Xiaoke Sun

Xiaoke Sun Cuiyan Zhang

Cuiyan Zhang

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 10 January 2023

Sec. Environmental Economics and Management

Volume 10 - 2022 | https://doi.org/10.3389/fenvs.2022.1104439

This article is part of the Research Topic China's Insurance and Green Economy Development in the Context of Sustainable Development View all 15 articles

By improving its total factor productivity, China may attain higher quality and more sustainable economic growth. As a key market-based incentive for environmental regulation, does environmental protection tax increase total factor productivity and provide a win-win situation for both economic and environmental performance? It is a debate-worthy topic. Based on data of Chinese listed companies, this paper uses the triple difference method to analyze China’s environmental protection tax reform as a natural experiment. The results show that the environmental protection tax can significantly boost the firm’s total factor productivity by encouraging technological innovation and enhancing resource allocation. Based on analysis of heterogeneity, it appears that state-owned enterprises, larger corporations, and regions with more strict environmental enforcement are more responsive to environmental protection tax policies. This report provides critical empirical evidence for upgrading China’s tax framework to protect the environment.

Since the reform and opening up, China’s economy has grown and developed rapidly, accomplishing incredible achievements. Due to the rising issues of climate change, environmental pollution, and resource shortages, China must urgently accelerate the transformation of its economic development mode, promote sustainable economic development, and build China into a country with a good environment (Liu et al., 2022). President Xi Jinping emphasized that we must plan for development from the perspective of harmony between humankind and nature. Early on in the history of environmental governance, the Chinese government primarily implemented command-and-control environmental laws and regulations and assumed complete responsibility for environmental protection (Karplus et al., 2021). In recent years, the Chinese government has paid significant attention to market-based environmental regulation in an attempt to strengthen the market’s natural incentive function. Taxation is a crucial method of macroeconomic management and control, as well as a critical instrument for social and economic development. The environmental protection tax system transfers the external cost of environmental pollution into the internal cost of the direct polluter (Rugman and Verbeke, 1998; Chiroleu-Assouline and Fodha, 2014). It is crucial to promote the green transformation of traditional businesses and to coordinate the upgrade of industrial structures. With the growing attention on environmental protection concerns in western industrialized nations since the 1970s, a rather mature environmental tax system based on the “polluter pays” principle has been established. However, China’s tax system for environmental protection is still in its infancy, as it was only officially established in 2018, attracting worldwide attention. Scholars and policymakers are concerned with whether the implementation of the environmental protection tax system contributes to achieving a win-win economic and environmental performance and sustainable development as China’s economy transitions from high-speed growth to a new stage of high-quality development.

Total factor productivity is the surplus remaining after deducting the growth of core factor input and its contribution to economic growth; it represents the level of production efficiency and the extent of technical advancement. With the transformation of China’s economic growth pattern, the enhancement of total factor productivity has become a requirement for the formulation and implementation of policy. The Communist Party of China at the 20th convention makes it abundantly clear that we must focus our efforts on improving total factor productivity, and promoting the effective improvement of quality and reasonable growth of the economy. After China’s economy enters a new stage of development, improving the total factor productivity is a critical concern that must be resolved without delay. Studies have explored the path of improving the total factor productivity of enterprises from government macro-control policies (Bartelsman et al., 2013; Alfaro and Chari, 2014), financial friction (Ziebarth, 2013; Midrigan and Xu, 2014; Lin et al., 2022), market information (Bennett et al., 2020), information and communication technology (Shao and Lin, 2016; Xie et al., 2020), and exchange rate fluctuations (Cao et al., 2022) and other aspects. Other studies have also explored the impact of environmental regulation on the total factor productivity of enterprises (Albrizio et al., 2017; Shen et al., 2019; Peng et al., 2021), however, most of them focus on command-and-control environmental policies and emission trading systems, and there is limited research on China’s environmental protection tax. This paper utilizes the “natural experiment” of China’s environmental protection tax to precisely identify the effect of environmental protection tax on the total factor productivity of enterprises, which has important theoretical and practical implications for evaluating the economic effects of green tax policies.

China’s tax system for environmental protection dates back to the late 1970s and early 1980s. The Environmental Protection Law of the People’s Republic of China (for Trial Implementation), promulgated in September 1979, for the first time introduced pollution charges, which were implemented on a trial basis in some locations. The State Council promulgated the Regulations on the Administration of the Collection and Use of Pollution Charge Fees in March 2003, which completely implements the pollution charge system and serves as a significant instrument for government environmental regulation. Although the pollution charge system can internalize the externalities of environmental pollution, problems such as low pollution charge standards, excessive administrative intervention, insufficient law enforcement, and a lack of standardization make it difficult to adapt to China’s current practical environmental protection and economic development requirements. The Environmental Protection Tax Law of the People’s Republic of China was adopted on 25 December 2016, and went into effect on 1 January 2018. This is the first tax law in China that expressly represents the “green tax system” and strives to protect the environment. It is essential for companies to establish internal pollution control and emission reduction restraining mechanisms and for China to develop an environment-friendly society. The reform of China’s environmental protection tax has resulted in the transition from a pollution charge system to an environmental protection tax with the following characteristics: First, the tax burden is transferred. The Environmental Protection Tax Law is consistent with the pollution charge system in terms of objects, collection items, calculation methods, and standards to ensure a smooth and stable transition from the pollution charge system to the environmental protection tax system and to prevent a significant increase of cost in enterprises. Second, the legislative level has also been raised. The environmental protection tax system relies on state mandatory legislation to guarantee implementation, and the legal effect is stronger, which is conducive to enhancing the environmental protection consciousness of businesses as well as their responsibility for pollution control and emission reduction. The collection of sewage fees is an administrative supervisory behavior that is solely supported by administrative norms and lacks implementation and supervision. Third, the tax burden is flexible. According to the Environmental Protection Tax Law, minimum requirements are established for major pollutants, and local governments may increase the standard by up to 10 times the minimum criteria; hence, regions have the ability to choose the collection standard for significant pollutants. After the implementation of the Environmental Protection Tax Law in 2018, some regions have kept the original pollution fee collection standard, while others have chosen a higher collection requirement. This is similar to a “natural experiment” with obvious exogenous characteristics in the area of economics, offering a unique chance to evaluate the influence of China’s environmental protection tax on the total factor productivity of firms.

