Yunfeng Zhao

Yunfeng Zhao Yiming Yue

Yiming Yue

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Energy Res. , 04 June 2021

Sec. Sustainable Energy Systems

Volume 9 - 2021 | https://doi.org/10.3389/fenrg.2021.696110

This article is part of the Research Topic Progress Towards Achieving Cross-Regional Carbon Mitigation Targets View all 14 articles

As an innovative green financial tool, green corporate asset-backed securities can effectively solve the problems of narrow financing channels and maturity mismatches for green projects, which can help achieve green and low-carbon development, carbon peaking, and carbon neutrality goals. In this paper, we examine the financing cost advantages of green corporate asset-backed securities and the related impact factors through a combination of empirical and case studies. Empirical research based on the propensity score matching method (PSM) shows that China’s green corporate asset-backed securities issuance rates are 36.97°bps lower than traditional corporate asset-backed securities on average. Credit rating, issuance scale, issuance interest rate, issuance period, and green factors have become the main impact factors of green corporate asset-backed securities financing advantages.

Industrialization has spurred long-term and rapid economic growth in China. However, the high levels of inputs and consumption have also increased the incidents of environmental pollution and ecological destruction. Studies have shown that the annual economic loss caused by environmental pollution in China is 0.6–1.8 trillion yuan, accounting for up to 3.05% of total GDP. The environmental carrying capacity has approached its limit, which makes the environmental problem one of the biggest practical challenges for China and all the rest of the world as well (Fang and Guo, 2018; Wang and Chen, 2018; UNEP, 2021). On September 22, 2020, the Chinese government announced at the General Assembly of the United Nations that China will strive to peak carbon dioxide emissions by 2030 and achieve “carbon neutrality” before 2060. At the Climate Ambition Summit (the commemorative meeting for the signing of the Paris Agreement) held on December 12 of the same year, Chinese President Xi Jinping made this same commitment in his statement. In this context, the development of green industry with the purpose of environmental protection has become an important part of accelerating China’s economic transformation. The latest evidence shows that investment in green projects in China can reduce China’s short- and long-term carbon emissions levels (Li et al., 2021). However, when a company develops a green project, it often requires a long period of time to pay back loans taken out to fund the project; thus, for the lending bank, the risks and benefits often do not meet the bank’s typical standards. Banks have become less willing to provide long-term loans for green projects, so it is difficult for companies to obtain the required funds at low cost, which greatly affects the development speed and quality of green projects.

As a new instrument of financial innovation, green asset backed securitization is regarded as one of the most important parts of a green financial system. Since only the credit rating of corporate green assets is performed, the rating is less affected by the financial status of corporate entities. Green asset securitization allows companies to issue green products with lower financing thresholds and financing costs. Before China’s green asset securitization was supported and promoted by government agency, green credit was the main channel of green financing. The implementation of China’s green credit policy reduces the risks for non-state-owned banks, while state-owned banks provide green credit at the expense of profits. This institutional design makes the Chinese government a global pioneer in the greening of the financial markets (Yin et al., 2021).

China’s asset securitization market has developed rapidly over the past decade, evolving from approximately US $2.14 billion at the end of 2005 to approximately US $405 billion at the end of 2018, and it has become the largest securitization market in Asia (Yang et al., 2020). As the Chinese government is committed to building the green financial system and promoting the rapid development of asset securitization, its pilot asset securitization program has been continuously expanded and has become a pivotal component of the world’s securitization market. At the same time, Seven Ministries such as the People's Bank of China vigorously promote the securitization business with green credit and PPP projects serving as the basic assets. In September 2015, the State Council of China published the “General Plans for the Reform of the Ecological Civilization System”, which places more emphasis on the green economy, significantly boosting green asset securitization. With the development of green asset securitization in China, the issuance of green corporate asset-backed securities has experienced a high rate of growth year by year. However, the pricing of green corporate asset-backed securities issued can vary greatly by institution.

In this paper, we use a combination of empirical research and case analysis to examine the issuance and pricing of green corporate asset-backed securities and their pricing factors, which will promote the development of green finance in China. First, we use Propensity Score Matching (PSM) to examine whether green corporate asset-backed securities have certain issuance cost advantages. Second, we analyze the impact factors of the financing costs of China’s first “Labelled” green corporate asset-backed securities (“Goldwind 2016-1”) through the Static Spread method, and we put forward corresponding development suggestions.

Our study contributes to the literature in the following three aspects. First, the project “Goldwind 2016-1” issued by the Shanghai Stock Exchange in August 2016 is the first green asset securitization project in China to be double certified by an internationally renowned green certification agency, which makes the project highly representative. We use this representative project to conduct case studies to provide strong evidence for the advantages and pricing of green securities. Second, the study of the impact factors of green corporate asset-backed securities provides the most intuitive evidence for the current issue pricing of green corporate asset-backed securities in China, and it provides a reference for other green enterprises as they seek to issue green corporate asset-backed securities. Third, our research expands the literature on green asset securitization, and helps companies and governments pay more attention to green asset securitization to promote carbon neutrality

The remainder of the paper proceeds as follows. In Literature Review, we provide the literature review. In Methodology and Data, we describe the methodology and data. Empirical Analysis presents the analysis results and discussion. In Factors Affecting the Issuance Pricing of Green Corporate Asset-Backed Securities, we present the pricing factors of green corporate asset-backed securities. In Conclusion and Recommendations, we conclude the paper and provide some recommendations.

