Xiao Gu1

Xiao Gu1 Lingui Qin

Lingui Qin Mei Zhang

Mei Zhang

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Earth Sci. , 12 January 2023

Sec. Interdisciplinary Climate Studies

Volume 10 - 2022 | https://doi.org/10.3389/feart.2022.1097346

This article is part of the Research Topic Curbing Global Warming with Multi-Scale and Multi-Sectoral Water-Energy-Food Nexus View all 5 articles

Reducing the use of traditional fossil energy and optimizing the energy consumption structure is an important starting point for China to balance sustainable and stable economic development, dual carbon goals and energy security. Green finance can help improve the energy consumption structure through providing financial support for green development. Based on this, taking the proportions of coal consumption as the index of energy consumption structure, this paper uses panel data for 30 provinces in China from 2009 to 2019, and analyzes the impact of green finance on energy consumption structure and its mechanism. The results show that the development of green finance in China has significantly improved the energy consumption structure, when considering the endogenous and robustness, the conclusion is still valid. In the mid-western region, green finance plays a greater role in improving the energy consumption structure. With the help of the quantile regression model, it is found that the higher the proportion of coal consumption, the greater the improvement effect of green finance on energy consumption structure. With the help of the threshold model, it is found that when exceeding the threshold value, the improvement effect of green finance on energy consumption structure will decline. Both the market and the government can enhance the role of green finance in optimizing the energy consumption structure. According to the research conclusion, the suggestions for improving the energy consumption structure of green finance are given from the aspects of developing green finance, formulating differentiated green finance development strategies, and encouraging green innovation.

Sustainable development of human society is being profoundly affected by climate change (Pardo Martínez and Alfonso P, 2018), while the large emissions of greenhouse gases, such as carbon dioxide, is the major cause of climate problems. China emits more than 6 billion tons of carbon dioxide every year, making it the largest carbon dioxide emitter in the world. Therefore, the Chinese government attaches great importance to climate issues and has proposed a “double carbon” target in 2020, which states that China aims to achieve carbon peaking by 2030 and carbon neutrality by 2060. The realization of China’s carbon neutrality goal is of great significance to the mitigation of global climate change. The main source of carbon dioxide is the burning of fossil fuels such as coal and oil in industrial production. To reduce carbon emissions, it is necessary to improve the energy consumption structure, reduce the use of traditional energy and increase the use of clean energy such as solar, wind and water. China’s “14th Five-Year Plan for Green Industrial Development” and “14th Five-Year Plan for Circular Economy Development” both set the improvement of energy consumption structure as an important goal during the “14th Five-Year Plan.”

Among traditional energy sources, coal and oil have larger carbon emission factors, while natural gas has a smaller one. In order to obtain 10,000 kcal of heat, 4.763 kg CO2 is emitted from burning coal, 3.370 kg CO2 is emitted from burning crude oil, and 2.217 kg CO2 is emitted from burning natural gas. However, China’s energy endowment is characterized by “rich in coal, poor in oil and little in gas,” which makes it difficult for China to transform its energy consumption structure and it requires a large amount of capital investment. Green finance provides the tools to help transform China’s energy consumption structure and can provide financial support to improve the energy consumption structure. Green finance refers to economic activities designed to support environmental improvement, climate change response and efficient use of resources, it provides financial services for project investment and financing, project operation and risk management in the fields of environmental protection, energy conservation and clean energy (Akomea-Frimpong et al., 2022).

The developed countries in Europe paid attention to the environment and climate issues earlier. The concept of environmental protection has been gradually accepted by people, and the philosophy of green development has been integrated into the financial field. In 1974, Germany established the world’s first policy-oriented environmental bank “Ecobank”. Since then, green finance has developed rapidly and become the focus of academic research. Existing studies generally agree that green finance has positive economic effects, and that green finance can reduce energy consumption intensity, improve energy efficiency and promote green development. However, few studies have explored the impact of green finance on energy consumption structure and its mechanism. Furthermore, the literature that systematically analyzes the asymmetric effects between green finance and regional location, energy consumption structure characteristics and green finance development level characteristics is scarce. Salazar (1998) put forward the green finance theory earlier. He pointed out that green finance is different from traditional finance, which emphasizes economic benefits while green finance emphasizes environmental benefits. Green finance builds a bridge between the financial world and the environmental world, which is conducive to solving environmental problems. Resources and environment are important parts of human economic and social development, and sustainable development can only be achieved if they are protected (Nedopil et al., 2021; Ma et al., 2022). Green finance is a financial innovation based on the protection of environment and resources, which is conducive to the balanced development of economy and environment (Cui et al., 2020). Meo and Abd Karim (2022) further pointed out that green finance can achieve economic development and environmental protection simultaneously through specific financial instruments.

China attaches great importance to the role of green finance because of the severe environmental pollution caused by its early rapid economic development. The Guidance on Building a Green Financial System issued by the Ministry of Environmental Protection (China) (MEP) in 2016 pointed out that green finance system refers to the institutional arrangement to support the transition to green economy through green credit, green bond, green stock index and related products, green development fund, green insurance, carbon finance and other financial instruments and related policies (MEP, 2016). This research focuses on the MEP’s definition of green finance, because we study Chinese issues. According to the definition of MEP, all related concepts such as green credit, green investment and green insurance are included in the scope of green finance in our research.

The relevant empirical research on green finance in the academic circle mainly focuses on its green effect, and it is generally believed that green finance has positive green effect, which can promote green innovation, improve the environment, upgrade the industrial structure, promote green economic growth and help carbon emission reduction. Huang and Chen (2022) studied the impact of green finance on environmental quality in China and believed that green finance can significantly improve local environmental quality. However, with the improvement of green finance development level, the improvement effect of green finance on environmental governance will weaken. Zhou et al. (2020) believed that the development of green finance in China not only reduced pollutant emissions, but also promoted economic development, achieving a win-win situation for growth and the environment. Khan et al. (2021) showed that the development of green finance in Asian countries improved environmental quality. From the perspective of green financing, Wu et al. (2021) believed that green finance was conducive to improving environmental quality. Every 1% increase in green financing level of G7 countries will lead to .375% improvement in environmental quality. Wang and Wang (2021) believed that the development of green finance in China promoted the tertiary industry more than the primary and secondary industries, thus promoting the upgrading of the industrial structure. The research of Wang et al. (2021) showed that green finance had a spatial spillover effect on the impact of high-quality energy development, and green finance could improve the high-quality development of local regions, however, the impact on adjacent regions was different. Huang et al. (2022) analyzed the impact of China’s green finance on green innovation, and believed that green finance could promote the level of green innovation in local and neighboring region, however, the strengthening of environmental supervision and the increase of green finance index would reduce the positive impact of green finance on green innovation. Muhammad Irfan et al. (2022) analyzed the impact of green finance on regional green innovation in China and found that green finance promoted the development of green finance through three mechanisms: industrial structure, economic growth and R&D input. In the pilot zone of green finance innovation and reform, green finance has a more obvious driving effect on green innovation. The study of Akomea-Frimpong et al. (2021) and Lyu et al. (2022) verified the carbon emission reduction effect of green finance. Jin et al. (2021) believed that green finance increased the consumption of non-fossil energy and reduced the carbon intensity. In addition, some scholars have also studied the green effect of green financial policies. These studies generally agree that green financial policies can increase green investment and financing, alleviate financing constraints for green innovation (Liu et al., 2021; Ning et al., 2022), promote green innovation (Jin and Han, 2018), facilitate green development (Ma et al., 2021; Gao et al., 2022), and reduce carbon emissions (Qin and Cao, 2022).

