Yanqiong Liu1

Yanqiong Liu1 Cunyi Yang

Cunyi Yang Zhenghui Li

Zhenghui Li

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Environ. Sci. , 29 July 2021

Sec. Environmental Economics and Management

Volume 9 - 2021 | https://doi.org/10.3389/fenvs.2021.722910

This article is part of the Research Topic Green Finance, Renewable and Non-Renewable Energy, and COVID-19 View all 26 articles

In the context of intensifying global geopolitical disputes and trade frictions, the relationship between geopolitics and energy trade has attracted extensive attention from scholars. The complexity of geopolitical risks mainly comes from the diversity of geopolitical events, which directly leads to the different responses of energy trade in the face of geopolitical risks. The purpose of this paper is to analyze the heterogeneity of the impact of geopolitical events on energy trade based on the difference of event types. This paper uses Regression Discontinuity Design (RDD) to simulate a quasi-natural experiment. Based on the monthly data and the Geopolitical Risk index (GPR index) of 17 emerging economies from 2000 to 2020, the empirical analysis can be concluded as follows: Wars and conflicts events lead to the increase of energy trade volume; terrorist attacks have no significant impact on energy trade; international tension can cause the decline in energy trade. Additional analysis shows that the impact of geopolitical events on energy trade in emerging economies is concentrated on the demand side, and the demand is severely inelastic.

Energy is bound up with geopolitics. In today’s world pattern, the relations between major powers are complicated, with extremely changeable political and economic situation. The situation of traditional oil-producing countries is turbulent, and energy has gradually become an effective domestic policy tool and a powerful foreign policy weapon. The new relationship between energy and geopolitics in recent years needs to be understood from a mutual perspective. On the one hand, the energy transition is transforming global geopolitics: the US shale oil revolution, China’s energy transition and global efforts to combat climate change are increasingly reducing the dependence on oil. This global energy transition has complex and far-reaching geopolitical implications, including triggering new competition among economies and creating winners and losers in a new energy order. On the other hand, the increasingly tense geopolitical relations have led to increasing challenges to energy security for all countries: the situation in the oil-producing region of the Middle East is tense; the United States has imposed sanctions on Iran because of the nuclear issue, which seriously threatens the security of oil and gas supply and channels; the disputes over the control of offshore oil and gas resources and transportation channels continue; the regions with proven oil reserves in Africa remain unstable for a long time; and the breakdown of international cooperation hinders energy trade. Countries and regions around the world are often very passive in the face of different geopolitical events. Therefore, it is necessary to study the heterogeneity of the impact of geopolitical events on energy trade.

The rest of this paper is structured as follows: the first part is the introduction of empirical facts and the summary of existing literature; the second section puts forward the research hypotheses based on the simple analysis of the relationship between geopolitical events and energy trade, and introduces the model and data of the empirical research in this paper; the third section uses RDD to analyze the heterogeneity of the impact of three geopolitical events on the energy trade of emerging economies; in the fourth section, the robustness test is carried out from the perspective of validity, algorithm and Bootstrap; the fifth section gives the basic conclusions and policy implications.

The impact of long-term fluctuation of geopolitical risks on energy market has aroused the attention of scholars all over the world. The view that political risk is the primary consideration of energy policy has been widely recognized (Yang et al., 2014; Lee et al., 2017; Duan et al., 2018). Through TVP-VAR model, Assaf et al. Found that the average impact of market uncertainty such as geopolitical risk on energy market is about 53% (Assaf et al., 2021). From the perspective of supply and demand relationship, the rise of national risk will lead to the decline of energy consumption, thus reducing a country’s dependence on global energy trade (Lee et al., 2017). Due to severe geopolitical uncertainty, tensions between nations that produces fuel/oil, and trade sanctions, almost no nation can guarantee a consistent fuel supply and that can affect the progress or development of countries significantly as fuel is the backbone of the energy supply (Anwar, 2021). The positive impact of global real aggregate demand has a significant negative effect on the uncertainty of American economic policy, while the impact on specific oil demand has the opposite effect (Kang and Ratti, 2013). The high risk will lead to the stagnation of national energy production and supply activities and the inability to provide enough energy to meet domestic demand and foreign export (Sun et al., 2014). Energy importing countries are also naturally more willing to import energy, such as natural gas (Zhang et al., 2018) and oil (Gupta, 2008), from regions with stable political situation. Geopolitical risks can also affect energy trade in dimensions other than supply and demand, such as impeding energy transport, weakening energy investment and making energy prices fluctuate significantly (Le Coq and Paltseva, 2009; Lee et al., 2017; Duan et al., 2018; Pena, 2020; Sukharev, 2020; Xie et al., 2020). In addition, there are many studies from the perspective of supply chain, sustainable development and renewable energy (Ilic et al., 2019; Kemfert and Schmalz, 2019; Pant et al., 2020).

Although Frontier countries are generally regarded as the leading players in the energy market (Simonia and Torkunov, 2016; Li T. et al., 2020), in fact, geopolitics has a more significant impact on the energy market of emerging economies. The “Three Seas Initiative” composed of some EU member countries is currently making efforts to reduce their dependence on natural gas from Russia and Ukraine (Kurecic, 2018); Oral and Ozdemir believe that under the current geopolitical background, Turkey should strive to become the center of global energy trade, because 70% of the world’s oil and gas reserves and consumption take place around it (Oral and Ozdemir, 2017). When geopolitical factors drive oil prices beyond realistic levels, Brazil should seize the opportunity to use shale oil as an important strategic resource (dos Santos and Lara dos Santos Matai, 2010); The Korean Peninsula should make strategic use of its own geopolitics to connect the Eurasian continent energy transportation and achieve prosperity through economic cooperation with the United States, China, Japan and Russia (Duk, 2018); China’s energy market is far from mature, and energy risks bring great fluctuations to the price of China’s energy asset market (Li, 2010). The tense geopolitical relationship between the United States and China has brought a huge impact on the world energy and trade markets (Iqbal et al., 2019; Qiu et al., 2019; Liu, 2020). Tunsjo puts forward new perspective on China’s strategy of acquiring energy resources in Sudan and Iran as well as the importance of China’s state-owned oil tanker fleet in China’s energy security policy by drawing lessons from hedging and risk management (Tunsjo, 2010); Oil is the main reason for United States intervention in the Middle East (Checkovich, 2005; Harvey, 2008). In the last 2 decades, the security situation and political stability in the Middle East has significantly worsened, in contrast with its strategic importance as the global economy’s energy engine (Baltar Rodríguez, 2021). Generally speaking, in the past, the energy related research of emerging economies in the geopolitical environment is seriously insufficient. Geopolitics and energy are hot topics in their respective fields, but there is a lack of sufficient interactive research. The empirical analysis of this paper is in the hope to fill the research gap of the impact of geopolitical events on energy trade of emerging economies.

The above studies provided reference experience and new ideas for this research.

The main work and marginal contributions of this paper are as follows: The heterogeneity of the impact of different types of geopolitical events on the energy trade of emerging economies is studied. Based on the monthly data of 17 sample emerging economies from 2000 to 2020, this paper employs the regression discontinuity design (RDD) model to analyze the changes in energy trade of emerging economies before and after 15 geopolitical events. The empirical findings of this paper show: 1) The impact of different types of geopolitical events on energy trade in emerging economies is heterogeneous. First, war and conflict events lead to an increase in energy trade. Second, terrorist attacks have no significant impact on energy trade. Third, international tensions lead to a decline in energy trade. Therefore, economies should respond to different types of geopolitical events in corresponding measures. 2) Through a comprehensive analysis of empirical results and facts, it is found that there is a complex relationship between geopolitical events and energy trade in emerging economies. First, the impact of geopolitical events on emerging economies’ energy trade is concentrated on the demand side, that is, the impact is concentrated in the energy importing countries. Second, energy demand in emerging economies is highly inelastic. This is reflected in the fact that energy trade basically keeps in line with the fluctuation direction of energy prices. Finally, fluctuations in energy trade are not entirely controlled by geopolitical events. Factors such as key technological innovations also influence energy markets. For example, the shale oil revolution in the United States fully covers the impact of the dangerous situation in the Middle East on energy trade.

When geopolitical risks occur, emerging economies will make discretionary choices in energy import and export according to the degree of correlation between energy trade and their own interests. Emerging economies are relatively independent decision-making units. Different emerging economies have different responses to the same type of geopolitical events, and the responses of the same emerging economy to different types of geopolitical events are also different. Therefore, the impact of rising geopolitical risks caused by different geopolitical events on the energy trade of emerging economies must be heterogeneous. Based on this, this paper puts forward the first preliminary hypothesis:

H1: The impacts of geopolitical events on the energy trade of emerging economies are heterogeneous.

Although the causes are complex and the related parties are full of contradictions, geopolitical events can be classified from the surface. For the convenience of analysis, geopolitical events are simply divided into wars and conflicts, terrorist attacks and international tensions. Among them, wars and conflicts are accompanied by violent confrontation, which has a greater impact. Wars and Conflicts is an intense armed conflict between states, governments, societies, or paramilitary groups such as mercenaries, insurgents, and militias. It is generally characterized by extreme violence, aggression, destruction, and mortality, using regular or irregular military forces. In the past 2 decades, wars and conflicts are mainly concentrated in the Middle East region with rich energy reserves, which is bound to hinder energy output and trade. Based on this analysis, this paper puts forward the following hypothesis:

H2: Wars and conflicts have a restraining effect on the energy trade of emerging economies.