Based on Chinese listed companies’ data, this paper uses the implementation of China’s environmental protection tax as a natural experiment and uses the triple difference method to examine the impact of environmental protection tax reform on the total factor productivity of enterprises by comparing before and after the implementation of the environmental protection tax, the regions with the increase of environmental protection tax rate and the regions with the unchanged environmental protection tax rate, and the polluting industries relative to clean industries. Furthermore, a number of heterogeneity and robustness tests are conducted based on the type of property rights, the size of the firm, and regional law enforcement. The total factor productivity of enterprises in polluting industries and in regions with increased environmental protection tax rates is much higher than in regions with unchanged environmental protection tax rates and in clean industries.

Compared to prior studies, the potential contributions of this work can be described as flows. First, the perspective of the study is innovative. Environmental protection tax is the most prominent symbol of China’s building of a green tax system, and it is an environmental economic policy instrument that may have a significant influence on the behavior of micro-enterprises. Studies on China’s environmental protection tax concentrate primarily on enterprise performance (Jin et al., 2020), innovation (Liu and Xiao, 2022), and environmental protection investment (Tian et al., 2022), whereas there are few studies that examine corporate production efficiency and technical progress. This paper evaluates the policy effect of environmental protection tax from the perspective of enterprise total factor productivity, which is an important contribution to the research literature on the effect of China’s environmental protection “fee-to-tax” policy, and deepens the understanding of the impact of market-based economic incentive environmental regulation on enterprise total factor productivity, and serves as an essential reference for the promotion of environmental protection. Secondly, the research methodology is scientific. This paper uses the quasi-natural experiment of China’s environmental protection tax system and the triple difference method, which not only avoids the endogeneity problems caused by only relying on environmental regulations measurement indicators such as environmental pollution expenditures, sewage charges, pollution emission reductions in the past (Cai et al., 2016), but also eliminates the interference of other policies during the pilot period and the interference of time-varying regional characteristics (Olden and Møen, 2022). It improves the accuracy with which policy impacts are evaluated. Thirdly, this paper provides micro evidence that environmental protection taxes influence the total factor productivity of businesses. This paper analyzes the influence mechanism of environmental protection tax on enterprises’ total factor productivity from the perspectives of capital allocation efficiency and technological innovation and investigates the strategic behavior of enterprises to enhance production efficiency under the pressure of environmental protection tax with stricter enforcement. It provides empirical data to demonstrate how government departments increase the total factor productivity of enterprises by utilizing market-based economic and environmental policy instruments to force and stimulate corporate subject responsibility awareness. In addition, it provides excellent references for the future improvement and optimization of the environmental protection tax system. It has significant practical implications for constructing a green development system and fostering high-quality economic growth.

The other sections of this paper are organized as follows. Section 2 presents the literature review and research hypothesis. Section 3 explains the research design and data. Section 4 presents the results of the empirical study. Section 5 presents a further discussion, including mechanism analysis and heterogeneity analysis. Section 6 concludes the study as well as gives some policy recommendations.

The influence of environmental regulation on the total factor productivity of enterprises has become a major area of research in economics, however, the conclusions are inconsistent. From the perspective of neoclassical economics, the regulatory pressure brought by environmental policies will increase the cost of pollution and tax burdens on enterprises, resulting in the crowding out of resources from “production” purposes toward “pollution control” purposes, thereby impeding the development and negatively affecting the production efficiency of enterprises (Jorgenson and Wilcoxen, 1990; Shadbegian and Gray, 2005; Lanoie et al., 2011; Tombe and Winter 2015). He et al. (2020) discovered that China’s water quality monitoring system immediate upstream polluters risk a total factor productivity decrease of more than 24%. Cai and Ye (2020) found that China’s new environmental protection law inhibits enterprises’ TFP with the impacts lasting for 2 years. Porter as well as other economists are opposed to this. The Porter Hypothesis (Porter, 1991; Porter and Van der Linde, 1995) asserted that strict and appropriate environmental regulation, particularly market-based tools, can enable businesses to positively adapt through innovation incentives, efficiency improvement, and internal redistribution, resulting in increased productivity. There are additional researches that support this conclusion (Ai et al., 2020). Both market-based and non-market-based policies promote productivity development, while green taxes have the greatest influence (De Santis et al., 2021). Peng et al. (2021) argued that China’s SO2 Emissions Trading Pilot provides favorable benefits to productivity. According to additional research, the influence of environmental legislation on the total factor productivity of businesses is ambiguous. Albrizio et al. (2017) discovered that environmental regulation had a short-term influence on productivity development at the industry level in the most technologically advanced nations, but had no effect on the typical company. Zhao et al. (2018) discovered a substantial inverted U-shaped correlation between environmental regulatory intensity and the total factor production, and Qiu et al. (2021) also discovered that the similar link between environmental rules and green total factor production.

In conclusion, the existing research on the impact of environmental regulation on total factor productivity has yielded a number of significant findings. However, no consistent finding has been established due to differences in environmental regulations among nations, samples, and study techniques. Even less research has been conducted on the impact of a market-based economic incentive environmental policy instrument at the micro level. In view of this, and based on the 2018 implementation of China’s environmental protection tax, this study investigates the impact and mechanism of environmental protection tax on the total factor productivity of firms, therefore extending previous research.

As an important market-based economic incentive environmental regulatory instrument, the environmental protection tax solves the market failure problem by internalizing the environmental externality costs of enterprises. Although the environmental protection tax raises the financial burden on businesses, it may distort the allocation of components, resulting in a reduction in earnings, preventing businesses from making optimal production decisions, and thereby decreasing their production efficiency and competitiveness (Cainelli et al., 2015; Tombe and Winter 2015). However, this viewpoint is “static.” It holds that in implementing environmental protection policy, enterprises will just passively accept environmental protection tax costs, disregarding the environmental protection tax’s compelled effect on pollution control and technological upgrading, as well as its positive impacts. From the perspective of long-term dynamic development, faced with the pressure of rising environmental compliance costs, enterprises can flexibly choose technological innovation and optimize resource allocation to improve production efficiency, thus further reducing production costs, and ultimately mitigating or offsetting the negative impact of environmental protection tax, thereby achieving environmental and economic dividends (Rubashkina et al., 2015). As the different features of technological innovation and resource allocation, the effect of environmental tax policy may be classified into long-term and short-term effects, but the overall effect will be positive. Therefore, this paper proposes the core hypothesis 1 to be tested:

