emissions while it may have a negative impact on the country’s economy.

Implementing environmental tax has the function of strengthening a green economy. As mentioned for China (Li et al., 2021), explained that the use of environmental taxes and regulatory supervision by relevant institutions can promote the use of green technologies and reduce industrial pollution. More stringent environmental taxes can encourage enterprises to reduce emissions, and there is an inverted U-shaped relationship between industrial pollution reduction and environmental tax rate (Cheng and Li, 2022). Proved that the industrial green total factor productivity (GTFP) increases significantly by increasing the standard pollutant discharge fee. Their conclusion remains valid after alleviating endogenous problems and conducting robustness tests. Increasing environmental costs can promote industrial green growth and improve the level of green technology innovation, which can better transform the mode of a country’s economic growth and achieve green industry development. The relationship between environmental taxes and green technology innovation is achieved through incentives for environmental regulatory instruments (Anthony et al., 2011; Jaffe et al., 2002). Some countries are improving green information systems, strengthening internal environmental management (Khan and Yu, 2020), and developing green practices (Khan et al., 2020) and green financial intermediary channels to achieve a zero-carbon economy (Umar et al., 2021).

In addition, environmental taxes affect the choice of pollutant products in the decision-making process, creating incentives to reduce high-pollution products and improve environmental quality (Elkins and Baker, 2002; Niu et al., 2018; He et al., 2019). In other words, environmental taxes correct environmental problems (such as pollution), in whole or in part, by increasing incentives for alternative behaviors. Environmental taxes can increase environmental investment and reduce air pollution emissions. Moreover, according to the idea of asylum tax, in complete competition, the optimal environmental tax can offset the gap between private costs and social costs. These findings suggest that well-designed environmental taxes may be an effective policy tool for the internalization of environmental costs. Threshold regression results have highlighted that there is an optimal tax rate for green technology innovation (Wang and Yu, 2021), However, it is important that China’s current environmental tax rate is lower than this tax rate.

World economic and finance development has an important impact on the emission of CO2 (Xiang et al., 2021; Ren et al., 2022a; Yin et al., 2022). Economic development is inseparable from the demand for resources. Increased demand for resources puts increasing pressure on the natural environment. One of the increasing pressures on the natural environment is that there are more carbon emissions, haze pollution, and unhealthy byproducts produced by different activities (Malghani, 2021), and the increase in economic development leads to more carbon emissions, especially in countries such as China and India (Ran et al., 2021). Except for the economic situation, coal prices can largely affect the use of coal, which are affected by many factors (Ren et al., 2021b). Proposes two new methods to evaluate the predictability of a large group of factors on carbon futures returns.

China’s economic growth has been accompanied by substantial energy consumption, surpassing the energy consumption of the United States for the first time in 2010. Furthermore, the annual report of China’s energy development illustrated that the renewable energy in China satisfies for only a small proportion of total energy consumption (accounting for 13% in 2016). Conversely, coal (characterized as a high-carbon, high-pollution, and high-emission energy source) represented a large proportion of the total energy consumption (61.8%), while oil and gas accounted for 18.3% and 6.4%, respectively. In addition, there are distinct differences in the energy consumption patterns between China and the world’s major developed countries and its energy consumption intensity is significantly higher than that of developed countries. Reliance on coal as a fuel for production is likely to cause higher carbon emissions. This paper verifies whether the increase in pollutant discharge fees can reduce the use of coal, the main contributor to greenhouse gases, and further reduce carbon emissions.

How to mitigate carbon emissions is a hot topic in recent years. There are many direct and indirect factors that affect corporate carbon emissions. For example, relying on fossil fuels for production produces a large amount of carbon dioxide, which puts a certain pressure on the global environment. In addition, increased national climate risk will also promote the carbon emissions of enterprises (Ren et al., 2021).

Meanwhile, researchers work to find ways to reduce carbon emissions. For example, increasing the use of renewable energy can effectively alleviate environmental pressure (Dong et al., 2020). Environmental innovation is also considered one of the critical tools for reducing CO2 emissions (Cws et al., 2020; Umar et al., 2020). Fostering a migration from traditional energy to renewable energy is not only environmental-friendly but also crucial for steady development of society and economy (Ayres et al., 2013; Wang et al., 2014b). For government policy, mandatory environmental regulation and soft policies directly or indirectly reduce carbon emissions. In addition, some researchers point out that China’s energy development will have a significant impact on its economic growth (Li et al., 2017; Xie et al., 2018).

Few studies have investigated the quantitative impact of environmental tax on carbon emissions. Some scholars believe that environmental tax will lead to environmental deterioration (Asmi et al., 2019). However, another school believes that environmental taxes help reduce carbon emissions (Thi et al., 2020). Studied the relationship between environmental taxes, natural resource consumption taxes, and carbon emissions from 2001 to 2018, and the multivariate analysis indicated that the increased environmental taxes can lead to Vietnam’s CO2 emissions reducing. Other studies have indicated that environmental taxes can reduce CO2 emissions at a higher level worldwide (Wolde-Rufael and Mulat-Weldemeskel, 2021). Collected data on aggregate environmental taxes, energy taxes, and environmental policies in seven emerging countries from 1994 to 2005 and tested the green dividend hypothesis, proving that aggregate environmental taxes and energy taxes improved the environmental quality of these countries.

