94% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Clim., 31 August 2023

Sec. Carbon Dioxide Removal

Volume 5 - 2023 | https://doi.org/10.3389/fclim.2023.1192706

This article is part of the Research TopicNature-Based Solutions, Climate Mitigation, Biodiversity ConservationView all 5 articles

João Paulo Braga1,2

João Paulo Braga1,2 Ekkehard Ernst3*

Ekkehard Ernst3*The transition to a green economy requires significant resources, both from private investors and public policy makers with important implications for employment and living standards. This paper argues that green macro-economic policies are essential in accelerating the transition through three channels: they can strengthen the price signals from externality pricing; they can mobilize additional public and hybrid funding for green transition projects; and they can soften the social and labor market impact of the transition for those workers currently still employed in polluting industries. The paper provides an overview of the main fiscal, monetary and financial market policies that can help provide the necessary fund for a successful transition. It highlights different trade-offs regarding instrument choice and policy outcomes, notably regarding the need to achieve a transition that is both ecological and socially sustainable. We provide an overview of current policy choices and document their economic, social and ecological outcomes. In particular, we demonstrate that the proper use of price regulation and financial instruments—carbon taxes, cap-and-trade schemes, green bonds, nature-based capital—can mobilize additional resources that can be usefully invested to ensure a socially just transition.

Rising awareness of the climate emergency has led to focus on how to finance the green transition without adversely impacting economic development and job growth. Phasing out of fossil fuels and other sources of carbon emissions requires significant technological adjustments in infrastructure, energy and agricultural production at a time where development gaps continue to loom large in many parts of the world. Reallocating funds across sectors, occupations and locations means workers will need to change jobs, often involving significant costs in changing skills and locations. Existing funds are not sufficient, however, to accelerate efforts for carbon removal whether through nature-based solutions or clean-tech approaches to extract carbon from the atmosphere (ILO, 2022). Indeed, current estimates suggest that significant funds of the order of 10 basis points of global GDP growth need to be mobilized for at least the next decade under the most optimistic scenarios, the equivalent of 1 trillion USD or roughly 5 per cent of US GDP (Carton and Natal, 2022). Moreover, funds will need to be reallocated both across different sectors and constituents to ensure their most efficient use in the transition.1 Taken together the adjustment required for the green transition will entail significant cost burden for existing carbon-intensive producers and consumers, affecting both living standards and job growth.

Further delaying the process, however, would be even more costly, easily destroying global incomes five times larger than swift action. In this respect, the Conference of Parties to the United Nations Framework Convention on Climate Change (COP27) that took place in November 2022 emphasized the need to focus on the need to provide a conducive financial environment to effectively address global warming. The Sixth Intergovernmental Panel on Climate Change Assessment Report warns that the recent changes in the climate system are “unprecedented” and are irreversible for centuries (IPCC, 2021).2 In 2019, the CO2 concentration in the atmosphere reached its highest level while temperatures continued to rise, increasing the likelihood of climate disasters and permanent negative shocks and forcing policymakers to simultaneously pursue climate mitigation and adaptation goals. Macroeconomic and growth policy should smooth the impact of these shocks on the economy, but also ensure a just transition in labor markets. Importantly, a just transition requires consultation with social partners to create decent work while supporting workers and enterprises in adaptation (ILO, 2015).

To achieve a green transition without eroding living standards and destroying jobs, a large portfolio of green instruments needs to be part of the policy toolbox to address the various trade-offs involved. One set of instruments needs to support carbon emission reduction goals by inducing the investment in green energy, clean transport, and cleaner production practices. Another set will need to focus on climate adaptation to help protect economies from climate shocks. Climate disasters and transition risks are likely to reduce growth, create poverty traps, inflation, limit fiscal space and worsen labor markets (Carney, 2018; Coeuré, 2018; Kjellstrom et al., 2019; Semmler et al., 2021). Financial market losses and instability, due to fossil fuel-stranded assets, can also constrain credit flows and reinforce a downward cycle (Carney, 2018; Bolton et al., 2020). Recently, climate stress tests undertaken by the European Central Bank (ECB) found that climate-related portfolios are 30 per cent more likely to default and that climate risks can generate 12 per cent of losses to European GDP (Alogoskoufis et al., 2021). The use of green fiscal, financial and monetary policy as well as foreign and commercial policy plays a key role in addressing these risks. Finally, climate policies will also affect various economic actors differently, requiring policy makers to put in place support for those most affected to help them to successfully transit to new economic and job opportunities (Just Transition).

Yet, climate change mitigation is not only about funding but also about coordination, both across jurisdictions and within countries. Multiple actors need to be aligned in order to ensure swift reduction in carbon emissions. Public initiatives become particularly important in this respect, both through coordination of different domestic actors and by negotiating and enforcing international agreements. Three main categories of policy instruments are relevant in this respect: regulation and taxation, public investment and procurement, and provisioning and issuing of financial instruments targeting decarbonisation efforts (“green bonds”). Given the unabated long-term rise in global temperature, putting in place these instruments quickly and simultaneously is becoming urgent. In this respect, macro-economic policy makers—fiscal authorities, central banks, market regulators as well as sovereign debt issuers and underwriters—can play a significant role in accelerating the transition.

Public spending or procurement policies, for instance, can be directed toward green investment—preferably with a large employment content to encourage a Just Transition—to decarbonise electricity production and transportation. Central banks through their large open market policies can prioritize bonds issued by market participants that respect certain sustainability criteria, thereby paving the way for a more liquid market for sustainable securities. Finally, market regulators and underwriters can put a premium on assets that fail to respect certain sustainability targets, thereby accelerating the depreciation of the underlying asset. So far, however, few policy actors are ready to engage in accelerating the transition to a decarbonised economy. At the fore are fiscal authorities in advanced economies that support green investment both by public and private investors. Central banks, on the other hand, are more reluctant even though recent advancements have been observed, notably by the European Central Bank, as clearly noticeable in its policy communication (see Section 3.2). Least advanced are sovereign debt issuers and market regulators, even though the potential to strengthen incentives of the private sector to decarbonise its activities could grow exponentially.

The green transformation will impact the sectoral distribution of jobs, labor productivity and supply (Kato et al., 2015; ILO, 2018; Batten et al., 2021). Climate policies can create better jobs and technologies, but job opportunities and income could decrease in certain regions and sectors. Those negative outcomes may lead to political constraints for climate policy implementation. Monitoring and accompanying labor market transitions, therefore, are essential to guarantee a successful green transformation, requiring economic policies to be coordinated across a range of instruments to support enterprises, workers and livelihoods (Wiebe et al., 2021).

This paper gives an overview of the various instruments, public policy makers have (already used) to accelerate the green transition and the mechanisms through which such adjustment could take place or has already been observed. The next section discusses the general considerations around green economic policies, the various trade-offs involved and the role for macro-economic policies in the overall choice between regulation vs. externality pricing. In Section 3, we delve deeper into the various macro-economic instruments for green policies: Section 3.1 discusses the use of fiscal policies for carbon pricing whereas Section 3.2 looks into the role of green bonds for resource mobilization to fund the green transition. Section 3.3 turns toward monetary and financial policies whereas Section 3.4 looks specifically at some new, hybrid ways of combining private and public resource to generate funds through payment for eco-system services. Section 4 discusses implications of green macro policies for labor markets and economic development. A final section concludes.

Market failures prevent economic agents from internalizing the costs (and risks) of global warming, leading to excessive carbon emissions (Nordhaus, 2008; Bonen et al., 2016). A growing literature emphasizes that an appropriate adjustment of macro policy instruments can account for the risks and challenges of climate change (Coeuré, 2018; Batten et al., 2021). Moreover, climate policy can be successfully coordinated with economic policy goals, with a potentially minimal adverse effect on job creation (OECD, 2021). Before discussing the different instruments available for public policy makers, this section will give an overview of the different considerations that have been discussed in the theoretical literature and that need inform policy makers in their strategy to set up their policies.

Standard economic theory suggests to internalize external effects such as the (estimated) costs of climate change and loss of biodiversity via additional taxes (“Pigou tax”) that increase the price until a welfare-optimizing solution has been found. In the case of carbon emissions, the tax levy would incentivise producers to substitute for less carbon-emitting technologies. At the same time, the tax receipts could be used to finance (technological) solutions to capture carbon from the atmosphere. The amount of carbon emitted, however, would be left to market-forces that would exclusively react to the (higher) price of pollution given the carbon tax levied. The appeal of the solution is the easiness with which it can be administered and the fact that the quantity reaction (including investment into cleaner technologies and technological development itself) would be left entirely to the market, leaving the profit maximization motive intact and hence produce—at least in principle—a welfare-optimizing solution.