Hypothesis 1:. The implementation of an environmental protection tax can improve the total factor productivity of enterprises.Innovation is a high-risk, high-investment, and high-turnover activity for enterprises (Bansal and Hunter, 2003), which is difficult to initiate. Technology’s public good characteristics are determined by its non-competitive nature, and thus lacks innovation drive and requires external incentives. Before introducing the environmental protection tax, the pollution charge system was also a market-based economic incentive for environmental regulation. However, it is not incorporated into the tax law management system. Due to the absence of enforcement and insufficient supervision, the effect of the implementation is poor. Currently, businesses seeking maximum profit are often more willing to pay environmental punishment costs than to invest in greater R&D and innovation expenditures, and their desire to engage in technological innovation activities is low. After the implementation of the environmental protection tax policy, environmental regulation becomes more stringent and the corporate tax burden increases. To maximize economic benefits, businesses will be more motivated to use technological innovation initiatives that minimize pollution and manufacturing costs (Hattori, 2017; Wang et al., 2021). Moreover, the implementation of the environmental protection tax system demonstrates the Chinese government’s determination and policy development direction to protect the environment, therefore increasing public awareness of environmental protection, and this social monitoring will enhance corporate innovation (Liu and Xiao, 2022). Furthermore, corporate technology innovation may be classified as invention technology innovation and non-inventive technology innovation. The latter includes utility patent and design innovation. Due to the high development difficulty and high resource investment associated with invention technology innovation, companies are more likely to embrace non-inventive technology innovations with low technical requirements and less development difficulty, also known as strategic innovation. Therefore, this paper suggests the core hypothesis 2 to be tested:

Hypothesis 2:. The environmental protection tax system encourages enterprises to increase their total factor productivity through technological innovation; however, the environmental protection tax has a more significant incentive effect on utility model and design technology innovation than on invention technology innovation.Besides the development of technology, the increase in production efficiency is also evident in the improvement of resource allocation efficiency within companies. The regulatory pressure and cost pressure imposed by the environmental protection tax policy encourage companies to decrease resource input in departments with higher pollution and lower production efficiency, while increasing investment in departments with larger cleanliness and higher production efficiency, thereby reducing the environmental protection tax burden. By optimizing the allocation of production factors, enterprises may help low-polluting and high-efficiency sectors gain additional production resources, as well as increase factor utilization and production efficiency (Wang et al., 2016; Ren et al., 2019; Yu et al., 2019). Therefore, this paper proposes the core hypothesis 3 to be tested:

Hypothesis 3:. The environmental protection tax system encourages enterprises to improve total factor productivity by optimizing resource allocation.To obtain credible causal inference, this article investigates the influence of environmental protection tax reform on the total factor productivity of businesses primarily through the triple difference method. Specifically, first of all, this paper compares the impact before and after the environmental protection tax reform using the time dimension as the primary distinction. Secondly, this paper takes the regional dimension as the second difference to compare the effect of the difference in environmental regulation intensity between regions with higher environmental tax rates and regions with unchanged environmental tax rates. This is because regions with higher taxation standards for taxable pollutants have greater environmental pressures and impacts on enterprises in these regions than regions with unchanged taxation standards for taxable pollutants. Thirdly, because environmental regulations primarily affect industries that directly release air pollutants, water pollutants, solid waste, and other taxable pollutants into the environment, clean industries that emit less or virtually no taxable pollutants will be affected very little (Hering and Poncet, 2014), the pollution level of the industry is used as the third distinction. By comparing the changes in total factor productivity of enterprises in polluting industries and clean industries before and after the environmental protection tax reform, in areas where the environmental protection tax rate was increased and unchanged, and by excluding as much as possible the influences of factors that do not change over time, are difficult to observe, and are outside the reform policy, this paper establishes the following benchmark model (Deschenes et al., 2017; Liu and Xiao, 2022):

In the model,

This sample comprises Chinese A-share companies listed on the Shanghai and Shenzhen stock exchanges between 2015 and 2021. Excluded from the sample are financial firms, companies with continuous losses, companies with asset-liability ratios larger than 1, and companies with significant missing values. Financial data comes from the Wind and CSMAR databases. The basic patent data comes from the State Intellectual Property Office of China. To reduce the impact of outliers on the estimated findings, all continuous variables are truncated at the 1% and 99% levels.

The explained variable in this paper is the total factor productivity of listed companies. Currently, semi-parametric approaches, such as the Olley-Pakes (OP) method, the Levinsohn-Petrin (LP) method, and the Ackerberg-Caves-Frazer (ACF) method, are used to estimate total factor productivity at the micro-enterprise level. The OP method uses the investment as the proxy variable, whereas the LP method utilizes intermediate inputs. Due to the lack of investment data for some companies, this article employs the LP approach to calculate the total factor productivity of the companies as the explained variable in order to minimize sample size loss. This paper uses the total factor productivity calculated by the ACF method as a substitute explained variable to ensure the robustness of the benchmark regression results, as the ACF method can reduce the interference of endogenous problems in the production function on measurement results to some extent.

To provide objective estimates of policy impacts, this article controls variables that may influence enterprises’ total factor productivity over time, such as debt levels, profitability, liquidity, and corporate governance (Ren et al., 2019). First of all, under the premise of an acceptable cost of debt, modest debt will enable businesses to raise funds, compensate for the lack of long-term development funds, and influence company choices and production efficiency. This paper uses the asset-liability ratio (Lev) to measure the debt levels of enterprises. Secondly, the more profitable an enterprise is, the more money it can generate and the more efficient it can be. This paper measures profitability based on return on equity (Roe). Furthermore, liquidity and governance structure are significant elements that influence the production and management efficiency of companies. This paper utilizes the ratio of current assets to total assets and the ownership ratio of the largest shareholder. The variables’ descriptive statistics are displayed in Table 1. The minimum total factor productivity of enterprises is 9.461 and the maximum is 12.85, demonstrating that there are significant variations in production efficiency among enterprises.

TABLE 1. Summary statistics of main variables.

