Dengyun Niu

Dengyun Niu Zhihua Wang

Zhihua Wang Songling Yang2

Songling Yang2- 1Business School, Shanxi Datong University, Datong, China

- 2College of Economics and Management, Beijing University of Technology, Beijing, China

Environmental regulation and economic development are consistent in the long run, but there are certain contradictions in the short term. Examining the characteristics of available environmental regulation tools and using them in a way that will align the interests of local governments and enterprises can improve environmental regulation and enhance green transformation and development. This study considers two general types of environmental regulation tools: negative punishment types and positive incentive types. Applying an intermediary effect model and the two-stage least squares method, a sample of Chinese A-share listed companies from 2007 to 2019 is used to test the impact of these different types of environmental regulation tools on the financial investment levels of entity enterprises. The mechanism through which these macro-environmental regulation tools function and the micro-enterprise heterogeneity factors that influence their impact are systematically studied. The results show that negative punishment type environmental regulation tools have a positive impact on the financial investment levels of entity enterprises, while positive incentive type environmental regulation tools inhibit financial investment levels. This impact is formed through managerial incentive mechanisms referred to as “whipping the fast ox” and “heavy rewards and light punishments.” Factors such as financing constraints, relocation costs, pollution levels, and enterprise scale have heterogeneous effects on these paths. Policy suggestions are offered based on the findings. This study makes a significant contribution to the literature by clarifying the channel through which environmental regulation influences micro-enterprise decision-making. It provides a theoretical basis and policy reference for local government officials as they address the conflict between economic growth and environmental protection in the short term. Moreover, the results offer long-term development decision-making ideas for shareholders and managers in the process of green transformation and upgrading of enterprises.

1 Introduction

Sustainable development is currently a key global issue, and, for many countries, the contradiction between rapid economic growth and environmental carrying capacity is becoming increasingly deeper. Environmental degradation has a serious impact on sustainable development (Arslan et al., 2022; Wen et al., 2021). However, although they are the main producers of pollutants, enterprises usually lack the motivation to perform environmental governance activities (Arouri et al., 2012; Borghesi et al., 2015). Consequently, governments are compelled to encourage enterprises to participate in environmental governance by establishing emission indicators and providing cash and tax incentives to reduce environmental pollution at its source. Accordingly, governments worldwide are exploring environmental regulation systems that consider both environmental protection and economic development and issuing a series of policies related to sustainable development (Kirikkaleli and Adebayo, 2021; Mughal et al., 2022).

Most existing studies divide environmental regulation tools into three categories: command-type, public-participation-type, and market-incentive-type. Among these, command-type environmental regulation tools usually involve the government formulating a series of emission caps and emission reduction standards and directly intervening in enterprise environmental strategies through non-market measures such as administrative orders or coercion. Public-participation-type environmental regulation tools are used to supervise enterprise pollution control processes through informal systems, relying on public opinion, mass petitions, and other forms. The market-incentive-type environmental regulation tool is a method, in which the government actively guides enterprises to adjust production decisions in market-oriented ways, such as through tax cuts, incentives, and emissions trading (Xie et al., 2017). Various environmental regulation tools have certain effects. For example, Chen et al. (2020) believe that market-incentive-type environmental regulation tools have stronger environmental governance effects. Dong et al. (2022) believe that environmental taxes can reduce pollutant emissions. Langpap and Shimshack (2010) argue that public-participation-type regulation tools play a significant role in pollution control.

There are certain differences in how environmental regulation tools impact enterprise operation and transformation development, and academia has not yet formed a consensus. One view holds that there is a pressure mechanism; that is, environmental regulations exert certain pressure on enterprises and add environmental governance costs, leading to cost increases (Zhang et al., 2018), R&D stagnation (Zhou et al., 2020), and reduced investment (Silvia et al., 2017). To overcome the stress stage, enterprises usually seek financing, production reduction, and other ways to increase income and reduce expenditure (Petroni et al., 2019) or migrate to areas with lower environmental regulation standards to form a pollution refuge (Mani and Wheeler, 1998). Another view proposes a compensation mechanism; that is, enterprises under environmental regulation may increase technological innovation and improve production efficiency to offset the increase in environmental protection expenditure costs (Qiaoxin, 2021).

Although previous studies have investigated the relationship between environmental regulation tools and business decision-making, research gaps remain. Existing studies have ignored the applicability of different types of environmental regulation tools, resulting in two opposite conclusions about the most effective regulatory mechanisms; some support the use of “pressure mechanisms,” while others favor “compensation mechanisms.” Additionally, past studies have focused on how environmental regulation impacts an enterprise’s choice of investment direction but have ignored the impact logic between the two. Enterprise investment decisions can be divided into financial investments and industrial operations. The mutual transformation of the two is essentially a choice of resource allocation and a change in efficiency (Li and Wenfeng, 2021). For example, Haijing et al. (2021) argue that environmental regulation places operational pressure on enterprises, making their profit-seeking motives more obvious and prompting them to improve their financial investment level. Maomao and Yanyan (2021) reached the opposite conclusion. They argue that the new Environmental Protection Law urges enterprises to transform and upgrade as soon as possible, while the improvement in the R&D level restrains the financial investment level. However, neither of these studies discuss the paths through which the laws influence enterprise behaviors.

This study’s objective is to resolve these key issues and fill the gap in existing research. First, it examines the impact of two different environmental regulation tools— “negative punishment” and “positive incentives”—on enterprise financial investments and discusses how various corporate characteristics, such as financing constraints, relocation costs, pollution levels, and firm size, affect these paths. Second, this study discusses the role of managerial incentive mechanisms in the path between environmental regulation and enterprise investment preferences and provides corresponding theoretical support. In view of this, this study takes Chinese A-share entity listed companies from 2007 to 2019 as its sample to conduct an empirical study that applies a fixed-effects panel regression model, the two-stage least squares method, and an intermediary effect model.

The results show that negative punishment environmental regulation tools have a positive impact on the financial investment levels of entity enterprises, while positive incentive environmental regulation tools inhibit financial investment. Managerial incentive mechanisms of “whipping the fast ox1” and “heavy rewards and light punishments” are the direct paths through which negative punishment environmental regulation tools act on the financial investment levels of entity enterprises. In contrast, positive incentive environmental regulation tools mainly act by alleviating cost pressures, obtaining tax cuts, and financial incentives. In addition, the sensitivity of different types of enterprises to environmental regulation tools differs and has a heterogeneous impact on the logical chain.

Our study contributes to both theory and literature, and the results have managerial implications. First, the study provides theoretical support for the two opposite conclusions of “pressure mechanisms” and “compensation mechanisms” produced by previous studies. From the perspective of enterprise financial investment, this study breaks down the relevant research on how environmental regulation impacts enterprise investment and discusses the effect of different corporate characteristics and applicability of environmental regulation tools. Second, it supplements the evidence of managerial incentive paths in terms of environmental regulation tool effectiveness, enriches the research on the transmission path between macro-environmental policy and micro-enterprise investment decision-making, and provides a certain theoretical basis and literature support for the relationship between environmental regulation and enterprise investment. Third, the results provide practical suggestions for local governments as they choose environmental protection policies and for enterprises in their decision-making processes, offering ideas conducive to the long-term development of shareholders and managers in the process of green transformation and development.

This study’s originality lies in its focuses on corporate behavior from the perspective of environmental regulation tool effectiveness, finding differences in the effectiveness of environmental regulation given various corporate characteristics. Second, it is one of a few studies to find the existence of a managerial incentive path between environmental regulation and enterprise behavior, showing that a managerial incentive mechanism plays an important role in the relationship between the two.

2 Hypotheses

Many scholars have studied the relationship between environmental protection and economic development and believe that the two are internally consistent in the long run. However, in the short run, implementing inappropriate environmental regulation tools may negatively impact local economic growth and business decision-making. In the long run, implementing environmental policies can improve the level and potential of economic growth through health effects and R&D effects (Raffin, 2014; Dao and Edenhofer, 2018). However, during the tenure of local government officials, environmental constraints have been incorporated into the promotion competition system, forcing officials to choose between short-term and conflicting goals. Consequently, some mandatory and executive-ordered policies have been implemented that impact the development of local economies and adjustments of industrial structures (Xueqing and Yong, 2021; Zhang, 2021). The environmental governance process also reflects local governments’ tendency to free ride (Cai et al., 2016), the transfer of pollution shelters by enterprises (Becker and Henderson, 2000), and a reduction in the quality of green innovation (Feng et al., 2021).

As an important external governance factor, macro environmental regulation tools will directly affect enterprise performance levels in the short term. On the one hand, environmental regulation will increase enterprise cost burdens, and strict and tough environmental policies will lead to a decline in enterprise performance. On the other hand, under the continuous action of an environmental indicator system, managers will comprehensively improve production methods by improving production processes and increasing investment in green innovation to meet the increasingly stringent requirements of environmental regulation (Cui et al., 2018). However, innovation input may still create performance pressure in the short term. Therefore, whether it is cost burden or innovation investment, it will weaken enterprise profitability in the physical field, place performance pressure on managers, and promote implementation of short-term financial investment decisions.

This study divides environmental regulation tools into negative punishment type and positive incentive type. Among these, the command-type and public-participation-type environmental regulation tools involve negative punishment, requiring enterprises to meet the government or public’s emission requirements in a short time frame, mainly through fines, public opinion pressure, and other means. These negative punishment methods expand enterprise operating and cost pressures. Motivated to protect their private benefits, managers will seek to alleviate these performance pressures through short, quick financial investments. As positive incentive methods, market-incentive-type environmental regulation tools can alleviate the cost pressures enterprises face in the process of meeting environmental protection requirements in terms of funds and curb the reduction in the industrial rate of return. When an enterprise makes a good environmental protection decision, it may also get to take advantage of tax cuts and capital rewards, which have a positive impact on enterprise performance and thus help alleviate managers’ tendency toward short-term financial investments.

To summarize, command-type and public-participation-type environmental regulation tools reduce the industrial rate of return, which will lead managers to enhance their preference for financial investment in response to short-term pressures and improve the financial investment level of enterprises. Market-incentive-type environmental regulation tools can reduce the cost pressure of enterprises in the process of environmental governance, such as through tax cuts and incentives, and alleviate managers’ short-term financial investment tendencies. Accordingly, the following hypotheses are proposed.

Hypothesis 1. There is a positive correlation between negative punishment environmental regulation tools and the financial investment levels of entity enterprises. That is, the stronger the command-type and public-participation-type environmental regulation tools, the higher the financial investment levels of entity enterprises.

Hypothesis 2. There is a negative correlation between positive incentive environmental regulation tools and the financial investment levels of entity enterprises. That is, the stronger the market-incentive-type environmental regulation tools, the lower the financial investment levels of entity enterprises.

3 Materials and methods

3.1 Research sample and data selection

As a traditional industrial country, China has paid a high price for its rapid economic development in terms of resource use and environmental impact. In recent years, China has made major changes in regards to environmental protection and carbon emissions. This context is ideal for reflecting the relationship between the effectiveness of environmental regulation policies and enterprise investment. Therefore, Chinese A-share listed companies are used to test the study’s hypotheses.

This study’s sample is limited to entity enterprises. The annual report data of A-share non-financial and non-real estate listed companies in China’s Shanghai and Shenzhen stock markets from 2007 to 2019 are used for this study’s analyses. The first reason for this choice is that long-term panel data of micro samples can contain more information and reflect actual situations accurately. Second, 2007 is chosen as the starting point because the measurement of financial assets for enterprises was changed in China’s accounting standards from the cost model to the fair value model in 2007. Third, although listed company data in 2020 is relatively complete, there is a serious lack of environmental-related data. To ensure preciseness, this study sets 2019 as the end time of the sample. Since quarterly and semi-annual reports of Chinese listed companies are not required to be externally audited to ensure data authenticity, only data disclosed in annual reports are used for the analyses.