Energy is the basic input factor in modern economic activities, with the rapid developments of China’s economy and society, the consumption of traditional energy continues to increase, exacerbating environmental pollution and increasing carbon emissions. The academic research on energy consumption mainly focuses on regional differences and influencing factors. There are huge differences in economic development levels and resource endowments among different regions in China, leading to great differences in energy consumption and energy structure (Yang et al., 2018; Louis vuitton, etc., 2020; Wu et al., 2021). At the macro level, economic development level, industrial structure, environmental regulation, government intervention, energy price, and urbanization can affect the energy consumption structure (Lin and Jiang, 2017; Llop, 2018; Zhou and Chen, 2019; Farooq, etc., 2021; Wang et al., 2021; Xiong et al., 2019; Luan et al., 2021). At the meso level, the development of foreign trade, service industry and new energy can affect the energy consumption structure (Zhou et al., 2019; Hafner et al., 2021; Shahzad et al., 2021). At the micro level, innovation, financing constraints and operational efficiency can affect the energy consumption structure (Warren, 2020; Liu et al., 2021; Lee and Lee, 2022).

According to the existing literature, green finance has a certain green effect. However, there are few studies on the impact of green finance on the energy consumption structure. Only Sun and Chen (2022) analyzed the relationship between the two in China, but only discussed the relationship between the two as a whole and in different regions, without further in-depth research, such as the mechanism of action, how to develop the positive role of green finance, etc. Therefore, the relationship between the two needs to be further studied. In view of this, this research selects the provincial panel data of China from 2009 to 2019, measures the green finance index using the entropy method, and uses the share of coal consumption as the energy consumption structure indicator to comprehensively analyze the impact of green finance on the energy consumption structure. The conclusion of this study shows that green finance can significantly reduce the proportion of coal consumption and improve the energy consumption structure. The mechanism of green finance to improve the energy consumption structure is to optimize the industrial structure, improve energy efficiency and promote green innovation. In addition, in the mid-western regions, and areas where coal consumption accounts for a relatively high proportion, green finance has a more obvious effect on improving the energy consumption structure. The impact of green finance on the energy consumption structure has a single threshold effect. Once the green finance value exceeds the threshold value, the energy consumption structure improvement effect of green finance will decline. In addition, both the government and the market can play an active role in improving the energy structure transformation effect of green finance.

The possible contribution of this research includes the following. Frist, this research analyzes in detail the impact of green finance on the transformation of energy consumption structure, which expands the related research of green finance. Second, this research discusses the heterogeneity of the relationship between green finance and energy consumption structure from various aspects, and analyzes the mechanism of the role of green finance in improving energy consumption structure, which enriches the theory related to green finance. Third, the conclusion of this research shows that the development of green finance is conducive to improving the energy consumption structure. By improving the energy consumption structure, green finance will become an important way to balance economic development and carbon emission reduction in China. Therefore, our research has important practical significance.

The rest of this research is arranged as follows. The second part carries out theoretical analysis and puts forward research assumptions. The third part introduces the research methods, variables and data. The fourth part presents and discusses the empirical results. Finally, the fifth part is the conclusion, policy implications and research limitations.

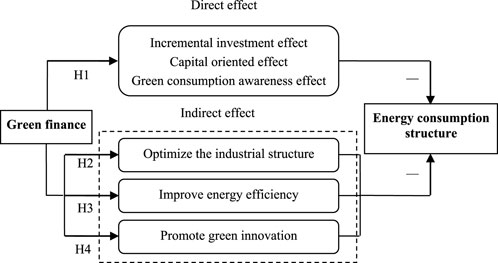

At the producer level, the improvement of the development level of green finance can make the financial resources in the green field more concentrated, promote the development of new energy industries more effectively, such as photovoltaic, lithium battery, hydropower, wind energy and other industries, reduce the dependence on coal, oil and other one-time energy, which will promote the transformation of the social energy consumption structure. The impact of green finance development on the energy consumption structure is mainly reflected in the following two aspects. On the one hand, green finance has the investment increment effect, which can increase the financial investment in green energy sector, promote the development of green energy industry sector, and increase the supply of new energy. Green finance has a leverage role, which enables it to restrict the consumption and investment loans of coal related industries, and encourage the consumption and investment of clean energy industries such as photovoltaic and natural gas from both the energy production and consumption ends, thus effectively promoting the transformation of energy consumption. On the other hand, green finance has the capital oriented effect, which can promote the development of energy conservation and environmental protection industries and promote the optimization and upgrading of industrial structure. With the development of green finance, a large number of financial resources flow to emerging energy-saving and environment-friendly enterprises, and traditional enterprises that actively carry out low-carbon transformation. In addition, the preferential policies obtained by these enterprises make them popular in the capital market, obtain more financing and higher valuation, and further attract more investment. With the entry of a large amount of investment, these enterprises will get further development, which will eventually improve the success rate of green innovation and activities, promote the technology research and technology transformation of emerging energy, reduce traditional energy consumption, and improve the energy consumption structure.

At the consumer level, the development of green finance will enhance consumers’ green consumption awareness. With the improvement of people’s living standards, consumer demand will develop in the direction of more diversified and high quality. The economic growth pattern will also change towards intensification and low carbon, which will drive consumption upgrading and promote green consumption (Yin and Xu, 2022). Guided by the concept of green development, and taking green products with high energy and resource utilization efficiency and friendly ecological environment as the consumption object, green consumption mode has become a new consumption trend under the current low-carbon economic development mode. Accelerating the development of green consumption is not only the requirement of promoting consumption upgrading and economic transformation, but also the long-term task of promoting ecological balance and achieving environmental protection. In addition to supporting green innovation and production activities, green finance will also support green consumption. By providing enterprises and residents with green credit funds and preferential interest rates, green finance can make green products have more price advantages and improve the market competitiveness of green products. Compared with other consumer goods, consumers will prefer to choose green consumer goods that have obvious price advantages and environmentally friendly. As a result, the overall consumption preference of the society will change, people’s green consumption awareness will be enhanced, and eventually a green consumption concept will be formed, which will promote the sustainable growth of green consumption. Under the guidance of the green consumption trend, consumers and producers will increase their preference for clean energy and renewable energy, so as to form a cleaner and low-carbon consumption structure.

To sum up, this reseach proposes the following hypothesis.

The development of green finance will help optimize the industrial structure. Each industry has different consumption of traditional energy. In contrast, green industries such as energy conservation, environmental protection and emerging industries consume less traditional energy, while traditional industries such as high pollution, high energy consumption and high water consumption consume more traditional energy. Therefore, the transformation of industrial structure is conducive to improving the energy consumption structure and promoting the transformation of energy consumption.

The development of green industry is inseparable from financial support. Green industry is different from ordinary industries. The development of green industry not only requires a lot of financial support, but also has a long investment return cycle and high risks. Therefore, it is difficult and costly for the green industry to obtain external funds, coupled with the widespread problem of insufficient internal funds, which together lead to the failure to meet the funding needs of green development, and green development has been seriously hindered. The emergence of green finance has brought a way to alleviate financial constraints for green development. On the one hand, green finance can guide capital investment into green industry through innovative financing tools. On the other hand, under the advocacy of relevant policies, the financial industry provides more low-cost services to the green industry, so that the green industry can obtain sufficient and low-cost external funds to meet the development needs. In addition, for highly polluting industries and production and operation activities, their financing behavior will be restricted to a certain extent. These restrictions will lead to the difficulty of obtaining external funds for highly polluting industries and production and operation activities, which will restrict their development. By encouraging green industries and green production activities and limiting energy consuming industries and production activities, it is conducive to the optimization of industrial structure. In other words, the development of green finance can optimize the industrial structure.

