Alberto Ballesteros-Rodríguez

Alberto Ballesteros-Rodríguez Juan De-Lucio2†

Juan De-Lucio2† Miguel-Ángel Sicilia

Miguel-Ángel Sicilia- 1Computer Science Department, University of Alcalá, Alcalá de Henares, Spain

- 2Economics Department, University of Alcalá, Alcalá de Henares, Spain

The voluntary carbon market offers a flexible and cost-effective way to reduce greenhouse gas emissions, which has led to increased interest in these markets. Within the decentralized finance ecosystem, Decentralized Autonomous Organizations leverage the tokenization of carbon credits to enhance efficiency and transparency. KlimaDAO, established in August 2021, aims to accelerate the adoption of carbon markets by integrating blockchain technology to facilitate transparent, secure, and accessible carbon trading. This study analyzes the evolution of KlimaDAO by evaluating its market capitalization, token prices, staking participation, carbon credit retirements, market participation, and concentration. The analysis reveals that while KlimaDAO initially achieved significant engagement and activity, it now faces challenges associated with market maturity and participant retention. Finally, the study highlights the importance of standardization and regulatory frameworks to enhance interoperability, transparency, and legitimacy within the tokenized carbon market.

1 Introduction

The Kyoto Protocol United Nations (1998), adopted in 1997, was the first major international treaty to set legally binding emission reduction targets for developed countries and establish a framework for carbon trading and other mechanisms to reduce greenhouse gas emissions. Its implementation highlighted the need for global cooperation and set the stage for more comprehensive climate action. Building on this foundation, the Paris Agreement United Nations (2015), adopted in 2015, brought together nearly all countries in a collective commitment to limit global warming to well below 2°C above pre-industrial levels, with efforts to cap the increase at 1.5°. The Paris Agreement introduced nationally determined contributions, allowing each country to set its own emissions reduction targets, while promoting transparency and accountability through regular reporting and review processes.

Interest in emissions trading is increasing as companies and governments recognize the financial and environmental advantages of carbon markets. Emission Trading Schemes (ETS) and Voluntary Carbon Markets (VCMs) are gaining traction globally as flexible and cost-effective approaches to reducing greenhouse gas emissions. The European Union Emissions Trading System (EU ETS), in particular, has successfully incentivized regulated manufacturing companies to reduce carbon dioxide emissions by 14%–16% Colmer et al. (2024). Over the past decade, environmental finance has experienced exponential growth, further highlighting the importance and viability of these market-based solutions, Tao et al. (2022).

In the emerging field of decentralized finance (DeFi), carbon markets are being explored as a complement to existing systems, with various initiatives aiming to integrate the benefits of DeFi composability and decentralization. One such initiative is KlimaDAO, a decentralized autonomous organization (DAO) Hassan and De Filippi (2021); Bellavitis et al. (2023) and DeFi protocol designed to bridge the gap between Web3 and established carbon offset markets. KlimaDAO uses smart contracts to manage transactions securely and transparently whereas experimenting with incentive mechanisms. In its manifesto, written by a pseudonymous team, KlimaDAO describes itself as “a network that coordinates the delivery of climate finance to high-impact and validated sustainability projects that deliver tangible environmental benefits.”

KlimaDAO aims to address the issues of illiquidity, opacity, and inefficiency within carbon markets. Illiquidity is not solely due to the various forms of carbon credits but also the lack of seamless integration and exchange mechanisms. By leveraging blockchain technology, KlimaDAO empowers the creation of pools that combine different carbon credit tokens. This tokenization allows credits to be treated as fungible or semi-fungible assets, enabling their use in a wide array of programmable smart contracts. Such an approach enhances market liquidity and allows for greater flexibility in how credits are utilized. These objectives align with the potential benefits of blockchain technologies identified by Kotsialou et al. (2022), which include improved verifiability, lower transaction costs, and addressing concerns related to additionality and permanence.1

The rest of this paper is organized as follows. Section 2 briefly presents the environment of VCMs and tokenization. Section 3 discuss the principal features of KlimaDAO, a blockchain-based protocol that tokened carbon credits. Section 4 provides an analysis of the transactions in KlimaDAO. Finally, conclusions and outlook are presented in Section 5.

2 Background: voluntary carbon markets and tokenization

This section is structured to provide a comprehensive overview of VCMs and the tokenization of carbon credits. The first subsection begins by defining VCMs and distinguishing them from compliance carbon markets. We discuss the motivations for participating in VCMs, the types of projects that generate carbon credits, and the challenges facing VCMs. The section highlights the importance of standards and certification in ensuring the credibility and effectiveness of carbon credits.

The second subsection explains the process and benefits of converting carbon credits into digital tokens on the blockchain. It also addresses common concerns and criticisms of tokenization and provides evidence of growing institutional support. Finally, it shows how tokenized carbon credits can be integrated into decentralized finance (DeFi) applications and contribute to climate action through various carbon reduction projects.

2.1 Voluntary carbon markets

VCMs are marketplaces where individuals, companies, and organizations can buy carbon credits to offset their greenhouse gas (GHG) emissions. Unlike compliance carbon markets, which are regulated by mandatory carbon reduction schemes such as the European Union Emissions Trading System (EU ETS), VCMs operate on a voluntary basis. This allows participants to take proactive steps toward sustainability without being subject to legal obligations.

Participants in VCMs typically purchase carbon credits to neutralize their carbon footprint. Participation in VCMs is driven by mutliple factors, including environmental responsibility, corporate sustainability goals, consumer demand, and investor pressure. Each carbon credit usually represents one metric ton of carbon dioxide equivalent (CO2e) that is either reduced, avoided, or removed from the atmosphere through various projects. These projects can include renewable energy initiatives, reforestation, afforestation, energy efficiency improvements, and methane capture from landfills. By engaging in VCMs, entities can demonstrate their commitment to sustainability and contribute to global efforts to combat climate change. This market mechanism not only provides a way for participants to offset their emissions but also supports projects that deliver tangible environmental benefits.

Carbon markets are systems designed to reduce GHG emissions by capping emissions and allowing the trading of emission allowances or credits. These markets operate through two main mechanisms: cap-and-trade systems and voluntary carbon markets. In a cap-and-trade system, a limit (cap) is set on the total amount of GHG emissions allowed, and companies or entities are issued emission allowances that can be traded. If an organization reduces its emissions below its allowance, it can sell the surplus to others who need more, thereby incentivizing efficient reduction efforts, Ellerman et al. (2016). Voluntary carbon markets, on the other hand, allow businesses and individuals to voluntarily purchase carbon credits to offset their emissions, supporting projects such as reforestation, renewable energy, and energy efficiency improvements, Goldstein et al. (2020). Carbon markets create financial incentives to reduce emissions and channel funds into environmental projects, contributing to global efforts to combat climate change, Kossoy (2015).

As shown in Table 1 the volume of transactions decreased significantly from 516 MtCO2e in 2021 to 254 MtCO2e in 2022, representing a decrease of 51%. This downward trend continued in 2023, with a further reduction to 111 MtCO2e. The total market value also declined, dropping from $2.1 billion in 2021 to $1.9 billion in 2022, a decrease of 10%. In 2023, the market value decreased to $723 million. Despite the decrease in volume and value, the price per tCO2e increased from $4.2 in 2021 to $7.8 in 2022, an 82% increase. In 2023, the price decreased slightly to $6.5 per tCO2e. The significant drop in transaction volume suggests potential challenges in the market, such as supply constraints or shifts in market dynamics. VCMs face challenges such as ensuring the credibility and verification of carbon credits, avoiding double counting, and maintaining market integrity. Standards and certifications, such as the Verified Carbon Standard (VCS) and the Gold Standard2, play a critical role in maintaining the quality and trustworthiness of carbon credits. These standards provide rigorous methodologies for project validation, monitoring, and verification, ensuring that carbon credits represent real, additional, and permanent emission reductions.

Table 1. Annual Total Voluntary Carbon Markets Transaction Volume, Value, and Price per tCO2e for All Projects. Pre 2005–2023 (YTD).

2.2 Tokenization of carbon credits

Tokenization is the process of converting real-world assets into digital representations on the blockchain. This transformation turns a physical certificate or tangible asset into a digital record on a public and decentralized ledger, ensuring secure, transparent, and immutable documentation of ownership and transaction history.

Carbon credit tokenization involves transferring carbon credit information to a blockchain, effectively removing it from the corresponding traditional registry. In this process, the carbon credit is represented as a digital token, a concept that has been explored in various contexts, such as the design and governance of decentralized platforms Gan et al. (2023) and the comparative advantages of token-based financing over traditional equity Malinova and Park (2023). Carbon bridges facilitate this transfer by connecting traditional registries, such as Verra3 and Gold Standard, to the blockchain. Once tokenized, carbon credits can be sold, transferred, or retired, and can be integrated with any existing or emerging protocol, including those focused on DeFi. A key feature of this bridging process is that it is ideally permissionless, meaning that anyone who owns credits in a connected registry can transfer them to their blockchain representation.

Tokenized carbon credits differ from regular tokens used in the cryptocurrency space in several fundamental ways. Firstly, they are backed by real-world assets, whereas most cryptocurrencies are not (with the possible exception of Non-Fungible Tokens (NFTs) linked to real-world assets or some stablecoins), and their value is determined by forces driving demand for carbon offsets. As a result, carbon tokens can be expected to align closely with the price of real-world credits. Secondly, while most cryptocurrencies are fungible, tokenized carbon credits, though also fungible, are derived from NFT baskets that have specific attributes, such as different vintages or links to specific categories of projects. This aggregation process makes carbon tokens distinct and not interchangeable between pools. Only tokens generated from the same project and vintage are fungible.

Tokenization enhances the efficiency and transparency of VCMs by facilitating direct interaction between buyers and sellers, enabling disintermediation, reducing transaction costs, and mitigating fraud risks. This process not only streamlines transactions but also builds trust in the market by ensuring that every transaction is transparent and verifiable on the blockchain.

In the field of carbon credit tokenization with DAO governance, KlimaDAO is one of the most representative examples, as it fully integrates decentralised governance with the purchase and management of carbon credits. However, Regen4 Network also uses a DAO model since 2021, where holders of their REGEN token can make decisions on the development of the protocol, including the tokenization of environmental assets.

