Alina Brad

Alina Brad Tobias Haas

Tobias Haas Etienne Schneider

Etienne Schneider

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Clim. , 15 January 2024

Sec. Carbon Dioxide Removal

Volume 5 - 2023 | https://doi.org/10.3389/fclim.2023.1268736

This article is part of the Research Topic Carbon dioxide removal: Perspectives from the social sciences and humanities View all 13 articles

Net zero targets have rapidly become the guiding principle of climate policy, implying the use of carbon dioxide removal (CDR) to compensate for residual emissions. At the same time, the extent of (future) residual emissions and their distribution between economic sectors and activities has so far received little attention from a social science perspective. This constitutes a research gap as the distribution of residual emissions and corresponding amounts of required CDR is likely to become highly contested in the political economy of low-carbon transformation. Here, we investigate what function CDR performs from the perspective of sectors considered to account for a large proportion of future residual emissions (cement, steel, chemicals, and aviation) as well as the oil and gas industry in the EU. We also explore whether they claim residual emissions to be compensated for outside of the sector, whether they quantify these claims and how they justify them. Relying on interpretative and qualitative analysis, we use decarbonization or net zero roadmaps published by the major sector-level European trade associations as well as their statements and public consultation submissions in reaction to policy initiatives by the EU to mobilize CDR. Our findings indicate that while CDR technologies perform an important abstract function for reaching net zero in the roadmaps, the extent of residual emissions and responsibilities for delivering corresponding levels of negative emissions remain largely unspecified. This risks eliding pending distributional conflicts over residual emissions which may intersect with conflicts over diverging technological transition pathways advocated by the associations.

Net zero targets have emerged as a new guiding principle of climate policy, replacing emission reduction targets (Net Zero Tracker, 2023). Conceptually, net zero targets imply the use of carbon dioxide removal (CDR) to compensate for continued residual emissions.1 Most modeled scenarios limiting global warming to 1.5°C but also 2°C in line with the Paris agreement envision large-scale CDR deployment, including CDR technologies such as Bioenergy with Carbon Capture and Storage (BECCS) or Direct Air Carbon Capture and Storage (DACCS), to compensate for residual, “hard to abate” emissions and, in select scenarios, reduce the temporary overshoot of temperature targets across the late century (Luderer et al., 2018; IPCC, 2022, 2023a). CDR is also increasingly mainstreamed within and recognized as an important component of national net zero strategies (Smith et al., 2022; Buck et al., 2023). To date, however, literature on CDR is dominated by techno-economic perspectives which do not adequately address the societal complexities and challenges, and—particularly—the politics and inherently conflictive nature of (future) large-scale CDR deployment (Carton et al., 2020).

Nascent social science debates on CDR have highlighted the potential of projected, hypothetical large-scale deployment of CDR technologies to undermine or delay emission reduction efforts (often termed “mitigation deterrence”; Markusson et al., 2018; Brad and Schneider, 2023; Carton et al., 2023), and analyzed how different stakeholder positions on CDR shape emergent patterns in CDR policy-making, what conflict cleavages may arise from this (Schenuit et al., 2021; Boettcher et al., 2023) and what governance principles could guide CDR policy design development (Honegger et al., 2022). Most recently, the concept of 'residual emissions' presupposed in net zero targets has been subjected to critical scrutiny (cf. Armstrong and McLaren, 2022; Buck et al., 2023; Lund et al., 2023). Buck et al. (2023) find that while countries' long-term mitigation strategies project a substantial levels of residual emissions which will need to be balanced by CDR residual emissions have so far remained ill-defined and largely unexplored. Also in the academic debate, there is currently no widely established definition of residual emissions. While Buck et al. (2023, p. 1) define them as “emissions that are regarded as hard to abate and will need to be compensated via carbon removal,” Schenuit et al. (2023, p. 4) understand residual emissions as “a quantity that simply describes which emissions actually enter the atmosphere in and after the net-zero year,” explicitly delineating the term from hard to abate emissions. Here we use the term residual emissions to refer to a specific quantity of emissions in reference to a net zero year which will necessitate negative emissions. As such residual emissions typically require justification as to why they cannot be abated. As Lund et al. (2023) and Schenuit et al. (2023) highlight, this implies potentials for conflicts and contestations regarding the crucial question what actors can legitimately claim residual emissions and which economic and social activities are considered socially necessary yet economically and/or politically “hard to abate” technically or politically from today's perspective. However, while these contributions have carved out that residual emissions are not objectively given but discursively constructed, legitimated and—ultimately—contested, different claims to residual emissions and corresponding requirements for CDR deployment (and the related distribution of negative emissions) have so far hardly been investigated empirically.

We explore what functions CDR plays in achieving net zero targets from the perspective of trade associations of four economic sectors in the EU which, besides agriculture, are considered to account for most residual emissions in the International Energy Agency's (IEA, 2021a) Net Zero by 2050 scenario and in the scenario studies analyzed in the IPCC Sixth Assessment Report (IPCC, 2023b), i.e., cement, steel, the chemical industry and aviation (cf. Buck et al., 2023). We also investigate the perspectives of the gas and (fossil) fuel industry as highly emission-intensive incumbent industries on possible functions of CDR in reaching net zero targets. As the business model of these industries is existentially threatened by climate change mitigation (Colgan et al., 2021), authors have argued that these industries may have an interest in CDR to slow down decarbonization (Carton, 2019) and possibly also to re-invent themselves as a carbon disposal industry based on its geological and engineering expertise (Hastings and Smith, 2020). We excluded shipping and agriculture from our analysis for methodological reasons as we did not find any net zero roadmaps or scenario documents from the main trade associations of these sectors (European Community Shipowners' Association, COPA COGECA), which we used as the main empirical basis for analysis and comparison of the other sectors in this study (for more details on our methodological approach see Section 3).

We adopt a critical political economy perspective on the transformation toward net zero (Newell, 2019) to transcend the overwhelmingly technological and economic focus of many academic and policy debates on CDR. Through this, we particularly seek to foreground diverging interests and strategies of different business sectors as well as related lines of conflicts as CDR technologies evolve from contested renderings in climate models (Beck and Mahony, 2018) toward an essential component of climate policies in the EU (Geden and Schenuit, 2020). Specifically, we asked how the main EU-level trade associations of these sectors position themselves toward the nexus of residual emissions and CDR, and what function CDR performs in their respective sector-specific visions to reach net zero. Regarding particular functions of CDR, we wanted to find out whether CDR is envisioned as part of the sector-specific decarbonization paths at all and, if so, what emissions CDR is supposed to compensate for. We also investigated whether these trade associations claim residual emissions for their sectors beyond 2050, how they justify these claims and whether they quantify residual emissions. Our focus is on whether these actors claim residual emissions in the sense that they do not compensate residual emissions in “their” respective value chains, which would require negative emissions in other economic sectors. Through this analysis we contribute to the nascent debate on the politics of residual emissions and potential distributional conflicts between sectors, specifically regarding the issue what and whose needs and interests are reflected in the construction of projected residual emissions (Lund et al., 2023).

In the following section we develop our analytical perspective based on approaches from critical political economy. Section 3 outlines our methodological approach. In Section 4 we briefly reconstruct how the net zero target for 2050 came about in the EU and situate more recent, particularly CDR-related EU climate policy initiatives in this context. Subsequently, Section 5 delves into the sector specific strategies to achieve net zero, presenting the core results from our analysis. In Section 6 we discuss our main findings regarding the implications for wider discussions on the integration of CDR into climate policy and the politics of net zero more broadly. Section 7 outlines areas for further investigation.