Therefore, we propose.

Figure 1 depicts the theoretical framework and research hypotheses.

FIGURE 1. The theoretical framework of the green finance on energy consumption structure.

This research used panel data from 30 provinces in China (excluding Tibet, Hong Kong, Macao and Taiwan) from 2005 to 2019. The original data is mainly from China Statistical Yearbook, China Industrial Statistical Yearbook, China Insurance Yearbook, statistical bulletins on national economic and social development of provinces, China Energy Statistical Yearbook, Wind database, CSMARSolution.

This research discusses the impact of green finance on the energy consumption structure in China. Eq. 1 is the benchmark regression model, where Erstrit is the energy consumption structure of province i in year t, Gfit is the green finance of province i in year t, CVit is a series of control variables, μi and δt are the fixed effects of province and year, respectively, εit is the random error term. If the coefficient of green finance α1 is significantly negative, it indicates that green finance can significantly improve the energy consumption structure.

This research also analyzes the indirect effects of green finance on the structure of energy consumption with the help of the mediating effects model. Using industrial structure optimization, energy efficiency and green innovation as mediating variables, respectively, the following mediating effect models are developed, drawing on Baron and Kenny (1986), and Hayes (2009).

where Medit is the mediating variable. The test steps for the mediating effect are as follows. Frist, Test whether α1 in Eq. 1 is significant. If α1 is not significant, there is no mediating effect. If α1 is significant, continue to the second step. Second, if neither β1 nor γ2 is significant, the bootstrap sampling method is needed to test for the presence of mediating effects. If both β1 and γ2 are all significant, and γ1 is insignificant, a complete mediating effect can be considered. If β1, γ1, and γ2 are all significant, a partial mediating effect can be considered.

We also assess whether green finance has non-linear spillover effects using the threshold model. Eq. 4 considers the single-threshold model, where green finance is the threshold variable, I (⋅) is the indicator function with a value of 1 or 0, where if the condition in the parentheses holds, it is 1, otherwise, it is 0.

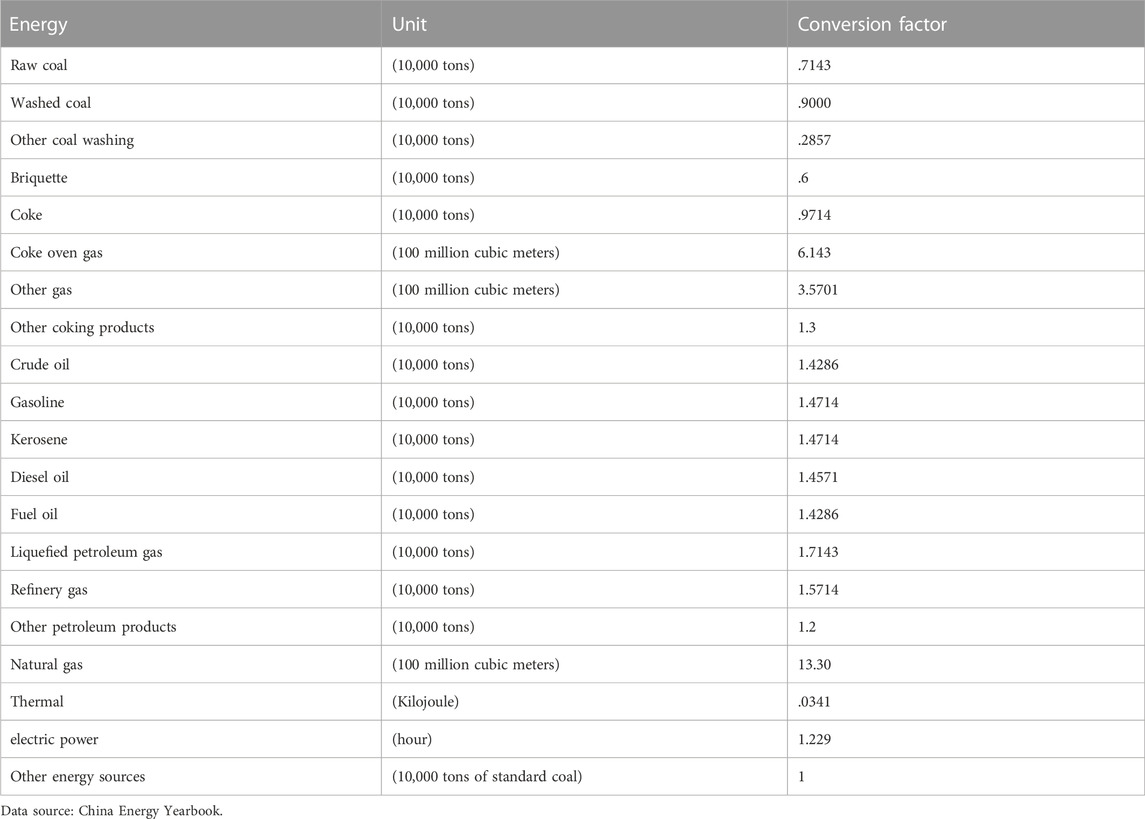

Although China has large coal reserves, the carbon emission factor of coal is the largest. Carbon dioxide from coal development and use is the main source of carbon emissions in China, accounting for about 60%–70% of China’s total carbon emissions (Liu et al., 2019). In order to reduce carbon emissions, China must reduce the use of coal, so the share of coal consumption is used to represent energy consumption structure. The specific calculation method is the ratio of coal consumption to total energy consumption, where coal consumption is the sum of seven coal related energy terminal consumption, and total energy consumption is the sum of twenty related energy terminal consumption. The conversion factor is shown in Table 1.

TABLE 1. Conversion factor of different energy sources.

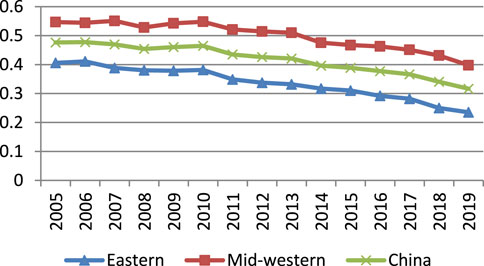

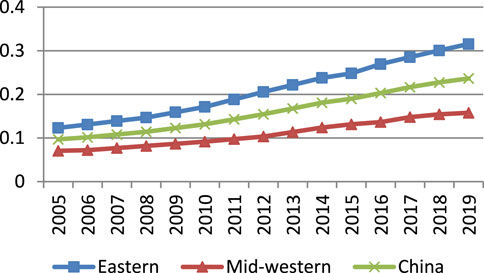

The energy consumption structure in different regions of China is shown in Figure 2. First, it can be seen that the energy consumption structure of different regions in China is quite different. Second, during the survey period, the energy consumption structure in eastern and mid-western regions continued to optimize, and coal consumption continued to decline. In contrast, the proportion of coal consumption in the eastern region is lower than that in the mid-western regions.

FIGURE 2. The energy consumption structure in different regions of China.

