David Mhlanga

David Mhlanga

95% of researchers rate our articles as excellent or good

Learn more about the work of our research integrity team to safeguard the quality of each article we publish.

Find out more

REVIEW article

Front. Blockchain , 06 February 2023

Sec. Blockchain Economics

Volume 6 - 2023 | https://doi.org/10.3389/fbloc.2023.1035405

There is a lot of hope that blockchain technology may be used to standardize money transactions and increase access to banking. It is believed that regulators and industry professionals have looked into the possibility of using blockchain technology to modernize and even replace the infrastructure that currently supports international payments and remittances, such as correspondent banking, in order to ensure that transactions can be verified and recorded using blockchain technology in a distributed ledger. The purpose of this study was to analyze how blockchain technology has helped to include previously underserved populations in the mainstream financial system, and to remark on the best practices and lessons learned from sustainable development. Using a systematic literature review, the study discovered the many ways in which blockchain technology can facilitate digital financial inclusion, including its application in financial transactions, its utility as a tool for increasing financial savings, its use in the provision of credit, and its application in the provision of insurance. According to the findings, even though the global goals do not specifically target financial inclusion, providing access to financial services for the majority of the population is a critical enabler for several of the global goals. Therefore, the study concluded that sustainable development can be ensured on many fronts if the technology behind blockchains can be successfully used to improve financial inclusion. If governments, especially in developing countries, are serious about increasing citizens’ access to financial services, they must prioritize blockchain investment.

Blockchain technologies have shown a lot of potential for institutionalizing remittances and increasing access to financial services since they were first developed (Rella 2019). It is believed that both authorities and practitioners have looked into the potential of blockchain technology to simplify and possibly even replace the infrastructure that supports international payments and remittances, such as correspondent banking. This is done so that transactions can be verified and recorded using blockchain technology in a decentralized ledger. Correspondent banking connections, often known as “Nostro-Vostro accounts,” are arrangements between governments that allow banks to operate in nations where they do not have a physical presence. These links are frequently referred to as “correspondent banking” (Rella 2019; Bai et al., 2020). Blockchain technology has been shown to promote the formalization of remittances rather than prevent it, claims Rella. (2019). The existing infrastructure, services, business plans, and regulatory frameworks are currently being updated to include these applications (Schuetz and Venkatesh 2020). The second crucial point is that blockchain technologies, as opposed to the introduction of fundamentally new monetary systems, are the most recent iteration of the technology that ushers in frictionless capitalism.

Making this distinction is crucial because blockchain technology is the most recent innovation to signal the advent of frictionless capitalism (Rella, 2019; Schuetz and Venkatesh 2020). According to research, regulators “developed banking institutions, and non-governmental organizations are increasingly looking to blockchain technologies as potentially useful tools for the “financial inclusion” of the unbanked and “underserved, as well as for the formalization of value transfers that were previously informal, such as remittances” (Rella, 2019; Abdulhakeem and Hu, 2021). To encourage greater financial inclusion, several new businesses as well as more established ones are working toward the same goal by developing more inclusive methods of international money transfers and cross-border payments (Rella, 2019; Abdulhakeem and Hu, 2021). Blockchain has become the most important word in the world in recent years. The experts agree that this online platform holds great promise for businesses around the world and will dominate the Internet in the next century. According to Abdulhakeem and Hu. (2021), blockchain technology has the greatest potential to improve people’s lives in the coming decades.

The use of “cryptocurrencies, online payments, and remittances” are just three examples of how blockchain technology is being incorporated into various industries. In addition to that, it finds applications on the Internet of Things, smart contracts, voting, the healthcare industry, and the verification of educational materials (Abdulhakeem and Hu, 2021). The technology behind blockchain can even be used to track physical items, as well as intellectual property rights and a wide variety of other things. The term blockchain refers to “a type of distributed ledger technology (DLT), which serves not only as a digital ledger but also as a method that enables assets to be transferred securely without the need for an intermediary” (Abdulhakeem and Hu, 2021). Blockchain is “a system that enables the exchange of value with the presence of collaboration, cryptography, and some smart codes. Anything from currencies to art and music can be tokenized, stored, and exchanged on a blockchain network. Scholars believe that blockchain is a technology that facilitates the transfer of information, just like the Internet”. Blockchain is a technology that makes it possible to transact value more easily (Abdulhakeem and Hu, 2021).

Academics believe that “blockchain technology has the potential to improve efficiency” by bringing together a variety of disparate systems. For example, the current financial systems that are in operation in various countries in institutions such as “banks and other intermediaries each have their systems, and each entity is in complete control of where and how its data is recorded, stored, and managed”. These systems are currently operating in various nations. Because of the nature of these systems, they are unable to communicate with one another or integrate effectively. This is because each institution can pick what kind of servers to use, where to site them, and how their security protocols operate. As a result, the movement of value across these restricted and centralized systems is ineffective, expensive, and time-consuming (Ohnesorge, 2018; Rieger et al., 2022).

Again, academics contend that the introduction of Bitcoin in 2008/2009 made it possible for individuals and organizations to send and receive money on a truly peer-to-peer basis across national and international borders without the need for a trusted central entity such as a bank. In the early days of technology, it is believed that only a small number of people grasped the entire potential of the technology. However, nowadays, blockchains are sometimes referred to as the internet of trust. According to Ohnesorge. (2018), this term refers to the universal potential of blockchain technology, which goes beyond the realm of payment systems and enables individuals who do not trust one another to directly trade (digitally representable) goods and services with one another. Ohnesorge believes that this term relates to the universal potential of blockchain technology. It is incredible how many different blockchain technologies there are now, including cryptocurrencies in their numerous forms. Start-ups and established companies in the information technology sector are continuously working to cut the amount of time, money, and effort required to transfer cryptocurrencies on a global scale. At the same time, they are increasing the transaction capacity and providing services that extend beyond payments.

It should come as no surprise that “one of the earliest and most promising applications of blockchain technology has been in the realm of international payments”. Blockchain technologies were initially developed to manage financial transactions in the decentralized network that Bitcoin uses (Dwyer, 2017; Janssen et al., 2020). At the moment, commercial implementations of blockchain technology are caught in a cycle of co-opetition, depoliticization of their design, and growing competition. Emerging outside of traditional finance and frequently in opposition to it are blockchain technology. The immutable and transparent recording of transactions, as well as rapid clearing and settlement, are promises made by blockchain and distributed ledger technology. Decentralized ledgers make it possible for these advantages. The financial services sector is experiencing hazy dynamics as a result of business use of blockchain technology. These processes are entangled in conflicts such as interoperability and confinement, disintermediation and re-intermediation, disruption, and rent extraction (Dwyer, 2017; Giungato et al., 2017; Janssen et al., 2020). According to Schuetz and Venkatesh. (2020), blockchain technologies can solve most of the problems that prevent isolated villages in India from being connected to both regional and international supply chains, which is a prerequisite for rural India’s economic development. Schuetz and Venkatesh. (2020), also argued that the success of financial inclusion programs in India hinges on the widespread adoption of blockchain technologies, thus it's important to learn about the local culture and norms around technology adoption. Financial exclusion is a major barrier to participation in these supply networks among rural Indians. Building on this foundation, the current study seeks to analyze the influence that blockchain technology has had on the financial inclusion of the excluded people and to comment on the most important lessons and advantages toward sustainable development.

According to Yaga et al. (2019) blockchains are a type of digital ledger that cannot be altered without leaving clear evidence of having been altered. Since these digital ledgers are deployed in a distributed fashion, there is typically no central repository or authority, such as a bank, corporation, or government. This is due to the lack of a necessity for a centralized repository and authority. At its most basic level, blockchains enable a group of people to track transactions among themselves via a shared ledger. Because of how the network was designed to work, once a transaction has been recorded on a blockchain, it cannot be modified, making it impossible to modify the transaction. In other words, a Blockchain is a decentralized, unchangeable ledger that makes it easier to record transactions and manage assets within a commercial network. An asset is anything that can be physically touched, like a house, car, money, or a piece of land. However, intangible things like intellectual property, patents, copyrights, or trademarks can also be viewed as assets. A blockchain network can be used to track and exchange anything of value, which lowers the associated risks and expenses for all parties involved (Saberi et al., 2019; Yaga et al., 2019). According to Yaga et al. (2019), the introduction of the Bitcoin network in 2009 marked the beginning of widespread public awareness of blockchain technology. When using Bitcoin and other systems that are theoretically similar to it, it is hypothesized that the transfer of digital information that represents digital payment takes place through a distributed network.