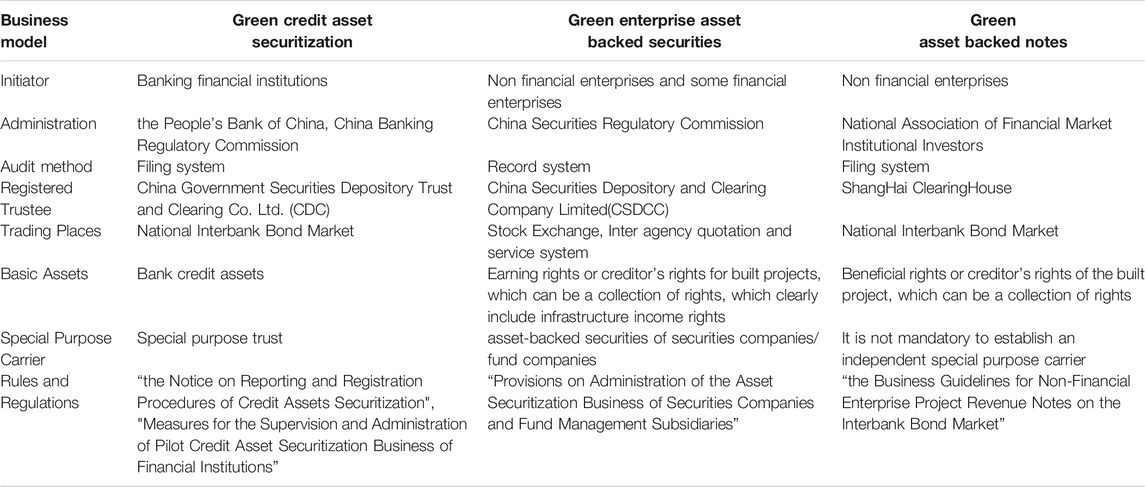

China’s financial industry has been in the situation of “Supervision Segregation” for a long time. The asset securitization market is divided into three markets: the inter-bank market, the securities exchange market, and the insurance fund market. The green asset securitization business can also be divided into three types according to the different regulatory agencies: green credit asset securitization, green asset-backed notes, and green corporate asset-backed securities. These differences are shown in Table 1.

TABLE 1. Comparison of three modes of green asset securitization.

The existing research on China’s green asset-backed securities mostly focuses on the theoretical and policy levels; however, the discussion of the advantages of financing costs and impact factors is relatively limited.

The development of China’s asset securitization has gone through a stage of theory first and then practice. As early as 1992, scholars conducted theoretical discussions, but it was not until 2005 that the pilot work of asset securitization began. However, the emergence of the global economic crisis caused Chinese regulators to adopt a cautious attitude until 2014. Since then, China’s asset securitization market has begun to grow rapidly. By the end of 2018, it reached approximately US $405 billion, making it the largest asset securitization market in Asia. With the gradual integration of the Chinese financial market and the global financial market, more international investors will give the Chinese asset securitization market the potential to become an indispensable part of the world securitization market (Yang et al., 2021).

China adopts stricter divisional supervision in financial supervision, and the supervision coordination mechanism plays a relatively limited role. Therefore, supervision of asset securitization is facing greater problems (Wang and Li, 2016). As far as asset securitization itself is concerned, stricter regulatory constraints are required for the following reasons: First, there are more entities participating in asset securitization, and the risk characteristics are complex; second, asset securitization makes the relationship between traditional financing intermediaries and the capital market closer; third, the basic function of asset securitization will increase the instability of the financial system.

From the existing literature, many scholars have focused on the research of regulatory policies on the asset securitization of the banking industry. (Acharya et al., 2013) conducted an empirical analysis based on the data of US commercial banks and pointed out that the tightening of regulatory constraints, the banking industry will have stronger incentives to carry out asset securitization business. This is because the bank implements asset securitization to reduce the proportion of its own risk assets to meet the minimum capital regulatory requirements (Ambrose et al., 2005). (Song and Zhang 2016) based on the perspective of international comparison, discussed the issue of self-retention supervision of China’s asset securitization risk, put forward the shortcomings of current China's risk self-retention supervision rules and put forward corresponding suggestions. (Li et al., 2019) empirically tested the two methods of regulatory arbitrage for bank asset securitization in my country based on the data from 2012 to 2018. The study found that the possibility of arbitrage between banks using regulatory differences is very small.

Regarding the research on asset securitization, most scholars have focused on the theoretical level, such as the definition of asset securitization, issuance pricing, impact factors analysis, and policy recommendations.

A common view is that asset securitization is a collection of assets that are insufficiently liquid but expected to have a certain return in the future, and a structural reorganization and package sale are required to obtain cash flow in advance (Rosenthal and Ocampo, 1988). In terms of issuance pricing, there are two commonly used pricing methods. One is the absolute pricing method, which refers to the calculation of the sum of the discounted value of the product’s underlying assets in the future as pricing. The other is the relative pricing method, which refers to the yields of comparable asset-backed securities with the same rating in the same period and floats a certain spread based on the benchmark interest rate for pricing calculations. Regarding the factors affecting issuance pricing, the research on China’s asset-backed securities has mainly focused on the credit rating (Kou et al., 2015), and some scholars have also conducted research using investor sentiment and credit enhancement methods (Shao et al., 2015). In general, the impact factors of issuance pricing show heterogeneity according to the characteristics of the bond and the issuer or the issuance market.

China is a country with a large population and large scale of industry, which makes its carbon emissions play a decisive role in achieving the global carbon neutral goal. As of 2015, China’s carbon emissions accounted for 30% of global emissions (Shan et al., 2018). Existing studies have discussed the influencing factors of carbon emission reduction. For example, technological innovation is generally recognized as promoting the reduction of carbon emissions (Yu and Du, 2019; Chen and Lee, 2020; Jiang et al., 2020; Shahbaz et al., 2020; Cheng et al., 2021).In the research on China, the development of natural gas infrastructure construction and the actual urbanization rate are pointed out as influencing factors that can significantly reduce carbon emissions (Shuai et al., 2018; Dong et al., 2020a), and the industrial distribution leads to significant reductions in carbon emissions (Shuai et al., 2018; Dong et al., 2020b). In addition, appropriate environmental regulations have been proven to have a positive impact on carbon emissions reduction (Zhao et al., 2020). There are also some studies focusing on the influencing factors of carbon prices, such as energy prices, oil supply and demand shocks, etc., which have been pointed out to have asymmetrical negative effects on carbon prices (Duan et al., 2021; Zheng et al., 2021).