According to the research needs, firms with special treatment, such as ST, *ST, and PT2, and those with missing data are excluded from the sample. A total of 23,268 valid observations were obtained. The data required for the study were obtained from the CSMAR database and the listed companies’ annual reports. To control for the impact of extreme values on the model, all continuous variables were winsorized at the 1% and 99% levels.

3.2 Model construction and variable definitions

To test H1 and H2 and examine the impacts of different types of environmental regulation tools on the financial investment levels of entity enterprises, the following fixed-effects regression model (Eq. 1) was constructed.

3.2.1 Explained variable

In model (Eq. 1), Fini,t is a proxy variable for the financial investment level of entity enterprises, i indicates the ith listed company, and t represents time. The difficulty measuring the financial investment level of entity enterprises lies in identifying and separating the assets invested in the financial field that are different from operational investments. Based on the Penman-Nissim analysis framework and referring to Demir (2009) and Songling et al. (2021), the financial investment levels of entity enterprises are characterized by the proportion of the sum of financial assets to total assets (Fini,t). The larger the value, the stronger the managers’ investment preference for financial assets and the higher the financial investment level of the entity enterprise. Since 2017, the Ministry of Finance has issued or revised a series of accounting standards for enterprises to regulate and update the presentation and disclosure of financial instruments, financial assets, and other related content. In view of this, the calculation formula for Fini,t is adjusted around 2017. The calculation used from 2007 to 2017 is shown in Eq. 2, while that used for 2018 and 2019 is shown in Eq. 3.

Financial Assets A includes trading financial assets, held-to-maturity investments, available-for-sale financial assets, investment real estate, other financial assets, and derivative financial assets. Financial Assets B includes trading financial assets, held-to-maturity investments, investment real estate, other financial assets, derivative financial assets, debt investments, other debt investments, other equity instrument investments, and other non-current financial assets.

Specifically, the accounting standards before 2017 classified financial assets into four categories: financial assets measured at fair value with changes included in current profits and losses, held-to-maturity investments, loans and receivables, and available-for-sale financial assets. Because loans and receivables are closely related to the production and operation activities of entity enterprises, they are an important part of supporting and maintaining the main business. Because it is difficult to separate financial assets, based on the conservatism principle, loans and receivables are excluded from the financial assets measurement in Eq. 2. Second, according to the revision of the accounting standards in 2017, Eq. 3 divides the available-for-sale financial assets into four categories—debt investments, other debt investments, other equity instrument investments, and other non-current financial assets—and brings them into the category of financial assets. In addition, because investment real estate, trust products, and other emerging financial assets and derivative financial assets also have financial asset attributes, which can reflect the financial investment preferences of entity enterprises, Eqs 2, 3 include investment real estate, various emerging financial assets (listed in other current assets), and derivative financial assets as financial assets.

3.2.2 Explanatory variables

In model (Eq. 1), there are three types of environmental regulation tools (GZp,t): command-type environmental regulation tools (GZ-Com), public-participation-type environmental regulation tools (GZ-Pub), and market-incentive-type environmental regulation tools (GZ-Inc). p indicates the region (matched using the place of the enterprise’s registration), and t indicates time.

Among the types of environmental regulation tools, command-type environmental regulation tools draw on the methods used by Fuxin et al. (2013) and Xiaosong et al. (2020). The measurement is calculated using indicators such as industrial wastewater discharge, industrial SO2 discharge, and industrial soot discharge. The specific calculation steps are as follows. In the first step, the data of these three pollutants are standardized. The weight of each pollutant is calculated in the second step, and the third step computes the comprehensive index (GZ-Com). The index is an inverse indicator. This means that the smaller the value, the lower the regional pollution emissions, and the stricter the mandatory control measures, that is, the higher the degree of command-type environmental regulation. The data required for this index are primarily obtained from the China Statistical Yearbook, China Environmental Statistical Yearbook, and China Urban Statistical Yearbook.

Existing studies have generally used the number of environmental letters and visits in each province and city to measure the degree of public-participation-type environmental regulation (Wugan and Qingqing, 2019). However, the statistics for this indicator, which were previously found in the China Environmental Yearbook and other channels, ended in 2015. Since the National People’s Congress embodies the national nature of the people’s democratic dictatorship, the number of recommendations by the National People’s Congress is used to measure the degree of public-participation-type environmental regulation tools (GZ-Pub). The smaller the value of this measure, the lower the degree of public-participation-type environmental regulation. The required data are mainly retrieved from the China Environmental Yearbook.

Common measures of market-incentive-type environmental regulation tools include emission fees, tradable emission permits, and environmental taxes (Ramanathan et al., 2017; Qin et al., 2018). Referring to Hong (2008), the ratio of investment completed in regional industrial pollution control to gross regional product is used as an indicator to measure the degree of market-incentive-type environmental regulation (GZ-Inc). The smaller the index value, the lower the degree of market-incentive-type environmental regulation. The data required for this measurement are primarily obtained from the China Environmental Statistics Yearbook and the China Statistical Yearbook.

3.2.3 Control variables

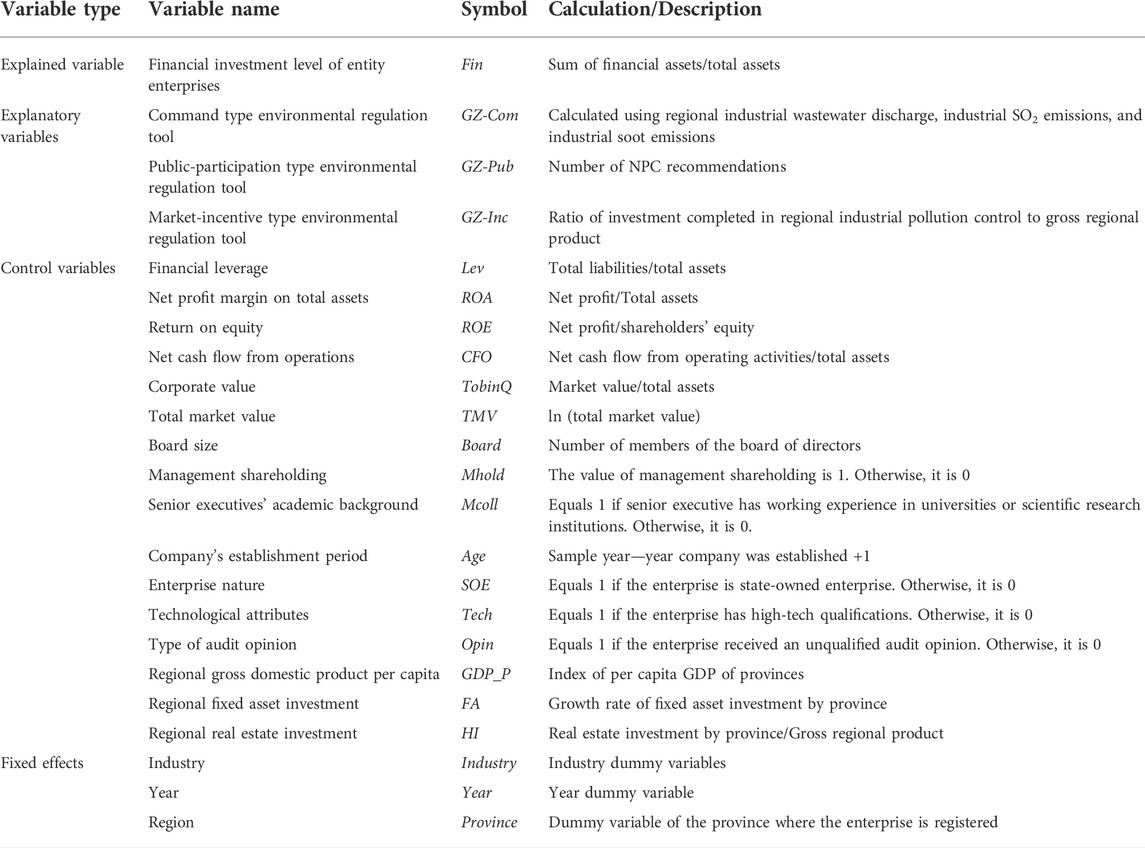

Relevant control variables are included in the model to avoid interference by other factors that may affect financial investments of entity enterprises. In model (Eq. 1), Xi,t represents the micro-level control variables constructed by enterprise-year, and Yp,t represents the macro-level control variables constructed by region-year. Micro-level control variables (Xi,t) from three aspects are used as controls: financial status, corporate governance characteristics, and enterprise characteristics. First, Duchin (2010) and Da Luz et al. (2015) confirmed that, based on the precautionary saving and speculative motivations, higher financial leverage and a lower return on assets may reduce enterprise cash holding and industrial investment levels, thus improving the financial investment level of entity enterprises. Based on this, controls for certain financial status variables are included, including financial leverage (Lev), net profit margin to total assets (ROA), return on equity (ROE), net cash flow from operations (CFO), corporate value (TobinQ), and total market value (TMV). Second, according to Malmendier and Tate (2015) and Songling et al. (2021), a higher level of corporate governance reduces managers’ independence and irrational decision-making, such as overconfidence, and restricts their short-term financial investment behavior. Based on this, controls for corporate governance characteristics are added, including board size (Board), management shareholding (Mhold), and senior executives’ academic background (MColl). Third, Feng et al. (2022) found that there are great differences in the financial investment levels of state-owned and non-state-owned enterprises, as well as enterprises with different technological attributes. Therefore, enterprise characteristics are controlled, including the company’s establishment period (Age), enterprise nature (SOE), technological attributes (Tech), and type of audit opinion (Opin). The selection of macro-level control variables (Yp,t) draws on Akdogu and MacKay (2008), Wang et al. (2014), and Kim and Kung (2017), adding industrial factors and macroeconomic factors that may affect enterprise investment behavior, including regional gross domestic product per capita (GDP_P), regional fixed asset investment (FA), and regional real estate investment (HI). In addition, to ensure the stability and accuracy of the test results, industry, time, and region fixed effects are also controlled. See Table 1 for detailed variable definitions.

TABLE 1. Variable definitions.