The first of several cryptocurrencies currently in use was Bitcoin, and there are currently many additional cryptocurrencies. Blockchain technology enables Bitcoin users to digitally sign documents and transfer their rights to those documents to other users. This transmission is publicly recorded in the Blockchain data, allowing all network participants to independently verify the validity of the transactions. The durability of the blockchain in the face of attempts to alter the ledger is aided by the use of cryptographic techniques as well as the fact that each participant in the bitcoin blockchain is in charge of keeping and administering their copy of the ledger. Blockchain technology’s advancement has made it feasible to create a variety of cryptocurrency systems, including Bitcoin and Ethereum. As a result of this, blockchain technologies are commonly considered to be limited to Bitcoin or maybe cryptocurrency applications in general. Nevertheless, this is not the case. This image continues to exist even though the technology is now used in a greater variety of applications and is being researched in a variety of different industries (Pilkington, 2016; Saberi et al., 2019; Yaga et al., 2019). Since businesses are dependent on information and their success is directly proportional to the speed with which they receive and act upon that information, “blockchain technology is ideally suited for the delivery of information since it provides information that is, immediately shared and completely transparent and that is, stored on an immutable ledger that can only be accessed by network members who have been granted permission to do so”. A blockchain network “can keep tabs on orders, payments, accounts, production, and a lot more. Since members of the network share a single view of the truth, you can view all of the details of a transaction from beginning to end”. This provides you with increased confidence, in addition to new opportunities and efficiencies.

Before Bitcoin, there were other electronic payment systems like cash and NetCash, but none of them attained the level of widespread adoption that Bitcoin accomplished. Simply put, Bitcoin was the first of many blockchain-based apps that may be created. Bitcoin was able to be deployed in a distributed fashion thanks to the use of a blockchain. This implied that there was no single point of failure and that no single user had power over the electronic money. The capacity to enable direct transactions between users without the need for a reliable third party enhanced the popularity of Bitcoin, and this was its main advantage. Miners are users who can create new blocks and maintain copies of the ledger. Additionally, this function allowed for the distribution of brand-new money in a preset way to those who were successful in doing so (Pilkington, 2016; Zheng et al., 2017; Saberi et al., 2019; Yaga et al., 2019). A self-policing mechanism was developed using a blockchain and general agreement corrections to ensure that only legitimate actions and blocks were added to the blockchain. This approach allowed for distributed system administration to be carried out without the need for organization thanks to the automated payment of the miners (Zheng et al., 2017; Saberi et al., 2019).

Since all digital currencies are accessible to the general public, Bitcoin can provide pseudo-anonymity since accounting entries can be created without the recognition or authorization steps that are frequently required by Know-Your-Customer (KYC) requirements. Additionally, because every Bitcoin transaction can be scrutinized, this characteristic enables Bitcoin to provide a type of pseudo-anonymity (Zheng et al., 2017; Saberi et al., 2019; Dutta et al., 2020). Before the deployment of blockchain technology, trust-building activities were often provided through intermediaries who were trusted by both parties. This was important in a setting where users could not be identified. However, the need for a setting where users could not be easily identified led to the requirement for trust-building activities. It was crucial to put processes in place that would make it easier for the Bitcoin community to establish trust because Bitcoin users cannot be easily identified.

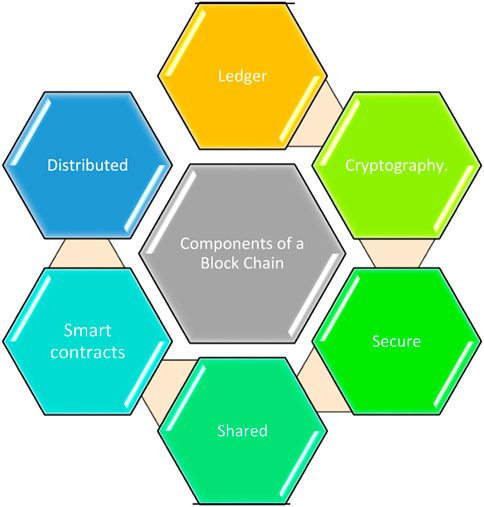

The four key features of blockchain technology, which are shown in Figure 1 below, enable the necessary level of trust that must exist among the users of a blockchain network These characteristics eliminate the need for trusted middlemen.

FIGURE 1. The fundamental components of a blockchain.

The blockchain has the potential to operate in a decentralized fashion. This makes it possible to scale up the number of nodes that make up a blockchain network, which in turn makes the network more resistant to attacks from malicious actors. The more nodes that are part of a blockchain, the more difficult it is for malevolent actors to interrupt the consensual mechanism that is, being used by the blockchain. A ledger is used by the technology, and it is an append-only ledger so that it can offer a complete history of all transactions. A blockchain, in contrast to traditional databases, does not allow for its transactions or values to be altered. Distributed ledgers are used to create an immutable record of all transactions that can be accessed by all users in the network. This shared ledger means that all transactions need only be recorded once, doing away with the usual effort duplication that comes with more conventional business networks. Cryptographically secure blockchains guarantee the integrity of the ledger’s data and make it possible to verify that no tampering has taken place with the ledger’s records. A “secure blockchain has been designed to prevent unauthorized access and because of this feature, once a transaction has been recorded in the distributed ledger, it can’t be altered by any of the users”. To fix an error in a transaction record, a new transaction must be entered and after this is complete, both deals can be viewed.

The ledger is accessible by several different parties at the same time. This ensures that all members of the blockchain network have access to the same level of information. Smart contracts are a way to speed up transactions by storing a set of rules on the blockchain that may be automatically implemented. These rules are referred to as a smart contracts. A smart contract can be used for a variety of purposes, such as containing the conditions for the transferring of corporate bonds and the terms for the payment of trip insurance, among many others. By allowing people and organizations to transact directly, this trust may enable faster and more affordable transaction delivery. These characteristics enable a certain amount of confidence between partners with no prior knowledge of one another. Direct transactions between people and organizations may be made possible by this trust. Blockchain networks that do not place any limits on who can create accounts or participate in transactions are referred to as “permissionless blockchain networks.” These qualities make it possible for parties who had never met before to develop a certain level of trust.

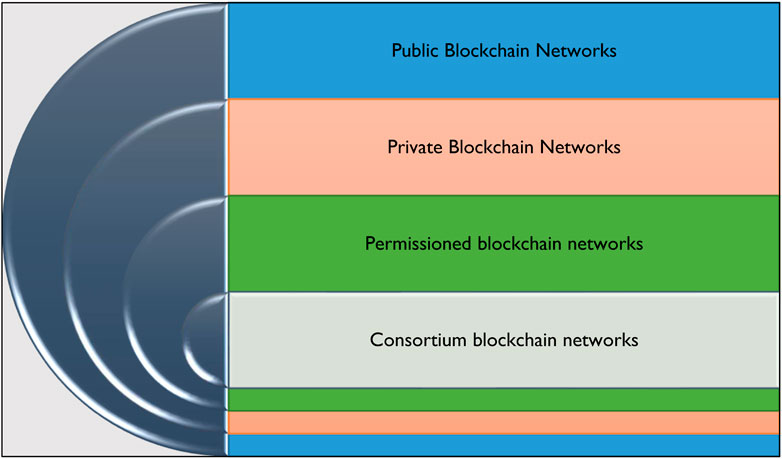

These functions help to reinforce the already-existing trust between users of a blockchain network known as a permissioned blockchain network, which more strictly controls access than other blockchain networks. According to Abdulhakeem and Hu. (2021), “a blockchain is a data structure that holds transactional records while ensuring security, transparency, and decentralization”. This “technology enables the management of transaction data to be decentralized on a network of computers around the world using open-source software. Blockchains are used in cryptocurrencies such as bitcoin and Ethereum”. Any modification to the software running on a blockchain must first go through a consensus procedure, which is outside the control of any single authority. Because all transactions are recorded on a public ledger that is, kept online and accessible to the public, this system adheres to the principle of transparency. Figure 2.