As environmental crisis deepen, a broad field of research has been established around the terms transition and transformation2 in recent decades (Köhler et al., 2019; Scoones et al., 2020). In this context, our study is specifically based on strands of critical political economy to conceptualize socio-technical change as a contested political process in which various actors with their respective interests and values struggle with each other or may form coalitions (Newell, 2019). While the study of interest conflict and coalition building for (or against) climate policy measures is not reserved to critical political economy approaches (Sabel and Victor, 2022), this lens allows us to understand competing interests and conflicts between actors and social forces as rooted in (although not directly determined by) social relations of production and the specific position they occupy in a given (capitalist) mode of production (Brand et al., 2022). Accordingly, there are not only competing and antagonistic interests between social classes, e.g., capital and labor, but also within capital. Capital is fractionalized along different bases of accumulation (e.g., fossil fuel extraction or deployment of renewables), and the related accumulation strategies are always contingent upon a specific spatial and temporal context and require a strategic orientation and political safeguarding by the state (Jessop, 1990; on the notion of capital fractions cf. Overbeek and van der Pijl, 1993).

Against this background, and despite the historical reliance of capitalism on fossil energy (Malm, 2016), Newell and Paterson (2010) emphasize that capitalism does have a certain capacity for change, and that both actors and governance regimes can change their orientation. At the same time, processes of low-carbon transition and transformation are inherently political, specifically regarding contentious issues as to “what is to be transformed, who is to do the transforming” and to what extent disruptive processes of change as opposed to incremental shifts are required to drastically reduce GHG emissions (Scoones et al., 2015, p. 1–2). This warrants particular attention as to which actors and social forces attempt to drive and shape social and economic change under capitalism in certain historical directions (Brand, 2016).

Such a perspective allows us to go beyond superficial assertions about 'green growth' and 'win-win solutions' in order to delve into the underlying conflicts and compromises associated with the process of fundamentally reshaping an economy and the power relations embedded in it in the process of 'deep' decarbonization (Newell, 2015, p. 70–71). This not only implies an analysis of struggles between incumbent actors seeking to preserve the status quo of a fossil fuel-based energy system and social forces trying to advance low-carbon transformation, breaking up fossil path dependencies which have been described as a 'carbon lock-in' (Unruh, 2000; Asayama, 2021). It also reveals how different actors advocate and promote diverging transition pathways based on different sets of low-carbon or 'net zero' technologies which benefit or disadvantage various capital fractions differently, based on their current accumulation strategy, but also the energy sources and feedstock they depend on (e.g., centralized nuclear vs. decentralized renewable energy) (Rosenbloom et al., 2018).

Against this background, we assume that different coalitions of capital fractions and other actors may form around the promotion of different pathways, giving rise to specific fault lines in the politics of low-carbon transformation and decarbonization. Such fault lines become specifically apparent at critical junctures or branching points leading to different pathways of transformative change (Newell, 2015). In these conflicts, visions and expectations of pathways and technologies, sustained by specific sociotechnical imaginaries—i.e., collectively held visions of the future, underpinned by interrelated ideas of future society and technological progress (Jasanoff and Kim, 2009)—as well as technological discourses and technology myths (Peeters et al., 2016), motivate real policy and investment decision, but also inaction (cf. Beckert, 2016). Such visions and expectations often rely on highly optimistic and uncertain assumptions regarding future technology development. Yet, even though highly uncertain, they are often (unintentionally) held or (intentionally) constructed and advanced because they serve specific purposes (Peeters et al., 2016), particularly by promising technological “fixes” to climate change and the ecological contradictions of capitalism more generally. Building on Harvey's (2006) concept of spatiotemporal fixes we understand technological fixes in the double sense of providing a temporary solution to (ecological) contradictions of capitalisms, while at the same time fixing capital in the form of investment in new infrastructure, machinery, built environment, etc. (cf. Markusson et al., 2017; Carton, 2019). We reveal how visions and expectations of CDR technologies reshape different capital fractions' vision of low-carbon transition pathways. Specifically, we are interested in whether the assumption of future large-scale availability of CDR technologies allows stakeholders to envision pathways toward net zero greenhouse gas emissions compatible with partly maintaining emission-intensive accumulation strategies.

To investigate these questions empirically, we focus on four sectors which are considered to account for most residual emissions in relevant IEA and IPCC scenarios—cement, steel, aviation, and the chemical industry—as well as the oil and gas industry as highly emission-intensive incumbent industries (see Section 1). Our approach to approximate the interests and strategies pursued by these capital fractions is based on analyzing publicly available statements and position papers of the major European branch-level trade associations. The scientific literature on lobbying activities in the EU has highlighted that many large companies in the EU chose to establish their own lobbying capacity in Brussels and increasingly rely on specialized service providers such as law firms, public affairs agencies and think tanks to influence the policy agenda in the 1990's and 2000's. Nonetheless, trade associations have remained key actors in business interest organization, intermediation and assertion in the EU (Eising, 2007; Coen and Richardson, 2011). As Fagan-Watson et al. (2015) point out, many companies consider trade associations lobbying advantageous over direct lobbying by individual firms because policymakers tend to regard their perspectives as more representative of the industry as a whole. To maintain this specific advantage, trade associations need to constantly aggregate and mediate diverse positions and interests and to articulate branch-level compromises, which makes them a particularly interesting entry point for our study.

However, the fact that trade associations typically articulate and advocate lowest common denominator compromises also implies that by focusing on their positions, we cannot account for the heterogeneity, internal conflicts and different strategic approaches of their members. Individual companies may substantially deviate from the positions adopted by their respective trade associations, and such differences may even lead companies to leave trade associations and possibly also found competing ones (Fagan-Watson et al., 2015). While this warrants closer attention to the extent to which major companies in the respective sectors are aligned with the trade associations' positions, we only consider in this analysis whether the major European producers in the respective industries are members of the trade associations (directly or indirectly through respective national trade associations) and whether there are alternative, competing trade associations in the industry, i.e., to what extent the trade association is indeed dominant in the industry. Assessing the exact extent to which trade associations are representing the entire industry (e.g., in terms of proportion of sector turnover or the percentage of members over the total number of companies in the industry) is complicated by the fact that trade associations typically do not make such data available publicly, as this would potentially contradict their claim to represent the entire industry.

Trade associations employ a variety of tools and strategies to exert policy influence, ranging from organizing events with policymakers and technical policy experts, briefing policymakers on specific (technical) subjects, and launching policy initiatives within the EU institutions, to press work, ad campaigns and the publication of position papers. Focusing on publicly available statements and position papers therefore only partly reflects the activities, strategies, and prioritizations of the associations' lobbying activities. Nonetheless, following Tilsted et al. (2022), we consider these documents particularly relevant because they can be read as attempts to maintain legitimacy, especially from the position of actors facing increasing pressure to reduce their GHG emissions. Against this background, these documents serve as a means to preserve the credibility of these actors, helping to demonstrate their commitment to sustainable practices and their ability to adapt to evolving environmental challenges. Additionally, these documents act as tools for interest mediation within the sectors causing and being affected by climate change. These documents both reflect the results of and facilitate the discussion and negotiations between different stakeholders within the respective industries and between the industry and other stakeholders.