3.3 Descriptive statistical analysis

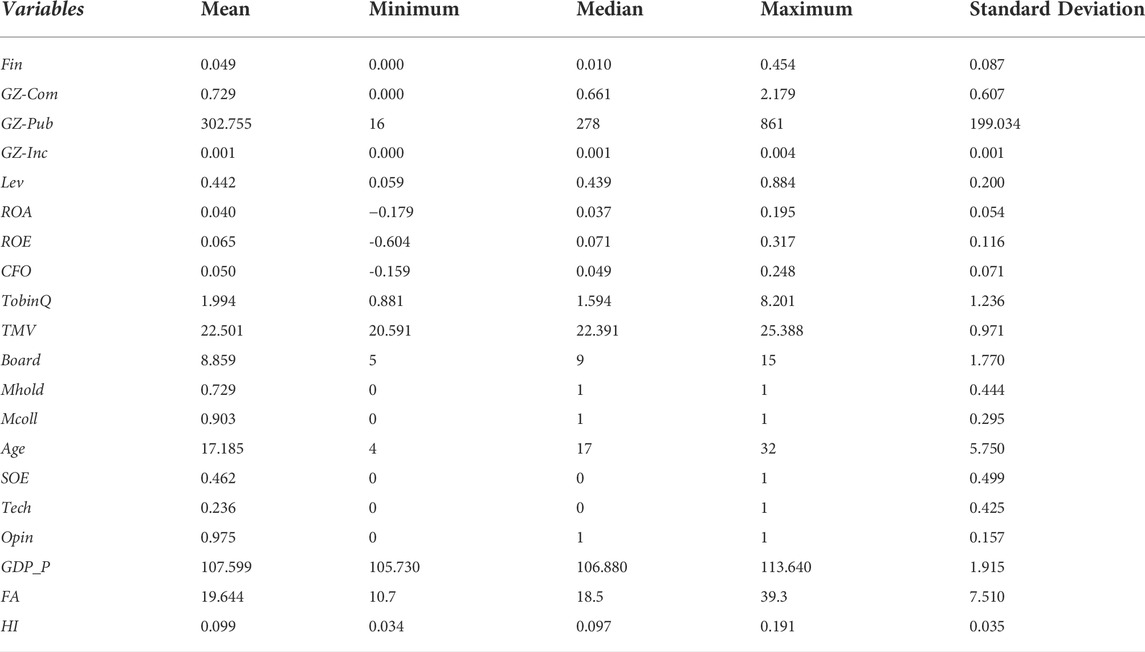

Table 2 presents the descriptive statistical results of the main variables. The average financial investment level (Fin) of entity enterprises is 0.049, but the median is only 0.010. This indicates that the financial investment level of some entity enterprises is relatively high and even exceeds their business investment level to become the main source of profit. The mean and standard deviation of command-type environmental regulation tools (GZ-Com) is 0.729 and 0.607, indicating that the sample distribution in each region and each year is relatively balanced. The average value of public-participation-type environmental regulation tools (GZ-Pub) is 302.755. However, there is a large gap between the minimum (16) and maximum values (861), indicating that there are great differences in the degree of public participation in different regions. The mean value of market-incentive-type environmental regulation tools (GZ-Inc) is 0.001, indicating that completed investment in industrial pollution control accounts for 0.1% of local GDP. In addition, the mean values of financial leverage (Lev), net profit margin to total assets (ROA), return on equity (ROE), and net operating cash flow (CFO) of the sample enterprises are 0.442, 0.040, 0.065, and 0.050, respectively. The financial indicators indicate that the sample companies are generally in good financial condition. The average size of the board of directors (Board) is 8.859, the proportion of companies with management shareholdings is 72.9%, and the proportion of senior executives with working experience in universities or scientific research institutions is 90.3%. Various indicators show that the corporate governance of the sample enterprises has strong convergence. Other macro control variables appear consistent with reality.

TABLE 2. Descriptive statistics for the main variables.

4 Results

4.1 Benchmark regression

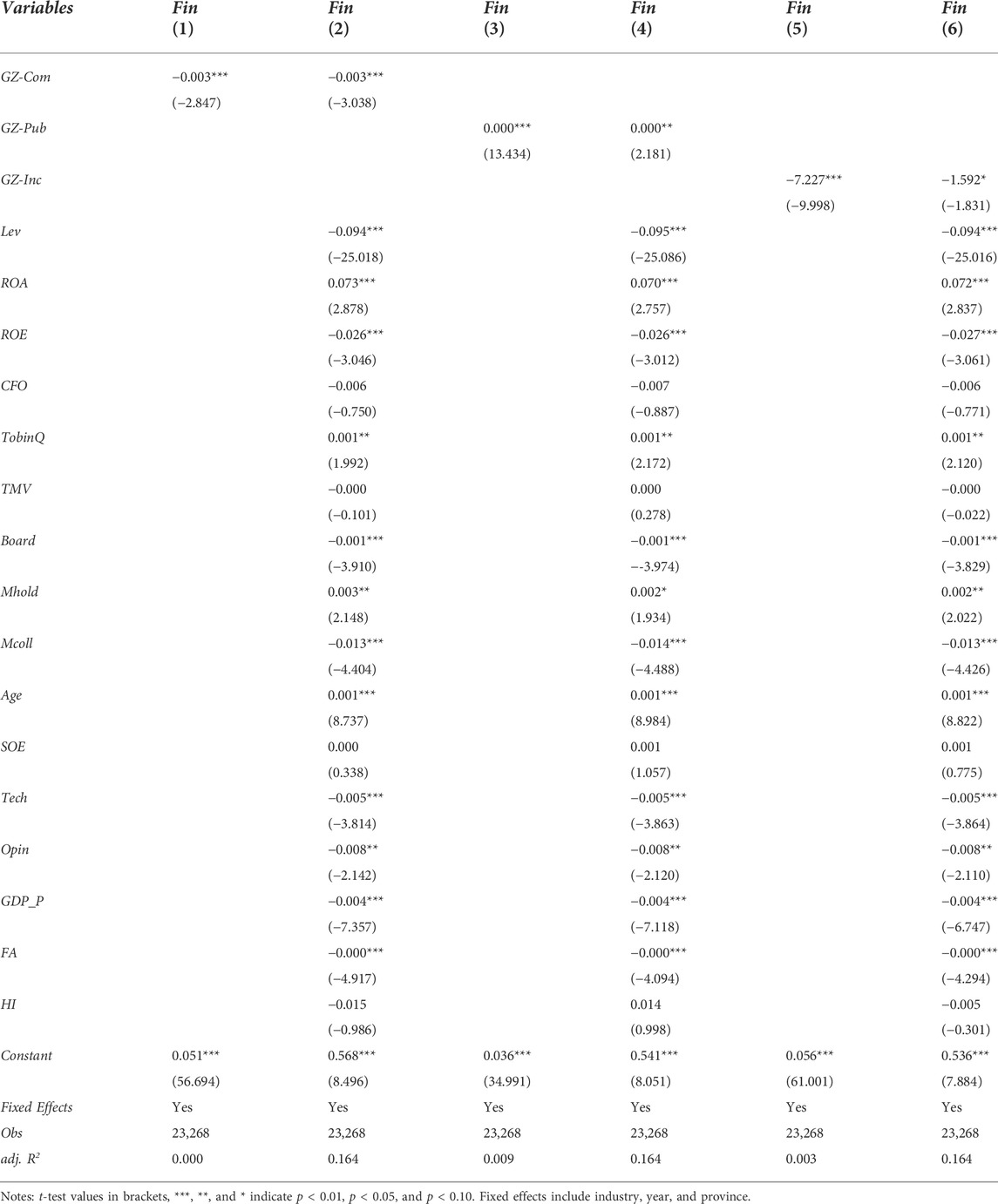

Table 3 reports the results of testing H1 and H2 regarding the direct impact of different types of environmental regulation tools on the financial investment levels of entity enterprises. In Table 3, columns (1), (3), and (5) are the regression results without the control variables, and columns (2), (4), and (6) are the regression results after adding the control variables. The coefficients of the indicators of the command-type environmental regulation tools (GZ-Com) are significantly negative at the 1% level. Since this indicator is an inverse indicator, the negative sign indicates that the stricter the command-type environmental regulation, the higher the financial investment level of entity enterprises, which supports Hypothesis 1. The coefficients of the indicators of public-participation-type environmental regulation tools (GZ-Pub) in columns (3) and (4) are significantly positive at the 1% and 5% levels, respectively, indicating that supervision using informal systems puts operating pressure on enterprises, thereby improving their financial investment levels. Both types of negative punishment measures have a boosting effect on the financial investment levels of entity enterprises, which further supports Hypothesis 1. The coefficients of the indicators of market-incentive-type environmental regulation tools (GZ-Inc) in columns (5) and (6) are significantly negative at the 1% and 10% levels, respectively, indicating that positive incentive measures alleviate the short-term financial investment tendency of enterprises and reduce financial investment levels, which supports Hypothesis 2.

TABLE 3. Impact of environmental regulation tools on financial investment level.

4.2 Robustness test

4.2.1 Endogeneity test

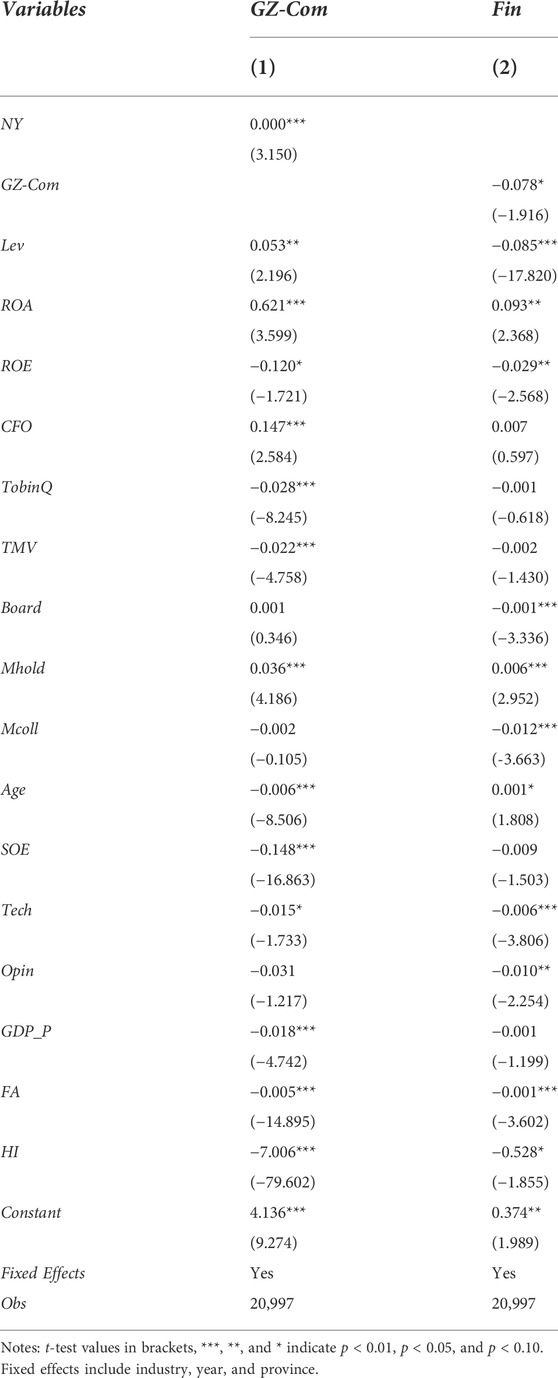

The two-stage least square method (2SLS) is used to further alleviate potential endogeneity problems. China’s energy consumption structure is still dominated by primary energy products such as coal and oil, and clean energy consumption accounts for a relatively small proportion. The consumption of primary energy products is usually accompanied by characteristics such as high consumption, high pollution, and low calorific value. Energy consumption efficiency has a strong correlation with the explanatory variable environmental regulation tools (GZ) and has no correlation with the disturbance term of the explained variable. Therefore, energy consumption efficiency (NY) is used as an instrumental variable (IV) and is measured by the ratio of energy consumption to the GDP of each province (see Table 4 for the test results). To ensure the IV estimates are not biased, the Cragg-Donald test for weak instruments is conducted. The F-statistic value is 10.905, which is greater than 10, indicating that the IV is not weak. In addition, there is only one IV, which is equal to the number of endogenous explanatory variables, so there is no overidentification problem. In the first stage, the coefficients of energy consumption efficiency (NY) and command-type environmental regulation tools (GZ-Com) are significantly positive at the 1% level, indicating that the instrumental variable has good explanatory power for environmental regulation tools. The regression results of the second stage are consistent with the main results, indicating that the research results remain robust after controlling for endogeneity.

TABLE 4. Endogeneity results of two-stage least squares test.