However, as pointed out early on by Weitzman (1974) and others, uncertainty regarding the evolution of costs and benefits from regulation play a crucial role in determining whether to regulate prices rather than quantities. In particular, while the costs of (adapting to) a reduction in pollution—for instance by introducing newer, cleaner technologies or reducing output altogether—can be easily assessed, at least for the currently available technology, the (social) costs of pollution might be hard to determine, especially as regards the impact of climate change that is long-lasting and dependent on the adjustments in a non-linear environment. In such a situation, when benefits of emission reductions or carbon removals are slow to emerge and uncertain while costs are immediate and steeply rising, a price regulation—carbon tax or emission trading system—is more efficient than a quantity regulation. In contrast, when benefits are certain and quick to materialize—for instance when it comes to avoiding tipping points—a quantitative restriction is the relevant policy tool (Hepburn, 2006).3

Such efficiency considerations need to be complemented with issues related to international collaboration, implementation, policy credibility and political economy considerations (Hepburn, 2006). Price regulation, for instance, produces additional (fiscal) resources that can be recycled through expenditure policies, for instance on social spending to smoothen the adjustment process. Quantitative restrictions, for instance by removing coal-fired power plants from the electricity grid, limit the aggregate production, do not produce any additional public revenues but will also require additional expenditures to soften the transition period to a more sustainable way of consumption and production.4 Hence, unless a climate crisis is considered or perceived to be as imminent, political economy considerations will also support price rather than quantity restrictions. We will see in the following, that the additional resources generated by such policies can be mobilized to produce wider benefits even outside the jurisdiction where they are being generated.

International collaboration and cooperation have come to play another key concern for policy makers. Indeed, strict domestic solutions do not account for green policies' international spill-over effects. Climate protection is a global public good and as such might induce a free-riding behavior that demands foreign and commercial policy instruments (Barrett, 1994). While some countries tackle climate change, others can benefit from these efforts by doing nothing. Moreover, increasing domestic prices of carbon-intensive goods and services will change countries' relative competitiveness and might induce a carbon leakage (polluting activities reallocation) to countries with a loose climate policy.

To address these issues, Nordhaus proposes “climate clubs”, in which members set an international carbon pricing to minimize their joint “social cost of carbon” and penalize non-members with import tariffs (Nordhaus, 2015). Recently, the EU has announced a Carbon Border Adjustment Mechanism in an attempt to charge carbon-intensive imports the same level of carbon price imposed by the EU ETS.5 Moreover, the World Trade Organization is already discussing the case of removing barriers and reducing tariffs for green and environmental goods and services (Ellard, 2021). Both efforts could add up to existent fiscal policy instruments in incentivizing green investment and protecting green infant industries. Importantly, integrating countries in the Global South in such climate clubs will make it easier to channel resources from green taxes and other green-related price regulation to support the adjustment process in these countries, with a view on successfully leapfrogging toward a sustainable mode of economic development. For the moment, climate finance is characterized by a large home bias with 80 per cent of financial resources generated by climate policies remaining within national borders (IPCC, 2022, ch. 15). However, considering the large natural resources in developing countries and their need to climate adaptation, climate finance is likely to significantly alter international capital flows, with consequences for capital account and exchange rate stability that will need to be properly addressed.

The transition to a carbon-neutral economy is likely to affect financial stability as well. For one, current wealth of carbon-intensive firms is tied to a fossil-fuel based production system, making them subject to sudden shifts in valuation should emission costs rise sharply. In the past, such shifts in the sources of energy production have been shown to lead to significant financial market disruptions (Kennedy, 2023). A fast transition to carbon neutrality is likely to lead to a re-assessment of wealth (“stranded assets”) with consequences for portfolio investment decisions, the value of collateral and banking sector stability (Semmler et al., 2022; Hengge et al., 2023). At the same time, rising costs of climate change, for instance in the form of natural disasters, will also affect the financial sector stability, in particular through its impact on premiums for (re-)insurance companies. Internalizing the costs of climate change through a carbon wealth tax rather than through carbon pricing would potentially allow to integrate these wealth effects more directly, thereby contributing to financial sector stability (Bastos Neves and Semmler, 2022).

Finally, alignment between different policy goals remains a key issue and one that continues to prevent a faster transition toward a greener economy: specifically, a conflict arises between economic development, socially acceptable transitions and ecological sustainability. As will be discussed in the rest of the paper, green macro policies have the potential to alleviate this trade-off by redirecting any revenues generated from pollution taxes—provided a price and not a quantity restriction is being used—to support job transitions toward greener sectors and occupations (so-called Just Transition, see ILO, 2015). At the international level, new opportunities arise for developing countries to leverage their important natural resources, for instance through payment for eco-system services (Section 3.4). At the national level, countries can opt for rebalancing taxes on capital and labor in order to alleviate the burden on labor (e.g., the German Green Tax reform in 1998). Existing evidence points to possible avenues to create triple wins with carefully designed policies to mitigate this trade-off (Van der Ploeg et al., 2022; see also below Section 4).

Given the long and uncertain time horizon over which climate policies operate in comparison to the cost of emission restrictions, policy makers have opted for a mix of price regulation—emission trading systems, carbon taxes, etc.—and quantity limitations (e.g., emission norms, heating system restrictions), with an emphasis on the former. Considerable discussion has ensued in recent years regarding the importance of tipping points in climatic developments that would considerably shift the balance toward more and stricter quantity restrictions in emissions to prevent the world climate from shifting suddenly—and most importantly irreversibly—upwards to much higher temperatures. So far, however, the scientific consensus seems to be that despite considerable global warming that has already taken place, the global climate has not yet reached such tipping points (IPCC, 2021). Nevertheless, given the continued rise in global temperatures, price regulations seem increasingly insufficient and are likely to be complemented if not substituted by measures focusing on quantitative restrictions, if at least to extract atmospheric carbon already emitted.

In this respect, greening macroeconomic policies attempts to properly price the cost of carbon emissions while generating sufficient resources to push for a large-scale green structural change, especially in energy production. At the same time, policy makers continue pursuing conventional economic goals, such as growth and price stability. A key challenge for climate policies is that it generates financial costs in the present while adverse climate impacts are expected to affect predominantly future generations (Sachs, 2015). Furthermore, financial markets do not price correctly long-term climate-related risks and benefits, leading to credit rationing and higher credit costs to green projects (Akerlof, 1970; Arrow and Fisher, 1974; Stiglitz and Weiss, 1981). Also, climate services provided by different ecosystems are not reflected in existing financial products, leading to significant geographical inequities regarding costs and benefits of climate policies. New approaches to value ecosystem services allow for a more balanced integration of spatial externalities but require significant adjustment to our current financial system (Chami et al., 2020; Ernst and Golz, 2021).

To support a faster transition to sustainable production and consumption, policymakers also act by de-risking green investments as well as ensuring that financial resources are channeled to create green jobs and technologies, replacing fossil fuels (Braga et al., 2021). Additionally, they can help overcome the short-term bias of economic agents to address the long-term consequences of climate change (Carney, 2018; Semmler et al., 2021). Both can be achieved through appropriate coordination of macroeconomic policies. Additionally, climate adaptation costs will need to be integrated into the macro-economic framework, especially to compensate countries with little adaptation capacity of their own, for instance by setting up a loss-and-damage fund.6

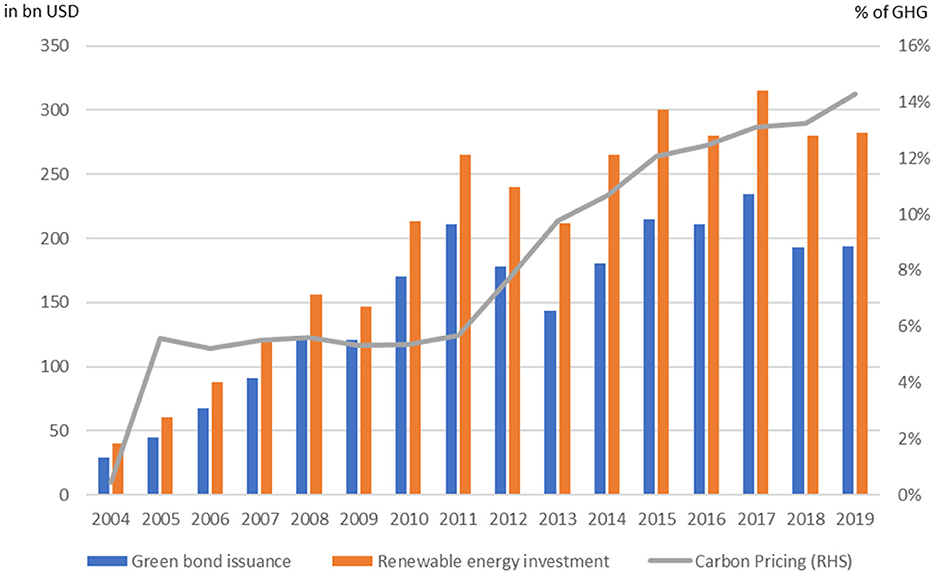

In practice, governments are already adapting economic policy to these new challenges. The use of fiscal instruments, notably, green bonds and carbon pricing, has increased significantly (Figure 1). However, the size and multi-dimensional perspective of climate challenges also require alternative instruments. Fiscal policy instruments can lower the competitiveness of countries engaged in climate policy which demands a complementary foreign and commercial policy. Furthermore, credit allocation failures demand the use of financial and monetary policy (Campiglio, 2016). These instruments are further discussed in the next sub-sections.