The Chinese government has been committed to promoting the achievement of environmental protection goals from the policy level. In 2016, China has achieved outstanding achievements in green financial products, tools, methods, and policies. Under the green corporate asset-backed securities mechanism, companies can package the cash flow generated by the green projects they own in a specific time in the future. Also, they can use the packaged cash flow as the basic asset to issue tradable securities. Green corporate asset-backed securities provide a new financing method for green enterprises. As China attaches importance to the concept of green development and the development of asset securitization, green asset securitization has received extensive attention from issuers and investors. However, China’s research on green asset securitization has focused more on theoretical aspects, such as exploring its development advantages and making path optimization suggestions. The analysis of the issuance costs, micro-price impact mechanisms, and financing benefits generated in the financing process is still in the exploratory stage.

The core of China’s green asset securitization development lies in its unique financing advantages. These include lowering the financing threshold, thereby facilitating the financing efficiency of green industries. At the same time, green project standards, information disclosure systems, and policy incentives can effectively promote the development of green asset-backed securities, but in the end, we need to rely on a complete green financial market system. There are also some problems in the development of China’s green asset securitization. For example, some scholars have pointed out that China’s green asset-backed securities at the emergence stage have problems such as mismatches in the financing scale, high financing costs, and uncertain cash flow for green projects, and the financing model needs to be further optimized.

Since the 2007 financial crisis, many academic research have focused on asset-backed securities and institutions involved in issuing these products. Foreign scholars have explored the pricing factors of structured products. In terms of credit rating, (Moreira and Zhao 2018) pointed out that there is a big connection between ABS ratings and their yield spread at issuance in the US market, Credit ratings may affect investors' investment decisions during the issuance stage. Fabozzi and Vink (2012) explored the influencing factors of asset-backed securitization in the European market, indicating that investors will consider other credit factors such as credit enhancement and underlying assets in addition to credit ratings. In terms of sponsor characteristics, (Faltin-Traeger et al., 2010) pointed out that the quality of sponsors will have an important impact on ABS pricing. (He et al., 2012) also confirmed that issuers with a larger market share in the US market are more likely to receive an inflated rating. Regarding China’s asset-backed securities market, (Tang et al., 2017) based on the Chinese securitization market and found that China’s asset securitization market is policy-driven, and the underlying assets are composed of corporate loans and assets, unlike the US or European markets, which is composed of secured or consumer loans. (Yang et al., 2020) explored the pricing factors of asset-backed securities in China’s leasing industry in an empirical and comprehensive way. The study found that when the promoter is closely related to the underlying assets sold to special purpose vehicles (SPVs) investors will pay special attention to the credit quality of the promoter.

In general, the research on asset securitization in foreign countries is relatively complete, and great progress has been made in terms of the regulatory issues and influencing factors of asset-backed securities. Compared with China, asset-backed securities started late and focused more on the theoretical level, with fewer actual case discussions.

China’s green asset-backed securities market belongs to the emerging development field of green bonds. Many studies have posited that there is indeed a spread between green bonds and ordinary bonds, which affirms the positive significance of the development of green bonds (Mathews et al., 2010; Yao, 2017; MacAskill et al., 2021). In terms of the research on the factors affecting the issuance interest rate, the mainstream view is that green bonds are similar to traditional bonds. That is, the support of macro and micro factors such as market interest rates, bonds, and the characteristics of the issuer can affect the green bond issuance rate. Environmental benefits and government support are also considered important factors affecting the pricing of green asset-backed securities.

In summary, the research on green asset-backed securities in China has thus far conducted only a limited discussion of the financing cost advantages and impact factors. In this paper, we use a combination of empirical research and case analysis to explore the issuance and pricing of green corporate asset-backed securities and their impact factors. This work has a certain role in promoting China's green finance development and green enterprise asset securitization pricing theory.

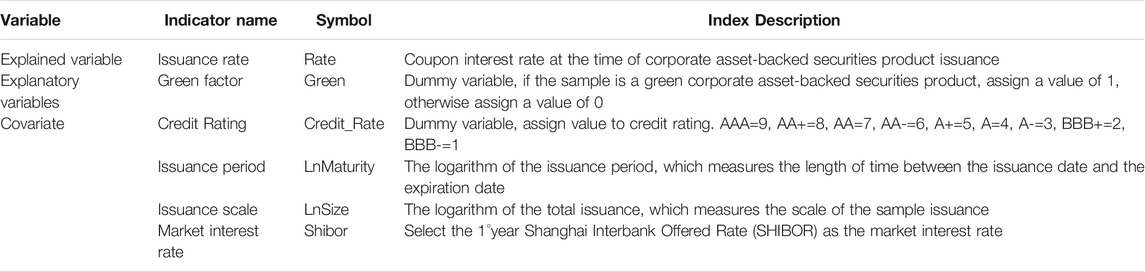

To compare and analyze the difference in the issuance pricing of green corporate asset-backed securities and traditional corporate asset-backed securities, we select all enterprise asset securitization products that were traded on exchanges (Shanghai Stock Exchange and Shenzhen Stock Exchange) from January 2012 to May 2019, and we screen them according to the following criteria: (Acharya et al., 2013) remove the delisted bond samples; (Ambrose et al., 2005) remove the progressive interest rate and floating interest rate samples; (Chen and Lee, 2020) remove the samples with incomplete data; and (Cheng et al., 2021) remove the mezzanine and sub-product samples. The final bond sample is 5,092, consisting of 167 green corporate asset-backed securities products and 4,925 traditional asset-backed securities products. The variables used in this paper are shown in Table 2. The data comes from the WIND database, the China Bond Information Network, the China Asset Securitization Analysis Network, and the China Financial Information Network Green Bond Database.

TABLE 2. Variable definition.

To accurately identify the impact of green factors, it is necessary to ensure that in the two sets of samples, except for the green attributes, there are no systematic differences in other variables related to the issuance rate. Therefore, we adopt the Propensity Score Matching method (PSM) for empirical research. The specific steps are as follows. First, the samples are divided into a test group and a control group according to whether they are green corporate asset-backed securities products. The sample of the test group is a green corporate asset-backed securities product; that is, the value of the “Green” variable is 1. The samples of the control group are traditional corporate asset-backed securities products; that is, the value of the “Green” variable is 0.