Environmental taxes may reduce carbon emissions through a variety of ways. Environmental taxes may lead to technological upgrades, potentially combatting the problems associated with high emissions (Borozan, 2019). Ulucak et al. (2020) believed that environmental taxes can achieve the non-linear impact on carbon emissions by improving innovation and energy efficiency. The marginal impact of environmental taxes on natural resource rents and renewable energy consumption rises in a statistically significant manner with increasing tax levels, further affecting carbon emissions. Raising environmental taxes can also have a negative impact on the consumption of traditional energy sources such as coal, indirectly reducing carbon emissions (Martins et al., 2021).

Many environmental tax studies have involved industrial pollution to measure environmental quality, yet rarely involve resource utilization, such as ecological footprint (Ac and Acar, 2018; Sun et al., 2020). Studies have reported that environmental tax can reduce water pollution (Higano et al., 2020), solid waste (Prats et al., 2020), and resource consumption (Söderholm, 2011).

In the research method, we use panel regression with time and individual fixed effects. The original intention for the establishment of the pollutant discharge fee was to reduce industrial pollution, so we first explored the direct emission reduction effect of the pollutant discharge fee on waste gas and wastewater. In addition, we regressed CO2 data to estimate whether this policy has an impact on CO2 emissions. The baseline measurement model is as follows:

Where i and t denote enterprise and year, respectively,

This study assessed the direct and indirect effects of pollutant discharge fees on carbon emissions by utilizing a mediating effect model. Higher environmental taxes can reduce the use of fossil fuels, such as coal (Murray and Brian, 2015), by promoting green technology and improving the quality of green investment (Lambertini et al., 2020) as well as competitiveness of renewable energy technologies (Wesseh and Lin, 2019). Simultaneously, changes in coal consumption will affect CO2 emissions in the short and long term (Martins et al., 2021). We speculated that the pollutant discharge fee system can reduce carbon emissions by reducing the use of coal, so our mechanism analysis addressed coal consumption as an intermediary variable. We adopted the following regression model:

Here, i and t denote enterprise and year.

The panel regression model only verifies the existence of a carbon emission reduction effect caused by the pollutant discharge fee, but whether there are other factors, such as population, that affect the carbon emission reduction effect (Wang et al., 2022). Believed that the multi-center structure of urban agglomeration would produce large amounts of carbon emissions (Fan et al., 2021; Wang and Wang, 2021). Indicated that there is a non-linear relationship between aging populations and carbon emissions. However, we believed that different population sizes also have an impact on the CO2 emission reduction effect. Due to the differences in geographical location, economic foundation, and construction conditions, the population size of cities in China vary. If the urban population size is larger than the population capacity, it indicates that the urban population has caused great pressure, or even damage, to the environment, which is not conducive to the green development of these urban environments. In this case, we speculated that the carbon emission reduction effect of the pollutant discharge fee may be heterogeneous with different population sizes, that is, the impact of urban population size on carbon emissions may have a threshold effect. According to the threshold model constructed by (Hansen, 1999), we constructed the threshold regression model explaining the non-linear influence of population size on CO2 emissions from pollution charges. In this study, the single-threshold econometric model was as follows:

In addition to the previously mentioned variables,

The data on firms’ pollution emissions comes from Annual Environmental Survey of Polluting Firms (AESPF), which was established by the Ministry of Ecology and Environment (formerly known as the Ministry of Environmental Protection) in the 1980s to record environmental pollution and emission reduction in China. AESPF provides information on corporate environmental performance, including emissions of major pollutants, pollution treatment equipment, and energy consumption. The CO2 emission data was converted from standard coal data.

Corporate financial control variables (such as asset-liability ratio, corporate scale, corporate age, and enterprise import and export data) are derived from the Annual Survey of Industrial Firms (ASIF), which is one of the most comprehensive and widely used Chinese firm-level dataset maintained by the National Bureau of Statistics of China (NBSC). The ASIF dataset covers all state-owned industrial firms and non-state-owned industrial firms with annual sales above 5 million RMB in China. It contains detailed financial and characteristic information about each firm. The gross domestic product per capita and urban population at the end of the year in the province where the enterprise is located are based on data from the NBSC. We matched the above data according to the enterprise name and the enterprise code and received 178,473 pieces of data. The following table indicates how the study variables are defined (Table 1).

TABLE 1. Definitions of variables.

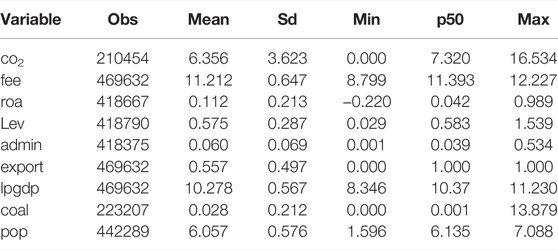

The summary statistics of variables such as CO2 emissions, pollutant discharge fees and coal consumption intensity are exhibited in Table 2.

TABLE 2. Descriptive statistics.