FIGURE 2. Types of blockchain networks.

There are many different approaches to putting together a blockchain network. They can be made available to the public, kept private, officially sanctioned, or be the work of a collaborative effort. Blockchain networks that are open to the public, such as Bitcoin, are referred to as public blockchains. Possible negatives include the requirement for a significant amount of computer power, the absence of transactional privacy, and inadequate levels of security. In the context of blockchain applications in businesses, these are essential considerations to keep in mind. Similar to public blockchain networks, private blockchain networks are peer-to-peer distributed computer networks. However, “the governance of the network is controlled by a single entity, which is also responsible for carrying out a consensus protocol and monitoring the shared ledger. Depending on the context, this has the potential to significantly boost participants’ levels of trust and confidence”. There is also the possibility of operating a private blockchain within the confines of an organization’s firewall and even of hosting it locally.

Companies that construct private blockchains are often the ones that are responsible for the creation of networks on blockchains with permits. It is essential to keep in mind that even public blockchain networks might have rights assigned to their nodes. As a direct consequence of this, there are restrictions placed on the types of transactions that can take place and the users that can take part in the network. Participants are required to get either an invitation or authorization before they can take part. Consortiums based on the blockchain: The task of ensuring that a blockchain is always up to date can be shared amongst multiple companies. These pre-selected organizations decide who is allowed to access the data or submit transactions. They also decide who can view the data. When all parties engaged in a transaction need to have authorization and must take turns being responsible for the blockchain, the best choice for a company to make is to use a blockchain that is, run by a consortium.

“Financial inclusion” is defined by the World Bank. (2022) as “individuals and enterprises having access to usable and affordable financial goods and services that fit their needs,” including “transactions, payments, savings, credit, and insurance supplied responsibly and sustainably.” According to the United Nations, eight of the seventeen Sustainable Development Goals have recognized financial inclusion as a key facilitator for their achievement. The World Bank Group recognizes the importance of financial inclusion as a major enabler in the fight against extreme poverty and the promotion of shared prosperity (Mhlanga, 2020; World Bank, 2022). Access to a “transaction account, which enables people to hold money as well as make and receive payments, is the first step toward broader financial inclusion”. This is because a “transaction account gives people the ability to send and receive payments. Because a transaction account acts as an entry point to other financial services, the Globe Bank Group (WBG) continues to place a primary emphasis on ensuring that people in all parts of the world have access to the capability of opening a transaction account”. The ongoing issue brought on by COVID-19 has further highlighted the importance of expanding access to digital financial services. Financial inclusion using digital technology entails “the deployment of cost-saving digital means to reach populations that are currently financially excluded or underserved with a variety of formal financial services that are suited to their needs and that are delivered responsibly at a cost that is, affordable to customers and sustainable for providers”. In other words, digital financial inclusion is the process of bringing currently financially excluded and underserved populations into the mainstream (Mhlanga and Denhere, 2020; Mhlanga, 2021). Between 2011 and 2017, significant headway was achieved toward the goal of financial inclusion, and the number of adults around the world who have access to a bank account increased by 1.2 billion. As of the year 2017, 69% of adults across the world had an online presence. More than 80 nations have now begun offering customers access to digital financial services, including some that may be accessed using mobile phones. Some of these services have reached a significant size (Mhlanga, 2020; World Bank, 2022).

According to the World Bank Digital financial inclusion means that people have access to a variety of formal financial services that meet their needs and are responsibly supplied at a price that is, both accessible to clients and sustainable for providers. Giving services to people who are currently unreached or underserved, requires the use of efficient and inexpensive digital tools. A digital transactional platform, retail agents, and the use of a device–most frequently a mobile phone - by both customers and retail agents to conduct transactions via the platform are the three key elements that make up any type of digital financial service. Any digital financial service is built on a platform for digital transactions. If a customer uses a digital transactional platform, they will be able to hold value electronically with a bank or non-bank that is, permitted to do so, as well as send and receive payments and transfers using a device. The consumer will also have the option of storing value electronically with a non-bank that is, permitted to do so. Customers have the option of converting cash into electronically stored value and back into cash when dealing with retail agents who are outfitted with digital devices connected to communications infrastructure to transmit and receive transaction details. Retail agents can send and receive transaction information. By sending and receiving transaction-related information, retail agents can achieve this purpose. Agents may also be required to do other tasks, depending on the laws currently in effect and the terms of their contract with the major financial institution. The customer device could be an instrument, like a credit card, that connects to a digital device, like a POS terminal, or it could be a digital device, like a mobile phone, which is a means of delivering data and information. Additionally, the customer’s system may mix analogue and digital functions.

The Fourth Industrial Revolution, sometimes known as “industry 4.0,” is a fundamental change in how people work, engage with one another, and go about their daily lives (Lasi et al., 2014; Sony and Naik, 2019; Mhlanga, 2020). The astounding technological advancements, comparable to those of the first, second, and third industrial revolutions, have added a new chapter to the chronicles of human history. The physical, digital, and biological worlds are becoming more interconnected because of technological advancements, which have the potential to bring forth both great promise and great peril (Lasi et al., 2014; Ghobakhloo, 2020). We are being forced to reconsider not only the processes by which nations thrive but also how enterprises create value and even the very essence of what it means to be a human being because of the velocity, extent, and depth of this transformation. The Fourth Industrial Revolution is a chance for everyone to use convergent technologies to create a future that is, inclusive and focused on people, including leaders, legislators, and people from all socioeconomic categories and nations. Every country has access to this chance and it involves more than just a technological revolution. In other words, the Fourth Industrial Revolution is about people as much as technology (Lasi et al., 2014; Ghobakhloo, 2020). The true chance is in looking beyond technology and figuring out how to empower the greatest number of people to have a positive impact on their families, organizations, and communities. This can be done by figuring out how to make technology accessible to as many people as possible.

The concept of “sustainable development” refers to growth that satisfies the requirements of the present without sacrificing the ability of future generations to provide for their own need. This broad notion of sustainable development includes many different aspects. Unintended effects of the pursuit of economic expansion include the destruction of the environment and the widening of socioeconomic gaps. The principles of sustainable development need a more comprehensive growth strategy. The three core pillars of social inclusion, environmental sustainability, and economic prosperity should all be advanced by this plan (Parris and Kates, 2003; Rogers et al., 2012; Jamwal et al., 2021). Along with a prodigious economic boom, the beginning of the industrial revolution was also the catalyst for numerous technological advances, including the creation of electricity. Coal has historically been a cost-effective energy source in many regions of the world but doing so comes at a cost to society and the environment. Burning coal releases dangerous greenhouse gases that are a major contributor to the acceleration of climate change. Coal is a non-renewable resource. Implementing technology that is, more energy-efficient and diversifying our energy sources would be a more sustainable solution (Jabareen, 2008; Sachs, 2015). An alternative energy source has no detrimental effects on the environment or human health. Wind, solar, and biomass energy are a few examples of this kind of energy source. Our Common Future, often known as the Brundtland Report, was published in response to the requirement for a more sustainable method of development. The Brundtland Report is another frequent name for this document. Innovations in the field of renewable energy might also open up new business prospects (Brundtland, 1987; Sachs, 2015). The concept of sustainable development and its guiding principles were originally introduced in the report published in 1987 by the United Nations Commission on Environment and Development.

The main advantage of blockchain technology is its capacity to address trust issues without the need for a central authority or third party. Blockchain technologies have shown a great deal of potential for the formalization of remittances and the growth of financial inclusion since their introduction. Additionally, there are an increasing number of studies that show how important blockchain technology is for financial inclusion in various contexts. The benefits of employing decentralized finance are looked at by Chen and Bellavitis. (2019), who also analyzes the various business models now in use and assesses any potential challenges and limitations. According to Chen and Bellavitis. (2019), blockchain technology can lower transaction costs, make decentralized platforms easier to use, and foster distributed trust, laying the groundwork for new business models. Blockchain technology enables the emergence of decentralized financial services in the financial sector that may be more decentralized, inventive, interoperable, borderless, and transparent. According to Chen and Bellavitis. (2019), blockchain technology can lower transaction costs, make decentralized platforms easier to use, and foster distributed trust, laying the groundwork for new business models.