Second, a Logit model of factors affecting enterprise asset securitization product issuance pricing is established to estimate the conditional probability of each sample entering the test group. The impact factors in the model include the credit rating, bond maturity, issuance scale, and market interest rate. The Logit model is shown in formula Eq. 3.1:

Among them: α0 is the constant term, ε is the error term, and αi(i=1,2,3,4) is the coefficient.

Finally, we calculate the propensity score value of each sample in the test group and the control group, and we match the control sample with the closest score for the test group sample.

The static spread method has made improvements to the discount factor. This method holds that the discount rate cannot be simply expressed by a fixed number. Combined with the theory of the term structure of interest rates, the corresponding interest rates are not consistent across different maturities. Based on this, the static spread method considers the spot interest rate (rt) of the national debt and the fixed spread (ss) to discount the future cash flow when determining the issuance pricing of the product. The calculation method is shown in formula Eq. 3.2:

Among them, P represents the product price, CFt represents the cash flow in the t period, rt represents the spot interest rate in the t period, and ss represents the fixed spread. This method incorporates the term structure of interest rates and fixed spreads into the model to reflect the difference in interest rate levels at different points in time and the risk premium of different assets; this approach can more accurately measure product prices.

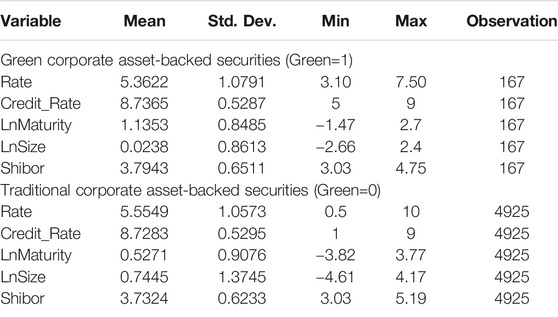

The descriptive statistics of the sample are shown in Table 3. The explanatory variable issuance interest rate has a certain difference between green corporate asset-backed securities (the test group) and traditional corporate asset-backed securities (the control group). The average issuance interest rate of the test group is 19.27°bps lower than that of the control group. This preliminarily shows that China’s green corporate asset-backed securities products are issued at low interest rates and have certain financing cost advantages. Among the covariates, the credit rating and issuance period of the test group are higher, while the issuance scale is lower. This is in line with our current understanding of the characteristics of green corporate asset-backed securities issuance. Since most of the green enterprises have undergone green certification and involve industries such as public utilities and natural resources, their company credit is relatively good. However, these industries typically have a long payback period for borrowed funds, so their financing periods are relatively high. At the same time, green enterprises are generally based on small and medium-sized enterprises with limited capital scale and capital demand, so the scale of issuance is relatively small.

TABLE 3. Descriptive statistics of the sample.

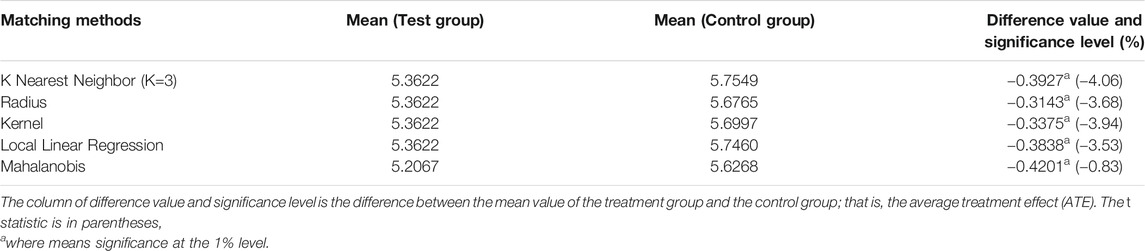

This paper uses a variety of matching methods (K Nearest Neighbor matching, radius matching, kernel matching, local linear regression matching, and Markov matching) to calculate and match the Propensity Score (PS). After the matching is completed, the average treatment effect (ATE) is calculated to examine whether the green enterprise asset securitization has an issue cost advantage. The regression results of the Logit model are shown in Table 4. The use of different matching methods results in a difference in the average issuance interest rate between the matched sample and the control group, but the average issuance interest rate of the test group is almost the same. The results obtained by different matching methods are similar, and the average treatment effect is between −31.43 and −42.01°bps, and is significant at the 1% level. Based on this, we can believe that green factors have significantly reduced the issuance interest rate of green corporate asset-backed securities, and the issuance interest rate of green corporate asset-backed securities is 36.97°bps lower than the absolute value of traditional enterprise asset-backed securitization.

TABLE 4. Results of average treatment effect.

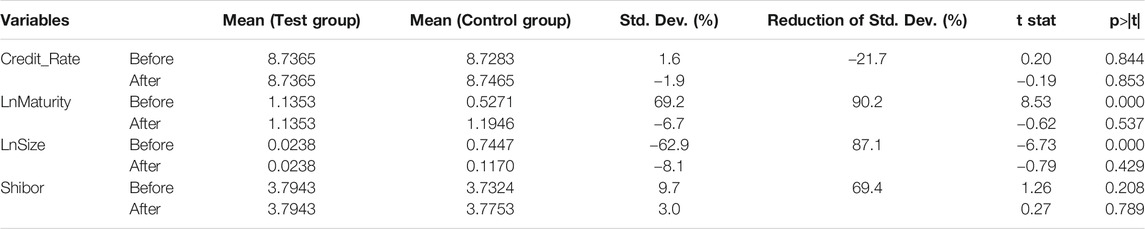

Before using the PSM method, the hypothesis of matching balance needs to be tested to verify the reliability of the matching results. We take K-nearest neighbor matching (K = 3) as an example to illustrate the test results. The specific results are shown in Table 5. Comparing the results before matching, the standard deviations of all variables after matching are significantly reduced and less than 10%, which shows that the matching method and matching samples used in this paper are reliable. At the same time, according to the t-test results, the t-statistics of all variables are not significant after matching, indicating that there is no systematic difference between the test group and the control group, so the matching method satisfies the balance hypothesis to be verified.