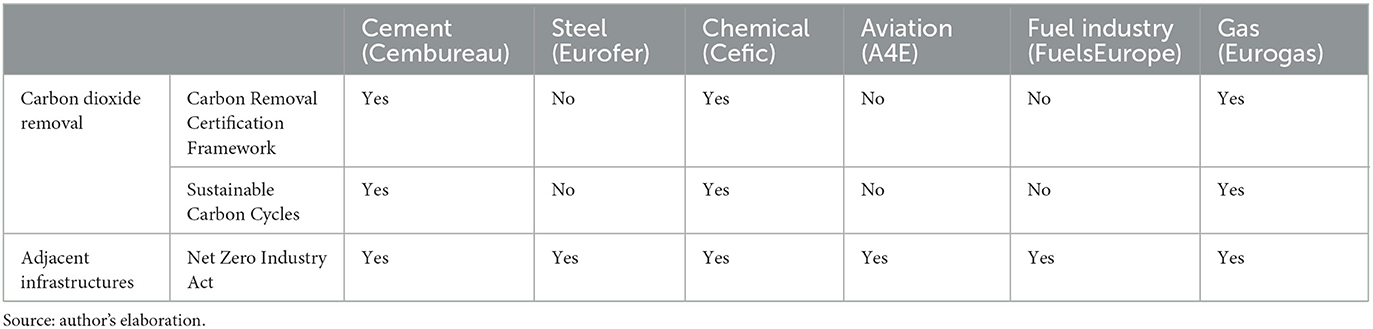

Our focus of analysis is on net-zero or decarbonization roadmaps of the selected associations to work out how the associations present their contribution to the EU's net-zero target.3 We specifically analyze the extent to which the associations claim residual emissions for their sector, and which approaches to emissions reduction and CDR are envisioned. To extend and refine this analysis, we use publicly available statements and position papers from the selected associations. Our investigation focused on two areas: First, position papers that directly relate to CDR, i.e., statements on the Commission's communication on Sustainable Carbon Cycles (which was published in December 2021) and the EU Carbon Removal Certification Framework (CRCF; which is currently under negotiations; see Section 4 for more details). Second, since not all associations positioned themselves on these policies (see Table 1), we expanded our focus and took into account the statements on the Net Zero Industry Act (NZIA), which was published in March 2023. Since the NZIA is particularly relevant for CCS and CCU applications, the statements by the trade associations provide insights on the positions toward important adjacent infrastructures for CDR (see Section 4 for more details). Besides statements on these three policy initiatives, we selectively considered further statements or position papers which allow us to analyze the trade associations' stance on CDR and adjacent infrastructures, as well as on EU climate policy initiatives more generally to contextualize our findings in the discussion.4 We analyze the positions of the oil and gas industry separately, even though oil and gas are often treated as one sector (cf. Green et al., 2022). The central reason for this is that there are two trade associations in the EU polity, FuelsEurope and Eurogas, which are composed of different constituencies, although there is a significant overlap (for more details on membership see Sections 5.5 and 5.6). What further motivates this analytical distinction is the fact that oil and gas occupy different roles in current politics of low-carbon transformation processes. Petrol has increasingly come under pressure as the central fuel for private transport due to the rise of e-mobility and policies to phase out internal combustion engines in the EU (Haas and Sander, 2020). At the same time, the gas sector successfully managed to promote gas as a low-carbon alternative to oil, particularly in domestic heating, and to portray its grid system as an essential component of the hydrogen transition (Ohlendorf et al., 2023).

Table 1. Positioning of key trade associations.

According to its self-image, the EU has established itself as a leader in global climate policy, aiming to become the world's first “climate-neutral” continent (Oberthür and Dupont, 2021; Tobin et al., 2023), and the “myth of a green Europe” (Lenschow and Sprungk, 2010) has been a long-standing driving force of the European integration process. The reality is much more ambivalent, however (Plehwe et al., forthcoming): Overall emissions declined by about 37.6% between 2005 and 2022 in the sectors currently covered by the so-called flagship of European climate policy, the European Union Emissions Trading Scheme (EU ETS) introduced in 2005 (Bayer and Aklin, 2020)—power and heat generation, civil aviation within the EU, as well as energy-intensive industry including oil refineries, steel, cement, lime, and chemicals (European Environment Agency, 2023). However, the emission trends across sectors are not uniform (e.g., emissions from aviation grew substantially between 2013 and 2019) and the price for CO2 emissions remained extremely low for more than a decade (Gerlagh et al., 2022)—below even highly conservative estimates of prices required for stringent mitigation (Pindyck, 2019). This was particularly due to numerous loopholes, an over-allocation of certificates and the free allocation of certificates that were created under pressure from industrial lobbies (Plehwe et al., forthcoming). It is only since 2019 that prices for emission certificates have reached a level from which positive mitigation incentives could emanate. The large energy companies were not only successful in lobbying for an EU ETS that largely corresponds to their interests but have also succeeded together with their political allies, such as conservative think tanks or parties, in slowing down the transition to renewable energies (Haas, 2019). In addition to a general narrowing of the sustainability discourse to the aspect of decarbonization (Morata and Solorio Sandoval, 2013; Eckert, 2023) and the decline of investment in renewables due to austerity policies in the aftermath in the Eurozone crisis, the abolition of feed-in tariff systems and the massive expansion of influence on green trade associations by large incumbent energy companies delayed the energy transition (Haas, 2019).

While these examples illustrate that already the decarbonization of the energy sector has been highly contested, EU climate policy has entered a new phase of development with the European Green Deal (EGD) and its goal to achieve climate neutrality by 2050 (European Commission, 2019). In this net-zero phase of EU climate policy the questions of how to mitigate hard to abate emissions, particularly those that cannot be abated through electrification and decarbonization of the energy system, and how to compensate for residual emission through CDR are increasingly entering the political arena and can be expected to be at least as contested as previous issues of EU climate policy. The EGDs climate neutrality goal is based on different scenarios toward climate neutrality developed in the Commission's Clean Planet for All communication (European Commission, 2018a). In addition to the climate neutrality goal, the EGD raised the emission reduction target for 2030 from 40% to a net emission reduction of 55% compared to 1990 [and more recently to 57% as part of the revision of the land use change and forestry (LULUCF) regulation]. Furthermore, emission trading underwent significant reform with maritime transport being included into EU ETS, the creation of a separate EU ETS for buildings, road transport and fuels and measures to reduce the number of allocations more quickly to raise carbon prices in the ETS (Oberthür and von Homeyer, 2023). Fundamentally, the EGD, advocated by the European Commission (2019, p. 2) as the EU's “new growth strategy,” relies on the EU's dominant climate policy paradigm that low-carbon technologies will foster emission reductions while at the same time stimulating green growth, based on the assumption that GDP growth can be progressively decoupled from GHG emissions and resource use (Brad and Schneider, 2023, p. 5).

The EGD's emission reduction targets and the extensive revisions of existing environmental and climate policy initiatives indicate EGD's level of ambition to achieve climate neutrality. However, a key question that has remained largely unanswered is how CDR will be integrated into EU climate policy and its three main pillars—the EU ETS, the LULUCF regulation and the Effort Sharing Regulation—in particular (Schenuit and Geden, 2022). The EU ETS has so far been kept separate from CDR,5 even though there are different proposals as well as initiatives to integrate CDR into emission trading (cf. Brad and Schneider, 2023), e.g., managed by a carbon central bank (Rickels et al., 2022). The second pillar, the LULUCF regulation, by contrast, already regulates removals in the land use and forestry sector, aiming to compensate accounted emissions from land use “by at least an equivalent amount of accounted removals” in the sector until 2025 (“no-debit rule”) and to reach a net removal of 310Mt CO2 by 2030 (European Commission, 2023a). CDR is also relevant for the third pillar, the Effort Sharing Regulation, which determines the distribution of emission reductions between Member States in sectors not covered by the ETS, in so far as removals from the LULUCF sector can balance emissions from ESR sectors up to 280Mt CO2eq (Savaresi et al., 2020). What has remained open so far, however, are crucial questions regarding the future role of CDR in EU climate policy: how many residual emissions will be emitted in 2050? Which economic sectors, industries and individual companies will emit how many (residual) emissions? How will the residual emissions be distributed among economic sectors and industries? Who is responsible for achieving the CDR targets? What incentive structures will be created for CDR? Which CDR technologies will be utilized? All these questions will shape future EU climate policy or are currently already—at least implicitly—under negotiation (Geden and Schenuit, 2020).

The most explicit initiatives to address the role of CDR in future EU climate policy are the communication on Sustainable Carbon Cycles (European Commission, 2021a) presented in December 2021 and the ongoing negotiations on a CRCF. The NZIA, which mainly focuses on the EU's competitiveness in “net zero” technologies is also relevant due to its specific emphasis on scaling-up CCS technologies and storage capacity in the EU as an adjacent infrastructure for BECCS and DACCS. The communication on Sustainable Carbon Cycles represents the first comprehensive effort by the Commission to initiate and shape the policy debate on the integration of CDR into EU climate policy, as it recognizes that “conventional” mitigation methods based on emission reductions are not sufficient to limit global warming to 1.5°C. Consequently, the communication sets specific targets, focussing not only on increasing the EU's land sink by 42 Mt of CO2 by 2030 through “carbon farming” activities (as part of 310Mt CO2 emission reduction goal under the LULUCF regulation), but also pursues the goal that another 5 Mt of CO2 “should be annually removed from the atmosphere and permanently stored” through CDR technologies such as BECCS and DACCS (European Commission, 2021a, p. 9, 17).