Terrorist attacks have caused heavy damage to the victim countries and regions, but they are usually small in scale and the actual international losses are not high. Terrorist attack is a kind of attack made by extremists against but not limited to civilians and civilian facilities, which is not in line with international morality. Since 1990s, terrorist attacks have been spreading rapidly all over the world. Terrorist attacks are hard to define. Even within the United States, the definitions used by the Department of defense, the FBI, and the State Department are different. Outside the United States, the United Nations and different countries define terrorist attacks in their own way. But on the whole, terrorist attacks are less influential than wars and conflicts, and it is difficult to directly affect the energy level of a country. Therefore, this paper proposes the third hypothesis:

H3: Terrorist attacks have no obvious impact on the energy trade of emerging economies.

International tension is a conflict between countries and regions that is not reflected by the war situation, but its adverse impact is not necessarily smaller than the direct war conflict. The current international situation and the level of weapons have caused conflicts between major powers to hardly erupt in the form of war. Therefore, conflicts are often manifested in tense international situations, which can hinder energy trade between countries, and even cause trade barriers, sanctions and vicious tariffs. At the same time, international tensions can also hit a country’s production and weaken energy consumption. Therefore, this paper puts forward the final hypothesis:

H4: International tensions inhibit the energy trade of emerging economies.

This paper uses the RDD model to test the impact of specific political events on the energy import and export volume of emerging economies and analyze the heterogeneity. The RDD is second only to random experiment and can effectively analyze the causal relationship between event occurrence and energy import and export volume by using realistic constraint conditions. When the random experiment is not available, RDD can avoid the endogenous problem of parameter estimation in the analysis of specific political events, so as to truly reflect the causal relationship between the rise of geopolitical risks (GPR) caused by political events and the energy import and export volume of emerging economies, and can use the jump effect of political events to estimate the causal relationship between them. In this paper, the validity of the RDD analysis is illustrated in the robustness test part. It should be noted that the experimental group of RDD is all the samples after the breakpoint (right), and the control group is all the samples before the breakpoint (left). The date of the experiment is the month in which the event happened. According to formula (1), in this paper, the months before the event happened is the control group, and the event after the months is the experimental group. The sample size of all empirical studies in this paper is 4,009, which will not be reported in the table. The accuracy of the RDD results is affected by the model setting, of which the bandwidth is the key. As for the selection of the bandwidth, the IK method (Imbens and Kalyanaraman, 2012) is used to calculate the Optimal Bandwidth (OB). It is worth mentioning that the optimal bandwidth in this section is 5–7 months, which can represent the short term and is represented by OB. The 2 times optimal bandwidth is about 10–14 months, which can represent the medium and long term and is represented by 2*OB. According to the research of Lee and Lemieux (2010), the following model is constructed:

where i represents individual economy and t is time; Eventit is the processing variable, that is, when the time t is after the event, the value is 1, otherwise it is 0; Yit is the execution variable, that is, the difference between t and the occurrence time of the event; X is a covariate, including GDP, interest rate and exchange rate; πi represents individual fixed effect; εit is the error term; λ1 represents the impact of the event on the volume of energy import and export, which is the main concern of this paper. This model is used in the regression of this section and will not be repeated later.

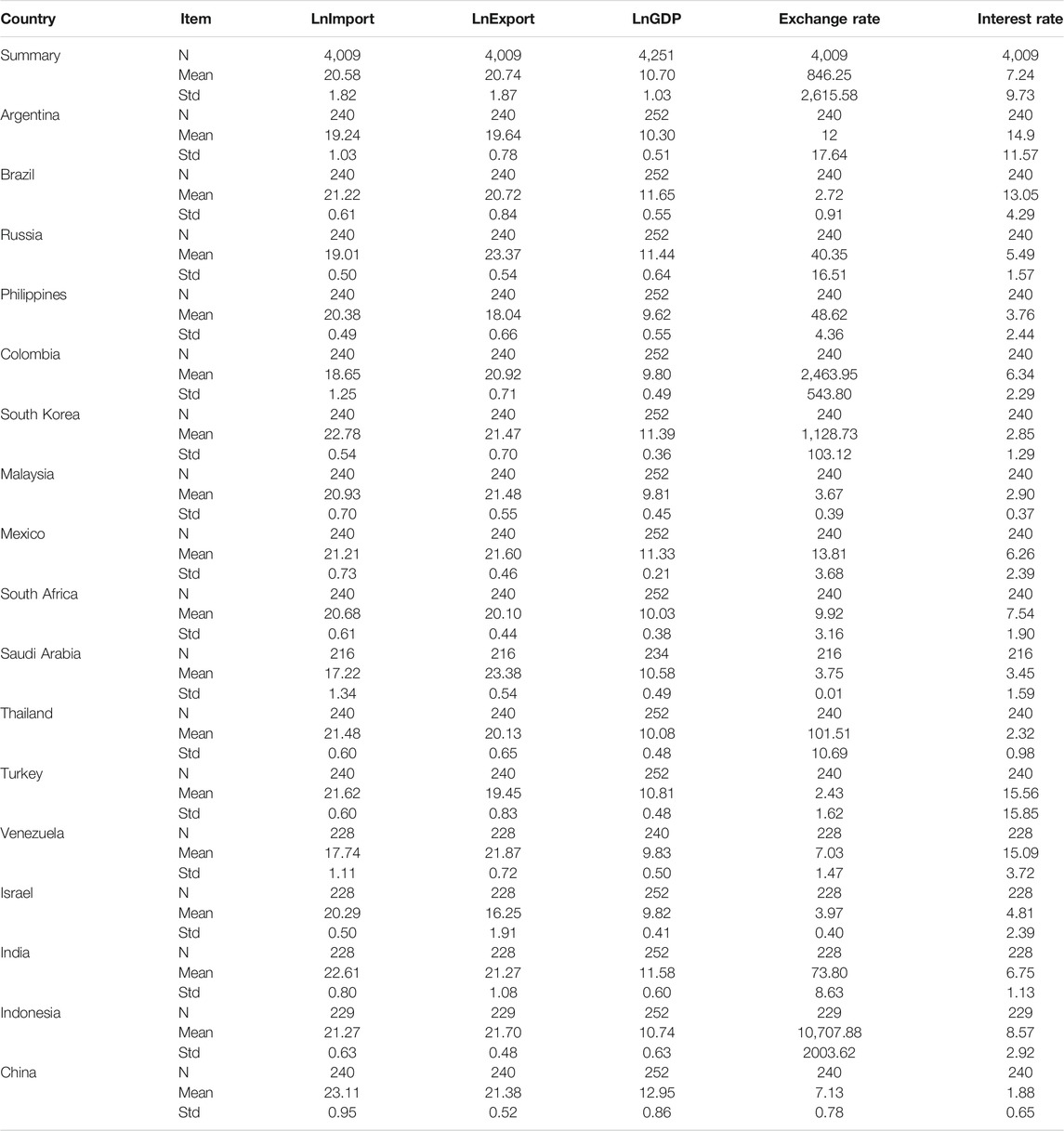

This paper selects 17 emerging economies as the initial research samples. Based on the purpose of this research and the availability of data, this paper includes monthly panel data from January 2000 to December 2020, and makes the analysis from the time dimension of the month. The dependent variable of this paper is the energy trade volume. The data of energy imports and exports (USD) are derived from the 27th category of Harmonized Commodity Description and Coding System (HS) of the International Trade Centre, including coal, coke and coal brick, petroleum, petroleum products and related raw materials, natural gas and man-made gas and electric current, and can represent the overall energy import and export level of the economy (Yang et al., 2021). The GPR Index originally provides the geopolitical risk indexes of 19 emerging economies (Caldara and Iacoviello, 2019), but the monthly data of energy trade of Ukraine and Hong Kong are seriously missing, so this paper only selects 17 emerging economies (see Table 1). The control variables include GDP, exchange rate and interest rate. The monthly GDP of each economy is obtained from its quarterly GDP (million USD, source: World Bank) through frequency conversion, which does not change its variation trend; data of the current exchange rate and interest rate of each economy are from the Wind database. In most studies, the index of trade volume is logarithmic, because the trade volume gap between economies is generally large, and the discrete trend of data is very strong. The purpose of logarithm is to slow down the fluctuation trend of data and alleviate the heteroscedasticity. According to the standard practice, this paper adopts the logarithmic processing for trade volume and GDP data. Table 1 reports the descriptive statistical results of relevant variables.

TABLE 1. Descriptive Statistics for dependent and control variables.

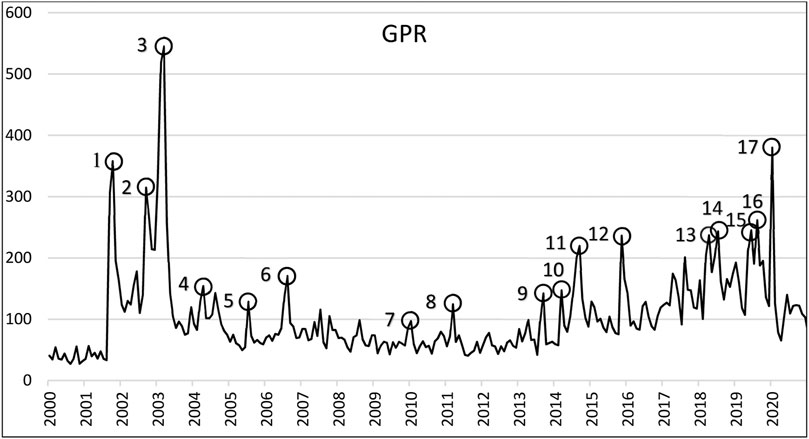

The independent variable in this paper is the Geopolitical Risk Index, GPR index, which was proposed by Caldara and Iacoviello. By analyzing newspaper articles in a specific period, it comprehensively quantifies the geopolitical risks of 19 emerging economies and the whole. Monthly data covering the period January 1985 to April 2021 are currently available (Caldara and Iacoviello, 2019). The rise of GPR is often closely related to the occurrence of specific political events. Figure 1 shows the trend of global GPR index since January 2000. It can be found that the GPR index shows great jumps at specific time points such as the 9/11 and the Iraq War. Although the occurrence of different types of events will lead to the rise of GPR, the impact on specific targets such as energy trade is bound to be heterogeneous. The task of this paper is to analyze this heterogeneity (Li Z. et al., 2020; Li and Liao, 2020; Li T. et al., 2021; Li Z. et al., 2021).