Decentralized financial services, according to Chen and Bellavitis. (2019), have the potential to lower transaction costs, expand the population’s access to financial services, facilitate open access, foster permissionless innovation, and open up new business opportunities for entrepreneurs interested in innovation. Decentralized finance, a recent area of financial technology, can alter the structure of contemporary finance and produce a new environment for innovation and entrepreneurship, according to Chen and Bellavitis. (2019). This demonstrates how decentralization can serve as a basis for the creation of novel business models. Muneeza et al. (2018) evaluated the value of crowdfunding for financial inclusion by offering the first analyses of Malaysian crowdfunding and Shariah-compliant crowdfunding. They examined the potential impact of blockchain technology on the growth of crowdfunding as well as the significance of crowdfunding for financial inclusion. According to Muneeza et alresearch.'s from 2018, the introduction of novel digital financial technologies, like crowdfunding and blockchain, opens up new opportunities to reach economically disadvantaged people and populations. According to Muneeza et al. (2018).'s research, crowdfunding is a successful strategy for increasing people’s access to financial services, and platform operators may be able to overcome some of their current difficulties by utilizing blockchain technology.

In a different study, Schuetz and Venkatesh. (2020) made the case that isolated communities in rural India must be linked to regional and international supply chains to enjoy economic prosperity. Rural Indians are unable to participate in these supply networks due to high rates of financial exclusion. A literature assessment on financial inclusion, adoption, and blockchain technology in India was carried out by Schuetz and Venkatesh in 2020. Based on their research, they make the following four predictions about how to deal with the problem of financial exclusion: geographic access, high cost, inadequate banking products, and financial illiteracy. Additionally, according to Schuetz and Venkatesh. (2020), blockchain technology has the power to get beyond the majority of these barriers. Schuetz and Venkatesh. (2020) established a research agenda on the causes of adoption, adoption patterns, and effects of adoption to propel the development of such an understanding. For blockchain technologies to become the mainstay of programs to promote financial inclusion, this is crucial.

Blockchain technology, according to Mavilia and Pisani. (2020), was first created as a mechanism to support Bitcoins, the most well-known and contentious cryptocurrency in the world. But in a relatively short amount of time, it has made a name for itself as a disruptive technology that can both transform and launch new industries. Mavilia and Pisani. (2020) gave a summary of the fundamental features and functionality of blockchain technology. The writers then concentrated on potential applications that might be employed for underdeveloped countries. The empirical analysis, according to Mavilia and Pisani. (2020), identifies the flaws in the continent’s current financial system and serves as the foundation for the discussion of potential blockchain solutions to lower the current level of financial exclusion and advance sustainable development for African nations. These arguments were offered to back up the authors’ earlier assertion that the empirical study revealed the flaws in the continent’s current financial system. According to Danho and Habte. (2019), centralized institutions have historically provided financial services. As a result, various central parties now have authority over financial systems. Some claim that the centralization of power has increased wealth inequality, nevertheless.

With the advent of blockchain, however, traditional views on democratization and transparency have changed more recently. Increasing financial inclusion has been underlined as a crucial step that must be taken to decrease poverty levels, and blockchain has been investigated as a technology that has the potential to make a difference in the attempt to do so. In their 2019 study, Danho and Habte look at how blockchain technology can help increase access to financial services across Africa. Blockchain is regarded as helpful for mobile financial services, according to the findings of Danho and Habte. (2019), primarily because it can reduce costs by doing away with middlemen, automating processes, and creating decentralized trust. Furthermore, Danho and Habte. (2019) found that the absence of uniform protocols and definitions has a considerable negative impact on the usability of blockchain today. Due to this, blockchain cannot yet significantly impact the growth of financial inclusion. Blockchain technology may be able to help developing countries with their poor access to traditional financial services, according to research by di Prisco and Strangio. (2021). Wala is an African blockchain firm that was founded to create a new financial ecosystem tailored to the needs of people with poor socioeconomic levels. di Prisco and Strangio. (2021) studied Wala’s history. Wala was developed to help those with poor socioeconomic levels overcome their problems. Di Prisco and Strangio claim that Wala was compelled to leave the market in 2019 despite its early success (2021). This offers a special case study to evaluate the barriers preventing blockchain technology from realizing its full potential in developing nations.

The existence of a mismatch between Blockchain technology (BCT)capabilities and low socioeconomic status (SES) requirements, as noted by di Prisco and Strangio. (2021), emphasizes the need for immediate action to address the issue of the digital divide and to encourage the adoption of new digital technologies in place of the pre-existing informal mechanisms. Norta et al. (2019) claim that obtaining credit and sending money over international borders are still challenging, time-consuming, and expensive processes. Current procedures for the transfer of money, according to Norta et al. (2019), have a variety of drawbacks, including long lineups, exchange rate losses, risks linked with counterparties, bureaucracy, and a lot of paperwork. Additionally, Norta et al. (2019) asserted that offering viable financial services to the target population is one of the most crucial stages in eliminating global poverty and reviving local economies. An estimated two billion adults lack bank accounts and have either no access to or very limited access to financial services, according to Norta et al. (2019). The Everex program uses blockchain technology for cross-border transfer, online payment, currency exchange, and microlending to make it easier to access financial services. Without the inherent volatility prevalent in cryptocurrencies that do not use stablecoins, this is accomplished.

Once more, Norta et al. (2019) noted that the Everex wallet allows for a gateway from money to cryptocurrency, making it simpler to access cryptocurrencies. This enables our users to rapidly buy and trade tokens without having to visit an exchange. The conventional financial system has fallen short of the standards set by other technical breakthroughs, despite the existence of this invention. According to Abdulhakeem and Hu. (2021), despite the internet’s development opening up a new Universe of potential in life, including banking, the existing financial system has fallen short of these expectations. Almost everyone in the modern world has access to the internet, yet not everyone has a bank account, according to research by Abdulhakeem and Hu. (2021). The Internet has made it possible to send information across the globe in a matter of milliseconds, but when it comes to financial assets, time and money are still needed. Around 1.7 billion people worldwide still don’t have any kind of access to banks, according to the World Bank Group. Additionally, Abdulhakeem and Hu. (2021) hypothesized that technological advancement and blockchain technology have recently sparked a growing trend toward decentralization in the financial sector. The Bitcoin Blockchain, created by Satoshi Nakamoto, was a game-changing invention that was the first to support peer-to-peer transactions without the use of any middlemen or centralized systems.

Once more, Abdulhakeem and Hu. (2021) 6 years later, Ethereum, another blockchain, was created. The foundation of possible decentralized financial systems has been Ethereum. Additionally, according to Rella. (2019), blockchain technologies have proven to have enormous promise for the formalization of remittances and the extension of financial inclusion ever since they were first developed. According to Rella. (2019), regulators and practitioners have recently investigated how blockchain technology could perhaps replace the correspondent banking infrastructure that supports cross-border payments and remittances. Again, according to Rella. (2019), blockchain technologies are not an example of fundamentally new monetary systems; rather, they are the most recent development in a line of technological innovations that signal the advent of frictionless capitalism.

This study used a qualitative research methodology and included both an analysis and a critique of the pertinent body of previous research. A “full review that enables researchers to evaluate past research to uncover research gaps, consistencies, and inconsistencies in earlier studies” is what a critical review is considered. Researchers can analyze published material, remark on it, critically evaluate it, and synthesize it with the use of a critical review (Carliner 2011; Wakefield 2015). To ensure that the study was as thorough as it could be, the researchers took the recommendations offered by Webster and Watson (2002) to heart. According to Webster and Watson (2002), “A full examination must take into account four crucial features.” The question “what’s new?” “so what?” “Why so?” and “well done?” are examples of these. To ensure that the review was thorough, the researchers made sure to go by this piece of advice.