TABLE 5. Propensity score matching balance test results.

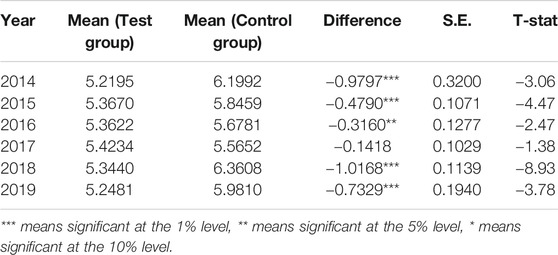

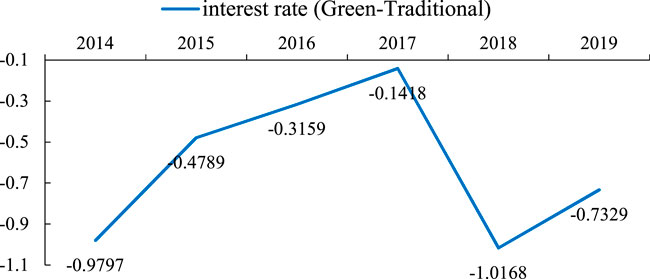

Further, in order to discover whether there is a temporal trend in this green premium, we use the year grouping propensity score matching method for matching and testing (with K Nearest Neighbor). The results showed that with the exception of 2017, the other groups showed significant differences. This may be due to the emergence of a large number of innovative green bond products in 2017 and the first sale of green financial bonds to individual investors in the over-the-counter market (OTC). From the perspective of time, the issuance interest rate of green corporate asset-backed securities is lower than that of traditional securities. The results are shown in Table 6 and Figure 1

TABLE 6. Results of average treatment effect grouped by year.

FIGURE 1. Time trend chart of issuance interest rate difference.

On the basis of empirical analysis, we further adopt the method of case analysis to test the spread advantage of green asset securitization products. In this paper, the static spread method is used to measure the issuance pricing of the “Goldwind 2016-1” products. This method uses the overall yield curve to determine the price of securitized bonds, which is suitable for the pricing of securitized products with relatively uniform cash inflows. The cash flow inflows of “Goldwind 2016-1” products are more evenly distributed in each period, and more accurate results can be obtained based on the static spread method for pricing measurement. Above all, determining the spot interest rate of the Chinese national debt and the cash flow on the repayment date of the “Goldwind 2016-1” products during the same period. Then, according to the spot interest rate on the principal and interest payment date, the interest calculation period, and the cash flow on the payment date, the static spread method is used to calculate the static spread of A1 – A5 senior securities through formula Eq. 4.1.

Since the cash flow of subordinated securities is not stable, and the coupon rate is not fixed, it is impossible to measure the static spread. The static spread calculation results of the priority securities of the “Goldwind 2016-1” products at all levels are shown in Table 7:

TABLE 7. Static spreads of assets at all levels.

To facilitate the assessment of the pricing of the coupon rates of the various senior securities of the “Goldwind 2016-1” green corporate asset-backed securities, we compare the spread between the yields of traditional corporate asset-backed securities issued with the same maturity and the same credit rating and the yields of treasury bonds. The specific situation is shown in Table 8:

TABLE 8. The spread of corporate asset-backed securities yield (AAA) and treasury bond yield.

Table 7 shows that the static spreads of the various senior securities of the “Goldwind 2016-1” products are lower than the spreads between the yields of comparable issued traditional corporate asset-backed securities and the yields of treasury bonds. This shows that compared with traditional corporate asset-backed securities, the coupon rate of “Goldwind 2016-1” green corporate asset-backed securities is relatively low at the time of issuance, and there is a certain "green" advantage in issuance costs.

The public utility attributes of green corporate asset-backed securities usually enable them to obtain policy-oriented support. First, their lower credit risk will lead to higher credit ratings. Based on the decline in risk concerns, the higher liquidity brought about by the large issuance scale has become apparent. Secondly, policy support makes their marketization degree slightly lower than that of traditional products. Moreover, green attributes bring higher policy incentives and active information disclosure. Finally, the long-term investment tendency of investors in green corporate asset-backed securities makes them have lower requirements for liquidity compensation. These attributes enable green corporate asset-backed securities to be issued with lower interest rate pricing.

The credit rating of asset-backed securities is the credit rating given to each file by a third-party rating agency when the product is issued. Different from the factors considered in traditional bond ratings, it is a comprehensive consideration of the transaction structure and credit enhancement measures of the issued products, the credit quality of the entire asset pool, and the order of securities repayment. Therefore, the higher the rating of the corporate asset-backed securities, the lower the probability of credit risk events and the lower the interest rate pricing should be (Elton et al., 2001). Green corporate asset-backed securities mostly involve industries such as natural resources, environmental protection, and new energy. They have certain attributes of public welfare or public resources, and they have a certain degree of policy orientation, so the risk of default is low. In addition, when some green corporate asset-backed securities are issued, professional institutions will be hired to fully evaluate the company’s business and financial status and carry out green certification to reduce the company’s environmental risks. Therefore, green corporate asset-backed securities usually have a relatively high credit rating, which helps green enterprises reduce their financing costs. Take the “Goldwind 2016-1” priority A1 level as an example. In the same year, all products except the “Rongyin 1 Optimization 6” (code: 142017) and the “Xingxin A4” have higher issuance rates than the “Goldwind 2016-1” priority A1 level. This shows that the “Golden Wind Green 2016-1” relies on the advantages of green attributes and the dual green certification of Det Norske Veritas and the International Finance Corporation (IFC) to reduce enterprise environmental risks and enhance the credibility of the company and its pooled assets. This reduces the risk of enterprise default, thereby reducing the product's issuance interest rate.

Based on the theory of the term structure of interest rates, bond coupon rates and bond maturity are correlated. Long-term interest rates are generally higher than short-term interest rates. Therefore, there is a positive correlation between maturity and bond issuance interest rates. According to the liquidity premium theory, bond maturity is positively correlated with bond price fluctuations caused by changes in interest rates.