FIGURE 1. GPR Trend line.

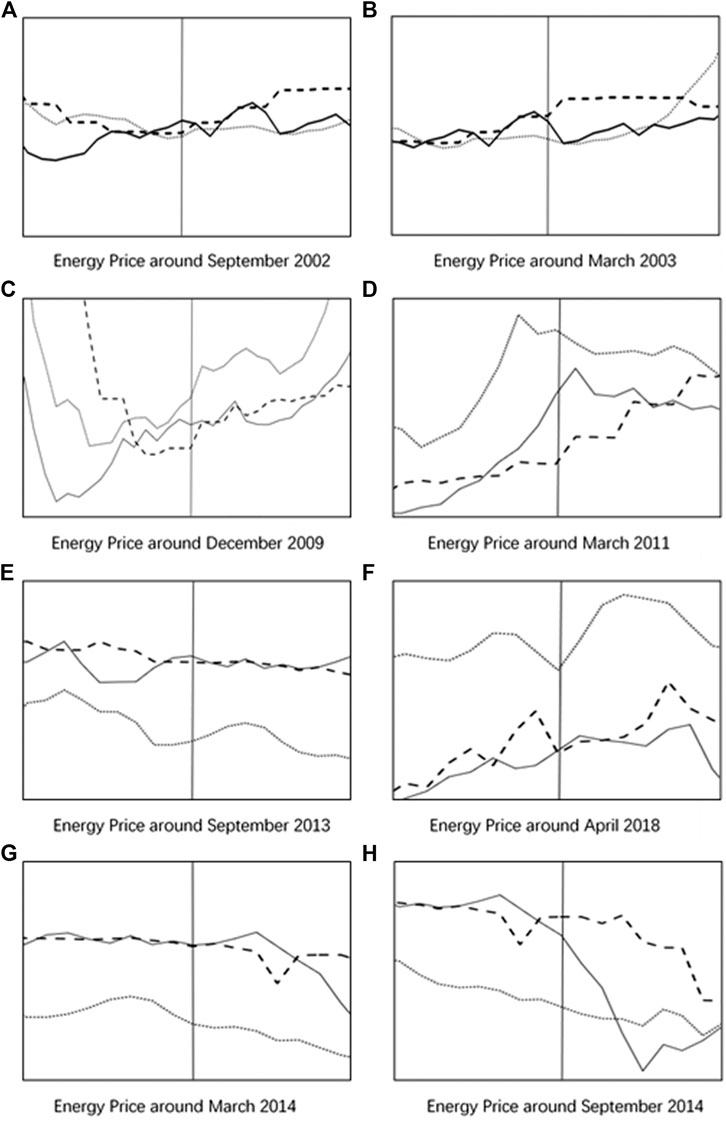

As can be seen from Figure 1, there are a certain number of “peaks” in the trend line of GPR. Combined with the historical facts of time, GPR index makers believe that geopolitical risk increases significantly in the following events: ①9/11 Attacks (September 2001) ②Fear of Iraq war (September 2002) ③Iraq Invasion (March 2003) ④Madrid bombings (March 2004) ⑤London bombings (July 2005) ⑥2006 transatlantic aircraft plot (August 2006) ⑦Obama announces surge Afghanistan (December 2009) ⑧Arab Spring: Syrian and Lybian War (March 2011) ⑨Syria war escalation (September 2013) ⑩Russia annexes Crimea (March 2014) ⑪ISIS escalation (September 2014) ⑫Paris Attacks (November 2015) ⑬Syrian tensions (April 2018) ⑭U.S.-Iran tensions (July 2018) ⑮U.S.-Iran tensions escalation (June 2019) ⑯U.S.-China tensions (August 2019) ⑰COVID-19 Outbreak (January 2020). In order to facilitate the consideration of the heterogeneity of the event impact, this paper divides the events into three categories according to their forms, namely Wars and Conflicts, Terrorist Attacks and Tension in International Relations. The above three groups of events will be analyzed in the following paper. Table 2 shows the grouping of different events.

TABLE 2. Classification of geopolitical events.

War and Conflicts is an intense armed conflict between states, governments, societies, or paramilitary groups such as mercenaries, insurgents, and militias. It is generally characterized by extreme violence, aggression, destruction, and mortality, using regular or irregular military forces.

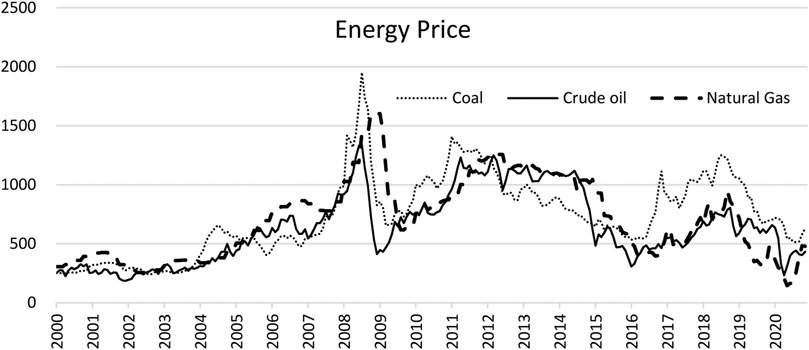

Previous studies have proved that energy prices play a mediating role in the impact of geopolitics on energy trade (Li F. et al., 2021). Therefore, when analyzing the impact of specific events, this section also considers the energy price factor and the elasticity of supply and demand. Due to the limitation of the RDD model, only words are used to supplement the role of energy price in the impact. In this paper, the monthly FOB price of steam coal spot in Newcastle and Kembla Port of Australia is selected to represent the overall coal price (USD/T), and the monthly FOB price of Brent crude oil spot in Britain is selected to represent the overall crude oil price (USD/barrel). The monthly FOB price of Russian produced natural gas from German port is selected to represent the overall natural gas price (USD/100 million standard British thermal units). The monthly trend is shown in Figure 2. It can be found that the three major energy price trends are basically consistent.

FIGURE 2. Energy Price Trend line.

The data processing is completed by SPSS24.0 and STATA16. The frequency conversion of GDP is completed by Eviews11, and the graphs are made by Excel.