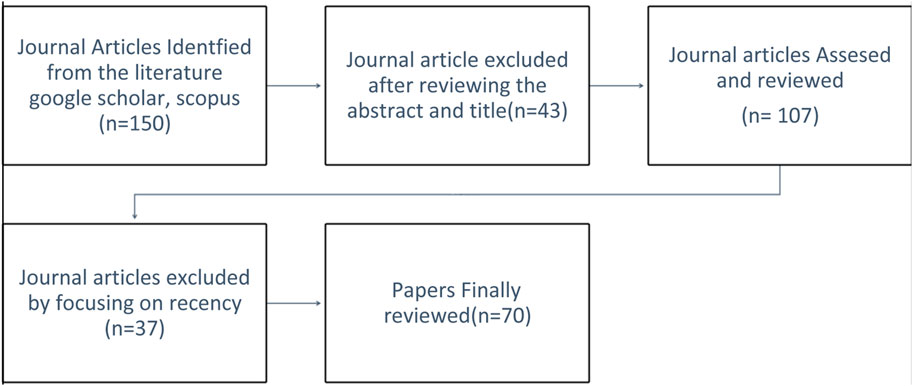

To get the necessary data, the “Publish or Perish” search tool was utilized to search both the Scopus and Google Scholar databases. For this review, a total of 70 articles were taken into account. Wee and Banister (2016) claim that between fifty and one hundred papers are the optimum quantity for a thorough review article. A thorough analysis of the pertinent literature was conducted after reaching the point of saturation, which is the point at which there is no longer any new information on the subject being researched as a result of the continued examination of more articles. After the saturation point was reached, this was done. Once it was concluded that there was no longer any new information regarding the subject under investigation, this was done (Carliner 2011; Mpofu. (2022)). As shown in a flowchart in Figure 3 below, the steps involved in doing a literature review can be divided into the following categories.

FIGURE 3. A flowchart depicting the process of conducting a literature review.

This study examined a total of 70 different publications, as seen in Figure 3 above, and the crucial data was gathered from both the Scopus database and the Google Scholar database. It is important to emphasize that the participation of two reviewers was necessary for the selection of papers when considering the findings that were reported in the publications by Snyder (2019). This was a prerequisite for the article selection process. According to Snyder (2019), it is advisable to have two reviewers to safeguard the effectiveness and dependability of the search technique. The criteria utilized to choose which studies would be included in the analysis were the length of time since the study was finished and the suitability of the study’s design concerning the research problem. The studies that would be included were chosen based on these criteria. However, work from earlier years was also taken into consideration. The publications that were largely focused on were those that had been published from the year 2000 up to the present. Most of the emphasis was placed on works that had been published between 2000 and the present. The publications that had been published beginning in 2000 and continuing up to the present day were the focus. The publications that included critical review articles and content analysis in the study design were the ones that caught our interest the most. This is because these publications were more relevant to our research, and the review articles we used allowed us to find more of the material we were looking for. Seventy publications in total were reviewed and considered for this research.

The “World Bank estimates that there are 1.7 billion people” who do not have bank accounts, which accounts for 31 percent of all adults. In some emerging nations, this number is “as high as 61 percent, and women are at an even greater disadvantage, making up 55 percent of the unbanked population”. Digital tools, such as credit cards and bank accounts. It is common practice to take automated teller machines (ATMs) for granted, even though they play a very important role in ensuring that excluded individuals can access formal financial services. The “1.7 billion people that the traditional banking system has neglected, many of whom are already struggling economically, have few ways to easily send and receive money, build up savings, gain access to credit, or secure insurance”. Emergencies can be devastating if you do not have a financial cushion, so it is important to have access to alternative financial services. Nevertheless, blockchain technology has surprising promise for increasing the number of people around the world who have access to the financial system. According to Cecilia Chapiro. (2021), “technology is global, open-sourced,” and available to anybody who has access to the Internet; this includes people of all nationalities, ethnicities, races, genders, and socioeconomic classes”. Although many people “associate blockchain technology with cryptocurrencies like Bitcoin and Dogecoin and possibly with greed, illegal activity, or environmental carnage, the technology is, at its core, nothing more than a decentralized method of organizing transactions in a database, or ledger, in such a way that multiple untrusted parties can agree on the state of those transactions without the need for a middleman”. As was mentioned previously, each transaction that is, recorded is both open and visible while also being encrypted. In this sense, blockchain is altering the role that banks, governments, and companies play by making it possible for monetary transactions to be carried out in a manner that is, more secure, less expensive, and more efficient than the traditional alternatives (Pilkington, 2016; Yaga et al., 2019; Saberi et al., 2019; Zheng et al., 2017; Cecilia Chapiro. (2021))

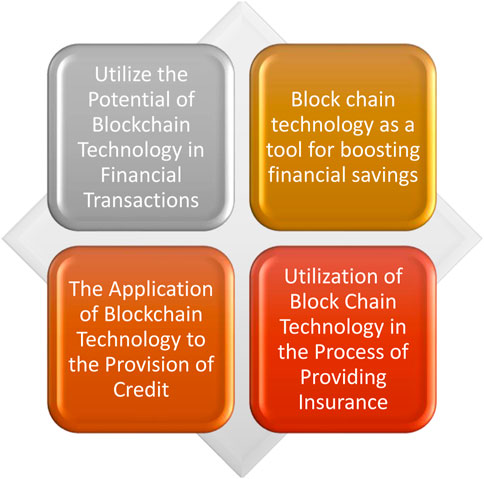

Blockchain technology has the potential to influence digital financial inclusion in several different ways. Figure 4 provides a visual representation of these possible scenarios.

FIGURE 4. Strategies for broadening access to financial services using blockchain.

Blockchain technology has the potential to influence digital financial inclusion in several different ways. Figure 4 provides a visual representation of these possible scenarios which include utilising the potential of blockchain technology in financial transactions, blockchain technology as a tool for boosting financial savings, the application of blockchain technology to the provision of credit and utilization of blockchain technology in the process of providing insurance.

Blockchain technology offers opportunities for faster, cheaper, and more secure payment processing in addition to a distributed ledger that can increase participant trust. Blockchain was first created to act as a platform for virtual currencies, but it is now being used in a wide range of industries, including payments. Blockchain technology enables worldwide payment processing services and other forms of transactions by using encrypted distributed ledgers, which offer reliable real-time verification of transactions. As a result, there is no longer any need for intermediaries like clearing houses and correspondent banks. Blockchain technology was primarily created to support the virtual currency known as bitcoin, but subsequent studies have indicated that it may have many other applications as well. Because executing a transaction can often take days, there are additional charges, and there is a lack of security, our payment system is rife with issues and needs to be overhauled. One of the main reasons why customers are hesitant to hold or transfer their money utilizing payment methods is because of this. Not only that, but a sizable portion of the populace lacks access to reliable banking and payment options. This field has the potential to be dramatically impacted by blockchain technology.

It is feasible for it to provide people with the chance they deserve while also fixing a sizable portion of the issues that have long plagued this business. Money transfers can be expensive; for instance, Western Union may charge a fee of up to 35% for transactions worth less than $10. While wealthier people might be able to afford it, for those who live in rural areas, this is a substantial chunk of money. Along with the high costs, access is another issue. In addition to finding, it more challenging to send and receive money, the 1.7 billion people who lack bank accounts frequently lack the documents needed to open an account, including a passport, proof of income, reliable internet, and a smartphone. Over the past 10 years, tremendous progress has been achieved in mobile payments toward this objective. Leaf is the name of one of the initiatives in which UNICEF has invested. It can be used by anyone in Rwanda to send and receive money straight from a mobile device, regardless of whether that device is a smartphone. Neither an internet connection nor a passport is required. As of October 2021, 5,871 users who were based in the nations of Kenya, Uganda, and Rwanda have completed a total of 97,819 transactions. The average amount sent from one person to another is $4.97, a level for which regular money transmitters would charge astronomical fees. Many of the users are Rwandans who had to leave the DRC and are now able to get financial assistance from relatives who live in other nations. Leaf is being used by other people to buy things like groceries and vegetables. Another app that can be used in Kenya is Kotani Pay. Regardless of the device’s quality, this service enables Kenyans to send and receive bitcoin by simply entering a short code on their phone, which subsequently converts the cryptocurrency to Kenyan shillings. As of October 2021, 2,598 users who were based in the nations of Kenya, Uganda, and Rwanda have completed a total of 137,195 transactions.