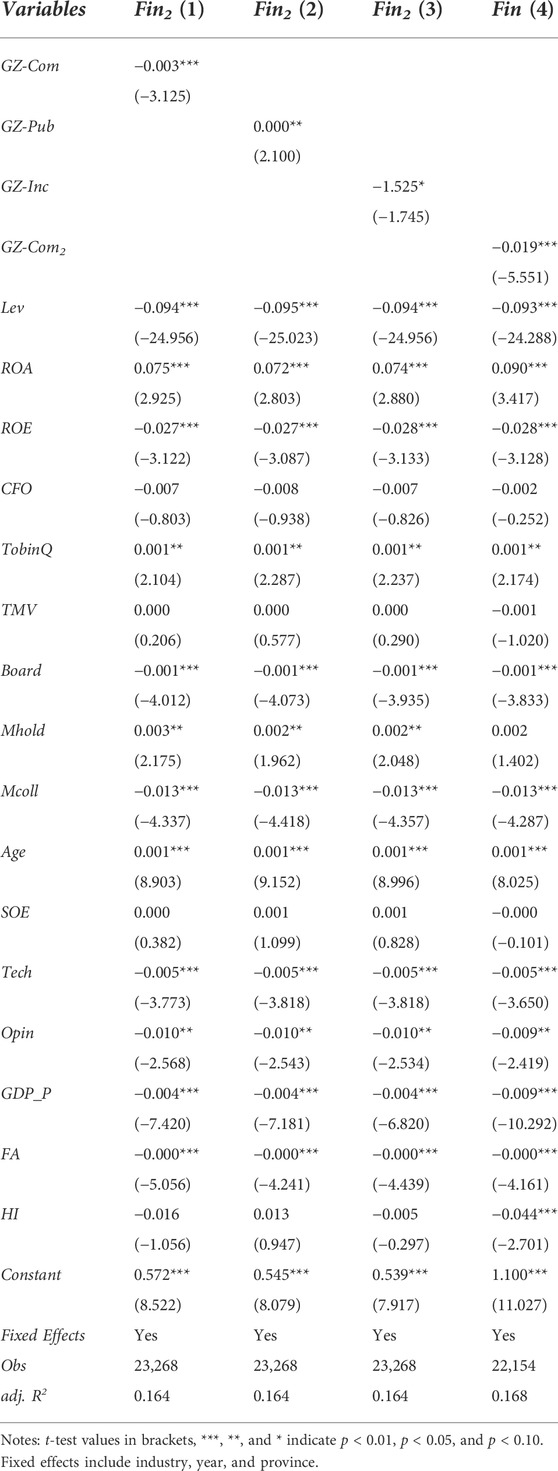

4.2.2 Replacing the explained and explanatory variables

Although the interest receivable and dividends receivable earned by an entity enterprise from equity investment have not actually been collected, they can also be included as financial assets according to the accrual basis accounting principle. Based on Chengsi and Ning (2020), interest receivable and dividends receivable are incorporated into the financial asset category and a new financial investment level indicator (Fin2) is formed for a robustness test. The test results are shown in columns (1), (2), and (3) of Table 5. When the explained variable is replaced by Fin2, the coefficients of the command-type (GZ-Com), public-participation-type (GZ-Pub) and market-incentive-type environmental regulation tools (GZ-Inc) are significant at the 1%, 5%, and 10% levels, respectively. These results are consistent with the main test results.

TABLE 5. Robustness test results after replacing the explained and explanatory variables.

In addition, the dimension of the industrial wastewater, industrial SO2, and industrial soot in the explanatory variable command type environmental regulation tools (GZ-Com) is reduced using the entropy method, and a new command-type environmental regulation tool index (GZ-Com2) is constructed for a robustness test. The test results are shown in column (4) of Table 5. The coefficients of GZ-Com2 and the financial investment level of entity enterprises (Fin) are significantly negative at the 1% level, and both the coefficients and their significance are greater than those in the original test. The results after replacing the explained and explanatory variables are consistent with the original test results, indicating that the research conclusions are sufficiently robust.

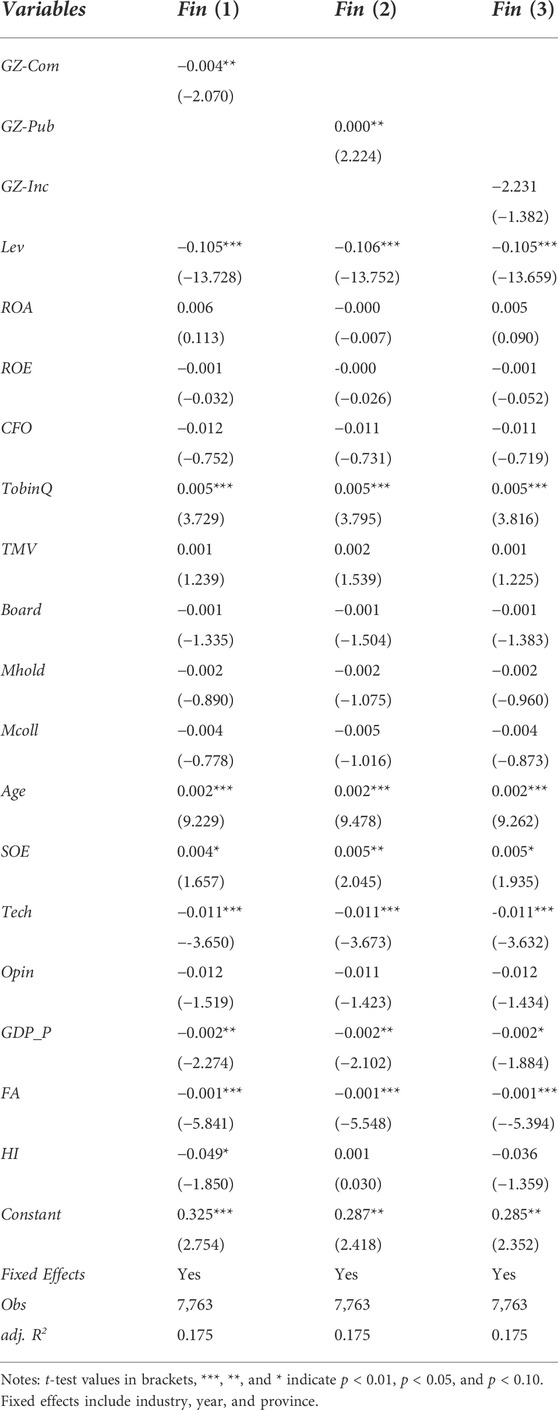

4.2.3 Reduced sample size

Compared with manufacturing enterprises, non-manufacturing enterprises receive relatively less attention and less intense environmental regulation. To test and verify the robustness of the main conclusion, this study draws on Qunhui’s (2017) hierarchical framework and narrows the definition of entity enterprises to non-manufacturing enterprises. According to the “Guidelines for Industry Classification of Listed Companies” (revised in 2012) issued by the China Securities Regulatory Commission (CSRC), the first digit of the manufacturing industry classification is used as the standard. The sample size is reduced to 7,763 observations, and the robustness test results are shown in Table 6. Among the non-manufacturing enterprises, the same influence path as the main test remains valid in command-type (GZ-Com) and public-participation-type environmental regulation tools (GZ-Pub) at the 5% significance level. Although the test result of market-incentive-type environmental regulation tools (GZ-Inc) is negative, it is not significant. This may indicate that non-manufacturing enterprises are somewhat insensitive to environmental regulation tools.

TABLE 6. Robustness test results of reduced sample of non-manufacturing enterprises.

4.3 Test of action mechanism

How managers of entity enterprises adjust their investment decisions under the influence of different types of environmental regulation tools has not previously been tested. This study’s argument is that negative punishment environmental regulation tools will weaken enterprise profitability in their primary business field. The “whipping the fast ox” and “heavy rewards and light punishments” mechanisms in the managerial incentive contracts will change the preferences for and investment proportion of enterprises’ physical and financial investments under environmental regulation by affecting their private benefits.

On the one hand, manager incentive compensation is usually positively correlated with enterprise short-term profits (Lin and Tomaskovic-Devey, 2013; Qiang and Bo, 2015); that is, entity enterprises will increase the compensation levels of managers who can increase enterprise performance, creating a “whipping the fast ox” effect. However, due to the inconsistent objective functions and asymmetric information between principals and agents, managers have greater discretion in making investment decisions. Under negative punitive environmental regulation tools, the increase in industrial operating costs reduces the rate of return on physical investment. To obtain rewards from “whipping the fast ox,” managers will further reduce physical investment by “pulling up the flowers to make up for the house” (Tosi et al., 2000), thereby increasing the intensity of financial investment with higher short-term returns.

On the other hand, there is a theory of “heavy rewards and light punishments” in manager incentives (Junxiong, 2011). When enterprises obtain high returns through financial investment, managers will attribute this to their own efforts (Xuxian et al., 2019). However, when the income obtained from financial investment contributes little to the entity’s profits, managers will blame this on external factors like market risk to avoid responsibility (Yong et al., 2017), and their own interests will suffer less damage. To summarize, command-type and public-participation-type environmental regulation tools reduce managers’ private benefits through the “whipping the fast ox” and “heavy rewards and light punishments” mechanisms. To ensure stability of their private benefits in the event the entity’s operating performance is impaired, managers enhance their preference for financial investment, thereby improving the financial investment level of entity enterprises.

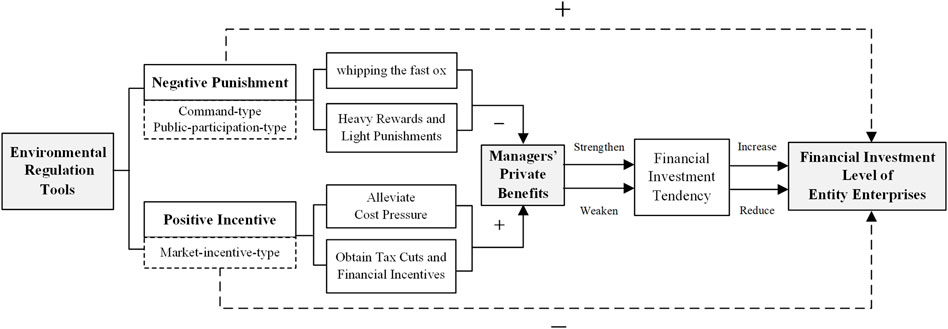

In contrast, positive incentive environmental regulation tools mainly adjust enterprise investment decisions through marketization, which will not have a significant impact on enterprise physical operations. Moreover, when entity enterprises adopt appropriate environmental protection policies, they may also benefit from tax cuts and financial incentives to ease the cost pressure. Overall, market-incentive-type environmental regulation tools can alleviate the damage environmental regulation does to managers’ private benefits through positive incentive means, weaken managers’ tendency toward short-term financial investment, and reduce the financial investment level of entity enterprises. Based on this, this study proposes that different types of environmental regulation tools affect managers’ private benefits and jointly affect their financial investment tendency, which in turn lead to changes in the level of financial investment of entity enterprises. This mechanism is represented by the logical chain illustrated in Figure 1.

FIGURE 1. Logic chain diagram of action mechanism.