The CRCF, in turn, aims to provide a consistent and transparent approach to defining, quantifying, accounting, verifying and monitoring carbon removals to make sure that CDR providers actually extract and durably store CO2 and are held liable in the event of reversals (i.e., if CO2 is released from storage; McLaren, 2020; Dahm, 2022). A key challenge in this respect is the differentiation of CDR from various methods of CCU, particularly regarding the issue of permanency, as in most cases CCU merely represents a delay of emissions [as the CO2 stored in the product is usually (re-)emitted after the end of the utilization period] so that no (net-)negative emissions are achieved beyond temporary storage (Smith et al., 2022; Schenuit et al., 2023). The relevance of the NZIA for the politics of CDR and residual emissions predominantly lies in the fact that it establishes for the first time a specific CO2 injection capacity target of 50 Mt per year by 2030. While this storage capacity target is intended to facilitate the emergence of a CCS value chain in the EU, CCS related transport and storage infrastructure is also necessary for engineered CDR methods such as BECCS or DACCS which can be shared or clustered with CCS (cf. Maher, 2018). The NZIA also explicitly holds the oil and gas industry responsible for exploring and developing the required storage sites based on its “assets, skills and knowledge” (European Commission, 2023b, p. 21).

In the following, we zoom-in on the positions of cement, steel, aviation, and the chemical industry as well as the oil and gas industry. Based on the methodological considerations described in Section 3, we proceed as follows: First, we introduce the relevance of each sector in terms of its share of total GHG emissions in the EU (based on the annual EU greenhouse gas inventory6) and the specific challenges in decarbonizing these sectors as well as the main trade association of these sectors in the EU. We then turn to the analysis of their net zero or decarbonization roadmaps and related position papers regarding CDR and the NZIA and highlight their main policy demands. Table 2 provides an overview of the main features of key trade associations' net zero or decarbonization visions.

Table 2. Overview of key trade associations' net zero visions.

According to the annual EU greenhouse gas inventory (European Environment Agency, 2021), cement production accounted for 78 Mt CO2 emissions in 2019 or 1.9% of total EU GHG emissions (4,067 Mt CO2-eq), with Germany (17%), Spain (11.6%), and Italy (10.1%) being the member states with the highest emissions. Compared to 1990, CO2 emissions from cement production decreased by 24.1% in the EU. However, these numbers exclude energy related emissions. Therefore, verified emissions from cement production under the EU ETS, which also cover emissions from the combustion of fossil fuels in the sector (European Environment Agency, 2021, p. 36–37), are significantly higher, i.e., 113 Mt CO2 or 2.7% of total EU GHG emissions in 2019.7 Some of the emissions from the sector are inherent to the cement production process and therefore classified as “hard to abate” (Marmier, 2023). Particularly the heating of limestone to make clinker through a chemical reaction produces CO2 emissions which are impossible to abate through electrification and renewable energy sources (Fennell et al., 2022; Marmier, 2023, p. 5). This process referred to as calcination accounts for 60–65% of current cement manufacturing emissions according to Cembureau, the EU-level trade association of the cement industry (Cembureau, 2020, p. 15), with the remaining emissions resulting from the combustion of fossil fuels in the heating processes. Cembureau acts as the umbrella organization for currently 23 national cement industry associations in the EU and beyond (Norway, Switzerland and the United Kingdom). Cembureau is highly inclusive in its role as the main branch association: the EU's largest cement producers according to production capacity in the EU such as HeidelbergCement, Holcim, Buzzi Unicem and CRH are all members of Cembureau.

While Cembureau foresees only limited reduction potentials regarding these process-related emissions in the production of clinker (e.g., through thermal efficiency and use of alternative raw materials), the industry nonetheless aims to reach net zero emissions across the cement value chain by 2050. The main share of the emission reductions required for this is to be achieved through Carbon Capture Utilization and Storage (CCUS), which is supposed to decarbonize roughly 42% of CO2 emissions per ton cement vs. 1990 emission levels (Cembureau, 2020, 2022a). Further emission reductions are to be attained through the use of alternative and biomass fuels, thermal efficiency, the use of decarbonated raw materials and clinker substitution (as part of alternative cement chemistries) and carbon neutral transport.

While Cembureau does not explicitly claim residual emissions, they assume in their net zero roadmap calculations that process emissions will continue to be emitted beyond 2050. As a result, CDR forms an integral part of its net zero vision, namely two specific CDR techniques: First, implementing capture and storage of biogenic CO2 from sustainable sources (e.g., biomass waste) in cement plants in the process of combusting biomass-based fuels in the heating process, i.e., BECCS (Cembureau, 2023a). Secondly, by removing carbon through a process called carbonation, i.e., the absorption of CO2 in concrete and cement. This is a process that already occurs naturally but which Cembureau is seeking to improve in terms of absorption capacity and would like to have recognized as a carbon sink, also reflected in national emission inventories (Cembureau, 2021a, 2023a). Importantly, apart from a 2030 interim target, the roadmap does not contain any details regarding the timing of mitigation efforts as well as the level of emissions and removals in 2050, as the calculations only refer to the output per ton of cement, not to absolute production volumes.

From this, Cembureau derives specific political demands regarding various CDR-related policies. First, it advocates for the rapid roll-out of a pipeline infrastructure to facilitate the transport of CO2 to storage sites (in case of CCS) or downstream usage (in case of CCU), given that many cement production sites are not located within large industrial clusters (Cembureau, 2020, 2023b, p. 19; Schenuit et al., 2023, p. 3). It also welcomes EU 2030 target for CO2 injection capacity put forward in the NZIA (Cembureau, 2023b). In case that CO2 is captured and then transferred to a storage site or used in a product, the association urges the Commission to allow the capturing installation (i.e., the cement producer) “to deduct the CO2 from its emissions” (Cembureau, 2021a, p. 2). Second—and relatedly—as production sites are decentralized and many of them landlocked, i.e., remote from offshore CO2 storage sites, the trade association—similar to the chemical industry (see below)—heavily promotes CCU, particularly the production of synthetic fuels (Cembureau, 2022b, 2023b). It opposes a phase-out of industrial CO2 resulting from CCU as a feedstock for the production of synthetic fuels as stipulated by the Commission's Delegated Act on the greenhouse gas saving criteria for renewable liquid and gaseous fuels of non-biological origin (RFNBOs; European Commission, 2006). In this context, Cembureau also takes a critical stance toward DACCS as a forecasted alternative source of CO2 for RFNBOs replacing industrial CO2 from CCU, highlighting unknown deployment capacity beyond 2040, especially regarding the high quantities of zero carbon electricity required (Cembureau, 2022a). With regard to the CRCF, the association demands that concrete carbonation is considered as a form of CCU and thus as carbon removal (when it arises from carbon-neutral cement production) under the EU CRCF (Cembureau, 2023a).8 Cembureau also demands that carbon removal certificates under the CRCF should be tradeable and exchangeable in the context of the EU ETS (Cembureau, 2023a). This step would benefit the cement industry not only as a supplier of industrial CO2 for CCU, but also as operator with significant demand for emission allowances under the EU ETS whose gradual tightening would be alleviated regarding price developments if carbon removal certificates were eligible to enter the market. At the same time, implementing these two key demands put forward by Cembureau regarding the CRCF—considering carbon storage in long-lasting products as a removal and making removal credits tradable in the EU ETS—would arguably exacerbate the main concerns regarding the CRCF put forward by environmental NGOs such as Carbon Market Watch: the inclusion of non-permanent removals into the scheme and the use of removal certificates as well as the possibility to sell removal certificates to companies wishing to delay and offset their emission reductions (cf. Carbon Market Watch, 2022; Brad and Schneider, 2023).