Figure 1. Use of green bonds, carbon taxation, and renewable energy investment (2004–2019). Source: Adapted from Heine et al. (2019) and Semmler et al. (2021).

Four main sets of macro policy instruments will be reviewed in the following:

a) Fiscal policies that directly change the relative costs of pollution, mitigation and adaption by levying carbon taxes and providing public climate goods (e.g., public infrastructure investment, subsidizing private climate-neutral technologies);

b) Green bonds for resource mobilization that channel public funds into specific (public) investment projects to accelerate the green transition, such as clean energy projects;

c) Monetary policy that influences climate mitigation costs indirectly through de-risking green bonds and other private sustainable finance instruments; financial market regulation also plays a role here inasmuch as it affects credit rating norms, for instance.7

d) Financial market policies that support the development of new sustainable finance instruments, including the development of completely new asset classes linked to eco-system services, in order to leverage natural resources for climate finance.

All four types of instruments will affect not only ecological but also social outcomes, adding further trade-offs to the design and implementation of these tools. We will discuss these in the next sub-sections.

Fiscal policy relies on the capacity of governments to spend and invest as well as to levy taxation to promote economic policy goals, such as growth and employment. Current production patterns, however, link economic growth to increased carbon emissions triggering future economic risks (Sanyé-Mengual et al., 2019). Public investment and procurement, taxes, and subsidies can change those patterns, helping agents to price correctly climate externalities (Pigou, 1932; Acemoglu et al., 2012).

Economic theory advocates that carbon pricing instruments, especially carbon taxes, are the most effective to accelerate climate transition (Nordhaus, 2008). Carbon pricing internalizes emission costs into private decisions by imposing a tax on carbon-intensive services and goods (carbon taxation) or by implementing a cap-and-trade (or emissions trading) scheme (ETS). The latter works by setting quantitative allowances to emissions (and emission rights) that are allocated by governments to firms and can be purchased (or sold) in the market in case firms have higher (or lower) effective emission rates.

Several carbon pricing initiatives can be found in North America and the European Union (EU), but the latter—especially due to the EU ETS—covers a greater share of emissions.8 Additionally, some middle-income countries, such as China, Chile and South Africa, have implemented carbon pricing mechanisms. In practice, policymakers seem to prefer ETS.9 ETS initiatives cover 13 per cent of global emissions of advanced countries, while carbon taxation covers 3.6 per cent (Semmler et al., 2021). However, managing such a mechanism is complex as an ETS demands a constant dynamic reallocation of carbon caps and allowances. In addition, as long as the ETS market is not mature, carbon prices are highly volatile, limiting its effectiveness.10 Additionally, the allocation of carbon allowances may be subjected to political influence, further decreasing the ETS efficacy. In developing countries with less developed regulatory and institutional capacity, its effectiveness might therefore be significantly lower.

Instead, carbon pricing can be achieved through a carefully designed carbon tax system that relies on the existing tax collection structure (Heine et al., 2019). However, carbon taxes imply a significant increase in tax rates, which can generate inflation, negative distributional effects, fall in (job) growth and political resistance (Grubb, 2014). For instance Sweden, usually mentioned as a successful case, raised its CO2 tax to a level >US$100 per ton (Andersson, 2019). Carbon taxation is a better solution for a greater variety of countries, but political challenges to implement such taxes might still be higher for countries with higher inequality and dependence on carbon-intensive activities.

To overcome political resistance, carbon taxation can be combined with additional public expenditures and green subsidies, compensating for welfare losses and avoiding negative distributional effects. The literature suggests that carbon tax revenues can be channeled to activities with positive externalities, such as green R&D, green infrastructure, or income distribution (Acemoglu et al., 2012; Parry et al., 2014). It could also be used to stimulate labor demand by reducing labor taxes or through just transition funds, such as the European Union's Just Transition Fund, to finance worker's training and social protection initiatives (OECD, 2020, ch. 2). Figure 2 estimates the potential for increasing revenues from carbon taxes.

Figure 2. Potential revenue increasing from carbon taxes in selected countries (% of GDP). Source: Based on IMF (2019) and Semmler et al. (2021).

Domestic tax revenues alone cannot fully respond to climate challenges (Lagarde and Gaspar, 2019). Therefore, a green transition requires a multilateral effort to mobilize international resources, for instance for investment in green energy production or nature-based solutions for carbon removal. The climate finance international architecture already relies on multilateral, regional, and bilateral public funds, some of them proposed by international climate agreements (Watson et al., 2023). However, green debt or equity instruments—such as green bonds—are also needed to leverage private resources and scale up low-carbon investment.

Green bonds are certified fixed-income debt securities, issued by public or private investors, to leverage resources in financial markets to green investments only (see Box 1). There are benefits in combining green bonds and carbon taxation. Green bonds can decrease capital costs while remaining attractive to financial market investors due to their lower volatility (Semmler et al., 2021). Green bonds can protect investors from climate change risks and future instabilities. After the COVID-19 outbreak, it showed greater resilience than fossil fuel bonds (Heine et al., 2019; Semmler et al., 2021).

Box 1. Green bonds: guidelines and practice.

Since the first green bond was issued in 2007, this market has consistently increased (Figure 1). In 2020, US$170 billion in green bonds were issued, according to the Climate Bonds Initiative, contributing to average market growth of 60 per cent per year since 2015.

Green bonds are debt securities, issued in financial markets by public or private agents, to fund green investments, such as renewable energy, clean transport and green buildings. The green bond issuers can be local or national governments, multilateral organizations and development banks, or private or public firms in financial and non-financial sectors. A green bond works exactly like a conventional bond but should be certified by a third party to ensure that the resources are invested on a pre-defined list of climate mitigation or adaptation projects. It mitigates the risk of “greenwashing” and helps to attract climate-aligned investors.

International standards have been released to better classify green investments eligible to be funded by green bonds. There are known global standards, such as those published by the Climate Bonds Initiative and the International Capital Market Association, but also regional ones. The European Union published the “EU green bond standard” and the “EU taxonomy for sustainable activities”. China also published its green bond standard. Issuers or audit firms in charge of a green bond classification should follow these rules to ensure a green bond label.

Besides green bonds, other asset classes exist that aim at similar objectives, including social bonds, sustainability bonds and sustainability-indexed funds. These assets differ from green bonds either in their structure or their underlying purpose. All have in common, however, that they include societal objectives beyond purely financial returns.

Green bonds can accelerate climate transition, ensure a fairer policy solution, and decrease political resistance against the implementation of carbon taxes. Firstly, it allows current generations to share the costs of climate policy with future generations (Sachs, 2015). Second, green bonds increase consumers' carbon price elasticity, and thus their willingness to switch to a low-carbon solution, by increasing the supply of low-carbon alternatives (Hu et al., 2015; Nadel et al., 2019; Semmler et al., 2021). Finally, green investment can create jobs, lowering the social fall-out from a green transition and thereby decreasing political resistance to climate policy.

However, most micro, small, and medium-sized enterprises (MSMEs) face financial constraints which might prevent them to issue green bonds. These firms face higher capital and transaction costs when accessing banks and financial markets (Hall and Lerner, 2010). SMEs' initial life cycle also demands equity sources, such as seed and venture capital (Berger and Udel, 1998). Governments already rely on equity funds, FinTechs, or public banks to fund SMEs' green projects (UNEP, 2017). Some of these initiatives are indirectly funded by green bonds.

Financial market failures can also prevent some countries from issuing green securities. Benefiting from green bonds depends on each country's fiscal space and its access to financial markets. Most of the green bonds are issued in high and middle-income countries (Braga et al., 2021). Several countries, such as Germany, France, Chile and Egypt, have already issued sovereign green bonds and reported lower costs and higher demand vis-à-vis conventional bonds.11 However, low-income countries without access to financial markets can rely on credit from multilateral development banks. Institutions such as the World Bank and the Inter-American Development Bank are among the largest green bond issuers and channel these resources to offer loans and de-risk green investment (Braga et al., 2021). Moreover, other instruments such as public guarantees, sovereign wealth funds (SWFs), and climate multilateral funds can provide additional funding.

Central banks and financial regulators play an important complementary role to fiscal policy by supporting the development of green financial instruments. Climate transition and physical risks will impact carbon-intensive assets and generate financial instability and losses to financial markets (Carney, 2018). Those risks involve balance sheet losses due to disasters, technology and market risks (such as a change in consumer behavior and the emergence of new green technology and sectors) or policy and regulatory risks (as governments and regulators will adjust instruments to penalize fossil fuel firms). Additionally, climate change will affect monetary policy effectiveness, as it impacts conventional central bank targets, such as inflation and output gap (Coeuré, 2018). Finally, to address market failures in private credit allocation, policymakers can channel credit flows to climate-friendly projects (Campiglio, 2016). Taken together, these challenges demand the involvement of financial regulators and central banks.