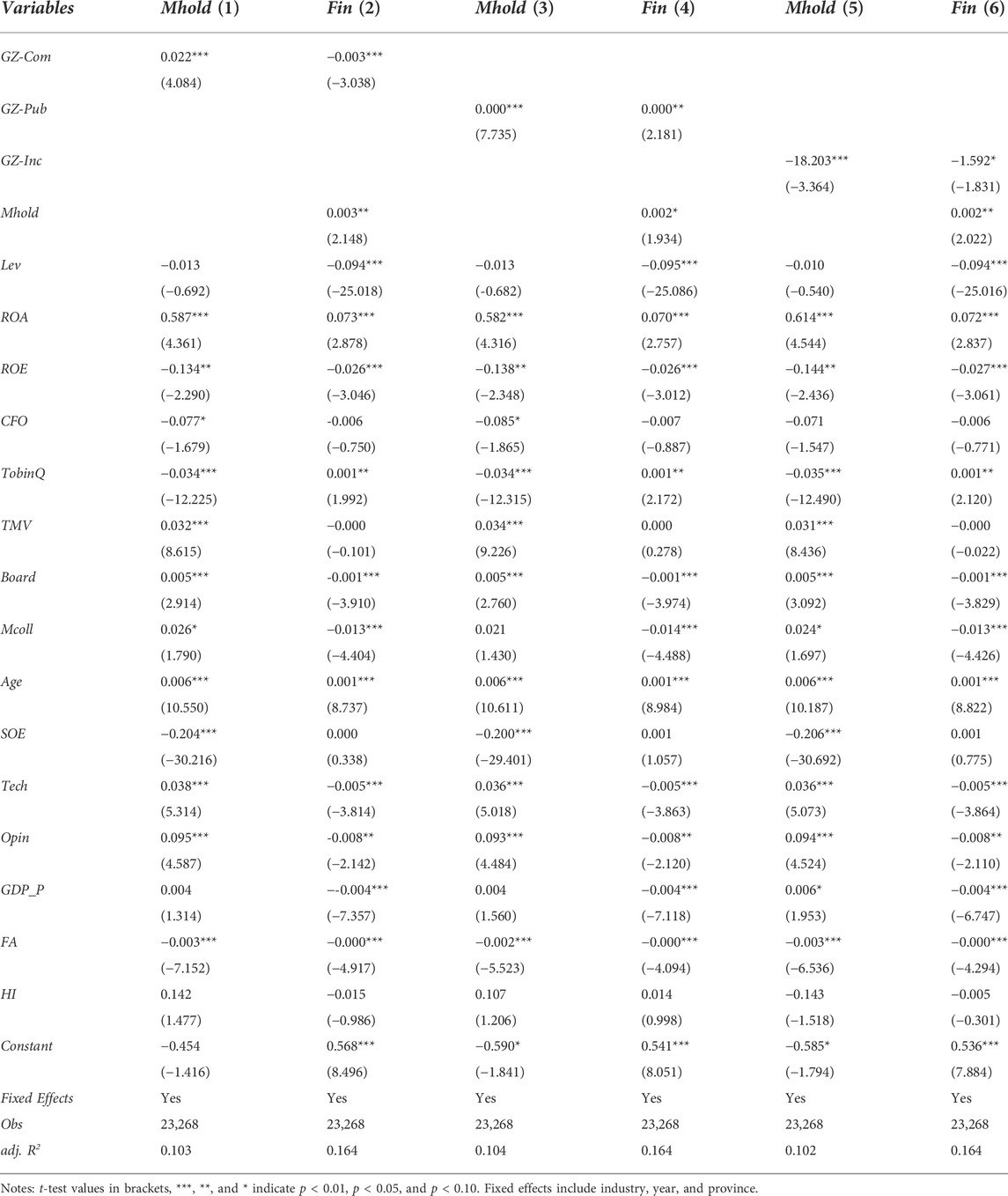

An intermediary effect model is used to test the logical chain, where management shareholding (Mhold) is the intermediary variable. The test results are reported in Table 7. Columns (1), (3), and (5) present the test results when the intermediary variable is used as the dependent variable, and columns (2), (4), and (6) are the test results of the intermediary effect model. The coefficients of all key variables of the intermediary effect are significant at the 1%, 5%. and 10% levels. According to Zhonglin and Baojuan (2014), the indirect effect and the direct effect in public-participation-type environmental regulation tools have opposite signs (|ab/c| is 0.022), and the effect is masked. The indirect effects in the other two types of environmental regulation tools have the same sign as the direct effects (ab/c are 0.023 and 0.000, respectively), which can be identified as a partial intermediary effect. In conclusion, the test results of the intermediary effect confirm that different types of environmental regulation tools affect managers’ private benefits, lead to changes in their financial investment preferences, and then affect the financial investment level of entity enterprises, verifying the existence of managerial incentives in the logical chain.

TABLE 7. Test of managerial incentive mechanism.

4.4 Heterogeneity test

4.4.1 Test of the moderating effect of financing constraints and relocation costs

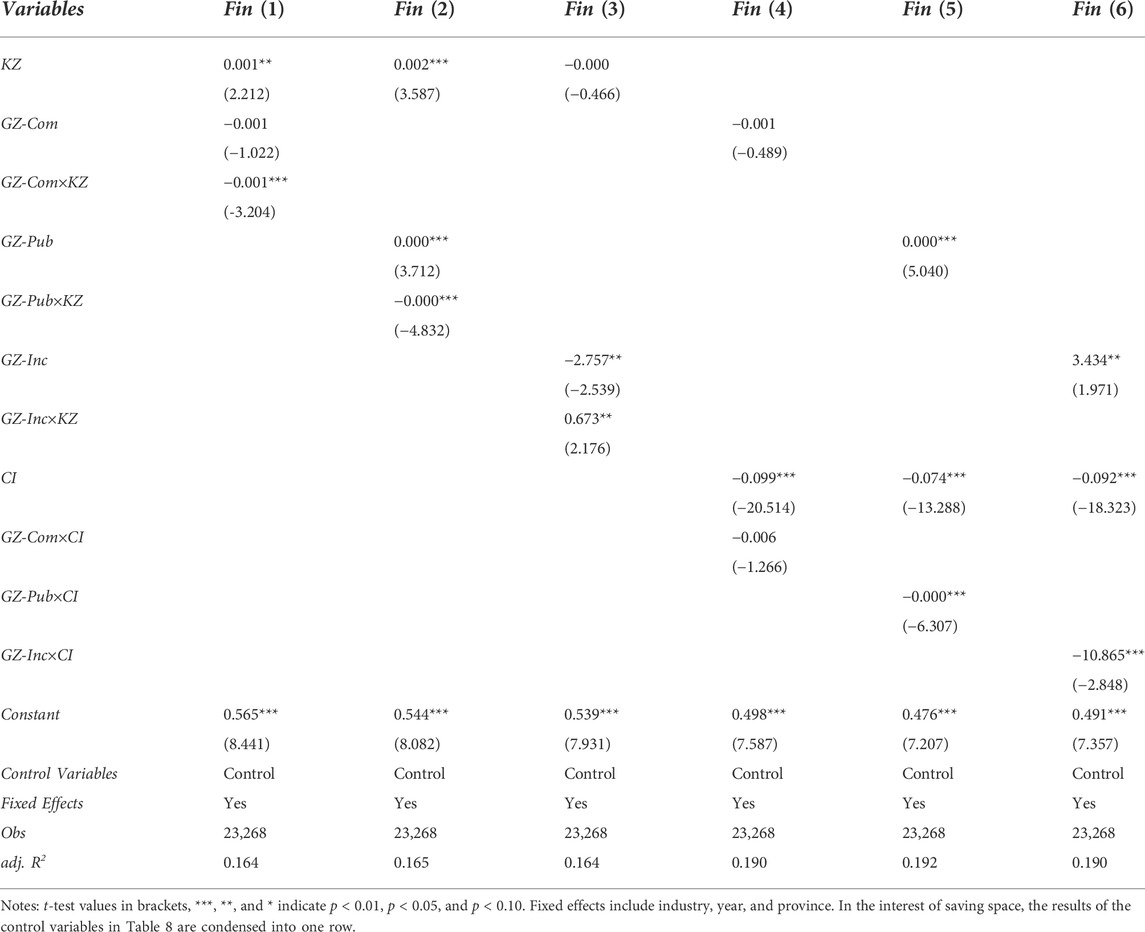

Previous studies have found that when facing severe environmental policies, enterprises will change their R&D and investment decisions based on the degree of financing constraints and relocation costs (Chengshi and Zhenyi, 2021). On the one hand, banks will raise the interest rates on loans of polluting enterprises, creating financing constraints (Haichao et al., 2021) and enhancing the potential for enterprises to obtain short-term profits through financial investment. On the other hand, in regions with strict environmental governance policies, the “pollution paradise” hypothesis in environmental governance suggests that high-polluting enterprises will be forced to relocate to areas with lower environmental protection requirements, forming a “pollution paradise” (Kellenberg, 2009); consequently, relocation costs may affect enterprise investment decisions. This study introduces two moderating variables—the degree of financing constraints and relocation costs—to test whether they are key factors that affect the benchmark regression model. The construction of the degree of financing constraints (KZ index) draws on the methods of Kaplan and Zingales (1997) and Zhihua et al. (2014). The measurement of relocation costs (CI) refers to Chengshi and Zhenyi (2021) and is computed as the ratio of fixed assets to total assets. The results of testing the moderating effect are shown in Table 8.

TABLE 8. Test of the moderating effect of financing constraints and relocation costs.

The degree of financing constraints (KZ) and the multiplicative terms of the three types of environmental regulation tools are all significant at levels above 5%. Among them, the coefficient of the interaction term GZ-Com×KZ is significantly negative at the 1% level, indicating that financing constraints enhance the promotion effect of command-type environmental regulation tools on the financial investment levels of entity enterprises. This is because when entity enterprises face financing constraints, tough environmental regulation tools place great pressure on them, leading them to seek short-term profits and increasing their financial investment level. However, the moderating effect of financing constraints does not affect all negative punishment means. The coefficient of the interaction term GZ-Pub×KZ is significantly negative at the 1% level, indicating that financing constraints do not enhance the positive relationship between public-participation-type environmental regulation tools and the financial investment level of entity enterprises. There is a certain substitution effect between the two on the contribution to the growth in the financial investment level of entity enterprises. In addition, the coefficient of the interaction term GZ-Inc×KZ is significantly positive at the 5% level, indicating that financing constraints weaken the negative relationship between market-incentive-type environmental regulation tools and the financial investment level. As the degree of financing constraints increases, enterprise cash flows tend to be tight, and managers will make decisions to increase financial investment, improving the financial investment levels of entity enterprises.

The results of testing the relocation costs (CI) and various environmental regulation tools are like the financing constraint (KZ) results. Due to the existence of a “pollution paradise,” enterprises tend to relocate high-pollution businesses to these locations when facing substantial pressures from environmental regulation. However, the impact of relocation costs on cash flows will become an important factor that may restrict enterprises from making such decisions. If relocation costs are high, managers may choose short-term financial investment to alleviate the private benefits reduction caused by the pressure of environmental protection. When relocation costs are high, the higher the pressure from environmental regulation, the higher the financial investment level of entity enterprises, similar to the financing constraint influence mechanism. Therefore, in the face of different environmental regulation tools, relocation costs and financing constraints play similar roles; both change managers’ financial investment decisions by affecting cash flows.