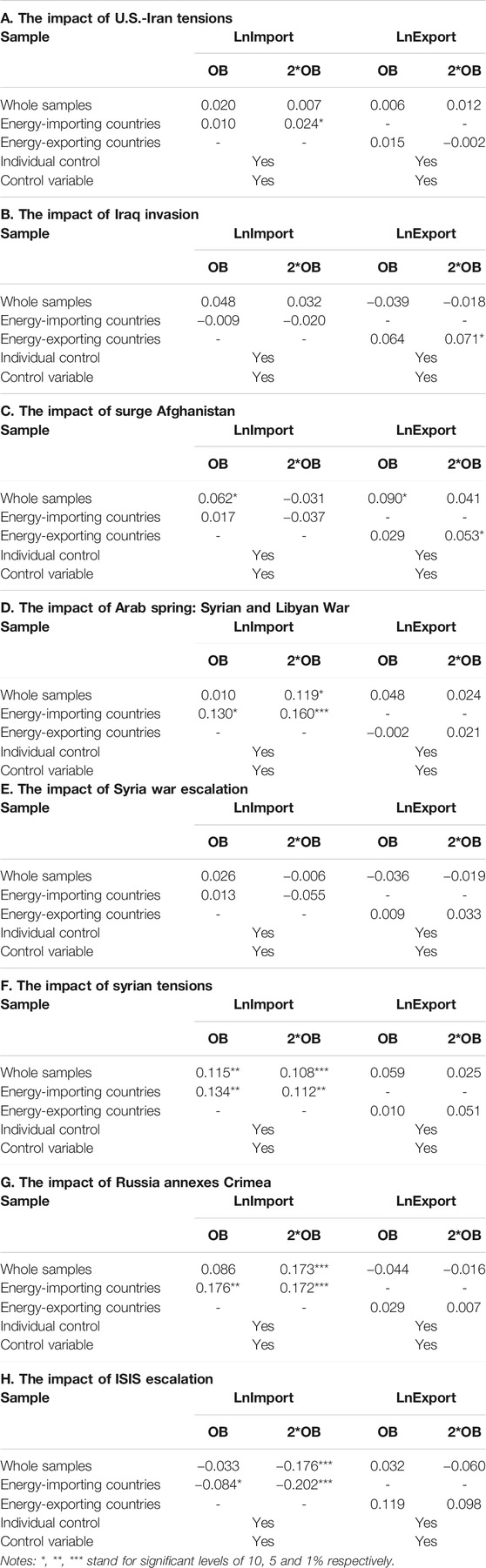

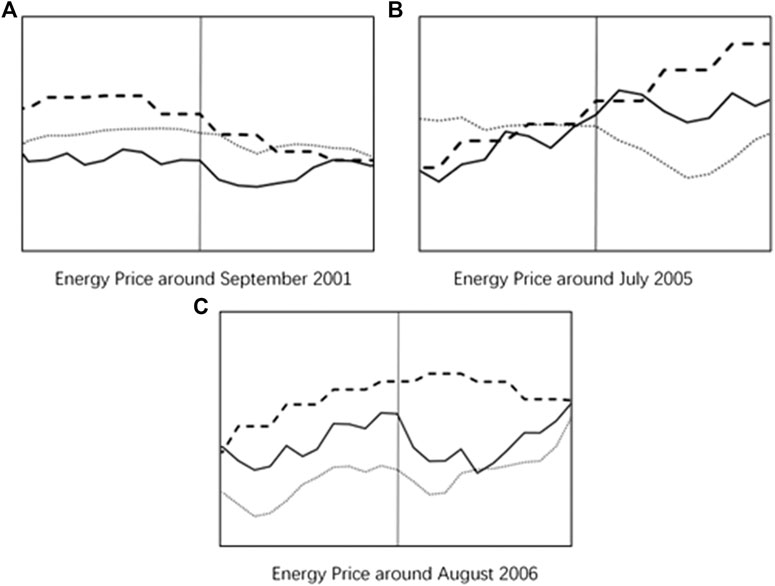

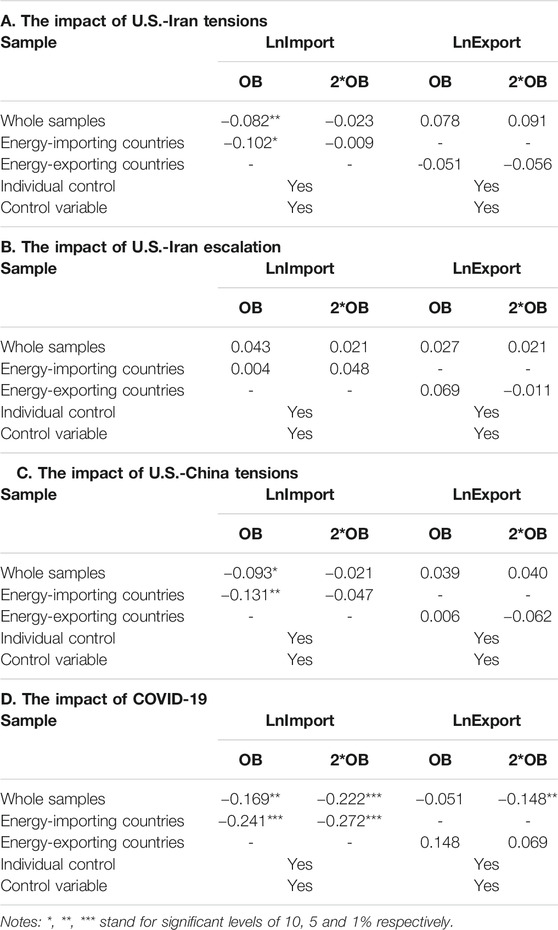

After the September 11 attacks, the Bush administration’s national security team actively discussed the invasion of Iraq. President Bush began laying the public groundwork for invading Iraq in his January 2002 State of the Union address, calling Iraq a member of an axis of evil and saying, “The United States of America will not allow the world’s most dangerous regime to threaten us with the world’s most destructive weapons.” In his speech to the UN Security Council in September 2002, he began to formally put forward the reasons for invading Iraq to the international community; In October 2002, Congress authorized President George W. Bush to decide whether to launch a military strike against Iraq. On March 20th, 2003, the joint forces led by the United States and Britain launched a military operation against Iraq. The United States, on the grounds that Iraq hid weapons of mass destruction and secretly supported terrorists, bypassed the UN Security Council and carried out a unilateral military attack against Iraq. The international community considers the Iraq War as the continuation of the Gulf War, also known as the second Gulf War. It took more than 7 years for the U.S. combat forces to withdraw from Iraq. On December 18th, 2011, all US forces withdrew. The events related to this section are ②Fear of Iraq War (September 2002) ③Iraq Invasion (March 2003) In this paper, a Sharp Regression Discontinuity (SRD) analysis is conducted for the two events to analyze the heterogeneity of the impacts of the events on the whole sample, as well as energy importing countries and energy exporting countries before and after the events (Hongwei et al., 2021). Tables 3A,B report the results of the SRD, and Figures 3A,B report the energy price changes before and after the events.

TABLE 3. The impact of Wars and Conflicts.

FIGURE 3. Energy price around wars and conflicts.

As can be seen from Table 3A, the impact of the Fear of Iraq War on the energy trade of emerging economies is only reflected in the increase of energy import volume of energy importing countries in the medium and long terms. The Fear of Iraq war is mainly a pre-war campaign, and its impact on world energy trade is limited, and the result of the increase in imports of energy importing countries may be due to a long term of slow increase in energy prices. Iraq was then the world’s largest oil producer with 112.5 billion barrels of proven reserves, ranking second in the world. At the same time, the drilling rate of its oil resources was only 23%, and only 17 of the 80 large oil fields discovered were developed. The oil potential was huge. The Fear of Iraq war raised the price of crude oil to a certain extent, which directly led to the increase of energy trade volume.

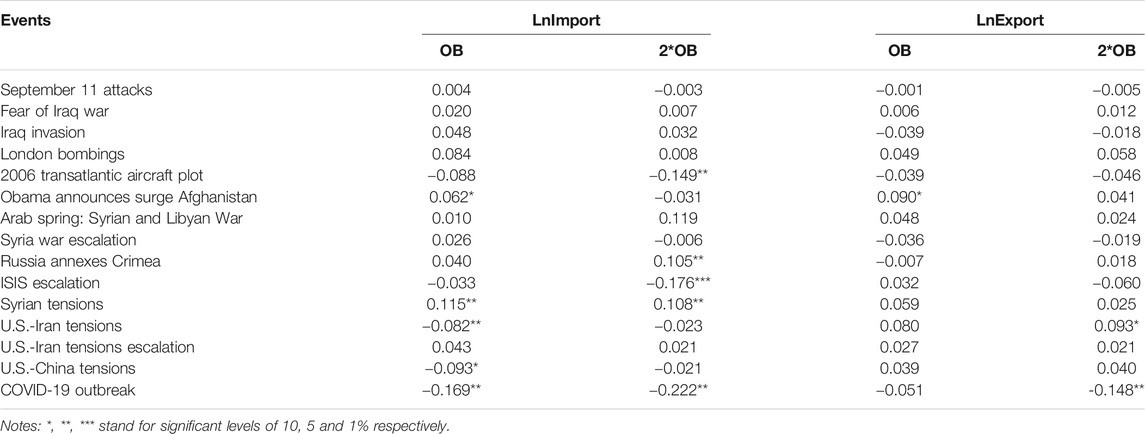

It can be seen from Table 3B that the impact of the Iraq Invasion on the energy trade of emerging economies is reflected in the increase of energy export volume in energy exporting countries in the medium and long term. After the Iraq war, it was expected that the world oil market would stabilize with the rapid victory of the United States military in the Iraq war and the control of the situation. However, since the beginning of 2004, the world oil price has been climbing all the way, from $30 a barrel in January to $55 a barrel in October. Take China as an example, in 2004, China spent 40 billion US dollars for importing oil. More than 8-billion-USD additional expenditure is spent due to the price rise alone. Therefore, it can be concluded that the increase of energy export volume is due to the significant rise of energy prices, and the demand elasticity of energy exports is small.

On the evening of December 1, 2009, UnitesStates President Barack Obama delivered a national television speech at West Point, officially announcing the specific plan of increasing troops in Afghanistan. Under the plan, the United States military would send 30,000 additional troops to Afghanistan in phases, bringing the total to more than 100,000 troops by the first half of 2010. At the same time, the United States also requested other NATO allies to send at least 7,000 to 10,000 more troops to Afghanistan to make up for the gap between the actual number of US troops and the needs of the front line. This paper uses RDD to analyze the heterogeneity of the whole sample, energy importing countries and energy exporting countries before and after the event. Table 3C reports the results, and Figure 3C reports the changes in energy prices before and after the event.

As can be seen from Table 3C, the surge of American troops in Afghanistan has increased the overall energy import and export volume of emerging economies in the short term, and the export volume of energy exporting countries in the medium and long term. The surge of American troops in Afghanistan has brought instability to central Asia to a certain extent, which is reflected in the direct military action in Afghanistan and the radiation effect on neighboring countries (such as Kazakhstan, Kyrgyzstan, etc.). The instability in energy-producing countries usually leads to the shortage of energy and the rise of energy prices. In Figure 3C, it can be observed that the prices of the three major energy sources increase significantly in the short and medium term, which is the direct reason for the significant increase of energy import and export volume in emerging economies. The supply and demand of energy in emerging economies shows a weak elasticity here (Lin and Liu, 2010; Labandeira et al., 2017).

The Arab Spring is a wave of revolutions in the Arab world, the civil war in Syria and the war in Libya being the main parts. The Syrian civil war usually refers to the conflict between the Syrian government and the Syrian opposition groups and the Islamic State since the beginning of 2011. The anti-government demonstrations in Syria started on January 26, 2011 and escalated on March 15, 2011, evolving into armed conflicts. The Libyan War is an armed conflict that occurred in Libya in 2011, often referred to as the “February 17 Revolution” in Libya. The fighting between the government of Muammar Gaddafi and the forces against Gaddafi. On the energy level, the biggest impact of the Arab Spring revolts is on Libya, whose crude oil production took a year to recover to normal levels: According to OPEC, before January 2011, Libya’s crude oil production was 1,600 thousand barrels per day, but after February, its crude oil production plummeted, reaching 375 thousand barrels per day in March; In July, however, its crude oil production bottomed out at 7,000 barrels per day; until May 2012, its crude oil production returned to 1,441,000 barrels per day. On April 14, 2018, the United States, Britain and France launched air strikes in Syria. The events related to this section are:⑧Arab Spring: Syrian and Libyan War (March 2011) ⑨Syria war escalation (September 2013) ⑬Syrian tensions (April 2018). This paper uses SRD to analyze the heterogeneity of the whole sample, energy importing countries and energy exporting countries before and after the events. Tables 3D–F report the results, and Figure 3D–F- 3(f) report the changes in energy prices before and after the events.