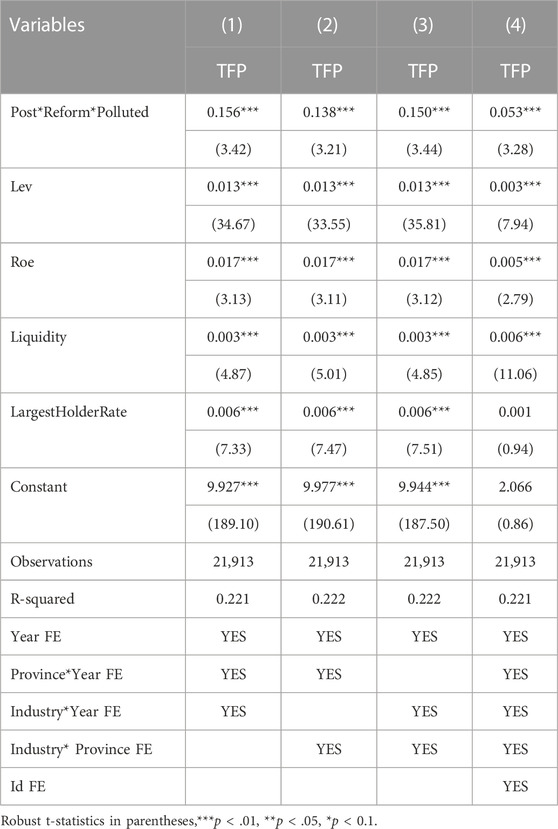

Based on the benchmark model, this paper controls various combinations of the time-fixed effect, region-fixed effect, industry-fixed effect and control variables in columns (1) to (3), as well as the individual fixed effect in column (4). The regression results of columns (1)–(3) in Table 2 reveal that the coefficients of the core explanatory variables

TABLE 2. The impact of environmental protection tax policy on total factor productivity.

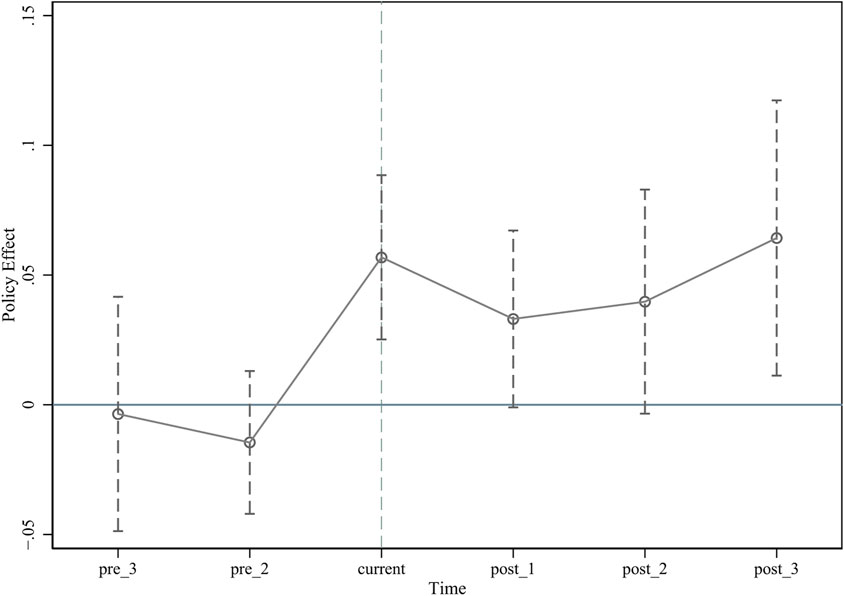

A parallel trend in the total factor productivity of enterprises in the treatment group and the control group prior to the adoption of the policy is required for an appropriate evaluation of policy impacts (Angrist and Pischke, 2009). In other words, when the experimental group is not exposed to policy shocks, the dependent variable should display the same temporal trend as the control group. In this paper, the event study method (Jacobson et al., 1993) is utilized to develop the following regression equation.

FIGURE 1. Parallel trend test.

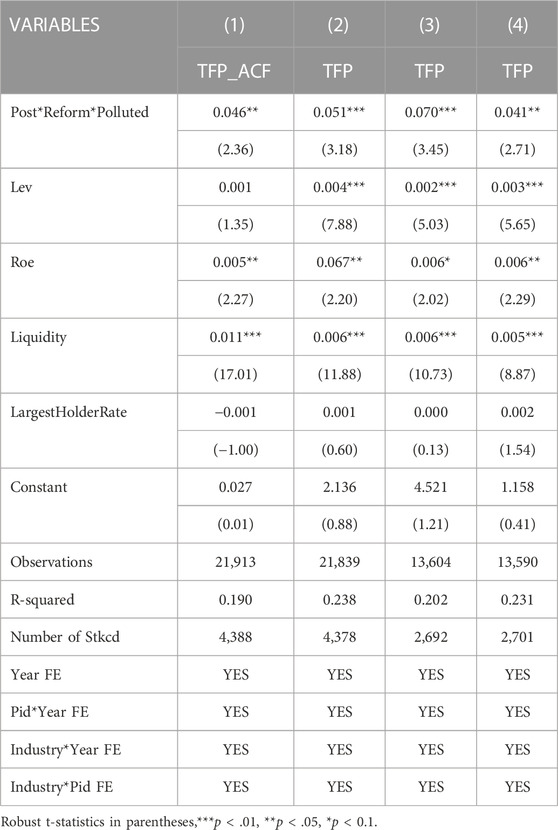

Due to the LP method used to estimate the total factor productivity of the company, there may be certain specific errors. This paper utilizes the ACF approach to recalculate the enterprise’s total factor productivity as the explained variable for robustness testing. Column (1) in Table 3 demonstrates that the environmental protection tax policy may greatly improve the total factor productivity of the enterprise, regardless of the method used to estimate it for regression, confirming the reliability of the baseline regression.

TABLE 3. Robustness test.

To reduce the disparities in individual characteristics between the treatment group and the control group, this research employs the propensity score matching approach to locate the most appropriate matching samples for the treatment group within the control group. This paper employs the year-by-year kernel matching approach (Heyman et al., 2007) and re-estimates using the matched data. The outcomes are displayed in column (2) of Table 3. The core explanatory factors are still significant. The environmental protection tax can greatly increase the total factor productivity of the company, and the reliability of the benchmark regression results has strengthened.