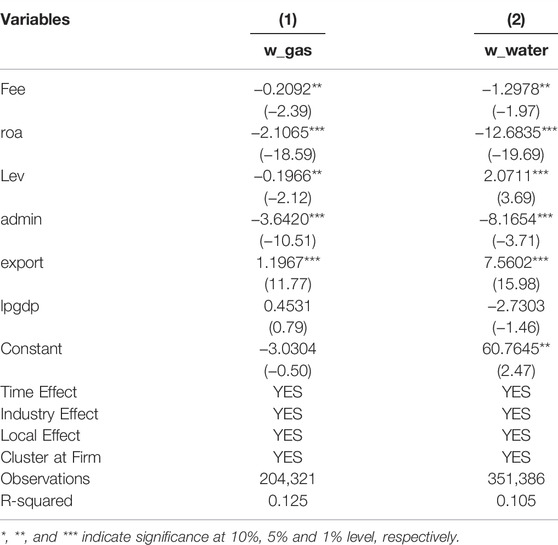

Before investigating the carbon reduction effect of the pollutant discharge fee, we examined its impact on industrial pollutant discharges. The quantities of industrial waste gas and wastewater were regressed on the number of pollutant discharge fees paid and other control variables. The results are reported in Table 3. The results prove that this policy has a significant inhibiting effect on industrial waste gas and wastewater emissions at the level of 5%. It proves that the increase of the pollutant discharge fee can promote enterprises to optimize their energy structure independently and replace traditional fossil fuels with clean energy to reduce the emissions of polluting exhaust and wastewater. The original intention of pollutant discharge fee system is to reduce emissions of pollutant, and the results illustrate that this system is effect. This paper attempts to explore whether the pollutant discharge fee has other effects in addition to inhibiting industrial pollution. Furthermore, we hope to explore whether the pollutant discharge fee is conducive to reducing enterprise carbon emissions.

TABLE 3. Full sample regression results.

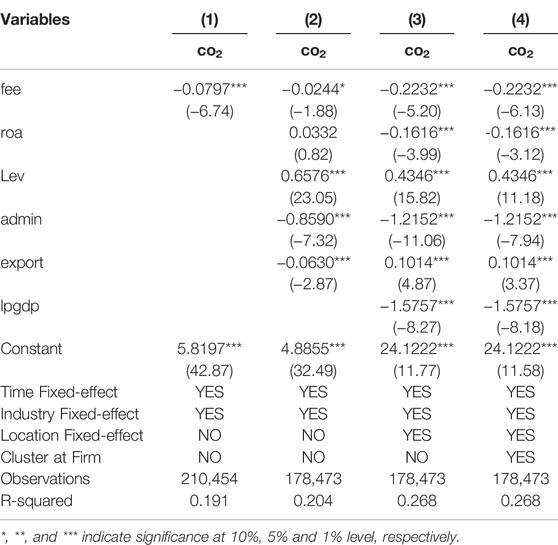

All columns in Table 4 present basic estimated results of the models with the original data, including firm fixed effects and year fixed effects. In column (1), the coefficient value is −0.0797 which is significant and negative. This result indicates that higher pollution charges will reduce CO2 emissions, while the effect decreases slightly as more corporate-level covariates are included in the regression. As for other control variables, we can see that rate of return, proportion of management costs, and regional per capita GDP are all important negative factors affecting CO2 emissions at the corporate level, while financial leverage has positive effects.

TABLE 4. Full sample regression results.

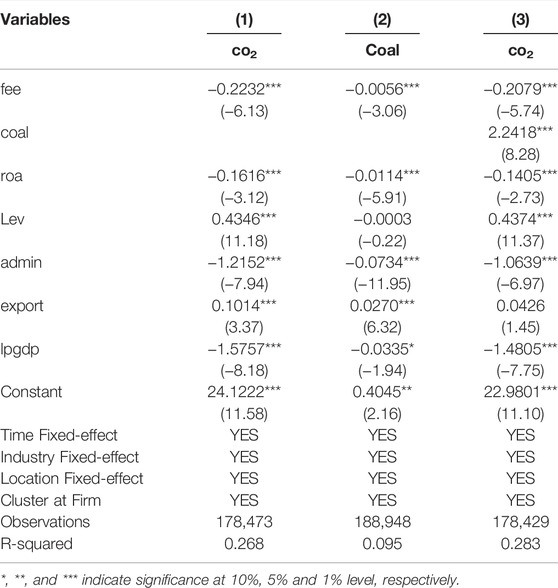

We used the stepwise regression coefficient method to verify the negative mediating effect of coal consumption intensity for CO2 emissions. Table 5 indicates that when there is no mediating effect, the coefficient is apparent, which explains the direct negative effect of pollutant discharge fees on CO2 emissions. When there is a mediator, the indirect impact of pollutant discharge fees on carbon emissions through coal consumption should also be considered. The pollutant discharge fee reduces the use of coal to the level of 1%, and coal consumption can significantly increase CO2 emissions. The coefficient was 2.2418, which concludes that coal consumption has a partial mediating effect on CO2 emissions.

TABLE 5. mediating effect analysis.