Central banks are already part of the global climate agenda, but their role is still under discussion. The Network for Greening the Financial System (NGFS) and the Sustainable Banking Network (SBN) are international networks, composed by central banks from advanced and developing countries, to propose and accompany green monetary and financial policy initiatives. However, concerns have arisen regarding the fear that contributing to climate goals harms central banks' independence, affecting their monetary policy decisions or inducing micro reallocation of financial resources (Mersch, 2018). Moreover, central banks are more constrained in terms of reserve management regarding the asset classes they can invest in (see Bouyé et al., 2021). However, their mandates already allow climate actions: both climate change and climate change policies affect conventional monetary policy targets (“transition risk”),12 and some central banks already have mandates to support the government's economic policy (such as the ECB) or climate transition (such as the Bank of England).13

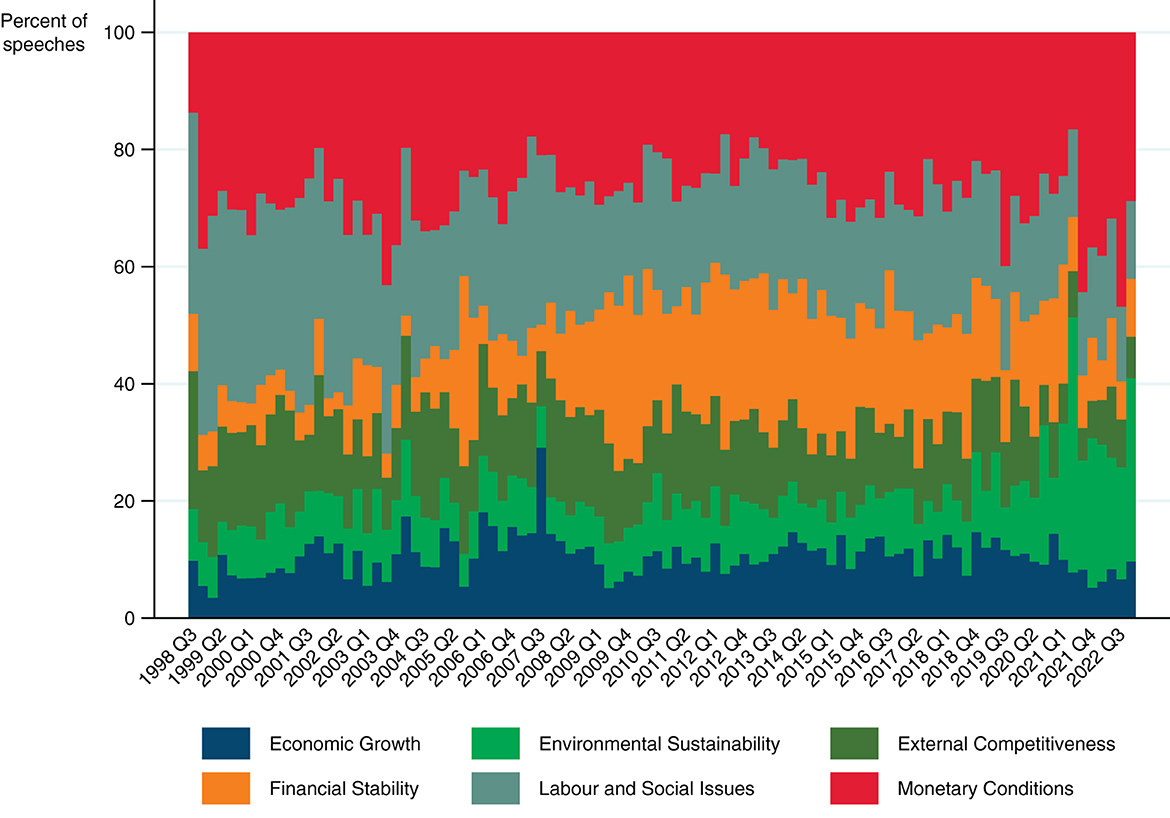

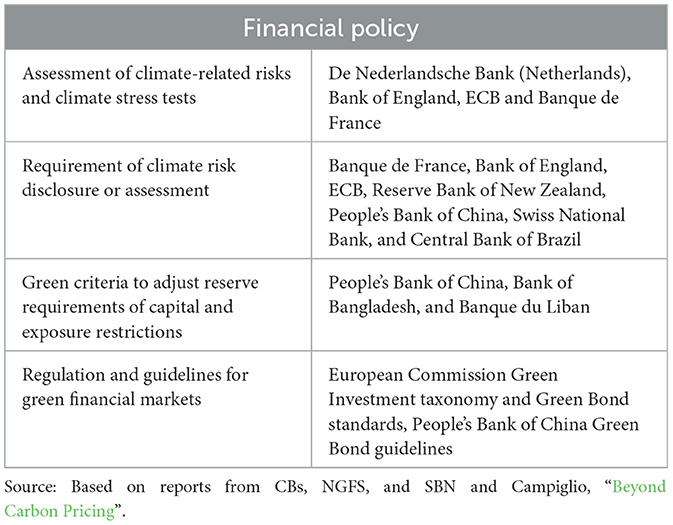

Regardless of explicit mandates, central banks and financial regulators are increasingly aware of the challenges that climate change poses for their mandate and are already adjusting their instruments to account for climate challenges. The ECB, for instance, has put increasing emphasis on environmental issues in their communication strategy and even put in place a Center for Climate Change to observe developments in this area (see Figure 3). So far, the majority of such initiatives rely on financial policy instruments, related to regulation and supervision initiatives to ensure financial stability and improve financial markets (see Table 1). In climate policy, it refers to micro and macro-prudential instruments to protect financial markets from climate risks or tools to promote and regulate green asset markets.

Figure 3. Share of speeches by ECB Executive Board members, by thematic domain (1998–2022). Source: BLS Central Bank speech database, own calculations.

Table 1. Financial policy instruments—recent experience.

Green financial policy instruments aim at inducing the financial sector to better manage climate risks. Some regulators are asking banks to add climate risks to their conventional risk assessments and disclosing their portfolio's carbon footprint and exposure to climate-related assets and loans. France has obliged institutional investors to report their climate-related exposure while the Bank of England announced that climate risk assessments will be mandatory. Commercial banks can follow standards such as the Greenhouse Gas Protocol or the UN Principles of Responsible Investment. Additionally, policy can induce banks to commit to portfolios' carbon footprint reduction goals and to demand the same from corporate lenders, regulating it, for example, through the “Science Based Targets” initiative patterns.

At the same time, several central banks are undertaking climate stress tests. These tests can be micro or macro-prudential-oriented (if focused on individual firms' and banks' vulnerabilities or the whole financial system) and measure, based on future emission scenarios, the potential losses in case of climate disasters or climate-related structural changes that affect fossil fuel firms and their likelihood of default. The Banque de France and the Bank of England have published, in 2021, new climate stress test methodologies.

Furthermore, central banks can help financial markets to price climate risks by giving incentives—such as lower reserve requirements—for those banks more active on climate finance. In China, banks can pay a higher interest rate on required reserves, depending on their internal green assessment of climate risks. The Bank of Bangladesh allowed lower equity margin requirements for climate-friendly projects. Government's current efforts in setting standards and regulating green security markets complement these incentives. The ECB, for example, had an important role in setting the European Commission guidelines for green financial markets.

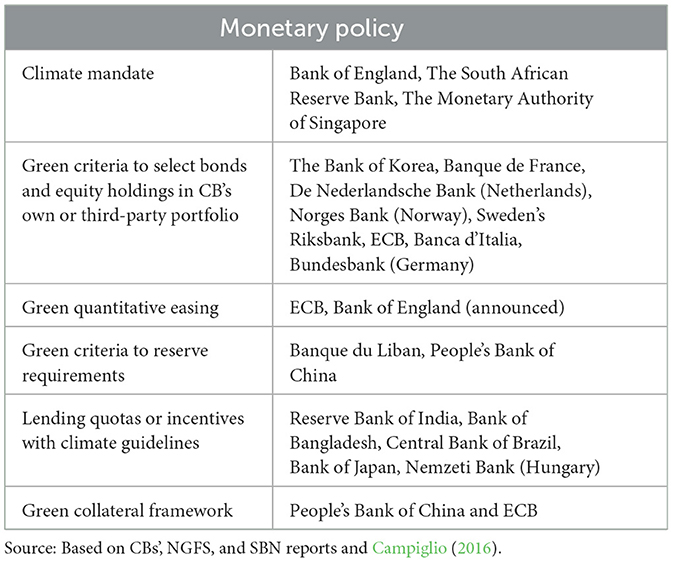

In addition to financial policy, central banks are adjusting those monetary policy instruments, that are related to the their balance sheet with a direct impact on credit flows (Table 2). A green monetary policy favors green credit flows instead of fossil fuels. An example is the adjustment of large-scale quantitative easing programmes (QE) by greening central banks' asset purchases and portfolios. QE helped reduce capital costs by decreasing the yields of purchased bonds (Joyce et al., 2011). Instead, where central banks' purchases are carbon-biased, their monetary policy favored carbon-intensive sectors and accelerated climate risks (Dafermos et al., 2020).