Therefore, long-term bonds need to give a certain liquidity premium (interest rate compensation) to the interest rate risks in order to attract investors. Similar to ordinary securitization products, the longer the issuance period, the higher the issuance interest rate of the green enterprise securitization products. However, as the maturity period increases, the increase in the issuance rate of traditional corporate asset-backed securities will be greater than the increase in the issuance rate of green corporate asset-backed securities.

The reason for this is that investors’ liquidity compensation requirements for green corporate asset-backed securities will be lower than for traditional corporate asset-backed securities. In practice, we find that green corporate asset-backed securities investors are more inclined to make long-term investments, and their preference for liquidity is weaker than that of traditional corporate asset-backed securities investors.

This is reflected in the fact that, according to the Wind database, China’s green enterprise securitization products are mainly mid- to long-term, and products with an issuance maturity of more than 3°years account for 48.31% of total products, and the average maturity is about 4°years.

Again taking the “Goldwind 2016-1” as an example, we compare it with the “Zhongmin 2016-1”, which has a similar issuance time and a credit rating of AAA, which is a traditional corporate asset-backed securities product. With the increase in bond maturity, the increase in the issuance interest rate of the “Zhongmin 2016-1” (total increase of 1.70%) has significantly exceeded the increase of the issuance interest rate of the “Goldwind 2016-1” (total increase of 1.10%). For the level of the same issuance period, the issuance interest rate of the “Goldwind 2016-1” is still lower than the issuance interest rate of the corresponding product of “Zhongmin 2016-1”. Moreover, for the same issuance maturity level, the issuance interest rate of the “Goldwind 2016-1” is still lower than the issuance interest rate of the corresponding “Zhongmin 2016-1” product.

This shows that investors in China’s green asset securitization market are more inclined to make long-term investments. This makes green corporate asset-backed securities less sensitive to the issuance period and has certain green advantages. The issuance interest rate is significantly lower than that of traditional corporate asset-backed securities of a similar nature.

On the one hand, the larger scale of bond issuance means higher market recognition and better asset quality, as well as better liquidity. According to the liquidity premium theory, asset liquidity will affect the pricing level, and liquidity is negatively correlated with issuance interest rates. On the other hand, higher issuance usually means higher risk, and investors will worry about whether the company has sufficient repayment ability. Therefore, there will be higher interest rate expectations, which may mean that the larger the issuance scale, the higher the issuance interest rate. For green corporate asset-backed securities, the issuance scale of the product depends on the financing needs of the green enterprise. The larger the scale of the issuance, the greater the need for funds for green projects that the issuer invests in, and the more difficult it is to complete the project. The more investors demand compensation for this part of the risk, the higher the issuance rate of the green corporate asset-backed securities. We again take the “Goldwind 2016-1” priority A1 product as an example. Among all corporate asset-backed securities products with the same issuance period and credit rating in the same year, two green enterprise asset-backed products, the “G Goldwind A” (code: 131995) and the “G Gezhouba 1” (code: 142526) are with the highest issuance scale in the sample. However, as far as the issuance rate is concerned, the “G Goldwind A” and the “G Gezhouba 1” are the lowest in the sample except for the “Rongyin 1 Optimization 6” and the “Xingxin A4”. From this we can determine that due to its large financing scale and green attributes, green companies have a higher recognition of investors in the asset securitization market, making them more liquid and able to successfully issue at lower interest rates.

The market interest rate refers to the interest rate that changes with changes in the supply and demand relationship in the capital market. When market interest rates rise, in order to maintain a competitive advantage, the coupon rate of green corporate asset-backed securities will also rise, and vice versa. For green corporate asset-backed securities, in addition to the commonality of general asset securitization products, they are also supported by stronger policies. Therefore, compared with traditional asset securitization products, the degree of marketization is slightly lower. As market interest rates increase, the rate of increase in the issuance of green corporate asset-backed securities will be smaller than that of traditional corporate asset-backed securities. Taking the “Gold wind 2016-1” as an example, and by observing the yield curve of China’s treasury bonds from 2015 to 2017, we can see that as market interest rates decrease, bond prices rise. This means that market investors have increased their risk aversion in the stock market and increased their demand for products in the bond market. Therefore, the company choosing to issue green corporate asset-backed securities at this time can effectively reduce financing costs.

As an innovative financing tool, green enterprise asset securitization can obtain financing in a low-cost manner by internalizing green factors at the financing end, and thus guide capital to flow into green projects. The fundamental difference between green corporate asset-backed securities and traditional corporate asset-backed securities lies in the investment direction of the raised funds. Green corporate asset-backed securities are exclusively invested in the construction and operation of green projects. Therefore, there are obvious “green” impact factors in the process of determining the interest rate of green corporate asset-backed securities issuance.

Taking the “Goldwind 2016-1” as an example, we can see that the negative effect of green factors on issuance interest rates is mainly reflected in two levels of policy incentives and information disclosure. In terms of policy incentives, the total amount of policy subsidies from Goldwind Technology, the original owner of the “Goldwind 2016-1” product, increased significantly from 2013 to 2016. Driven by government policies, the cash flow of the “Goldwind 2016-1” green corporate asset-backed securities project received strong support to reduce its default risk, so the issuance rate was low. In terms of information disclosure, green enterprise asset securitization issuers took the initiative to conduct green certification. Information disclosure was carried out in a timely manner, and the information that the product met the green bond certification requirements was conveyed to investors. Green certification played a role in supervising the project, reducing the risk of default, and thereby reducing the issuance rate of the “Gold wind 2016-1” green corporate asset-backed securities.

As an innovative green financial tool, green corporate asset-backed securities can effectively solve the problems of narrow financing channels and maturity mismatches for green projects, which can provide strong support for achieving carbon neutrality goals and green development. We examine the financing cost advantages of green corporate asset-backed securities and its impact factors through a combination of empirical and case studies.

