95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

ORIGINAL RESEARCH article

Front. Blockchain , 09 March 2023

Sec. Blockchain Technologies

Volume 6 - 2023 | https://doi.org/10.3389/fbloc.2023.972183

This article is part of the Research Topic Insights in Blockchain Technologies: 2022 View all 4 articles

Christos A. Makridis1,2,3*

Christos A. Makridis1,2,3* Gordon Y. Liao4

Gordon Y. Liao4There is a large body of empirical and theoretical literature on the effects of technological change on individuals, labor markets, and overall economic activity. Theories of skill-biased technical change (SBTC) suggest that technology increases the earnings power of skilled workers, but substitutes for less skilled workers. Distributed ledger technologies (DLTs) provide a new context for examining and understanding the impact of technology change on labor, competition, and economic outcomes. This paper explores the theoretical frameworks through which DLTs could enhance economic mobility and provides examples from several areas, including: i) the creation of new jobs and higher value-added jobs, and the modularization of complex tasks; ii) improvements in the way people learn and acquire human capital; iii) increased competition in the marketplace; and iv) more inclusive access to financial services with fewer intermediaries.

Economists have long recognized that technological change is the primary catalyst for sustained economic growth (Hansen and Prescott, 2002). However, it is less clear whether the benefits of technological change are widely shared among all members of society. Some theories, such as skill-biased technical change (SBTC)1, argue that technological change disproportionately benefits skilled workers (Katz and Murphy, 1992), while others suggest that the gains of innovation eventually trickle down to low-skilled workers and communities (Hornbeck and Moretti, 2022).

The recent emergence of distributed ledger technologies (DLTs) has sparked a new conversation about the effects of technological change on economic mobility. Unlike previous technological revolutions, such as the internet and social media, which rely on centralization to achieve network and scale effects, DLTs often rely on decentralization to function.2 This decentralized model allows for economic activity to occur among individuals who may not trust each other, but who are brought together by the governance of the blockchain. The concept of Web3, a decentralized version of the internet powered by blockchain and token-based incentives, also challenges the notion that innovation must be accompanied by traditional economic rent to reward the costs of research and development—other forms of non-pecuniary remuneration are also effective. DLTs present a new way of thinking about the relationship between technological change and economic mobility, as decentralization challenges the traditional incentives for innovation.

The emergence of blockchain technology and programmable money has occurred at a crucial juncture in history, as income inequality has begun to worsen after a period of improvement (Piketty and Saez, 2003) and inflation has risen, ending a prolonged period of price stability (Powell, 2022). There has also been a decline in labor market dynamism and a degradation of competition in the market.3 DLTs have the potential to improve competition and promote more inclusive economic growth. In addition, DLTs are enabling the creation of a financial infrastructure that is native to the internet, which has the potential to benefit billions of individuals around the world who are currently underserved by traditional financial service providers.

While there is limited data available to study the causal relationship between DLTs and economic mobility, economic theory can still provide a useful framework for understanding the potential mechanisms through which DLTs may enhance economic mobility. The primary objective of this paper is to establish a theoretical framework for examining the possible ways in which DLTs could impact economic mobility. This paper focuses on four potential channels and provides examples in the areas of finance, education, and media/entertainment to illustrate how DLTs may have the ability to improve economic mobility. Specifically, the study outlines the following channels through which DLTs may potentially improve economic mobility.

• Employment and Wages: DLTs have the potential to create new employment opportunities by altering the distribution of tasks that are valued in the labor market. According to the task-based approach outlined by Autor (2013), jobs are composed of a collection of tasks, and technological change can modify the set of tasks that are in demand and create entirely new types of jobs. Additionally, if DLTs are able to modularize complex tasks effectively and efficiently, it could reduce coordination costs and create new employment opportunities.

• Human Capital Accumulation: Since the work of Spence (1978), economists have recognized that educational attainment serves as a valuable signal to employers, in addition to providing individuals with new skills. Blockchain technology, particularly through the emergence of programmable verifiable credentials, can offer more accurate and precise signals of an individual’s skills and core competencies because these signals, which are recorded on public ledgers, can be highly customized (compared to traditional degree programs or even individual classes) and are authenticated. The emergence of on-chain credentials and skill verifications allows individuals to have greater control over their own data and enables them to move between different educational institutions more easily.

• Information Asymmetry and Competition: Economists have observed a decline in competition over the past few decades (Autor et al., 2020; De Loecker et al., 2020). One factor that has contributed to this decline is the existence of scale economies, which make it difficult for smaller firms to compete with larger ones. DLTs, however, can improve the enforceability of contracts and deliver transparency, thereby allowing more disaggregation of scale economies and more companies to differentiate themselves in the marketplace. Additionally, DLTs enable content creators, including artists, to receive compensation for their work without having to rely on a central intermediary, reducing information asymmetry and increasing competition in the market.

• Financial Inclusion: Despite recent improvements in banking access, there are still significant portions of the global population that remain unbanked or underbanked. In emerging economies, DLTs have the potential to greatly increase financial inclusion by providing everyday payment, saving, and lending services, as well as facilitating business finance operations and enhancing North-to-South capital flows. DLTs not only have the ability to provide financial services without intermediaries, but they can also be used by traditional financial institutions to reduce operational complexity and associated risks. In addition, representations of exclusive digital value, such as non-fungible tokens (NFTs), have the potential to create new market opportunities for skilled individuals who previously did not have access to them. This expansion of market opportunities could further contribute to increased financial inclusion, as it allows more individuals to participate in the economy and access financial services.

The objective of this paper is not to conduct a detailed empirical analysis, but rather to present conceptual frameworks for understanding the impact of DLTs on economic mobility. It is important to have a clear understanding of the potential ways that DLTs can affect the economy because it can inform policymakers on how to establish a regulatory framework that both empowers innovators and protects against negative consequences. This balanced approach is necessary in order to promote the positive effects of DLTs on economic mobility while also mitigating any negative impacts.4

A large literature on economic mobility in recent years has honed in on factors related to intergenerational mobility across times series and geographies. Several conclusions from this literature are helpful for understanding how technology may interact with mobility.

First, historical measures constructed using administrative data suggest that intergenerational economic mobility has not improved since the 1970s (Chetty et al., 2014a). Related to economic mobility, income inequality worsened during this time period (Piketty and Saez, 2003). Researchers and policymakers alike are actively looking for ways to promote greater mobility, often by promoting social capital. Second, large geographical variations exist in economic mobility, linked to segregation, differences in school quality, and social capital (Chetty et al., 2014b). Third, this lack of progress in economic mobility and inequity occurred during a period of substantial growth in financial services, with the finance sector expanding from 4.9% of GDP in 1980% to 7.9% of GDP in 2007 (Greenwood and Scharfstein, 2013).

The relation between continued financial sector growth and increasing inequality may possibly be related to the capturing of financial regulations that benefited few elites while socializing the risks to the broader public (Claessens and Perotti, 2007). The deregulation of the Savings and Loan industry in the 1980s and the repeal of Glass-Steagall in the late 1990s appropriately fits this regulatory capture framework that might have contributed to financial crises and subsequent bailouts by the public sector. The need to incorporate social and political factors that intertwines with economics in explaining pervasive inequality has also led to multifaceted approaches with focus on entangled political economy (Novak, 2018).

Innovations in blockchain and decentralized finance (DeFi) have the potential to improve several of the factors identified in the literature relating to economic mobility. In particular, the transparency and inclusiveness afforded by blockchain innovations can impart direct progress in reducing discrimination, increasing educational attainment and equality in employment, access to financial services for the underbanked, and increasing rule-based accountability that strengthens financial stability. These aspects of blockchain innovation are discussed in-depth in Section 4.

A small strand of literature is also emerging predicated on understanding the impact of blockchain, which touches on economic mobility. Conley (2019) discusses potential reasons that blockchain could be helpful, focusing on its ability to lower costs (e.g., avoid brick and mortar infrastructure or operate with lower labor intensity), the ease of setting up a digital wallet, and the security to transact with less discrimination based on observable personal attributes. Davidson et al. (2018) also explore how blockchain functions as an “institutional technology”—that is, an advance that not only changes the productivity of given factors of production, but shifts the entire governance structure that allocates the factors of production (i.e., coordinating activities).