In order to further strengthen the robustness of the conclusion, this paper excludes the influence of other policies that might affect the total factor productivity of firms and interfere with the results. In 2007, the Chinese government formally introduced the pilot project for paying for the use and trading of SO2 emission rights, and 11 pilot provinces, including Jiangsu, Tianjin, Shanxi, Chongqing, Hubei, Shaanxi, Inner Mongolia, Hunan, and Henan, were subsequently authorized. In 2011, China’s National Development and Reform Commission issued the Notice on Conducting Pilot Programs for Carbon Emissions Trading, mandating that carbon emissions trading pilot projects be implemented in seven provinces and cities, including Beijing, Shanghai, Hubei, Chongqing, Guangdong, Tianjin, and Shenzhen. As environmental regulations, these two policies might have an effect on the total factor productivity of enterprises. Therefore, this research re-estimates the outcomes as presented in columns (3) and (4) of Table 3 by removing the data for these provinces from the sample, respectively. The continued significance of the results supports the validity of the paper’s conclusions.

The preceding research findings indicate that implementing an environmental protection tax policy can increase the total factor productivity of the company. Then, how does the tax on environmental protection impact the total factor productivity of enterprises? This paper adopts two methods of technological innovation and resource allocation to test the transmission mechanism, based on the preceding theoretical analysis.

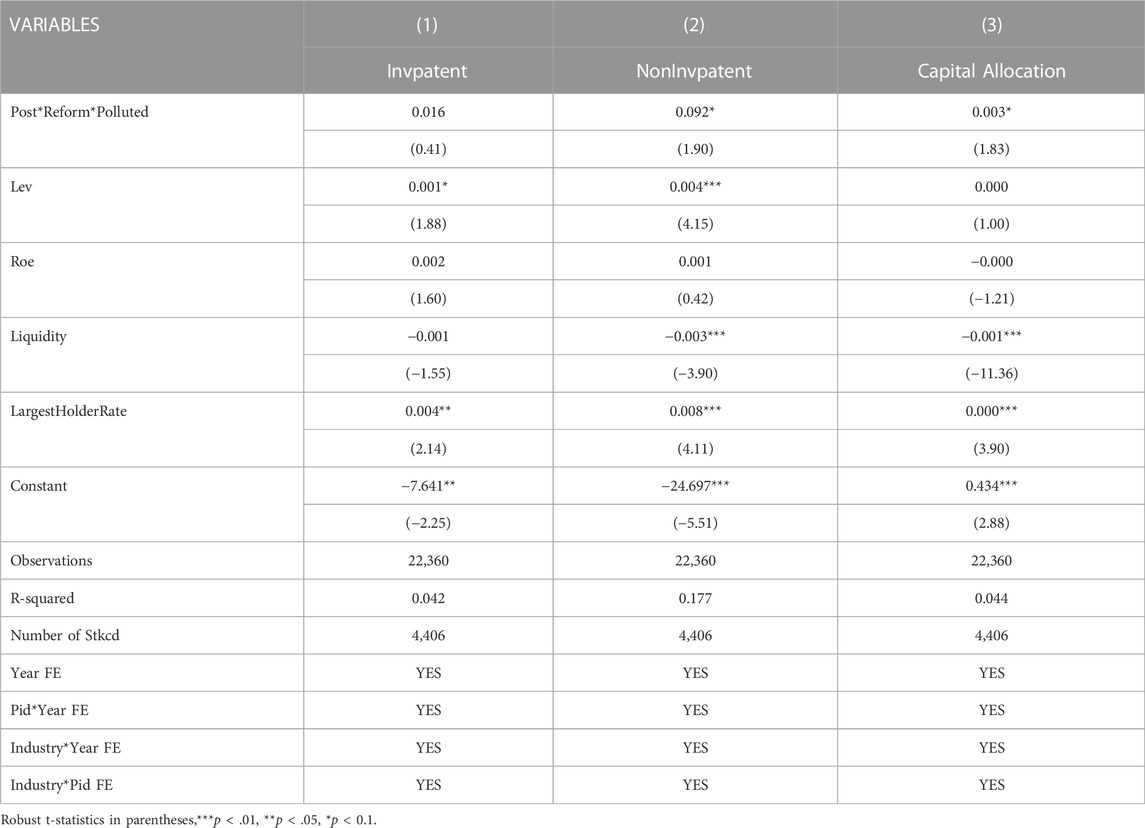

In order to examine whether the environmental protection tax improves the total factor productivity of enterprises through technological innovation, this paper uses patent authorization as a proxy variable for technological innovation in enterprises for empirical research (Ren et al., 2019). Indicating an enterprise’s ability to innovate independently, a patent is an indication of the firm’s investment in scientific research. This paper also conducts regressions on invention patents and non-invention patents (utility model patents and design patents) in order to evaluate specific types of technological innovation. Table 4 shows the findings in columns (1) and (2). It can be seen that the adoption of the environmental protection tax policy has a greater incentive effect on utility model and design innovation technology, indicating that the transition from the pollution charge fee system to the environmental tax system encourages polluters to boost their efforts in technological innovation. Nevertheless, considering the high difficulty of innovation and the long investment period of the invention of technology, the implementation of a pollution charge fee to tax has a greater impact on encouraging technological innovation in utility models and designs. Hypothesis two is confirmed.

TABLE 4. Mechanism analysis.

This research utilizes capital allocation efficiency as a proxy variable to evaluate the efficacy of enterprise resource allocation in order to determine whether the environmental protection tax can increase the total factor productivity of firms by improving the efficiency of resource allocation (Ren et al., 2019). Capital allocation efficiency = (cash paid for purchase and construction of fixed assets, intangible assets, and other long-term assets minus cash recovered through sale of fixed assets, intangible assets, and other long-term assets)/total assets at the end of the period. The outcomes are displayed in column (3) of Table 4. The core explanatory variable’s regression coefficient is significantly positive, suggesting that environmental protection tax policy can increase total factor productivity by optimizing the allocation of enterprise factors and enhancing resource consumption efficiency.