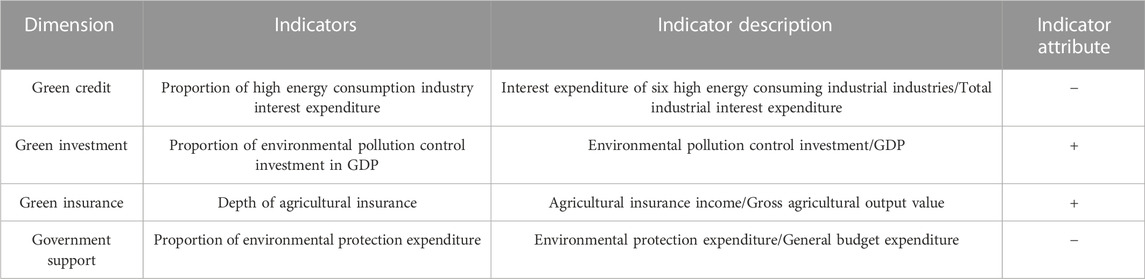

According to the Guiding Opinions on Building a Green Financial System issued by the People’s Bank of China, the green financial system includes green credit, green securities, green insurance, green investment and carbon finance, etc. Considering the availability of data, this research selects corresponding indicators from four aspects of green credit, green investment, green insurance and government support to build a green financial indicator system (Zhu et al., 2022). Table 2 presents the comprehensive green finance.

TABLE 2. Green finance index system.

The entropy method is further used to calculate the green financial index of each province. The calculation steps are as follows.

1) Build the original matrix. We create a matrix containing n rows and m columns, as shown below:

where Xij represents the value of index j in year i.

2) Normalize the sample data and calculate the proportion of index j in year i:

3) Calculate the entropy value Ej of index j:

4) Calculate the weight of index j:

where

5) The green finance index Gfit of province i in year t can be obtained according to the weight:

The development level of green finance in different regions of China is shown in Figure 3. First, it can be seen that the development level of green finance in different regions of China is quite different. Second, during the inspection period, the green finance level in eastern China and the mid-western regions continued to improve. In contrast, the green finance development level in eastern China was higher and the growth rate was faster.

FIGURE 3. The green finance index in different regions of China.

1) Industrial structure upgrading (Tps). The ratio of the added value of the tertiary industry to that of the secondary industry is used to represent industrial structure upgrading. 2) Energy efficiency (Ee). The ratio of the amount of traditional energy consumed by each province to GDP is used to represent energy efficiency. Traditional energy is converted to standard coal, and the conversion coefficient is shown in Table 1. 3) Green innovation (Gpat). The number of green patents authorized by each province is used to represent green innovation, whcih takes logarithm for demonstration.

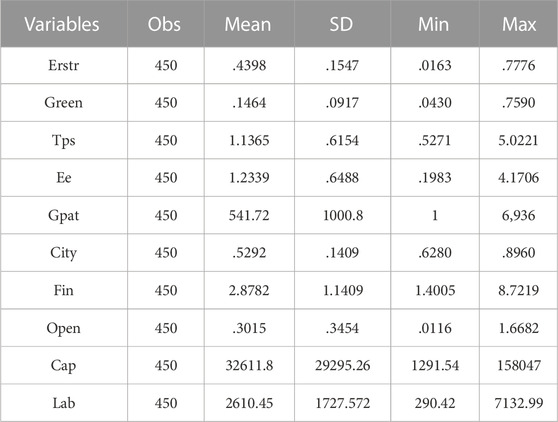

There are many factors that can affect the energy consumption structure. We also select a series of variables as control variables. 1) Urbanization level (City). It is expressed by the proportion of permanent population in the total population. 2) Financial development level (Fin). It is expressed by the ratio of the sum of deposit and loan balances to GDP. 3) Opening to the outside world (Open). It is expressed by the proportion of total import and export trade to GDP. 4) Capital investment (Cap). It is expressed by logarithm of fixed asset investment. 5) Labor input (Lab). It is expressed by the logarithm of the number of employees.

Table 3 presents the descriptive statistics.

TABLE 3. Descriptive statistics.

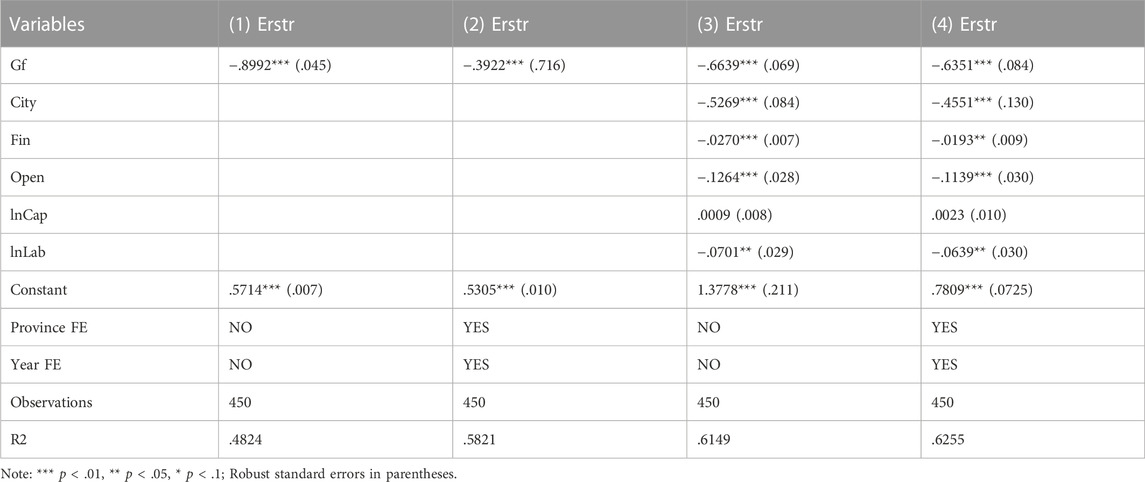

Table 4 presents the benchmark regression results of direct effects. It can be seen that in the four different models, the coefficient of green finance is significantly negative. It shows that green finance can have a significant negative impact on energy consumption structure with or without the inclusion of province fixed effects and year fixed effects, and with or without the inclusion of control variables. The results indicate that green finance reduces the use of conventional energy and improves the energy consumption structure, thus Hypothesis 1 is verified.

TABLE 4. Baseline regression results.

In addition, Column (4) presents the results controlling for province and year, and adding all control variables. The coefficient of urbanization is significantly negative, indicating that the improvement of urbanization level can improve the energy consumption structure. The coefficient of financial development level is significantly negatively, indicating the improvement of financial development level can improve the energy consumption structure. The coefficient of opening to the outside world is significantly negatively, indicating that opening to the outside world can improve the energy consumption structure. The results verify that China’s opening to the outside world pays more attention to green and high-quality development. The coefficient of capital investment is not significant, indicating that capital investment can not improve the energy consumption structure. Traditional capital investment pays more attention to economic benefits, but pays less attention to energy consumption structure and carbon emissions, which also shows the importance of developing green finance. The coefficient of labor input is significantly negative, indicating that the increase of labor can improve the energy consumption structure.