While Davidson et al. (2018) do not make claims about the effects of blockchain on mobility, the presence of decentralization and fundamental shifts in coordination are likely to have profoundly positive effects. Building on top of Davidson et al. (2018), Allen et al. (2019) apply the “institutional technology” framework to supply chains and conclude that economic power is shifted in favor of primary producers. Similarly, Utile et al. (2020) explain how new sources of employment could arise, including for workers, including the need to validate, adjudicate, and moderate content creation5.

Relative to the existing literature on economic mobility and technology change, this study focuses on the potential impact on economic mobility in the unique context of a general purpose technology that is based on the concepts of decentralization of governance, ownership, and intermediation. This context is distinguished from other technology changes that typically accrue market power to the innovators and reward workers that can adapt to the technology by developing new complementary skills. This contextual difference allows an examination of existing theories of skill-biased technology change in a new setting, much like recent work that has examined the artificial intelligence as a general purpose technology and its impact on new task formation (Frank et al., 2019; Brynjolfsson et al., 2021).

Crucial to these aims is that blockchain applications are decentralized at the transaction level (Zhang et al., 2022). Cong et al. (2022) suggests that the use of airdrops—or the transfer of tokens, often with governance capabilities—has a democratizing effect on participation, drawing on the OmiseGo airdrop on the Ethereum blockchain. Furthermore, Makridis et al. (2023) show that the use of airdrops and governance tokens by decentralized exchanges have had positive effects on the number and value of trades on the exchanges. Understanding the frameworks and channels through which DLTs can affect economic mobility also has wide ranging implications on public policy, especially the regulatory discussions that have focused on consumer welfare.

While real-world use cases of DLTs still need further innovation and regulatory clarity before they can be adopted by the mainstream and become normalized for the average household, the ownership of digital assets offers some limited insights into the adoption readiness of DLTs. As of February 2022, it is estimated that there are 221 million digital wallets (Statista, 2021). While these users still constitute a narrow portion of the population, ownership of digital assets continues to grow each year.

More recent survey evidence shows the increasing acceptance of digital assets. For example, survey by Morning Consult (2022) found that 24% of United States adults own some form of cryptocurrency as of December 2021, up from 22% in July 2021. For perspective, that compares with 23% who report having a certificate of deposit and 31% who report having a brokerage account among at least one person in the household. Not surprisingly, that amount is even higher in more unstable countries, like Argentina, where nearly 50% of respondents reported holding cryptocurrency as of December 2021. Millennials and higher income earners are especially likely to hold cryptocurrency at rates of 47% and 41%, respectively.

The Morning Consult survey also shows that the digital asset ownerships are possibly diverse: 30% of crypto ownership is among females, 39% among those earning under $50,000, and 36% among those earning $50,000–99,000. Furthermore, 62% are White, but it is important to take into account that 69% of the United States population is White. Indeed, 8% of crypto owners are Black and 24% are Hispanic even though the corresponding shares in the United States are roughly 10% and 16%, respectively.

Consistent with these adoption patterns is 2021 survey evidence from Gallup (Saad, 2021), finding that 6% of the United States population owns Bitcoin, up from 2% in 2018, demonstrating the rapid growth. Furthermore, 13% of those under the age of 50 own Bitcoin. That rate is a large underestimate of overall crypto owners given that Bitcoin is only one of many digital assets.

Data on non-fungible tokens (NFTs) reveal similar trends to that of crypto, demonstrating the diversity in the sphere. Men and women aged 18–34 own NFTs fairly equally, with 24% and 21% ownership respectively (Statista, 2022b). Heterogeneity extends to income as well, with those earning under $25,000 annually investing in NFTs at similar rates to those earning over $150,000 annually. Furthermore, survey research by the Holmgren et al. (2021) suggests similar estimates with 16% of Americans saying they have “ever invested in, traded, or used cryptocurrency.” These results are concentrated among males between ages 18–29 with a rate of 43% ever invested in, traded, or used. Rates among Whites, Blacks, Hispanics, and Asians are fairly similar with Whites holding the least (13% versus 18% among Blacks, 21% among Hispanics, and 23% among Asians).

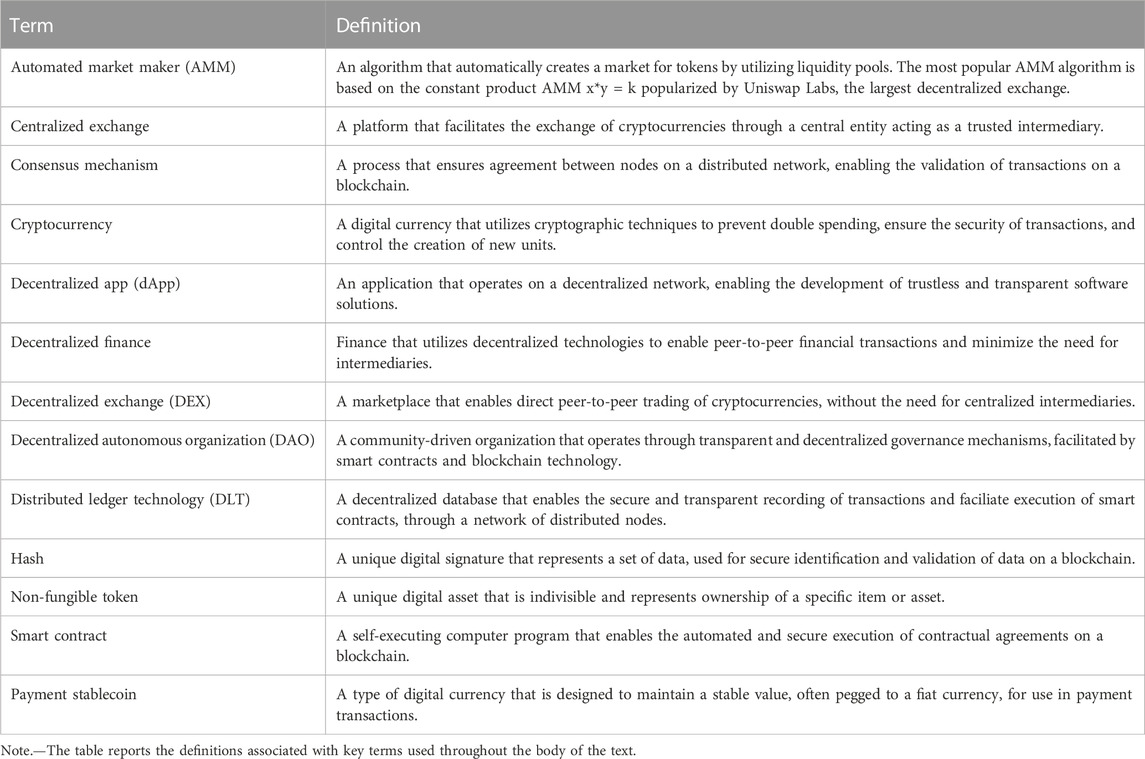

An important caveat to these observations is that the adoption of DLTs does not predicate on the holding of digital assets. In fact, one often discussed path to adoption involves companies relying on DLTs as the backend and providing front-end interface to users who might not know they are utilizing technologies powered by blockchain6. Therefore, the statistics on digital asset holdings provide a lower bound on the adoption potential of DLTs. See Table 1 with a summary of some background terms that will surface in the text that follows.

TABLE 1. Definitions for key terms.

This section establishes a theoretical framework for considering the potential effects of DLTs on economic mobility. The canonical model of skill-biased technical change (SBTC) models posits that production is a function of low and high skilled labor that are influenced by different processes of technological change in the economy (Katz and Murphy, 1992). Specifically:

where output,

In addition to changing the elasticity of substitution between skilled and unskilled workers - for example, if DLTs lead to new methods of increasing human capital accumulation - DLTs also have the potential to transform the entire production function. For example, the ability to modularize complex tasks and distribute work among people who may not interact with each other and live in different geographic locations fundamentally changes the labor inputs in the production function.