Table 2. Monetary policy instruments—recent experience.

Critics of this proposal advocate that asset purchases should be market neutral and not foster micro reallocation of assets (Mersch, 2018). Though, the ECB and the Bank of England have announced in 2021 the intention of increasing green bond purchases and adding climate criteria to their asset purchases.14 Additionally, other central banks have already implemented negative (or positive) screening to divest carbon-intensive assets (or to invest in climate-related assets). The Bank of Korea has excluded companies with low ESG ratings from its portfolio of foreign currency assets. The Banque de France uses negative screening to align its portfolios with a 2°C warming trajectory.

Central banks' actions should be coordinated with other public asset holders. According to the Global SWF Data Platform, pension and sovereign wealth funds (SWF) hold roughly US$31 trillion in assets. Long-term institutional investors are important players in the green bond market (Sangiorgi and Schopol, 2021). However, although SWFs are increasingly aware of climate risks, only 12 per cent have a “specific climate change framework in place” and only 29 per cent have more than 10 per cent of climate-aligned securities in their portfolios (IFSWF and OPSWF, 2021). In 2021, Norway's wealth fund announced steps to fully divest oil-related securities, and a plan to induce firms to pursue net-zero emissions is under discussion.15 However, some of the largest sovereign funds are located in fossil fuels exporters countries, such as Kuwait, Abu-Dhabi and Qatar.

Meanwhile, monetary policy can also improve collateral frameworks and credit allocation criteria to increase credit flows to green initiatives. Bank reserve requirements can be relaxed if banks' exposure is higher to green activities. In 2010, the Banque du Liban reduced reserve requirements by 100 per cent to 150 per cent of the value of loans to green projects. Central banks can also set restrictions and quotas on carbon-intensive assets or incentives for loans to sustainable investment. The Bank of Japan offers loans at a lower interest rate for banks that lend to climate projects. The Bangladesh Bank and the Reserve Bank of India imposed a minimum proportion of bank lending to climate projects. Finally, central banks can provide liquidity to the banking system based on a green collateral framework. Since 2018, the People's Bank of China has allowed green bonds as collateral to their lending facility operations. Recently, the ECB announced the use of sustainable-linked bonds as collateral to Eurosystem credit operations.

Developing climate finance through the diversification of funding sources and the development of new asset classes has become the fourth pillar for green macro policies. Indeed, green bonds and other forms of climate finance securities seem insufficient given the scale of economic transformation needed. Novel, hybrid forms of asset classes have been designed to accelerate both the availability of funds for climate action and the liquidity of climate finance assets. Hybridisation has led to two major securities gaining more prominence over the past decade, even though they still remain relatively underdeveloped given major institutional challenges: debt-for-nature swaps and natural capital backed securities.

Debt-for-nature (DfN) swaps combine traditional (sovereign) debt contracts with payments for eco-system services (PES). In this scheme, creditors concede part of their interest payments or their principal in exchange for guarantees by debtors to use the cash flow in order to restore and maintain eco-systems within their national borders such as rain forests, mangroves or coastal areas. Currently, these swaps are mostly used in cases where highly indebted countries receive debt relief in exchange for restoration efforts of natural capital (Chamon et al., 2022). Depending on the exact set-up of these funds, they can also provide immediate disaster relief, for instance when sovereign debt is rescheduled in exchange for using debt payments for adaption efforts (Hebbale and Urpelainen, 2023). First examples date back to the 1980s but have not reached much clout so far, in part because of debtors fearing to be cut off from future concessional funding or access to international markets altogether. Recent discussions in Ecuador around the risk of sovereign debt downgrading show that these concerns need to be taken into account and are likely to limit the appetite by governments to enter such schemes.16 In the absence of an international guiding framework that would specify conditions under which such schemes can and should be set up, DfNs are likely to remain little used.

Instead, a recent financial innovation aims at establishing nature-based securities that combine financial and ecological rewards, so- called valuing natural capital (VNC). In principle, both private and public owners of eco-systems can issue such securities in exchange for eco-system restoration and conservation. The advantage over DfNs is that such deals offer a novel way to value the wide range of ecosystem services that natural capital provides (see Figure 4). These benefits are both ecological and economic and can, in principle, by valued through appropriate financial valuation techniques. Payments can originate from beneficiaries of the environmental services, such as water users and hydropower companies. Alternatively, payments can also be made by those indirectly benefiting from these services such as national or local governments (mostly in the Global North). They can also be linked to pollution permission rights, for instance on carbon trading platforms. Irrespective of the specific way these securities are being structured, they allow for an enhanced role of the private sector that help grow PES schemes at both international and local levels. While the scheme is widely used on land, coastal and marine ecosystems are becoming a focus of this market-based mechanism.

Figure 4. Overview of eco-system services. Source: McKinsey (2020).

As with other securities, VNC schemes are flexible, easily applied and cost-effective, allowing high customization to local circumstances. They also help reduce inequalities if communities can improve their livelihoods by offering and selling ecological services of their (common) land or sea assets. VNC provides a potential platform to integrate conservation and climate efforts into a common policy framework and facilitates the transition from an economy of production to an economy of stewardship. Moreover, in jurisdictions with restricted public budgets, conservation policies often are de-prioritized at the benefit of other, developmental objectives. In this regard, valuing eco-system services can help empower poorer countries and provide them with fresh resources to pursue both ecological and economic objectives (Ernst, 2022).

Despite these apparent benefits, current approaches to VNC face significant challenges. First, a key problem for their implementation is weak ownership and tenure rights of forest land. Forest tenure must be clearly defined and recognized, and the ecosystem service provider must hold the rights of the service as a pre-condition. Transaction costs also occur while arranging and signing contracts, including economic assessment and information costs, contracting and monitoring costs. Moreover, additionality needs to be ensured, i.e., ecological services cannot be sold more than once. This requires, however, a clear accountability framework that so far is missing. Recent discussions around private providers of carbon credit valuations pose significant questions as to whether such additionality can be guaranteed easily and without public oversight.17 Current financial regulators are so far not in a position to properly evaluate whether additionality is guaranteed, in part because of a lack of international standards. Similarly, credit risk agencies continue to struggle in properly taking into account the contributions of green (financial) investments in affecting the risk profile of the underlying assets, which much of the drive for change coming from re-insurance companies given their much larger exposure to climate risks.18 Given the intangible nature of many of the eco-system services, economic valuation might undervalue such services and hence provide no or little incentives for eco-system maintenance and restoration.

Three inter-related social implications of the green transition have increasingly come into focus of policy makers: (i) green transitions will lead to job turnover, away from occupations in polluting industries toward emerging clean-tech jobs; (ii) they will offer improvements in health and occupational safety; (iii) and they will impact the value of physical and natural assets in an economy, implying significant wealth transfer.

The possibility for substantial job creation in green sectors or by greening existing polluting industries (“green jobs”) has entered policymakers' agenda as the number of green economic policy instruments and green recovery plans following the COVID-19 pandemic has proliferated (Hepburn et al., 2019). In practice, only roughly 20 per cent of these resources have been channeled to green initiatives (OECD, 2021). Environmental goals have historically been perceived as a constraint to growth and estimating the economic impact of green economic policy is still a challenge. Recently, however, economic recovery packages put together after the pandemic have focused more strongly on integrating a green component which are likely to accelerate the green transition.19

The perceived or actual trade-off between economic development, job creation and ecological transition is a particular challenge for countries in the Global South. Such trade-offs become particularly acute when considering the vast natural resources—forests, mangroves, seagrass, etc.—that constitute natural carbon sinks and require protection in these countries. Often, these resources are jeopardized by local needs for economic development, or their value is diminished by pollution and natural erosion in the absence of protective measures. New institutional and legal frameworks to provide governments or local communities with custodian responsibilities to protect these ecological assets promise to address both the need for ecological preservation and restoration, and the desire for improved wellbeing and livelihoods. One possibility to establish coherence between different policy goals is to establish national development boards such as in Ghana or National Development Banks (e.g., Rwanda) that can integrate potentially conflicting goals.

There is evidence that green macro policies can alleviate these trade-offs by contributing to job creation. However, assessing the impact of climate policy on labor markets demands understanding each country's structure and climate challenges. The “Green Jobs Assessment Institutions Network” studies different green employment impact assessment methods—from macro and econometric to input-output models. Input-output models were recently applied for the cases of Nigeria and Zimbabwe (Wiebe et al., 2021) and a macro-econometric general equilibrium model (Cambridge's E3ME energy-economy-environment model) was applied for COVID-19 green recovery plans (Lewney et al., 2021). These studies show that a green fiscal policy benefits employment, but its relative effectiveness is higher in the long-term and for certain sectors and places. Benefits might be lower, for example, where fossil fuel industries play a more important role in the energy mix of a country.