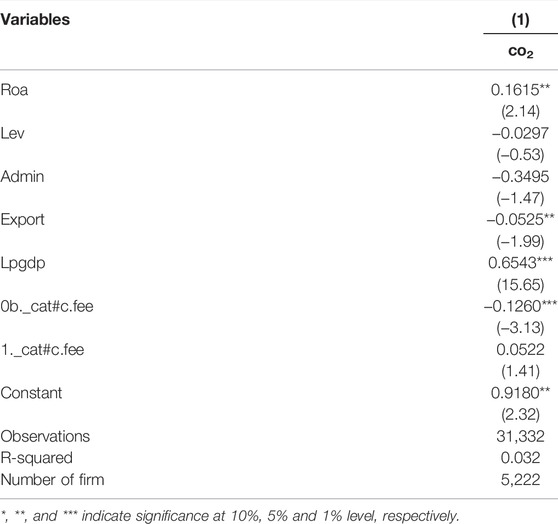

According to the threshold model constructed by urban population size, the single-threshold test results are clear, while the model rejects the double-threshold hypothesis as shown in Table 6. So the effectiveness of pollutant discharge fees in carbon emission reduction is only applicable to the single-threshold hypothesis of population size. According to Table 7, we found that when the population size is below the threshold value of 4.9577, the pollutant discharge fee has a significantly negative effect on CO2 emissions. When the threshold value is 4.9577–5.8875, the coefficient changes from negative to positive, but the effect is not noticeable. It is shown that when the population does not reach the first threshold, the increase in pollutant discharge fees is significantly conducive to the reduction of carbon emissions. However, after exceeding the threshold, the increase in pollutant discharge fees will increase carbon emissions and cause certain damage to the environment. The population size of a city should be controlled within a certain range. Currently, the inhibitory effect of this policy on carbon emissions is effective. Unrestrained population expansion will not only impose a substantial burden on the environment itself but also weaken the energy saving and emission reduction effect of environmental protection policies, such as emission fee policies.

TABLE 6. Test for multiple thresholds.

TABLE 7. Threshold effect test results.

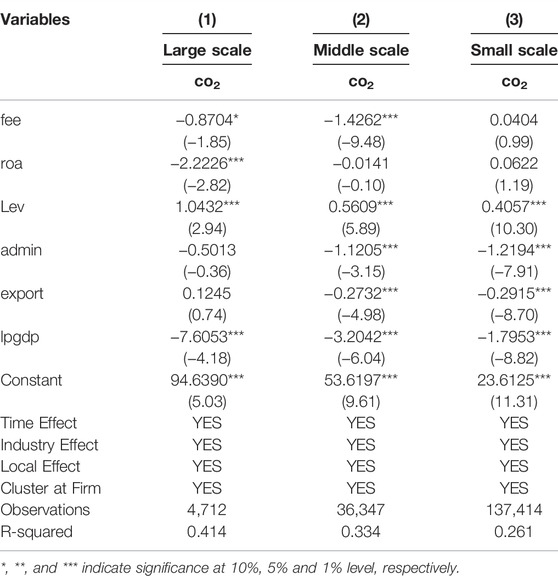

We divided the enterprise scale into three categories (large, medium, and small) and then completed regression respective to each category to observe whether the CO2 emission level of enterprises of different scales is affected by variables such as the pollutant discharge fee. For large-scale enterprises, the pollutant discharge fee has a significant inhibitory effect on carbon emissions at the level of 10%, and the return on assets and financial leverage of enterprises have significant positive and negative effects on carbon emissions, respectively. For medium-sized enterprises, the suppressive effect of the increase of the pollutant discharge fee on carbon emissions is significant at the 1% level, while it is not significant for small enterprises. It is necessary to strengthen the supervision of large- and medium-sized enterprises’ emission payments and continue the innovation to create useful policies for small-sized enterprises. The results in Table 8 illustrate that pollutant discharge fees are beneficial to environmental protection and effectively reduce the carbon emissions of large- and medium-sized enterprises.

TABLE 8. Heterogeneity—enterprise scale.

Statistics indicate that between 2005 and 2019, the average ratio of the Chinese heavy industry’s CO2 emissions to the total CO2 emissions was about 55%. The heavy industry is the pillar of the Chinese national economy (Xu and Lin, 2020). In the early development stages, broad economic growth spurred rapid growth in the industry, accompanied by high levels of CO2 emissions (Zhang and Ma, 2020). Statistics demonstrate that between 2005 and 2019, China’s heavy industry CO2 emissions accounted for an average of about 55% of the country’s total CO2 emissions.

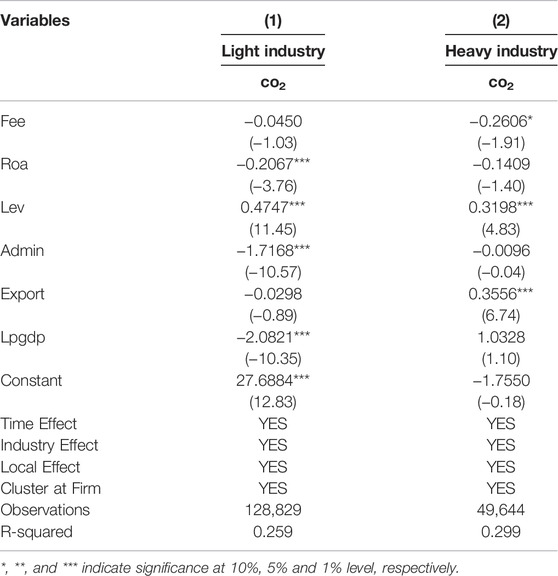

To observe the role of the pollutant discharge fee more specifically, we categorized enterprises as part of the light industry or heavy industry. Empirical test proves that the pollutant discharge fee has a significant inhibitory effect on the carbon emissions of heavy industry. For light industry, the coefficient of pollutant discharge fees is negative, but insignificant. The heavy industry does more harm to the environment than the light industry, so it is acceptable that the effect of the pollutant discharge fee on the heavy industry is greater than that of the light industry. Table 9 demonstrates that the pollutant discharge fee can significantly reduce carbon emissions from heavy industry enterprises.

TABLE 9. Heterogeneity—Light/heavy industries.

