Tinghua Liu

Tinghua Liu Weiya Liu

Weiya Liu Ehsan Elahi

Ehsan Elahi Xiao Liu2*

Xiao Liu2*- 1School of Economics, Shandong University of Technology, Zibo, China

- 2School of Urban and Regional Science, Shanghai University of Finance and Economics, Shanghai, China

Sustainable development is crucial to the survival and healthy development of enterprises, which is closely related to their financing situation. Supply chain finance is an effective way to improve and enhance the financing situation by easing financing constraints and reducing financing costs. As an important source of supply chain short-term financing, trade credit plays an important role in enterprise production and circulation. Taking Chinese listed companies from 2011 to 2020 as samples, this paper studied the impact of trade credit on sustainable growth and its internal mechanism. Furthermore, we analyzed the moderating effect of digital finance development on the influence of trade credit on sustainable growth. It is found that receiving trade credit benefited firms’ sustainable growth. Furthermore, study found that receiving trade credit has a greater positive impact on the sustainable growth of enterprises in regions with higher levels of financial development, high-tech industries, state-owned enterprises and small enterprises. Whereas, the provision of trade credit had an obvious inhibiting effect on the sustainable growth of enterprises in the regions with low level of financial development, non-high-tech industries, private enterprises and small enterprises. The results of the influencing mechanism showed that receiving trade credit promoted firm’s sustainable growth by “agency cost reducing effect,” while providing trade credit inhibited firm’s sustainable growth by “forcing effect.” In addition, the development of digital finance weakens the positive impact of trade credit financing on enterprises’ sustainable growth but strengthens the negative impact of providing trade credit on sustainable growth. From the perspective of sustainable growth, this paper explained the role of trade credit financing in alleviating the financing dilemma of enterprises, which is urgently needed by most emerging economies pursuing high-quality development. Therefore, in order to give full play to the role of trade credit financing, the government should actively create a good credit environment. At the same time, the government should vigorously develop digital finance to enhance its ability to serve the real economy.

1 Introduction

Growth is the eternal theme of the enterprise, and whether sustainable growth can be achieved is related to the fate of the enterprise’s future development. In the context of the global financial crisis and the pursuit of economic recovery and sustainable growth, the economic growth model based on sustainable growth is proposed to achieve sustainable growth. Sustainable growth refers to the realization of ecological balance and economic and social development on the premise of coordinated development between the speed and scale of economic and social development and the ecological environment. The concept of agricultural and environmental sustainability refers to minimizing the degradation of natural resources while increasing crop productions (Abbas et al., 2022). Currently, fertilizers account for about half of the total input energy in maize production in Pakistan (Abbas et al., 2020), and reducing overuse of farm inputs is a potential sustainable crop production strategy (Abbas et al., 2021). The real economy is the mainstay of sustainable growth. The sustainable growth of enterprises refers to that in the process of pursuing survival and development, enterprises should not only achieve their business objectives but also maintain their continuous profitability, and ultimately ensure the long-term prosperity of enterprises. The realization of sustainable growth goals is conducive to improve enterprises’ ability to create wealth, increasing employment, improving the quality of economic growth and social and economic value (Xiao and Wang, 2004), which is of great significance to promote the healthy development of real economy. In the process of economic transformation from high-speed growth stage to high-quality development stage, how to realize the sustainable growth of enterprises and inject sustainable impetus into the high-quality development of China’s real economy has become an important issue. Therefore, it is of great theoretical and practical significance to explore the factors affecting the sustainable growth of enterprises to prevent the financial risks of enterprises and promote the healthy development of entity enterprises. The production and operation of enterprises need funds, and the financing capacity determines the sustainable growth prospects of enterprises. Due to the existence of credit rationing, enterprises are often excluded from the traditional financial system due to their weak conditions, and indirectly obtain limited financial services. In addition, the direct financing channels of equity and creditor’s rights are not perfect. The current financing problem is still the key factor restricting the sustainable development of Chinese enterprises.

Supply chain finance is a professional field of commercial bank credit business, but also a financing channel for enterprises, especially small and medium-sized enterprises. It is a financing model that can provide flexible financial products and services, and a systematic financing arrangement for all members of the supply chain. Supply chain finance is a series of technology-based business and financing processes that link transaction buyers, sellers and financing institutions with the aim of easing corporate financing constraints, reducing financing costs, and optimizing working capital (Tang and Zhuang, 2021). Supply chain financing types include bank credit financing and trade credit financing (Tang et al., 2017). Under the trade credit financing mode, enterprises often transfer credit to the upstream and downstream enterprises in the supply chain in the form of short-term credit. But bank credit financing makes it difficult for enterprises to obtain loans because of harsh lending conditions. Therefore, trade credit financing is more common and important for enterprises, and is more conducive to supply chain coordination (Chang and Rhee, 2011). As an important source of short-term financing in the supply chain, trade credit financing plays a role in accelerating capital turnover and lubricating production and circulation in industrial development, which is of great significance to short-term financing for enterprises in a vulnerable position in the supply chain (Liang et al., 2016). Therefore, this paper discusses the impact of trade credit based on supply chain finance on firm’s sustainable growth.

Trade credit is a kind of direct finance which is born in the entity enterprise. Companies can alleviate short-term capital shortages by occupying capital from upstream and downstream enterprises, thus reducing financing problems. In particular, the advantages of convenient financing and fewer restrictions are favored by more and more enterprises. Studies have confirmed that more than 65% of American enterprises and 75% of British enterprises use trade credit as a financing method in the production and sales process (Atanasova and Wilson, 2003). Moreover, the contribution of trade credit financing to economic development is no less than that of bank credit (Ge and Qiu, 2007). Trade credit financing can realize higher resource allocation efficiency than bank loan (Shi and Zhang, 2010). Therefore, especially for the immature financial development of China, the use of trade credit is of great significance to realize the sustainable growth of enterprises.

Digital finance is a new financial mode in which traditional financial institutions and Internet companies use digital technology to realize financing, payment, investment and other financial activities (Huang and Huang, 2018). Traditional financial development is the foundation of digital financial development, the better traditional finance develops, the faster digital finance develops (Wang et al., 2021). Trade credit financing is an effective supplement to traditional finance and plays an alternative financing role. Therefore, it is necessary to further subdivide the impact of trade credit on sustainable growth under different levels of financial resources. Based on this, this paper further analyzes the impact of trade credit on sustainable growth of enterprises at different levels of digital finance development.

Compared with the article of Huang et al. (2019), our research contributes to the literature in three aspects. Firstly, this paper discusses the impact on the sustainable growth of enterprises from the dual perspective of trade credit supply and demand. It enriches the research perspective of the influencing factors of enterprises’ sustainable growth and provides theoretical support for enterprises’ sustainable growth policy formulation at the level of trade credit. Secondly, it enriched the research on the economic effect of trade credit and confirmed the influence mechanism and intermediary effect of trade credit on sustainable growth. More importantly, it discusses the moderating effect of digital finance development on trade credit and sustainable growth, and expands related research on trade credit from the perspective of regional financial development.

The remaining article is structured as: We first review the literature and develop our hypotheses in Section 2. Section 3 describes the data, variable and model. Section 4 presents the empirical results of how trade credit affects the sustainable growth of enterprises and discusses the moderating effect of digital finance development. Conclusions are provided in the final section.

2 Literature Review and Research Hypotheses

China’s financial system is dominated by bank loans, but there is a mismatch of financial resources. Enterprises’ production and operation are short of capital sources and the efficiency of resource allocation is low for a long time, which is not conducive to sustainable growth of enterprises and seriously hinders the economic development process (Sui, 2017; Zhou et al., 2021). The emergence of trade credit financing can effectively make up for the deficiency of traditional finance. In the case of imperfect financial market development, insufficient supply of credit resources and limited financing channels for enterprises, trade credit assumes the supplementary function of financing and is an important external financing channel for enterprises (Sun et al., 2014). Enterprises facing financing constraints that are more inclined to replace traditional bank loans with trade credit (Zhang, 2019), and trade credit can achieve greater scale efficiency than traditional bank loans (Shi and Zhang, 2010). Fisman and Love (2003) found that in regions with relatively slow financial development, the growth rate of industries dependent on trade credit was higher. Trade credit is a kind of credit behavior frequently occurring in supply chain enterprises. It is a kind of informal financing, widely existing in the business activities of enterprises. On the one hand, enterprises obtain funds through deferred payment, advance collection and other ways to solve the problem of short-term capital shortage and reduce financing constraints. Thus, the efficiency of enterprise resource allocation can be improved (Elahi et al., 2018b) to promote the efficient investment (Tian, 2019; Liu et al., 2021; Elahi et al., 2022), and profitability and performance of system can be improved (Elahi et al., 2018a; Gao, 2019). On the other hand, the use of trade credit can add certainty to the inflow and outflow of cash. The production and operation environment of enterprises is improved, more funds will be invested in R&D and innovation activities, which is of great significance to improve market competitiveness and production efficiency (Liu et al., 2022). Therefore, trade credit financing has a positive impact on the sustainable growth of enterprises.