It can be seen from Table 3D that the outbreak of wars in Syria and Libya increased the energy import volume of energy importing countries in the short term, and increased the energy import volume of the whole sample and energy importing countries in the long term. From Figure 3D, we can see that world energy prices have risen sharply throughout the Arab Spring, with crude oil prices not peaking until May and coal prices continuing to climb. The rise of energy price in the short term is the direct cause of the increase of energy import volume of energy importing countries in the short term. In the medium and long term, energy prices continued to rise during the turmoil in the Middle East and remained there for a long time after reaching the peak in May, which directly led to a significant increase in energy import volume in the medium and long term. Energy demand in emerging economies shows weak elasticity.

According to Table 3E, it can be seen that the impact of the escalation of the Syrian war on the energy trade of emerging economies is not significant in the short and medium to long term. The turmoil in the Middle East has lasted for a long time, and the neighboring countries have gradually adapted to the political environment; meanwhile, although Syria is located in the Middle East, it is not an oil producing country, and its turbulence has not affected the energy supply in the Middle East. According to Figure 3E, the fluctuation of energy price tends to be flat at this time.

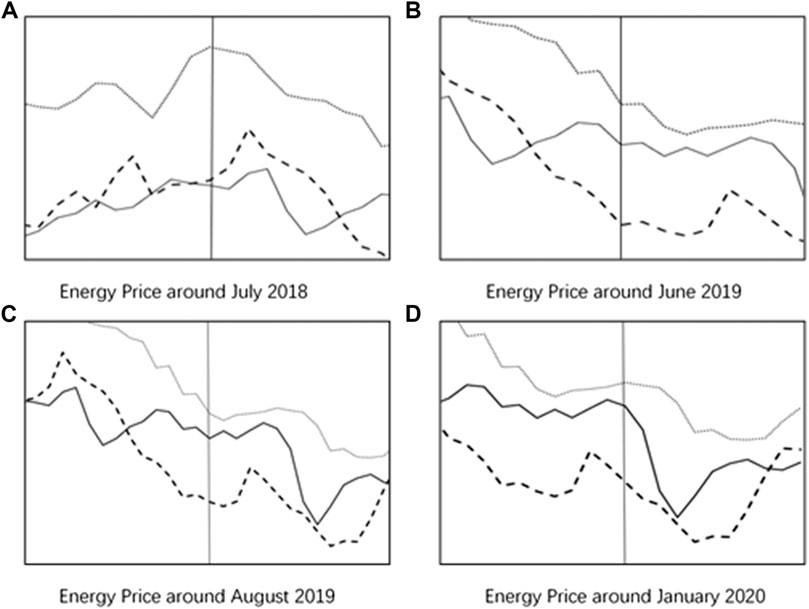

According to Table 3F, the tensions in Syria in 2018 significantly increased the energy import volume of the whole sample and energy importing countries in the short term as well as in the medium to long term, and also increased the energy exports volume to a certain extent. By observing Figure 3F, we can see that energy prices continue to rise in the medium and long term until the peak in October 2018. The price rise directly leads to the short-term and medium and long-term increase of energy imports. Although the price plummeted after October, it did not change the jumping trend of energy imports before and after the discontinuity. Once again, energy demand in emerging economies shows weak elasticity.

The Russian annexation of Crimea usually refers to the annexation of the Ukrainian Autonomous Republic of Crimea into the Russian Federation in March 2014. Since the annexation on March 18, 2014, Russia has in fact taken over the territory and established the Crimean Federal District, under which there are two federal subjects, namely, the Republic of Crimea and Sevastopol. In this paper, the SRD analysis is performed to analyze the heterogeneity of the impacts on the whole sample, energy importing countries and energy exporting countries before and after the event. Table 3G reports the results and Figure 3G reports the energy price changes before and after the event.

It can be seen from Table 3G that Russia’s annexation of Crimea increased the import volume of energy importing countries in the short term as well as the import volume of the whole sample and energy importing countries in the medium and long term. The long-term and sustained rise in crude oil prices can explain the increase in imports of energy importing countries. Meanwhile, the energy demand brought by the strong development of emerging economies, such as China, can also explain the increase in imports to some extent. The first half of 2014 was marked by a series of geopolitical events that rattled markets: the crisis in Syria, the unrest in Iraq, and strikes in Libya, which continued to drive up energy prices. From this point of view, the upward jump in energy trade imports around March also came from the increase in energy prices, and demand shows weak elasticity.

In 2014, ISIS troops battled Iraqi government forces and quickly seized control of several areas of Iraq. On June 28, the group’s leader, Abu Bakr al-Baghdadi, declared himself the caliphate, renamed the regime the Islamic State, and claimed authority over the entire Muslim world, including areas historically ruled by the Arab empire. In September, the United States formed an international alliance of 54 countries, including Britain and France, as well as regional organizations such as the European Union, NATO and the Arab League, to fight IS. We adopt SRD to analyze the heterogeneity of the impacts on the whole sample, energy importing countries and energy exporting countries before and after the event. Table 3H reports the results and Figure 3H reports the energy price changes before and after the event.

According to Table 3H, energy import volume decreased in the medium and long term before and after ISIS upgrading, and the energy import volume of importing countries also decreased significantly in the short term. Figure 3H shows that crude oil price has plummeted at this point. The main reasons for the collapse include: the rapid growth of production due to the technological revolution of shale oil in the United States; while OPEC refused to reduce production and chose to increase production in an attempt to squeeze out shale oil from the market besides, the United States lifted economic sanctions on Iran, which led to loose global demand and a large accumulation of crude oil dominant inventory. The decline of the import volume is directly related to the decline of energy prices, which proves that the energy demand of emerging economies is lack of elasticity. Meanwhile, in 2014, the global economy slowed down, the global crude oil demand growth fell to the lowest in 5 years, and the annual global oil demand only increased 700,000 barrels per day, which is the lowest level since the 2008 financial crisis, leading to a long-term significant decline in energy imports. In general, ISIS upgrading does not have a significant impact on energy trade at the discontinuity. At this time, the energy market is more affected by the United States shale oil technology revolution, which indicates that energy trade is not completely controlled by geopolitical risks, especially when more important events occur. Meanwhile, emerging economies have not taken the opportunity to increase their efforts to buy energy with lower prices, which is another example of the weak elasticity of energy demand.

The 9/11 Attack is a series of suicide terrorist attacks on the United States on September 11, 2001. Al-Qaeda claimed responsibility for the attacks, which killed at least 2,996 people. The event has a significant impact on the world economy and the US economy. Many large companies located in the World Trade Center lost a lot of property, employees and data. Many stock markets around the world have been affected, and some, such as the London Stock Exchange, had to evacuate. The New York Stock Exchange did not reopen until the first Monday after 9/11. The Dow Jones Industrial Average fell 14.26% on the first day of trading. This paper employs the RDD to analyze the heterogeneity of the whole sample, energy importing countries and energy exporting countries before and after the event. Table 4A reports the results and Figure 4A reports the changes in energy prices before and after the event.

TABLE 4. The impact of Terrorist Attacks.

FIGURE 4. Energy price around terrorist attacks.

As can be seen from Table 4A, the 9/11 terrorist attacks have almost no impact on the energy trade of emerging economies. Figure 4A shows that there is no obvious change in energy prices before and after the event. It can be seen that although the 9/11 terrorist attack caused serious economic losses to the United States and even the world, it did not affect the global energy market. The worst terrorist attack in history did not affect the trade volume of energy, so we can conclude that terrorist attacks will not directly affect the energy market.

The London bombings refer to at least seven bombings in London in the morning rush hour on July 7, 2005. Several London subway stations and buses were exploded, killing 56 people (including four bombers) and injuring more than 100. The British government and Prime Minister Anthony Charles Lynton Blair identified the event as a terrorist attack. The explosion occurred less than a day after London won the bid to host the 2012 Summer Olympic Games, while the G8 summit in Scotland was under way. After the incident, in 2018, all subways were closed, buses in the city center were shut down, and airports were still operating normally. Although the local communication network in London were operating normally, some communication had been restricted due to signal congestion. Two weeks later, i.e., on July 21, there were three more attacks on different subway stations in London, and a bus No. 26 in motion was suspected of being shot. This paper uses SRD to analyze the heterogeneity of the impacts on the whole sample, energy importing countries and energy exporting countries before and after the event. Table 4B reports the results and Figure 4B reports the changes in energy prices before and after the event.

As can be seen from Table 4B, the London bombings have almost no impact on the energy trade of emerging economies. Figure 4B shows that the energy price has a certain insignificant rise before and after the discontinuity, which may be the reason for the positive coefficient in Table 4B, but it has little to do with the terrorist attack. Although the London bombings brought a certain loss and panic to the British society, they did not affect the global energy market, which once again proved that terrorist attacks have no direct impact on the energy market.

The 2006 Transatlantic aircraft terrorist plot refers to a plot in which terrorists were suspected of blowing up flights from Britain to the United States. On August 10, 2006, the London Police Department announced the arrest of the main people involved in the plot, all of whom were Islamists with British nationality. The authority said they immediately disrupted the plot because the plan was “approaching the execution stage”. According to United States intelligence officials, the suspects planned to rehearse the attack within 2 days after the arrest day. This part also uses SRD to analyze the heterogeneity of the impacts on the whole sample, energy importing countries and energy exporting countries before and after the event. Table 4C reports the results and Figure 4C reports the energy price changes before and after the event.