Users have so far exchanged more than $400,000 in total, with the average amount going from one user to another being $1. According to Cecilia Chapiro. (2021), “both Leaf and Kotani Pay are using blockchain technology to enable quicker and more secure money transfers”. They offer the same advantages that mobile money does to the user, but furthermore, they offer a safe peer-to-peer transaction interface that operates at minimal costs free to run, below 2% to cash out, and cut the transaction time from three to 5 seconds. Unlike mobile money, which was first intended to be a domestic alternative, Leaf and Kotani Pay both operate on a worldwide, decentralized application. This would imply that the only other cost associated with conducting business on a global scale is the currency exchange rate. Due to instantaneous, inexpensive, and traceable transactions that can hold multiple currencies in multiple mobile networks both domestically and internationally, blockchain applications are becoming an increasingly appealing technology to use for remittances, especially for the transfer of small amounts of money. Applications using blockchain technology can also store several currencies across various mobile networks. Blockchain-based applications have the potential to store several types of currencies.

The cost of implementing new technology has traditionally been one of the most important deciding factors. Using technology that provides self-service can save you money, as well as reduce the amount of time and emotional labour required. It refers to “the degree to which the client believes that utilizing a particular framework would reduce the amount of money spent on operating the service.” Banks have traditionally fulfilled the role of an intermediary between individuals who have a financial surplus of money and individuals who have a financial shortage of money. In this capacity, banks have been able to profit from the “spread of the transaction, which is the difference between the interest rate that a bank charges a borrower and the interest rate that a bank pays a depositor”. The financial system has succeeded in accomplishing that goal; yet, because of its complexity and high running expenses, they have only been able to do so by erecting barriers to admission, which has caused many people to fall behind. According to Cecilia Chapiro. (2021), a large portion of the world does not have access to savings accounts. This means “that if villagers or farmers are fortunate enough to have any savings at all, it is often in the form of physical assets, such as cattle”. It can be challenging to liquidate these assets in times of emergency, and hoarding cash makes people more susceptible to inflation.

According to Ullah et al. (2022) blockchain technology can handle financial activities more efficiently than the previous approach. Ullah et al. (2022) also suggested that earlier research findings demonstrate that e-commerce and self-service technologies can help reduce transaction costs. The use of cutting-edge, game-changing technology has the potential to reduce transaction costs, such as those associated with data encryption for example, as well as distribution costs like those associated with e-logistic services. It is generally agreed upon that a reduction in costs will have a favourable influence on perceived ease of use, a beneficial influence on perceived usefulness, and a beneficial influence on perceived intention to use, all of which can have a beneficial influence on financial inclusion. There are a lot of examples of platforms where blockchain is employed, and one of them is that it has shown to be a useful tool in terms of saving money for low-income households. For example, Xcapit, which is based in “Argentina, is utilizing the decentralized ledger that blockchain technology provides to provide an alternative platform that makes it simpler and less intimidating for individuals who do not have a bank account, credit, or financial expertise to save money and invest”.

Downloading the app and enabling the wallet are the only requirements for opening an account, making participation open to anyone. According to Cecilia Chapiro. (2021), the only thing an individual needs to start investing in is a cryptocurrency, which they can either transfer from another platform or buy from Xcapit’s app partners. This is the sole requirement. Users select the amount of money they want to spend and the level of risk they are willing to take after passing a screening process that requires them to give out personal information, which may consist of information as fundamental as their name and mobile phone number. They are allowed to learn about their investor profile by responding to a test that is, integrated into the app, and Xcapit has developed a variety of financial products that offer varying rates of return. Users can monitor the performance of their investments on the app, and they are also given the option to withdraw their money at any time. Even if it is being invested, the money is always non-etheless readily available in their possession. Blockchain makes it possible for Xcapit to provide consumers with an easy-to-use investment interface, one in which they can place their trust in the integrity of the network to ensure the safety of their assets and benefit from a more streamlined and cost-effective investment process. It had “3,590 users from Argentina, Mexico, Brazil, and Colombia with average investments of $1,500 each over the preceding 2 years, and it managed around $3.6 million in total assets”. Active techniques employed by it generated returns of up to 15.36 percent in Bitcoin units and “up to 8.83 percent in dollars between January 2021 and 19 October 2021” Cecilia Chapiro. (2021).

Credit ratings, which financial institutions have traditionally used to systematically identify eligibility and type, are essential to the expansion of the economy because they allow families to buy homes and obtain consumer credit, give businesses access to capital, and aid nations in stabilizing consumption levels during difficult economic times. The majority of people, more than one-third of them, do not have credit histories, so they have no safety net to fall back on in times of need. According to the International Finance Corporation, micro, small, and medium-sized firms in developing nations experience a $5.2 trillion annual credit deficit. Decentralized credit scoring is the idea of determining a borrower’s creditworthiness without the use of a middleman using either off-chain or on-chain data. This analysis is done on a blockchain, which is a decentralized database that is, controlled by a distributed P2P network of computers. One project that aims to lessen the discrepancy in access to credit that exists in low-income communities is Grassroots Economics, a blockchain-based project with a Kenyan base and funding from UNICEF’s Innovation Fund. In times of crisis, villagers might not have access to a line of credit or a sizable sum of money, but they still have tangible commodities and services, like crops or garments, or even the labour of a cook or teacher.

In these circumstances, the concept behind the project created by Grassroots Economics is useful. Community Inclusion Currencies are a concept created by Grassroots Economics. With this idea, the business can issue tokens that are backed by all the actual goods and services offered in a given community. The town’s food and water supply, as well as the labour of carpenters and babysitters, are a few examples of these products and services. Villages in Kenya can use the tokens to create a credit line that is, backed by their assets and can be utilized in an emergency. Through the usage of Community Inclusion Currencies, people can monetize their resources and give or take credit without using Kenyan shillings or a bank. Users can instead get up to 10% of their prior annual revenue in the form of credits for future production based on past trades, allowing them to continue trading even when their liquidity is low. All transactions made between users exchanging tokens using feature phones are documented on a blockchain. This guarantees the highest level of security for users’ financial transactions with one another. People who have a track record of good financial management within the same community have a higher chance of getting loans granted. In 2020, 58,400 users of Grassroots Economics carried out transactions worth $3 million in tokens, according to Cecilia Chapiro. (2021). More than 95% of consumers were able to redeem their CICs. Blockchain technology “eliminates the traditional limitations of information gaps, traceability, transaction transparency, and credit problems in supply chain management. It is based on technological innovations such as distributed ledgers, symmetric encryption, authorization, consensus mechanisms, and smart contracts”. This is in line with Tan et al. (2020).'s claim that Supply Chain Management has made substantial use of blockchain technology.

Furthermore, Zou and Xue. (2020) suggested that while credit banks provide learning avenues and orientations for growing abilities, their existing centralized management structure makes it difficult to oversee the outcomes of learning. They hypothesized that the issue of credit management in credit bank systems might be resolved by blockchain technology. Blockchain technology creates a link between the block, the course’s enrolled students, and the learning outcomes. Blockchain technology can “save management resources for credit banks and increase confidence because of its potential to actualize decentralization of management, automation of transfer regarding learning credit and education, traceable outcomes, and inability to be tampered with”. Utilizing the Hyperledger fabric technology, it is feasible to achieve the credit management of a credit bank system through system design and experimentation. To increase the effectiveness of management and supervision within the food supply chain, Mao et al. (2018) also created a credit rating system based on blockchain technology. The technology collects traders’ credit evaluation text by use of smart contracts that are kept on the blockchain. After that, an extensive examination of the compiled text is performed using a deep learning network called Long Short-Term Memory. In conclusion, regulators use the results of traders’ credit as a guide for their oversight and management. If blockchain technology is used, traders can be held responsible for how they behaved during the transaction and credit evaluation process. Regulators can gather information about traders that is, more reliable, accurate, and comprehensive. The outcomes of studies carried out by Mao et al. (2018) reveal that using Long Short-Term Memory leads to superior performance than conventional machine learning techniques like Support Vector Machine and Naive Bayes when it comes to interpreting the credit evaluation text. The system’s interface’s usability helps the application’s overall ease.