More generally, the standard labor model omits a wide array of factors, perhaps most importantly: principal-agent problems and contracting. Of note, the advent of blockchain technology that came with the cryptographic proofs and programmability of smart contracts are blurring the boundaries of incomplete contracts theory (Grossman and Hart, 1986; Hart and More, 1990).

A large part of economics has been devoted to the study of principal-agent problems in which information asymmetry constrains the ability to obtain first-best outcomes. These information asymmetry problems are so large that even in presence of commonly observable events, absent of verifiability and enforcement by the court, contract theory models often suggest suboptimal economic outcomes. Contract theory also provides a view on the boundaries of firms (i.e., the natural size of the firm) that are set by the residual rights from incompleteness in contracting. Such frictions in contracting explains why not every firm is an individual working in a gig economy or why some firms naturally integrate downstream suppliers.

Blockchain technology provides a step forward in addressing fundamental challenges in contracting by providing transparency, verifiability, and enforceability of contracts. The verifiability of on-chain events and transactions combined with enforceability of immutable predefined logics translates into reduction of ex-ante information asymmetry and ex-post morale hazard. Lower contracting frictions lead to changes in firm boundaries, as well as finance, governance, and employment.

Below sections discuss applying the canonical labor and contract theory framework to several channels of growth in economic mobility that DLTs plausibly could encourage.

DLTs have the potential to create new employment opportunities, as well as higher value ones, through the creation of new tasks and enlarging an already growing gig economy. One strand of labor research has focused on jobs as distributions of tasks (Autor, 2013). When technology changes, it alters the price of different skills associated with the completion of different tasks. Furthermore, new jobs are created following technological change. For example, the rise of social media platforms fundamentally changed how marketing is done, creating a demand for social media marketers to interact and create content for the platforms.

The DLT revolution is having a similar impact on the labor market. Though lacking data comprehensiveness, Zhao (2018) reports data from Glassdoor that job postings for blockchain developers are one of the fastest growing areas. These jobs tend to overlap with conventional software engineering, product manager, and front-end engineering occupations. Since 2021, there has also been an explosion in the non-fungible token (NFT) market. NFT creators are often creatives who produce their content, such as art and music, on the blockchain and sell directly to consumers without going through traditional intermediaries (Kaczynski and Kominers, 2021); such opportunities hold great promise for content creators to receive remuneration for their talents as opposed to giving it away for free.

Stepwise advances have also been made in crowd-sourcing complex work. For example, Valentine et al. (2017) introduces the concept of “flash teams” that can arise rapidly to execute micro-tasks for complex work among participants who do not know or trust each other. Similarly, Vaish et al. (2017) shows how crowd-sourced strategies can bring talented people together to produce high quality research, drawing on a graph-based peer credit system. Motivated by these pioneering examples of crowd-sourced work, DLTs have the potential to help further by creating strong incentives using tokens that reward and penalize specific behaviors that are needed for task completion.

If blockchain can help decentralize and modularize work, then there is the potential for significant wage and employment growth. While occupations with tasks that require more coordination pay more, they also are associated with lower employment (Lee and Makridis, 2021). Coordinating complex work is not easy, so having fewer people on a team or contributing to a complex task is generally preferable due to such frictions. However, they show that changes in the cost of coordinating activity, potentially with artificial intelligence or decentralized matching algorithms, affect the equilibrium level of employment and wages. In sum, blockchain technologies may not only create fundamentally new jobs, but also reduce the coordination costs and contracting frictions associated with doing existing jobs—and focus peoples’ attention on higher value-added tasks. This process could lead to economic mobility since improvements in employment opportunities—both on the extensive and intensive margin—would reduce income inequalities.

Second, blockchains can promote greater human capital accumulation through public ledger verification of skills and experiences, thereby allowing people to learn new skills and upskill with fewer barriers. Since the seminal work of Spence (1978), educational attainment has been viewed as a costly signal in the job market that may not reflect the true informational content (e.g., candidate’s ability or knowledge), which leads to inefficiencies in the market. For example, the presence of a college degree does not necessarily indicate competency. Indeed, the return to a college degree has increased in less digitally intensive occupations despite continued increases in the rate of student tuition (Gallipoli and Makridis, 2018). However, the use of DLTs allows learners and institutions alike to decompose certificates that are otherwise associated with entire degree programs into a sequence of smaller and verifiable skill certifications. Decoupling skills from degrees is important given the increasing complexity and heterogeneity of work.

In addition to allowing for the decomposition of degree programs, DLTs also endow the learner with greater autonomy and ownership of their learning journey. Rather than having to rely on and pay a university registrar to certify their degree completion for another institution or employer, users can access their own digital credentials at any time and grant others access to them too. Such decentralization also has the benefit of allowing learners to interact with other web3 technologies in a more personalized way, particularly with metaverse applications that are designed to fit a learner’s individual journey in a more experiential way (Makridis, 2022a). The acquisition of new skills will raise incomes and lead to a more robust and dynamic economy.

Third, blockchain technology, as a general-purpose technology that reduces information asymmetry in contracting, can also reduce anti-competitiveness. A large empirical literature highlights the growing concentration and market power (Autor et al., 2020; De Loecker et al., 2020). The scalability of networks through Web2 platforms have created incentives for large market concentration—that is, monopoly power. By reducing the role of intermediaries and completing markets through smart contracts and tokens, competition could be greatly enriched allowing distribution of economic gains among a greater number of users rather than accruing to the platform.

Over the past two decades, a select few technology companies have grown to dominate the bulk of the internet and broader tech sector. Markups have also increased substantially since the 1980s in the United States (De Loecker et al., 2020) and abroad (Bajgar et al., 2021). Such patterns have profound implications for inequality. For example, Autor et al. (2020) find that industry sales increasingly cluster among a small number of “superstar” firms in industries in which the labor share has fallen the most substantially.

Furthermore, Bessen (2020) shows that proprietary investments among large technology companies helps account for much of the increase in industry concentration. Even though individual differences in human capital may remain the largest determinant of wages, recent firm-level evidence across public and a broader census of firms suggests a tight link between industry concentration and inequality (Barkai, 2020; Rinz, 2022).

Web3 challenges the incentives for rising concentration by embedding decentralized governance into the design of the technology infrastructure. Rather than relying on a single entity to make decisions, DLTs allow people from geographically disparate areas to come together and decide on what activity gets recorded and validated on the network, whether as a validator on a blockchain or through governance rights on a protocol. For example, Makridis et al. (2023) study the effects of airdrops and governance tokens on centralized and decentralized exchanges, finding that the decentralized exchanges that conduct airdrops or give governance capabilities to users are the ones that experience the greatest growth in market capitalization and volume. Further, Cong et al. (2022) find that the OmiseGo airdrop on the Ethereum network led to greater democratization. In this sense, DLTs do not guarantee decentralization, but they encourage it.

Fourth, decentralized finance can advance economic mobility by breaking down barriers that have prevented many people from gaining access to financial services. These services include faster payment and remittance options, as well as depository and credit services. These opportunities are particularly significant in emerging markets, where basic financial services are often lacking. Even in the United States, the Frank et al. (2019) estimates that nearly one-sixth of Americans are underbanked. Access to payment systems is also unevenly distributed, with lower income households, who often have the greatest need for fast payments, having the least access. This lack of access to financial services is evident in the high usage of cash checking services, with 70% of cash checking customers having bank accounts and the majority of checks cashed coming from these customers (Klein, 2021). DeFi has the potential to address these issues and increase financial inclusion, thereby improving economic mobility.

One common challenge faced by low-income earners and the self-employed is accessing loans from banks, insurance services from insurers, and even rental agreements from landlords (Vanderkam, 2009). This challenge has been exacerbated by the COVID-19 pandemic (Small Business Majority, 2021; Granja et al., 2022). Self-employed individuals often do not have typical employment pay stubs and have different spending patterns, which can make it difficult for them to obtain traditional financing options. DLTs have the potential to address these challenges and increase financial inclusion by providing alternative financing mechanisms for these groups.