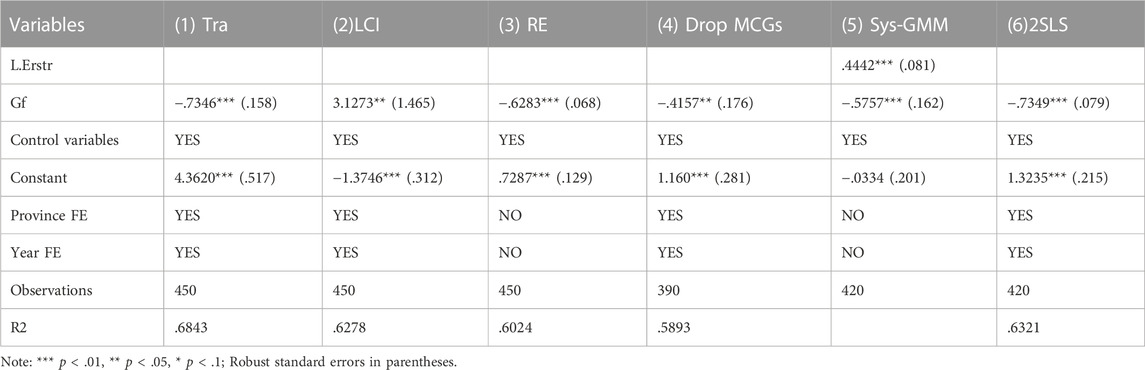

In order to further enhance the reliability of our conclusion, this research conducts robustness checks from three aspects. First, the new explained variable is used to replace the old one. The proportion of coal and oil consumption (Tra), the low-carbon indicator of energy consumption structure (LCT) are used as new explained variables, respectively. The specific calculation method of LCT is:

Use α, β, γ represents the proportion of coal, oil and gas and other energy consumption in each province, and

Then, the low-carbon indicator LCI can be expressed as:

The larger the LCT, the higher the degree of low carbonization.

Second, a new method is used. The random effect is used to replace the fixed effect.

Third, the sample is changed. In contrast, more people, resources and capital are concentrated in municipalities directly under the Central Government (abbreviated as MCG). Therefore, remove four MCGs from the sample and conduct regression again.

Table 5 shows the results of robustness test, it can be seen that the coefficient of green finance is still significantly negative through using different methods for robustness checks, revealing that green finance can still improve the energy consumption structure and the conclusion of our research has strong robustness, and further supporting the research hypotheses.

TABLE 5. Robustness test and endogenous check.

In order to alleviate the endogenous problem, the following two methods are used in our research. First, we use the system generalized method of moments (sys-GMM) to perform regression. The sys-GMM is a dynamic panel model, which takes the explained variable with a lag of one period as an explanatory variable. The sys-GMM can effectively alleviate the endogenous problem through taking the explanatory variable lagging behind one phase as the tool variable. Second, we use the instrumental variable method for regression (2SLS). The 2SLS needs to select appropriate instrumental variables. In our research, referring to the method of Wang and Zhou (2022), the average value of green finance in three provinces with the closest GDP scale among neighboring provinces is selected as the instrumental variable of green finance. In neighboring provinces with similar GDP, the development level of green finance is more similar, so it meets the correlation requirements of instrumental variables. Green finance in neighboring provinces can not affect the local energy consumption structure, so it meets the exogenous requirements of instrumental variables.

Table 5 shows the results of endogenous test. In the results of sys-GMM, the p-value of AR (1) and AR (2) is .017 and .412, respectively, which indicating that there is no autocorrelation in the random errorterm. The Sargan test result is 1.000, which indicating that there is no over-identification in instrumental variables, and the selection of instrumental variables is effective. According to the 2SLS estimation results, the Kleibergen–Paap rk LM statistic and the Kleibergen–Paap rk Wald F statistic is 54.692 and 79.603, respectively, which significantly reject the null hy-pothesis, showing it has passed the endogenous test.

It can be seen that the coefficient of green finance is still significantly negative through different methods for endogenous test, indicating that green finance still has a significant negative impact on the energy consumption structure when considering endogenous.

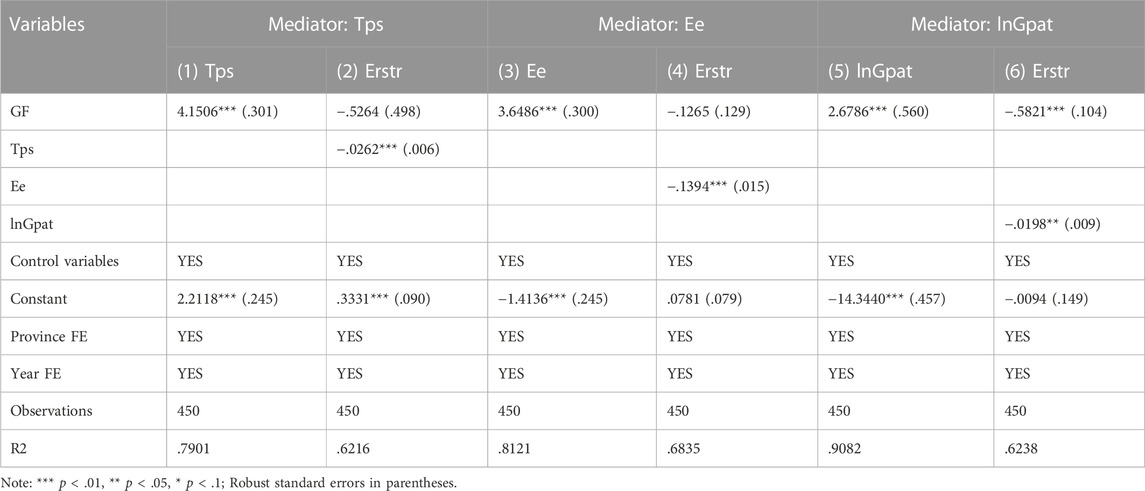

Table 6 shows the results of indirect effects, combined with the results of Column (4) in Table 3, we can see the following. First, Columns (1) and (2) shows the results when the mediating variable is industrial structure upgrading (Tps). Column (1) in Table 3 shows that green finance has significantly optimized the industrial structure. Column (2) shows that the upgrading of industrial structure has significantly improved the energy consumption structure. However, the coefficient of green finance is not significant, indicating that the upgrading of industrial structure presents complete mediating effect between green finance and energy consumption structure. Moreover, we can obtain the direct effect of green finance on energy consumption structure is −.5264, the indirect effect of that is .1087 (−.0262 × 4.1506=−.1087), and the total effect is −.6351. Thus, Hypothesis 2 is confirmed.

TABLE 6. Mediating effects.

Second, Columns (3) and (4) shows the results when the mediating variable is energy efficiency (Ee). Column (3) shows that green finance has significantly improved energy efficiency, and Column (4) shows that improving energy efficiency can significantly improve energy consumption structure. However, the coefficient of green finance is not significant, indicating that energy efficiency presents complete mediating effect between green finance and energy consumption structure. Moreover, we can obtain the direct effect of green finance on energy consumption structure is −.1265, the indirect effect of that is −.5086 (−.1394 × 3.6486=−.5086), and the total effect is −.6351. Thus, Hypothesis 3 is confirmed.

Third, Columns (5) and (6) shows the results when the mediating variable is green innovation (lnGpat). Column (5) shows that green finance has significantly promoted green innovation, and Column (6) shows that both green finance and green innovation can significantly improve the energy consumption structure, indicating that energy efficiency presents partial mediating effect. Moreover, we can obtain the direct effect of green finance on energy consumption structure is .5821, the indirect effect of that is −.0530 (−.0198 × 2.6786=−.0530), and the total effect of that is −.6351. Thus, Hypothesis 4 is confirmed.

The development level, green finance level and energy consumption structure of different regions in China vary greatly, therefore, we further check heterogeneous impacts.