Other recent studies add to these findings, showing that a green active fiscal policy has a higher employment multiplier effect than conventional ones. Garrett-Peltier (2017) finds that each US$1 million shifted from fossil fuels to renewable energy creates five additional jobs. If the same amount is invested in green energy, it creates 7.5 direct and indirect jobs (vs. 2.7, when invested in fossil fuels). Green investment is more labor-intensive and demands a higher domestic content. Batini et al. find that the multiplier for renewable energy investment can be up to 1.5 while, for fossil fuels, up to 0.6 (Batini et al., 2021). The authors also find a larger multiplier for green land-use investment (vs. non-eco-friendly investment) as large-scale agriculture is dependent on imported chemical inputs and high-cost machinery.

These results depend on the sectoral distribution of investment and should be interpreted based on each country's context. Nevertheless, they provide lessons as to how green instruments can promote economic structural change, such as carbon taxes and monetary policy. Metcalf and Stock (2020) find no robust evidence of a negative impact of a carbon tax on employment and GDP. Kato et al. (2015) find that the most desirable economic outcome is achieved when carbon tax revenues are used to subsidize green initiatives. Output and employment levels decrease in high carbon-intensive sectors and increase in low-carbon activities with a positive balance on employment creation.

As projected by OECD (2018) emission-intensive sectors—such as coal and mining, fossil fuels, and fossil fuel electricity—and low-skilled positions—such as plant machine operators—will lose jobs. Meanwhile, low-carbon services and industries that are part of green supply chains will face a job increase. For Europe, Marin and Vona (2019) find that climate policies explain up to 17.5 per cent of the increase in the share of technicians and up to 8 per cent of the decrease of manual workers. It could lead to a job reallocation between countries and regions if those dependent on fossil-fuel goods do not prepare in advance to attract green investments. Just transition policies can protect workers and communities from climate transition risks, support business continuity and adaptation and ensure that workers acquire the required capabilities to be reallocated for new activities (Lewney et al., 2021).

For this purpose, green fiscal policy needs to be adjusted. Carbon tax revenues should be used to fund initiatives with positive externalities (Acemoglu et al., 2012; Parry et al., 2014). These revenues should also fund labor-related initiatives to smooth the climate transition impact on labor markets, including funds such as the European Union's Just Transition Fund. To counter the rise in economic inefficiencies from higher tax rates, fiscal-neutral green tax reforms can minimize distortions (Pearce, 1991). In particular, a carbon tax could replace or reduce the incidence of known distortionary and regressive labor taxes, reducing labor costs and inequality, and maximizing the reform benefits, as advocated by the “double dividend hypothesis”.20 To increase the benefits of a just transition in labor markets, economic policy can also be combined with other policy instruments ensuring a fairer green structural change.

Nevertheless, this sectoral shift can lead to an improvement of working conditions as some of these carbon-intensive sectors are associated with higher rates of injuries and diseases demanding tight occupational health and safety. However, some green labor-intensive activities—such as low-carbon agriculture and biofuels—might also need adequate regulatory frameworks and compliance to ensure decent wages, avoid informal employment and ban non-desirable practices. Moreover, climate policies will not only directly affect labor markets but also have co-benefits to workers' welfare and health. First, it will induce the reduction of pollutants (also in the workplace) which decreases mortality and diseases (Silva et al., 2013). Second, work accidents are likely to reduce in certain sectors. One example is transport: lower traffic congestion and road accident levels are expected outcomes of carbon taxes (Parry et al., 2014). Third, additional tax revenue from carbon taxation can be channeled to just transition initiatives to protect workers and enterprises from climate transition risks.

Despite the overall positive effects on both the quantity and quality of jobs that an ecological transition stimulated through green macro policies can generate, the challenges remain substantial. Green fiscal and monetary policies aim primarily at influencing the flow of activities (e.g., the structure of energy production, consumption and mobility). Increasingly, however, policy makers realize the impact of their policies on the value of a country's capital stock: existing fossil-fuel assets lose value as their extraction becomes less profitable (“stranded assets”), impacting both private companies and SWFs that are financed through the extraction of non-renewables. Such a destruction of existing economic wealth might significantly alter the investment pattern and hence depress economic development and job creation, although recent estimates suggest that such effects might be small, with wealth effects from stranded assets falling on the wealthiest decile of the population in advanced economies (Semieniuk et al., 2023). Nevertheless, green macro policies will also need to ensure a Just Transition in a country's wealth balance sheet, ensure a proper valuation of its natural (renewable) resources and an accelerated depreciation of its non-renewable wealth.

In this regard, the introduction of green bonds has opened the perspective for a completely new type of asset classes, based on the monetary value of services provided by large ecological systems (e.g., forests, oceans, tundra, etc.). Setting up legal framework that helps collateralising natural resources is expected to significantly speed up the green transition. Their particular promise lies in the fact that they can substantially expand the financial capacity in particular of low-income countries in promoting their ecological transition while maintaining their country on a path toward economic development and rising living standards. A major challenge will be to ensure that indigenous populations and local communities are properly being integrated in the effort for a green transition. In this regard, green macro policies need to ensure a proper balance between emission reduction efforts, carbon removal—preferably through nature-based solutions—and local community development (Chausson et al., 2023). Focussing exclusively on one of these three goals might significantly slow down a successful Just Transition.

From a capital account point of view, an additional concern arises from the transition to a nature-based balance sheet. Regardless of whether a country introduces new nature-based assets or whether it receives large capital inflows into restauration projects through DfNs for instance, together they might have a significant impact on the terms of trade of the receiving country. Indeed, considering that in low-income countries natural assets are likely to constitute their largest wealth and to the extent that PES provide resources to maintain and restore eco-systems without strengthening the productive potential of a country, international capital flows toward natural capital are likely to appreciate a receiving country's exchange rate, with adverse consequences for competitiveness. A country that desires to value its natural resources, hence, should opt for an approach similar to other resource-rich countries in setting up nature-based SWFs to manage both its domestic natural resources and the corresponding financial flows for its maintenance and restoration. This will prevent large fluctuations in its external balance that runs counter to maintaining the country on a path to a Just Transition with Decent Work conditions for all.

Climate change increases the likelihood of disasters and permanent negative shocks that might affect the economy, generating financial losses as well as GDP and employment reduction. Climate transition will also impact the sectoral distribution of jobs and labor productivity. Private sector initiatives and regulation through quantitative restrictions or pricing signals alone are unlikely to be sufficient or act sufficiently rapidly. Green macro policies not only help in smoothing the impact of the green transition on the economy, but they can also actively contribute to accelerate it and ensure its ecological and social sustainability.

A global policy framework should be developed and adapted to each country's context, in consultation with social partners, to adjust economic policy instruments to address the impact of climate transition on labor markets and the business environment. Just transition policies could induce better job creation, business resilience, social inclusion, and inclusive growth. They demand complementary initiatives such as training (and reskilling) programmes, investment in long-term climate projects and green entrepreneurship (to promote green innovation and jobs), improvement of social protection networks and occupational health and safety conditions and initiatives to help workers' reallocation to green activities.

Finally, countries in particular in the Global South should develop new mechanisms to leverage their large natural wealth in a way that protects these assets while contributing to their economic development. Carefully developed new, hybrid forms of natural assets can support this effort by leveraging the positive contribution of natural assets to climate regulation to generate new funds that help generate the necessary financial means to leapfrog toward clean energy production and local economic development. Such a transition is likely to require the introduction of new financial tools and a revamp of the international financial architecture in order to recognize the legal and economic importance of these instruments. New digital tools can help in this respect (Hilmi et al., 2023).

The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

JB drafted sections 3.1, 3.2, 3.3, and 4 with input from EE who also drafted sections 2, 3.4, and 5. All authors contributed to the article and approved the submitted version.

The authors gratefully acknowledge input on central bank speech analysis by Pawel Gmyrek (ILO). The draft benefited from feedback from Marek Harsdorff, Massimilano La Marca, Nicholas Maître, Catherine Saget, and Daniel Samaan (all ILO). Comments from two referees are gratefully acknowledged. All remaining errors are ours.

JB is an economist at the Brazilian Development Bank (BNDES).

The remaining author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1. ^For instance, coal-based power plants might currently not be located at places where renewable energy can best be generated. Similarly, many nature-based solutions for carbon removal can be found in developing countries whereas most financial resources are generated in advanced economies.

2. ^The report highlights, for instance, that in the last decade the global sea level has risen faster, and the annual average Arctic Sea ice area has reached its lowest level. Furthermore, evidence of climate-induced disasters, such as heatwaves, floods, droughts, and hurricanes, is higher than in 2014.

3. ^Carbon taxes and emission trading systems (“cap-and-trade”) are typically considered to be part of a carbon pricing system as it leaves to the individual producer or consumer to decide whether to pay the tax/carbon price or to adjust carbon emissions through lower production/investment in more efficient technologies. On the other hand, quantity restrictions involve, for instance, the certification of specific (less polluting) technologies or the removal of highly polluting power plants from the grid, see https://www.worldbank.org/en/programs/pricing-carbon.