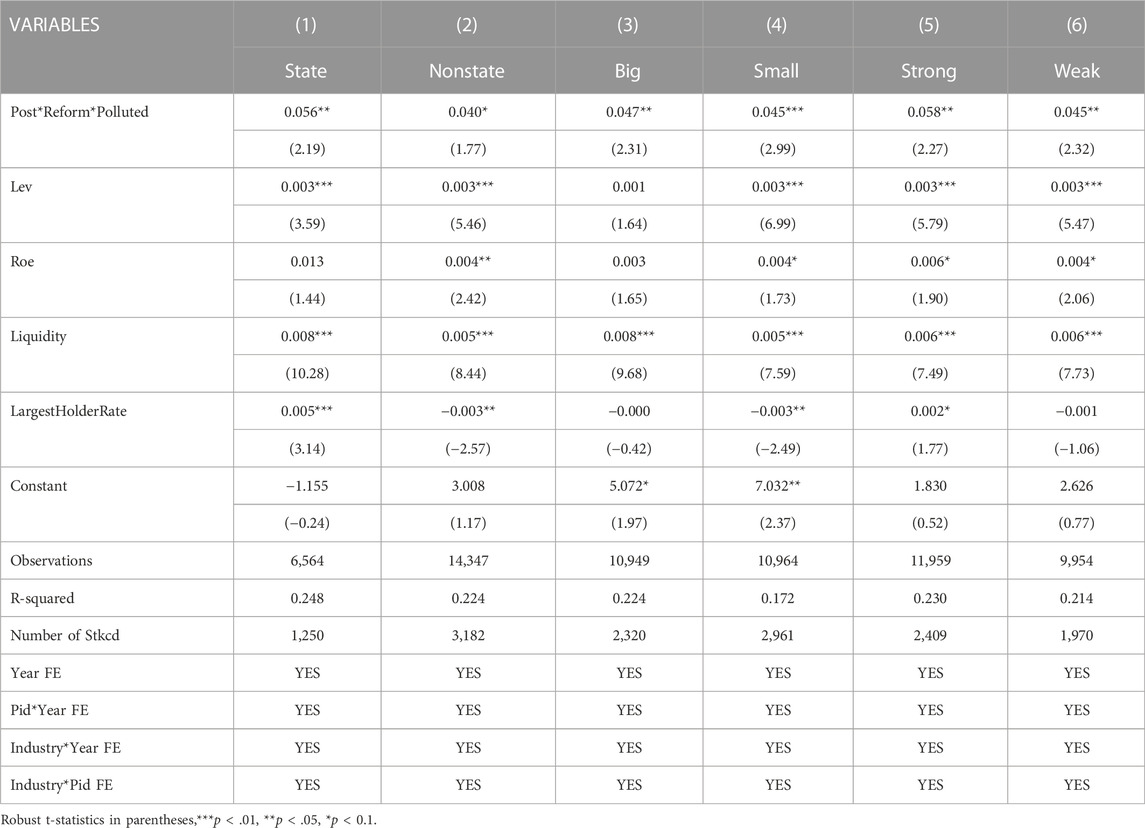

Despite the fact that the environmental protection tax policy can increase the total factor productivity of enterprises, the promotion effect of environmental protection tax on the total factor productivity of enterprises may vary depending on regional characteristics and enterprise attributes. This research examines the variety of the influence of the environmental protection tax system on the total factor productivity of enterprises based on their internal and external features. The internal features of companies include corporate ownership and enterprise scale, whereas the external characteristics are mostly evaluated based on environmental law enforcement effectiveness. This will help the government in adapting policy implementation methods to the circumstances and in maximizing the policy impact of the environmental protection tax system.

In this study, the total sample is separated into state-owned and non-state-owned enterprises. The regression results for the two subsamples are shown in Table 5 columns (1) and (2). Overall, the treatment effect is robust in both subsamples. However, the estimated coefficient is smaller for non-state-owned enterprises than for state-owned enterprises. This suggests that state-owned enterprises under the environmental protection tax system are less likely to improve total factor productivity than state-owned enterprises. State-owned companies in China have generally consistent funding sources and certain resource advantages. They are able to invest adequate people, material, and financial resources in technological research and development, and have a high possibility of technological innovation success. Moreover, state-owned enterprises are subject to tougher government and public supervision, have a higher sense of social responsibility, and are more driven to adjust resource allocation within the enterprise, hence enhancing the utilization efficiency of production factors. Research and development capabilities of non-state-owned companies may be constrained by financial limitations. Additionally, the comparatively low awareness of social responsibility dampens the enthusiasm of non-state-owned enterprises for technological advancement. Consequently, environmental protection tax policy has a greater influence on the total factor productivity of state-owned enterprises.

TABLE 5. Heterogeneity analysis.

This paper uses the median asset size as the quantile point and splits the entire sample into two subgroups: large-scale and small-scale businesses. In columns (3) and (4) of Table 5, the regression results for the two subsamples are displayed. In general, the effect of environmental protection tax on the total factor productivity of enterprises is stable across the two subsamples, and the coefficients are not significantly different, indicating that enterprises of various sizes are affected similarly by environmental protection tax policy. Nevertheless, it has a higher effect on the total factor productivity of big enterprises. This could be due to the fact that larger companies have scale advantages and superior technical capabilities, which are beneficial for innovative technology research and development. Due to the fact that smaller companies have inadequate technological capabilities and have greater resource constraints, it is challenging for them to engage in technological innovation.

The implementation of the environmental protection tax, despite being authoritative and mandatory, non-etheless requires a robust legal framework. Environmental law enforcement represents the degree to which local governments are concerned about environmental issues. In general, a higher level of environmental law enforcement can make environmental policies more fully implemented and improve their performance. In order to investigate the heterogeneity of the impact of the environmental protection tax system on the total factor productivity of enterprises under different environmental law enforcement efforts, in this paper, the ratio of the frequency of words related to “environmental protection” in provincial government work reports to the number of words in the full text of the reports is taken as the proxy variable of environmental governance. On the one hand, it can reflect the government’s efforts in environmental governance, and on the other hand, it can alleviate endogenous problems. Local government work reports are generally released at the beginning of the year, while economic activity runs throughout the year. The samples are divided based on the number of environmental governance word frequency in the year preceding the implementation of the environmental protection tax policy (2017). Regions with lower environmental law enforcement intensity are those where the number of environmental governance word frequency is less than the median value, and provinces with higher environmental law enforcement intensity are those where the number of environmental governance word frequency is equal to or greater than the median value. The regression findings for the two subsamples are displayed in columns (5) and (6) of Table 5. In regions where environmental law enforcement is more stringent, the environmental protection tax system has a stronger impact on the total factor productivity of enterprises. This could be due to the fact that if companies are located in regions with weaker law enforcement, they are less likely to be punished for emissions violations. As a result, the incentive for innovation research and development and resource allocation upgrades is diminished, and the policy’s impact is limited.