As can be seen from Table 4C, energy imports show a decline in the medium and long term. But in reality, there is no obvious connection between the energy market and the Transatlantic Aircraft Plot at this time. In early 2006, the Iranian nuclear issue gradually escalated, which promoted the continuous rise of energy prices. Crude oil rose from $64 at the beginning of the year to $80 at the peak in July. Due to high inventory and economic slowdown, crude oil prices continued to decline after that. The turning point of energy prices in August coincides with the time point of the Transatlantic Aircraft Plot. Combined with Figure 4C, it can be seen that the decrease in import volume is mainly due to the decrease in energy price, which is not closely related to terrorist attacks. Similarly, energy demand shows a lack of elasticity here.

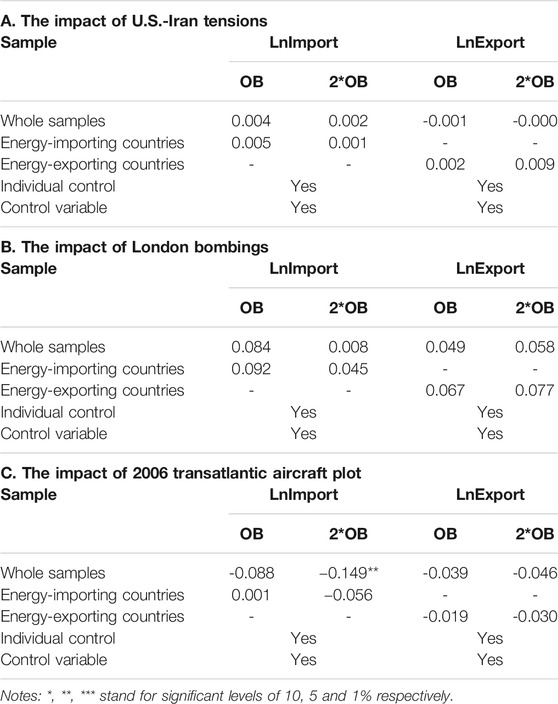

The US administration unilaterally withdrew from the Joint Comprehensive Plan of Action (JCPOA) in May 2018, and subsequently restarted and added a series of sanctions against Iran in August and November. Iran’s Revolutionary Guards shoot down an RQ-4 “Global Hawk” drone in the southern Iranian province of Hormuzgan, near the Strait of Hormuz, on June 20, 2019. Iran has significant oil and gas reserves. The events related to this section are: ⑭U.S.-Iran tensions (July 2018) ⑮U.S.-Iran tensions escalation (June 2019). This paper conducts SRD for the two events to analyze the heterogeneity of the impacts of the events on the whole sample, energy importing countries and energy exporting countries before and after the events. Tables 5A,B report the results and Figures 5A,B report the energy price changes before and after the events.

TABLE 5. The impact of Tension in International Relations.

FIGURE 5. Energy price around tension in international relations.

As can be seen from Table 5A, the impact of the tension between the United States and Iran on energy trade is reflected in the short-term reduction of the overall energy import volume and that of the importing countries. It can be found from Figure 5A that energy prices at this time declined significantly. The reason for the sharp drop of crude oil prices is that major oil producing countries have increased production to cope with the supply gap brought about by US sanctions against Iran. Saudi Arabia’s production reached 10.7 million barrels per day at the end of 2018, while US shale oil production rose all the way to 8.13 million barrels per day in October. The EIA report predicts that the US crude oil production in 2019 will exceed 12 million barrels per day, and the commercial inventory of crude oil disclosed in the EIA report in late November has increased for ten consecutive years. However, the pace of US sanctions against Iran is lower than expected, resulting in oversupply and price drop. The short-term collapse of energy prices directly leads to the decline of energy imports in the short term, where energy demand shows a lack of elasticity.

As can be seen from Table 5B, the impact of the upgrading of us Iran relations on energy trade is not significant. In 2018, the tension between the United States and Iran has caused a big blow to the global energy market which continues to be depressed for a while, making the energy trade of emerging economies forms a certain adaptability. So the upgrading of the U.S. - Iran relationship has not brought a big impact. As can be seen from Figure 5B, the prices of major energy sources also tend to be stable.

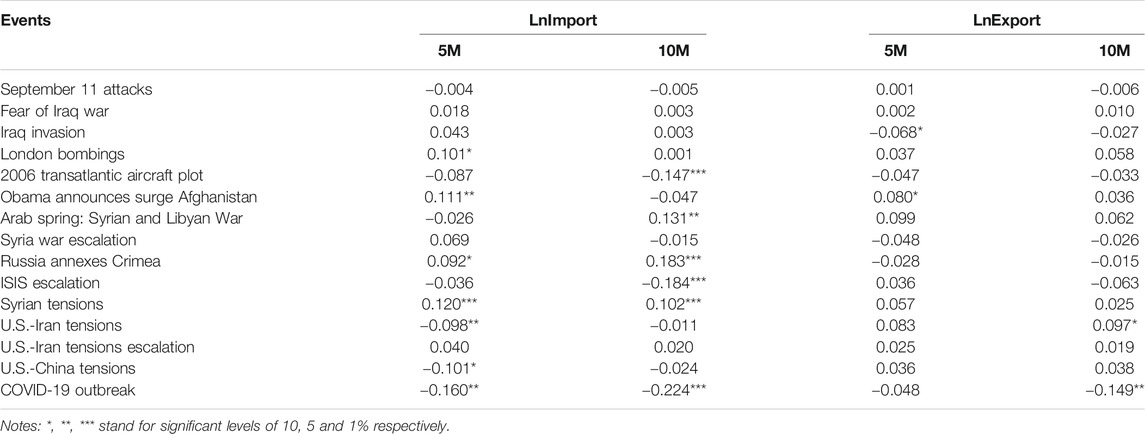

The U.S.-China trade war has attracted attentions from academics, policy makers, businesses and investors around the world (Iqbal et al., 2019; Qiu et al., 2019; Liu, 2020). On August 1, 2019, due to the Trump administration’s dissatisfaction with the Chinese government’s purchase process of US agricultural products, Trump announced on Twitter that he would impose a 10% tariff on all remaining $300 billion worth of Chinese imports to the US starting from September 1, 2019. On August 5, the Renminbi to the dollar fell below 7. On the same day, the US Treasury announced that China was listed as a currency manipulator. Subsequently, the Chinese government announced a suspension of the purchase of American agricultural products; on August 24, it announced additional tariffs of 10% or 5% on $75 billion worth of US goods and resumed additional tariffs on US cars and parts. The United States responded the next day by imposing a 15% tariff on $300 billion worth of Chinese goods and a 25–30% tariffs on $250 billion worth of Chinese goods, which was later shelved. This paper conducts SRD for this event to analyze the heterogeneity of the impact of the event on the whole sample, energy importing countries and energy exporting countries before and after the event. Table 5C reports the results and Figure 5C reports the energy price changes before and after the event.

As can be seen from Table 5C, the impact of United States-China tensions on energy trade is reflected in the short-term reduction of energy imports in the whole sample as well as in the energy importing countries. The world bank issued a report on October 29, 2019, saying that affected by the decline in demand caused by the weak global economic growth prospects, the prices of energy, metals and other commodities will “fall sharply” in 2019, as evidenced by the significant decline in energy prices in Figure 5C. John Yergin, chairman of Cambridge Energy Research Associates, once said that “at present, China’s demand growth is the fundamental driving force behind the world oil market”. Trade frictions between China and the United States have dampened China’s energy imports to some extent. Overall, the decline in prices and demand is the main reason for the short-term decline in energy imports. Demand for energy in emerging economies has also proved inelastic.

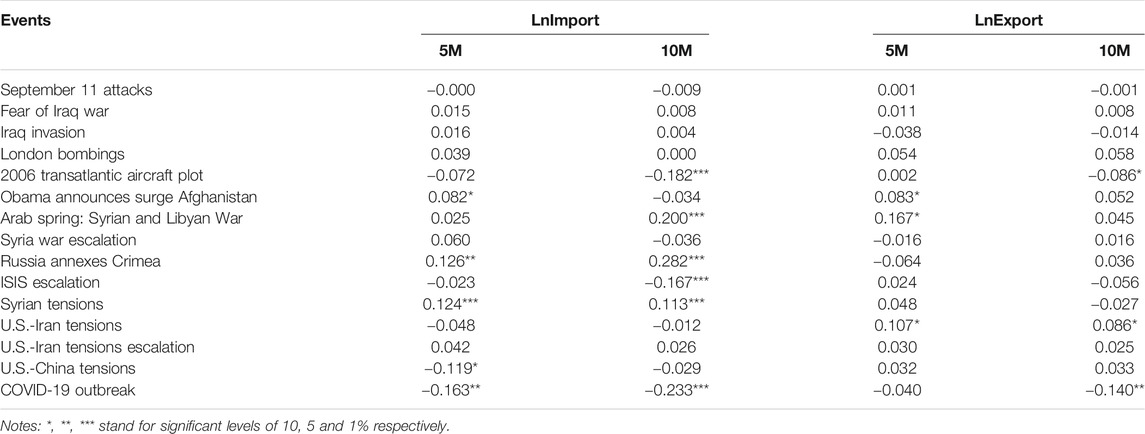

The first case of COVID-19 was detected in Wuhan, China, in December 2019. Since then, the disease has spread all over the world, leading to persistent pandemics and tensions in international trade cooperation, population movements, etc. According to the Annual Energy Outlook 2021 (AEO 2021) issued by the United States Energy Information Administration (EIA) on February 3, 2021, it may take several years for the United States to return to the energy consumption and carbon dioxide emission level in 2019 due to the impact of COVID-19 on the United States economy and the global energy sector. “It will take some time for the energy industry to reach a new normal,” said Stephen Nalley, EIA Acting Administrator. In 2020, the epidemic triggered a historic energy demand shock, leading to reductions in greenhouse gas emissions, reduced energy production and volatile commodity prices. The pace of economic recovery, technological advances, changes in trade flows and energy incentives will determine how the world produces and consumes energy in the future. This part also uses SRD to analyze the heterogeneity of the impact of the event on the whole sample, energy importing countries and energy exporting countries before and after the event. Table 5D reports the results of the regression and Figure 5D reports the energy price changes before and after the event.