Decentralized finance, in contrast, is open to all with transaction fees that are trending downward with each iteration of innovation. As it becomes increasingly integrated with appropriate levels of know-your-customer and anti-money-laundering controls, DeFi has the potential to achieve widespread adoption and empower households to save, secure, send, and spend (Disparte, 2021). DeFi has the potential to achieve these better outcomes for at least two reasons. First, the open access nature of DeFi allows a larger pool of potential lenders to provide credit. Unlike traditional financial institutions, which tend to be concentrated at the local level, DeFi is global by default and open to a wider range of capital, increasing the probability that options will exist for unconventional borrowers to access capital. Second, traditional finance tends to have high overhead costs, while DeFi can achieve cost savings through the automation of back-office functions such as settlement reconciliation, reporting, and record keeping, which can be passed on to users. While there are also risks associated with DeFi, such as the recent failure of FTX, many of the greatest threats such as fraud are associated with more centralized approaches that claim to be decentralized finance.

These are channels through which DLTs can improve economic mobility, as viewed through the lens of labor, education, and contract theory. The following sections will explore these ideas in more detail, beginning with a review of the applications.

The macroeconomic literature on the determinants of growth has long emphasized technological change as a major factor (Hansen and Prescott, 2002). But not all technologies are created equal. For example, general purpose technologies (GPTs) are viewed as innovations that have applications across sectors (Bresnahan and Trajtenberg, 1995). Such technologies can have profound effects on productivity and human flourishing, although they might not be immediately recognizable in national statistics because they function as complementary investments (Brynjolfsson et al., 2021).

The following section discusses specific applications of DLTs that are likely to have substantial ramifications on economic mobility through the lens of three sectoral case studies.

Decentralized finance provides the ability for anyone across the globe with a mobile device to access basic financial services. Several exemplary use cases are highlighted below.

The global average cost of remittance remains at around 6% in 2022 and remittances through banks remain the most expensive with an average cost of over 10%. More troubling than the average, 18% of the corridors have remittance costs over 15 percent (Coinbase Volume, 2022). These high remittance costs, far exceeding the United Nations Sustainable Development Goals of 3% by 2030, are a drag coefficient on global economic mobility.

One of the challenges in the remittance industry is the “last mile” problem, which refers to the difficulty of delivering funds to their final destination. DLTs, by allowing for device-centric exchange of value through public distributed ledgers, can eliminate multiple layers of intermediaries between senders and receivers. Payment stablecoins, such as USD Coin, which are fully backed by high-quality fiat cash-equivalent assets, combined with on-chain decentralized exchanges such as the Uniswap protocol, already provide end-to-end currency exchange and near-instantaneous settlement of funds in some major currency corridors, such as between the dollar and the euro. Furthermore, the economic value of these foreign exchange services can be captured by remittance users, who can also use their holdings to participate in decentralized exchanges for automated market making. This can provide additional income streams for individuals and increase financial inclusion.

According to the World Bank, approximately 25% of the global population lacks any kind of financial accounts, and half of adults in developing economies do not have access to extra funds within 30 days7 This demonstrates a significant need for more inclusive saving and lending services. Intermediation platforms enabled by smart contracts, such as AAVE and Compound, have been a key part of decentralized finance and have mostly provided loans that are overcollateralized with digital assets. These platforms have demonstrated resilience through various market conditions due to mechanisms for real-time liquidation that limit risk exposure for lenders. There have also been some early successes in credit-based lending (under-collateralized lending), with projects such as Goldfinch targeting emerging markets to address challenges in credit access. Decentralized identity services, such as those offered by Verite, have the potential to on-board billions of people around the world who currently do not have access to credit. Overall, these developments in DeFi have the potential to greatly increase financial inclusion and improve economic mobility.

Land deeds are notoriously complex and prone to errors, and DLTs have the potential to more effectively manage digital registries of land records. These registries can also provide greater clarity and predictability in areas with less stable governments. Digital land rights present an opportunity for economic development and women’s empowerment. In fact, according to the 2020 Prindex Global Comparative Report, “roughly half of women in sub-Saharan Africa feel insecure about their land and property when faced with the prospect of widowhood or divorce,” and 24% of those between 18–24 also felt insecure about their property rights.8 In this context, transparency and clarity around land ownership can function as a catalyst for investment and economic mobility. While digital land rights are not a complete solution, as enforcement is also necessary, improved measurement and tracking is an important step forward.

Economists have long recognized the efficiency and welfare gains of tradable permit schemes, whether for potential application over carbon or simply over particulate matter emissions and energy (Schmalensee and Stavins, 2017). One of the best examples of these was the sulfur dioxide (SO2) allowance trading program instituted by Title IV of the Clean Air Act Amendments of 1990, which allowed power plants the ability to emit allowances, or specific tonnages, of SO2, or reduce emissions if it was less costly to do so. Such schemes create incentives for facilities to reduce SO2 emissions at least cost.

Establishing an emissions trading system—whether on carbon or particulate matter—is a complex and challenging task that requires the coordination and cooperation of multiple stakeholders, including governments, businesses, and environmental organizations. One of the challenges is having a reliable and secure system to measure the lifecycle emissions of different industries. The emissions from each industry must be accurately measured in order to determine the amount of carbon credits they need to purchase, requiring the use of sophisticated technology, such as remote sensing, monitoring systems, and databases, to track and measure emissions. However, these technologies are often expensive and may not be widely available, making it difficult to implement a uniform carbon trading system across different regions.

Another challenge is the lack of standardization in the carbon market. Different countries and regions have varying regulations and policies, which can make it difficult for businesses to navigate the market and participate in carbon trading. Additionally, the lack of transparency in the market can lead to fraud and market manipulation, reducing the effectiveness of carbon trading as a tool to combat climate change.

Tokenizing emissions and credits can help overcome these challenges by providing a more secure, transparent, and accessible platform for carbon trading. Tokenizing carbon emissions, credits, and energy products involves the creation of digital tokens that represent a unit of measurement for these quantities. The use of tokens can substantially reduce the costs associated with trading allowances and verify reductions in emissions. Traditional compliance can be costly, requiring multiple measures for verification and enterprise software for trading. Tokens can facilitate exchange transparently and publicly on the blockchain, rather than a centralized system.

However, these capabilities do not substitute for the operational elements that must be in place. For example, confidence in tokenized emissions will require third-party audits that ensure companies who issue the tokens are legitimately making physical changes in their operations. Fortunately, much of the oversight can be automated through the use of standards, but the more challenging element will involve building an audit trail on the life cycle of emissions involving activities outside of the company. For example, if a company uses an input that is more emissions-intensive, then there must be an audit trail connecting that input to the final good and service.

Tokens can also be used to build financial products around real world energy assets, such as coal and natural gas, thereby allowing institutions to trade the rights and services associated with these assets. For example, oil in a refinery could be tokenized based on the expected discounted future cash flow that it would deliver, and that token could be traded and securitized. Although energy ETFs already exist, tokenizing real world assets puts them on the blockchain for greater transparency and ease of transaction. Non-etheless, there are regulatory considerations with tokenized real world assets since it converts the asset into more of a security, which comes with new regulation.

Additionally, these tokens can be integrated with internet-of-things (IoT) connected devices, such as smart thermostats or appliances, to enable on-chain movements of carbon intensities and offsets. This has the potential to provide greater accountability for firms and countries, particularly in helping lower income communities and countries that are often most vulnerable to climate change.

One potential use case for this technology is in the tracking and reduction of carbon emissions. By tokenizing carbon credits, companies and governments can more easily track and verify the reduction of their carbon footprint. This can be done by integrating carbon credit tokens with IoT devices, such as industrial equipment or vehicles, which can automatically track and report their carbon emissions in real-time. This information can then be used to create a transparent and verifiable record of a company or country’s efforts to reduce their carbon emissions.

In addition to providing accountability, tokenizing carbon emissions and credits can also help to unlock the value of these assets. By creating a digital representation of these quantities, it becomes easier to trade and exchange them on various marketplaces. This can provide an additional source of revenue for companies and governments that are able to reduce their carbon emissions and generate credits.