Other projects that are not DAOs but incorporate elements of community governance include Toucan Protocol5, which provides the infrastructure for carbon credit tokenization, and Flowcarbon6 and Carbonable7, which are moving towards decentralised structures in the future.

Some projects such as Open Forest Protocol8 (OFP) and Celo Climate Collective9, part of the Celo ecosystem, have structures that allow for decentralisation in specific aspects, but are not full DAOs. Finally, Nori10 tokens carbon credits, but does not have a decentralised governance structure.

Blockchain technology promotes more liquid markets by enabling instant trade settlements and eliminating the need for account setups or approvals. This technology also enhances price discovery through publicly visible transactions, which helps prevent double-counting of claims and ensures market integrity. By making all transactions transparent, blockchain ensures that each carbon credit is unique and can only be claimed once, thus preserving the credibility of the market.

Tokenized carbon credits can be seamlessly integrated into DeFi protocols, expanding demand and incentivizing the development of new projects. These credits can be staked for returns or used as collateral in lending protocols, providing additional financial incentives for participation in carbon markets. Furthermore, tokenization can streamline financing for project developers through standardized pre-purchase agreements, which improve price transparency and reduce the risk of unsold credits. The fractionalization of carbon credits into smaller units benefits small projects and sectors that require precise offsets, such as retail and transport. This approach makes the carbon market more inclusive and accessible, improving financing options for developers by allowing them to reach a broader range of buyers.

Common concerns about tokenized carbon credits include the perception that tokenization is a passing fad with no long-term relevance in the carbon market. However, the International Emissions Trading Association (IETA) announced guiding principles on tokenization, the World Economic Forum (WEF) launched a crypto sustainability forum, and the International Finance Corporation (IFC) affiliated with the World Bank endorsed blockchain-based platforms for scaling carbon markets. These endorsements suggest a growing institutional recognition of the potential for tokenization in the carbon market, Toucan (2022).

Another concern is that tokenization has not benefited any industry so far. However, studies have shown that blockchain technology has had a significant impact on financial flows, helping to unlock illiquid assets and increase the volume of carbon trading, making it more accessible, Zhao et al. (2022). There is also an argument that tokenized carbon credits are of low quality. Some fear that tokenized carbon credits could be used by bad actors to deceive buyers. Another criticism is that tokenization gives new life to non-additional credits that would otherwise be ignored by the market. Additionally, some argue that cryptocurrencies consume a lot of energy and are therefore detrimental to the climate.

Tokenized carbon credits can be utilized in DeFi applications. Actions such as automatic carbon credit retirements or royalty payments to credit developers can be programmed into transactions. Tokenization allows embedding royalties into each carbon credit, so that a portion of the value from each trade is returned to the project creator. This continuous revenue stream incentivizes further climate action and supports project financing. Royalties can also be applied to bridging, redemption, or retirement fees. Tokenization simplifies the sale of future carbon credits, allowing individuals or corporations to buy “future carbon tokens” directly from developers with minimal fees. Tokenized carbon credits can be used to earn yield or as collateral for borrowing, providing additional financial opportunities. Protocols can add carbon credits to their treasury to diversify their balance sheet, hedging against the volatility of traditional cryptocurrencies. Finally, gamifying carbon credits can incorporate carbon credits as green in-game assets, creating a significant market opportunity.

These tokenized carbon credits are generated through specific carbon projects aimed at reducing or eliminating greenhouse gas (GHG) emissions from the atmosphere. These projects are essential for the KlimaDAO ecosystem, allowing users and organizations to offset their own carbon emissions. Through the implementation of these diverse carbon projects and the active retirement of carbon credits, KlimaDAO facilitates significant contributions to combating climate change. Various types of compensation projects are utilized, including reforestation and afforestation, renewable energy, energy efficiency, carbon capture and storage, and waste management.

2.3 KlimaDAO: a blockchain-based protocol using tokenized carbon credits

KlimaDAO is a DAO dedicated to creating a digital carbon economy by tokenizing carbon credits, which can be traded and retired on the blockchain. Through the use of its native token, KLIMA, the DAO incentivizes the removal of carbon dioxide from the atmosphere. This community-driven model aims to promote sustainable practices and support carbon offset projects, thereby contributing to global climate action. KlimaDAO incentivizes the issuance of new Tokenized Carbon Tonnes (TCT) on the blockchain through the KLIMA token. Rather than simply offsetting their carbon footprint with carbon credits, companies are encouraged to engage in more environmentally friendly actions.

To fully understand the current proposition of KlimaDAO, it is essential to consider its roots and inspiration from the OlympusDAO11 protocol, which centers on building a treasury through the complementary mechanisms of bonding and staking in a game-theoretic setting, hypothesized to stabilize prices, Chitra et al. (2022). Staking encourages long-term holding of KLIMA tokens and provides market participants with exposure to rising carbon prices. Bonding allows any address to purchase discounted KLIMA tokens over a vesting period, with the premium increasing and the discount decreasing as demand for bonds rises, and vice versa.

A natural extension of this economic model is the governance system that KlimaDAO employs. The governance framework allows token holders to actively participate in decision-making through a decentralized voting mechanism. Utilizing KLIMA tokens, community members can propose new additions or changes to the ecosystem via a dedicated web portal12. These proposals are then subject to voting, where the balance of tokens in users’ wallets is used to determine their voting power.

The governance process typically follows a structured flow. It begins with an idea, which is then discussed in the KlimaDAO forum through a Request for Comment (RFC). After achieving soft consensus, the idea is formalized into a Klima Improvement Proposal (KIP) and undergoes further assessment by relevant committees, such as the Guarantee Committee for decisions. Finally, once the proposal reaches hard consensus, it is put to a formal vote through Snapshot, ensuring the participation of the broader community and alignment with the project’s long-term goals.

Building on the foundational concepts inspired by OlympusDAO, the performance and stability of the KlimaDAO ecosystem are critically dependent on the assets and tokens owned by the protocol’s treasury. These holdings provide the necessary backing for the KLIMA token and fund various projects and operations within the protocol. By maintaining sufficient liquidity and support for bond issuance and staking, the treasury ensures the robustness and resilience of the ecosystem. The strategic management of these assets helps KlimaDAO to achieve its mission of promoting sustainable practices and supporting carbon offset projects. Among the most notable tokens within the KlimaDAO ecosystem are BCT, NCT, UBO, NBO, and MCO2.

Liquidity Pool Tokens (LP Tokens) are tokens received by users who provide liquidity to decentralized exchanges (DEXs) by depositing pairs of assets into liquidity pools. These tokens represent the user’s share in liquidity pools that include pairs such as KLIMA/USDC18, BCT/USDC, and others. These tokens entitle the holder to a portion of the transaction fees generated by the pool. Additionally, LP tokens can be staked or used as collateral within the KlimaDAO ecosystem to earn additional rewards, participate in governance, and support the stability and liquidity of the protocol.

This asset-backed structure is fundamental to KlimaDAO’s monetary policy. KlimaDAO’s monetary policy is centered around dynamically managing the supply of KLIMA tokens to align with the growth of the carbon market while ensuring market stability. At the core of this policy is the intrinsic value of KLIMA, stems from the fact that each token is backed by at least one tonne of carbon credits, such as BCT. This backing ensures that each KLIMA token has a tangible, minimum value tied to real-world environmental assets. The treasury holds these carbon credits, acting as a reserve, and each KLIMA token reflects the health of the carbon market. This provides a price floor and guarantees that the token’s value is directly linked to global environmental sustainability efforts.

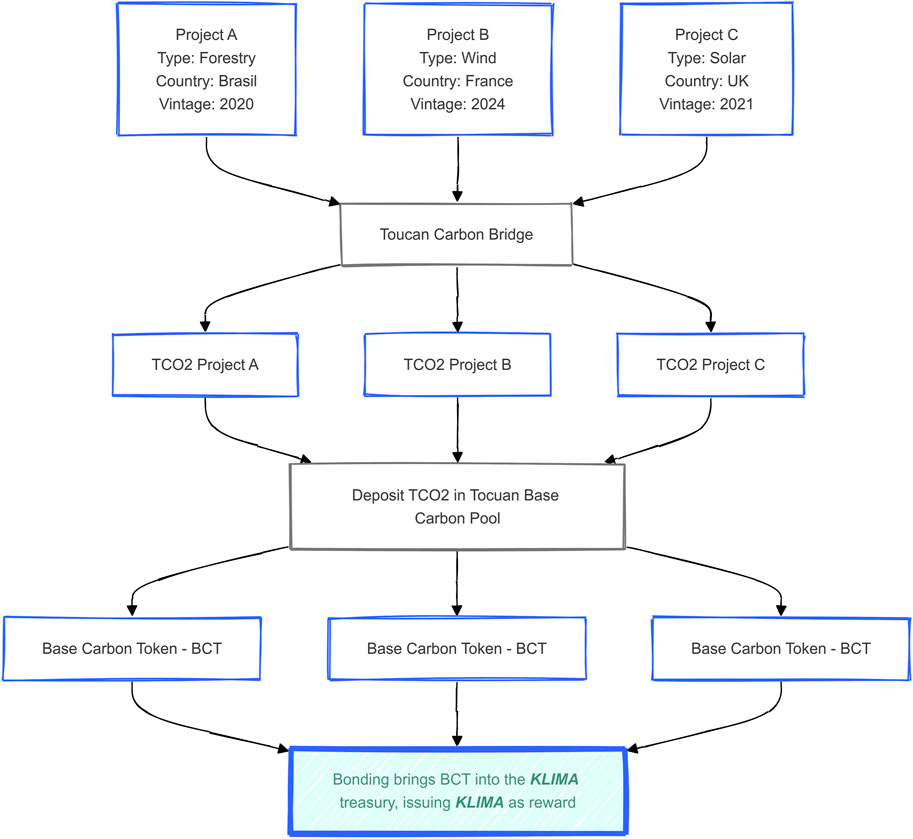

In practice, the process begins with the acquisition of carbon credits from diverse environmental projects. As shown in Figure 1, projects such as forestry, wind, and solar initiatives generate carbon credits (represented as TCO2 tokens) that are deposited into the Toucan Base Carbon Pool. These credits are then tokenized into BCTs. Once these BCT tokens are available, they can be used in the bonding mechanism, which brings BCT into the KlimaDAO treasury. Through this process, users exchange their BCT for newly issued KLIMA tokens, with the treasury holding the BCT as backing for the KLIMA that enters circulation. This ensures that every KLIMA token is backed by at least one tonne of carbon, as demonstrated in the diagram, and guarantees that KlimaDAO’s supply expansion is always aligned with the growth of the carbon market.