We find that during the sample research period, the issuance interest rate of green corporate asset-backed securities is 36.97°bp lower than that of traditional corporate asset-backed securities on average, which has certain advantages in green enterprise financing. The issuance rate of “Goldwind 2016-1” green corporate asset-backed securities is lower than that of traditional corporate asset-backed securities of the same level. It is specifically manifested in the high product credit rating, low sensitivity of Chinese green asset securitization market investors to the issuance period, and large issuance scale.

Through the combing of the development of China’s green corporate asset-backed securities market, and a comparative analysis of the issuance and pricing of green corporate asset-backed securities and traditional corporate asset-backed securities. We find that China’s green corporate asset-backed securities have obstacles such as non-standard green certification, insufficient basic asset profitability, low level of development of the green product market, and lack of relevant policies and regulations for green asset securitization. The development of China’s green enterprise asset securitization is still in its infancy, and the government is the main force to promote its development. The policy recommendations for this article are as follows:

Firstly, cultivate and attract long-term green investors. Investors’ long-term attention to the securitization of green enterprise assets is very important to its sustainable development. Specifically, we can proceed from the following perspectives: Provide tax incentives for investors to purchase green enterprise asset securitization products, including interest income tax reduction and exemption for investors; The government participates in investment in the form of industrial funds to reduce the risks faced by social capital, or to provide financial discounts for the issuance of green enterprise asset securitization; Strengthen the promotion of the concept of carbon neutrality and green development, and guide investors to join the green investment market.

Secondly, standardize the development of the green certification market. Green third-party certification can help investors screen green financial products and reduce information asymmetry. To standardize the green certification market, first of all, we should formulate a unified green industry standard, complete green industry standard documents, and enhance the authority of the certification evaluation results. Secondly, cultivate and support local certification agencies. As China’s green certification evaluation system started late, the market is mainly occupied by international agencies with years of professional knowledge and service experience. Therefore, it is necessary to support third-party green certification agencies with both professional capabilities and local positioning to promote the sustainable development of the green certification market with Chinese characteristics.

Thirdly, strengthen information disclosure. Continuous and transparent information disclosure is the key to ensuring the healthy development of green enterprise asset securitization. First, increase the market’s emphasis on environmental information and strengthen public disclosure of environmental information; Secondly, improve the information sharing mechanism, and establish a comprehensive inter-departmental coordination mechanism through the development of green enterprise asset securitization involving government departments, financial institutions, and other social institutions, so as to ensure the orderly development of green asset securitization.

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

YZ is responsible for text writing and data analysis; YY is responsible for mechanism analysis and data collection; PW is responsible for research direction proposal and article modification guidance

This research was supported by the general project of the Hunan Natural Science Foundation (2019JJ40389) and the general project of the Hunan Social Science Foundation (18YBA432).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

The Supplementary Material for this article can be found online at: https://www.frontiersin.org/articles/10.3389/fenrg.2021.696110/full#supplementary-material

Acharya, V. V., Schnabl, P., and Suarez, G. (2013). Securitization without Risk Transfer. J. Financial Econ. 107 (3), 515–536. doi:10.1016/j.jfineco.2012.09.004

Ambrose, B. W., Lacour-Little, M., and Sanders, A. B. (2005). Does Regulatory Capital Arbitrage, Reputation, or Asymmetric Information Drive Securitization? J. Finan Serv. Res. 28, 113–133. doi:10.1007/s10693-005-4358-2

Chen, Y., and Lee, C.-C. (2020). Does Technological Innovation Reduce CO2 emissions?Cross-Country Evidence. J. Clean. Prod. 263, 121550. doi:10.1016/j.jclepro.2020.121550

Cheng, C., Ren, X., Dong, K., Dong, X., and Wang, Z. (2021). How Does Technological Innovation Mitigate CO2 Emissions in OECD Countries? Heterogeneous Analysis Using Panel Auantile Regression. J. Environ. Manage. 280, 111818. doi:10.1016/j.jenvman.2020.111818

Dong, K., Dong, X., and Jiang, Q. (2020a). How Renewable Energy Consumption Lower Global CO 2 Emissions? Evidence from Countries with Different Income Levels. 43(6): 1665–1698. doi:10.1111/twec.12898

Dong, K., Dong, X., and Ren, X. (2020b). Can Expanding Natural Gas Infrastructure Mitigate CO2 Emissions? Analysis of Heterogeneous and Mediation Effects for China. Energ. Econ. 90, 104830. doi:10.1016/j.eneco.2020.104830

Duan, K., Ren, X., Shi, Y., Mishra, T., and Yan, C. (2021). The Marginal Impacts of Energy Prices on Carbon price Variations: Evidence from a Quantile-On-Quantile Approach. Energ. Econ. 95, 105131. doi:10.1016/j.eneco.2021.105131

Elton, E. J., Gruber, M. J., Agrawal, D., and Mann, C. (2001). Explaining the Rate Spread on Corporate Bonds[J]. J. Finance 56 (1). doi:10.1111/0022-1082.00324

Fabozzi, F. J., and Vink, D. (2012). Looking beyond credit ratings: Factors investors consider in pricing European asset-backed securities. Eur. Finan. Manag. 18, 515–542.

Faltin-Traeger, O., Johnson, K. W., and Mayer, C. (2010). Issuer Credit Quality and the Price of Asset Backed Securities. Am. Econ. Rev. 100 (2), 501–505. doi:10.1257/aer.100.2.501

Fang, Y., and Guo, J. (2018). Is the Environmental Violation Disclosure Policy Effective in China? —Evidence from Capital Market Reactions. Econ. Res. J. 53 (10), 158–174.

He, Jie., Jun, Q. Q., and Strahan, P. (2012). Are All Ratings Created Equal? the Impact of Issuer Size on the Pricing of Mortgage-Backed Securities[J]. J. Finance 67 (6). doi:10.1111/j.1540-6261.2012.01782.x

Jiang, H., Dong, X., Jiang, Q., and Dong, K. (2020). What Drives China's Natural Gas Consumption? Analysis of National and Regional Estimates. Energ. Econ. 87, 104744. doi:10.1016/j.eneco.2020.104744

Kou, Z., Pan, Y., and Liu, X. (2015). Does Credit Rating Really Affect Debt Issuance Costs in China?[J]. J. Financial Res. (10), 81–98.