CO2 emissions from the production of iron and steel amounted to 157 Mt in 2019 or 3.8% of total GHG emissions in the EU, with emissions down 44.4% compared to 1990 levels (European Environment Agency, 2021). Germany stands out as the EU's member state with the highest share of emissions from the sector (34.2%), followed at a great margin by France (10.6%) and Austria (7.7%; European Environment Agency, 2021). The main EU level trade association of steel industry, Eurofer, represents 14 national steel trade associations, including all main steel producing countries in the EU (Somers, 2022). The main steel producing companies in the EU, such as according to the Joint Research Center of the European Commission (Somers, 2022, p. 41), ArcelorMittal, Thyssenkrupp, Tata Steel, Voestalpine, SSAB and Salzgitter, are also direct members of Eurofer (Eurofer, 2023a).

The production of steel is not only highly energy-intensive, but also—and crucially—the two currently dominant steelmaking routes rely on fossil inputs (mainly coal-based coke and natural gas) for chemical reactions and heating to convert raw materials to iron and iron to steel, implying substantial process-related CO2 emissions (from the steel making process itself, but also in the process of heating coal to produce coke). In the first production route, the so-called blast furnace—basic oxygen furnace (BF-BOF) procedure (accounting for almost 60% of total steel production in the EU in 2020, cf. Somers, 2022, p. 11), coal and coke are used with a blast furnace to produce hot metal from iron ore. Additional emissions result from the combustion of fossil energy carriers to heat the blast furnace and the basic oxygen furnace as well as from reducing the carbon content of metal to generate steel in the basic oxygen furnace. In the second route, based on an electric arc furnace, steel is produced either from recycled steel scrap or in combination with a process called direct reduction, where natural gas or coal are used to generate reducing agents to produce sponge iron from iron ore (cf. Kim et al., 2022). The two main decarbonization options for the coal-based BF-BOF route are either the direct reduction of iron ore to iron using hydrogen as a reduction agent (depending on the availability of large amounts of 'green' or 'low carbon' hydrogen) or an electrolytical reduction process relying solely on electricity (but not expected to be deployable at scale before 2040; Somers, 2022, p. 22–32). In addition, CCS and CCU are also considered, mainly to retrofit the BF-BOF production process, but also for direct reduction production approach based on natural gas (Somers, 2022, p. 27–30). High capital costs and long investment cycles are considered a particular challenge in decarbonizing the steel industry (Kim et al., 2022).

In 2019 Eurofer presented its “low carbon roadmap” which contains emission reduction targets by 30% by 2030 and by 80–95% by 2050 compared to 1990 levels (Eurofer, 2019, p. 6). Actual emission reduction potentials within this range, the association argues, mainly depend on technology development (including CCS and CCU) and on whether sufficiently large quantities of entirely CO2 free energy in the form of electricity and hydrogen will be available in 2050. The latter factor, Eurofer asserts, largely lies outside of the control of the sector (Eurofer, 2019, p. 5, 9). Correspondingly, the association outlines not only one decarbonization pathway but six different scenarios, ranging from “business as usual,” “ongoing retrofit,” and “current projects with low CO2-energy” to more ambitious scenarios, i.e., full deployment of low-emission technologies with low CO2-energy (80% emission reduction by 2050 compared to 1990), “current projects with CO2-free energy” (85% reduction) and full deployment of low-emission technologies with CO2-free energy (95% reduction). Notably, Eurofer does not assert to reach net zero by 2050 and does not refer to any form of CDR in its decarbonization strategy, thereby implicitly claiming residual emissions in 2050 and beyond which will need to be compensated by deployment outside of the sector. In addition, while the most ambitious decarbonization scenario aims to get at least close to net zero with a 95% emission reduction compared to 1990, the other scenarios would imply substantial amounts of residual emissions. In the “ongoing retrofit” scenario, which merely projects a 15% emissions reduction compared to 1990 levels, residual emissions would amount even up to 255 Mt CO2 emissions in 2050 (Eurofer, 2019, p. 5). This would equal 42.4% of total economy wide residual emissions anticipated in the European Commission's indicative 1.5TECH scenario to reach net zero by 2050, and more than twice as many emissions as envisaged for the entire industrial sector in this scenario (European Commission, 2018b, Annex 7.7.). Against this background, Eurofer specifically justifies and highlights its sector's role for decarbonization, arguing that the “foundations of the Net zero Age are made of steel, from wind turbines to electric vehicles” which it does not see adequately reflected in the NZIA (Eurofer, 2023b).

Corresponding to the fact that CDR is entirely missing from the European steel industry's decarbonization perspectives, Eurofer has not yet engaged (at least publicly) with the integration of CDR into EU climate policy. The trade association neither commented on to the Sustainable Carbon Cycles communication nor to the CRCF (see Table 1), focusing instead mainly on the EU's proposals for a Carbon Border Adjustment Mechanism (CBAM; European Commission, 2021b) given the particular importance of this policy for the sector. Moreover, and in line with the main pillars of its decarbonization scenarios, the association advocates for the expansion of renewable energy and hydrogen production—partly also with support from green trade associations (cf. Eurofer, 2022)—as well as for improving access, deployment and infrastructure development for CCUS (Eurofer, 2023b). Eurofer's strong emphasis on the issue of the availability of renewable energy and “green” “CO2-free” hydrogen arguably also foreshadows future conflicts over the prioritization of these renewable energy inputs, given that there will be huge demand from the steel industry against limited supply.

The chemical industry emitted 133 Mt CO2-eq or 3.3% of total EU GHG emissions, down 59% compared to 1990 levels (European Environment Agency, 2021). However, these numbers underestimate actual emissions from the sector, as Germany reports its emissions from the chemical industry under a different category (other manufacturing and construction activities, cf. European Environment Agency, 2021, p. 161). As a feedstock industry, chemicals play a significant role in overall economic development. Cefic is the umbrella organization of the European chemical industry. Members include all major European chemical companies such as BASF or Bayer, but also bp, ExxonMobil Chemical Europe, Shell Chemicals and the fertilizer producer Yara. In addition to very large and medium-sized corporations, all major national umbrella organizations of the chemical industry are also members of Cefic. As the chemical industry encompasses many different production processes, there are many overlaps with other associations, but Cefic is the central interest group for the chemical industry in the EU. While it is supportive of the EU's net zero target by 2050, the chemical industry has a special role in that it will continue to rely on carbon as a feedstock beyond 2050. Against this background, Cefic argues that the political debate should be less about decarbonization and more about a carbon cycle economy: “Establishing sustainable and climate-resilient carbon cycles is, in our view, a more efficient approach to climate mitigation than an approach that is essentially geared toward ‘decarbonization,' which may result in the wrong diagnosis and thus will lead to suboptimal solutions. In fact, carbon is an essential element in organic compounds: it is not possible to reduce the carbon density of our products and we will remain strongly reliant on carbon as a source of feedstock” (Cefic, 2023a, p. 1).

Accordingly, Cefic emphasizes that it will be extremely costly and nearly impossible to reduce the sector's emissions to zero by 2050: “Certain sources of GHG emissions emitted by our plants will remain extremely costly or even impossible to abate—at least by 2050, and therefore need to be removed/compensated elsewhere in the chemical industry or the economy, necessitating exploiting cross-sectoral synergies, industrial symbiosis and long-term carbon storage solutions” (Cefic, 2023a, p. 2). Unlike most other associations, Cefic has not published a decarbonization roadmap. However, with the help of the business consultancy and accounting firm Deloitte, it developed four scenarios toward climate neutrality: “high electrification,” “fostering circularity,” “sustainable biomass,” and “CO2 capture” (Cefic, 2021, p. 6). The scenario analyses show that there are many different production processes in the chemical industry for which several different approaches to reducing emissions are conceivable. The umbrella organization acknowledges that there will be some need for CDR. Depending on the scenario the remaining emissions within the sector are between 68 and 111 Mt CO2 by 2050 (Cefic, 2021, p. 107), which would amount to 11.3–18.4% of total residual emissions anticipated in the European Commission's indicative 1.5TECH scenario and 61.9–101% of residual emissions projected for the entire industrial sector under this secnario (European Commission, 2018b, Annex 7.7). It remains unclear whether the necessary negative emissions are to be realized entirely within the chemical industry. In its Fact Sheet on restoring sustainable carbon cycles, Cefic claims that the chemical industry can contribute to CDR by storing biogenic or air-extracted CO2 (DAC) either in products (CCU) or underground (DACCS/BECCS; Cefic, 2023a, p. 4). In the case of CCU, however, it is very controversial whether and to what extent this can be evaluated as a removal, because in most cases the carbon bound in products is released after a certain time. Against this background, it appears that the chemical industry has an interest in CCU being classified as a removal. This is also reflected in its statement on the CRCF. The association argues that the term “carbon storage in products” is not appropriate, but pleads for the term “carbon removal products” (Cefic, 2023a, p. 14)—a notion that presumably shall open marketing opportunities for several products.