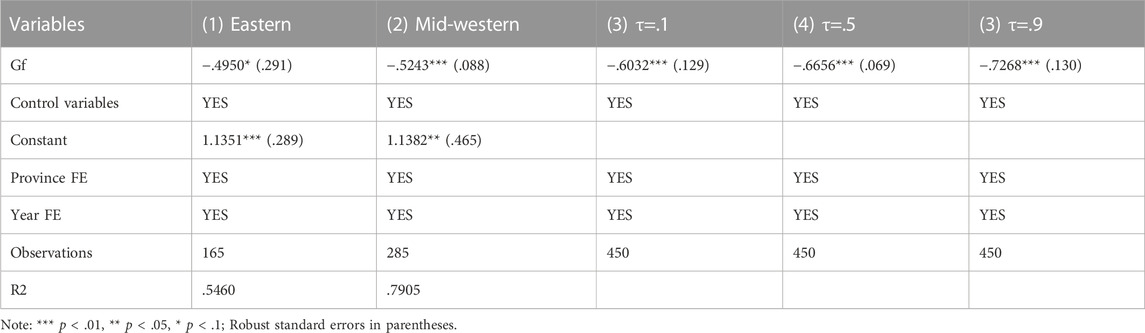

We first discuss the heterogeneity of geographical location. According to traditional criteria, we divide the whole country into 2 regions: eastern region (including 11 provinces) and mid-western region (including 19 provinces), and Columns (5) and (6) in Table 7 presents the results. It can be seen that in the two results, the coefficient of green finance is significantly negative. However, the absolute value of the coefficient of green finance in the mid-western region is greater. This means that green finance can improve the energy consumption structure in both the eastern region and the mid-western region. In contrast, in the mid-western region, green finance has a greater effect on improving the energy consumption structure.

TABLE 7. The results of geographical heterogeneity and quantile regression results.

The energy consumption structure index of the mid-western region is higher than that of the eastern region, the proportion of coal consumption is higher, and the marginal cost of reducing coal consumption is lower. Whether the above reason leads to a greater impact of green finance on the energy consumption structure in the mid-western region? That is, the greater the energy consumption structure index, the greater the impact of green finance on the energy consumption structure. We tested it using the quantile regression model. The results are showed in Columns (3)–(5) of Table 7. It can be seen that the green financial coefficient is significantly negative at different quantiles. With the increase of quantile, the absolute value of green financial coefficient increases, indicating with the increase of the energy consumption structure index, the role of green finance in improving it will also be strengthened, that is, the higher the proportion of traditional energy consumption, the easier the green finance will play a role. Therefore, the above question has been answered.

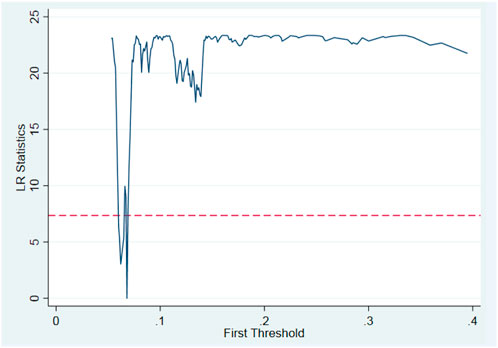

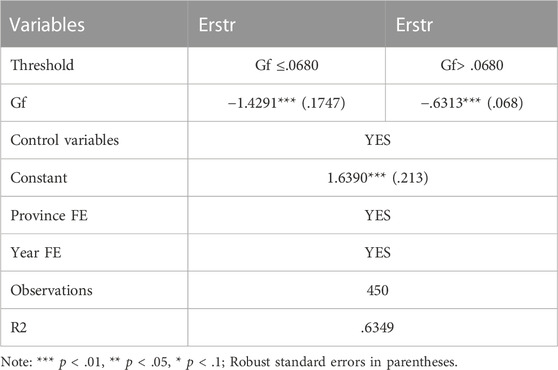

The green financial index in the eastern region is higher than that in the mid-western region, which may reduce its marginal effect. Whether this leads to a smaller impact of green finance on the energy consumption structure in the eastern region? That is, the greater the green finance index, the smaller the impact of green finance on the energy consumption structure. The threshold effect model is used to check this question. According to Hansen (1999), the threshold values are estimated through repeated sampling 300 times through the bootstrapping method. Table 8 and Figure 4 show the threshold test results. It can be seen that the single threshold effect passed the significance test, while the double threshold effect failed the significance test. The results show that there is a single threshold effect of green finance on energy consumption structure, and the threshold value is .0680. Table 9 shows the threshold effect regression results. It can be seen that in both regions, green finance can significantly improve the energy consumption structure. However, when the green finance value exceeds the threshold value of .0680, the impact of green finance on the energy consumption structure becomes smaller. Therefore, the above question has been answered.

TABLE 8. Threshold test.

FIGURE 4. Threshold value LR diagram of energy consumption structure.

TABLE 9. Threshold regression results.

One of the purposes of this paper to analyze how green finance affects the transformation of consumption structure is to play a positive role of green finance through appropriate means and enhance the role of green finance in promoting the transformation of energy consumption structure. The debate about who is playing the leading role between the government and the market has never stopped. Therefore, this paper further discusses the role of the two in the relationship between green finance and energy consumption structure. Referring to the method of Lin and Zhou (2021), on the basis of model (1), the interaction between government intervention, marketization and green finance is introduced to analyze their interaction mechanism, respectively. Furthermore, the marketization index of Wang et al. (2021) is used as the indicator of marketization, and the proportion of fiscal expenditure in GDP of each province is used as the indicator of government intervention.

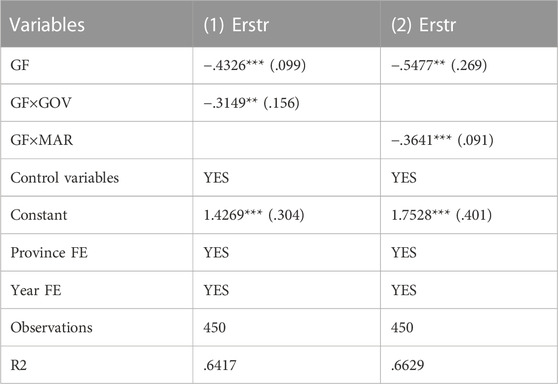

According to Table 10, the coefficient of interaction between green finance and government intervention and marketization degree is significantly negative, respectively, which indicates that both government and market have played a positive role in the relationship between green finance and energy consumption structure. Green development is an important national strategy of China and an important assessment standard for local officials. Therefore, local governments attach great importance to green development, which is conducive to the positive role of green finance. The higher the degree of marketization, the more conducive to optimizing resource allocation, which is conducive to guiding green finance to play a positive role in the external environment of green and low-carbon development. It is not contradictory that both the government and the market can enhance the role of green finance in optimizing the energy consumption structure. In reality, on the one hand, major developed countries and China attach importance to the role of the market in resource allocation in economic development; on the other hand, they also attach importance to the role of the government in guiding and supervising economic development to avoid overheating or cooling the economy.

TABLE 10. The role of government and market.

The low-carbon transformation of energy consumption is of great significance for China to ensure the security of energy supply and achieve the dual carbon goal. This research uses China’s provincial panel data to empirically analyze the impact of green finance on energy consumption transformation from multiple dimensions. Our conclusions confirm the positive impact of green finance on the transformation of energy consumption, and its mechanism is to optimize the industrial structure, improve energy efficiency and promote green innovation. It is also found that the impact of green finance on the energy consumption structure has obvious heterogeneity in different regions. In the mid-western region, the effect of green finance on improving the energy consumption structure is more obvious. According to the above calculation results, the energy consumption structure index in the eastern region is relatively small. According to the law of diminishing marginal benefits, we guess that the energy consumption structure index is relatively small, that is, the smaller the proportion of coal consumption, the smaller the impact of green finance on the energy consumption structure. Because the energy consumption structure is an explanatory variable, we will test this problem by quantile regression. With the help of the quantile regression model, we find that the higher the proportion of coal consumption, the more obvious the transformation effect of green finance on energy consumption structure. In addition, the level of green finance in the eastern region is high. According to the law of increasing marginal cost, we guess that when the level of green finance is high, the impact of green finance on the energy consumption structure may be smaller. Because green finance is the core explanatory variable, we use the threshold model to verify this problem. With the help of the threshold model, we find that although green finance can significantly improve the energy consumption structure, the improvement effect will decline when the threshold value is exceeded. Furthermore, both the market and the government can enhance the role of green finance in optimizing the energy consumption structure.