China’s modernizing progress is contingent on achieving harmony between humanity and nature. Using China’s environmental protection tax policy reform as a natural experiment, this paper empirically investigates the influence of environmental protection tax on the total factor productivity of firms using the triple difference approach. The study concludes that the implementation of an environmental protection tax substantially increases the total factor productivity of listed companies. Further investigation reveals that total factor productivity can be enhanced primarily through two routes: increasing the level of technical innovation and optimizing resource allocation. Analysis of heterogeneity suggests that state-owned enterprises, large businesses, and regions with stronger enforcement of environmental laws are more responsive to environmental protection tax policies.

This paper concludes the following policy implications based on these findings. First, the environmental protection tax reform has a positive policy effect, demonstrating that China’s use of market mechanisms to regulate environmental pollution within the context of high-quality economic development is beneficial. We should continue to optimize and improve the tax system for environmental protection and create more fair taxation scope and tax rate criteria. Simultaneously, the enforcement of environmental taxes should be strengthened, the relationship between the government and the market should be properly managed, and the intervention of local governments should be reduced. Second, when implementing and regulating environmental economic tax laws, the varied characteristics of enterprises and areas must also be taken into account. Emphasis must be placed on increasing the supervision of high-pollution and high-emission industries, enhancing policy guidance, and helping small and medium-sized businesses. Lastly, companies should be encouraged to take the initiative to implement strategic reform through technological innovation and factor structure adjustment in order to rationally address environmental protection tax policies.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

XS designed the research and wrote the manuscript. CZ completed the empirical test and analysis. All authors discussed the results and contributed to the final manuscript. All authors have read and agreed to the published version of the manuscript.

This study is supported by the Ministry of Education of China (Grant No. 22YJC840025) and Guangdong Basic and Applied Basic Research Foundation (Grant No. 2022A1515111007).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenvs.2022.1104439/full#supplementary-material

Ai, H., Hu, S., Li, K., and Shao, S. (2020). Environmental regulation, total factor productivity, and enterprise duration: Evidence from China. Bus. Strategy Environ. 29 (6), 2284–2296. doi:10.1002/bse.2502

Albrizio, S., Kozluk, T., and Zipperer, V. (2017). Environmental policies and productivity growth: Evidence across industries and firms. J. Environ. Econ. Manag. 81, 209–226. doi:10.1016/j.jeem.2016.06.002

Alfaro, L., and Chari, A. (2014). Deregulation, misallocation, and size: Evidence from India. J. Law Econ. 57 (4), 897–936. doi:10.1086/680930

Angrist, J. D., and Pischke, J. S. (2009). Mostly harmless econometrics: An empiricist's companion. New Jersey, United States: Princeton university press.

Bansal, P., and Hunter, T. (2003). Strategic explanations for the early adoption of ISO 14001. J. Bus. ethics 46 (3), 289–299. doi:10.1023/a:1025536731830

Bartelsman, E., Haltiwanger, J., and Scarpetta, S. (2013). Cross-country differences in productivity: The role of allocation and selection. Am. Econ. Rev. 103 (1), 305–334. doi:10.1257/aer.103.1.305

Bennett, B., Stulz, R., and Wang, Z. (2020). Does the stock market make firms more productive? J. Financial Econ. 136 (2), 281–306. doi:10.1016/j.jfineco.2019.09.006

Cai, W., and Ye, P. (2020). How does environmental regulation influence enterprises’ total factor productivity? A quasi-natural experiment based on China’s new environmental protection law. J. Clean. Prod. 276, 124105. doi:10.1016/j.jclepro.2020.124105

Cai, X., Lu, Y., Wu, M., and Yu, L. (2016). Does environmental regulation drive away inbound foreign direct investment? Evidence from a quasi-natural experiment in China. J. Dev. Econ. 123, 73–85. doi:10.1016/j.jdeveco.2016.08.003

Cainelli, G., De Marchi, V., and Grandinetti, R. (2015). Does the development of environmental innovation require different resources? Evidence from Spanish manufacturing firms. J. Clean. Prod. 94, 211–220. doi:10.1016/j.jclepro.2015.02.008

Cao, W., Feng, Y., Yu, C., and Wan, D. (2022). RMB exchange rate fluctuations, enterprise innovation and total factor productivity of manufacturing Industry. Econ. Res. J. 57 (03), 65–82.

Chiroleu-Assouline, M., and Fodha, M. (2014). From regressive pollution taxes to progressive environmental tax reforms. Eur. Econ. Rev. 69, 126–142. doi:10.1016/j.euroecorev.2013.12.006

De Santis, R., Esposito, P., and Lasinio, C. J. (2021). Environmental regulation and productivity growth: Main policy challenges. Int. Econ. 165, 264–277. doi:10.1016/j.inteco.2021.01.002

Deschenes, O., Greenstone, M., and Shapiro, J. S. (2017). Defensive investments and the demand for air quality: Evidence from the NOx budget program. Am. Econ. Rev. 107 (10), 2958–2989. doi:10.1257/aer.20131002

Hattori, K. (2017). Optimal combination of innovation and environmental policies under technology licensing. Econ. Model. 64, 601–609. doi:10.1016/j.econmod.2017.04.024

He, G., Wang, S., and Zhang, B. (2020). Watering down environmental regulation in China. Q. J. Econ. 135 (4), 2135–2185. doi:10.1093/qje/qjaa024

Hering, L., and Poncet, S. (2014). Environmental policy and exports: Evidence from Chinese cities. J. Environ. Econ. Manag. 68 (2), 296–318. doi:10.1016/j.jeem.2014.06.005

Heyman, F., Sjöholm, F., and Tingvall, P. G. (2007). Is there really a foreign ownership wage premium? Evidence from matched employer-employee data. J. Int. Econ. 73 (2), 355–376. doi:10.1016/j.jinteco.2007.04.003

Jacobson, L. S., LaLonde, R. J., and Sullivan, D. G. (1993). Earnings losses of displaced workers. Am. Econ. Rev. 83, 685–709.