Based on the enterprise pollution emission data and financial data, this paper analyzes whether the increase in pollutant discharge fees can reduce industrial pollution. Furtherly, whether it can achieve the purpose of reducing carbon emissions. We established a panel model with time fixed effects and individual fixed effects. The empirical analysis shows that the increase of pollutant discharge fees is useful for companies to increase the use of clean energy, and ultimately achieve the purpose of reducing waste water and waste gas. Meanwhile, by promoting the optimization of the energy structure of enterprises, the increase in pollutant discharge fees can also reduce carbon emissions. With the addition of more corporate variables, pollutant discharge fees continue to maintain a restraining effect on carbon emissions. In addition to the direct impact, pollutant discharge fees can also indirectly reduce carbon emissions. The increase in pollutant discharge fees is conducive to promoting the improvement of green technology and improving the competitiveness of renewable energy, thereby reducing the use of fossil fuels such as coal. The reduction of coal use can reduce CO2 emissions. Therefore, we believe that the increase in pollutant discharge fees can further reduce carbon emissions by inhibiting the use of coal (i.e., the main contributor of China’s greenhouse gases). We also established a threshold model and found that when the urban population is within a certain scale, the inhibitory effect of sewage charges is more significant.

From a national perspective, China should be attentive to its environmental protection efforts while promoting economic development and weigh its speed of economic development with its status quo of environmental governance. The pollutant discharge fee system is not only a mandatory environmental law but also a driver for economic development in the Chinese market, supporting enterprises to reduce the intensity of coal use, encouraging the use of clean energy, and promoting technological innovation and environmental awareness. The Chinese government should introduce mature regulatory policies as well as improve the regulatory system to implement these policies. Simultaneously, researchers should recognize that population size has a certain impact on the effectiveness of environmental protection measures and population size should be controlled as reasonably possible to prevent it from exceeding the threshold to weaken the effect of the country’s emission policy.

As mentioned for the enterprises, improving the use of clean gas can reduce CO2 emissions and reduce harmful gas emissions to improve the environment, thereby reducing the amount of emission fees, achieving the goal of energy structure optimization in the short term, and establishing a more comprehensive carbon neutralization in the long term. While achieving economic goals, the government should continually have a global view and strengthen technological innovations to optimize enterprise energy structures. Enterprises should be environmentally conscious and bear its corresponding social responsibility, comply with the market and government forces, and enhance the competitiveness of their respective markets. Enterprises should also improve their production technology, reduce industrial pollution, reduce energy supplies using coal as fuel for product production, and increase the use of clean energies, such as natural gas, to effectively reduce carbon emissions.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

ZW: methodology, writing—review and editing, validation, resources, and data curation. LY: methodology, software, resources and visualization. MZ: data curation, supervision and investigation. YX: formal analysis, writing—review and editing, and project administration. XL: data curation, formal analysis and data curation. YW: resources, software, and visualization. ZX: conceptualization, supervision, funding acquisition and writing original draft. All authors: contributed to the article and approved the submitted version.

We acknowledge the financial support from Shandong Province Key Research Project of Financial Application (2019-JRZZ-15), Taishan Scholars Program of Shandong Province, China (Grant Numbers: ts201712059; tsqn201909135) and Youth Innovative Talent Technology Program of Shandong Province, China (Grant Number: 2019RWE004). All errors remain our own.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

COP21, 21st Conference of the Parties; CO2, Carbon Dioxide; APEC, Asia-Pacific Economic Cooperation; DID, Difference-in-Difference; PM2.5, Fine Particulate Matter; GHG, Greenhouse Gas; GDP, Gross Domestic Product; AESPF, Annual Environmental Survey of Polluting Firms; ASIF, Annual Survey of Industrial Firms; NBSC, National Bureau of Statistics of China

Aşıcı, A. A., and Acar, S. (2018). How Does Environmental Regulation Affect Production Location of Non-carbon Ecological Footprint? J. Clean. Prod. 178, 927–936. doi:10.1016/j.jclepro.2018.01.030

Asmi, F., Anwar, M. A., Zhou, R., Wang, D., Sajjad, A., Powe, D. N., et al. (2019). Social Aspects of 'climate Change Communication' in the 21st Century: a Bibliometric View. J. Environ. Plan. Manag. 62 (4), 2393–2417. doi:10.1080/09640568.2018.1541171

Ayres, R. U., van den Bergh, J. C. J. M., Lindenberger, D., and Warr, B. (2013). The Underestimated Contribution of Energy to Economic Growth. Struct. Change Econ. Dyn. 27, 79–88. doi:10.1016/j.strueco.2013.07.004

Borozan, D. (2019). Unveiling the Heterogeneous Effect of Energy Taxes and Income on Residential Energy Consumption. Energy Policy 129, 13–22. doi:10.1016/j.enpol.2019.01.069

Cheng, Z., and Li, X. (2022). Do raising Environmental Costs Promote Industrial Green Growth? A Quasi-Natural Experiment Based on the Policy of Raising Standard Sewage Charges. J. Clean. Prod. 343, 131004. doi:10.1016/j.jclepro.2022.131004

Chien, F., Sadiq, M., Nawaz, M. A., Hussain, M. S., Tran, T. D., and Le Thanh, T. (2021). A Step toward Reducing Air Pollution in Top Asian Economies: The Role of Green Energy, Eco-Innovation, and Environmental Taxes. J. Environ. Manag. 297, 113420. doi:10.1016/j.jenvman.2021.113420