The policy implications of our conclusion are very obvious. First, green finance should be developed continuously. The green financial policy system should be improved, and the policy implementation should be strengthened. The government takes the lead in standardizing relevant standards and systems of green finance. All kinds of capital, especially social capital, should be guided into green industries through policy publicity, subsidy guidance, tax reduction and exemption, which will enhance the internal motivation of social subjects to participate in green finance. The innovation of green financial products and services should be encouraged to provide diversified green financial products. The performance of green financial business should be effectively improved through fully mobilizing the enthusiasm of market players to innovate green financial business model. Second, the differentiated green financial development strategies should be formulated and implementd in different regions. For the eastern region with a high level of green finance development, green finance should pay more attention to the quality of development, and focus on supporting high-tech green environmental protection industries or projects. For the mid-western region with a normal level of green finance development, the coverage of green finance should be expanded continuously, and more projects should be covered by green finance. Third, the green innovation should be encouraged. The government should increase support for green and low-carbon innovation and improve the capacity for independent innovation in the environmental field.

As is the case with all empirical studies, our research has some limitations. First, considering the availability of data, our research constructs an indicator system from four aspects of green credit, green investment, green insurance and government support to calculate the green financial index. If more data can be obtained in the future, we will establish a more perfect green financial indicator system. Second, our research is based on provincial level data. However, there are still large differences within each province in China. If the data of city level can be obtained in the future, the discussion on city level will be very interesting. Third, this paper discusses the impact of green finance on the energy consumption structure from the macro level. However, the energy consumption of each industry is different. Therefore, the relationship between green finance and industry energy consumption structure will be further discussed in the future. Fourth, relevant policies are an important part of green finance. In further research, we will continue to discuss the impact of relevant policies on the energy consumption structure. Dikau and Volz, 2021, Lv et al., 2020.

Publicly available datasets were analyzed in this study. This data can be found here: The original data is mainly from China Statistical Yearbook, China Industrial Statistical Yearbook, China Insurance Yearbook, statistical bulletins on national economic and social development of provinces, China Energy Statistical Yearbook, Wind database, CSMARSolution.

XG was the first author who contributed to funding acquisition, project administration, and manuscript revision. LQ was the corresponding author who contributed to data collection, statistical analysis, and manuscript writing. MZ helped with data collection and statistical analysis.

This work was supported by the Major Project of the National Social Science Foundation of China “Research on the international trade competitiveness of China’s digital copyrights under the double-circulation background” (grant numbers No.21&ZD322).

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Akomea-Frimpong, I., Adeabah, D., Ofosu, D., and Tenakwah, E. J. (2022). A review of studies on green finance of banks, research gaps and future directions. J. Sustain. Financ. Inv. 12 (4), 1241–1264. doi:10.1080/20430795.2020.1870202

Baron, R. M., and Kenny, D. A. (1986). The moderator-mediator variable distinction in social psychological research: Conceptual, strategic and statistical considerations. J. Per. Soc. Psychol. 51 (6), 1173–1182. doi:10.1037/0022-3514.51.6.1173http://refhub.elsevier.com/S0148-2963(22)00276-4/h0385

Clara Inés Pardo, M., William, H., and Alfonso, P. (2018). Climate change in Colombia: A study to evaluate trends and perspectives for achieving sustainable development from society. Int. J. Clim. Chang. Str. 10, 632–652. doi:10.1108/IJCCSM-04-2017-0087

Cui, H. R., Wang, R. Y., and Wang, H. R. (2020). An evolutionary analysis of green finance sustainability based on multi-agent game. J. Clean. Prod. 269, 121799. doi:10.1016/j.jclepro.2020.121799

Dikau, S., and Volz, U. (2021). Central bank mandates, sustainability objectives and the promotion of green finance. Ecol. Econ. 184, 107022. doi:10.1016/j.ecolecon.2021.107022

Farooq, U., Ahmed, J., Tabash, M. I., Anagreh, S., and Subhani, B. H. (2021). Nexus between government green environmental concerns and corporate real investment: Empirical evidence from selected Asian economies. J. Clean. Prod. 314, 128089. doi:10.1016/j.jclepro.2021.128089

Gao, L., Tian, Q., and Meng, F. (2022). The impact of green finance on industrial reasonability in China: Empirical research based on the spatial panel durbin model. Environ. Sci. Pollut. Res., 1–17. doi:10.1007/s11356-022-18732-y

Hafner, S., Jones, A., Anger-Kraavi, A., and Monasterolo, I. (2021). Modelling the macroeconomics of a ‘closing the green finance gap’ scenario for an energy transition. Environ. Innov. Soc. Tr. 40, 536–568. doi:10.1016/j.eist.2021.10.006

Hansen, B. E. (1999). Threshold effects in non-dynamic panels: Estimation, testing, and inference. J. Econ. 93 (2), 345–368. doi:10.1016/S0304-4076(99)00025-1

Hayes, A. F. (2009). Beyond Baron and Kenny: Statistical mediation analysis in the new millennium. Commun. Monogr. 76 (4), 408–420. doi:10.1080/03637750903310360

Huang, Y., Chen, C., Lei, L., and Zhang, Y. (2022). Impacts of green finance on green innovation: A spatial and nonlinear perspective. J. Clean. Prod. 365, 132548. doi:10.1016/j.jclepro.2022.132548

Huang, Y., and Chen, C. (2022). The spatial spillover and threshold effect of green finance on environmental quality: Evidence from China. Environ. Sci. Pollut. Res. 29, 17487–17498. doi:10.1007/s11356-021-16892-x

Jin, J., and Han, L. (2018). Assessment of Chinese green funds: Performance and industry allocation. J. Clean. Prod. 171, 1084–1093. doi:10.1016/j.jclepro.2017.09.211

Jin, Y., Gao, X., and Wang, M. (2021). The financing efficiency of listed energy conservation and environmental protection firms: Evidence and implications for green finance in China. Energy Policy. 153, 112254. doi:10.1016/j.enpol.2021.112254

Khan, M. A., Riaz, H., Ahmed, M., and Saeed, A. (2022). Does green finance really deliver what is expected? An empirical perspective. Borsa. istanb. Rev. 22 (3), 586–593. doi:10.1016/j.bir.2021.07.006

Lee, C. C., and Lee, C. C. (2022). How does green finance affect green total factor productivity? Evidence from China. Energy Econ. 107, 105863. doi:10.1016/j.eneco.2022.105863

Lin, B., and Zhu, J. (2017). Energy and carbon intensity in China during the urbanization and industrialization process: A panel var approach. J. Clean. Prod. 168, 780–790. doi:10.1016/j.jclepro.2017.09.013

Liu, H., Tang, Y. M., Iqbal, W., and Raza, H. (2022). Assessing the role of energy finance, green policies, and investment towards green economic recovery. Environ. Sci. Pollut. Res. 29, 21275–21288. doi:10.1007/s11356-021-17160-8

Liu, J., Wang, K., Zou, J., and Kong, Y. (2019). The implications of coal consumption in the power sector for China’s CO2 peaking target. Appl. Energy 253, 113518. doi:10.1016/j.apenergy.2019.113518