The separation of ownership and management leads to serious principal-agent problems between shareholders and management, which may lead to “short-sighted behavior” of management. As a result, resource allocation efficiency is low for a long time, which is not conducive to the sustainable growth of enterprises (Chen and Tang, 2006). Compared with other creditors, trade creditors have advantages in information acquisition, customer control and property recovery (Du, et al., 2021). Therefore, it can better play the supervision function of creditors and restrain agency behavior, thus effectively reducing agency cost and improving investment efficiency (Liu and Guan, 2016). Moreover, as a short-term liability, trade credit can limit managers’ pursuit of profitable financial assets (Du et al., 2021). Therefore, industrial investment will be promoted and R&D investment and innovation activities of enterprises will be improved (Xu and Zhu, 2017; Xiao et al., 2021; Zhao et al., 2021; Rathnayake et al., 2022), and ultimately promote the sustainable growth of enterprises. At this point, trade credit, as a short-term liability, may affect the sustainable growth of enterprises by reducing agency costs. Therefore, we propose the first hypothesis of this paper, namely hypothesis 1.

Enterprises provide trade credit also bear credit risks. If customers intentionally occupy corporate funds, trade credit will become a malicious default to obtain corporate liquidity at a lower cost (Fabbri and Menichini, 2010). Such behavior will squeeze enterprise resources, lead to limited operating cash flow, increase operating risks, and thus adversely affect the sustainable growth of enterprises. Firstly, the role of the firm in providing liquidity may increase the risk of overdue collection and capital chain disruption, thus affecting overall efficiency (Wu et al., 2021). Secondly, providing trade credit means giving up the opportunity to earn interest income, resulting in opportunity costs. At the same time, the provision of trade credit also increases the cost of credit management. In particular, companies spend more time and money closely monitoring the flow of customers’ funds. Finally, the provision of trade credit also means that enterprises have tax obligations before they get the cash flow of sales revenue, leading to the outflow of tax funds and the reduction of internal funds of enterprises, thus hindering sustainable growth. Li and Song (2021) found that the “compulsory credit” formed by debt default that was not conducive to the development of enterprises. Therefore, trade credit may be a kind of “mandatory credit,” and malicious breach of contract increases market transaction costs, operational risks and resource allocation costs (Chen et al., 2016). Thus, it increases the uncertainty of enterprise production and operation and seriously hinders the sustainable growth of enterprises. To sum up, the provision of trade credit increases the risks and costs of enterprises, produces a “mandatory effect,” and has a negative impact on the sustainable growth of enterprises. Therefore, we propose hypothesis 2.

There are obvious regional differences in China’s economic development. Higher development level of traditional finance, there will be more perfect the financial system, and the level of credit issued by banks will also higher. The use of trade credit financing will further increase the capital of enterprises and reduce financing constraints. Thus, the guarantee of funds ensures the normal operation of production and management and promotes the sustainable growth of enterprises. In highly developed financial areas, the use of trade credit plays a “icing on the cake” role for enterprises. In areas with low level of financial development, the financial system is imperfect and financing channels for enterprises are limited (Sheng, 2021; Sun, 2021). The provision of trade credit increases the cost and management risk of enterprises, and the production environment deteriorates further, which is not conducive to improve the sustainable growth level of enterprises.

Similarly, the response to trade credit varies by industry. High-tech industrial enterprises are characterized by high skills, high investment and high risk. They have difficulty in financing and are highly dependent on external capital (Zhang and Hu, 2020; Elahi et al., 2021). However, traditional financial institutions pay more attention to hard assets that can be secured when lending, which makes it difficult for high-tech enterprises to obtain financing from banks and they have to turn to other financing channels for financing. At this point, trade credit financing can effectively solve this problem. It can improve the capital environment of enterprises, improve the level of investment in R&D, and then promote the sustainable growth of high-tech industry enterprises. At the same time, it is worth noting that high-tech enterprises themselves are facing strong competitive pressure and are keener to carry out innovative activities to compete for market position (Zhu et al., 2019). In addition, the government’s policy support for high-tech enterprises makes it easier for them to obtain government innovation subsidy funds. Therefore, the provision of trade credit has little effect on inhibiting innovation and has limited ability to reduce the level of sustainable growth. As a result, the negative impact of the provision of trade credit is more obvious in non-high-tech enterprises than high-tech enterprises.

China’s financial resources are badly mismatched. Compared with private companies, state-owned enterprises are more favored by the credit sector. The better relationships with governments tend to give them access to bigger credit lines, longer loan maturities and lower interest costs. Despite their significant contribution to economic development, private enterprises are often excluded from the formal financial system due to their lack of effective collateral assets, unsecured records and poor credit histories, making it difficult for them to obtain the financial services they need. At this time, the emergence of trade credit as an informal financing method is beneficial to the development of private enterprises. It can increase the external financing channels of private enterprises and promote the sustainable growth of enterprises. There is also an empirical fact that state-owned enterprises are obliged to shoulder the burden of government policies, including some of the construction of projects in the form of overinvestment. State-owned enterprises often suffer from excessive investment and overcapacity (Liu et al., 2018), and low investment efficiency. However, the phenomenon of providing trade credit occupying their funds will reduce excessive investment behavior. As a result, state-owned enterprises can allocate capital more efficiently and invest more efficiently, thus promoting sustainable growth. Namely, the provision of trade credit significantly promoted the sustainable growth of state-owned enterprises.

There exists “scale discrimination” in the allocation of financial resources in China. Small enterprises are small in scale, lack of effective asset guarantee, and have low quality of external information disclosure. Therefore, it is difficult for them to obtain traditional bank credit. As an informal financing mode, trade credit has positive impact on the sustainable growth of small enterprises. However, due to their low market position, small enterprises are often forced to provide trade credit to large enterprises, resulting in their capital encroachment. Moreover, it is difficult for small enterprises to obtain external capital, leading to a high possibility of capital chain fracture. Therefore, the provision of trade credit has a greater negative impact on the sustainable growth of small businesses. Therefore, we propose hypothesis 3 about heterogeneity.

Whether the use of trade credit can promote the sustainable growth of enterprises is also closely related to digital finance. With the application of digital technology, digital finance occupies a considerable position in China’s modern financial system and has a significant impact on China’s economic development. Digital finance has financial attributes and does not change the essence of financial services. However, different from traditional finance, digital finance can cover customers that are difficult to be covered by traditional finance, cover more long-tail groups, and improve the convenience and availability of financial services (Chen et al., 2021). China’s financial system is dominated by commercial banks. In areas with low level of digital finance development, enterprises rely more on traditional bank loan financing mode. With the improvement of the development level of digital finance, Internet finance, online lending and other network services continue to occupy the traditional banking business (assets, liabilities, and intermediate business). The development of digital finance makes traditional financial institutions compete with each other for market share, actively carry out digital transformation, and constantly improve the efficiency and quality of financial services (Wu, 2015). Therefore, the financing difficulty of enterprises is reduced (Tang et al., 2020), thus weakening the positive impact of informal finance-trade credit financing on sustainable growth.

In areas with a high level of digital finance development, online services such as Internet financial products are increasing. As the real economy is struggling and inefficient, enterprises invest more money in online financing in pursuit of higher short-term returns and profit maximization. The development of the real economy was not given much attention. Moreover, the financial products chosen may face higher risks, for example, some Internet loan asset-backed securities are highly leveraged. Chen and Ye (2016) found that the interest rate fluctuations of online loans have agglomeration and risk accumulation effects. Loan market has strong risks, but market participants have weak awareness of risk identification and are prone to temptation of high returns. One of the most direct evidences of the negative impact of the development of digital finance is the explosive phenomenon of P2P products. It reduces the possibility for enterprises to recover capital, including principal and interest, resulting in credit risk, resulting in a shortage of capital flow needed for production and operation. Thus, the development of digital finance reinforces the negative impact of the provision of trade credit on sustainable growth. In summary, our assumptions are given as follows:

Hypothesis 1: Receiving trade credit has a positive impact on sustainable growth, which may be achieved through a channel of reducing firm’s agency costs.

Hypothesis 2: The provision of trade credit is not conducive to the sustainable growth of enterprises.