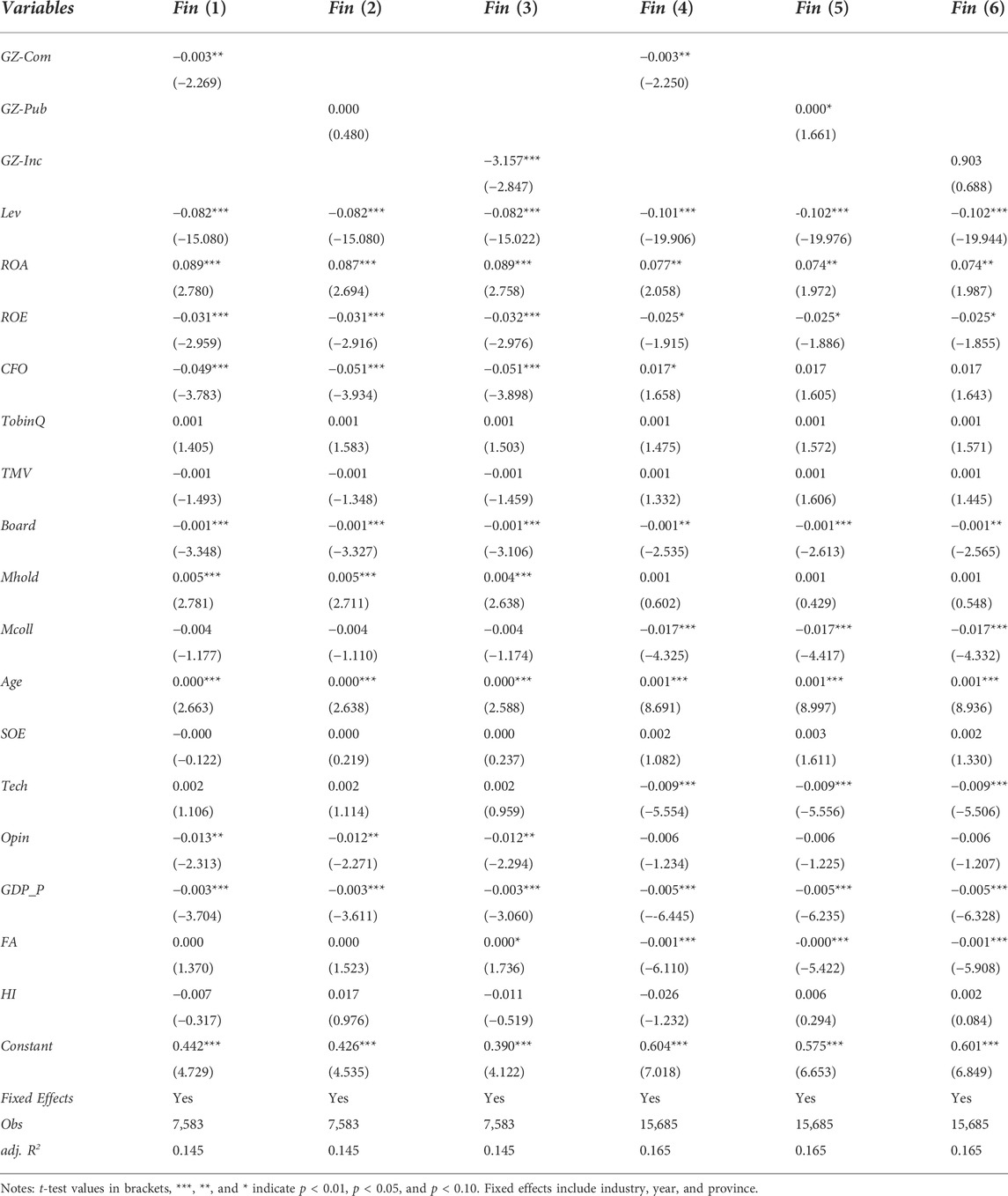

4.4.2 Heterogeneity test of heavy pollution industries

The environmental protection requirements for heavy pollution industries are higher, and the performance pressure on these entity enterprises is correspondingly greater. Based on Wenjing and Xiaoyan (2015), the enterprises were grouped into heavy pollution and non-heavy pollution industry groups according to the standards in the “Guidelines for Environmental Information Disclosure of Listed Companies” published by the Ministry of Environmental Protection in 2010. Group regressions were performed, and the test results are shown in Table 9. Enterprises in 16 industries are classified as the heavy pollution industry group, including thermal power (D44), iron and steel (C31), cement (C30), electrolytic aluminum (C32), coal (B06), metallurgy (C31/32), chemical (C26), petrochemical (C25), building materials (C30), papermaking (C22), brewing (C15), pharmaceutical (C27), fermentation and textile (C17), tanning (C19) and mining (b), and those in all other industries are included in the non-heavy pollution industry group. Columns (1), (2), and (3) are the grouping regression results of the heavy pollution industries, and columns (4), (5), and (6) are the grouping results of the non-heavy pollution industries.

TABLE 9. Grouping test results of heavy and non-heavy pollution industries.

From the results in columns (1) and (4), command-type environmental regulation tools (GZ-Com) play a significant role in both subsamples (p < 0.05), indicating that mandatory environmental regulation tools place great pressure on managers, leading to an increase in financial investment levels. As columns (2) and (5) show, public-participation-type environmental regulation tools (GZ-Pub) play a stronger role in the subsample of non-heavy pollution industries (p < 0.1), indicating that public supervision such as public opinion does not increase pressure on managers of heavy pollution enterprises. The results in columns (3) and (6) indicate that market-incentive-type environmental regulation tools (GZ-Inc) play a stronger role in the heavy pollution subsample (p < 0.01). Although the regression coefficient in the subsample of non-heavy pollution industries is positive, it is not significant. This shows that heavy pollution entity enterprises face strong pressure from environmental protection indicators and urgent demand for green innovation. Positive incentive tools such as taxation can encourage them to focus more on process improvement and green innovation, thus effectively reducing their financial investment level. However, there is not enough motivation for non-heavy pollution entity enterprises to continue to devote themselves to environmental protection innovation after they obtain environmental regulation incentives. Instead, part of the incentives may be reused for financial investment.

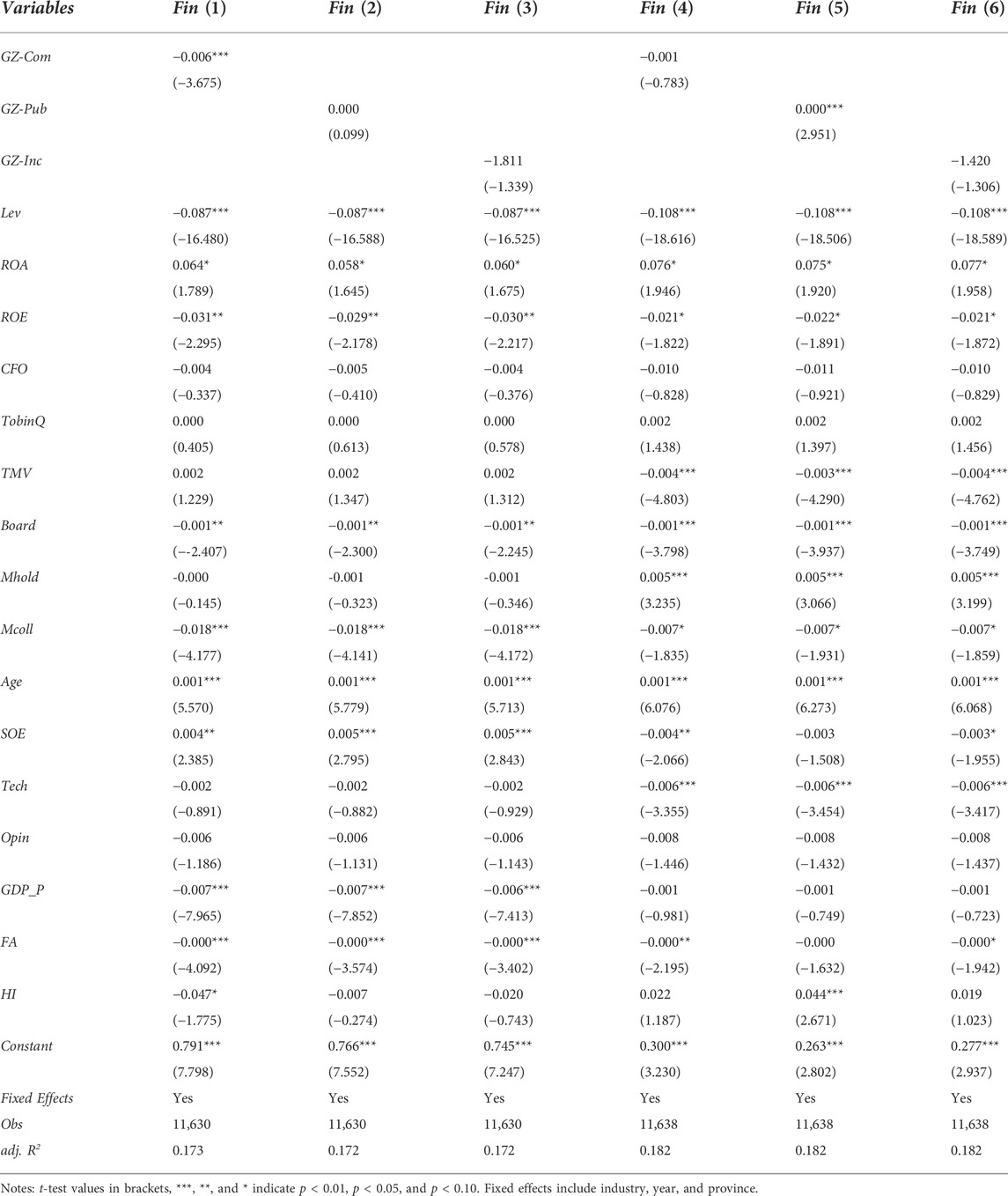

4.4.3 Firm size heterogeneity test

To some extent, a company’s size can represent its capability to resist risk. In the presence of strict environmental regulation tools, large enterprises tend to more easily digest the performance pressure brought about by environmental protection policies and transform themselves with the help of regulatory tools. However, this is not the case for small and medium-sized enterprises. Based on Yuping et al. (2021), the study’s full sample is divided into two subsamples, large enterprises and small and medium-sized enterprises (SMEs), for an additional grouping test. The median of total assets is used to divide the sample. Columns (1), (2), and (3) in Table 10 present the grouping test results of SMEs (where firm size is smaller than the median), and columns (4), (5), and (6) report the grouping test results of large enterprises (where firm size is larger than the median).

TABLE 10. Grouping test results of firm size.

Compared with SMEs, the relationship between command-type environmental regulation tools (GZ-Com) and the level of financial investment (Fin) disappears in the subsample of large entity enterprises, but the coefficient of public-participation-type environmental regulation tools (GZ-Pub) is still significantly positive at the 1% level. This shows that although large enterprises can better absorb the pressure of a performance decline brought about by environmental protection policies, public-participation-type environmental regulation tools may still put more pressure on managers through corporate social responsibility, word of mouth, and other means, resulting in further improvement in the financial investment level of entity enterprises.

5 Discussion

This study uses Chinese A-share entity listed companies from 2007 to 2019 as its sample to test the relationship between various environmental regulation tools and entity enterprise financial investments. Three approaches are used to perform the tests: a fixed-effects panel regression model, the two-stage least squares method, and an intermediary effects model.

First, negative punishment-type environmental regulation tools increase the financial investment levels of entity enterprises, while positive incentive-type environmental regulation tools have a negative impact on financial investment levels (see Table 3). This indicates that command-type and public-participation-type environmental regulation tools apply “pressure mechanisms” to enterprises (He et al., 2022), a result that is consistent with Zhang and Cheng’s (2022) conclusions. This occurs because environmental regulation increases enterprise cash holding levels, which has the same effect as increasing financial investment levels; both are aimed at overcoming short-term difficulties. However, market-incentive-type environmental regulation tools do not increase enterprise financial investment levels (Xing and Fengzhong, 2022), although they do increase industrial investment such as green innovation; this applies a “compensation mechanism” (Pickman, 1998; Chen et al., 2022; Shi and Li, 2022). These findings explain why there are two opposing conclusions in the previous studies.

Second, the managerial incentive mechanism is the intermediary between environmental regulation and enterprise investment (see Table 7 and Figure 1), a finding unique to this study. Research on the relationship between macro-environmental policies and micro-enterprise decision-making primarily focuses on internal and external factors such as government subsidies (Zhang and Cheng, 2022) and financing constraints (He et al., 2022). However, enterprise investment decisions reflect the behaviors of managers who form investment preferences after combining various factors and private benefits. Different environmental regulation tools change managers’ private benefits through the mechanisms of “whipping the fast ox” and “heavy rewards and light punishments,” causing their investment preferences to shift to financial investment or green innovation; this in turn determines the level of investment. This is a major finding of this study.

Third, financing constraints increase the financial investment level of entity enterprises (see Table 8). The results of this study are supported by Zhang and Cheng (2022), who indicate that limited bank loans will lead to an increase in the cash holdings of high pollution enterprises due to financing constraints. Therefore, enterprises are more inclined to seek short-term profits through the financial market to alleviate the pressure brought about by tough environmental regulation tools. At the same time, relocation costs enhance the positive effect of “negative punishment” type environmental regulation tools on financial investment (see Table 8). This supports the “pollution paradise” hypothesis; that is, high-polluting enterprises will be forced to relocate to areas with lower environmental protection requirements (Jaffe et al., 1995; Kellenberg, 2009). Affected by relocation costs when faced with intense environmental regulation, entity enterprises will face serious operating pressure, and managers tend to alleviate the reduction of private benefits through short-term financial investment.

Fourth, in heavy pollution industries, the significance between “negative punishment” environmental regulation tools and financial investment levels decreases (see Table 9). Consequently, when faced with strong environmental protection indicators, heavy pollution entity enterprises tend to change the situation through process improvement and green innovation (Guangsheng et al., 2021; Xing and Fengzhong, 2022). Moreover, large enterprises are more tolerant of command-type environmental regulation tools and more sensitive to public-participation-type environmental regulation tools (see Table 10). The larger the firm, the more likely that public-participation-type environmental regulation tools will pressure managers through social responsibility, goodwill, and other ways, increasing financial investment levels.