As can be seen from Table 5D, the impact of COVID-19 on energy trade is reflected in the short and long term of suppressing the energy import volume of the whole and energy importing countries, while significantly inhibiting the overall energy export in the medium and long term. At the same time, it can be found from Figure 5D that the energy price falls sharply near the discontinuity point, which is the direct reason for the decrease of energy import and export volume in the short term. In addition, due to the obstacles of trade circulation caused by the epidemic and the uncertainty of the future of production activities, energy demand is bound to be lower than before the outbreak. Generally speaking, the sharp drop in price and demand together led to a significant decline in the volume of energy trade.

To sum up, it is found that there is indeed heterogeneity in the impact of geopolitical risks caused by specific political events on energy trade of emerging economies, which is reflected in the heterogeneity of political event types. 1) Wars and conflicts usually lead to an increase in energy trade volume. Wars and conflicts are usually large in scale and will bring about serious regional tension, which to a large extent leads to the shortage of energy supply and the rise of energy prices. 2) The impact of terrorist attacks on energy trade is not significant. Although terrorist attacks have a large negative effect on society, they are usually small in scale and have little impact on the real economy, so it is difficult to directly impact energy trade as well as supply and demand. 3) International tensions usually lead to a decline in energy trade volume. This is because international tensions are usually accompanied by trade frictions, sanctions by major powers and deterioration of the business environment, which has a direct negative impact on energy demand and is often accompanied by a decline in energy prices. Based on the above analysis, hypothesis H1, H3 and H4 are accepted and hypothesis H2 is rejected in this paper.

In addition, there are three other empirical findings in this paper. 1) The impact of geopolitical events on the energy trade of emerging economies is mainly concentrated on the demand side. Before and after the occurrence of geopolitical events, the energy supply is almost not affected, and the supply rigidity is strong. 2) Energy demand is seriously inelastic. By linking empirical results and energy price fluctuations, it can be found that energy trade volume almost completely rises (falls) with the rise (fall) of energy price. 3) The fluctuation of energy trade is not completely controlled by geopolitical events. Taking ISIS escalation as an example, the dangerous situation in the Middle East should affect the energy output and thus lead to the rise of energy prices, but the impact of the US shale oil technology revolution on the market completely covers the regional crisis situation. Technological progress has obviously had a significant impact on energy (Wang et al., 2021). This suggests that the impact of geopolitical risks on energy trade is likely to be fully offset when there is a greater impact of shocks.

The robustness of RDD is usually tested from the perspectives of validity, bandwidth selection, discontinuity point placebo, adjustment of dependent variables, and algorithm testing. In fact, the empirical study in this paper has already included the tests of bandwidth change, placebo and adjustment of dependent variables. Therefore, this section only carries out validity, algorithm and Bootstrap tests.

The validity of the RD estimate depends on two assumptions. First, the driving variables themselves are not manipulated. Since the processing variable in this paper is the month variable and the driving variable is the occurrence of geopolitical events, the month exists objectively and is not affected subjectively, so it meets the premise that the driving variable is not manipulated.

Secondly, the validity of RD estimation also depends on the smoothness assumption, that is, the control variables affecting the energy trade volume should not have obvious jump on both sides of the discontinuity point. Therefore, this paper also tests the continuity of the covariables of the RD model at the discontinuity point. The test results are shown in Table 6.

TABLE 6. Jumping information for each covariable at the discontinuity point.

As can be seen from Table 6, each covariable has no significant jump at each discontinuity point, which meets the premise requirements of the RDD smoothness hypothesis.

The estimation method of the discontinuity point will affect the RDD result. Previous section uses the default triangular kernel function estimation method of the RDD. In this section, Epanechnikov and Uniform estimation methods are used to infer regression results respectively. Tables 7 and 8 report the RD estimation results under the two algorithms. For the sake of space, only the regression results of the full sample are shown, and no distinction is made between energy exporting countries and importing countries. The short-term bandwidth is about 5 months, and the medium and long-term bandwidth is about 10 months, which is basically consistent with the previous benchmark regression.

TABLE 7. Robustness test for Epanechnikov.

TABLE 8. Robustness test for Uniform.

In the benchmark empirical study, the bandwidth is short and the number of samples involved in the regression is small. Based on this, Bootstrap sampling with put back is used to get more progressive and effective estimators. Based on the RDD model, this paper uses 2000 repeated sampling for regression coefficients. For the sake of space, only the regression results of the full sample are presented, and no distinction is made between energy exporting countries and importing countries. The regression results are shown in Table 9.

TABLE 9. Robustness test for Bootstrap.

As can be seen from Table 9, after repeated sampling, the impact of geopolitical events on energy trade is consistent with the benchmark regression, with only minor differences in significance. This indicates that the small sample size does not affect the validity of the empirical results, and the conclusion is still robust. Robustness test passed.

Based on the monthly data of 17 sample emerging economies from 2000 to 2020, this paper uses the GPR index to determine the position of geopolitical risk discontinuity points, and empirically analyzes the heterogeneity of the impact of 15 geopolitical events on energy trade by means of RDD.

In terms of heterogeneity, this paper draws the following conclusions: 1) when the events of wars and conflicts occur, the energy trade volume of emerging economies usually shows a upward jump, which is mainly because wars and conflicts often occur in regions and countries with abundant energy resources, and the complex political situation will seriously affect the output and price of energy (usually price rise), resulting in the rise in energy trade in emerging economies. 2) When terrorist attacks occur, the energy trade volume of emerging economies is usually not affected, which is reflected in the fact that there is no significant jump in the energy trade variable before and after the event, indicating that the impact of the terrorist attack on the global situation will not spread to the energy trade field, and the real economy is not affected much. 3) When the international situation is suddenly tense, the energy trade of emerging economies usually shows a downward jump. This is mainly because the international tension often brings about negative effects such as trade disputes, sanctions and trade barriers, thus weakening the energy demand of emerging economies. At the same time, international tensions do not dampen energy supply, so from a supply and demand perspective, prices will fall, further reducing energy trade.

Through empirical analysis, this paper also draws additional conclusions. 1) The impact of geopolitical events on emerging economies is concentrated on the demand side. On the one hand, it is because emerging economies are usually not energy producing countries, and energy exports do not play a major role in their international trade process, so they are less impacted. On the other hand, emerging economies are usually in the stage of rapid development, and energy demand side is the key factor in their development, so it is also the main target affected. 2) Energy demand in emerging economies is seriously inelastic. Among the 15 events in this paper, 11 have significant jumps in energy trade volume, and the jump direction is consistent with the fluctuation direction of energy price, which shows that emerging economies will not significantly reduce energy imports because of the rise of energy price, nor will they significantly reduce energy imports because of the fall of energy price. This is because the rapid development of emerging economies is inseparable from the import of energy. To ensure energy supply is the primary goal of their international energy trade, while the price factor becomes a secondary consideration. 3) The fluctuation of energy trade is not completely controlled by geopolitical events, and key technological innovation also affects the energy market. From the ISIS upgrade case we can find that the dangerous situation in the Middle East should have affected the energy production and led to the rise of energy prices, but the impact of the shale oil technology revolution in the United States on the market completely covered the regional crisis situation. This shows that the impact of geopolitical risk on energy trade is likely to be fully offset when there is a more significant impact. In other cases of this paper, because the time point is relatively independent, there is no significant external change, so we can observe the event impact more clearly.

The conclusions of this paper have implications for the energy trade strategies of emerging economies. First, emerging economies need to pay more attention to global geopolitical events. It can be predicted that geopolitical events will continue to emerge in an endless stream for a long time in the future, and the regions where geopolitical risks occur are often the places of energy production, so they tend to have a greater impact on the energy market. The empirical study of this paper confirms the significant impact of geopolitical risks on energy trade. Second, emerging economies need to strengthen the pertinence of response measures to geopolitical events. Based on the empirical finding, the impacts of three kinds of geopolitical events on energy trade of emerging economies exist significant heterogeneity, in which wars and conflicts are often associated with rising energy prices and energy trade, while international tensions often lead to a decline in energy prices and demand. Therefore, only when the right measure is applied can normal energy trade be maintained at every geopolitical risk. Third, the emerging economies need to strengthen the control on energy imports. The empirical analysis indicates that energy exports of emerging economies are almost not affected by geopolitical events, since risks concentrate on energy imports; meanwhile, energy import side also lacks of elasticity, thus increasing reserves to soften the rigid demand for energy may be one of the improvement directions of energy strategies in emerging economies.

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

YL, LY, CY, and ZL contributed to conception and design of the study. CY organized the database. CY performed the statistical analysis. CY and ZL wrote the first draft of the manuscript. YL, LY, CY, and ZL wrote sections of the manuscript. All authors contributed to manuscript revision, read, and approved the submitted version.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Anwar, M. (2021). Potential vs Prevalent vs Popular vs Proven Biodiesel Feedstocks: A Critical 4P Selection Process. Fuel 298, 120712. doi:10.1016/j.fuel.2021.120712

Assaf, A., Charif, H., and Mokni, K. (2021). Dynamic Connectedness between Uncertainty and Energy Markets: Do Investor Sentiments Matter? Resour. Pol. 72, 102112. doi:10.1016/j.resourpol.2021.102112

Baltar Rodríguez, E. (2021). Medio Oriente: inestabilidad y crisis del orden regional. Eaa 56, 265–296. doi:10.24201/eaa.v56i2.2649

Caldara, D., and Iacoviello, M. (2019). Measuring Geopolitical Risk, Board Governors Fed. Reserve Board.