Cws, A., Bn, B., Xfs, C., Jpl, D., and Zj, E. (2020). Trade and Technological Innovation: The Catalysts for Climate Change and Way Forward for COP21. J. Environ. Manag. 269, 774. doi:10.1016/j.jenvman.2020.110774

Dong, K., Dong, X., and Jiang, Q. (2020). How Renewable Energy Consumption Lower Global CO2 Emissions? Evidence from Countries with Different Income Levels. World Econ. 43, 1665–1698. doi:10.1111/twec.12898

Elkins, P., and Baker, T. (2002). Carbon Taxes and Carbon Emissions Trading. J. Econ. Surv. 15 (3), 325–376. doi:10.1111/1467-6419.00142

Fan, J., Zhou, L., Zhang, Y., Shao, S., and Ma, M. (2021). How Does Population Aging Affect Household Carbon Emissions? Evidence from Chinese Urban and Rural Areas. Energy Econ. 100, 105356. doi:10.1016/j.eneco.2021.105356

Floros, N., and Vlachou, A. (2005). Energy Demand and Energy-Related CO2 Emissions in Greek Manufacturing: Assessing the Impact of a Carbon Tax. Energy Econ. 27, 387–413. doi:10.1016/j.eneco.2004.12.006

Han, F., and Li, J. (2020). Assessing Impacts and Determinants of China's Environmental Protection Tax on Improving Air Quality at Provincial Level Based on Bayesian Statistics. J. Environ. Manag. 271, 111017. doi:10.1016/j.jenvman.2020.111017

Hansen, B. E. (1999). Threshold Effects in Non-dynamic Panels: Estimation, Testing, and Inference. J. Econ.. doi:10.1016/S0304-4076(99)00025-1

He, P., Ning, J., Yu, Z., Xiong, H., Shen, H., and Jin, H. (2019). Can Environmental Tax Policy Really Help to Reduce Pollutant Emissions? an Empirical Study of a Panel ARDL Model Based on OECD Countries and China. Sustainability 11, 4384. doi:10.3390/su11164384

Heyes, A., and Kapur, S. (2011). Regulatory Attitudes and Environmental Innovation in a Model Combining Internal and External R&D. J. Environ. Econ. Manag. 61, 327–340. doi:10.1016/j.jeem.2010.12.003

Higano, Y., Shen, Z., and Mizunoya, T. (2020). Analysis of Spatial Effects of Environmental Taxes on Water Pollution in China's Taihu Basin. Innovations Urban Regional Syst., 417–441. doi:10.1007/978-3-030-43694-0_19

Hu, B., Dong, H., Jiang, P., and Zhu, J. (2020). Analysis of the Applicable Rate of Environmental Tax through Different Tax Rate Scenarios in China. Sustainability 12. doi:10.3390/su12104233

Jaffe, A. B., Newell, R. G., and Stavins, R. N. (2002). Environmental Policy and Technological Change. Environ. Resour. Econ. 22, 41–70. doi:10.1023/A:1015519401088

Ji, X., Zhang, Y., Mirza, N., Umar, M., and Rizvi, S. K. A. (2021). The Impact of Carbon Neutrality on the Investment Performance: Evidence from the Equity Mutual Funds in BRICS. J. Environ. Manag. 297, 113228. doi:10.1016/j.jenvman.2021.113228

Jia, Z. J., and Lin, B. Q. (2021). How to Achieve the First Step of the Carbon-Neutrality 2060 Target in China: The Coal Substitution Perspective. Energy 233, 14. doi:10.1016/j.energy.2021.121179

Khan, S. A. R., and Yu, Z. (2020). Assessing the Eco-Environmental Performance: an PLS-SEM Approach with Practice-Based View. Int. J. Logist. 24, 1–19. doi:10.1080/13675567.2020.1754773

Khan, S. A. R., Yu, Z., Sharif, A., and Golpîra, H. (2020). Determinants of Economic Growth and Environmental Sustainability in South Asian Association for Regional Cooperation: Evidence from Panel ARDL. Environ. Sci. Pollut. Res. 27, 45675–45687. doi:10.1007/s11356-020-10410-1

Lambertini, L., Pignataro, G., and Tampieri, A. (2020). The Effects of Environmental Quality Misperception on Investments and Regulation. Int. J. Prod. Econ. 225, 107579. doi:10.1016/j.ijpe.2019.107579

Li, G., Liu, W., Wang, Z., and Liu, M. (2017). An Empirical Examination of Energy Consumption, Behavioral Intention, and Situational Factors: Evidence from Beijing. Ann. Oper. Res. 255, 507–524. doi:10.1007/s10479-016-2202-8

Li, P., Lin, Z., Du, H., Feng, T., and Zuo, J. (2021). Do environmental Taxes Reduce Air Pollution? Evidence from Fossil-Fuel Power Plants in China. J. Environ. Manag. 295, 113112. doi:10.1016/j.jenvman.2021.113112

Lin, B., and Li, X. (2011). The Effect of Carbon Tax on Per Capita CO2 Emissions. Energy Policy 39, 5137–5146. doi:10.1016/j.enpol.2011.05.050

Lu, C., Tong, Q., and Liu, X. (2010). The Impacts of Carbon Tax and Complementary Policies on Chinese Economy. Energy Policy 38, 7278–7285. doi:10.1016/j.enpol.2010.07.055