Li, J., Yin, P., and Qiu, X. (2019). Is There Regulatory Capital Arbitrage in China's Banking Asset Securitization? Financial Regul. Res. (11), 36–49. doi:10.13490/j.cnki.frr.2019.11.003

Li, Z.-Z., Li, R. Y. M., Malik, M. Y., Murshed, M., Khan, Z., and Umar, M. (2021). Determinants of Carbon Emission in China: How Good Is Green Investment? Sustainable Prod. Consumption 27, 392–401. doi:10.1016/j.spc.2020.11.008

MacAskill, S., Roca, E., Liu, B., Stewart, R. A., and Sahin, O. (2021). Is There a green Premium in the green Bond Market? Systematic Literature Review Revealing Premium Determinants. J. Clean. Prod. 280 (P2), 124491. doi:10.1016/j.jclepro.2020.124491

Mathews, J. A., Kidney, S., Mallon, K., and Hughes, M. (2010). Mobilizing Private Finance to Drive an Energy Industrial Revolution. Energy Policy 38 (7), 3263–3265. doi:10.1016/j.enpol.2010.02.030

Moreira, F., and Zhao, S. (2018). Do credit Ratings Affect Spread and Return? A Study of Structured Finance Products. Int. J. Fin Econ. 23 (2), 205–217. doi:10.1002/ijfe.1612

Rosenthal, J. A., and Ocampo, J. M. (1988). Securitization of Credit: Inside the New Technology of Finance[M]. New York: John Wiley & Sons. 978-0-471-61368-8.

Shahbaz, M., Raghutla, C., Song, M., Zameer, H., and Jiao, Z. (2020). Public-private Partnerships Investment in Energy as New Determinant of CO2 Emissions: The Role of Technological Innovations in China. Energ. Econ. 86, 104664. doi:10.1016/j.eneco.2020.104664

Shan, Y., Guan, D., Zheng, H., Ou, J., Li, Y., Meng, J., et al. (2018). Data Descriptor: China CO2 Emission Accounts 1997-2015[J]. Scientific Data. 5, 170201. 10.1038/sdata.2017.201

Shao, X., He, M. I., and Jiang, P. (2015). The Management of Media Public Relation, Investor Sentiment and Security Offerings[J]. J. Financial Res. (09), 190–206.

Shuai, C., Chen, X., Wu, Y., Tan, Y., Zhang, Y., and Shen, L. (2018). Identifying the Key Impact Factors of Carbon Emission in China: Results from a Largely Expanded Pool of Potential Impact Factors. J. Clean. Prod. 175, 612–623. doi:10.1016/j.jclepro.2017.12.097

Song, M., and Zhang, Y. P. (2016). Research on the Problem and Optimization of Risk Retention Regulation of Credit Assets Securitization in China: Based on International Comparison[J]. Econ. Probl. 2016 (11), 48–52. doi:10.16011/j.cnki.jjwt.2016.11.010

Tang, Y., Chen, D., Chen, J., and Xu, J. (2017). The Rise of China's Securitization Market. Financial Markets, Institutions Instr. 26 (5), 279–294. doi:10.1111/fmii.12090

UNEP (2021). Making Peace with Nature [R]. United Nations Environment Programme Available at: https://wedocs.unep.org/handle/20.500.11822/34807.

Wang, F. Z., and Chen, F. Y. (2018). Board Governance, Environmental Regulation and green Technology Innovation——Empirical test based on listed companies in China's heavy polluting Industry[J]. Stud. Sci. Sci. 36 (02), 361–369. doi:10.16192/j.cnki.1003-2053.2018.02.019

Wang, X., and Li, J. (2016). Innovation and Regulation of Asset Securitization on Functional Perspective——Against the Back Ground of the New Normal[J]. Finance Econ. (06), 35–46.

Yang, L., Wang, R., Chen, Z., and Luo, X. (2020). What determines the issue price of lease asset-backed securities in China? Int. Rev. Financial Anal. 72, 101583. doi:10.1016/j.irfa.2020.101583

Yang, X., Jia, Z., Yang, Z., and Yuan, X. (2021). The effects of technological factors on carbon emissions from various sectors in China—A spatial Perspective[J]. J. Clean. Prod. 301, 126949. doi:10.1016/j.jclepro.2021.126949

Yao, M. L. (2017). On the Discount Factors of Green Bond Interest Rate [J]. Zhejiang Finance 08, 55–59.

Yin, W., Zhu, Z., Kirkulak-Uludag, B., and Zhu, Y. (2021). The determinants of green credit and its impact on the performance of Chinese banks. J. Clean. Prod. 286, 124991. doi:10.1016/j.jclepro.2020.124991

Yu, Y., and Du, Y. (2019). Impact of technological innovation on CO2 emissions and emissions trend prediction on 'New Normal' economy in China. Atmos. Pollut. Res. 10 (1), 152–161. doi:10.1016/j.apr.2018.07.005

Zhao, J., Jiang, Q., Dong, X., and Dong, K. (2020). Would environmental regulation improve the greenhouse gas benefits of natural gas use? A Chinese case study. Energ. Econ. 87, 104712. doi:10.1016/j.eneco.2020.104712

Keywords: green finance, asset securitization, green assets, issuance pricing, static spread method JEL classification: G21

Citation: Zhao Y, Yue Y and Wei P (2021) Financing Advantage of Green Corporate Asset-Backed Securities and its Impact Factors: Evidence in China. Front. Energy Res. 9:696110. doi: 10.3389/fenrg.2021.696110

Received: 16 April 2021; Accepted: 21 May 2021;

Published: 04 June 2021.

Edited by:

Kangyin Dong, University of International Business and Economics, ChinaReviewed by:

Fujing Jin, Beijing Jiaotong University, ChinaCopyright © 2021 Zhao, Yue and Wei. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Ping Wei, cHdlaUBjc3UuZWR1LmNu

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.