Hypothesis 3: The impact of trade credit on sustainable growth has obvious regional differences and enterprise characteristics differences.

Hypothesis 4: The development of digital finance weakens the positive effect of obtaining trade credit financing on sustainable growth of enterprises, while strengthens the negative effect of providing trade credit on sustainable growth.

3 Materials and Methods

In this stage, sample data, variable definitions and econometric models used in this paper are introduced in three sections respectively.

3.1 Data and Sampling

This paper takes listed non-financial companies in China from 2011 to 2020 as research samples. To eliminate the effects of variable outliers, we also winsorize all main continuous variables at 1% level. The main financial data obtained from the China Stock Market and Accounting Research Database (CSMAR), the property of ownership indicators is derived from CCER China Economic and Financial Database. The data of digital finance index come from “The Peking University Digital Financial Inclusive Index of China (PKU-DFIIC)” released by Peking University Digital Finance Research Center, which has been widely used by Chinese scholars. Grouped variable-financial development level data were obtained from China Statistical Yearbook.

3.2 Definitions of Variables

3.2.1 Sustainable Growth

The dependent variable “sustainable growth of firm,” denoted as SGR. Chinese scholars found that sustainable growth rate refers to the maximum sales growth rate that an enterprise can achieve without increasing external equity funds (Guo and Guo, 2002). Most of the existing literature adopts the sustainable growth model proposed by Higgins (1988) and Van Horne (1988). In this paper, the model constructed by Higgins is used to calculate the dependent variable in the basic regression. It is explained the sustainable growth rate as the maximum sales growth rate an enterprise can achieve without exhausting its resources, which is a balanced growth and reveals the financial factors that restrict the growth of an enterprise. In a robustness test, we used Van Horne’ model to calculate the sustainable growth rate, emphasizing the target value of sustainable growth.

3.2.2 Trade Credit

This paper studies trade credit from the perspective of supply and demand, which can be divided into “access to trade credit” (AP) and “provision of trade credit” (AR). Among them, the independent variable AP is measured as the sum of accounts payable, notes payable and advance receivable scaled by total assets, and AR is measured as the sum of notes receivable, accounts receivable and prepayments scaled by total assets (Lu and Yang, 2011; Liu, 2021).

3.2.3 Digital Finance

We adopt the PKU-DFIIC as a proxy variable to measure the level of digital finance of each city, which is compiled by a joint research team composed of the Peking University Digital Finance Research Center and Ant Financial Group. The data, which started in 2011 and is updated until 2020, can effectively measure the development of digital finance in China (Guo et al., 2020). In the analysis, we not only use aggregate index (Fin) to describe the digital finance level of each city, but also use first-level indicators including coverage_breadth (B), usage_depth (D), and digitization_level (S). In order to avoid the influence of excessive value and improve the fitting of regression, we take logarithm of digital finance index.

3.2.4 Control Variables

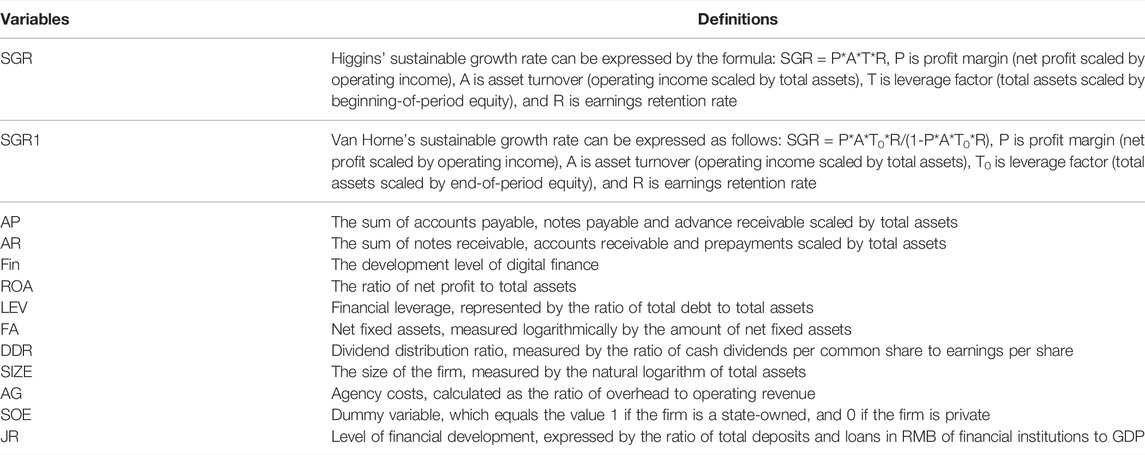

According to the existing literature on the sustainable growth of enterprises, control variables including return on total assets (ROA), leverage ratio (LEV), net fixed assets (FA), dividend distribution ratio (DDR) and enterprise size (SIZE) are selected. The specific meaning of each variable is presented in Table 1.

TABLE 1. The definitions of the main variables.

3.3 Econometric Model

3.3.1 Basic Regression Model

Benchmark model was used to estimate the impact of trade credit on the sustainable growth of enterprises (Fisman and Love, 2003).

Here subscripts i and t respectively represent individual enterprise and year. SGR represents sustainable growth of enterprise. AP and AR represent the acquisition and provision of trade credit, respectively. Control represents the control variables that may affect the sustainable growth of an enterprise. U is the individual effect of the enterprise, which is used to control the characteristics of the enterprise that do not change with time and cannot be observed. In addition, we control for year.

3.3.2 Mediating Effect Model

To further explore the potential mechanism of trade credit financing affecting sustainable growth of enterprises, this paper refers to the mediation effect test model proposed by Wen and Ye (2014) to test whether trade credit can promote sustainable growth of enterprises by reducing agency costs.

AG is the selected intermediary variable-agency cost. Other variables are defined in the same way as Eqs 1, 2.

3.3.3 Moderating Effect Model

To further analyse the relationship between trade credit and sustainable growth of enterprises in the external environment of digital finance development, this paper sets the following moderating effect model for empirical analysis. The main method to judge whether the moderating effect exists or not is to verify the significance of interaction coefficient. In this study, it can be achieved by judging whether the interaction coefficients (

Subscript c stands for city. Fin represents the development level of digital finance. The definitions of other variables are the same as above.

4 Results and Discussion

In this stage, firstly, the statistical characteristics of the data are briefly analyzed. Secondly, we first analyze the effect of trade credit on sustainable growth of enterprises, including baseline regression, heterogeneity analysis and robustness analysis, and then analyze the mechanism of trade credit on sustainable growth. Finally, the moderating effect of digital finance development is analyzed. In addition, in the regression results of all our tables, standard errors are reported in parentheses, with *, **, and ** indicating statistical significance at 10%, 5%, and 1% levels, respectively.

4.1 Descriptive Statistics

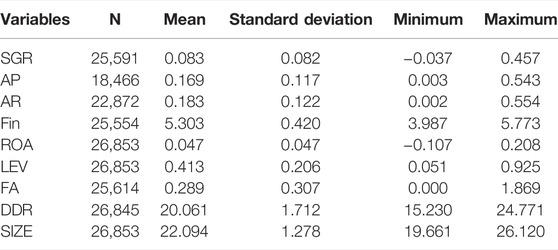

The descriptive statistics are presented in Table 2. The minimum value of SGR is −0.037, while the maximum value is 0.457, indicating that there are significant differences in sustainable growth among enterprises. The minimum AP value is 0.003 and the average value is 0.169, the minimum value of AR was 0.002 and the average value was 0.183, indicating that the use of trade credit by some enterprises has not reached the average level. After taking the logarithm, the minimum value of Fin is 3.987, and the maximum value is 5.773, indicating that there are obvious differences in the development of digital finance among regions. Other variables are also different in different degrees, which lays a foundation for this study. It is worth noting that when the sustainable growth of an enterprise is negative, it indicates that the company’s current operating efficiency and financial policies are unreasonable. When this situation occurs, enterprises should make adjustments in time to reverse the adverse situation.

TABLE 2. Descriptive statistics.