Figure 1. KLIMA token issuance process using the on-chain Toucan protocol for carbon offset projects as an example of how the mechanism works.

KlimaDAO algorithmically controls the supply of KLIMA tokens, functioning as a type of asset manager. The protocol has exclusive authority to mint or burn KLIMA tokens using smart contracts. Supply expansion is aligned with the growth of the carbon market through the Annual KLIMA Rate (AKR), ensuring that KLIMA’s supply grows in harmony with the market to prevent excessive volatility. If the KLIMA supply expands too quickly, it could lead to inflation, reducing its value. Conversely, if it grows too slowly, deflationary pressure could increase, raising the cost of entry into the market. This dynamic adjustment of supply ensures KLIMA remains stable and serves as an effective medium for trading carbon credits.

Another key component of KlimaDAO’s monetary policy is Protocol-Owned Liquidity (POL), where Klima manages its own liquidity pools, such as KLIMA/BCT and KLIMA/USDC. This ensures that KLIMA remains liquid and can be traded across carbon credit markets efficiently, facilitating price discovery and reducing slippage. By controlling its liquidity, KlimaDAO enhances the stability and resilience of carbon markets, supporting liquidity provisioning and ensuring that KLIMA remains a reliable instrument for both digital finance and real-world environmental projects.

On the supply contraction side, KlimaDAO uses retirement bonds as a primary mechanism to remove KLIMA tokens from circulation. When a user exchanges KLIMA tokens for carbon credits, those credits are retired, permanently removed from circulation, thus reducing the supply of KLIMA tokens. This deflationary mechanism helps balance the inflationary pressures caused by supply expansion. The retired carbon credits contribute to environmental sustainability, while the contraction in KLIMA token supply maintain the token’s value stability over time.

The fundamental building block of KlimaDAO is the KLIMA token, a fungible token compliant with the ERC20 standard19. Each KLIMA token is backed by at least one tonne of tokenized verified carbon offsets stored in the KlimaDAO treasury. Additionally, the KLIMA token functions as a governance token, granting holders the ability to vote on KlimaDAO policies. Proponents conceptualize KlimaDAO as a “decentralized” bank that governs the monetary policy of KLIMA. Token holders enjoy a range of incentives, including access to exclusive features, discounts, revenue sharing, rewards, potential earnings, token appreciation, enhanced reputation, and participation in governance, as discussed by Freni et al. (2022).

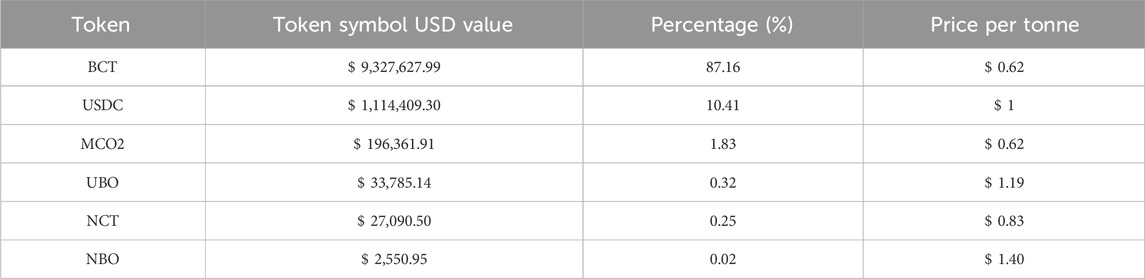

In the current KlimaDAO treasury, the primary token is BCT, which corresponds to real-world Verified Carbon Units (VCUs) from registries such as Verra20. As shown in Table 2, the treasury is heavily weighted in BCT, reflecting a strong commitment to carbon offset credits. Significant holdings of USDC, a stablecoin, provide liquidity and stability. Investments in MCO2 and NCT indicate a strategy focused on carbon credits, while smaller holdings in UBO and NBO demonstrate a diversified approach within the realm of carbon credits. This balanced portfolio strategy underscores the importance of both carbon offset assets and stablecoins for maintaining liquidity and stability.

Table 2. Main currencies in the KlimaDAO Treasury as of May 2024. Data collected from the KlimaDAO protocol metrics subgraph.

The management of the KlimaDAO treasury is essential to its stability and long-term sustainability. The treasury holds a diversified portfolio of assets, with a strong emphasis on carbon-backed tokens like BCT, as well as stablecoins like USDC, which provide liquidity. The strategic management of these assets is governed by an overarching framework known as the Green Ratio, established in KIP-55, which dictates how the treasury allocates its resources to maintain its mission of sustainability while ensuring operational stability and economic resilience.

At its core, the Green Ratio divides the treasury’s assets into four key categories to ensure a balanced and strategic allocation. Forward Carbon (22%) represents KlimaDAO’s future commitments to purchase carbon offsets from projects like reforestation and carbon capture. Treasury Reserves (48%) are assets not immediately used for KLIMA backing, including protocol-owned liquidity, spot carbon credits, and stablecoins like USDC, which help provide liquidity and financial stability. Operational Expenditure (OpEx, 10%) covers the day-to-day costs of running the protocol, such as development and marketing, primarily funded through idle USDC or similar assets. Finally, Carbon Backing (20%) ensures that every KLIMA token is backed by tangible environmental assets, with BCT playing a critical role in linking KLIMA’s value to real-world carbon offset efforts. This strategic division, guided by the Green Ratio, maintains the balance between sustainability and operational effectiveness, ensuring that KlimaDAO can continuously support carbon offset projects while maintaining liquidity and stability.

The Green Ratio allows KlimaDAO to strategically manage its assets while ensuring that the protocol remains both economically viable and true to its mission. As seen in Table 2, BCT dominates the treasury holdings, reflecting KlimaDAO’s strong commitment to carbon-backed assets. However, the presence of other assets like USDC and MCO2 indicates a balanced approach that combines liquidity with environmental impact.

3 Results and discussion

This section first explains the data acquisition process, detailing how data were gathered from KlimaDAO’s production subgraphs and the Polygon blockchain. It then examines various aspects of the protocol’s performance, including transaction volumes (capitalization and prices), staking activities, carbon credit retirements, user engagement (participation and adoption), and market concentration. The goal is to assess past activity and identify future enhancement opportunities within the KlimaDAO protocol.

3.1 Data acquisition

The data were obtained from the KlimaDAO protocol subgraphs21. Specifically, the data were extracted from the production subgraphs hosted on The Graph22. While all available data were systematically extracted, not all were used in the subsequent analyses. This was due to the incompleteness of some data or their lack of relevance to the study. The subgraphs from which relevant information was obtained are.

The extraction process used the GraphQL endpoints provided by these hosted services. For each endpoint, the available entities were identified using a schema query. Subsequently, queries were constructed to retrieve all fields declared in the schema, ensuring a comprehensive download of the available data. Pagination was implemented by sorting using the identifier fields available for all entities. The resulting data were saved in CSV files for further processing using dataframes and other tools in Jupyter notebooks.

Additionally, specific transactions related to staking were obtained through direct analysis of the Polygon23 blockchain. This involved querying the blockchain for staking events, verifying the integrity of the data, and cross-referencing with the subgraph data to ensure accuracy. The analysis focused on understanding staking patterns, user behaviour, and the overall impact on the KlimaDAO ecosystem.

The analysis is based on the data provided by KlimaDAO and aims to provide evidence of KlimaDAO’s success over the past 3 years, as well as insights into potential key developments and improvements for the project. By examining transaction volumes, staking activities, and user engagement, this report seeks to highlight both the achievements and the areas for future enhancement in the KlimaDAO protocol.

3.2 Capitalization

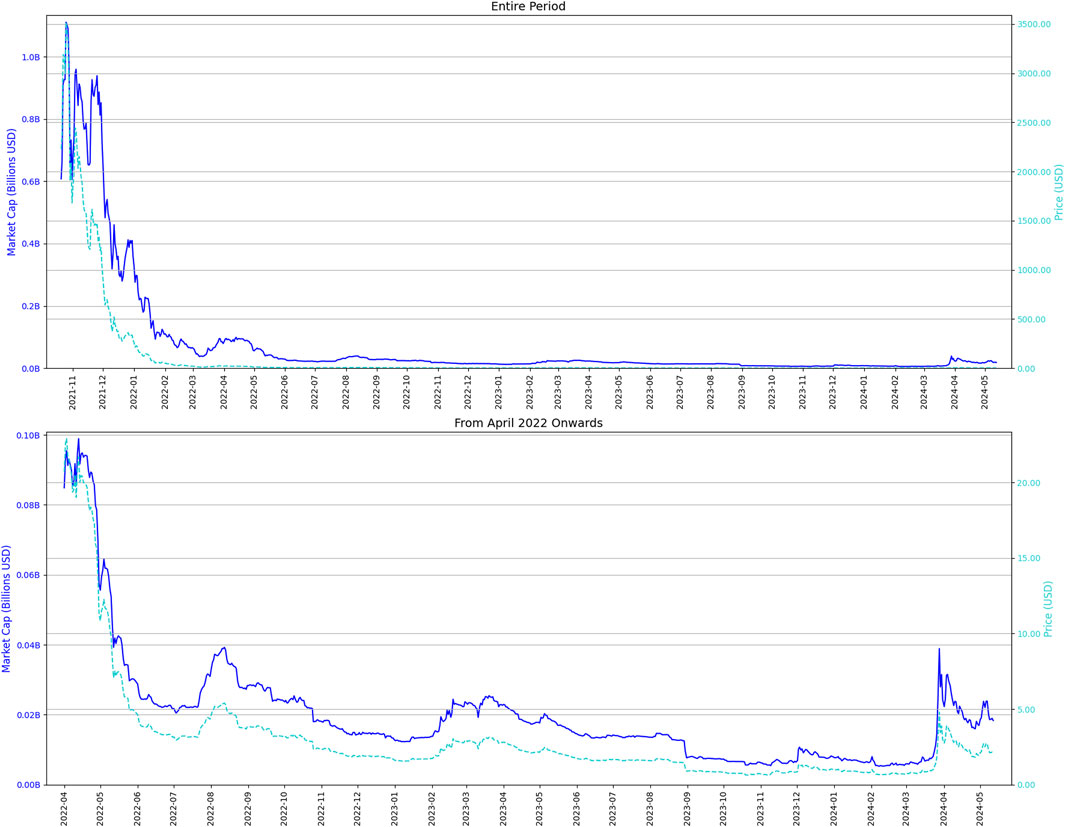

The economic performance of KlimaDAO can be assessed through an analysis of its market capitalization (solid blue line) and token price over time (dashed cyan line) in Figure 2. This section examines the trends and fluctuations in these metrics, providing insights into investor behaviour, market dynamics, and the overall financial health of the protocol.

Figure 2. Evolution of market capitalization and price in USD of KlimaDAO.

Figure 2 comprises two panels, each presenting a time series plot of market capitalization (in billions USD) for KlimaDAO and price (USD). Initially, the market capitalization stands at around 1.2 billion USD in November 2021, then undergoes a significant decline, reaching approximately 0.2 billion USD by May 2022. This decline is steepest during the initial months, followed by a more gradual decrease. The top panel illustrates this sharp drop in market cap, indicating strong initial interest that significantly wanes over time. In contrast, the bottom panel reveals that market capitalization stabilizes, suggesting periods of renewed but short-lived interest in KlimaDAO.

In addition, Figure 2 also includes price evolution, right axis, of KlimaDAO in USD over different time periods. The top panel indicates that the price starts very high, at around 2500 USD in November 2021, followed by a dramatic decline over the next few months, with prices falling to below 500 USD by February 2022. This sharp drop suggests substantial initial interest that quickly faded, possibly due to market corrections, loss of investor confidence, or initial overvaluation. Meanwhile, the bottom panel shows that the price continues to decline, eventually stabilizing at lower levels. Throughout 2023 and early 2024, the price fluctuates between one and 5 USD, with occasional minor spikes. By May 2024, the price shows a slight increase but remains significantly lower than its initial value in late 2021.

The charts demonstrate a positive correlation between market capitalization and token price, indicating that these two measures generally move in tandem. However, they are not perfectly synchronized, as fluctuations in price may not immediately reflect in the market cap. This strong correlation suggests that changes in token price significantly influence market capitalization, which aligns with the findings of Nadler and Guo (2020), who describe market capitalization as a dynamic, value-weighted index influenced by both token prices and supply. This relationship underscores how variations in token price can directly impact the overall market cap, thereby reinforcing the observed correlation.

3.3 Staking

Staking within KlimaDAO is the process where users lock their KLIMA tokens within the protocol to earn rewards in the form of additional KLIMA tokens. This mechanism incentivizes participation and supports the stability and growth of the KlimaDAO ecosystem, promoting environmental sustainability by linking the value of the tokens to carbon emission reductions.

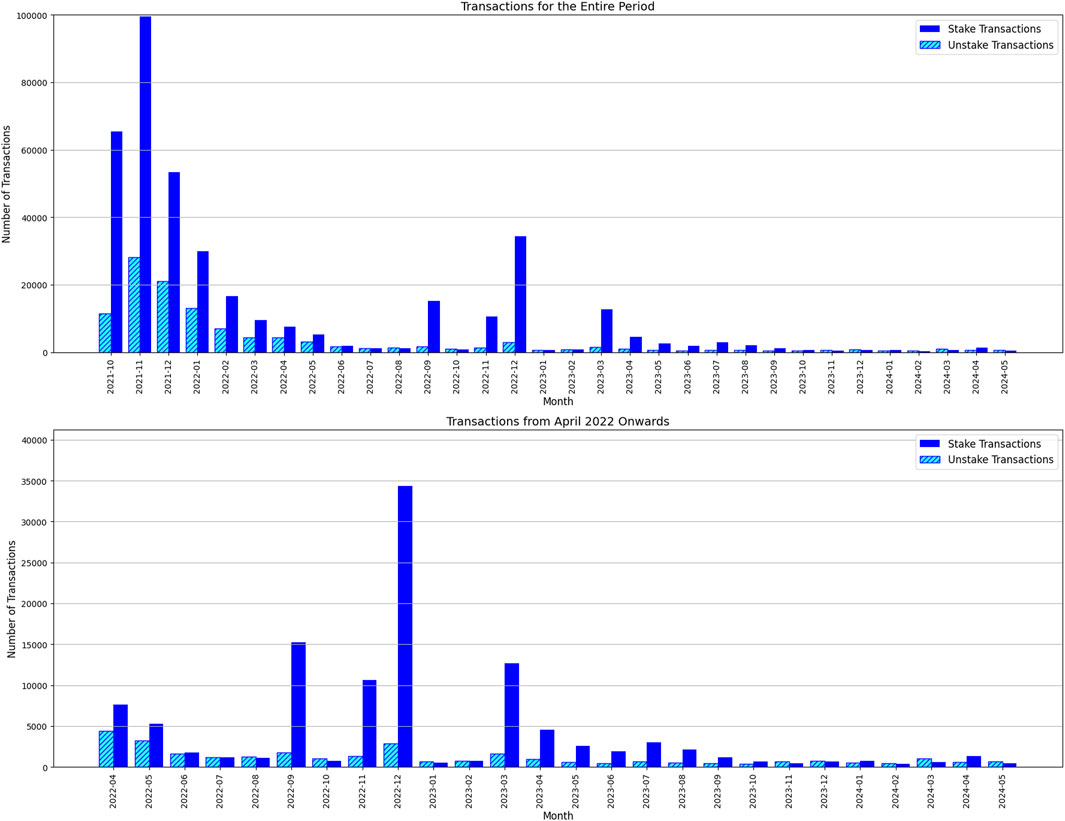

An analysis of the number of staking and unstaking transactions, shown in Figure 3, reveals distinct phases in user engagement with the KlimaDAO protocol. From October 2021 to April 2022, KlimaDAO experienced a period of high activity in both staking and unstaking transactions. In October 2021, the protocol recorded 65,522 staking transactions, reflecting strong initial interest. This activity increased by 51.8% in November 2021, reaching 99,483 transactions. However, beginning in December 2021, staking activity saw a significant decline, with transactions dropping by 46.3% compared to November. This downward trend continued into January 2022, where transactions further decreased by 44% from December, resulting in 29,881 staking transactions. By April 2022, staking transactions fell even further to 7,636, indicating a sustained decrease in activity since the protocol’s launch. Unstaking activity followed a similar pattern during this initial period. In October 2021, there were 11,455 unstaking transactions, which increased by 145.5% in November 2021. However, December 2021 saw a 25.4% decrease compared to November, with transactions falling to 20,966. By April 2022, unstaking activity had continued to decrease, with 4,374 transactions recorded, reflecting a consistent decline alongside staking activity.

Figure 3. Number of Staking and Unstaking operations within KlimaDAO.

Between April and September 2022, both staking and unstaking activities continued to decline, although with less dramatic variations. In August 2022, staking transactions reached a low point of 1,081, marking a 93.5% drop from February 2022. However, in September 2022, there was a significant rebound, with staking transactions increasing by 1,308% compared to August, rising to 15,232. Unstaking transactions also decreased during this period, dropping to 1,262 in August 2022, before slightly recovering to 1,738 in September, a 37.7% increase from the previous month.

A brief recovery in staking activity occurred in December 2022, with transactions rising to 34,365, a 224.3% increase compared to November 2022. However, from February 2023 onwards, staking activity stabilized at significantly lower levels. Between March 2023 and May 2024, staking transactions ranged between 1,000 and 4,000 per month, averaging around 2,000 transactions, with monthly variations generally below 1%, indicating a stabilization of user participation. Similarly, unstaking activity also stabilized during this period, with monthly transactions ranging between 400 and 1,000. For instance, May 2023 recorded 613 unstaking transactions, while May 2024 saw a slight increase to 651 transactions, reflecting a stagnation in user engagement with minimal fluctuations in staking and unstaking activities in recent months.

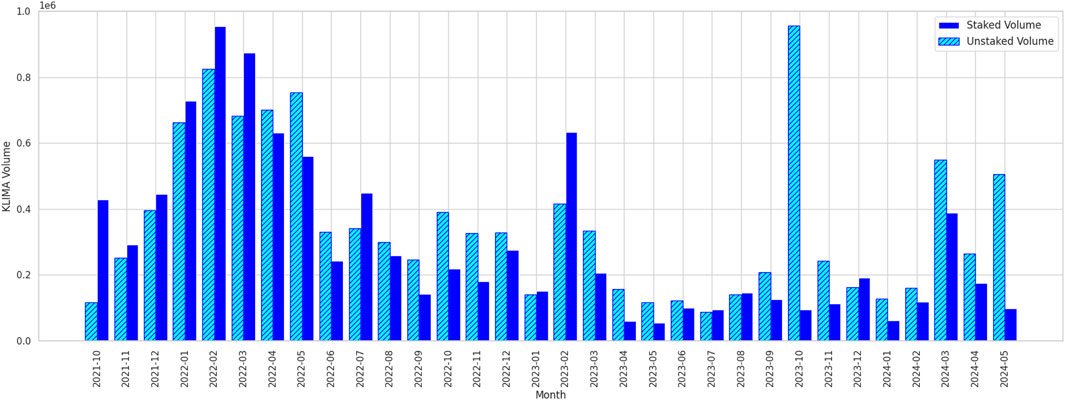

Complementing this analysis, Figure 4 depicts the volume of KLIMA tokens involved in these staking and unstaking operations. The pattern mirrors the transaction count, with substantial volumes in the early months, peaking in late 2021 and early 2022. This high volume indicates significant asset movement and possibly high investor confidence during this period. Over time, the volume of these operations also declines, with occasional spikes. By mid-2022 and throughout 2023, the volume stabilizes at much lower levels, reflecting reduced market activity and possibly a more stable but less engaged user base. These fluctuations highlight the initial volatility and subsequent stabilization in user engagement and transaction volumes within the KlimaDAO ecosystem.

Figure 4. Volume of Staked and Unstaked operations within KlimaDAO.

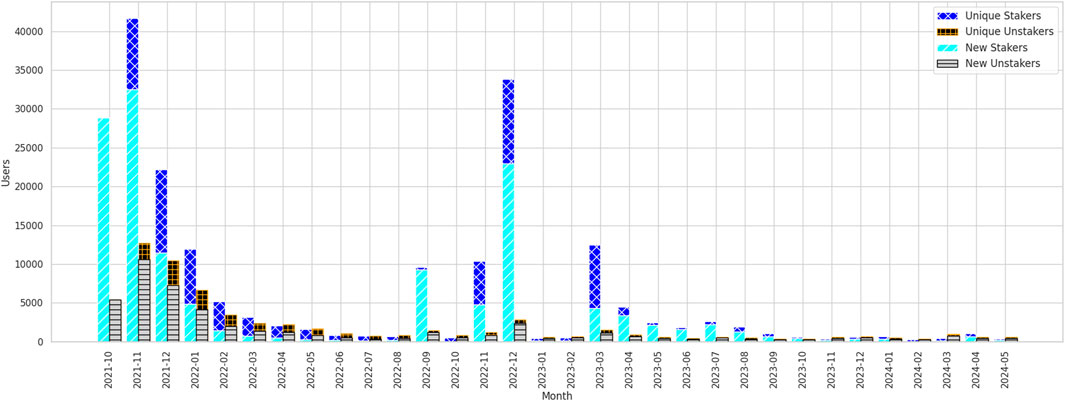

Additional insights can be gathered from Figure 5, which visualizes the number of unique and new stakers (first bar) and unstakers (second bar) by month for the KlimaDAO platform. The graph distinguishes between unique and new stakers and unstakers. In the early months from October 2021 to January 2022, staking activity saw significant changes in both total participants and first-time users. In October 2021, there were 28,870 unique stakers, all of whom were new users. In November 2021, the total number of unique stakers increased by 44.38% to 41,690, with 32,539 new stakers joining that month. However, in December 2021, there was a 46.75% decrease in unique stakers, dropping to 22,206, while the number of new stakers also decreased by 64.75%, with only 11,478 new users joining. By January 2022, the decrease continued, with unique stakers falling by another 46.28% to 11,929, and new stakers further dropping to 4,863, representing a 57.62% decline from the previous month.

Figure 5. Number of unique and new Stakers/Unstakers of KlimaDAO.

From February to September 2022, the downward trend continued, but with smaller variations. In February 2022, unique stakers fell by 56.52% from the previous month, down to 5,186, and new stakers dropped to 1,453. By September 2022, unique stakers had further decreased by 57.92% over these months, reaching just 2,182. However, in the last quarter of 2022, a resurgence occurred. In November 2022, the number of unique stakers increased by 1,152.71%, jumping from 2,182 to 27,340, while new stakers saw a 1,440.68% increase, reaching 22,387 new users. This growth persisted into December 2022, with unique stakers increasing by 8.99%–29,801, and new stakers rising by 14.58%–25,654.

From February 2023, the staking activity stabilized. Between March and September 2023, the total number of unique stakers saw variations ranging from −10% to 15% month to month, with fewer than 2,000 new users joining staking for the first time each month. From October 2023 to May 2024, staking activity saw marginal variations, with total unique stakers growing by less than 5% overall during this period, and new stakers hovering around 500 to 1,000 per month, indicating a clear stagnation in staking participation.

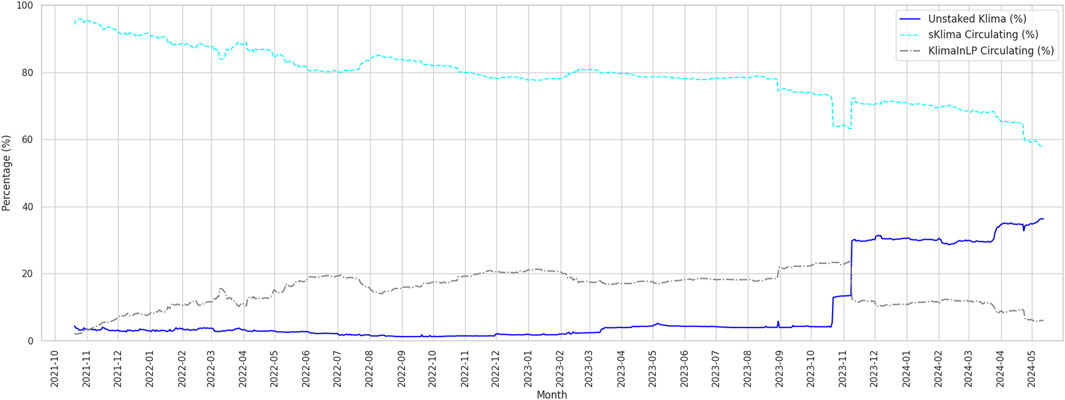

To further understand the dynamics of staked and unstaked KLIMA tokens, Figure 6 provides insight into the percentages of unstaked KLIMA, sKLIMA circulating, and KLIMA in LP circulating over time. Initially, a high percentage of KLIMA tokens are staked, indicated by the high level of sKLIMA circulating. However, as time progresses, there is a noticeable decline in the percentage of staked tokens, with a corresponding increase in unstaked KLIMA. This trend aligns with the earlier observed decline in staking transactions and volume, suggesting a decrease in user engagement and staking activity. The fluctuations in the percentages also highlight periods of increased liquidity and token movement within the ecosystem, reflecting changes in user behaviour and market conditions.

Figure 6. KLIMA circulating tokens relative to the total supply.

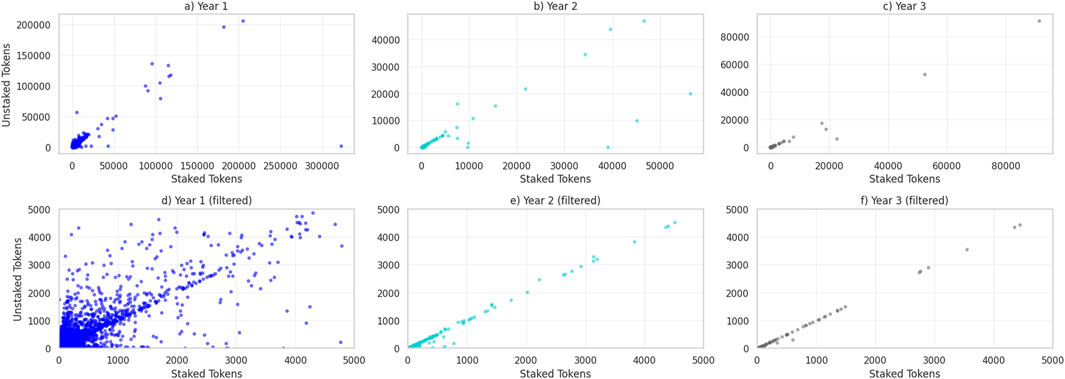

Further, Figure 7 illustrates the relationship between staked and unstaked tokens on KlimaDAO across its first 3 years. In Year 1 (panel a), we observe a wide dispersion of data points, indicating significant activity in both staking and unstaking, with some instances of very high token movements. As we move to Year 2 (panel b), the scatter plot shows a more concentrated cluster of data points, suggesting a reduction in extreme staking and unstaking events, although there are still noticeable outliers. By Year 3 (panel c), the dispersion further narrows, indicating a stabilization in staking and unstaking activities with fewer large token movements. The bottom row (panels d, e, f) of Figure 7 provides a zoomed-in view (filtered data) of the same scatter plots for each year, focusing on a smaller range of staked and unstaked tokens. In the filtered view for Year 1 (panel d), the data points are more densely packed, showing frequent smaller transactions. For Year 2 (panel e), the zoomed-in plot continues to show a tight clustering of data points, reinforcing the observation of reduced volatility in staking and unstaking activities. Finally, the filtered view for year 3 (panel f) highlights a consistent pattern of smaller, more stable transactions, indicating a mature phase of the platform with a stable core user base. Overall, these figures illustrate the evolution of staking and unstaking behaviour on KlimaDAO, showing a transition from high volatility and large token movements in the early stages to more stable and consistent patterns of activity over time, as well as a lower number of transactions.

Figure 7. Relationship between staked and unstaked KLIMA tokens from the first year to May of the third year (2024). Plots (A–C) show the complete data, while plots (D–F) show the data zoomed to a maximum of 5,000 tokens.

From Figure 7 several conclusions can be drawn about the staking dynamics of KlimaDAO. The high initial engagement (high levels of staking and unstaking activity), reflecting possibly speculative behaviour as users explore the new platform, gives way to a stabilization with lower numbers of transactions and narrowing dispersion/volatility. The initial high movement of tokens implies significant liquidity and profit opportunities. As the market stabilizes, these opportunities become less frequent, reflecting a more stable but less dynamically profitable environment. The early stages are likely to offer higher rewards, but also higher risks, with the potential for significant gains or losses. In contrast, the later stages offer lower but more stable returns, consistent with a more mature and less speculative market phase.

Building on the previous analysis of the relationship between staked and unstaked tokens over the first 3 years, we can further evaluate the economic performance of staking in KlimaDAO. Table 3 illustrates the median economic performance of staked versus unstaked tokens over different periods (30, 60, and 90 days) across these years. It highlights the diminishing returns over time, showing a clear trend where the initial high rewards for staking progressively decrease over the following years. In Year 1, the unstaked-staked ratio shows significant returns for staking over short, medium, and long periods. Specifically, the median return after 30 days of staking is 6.03%, increasing to 12.66% after 60 days, and further to 23.29% after 90 days. This indicates that the initial phase of KlimaDAO provided substantial economic incentives for users to stake their tokens. Moving to Year 2, the median returns from staking show a noticeable decline. The 30-day return drops to 1.45%, the 60-day return to 2.75%, and the 90-day return to 4.19%. Although the returns are still positive, the decrease compared to Year one suggests reduced profitability and possibly lower market interest or token valuation stability. In Year 3, the median returns from staking become negligible, with the 30-day return at 0.01%, the 60-day return at 0.03%, and the 90-day return at 0.04%. This minimal growth indicates that the economic benefits of staking have drastically reduced, reflecting a mature market phase where the initial high returns have stabilized and plateaued. This pattern is typical in many staking ecosystems where early adopters benefit the most, and returns stabilize as the platform matures.

Table 3. Median economic performance of Staked vs. Unstaked tokens over different time periods (30, 60, and 90 Days) during the first 3 years of KlimaDAO’s activity.

3.4 Participation and adoption

Understanding the participation and adoption trends within KlimaDAO is crucial to evaluating the project’s impact and growth. The KlimaDAO community, known as “Klimates,” includes all holders of any type of KLIMA token, whether staked or not.

Figure 8 shows the monthly variation in the number of KLIMA participants, divided into three categories: Community Members (klimates), sKLIMA Holders and KLIMA Holders. Again, during the initial period from October 2021 to February 2022, there is a significant number of new participants, especially in November and December 2021. This high level of activity is likely to correspond to the launch period or initial promotion of the platform, attracting a large number of new users and generating significant interest. From March 2022 onwards, there is a noticeable decline in the number of new participants in all categories. However, there are occasional spikes, such as in November 2022 and December 2022, suggesting temporary spikes in interest or specific events that led to a spike in new participants. Despite these spikes, the overall trend shows a decrease in user engagement over time. In the final period, from January 2023 to May 2024, the number of new participants stabilises at a much lower level than in the early months. The bars are consistently shorter, indicating a steady but minimal increase in new users. The presence of black bars (KLIMA Holders) shows that some activity continues, but at a much lower level compared to the early period. This stabilisation suggests that the platform has settled into a phase of lower, more consistent user growth, possibly relying on a core group of users rather than attracting large numbers of new participants.

Figure 8. Combination chart showing the monthly variation and total participants within KlimaDAO. The bar chart represents the monthly variation in community members (klimates), sKLIMA holders, and KLIMA holders. The line chart shows the total number of community members (klimates), total sKLIMA holders, and total KLIMA holders over the same period.

It is important to clarify that the number of ‘klimates’ presented in Figure 8 is derived from addresses with a positive balance of KLIMA tokens. The query employed24 excludes wallets with zero balances, as we only consider addresses that hold a positive amount of KLIMA or sKLIMA at any given time. This approach differs from traditional definitions of users that may include inactive wallets or those with negligible balances. As a result, the graph shows a generally increasing number of users, representing only those wallets with a non-zero balance. However, there are occasional slight decreases in the number of users, reflecting periods where a small number of wallets no longer hold a positive balance. Despite these fluctuations, the overall trend remains upward, indicating the persistence of positive balances over time.

Additionally, three lines representing cumulative total community members (solid blue line with circular markers), total KLIMA holders (solid black with square markers), and total sKLIMA holders (solid light blue line with triangular markers) are shown in Figure 8. Overall, all three lines show the growth of their respective metrics during two specific time periods, the launch of KlimaDAIO and the last quarter of 2022.

Figure 8 depicts the typical lifecycle of interest and engagement with new platforms. Between October 2021 and January 2022, KlimaDAO adoption experienced rapid growth. In November 2021, the number of KLIMA holders increased from 1,669 to 3,296, representing a 97.47% increase, while sKLIMA holders grew by 118.30%, and the total klimates community increased from 19,594 to 42,562, a 117.22% rise. In December 2021, although growth rates slowed, KLIMA holders still grew by 35.85%, and sKLIMA holders by 36.04%, while the total klimates community expanded by 38.17%, reaching 58,806 users. By January 2022, growth stabilized, with a 9.90% increase in KLIMA holders and a 6.05% rise in klimates, adding around 3,555 new users during this stabilization phase.

From February to September 2022, growth was more moderate. During this period, the number of KLIMA holders increased from 5,380 to 8,678, representing a 52.66% rise over the entire period, although monthly increases were smaller, generally between 2% and 5%, adding approximately 200–300 new users per month. Meanwhile, sKLIMA holders saw slight declines in some months. However, in the last quarter of 2022 (from October 2022 to January 2023), there was a resurgence, with a total growth of 27,534 users, representing a 38.62% increase in the klimates community. From February 2023 onwards, growth was minimal, although between March and September 2023, accumulated variations reached 11.26%. From October 2023 to May 2024, variations were even smaller, with an accumulated growth of only 1.37%, reflecting a slight stagnation in the user base.

It is important to note that the actual number of unique holders may be difficult to determine due to the potential for users to hold multiple accounts. This multi-account scenario is a known issue in blockchain-based platforms and may affect the accuracy of Figure 8. Therefore, the trends observed should be interpreted with caution, acknowledging the possibility of discrepancies between the number of accounts and the actual number of distinct users.

3.5 Market concentration

Understanding market concentration within the KlimaDAO ecosystem is essential to assessing market stability, depth, liquidity, and asset distribution. A key aspect of market concentration is the management of treasury assets, which are required to the overall health and functionality of the protocol. These assets, managed by the protocol’s treasury, support the value of the KLIMA token, provide liquidity, and finance different initiatives within the KlimaDAO ecosystem.

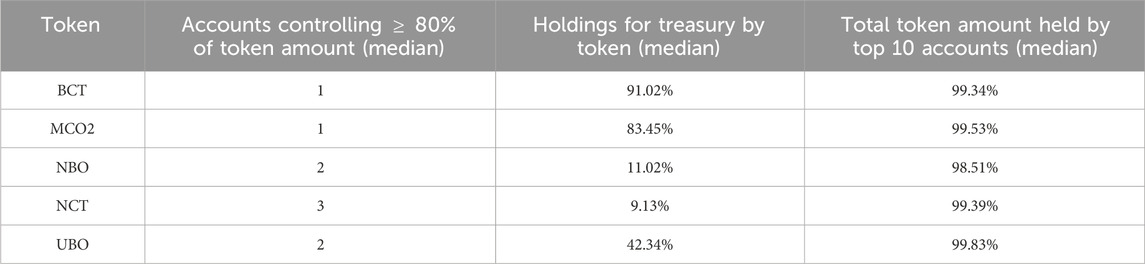

Table 4 analyzes the concentration of holdings for the five main tokens within the KlimaDAO ecosystem. The columns provide insights into the distribution of these tokens by showing the median number of accounts controlling 80% or more of the token amount, the median percentage of holdings for the treasury by token, and the median total token amount held by the top 10 accounts. For BCT, which represents 87% of the treasury as shown in Table 2, one account controls 80% or more of the token amount.

Table 4. Analysis of Token Holdings Concentration (median) from November 2021 to May 2024: The first column lists the number of accounts controlling at least 80% of the token amount; the second column presents the percentage of token holdings for the treasury; the third column indicates the total percentage of the token amount held by the top 10 accounts for various tokens. Data collected from the KlimaDAO protocol metrics subgraph.

In order to assess market concentration within the KlimaDAO ecosystem, we focus on three key metrics: (1) the number of accounts controlling 80% or more of the total token supply, (2) the percentage of tokens held by the KlimaDAO treasury, and (3) the percentage of the total token supply controlled by the top 10 accounts. These metrics provide a comprehensive view of the concentration of token ownership and asset distribution. The first metric, the number of accounts controlling 80% or more of a token, illustrates the extent to which token holdings are centralized. In the case of BCT and MCO2, for example, a single account controls 80% or more of the supply, which includes the holdings managed by the treasury. The second metric, the percentage of tokens held by the treasury, is crucial because the treasury is fundamental in supporting liquidity and backing the value of the KLIMA token. For tokens like BCT and MCO2, the treasury holds over 80% of the total supply, highlighting its significant role in the ecosystem’s financial stability. The third metric, the total amount of tokens held by the top 10 accounts, further underscores the concentration of ownership, with all top 10 accounts collectively holding nearly 100% of each token, with minor variations depending on the token type.

The treasury holds 91.02% of the BCT tokens, and the top 10 accounts collectively hold 99.34% of the total BCT tokens. Similar figures are found for MCO2, where a single account controls 80% or more of the tokens, the treasury holds 83.45%, and the top 10 accounts hold 99.53% of the tokens. Conversely, the concentration appears to be lower for NBO and NCT, with more accounts controlling the token amounts and lower percentages held by the treasury. However, the weight of these tokens in the treasury is marginal, representing only 0.27% of the total holdings, as depicted in Table 2.

This data shows that some accounts consistently hold the vast majority of each token type, highlighting the centralized nature of token ownership within the KlimaDAO ecosystem. This level of centralization is not uncommon for emerging projects, especially in their early stages, but it raises considerations for long-term sustainability and community trust. In order to increase the longevity of the project and foster positive perceptions, strategies to gradually decentralize token ownership could be beneficial. This could include broader distribution mechanisms, increased community participation, and transparent governance practices to ensure a more equitable distribution of assets over time.

3.6 Carbon credits retirements

Retirements refer to the action of permanently removing carbon credits from the market to offset a specific amount of carbon dioxide (CO2) emissions. This process ensures that the carbon emissions represented by the retired credits are effectively neutralized, contributing to the global effort to reduce carbon emissions.

Carbon offsets are compensations designed to neutralize carbon emissions. These offsets represent a specific amount of CO2 that has been avoided or removed from the atmosphere through various mitigation projects. Within the KlimaDAO ecosystem, these carbon offsets are tokenized on the blockchain, creating tokens that represent one ton of compensated CO2. These tokens can be bought, sold, and retired on the Polygon blockchain. By acquiring and retiring (burning) carbon offset tokens, users contribute to the global reduction of carbon emissions. This mechanism not only creates demand for carbon mitigation projects but also helps finance additional environmental initiatives.

It is important to clarify that in the KlimaDAO ecosystem, when carbon credits are “burned” or retired, the credits being removed are the carbon tokens themselves, such as BCT, not the KLIMA tokens. When BCT or similar carbon credits are retired, they are permanently removed from circulation to offset emissions, reducing the total supply of these carbon credits in the market. However, this process does not involve the burning of KLIMA tokens. The KLIMA tokens are not destroyed in this process; instead, they are issued or remain out of circulation, stored in the treasury as reserves. This ensures that the treasury’s backing of KLIMA tokens is maintained while the total number of carbon credits in circulation decreases. In essence, the carbon credits leave the market permanently, but the KLIMA tokens used in the transaction are retained or kept in reserve, ensuring that the protocol’s supply dynamics are not directly affected by the burning of carbon credits.

In addition to retiring carbon credits like BCT, KlimaDAO also allows users to retire KLIMA tokens through a mechanism known as retirement bonds. In this process, KLIMA tokens are exchanged for carbon credits that are immediately retired, effectively removing both the KLIMA tokens and the associated carbon credits from circulation. This process helps balance the expansion of the KLIMA supply by reducing the circulating KLIMA tokens, contributing to a deflationary effect. The dual impact of removing both KLIMA tokens and carbon credits supports KlimaDAO’s goal of sustainability while maintaining a stable token economy within the ecosystem.

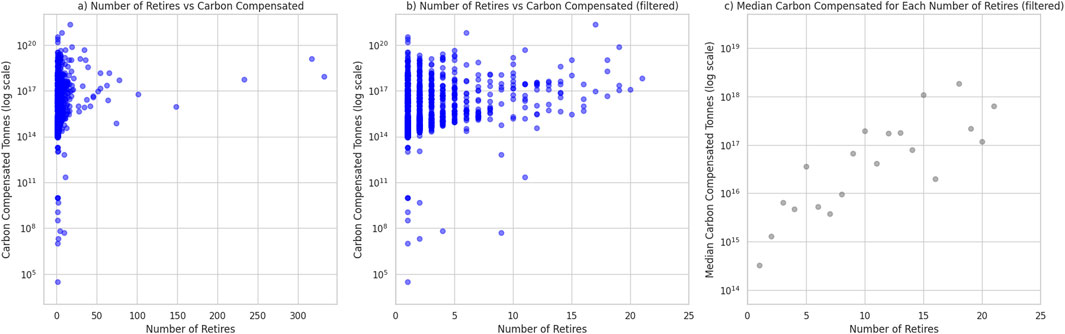

Following the above, an analysis of retirements and their impact on carbon compensation has been conducted. Figure 9 reveals the relationship between the number of retires and the total carbon compensated. Panel a plots the number of retires against the total carbon compensated using a logarithmic scale for the y-axis. The data shows a high concentration of points where the number of retires is low, indicating that most carbon compensation actions involve a smaller number of retires. As the number of retires increases, carbon compensated increase, with some instances showing exceptionally high amounts of carbon compensated. This suggests that while fewer retirements are common, larger retirements can sometimes correspond to significant carbon offsets.

Figure 9. Relationship between the number of retires per account and the carbon compensated in tonnes (log scale) is shown in Plot (A) and filtered to 25 retires, revealing a more detailed distribution in Plot (B). Plot (C) presents the median carbon compensated for each number of retires.

Focusing more closely on specific cases, Panel b of Figure 9 graph narrows the focus to cases with up to 25 retires, providing a more detailed view of this range. Like the first graph, it uses a logarithmic scale for the y-axis. This limited view reveals a dense clustering of points in the lower retire range, emphasizing that small numbers of retires dominate the dataset. The close inspection within this range highlights the consistent variability in carbon compensation even for a limited number of retires, reinforcing the idea that significant number of carbon compensation can occur at relatively low retire counts.

To further enhance our understanding, the median carbon compensated for each number of retires is examined in Panel c of Figure 9. The trend line indicates a general increase in the median carbon compensated as the number of retires grows. This pattern suggests that as entities perform more retires, the typical amount of carbon compensated tends to increase. However, the logarithmic scale indicates that this relationship is not linear and that there are substantial increases in carbon compensation with higher retire counts. This median-focused view provides a clearer picture of the central tendency in carbon compensation across different retire counts, highlighting the overall growth trend.

The graphs collectively indicate that users who retire carbon credits more than once are not consistent; that is, while a large number of users perform a single retire, fewer users engage in multiple retires. This is evidenced by the high concentration of points in the lower retire ranges across all graphs. Specifically, the steep drop-off in the number of retires as we move from left to right in each graph suggests a declining number of users who repeat the process. This trend implies that the majority of carbon retirements are performed by users who do it once, with progressively fewer users making additional retires.

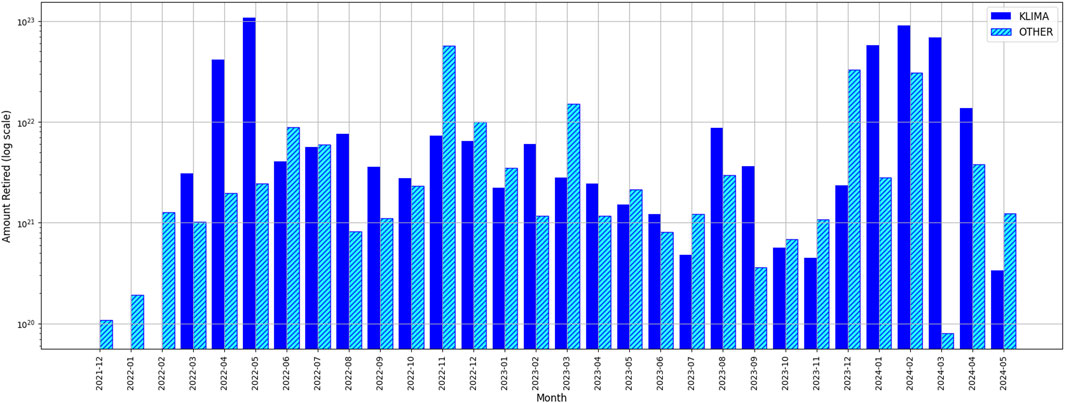

Following the analysis of the relationship between the number of retires and carbon compensation, we can delve into the monthly volume of retires to gain further insights. The volume of carbon credits retired over time is illustrated in Figure 10. This figure uses a logarithmic scale on the y-axis to capture the wide range of retire amounts. The graph distinguishes between KLIMA and other tokens, providing a comparative view of their retirement volumes. In the initial months, there is a notable increase in the volume of retires, peaking in mid-2022. This surge is primarily driven by KLIMA token retirements. The high volume of retires during this period suggests a robust engagement with carbon offsetting activities. As we move through 2022 and into early 2023, the volume of retires fluctuates but generally remains at a high level. Occasional peaks, such as in November 2022 and March 2023, indicate periods of intensified activity. These spikes may correspond to specific campaigns or increased awareness of carbon offsetting efforts. From mid-2023 onwards, the volume of retires shows a more stabilized pattern, with both KLIMA and other tokens maintaining consistent levels of activity. This stabilization suggests a mature and sustained commitment to carbon offsetting by the KlimaDAO community. The steady volume of retires in this period highlights the platform’s ability to maintain user engagement and support ongoing carbon compensation initiatives.

Figure 10. Amount of carbon retired (log scale) using KLIMA tokens vs. other tokens in KlimaDAO.

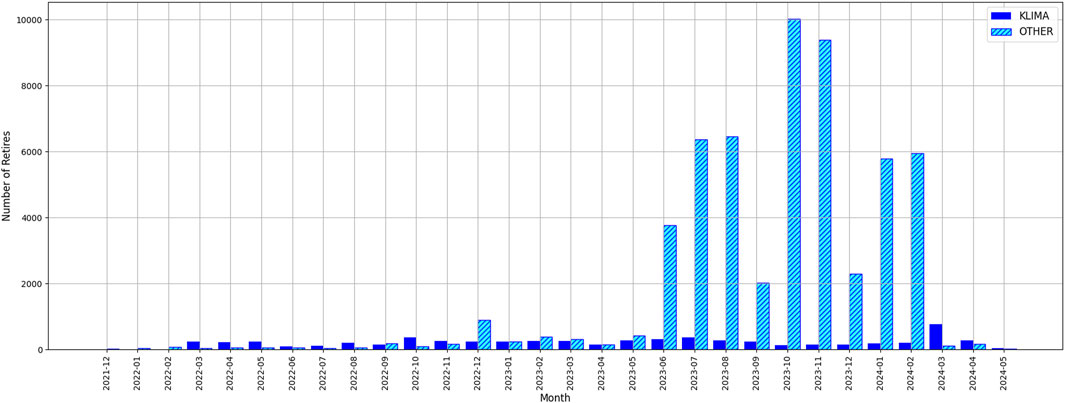

Ultimately, Figure 11 illustrate the monthly number of retirements within KlimaDAO, revealing notable trends in user engagement and the dynamics of carbon credit retirements. Initially, retirements using KLIMA tokens were predominant. This surge indicates robust initial engagement with KLIMA token retirements y the lack of alternatives using other token types. However, as we progress towards the latter part of the graph, from early 2023 onwards, we observe a notable shift. The number of retirements using other tokens begins to surpass those using KLIMA, highlighting a diversification in the types of tokens utilized for retirements. This transition suggests a broadening of the platform’s adoption toward a wider array of tokens. The overall pattern demonstrates periodic fluctuations with peaks indicating episodes of increased activity. Despite the decline in KLIMA retirements, the enduring presence of other tokens by the end of the period suggests a matured and diversified engagement within the KlimaDAO community, illustrating its capability to sustain interest in various carbon compensation initiatives.

Figure 11. Number of retires per month within KlimaDAO.

This shift in token utilization for retirements within KlimaDAO is analogous to broader trends observed in platform adoption and stakeholder engagement. Over time, there has been a noticeable decrease in the influx of new users, stabilizing into a core base of participants who demonstrate sustained interest in the protocol’s objectives. Similarly, this pattern mirrors developments in staking activities, where there has been a discernible decline. Such a trend might suggest that users’ interest is shifting from purely investment-driven motives towards a more intrinsic alignment with the protocol’s operational uses and environmental goals. This evolution in user behaviour emphasizes a maturation within the KlimaDAO users, indicating a deepening commitment to the protocol’s underlying principles rather than transient financial benefits.

4 Conclusion and outlook

KlimaDAO showcases the potential of DAOs to innovate organizational structures, playing a crucial role in building trust within VCMs Adams et al. (2021), Slavin and Werbach (2022). However, the challenge lies in translating this potential into tangible impact. The future of tokenized carbon markets is promising, offering efficient, transparent, and accessible trading mechanisms. Standardization will be essential to ensure interoperability and trust among participants. Additionally, the establishment of regulatory frameworks is expected to provide legitimacy, enhance transparency, and ensure the quality and environmental impact of these markets. Integrating tokenized carbon credits with DeFi protocols will generate new demand and foster broader engagement with environmental initiatives.

High-integrity carbon credit projects within the KlimaDAO ecosystem contribute significantly to broader Sustainable Development Goals, including biodiversity conservation and ecosystem services. To ensure that these projects are effective and climate-resilient, both public and private oversight is essential. This oversight should align with nature conservation targets and promote climate resilience. In addition, more evidence on the social impacts and community engagement of these projects is needed, with a focus on improving access for disadvantaged groups such as tenant farmers.

The economic analysis of KlimaDAO reveals a complex dynamic regarding prices and market concentration. Initially, KlimaDAO issued tokens at a much higher price. This issuance is part of the protocol’s mechanism to build liquidity through bonds, encouraging user investments. However, the platform also incorporates deflationary aspects through staking, which plays a crucial role in stabilizing the token’s value over time. Staking allows users to earn additional KLIMA tokens, effectively removing them from circulation and creating deflationary pressure.

Regarding staking, there is an evident loss of interest from users, as the number and volume of transactions have decreased over time, except for occasional spikes. Furthermore, fewer new users are participating in staking, leaving mainly those who have been involved with the protocol for a longer time. In terms of returns, staking has ceased to be profitable from the second year onward, with KLIMA token yields stabilizing. This indicates a reduced interest from users in obtaining economic returns through staking on the platform.

In terms of retirements, as the number of retirements increases, the number of users involved decreases, suggesting that compensation actions are not recurrent but rather sporadic in most cases. However, despite the infrequent compensations, the volume is often significant. Currently, aside from occasional peaks, there is a stabilization in carbon compensations. When linked with the declining interest in staking, we can conclude that the protocol is reaching a maturity stage where speculative interest wanes, and the focus shifts to its intended purpose.

Participation and adoption show that user activity has stabilized, including those who stake and hold KLIMA tokens. This result is in line with the results of the dynamic general equilibrium model of token pricing and platform adoption of Cong et al. (2021). This suggests that the protocol retains users genuinely interested in carbon compensations rather than speculation. This stabilization is reflected in a lower monthly variation and a decrease in the number of new users, indicating that the protocol is no longer novel but well-known, retaining users with a genuine interest.

Finally, the low participation and focus on core users have resulted in a high concentration of tokens in a few accounts. The structure of KlimaDAO involves issuing KLIMA tokens in exchange for carbon credits, which are then held in the treasury. This centralization is partly due to the continuous issuance of tokens by KlimaDAO, often controlled by the protocol itself. This situation reinforces the idea that the protocol has matured, focusing on its primary goal of carbon compensations. As a result, KlimaDAO has managed to maintain a loyal user base while reducing speculative interest. The transition from high initial participation to a more stable and concentrated user base reflects the protocol’s shift towards long-term sustainability and its commitment to environmental objectives.

As KlimaDAO continues to evolve, the establishment of a robust monitoring, reporting, and verification framework will be crucial for the credibility and success of future carbon credit transactions. Looking forward, further advances in these areas, alongside ongoing collaborative efforts within the KlimaDAO community, hold the potential to transform climate action and sustainability initiatives significantly. This proactive approach is expected to create unprecedented value, drive positive environmental outcomes, and contribute to a more sustainable and equitable future. The continued development and implementation of high-integrity carbon projects are essential for KlimaDAO to achieve its environmental and social objectives, ultimately making a significant impact on global climate goals. Through these initiatives, KlimaDAO not only aims to enhance its own ecosystem but also to set a benchmark for other climate action projects worldwide, emphasizing the importance of innovation and community engagement in shaping the future of environmental sustainability.

It is also essential to increase the involvement of different actors in the ecosystem, including institutional investors, policymakers, and other key stakeholders, to contribute to a more vibrant and dynamic market. Simultaneously, it is crucial to strengthen the foundational aspects of the klimaDAO protocol. By establishing a solid foundation based on reliable and transparent fundamentals, KlimaDAO can foster a more stable and trustworthy market environment. This approach will not only enhance market participation but also ensure the integrity and effectiveness of the carbon market as a whole.

However, there is a significant risk that voluntary carbon markets could hinder progress towards net zero and negatively impact other climate priorities. While these markets are expanding and high-integrity carbon credits can significantly support the transition to net zero, it is critical that stronger guidance, regulation, and standards are put in place. This will prevent carbon credits from being used as substitutes for direct emission reductions and increase the integrity and transparency of the carbon market.

Initiatives related to the tokenisation of carbon credits have demonstrated the technical feasibility of the approach of transferring the existing practices for the curation of those credits in centralised registries. The analysis of the evolution of KlimaDAO evidence that these assets can then be combined in various ways resulting in aggregations as carbon pools that can incorporate different qualities or preferences about the underlying projects or initiatives and their diversity in quality and/or environmental impact. This is demonstrated by the fact that the same mechanisms in KlimaDAO have been used to bring on-chain different tokens with different patterns of demand. In addition, initiatives as KlimaDAO have also demonstrated that tokenomics are applicable to tokenized carbon credits using well known mechanisms already tested and used in DeFi, as, for example, staking, bonding, or the use of pools in decentralised liquidity providers, which is also a realisation of the composable approach in DeFi. These combine in KlimaDAO with the main outcome of carbon credit retirement, so that all the DeFi mechanisms implemented are aimed at contributing to expanding carbon credit markets by incentivizing token holders.

However, the adoption of decentralised carbon markets depends on a number of different factors. On one hand, there are external factors that affect adoption but are not related to the protocols themselves. Notably, in voluntary carbon markets, the control of the quality of the projects that constitute the emission reductions is subject to controversy, and KlimaDAO will be affected positively or negatively by the increase or decrease in availability of those validated projects and by the perception of users about them. The second external factor is the unstable and volatile status of cryptocurrency markets overall, that affect the user base and liquidity. It is well known that the price and volume of transactions in Bitcoin is a reflection of cycles in cryptocurrency markets, and this is also a factor for on-chain carbon markets. Among the internal factors, which are the ones that depend on the protocols themselves, governance and tokenomics are the two most important factors. In the case of KlimaDAO, governance procedures are similar to those in the frameworks that can be found in many other DeFi projects. That governance is fundamentally realised by an online (but off-chain) community discussion in which improvement proposals (KIPs) can be discussed in online forums, and then voted on-chain by token holders. The governance framework is also changed using this same mechanism, and is, as any other similar governance structure, subject to problems of concentration of tokens. Actually, this led to a trial and subsequent vote for use of a quadratic voting scheme (KIP-40R), that reflects the capacity of the DAO to deliberate for an eventual change in governance processes. The detailed analysis of the actual history of governance changes can be traced in KlimaDAO, but it is out of the scope of our current research.

Regarding tokenomics, KlimaDAO, the approach of KlimaDAO having a treasury that has combined bonding and staking appears to be a sustainable strategy to promote liquidity for the protocol. Treasury levels can be adjusted in the protocol to account for increased demand for retirement. Since the ultimate goal of these protocols is incentivize voluntary retirements by companies or individuals (e.g., to achieve zero emission policies), the success of the protocol entails higher demand for retirement, since this in turn will result in increased environmental impact. The mechanisms inside the treasury account for changes in that demand, preserve a minimum value for carbon credits, and can be adjusted to incentivize some level of treasury reserves for DeFi users. Future research may address how changes in the actual formulation of these mechanisms may affect liquidity, but the data currently available is not sufficient for simulations especially since it is very difficult to separate the influence of the external factors mentioned above.

Data availability statement

The original contributions presented in the study are included in the article/Supplementary Material, further inquiries can be directed to the corresponding author.

Author contributions

AB-R: Conceptualization, Data curation, Formal Analysis, Investigation, Methodology, Project administration, Resources, Software, Supervision, Validation, Visualization, Writing–original draft, Writing–review and editing. JD-L: Conceptualization, Data curation, Formal Analysis, Investigation, Methodology, Project administration, Resources, Software, Supervision, Validation, Visualization, Writing–original draft, Writing–review and editing. M-AS: Conceptualization, Data curation, Formal Analysis, Investigation, Methodology, Project administration, Resources, Software, Supervision, Validation, Visualization, Writing–original draft, Writing–review and editing.

Funding

The author(s) declare that financial support was received for the research, authorship, and/or publication of this article. D-LJ acknowledge financial support from Comunidad de Madrid and UAH (ref: EPU-INV/2020/006).

Conflict of interest

The authors declare that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

Publisher’s note

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Footnotes

1Carbon credits empower a financial exchange where one entity buys credits to claim an emissions reduction, while another entity sells these credits to finance actions that achieve that reduction. Buyers use carbon credits to enhance their climate credentials, demonstrating a commitment to sustainability. Sellers, on the other hand, use the proceeds from these sales to implement measures that actively reduce emissions, such as investing in renewable energy projects or reforestation efforts. This system not only incentivizes emission reductions but also channels funds into projects that contribute to environmental sustainability.

2Gold Standard is a certification body established by the World Wildlife Fund (WWF) and other non-governmental organizations (NGOs) to ensure that projects reducing carbon emissions also contribute to sustainable development. It sets rigorous standards for climate and development interventions, ensuring that projects deliver verified emissions reductions and broader benefits to local communities and ecosystems.

3Verra is a non-profit organization that develops and manages standards for climate action and sustainable development. It is best known for its VCS, which is the world’s most widely used voluntary GHG program. The VCS program certifies carbon emission reduction projects to ensure they meet high-quality criteria.

4https://www.regen.network/- Decentralised environmental asset tokenization platform.

5https://toucan.earth/- Infrastructure for carbon credit tokenization.

6https://www.flowcarbon.com/- Carbon markets platform moving towards decentralisation.

7https://www.carbonable.io/- Project focused on decentralised carbon credit tokenization.

8https://www.openforestprotocol.org/- Blockchain-based forest carbon tracking platform.

9https://climatecollective.org/- Environmental initiative within the Celo ecosystem.

10https://nori.com/- Carbon credit tokenization platform without decentralised governance.

11OlympusDAO is a decentralized autonomous organization focused on creating a decentralized reserve currency called OHM, backed by a basket of assets including stablecoins. The protocol utilizes bonding and staking mechanisms to manage its treasury and regulate the supply of OHM, aiming to achieve price stability and growth. https://www.olympusdao.finance

12KlimaDAO utilizes the Snapshot platform for governance proposals and voting: https://snapshot.org/\#/klimadao.eth. Snapshot is a decentralized voting system commonly used by DAOs, where users can vote on proposals without incurring gas fees. The platform records votes off-chain, employing the on-chain balance of tokens in users’ wallets to determine voting power, making governance more efficient and accessible.