Overall, the tokenization of carbon emissions, credits, and energy products has the potential to provide greater accountability and transparency in the tracking and reduction of carbon emissions. It can also help to unlock the value of these assets and provide an additional source of revenue for companies and governments that are able to reduce their carbon footprint.

The importance of metrics such as institutional brand and degree program as indicators of job candidates’ educational attainment has been widely recognized (Hastings et al., 2014; Zimmerman, 2019). However, there is ongoing debate about the validity of these metrics in the face of rising grade inflation and a rapidly changing labor market, with some suggesting that network effects may be driving these patterns (Michelman et al., 2021). Despite these debates, it remains the case that employers and institutions often continue to place significant value on traditional markers of educational achievement. As a result, individuals who are unable to effectively demonstrate their skills and knowledge through these traditional markers may miss out on the potential benefits of education.

The higher education system is currently facing two significant issues.9 First, educational institutions often hold a monopoly over their services, meaning that once a student decides where to study, it can be costly to switch due to the difficulties of transferring credits and the time involved in doing so.10 Second, if an individual wants to continue their education at a later stage, it is often difficult to transfer credits or qualifications between institutions due to differing curricula and assessment strategies. This can lead to students having to retake classes and can create administrative barriers and delays in requesting and sharing transcripts. This can be particularly challenging for students who are seeking degrees or moving between countries, hindering economic mobility, particularly for refugees. The Organisation for Economic Co-operation and Development, OECD (2022), has recognized the need for reform in this area, noting that “the inherent global nature of blockchain technology, and need for international policy consistency to both harness the cross-border benefits and manage the risks, require countries to co-operate on blockchain governance.”

DLTs provide a way to authenticate learning records. Interoperable learning and employment records (LERs), often discussed in the context of self-sovereign identity (SSI), offer the possibility that individuals can own and control their own digital identities and data. Cryptographic advances allow individuals to collect credentials, attestations, and other discrete pieces of data and associate them with their digital identity to be shared with people or institutions when needed (OECD, 2022). While LERs do not have to be used exclusively in place of accredited degrees, they can be and can significantly simplify the process of verifying accreditation. For example, learners could store their educational information on a non-fungible token (NFT) after validating the accreditation once, and every time an employer or other institution wants to check the accreditation, they could simply scan the NFT.

Interest in LERs has been growing in recent years (Ates and Alsal, 2012; Volles, 2016; Wang and De Filippi, 2020; Grech et al., 2021). Moreover, the American Council on Education (Lemoie and Soares, 2020) articulated three themes in their review of the empirical and policy literature: personal data agency, lifelong learning, and the power of connected systems. Despite the genuine interest in the promise of LERs, the challenge has been largely around impact-driven implementation and coordination across fragmented education and employment institutions and ecosystems. Differences in technical capabilities and infrastructure influence the willingness of incumbents to adopt these more novel approaches with adherence to shared open-source protocols and standards. Moreover, as Grech et al. (2021) point out, “interoperability is rarely about technology,” recognizing that there are many behavioral factors and political and economic incentives at play.

Despite the challenges, LERs could have dramatic benefits to learners and earners over the course of their lifelong learning and employment journeys. First, learners could take their record with them to different educational institutions and pursue modular degrees across a portfolio of institutions. That would require educational institutions to compete for learners, in the same way learners currently compete to gain acceptance. These dynamic, learner-controlled LERs would also create a framework for expressing skills, knowledge, and abilities in a harmonized fashion.

Second, allowing learners to document, package and present their competencies and achievements acquired throughout their unique educational journey would position them for greater career opportunities. Consequently, a substantial positive effect on learner mobility could be realized as learners are better equipped to transition either from education to a career, or shift to better opportunities as their skills evolve. With LERs allowing for a more dynamic representation of an individual’s skills and experience, employers would be more inclined to provide pay raises and increase benefits for workers, yet another driver of career advancement and upward mobility.

Such benefits would have profound implications in the labor market. The decline in the college premium documented by Valletta (2016) is at least driven in part by the proliferation of new degrees and the rise of grade inflation. By building a more cohesive, interoperable market for educational data, learners would be empowered and employers would have access to an entirely new suite of tools hiring and vetting qualified talent, in contrast to defaulting to legacy degrees and brands.

In sum, learning experience records have the potential to shift the emphasis from institutions to individual learners, increasing the accessibility and fairness of educational opportunities. This is especially beneficial for individuals who may have dropped out of college and subsequently been confined to low-paying jobs due to their lack of credentials. By utilizing LERs, these learners can attain the necessary qualifications and find employment that aligns with their skills, preferences, and career aspirations. Overall, LERs hold promise in democratizing the quality of educational services and enabling learners to effectively engage with and learn from institutional materials.

The arts and entertainment sector contributes over $355 billion in gross domestic product (GDP) in the United States as of 2021, and a more comprehensive report by the Bureau of Economic Analysis (2017) finds that the broader categorization of arts and culture accounted for $729.6 billion in 2014, or 4.2% of GDP at the time. Despite the continued GDP growth of the sector, wages in the sector have been stagnant and many artists are self-employed, resulting in a lack of traditional benefits such as health insurance.

The slow wage growth in the arts and culture industry can be largely attributed to the expansion of large arts and culture institutions without corresponding investments in resources or support for the artists.11 This has resulted in artists often being required to relinquish their copyright to record labels, leading to a lack of intellectual property once their contracts end.

The emergence of non-fungible tokens (NFTs) has had a significant impact on the art and music industry.12 With the ability to mint NFTs and utilize social media to establish a personal brand and connect with their audience, creators have the opportunity to sell directly to fans, bypassing the traditional role of labels in building a fan base.

NFTs can also provide a significant source of income for artists through secondary transactions. Through the use of NFTs, artists are able to capture a portion of the profits made from the resale of their work in the secondary market, something that was previously not possible. This allows artists to continue to monetize their creations even after they have been sold through primary markets, providing a new revenue stream for artists.

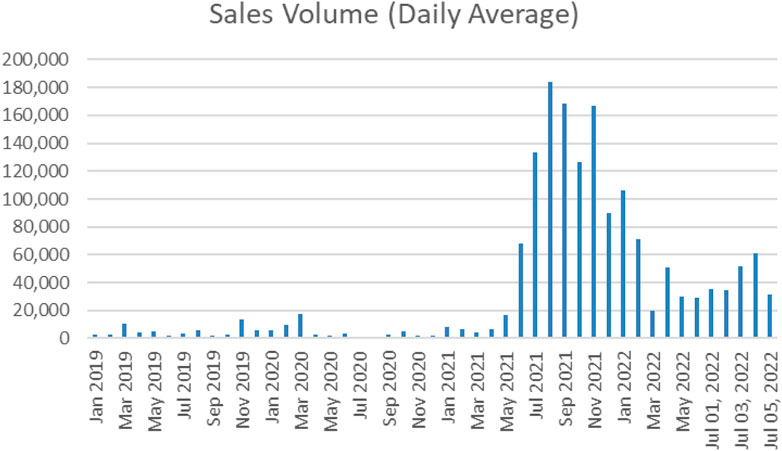

The vast majority of NFT transactions have occurred through NFT marketplaces that specialize in visual art and, occasionally, music. These marketplaces, such as OpenSea, have been instrumental in the growth and expansion of the NFT market. Figure 1 plots the number of daily average sales across months between 2019 and July 2022, documenting a substantial increase particularly in 2021. Roughly over half of these sales are through the secondary market—that is, after the initial NFT has been sold, the holder sells it to another buyer.

FIGURE 1. Time series patterns of NFT sales.

Collectibles and art (and music) constitute the bulk of NFT sales, at least up until 2021 (see Table 2). However, an increasing amount is also going to gaming and, more recently, metaverse. Metaverse is poised for substantial growth with a total addressable market between $8–13 trillion by 2030, according to Citibank (2022). Of note, NFTs are likely to play a major role in accounting for the rise as digital assets, ranging from artwork to music to real estate, and the metaverse.