4. ^These considerations are important limitations, for instance, for implementing socio-economic shifts as recommended by the De-growth movement.

5. ^The EU Carbon Border Adjustment is coming into effect in October 2023 (https://taxation-customs.ec.europa.eu/carbon-border-adjustment-mechanism_en).

6. ^https://www.unep.org/news-and-stories/story/cop27-ends-announcement-historic-loss-and-damage-fund

7. ^https://prospect.org/economy/2023-04-12-rise-climate-rating-agencies/

8. ^For an overview, see The World Bank Carbon Pricing Dashboard. In Europe, 84 carbon pricing initiatives are found at the federal and regional levels.

9. ^The Kyoto Protocol incentivized the implementation of ETS and allowed Annex I countries to trade carbon in the market. Moreover, the Clean Development Mechanism allowed the generation of GHG certifications from projects, which could be traded to help achieving emission caps.

10. ^This volatility is also due to the currently small size of carbon markets. Nell et al. (2011) find that the EU ETS carbon price return volatility is 10 times higher than the one for equity investments.

11. ^The Government of Chile reports a lower interest rate for sovereign green bonds (Government of Chile, “Chile Obtains Historical Yields in Euro and US Dollar Green Bond Issuances”, 22 January 2020). The German sovereign green bond was five times oversubscribed leading to lower yields (Bloomberg, “Germany's Debut Five-Year Green Bond Meets Tepid Demand”, 4 November 2020).

12. ^See, for instance, Parker et al. (2021).

13. ^UK House of Lords, “Quantitative Easing: a Dangerous Addiction?” Economic Affairs Committee, HL Paper 42, 16 July 2021. For a comprehensive survey on central banks mandate and climate goals, see Dikau and Volz (2021).

14. ^The Bank of England announced in May 2021 that it will account for the climate impact of their holdings. The ECB, in July 2021, announced that it is considering climate risks in due diligences for its corporate asset portfolios and will incorporate climate criteria for purchases.

15. ^Bloomberg, “Norway's $1.4 Trillion Wealth Fund Set to Get Strict CO2 Mandate”, 26 September 2021.

16. ^https://www.theguardian.com/environment/2023/jun/21/are-debt-for-nature-swaps-way-forward-for-conservation-aoe

17. ^https://www.theguardian.com/environment/2023/jan/18/revealed-forest-carbon-offsets-biggest-provider-worthless-verra-aoe

18. ^https://prospect.org/economy/2023-04-12-rise-climate-rating-agencies/; https://www.swissre.com/our-business/public-sector-solutions/our-solutions/nature-based-solutions.html

19. ^https://www.theatlantic.com/science/archive/2022/10/inflation-reduction-act-climate-economy/671659/

20. ^In Canada, British Columbia's carbon taxation was designed to be revenue-neutral by the combination of increasing carbon taxes with the reduction of regressive taxes to households and small firms and the increase of lump-sum transfers. Evidence shows that this policy impacted positively employment and distribution, although this effect seems small (Murray and Rivers, 2015; Yamazaki, 2017). In Australia, an intermediate solution was implemented with a “partially-revenue-recycling” carbon taxation (Carl and Fedor, 2012).

Acemoglu, D., Aghion, P., and Hemous, D. (2012). The environment and directed technical change. Am. Econ. Rev. 102, 131–166. doi: 10.1257/aer.102.1.131

Akerlof, G. A. (1970). The market for ‘lemons': quality uncertainty and the market mechanism. Q. J. Econ. 84, 489–490. doi: 10.2307/1879431

Alogoskoufis, S., Dunz, N., Emambakhsh, T., Hennig, T., Kaijser, M., Kouratzoglou, C., et al. (2021). “ECB economy-wide climate stress test. Methodology and result,” in Occasional Paper, No. 281. (Frankfurt: European Central Bank).

Andersson, J. J. (2019). Carbon taxes and CO2 emissions: Sweden as a case study. Am. Econ. J. 11, 1–30 doi: 10.1257/pol.20170144

Arrow, K. J., and Fisher, A. C. (1974). “Environmental preservation, uncertainty, and irreversibility”, in Classic Papers in Natural Resource Economics, Gopalakrishnan, C. (ed.). (London: Palgrave Macmillan), 76–84.

Barrett, S. (1994). Self-enforcing international environmental agreements. Oxf. Econ. Pap. 46, 878–894. doi: 10.1093/oep/46.Supplement_1.878

Bastos Neves, J. P., and Semmler, W. (2022). “A proposal for a carbon wealth tax. Modelling, empirics and policy”, in SSRN. doi: 10.2139/ssrn.4114243

Batini, N., Di Serio, M., Fragetta, M., Melina, G., and Waldron, A. (2021). “Building back better: how big are green spending multipliers?,” in Working Paper, No. 87. (Washington, DC: IMF).

Batten, S., Sowerbutts, R., and Tanaka, M. (2021). “Let's talk about the weather,” in Working Paper No. 603. (London: Bank of England).

Berger, A., and Udel, G. (1998). The economics of small business finance: the roles of private equity and debt markets in the financial growth cycle. J. Bank. Financ. 22, 613–73. doi: 10.1016/S0378-4266(98)00038-7

Bolton, P., Despres, M., Pereira da Silva, L. A., Samama, F., and Svartzman, R. (2020). “The green swan,” in Central Banking and Financial Stability in the Age of Climate Change. (Basel: Bank for International Settlements).

Bonen, A., Loungani, P., Semmler, W., and Koch, S. (2016). “Investing to mitigate and adapt to climate change: a framework model,” in Working Paper, No. 164. (Washington, DC: IMF).

Bouyé, E., Klingbiel, D., and Ruiz, M. (2021). Environmental, Social, and Governance Investing: A Primer for Central Banks' Reserve Managers (Washington, DC: World Bank).

Braga, J. P., Semmler, W., and Grass, D. (2021). De-risking of green investments through a green bond market – Empirics and a dynamic model. J. Econ. Dynam. Control. 131, 104201. doi: 10.1016/j.jedc.2021.104201

Campiglio, E. (2016). Beyond carbon pricing: the role of banking and monetary policy in financing the transition to a low-carbon economy. Ecol. Econ. 121, 220–230. doi: 10.1016/j.ecolecon.2015.03.020

Carl, J., and Fedor, D. (2012). “Revenue-Neutral Carbon Taxes in the Real World: Insights from British Columbia and Austrailia”, in Task Force on Energy Policy, (Stanford, CA: Hoover Institute).

Carney, M. (2018). “A transition in thinking and action”, in Speech delivered at the International Climate Risk Conference for Supervisors, (Amsterdam: De Nederlandsche Bank).

Carton, B., and Natal, J.-M. (2022). Further Delaying Climate Policies Will Hurt Economic Growth. (Washington, DC: IMF).

Chami, R., Cosimano, T., Fullenkamp, C., and Español, S. (2020). “On valuing nature-based solutions to climate change: a framework with application to elephants and whales”, in Economic Research Initiatives at Duke Working Paper Series, No. 297. (Durham: Duke University).

Chamon, M., Klok, E., Thakoor, V., and Zettelmeyer, J. (2022). “Debt-for-Climate Swaps: Analysis, Design, and Implementation”, in IMF Working Paper, No. WP/22/162. (Washington, DC: IMF). doi: 10.5089/9798400215872.001

Chausson, A., Welden, E. A., Melanidis, M. S., Gray, E., Hirons, M., and Seddon, N. (2023). Going beyond market-based mechanisms to finance nature-based solutions and foster sustainable futures. PLoS Clim. 2, e0000169. doi: 10.1371/journal.pclm.0000169

Dafermos, Y., Gabor, D., Nikolaidi, M., Pawloff, A., and van Lerven, F. (2020). Decarbonising is Easy: Beyond Market Neutrality in the ECB's Corporate QE (London: New Economics Foundation).

Dikau, S., and Volz, U. (2021). Central Bank mandates, sustainability objectives and the promotion of green finance. Ecol. Econ. 184, 2021. doi: 10.1016/j.ecolecon.2021.107022

Ellard, A. (2021). Trade Plays an Important Role in Climate Change Mitigation and Adaptation. (Geneva, WTO).

Ernst, E. (2022). How Much is an Elephant Worth? Valuing Natural Capital to Protect Nature and Improve Wellbeing. (Paris: OECD).

Ernst, E., and Golz, V. (2021). Valuing Our Eco-Systems: A Case for Blue Carbon and Beyond. Available online at: https://medium.com/@ekkehard_ernst/valuing-our-eco-systems-a-case-for-blue-carbon-and-beyond-3a2aff9594c9 (accessed August 21, 2023).

Garrett-Peltier, H. (2017). Green versus brown: comparing the employment impacts of energy efficiency, renewable energy, and fossil fuels using an input-output model. Econ. Modelling 61, 439–447 doi: 10.1016/j.econmod.2016.11.012

Grubb, M. (2014). Planetary Economics: Energy, Climate Change and the Three Domains of Sustainable Development. (London: Routledge).