Overall, this study has made innovative breakthroughs in the aspects of environmental regulation, enterprise investment, managerial incentive mechanisms, and the applicability of environmental regulation tools. On the one hand, it enriches the existing literature on the transmission path of macro-environmental policies to micro-enterprise decision-making and highlights managers’ behavior as the main path. On the other hand, the study proposes that there is certain applicability and combinations of environmental regulation tools, and some important combinations are revealed. When the degree of financing constraints, relocation costs, pollution, and firm size differ, the effectiveness of various types of environmental regulation tools also differs. These findings are similar to those of the latest studies by Cheng and Kong (2022), Shi and Li (2022), and Zhang et al. (2022), all of whom conclude that different environmental tools need to be used together. Therefore, as policy makers and executors, government officials and managers should fully consider multiple factors such as region, environment, and enterprise characteristics, to implement reasonable environmental regulation tools.

6 Conclusion

This study empirically tests the relationship between different types of environmental regulation tools and financial investment levels of entity enterprises using provincial data including pollution emission, pollution control investment, and recommendations by the National People’s Congress, combined with data from Chinese A-share listed companies. Fixed-effects regression results show that negative punishment-type environmental regulation tools have a positive impact on the financial investment levels of entity enterprises, while positive incentive-type environmental regulation tools inhibit financial investment levels. The results of the mechanism analysis show that these impacts are formed through managerial incentive mechanisms. Heterogeneity tests found that the degree of financing constraints and relocation costs affect managers’ financial investment decisions by changing enterprise cash flows, strengthening the positive effect of command-type and public-participation-type environmental regulation tools on the financial investment level, and inhibiting the negative effect of market-incentive-type environmental regulation tools. Meanwhile, entity enterprises in high-pollution industries are more sensitive to command-type environmental regulation tools, and public-participation-type environmental regulation tools play a more significant role in large entities.

6.1 Theoretical contribution

First, although Dong et al. (2022), Chen et al. (2020), and Langpap and Shimshack (2010) all confirmed that environmental regulation tools have certain governance effects, there was still an absence of heterogeneity analysis of different types of environmental regulation tools. This resulted in two opposite conclusions about the most effective regulatory mechanism; some supported the use of “pressure mechanisms” (Mani and Wheeler, 1998; Silvia et al., 2017; Zhang et al., 2018; Petroni et al., 2019; Zhou et al., 2020), while other favored “compensation mechanisms” (Qiaoxin, 2021). This study considers two general types of environmental regulation tools—negative punishment types and positive incentive types—and examines their influence mechanisms. The results show that command-type and public-participation-type environmental regulation tools have the characteristics of negative punishment, which can positively promote the financial investment levels of entity enterprises in the short term. Market-incentive-type environmental regulation tools have the characteristics of positive incentives, which can restrain enterprise financial investment and allow enterprises to invest more resources in physical investment fields such as green transformation and development. The findings provide support for applying different types of environmental regulation tools.

Second, previous studies have focused on the impact of environmental regulation on the investment direction of enterprises (Haijing et al., 2021; Maomao and Yanyan, 2021), ignoring the influence logic between them. Few studies have deeply explored the transmission mechanism between cross-latitude factors. The results of the mechanism analysis show that environmental regulation tools mainly affect managers’ private benefits through incentive mechanisms such as “whipping the fast ox” and “heavy rewards and light punishments,” alleviating cost pressures, obtaining tax reductions, and financial incentives, which in turn affect their financial investment preferences, and ultimately change the financial investment levels of entity enterprises. This study decodes the “black box” between macro-environmental policy and micro-enterprise decision-making and proposes that a managerial incentive mechanism plays an intermediary role between environmental regulation tools and the financial investment levels of entity enterprises. This finding establishes the relationship between the two and reveals the specific path of policy effects.

6.2 Managerial implication

Green mountains, clear water, clear seas, and blue sky are precious treasures that cannot be bought or borrowed. Different types of environmental regulation tools have played a huge role in improving China’s environmental problems. However, in the implementation process, there is a contradiction between the government’s environmental competition and the environmental pressures placed on enterprises (Raffin, 2014; Dao and Edenhofer, 2018). Under the comprehensive effect of environmental regulation tools and green transformation and development, managers’ investment decisions and the financial investment levels of entity enterprises will change accordingly.

This study’s findings can be of significant help to enterprises in better designing their managerial incentive mechanisms and adjusting their investment direction. The study suggests that enterprises should pay attention to the long-term aspect when designing managerial incentive systems. Managers are at the helm of an enterprise. When environmental problems are more prominent, environmental protection indicators should be added to managerial incentive mechanisms, so they can actively cooperate with regional environmental protection policies to achieve green production. This finding’s managerial implications confirm that the choice of environmental regulation tools, the intensity of managerial incentives, and the financial investment levels of entity enterprises need to be controlled within reasonable ranges.

6.3 Practical/social implications

First, this study provides practical suggestions for local governments as they choose environmental protection policies. During the tenure of local government officials, environmental constraints have been incorporated into the promotion competition system, forcing officials to choose between short-term and conflicting goals. The methods must suit the situation based on the pollution levels and enterprise characteristics. The findings provide a theoretical basis for the proposed policy recommendations for local governments.

Second, entity enterprises are also faced with the two contradictory goals of economic growth and short-term environmental protection. With a goal of minimizing their pains in the process of green transformation and development, this study provides decision-making ideas conducive to long-term development. For entity enterprises with low degrees of pollution, the application scenarios and practices of market-incentive-type environmental regulation tools should be expanded and strengthened. As positive incentive types of environmental regulation tools, they not only can reduce enterprise resistance to environmental protection indicators, but also avoid the emergence of “pollution paradises.” For large enterprises with high pollution, environmental violations should be curbed and punished more severely, although strict environmental law enforcement and environmental indicator systems will lead to some increase in the financial investment levels of entity enterprises, the lesser evil should be chosen when the two evils intersect. For this purpose, financial investment can be used to overcome short-term difficulties.

Third, the use of Chinese A-share listed companies as a sample for the empirical research is a valuable supplement to the study of environmental regulation effects. Unlike developed countries, which prefer market-incentive-type environmental regulation tools, developing countries mainly use command-type tools, such as performance assessments, laws, and regulation. This study overcomes the limitations of previous studies of mature companies in developed countries and provides a useful supplement and empirical reference for forming environmental regulation policies in emerging economies.

6.4 Limitations and future work

This study focuses only on the implementation effects of three types of environmental regulation tools at the micro level and thus has certain limitations. For example, although it examines the impact of environmental regulation tools on short-term financial investments of entity enterprises, its ultimate impact on green transformation and development of enterprises has not been comprehensively evaluated from a long-term perspective. At the same time, due to changes in external environments such as COVID-19 and financial supervision, current theoretical development is far behind the progress of practical evolution, which needs further in-depth research. In addition, this study only uses data from Chinese listed companies, which certainly affects generalizability. In the future, data from major developing countries such as Russia and Brazil, as well as data from developed countries like the United States, should be used for comparative analysis.

Data availability statement

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

Author contributions

DN led the conception and design of the study and wrote the original manuscript. DN and ZW collected and analyzed the data regarding environmental regulation tools and financial investment levels of entity enterprises. SY was responsible for reviewing and editing the manuscript. All authors actively participated in the experimental design, data interpretation, and manuscript preparation, and approved the manuscript for publication.

Funding

The authors acknowledge financial support by the Philosophy and Social Science Planning Project of Shanxi Province (No. 2020YY186 and No. 2022YD125), and the funder is the office of philosophy and social sciences of Shanxi Province.

Acknowledgments

We would like to thank the editor and reviewers for their insightful comments and constructive suggestions. We are also grateful to Editage (www.editage.cn) for English language editing.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

1It has been argued that the incentives enterprises use for managers often end up having the effect of “whipping the fast ox,” that is, the higher the manager’s profits, the greater their requirements are. In effect, the incentives actually punish the managers that are more efficient.

2The stock exchange uses the notation “special treatment” (ST) for listed companies with abnormal financial or other conditions to alert investors of the associated risks. A company that has experienced losses for more than 3 years is then marked as *ST. PT stands for ‘particular transfer’ and refers to the special transfer service for suspended stocks.

References

Akdoğu, E., and MacKay, P. (2008). Investment and competition. J. Financ. Quant. Anal. 43, 299–330. doi:10.1017/s0022109000003537

Arouri, M. E. H., Caporale, G. M., Rault, C., Sova, R., and Sova, A. (2012). Environmental regulation and competitiveness: evidence from Romania. Ecol. Econ. 81, 130–139. doi:10.1016/j.ecolecon.2012.07.001

Arslan, Z., Kausar, S., Kannaiah, D., Shabbir, M. S., Khan, G. Y., and Zamir, A. (2022). The mediating role of green creativity and the moderating role of green mindfulness in the relationship among clean environment, clean production, and sustainable growth. Environ. Sci. Pollut. Res. 29, 13238–13252. doi:10.1007/s11356-021-16383-z

Becker, R., and Henderson, V. (2000). Effects of air quality regulations on polluting industries. J. Polit. Econ. 108, 379–421. doi:10.1086/262123

Borghesi, S., Cainelli, G., and Mazzanti, M. (2015). Linking emission trading to environmental innovation: evidence from the Italian manufacturing industry. Res. Policy 44, 669–683. doi:10.1016/j.respol.2014.10.014

Cai, H., Chen, Y., and Gong, Q. (2016). Polluting thy neighbor: unintended consequences of China’s pollution reduction mandates. J. Environ. Econ. Manage. 76, 86–104. doi:10.1016/j.jeem.2015.01.002

Chen, Z., Niu, X., Gao, X., and Chen, H. (2022). How does environmental regulation affect green innovation? A perspective from the heterogeneity in environmental regulations and pollutants. Front. Energy Res. 10, 885525. doi:10.3389/fenrg.2022.885525

Chen, Z., Zhang, X., and Ni, G. (2020). Decomposing capacity utilization under carbon dioxide emissions reduction constraints in data envelopment analysis: an application to Chinese regions. Energy Policy 139, 111299. doi:10.1016/j.enpol.2020.111299

Cheng, Z., and Kong, S. (2022). The effect of environmental regulation on green total-factor productivity in China's industry. Environ. Impact Assess. Rev. 94, 106757. doi:10.1016/j.eiar.2022.106757

Chengshi, T., and Zhenyi, H. (2021). Can stringent environmental policy encourage technological innovation in industrial enterprises? Sci. Res. Manag. 42, 166–173. doi:10.19571/j.cnki.1000-2995.2021.10.019

Chengsi, Z., and Ning, Z. (2020). What drives the financialization of China’s real sector: monetary expansion, profit-seeking capital or risk aversion? J. Financ. Res. 09, 1–19.