Cefic has formulated a strong critique of the NZIA, pointing to tensions between different industries in the process of reaching the net zero goal. The umbrella organization argues that the NZIA is actually a Net Zero Technology Act that bypasses the feedstock industries, to some extent similar to the criticism of the NZIA put forward by Eurofer. Cefic specifically criticizes that many components of technologies defined as priorities are based on chemicals and materials produced by the chemical industry. In this respect, unlike other trade associations, Cefic refers to the NZIA's goal to enhance the EU's strategic autonomy to argue that this goal would be undermined if it doesn't cover the full industrial value chain of strategic net zero technologies.9 Against this background, CEFIC demands that the chemical industry should also receive the benefits (subsidies, accelerated planning) that the NZIA only envisions to provide for a few downstream industries (Cefic, 2023b).

CO2 emissions from the aviation sector in the EU amount to 187.76 Mt or 4.6% of total EU GHG emissions if data on domestic aviation (i.e., within member states) and on international aviation is summed up (European Environment Agency, 2021). The central lobbying association of the aviation industry in the EU is Airlines for Europe (A4E), in which 16 airlines (including all major European airlines such as AirFrance, KLM, easyjet, Lufthansa, and Ryanair) as well as the major manufacturers Airbus and Boeing are represented. Despite enormous progress in efficiency, greenhouse gas emissions have increased significantly since 1990 because of rapid growth in air traffic. While other areas of the mobility sector can be electrified relatively well, A4E emphasizes that this is not or only possible to a limited extent in air transport due to battery weights (A4E, 2021, p. 32). In this respect, the key challenge for the aviation sector is to find other decarbonization options.

In 2021, A4E, together with the associations CANSO (Civil Air Navigation Services Organization), ERA (European Regions Airline Association), Airports Council International-EUROPE (ACI), and Aerospace and Defense Industries Association of Europe (ASD) presented a net zero scenario until 2050 in line with the EU's goal of net zero CO2 emissions by 2050. The Netherlands Aerospace Center (NLR) and SEO Amsterdam Economics supported the trade associations in the development of the scenario study. The scenario includes air traffic within the EU and outgoing flights [specifically: the EU, the UK, and the European Free Trade Association (EFTA)]. To reach the net zero target in air traffic by the year 2050 is essentially based on four building blocks: “1. Aircraft and engine technology,” “2. Air traffic management and aircraft operations,” “3. Sustainable Aviation Fuels,” and “4. Smart economic measures” (A4E, 2021, p. i). About 92% of the greenhouse gas emission reductions refer to the first three pillars. In addition to efficiency improvements, the use of hydrogen, the introduction of (hybrid-)electric aircraft, synthetic fuels and agrofuels are supposed to play a key role in decarbonising aviation. Nevertheless, the aviation industry assumes that it will still be using fuels from fossil sources in 2050, about 17% of the total amount of kerosene used by 2050 (A4E, 2021, p. v). Therefore, the decarbonization scenario assumes residual emissions of 22 MtCO2, i.e., 3.7% of total residual emissions anticipated in the European Commission's 1.5TECH scenario and 25.7% of residual emissions earmarked for the transport sector in this scenario. These residual emissions shall be compensated by means of “smart economic measures,” i.e., CDR. The sector only reaches net zero by “realizing out-of-sector carbon removals” (A4E, 2021, p. 150). However, the scenario analysis is based on rather optimistic assessments regarding technological innovation and progress, specifically with respect to “breakthrough” or “disruptive technologies” to net zero. Most importantly, the scenario assumes that between 2030 and 2050, the use of sustainable aviation fuels (SAF) will increase from 3 to 32 Mt. In this respect, it is uncertain whether climate-neutral air traffic in 2050 will actually be possible with CDR on the scale of 22 Mt per year.

Regarding CDR deployment options, the net zero study refers to DACCS, but remains rather general on how to scale up DACCS (or other CDR options) to the required deployment levels. This contrasts with A4E's recognition that the short-term possibilities to mitigate aviation emissions are limited as “the lion's share of emissions can only be abated from the mid-2030's onwards” (A4E, 2022, p. 2). At the global level, and in cooperation with CORSIA (Carbon Offsetting and Reduction Scheme for International Aviation), the growth in aviation emissions shall be neutralized through certificate trading. Regarding the Fit for 55 Package, A4E has clearly positioned itself against, for example, abolishing the kerosene tax exemption or restricting the free allocation of emission certificates. In this respect, A4E defends the existing regulatory framework and calls for both research funding and subsidies for the market ramp-up of new technologies. It is noteworthy that A4E contradicts the European Commission regarding the cost development of SAFs and accordingly calls for subsidies to compensate for high SAF costs: “A4E does not share the optimistic price projections of the European Commission's Impact Assessment. The cost to produce SAFs will remain multiple times the price of conventional jet fuel until 2030 and will remain higher than that of alternative fuels used in other transport modes. In absence of an orchestrated support strategy, the increased cost of SAFs will lead to the closure of routes and may put individual airlines in financial difficulty” (A4E, 2022, p. 4). This indicates that the decarbonization pathway is full of uncertainties. The simplest way to avoid emissions, reducing air traffic, is strongly opposed by A4E, as the association argues that offsetting “is the sole way to tackle global CO2 emissions from aviation today” (A4E, 2022, p. 6).

Also core EU trade associations of “fossil capital” have embraced net zero emission targets. FuelsEurope, a division of the European Petroleum Refiners Association whose membership encompasses all 40 companies which operate petroleum refineries in the European Economic Area in 2019 (European Environment Agency, 2023), including the major European (and other multi-national) oil and gas companies such as BP, Eni, Equinor, OMV, Shell, TotalEnergies, or ExxonMobil, published a proposal for a “Potential Pathway to Climate Neutrality by 2050” in 2020 (FuelsEurope, 2020a). The pathway is based on so called “clean fuels” or “low-carbon liquid fuels” for road, maritime and air transport. It assumes an increased uptake of hydrotreated vegetable oils and of lignocellulosic residues and waste as feedstock as well as a massive increase in the use of e-fuels, i.e., synthetic fuels based on carbon dioxide or carbon monoxide combined with “clean” hydrogen to achieve net zero in road transport (as well as a 50% CO2 emission reduction in the aviation and maritime sector). Together, the production of these fuels, denoted by the trade association as low-carbon liquid fuels, could reach up to 150 Mt by 2050, with the lion share coming from lignocellulosic residues and waste as well as e-fuels (in roughly equal proportions).

However, as the projected uptake of low-carbon liquid fuels use still relies on blending these fuels with conventional fossil fuels (FuelsEurope, 2020b, p. 19), the pathway to net zero in road transport ultimately relies on CDR technologies, namely BECCS, to achieve net zero emissions in 2050. This is mentioned in an asterisk to the claim of reducing CO2 emissions in road transport by 100% by 2050, but not further specified in any way. On the contrary, in an FAQ document accompanying the road map, FuelsEurope argues that it is impossible to specify the amount of low-carbon liquid fuels in relation to conventional fossil fuels used in 2050, which indicates a high level of uncertainty regarding the trade association's claim to reach net zero by 2050 by way of compensating (an unspecified amount of) residual emissions through BECCS.

