Christine Krüger

Christine Krüger Larissa Doré

Larissa Doré Tomke Janßen1

Tomke Janßen1 Mathieu Saurat

Mathieu Saurat Arjuna Nebel

Arjuna Nebel Peter Viebahn

Peter Viebahn- 1Wuppertal Institute for Climate, Environment and Energy, Wuppertal, Germany

- 2Cologne Institute for Renewable Energy, TH Köln – University of Applied Sciences, Cologne, Germany

For reaching the European greenhouse gas emission targets, the phase-in of alternative technologies and energy carriers is crucial for all sectors. For the transport sector, synthetic fuels are–next to electromobility–a promising option, especially for long-distance shipping and air transport. Within this context, the import of synthetic fuels from the Middle East and Northern Africa (MENA) region seems attractive due to low costs for renewable electricity in this region and low transport costs of synthetic fuels at the same time. Against this background, this paper analyzes the role of the MENA region in meeting the future synthetic fuel demand in Europe using a cost-optimizing energy supply model. In this model, the production, storage and transport of electricity, hydrogen and synthetic fuels by various technologies in both European and MENA countries in the period up to 2050 are explicitly modeled. Thereby, different scenarios are analyzed to depict regional differences in investment risks: a base scenario that does not take into account regional differences in investments risks and three risk scenarios with different developments of regional investment risks. Sensitivity analyses are also carried out to derive conclusions about the robustness of results. Results show that meeting the future synthetic fuel demand in Europe to a large extent by imports from the MENA region can be an attractive option from an economic point of view. If investment risks are incorporated, however, lower import quotas of synthetic fuels are economically attractive for Europe: the higher generation costs are outweighed by the lower investments risks in Europe to a certain extent. Thereby, investment risks outweigh other factors such as transport distance or renewable electricity generation costs in terms of exporting MENA regions and a synthetic fuel import is especially attractive from MENA countries with low investment risks. Concluding, within this paper, detailed export relations between MENA and EU considering investment risks were modeled for the first time. These model results should be complemented by a more in-depth analysis of the MENA countries, including evaluating opportunities for local value chain development, sustainability concerns (including social factors), and optimal site selection.

1 Introduction

The transport sector accounts for 26% of the European and 22% of the German GHG emissions in 2020 (Eurostat, 2022). The defossilization of the transport sector therefore plays an important role in achieving the goals set out in the Paris Agreement. Currently, fossil fuels dominate the transport sector. In 2022, fossil fuels such as oil and petroleum products (including kerosene) or natural gas provided about 93% of the final energy demand for transport, while biofuels contributed only five–6% and electricity about 2%, both in Europe and in Germany according (Eurostat, 2024) and (AG Energiebilanzen, 2024). Regarding the distribution of final energy sources in the different transport sectors, air and water transport were almost entirely based on fossil fuels. In road transport, 6% biofuels were used and electricity accounted for less than 1%, whereas in rail transport, 79% of the final energy demand was covered by electricity (Eurostat, 2024).

In order to reduce the GHG emissions of the transport sector, avoiding traffic and shifting to climate-friendly modes of transport is crucial. In addition, different drives and fuels offer alternatives: electric mobility, new fuels such as hydrogen or synthetically produced methanol, and synthetic fuels such as synthetic diesel, gasoline, or kerosene, are discussed. Since synfuels consist of hydrocarbons just like fossil fuels, except that they are produced from green hydrogen and carbon dioxide (CO2), we cannot speak of decarbonization here. Defossilization therefore is the more appropriate term.

The production of hydrogen and synthetic fuels is extremely energy intensive. For this reason, there is a broad consensus that a large proportion of synthetic fuels will be imported in the future because production costs outside of Europe are lower. Against this backdrop, the MENA region appears particularly attractive for the production of these energy carriers, as it possesses a high potential for renewable energy and is geographically close to Europe.

Numerous studies have been conducted to identify different pathways to a carbon neutral energy system in Europe (Capros et al., 2019; Korkmaz et al., 2020; Jeroen Dommisse and Jean-Louis Tychon, 2020). Some of these studies have focused in particular on the role of the transport sector in the European energy transition (Dominković et al., 2018; Jan et al., 2019; Colbertaldo et al., 2018). In these studies, the option of using synthetic fuels produced from renewable energies to facilitate a rapid transition away from fossil fuels is frequently discussed (Evangelopoulou et al., 2019; Ridjan et al., 2013; Pregger et al., 2020; Grant Wilson and Styring, 2017).

The first studies linking the European energy transition with the MENA region were carried out at the beginning of the century with the idea of importing electricity from the MENA region to Europe (Franz and Müller-Steinhagen, 2007). This concept has been replaced by the idea of importing hydrogen (Timmerberg and Kaltschmitt, 2019; Cavana and Leone, 2021; van Wijk and Wouters, 2021; Eddy et al., 2022) or synthetic fuels (Fasihi et al., 2017; Berger et al., 2021). However, both the transport infrastructure required to establish such an energy system and the possible demand structure in the MENA region and Europe have not yet been analyzed in detail. Despite this, a review by (Razi and Dincer, 2022) shows the potential of a hydrogen-based and renewable energy future for the MENA region.

To model the possible techno-economic supply structures of synthetic fuels from the MENA region into Europe, a calculation of possible supply costs for renewable fuels must be performed in MENA (Lux et al., 2021). give a detailed insight into the calculation of the cost potential curves of renewable-based fuels. However, this study also only slightly discusses the necessary infrastructure and does not take into account the fuel requirements for the transport sector in Europe.

Therefore, the framing research questions to be investigated in this paper are “How can cost optimal supply paths be designed to meet Germany’s and whole Europe’s future demand for renewable electricity, hydrogen, intermediate products, and synthetic fuels? What could be the role of the MENA region in this? And what influence do investment risks in the MENA region have on the structure of these supply paths?”. This frame was broken down into the following underlying research questions:

• Which part of the synfuel demand would be covered by domestic sources and which by imports from the MENA region?

• What power generation potentials in Europe and MENA could be exploited to produce these fuels?

• Which countries or regions in MENA would be favorable exporters of synfuels?

• What influence do the investment risks in MENA have?

• How could the synfuels be transported?

• Which technologies could be used for the production of synfuels?

Consequently, the present study aims to analyze how the projected long-term demand for electricity and synfuels in Europe can be met as economically as possible, if European renewable potentials, as well as those of the MENA region (taking into account their domestic energy demands) can be exploited. A modeling approach is chosen to answer the research questions. The model, the underlying system boundaries and the data used are described in detail in Section 2. Section 3 presents the results. First, a baseline scenario is analyzed without considering country-specific investment risks (Section 3.1). The robustness of these results is examined in Section 3.2. Subsequently, the results considering country-specific investment risks are presented in Section 3.3 and analyzed in terms of their sensitivity in Section 3.4. Finally, in Section 4 the results are summarized and discussed in the context of the research questions.

2 Scope and methods

The cost-optimizing energy supply model Energy Supply Model - Invest Module (ESM-I), a model within in the Wuppertal Institute System Model Architecture for Energy and Emission Scenarios (WISEE) model family, is used to answer the research question. The application of this model is explained below. Section 2.1 describes the modeled system section in regional, temporal, and technological terms and describes the input data that represent the most important drivers for the model. Section 2.2 explains the structure and functionality of the model. Finally, Section 2.3 describes how investment risks are mapped in the model.

2.1 Scope

First, the system layout in terms of regional, temporal, and technological scope is defined in Section 2.1.1. For modeling this scope, a wide range of input data is required, of which the most important are described in Sections 2.1.2 and 2.1.3, where Section 2.1.2 shows development of demand for electricity, green hydrogen and synthetic fuels, and the renewable generation potential which can be used to meet these demands is shown in Section 2.1.3. In addition to these input data, techno-economic parameters such as costs, conversion efficiencies, and lifetimes are needed for all depicted energy generators, converters, transport, and storage technologies. These are reported in the supplementary material.

2.1.1 Spatial, temporal and technological layout

The present study deals with the interactions between Europe and MENA. Therefore, these regions are explicitly modeled. In order to reduce complexity and realize manageable computing times, clusters are formed in which several countries are grouped together. Europe is grouped into five clusters, the MENA region is divided into eight clusters (see Figure 1).

• Germany (DE) as focus region is depicted as a single region in Europe

• EU_West includes Benelux, France, Great Britain, Ireland, Spain and Portugal

• EU_North stands for the Scandinavian countries Norway, Sweden and Denmark

• EU_East_Southeast is a large cluster representing several countries in Eastern Europe, all from Poland to Greece

• EU_South is a small cluster representing Italy and Switzerland

• Four of the MENA -regions represent single countries: Algeria, Tunisia, Libya, and Egypt

• Maghreb w/o Tun/Alg represents the Maghreb region without Tunisia and Algeria

• Middle East is a larger cluster including Jordan, Iraq, Iran, Syria, Lebanon and Israel

• North-Arabia is the Northern cluster on the Arabian Peninsula consisting of Saudi Arabia, Qatar, Bahrain and Kuwait

• South-Arabia is the Southern cluster on the Arabian Peninsula consisting of United Arab Emirates, Yemen and Oman

Figure 1. Covered region and clustering (map based on OpenStreetMap.

The projection period of the model WISEE-ESM-I covers the years 2030–2059, where only the years 2030, 2040 and 2050 are explicitly modeled, each representing a decade (i.e. 2030 represents the period from 2030–2039). The model uses a sub annual resolution to account for the fluctuating availability of renewable electricity (RE). For complexity reduction reasons, each year is reduced to 25 time steps (see Section 2.2.2).

The energy carriers and feedstocks represented in the model are renewable electricity, hydrogen from electrolysis, synthetic methane and methanol, synthetic diesel, gasoline and kerosene, synthetic naphtha and ammonia, all based on green hydrogen. In addition, the model includes the necessary intermediate products water (

An important delimitation of the modeled scope is the fact that only the share of the energy system to be covered by wind and solar energy is included. Consequently, the demand scenarios include only the share of demand that will be met from wind and solar energy. The fossil share of the demand for electricity, hydrogen (H2), and synfuels (including feed stocks) is not depicted. In addition, also the share of energy that is produced by other RE sources than wind and solar (e.g., biomass and run-of-river) is excluded similarly.

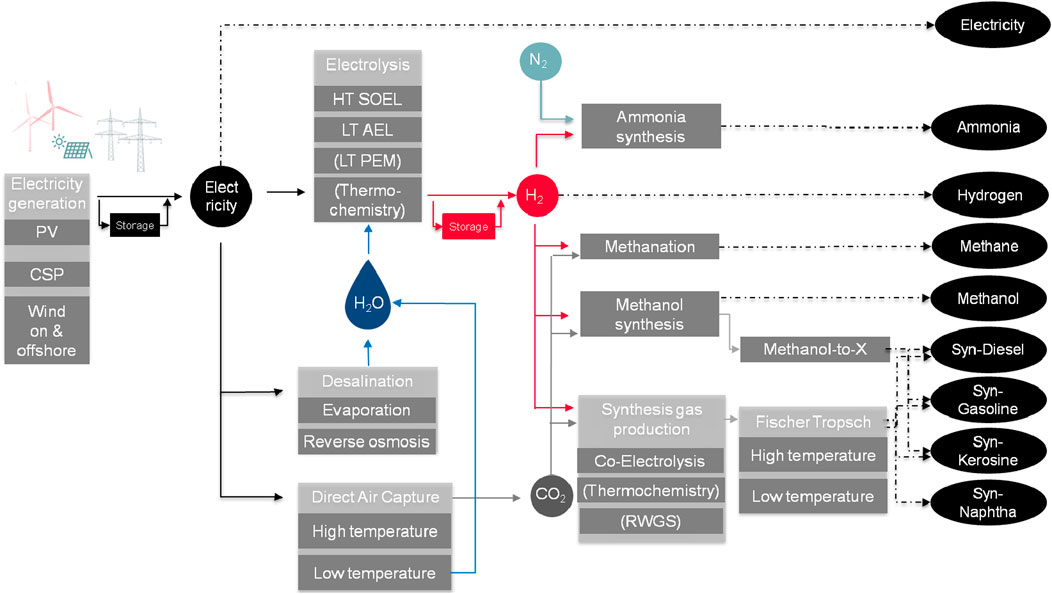

Various conversion and synthesis technologies along the Power-to-X (PtX) route are depicted. Water can be obtained from seawater through reverse osmosis and evaporation, from ground water, if available, or as a byproduct from DAC and Fischer-Tropsch (FT). Low temperature (LT)-(alkaline water electrolysis (AEL)) and high temperature (HT)- solid oxide electrolysis (SOEL) are technologies considered for hydrogen production. High-temperature coelectrolysis is considered for gas synthesis generation. The synthesis technologies in the model include FT synthesis for the production of diesel, gasoline, kerosene, and naphtha in fixed proportions (differentiating between high and low temperature FT-routes which has naphtha or diesel, respectively, as the main output), methanation, ammonia synthesis, and methanol synthesis with optional subsequent methanol-to-X process. The processes for further processing of methanol into various products (syn-diesel, syn-gasoline, and syn-kerosene) are represented separately in the model; for simplicity, they are named “methanol-to-X″ here. Methanol-to-Diesel and Methanol-to-Kerosene are not expected to be available until 2040.

Regarding carbon sources for conversion processes, only CO2 from DAC, i.e., capture from ambient air, is implemented in the model. The consideration of using carbon sources from biomass has been omitted due to its constrained availability, and the capture of carbon from industrial waste gases is not incorporated into the model, as the objective of achieving climate neutrality necessitates the establishment of closed carbon cycles. Heat demand and waste heat are modeled, differentiating between low- and high-temperature heat. These demands can be met by electric heaters or, if the temperature differences between processes are sufficient, through waste heat from FT, methanation or methanol-to-X processes. The extraction of nitrogen (

Figure 2 gives an overview over the depicted PtX-technologies. In addition to the technologies listed above, LT-polymer electrolyte membrane electrolysis (PEM), reverse water-gas shift reaction (RWGS) and thermochemistry have been modeled, but are not included in the present analysis because they were assumed to be inferior from the model point of view; therefore, they are bracketed in the figure.

Figure 2. Overview about considered technologies along the PtX-route.

Beyond conversion and production infrastructures, storage (battery and hydrogen tank storage) and transport technologies are included in the model. For transport, multiple options are considered: electricity is transported via high-voltage direct current lines. Gaseous and liquid fuels are transported via onshore or offshore pipelines or tankers.

The model uses a greenfield approach regarding energy. This is a simplification and means that the existing infrastructure, such as existing RE plants, storage units or transmission capacity, is not mapped. Consequently, it is assumed that the corresponding investments are necessary for all components of the modeled system. This may lead to different supply structures being identified as cost-optimal than if existing infrastructure had been taken into account. As the expansion of renewables is still in the ramp-up phase and the other technologies along the PtX route do not yet represent significant capacity, the inaccuracy introduced by the greenfield approach is relatively small in these areas. It is greater in the case of transport infrastructure, where existing pipelines represent a valuable asset. To address this, the model results for transport infrastructure were compared ex post with existing capacities and have been validated in this way.

2.1.2 Energy demand

As described in Section 2.1.1, the development of the energy demand for the transport and industrial sectors, as well as the surrounding energy system, is the most important input of the model. With a focus on the transport sector, different developments have been projected in the mix of driving technologies. The results described in this paper focus on a scenario of a broad mix of driving technologies - called the base scenario. Sensitivities are conducted for a variant with a very high share of battery electric vehicles as well as a very high use of synfuels. The demand scenario includes the demand for renewable energy sources in the transport sector, the industrial sector and also the proportion of general electricity demand which is to be supplied from renewable energy sources. For the transport sector, it is assumed that the transport demand in Germany develops as in the “Technology Mix scenario” from (Bründlinger et al., 2018). The base scenario is also closely based on this scenario in terms of the fuels used. This scenario represents the target year 2050. Methanol was also taken into account in this scenario and plausible developments were assumed for the years up to 2050. A similar development in demand from the transport sector was assumed for the other European countries. The industrial demand for hydrogen and synthetic feedstocks in Europe is based on (Schneider et al., 2018) for the steel sector and (Prognos, 2020) for the petrochemicals sector and ammonia demand. The demand of the surrounding energy system for renewable energy sources is derived from (Fraunhofer IFAM, DLR, and GWI, 2020).

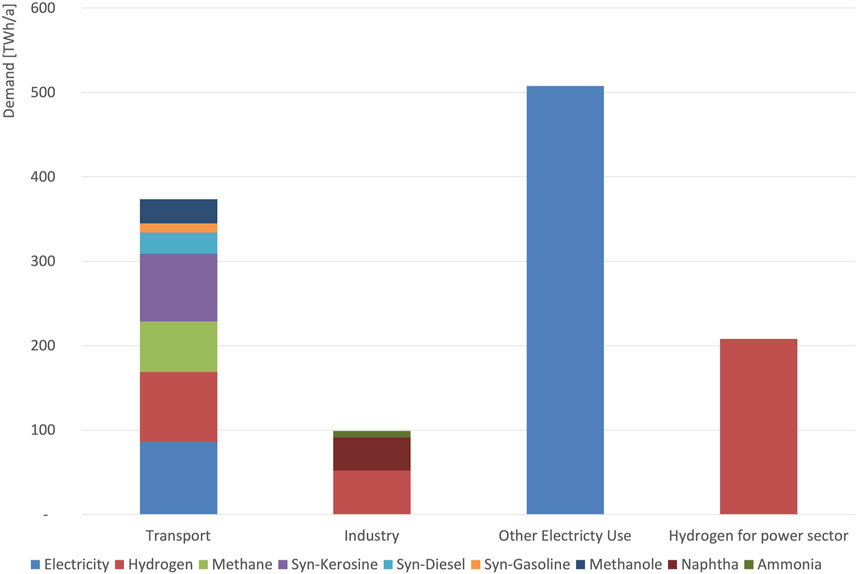

The resulting development of the demand for renewable energy, feedstocks and fuels is documented in the supplementary material. Exemplarily, the resulting demand for renewable energy in DE in 2050 in the base scenario is shown in Figure 3. It can be seen that electricity is the dominating form of demand for renewable energy. It is followed by hydrogen, which is used in transport, as well as in the industry and for power generation. Synthetic kerosene, methane, methanol, diesel, and gasoline are used in the transport sector in descending magnitude. Synthetic naphtha as well as ammonia are needed for industrial use only. The use of ammonia for transport has not been considered here, although it is under discussion, especially for maritime transport.

Figure 3. Renewable energy demand for transport, industry and power sector for Germany in 2050.

The energy demand of the countries in the MENA region has not been included in this model but has been handled differently. Based on ambitious scenarios for the development of energy demand and supply within the MENA region (Thomas, 2022), the renewable energy potentials that are intended to be available for export are reduced by domestic demands in the MENA region. The generation potentials in the region were allocated to cover these demands with priority, so the most cost-effective renewable generation is reserved for that purpose.

2.1.3 Potential for renewable power generation

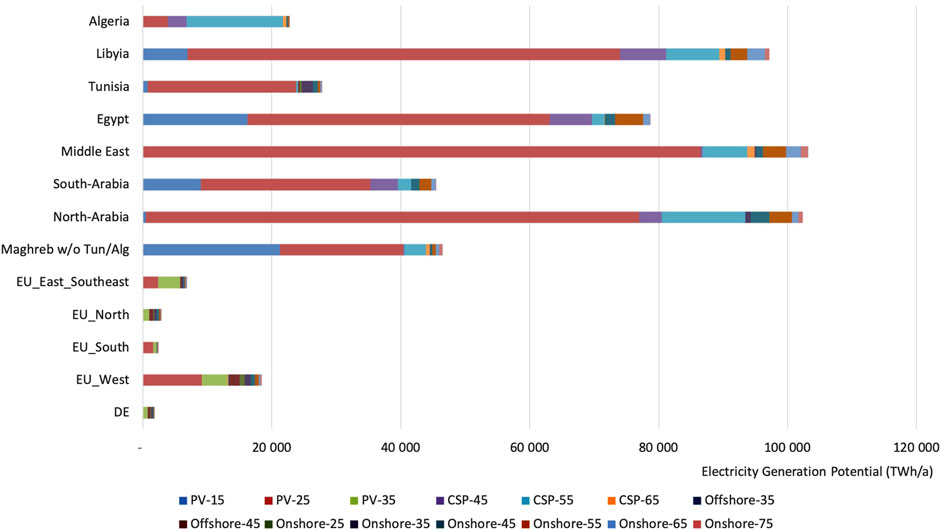

The scope of the model includes renewable electricity generation from photovoltaics (PV), concentrated solar power (CSP), wind-onshore and wind-offshore in both Europe and MENA. The potentials are characterized by the installable generation capacities and hourly time series of their infeed. The potentials per technology and country are differentiated into classes of similar levelized cost of electricity (LCOE) expected for the year 2050. The range of classes is 10 EUR/MWh. The site-specific LCOE result from the strongly varying wind and solar potentials; the investment and fixed operating costs are assumed to be identical at all sites in the base scenario. The derivation of these potentials and the underlying methodology as well as all underlying assumptions can be found in (Braun et al., 2022).

In this paper, the cost potential categories are always indicated by the mean value of the respective range. 15 EUR/MWh, for example, represents potentials with electricity production costs between 10 and 20 EUR/MWh. The RE potentials which are available for export are reduced by domestic demands in the MENA-region, to make sure that the exports do not hinder the development of a renewable domestic energy supply. Also, the most cost-intensive potentials are not included (see Section 2.2.2). Figure 4 shows the amounts of electricity that can be generated per technology and region for the year 2050 in the different categories of cost potential depicted in the model. This remaining potential after the exclusion of the most expensive categories covers 98% of the total potential available for export calculated for the region. The dominance of solar potentials is striking: PV can provide about 65% of the total amount of energy that can be generated, 27% from CSP and about 8% from wind. A total of 64% of the potentials can be developed for less than 30 EUR/MWh under the given premises.

Figure 4. Potential electricity generation in 2050 for the cost potential categories considered remaining for export purposes.

2.2 The WISEE-ESM-I model

2.2.1 Model design

The ESM-I model used here is a cost-optimizing capacity-expansion energy system model. It is built upon Open Source Energy Modeling System (OSeMOSYS), a framework for the optimization of long-term energy systems (Howells et al., 2011; Royal Institute of Technology, 2022). Such a model optimizes the overall cost of the system.

ESM-I retains the original objective function of OSeMOSYS, that is “to estimate the lowest net present value cost of an energy system to meet given demand(s) for energy or energy services” (Howells et al., 2011). The basic “blocks” constituting the OSeMOSYS framework (cost accounting, annual and timeslice-based capacity adequacy, annual and timeslice-based energy balance, constraints on capacity and generation, energy storage, and emission accounting) also remain with, in some cases, modifications and the addition of a new transport module, described in detail in (Saurat et al., 2024).

A linear optimization model such as ESM-I defines parameters, variables, constraints, and an objective function. Parameters represent model-exogenous specifications and are thus input data of the model. They determine the system boundaries of a model run in terms of considered energy sources, technologies, temporal and geographic resolution. The variables are the output of the model and thus represent the cost-optimal decisions of the model with respect to the design of the future energy system. Constraints limit the expression of the variables and thus the solution space of the model. The objective function represents the decision criterion with respect to which the design of the energy system is optimized.

The model is technologically detailed, that is it explicitly represents the production of exogenously demanded commodities from primary inputs (e.g., solar energy) in production plants through intermediate products. These commodities can be energy carriers as well as products such as ammonia. Both energy supply and demand have a given geographical and temporal resolution, set by the user. We consider separate geographical regions that can exchange energy carriers. The exchange takes place via explicitly modeled transport capabilities. Transmission capacities are represented as connections between the regions, defined as transmission power at the region borders. A transmission capacity for one energy carrier is therefore representative for all infrastructure connecting two regions. Assumptions about pipe diameters, voltage levels, etc., Determine transmission capacity. Physical lines are not explicitly represented in the model, as it does not include load flow calculations or flow dynamic aspects.

On the temporal level, the model differentiates between years and timeslices. The former enables long-term modeling of the power system over decades. Timeslices represent time periods throughout the year and enable mapping short-term fluctuations in energy supply and demand. Storage facilities explicitly included in the model compensate for these fluctuations. Storage charge and discharge are represented as production technologies in the model.

2.2.2 Reducing model complexity

The consideration of a range of countries, time periods, fuels, production technologies, and especially transport infrastructures leads to a complex planning problem. Therefore, different measures are implemented to reduce model complexity. These measures address the number of time periods (temporal complexity) and regions (spatial complexity) which are explicitly modeled, as well as the inter-annual handling of energy storage within the model and a reduction in the number of categories of renewable potential included in the modeling.

On a temporal level, years and timeslices are modeled in order to take into account both long-term developments and short-term fluctuations in energy supply and demand. The reduction of temporal complexity starts at both temporal levels: On the one hand, only specific years are explicitly modeled. For more information on the so called timestep-modeling see (Saurat et al., 2024). On the other hand, the number of time steps during 1 year is reduced by aggregating the hours. Thereby, demand and solar radiation data are aggregated by selecting data points from the entire year at regular intervals. For example, for a temporal resolution of 25 h, every 350th hour is considered (corresponding to a biweekly rhythm). In this way, a synthetic daily time series is built, which represents the typical intraday fluctuations and–however, only very stylized at low temporal resolution - also the seasonality of the feed-in and the load. For the feed-in of wind energy, a different aggregation method is used: In each case, the continuous time interval from the seasonal series that has the highest spread between maximum and minimum availability of the potentials is used. This approach ensures that fluctuations are adequately represented. Furthermore, by scaling the aggregated time series, it is ensured that the full load hours of the aggregated time series correspond to those of the non-aggregated original time series.

Spatial complexity is reduced by clustering individual countries to larger regions, the so-called clusters. For this, data country-specific input data is aggregated prior to optimization. Thus, the following methodology for aggregation is used: Data regarding demand as well as minimum and maximum installable capacities (including renewable energy potentials) are summed for all countries within a cluster. Also, the exchange capacities to and from other clusters/countries are summed for all countries within a cluster. The course of demand during the year, the demand profile, is aggregated based on the weighted average, with the share of each country’s demand of the total demand of the cluster as the weighing factor. All other input data, this especially relates to the techno-economic data of the production, storage, and transportation technologies as well as the transportation distance, are clustered on the basis of the arithmetic mean. An additional measure is to limit storage capabilities to balance within each year, that is, storage between years is not possible. By reducing the number of explicitly modeled time periods and regions and avoiding inter-annual energy storage, the number of decision variables and equations, and thus, the model complexity is significantly reduced. In order to further reduce the complexity, we reduce the amount of potentials depicted for renewable energy generation. As stated above, the generation potential exceeds the total demand to be met by a multiple (approximately 80 times). Moreover, particularly high potentials are found in the more low-cost potential categories, so that it is permissible to exclude particularly expensive categories for complexity reduction in the modeling. This remaining potential after the exclusion of the most expensive categories covers 98% of the total potential available for export calculated for the region.

2.3 Consideration of investment risks

In the base scenario, the investment costs are the same for all regions. In a second set of scenarios, referred to as risk scenarios in the following, country-specific investment risks are considered by assuming country-specific investment costs for production and storage facilities, which are supposed to reflect cost increases due to higher risks. The methodology for calculating country-specific investment costs is as follows:

• Based on an assessment of macro and micro risks in the MENA region and Europe, investment risks are quantified as a premium on Weighted Average Cost of Capital (WACC) for each country, in the following denoted as risk assessed WACC.

• Annuity factors for both the country-specific risk assessed WACC data as well as for a reference WACC of 6% are calculated according to Equation 1.

where

• Determination of scaling factors by diving the annuity factor for the country-specific risk assessed WACC by the annuity factor for the reference WACC according to Equation 2.

where

For the first step - assessment of risks and quantification of investment risks as WACC premiums - this paper builds on work from (Terrapon-Pfaff et al., 2024) for MENA and (Horst and Klann, 2022) for European Countries (Terrapon-Pfaff et al., 2024). conducted an assessment of risks for the development of renewable energy and synfuel sectors in the MENA region from a European and German perspective. Thereby, risk assessed WACC data are quantified, differentiated for both renewable energy and synfuel plants, as well as for the years 2030, 2040 and 2050 for the MENA countries. While country risks originally were defined as economic risks, the authors developed a broader concept of risk that encompasses both macro and micro risks. They identified eleven risks and divided them into five categories. Two categories of macro risks comprise political risks and macro-economic and business risks. Three categories of micro risks specifically affect the development of the renewable and green hydrogen and synthetic fuel sectors and include sector and technology development risks, social risks and nature risks. Overall, the risk assessment framework includes more than 100 risk indicators.

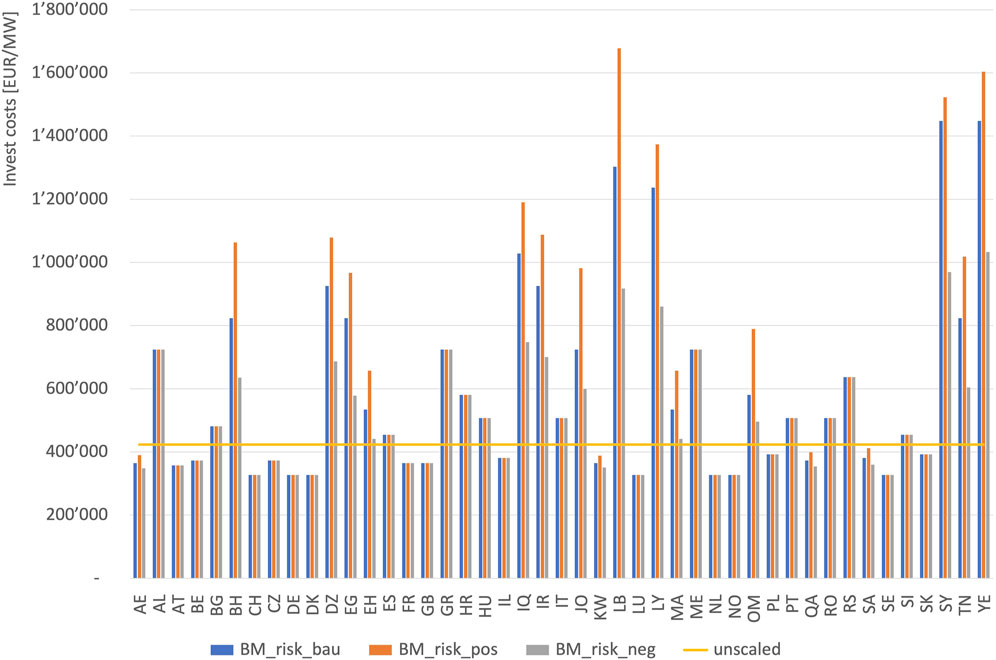

Three scenarios for the development of the risk assessed WACC in the MENA countries are developed - positive, business-as-usual and challenging development. Based on the risk assessed WACC data given in (Terrapon-Pfaff et al., 2024), country-specific investment cost data for production and storage facilities are derived for all MENA and European countries for the years 2030, 2040 and 2050. Corresponding to the scenarios in (Terrapon-Pfaff et al., 2024), three scenarios are considered here - base scenario plus positive development of investment risk (BM_risk_pos), base scenario plus business-as-usual development of investment risk (BM-risk-bau) and base scenario plus negative development of investment risk (BM_risk_neg). These differ in terms of data for the MENA countries, on the contrary uniform cost data is assumed for all European countries. In Figure 5, the country-specific investment cost data resulting from (Terrapon-Pfaff et al., 2024) are shown illustratively for PV plants in 2050 BM_risk_pos.

Figure 5. Example for country-specific investment costs: PV plants in 2050, based on (Terrapon-Pfaff et al., 2024).

3 Model results and discussion

This section first presents the model results in the base scenario (Section 3.1) and discusses their robustness via sensitivity analyzes (Section 3.2). Subsequently, the results of the modeling with consideration of the investment risks (Section 3.3) are discussed, followed by a sensitivity analysis with regard to the investment risks (Section 3.4). The evaluations all focus on the target year 2050.

3.1 Results in the base scenario without consideration of investment risks

The following results are for the base scenario which does not include any risk-capital cost additions. The investment costs are thus identical in all regions, and the regions’ supply options differ only in terms of their geographical location (and thus their distance and transport options) and the potential for renewable power generation (both installable capacity and the wind and solar characteristics), and the availability of water. These results show which supply paths with RE, green hydrogen and synthetic fuels from MENA and Europe would be advantageous from an overall economic perspective. The potential for renewable generation significantly exceeds the energy demand, while the available potentials in the MENA region are many times greater than those of Europe.

When assessing the possible role of the MENA region and Europe, respectively, the share of imports into Europe and Germany is of interest. According to the results of the model, the supply of synthetic fuels in Germany and Europe is strongly characterized by imports (see Table 1). Both Germany and the whole of Europe have import quotas well above 80% for gaseous and liquid fuels. In contrast, electricity is generated mainly close to consumption due to the higher specific transport costs.

Table 1. Import quotas in the base scenario to Germany and whole Europe in 2050.

Overall, DE has higher import quotas than the European average, as Scandinavia and the Iberian Peninsula in particular have higher renewable potentials on a large scale. Hydrogen and synthetic diesel, gasoline and naphtha, in particular, are therefore generated to a larger share in these countries. All European regions are net importers, therefore imports to DE do not originate from surrounding Europe but come from the MENA region. However, because of DE’s geographic location, they are routed through neighboring European countries.

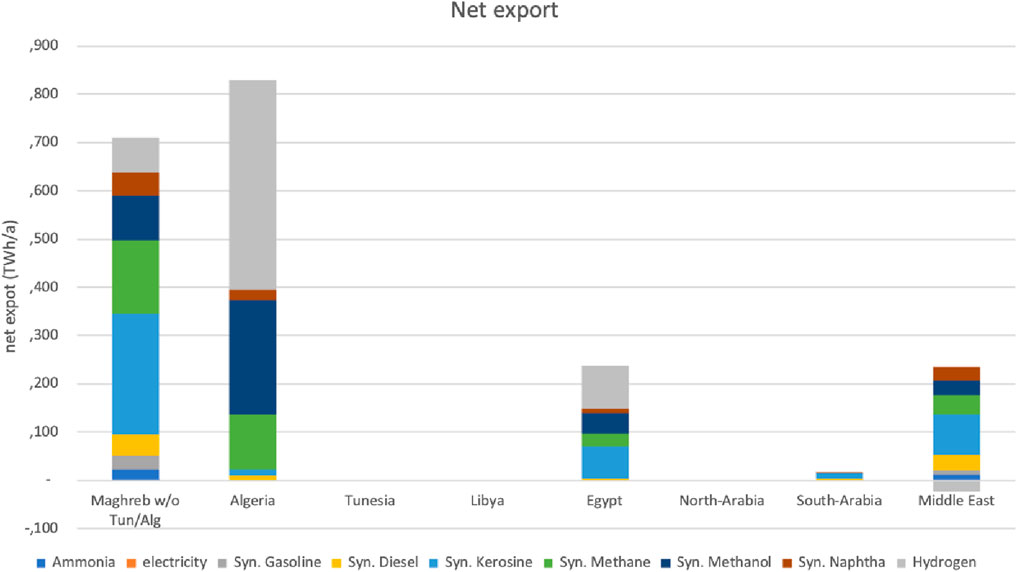

Regarding the exporting countries in the MENA region, it can be observed that Algeria, Maghreb without Tun/Alg, Egypt and the Middle East cluster play an important role (see Figure 6). Although all countries in the MENA region offer favorable RE generation potential, the peculiarity of the resulting countries is that they have lower transport costs to Europe and DE due to the possibility of an onshore pipeline connection. In the Middle East cluster and Maghreb without Tun/Alg, in addition, there is not only a favorable solar power generation potential, but also a comparably cheap wind power potential that complements solar power generation. A small share of imports come from the cluster in southern Arabia, which offers very advantageous solar potential, which compensates the disadvantage of the larger distance.

Figure 6. Net export of electricity, hydrogen and synfuels from clusters in the MENA region in the base scenario in 2050.

Hydrogen is exported to Europe mainly from Algeria and, to a lesser extent, from Egypt and Maghreb without Tun/Alg. For methanol, the largest export volumes also come from Algeria. Synthetic kerosene is mostly exported from the Maghreb without Tun/Alg and is the main export fuel from both Maghreb without Tun/Alg and the Middle East cluster. Synthetic methane, synthetic gasoline, diesel, and naphtha are also exported primarily from Maghreb without Tun/Alg. In total, it can be observed that all supplier countries export a wide range of synthetic fuels. This applies to FT products (synthetic naphtha, gasoline, diesel, and kerosene), which are produced in a coupled way, as well as methanol and synthetic methane. However, there is a tendency to import gaseous fuels such as hydrogen and methane over relatively short distances, while higher transport distances are tolerated for liquid fuels because of the lower specific transport costs.

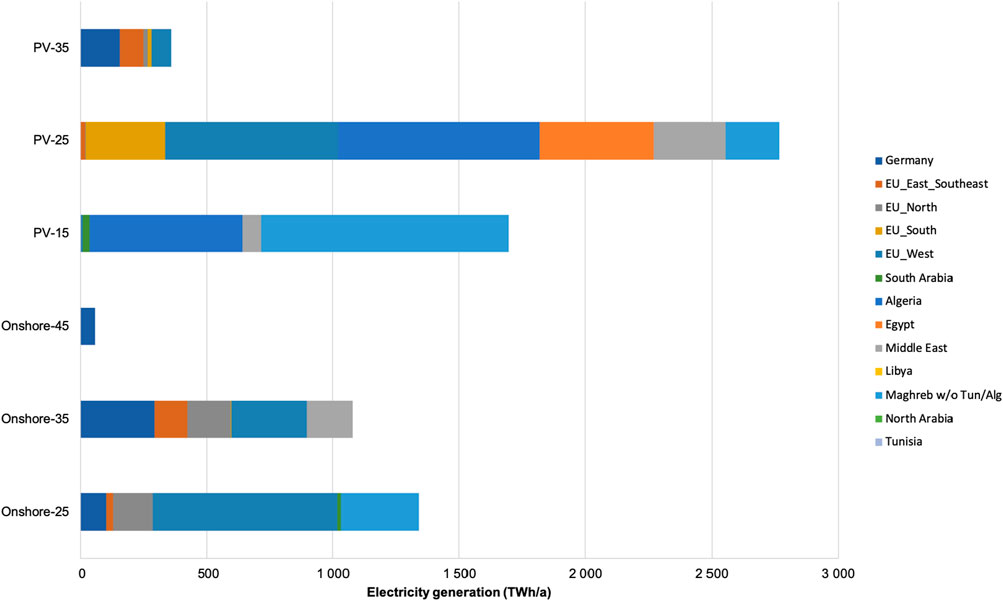

When examining the model results with regard to the question, which renewable generation potentials are being used (see Figure 7), it first needs to be stated that nearly all MENA countries offer favorable solar generation potentials. Therefore, in the MENA region, most of the generated energy is expected to come from solar. Algeria, the Middle East cluster and Maghreb without Tun/Alg have the most favorable solar irradiation conditions (i.e., the highest specific yield), and their potentials of this cheapest category (PV-15) are fully exploited. The largest potentials overall are in the PV-25 category, which is used in Europe and the MENA countries. The potentials of this category exceed the amounts of energy used by far, so that only very small shares are used. These large and cheap potentials in the MENA region cause the high share of imports from MENA to Europe described above. In that context, it should be noted that in the MENA region, PV is chosen as the solar electricity generation technology due to the slightly lower costs of the PV technology compared to the CSP technology (including the necessary batteries). However, differences in costs are small and–given the fact that future costs of the technologies are subject to uncertainty - future cost differences are also subject to uncertainty. Furthermore, it should be noted that the CSP technology is associated with other benefits, such as the supply of waste heat or the provision of guaranteed capacity, which will foster the deployment of the CSP technology in the future. Wind energy plays a minor role in MENA in comparison to solar (only 12% of the energy generated in the MENA region is from wind), but the best potentials in Maghreb without Tun/Alg, the Middle East cluster and South Arabia are fully exploited. That is because though the wind energy potentials in MENA are much lower than the enormous solar potentials, their use reduces the need for storage compared to the generation from solar alone and, thereby, reduces system costs. Due to this context, the possibility of wind energy generation is a location advantage in the MENA region, where almost all countries have favorable solar potential.

Figure 7. Electricity generation per category of potential, 2050, base scenario.

Wind energy is more dominant in Europe, as it accounts for 59% of RE generation. Most of this comes from the onshore-25 and onshore-35 categories. In terms of solar, PV-25 is the most dominant category in Europe; there are only small amounts of PV-15 in South Europe.

When evaluating the model results with regard to the transport of energy, it should be noted that the modeling carried out here works with a greenfield approach. This means that the existing infrastructure is not considered in the model.

According to the results of the model, electricity transport takes place only within Europe. That is because electricity has high specific transport costs, as has been stated above when discussing the import ratios. The model results show that transport via onshore pipelines is the preferred option due to the lower specific costs of transport compared to tankers. The break-even-distance of pipeline versus tanker costs depends on the assumed costs. Cost data vary strongly among the literature. The data used here (which are documented in the supplemental material) lead to a preference for pipelines for both gaseous and liquid energy carriers, while tanker transport plays a clearly subordinate role and is only used for synthetic kerosene and, to a very small extent, for synthetic naphtha. Tanker transport takes place between the South Arabia cluster and northern Europe, since, as mentioned above, South Arabia shows very favorable generation potentials, which compensates for the higher transport costs. Due to the long distance, the tanker is superior to pipelines on this route.

In general, the conversion steps in the power-to-x chain take place as far as possible at the point of generation, and the transport of intermediate products is avoided. There is a tendency that the further energy carriers are processed, the longer transport distances are accepted. That is because on the one hand, specific transmission costs are lower for liquid energy carriers such as gasoline or diesel compared to those of hydrogen or electricity, and on the other hand, there is more energy required for the production process, so that favorable production conditions become even more important.

The model results show that for technologies for PtX production, in most cases there is one advantageous technology from the model’s perspective. The preferred technologies are vaporization for water production, SOEL for electrolysis, DAC-LT for CO2 capture and high-temperature-co-electrolysis for production of synthesis gas. But regionally, also other technologies are used to a small extent according to the modeling results: reverse osmosis in Algeria and AEL electrolysis in Maghreb without Tun/Alg in 2030 and 2040 respectively. Thereby, especially the efficiency of a process and the option to cover part of the process energy demand with low temperature heat as a by-product of other processes is crucial and decisive for technology choice: SOEL electrolysis and vaporization are chosen despite higher investments costs, but higher efficiency; in case of vaporization, electrical efficiency is especially higher due to the usage of low temperature heat which is provided as by-product of other processes. However, for fuel synthesis, the results of the model show a mix of production technologies. This is mainly due to the fact that a variety of synthetic fuels is analyzed in this study, for which only one production technology is considered. The FT products gasoline, diesel, kerosene and naphtha can be produced by two pathways–LT and HT-FT synthesis; gasoline, diesel and kerosene can additionally be produced by methanol synthesis followed by a methanol-to-X process. Thus, the capacities of each technology are mainly determined by the output ratios of the FT pathways compared to the ratio of demand as well as the technological availability readiness level of the technologies.

3.2 Robustness of results

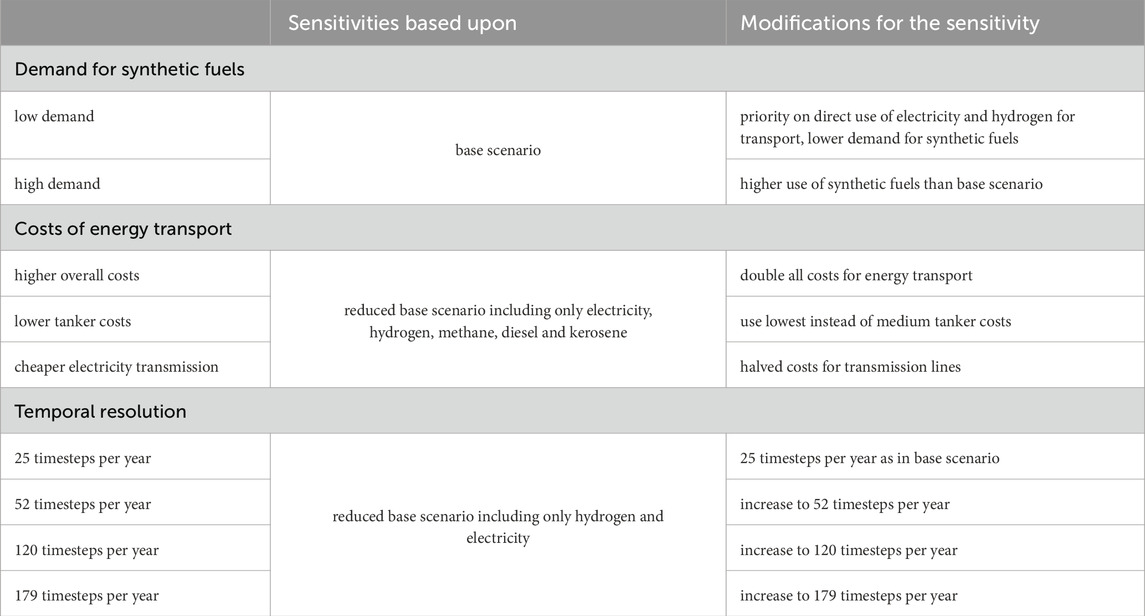

In order to assess the uncertainties of these results, several sensitivity analyzes were performed. The impact of a deviating development of the demand for synthetic fuels, the influence of different assumptions on transport costs, as the data basis for these parameters has high fluctuation ranges, as well as the effect of a higher temporal resolution during the year has been considered (see Table 2).

Table 2. Overview over conducted sensitivity analyses.

The development of the demand for synthetic fuels is not predictable. Therefore, two additional different developments of demand have been applied as sensitivities, one representing a very low demand (via a focus on direct electrification), and the other one representing a rather high use of synfuels. These sensitivities show that the selected supplier countries (Maghreb w/o Tun/Alg, Algeria, Egypt, Middle East, South Arabia) are rather robust against different developments in the demand for synthetic fuels. In case of a very high demand for liquid fuel, Libya is an additional supplier country. If on the other hand the fuel demand is lower and the share of electricity in the transport sector’s consumption is higher, a higher electricity production in Europe and lower production volumes of synfuels in MENA are observed.

There is a wide range in the literature for the costs of infrastructures for energy transport. Therefore, the impact of different costs assumptions is discussed here. It can be observed that an overall increase in transport costs has an impact on import quotas and on the internal ratio of production sites in the MENA region: Especially fuels with high specific transport costs are produced in or close to Europe to a larger extent. Lower costs for tanker transport lead to a shift from pipelines to tankers for liquid fuels. That leads to the conclusion that the modeling results in the base scenario regarding the use of pipelines or tankers are subject to uncertainties. However, despite the different modes of transport, there are only very minor shifts in the regional distribution of production. Similarly, lower cost assumptions for electricity transmission result in a slight increase in transported electricity, but have only minor influence on the regions of energy production. Lower costs for hydrogen pipeline transport lead to a shift in energy transport routes for hydrogen, causing shifts also in the other carriers. These results show that, despite possible shifts in the forms of transport, the choice of exporting regions and the amount of energy produced there is rather robust to individual variations in transport costs, i.e., when the internal ratios of transport costs change. Only a significant increase in all transport costs leads to a change in the role of the production regions and to lower import shares. This leads to the conclusion that the regional characteristics of renewable electricity generation dominate the role of the generation regions and that the transport cost assumptions are of minor importance. The selection of supplier countries can therefore be considered robust against transport costs, but the form of transport is subject to uncertainties.

As described in Section 2.2.2, one measure to reduce model complexity is to limit the temporal resolution during the year to 25 timesteps per year. However, region-specific characteristics can be better represented at higher temporal resolutions, so this has an influence on the modeling results. Therefore, a sensitivity with reduced complexity but higher resolution has been performed to assess its influence. The results show that with increasing temporal resolution the energy generation shifts from MENA to Europe. While in a resolution of 25 h, 31% of the electricity generation takes place in MENA, this share decreases with an increasing resolution down to 18%. That is because the advantageous seasonal characteristic of wind energy comes into play more strongly with higher temporal resolution.

Together, there are the following implications for the robustness of the results: While the amount of imports from MENA depends on the development of synfuel demand and on the temporal resolution, the import plays a significant role in all these cases. The choice of exporting countries is largely robust, but depending on the development of demand or the costs of transport, single additional countries or regions could become relevant. The preference of pipelines over tanker transport is subject to uncertainties regarding the cost assumptions. The determination of which fuel is generated in a particular country is dependent on transportation expenses and the evolution of demand. However, aggregate energy generation within these countries remains relatively stable, except in the cases where there is a broad escalation in transportation costs.

3.3 Results in the risk scenarios considering investment risks

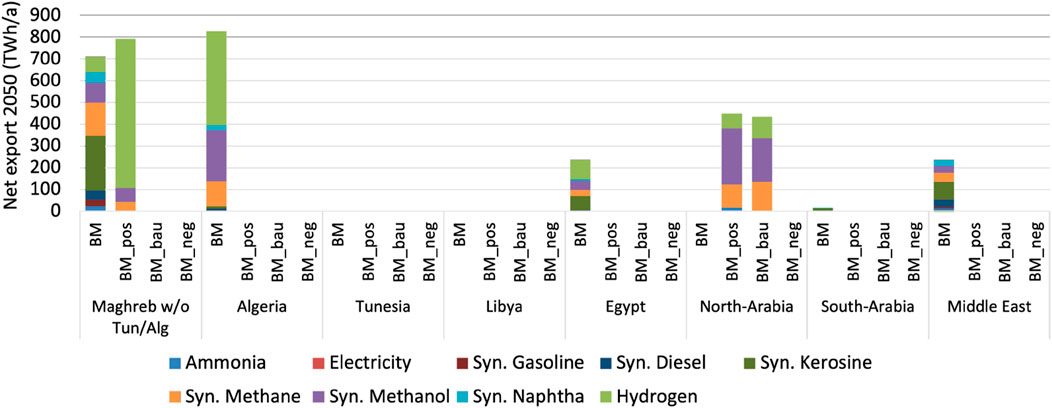

The base scenario analyzed above gives implications on the supply structures considering solely techno-economic criteria. However, investment risk is a relevant criterion for investment decisions. Thus, as a next step, investment risks both in MENA and Europe are explicitly accounted for within the technoeconomic modeling to examine the effects of investment risks on the synfuel supply structures (as described in Section 2.3). The results of these risk scenarios with respect to the German and European import quotas and export volume of MENA regions are shown in Table 3 and Figure 8, respectively. In these, results for the risk scenarios are displayed in comparison to the base scenario.

Table 3. Import quotas for whole Europe and Germany, 2050, scenarios base, BM_risk_pos, BM_risk_bau and BM_risk_neg.

Figure 8. Net export of energy, 2050, scenarios base, BM_risk_pos, BM_risk_bau and BM_risk_neg.

As can be seen in Table 3, the consideration of investment risks leads to lower import quotas for both DE and also, Europe as a whole and accompanying higher production volumes in DE and Europe, respectively. This is more pronounced, the higher the investment risks assumed for MENA are. Investment risks in most MENA regions are higher–even for the positive development of investment risks in MENA–than in large parts of Europe, especially in DE and in Northern and Western Europe. Thus, higher production within DE and Europe is economically attractive despite the higher generation costs of renewable electricity here. In case of a challenging development of investment risks, production even takes place completely in Europe according to the modeling results. This also implies that, under the given assumptions (see Section 2.1.3) - the renewable energy potential in Europe is sufficient to cover the future European demand for renewable electricity and synthetic fuels (unless the European demand rises significantly higher than assumed in the base scenario). In contrast, DE relies on imports also in case of a challenging development of investment risks. However, in the scenario BM_risk_neg, energy is solely imported from Europe; Northern and Western Europe are net exporters in this case. In contrast, in the base scenario, all European regions are net importers, which means that the net energy imports to both DE and the other European regions come from MENA. However, it should be noted that specific import flows cannot be traced in an integrated approach.

The consideration of investment risks also implies a shift in exporting MENA regions, as shown in Figure 8. In the base scenario, energy is mainly imported from countries in North Africa. In contrast, when considering investment risks, North-Arabia and - in case of a positive development of the investment risk - also, Maghreb without Tun/Alg are the exporting regions. This is mainly due to the low risk-assessed WACC data in these regions. This points out that investment risks - considered as WACC premiums - are a dominant factor for site decisions, which might compensate for other factors such as higher generation costs.