TABLE 2. Composition of NFT sales, by major application.

There is a significant portion of the NFT market that consists of collectors who are drawn to the intrinsic value of the artwork itself. However, a large portion of NFT holders are also motivated by the potential for financial gain. A survey conducted by Statista found that among males aged 18–34, 41% saw NFTs as an investment opportunity, while only 30% were primarily interested in collecting art for its own sake.13 Among males aged 35–44, the fraction of those viewing NFTs as an investment drops to 25%, but it begins to rise again among those aged 45–54 (36%) and 55–64 (54%). Similar patterns are observed among females in these age groups.

This demand for NFTs as assets is consistent with results from Borri et al. (2022) who find that NFT market return resembles a high-beta asset class with more volatility and higher exposure to risk sentiments. While most of the variation in NFT returns are not driven by fluctuations in the cryptocurrency market, which only explains 20% of the activity, the overall increase in cryptocurrency demand has had ripple effects on the demand for NFTs.

While there are some speculative activities associated with NFTs (Rahuveera, 2021; Borri et al., 2022), the fundamental purpose of NFTs is to authenticate and establish ownership. Content creators, for instance, often seek to retain ownership of their intellectual property, but current technological infrastructure often requires them to make their data available for free. NFTs provide a solution to this issue by allowing creators to gate access to their content by requiring the purchase of an NFT. The security and transparency of NFTs facilitate direct connections between creators and their fans, enabling creators to monetize their ideas while maintaining control over their intellectual property.

The emergence of NFTs is unlikely to entirely replace record or centralized entities, but it may shift the balance of bargaining power in favor of artists when negotiating with these entities (Makridis, 2022b). While it is true that record labels can provide valuable support and guidance for artists in developing their careers, as argued by Marshall (2012), and only a small percentage of colleges offer explicit instruction in these entrepreneurial skills (Makridis and Kuuskoski, 2022), NFTs offer an alternative avenue for content creators to monetize their work without needing the approval of a centralized entity, potentially leading some creators to adopt a hybrid approach of working with traditional labels while also producing and selling their own independent work.

Despite the potential benefits of blockchain technology, it is important to recognize that there are also significant risks involved. One such risk is the issue of centralization, as the distribution of tokens among those in control of governance can often be concentrated among early developers and investors. This has been a point of contention within well-known protocols such as Bitcoin and Ethereum, with debate surrounding the extent to which they are truly decentralized. More research and work is required to ensure that the networks stay decentralized across transactions (Zhang et al., 2022).

Another significant risk is the anonymity of blockchain users and the lack of identity controls, which can lead to fraudulent activity and scams such as rug pulls. The presence of anonymity can exacerbate incentives to deceive customers as there are fewer dynamic considerations. Additionally, there have been many instances of hacks at the protocol and interface layers, despite the overall security of the blockchain consensus layer. These types of financial fraud can often afflict those who are less financially literate or crypto literate, and therefore pose risks of setting back economic mobility if unchecked.

Peer-to-peer transfers can also be exploited for illicit transactions, including sanctions violations, if there is insufficient screening for fiat on- and off-ramps. However, advances in the tracing of transactions through multiple hops on public blockchains has also enabled effective and efficient detection and investigations of fraud and financial crimes (Redbord, 2022).

Market manipulation is a significant issue in the blockchain industry, and one example of this is mining extraction value (MEV), which has more recently been reformulated as maximum extractable value. MEV refers to the value extracted from the blockchain through certain actions, such as frontrunning, reordering, and arbitrage. These actions can be used for market manipulation and can have negative impacts on the fairness and integrity of the market. Frontrunning occurs when a miner or entity with access to information about upcoming transactions (e.g., data from public mem pools uses this information to make trades ahead of others in the market. This can give them an unfair advantage and harm smaller market participants. Reordering is another issue, as it involves changing the order in which transactions are processed in order to extract value. This can cause delays and uncertainty for market participants and can also be used for manipulation.14

Furthermore, centralized entities utilizing distributed ledger technologies have demonstrated significant governance issues, as seen in the case of FTX, which used its own token for accounting manipulations, among other deceptive and fraudulent practices. Some evidence suggests that more decentralized entities that do not hold users’ funds on their balance sheets have performed better in the market and have been less likely to experience negative outcomes such as bankruptcy or the theft of consumer or investor funds. It is crucial to consider these risks when examining the potential adoption and implementation of blockchain technologies.

The primary aim of this paper is to examine the channels through which the emergence of distributed ledger technologies (DLTs) can affect economic mobility. This paper provides a conceptual framework for categorizing the effects of DLTs on economic mobility and presenting supporting evidence from relevant use cases, focusing on four potential channels.

• The creation of new jobs and higher value-added jobs, and the modularization of complex tasks

• Improvements in the way people learn and acquire human capital

• Increased competition in the marketplace

• Expansion and access to financial services

Although there is not yet large-scale data in this area to empirically test whether DLTs have a positive effect on economic mobility, this paper takes a first step towards formalizing the theory, focusing on areas where DLTs are being applied and having democratizing effects.

All relevant data is contained within the article: The original contributions presented in the study are included in the article/supplementary material, further inquiries can be directed to the corresponding author.

All authors listed have made a substantial, direct, and intellectual contribution to the work and approved it for publication.

CM thanks Stand Together for support to study the impact of blockchain on economic mobility. Stand Together contributed funds towards research on the broader question, but had no say in what was put together for submission.

Author GL was employed by Circle Internet Financial.

The remaining author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

1Christos A. Makridis, Stanford University and Columbia Business School, Y21ha3JpZGlAc3RhbmZvcmQuZWR1. Gordon Liao, Circle Internet Financial, Z29yZG9uQGNpcmNsZS5jb20=. Thank you to Chris Purifoy, Taylor Kendall, and Neil Chilson for comments and suggestions. Makridis also thanks Stand Together for funding some of the research into distributed ledger technologies and mobility.

2Decentralization in this context does not necessarily mean that the validation of blockchain is decentralized. Even for “permissionless blockchains,” there are valid concerns that the consensus-making process can become centralized. For example, Bohme et al. (2015) suggest that 95% of all Bitcoin trades are processed by seven centralized exchanges; see Sai et al. (2021) for a more detailed review of the taxonomy around centralization. Hoffman et al. (2020) also point out that there is a spectrum of decentralization and Conway (2022) surveys the different blockchains and their degree of centralization versus decentralization.

3See, for example, Hoffman et al. (2020) for the rise in income inequality, Molloy et al. (2016) for the decline in labor market dynamism, and De Loecker et al. (2020) for the deterioration of competition.

4For example, the OECD (2022) explains the importance of blockchain for fostering cross-country cooperation and exchange, and recommends further research on the economic channels that DLTs can impact the world.

5In fact, overlaps between NFTs and existing patents and trademarks is a substantial area of current research without an answer; eventually, these two realms of digital activity will need to be reconciled, and that will require at least some degree of human judgment and expertise.s.

6See for instance, Strange et al. (2021).

7Global Findex Database, the World Bank, 2021.

8https://www.prindex.net/reports/prindex-comparative-report-july-2020/.

9See, also, Grech et al. (2021) who provide a succinct summary of the literature on credentials and signaling. They explain the evolution of thought on credentials for signaling and the emergence of digital credentials that contain more functional elements—that is, conveying information about competencies.

10For example, Lakin and Cardenas-Elliott (2016) show that science, technology, engineering, and math (STEM) learners who transfer institutions experience a 0.6 point GPA drop in their first semester. Additional data from the National Center for Education Statistics finds that college students who attend only one institution take 4 years and 3 months (i.e., 51 months) to graduate with, compared with students who attend two institutions taking 59 months, which is a result of only a third of students being able to successfully transfer their previously earned credits. Hayes (2010) shows that the economic costs associated with a delayed graduation are roughly $49,109 to $163,974.

11For instance, the media and entertainment sector has seen an expansion of record labels and the use of “360 deals” that take a significant share of earnings from an artist’s activities (Kjus, 2021). Even if a song becomes successful, the label has priority on the flow of revenues.