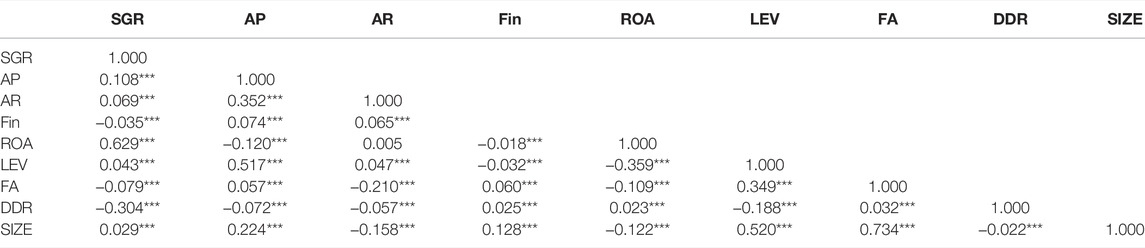

Before the multiple regressions, we report the Pearson correlation matrix in Table 3. The correlation between AP and SGR is significantly positive, which provides preliminary evidence that access to trade credit can help to improve the sustainable growth of enterprises. The AR is also positively correlated with SGR. Sustainable growth (SGR) is positively correlated with return on total assets (ROA), leverage ratio (LEV) and enterprise size (SIZE), and negatively correlated with net fixed assets (FA) and dividend distribution ratio (DDR).

TABLE 3. Correlation matrix.

4.2 Basic Regression Results

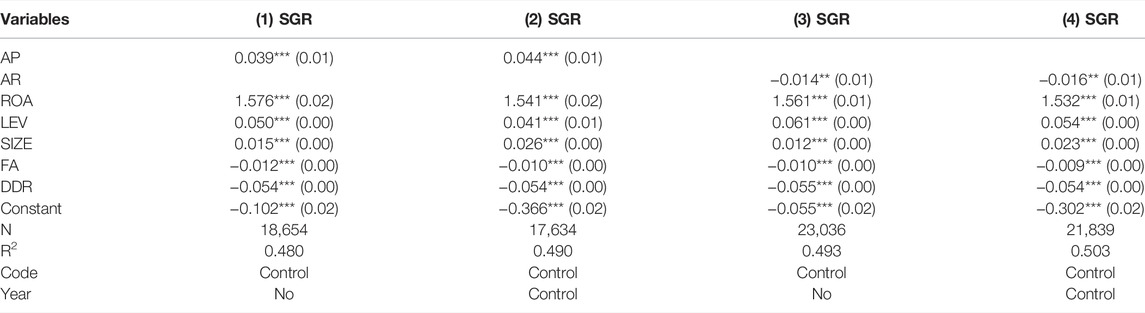

The Hausmann test results indicate that the fixed effects model should be used. The fixed effect regression results after controlling the influence of other variables are shown in Table 4. As can be seen from columns (1) and (2) of the Table 4, the regression coefficient between the AP and SGR is positive and significant at 1% level. That is, the acquisition of trade credit significantly promotes the sustainable growth of enterprises, and hypothesis 1 is partially verified. The possible explanation is that the access to trade credit effectively alleviates the financial pressure of enterprises and alleviates the financing constraints. The financial situation of enterprises is improved, the level of R&D investment of enterprises is increased, the market competitive advantage is enhanced, and the sustainable growth of enterprises is promoted. There is a significant negative correlation between the AR and SGR in columns (3) and (4), indicating that the provision of trade credit has a negative impact on the sustainable growth of enterprises, which verifies hypothesis 2 proposed in this paper. This may be because the provision of trade credit increases the cost of enterprises, and the situation of capital occupation is not conducive to the guarantee of normal production and operation in the later period. That is, the provision of trade credit has a “mandatory effect,” which is not conducive to the improvement of enterprises’ sustainable growth ability. In the analysis of control variables, ROA, LEV, and SIZE are positively correlated with the sustainable growth of enterprises, while FA and DDR are negatively correlated with the sustainable growth of enterprises. By comparing the results of columns (1), and (2), (3) and (4), it can be seen that the impact of trade credit on sustainable growth is more obvious after year is controlled, so two-way fixed effect model is adopted in the subsequent regression.

TABLE 4. Benchmark regression results: Trade credit and sustainable growth.

4.3 Heterogeneity Analysis

In hypothesis 3, we assume that there are obvious regional differences and firm characteristics differences in the impact of trade credit on firm sustainable growth. Therefore, we test the hypothesis in the empirical part.

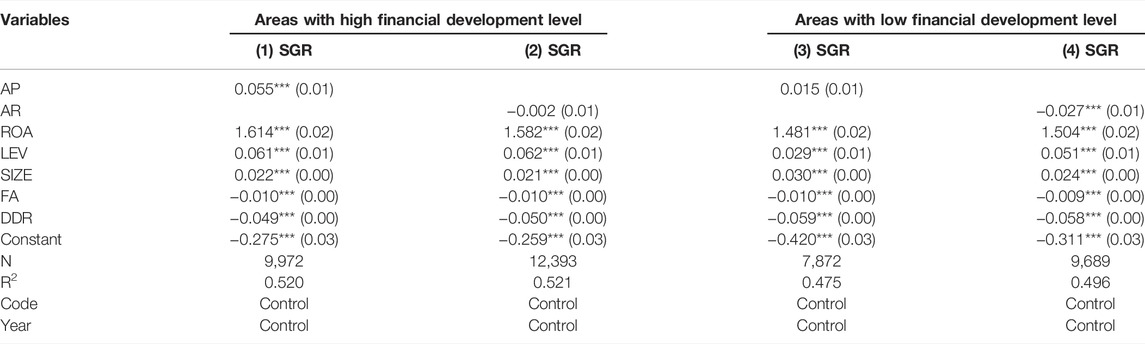

4.3.1 Heterogeneous Impact on Areas With Different Levels of Financial Development

Table 5 reports the regression results. In column (1) of Table 5, the coefficient of AP is significantly positive, while the coefficient in column (3) is not significant. The promoting effect of AP on SGR is more obvious in the regions with higher level of financial development. In column (2) of Table 5, the coefficient of AR is negative but not significant, and that in column (4) is significantly negative. The inhibition effect of AR on SGR is more obvious in enterprises in low level of financial development. The results were as expected.

TABLE 5. Heterogeneity analysis: Level of financial development.

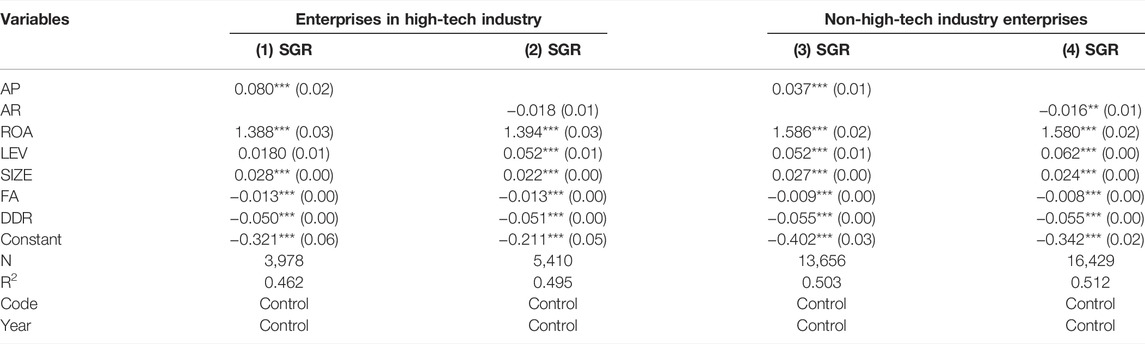

4.3.2 Heterogeneous Impact on Different Industries

Table 6 reports the regression results by industry type. The coefficients of AP in columns (1) and (3) of Table 6 are positive at the 1% significance level, indicating that the acquisition of trade credit has a positive impact on the sustainable growth of enterprises in high-tech and non-high-tech industries. Further, the comparison of coefficients shows that the promotion effect is more obvious in high-tech enterprises. In column (4) of Table 6, the coefficient of AR is significantly negative, while the coefficient in column (2) is not significant. The provision of trade credit significantly inhibits the sustainable growth of non-high-tech enterprises, but has no significant effect on high-tech enterprises.

TABLE 6. Heterogeneity analysis: High-tech and non-high-tech industries.