Martins, T., Barreto, A. C., Souza, F. M., and Souza, A. M. (2021). Fossil Fuels Consumption and Carbon Dioxide Emissions in G7 Countries: Empirical Evidence from ARDL Bounds Testing Approach. Environ. Pollut. 291, 118093. doi:10.1016/j.envpol.2021.118093

Meng, S., Siriwardana, M., and Mcneill, J. (2013). The Environmental and Economic Impact of the Carbon Tax in Australia. Environ. Resour. Econ. 54, 313–332. doi:10.1007/s10640-012-9600-4

Murray, B. (2015). British Columbia's Revenue-Neutral Carbon Tax: A Review of the Latest "grand Experiment" in Environmental Policy. Energy Policy 86, 674–683. doi:10.1016/j.enpol.2015.08.011

Nawaz, M. A., Hussain, M. S., Kamran, H. W., Ehsanullah, S., Maheen, R., and Shair, F. (2021). Trilemma Association of Energy Consumption, Carbon Emission, and Economic Growth of BRICS and OECD Regions: Quantile Regression Estimation. Environ. Sci. Pollut. Res. 28, 16014–16028. doi:10.1007/s11356-020-11823-8

Niu, T., Yao, X., Shao, S., Li, D., and Wang, W. (2018). Environmental Tax Shocks and Carbon Emissions: An Estimated DSGE Model. Struct. Change Econ. Dyn. 47, 9–17. doi:10.1016/j.strueco.2018.06.005

Onofrei, M., Vintila, G., Dascalu, E. D., Roman, A., and Firtescu, B.-N. (2017). The Impact of Environmental Tax Reform on Greenhouse Gas Emissions: Empirical Evidence from European Countries. Environ. Eng. Manag. J. 16, 2843–2849. doi:10.30638/eemj.2017.293

Prats, G. M., Álvarez García, Y. I., Hernández, F. S., and Zamora, D. T. (2020). Environmental Taxes. Its Influence on Solid Waste in Mexico. J. Environ. Manag. Tour. 11, 755–762. doi:10.14505//jemt.v11.3(43).29

Ran, T. A., Mu, A., An, A., and Ur, B. (2021). The Dynamic Effect of Eco-Innovation and Environmental Taxes on Carbon Neutrality Target in Emerging Seven (E7) Economies - ScienceDirect. J. Environ. Manag. 299, 113525. doi:10.1016/j.jenvman.2021.113525

Ren, X., Cheng, C., Wang, Z., Yan, C., and Welford, R. (2021). Spillover and Dynamic Effects of Energy Transition and Economic Growth on Carbon Dioxide Emissions for the European union: a Dynamic Spatial Panel Model. Sustain. Dev. 29 (1), 228–242. doi:10.1002/sd.2144

Ren, X., Duan, K., Tao, L., Shi, Y., Yan, C., Tol, R., et al. (2022a). Carbon Prices Forecasting in Quantiles. Energy Econ. 108, 105862. doi:10.1016/j.eneco.2022.105862

Ren, X., Li, Y., Shahbaz, M., Dong, K., and Lu, Z. (2022b). Climate Risk and Corporate Environmental Performance: Empirical Evidence from china. Sustain. Prod. Consum. 30, 467–477. doi:10.1016/j.spc.2021.12.023

Söderholm, P. (2011). Taxing Virgin Natural Resources: Lessons from Aggregates Taxation in Europe. Resour. Conservation Recycl. 55, 911–922. doi:10.1016/j.resconrec.2011.05.011

Sun, Y., Mao, X., Liu, G., Yin, X., and Zhao, Y. (2020). Modelling the Effects of Energy Taxes on Ecological Footprint Transfers in China's Foreign Trade. Ecol. Model. 431, 109200. doi:10.1016/j.ecolmodel.2020.109200

Thi, H. D., Thi, K., Phuong, D. L., Thu, V. P., and Minh, C. (2020). Impact of Environmental Tax Collection on CO2 Emission in Vietnam. Int. J. Energy Econ. Policy 10 10 (6), 299–304. doi:10.32479/ijeep.10153

Ulucak, R., DanishKassouri, Y., and Kassouri, Y. (2020). An Assessment of the Environmental Sustainability Corridor: Investigating the Non‐linear Effects of Environmental Taxation on CO2 Emissions. Sustain. Dev. 28, 1010–1018. doi:10.1002/sd.2057

Umar, M., Ji, X., Kirikkaleli, D., Shahbaz, M., and Zhou, X. (2020). Environmental Cost of Natural Resources Utilization and Economic Growth: Can China Shift Some Burden through Globalization for Sustainable Development?. Sustainable Development. doi:10.1002/sd.2116

Umar, M., Ji, X., Mirza, N., and Naqvi, B. (2021). Carbon Neutrality, Bank Lending, and Credit Risk: Evidence from the Eurozone. J. Environ. Manag. 296, 113156. doi:10.1016/j.jenvman.2021.113156

Vallés-Giménez, J., and Zárate-Marco, A. (2020). A Dynamic Spatial Panel of Subnational GHG Emissions: Environmental Effectiveness of Emissions Taxes in Spanish Regions. Sustainability 12, 872. doi:10.3390/su12072872

Wang, Q., and Wang, L. (2021). The Nonlinear Effects of Population Aging, Industrial Structure, and Urbanization on Carbon Emissions: A Panel Threshold Regression Analysis of 137 Countries. J. Clean. Prod. 287, 125381. doi:10.1016/j.jclepro.2020.125381