12NFTs are a type of digital asset. Unlike fungible tokens that are interchangeable, NFTs are not. Instead, NFTs tokenize ideas at their most granular level (Makridis, 2021), allowing for the measurement and authentication of anything that can be described in a contractual format, including much more than art and music.

13See “Reasons why consumers would buy NFT in the United States in March 2021, by age and gender” on Statista.

14See, for instance, Robinson and Konstantopoulos (2020) for overview and technical discussions.

Allen, D. W., Berg, C., Davidson, S., Novak, M., and Potts, J. (2019). International policy coordination for blockchain supply chains. Asia Pac. Policy Stud. 6 (3), 367–380. doi:10.1002/app5.281

Ates, H., and Alsal, K. (2012). The importance of lifelong learning has been increasing. Procedia Soc. Behav. Sci. 46, 4092–4096. doi:10.1016/j.sbspro.2012.06.205

Autor, D., Dorn, D., Katz, L. F., Patterson, C., and Van Reenen, J. (2020). The fall of the labor share and the rise of superstar firms. Q. J. Econ. 135 (2), 645–709. doi:10.1093/qje/qjaa004

Autor, D. H. (2013). The “task approach” to labor markets: An overview. J. Labour Mark. Res. 46, 185–199. doi:10.1007/s12651-013-0128-z

Bajgar, M., Criscuolo, C., and Timmis, J. (2021). Intangibles and industry concentration: Supersize Me. OECD Science. Technology and Industry Working Papers.

Barkai, S. (2020). Declining labor and capital shares. J. Finance 75 (5), 2421–2463. doi:10.1111/jofi.12909

Bessen, J. (2020). Industry concentration and information technology. J. Law Econ. 63 (3), 531–555. doi:10.1086/708936

Böhme, R., Christin, N., Edelman, B., and Moore, T. (2015). Bitcoin: Economics, technology, and governance. J. Econ. Perspect. 29 (2), 213–238. doi:10.1257/jep.29.2.213

Borri, N., Liu, Y., and Tsyvinski, A. (2022). The economics of non-fungible tokens. Available at: https://ssrn.com/abstract=4052045 (Accessed March 7, 2022).

Bresnahan, T., and Trajtenberg, M. (1995). General purpose technologies "engines of growth. J. Econ. 65 (1), 83–108. doi:10.1016/0304-4076(94)01598-t

Brynjolfsson, E., Rock, D., and Syverson, C. (2021). The productivity J-curve: How intangibles complement general purpose technologies. Am. Econ. J. Macroecon. 13 (1), 333–372. doi:10.1257/mac.20180386

Bureau of Economic Analysis (2017). New data showcase economic impact of arts and culture in U.S. And States. Available at: https://www.bea.gov/news/blog/2017-04-19/new-data-showcase-economic-impact-arts-and-culture-us-and-states (Accessed April 19, 2017).

Chetty, R., Hendren, N., Kline, P., Saez, E., and Turner, N. (2014a). Is the United States still a land of opportunity? Recent trends in intergenerational mobility. Am. Econ. Rev. 104 (5), 141–147. doi:10.1257/aer.104.5.141

Chetty, R., Hendren, N., Kline, P., and Saez, E. (2014b). Where is the land of opportunity? The geography of intergenerational mobility in the United States. Q. J. Econ. 129 (4), 1553–1623. doi:10.1093/qje/qju022

Citibank (2022). Metaverse and money: Decrypting the future. Citi GPS: Global perspectives & solutions. Available at: https://ir.citi.com/gps/BGrBay2thaQaH9HYofo3Uf3ThNldHDse_iJbe_md8Xk2SX5N3rdCq70nBWVa5mRqVYO3BHcw4Htuf7ihwIzrP6f0AN2kKVQZ (Accessed March 3, 2022).

Claessens, S., and Perotti, E. (2007). Finance and inequality: Channels and evidence. J. Comp. Econ. 35 (4), 748–773. doi:10.1016/j.jce.2007.07.002

Coinbase Volume (2022). Market Prices & listings, trading pairs. Available at: https://nomics.com/exchanges/gdax-coinbase-exchange (Accessed April 17, 2022).

Cong, W., Tang, K., Wang, Y., and Zhao, X. (2022). Inclusion and democratization through Web3 and DeFi? Initial evidence from the Ethereum ecosystem. SSRN working paper Available at: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4162966 (Accessed July 29, 2022).

Conley, J. P. (2019). Blockchain as a decentralized mechanism for financial inclusion and economic mobility. Tennessee: Vanderbilt University Department of Economics Working Papers. VUECON-19-00012.

Davidson, S., De Filippi, P., and Potts, J. (2018). Blockchains and the economic institutions of capitalism. J. Institutional Econ. 14 (4), 639–658. doi:10.1017/s1744137417000200

De Loecker, J., Eeckhout, J., and Unger, G. (2020). The rise of market power and the macroeconomic implications. Q. J. Econ. 135 (2), 561–644. doi:10.1093/qje/qjz041

Disparte, D. A. (2021). “Privately issued digital currencies,” in Disintermediation economics (Cham: Palgrave Macmillan), 173–191.

Frank, M. R., Autor, D., Bessen, J. E., Brynjolfsson, E., Cebrian, M., Deming, D. J., et al. (2019). Toward understanding the impact of artificial intelligence on labor. Proc. Natl. Acad. Sci. 116 (14), 6531–6539. doi:10.1073/pnas.1900949116

Gallipoli, G., and Makridis, C. A. (2018). Structural transformation and the rise of information technology. J. Monetary Econ. 97, 91–110. doi:10.1016/j.jmoneco.2018.05.005

Granja, J., Makridis, C. A., Yannelis, C., and Zwick, E. (2022). Did the paycheck protection program hit the target? J. Financial Econ. 145 (3), 725–761. doi:10.1016/j.jfineco.2022.05.006

Grech, A., Sood, I., and Arino, L. (2021). Blockchain, self-sovereign identity and digital credentials: Promise versus praxis in education. Front. Blockchain 4, 616779. doi:10.3389/fbloc.2021.616779

Greenwood, R., and Scharfstein, D. (2013). The growth of finance. J. Econ. Perspect. 27 (2), 3–28. doi:10.1257/jep.27.2.3

Grossman, S. J., and Hart, O. D. (1986). The costs and benefits of ownership: A theory of vertical and lateral integration. J. political Econ. 94 (4), 691–719. doi:10.1086/261404

HansenGary, D., and Prescott, E. C. (2002). Malthus to solow. Am. Econ. Rev. 92 (4), 1205–1217. doi:10.1257/00028280260344731

Hart, O., and Moore, J. (1990). Property rights and the nature of the firm. J. political Econ. 98 (6), 1119–1158. doi:10.1086/261729

Hastings, J. S., Neilson, C. A., and Zimmerman, S. D. 2014. Are some degrees worth more than others? Evidence from college admission cutoffs in Chile. NBER Working Paper 19241.

Hayes, S. K. (2010). Student employment and the economic cost of delayed college graduation. J. Bus. Leadersh. Res. Pract. Teach. 6 (1), 2005–2012. Article 14.

Hoffman, F., Lee, D. S., and Lemieux, L. (2020). Growing income inequality in the United States and other advanced economies. J. Econ. Perspect. 34 (4), 52–78. doi:10.1257/jep.34.4.52

Holmgren, A. Jay, Downing, N. L., Bates, D. W., Shanafelt, T. D., Milstein, A., Sharp, C. D., et al. (2021). Assessment of electronic health record Use between US and non-US health systems. JAMA Intern. Med. 181 (2), 251–259. doi:10.1001/jamainternmed.2020.7071

Katz, L. F., and Murphy, K. M. (1992). Changes in relative wages, 1963-1987: Supply and demand factors. Q. J. Econ. 107 (1), 35–78. doi:10.2307/2118323

Kjus, Y. (2021). Twists and turns in the 360 deal: Spinning the risks and rewards of artist–label relations in the streaming era. Eur. J. Cult. Stud. 25 (2), 463–478. doi:10.1177/13675494211044731

Lakin, J. M., and Cardenas-Elliott, D. (2016). STEMing the shock: Examining transfer shock and its impact on STEM major and enrollment persistence. J. First-Year Exp. Students Transition 28 (2), 9–31.