Checkovich, A. (2005). Neil Smith. American Empire: Roosevelt's Geographer and the Prelude to Globalization. Xxvii + 557 pp., illus., Notes, index. Berkeley/Los Angeles/London: University of California Press, 2003. $39.95 (Cloth). Isis 96, 455–456. doi:10.1086/498797

Duan, F., Ji, Q., Liu, B.-Y., and Fan, Y. (2018). Energy Investment Risk Assessment for Nations along China's Belt & Road Initiative. J. Clean. Prod. 170, 535–547. doi:10.1016/j.jclepro.2017.09.152

Duk, C. J. (2018). Strengthening the Initiative of the South and North Korea in Process of Establishing a Peace System on the Korean Peninsula : Focusing on Geo-Economic Approach. Natl. Strategy 24, 41–70. doi:10.35390/sejong.24.4.201811.002

Gupta, E. (2008). Oil Vulnerability index of Oil-Importing Countries. Energy Policy 36, 1195–1211. doi:10.1016/j.enpol.2007.11.011

Harvey, T. (2008). Book Review: Harvey, D. 2007: The Limits to Capital (Third Edition). London: Verso. 478 Pp. £17.99 Paper. ISBN: 978 1 84467 095 6. Prog. Hum. Geogr. 32, 485–486. doi:10.1177/03091325080320031007

Hongwei, Z., Ying, W., Cai, Y., and Yaoqi, G. (2021). The Impact of Country Risk on Energy Trade Patterns Based on Complex Network and Panel Regression Analyses. Energy 222. doi:10.1016/j.energy.2021.119979

Ilic, B., Stojanovic, D., and Djukic, G. (2019). Green Economy: Mobilization of International Capital for Financing Projects of Renewable Energy Sources. Green. Finance 1, 94–109. doi:10.3934/gf.2019.2.94

Imbens, G., and Kalyanaraman, K. (2012). Optimal Bandwidth Choice for the Regression Discontinuity Estimator. Rev. Econ. Stud. 79, 933–959. doi:10.1093/restud/rdr043

Iqbal, B. A., Rahman, N., and Elimimian, J. (2019). The Future of Global Trade in the Presence of the Sino-US Trade War. Econ. Polit. Stud. 7, 217–231. doi:10.1080/20954816.2019.1595324

Kang, W., and Ratti, R. A. (2013). Structural Oil price Shocks and Policy Uncertainty. Econ. Model. 35, 314–319. doi:10.1016/j.econmod.2013.07.025

Kemfert, C., Schmalz, S., and Schmalz, S. (2019). Sustainable Finance: Political Challenges of Development and Implementation of Framework Conditions. Green. Finance 1, 237–248. doi:10.3934/gf.2019.3.237

Kurecic, P. (2018). The Three Seas Initiative: Geographical Determinants, Geopolitical Foundations, and Prospective Challenges. Hrvatski Geografski Glasnik-Croatian Geographical Bull. 80, 99–124. doi:10.21861/hgg.2018.80.01.05

Labandeira, X., Labeaga, J. M., and López-Otero, X. (2017). A Meta-Analysis on the price Elasticity of Energy Demand. Energy Policy 102, 549–568. doi:10.1016/j.enpol.2017.01.002

Le Coq, C., and Paltseva, E. (2009). Measuring the Security of External Energy Supply in the European Union. Energy Policy 37, 4474–4481. doi:10.1016/j.enpol.2009.05.069

Lee, C.-C., Lee, C.-C., and Ning, S.-L. (2017). Dynamic Relationship of Oil price Shocks and Country Risks. Energ. Econ. 66, 571–581. doi:10.1016/j.eneco.2017.01.028

Lee, D. S., and Lemieux, T. (2010). Regression Discontinuity Designs in Economics. J. Econ. Lit. 48, 281–355. doi:10.1257/jel.48.2.281

Li, F., Yang, C., Li, Z., and Failler, P. (2021a). Does Geopolitics Have an Impact on Energy Trade? Empirical Research on Emerging Countries. Sustainability 13, 5199. doi:10.3390/su13095199

Li, T., and Liao, G. (2020). The Heterogeneous Impact of Financial Development on Green Total Factor Productivity. Front. Energ. Res. 8. doi:10.3389/fenrg.2020.00029

Li, T., Ma, J., and Mo, B. (2021b). Does the Land Market Have an Impact on Green Total Factor Productivity? A Case Study on China. Land 10, 595. doi:10.3390/land10060595

Li, T., Zhong, J., and Huang, Z. (2020a). Potential Dependence of Financial Cycles between Emerging and Developed Countries: Based on ARIMA-GARCH Copula Model. Emerging Markets Finance and Trade 56, 1237–1250. doi:10.1080/1540496x.2019.1611559

Li, Y. (2010). The Risk Analysis on Energy Price Volatility of China Market Based on GARCH Model. Ebm 2010: Int. Conf. Eng. Business Manag., 1–8.

Li, Z., Wang, Y., and Huang, Z. (2020b). Risk Connectedness Heterogeneity in the Cryptocurrency Markets. Front. Phys. 8. doi:10.3389/fphy.2020.00243

Li, Z., Zou, F., Tan, Y., and Zhu, J. (2021c). Does Financial Excess Support Land Urbanization-An Empirical Study of Cities in China. Land 10, 635. doi:10.3390/land10060635

Lin, B.-Q., and Liu, J.-H. (2010). Estimating Coal Production Peak and Trends of Coal Imports in China. Energy Policy 38, 512–519. doi:10.1016/j.enpol.2009.09.042

Liu, K. (2020). The Effects of the China-US Trade War during 2018-2019 on the Chinese Economy: an Initial Assessment. Econ. Polit. Stud. 8, 462–481. doi:10.1080/20954816.2020.1757569

Oral, M., and Özdemir, Ü. (2017). Küresel Enerji Jeopolitiğinde Türkiye: Fırsatlar Ve Riskler/the Position of Turkey in Global Energy Geopolitics: Opportunities and Risks. Taksad 6, 948–959. doi:10.7596/taksad.v6i4.1054

Pant, B., Rai, R. K., Kumar Rai, R., Bhattarai, S., Neupane, N., Kotru, R., et al. (2020). Actors in Customary and Modern Trade of Caterpillar Fungus in Nepalese High Mountains: Who Holds the Power? Green. Finance 2, 373–391. doi:10.3934/gf.2020020

Peña, G. (2020). A New Trading Algorithm with Financial Applications. Quantitative Finance Econ. 4, 596–607. doi:10.3934/qfe.2020027

Qiu, L. D., Zhan, C., and Wei, X. (2019). An Analysis of the China-US Trade War through the Lens of the Trade Literature. Econ. Polit. Stud. 7, 148–168. doi:10.1080/20954816.2019.1595329

Santos, M. M. d., and Matai, P. H. L. d. S. (2010). A importância da industrialização Do xisto brasileiro frente ao cenário energético mundial. Rem: Rev. Esc. Minas 63, 673–678. doi:10.1590/s0370-44672010000400012

Simonia, N. A., and Torkunov, A. V. (2016). THE IMPACT of GEOPOLITICAL FACTORS on INTERNATIONAL ENERGY MARKETS (The US Case). Moscow: Polis-Politicheskiye Issledovaniya, 38–48. doi:10.17976/jpps/2016.02.04

Sukharev, O. S. (2020). Structural Analysis of Income and Risk Dynamics in Models of Economic Growth. Quantitative Finance Econ. 4, 1–18. doi:10.3934/qfe.202000110.3934/qfe.2020018

Sun, M., Gao, C., and Shen, B. (2014). Quantifying China's Oil Import Risks and the Impact on the National Economy. Energy Policy 67, 605–611. doi:10.1016/j.enpol.2013.12.061

Tunsjø, Ø. (2010). Hedging against Oil Dependency: New Perspectives on China's Energy Security Policy. Int. Relations 24, 25–45. doi:10.1177/0047117809340543

Wang, M., Li, Y., and Liao, G. (2021). Research on the Impact of Green Technology Innovation on Energy Total Factor Productivity, Based on Provincial Data of China. Front. Environ. Sci. 9. doi:10.3389/fenvs.2021.710931

Xie, R., Zhao, Y., Zhao, Y., and Chen, L. (2020). Structural Path Analysis and its Applications: Literature Review. Natl. Account. Rev. 2, 83–94. doi:10.3934/NAR.2020005

Yang, C., Li, T., and Albitar, K. (2021). Does Energy Efficiency Affect Ambient PM2.5? the Moderating Role of Energy Investment. Front. Environ. Sci. 9. doi:10.3389/fenvs.2021.707751

Yang, Y., Li, J., Sun, X., and Chen, J. (2014). Measuring External Oil Supply Risk: A Modified Diversification index with Country Risk and Potential Oil Exports. Energy 68, 930–938. doi:10.1016/j.energy.2014.02.091

Keywords: geopolitical event, heterogeneity, regression discontinuity design, empirical study, energy trade

Citation: Liu Y, Yu L, Yang C and Li Z (2021) Heterogeneity of the Impact of Geopolitical Events on Energy Trade: An Empirical Study Based on Regression Discontinuity Design. Front. Environ. Sci. 9:722910. doi: 10.3389/fenvs.2021.722910

Received: 09 June 2021; Accepted: 22 July 2021;

Published: 29 July 2021.

Edited by:

Qiang Ji, Institutes of Science and Development (CAS), ChinaReviewed by:

Xuejiao Ma, Dalian University of Technology, ChinaCopyright © 2021 Liu, Yu, Yang and Li. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Zhenghui Li, bGl6aEBnemh1LmVkdS5jbg==

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.