Cui, J., Zhang, J., and Zheng, Y. (2018). Carbon pricing induces innovation: Evidence from China's regional carbon market pilots. AEA Pap. Proc. 108, 453–457. doi:10.1257/pandp.20181027

Da Luz, A. R., Bittencourt, J. T., and Taioka, T. (2015). Wealth financialization: operating profit as conditioning of financial revenue. J. Financ. Innov. 1, 1–5. doi:10.15194/jofi_2015.v1.i1.4

Dao, N. T., and Edenhofer, O. (2018). On the fiscal strategies of escaping poverty-environment traps towards sustainable growth. J. Macroecon. 55, 253–273. doi:10.1016/j.jmacro.2017.10.007

Demir, F. (2009). Financial liberalization, private investment and portfolio choice: financialization of real sectors in emerging markets. J. Dev. Econ. 88, 314–324. doi:10.1016/j.jdeveco.2008.04.002

Dong, K., Shahbaz, M., and Zhao, J. (2022). How do pollution fees affect environmental quality in China? Energy Policy 160, 112695. doi:10.1016/j.enpol.2021.112695

Duchin, R. (2010). Cash holdings and corporate diversification. J. Finance 65, 955–992. doi:10.1111/j.1540-6261.2010.01558.x

Feng, T., Jinyu, Z., and Hao, Z. (2021). Does environmental regulation improve the quantity and quality of green innovation - evidence from the target responsibility system of environmental protection. China Ind. Econ. 02, 136–154. doi:10.19581/j.cnki.ciejournal.2021.02.016

Feng, Y., Yao, S., Wang, C., Liao, J., and Cheng, F. (2022). Diversification and financialization of non-financial corporations: Evidence from China. Emerg. Mark. Rev. 50, 100834. doi:10.1016/j.ememar.2021.100834

Fuxin, J., Zhujun, W., and Junhong, B. (2013). The dual effect of environmental regulations’ impact on innovation-an empirical study based on dynamic panel data of Jiangsu manufacturing. China Ind. Econ. 07, 44–55. doi:10.19581/j.cnki.ciejournal.2013.07.004

Guangsheng, J., Jianci, L., and Weian, L. (2021). Do green investors play a role? Empirical research on firms’ participation in green governance. J. Financ. Res. 05, 117–134.

Haichao, F., Yuchao, P., Huanhuan, W., and Zhiwei, X. (2021). Greening through finance? J. Dev. Econ. 152, 102683. doi:10.1016/j.jdeveco.2021.102683

Haijing, C., Qiaoxin, X., and Huimin, Z. (2021). Active adaptability or short-run profit pursuing: Institutional logic of entity enterprises financialization from the perspective of environmental regulation. Acc. Res. 04, 78–88.

He, L., Zhong, T., Gan, S., Liu, J., and Xu, C. (2022). Penalties vs. subsidies: a study on which is better to promote corporate environmental governance. Front. Environ. Sci. 10, 1–13. doi:10.3389/fenvs.2022.859591

Hong, Z. (2008). The impact of environmental regulation on industrial technological innovation -An empirical research based on the panel data from China. Ind. Econ. Res. 03, 35–40. doi:10.13269/j.cnki.ier.2008.03.001

Jaffe, A. B., Peterson, S. R., Portney, P. R., and Stavins, R. N. (1995). Environmental regulation and the competitiveness of US manufacturing: What does the evidence tell us? J. Econ. Lit. 33, 132–163.

Junxiong, F. (2011). Managerial power and asymmetry of compensation change in China’s public companies. Econ. Res. J. 46, 107–120.

Kaplan, S. N., and Zingales, L. (1997). Do investment-cash flow sensitivities provide useful measures of financing constraints? Q. J. Econ. 112, 169–215. doi:10.1162/003355397555163

Kellenberg, D. K. (2009). An empirical investigation of the pollution haven effect with strategic environment and trade policy. J. Int. Econ. 78, 242–255. doi:10.1016/j.jinteco.2009.04.004

Kim, H., and Kung, H. (2017). The asset redeployability channel: how uncertainty affects corporate investment. Rev. Financ. Stud. 30, 245–280. doi:10.1093/rfs/hhv076

Kirikkaleli, D., and Adebayo, T. S. (2021). Do renewable energy consumption and financial development matter for environmental sustainability? New global evidence. Sustain. Dev. 29, 583–594. doi:10.1002/sd.2159

Langpap, C., and Shimshack, J. P. (2010). Private citizen suits and public enforcement: Substitutes or complements? J. Environ. Econ. Manage. 59, 235–249. doi:10.1016/j.jeem.2010.01.001

Li, X., and Wenfeng, W. (2021). Do regional differences affect the degree of transformation between financial investment and operating profit? An exploration from the Micro⁃perspective of listed manufacturing companies. Manag. Rev. 33, 3–14. doi:10.14120/j.cnki.cn11-5057/f.2021.12.016

Lin, K. H., and Tomaskovic-Devey, D. (2013). Financialization and U.S. income inequality, 1970–2008. Am. J. Sociol. 118, 1284–1329. doi:10.1086/669499

Malmendier, U., and Tate, G. (2015). Behavioral CEOs: the role of managerial overconfidence. J. Econ. Perspect. 29, 37–60. doi:10.1257/jep.29.4.37

Mani, M., and Wheeler, D. (1998). In search of pollution havens? Dirty industry in the world economy, 1960-1995. J. Environ. Dev. 7, 215–247. doi:10.1177/107049659800700302

Maomao, Y., and Yanyan, M. (2021). The influence of environmental regulation on the behavior of firms’ financialization-based on a quasi-natural experiment of “new environmental protection law”. J. Beijing Inst. Technol. Soc. Sci. Ed. . 23, 30–43. doi:10.15918/j.jbitss1009-3370.2021.2846

Mughal, N., Arif, A., Jain, V., Chupradit, S., Shabbir, M. S., Ramos-Meza, C. S., et al. (2022). The role of technological innovation in environmental pollution, energy consumption and sustainable economic growth: evidence from south asian economies. Energy Strategy Rev. 39, 100745. doi:10.1016/j.esr.2021.100745

Petroni, G., Bigliardi, B., and Galati, F. (2019). Rethinking the porter hypothesis: the underappreciated importance of value appropriation and pollution intensity. Rev. Policy Res. 36, e0001–e0140. doi:10.1111/ropr.12317

Pickman, H. A. (1998). The effect of environmental regulation on environmental innovation. Bus. Strategy Environ. 7, 223–233. doi:10.1002/(sici)1099-0836(199809)7:4<223::aid-bse164>3.0.co;2-s

Qiang, L., and Bo, F. (2015). Study on the relationship between executive incentive and quality of environmental information disclosure - based on the moderating effects of governance and market. J. Shanxi Univ. Fin. Econ. 37, 93–104. doi:10.13781/j.cnki.1007-9556.2015.02.009

Qiaoxin, X. (2021). Environmental regulation, green financial development and technological innovation of firms. Sci. Res. Manag. 42, 65–72. doi:10.19571/j.cnki.1000-2995.2021.06.009

Qin, Y., Gang, Z., Qing, D. S., and Fenglong, W. (2018). Research on the effects of different policy tools on China’s emissions reduction innovation: based on the panel data of 285 prefectural-level municipalities. China Popul. Resour. Environ. 28, 115–122. doi:10.12062/cpre.20170915

Qunhui, H. (2017). On the development of China’s real economy at the new stage. China Ind. Econ. 09, 5–24. doi:10.19581/j.cnki.ciejournal.2017.09.001

Raffin, N. (2014). Education and the political economy of environmental protection. Ann. Econ. Stat. 115–116, 379–407. doi:10.15609/annaeconstat2009.115-116.379

Ramanathan, R., He, Q., Black, A., Ghobadian, A., and Gallear, D. (2017). Environmental regulations, innovation and firm performance: a revisit of the porter hypothesis. J. Clean. Prod. 155, 79–92. doi:10.1016/j.jclepro.2016.08.116

Shi, Y., and Li, Y. (2022). An evolutionary game analysis on green technological innovation of new energy enterprises under the heterogeneous environmental regulation perspective. Sustainability 14, 6340. doi:10.3390/su14106340

Silvia, A., Tomasz, K., and Vera, Z. (2017). Environmental policies and productivity growth: evidence across industries and firms. J. Environ. Econ. Manage. 81, 209–226. doi:10.1016/j.jeem.2016.06.002

Songling, Y., Dengyun, N., Tingli, L., and Zhihua, W. (2021). Research on the influence of investor sentiment on the industrial companies’ financialization from the perspective of behavioral finance. Manag. Rev. 33, 3–15. doi:10.14120/j.cnki.cn11-5057/f.2021.06.001

Tosi, H. L., Werner, S., Katz, J. P., and Gomez-Mejia, L. R. (2000). How much does performance matter? A meta-analysis of CEO pay studies. J. Manag. 26, 301–339. doi:10.1177/014920630002600207

Wang, Y., Chen, C. R., and Huang, Y. S. (2014). Economic policy uncertainty and corporate investment: evidence from China. Pacific-Basin Finance J. 26, 227–243. doi:10.1016/j.pacfin.2013.12.008

Wen, J., Mughal, N., Zhao, J., Shabbir, M. S., Niedbała, G., Jain, V., et al. (2021). Does globalization matter for environmental degradation? Nexus among energy consumption, economic growth, and carbon dioxide emission. Energy Policy 153, 112230. doi:10.1016/j.enpol.2021.112230

Wenjing, L., and Xiaoyan, L. (2015). Do institutional investors care firm environmental performance? Evidence from the most polluting Chinese listed firms. J. Financ. Res. 12, 97–112.

Wugan, C., and Qingqing, L. (2019). Dual effect of environmental regulation on enterprise’s eco-technology innovation. Sci. Res. Manag. 40, 87–95.

Xiaosong, R., Yujia, L., and Guohao, Z. (2020). The impact and transmission mechanism of economic agglomeration on carbon intensity. China Popul. Resour. Environ. 30, 95–106. doi:10.12062/cpre.20200113

Xie, R. H., Yuan, Y. J., and Huang, J. J. (2017). Different types of environmental regulations and heterogeneous influence on “green” productivity: evidence from China. Ecol. Econ. 132, 104–112. doi:10.1016/j.ecolecon.2016.10.019

Xing, L., and Fengzhong, L. (2022). Environmental regulation and corporate financial asset allocation: A natural experiment from the new environmental protection law in China. Financ. Res. Lett. 47, 102974. doi:10.1016/j.frl.2022.102974

Xueqing, W., and Yong, L. (2021). Mechanism of how air pollution control and environmental regulation influence enterprises’ inventory: Based on the data of industrial enterprises in Guangdong Province. Manag. Rev. 33, 60–70.

Xuxian, W., Hong, W., and Jia, H. (2019). Does the allocation of financial assets widen the compensation gap of executives. Mod. Fin. Econ. 39, 25–39.

Yong, D., Huan, Z., and Jianying, C. (2017). The impact of financialization on future development of real enterprises’ core business: promotion or inhibition. China Ind. Econ. 12, 113–131. doi:10.19581/j.cnki.ciejournal.20171214.007

Yuping, D., Lun, W., and Wenjie, Z. (2021). Does environmental regulation promote green innovation capability? - evidence from China. Stat. Res. 38, 76–86. doi:10.19343/j.cnki.11-1302/c.2021.07.006

Zhang, C., and Cheng, J. (2022). Environmental regulation and corporate cash holdings: evidence from China’s new environmental protection law. Front. Environ. Sci. 10, 1–15. doi:10.3389/fenvs.2022.835301

Zhang, P. (2021). Target interactions and target aspiration level adaptation: how do government leaders tackle the “environment-economy” nexus? Public admin. Rev. 81, 220–230. doi:10.1111/puar.13184

Zhang, W., Li, G., and Guo, F. (2022). Does carbon emissions trading promote green technology innovation in China? Appl. Energy 315, 119012. doi:10.1016/j.apenergy.2022.119012

Zhang, Y., Wang, J., Xue, Y., and Yang, J. (2018). Impact of environmental regulations on green technological innovative behavior: An empirical study in China. J. Clean. Prod. 188, 763–773. doi:10.1016/j.jclepro.2018.04.013

Zhihua, W., Aimin, Z., and Bo, L. (2014). Financial ecological environment and corporate financial constraints: Evidence from Chinese listed firms. Acc. Res. 05, 73–80+95.

Zhonglin, W., and Baojuan, Y. (2014). Analyses of mediating effects: the development of methods and models. Adv. Psychol. Sci. 22, 731–745. doi:10.3724/SP.J.1042.2014.00731

Keywords: environmental regulation tools, negative punishment, positive incentive, entity enterprises, financial investment

Citation: Niu D, Wang Z and Yang S (2022) Are environmental regulation tools effective? An analysis based on financial investment of entity enterprises. Front. Environ. Sci. 10:1019648. doi: 10.3389/fenvs.2022.1019648

Received: 15 August 2022; Accepted: 05 October 2022;

Published: 18 October 2022.

Edited by: