Shixian Ling

Shixian Ling Hongfu Gao

Hongfu Gao

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Energy Res. , 05 June 2023

Sec. Sustainable Energy Systems

Volume 11 - 2023 | https://doi.org/10.3389/fenrg.2023.1177927

This article is part of the Research Topic Enabling technologies and business models for energy communities View all 15 articles

Chinese heavy-polluting companies have been facing enormous challenges in responding to climate risk and energy transformation. This paper uses panel regression model and investigates the impact of climate risk on corporate green innovation in Chinese heavy-polluting listed companies from 2011 to 2020. The empirical results show that climate risk adversely affects green innovation in heavy-polluting companies, and this effect persists throughout a series of robustness and endogeneity tests. Climate risk may affect corporate green innovation through decreasing R&D investment, lowing resource allocation efficiency and increasing company risk. Climate risk has a greater negative impact on mid-western, state-owned and large-size heavy-polluting companies, but can be mitigated by the development of green finance, digital finance and marketization. These findings may help heavy-polluting companies fully utilize existing resources, policies, and channels for green innovation and mitigate climate risks.

Climate risk is becoming an unprecedented threat that has a pronounced impact on the sustainability of human lives, natural resources and economic development (Eckstein et al., 2021; Ren et al., 2022; Venturini, 2022; Wagner, 2022; Estrada et al., 2023). According to the China Social Statistical Yearbook 2022 released by the National Bureau of Statistics of China, in 2021, over 107.31 million people are affected by climate events, and direct economic losses totaled around USD 48.28 billion due to extreme weather events in China. The previous researches note that climate risk is becoming an unprecedented threat to Chinese corporate behavior, such as sales and operating revenue (Lin and Sheng, 2022; Chen et al., 2023), investment (Rao et al., 2022a), financing cost (Shih et al., 2021; Huang et al., 2022; Zhou et al., 2022) and environmental strategic decision (Ren et al., 2022).

In Chinese heavy-polluting companies, green innovation is an important component of corporate behavior, especially in the face of severe climate risks and strict climate policies (Rao et al., 2022b; Khalfaoui et al., 2022; Li and Gao, 2022). It is widely known that, in 2020, Chinese President Xi Jinping announced that China would strive to peak its carbon emissions by 2030 and achieve carbon neutrality by 2060. This is the first time that China has announced a definite timeline for carbon neutrality to the rest of the world, and it is also the largest climate pledge made by all countries to date. As important key sources and stakeholders in the conflict between environmental protection and economic interest, heavy-polluting companies must find a way to assume a high degree of environmental responsibility for their polluting activities (Walter and Chang, 2020). In this context, many heavy-polluting companies are forced to transform and upgrade with the help of green innovation, which is innovative activity to improve resource utilization efficiency and reduce energy consumption and is usually characterized by high risk, high cost and high return (Schiederig et al., 2012; Rao et al., 2022a; Li and Gao, 2022).

Although there are numerous studies about the impact of climate risk on corporate behavior (Shih et al., 2021; Yu et al., 2022a; Rao et al., 2022b; Huang et al., 2022; Lin and Sheng, 2022; Zhou et al., 2022; Ahmad et al., 2023; Lee et al., 2023; Ozkan et al., 2023), research on the impact of climate risk on corporate green innovation is very limited and controversial. On the other hand, climate risk will inevitably bring varying degrees of damage to corporations, thereby directly or indirectly affecting green innovation. For example, climate risk can directly destroy corporate equipment or fixed assets (Rao et al., 2022a; Xu et al., 2022) and block the supply channel (Godde et al., 2021; Pankratz and Schiller, 2021), which hinders corporate green innovation. Climate risk can also prompt the government to tighten environmental laws, forcing heavy-polluting companies to increase production and financing costs (Shih et al., 2021; Dong et al., 2022; Zhou et al., 2022), and indirectly affecting their investment in green innovation. On the other hand, the strategic growth options model indicates uncertainty such as climate risk may breed potential growth opportunities, prompting corporations to increase investment to obtain greater market competition (Kulatilaka and Perotti, 1998). Green innovation, as an important means of gaining greater market competition, will also attract more investment. It appears that climate risk may also have some indirect and potential promoting effects on green innovation, although there is a lack of direct evidence. Therefore, it is necessary to conduct in-depth research on the impact of climate risk on corporate green innovation.

This paper tries to extend the existing research by investigating the impact of climate risk on green innovation in Chinese heavy-polluting listed companies. To examine how climate risk affects green innovation, mediating effect models are proposed. Empirical findings show extreme climate events significantly hinder green innovation in heavy-polluting companies, and this negative effect persists throughout a series of robustness tests. The mechanism analysis reveals that research and development (R&D) investment, resource allocation efficiency and company risk are three potential mediating variables. The heterogeneity analysis demonstrates climate risk has a greater negative impact on midwestern, state-owned, and large companies. However, it is noteworthy that, the development of green finance, digital finance, and marketization can further promote heavy-polluting companies to actively explore green innovation and reduce the negative impact of climate risk.

This paper contributes to the literature in three aspects. First, the existing literature primarily focuses on the impact of a single index like temperature when evaluating the micro-level consequence of climate change. But the manifestations of different types of climate risk are different, not only in the form of temperatures (Lin and Sheng, 2022). This research studies the influencing factors of corporate green innovation in heavy-polluting companies from the perspective of extreme climate events and provides new theoretical and empirical evidence of corporate responses to climate risk. This will aid heavy-polluting companies in emerging markets like China to recognize the impact of climate risk on green innovation and take action. Second, this paper performs heterogeneity analyses on the influence of climate risk on the green innovation of different heavy-polluting companies. It will help the state and local governments provide targeted policy support for heavy-polluting companies in different regions, company ownership and size, to encourage corporate green innovation and resist climate risks. Third, it identifies the potential mechanism behind the negative impact of climate risk on corporate green innovation. Empirical findings may help heavy-polluting companies make full use of available resources, policies and channels to carry out green innovation, thus reducing the premium of green products and the cost of coping with climate risk.

The remainder of this paper is organized as follows. Section 2 develops the hypothesis based on the literature review. Section 3 describes the sample and research methods. Section 4 discusses the empirical results. Section 5 examines the influence mechanism, and Section 6 further analyses the heterogeneity and moderating effects. The final part concludes and provides policy implications.

Numerous studies have shown the significant impact of climate risk on corporate behavior, such as corporate profitability (Hugon and Law, 2019; Addoum et al., 2020; Anton, 2021; Chen et al., 2023), investment (Rao et al., 2022b), financing management (Huang et al., 2022), environmental performance (Ren et al., 2022; Sautner et al., 2023), but research on the impact of climate risk on corporate green innovation is very limited and controversial.

On the other hand, climate risk will inevitably bring varying degrees of damage to corporations, thereby directly or indirectly affecting green innovation. From the perspective of direct effect, climate risk is generally associated with the full or partial destruction of equipment or fixed assets of corporates (Rao et al., 2022a; Xu et al., 2022) and block of the supply channel (Godde et al., 2021; Pankratz and Schiller, 2021), which will abate the efficiency and ability of corporate green innovation. Corporations have to adjust the original resource allocation planning to maintain their operation. From the perspective of indirect effect, climate risk has compelled the government to take further measures to combat environmental pollution, resulting in stronger and improved environmental policies. These policies will prohibit firms from using low-cost but high-polluting energy sources (Dong et al., 2022) and restrict the availability of traditional credit to polluting companies. (Shih et al., 2021; Zhou et al., 2022). This will lead to an increase in financing costs (Shih et al., 2021; Zhou et al., 2022) and a decrease in available funds, thereby affecting corporate investment in green innovation. Besides, climate risk will also urge companies to change their strategies, making them more inclined to hold high liquidity assets such as cash to insist on potential climate risk and reduce available resources for corporate green innovation. Huang et al. (2022) demonstrate that corporates characterized by several climate risks prefer to hold more cash rather than high-risk investment and thereby increase corporate resilience to climate risk.

On the one hand, the strategic growth options model indicates that uncertainty such as climate risk may breed potential growth opportunities, prompting corporations to increase investment to obtain greater market competition (Kulatilaka and Perotti, 1998). Green innovation, as an important means of gaining greater market competition, will also attract more investment. For example, Hugon and Law (2019) show that some corporates will benefit from unusually warm climate because of diversified operation strategy and climate lobby. Sautner et al. (2023) demonstrate that climate risk provides opportunities for renewable energy, electric cars, or energy storage corporates. Rao et al., 2022b find some corporates will stimulate investment after the experience of excess rainfall to regain market competition. Yu et al. (2022b) illustrate that climate risk can significantly improve the investment efficiency of renewable energy firms. It appears that climate risk may also have some indirect and potential promoting effects on green innovation, although there is a lack of direct evidence.

Given the majority of research findings, we propose a hypothesis that needs to be tested for heavily polluting enterprises in China.

H1:. Climate risk has a negative impact on corporate green innovation of heavy-polluting companies.

Previous studies have shown that climate risk can affect corporate green innovation through three channels, including R&D investment, resource allocation efficiency, and company risk.

First, climate risk could reduce corporate profits (Lin and Sheng, 2022; Pankratz et al., 2023), impair the supply chain (Godde et al., 2021; Pankratz and Schiller, 2021), increase operation cost (Hugon and Law, 2019) and harm corporate credit reputation (Capasso et al., 2020), thereby decreasing available funds for high-risk green innovation R&D investments. Second, climate risk will have a direct impact on corporate allocative efficiency of resources. Extreme climate events have a direct impact on corporate tangible assets (Ding et al., 2021) and may damage the equipment and environment required for R&D activities. Unlike traditional economic risks, climate risk will harm human health (McMichael et al., 2006) and attenuate labor supply and production efficiency (Dasgupta et al., 2021; Zhang et al., 2023). The decline in labor supply and productivity will abate the efficiency and ability of corporate green innovation. Third, climate risk also results in a change in corporate strategy (Huang et al., 2022) and forces corporates to postpone high-risk green innovation R&D investment. Previous research has shown that managers are typically risk averse because they are prepared to implement more robust operating strategies to avoid the potential adverse impact of high risks on their careers and salaries (Amihud and Lev, 1981; Gormley and Matsa, 2016). When the potential company risk is very high, its management may take low-risk operating activities rather than high-risk innovations to hedge risk. Climate risk will cause an increase in company risk, which will make a company tend to hold more cash (Huang et al., 2022) and reduce high-risk R&D investments to improve its climate resilience. Based on these previous research findings, this paper proposes the second hypothesis to be tested.

H2:. Climate risk negatively impacts corporate green innovation of heavy-polluting companies through decreasing R&D investment, lowing resource allocation efficiency, and increasing company risk.

According to previous research, the impact of climate risk on different companies is heterogeneous and mainly depends on company-specific factors such as location, ownership and size (Ren et al., 2022).

First, the natural environment, economic development and environmental policies in different regions of China vary significantly. The central and western regions are more susceptible to extreme climate events such as droughts, sandstorms and landslides (Ren et al., 2022), which could result in a more severe impact on corporate operating activities and assets. Du et al. (2021) note that when the economic development level is low, environmental regulation inhibits the development of green innovation, while the contrary is true when the level of economic development is high. Meanwhile, the eastern region’s financial market, infrastructure and environmental policies are superior to those of the central and western regions (Rao et al., 2022a), which could help companies mitigate the negative effect of climate risk.

Second, company ownership is one of the crucial factors affecting corporate strategy for resisting risk and improving environmental performance. Managers of state-owned companies prefer to avoid risk and select conservative operating activities to preserve their current position (Gao-Zeller et al., 2019; Gao et al., 2022). Meanwhile, state-owned companies need to assume more social and environmental protection responsibility, that is, pay higher costs for their pollution activities, thereby reducing their available resources.

Third, companies of different sizes may adopt different strategies to fend against external hazards. Prior research has shown that mid- and small-size companies are more flexible and adventurous than large-size companies under idiosyncratic risk, and are more willing to pursue high-risk, high-reward activities (Xu et al., 2022). Lin et al. (2019) find that small-size companies are more inclined to seek and access resources for green innovation because the return on green innovation investments for small-size companies is significantly higher than for larger-size companies. Therefore, non-state-owned and small-size companies may be more flexible to deal with climate risk and have a more proactive operating strategy, which decreases the negative impact of climate risk on corporate green innovation. Based on the above analysis, this paper proposes the third hypothesis.

H3:. Climate risk has a greater influence on mid-western, state-owned, and large-size heavy-polluting companies.

According to the industry classification list of listed companies in environmental verification issued by the former Ministry of Environmental Protection of China in 2008, we select the listed heavy-polluting companies in China1. The patent and green patent data are collected from the Chinese Research Data Services Platform (CNRDS). The financial data of the sampled companies comes from China Stock Market & Accounting Research Database (CSMAR). The sample interval is set between 2011 and 2020, as the fintech index has been available since 2011, while the climate risk index is usually released 2 years later. For example, the Global Climate Risk Index 2021 analyses what extent to countries and regions have been affected by the impacts of weather-related loss events in 2019. And Global Climate Risk Index 2022 is delayed due to a temporary lack of data and is expected to be published in 2023. The data are preprocessed as outlined below: 1) deleting ST and *ST companies; 2) erasing observations with incomplete data for critical variables. Additionally, to reduce the interference of outliers, we apply the Winsorize treatment of 1% and 99% quantiles for continuous financial indicators. Finally, 783 companies and 4,417 firm-year observations are taken as the final sample.

The explained variable is corporate green innovation, which is proxied by the number of green patent applications, following Tang et al. (2021), Rao et al., 2022b and Zhong and Peng (2022). Green patent applications that reflect the R&D investment in green innovation and emphasize the application of green innovation can more accurately represent a company’s green innovation capacity. Meanwhile, owing to the shorter time between the start of R&D and the filing of a patent application, the number of patent applications is timelier and more sensitive to innovation than the number of patent authorizations, and can better reflect the innovation intention and responses of companies. The number of green patent authorizations is adopted in the robustness analysis instead of green patent applications. We identify corporate green innovation by referring to the research of Wurlod and Noailly (2018). First, we begin by querying the corresponding intellectual property classification number (IPC) of each patent through SIPO based on all patents of the CSMAR and CNRDS databases. Second, the patents belonging to green patents are selected according to the IPC number in the green patent classification database published by the World Intellectual Property Organization (WIPO). Third, green patents are separated into green invention patents and green utility model patents according to the green patent classification database released by WIPO. Finally, we sum up the number of green invention patent applications and green utility model patent applications to present corporate green innovation. It is measured by taking the natural logarithm of the sum of the number of green patent applications.

The explanatory variable in this study is climate risk, proxied by the Germanwatch Climate Risk Index (CRI), which measures climate risk in terms of overall mortality from extreme climate events as well as relative and absolute economic damages2. It is constructed based on data from Munich Re NatCatSERVICE, which is one of the most reliable and complete databases about climate loss (Eckstein et al., 2021). The CRI is a score measured comprehensively by four indicators: fatalities, deaths per 100,000 inhabitants, losses on purchasing power parity, and loss per unit of GDP. A lower CRI score indicates that a region experiences more frequent and abnormal climate catastrophes. The CRI has been employed extensively in previous research, such as by Ding et al. (2021), Huang et al. (2018), Ren et al. (2022), and Xu et al. (2022), which use it to investigate the impact of climate risk on corporate revenue management, financial performance, carbon emissions, and risk-taking, respectively.

According to Huang et al. (2022), this paper develops a comprehensive index to measure provincial green finance by composing green credit (interest expense of six high heavy-polluting industries/total industrial interest expense), green investment (investment in environmental pollution control/GDP), green insurance (Agricultural insurance/gross agricultural output value) and government support (financial environmental protection expenditure/financial general budget expenditure). The weight of each index is estimated using the entropy weight approach. All the data are obtained from China Statistical Yearbooks, each province’s Statistical Yearbooks, and the China Insurance Yearbooks. Some missing data is substituted by the average value of the data from the previous 5 years.

The digital financial inclusion index released jointly by the Institute of Digital Finance at Peking University and the Ant Financial Services Group is chosen as a proxy for digital finance in this paper. It assesses the degree of digital finance in different regions of China from three perspectives: breadth of coverage, depth of usage, and level of digitization. The index can be used to quantify corporate capacity to access low-cost financial services and to represent the economic impact of China’s digital finance (Guo et al., 2020; Rao et al., 2022a).

We select the marketization index proposed by Fan et al. (2011) to evaluate the degree of marketization in various regions and to analyze the moderating effect of marketization on the association between climate risk and corporate green innovation. This index can reflect the market efficiency of resource allocation and the degree of government intervention to some extent.

Numerous other elements also have an impact on corporate green innovation. Referring to previous studies (Anton, 2021; Ren et al., 2022; Zhong and Peng, 2022), we select the company size (

Some empirical findings have shown that the efficiency of small-size companies is higher than that of large-size companies (Lin et al., 2019). To control the impact of the company size, this research uses the natural logarithm of the company’s total assets at the end of each year as a control variable.

Since the R&D investment of a company is highly correlated to its profitability, the corporate profit is considered and is calculated as the ratio of the net profit to the total assets.

Prior research has divided corporate slack resources into absorbed and unabsorbed ones. Unabsorbed slack resources have high liquidity and flexibility and can be leveraged to lessen the effect of external risk on corporate operation activities. A higher unabsorbed slack resource has been demonstrated to enhance the development and implementation of corporate green innovation (Wu and Hu, 2020). Following Iyer and Miller (2008), the current ratio calculated as current assets divided by current liabilities is employed to control the impact of slack resources.

The better the development prospects of a company, the higher its R&D willingness. Tobin Q value is often used to represent corporate development prospects (Anton, 2021). This paper selects the Tobin Q value to control the impact of development prospects.

There is a close relationship between a company’s operating ability and its R&D decision-making (Anton, 2021). This paper considers the corporate operating ability measured by total assets turnover, which is dividing operating revenue by total assets.

Companies in different life cycles often make different innovation decisions. For example, companies at the mature stage invest less in innovation than those at the start-up and growth stage under specific risk (Shahzad et al., 2022). Therefore, this paper takes company age to control the impact of life cycle.

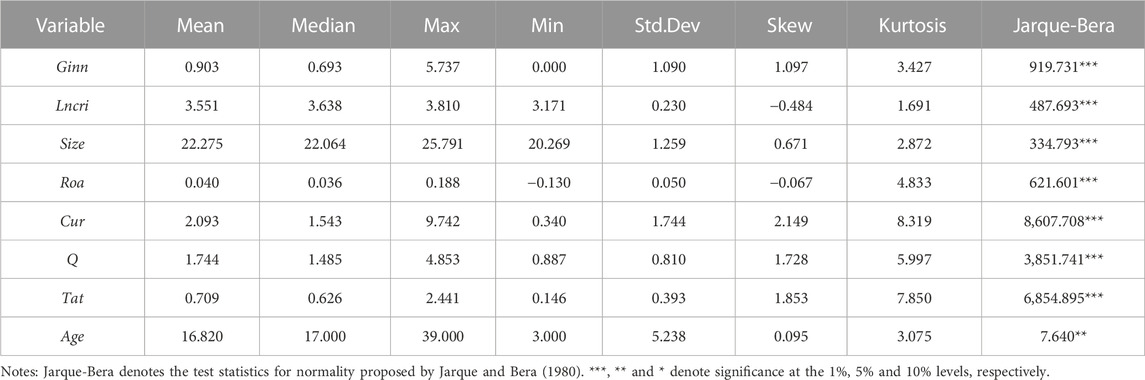

Table 1 shows the definition and description of the main variables, and Table 2 reports the descriptive statistics. The average value of

TABLE 1. Definition and description of main variables.

TABLE 2. Descriptive analysis.

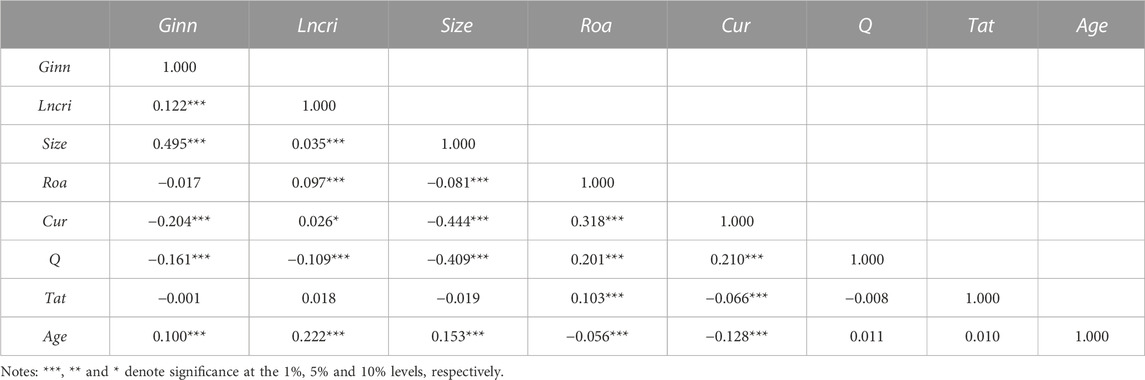

Table 3 displays the Pearson correlation coefficients of the main variables. The results suggest a significant positive relationship between the climate risk index and the number of corporate green patent applications, implying that corporate green innovation may be negatively influenced by climate risk and providing preliminary support for H1. There seems no serious multicollinearity since the correlation coefficient of each pair of explanatory variables is less than 0.50.

TABLE 3. Main variable correlation analysis.

This research begins by constructing the panel regression model (1) to test H1 that climate risk will decrease green innovation in heavy-polluting companies.

where

Referring to Baron and Kenny (1986), we use the following models to test the mediating effect:

where

To test the moderating effect of green finance, digital finance and marketization, we develop the following models:

where

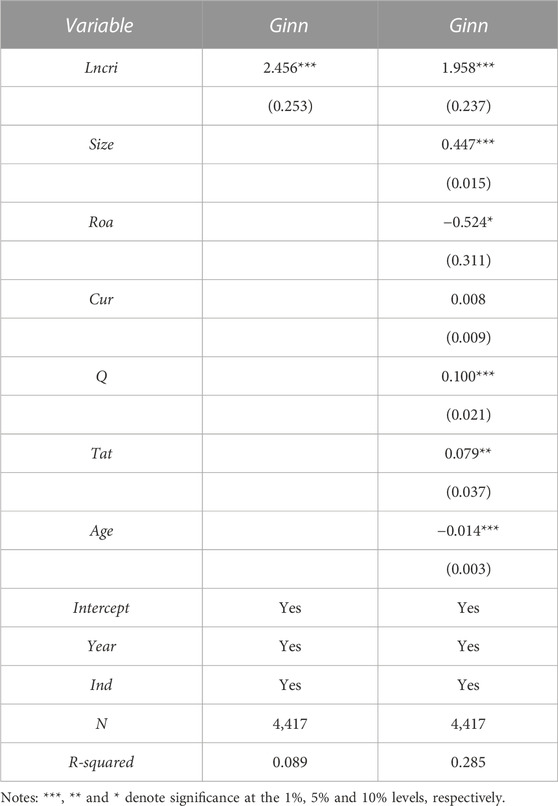

The results of the benchmark regression are presented in Table 4. Column (1) shows there is a statistically significant negative impact of climate risk on corporate green innovation at the 1% level when controlling for year and industry-fixed effects. When all control variables are included in column (2), the coefficient of climate risk (

TABLE 4. Benchmark regression results.

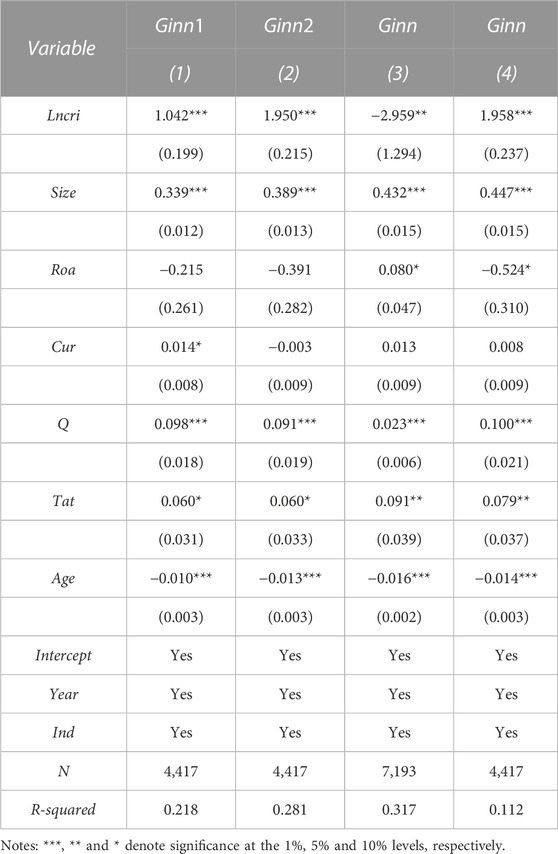

This paper employs the number of green invention patent applications (

TABLE 5. Robustness tests results.

Following Alstadt et al. (2022), Hoeppe (2016) and Neumayer and Barthel. (2011), to further prove the relationship between climate risk and corporate green innovation, we use the proportion of economic losses of climate risk to current GDP as an alternative measure of climate risk to test the robustness of the empirical results. The greater the proportion of direct economic losses to GDP, the worse the climate risk. The sample interval is set between 2011 and 2021 because the green innovation data is available until 2021. The economic losses of climate risk data are from the China Social Statistical Yearbook compiled by the National Bureau of Statistics of China. The results of column (3) in Table 5 confirm that when the direct economic loss of climate disasters/current GDP is used as an alternative variable in the analysis, the correlation between climate risk and corporate green innovation is robust.

It is challenging for OLS estimation to obtain a consistent estimate for regression models where the dependent variable has a partial value of 0 (Davidson and MacKinnon, 2004). In our sample, the number of green patent applications exhibits a pattern of zero and positive values coexisting. Following Rao et al., 2022b and Tang et al. (2021), we employ the Tobit model in place of the original model for further robustness tests in order to more accurately identify the impact of climate risk on corporate green innovation. The results of column (4) in Table 5 demonstrate that the sign, magnitude and significance of the coefficient of climate risk are essentially consistent with those in the benchmark regression, demonstrating that climate risk severely inhibits corporate green innovation in heavy-polluting companies.

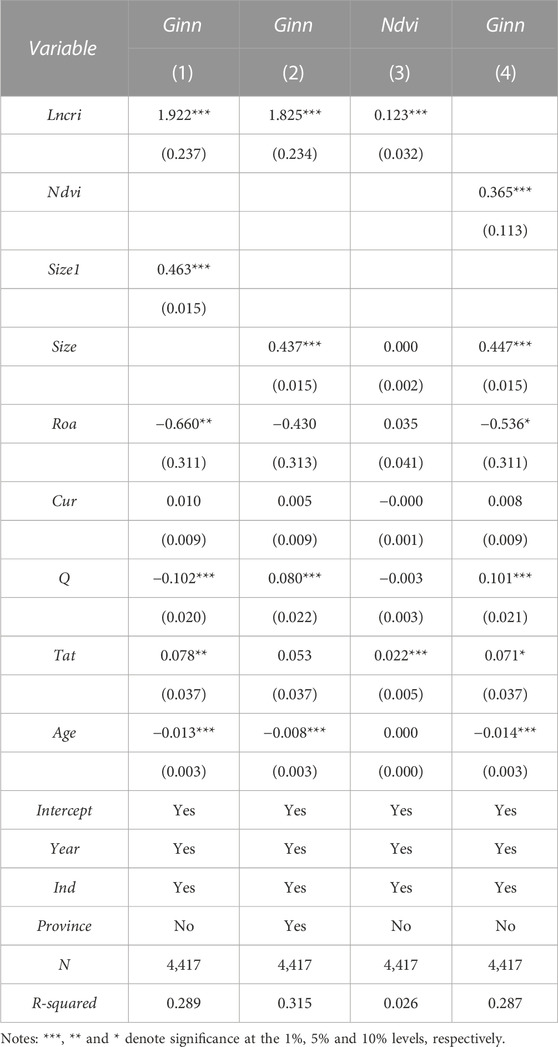

Company size has been proven to be a substantial contributor to the heterogeneity in company finance (Dang et al., 2018), that is, the sign, magnitude and significance of the coefficients of explanatory variables may vary when different company size measures are used. Referring to Anton (2021), we conduct the robustness tests by using the natural logarithm of market capitalization as an alternative measure of company size. The empirical results in column (1) of Table 6 indicate that the previous regression results are robust when market capitalization is employed as a substitute proxy for company size.

TABLE 6. Endogeneity tests results.

In benchmark regression, year and industry fixed effects are controlled for, but unobserved regional characteristics could lead to estimation bias. For instance, company location may be accompanied by different resource endowments and regional economic policies, which may result in estimation bias. After controlling for province fixed effect, column (2) of Table 6 shows that the coefficient of climate risk is still significantly positive at the 1% level, suggesting that the impact of climate risk on corporate green innovation seems not to be affected by unobservable regional factors.

This research adopts instrumental variable (IV) estimation as a robustness test to further address the endogeneity issue that may be caused by the two-way causal relationship between climate risk and corporate green innovation. Following Liu et al. (2021), the normalized differential vegetation index (

Columns (2) in Table 6 reports that there is a significantly positive correlation between

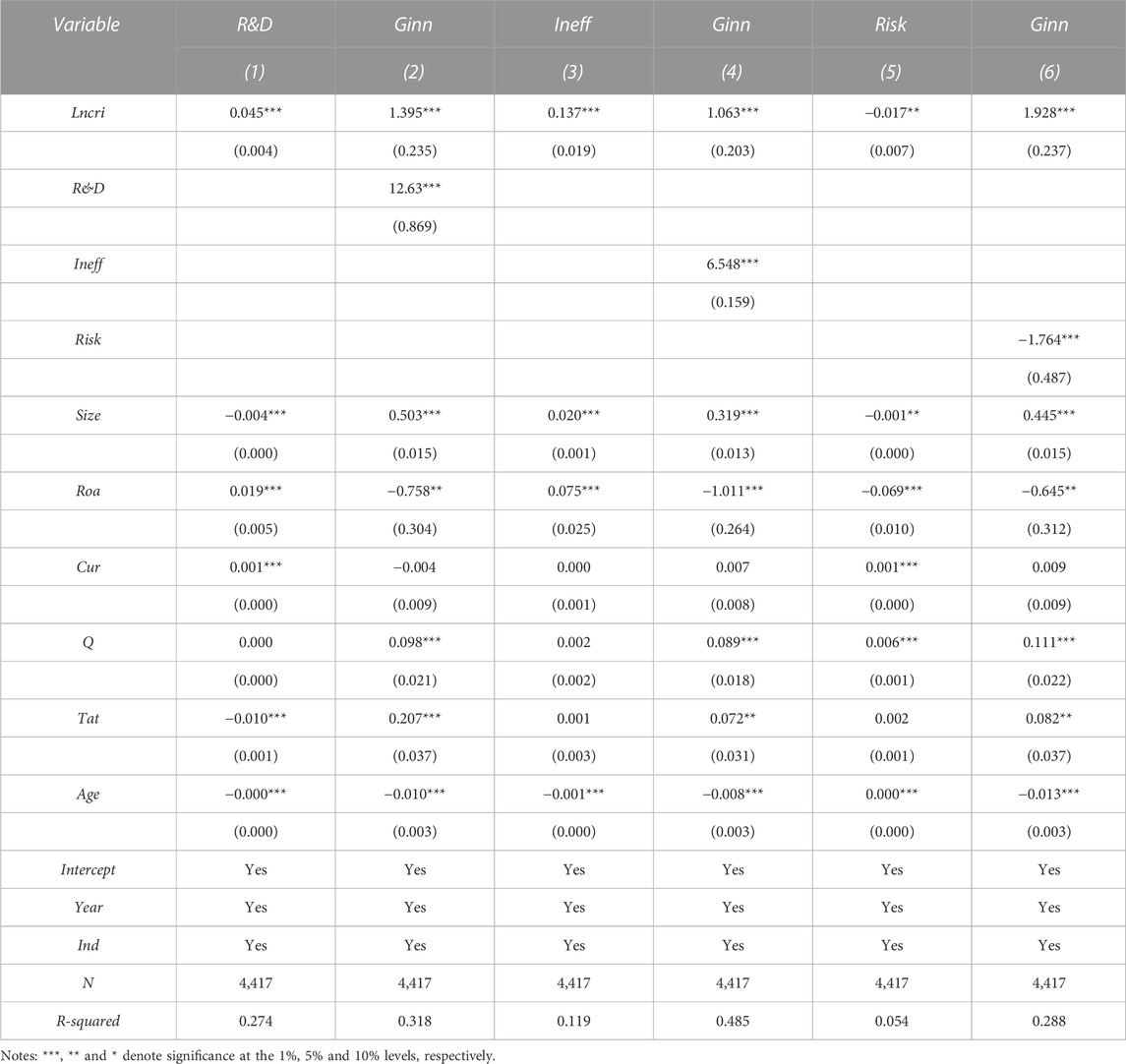

The above results indicate that climate risk has a significantly detrimental effect on corporate green innovation. In this section, we examine the following three potential channels through which climate risk decreases corporate green innovation: R&D investment, resource allocation efficiency and company risk.

Corporate innovation, especially corporate green innovation, is a high-risk, high-reward activity requiring large investments. However, climate risk endangers the creditworthiness of loans and bonds issued by heavy-polluting companies, increases financing costs and reduces available funds for corporate green innovation. Due to limited capital, companies that are susceptible to serious climate risks may choose to hold cash rather than invest in green innovation to resist climate risk. Therefore, this research investigates whether the climate risk inhabits corporate green innovation by decreasing R&D investment. A company’s R&D investment (

TABLE 7. Mechanism analysis results.

Extreme climate events can cause direct physical damage to corporate tangible assets, and may even damage the R&D equipment and environment at the crucial moment of core technology innovation, hence decreasing corporate R&D efficiency. Secondly, the existing research has discovered that climate risk might be anticipated to decrease both labor supply and productivity (Dasgupta et al., 2021). Insufficient scientific research supply and ineffective labor productivity will prevent companies from implementing green innovation. Thirdly, climate risk will increase the uncertainty of corporate operation position, making it more difficult for financial institutions to estimate corporate operating status and reducing the efficiency of the available resources provided by financial institutions for corporate green innovation. We measure the resource allocation efficiency (

Green innovation has a larger initial uncertainty risk than other operating activities. Climate risk may affect asset safety and trigger stricter environmental regulation, thus aggravating the operational and regulatory risks of heavy-polluting companies. Heavy-polluting companies may prefer to lower risk via low-risk operational activities rather than high-risk green innovation. Therefore, this paper examines if climate risk can prevent corporate green innovation in heavy-polluting companies by increasing company risk. Following Zhou et al. (2022), company risk can be calculated as

The larger the value of

In summary, the above results support H2, that is, Climate risk negatively impacts corporate green innovation through decreasing R&D investment, lowing resource allocation efficiency, and increasing company risk.

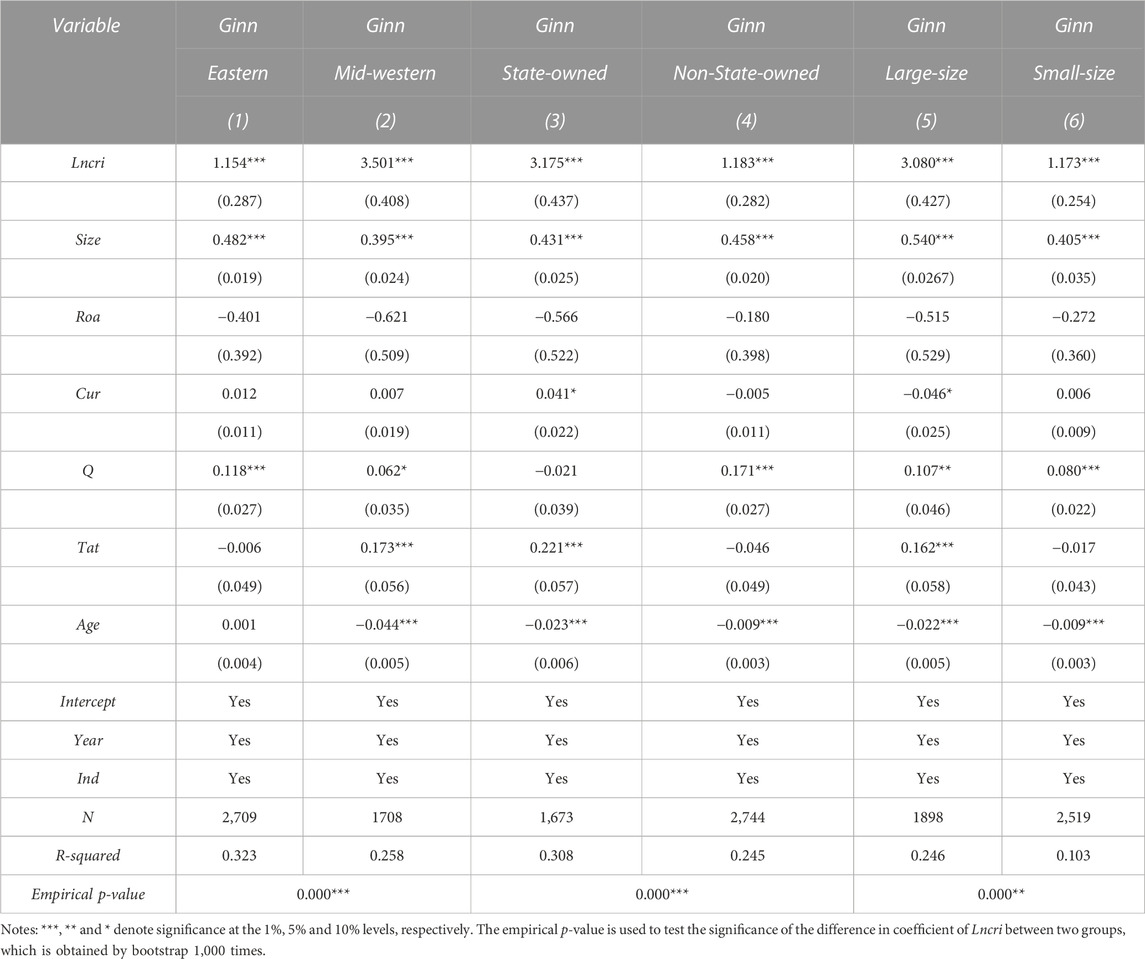

In this section, we further study the heterogeneous impact of climate risk on corporate green innovation in different heavy-polluting companies. According to the analysis in Section 2, the negative impact of climate risk on corporate green innovation may vary with region, company ownership and size.

In order to investigate whether the impact of climate risk on corporate green innovation varies significantly across regions, the original sample is split into two sub-samples according to the provinces where the sample companies are registered, namely, the eastern (Eastern) and the central and western (Mid-Western) provinces3. Columns (1) and (2) of Table 8 report the coefficients of Eastern and Mid-Western are significant at the 1% level, which are 1.154 and 3.501, respectively. The empirical p-value is significantly less than 0.01, indicating a statistically significant difference between the two coefficients at the 1% level. These findings show that companies in the central and western regions are more significantly and severely impacted by climate risk. This may be because central and western regions of China are more inclined to mitigate climate risk through mandatory regulations such as emission permits, but eastern regions are more likely to implement market regulations such as R&D subsidies. Mandatory regulations will limit corporate operations, exacerbating the negative effects of climate risk. While market regulations could compensate for the extra costs associated with strict mandatory regulations, thus alleviating the strain of extreme climate events and environmental regulations. Additionally, the eastern region has a higher-quality financial and market environment than the central and western regions, which may make it easier for heavy-polluting companies in the eastern region to access more resources for conducting green innovation.

TABLE 8. Heterogeneity analysis results.

Columns (3) and (4) of Table 8 present the estimated results for state-owned companies (PR = 1) and non-state-owned companies (PR = 0), respectively. The coefficient of climate risk for state-owned is higher than that of non-state-owned companies. Therefore, we could believe that the impact of climate risk on corporate green innovation in state-owned heavy-polluting companies may be stronger than that of non-state-owned heavy-polluting companies. One possible reason is that state-owned heavy-polluting companies are subject to harsher environmental regulations and are expected to assume more social responsibilities because of the characteristics of China’s political system. They are more vulnerable to climate risk and incur higher costs due to climate risk than other types of companies, hence reducing the funds available for green innovation. Secondly, compared with state-owned companies, privately-owned companies are usually more prone to seek diversity and flexibility in resource allocation and corporate strategy than state-owned companies to alleviate the negative impact of climate risk.

We define the company whose total assets exceed the average value of the heavily polluting companies’ total assets as a large company (large) and assign it a value of 1; otherwise, we assign it a value of 0 in order to compare the impact of climate risk on corporate green innovation across company sizes. The empirical results in columns (5) and (6) of Table 8 indicate that the coefficient of climate risk of large-size companies is greater than that of small-size companies, which shows that climate risk has a greater impact on corporate green innovation of large-size companies. This may be because large-size companies have to consider more aspects of responsibility such as shareholder responsibility and employ more robust operating strategies than those of small-size companies. This result is consistent with Lin et al. (2019), who find that small-size companies which are more maneuverable and variated are more inclined to pursue green innovation than large-size companies.

To sum up, we conclude that climate risk has a greater negative impact on mid-western, state-owned, and large-size heavy-polluting companies, which supports H3.

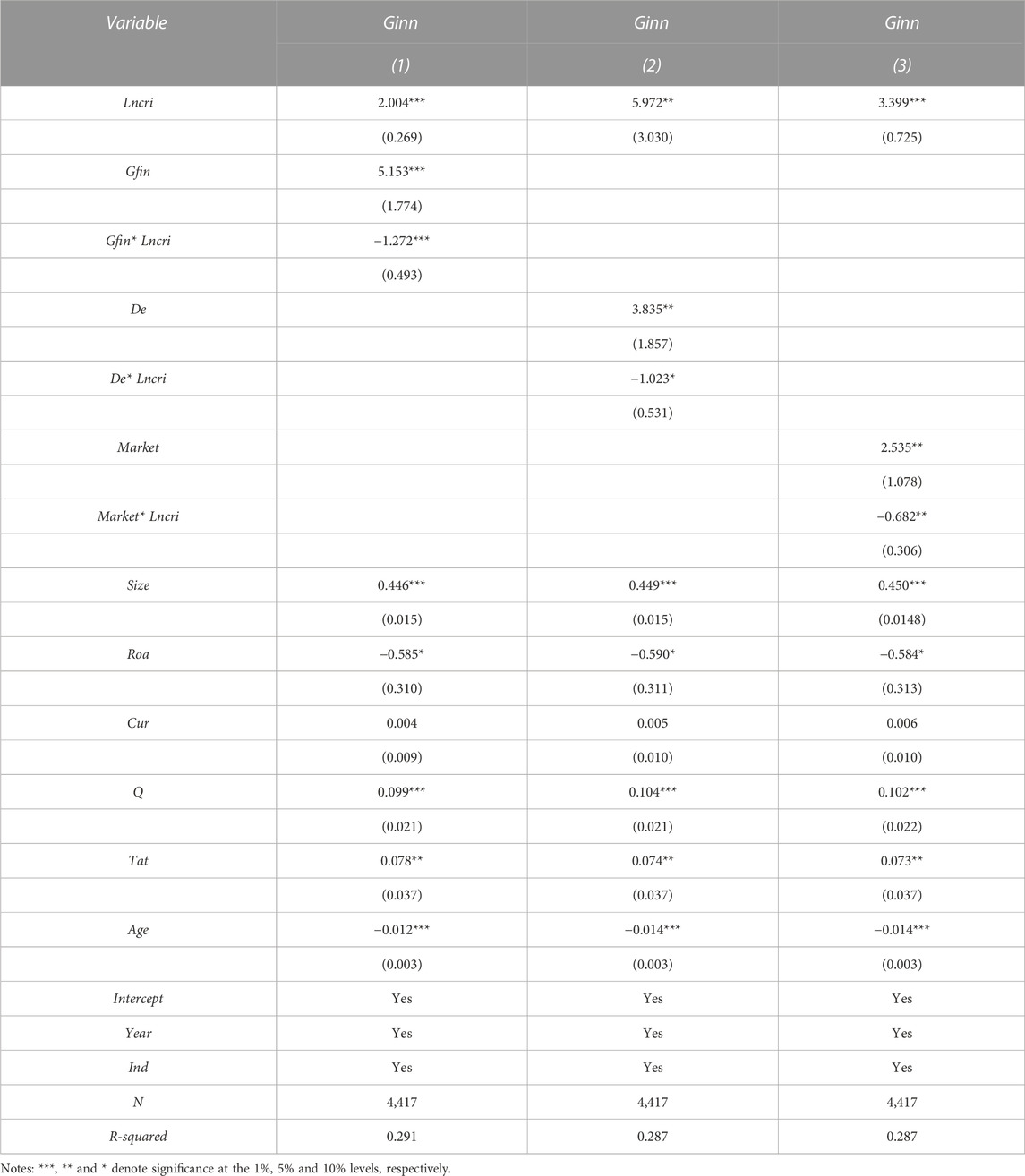

Green finance has been proven to play an important and positive role in promoting green innovation through radiation and trickle-down functions (Huang et al., 2022), which motivates us to examine the moderating of green finance. Column (1) in Table 9 reports that the coefficient of

TABLE 9. The moderating effect analysis results.

The existing research finds that digital finance can improve factor productivity (Chen et al., 2022), and independent innovation (Li and Liu, 2022) and negatively impact companies’ default and bankruptcy risk (Ji et al., 2022). The results in column (2) of Table 9 show that the coefficient of

According to Feng et al. (2022) and Sha et al. (2022), marketization contributes to corporate green innovation by alleviating financing constraints, reducing information asymmetry, and enhancing environmental consciousness. Column (3) of Table 9 demonstrates that the coefficient of

This paper investigates the impact of climate risk on corporate green innovation in Chinese heavy-polluting listed companies from 2011 to 2020. The empirical results show that climate risk adversely affects corporate green innovation of heavy-polluting companies, and this effect persists throughout a series of robustness and endogeneity tests. Climate risk may affect corporate green innovation through decreasing R&D investment, lowing resource allocation efficiency, and increasing company risk. Climate risk has a greater negative impact on mid-western, state-owned, and large-size heavy-polluting companies, but can be mitigated by the development of green finance, digital finance, and marketization.

The findings in this paper are particularly helpful for governments and companies. First, although climate risk has a negative impact on the corporate green innovation of heavy-polluting companies, corporate green innovation is still a favorable means for heavy-polluting companies to cope with climate risk. Compared with defensive and adaptive responses such as industrial restructuring and withdrawal, green innovation is an aggressive response to climate risk, which can better balance the two goals of economic development and energy transformation. The government should provide policy support for heavy-polluting companies to encourage green technology innovation, especially for mid-western, state-owned, and large-size heavy-polluting companies. Second, local governments, particularly those in central and western regions, are suggested to promote the development of green finance such as green credit and green insurance and help heavy-polluting companies mitigate the negative impact of climate risk. Third, the state and local governments need to continue to promote the development of digital finance, especially those in emerging economies, and encourage heavy-polluting companies to use digital financial services to reduce information asymmetry between the market and companies. This can ease the financing constraints and reduce the financing costs, thus promoting corporate green innovation. Forth, in addition to the mandatory provisions on energy conservation and emission reduction, the government should give full play to its “guiding” role, and employ flexible policy tools in combination with the market mechanism to further promote marketization and enhance the green innovation willingness of heavy-polluting companies. Finally, it is suggested that heavy-polluting companies actively strive for national industrial transformation and upgrading funds, green credit and other relevant policy support, and make full use of green finance and digital financial services, so as to actively carry out green technology innovation, reduce the premium of green products and reduce the cost of coping with climate risk.

The raw data supporting the conclusion of this article will be made available by the authors, without undue reservation.

HG: Writing—original draft, data curation, software, and writing—review and editing; SL: Conceptualization, writing—original draft, methodology, funding acquisition, supervision, and writing—review and editing. All authors contributed to the article and approved the submitted version.

The authors gratefully acknowledges the financial support from the National Social Science Foundation of China under Grant No. 21BJY146.

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1The paper selects coal mining (B06), gas exploration (B07), ferrous mining (B08), nonferrous mining (B09), nonmetal mining (B10), wine, beverage and refined tea manufacturing (C15), textile (C17,C18,C19), paper (C22), coking and nuclear fuel (C25), chemical raw materials and chemical manufacturing (C26), chemical fiber manufacturing (C28), rubber and plastic products (C29), nonmetallic mineral products (C30), ferrous metal smelting and rolling processing (C31), nonferrous metals smelting and rolling processing (C32), ferrous metals smelting and rolling processing (C33), and electricity, thermal production, and supply (D44) industries as sample.

2Extreme climate events include climatological events such as droughts, wildfires and freezing; meteorological events such as tornados, storms and extreme weather; hydrological events such as floods and landslide.

3The eastern regions include Beijing, Tianjin, Shanghai, Hebei, Shandong, Jiangsu, Zhejiang, Fujian, Guangdong and Hainan, other regions are mid-western regions.

Addoum, J. M., Ng, D. T., and Ortiz-Bobea, A. (2020). Temperature shocks and establishment sales. Rev. Financial Stud. 33 (3), 1331–1366. doi:10.1093/rfs/hhz126

Ahmad, M. F., Aktas, N., and Croci, E. (2023). Climate risk and deployment of corporate resources to working capital. Econ. Lett. 224, 111002. doi:10.1016/j.econlet.2023.111002

Alstadt, B., Hanson, A., and Nijhuis, A. (2022). Developing a global method for normalizing economic loss from natural disasters. Nat. Hazards Rev. 23 (1), 04021059. doi:10.1061/(asce)nh.1527-6996.0000522

Amihud, Y., and Lev, B. (1981). Risk reduction as a managerial motive for conglomerate mergers. Bell J. Econ. 12 (2), 605–617. doi:10.2307/3003575

Anton, S. G. (2021). The impact of temperature increase on firm profitability. Empirical evidence from the European energy and gas sectors. Appl. Energy 295, 117051. doi:10.1016/j.apenergy.2021.117051

Baron, R. M., and Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Personality Soc. Psychol. 51 (6), 1173–1182. doi:10.1037/0022-3514.51.6.1173

Capasso, G., Gianfrate, G., and Spinelli, M. (2020). Climate change and credit risk. J. Clean. Prod. 266, 121634. doi:10.1016/j.jclepro.2020.121634

Chen, G., Chen, W., Wang, J., and Zhao, X. (2023). High-temperature exposure risk, corporate performance and pricing efficiency of the stock market. Account. Finance, 13051. doi:10.1111/acfi.13051

Chen, Y., Yang, S., and Li, Q. (2022). How does the development of digital financial inclusion affect the total factor productivity of listed companies? Evidence from China. Finance Res. Lett. 47, 102956. doi:10.1016/j.frl.2022.102956

Dang, C., Li, Z. F., and Yang, C. (2018). Measuring firm size in empirical corporate finance. J. Bank. finance 86, 159–176. doi:10.1016/j.jbankfin.2017.09.006

Dasgupta, S., van Maanen, N., Gosling, S. N., Piontek, F., Otto, C., and Schleussner, C. F. (2021). Effects of climate change on combined labour productivity and supply: An empirical, multi-model study. Lancet Planet. Health 5 (7), e455–e465. doi:10.1016/s2542-5196(21)00170-4

Davidson, R., and MacKinnon, J. G. (2004). Econometric theory and methods. New York: Oxford University Press.

Ding, R., Liu, M., Wang, T., and Wu, Z. (2021). The impact of climate risk on earnings management: International evidence. J. Account. Public Policy 40 (2), 106818. doi:10.1016/j.jaccpubpol.2021.106818

Dong, Z., Wang, S., Zhang, W., and Shen, H. (2022). The dynamic effect of environmental regulation on firms’ energy consumption behavior-Evidence from China's industrial firms. Renew. Sustain. Energy Rev. 156, 111966. doi:10.1016/j.rser.2021.111966

Drisya, J., and Roshni, T. (2018). Spatiotemporal variability of soil moisture and drought estimation using a distributed hydrological model. Integrating Disaster Sci. Manag. 2018, 451–460. doi:10.1016/B978-0-12-812056-9.00027-0

Du, K., Cheng, Y., and Yao, X. (2021). Environmental regulation, green technology innovation, and industrial structure upgrading: The road to the green transformation of Chinese cities. Energy Econ. 98, 105247. doi:10.1016/j.eneco.2021.105247

Eckstein, D., Künzel, V., and Schäfer, L. (2021). The global climate risk index 2021. Bonn: Germanwatch.

Estrada, F., Perron, P., and Yamamoto, Y. (2023). Anthropogenic influence on extremes and risk hotspots. Sci. Rep. 13 (1), 35. doi:10.1038/s41598-022-27220-9

Fan, G., Wang, X., and Ma, G. (2011). Contribution of marketization to China’s economic growth. Econ. Res. J. 9 (283), 1997–2011.

Feng, G. F., Niu, P., Wang, J. Z., and Liu, J. (2022). Capital market liberalization and green innovation for sustainability: Evidence from China. Econ. Analysis Policy 75, 610–623. doi:10.1016/j.eap.2022.06.009

Gao, K., Wang, L., Liu, T., and Zhao, H. (2022). Management executive power and corporate green innovation——empirical evidence from China's state-owned manufacturing sector. Technol. Soc. 70, 102043. doi:10.1016/j.techsoc.2022.102043

Gao-Zeller, X., Li, X., Yang, F., and Zhu, W. (2019). Driving mechanism of CSR strategy in Chinese construction companies based on neo-institutional theory. KSCE J. Civ. Eng. 23, 1939–1951. doi:10.1007/s12205-019-0989-y

Godde, C. M., Mason-D’Croz, D., Mayberry, D. E., Thornton, P. K., and Herrero, M. (2021). Impacts of climate change on the livestock food supply chain; a review of the evidence. Glob. food Secur. 28, 100488. doi:10.1016/j.gfs.2020.100488

Gormley, T. A., and Matsa, D. A. (2016). Playing it safe? Managerial preferences, risk, and agency conflicts. J. Financial Econ. 122 (3), 431–455. doi:10.1016/j.jfineco.2016.08.002

Guo, F., Wang, J., Wang, F., Kong, T., Zhang, X., and Cheng, Z. (2020). Measuring China’s digital financial inclusion: Index compilation and spatial characteristics. China Econ. Q. 19 (4), 1401–1418.

Hoeppe, P. (2016). Trends in weather related disasters—consequences for insurers and society. Weather Clim. Extreme 11 (2), 70–79. doi:10.1016/j.wace.2015.10.002

Huang, H. H., Kerstein, J., and Wang, C. (2018). The impact of climate risk on firm performance and financing choices: An international comparison. J. Int. Bus. Stud. 49, 633–656. doi:10.1057/s41267-017-0125-5

Huang, Y., Chen, C., Lei, L., and Zhang, Y. (2022). Impacts of green finance on green innovation: A spatial and nonlinear perspective. J. Clean. Prod. 365, 132548. doi:10.1016/j.jclepro.2022.132548

Hugon, A., and Law, K. (2019). Impact of climate change on firm earnings: Evidence from temperature anomalies. Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3271386 (Accessed January 24, 2019).

Iyer, D. N., and Miller, K. D. (2008). Performance feedback, slack, and the timing of acquisitions. Acad. Manag. J. 51 (4), 808–822. doi:10.5465/amr.2008.33666024

Ji, Y., Shi, L., and Zhang, S. (2022). Digital finance and corporate bankruptcy risk: Evidence from China. Pacific-Basin Finance J. 72, 101731. doi:10.1016/j.pacfin.2022.101731

Khalfaoui, R., Stef, N., Wissal, B. A., and Sami, B. J. (2022). Dynamic spillover effects and connectedness among climate change, technological innovation, and uncertainty: Evidence from a quantile VAR network and wavelet coherence. Technol. Forecast. Soc. Change 181, 121743. doi:10.1016/j.techfore.2022.121743

Kulatilaka, N., and Perotti, E. C. (1998). Strategic growth options. Manag. Sci. 44 (8), 1021–1031. doi:10.1287/mnsc.44.8.1021

Lee, S. H., Choi, D. J., and Han, S. H. (2023). Corporate cash holdings in response to climate risk and policies. Finance Res. Lett., 103910. doi:10.1016/j.frl.2023.103910

Li, H., and Lu, J. (2022). Temperature change and industrial green innovation: Cost increasing or responsibility forcing? J. Environ. Manag. 325, 116492. doi:10.1016/j.jenvman.2022.116492

Li, M., and Gao, X. (2022). Implementation of enterprises’ green technology innovation under market-based environmental regulation: An evolutionary game approach. J. Environ. Manag. 308, 114570. doi:10.1016/j.jenvman.2022.114570

Li, Y., and Liu, X. (2022). Digital finance, trade credit and enterprise independent innovation. Procedia Comput. Sci. 202, 313–319. doi:10.1016/j.procs.2022.04.042

Lin, W. L., Cheah, J. H., Azali, M., Ho, J. A., and Yip, N. (2019). Does firm size matter? Evidence on the impact of the green innovation strategy on corporate financial performance in the automotive sector. J. Clean. Prod. 229, 974–988. doi:10.1016/j.jclepro.2019.04.214

Lin, Z., and Sheng, Y. (2022). Climate change and firm productivity: The case of drought. Appl. Econ. Lett., 1–11. doi:10.1080/13504851.2022.2116385

Liu, B., Wang, X. H., and Li, X. M. (2021). Climate change and the credit risk of rural financial institutions. J. Financial Res. 498, 96–115.

McMichael, A. J., Woodruff, R. E., and Hales, S. (2006). Climate change and human health: Present and future risks. Lancet 367 (9513), 859–869. doi:10.1016/s0140-6736(06)68079-3

Möllmann, J., Buchholz, M., Kölle, W., and Musshoff, O. (2020). Do remotely-sensed vegetation health indices explain credit risk in agricultural microfinance? World Dev. 127, 104771. doi:10.1016/j.worlddev.2019.104771

Neumayer, E., and Barthel, F. (2011). Normalizing economic loss from natural disasters: A global analysis. Glob. Environ. Change 21 (1), 13–24. doi:10.1016/j.gloenvcha.2010.10.004

Ozkan, A., Temiz, H., and Yildiz, Y. (2023). Climate risk, corporate social responsibility, and firm performance. Br. J. Manag. 12665.

Pankratz, N., Bauer, R., and Derwall, J. (2023). Climate change, firm performance, and investor surprises. Manag. Sci., 4685. doi:10.1287/mnsc.2023.4685

Pankratz, M. C., and Schiller, C. M. (2021). Climate change and adaptation in global supply-chain networks. Finance and Economics Discussion Series 2022-056.

Rao, S., Koirala, S., Thapa, C., and Neupane, S. (2022a). When rain matters! Investments and value relevance. J. Corp. Finance 73, 101827. doi:10.1016/j.jcorpfin.2020.101827

Rao, S., Pan, Y., He, J., and Shangguan, X. (2022b). Digital finance and corporate green innovation: Quantity or quality? Environ. Sci. Pollut. Res. 29 (37), 56772–56791. doi:10.1007/s11356-022-19785-9

Ren, X., Li, Y., Shahbaz, M., Dong, K., and Lu, Z. (2022). Climate risk and corporate environmental performance: Empirical evidence from China. Sustain. Prod. Consum. 30, 467–477. doi:10.1016/j.spc.2021.12.023

Sautner, Z., van Lent, L., Vilkov, G., and Zhang, R. (2023). Firm-level climate change exposure. J. Finance 78, 1449–1498. doi:10.1111/jofi.13219

Schiederig, T., Tietze, F., and Herstatt, C. (2012). Green innovation in technology and innovation management–an exploratory literature review. Randd Manag. 42 (2), 180–192. doi:10.1111/j.1467-9310.2011.00672.x

Sha, Y., Zhang, P., Wang, Y., and Xu, Y. (2022). Capital market opening and green innovation——evidence from Shanghai-Hong Kong stock connect and the shenzhen-Hong Kong stock connect. Energy Econ. 111, 106048. doi:10.1016/j.eneco.2022.106048

Shahzad, F., Ahmad, M., Fareed, Z., and Wang, Z. (2022). Innovation decisions through firm life cycle: A new evidence from emerging markets. Int. Rev. Econ. Finance 78, 51–67. doi:10.1016/j.iref.2021.11.009

Shih, Y. C., Wang, Y., Zhong, R., and Ma, Y. M. (2021). Corporate environmental responsibility and default risk: Evidence from China. Pacific-Basin Finance J. 68, 101596. doi:10.1016/j.pacfin.2021.101596

Tang, C., Xu, Y., Hao, Y., Wu, H., and Xue, Y. (2021). What is the role of telecommunications infrastructure construction in green technology innovation? A firm-level analysis for China. Energy Econ. 103, 105576. doi:10.1016/j.eneco.2021.105576

Venturini, A. (2022). Climate change, risk factors and stock returns: A review of the literature. Int. Rev. Financial Analysis 79, 101934. doi:10.1016/j.irfa.2021.101934

Wagner, G. (2022). Climate risk is financial risk. Science 376 (6598), 1139. doi:10.1126/science.add2160

Walter, J. M., and Chang, Y.-M. (2020). Environmental policies and political feasibility: Eco-labels versus emission taxes. Econ. Analysis Policy 66, 194–206. doi:10.1016/j.eap.2020.04.004

Wu, H., and Hu, S. (2020). The impact of synergy effect between government subsidies and slack resources on green technology innovation. J. Clean. Prod. 274, 122682. doi:10.1016/j.jclepro.2020.122682

Wurlod, J.-D., and Noailly, J. (2018). The impact of green innovation on energy intensity: An empirical analysis for 14 industrial sectors in OECD countries. Energy Econ. 71, 47–61. doi:10.1016/j.eneco.2017.12.012

Xu, W., Gao, X., Xu, H., and Li, D. (2022). Does global climate risk encourage companies to take more risks? Res. Int. Bus. Finance 61, 101658. doi:10.1016/j.ribaf.2022.101658

Yan, X., Zhang, Y., and Pei, L. L. (2021). The impact of risk-taking level on green technology innovation: Evidence from energy-intensive listed companies in China. J. Clean. Prod. 281, 124685. doi:10.1016/j.jclepro.2020.124685

Yu, S., Wang, L., and Zhang, S. (2022a). Climate risk and corporate cash holdings: Mechanism and path analysis. Front. Environ. Sci. 10, 1360. doi:10.3389/fenvs.2022.979616

Yu, S., Zheng, Y., and Hu, X. (2022b). How does climate change affect firms' investment efficiency? Evidence from China's listed renewable energy firms. Bus. Strategy Environ. 2022, 3349. doi:10.1002/bse.3349

Zhang, W., Ding, N., Han, Y., He, J., Zhang, N., Wu, N., et al. (2023). Separation of temperature-induced response for bridge long-term monitoring data using local outlier correction and savitzky-golay convolution smoothing. Front. Environ. Sci. 10, 2632. doi:10.3390/s23052632

Zhong, Z., and Peng, B. (2022). Can environmental regulation promote green innovation in heavily polluting enterprises? Empirical evidence from a quasi-natural experiment in China. Sustain. Prod. Consum. 30, 815–828. doi:10.1016/j.spc.2022.01.017

Keywords: climate risk, heavy-polluting companies, corporate green innovation, panel regression, fintech

Citation: Ling S and Gao H (2023) How does climate risk matter for corporate green innovation? Empirical evidence from heavy-polluting listed companies in China. Front. Energy Res. 11:1177927. doi: 10.3389/fenrg.2023.1177927

Received: 02 March 2023; Accepted: 25 May 2023;

Published: 05 June 2023.

Edited by:

Michal Jasinski, Wrocław University of Science and Technology, PolandReviewed by:

Nallapaneni Manoj Kumar, City University of Hong Kong, Hong Kong SAR, ChinaCopyright © 2023 Ling and Gao. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Hongfu Gao, Z2FvaG9uZ2Z1MUAxMjYuY29t

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.