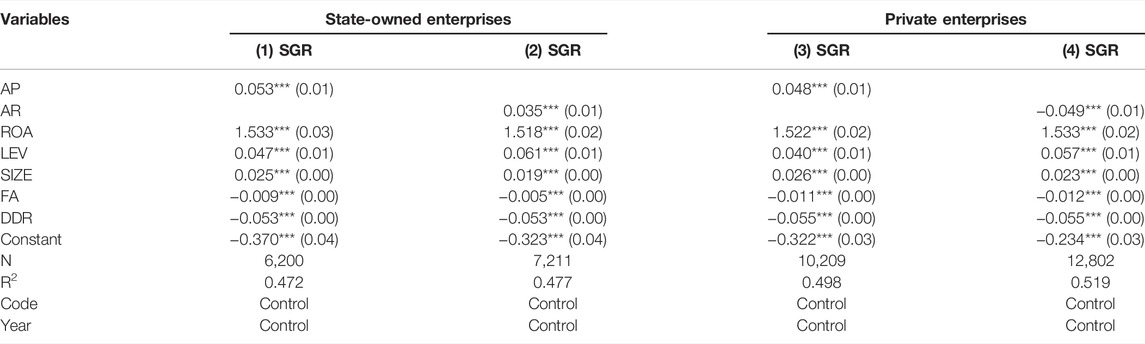

4.3.3 Heterogeneous Impact on Enterprises With Ownership

Table 7 reports the regression results for the differentiation of business ownership. In columns (1) and (3) of Table 7, the coefficient of AP is positive at the significant 1% level, indicating that access to trade credit has a positive impact on the sustainable growth of enterprises regardless of the nature of ownership. Further comparison of the coefficients showed that this effect is more obvious in state-owned enterprises. In column (2) of Table 7, the coefficient of AR is positive at the significant level of 1%, indicating that the provision of trade credit has a positive impact on the sustainable growth of state-owned enterprises.

TABLE 7. Heterogeneity analysis: Division of enterprise ownership.

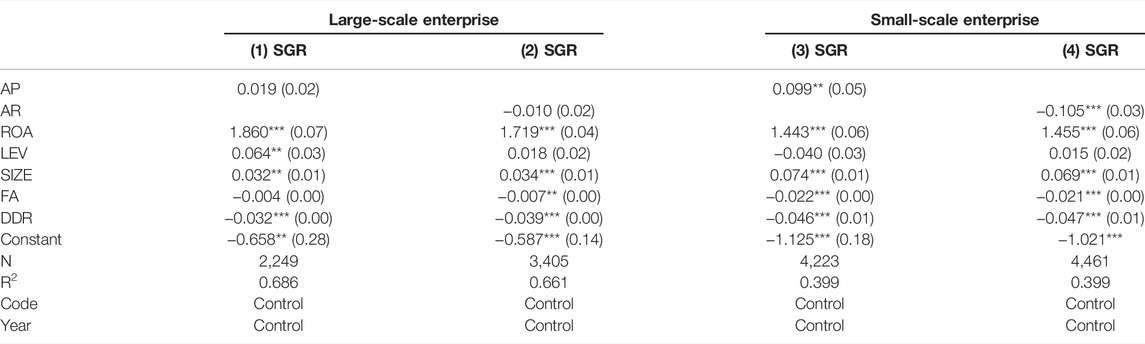

4.3.4 Heterogeneous Impact on Enterprise Size

Divide the top 25% of the size of the enterprise into small enterprises and the bottom 25% into large enterprise. Table 8 reports the results of the regression by firm size. In column (3) of Table 8, the coefficient of AP is positive at the significant level of 5%, indicating that access to trade credit has a positive impact on the sustainable growth of small enterprises. In contrast, in column (1) of Table 8, the coefficient of AP is not significant. As an alternative financing, trade credit plays an important role in increasing financing sources of small enterprises, effectively alleviating the dilemma of insufficient funds, reducing the negative impact of credit discrimination. Thus improving their sustainable growth level. Moreover, the coefficient of AR is significantly negative at the 1% level. The result verified hypothesis.

TABLE 8. Heterogeneity analysis: Division of enterprise size.

4.4 Robustness Tests

4.4.1 Measure of Substitution Variable

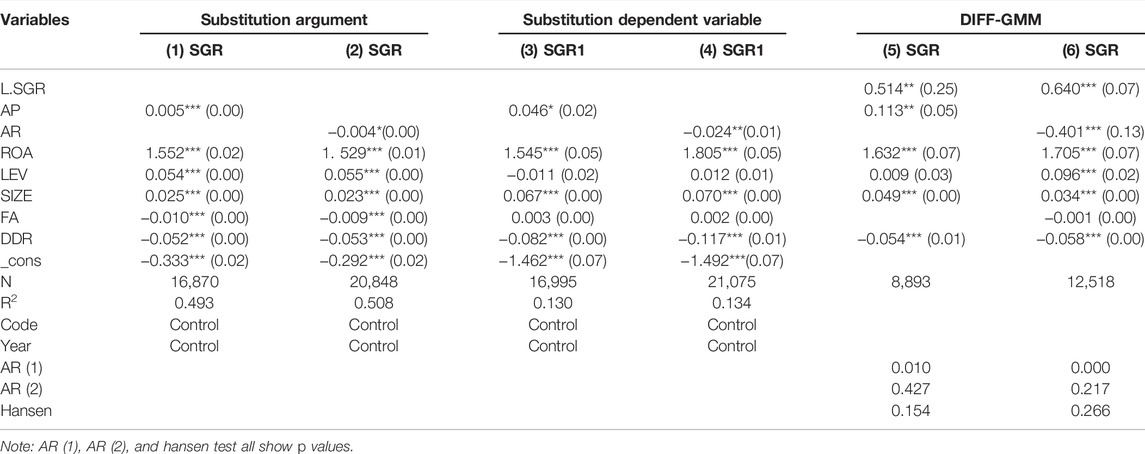

Since the measurement method of variables will produce bias to the results, we refer to Chen and Ma (2018) measurement of trade credit. AP is measured as the sum of accounts payable, notes payable and advance receivable scaled by operating cost, and AR is measured as the sum of notes receivable, accounts receivable and prepayments scaled by operating income. Regression results are shown in Columns (1) and (2) of Table 9. The sustainable growth rate calculated by Van Horne is used to measure the dependent variable in this paper, and the results are listed in columns (3) and (4) of Table 9. The above regression coefficients were expected and significant. The results of variable substitution show that the conclusions of this paper are still robust after the measurement methods of trade credit and sustainable growth are replaced.

TABLE 9. Substitution variables and regression methods.

4.4.2 Substitution Regression Method

To further test the robustness of our empirical results, we change regression method to help establish the causality. We use DIFF-GMM to investigate the impact of trade credit on the sustainable growth of enterprises (Yang et al., 2020). The first order lag of SGR was added into the DIFF-GMM model as an explanatory variable. The results of DIFF-GMM regression are shown in columns (5) and (6) of Table 9. The regression results show that the sustainable growth of the previous period is significantly positively correlated with the sustainable growth of the current period. This means that the sustainable growth of enterprises is affected by its own inertia, showing a strong self-cumulative effect. The results in the table show that AP is positively correlated with SGR, while AR is negatively correlated with SGR. The results are robust.

4.4.3 Management of Endogeneity Problem

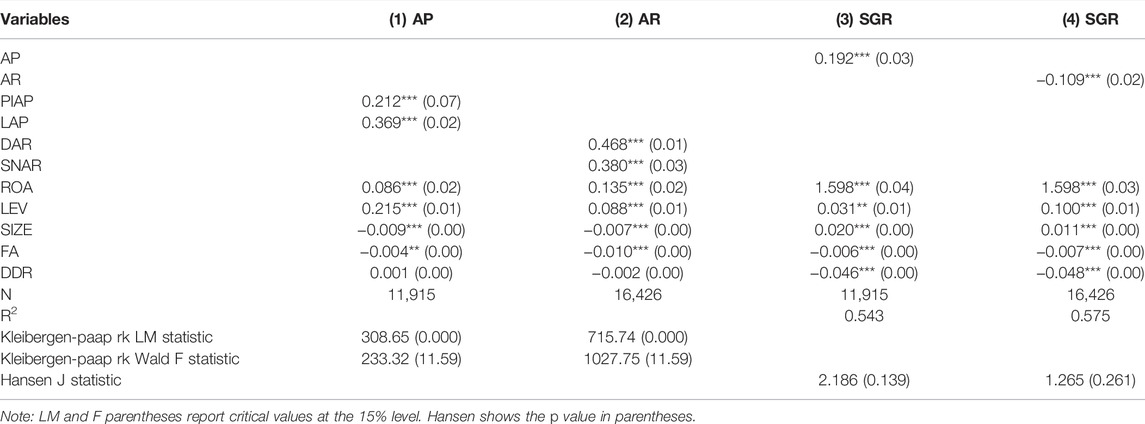

Finally, we used the idea of controlling endogenous problems to perform robustness tests. There may be a reverse causality relationship between trade credit and sustainable growth, which leads to the bias in the research results of this paper. The omission of variables in model selection may also lead to endogeneity. Therefore, two-stage instrumental-variable regression model is used to alleviate the endogeneity problem. In this study, the selection of instrumental variables draws on the ideas of Yu (2013) and Zhang et al. (2020). Details are as follows: the mean value of AP calculated by province and industry (PIAP) and first-order lag of AP (LAP) are used as instrumental variables of AP, and the mean value of AR calculated by year and industry (SNAR) and first-order difference of AR (DAR) are used as instrumental variables of AR.

The 2SLS regression results are reported in Table 10. It can be clearly seen from columns (1) and (2) in Table 10 that there are no weak instrumental variables, under-recognition and over-recognition problems, indicating that instrumental variables are effective. In addition, in columns (3) and (4), the coefficients are in line with expectations and significant, confirming that the results are still robust.

TABLE 10. Regression results of instrumental variables.

4.5 Test of Influence Mechanism

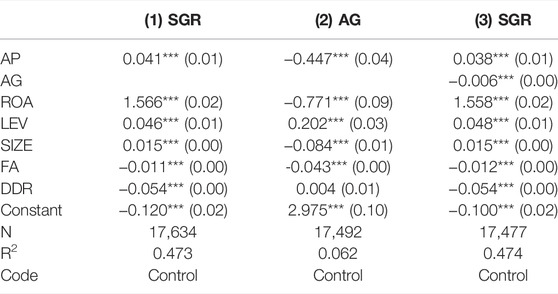

We used the mediating effect model to verify the influencing mechanism by referring to the current common practice of scholars. The selection of intermediary variable-AG index refers to the research of Liu (2021). The mediation effect proportion was calculated by ab/c. The mediating effect mechanism results are reported in Table 11. In column (2) of Table 11, AP is negatively correlated with AG, indicating that obtaining trade credit reduces the agency cost of enterprises. In column (3) of Table 11, AG is negatively correlated with SGR, indicating that agency cost seriously hinders enterprises from improving their sustainable growth level. The coefficient of column (3) is lower than that of column (1). The above results indicate that agency cost plays a partial intermediary role in the process of obtaining trade credit to promote the sustainable growth of enterprises. The mediation effect accounts for about 6.54% of the total effect. Obtaining trade credit promotes the sustainable growth of enterprises through reducing agency costs.

TABLE 11. Analysis of AP influence mechanism.

The empirical findings show that providing trade credit inhibits the sustainable growth of enterprises, confirming the “mandatory effect” proposed in the theoretical part. However, since there is no suitable proxy variable for the “mandatory effect” in the existing literature, this stage only examines its effect from the division of large and small enterprises. If the provision of trade credit significantly inhibits the sustainable growth of small enterprises, but the inhibitory effect on large-scale enterprises is not ideal, or the inhibitory effect on large-scale enterprises is not as good as that of small enterprises, it means that “mandatory effect” is established. The regression results of columns (2) and (4) in Table 8 are in line with expectations. In other words, the provision of trade credit produces a “mandatory effect” that inhibits sustainable growth of firms.

4.6 Analysis of External Environment of Digital Finance

To test hypothesis 4, we further explore the impact of trade credit on the sustainable growth of enterprises in the context of regional financial development from the perspective of digital finance. In the regression of moderating effect, digital financial data at city level were used and the data were decentralized.

4.6.1 The Impact of Total Indicators of Digital Finance

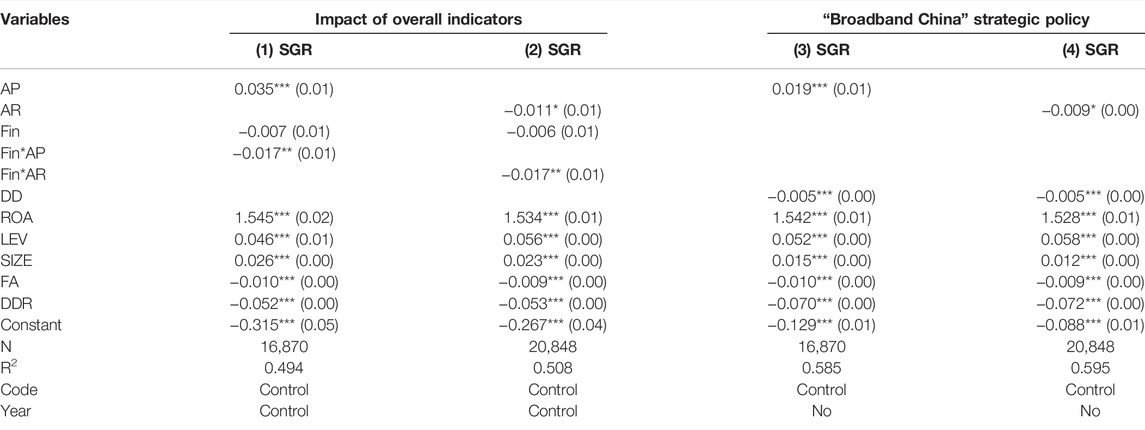

In column (1) of Table 12, the main effect coefficient is significantly positive, while the interaction coefficient is significantly negative. This suggests that the development of digital finance has weakened the positive impact of access to trade credit on sustainable growth. It may be that the development of digital finance has improved the degree of competition in the banking (Thakor, 2020), and thus prompted financial institutions to improve the efficiency and quality of financial services, so that enterprises can meet their loan needs more effectively. The service effect of informal finance is weakened, thus weakening the promotion effect of obtaining trade credit on sustainable growth. In column (2) of Table 12, the main effect coefficient is significantly negative, and the interaction effect coefficient is significantly negative. The development of digital finance has enhanced the negative impact of trade credit provision on sustainable growth. The possible reason is that with the high level of development of digital finance, enterprises are vulnerable to the temptation of high-risk and high-yield internet products. As a result, enterprises will put more money into internet financial products, which may reduce the probability of the return of investment funds. The funds needed for the development of the real economy have not been met. Thus, enhancing to the negative impact of trade credit provision on sustainable growth.

TABLE 12. Total digital finance index and “Broadband China” policy impact.

4.6.2 “Broadband China” Strategic Policy

The development of digital finance is inseparable from the construction of digital infrastructure. This paper chooses the “Broadband China” strategy pilot as exogenous policy impact, and uses the difference-in-differences model to explore the impact of trade credit on the sustainable growth of enterprises in the external environment of digital finance development. Since the “Broadband China” strategy was carried out in 3 years in 2014, 2015, and 2016, the policy implementation time was different, so the multi-period DID model should be adopted for empirical analysis. DD is the impact effect of the implementation of “Broadband China” policy. The results in columns (3) and (4) of Table 12 show that the effect of the implementation of “Broadband China” strategy policy is the same as that of basic regression.

4.6.3 Structured Analysis

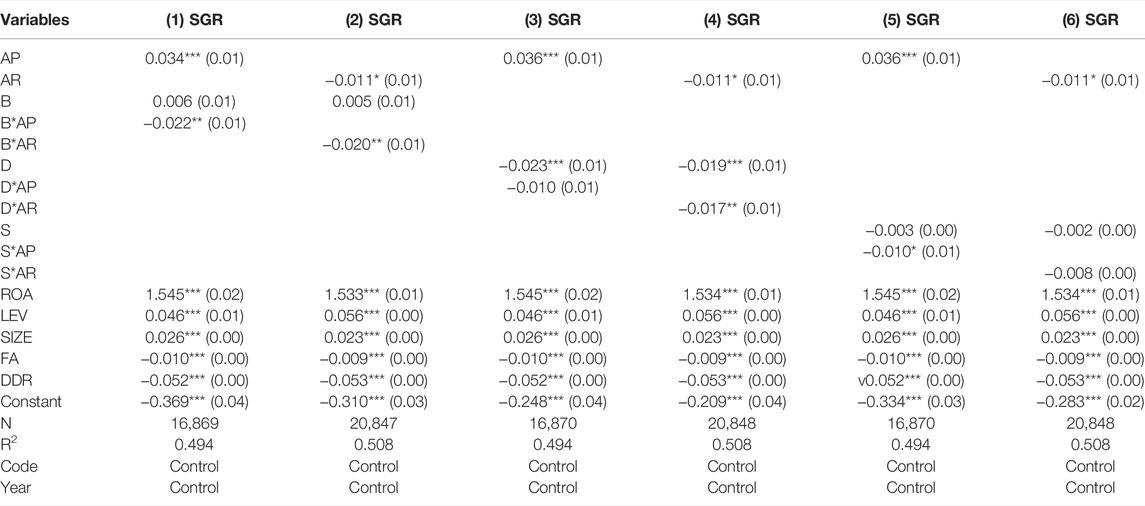

Digital finance has three first-level indicators: coverage_breadth (B), usage_depth (D) and digitization_level (S). To further analyze which dimension of digital finance plays a more obvious role, we carry out structural analysis of digital finance. It can be clearly seen from Table 13 that B and S weaken the promotion effect of trade credit access on sustainable growth, while D has no significant effect. In addition, by comparing the coefficients, it is found that B plays a stronger role. The larger the coverage breadth is, the more “long tail customers” are covered by financial services. The problem of financial exclusion is well solved, and the alternative financing role of informal finance is weakened. In columns (2) and (4) of Table 13, B and D significantly enhance the negative impact of the provision of trade credit on sustainable growth, and B plays a larger role. The above results can be further interpreted as that digital finance mainly affects the impact of trade credit on the sustainable growth of enterprises through the coverage of breadth channel.

TABLE 13. The structural impact of digital finance.

5 Conclusion and Policy Implications

Financing is the key factor restricting the development of enterprises. As an important part of supply chain finance, trade credit financing plays an important role in the business activities of enterprises. This paper took Chinese listed companies as research samples to explore the impact and mechanism of trade credit on sustainable growth, as well as the moderating effect of digital finance. The results showed that access to trade credit contributes to the sustainable growth of enterprises, and this relationship is more obvious in enterprises in areas with higher financial development level, enterprises in high-tech industry, state-owned enterprises and small enterprises. The provision of trade credit significantly inhibits the sustainable growth of enterprises, and this effect is more obvious in enterprises in areas lower financial development level, enterprises in non-high-tech industries, private enterprises and small enterprises. The results of influence mechanism showed that access to trade credit has an impact on sustainable growth through reducing agency cost. Providing trade credit will produce “compulsion effect,” which restricts the sustainable growth of enterprises. Further analysis showed that the development of digital finance has a moderating effect on the relationship between trade credit and enterprise sustainable growth. Specifically, the higher the development level of digital finance, the weaker the positive impact of trade credit access on sustainable growth of enterprises, and the stronger the negative impact of trade credit provision on sustainable growth. As can be seen from the above results, the effect of digital finance in serving the real economy has not been fully manifested.

The empirical results show that trade credit financing significantly promotes the sustainable growth of Chinese enterprises. Therefore, trade credit financing remains a viable alternative to corporate financing in the context of imperfect financial systems in China and other countries. In order to fully mobilize the impetus of sustainable growth of enterprises and maximize the role of trade credit financing, the government must strengthen the construction of credit, enhance the quality of contract, and realize the healthy development of trade credit. At the same time, we found that the service effect of digital finance on the sustainable growth of enterprises is not ideal. It can be seen that although China’s digital finance development level is at the forefront of the world, it does not play a greater role. Therefore, governments of all countries should strengthen the construction of digital financial infrastructure, enhance the coverage of network services, fully mobilize the ability of digital finance to serve the real economy, and jointly undertake the task of high-quality economic development together with trade credit.

Data Availability Statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Author Contributions

TL: Conceptualization, Supervision, Validation, Project administration, funding support and Writing‐review. WL: Formal analysis, Writing‐original draft, Writing‐review and editing. EE: Writing‐review and language polishing. XL: Logicalization, content modification, review and accountability. Conceptualization, formal analysis, writing‐revise, project administration. All authors contributed to manuscript revision and approved the submitted version.

Funding

This research was supported by the National Social Science Foundation of China (21BJL035).

Conflict of Interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s Note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

References

Abbas, A., Waseem, M., and Yang, M. (2020). An Ensemble Approach for Assessment of Energy Efficiency of Agriculture System in Pakistan. Energy Effic. 13(20), 683–696. doi:10.1007/s12053-020-09845-9

Abbas, A., Zhao, C., Ullah, W., Ahmad, R., Waseem, M., and Zhu, J. (2021). Towards Sustainable Farm Production System: A Case Study of Corn Farming. Sustainability 13 (16), 9243. doi:10.3390/SU13169243

Abbas, A., Zhao, C., Waseem, M., Ahmed khan, K., and Ahmad, R. (2022). Analysis of Energy Input-Output of Farms and Assessment of Greenhouse Gas Emissions: A Case Study of Cotton Growers. Front. Environ. Sci. 9, 826838. doi:10.3389/fenvs.2021.826838

Atanasova, C. V., and Wilson, N. (2003). Bank Borrowing Constraints and the Demand for Trade Credit: Evidence from Panel Data. Manage. Decis. Econ. 24 (6-7), 503–514. doi:10.1002/mde.1134

Chen, B., Lu, D., and Tian, L. (2016). Commercial Credit, Resource Reallocation and Credit Distortion: A Case Study of Unlisted Firms in China. Nankai Economic Studies 5, 3–18. doi:10.14116/j.nkes.2016.05.001

Chen, C., Cao, W., Cao, Y., and Shao, X. (2021). The Development of Digital Finance and the Transformation of Enterprises From Virtual to Real. Journal of Finance and Economics 47 (9), 78–92. doi:10.16538/j.cnki.jfe.20210606.101

Chen, S., and Ma, H. (2018). Loan Availability and Corporate Trade Credit: Evidence from Quasi-Natural Experiment of China's Interest Rate Liberalization. Manag. World 34 (11), 108–120+149. doi:10.19744/j.cnki.11-1235/f.2018.0009

Chen, X., and Ye, D. (2016). Research on Interest Rate Fluctuation of P2P Online Lending in China. Studies of International Finance 1, 83–96. doi:10.16475/j.cnki.1006-1029.2016.01.008

Chen, Y., and Tang, X. (2006). Enterprise Sustainable Growth Ability and its Generating Mechanism. Manag. World 12, 111–114+141. doi:10.19744/j.cnki.11-1235/f.2006.12.011

Du, Y., Zong, Z., and You, H. (2021). Trade Credit and Financialization of Real Enterprises. J. Bus. Econ. 6, 65–75. doi:10.14134/j.cnki.cn33-1336/f.2021.06.006

Elahi, E., Abid, M., Zhang, H., Cui, W., and Ul Hasson, S. (2018a). Domestic Water Buffaloes: Access to Surface Water, Disease Prevalence and Associated Economic Losses. Prev. Veterinary Med. 154 (1), 102–112. doi:10.1016/j.prevetmed.2018.03.021

Elahi, E., Abid, M., Zhang, L., ul Haq, S., and Sahito, J. G. M. (2018b). Agricultural Advisory and Financial Services; Farm Level Access, Outreach and Impact in a Mixed Cropping District of Punjab, Pakistan. Land Use Policy 71, 249–260. doi:10.1016/j.landusepol.2017.12.006

Elahi, E., Khalid, Z., Tauni, M. Z., Zhang, H., and Lirong, X. (2021). Extreme Weather Events Risk to Crop-Production and the Adaptation of Innovative Management Strategies to Mitigate the Risk: A Retrospective Survey of Rural Punjab, Pakistan. Technovation 4, 102255. doi:10.1016/j.technovation.2021.102255

Fabbri, D., and Menichini, A. M. C. (2010). Trade Credit, Collateral Liquidation, and Borrowing Constraints. J. Financial Econ. 96 (3), 413–432. doi:10.1016/j.jfineco.2010.02.010

Fisman, R., and Love, I. (2003). Trade Credit, Financial Intermediary Development, and Industry Growth. J. Finance 58 (1), 353–374. doi:10.1111/1540-6261.00527

Gao, Y. (2019). Research on the Upgrading of Enterprise Value Chain under the Mode of International Fragmentation. Beijing: People's Publishing House.