Lee, D. T., and Makridis, C. A. 2021. Towards a model of human collaboration and computation. arXiv.

Lemoie, K., and Soares, L. (2020). Connected impact. Unlocking education and workforce opportunity through blockchain.C., United States: American Council on Education.

Makridis, C. A., Froewis, M., Sridhar, K., and Boehme, R. (2023). forthcoming, 102358. doi:10.1016/j.jcorpfin.2023.102358The rise of decentralized cryptocurrency exchanges: Evaluating the role of airdrops and governance tokensJ. Corp. Finance

Makridis, C. A. (2022a). How EdTech firms are bringing higher education to the metaverse. Forbes. Available at: https://www.forbes.com/sites/zengernews/2022/07/28/how-edtech-firms-are-bringing-higher-education-to-the-metaverse/ (Accessed July 28, 2022).

Makridis, C. A., and Kuuskoski, J. (2022). The labor market and public policy implications of arts Entrepreneur. Social Sciences Research Network (SSRN).

Makridis, C. A. 2021. NFTs will replace copyrights and trademarks. Finance Magnates. Accessed 29 Deember, 2021, Available at: https://www.financemagnates.com/cryptocurrency/nfts-will-replace-copyrights-and-trademarks/.

Makridis, C. A. (2022b). Record music streaming profits highlight how NFTs will empower content creators. Cointelegraph.

Marshall, K. (2012). The 360 deal and the ‘new’ music industry. Eur. J. Cult. Stud. 16 (1), 77–99. doi:10.1177/1367549412457478

Michelman, V., Price, J., and Zimmerman, S. (2021). Old Boys’ clubs and upward mobility among the educational elite. Q. J. Econ. 137 (2), 845–909. doi:10.1093/qje/qjab047

Molloy, R., Trezzi, R., Smith, C. L., and Wozniak, A. (2016). Understanding the Cining Fluidity in the U.S. Labor market. Washington: Brookings Papers on Economic Activity.

Morning Consult (2022). The state of consumer banking & payments. Available at: https://go.morningconsult.com/rs/850-TAA-511/images/220120_State_of_Consumer_Banking.pdf (Accessed Mar 3, 2022).

Novak, M. (2018). Inequality: An entangled political economy perspective. Berlin, Germany: Springer.

OECD (2022). Blockchain at the frontier: Impacts and issues in cross-border co-operation and global governance, OECD Business and Finance Policy Papers. Paris: OECD Publishing.

Pew Research Center (2021). 16% of Americans say they have ever invested in, traded or used cryptocurrency. Available at: https://www.pewresearch.org/fact-tank/2021/11/11/16-of-americans-say-they-have-ever-invested-in-traded-or-used-cryptocurrency/ (Accessed November 11, 2021).

Piketty, T., and Saez, E. (2003). Income inequality in the United States, 1913–1998. Q. J. Econ. 118 (1), 1–41. doi:10.1162/00335530360535135

Powell, J. (2022). Monetary policy and price stability, Reassessing Constraints on the economy and policy,” an economic policy symposium sponsored by the Federal Reserve bank of Kansas city.

Raghuveera, N. (2021). Designing decentralized finance for financial inclusion. Atlantic Council GeoEconomics Center.

Redbord, A. (2022). Alternative payment systems and national security impacts of their growth. Washington: Testimony before the U.S. House Committee on Financial Services.

Rinz, K. (2022). Labor market concentration, earnings, and inequality. J. Hum. Resour. 57, S251–S283. doi:10.3368/jhr.monopsony.0219-10025r1

Saad, L. (2021). Bitcoin making Inroads with Younger U.S. Investors. Gallup. Available at: https://news.gallup.com/poll/352508/bitcoin-making-inroads-younger-investors.aspx (Accessed July 22, 2022).

Sai, A. R., Buckley, J., Fitzgerald, B., and LeGear, A. (2021). Taxonomy of centralization in public blockchain systems: A systematic literature review. Inf. Process. Manag. 58 (4), 102584. doi:10.1016/j.ipm.2021.102584

Schmalensee, R., and Stavins, R. (2017). Lessons learned from three decades of experience with cap and trade. Rev. Environ. Econ. Policy 11 (1), 59–79. doi:10.1093/reep/rew017

Small Business Majority (2021). Small businesses struggling to access capital, harming their financial recovery. Available at: https://smallbusinessmajority.org/our-research/access-capital/small-businesses-struggling-access-capital-harming-their-financial-recovery (Accessed February 17, 2021).

Spence, M. (1978). “Job market signaling,” in Uncertainty in economics (Massachusetts, United States: Academic Press), 281–306.

Statista (2022b). NFT ownership among investors in the United States in March 2021, by age and gender.

Strange, A., Singh, S., Tillemann, S., Rathmell, J., Haber, D., Yoo, J., et al. (2021). The big ideas that fintech will tackle in 2022. Available at: https://a16z.com/2021/12/20/the-big-ideas-that-fintech-will-tackle-in-2022/ (Accessed December 20, 2021).

Utile, I., Hahs, T., and Makridis, C. A. (2020). Decentralized Voice tech will Disrupt centralized interfaces. attn.live whitepaper.

Vaish, R., Gaikwad, S., Kovacs, G., Veit, A., Krishna, R., Ibarra, I. A., et al. (2017). Crowd research: Open and scalable university Laboratories. Berlin, Germany: Springer. UIST ‘17.

Valentine, M. A., Retelny, D., To, A., Rahmati, N., Doshi, T., and Bernstein, M. S. (2017). “Flash organizations: Crowdsourcing complex work by structuring crowds as organizations,” in CHI '17: Proceedings of the 2017 CHI Conference on Human Factors in Computing Systems, Denver Colorado USA, May 6 - 11, 2017, 3523–3537.

Valletta, R. G. (2016). “Recent flattening in the higher education wage premium: Polarization, skill downgrading, or both?,” in Education, skills, and technical change: Implications for future U.S. GDP growth (New York City: National Bureau of Economic Research).

Vanderkam, L. (2009). The promise and peril of the freelance economy. Availabe at: https://www.city-journal.org/html/promise-and-peril-freelance-economy-13145.html.

Volles, N. (2016). Lifelong learning in the EU: Changing conceptualisations, actors, and policies. Stud. High. Educ. 41 (2), 343–363. doi:10.1080/03075079.2014.927852

Wang, F., and De Filippi, P. (2020). Self-sovereign identity in a globalized world: Credentials-based identity systems as a driver for economic inclusion. Front. Blockchain 2, 28. doi:10.3389/fbloc.2019.00028

Zhao, D. (2018). The rise of Bitcoin & blockchain: A growing demand for talent. Glassdoor. Availabe at: https://www.glassdoor.com/research/rise-in-bitcoin-jobs/ (Accessed December 18, 2018).

Keywords: blockchain, distributed ledger technologies, economic mobility, inequality, labor markets

Citation: Makridis CA and Liao GY (2023) Democratizing effects of digital ledger technologies: Implications for economic mobility. Front. Blockchain 6:972183. doi: 10.3389/fbloc.2023.972183

Received: 17 June 2022; Accepted: 06 February 2023;

Published: 09 March 2023.

Edited by:

Adrian Loy, Monash University, AustraliaReviewed by:

Piotr Soja, Kraków University of Economics, PolandCopyright © 2023 Makridis and Liao. This is an open-access article distributed under the terms of the Creative Commons Attribution License (CC BY). The use, distribution or reproduction in other forums is permitted, provided the original author(s) and the copyright owner(s) are credited and that the original publication in this journal is cited, in accordance with accepted academic practice. No use, distribution or reproduction is permitted which does not comply with these terms.

*Correspondence: Christos A. Makridis, Y21ha3JpZGlAc3RhbmZvcmQuZWR1

Disclaimer: All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article or claim that may be made by its manufacturer is not guaranteed or endorsed by the publisher.

Research integrity at Frontiers

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.