Liu, S., Xu, R., and Chen, X. (2021). Does green credit affect the green innovation performance of high-polluting and energy-intensive enterprises? Evidence from a quasi-natural experiment. Environ. Sci. Pollut. Res. 28, 65265–65277. doi:10.1007/s11356-021-15217-2

Llop, M. (2018). Measuring the influence of energy prices in the price formation mechanism. Energy Policy 117, 39–48. doi:10.1016/j.enpol.2018.02.040

Luan, B., Zou, H., Chen, S., and Huang, J. (2021). The effect of industrial structure adjustment on China’s energy intensity: Evidence from linear and nonlinear analysis. Energy 218, 119517. doi:10.1016/j.energy.2020.119517

Lv, Y., Chen, W., and Cheng, J. (2020). Effects of urbanization on energy efficiency in China: New evidence from short run and long run efficiency models. Energy Policy 147, 111858. doi:10.1016/j.enpol.2020.111858

Lyu, B., Da, J., Ostic, D., and Yu, H. (2022). How does green credit promote carbon reduction? A mediated model. Front. Environ. Sci. 10, 878060. doi:10.3389/fenvs.2022.878060

Ma, Q., Tariq, M., Mahmood, H., and Khan, Z. (2022). The nexus between digital economy and carbon dioxide emissions in China: The moderating role of investments in research and development. Technol. Soc. 68, 101910. doi:10.1016/j.techsoc.2022.101910

Ma, X., Ma, W., Zhang, L., Shi, Y., Shang, Y., and Chen, H. (2021). The impact of green credit policy on energy efficient utilization in China. Environ. Sci. Pollut. Res. 28, 52514–52528. doi:10.1007/s11356-021-14405-4

Meo, M. S., and Abd Karim, M. Z. (2022). The role of green finance in reducing CO2 emissions: An empirical analysis. Borsa. istanb. Rev. 22 (1), 169–178. doi:10.1016/j.bir.2021.03.002

Mep, (2016). Guiding Opinions on building a green financial system. https://www.mee.gov.cn/gkml/hbb/gwy/201611/t20161124_368163.htm.

Muhammad Irfan, M., Razzaq, A., Sharif, A., and Yang, X. (2022). Influence mechanism between green finance and green innovation: Exploring regional policy intervention effects in China. Technol. Forecast. Soc. 182, 121882. doi:10.1016/j.techfore.2022.121882

Nedopil, C., Dordi, T., and Weber, O. (2021). The nature of global green finance standards—evolution, differences, and three models. Sustainability 13, 3723. doi:10.3390/su13073723

Ning, Y., Cherian, J., Sial, M. S., Álvarez-Otero, S., Comite, U., and Zia-Ud-Din, M. (2022). Green bond as a new determinant of sustainable green financing, energy efficiency investment, and economic growth: A global perspective. Environ. Sci. Pollut. Res., 21 1–16. doi:10.1007/s11356-021-18454-7

Qin, J., and Cao, J. (2022). Carbon emission reduction effects of green credit policies: Empirical evidence from China. Front. Environ. Sci. 10, 798072. doi:10.3389/fenvs.2022.798072

Salazar, J. (1998). Environmental finance: Linking two worlds. A Workshop Financial Innovations Biodivers. Bratislava 1, 2–18. https://www.scirp.org/reference/referencespapers.aspx?referenceid=2806043.

Shahzad, U., Lv, Y., Dogan, B., and Xia, W. (2021). Unveiling the heterogeneous impacts of export product diversification on renewable energy consumption: New evidence from G-7 and E-7 countries. Renew. Energy 164, 1457–1470. doi:10.1016/j.renene.2020.10.143

Sun, H., and Chen, F. (2022). The impact of green finance on China's regional energy consumption structure based on system GMM. Resour. Policy 76, 102588. doi:10.1016/j.resourpol.2022.102588

Wang f, F., Wang, R., and He, Z. (2021). The impact of environmental pollution and green finance on the high-quality development of energy based on spatial Dubin model. Resour. Policy. 74, 102451. doi:10.1016/j.resourpol.2021.102451

Wang m, M., Li, X., and Wang, S. (2021). Discovering research trends and opportunities of green finance and energy policy: A data-driven scientometric analysis. Energy Policy. 154, 112295. doi:10.1016/j.enpol.2021.112295

Wang, X., and Wang, Q. (2021). Research on the impact of green finance on the upgrading of China’s regional industrial structure from the perspective of sustainable development. Energy Policy. 74, 102436. doi:10.1016/j.resourpol.2021.102436

Wang, Y., and Zhou, Y. (2022). Green finance development and enterprise innovation. J. Financ. Econ., 1–15. doi:10.16538/j.cnki.jfe.20220615.101

Warren, P. (2020). Blind spots in climate finance for innovation. Adv. Clim. Chang. Res. 11 (1), 60–64. doi:10.1016/j.accre.2020.05.001

Wu, W., Cheng, Y., Lin, X., and Yao, X. (2019). How does the implementation of the Policy of Electricity Substitution influence green economic growth in China? Energy Policy. 131, 251–261. doi:10.1016/j.enpol.2019.04.043

Wu, X., Sadiq, M., Chien, F., Ngo, Q. T., Nguyen, A. T., and Trinh, T. T. (2021). Testing role of green financing on climate change mitigation: Evidences from G7 and E7 countries. Environ. Sci. Pollut. Res. 28, 66736–66750. doi:10.1007/s11356-021-15023-w

Xiong, S., Ma, X., and Ji, J. (2019). The impact of industrial structure efficiency on provincial industrial energy efficiency in China. J. Clean. Prod. 215, 952–962. doi:10.1016/j.jclepro.2019.01.095

Yang, T., Chen, W., Zhou, K., and Ren, M. (2018). Regional energy efficiency evaluation in China: A super efficiency slack-based measure model with undesirable outputs. J. Clean. Prod. 198, 859–866. doi:10.1016/j.jclepro.2018.07.098

Yin, X., and Xu, Z. (2022). An empirical analysis of the coupling and coordinative development of China's green finance and economic growth. Resour. Policy. 75, 102476. doi:10.1016/j.resourpol.2021.102476

Zhou, C., and Chen, X. (2019). Predicting energy consumption: A multiple decomposition-ensemble approach. Energy 189, 116045. doi:10.1016/j.energy.2019.116045

Zhou, D., Yu, Y., Wang, Q., and Zha, D. (2019). Effects of a generalized dual-credit system on green technology investments and pricing decisions in a supply chain. J. Environ. Manage. 247, 269–280. doi:10.1016/j.jenvman.2019.06.058

Zhou, X., Tang, X., and Zhang, R. (2020). Impact of green finance on economic development and environmental quality: A study based on provincial panel data from China. Environ. Sci. Pollut. Res. 27, 19915–19932. doi:10.1007/s11356-020-08383-2

Keywords: green finance, coal consumption, energy consumption structure, carbon emission reduction, indirect effects

Citation: Gu X, Qin L and Zhang M (2023) The impact of green finance on the transformation of energy consumption structure: Evidence based on China. Front. Earth Sci. 10:1097346. doi: 10.3389/feart.2022.1097346

Received: 13 November 2022; Accepted: 30 December 2022;

Published: 12 January 2023.

Edited by:

Hong Chen, Jiangnan University, ChinaReviewed by:

Ziqian Xia, Tongji University, ChinaCopyright © 2023 Gu, Qin and Zhang. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Lingui Qin, cWlubGluZ3VpQHN5YXUuZWR1LmNu

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.