Ge, Y., and Qiu, J. (2007). Financial Development, Bank Discrimination and Trade Credit. J. Bank. Finance 31 (2), 513–530. doi:10.1016/j.jbankfin.2006.07.009

Guo, F., Wang, J., Wang, F., Kong, T., Zhang, X., and Cheng, Z. (2020). Measuring the Development of Digital Inclusive Finance in China: Index Compilation and Spatial Characteristics. China Econ. Q. 19 (4), 1401–1418. doi:10.13821/j.cnki.ceq.2020.03.12

Guo, Z., and Guo, B. (2002). Research on the Financial Problems of Corporate Growth-The Correlation Analysis of Stock Issuance, Corporate Debt and Corporate Growth. Account. Res. 7, 11–15+65. doi:10.3969/j.issn.1003-2886.2002.07.002

Huang, L., Ying, Q., Yang, S., and Hassan, H. (2019). Trade Credit Financing and Sustainable Growth of Firms: Empirical Evidence from China. Sustainability 11 (4), 1032. doi:10.3390/su11041032

Huang, Y., and Huang, Z. (2018). The Development of Digital Finance in China: Present and Future. China Econ. Q. 17 (04), 1489–1502. doi:10.13821/j.cnki.ceq.2018.03.09

Lee, C. H., and Rhee, B.-D. (2011). Trade Credit for Supply Chain Coordination. Eur. J. Operational Res. 214 (1), 136–146. doi:10.1016/j.ejor.2011.04.004

Liang, Y., Zhang, Z., and Lin, X. (2016). Research Progress of Supply Chain Finance Based on Trade Credit. J. Commer. Econ. 9, 144–148. doi:10.3969/j.issn.1002-5863.2016.09.055

Liu, 'e., and Guan, J. (2016). Two-way Governance of Trade Credit to Inefficient Investment of Enterprises. J. Manag. Sci. 29 (6), 131–144. doi:10.3969/j.issn.1672-0334.2016.06.011

Liu, D., Tang, B., and Fan, S. (2018). Measurement and Characteristic Analysis of Overinvestment Behavior of State-Owned Enterprises. Statistics Decis. 34 (16), 161–164. doi:10.13546/j.cnki.tjyjc.2018.16.040

Liu, P., Han, G., and Wang, X. (2021). Individual Entrepreneurship, Regional Entrepreneurship and Subjective Social Class. Nankai Econ. Stud. 6, 216–233. doi:10.14116/j.nkes.2021.06.013

Liu, T., Kou, F., Liu, X., and Elahi, E. (2022). Cluster Commercial Credit and Total Factor Productivity of the Manufacturing Sector. Sustainability 14 (6), 3601. doi:10.3390/SU14063601

Liu, T. (2021). Study on the Influence of Trade Credit on Technological Innovation of Enterprises. Beijing: China Social Sciences Press.

Li, X., and Song, M. (2021). Debt Payment Arrears of Zombie Firms and Total Factor Productivity of Private Firms. The Journal of World Economy 44 (11), 49, 74. doi:10.19985/j.cnki.cassjwe.2021.11.004

Lu, Z., and Yang, D. (2011). Business Credit: Alternative Financing or Buyer's Market? Manag. World 4, 6–14+45. doi:10.19744/j.cnki.11-1235/f.2011.04.003

Rathnayake, D. N., Wang, J., and Louembé, P. A. (2022). The Impact of Commercial Credit on Firm Innovation: Evidence from Chinese A-Share Listed Companies. Sustainability 14 (3), 1481. doi:10.3390/su14031481

Sheng, K. (2021). Urban Network under Production Fragmentation: Structure, Mechanisms and Effects. Beijing: Economy & Management Publishing House.

Shi, X., and Zhang, S. (2010). Constraints and Efficiency of Trade Credit Financing. Econ. Res. J. 45 (1), 102–114.

Sui, H. (2017). Study on the Influence of Foreign Direct Investment on the Quality of Economic Growth: Mechanism, Effect and Structural Evolution. Beijing: Post and Telecom Press.

Sun, L. Y. (2021). Research on Financing of Enterprises, Technological Innovation. Beijing: China Social Sciences Press.

Sun, P., Li, F., and Gu, L. (2014). An Analysis of Trade Credit as an Effective Financing Channel for Enterprises Based on Investment Perspective. China Econ. Q. 13 (4), 1637–1652. doi:10.13821/j.cnki.ceq.2014.04.017

Tang, C. S., Wu, J., and Yang, S. A. (2017). Sourcing from Suppliers with Financial Constraints and Performance Risk. SSRN J. 20 (1), 70–84. doi:10.2139/ssrn.2679618

Tang, D., and Zhuang, X. (2021). Manufacturing Financing Decisions: Bank, Trade Credit or Blockchain Supply Chain Finance. J. Northeast. Univ. Nat. Sci. 42 (8), 1202–1209. doi:10.12068/j.issn.1005-3026.2021.08.020

Tang, S., Wu, X., and Zhu, J. (2020). Digital Finance and Technological Innovation: Structural Characteristics, Mechanism Recognition and Effect Difference under Financial Regulation. Manag. World 36 (5), 52–66+9. doi:10.19744/j.cnki.11-1235/f.2020.0069

Thakor, A. V. (2020). Fintech and Banking: What Do We Know? J. Financial Intermediation 41 (C), 100833. doi:10.1016/j.jfi.2019.100833

Tian, S. (2019). The Impact of Exchange Rate Fluctuations on Chinese Enterprises' Export. Beijing: China Economic Publishing House.

Wang, Y., Xiuping, S., and Zhang, Q. (2021). Can Fintech Improve the Efficiency of Commercial Banks? -An Analysis Based on Big Data. Res. Int. Bus. Finance 55, 101338. doi:10.1016/j.ribaf.2020.101338

Wang, Z., Chen, Y., and Zhang, M. (2021). Traditional Financial Supply and Digital Finance Development: Supplement or Substitute? Bus. Manag. J. 43 (5), 5–23. doi:10.19616/j.cnki.bmj.2021.05.001

Wen, Z., and Ye, B. (2014). Mediating Effects Analysis: Method and Model Development. Advances in Psychological Science 22 (5), 731–745. doi:10.3724/SP.J.1042.2014.00731

Wu, S., Zhang, H., and Wei, T. (2021). Corporate Social Responsibility Disclosure, Media Reports, and Enterprise Innovation: Evidence from Chinese Listed Companies. Sustainability 13 (15), 8466–8483. doi:10.3390/SU13158466

Wu, X. (2015). Internet Finance: The Logic of Growth. Finance Trade Econ. 2, 5–15. doi:10.19795/j.cnki.cn11-1166/f.2015.02.001

Xiao, H., and Wang, F. (2004). Enterprise Growth, Enterprise Development and Enterprise Sustainable Growth. J. Zhongnan Univ. Econ. Law 4, 46–50+109. doi:10.3969/j.issn.1003-5230.2004.04.007

Xiao, Z., Lin, L., Chen, Z., and Xu, D. (2021). The Moderating Effect of Board Governance and Innovation Culture on Corporate Financialization and Innovation R&d Investment of Listed Companies. Nankai Econ. Stud. 1, 143–163. doi:10.14116/j.nkes.2021.01.009

Xu, G., and Zhu, W. (2017). Financialization, Market Competition and R&D Investment Crowding: Empirical Evidence from Non-financial Listed Companies. Stud. Sci. Sci. 35 (5), 709–719+728. doi:10.16192/j.cnki.1003-2053.2017.05.008

Yu, H. (2013). Relationship Network, Trade Credit Financing and Growth of Private Enterprises. Econ. Sci. 4, 116–128. doi:10.19523/j.jjkx.2013.04.010

Zhang, Y., and Hu, Z. (2020). A New Pattern of Regional Specialization in East Asia: Based on the Evolution of Comparative Advantages. Beijing: China Economic Publishing House.

Zhang, Y., Sun, L., and Wang, Z. (2020). Trade Credit Financing Can Improve the Capital Efficiency of Real Economy: Based on the Perspective of Economic Policy Uncertainty. Mod. Finance. Economics. J. Tianjin. Univ. Finance Econ. 40 (11), 53–67. doi:10.19559/j.cnki.12-1387.2020.11.004

Zhang, Z. (2019). Research on Rural Labor Transfer and Government Supporting Policies Based on Urban-Rural Overall Development. Beijing: People's Publishing House.

Zhao, Y., Peng, B., Elahi, E., and Wan, A. (2021). Does the Extended Producer Responsibility System Promote the Green Technological Innovation of Enterprises? an Empirical Study Based on the Difference-In-Differences Model. J. Clean. Prod. 319, 128631. doi:10.1016/j.jclepro.2021.128631

Zhou, J., Raza, A., and Sui, H. (2021). Infrastructure Investment and Economic Growth Quality: Empirical Analysis of China’s Regional Development. Appl. Econ. 53 (23), 2615–2630. doi:10.1080/00036846.2020.1863325

Keywords: supply chain finance, trade credit, sustainable growth, mandatory effect, digital finance

Citation: Liu T, Liu W, Elahi E and Liu X (2022) Supply Chain Finance and the Sustainable Growth of Chinese Firms: The Moderating Effect of Digital Finance. Front. Environ. Sci. 10:922182. doi: 10.3389/fenvs.2022.922182

Received: 17 April 2022; Accepted: 17 May 2022;

Published: 09 June 2022.

Edited by:

Muhlis Can, BETA Akademi-SSR Lab, TurkeyReviewed by:

Adnan Abbas, Nanjing University of Information Science and Technology, ChinaMuhammad Rehan, Université de Montréal, Canada

Copyright © 2022 Liu, Liu, Elahi and Liu. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Xiao Liu, bHhfbGl1eGlhb0AxMjYuY29t