While we did not find any statements of FuelsEurope on the Sustainably Carbon Cycle communication and on the CRCF, the trade association's position toward NZIA reveals its emerging approach to CDR (FuelsEurope, 2023). Here FuelsEurope pursued the goal to broaden the definition of sustainable alternative fuels to include not only SAFs and bunker fuels (for shipping) but also “low-carbon fuels for road transport and chemical products” (FuelsEurope, 2023). It also welcomed the NZIA's strong emphasis on CCS, highlighting the “carbon abatement potential [of] combining CCS solutions with biomass feedstocks in bioenergy (BECCS)” (FuelsEurope, 2023, p. 2). However, FuelsEurope urged to include in the NZIA's focus on CCS as a strategic net zero technology the relevant transport and storage infrastructures (which are largely operated by the oil and gas industry), not least as a way of “reducing stranded asset risk” (FuelsEurope, 2023, p. 3).

Like FuelsEurope, Eurogas, the main trade association of the European gas industry, has put forward a pathway to carbon neutrality in 2050, based on a study conducted by Norwegian registrar and consultancy DNV GL (2020). Eurogas represents different national associations of the gas industry (including the German gas and hydrogen industry association Zukunft Gas, Francegaz, and Italgas) as well as more than 70 companies. Among them are major oil and gas companies which are also members of FuelsEurope (Eni, Equinor, Shell, and TotalEnergies), but also energy suppliers (such as the Italian A2A, the German RWE, or the French Engie) and distribution network operators (such as the Austrian Wiener Netze or the French GRDF). The membership structure is both heterogenous (in that it covers companies with significantly different bases of accumulation, i.e., production of natural gas but also energy and heating provision more generally) and—compared to the other trade associations investigated here—less encompassing. Besides Eurogas, there are two further trade associations articulating positions of the European gas industry: Gas Infrastructure Europe (GIE), which represents the European gas transmission system operators, the LNG terminal operators and the gas storage system operators, as well as Gas for Climate. While there is some overlapping membership between Eurogas and GIE (for instance RWE and Uniper), the main functional difference between the two associations is that Eurogas represents companies producing and/or supplying natural gas to end users, while members of GIE are responsible for supra-regional transmission systems, storage, and LNG terminals. Gas for Climate is an association representing 11 gas infrastructure and transport companies (10 of which are also members of GIE) as well as three biogas trade associations (among them the European Biogas Association which, in turn, also counts oil and gas companies such as Eni, Shell or TotalEnergies among its members, i.e., companies which also hold membership with Eurogas). While GIE has neither come forward with a decarbonization or net roadmap nor positioned itself independently to the CRCF, the SCC communication or the NZIA,10 Gas for Climate developed a decarbonization roadmap which fundamentally differs from the one put forward by Eurogas (Gas for Climate, 2020). Even though Gas for Climate did not position itself to the CDR-related EU policies investigated here, its alternative roadmap arguably weakens the claim of Eurogas to speak for the entire industry.

The decarbonization scenario promoted by Eurogas (DNV-G, 2020) is set up in juxtaposition to the European Commission's 1.5. TECH scenario to reach net zero by 2050—notably the Commission's scenario which is already significantly dependent on BECCS and DACCS as compared to the alternative 1.5 LIFE scenario with a stronger emphasis on lifestyle-based mitigation options (as well as ecosystem-based sinks; European Commission, 2018b). The Commission's 1.5 TECH scenario projects a considerable absolute decline in gaseous energy supply by 2050 (by more than 20% compared to 2015 levels) and a substitution of natural gas with so called carbon free gases (e-gas, biogas, and waste gas) and hydrogen by over 50% (European Commission, 2018b, p. 85). The decarbonization scenario put forward by Eurogas, by contrast, foresees an absolute increase of gaseous energy supply in 2050 by 18%, with the majority (55%) still based on natural gas (Eurogas, 2020, p. 6). Eurogas asserts that this scenario is consistent with an 89% emission reduction in the gaseous energy supply chain (heavily reliant on CCS) and can even be considered net zero (“fully decarbonized”) if negative emissions from biomethane in power generation (i.e., BECCS) are accounted for (DNV-G, 2020, p. 21, 33). By contrast, while the alternative net zero pathway advocated by Gas for Climate similarly emphasizes the important role of gas (and hydrogen) transport infrastructure, the key difference to the Eurogas scenario is that it envisions an absolute phase out of natural gas by 2050,11 its substitution with biomethane and hydrogen, and an absolute decline in gaseous energy supply (by 37.1%; Gas for Climate, 2020, p. 3–9).

The main argument put forward by Eurogas in favor of its decarbonization pathway (as opposed to the Commission's 1.5 TECH scenario) is cost-efficiency. Eurogas claims that its scenario would allow the EU to reach net zero using to a large extent existing infrastructure. The EU could thus save €4,1 trillion until 2050 for infrastructure investment, particularly in highly intricate areas such as the electrification of heating, where Eurogas considers the continued use of gaseous energy a cost-efficient decarbonization option for the building sector. Along these lines, Eurogas maintains that “[e]lectrification makes sense, but only up to a point” (Eurogas, 2020, p. 3). The main infrastructure investment needs in the Eurogas scenario therefore do not stem from the transition to renewable energy as well as related grid systems and electrification processes, but from retrofitting existing and building new transport networks for hydrogen12 (DNV-G, 2020, p. 2).

Due to the all-encompassing role of CCS in its decarbonization scenario, Eurogas is highly supportive of the NZIA's strong focus on CCS (Eurogas, 2023a, p. 1). It sees the CO2 injection capacity targets formulated in the NZIA (50 Mt per year by 2030) broadly in line with its own study estimates (54 Mt by 2030) but urges to fully consider not only CO2 storage capacity in the EU but also on the territory of the European Economic Area (i.e., Norway; Eurogas, 2023b, p. 2). In a similar vein, Eurogas uses the debate about carbon removal triggered by the CRCF to further promote transport and storage infrastructure as well as capture technology for CCUS which, as Eurogas asserts, “would enable and enhance the deployment of certain technology-based carbon removal solutions (e.g., BECCS, DACCS)” in the future (Eurogas, 2023b, p. 1). At the same time, Eurogas also advocates to increase the tradability of CDR certificates, particularly through their integration into the EU ETS. While Eurogas justifies this position by stressing that it would “enhance the business case” for CDR (Eurogas, 2023b, p. 2), such a step of establishing “some level of equivalence between ETS CO2 equivalent quotas and carbon removal certificates” (Eurogas, 2023b, p. 3) would arguably be highly prone to mitigation deterrence as it would create strong incentives to substitute emission reductions in the gas industry by purchasing removal credits if carbon removal certificates are cheaper than emission allowances.

Based on the analysis and comparison of the roadmaps and policy papers of EU level trade associations representing sectors considered to account for a large share of residual emissions as well as associations representing the incumbent fuel industry, we can draw five findings. First, all capital fractions project largely “conservative” accumulation strategies into the future, insofar as changes merely relate to technological innovations, whereas absolute reduction of production quantities as a crucial mitigation option is absent from the low carbon or net zero roadmaps (except for the Gas for Climate scenario). For instance, Eurofer, projects an increase in crude steel production from 166 Mt (in 2015) to 200 Mt in 2050, Airlines for Europe (A4E) assumes an annual passenger growth rate of 1.4% until 2050, and Eurogas estimates an increase of gaseous energy supply (including hydrogen and biomethane, but mostly natural gas) by 18% compared to 2017 levels. This is in line with the EU's dominant climate policy paradigm based on the notion that decarbonization and GDP growth can be reconciled through decoupling, but at odds with recent debates which stress the importance of absolute reductions in production and consumption for effective mitigation (e.g., within consumption and production corridors or by focusing on demand-side measures; c.f. Creutzig et al., 2018; Fuchs, 2021; Bärnthaler and Gough, 2023). We can therefore observe a parallel between climate mitigation scenarios which treat GDP growth as “an unquestioned norm” (Hickel et al., 2021, p. 766) and the fact that all low carbon or net zero roadmaps put forward by the investigated trade associations project sector-specific growth trajectories (regardless of their respective role in low-carbon transitions). At the same time, growth in some sectors may be more reconcilable with (and indeed required for) stringent mitigation efforts than in others: While some proportion of the production of steel and cement is critical for the infrastructures anticipated to underpin net zero (even if this may not necessarily require overall growth in these sectors; Wang et al., 2023), others—especially aviation—may need to substantially contract, particularly given the technological obstacles to the decarbonization of the sector as highlighted by A4E (see Section 5.4).