Insurance policies frequently require identification documents, proof of financial stability, and additional paperwork, all of which may operate as a barrier to entry. Even for individuals who have insurance, it is not always clear who will cover the costs and how much they will be after a tragedy. Significant efficiency improvements, cost reductions, transparency, quicker payouts, and fraud avoidance will all be made possible by blockchain technology. It will also enable data to be transferred in real time between diverse parties in a trusted and traceable way. The usage of the technology will lead to the realization of these advantages. New insurance business models can be developed with the help of blockchain technology, which could improve products and markets. Insurance companies operate in a highly competitive environment where consumers and businesses alike demand the best value for their money and a top-notch online shopping experience from the businesses, they do business with. The emergence of blockchain technology offers the insurance industry a chance for positive disruption and growth.

The technology has the potential to be helpful, even though there aren’t as many blockchain projects focusing on insurance as there are other aspects of financial inclusion. One example of a group that has worked together to create a decentralized insurance policy to protect small farmers in Africa is the ETHERISC, which is supported by the Ethereum Foundation, and ACRE Africa. The software gives farmers access to weather index insurance plans that are supported by smart contracts, which are self-executing contracts kept on a blockchain. These contracts trigger payouts if extreme weather influences the crops that the farmers are growing. These smart contracts operate similarly to a simple if-then formula; for instance, if it rains 5 inches in 24 h across all locations, the insured farmer will immediately be compensated for flood-related damages following the contract. The contracts are connected to weather data that is, updated in real-time, including details on temperature, precipitation, wind speed, daylight hours, and even hurricanes and hail. The automated method enhances the insurer company’s operations if a climate-related threat materializes, and the farmers are safeguarded from the risk by fair and transparent reimbursement. If blockchain technology did not provide transparency and automation, farmers would need to justify the harm, which is a process that can be time-consuming and may prevent them from quickly recovering from the tragedy.

By the end of 2021, 17,000 Kenyan farmers had received this insurance, and they were taking advantage of the program’s flexibility Cecilia Chapiro. (2021). Furthermore, Singh et al. (2019) asserted that using blockchain technology is an effective solution to address the problems associated with the traditional types of auto insurance. To determine the appropriate premium amount to be paid by automobiles, typical vehicle insurance processes utilized by insurance firms, according to Singh et al. (2019), rely on evaluating the history of the actions of the drivers. However, usage-based insurance (UBI), which is based on telematics, proves to be a cutting-edge and successful method for insuring vehicles. Singh et al. made the following claim (2019). As opposed to the conventional method, the UBI’s premiums are established by considering the current behaviour of drivers. There is a lack of openness in the way claims are handled when it comes to conventional methods for motor vehicle insurance. This lack of transparency leads to several fraudulent actions in addition to delays in the acceptance of claims. The usage of blockchain technology could prove to be a successful means of overcoming difficulties.

Financial inclusion is emphasized as a key enabler of numerous developmental goals in the Sustainable Development Goals for 2030, where it is specified as an objective in eight of the seventeen goals. It is highlighted specifically as a supporter of gender equality. These include “Sustainable Development Goal 1 (SDG 1), which focuses on ending poverty; Sustainable Development Goal 2 (SDG 2), which focuses on preventing hunger, achieving food security, and promoting sustainable agriculture; the Sustainable Development Goal 3 (SDG 3), which focuses on improving health and wellbeing; the Sustainable Development Goal 5 (SDG 5), which focuses on achieving gender equality and the economic empowerment of women; the Sustainable Development Goal 6 (SDG 6), which focuses on preventing climate change; Goal 17 of the Sustainable Development Goals is also concerned with improving the methods for implementation”. Greater financial inclusion has an implicit role in achieving these goals, which can be done by boosting the mobilization of savings for consumption and investment, both of which can boost growth. Sustainable development can be ensured on many different fronts if the technology underlying blockchains can be successfully applied to improve financial inclusion. According to Manyika et al. (2016), the usage of digital finance alone might benefit billions of people by promoting inclusive growth that increases emerging economies’ GDP by $3.7 trillion over the next 10 years. As more people have access to financial services, there is mounting evidence that these services promote economic and financial stability, the mobilization of domestic savings, and the growth of government income. Academic research has provided evidence that financial inclusion models can support both overall economic growth and the achievement of more general development objectives. According to Kuada. (2019), financial inclusion has been marketed as a tool for eradicating poverty in the developing world in several policy documents. The research was referring to the activities of institutions like the World Bank and the International Monetary Fund. As a result, it is hoped that low-income families will be better able to safeguard themselves against unforeseen financial occurrences, invest in their human capital through things like healthcare and education, and/or accumulate modest assets. This will enable them to take advantage of promising investment opportunities in their respective economies. The important contribution is that financial inclusion is one of the more recent strategies that financial institutions have been utilizing to provide relevant education for potential customers from societal groups who have poor levels of education in general and nearly no financial access. This is one of the problems brought on by the fact that one of the more recent techniques used by financial institutions is financial inclusion (Kuada, 2019). believes that promoting financial inclusion through activities that inform people with lower levels of knowledge about the inner workings of financial instruments they have access to and that can improve their daily lives.

Since their introduction, distributed ledger technologies have shown a lot of promise for institutionalizing remittances and boosting access to a range of financial services. In order to ensure that transactions can be verified and recorded using blockchain technology in a decentralized ledger, it is believed that both authorities and practitioners have looked into the potential of blockchain technology to simplify and possibly even replace the infrastructure that supports international payments and remittances, such as correspondent banking. This is due to the fact that blockchain technology has the potential to streamline and potentially replace the infrastructure that underpins global payments and remittances. This essay’s goals were to analyze how blockchain technology has impacted the process of bringing previously uninvolved parties into the financial system and to offer opinion on the most important advantages and lessons that can be drawn from sustainable growth. The authors of this study came to the conclusion that blockchain technology has the ability to promote digital financial inclusion in a range of contexts after thoroughly analyzing the pertinent prior research. These applications include the use of blockchain technology in financial transactions, the use of blockchain technology to help people save more money, the use of blockchain technology to extend credit, and the use of blockchain technology to provide insurance. According to the findings of the study, financial inclusion is an enabler for at least eight of the seventeen development goals, despite the fact that it is not stated as a target for several of the goals. The study came to the conclusion that sustainable development can be secured on many different fronts if the technology that underpins blockchains can be successfully applied to boost financial inclusion. Governments, especially those in developing economies, must give blockchain investments the serious consideration they require in order to increase financial inclusion.

The author confirms being the sole contributor of this work and has approved it for publication.

The author declares that the research was conducted in the absence of any commercial or financial relationships that could be construed as a potential conflict of interest.

All claims expressed in this article are solely those of the authors and do not necessarily represent those of their affiliated organizations, or those of the publisher, the editors and the reviewers. Any product that may be evaluated in this article, or claim that may be made by its manufacturer, is not guaranteed or endorsed by the publisher.

Abdulhakeem, S. A., and Hu, Q. (2021). Powered by blockchain technology, DeFi (decentralized finance) strives to increase financial inclusion of the unbanked by reshaping the world financial system. Mod. Econ. 12 (01), 1–16. doi:10.4236/me.2021.121001

Bai, C. A., Cordeiro, J., and Sarkis, J. (2020). Blockchain technology: Business, strategy, the environment, and sustainability. Bus. Strategy Environ. 29 (1), 321–322. doi:10.1002/bse.2431

Carliner, S. (2011). Workshop in conducting integrative literature reviews. In 2011 IEEE International Professional Communication Conference IEEE, 1–3.

Cecilia Chapiro (2021). Working toward financial inclusion with blockchain. Avaliable At: https://ssir.org/articles/entry/working_toward_financial_inclusion_with_blockchain#.

Chen, Y., and Bellavitis, C. (2019). Decentralized finance: Blockchain technology and the quest for an open financial system. Stevens Institute of Technology School of Business Research Paper. Avaliable At: https://ssrn.com/abstract=3418557.