Jin, Y., Gu, J., and Zeng, H. (2020). Does "Environmental protection fees replaced with environmental protection taxes" affect corporate performance? Account. Res. 41 (05), 117–133.

Jorgenson, D. W., and Wilcoxen, P. J. (1990). Environmental regulation and US economic growth. Rand J. Econ. 21, 314–340. doi:10.2307/2555426

Karplus, V. J., Zhang, J., and Zhao, J. (2021). Navigating and evaluating the labyrinth of environmental regulation in China. Rev. Environ. Econ. Policy 15 (2), 300–322. doi:10.1086/715582

Lanoie, P., Laurent-Lucchetti, J., Johnstone, N., and Ambec, S. (2011). Environmental policy, innovation and performance: New insights on the porter hypothesis. J. Econ. Manag. Strategy 20 (3), 803–842. doi:10.1111/j.1530-9134.2011.00301.x

Lin, D., Cui, X., and Gong, L. (2022). Financial friction heterogeneity, resources misallocation and TFP loss. Econ. Res. J. 57 (01), 89–106.

Liu, D., Xie, Y., Hafeez, M., and Usman, A. (2022). The trade-off between economic performance and environmental quality: Does financial inclusion matter for emerging asian economies? Environ. Sci. Pollut. Res. 29 (20), 29746–29755. doi:10.1007/s11356-021-17755-1

Liu, J., and Xiao, Y. (2022). China's environmental protection tax and green innovation: Incentive effect or crowding-out effect? Econ. Res. J. 57 (01), 72–88.

Midrigan, V., and Xu, D. Y. (2014). Finance and misallocation: Evidence from plant-level data. Am. Econ. Rev. 104 (2), 422–458. doi:10.1257/aer.104.2.422

Olden, A., and Møen, J. (2022). The triple difference estimator. Econ. J. 25 (3), 531–553. doi:10.1093/ectj/utac010

Peng, J., Xie, R., Ma, C., and Fu, Y. (2021). Market-based environmental regulation and total factor productivity: Evidence from Chinese enterprises. Econ. Model. 95, 394–407. doi:10.1016/j.econmod.2020.03.006

Porter, M. E., and Van der Linde, C. (1995). Toward a new conception of the environment-competitiveness relationship. J. Econ. Perspect. 9 (4), 97–118. doi:10.1257/jep.9.4.97

Qiu, S., Wang, Z., and Geng, S. (2021). How do environmental regulation and foreign investment behavior affect green productivity growth in the industrial sector? An empirical test based on Chinese provincial panel data. J. Environ. Manag. 287, 112282. doi:10.1016/j.jenvman.2021.112282

Ren, S., Zheng, J., Liu, D., and Chen, X. (2019). Does emissions trading system improve firm’s total factor productivity-Evidence from Chinese listed companies. China Ind. Econ. 35 (05), 5–23.

Rubashkina, Y., Galeotti, M., and Verdolini, E. (2015). Environmental regulation and competitiveness: Empirical evidence on the Porter Hypothesis from European manufacturing sectors. Energy Policy 83, 288–300. doi:10.1016/j.enpol.2015.02.014

Rugman, A. M., and Verbeke, A. (1998). Corporate strategies and environmental regulations: An organizing framework. Strategic Manag. J. 19 (4), 363–375. doi:10.1002/(sici)1097-0266(199804)19:4<363:aid-smj974>3.0.co;2-h

Shadbegian, R. J., and Gray, W. B. (2005). Pollution abatement expenditures and plant-level productivity: A production function approach. Ecol. Econ. 54 (2-3), 196–208. doi:10.1016/j.ecolecon.2004.12.029

Shao, B. B., and Lin, W. T. (2016). Assessing output performance of information technology service industries: Productivity, innovation and catch-up. Int. J. Prod. Econ. 172, 43–53. doi:10.1016/j.ijpe.2015.10.026

Shen, N., Liao, H., Deng, R., and Wang, Q. (2019). Different types of environmental regulations and the heterogeneous influence on the environmental total factor productivity: Empirical analysis of China's industry. J. Clean. Prod. 211, 171–184. doi:10.1016/j.jclepro.2018.11.170

Tian, L., Guan, X., Li, Z., and Li, X. (2022). Reform of environmental protection fee-to-tax and enterprise environmental protection investment: A quasi-natural experiment based on the implementation of the environmental protection tax law. J. Finance Econ. 48 (09), 32–46+62.

Tombe, T., and Winter, J. (2015). Environmental policy and misallocation: The productivity effect of intensity standards. J. Environ. Econ. Manag. 72, 137–163. doi:10.1016/j.jeem.2015.06.002

Wang, F., He, J., and Sun, W. (2021). Mandatory environmental regulation, ISO 14001 certification, and green innovation: A quasi-natural experiment based on Chinese ambient air quality standards. China Soft Sci. 36 (09), 105–118.

Wang, S., Wang, S., and Teng, Z. (2016). Total factor productivity growth in the service industry in China under environmental constraints. J. Finance Econ. 42 (5), 123–134.

Xie, L., Chen, J., and Wang, S. (2020). ICT Investment, internet penetration and total factor productivity. Stat. Res. 37 (09), 56–67. doi:10.19343/j.cnki.11-1302/c.2020.09.006

Yu, Y., Liu, D., and Gong, Y. (2019). Target of local economic growth and total factor productivity. Manag. World 35 (7), 26–42+202.

Zhao, X., Liu, C., and Yang, M. (2018). The effects of environmental regulation on China's total factor productivity: An empirical study of carbon-intensive industries. J. Clean. Prod. 179, 325–334. doi:10.1016/j.jclepro.2018.01.100

Keywords: environmental protection tax, total factor productivity, porter hypothesis, environmental regulation, the triple difference estimator

Citation: Sun X and Zhang C (2023) Environmental protection tax and total factor productivity—Evidence from Chinese listed companies. Front. Environ. Sci. 10:1104439. doi: 10.3389/fenvs.2022.1104439

Received: 21 November 2022; Accepted: 23 December 2022;

Published: 10 January 2023.

Edited by:

Yuantao Xie, University of International Business and Economics, ChinaReviewed by:

Yu Mao, Tsinghua University, ChinaCopyright © 2023 Sun and Zhang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Cuiyan Zhang, emN5MTk5MnlhbkAxNjMuY29t

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.