Second, however, none of the trade associations explicitly opposes the EU's net zero target. All associations have developed decarbonization or net zero roadmaps, and five out of six have committed to net zero (carbon neutrality) targets, the achievement of which depends on CDR technologies (see Table 2). At the same time, on a more general level, a cursory look at positions adopted by these associations toward other EU climate legislations reveals opposition against individual policies that aim to reach climate neutrality in the EU. One example is the opposition of A4E against ending the kerosene tax exemption (A4E, 2022, p. 7). FuelsEurope's attempts to undermine the planned phase out of internal combustion engines in new cars after 2035 (FuelsEurope, 2022). Also, all of the associations analyzed, except Eurogas, spoke out against the expiry of free allowances as part of the recent EU ETS reform (A4E, 2021; Cembureau, 2021b; Eurofer, 2021; FuelsEurope, n.d.), even though these are hardly justifiable as a safeguard against carbon leakage protection with the CBAM entering into force. There is a tension between the sectors' commitment to the long-term net zero target and the opposition on behalf of individual sectors to take decisive steps toward this target in the short- and medium-term. This indicates that despite rhetorical commitment to decarbonization or net zero targets, there are strong continuities regarding climate policy opposition by emission intensive sectors in the EU (Plehwe et al., forthcoming).

Third, and relatedly, our findings support research highlighting the problematic ambiguities of net zero targets (McLaren and Markusson, 2020; Armstrong and McLaren, 2022). The ambiguities of net zero target framings enable emission intensive sectors to resolve the tension between long-term ambition and short-term opposition in climate policy, as many of the net zero roadmaps investigated fail to define a clear timing of mitigation efforts as well as the relation of emissions and removals over time and levels of residual emissions when net zero is achieved. As shown in Table 2, most trade associations do not make any efforts to explicitly estimate the level of residual emissions or provide only very large ranges for future residual emissions which will need to be compensated by negative emissions, let alone the timing for scaling negative emissions before the net zero year (and corresponding timing for emission reductions). While CCUS is constructed as the key technology that allows the trade associations under investigation (except for aviation, which has no prospect for using CCS) to assert that deep emission reductions in their sectors can be achieved, it is ultimately CDR technologies which bring the pathways of Cembureau, Cefic, A4E, FuelsEurope, and Eurogas on a net zero trajectory by filling the remaining, largely unspecified emission reduction gaps. Resolving the tension between long-term ambition and short-term opposition therefore (over)relies on promises of technological innovation, even though it is highly uncertain whether the CDR technologies mentioned in the roadmaps (mainly BECCS and DACCS) can be scaled up in a sustainable and socially just manner (Dooley and Kartha, 2018; Larkin et al., 2018; Creutzig et al., 2021). Thus, even though the sociotechnical imaginaries produced by these roadmaps mostly revolve around CCUS and other sector-specific technological promises (e.g., SAFs or green hydrogen in the case of steel), the roadmaps' consistency with net zero targets is heavily reliant on optimistic technological expectations—if not myths (Peeters et al., 2016)—regarding future CDR technology viability and deployment. CDR technologies can therefore be considered to act as techno-fixes in that they resolve the contradiction between maintaining (parts of) emission-intensive accumulation strategies and climate change mitigation (even though they do not—at least not yet—facilitate the fixing of major capital investment in new infrastructure, machinery and built environment). Up to this point, our findings confirm other studies (McLaren and Markusson, 2020) that net zero framings enable—and are enabled by—techno-fix thinking regarding CDR technologies.

Fourthly, however, the roadmaps and policy papers investigated do not simply reflect a uniform techno-fix thinking based on highly optimistic expectations regarding future technology breakthroughs.13 We also found pessimistic views regarding specific technological pathways, suggesting that techno-optimism and -pessimism depend on respective economic interests and accumulation strategies For instance, A4E questions the optimistic projections regarding the price development of SAFs of the European Commission—even though SAFs are at the heart of its decarbonization pathway—in order to underline the need for subsidies for the sector (Section 5.4). While A4E is optimistic about the future viability of large-scale deployment of DACCS, Cembureau takes a critical perspective on future potentials of DACCS (particularly in terms of energy requirements) in order to assert that industrial CO2 from CCU (e.g., derived from cement production) should continue to be allowed as a feedstock for renewable liquid and gaseous fuels of non-biological origin (RFNBOs) beyond 2040 (Section 5.1). Eurogas, in turn, is pessimistic regarding the economic viability of end-use electrification, particularly in the area of heating—a stance adopted to promote natural gas combined with CCS as the allegedly cost-efficient alternative for decarbonizing the building sector (Section 5.6). By contrast, the alternative decarbonization pathways articulated by Gas for Climate eliminates natural gas from EU energy supply. This supports our theoretical assumption that different capital fractions (or coalitions of them) promote different transition and decarbonization pathways, relying on different sets of technologies and sociotechnical imaginaries. While fossil capital foresees only a limited role of electrification and renewable energy sources in housing and transport and advocates for a continued role for fossil infrastructures and—in part—also fossil fuel extraction and production in the transition to net zero, the steel industry (and to some extent also the chemical industry) emphasize the importance of electrification and the rapid expansion of renewable energies. The key role of hydrogen both in the decarbonization scenario of Eurofer and A4E as well as in the net zero roadmaps of FuelsEurope (as a feedstock for e-fuels) and of Eurogas also foreshadows future conflicts of prioritized use which already pervade current hydrogen politics (Ohlendorf et al., 2023). Moreover, the participation of some major gas infrastructure providers in Gas for Climate indicates emerging splits within fossil capital particularly regarding the questions to what extent and which elements of carbon lock-in should be discontinued (e.g., natural gas production) to preserve others (e.g., pipelines for biogas and green hydrogen transport) in face of mounting political pressure. What all associations except A4E converge on, however, is a strong focus on CCUS and strong confidence in building a massive CCUS infrastructure—as a way to deal with process-related emissions (Cembureau, Eurofer), as a way to promote its products as a form of carbon storage or removal (Cefic) and as a way to abate emissions from the combustion of fossil fuels (Eurogas, FuelsEurope). This convergence is also evident from the fact that these associations signed a joint letter demanding that, besides CCS, CCU should also be recognized as a “strategic net-zero technology” under the NZIA (Cefic, 2023).

Fifth and finally, we find diverging approaches among the sectors regarding residual emissions, even as the extent of residual emissions and how to address them generally remains imprecise in the roadmaps. Steel is arguably unique in that Eurofer has not committed itself to a net zero target, thus acknowledging their inability to become fully decarbonized by 2050 and explicitly claiming residual emissions which need to be compensated outside the sector. This is coupled with an attempt to generate legitimacy for continued emissions, e.g., when Eurofer emphasizes the particular importance of steel for the transition toward a decarbonized economy (Section 5.2). A4E also admits that reaching net zero hinges on CDR to be realized outside of the aviation sector (Section 5.4). By contrast, the cement industry as well as the oil and gas industry do not claim any residual emissions which need to be compensated outside of the sector, arguing that they can achieve net zero based on CDR occurring within the sectors' value chains. We understand this position of the oil and gas industry as indicative that fossil capital is in a much weaker position than sectors required for the energy transition (e.g., steel) to legitimately demand residual emission to be compensated outside the sector, given growing political pressure to decarbonize or phase out fossil fuels entirely (Kenner and Heede, 2021; Green et al., 2022). The chemical industry is a special case in this regard as it does not specify whether compensation for its residual emissions via CDR will take place entirely within the sector.