Wang, Q., Yuan, X., Zuo, J., Mu, R., Zhou, L., and Sun, M. (2014a). Dynamics of Sewage Charge Policies, Environmental Protection Industry and Polluting Enterprises-A Case Study in China. Sustainability, 6(8), 4858–4876. doi:10.3390/su6084858

Wang, Z., Feng, C., and Zhang, B. (2014b). An Empirical Analysis of China's Energy Efficiency from Both Static and Dynamic Perspectives. Energy 74, 322–330. doi:10.1016/j.energy.2014.06.082

Wang, Y., Niu, Y., Li, M., Yu, Q., and Chen, W. (2022). Spatial Structure and Carbon Emission of Urban Agglomerations: Spatiotemporal Characteristics and Driving Forces, Sustain. Cities Soc., 78, 103600. doi:10.1016/j.scs.2021.103600

Wang, Y., and Yu, L. (2021). Can the Current Environmental Tax Rate Promote Green Technology Innovation? - Evidence from China's Resource-Based Industries. J. Clean. Prod. 278, 123443. doi:10.1016/j.jclepro.2020.123443

Wesseh, P. K., and Lin, B. (2019). Environmental Policy and 'double Dividend' in a Transitional Economy. Energy Policy 134, 110947. doi:10.1016/j.enpol.2019.110947

Wolde-Rufael, Y., and Mulat-Weldemeskel, E. (2021). Do environmental Taxes and Environmental Stringency Policies Reduce CO2 Emissions? Evidence from 7 Emerging Economies. Environ. Sci. Pollut. Res. 28 (18), 22392–22408. doi:10.1007/s11356-020-11475-8

Xiang, L., Chen, X., Su, S., and Yin, Z. (2021). Time-Varying Impact of Economic Growth on Carbon Emission in BRICS Countries: New Evidence from Wavelet Analysis. Front. Environ. Sci. 36, 5149. doi:10.3389/fenvs.2021.715149

Xiao, Z., Yu, L., Liu, Y., Bu, X., and Yin, Z. (2022). Does Green Credit Policy Move the Industrial Firms toward a Greener Future? Evidence from a Quasi-Natural Experiment in China. Front. Environ. Sci. 9. doi:10.3389/fenvs.2021.810305

Xie, R., Wang, F., Chevallier, J., Zhu, B., and Zhao, G. (2018). Supply-side Structural Effects of Air Pollutant Emissions in China: A Comparative Analysis. Struct. Change Econ. Dyn. 46, 89–95. doi:10.1016/j.strueco.2018.04.005

Xing, C., Zhang, Y., and Wang, Y. (2020). Do Banks Value Green Management in China? the Perspective of the Green Credit Policy. Finance Res. Lett. 35. doi:10.1016/j.frl.2020.101601

Xu, B., and Lin, B. (2020). Investigating Spatial Variability of CO2 Emissions in Heavy Industry: Evidence from a Geographically Weighted Regression Model, 112011. Energy Policy.

Yang, M., Fan, Y., Yang, F., and Hu, H. (2014). Regional Disparities in Carbon Dioxide Reduction from China's Uniform Carbon Tax: A Perspective on Interfactor/interfuel Substitution. Energy 74, 131–139. doi:10.1016/j.energy.2014.04.056

Yin, Z., Peng, H., Xiao, Z., Fang, F., and Wang, W. (2022). The Carbon Reduction Channel through Which Financing Methods Affect Total Factor Productivity: Mediating Effect Tests from 23 Major Carbon-Emitting Countries. Environ. Sci. Pollut. Res., 1–13. doi:10.1007/s11356-022-19945-x

Zhang, L., and Ma, L. (2020). The Relationship between Industrial Structure and Carbon Intensity at Different Stages of Economic Development: an Analysis Based on a Dynamic Threshold Panel Model. Environ. Sci. Pollut. Res. 27, 33321–33338. doi:10.1007/s11356-020-09485-7

Zhang, X., and Wang, Y. (2017). How to Reduce Household Carbon Emissions: A Review of Experience and Policy Design Considerations. Energy Policy 102, 116–124. doi:10.1016/j.enpol.2016.12.010

Zhao, G., Zhou, P., and Wen, W. (2021). Feed-in Tariffs, Knowledge Stocks and Renewable Energy Technology Innovation: The Role of Local Government Intervention. Energy Policy 156, 112453. doi:10.1016/j.enpol.2021.112453

Keywords: pollutant discharge fee, industrial pollution, carbon emission, panel regression, mediation effect, threshold effect

Citation: Wang Z, Yu L, Zheng M, Xing Y, Liu X, Wang Y and Xiao Z (2022) One Fee, Two Reductions: The Double Abatement Effect of Pollutant Discharge Fees on Industrial Pollution and Carbon Emissions. Front. Environ. Sci. 10:928434. doi: 10.3389/fenvs.2022.928434

Received: 25 April 2022; Accepted: 23 May 2022;

Published: 08 June 2022.

Edited by:

Xiaohang Ren, Central South University, ChinaReviewed by:

Kangyin Dong, University of International Business and Economics, ChinaCopyright © 2022 Wang, Yu, Zheng, Xing, Liu, Wang and Xiao. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Zumian Xiao, eGlhb3p1bWlhbkBzZHVmZS5lZHUuY24=

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.