3.4 Sensitivity analysis with regard to investment risks

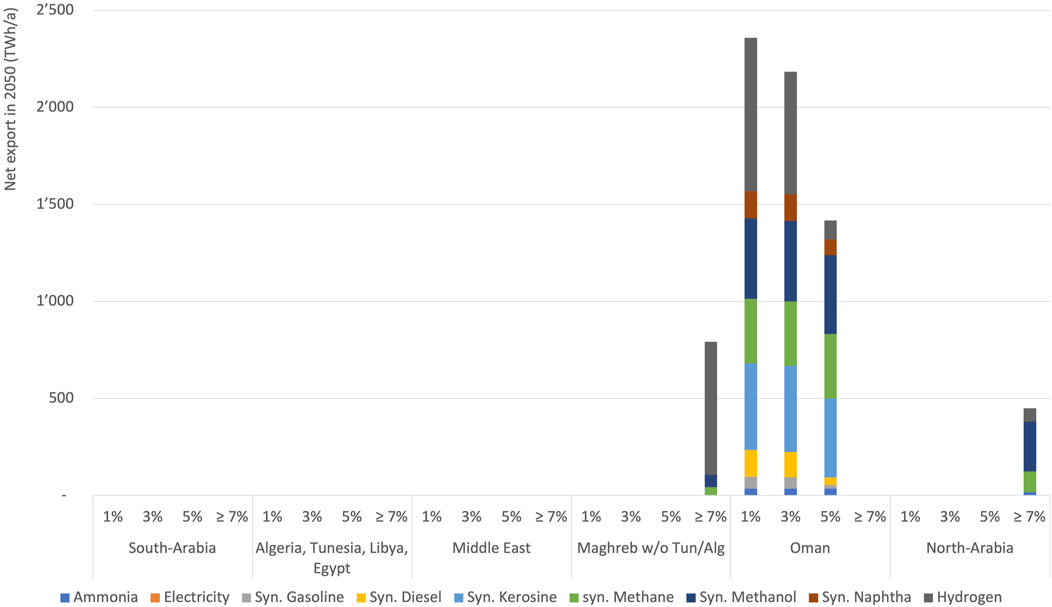

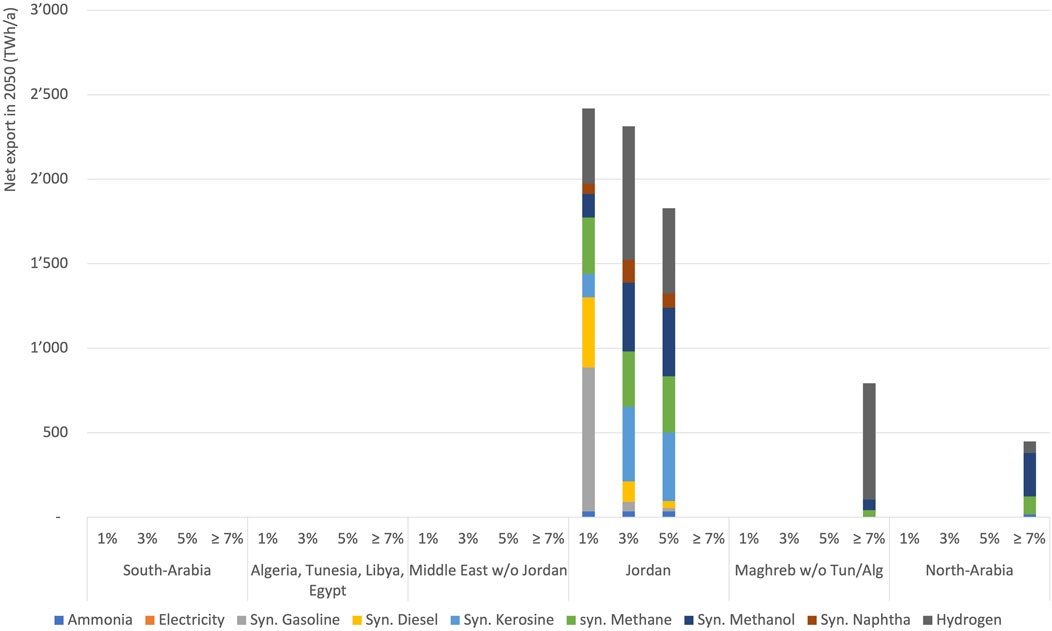

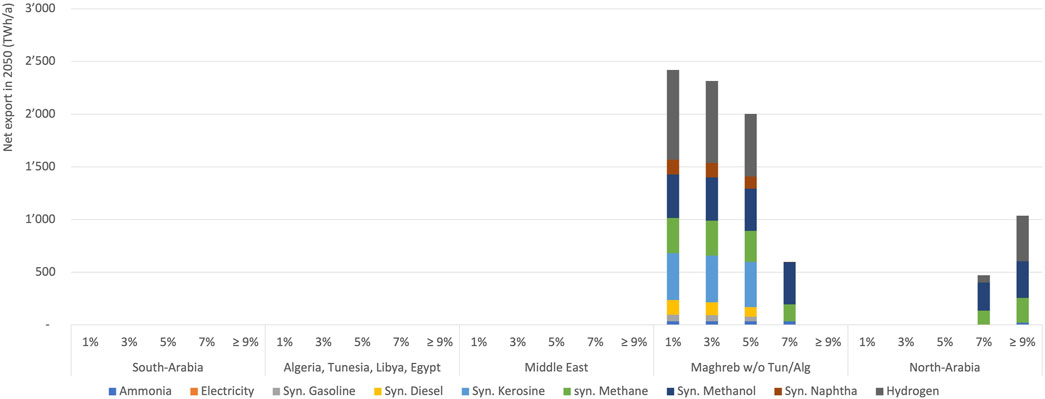

The analysis done above builds on assumptions on the future development of the investment risks–quantified as risk assessed WACC - in the different MENA regions. However, these future risk assessed WACC data are subject to uncertainty. Furthermore, capital costs might be reduced in the future, e.g., by the long-term promotion of investments. Thus, in the following, the sensitivity of the results with respect to the risk assessed WACC will be analyzed. For this, the risk assessed WACC is varied exemplary for the MENA regions Oman, Jordan and Maghreb without Tun/Alg in the range between 1% and 13% each. Thus, investment cost data for the other MENA and European countries are assumed as in the scenario with a positive risk development. The results of this sensitivity analysis are shown in Figures 9–11. As can be seen in the figure, a lower risk assessed WACC of up to 5% leads to a production change in regions with low risk assessed WACC. Thus, production is completely shifted from the supplying MENA regions in the default case, North-Arabia, and in the case of the sensitivity analysis for Oman and Jordan also Maghreb without Tun/Alg–and partly from Europe. Consequently, European import quotas for energy from MENA are higher. This is even more pronounced, the lower the risk assessed WACC in the MENA regions. It should be noted that for Maghreb without Tun/Alg–in contrast to Oman and Jordan–production and therefore export take place for a risk assessed WACC of up to 7%. 7% corresponds approximately to the default risk assessed WACC of Maghreb without Tun/Alg in the scenario BM_risk_pos. Thus, supplying structures for a risk assessed WACC of 7% are similar to the results with the default risk assessed WACC. Especially, in this case, Maghreb without Tun/Alg is not the only exporting MENA region, energy is also exported from North-Arabia. In summary, the results of the sensitivity analysis foster the conclusion above that investment risks–quantified as risk assessed WACC–have a high impact on economically advantageous exporting MENA regions. Further criteria, such as transportation distance or feed-in characteristics of renewable electricity generation, are also relevant. This is pointed out by the sensitivity analysis for Maghreb without Tun/Alg. However, the level of risk assessed WACC is the dominating factor and might outweigh other criteria as long as risk assessed WACC are low enough.

Figure 9. Net export of energy, 2050, sensitivity of WACC for Oman.

Figure 10. Net export of energy, 2050, sensitivity of WACC for Jordan.

Figure 11. Net export of energy, 2050, sensitivity of WACC for Maghreb without Tun/Alg.

4 Conclusions and outlook

Due to the high potential for renewable energy at low generation costs in MENA, the MENA region might play a pivotal role in supplying Germany and whole Europe with renewable energy. Thus, especially the export of synthetic fuels is an attractive option because of comparatively low transport costs. This offers the opportunity to the MENA region to build the complete value chain from electricity generation up to fuel synthesis within the region. If investment risks are considered, however, the significance of exports from MENA to Europe diminishes, since higher investment risks in MENA outweigh the lower renewable energy generation costs. Thereby, it is interesting to note that the renewable energy potential in Europa is sufficiently high under the given assumptions to cover the future demand for renewable electricity and synthetic fuels, unless this demand rises significantly higher than expected in the base scenario.

Almost all MENA regions have great solar energy potentials at low costs, but the availability of wind energy generation potentials is a location advantage, and so is a short distance to Europe. However, restrictively, it should be noted that these factors should not be overestimated. First, transport costs do not seem to have such a large influence on exporting regions, as can be seen from the sensitivity analyses. Second, due to the low temporal resolution, feed-in characteristics of the renewable energy cannot be mapped adequately. This could distort the results for the MENA exporting regions. This holds especially due to the fact that almost all MENA regions have PV potentials with high capacity factors and differences are therefore small. However, the factor risk investments might outweigh other factors such as transportation costs or feed-in characteristics of renewable energy. These results clearly point out that it is crucial to consider country-specific investment risks within techno-economic modeling.

The conveyance of energy in its final form is favored over the transport of intermediate products, attributable to reduced transportation expenses and a more effective utilization of the advantageous energy generation capacities in the exporting regions. Pipeline transport is preferred over tanker transport in the modeling results. However, it should be noted that the transport costs are subject to uncertainty, and thus also the break-even distance, at which pipeline and tanker transport have the same costs, is subject to uncertainty.

In terms of conversion technologies, especially the efficiency of a process and the option to cover part of the process energy demand with low-temperature heat as a by-product of other processes are crucial for technology choice. These results also stress that it is necessary to explicitly depict by-products in energy system modeling. However, limiting, it must be noted that the assumptions regarding future efficiencies and costs are subject to uncertainty. Furthermore, further criteria, which are out of the scope of the present techno-economic modeling, should be considered to be relevant in practice in terms of technology choice. Concluding, these results point out that it is crucial to not focus on a few technologies, but rather expedite the development of a broad set of technologies. As can be seen from the modeling results, significant capacity for synfuel production would be necessary already in 2030. For this, scaling of these technologies and cost reductions are necessary.

In general, it is important to note that these results are based on modeling. As a model can never capture the full complexity of the real world, the results need to be carefully categorized and complemented with additional knowledge to derive recommendations for action. This concerns, for example, the inclusion of industrial policy aspects, security of supply, and diversification issues, but also, in particular, social factors. Further research is also needed on the technical modeling itself:

The work carried out here is based on the previous climate protection target, which envisaged a 95% reduction in GHG by 2050. It would have to be adapted to the updated target, which envisages complete greenhouse gas neutrality in the EU by 2050 and in Germany by 2045. The implications resulting from this higher ambition, for example, on the expansion rate of renewable energy generation and cogeneration plants, would have to be analyzed.

Energy transport within regions is not taken into account in the WISEE-ESM-I model. This leaves questions unanswered as to where installations of RE and conversion plants should be located within the regions and what infrastructure expenditures would be associated. For example, power generation plants would be more likely to be located in the inland, while locations close to ports or pipelines could be advantageous for the production of hydrogen or synthetic fuels.

The analysis does not address the question of which countries will be able to meet the rigorous standards of the EU for green hydrogen and synthetic fuels.

To come to a realistic assessment of the export potential from MENA countries, a more in-depth analysis is required, considering their perspectives. This includes evaluating opportunities for local value chain development, sustainability concerns (including social factors), and optimal site selection. By integrating the findings of these analyses with the results of the model, it could be possible to identify supply pathways that may prioritize overall sustainability over economic efficiency.

It should also be considered that there are potential exporters of synthetic fuels outside the MENA region, such as Chile or Australia. It should be analyzed how the role of the MENA region changes if the regional scope is expanded accordingly.

Finally, it should be noted that the deterministic WISEE-ESM-I model can show penny-flip effects, where small differences in the input data lead to significant preferences for individual technologies or regions that are not justified in this clarity. In addition, uncertainties cannot be taken into account in the model. A better handling of these aspects could improve the validity and robustness of the results.

Data availability statement

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

Author contributions

CK: Conceptualization, Investigation, Methodology, Project administration, Software, Supervision, Visualization, Writing–original draft, Writing–review and editing. LD: Conceptualization, Data curation, Investigation, Methodology, Software, Validation, Writing–original draft. TJ: Conceptualization, Data curation, Methodology, Software, Validation, Writing–original draft. MS: Conceptualization, Investigation, Methodology, Software, Writing–original draft. AN: Funding acquisition, Investigation, Methodology, Project administration, Supervision, Writing–original draft. PV: Conceptualization, Supervision, Writing–review and editing.

Funding

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. The authors gratefully acknowledge the financial support of the German Federal Ministry for Economic Affairs and Climate Action (grant no. 3EIV181A). The sole responsibility for the content of this paper lies with the authors.

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Generative AI statement

The author(s) declare that no Generative AI was used in the creation of this manuscript.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Supplementary material

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenrg.2025.1524907/full#supplementary-material

Abbreviations

AEL, alkaline water electrolysis; BM_risk_pos, base scenario plus positive development of investment risk; BM_risk_bau, base scenario plus business-as-usual development of investment risk; BM_risk_neg base scenario plus negative development of investment risk; CO2, carbon dioxide; CSP, concentrated solar power; DAC, direct air capture; DE, Germany; ESM-I, Energy Supply Model - Invest Module; FT, Fischer-Tropsch; GHG, greenhouse gas; H2, hydrogen; HT, high temperature; LCOE, levelized cost of electricity; LT, low temperature; MENA, Middle East and Northern Africa; OSeMOSYS, Open Source Energy Modeling System; PEM, polymer electrolyte membrane electrolysis; PV, photovoltaics; PtX, Power-to-X; RE, renewable electricity; RWGS, reverse water-gas shift reaction; SOEL, solid oxide electrolysis; WACC, Weighted Average Cost of Capital; WISEE, Wuppertal Institute System Model Architecture for Energy and Emission Scenarios.

References

AG Energiebilanzen (2024). Auswertungstabellen zur Energiebilanz Deutschland - Daten für die Jahre von 1990 bis 2023. Available online at: https://ag-energiebilanzen.de/daten-und-fakten/auswertungstabellen/.

Berger, M., Radu, D., Detienne, G., Deschuyteneer, T., Richel, A., and Ernst, D. (2021). Remote renewable hubs for carbon-neutral synthetic fuel production. Front. Energy Res. 9. doi:10.3389/fenrg.2021.671279

Braun, J., Kern, J., Scholz, Y., Hu, W., Moser, M., Schillings, C., et al. (2022). Technische und risikobewertete Kosten-Potenzial-Analyse der MENA-Region. Wuppertal, Stuttgart, Köln, Saarbrücken: MENA-Fuels: Teilbericht 10 des Deutschen Zentrums für Luft- und Raumfahrt (DLR) und des Wuppertal Instituts an das Bundesministerium für Wirtschaft und Klimaschutz (BMWK). Technical report.

Bründlinger, T., König, J. E., Frank, O., Gründig, D., Jugel, C., Kraft, P., et al. (2018). Dena-leitstudie integrierte energiewende. Tech. Rep. Dtsch. Energie-Agentur GmbH (dena). Available online at: https://shop.dena.de/fileadmin/denashop/media/Downloads_Dateien/esd/9261_dena-Leitstudie_Integrierte_Energiewende_lang.pdf.

Capros, P., Zazias, G., Evangelopoulou, S., Kannavou, M., Fotiou, T., Siskos, P., et al. (2019). Energy-system modelling of the eu strategy towards climate-neutrality. Energy Policy 134, 110960. doi:10.1016/j.enpol.2019.110960

Cavana, M., and Leone, P. (2021). Solar hydrogen from north africa to europe through greenstream: a simulation-based analysis of blending scenarios and production plant sizing. Int. J. Hydrogen Energy 46 (43), 22618–22637. ISSN 0360-3199. doi:10.1016/j.ijhydene.2021.04.065

Colbertaldo, P., Guandalini, G., and Campanari, S. (2018). Modelling the integrated power and transport energy system: the role of power-to-gas and hydrogen in long-term scenarios for Italy. Energy 154, 592–601. ISSN 0360-5442. doi:10.1016/j.energy.2018.04.089

Dominković, D. F., Bačeković, I., Pedersen, A. S., and Krajačić, G. (2018). The future of transportation in sustainable energy systems: opportunities and barriers in a clean energy transition. Renew. Sustain. Energy Rev. 82, 1823–1838. ISSN 1364-0321. doi:10.1016/j.rser.2017.06.117

Eddy, J., Genge, L., and Muesgens, F. (2022). “H2europe: an analysis of long-term hydrogen import potentials from the mena region,” in 2022 18th international conference on the European energy market (EEM), USA, 13th to 15th of September 2022, 1–7. doi:10.1109/EEM54602.2022.9921055

Eurostat (2022). Greenhouse gas emissions by source sector. Available online at: https://ec.europa.eu/eurostat/databrowser/view/ENV_AIR_GGE__custom_1300599.

Eurostat (2024). Final energy consumption in transport - detailed statistics. Available online at: https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Final_energy_consumption_in_transport_-_detailed_statistics.

Evangelopoulou, S., De Vita, A., Zazias, G., and Capros, P. (2019). Energy system modelling of carbon-neutral hydrogen as an enabler of sectoral integration within a decarbonization pathway. Energies 12 (13), 2551. ISSN 1996-1073. doi:10.3390/en12132551

Fasihi, M., Bogdanov, D., and Breyer, C. (2017). Long-term hydrocarbon trade options for the maghreb region and europe—renewable energy based synthetic fuels for a net zero emissions world. Sustainability 9 (2), 306. ISSN 2071-1050. doi:10.3390/su9020306

Franz, T., and Müller-Steinhagen, H. (2007). The DESERTEC concept-sustainable electricity and water for Europe, Middle East and North Africa, 23–43.

Fraunhofer IFAM, DLR, and GWI (2020). Multi-Sektor-Kopplung - Modellbasierte Analyse der Integration Erneuerbarer Stromerzeugung durch die Kopplung der Stromversorgung mit dem Wärme, Gas-und Verkehrssektor. Tech. Rep. Available online at: https://elib.dlr.de/135971/1/MuSeKo-Endbericht-2020-08-31.pdf.

Grant Wilson, I. A., and Styring, P. (2017). Why synthetic fuels are necessary in future energy systems. Front. Energy Res. 5. ISSN 2296-598X. doi:10.3389/fenrg.2017.00019

Horst, J., and Klann, U. (2022). “MENA-Fuels - Analyse eines globalen Marktes für Wasserstoff und synthetische Energieträger hinsichtlich künftiger Handelsbeziehungen,” in Teilbericht 12 an das Bundesministerium für Wirtschaft und Klimaschutz (BMWK). Wuppertal, Stuttgart, Saarbrücken: Technical report, Wuppertal Institut, DLR, IZES.

Howells, M., Rogner, H., Strachan, N., Heaps, C., Huntington, H., Kypreos, S., et al. (2011). OSeMOSYS: the open source energy modeling system. Energy Policy 39 (10), 5850–5870. ISSN 0301-4215. doi:10.1016/j.enpol.2011.06.033

Jan, M., Poltrum, M., and Ulrich, B. (2019). The role of renewable fuel supply in the transport sector in a future decarbonized energy system. Int. J. Hydrogen Energy 44 (25), 12554–12565. ISSN 0360-3199. doi:10.1016/j.ijhydene.2018.10.110

Jeroen Dommisse and Jean-Louis Tychon (2020). Modelling of low carbon energy systems for 26 european countries with EnergyScopeTD: can european energy systems reach carbon neutrality independently? PhD thesis, UCL - Ecole Polytech. Louvain. Available online at: http://hdl.handle.net/2078.1/thesis:25202.

Korkmaz, P., Gardumi, F., Avgerinopoulos, G., Blesl, M., and Ulrich, F. (2020). A comparison of three transformation pathways towards a sustainable european society - an integrated analysis from an energy system perspective. Energy Strategy Rev. 28, 100461. ISSN 2211-467X. doi:10.1016/j.esr.2020.100461

Lux, B., Gegenheimer, J., Franke, K., Sensfuß, F., and Pfluger, B. (2021). Supply curves of electricity-based gaseous fuels in the mena region. Comput. and Industrial Eng. 162, 107647. ISSN 0360-8352. doi:10.1016/j.cie.2021.107647

Pregger, T., Schiller, G., Cebulla, F., Dietrich, R.-U., Maier, S., Thess, A., et al. (2020). Future fuels—analyses of the future prospects of renewable synthetic fuels. Energies 13 (1), 138. ISSN 1996-1073. doi:10.3390/en13010138

Prognos (2020). “Öko-Institut, and Wuppertal Institut. Klimaneutrales Deutschland - In drei Schritten zu null Treibhausgasen bis 2050 über ein Zwischenziel von -65% im Jahr 2030 als Teil des EU-Green-Deals Studie (im Auftrag von Agora Energiewende, Agora Verkehrswende und Stiftung Klimaneutralität),” in Technical report, Agora Energiewende, Agora Verkehrswende und Stiftung Klimaneutralität (Berlin, Wuppertal). Available online at: https://static.agora-verkehrswende.de/fileadmin/Projekte/2020/KNDE2050/A-EW_195_KNDE_Langfassung_DE_WEB.pdf.

Razi, F., and Dincer, I. (2022). Renewable energy development and hydrogen economy in mena region: a review. Renew. Sustain. Energy Rev. 168, 112763. ISSN 1364-0321. doi:10.1016/j.rser.2022.112763

Ridjan, I., Vad Mathiesen, B., Connolly, D., and Duić, N. (2013). The feasibility of synthetic fuels in renewable energy systems. Energy 57, 76–84. ISSN 0360-5442. doi:10.1016/j.energy.2013.01.046

Royal Institute of Technology (KTH) (2022). OSeMOSYS documentation. Available online at: https://osemosys.readthedocs.io/en/latest/manual/StructureSYS.html.

Saurat, M., Doré, L., Janßen, T., Kiefer, S., Krüger, C., and Nebel, A. (2024). “Description of the energy supply model WISEE-ESM-I,” in MENA-fuels: sub-report 4 to the FederalMinistry of economic Affairs and climate action (BMWK) (Wuppertal, Stuttgart, Köln, Saarbrücken: Technical report).

Schneider, C., Boer, H.-S. de, van Sluisveld, M., Hof, A., Vuuren, D. van, and Lechtenböhmer, S. (2018). EU decarbonisation scenarios for industry - deliverable 4.2, REINVENT. Tech. Rep.

Terrapon-Pfaff, J., Raquel Ersoy, S., Prantner, M., and Viebahn, P. (2024). Country risks analysis for the development of green hydrogen and synthetic fuel sectors in the MENA region. Front. Energy Res. 12. ISSN 2296-598X. doi:10.3389/fenrg.2024.1466381

Thomas, P. (2022). “Szenarien zur Eigenbedarfsanalyse für die MENA-Länder,” in MENA-Fuels: Teilbericht 9 des Deutschen Zentrums für Luft-und Raumfahrt (DLR) an das Bundesministerium für Wirtschaft und Klimaschutz (BMWK). Wuppertal, Stuttgart, Köln, Saarbrücken: Technical report.

Timmerberg, S., and Kaltschmitt, M. (2019). Hydrogen from renewables: supply from north africa to central europe as blend in existing pipelines – potentials and costs. Appl. Energy 237, 795–809. ISSN 0306-2619. doi:10.1016/j.apenergy.2019.01.030

Keywords: defossilization, transport sector, synthetic fuels, import, modeling, investment risks, mena, europe

Citation: Krüger C, Doré L, Janßen T, Saurat M, Nebel A and Viebahn P (2025) Providing the transport sector in Europe with fossil free energy - a model-based analysis under consideration of the MENA region. Front. Energy Res. 13:1524907. doi: 10.3389/fenrg.2025.1524907

Received: 08 November 2024; Accepted: 25 February 2025;

Published: 19 March 2025.

Edited by:

Yirui Wang, Ningbo University, ChinaCopyright © 2025 Krüger, Doré, Janßen, Saurat, Nebel and Viebahn. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Christine Krüger, Y2hyaXN0aW5lLmtydWVnZXJAd3VwcGVyaW5zdC5vcmc=