Hall, B., and Lerner, J. (2010). “The financing of R&D and innovation”, in Handbook of the Economics of Innovation, 1, Hall, B., Rosenberg, N. (eds.). (North Holland: Elsevier), 609–639. doi: 10.1016/S0169-7218(10)01014-2

Hebbale, C., and Urpelainen, J. (2023). Debt-for-Adaptation Swaps: A Financial Tool to Help Climate Vulnerable Nations. (Washington, DC: Brookings Institution).

Heine, D., Semmler, W., Mazzucato, M., Braga, J. P., Flaherty, M., Gevorkyan, A., et al. (2019). “Financing Low-Carbon Transitions through Carbon Pricing and Green Bonds,” in Policy Research Working Paper, No. 8991 (Washington, DC: World Bank).

Hengge, M., Panizza, U., and Varghese, R. (2023). “Carbon policy surprises and stock returns: Signal from financial markets,” in Working Paper, No. 2023/013. (Washington, DC: IMF).

Hepburn, C. (2006). Regulation by prices, quantities or both: a rview of instrument choice. Oxfod Rev. Econ. Policy 22, 226–247. doi: 10.1093/oxrep/grj014

Hepburn, C., O'Callaghan, B., Stern, N., Stiglitz, J., and Zenghelis, D. (2019). Will COVID-19 fiscal recovery packages accelerate or retard progress on climate change? Oxfod Rev. Econ. Policy 36, S359–S381. doi: 10.1093/oxrep/graa015

Hilmi, N., Sutherland, M., Farahmand, S., Haraldsson, G., van Doorn, E., Ernst, E., et al. (2023). Deep sea nature-based solutions to climate change. Front. Climate 5, 1169665. doi: 10.3389/fclim.2023.1169665

Hu, J., Crijns-Graus, W., Lam, L., and Gilbert, A. (2015). Ex-ante evaluation of EU ETS during 2013–2030: EU-internal abatement. Energy Policy 77, 152–163. doi: 10.1016/j.enpol.2014.11.023

IFSWF and OPSWF (2021). Mighty Oaks from Little Acorns Grow: Sovereign Wealth Funds' Progress on Climate Change.

ILO (2015). Guidelines for a Just Transition Towards Environmentally Sustainable Economies and Societies for all. (Geneva: ILO).

IMF (2019). “Fiscal policies for Paris climate strategies: from principle to practice,” in Policy Paper, No. 2019/010. (Washington, DC: IMF).

Joyce, M. A. S., Lasaosa, A., Stevens, I., and Tong, M. (2011). The financial market impact of quantitative easing in the United Kingdom. Int. J. Central Bank. 7, 113–161. Available online at: https://www.ijcb.org/journal/ijcb11q3a5.htm

Kato, M., Mittnik, S., Samaan, D., and Semmler, W. (2015). “Employment and Output Effects of Climate Policies”, in The Oxford Handbook of the Macroeconomics of Global Warming, Bernard, L., and Semmler, W. (eds.). (Oxford: Oxford University Press), 445–476.

Kennedy, C. A. (2023). Biophysical economic interpretation of the Great Depression: A critical period of an energy transition. J. Industrial Ecol. 27, 1197–211. doi: 10.1111/jiec.13404

Kjellstrom, T., Maître, N., Saget, C., Otto, M., and Karimova, T. (2019). Working on a Warmer Planet. The Effect of Heat Stress on Productivity and Decent Work. (Geneva: ILO).

Lagarde, C., and Gaspar, V. (2019). Getting Real on Meeting Paris Climate Change Commitments, (Washington, DC: IMF).

Lewney, R., Kiss-Dobronyi, B., Van Hummelen, S., and Barbieri, L. (2021). Modelling a Global Inclusive Green Economy COVID-19 Recovery Programme. (Cambridge: Partnership for Action on Green Economy).

Marin, G., and Vona, F. (2019). Climate policies and skill-biased employment dynamics: evidence from EU countries. J. Environm. Econ. Manage. 98, 102253. doi: 10.1016/j.jeem.2019.102253

McKinsey (2020). Valuing Nature Conservation. A Methodology for Quantifying the Benefits of Protecting the Planet's Natural Capital. (Washington, DC: McKinsey).

Metcalf, G. E., and Stock, J. H. (2020). Measuring the macroeconomic impact of carbon taxes. AEA Papers Proc. 110, 101–106. doi: 10.1257/pandp.20201081

Murray, B. C., and Rivers, N. (2015). British Columbia's revenue-neutral carbon tax: a review of the latest grand experiment. Environm. Policy 86, 674–683. doi: 10.1016/j.enpol.2015.08.011

Nadel, S., Gaede, J., and Haley, B. (2019). State and Provincial Efforts to Put a Price on Greenhouse Gas Emissions, with Implications for Energy Efficiency. (Washington, DC: American Council for an Energy-Efficient Economy).

Nell, E., Semmler, W., and Rezai, A. (2011). “Economic Growth and Climate Change: Cap-And-Trade or Emission Tax?,” After Cancún. Climate Governance or Climate Conflicts, eds E. Altvater, and A. Brunnengräber (Berlin: Springer), 95–110.

Nordhaus, W. (2008). A Question of Balance: Economic Models of Climate Change. (Princeton: Princeton University Press).

Nordhaus, W. (2015). Climate clubs: overcoming free-riding in international climate policy. Am. Econ. Rev. 105, 1339–1370. doi: 10.1257/aer.15000001

OECD (2018). Impacts of Green Growth Policies on Labour Markets and Wage Income Distribution: A General Equilibrium Application to Climate and Energy Policies. (Paris: OECD).

OECD (2021). Assessing the Economic Impacts of Environmental Policies: Evidence from a Decade of OECD Research. (Paris: OECD).

Parker, M., Stracca, L., and Faccia, D. (2021). “What we know about climate change and inflation?”, in VoxEU. (Washington: CEPR).

Parry, I. W. H., Heine, D., Lis, E., and Li, S. (2014). Getting Energy Prices Right: From Principle to Practice. (Washington, DC: IMF).

Pearce, D. (1991). The role of carbon taxes in adjusting to global warming. Econ. J. 101, 938–948. doi: 10.2307/2233865

Sachs, J. (2015). “Climate Change and Intergenerational Well-being,” in The Oxford Handbook of the Macroeconomics of Global Warming, eds L. Bernard, and W. Semmler (Oxford: Oxford University Press), 248–259.

Sangiorgi, I., and Schopol, L. (2021). Why do institutional investors buy green bonds: Evidence from a survey of European asset managers. Int. Rev. Financ. Analysis 75, 101738. doi: 10.1016/j.irfa.2021.101738

Sanyé-Mengual, E., Secchi, M., Corrado, S., Beylot, A., and Sala, S. (2019). Assessing the decoupling of economic growth from environmental impacts in the European Union: a consumption-based approach. J. Cleaner Product 236, 10. doi: 10.1016/j.jclepro.2019.07.010

Semieniuk, G., Chancel, L., Saïsset, E., Holden, P. B., Mercure, J.-F., and Edwards, N. R. (2023). Potential pension fund losses should not deter high-income countries from bold climate action. Joule 7, 1383–1387. doi: 10.1016/j.joule.2023.05.023

Semmler, W., Braga, J. P., Lichtenberge, A., Toure, M., and Hayde, E. (2021). Fiscal Policies for a Low-Carbon Economy. (Washington, DC: World Bank).

Semmler, W., Lessmann, K., Tahri, I., and Braga, J. P. (2022). Green transition, investment horizon, and dynamic portfolio decisions. Ann. Operat. Res. doi: 10.1007/s10479-022-05018-2

Silva, R., West, J. J., Zhang, Y., Anenberg, S. C., Lamarque, J-F., Shindell, D., et al. (2013). Global premature mortality due to anthropogenic outdoor air pollution and the contribution of part climate change. Environ. Res. Lett. 8, 034005. doi: 10.1088/1748-9326/8/3/034005

Stiglitz, J., and Weiss, A. (1981). Credit rationing in markets with imperfect information. Am. Econ. Rev. 71, 393–410.

UNEP (2017). “Mobilizing sustainable finance for small and medium sized enterprises: reviewing experience and identifying options in the G7,” in The UN Environment Inquiry. (Geneva: UNEP).

Van der Ploeg, F., Rezai, A., and Reanos, M. T. (2022). Gathering support for green tax reform: Evidence from German household surveys. Eur. Econ. Rev. 141, 103966. doi: 10.1016/j.euroecorev.2021.103966

Watson, C., Schalatek, L., and Evéquoz, A. (2023). The Global Climate Finance Architecture. (Washington, DC: Henrich Böll Foundation).

Wiebe, K. S., Andersen, T., Simas, M., and Harsdorff, M. (2021). Zimbabwe: Measuring the Socioeconomic Impacts of Climate Policies to Guide NDC Enhancement and a Just Transition. (Geneva: ILO and UNDP).

Keywords: just transition, green macro-economic policies, sustainability, green bonds, carbon pricing