Danho, S., and Habte, Y. (2019). Blockchain for financial inclusion and mobile financial services: A study in sub-saharan Africa. Thesis. STOCKHOLM, SWEDEN: Degree Project in Industrial ENGINEERING and Management.

di Prisco, D., and Strangio, D. (2021). Technology and financial inclusion: A case study to evaluate potential and limitations of blockchain in emerging countries. Technol. Analysis Strategic Manag. 2021, 1–14. doi:10.1080/09537325.2021.1944617

Dutta, P., Choi, T. M., Somani, S., and Butala, R. (2020). Blockchain technology in supply chain operations: Applications, challenges and research opportunities. Transp. Res. part e Logist. Transp. Rev. 142, 102067. doi:10.1016/j.tre.2020.102067

Dwyer, G. P. (2017). “Blockchain: A primer,” in The most important concepts in finance (Cheltenham, United Kingdom: Edward Elgar Publishing).

Ghobakhloo, M. (2020). Industry 4.0, digitization, and opportunities for sustainability. J. Clean. Prod. 252, 119869. doi:10.1016/j.jclepro.2019.119869

Giungato, P., Rana, R., Tarabella, A., and Tricase, C. (2017). Current trends in sustainability of bitcoins and related blockchain technology. Sustainability 9 (12), 2214. doi:10.3390/su9122214

Jabareen, Y. (2008). A new conceptual framework for sustainable development. Environ. Dev. Sustain. 10 (2), 179–192. doi:10.1007/s10668-006-9058-z

Jamwal, A., Agrawal, R., Sharma, M., and Giallanza, A. (2021). Industry 4.0 technologies for manufacturing sustainability: A systematic review and future research directions. Appl. Sci. 11 (12), 5725. doi:10.3390/app11125725

Janssen, M., Weerakkody, V., Ismagilova, E., Sivarajah, U., and Irani, Z. (2020). A framework for analysing blockchain technology adoption: Integrating institutional, market and technical factors. Int. J. Inf. Manag. 50, 302–309. doi:10.1016/j.ijinfomgt.2019.08.012

Kuada, J. (2019). “Financial inclusion and sustainable development goals,” in Extending financial inclusion in Africa (Academic Press), 259–277. doi:10.1016/B978-0-12-814164-9.00012-8

Lasi, H., Fettke, P., Kemper, H. G., Feld, T., and Hoffmann, M. (2014). Industry 4.0. Bus. Inf. Syst. Eng. 6 (4), 239–242. doi:10.1007/s12599-014-0334-4

Manyika, J. S., Singer, M., White, O., and Berry, C. (2016). How digital finance could boost growth in emerging economies. Available At: https://www.mckinsey.com/featured-insights/employment-and-growth/how-digital-finance-could-boost-growth-in-emerging-economies.

Mao, D., Wang, F., Hao, Z., and Li, H. (2018). Credit evaluation system based on blockchain for multiple stakeholders in the food supply chain. Int. J. Environ. Res. public health 15 (8), 1627. doi:10.3390/ijerph15081627

Mavilia, R., and Pisani, R. (2020). Blockchain and catching-up in developing countries: The case of financial inclusion in Africa. Afr. J. Sci. Technol. Innovation Dev. 12 (2), 151–163. doi:10.1080/20421338.2019.1624009

Mhlanga, D., and Denhere, V. (2020). Determinants of financial inclusion in southern Africa. Oeconomica 65 (3), 39–52. doi:10.2478/subboec-2020-0014

Mhlanga, D. (2021). Factors that matter for financial inclusion: Evidence from sub-sharan africa-the Zimbabwe case. Acad. J. Interdiscip. Stud. 10 (6), 48. doi:10.36941/ajis-2021-0152

Mhlanga, D. (2020). Industry 4.0 in finance: The impact of artificial intelligence (ai) on digital financial inclusion. Int. J. Financial Stud. 8 (3), 45. doi:10.3390/ijfs8030045

Mpofu, F. Y. (2022). Industry 4.0 in Financial Services: Mobile Money Taxes, Revenue Mobilisation, Financial Inclusion, and the Realisation of Sustainable Development Goals (SDGs) in Africa. Sustainability 14 (14), 8667.

Muneeza, A., Arshad, N. A., and Arifin, A. T. (2018). The application of blockchain technology in crowdfunding: Towards financial inclusion via technology. Int. J. Manag. Appl. Res. 5 (2), 82–98. doi:10.18646/2056.52.18-007

Norta, A., Leiding, B., and Lane, A. (2019). “Lowering financial inclusion barriers with a blockchain-based capital transfer system,” in IEEE INFOCOM 2019-IEEE Conference on Computer Communications Workshops (INFOCOM WKSHPS), Paris, France, 29 April 2019 - 02 May 2019 (IEEE), 319–324.

Ohnesorge, J. (2018). A primer on blockchain technology and its potential for financial inclusion (No. 2/2018). Bonn-German Institute of Development and Sustainability.

Parris, T. M., and Kates, R. W. (2003). Characterizing and measuring sustainable development. Annu. Rev. Environ. Resour. 28 (1), 559–586. doi:10.1146/annurev.energy.28.050302.105551

Pilkington, M. (2016). “Blockchain technology: Principles and applications,” in Research handbook on digital transformations (Cheltenham, United Kingdom: Edward Elgar Publishing).

Rella, L. (2019). Blockchain technologies and remittances: From financial inclusion to correspondent banking. Front. Blockchain 14, 14. doi:10.3389/fbloc.2019.00014

Rieger, A., Roth, T., Sedlmeir, J., and Fridgen, G. (2022). We need a broader debate on the sustainability of blockchain. Joule 6 (6), 1137–1141. doi:10.1016/j.joule.2022.04.013

Rogers, P. P., Jalal, K. F., and Boyd, J. A. (2012). An introduction to sustainable development. London Routledge.

Saberi, S., Kouhizadeh, M., Sarkis, J., and Shen, L. (2019). Blockchain technology and its relationships to sustainable supply chain management. Int. J. Prod. Res. 57 (7), 2117–2135. doi:10.1080/00207543.2018.1533261

Sachs, J. D. (2015). “The age of sustainable development,” in The age of sustainable development (Columbia University Press, New York,).

Schuetz, S., and Venkatesh, V. (2020). Blockchain, adoption, and financial inclusion in India: Research opportunities. Int. J. Inf. Manag. 52, 101936. doi:10.1016/j.ijinfomgt.2019.04.009

Singh, P. K., Singh, R., Muchahary, G., Lahon, M., and Nandi, S. (2019). “A blockchain-based approach for usage-based insurance and incentive in its,” in TENCON 2019-2019 IEEE Region 10 Conference (TENCON), Kochi, India, 17-20 October 2019 (IEEE), 1202–1207.

Snyder, H. (2019). Literature review as a research methodology: An overview and guidelines. Journal of business research 104, 333–339.

Sony, M., and Naik, S. (2019). Key ingredients for evaluating industry 4.0 readiness for organizations: A literature review. Benchmarking Int. J. 27, 2213–2232. doi:10.1108/bij-09-2018-0284

Tan, R., Li, Y., Zhang, J., and Si, W. (2020). “Application of blockchain technology to the credit management of supply chain,” in International conference on Frontiers in cyber security (Singapore: Springer), 121–132.

Ullah, N., Al-Rahmi, W. M., Alfarraj, O., Alalwan, N., Alzahrani, A. I., Ramayah, T., et al. (2022). Hybridizing cost saving with trust for blockchain technology adoption by financial institutions. Telematics Inf. Rep. 6, 100008. doi:10.1016/j.teler.2022.100008

Wakefield, A. (2015). Synthesising the literature as part of a literature review. Nursing Standard (2014+) 29(29), 44.

Wee, B. V., and Banister, D. (2016). How to write a literature review paper?. Transport reviews 36, 2, 278–288.

Webster, J., and Watson, R. T. (2002). Analyzing the past to prepare for the future: Writing a literature review. MIS quarterly, 8–18.

World Bank (2022). IBM what is blockchain technology. Avaliable At: https://www.ibm.com/za-en/topics/what-is-blockchain.